eCom Chargeback Process Guide

April 2020

V3.1

eComm Chargeback Process Guide V3.1

All information whether text or graphics, contained in this manual is confidential and proprietary information of Worldpay, LLC and is provided

to you solely for the purpose of assisting you in using a Worldpay, LLC product. All such information is protected by copyright laws and

international treaties. No part of this manual may be reproduced or transmitted in any form or by any means, electronic, mechanical or otherwise

for any purpose without the express written permission of Worldpay, LLC. The possession, viewing, or use of the information contained in this

manual does not transfer any intellectual property rights or grant a license to use this information or any software application referred to herein

for any purpose other than that for which it was provided. Information in this manual is presented "as is" and neither Worldpay, LLC or any other

party assumes responsibility for typographical errors, technical errors, or other inaccuracies contained in this document. This manual is subject to

change without notice and does not represent a commitment on the part Worldpay, LLC or any other party. Worldpay, LLC does not warrant that

the information contained herein is accurate or complete.

Worldpay, the logo and any associated brand names are trademarks or registered trademarks of Worldpay, LLC and/or its affiliates in the US, UK

or other countries. All other trademarks are the property of their respective owners and all parties herein have consented to their trademarks

appearing in this manual. Any use by you of the trademarks included herein must have express written permission of the respective owner.

Copyright © 2009-2020, Worldpay, LLC- ALL RIGHTS RESERVED.

CONTENTS

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

iii

Chapter 1 Introduction

Chapter 2 Visa (Pre-VCR) and MasterCard Chargeback Process

Retrieval Requests........................................................................................................................ 4

First Chargeback........................................................................................................................... 7

Changes to Visa Dispute Resolution Process ...................................................................... 13

MasterCard Arbitration Chargeback ........................................................................................... 15

Visa Arbitration Chargeback ....................................................................................................... 17

Chapter 3 Discover Chargeback Process

Discover Retrieval Requests....................................................................................................... 20

Discover Chargeback.................................................................................................................. 22

Discover Pre-Arbitration.............................................................................................................. 24

Discover Arbitration..................................................................................................................... 25

Chapter 4 American Express Chargeback Process

American Express Inquiry........................................................................................................... 28

American Express Chargeback .................................................................................................. 31

Chapter 5 Visa Claims Resolution Process

Retrieval Request ....................................................................................................................... 34

Collaboration Workflow............................................................................................................... 35

Dispute Reason Codes - Collaboration Workflow................................................................. 36

Allocation Workflow..................................................................................................................... 37

Dispute Reason Codes - Allocation Workflow ...................................................................... 37

Appendix A Terminology

Contents

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

iv

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

v

About This Guide

This manual serves as an overview of the Chargeback process including Retrieval Requests.

Intended Audience

This document is intended for technical personnel and others who with to have a broad understanding of

the chargeback process.

Revision History

This document has been revised as follows:

TABLE 1 Document Revision History

Doc.

Version

Description Location(s)

3.1 Revised some Mastercard Chargeback Reason

Codes/descriptions.

Chapter 2

3.0 Re-branded entire document format due to the Vantiv-Worldpay

merger; replaced many instances of the 'Vantiv' with 'Worldpay.’

All

2.0 Restructure and update document to include Visa Claims

Resolution process.

Chapters 1, 2 and

5

1.10 Replaced Litle with Vantiv in Queue and Cycle names. All

1.9 Replaced LitleXML with cnpAPI. All

1.8 Added American Express chargeback information Chapter 3

1.7 Updated format All

1.6 General update and rebranding. All

About This Guide

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

vi

Document Structure

This manual contains the following sections:

Chapter 1, "Introduction"

This chapter provides information about the Visa and MasterCard chargeback process.

Chapter 3, "Discover Chargeback Process"

This chapter provides information about the Discover Card chargeback process.

Chapter 4, "American Express Chargeback Process"

This chapter provides information about the American Express Card chargeback process.

Appendix A, "Terminology"

This appendix provides definitions of various terms used in this guide.

Documentation Set

Our documentation set also include the items listed below. Please refer to the appropriate guide for

information concerning other Worldpay eComm product offerings.

• Worldpay eComm cnpAPI Reference Guide

• Worldpay eComm iQ Reporting and Analytics User Guide

• Worldpay eComm Chargeback API Reference Guide

• Worldpay eComm PayPal™ Integration Guide

• Worldpay eComm PayFac API Reference Guide

1.5 Removed unused Visa (60) and Discover (4580) Chargeback

Codes

Added Section 1.2.1 and Note on page 14

Chapters 1 and 2

Chapter 1

1.4 Updated Discover chapter for April (2012) Enhancements Chapter 2

1.3 Changed Discover Reason Codes to match what is shown in the

UI.

Chapter 2

1.2 Added chapter providing information about the Discover

chargeback process.

Chapter 2

1.1 Corrections to several illustrations. Chapter 1

1.0 Initial release N/A

TABLE 1 Document Revision History (Continued)

Doc.

Version

Description Location(s)

About This Guide

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

vii

• Worldpay eComm PayFac Portal User Guide

• Worldpay eComm eProtect Integration Guide

• Worldpay eProtect Enterprise Integration Guide

• Worldpay eComm cnpAPI Differences Guide

• Worldpay eComm Scheduled Secure Reports Reference Guide

Typographical Conventions

Table 2 describes the conventions used in this guide.

TABLE 2 Typographical Conventions

Convention Meaning

.

.

.

Vertical ellipsis points in an example mean that information not directly related to

the example has been omitted.

. . . Horizontal ellipsis points in statements or commands mean that parts of the

statement or command not directly related to the example have been omitted.

< >

Angle brackets are used in the following situations:

• user-supplied values (variables)

• XML elements

[ ]

Brackets enclose optional clauses from which you can choose one or more

option.

bold text Bold text indicates emphasis.

Italicized text Italic type in text indicates a term defined in the text, the glossary, or in both

locations.

blue text Blue text indicates a hypertext link.

About This Guide

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

viii

Contact Information

This section provides contact information for organizations within Worldpay eComm.

Chargebacks - For business-related issues and questions regarding financial transactions and

documentation associated with chargeback cases, contact the Chargebacks Department.

Technical Support - For technical issues such as file transmission errors, email Technical Support. A

Technical Support Representative will contact you within 15 minutes to resolve the problem.

Relationship Management/Customer Service - For non-technical issues, including questions

concerning iQ Reporting and Analytics, help with passwords, modifying merchant details, and changes to

user account permissions, contact the Relationship Management/Customer Service Department. If you

are a Payment Facilitator (PayFac), refer to the second table.

Technical Publications - For questions or comments about this document, please address your

feedback to the Technical Publications Department. All comments are welcome.

Chargebacks Department Contact Information

Telephone 1-844-843-6111 (option 4)

E-mail [email protected]

Hours Available Monday – Friday, 7:30 A.M.– 5:00 P.M. EST

Technical Support Contact Information

E-mail ecommercesupport@worldpay.com

Hours Available 24/7 (seven days a week, 24 hours a day)

Relationship Management/Customer Service Contact Information - Merchants

Telephone 1-844-843-6111 (Option 3)

E-mail ecomcustomercare@worldpay.com

Hours Available Monday – Friday, 8:00 A.M.– 6:00 P.M. EST

Relationship Management/Customer Service Contact Information - Payment Facilitators

Telephone 1-844-843-6111 (Option 5)

E-mail PayFacEComm@worldpay.com

Hours Available Monday – Friday, 8:00 A.M.– 5:00 P.M. EST

Technical Publications Contact Information

E-mail [email protected]

About This Guide

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

ix

About This Guide

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

x

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1 • API Release: 5.0

1

1

Introduction

The Chargeback process is a mechanism used by an issuing bank to remove a charge from the

cardholder’s account and to recoup the funds. The issuing bank does this either on behalf of, or at the

request of a cardholder. The consumer or issuing bank can initiate a Chargeback for a variety of reasons

ranging from simple clerical errors, such as duplicate billing, to fraud claims, such as those associated

with identity theft.

The Chargeback process often starts with a request for information called a Retrieval Request. The

Retrieval Request does not have a financial impact and is the only opportunity for you to resolve the issue

before the movement of funds from your account. Whether the process starts with a Retrieval Request or

a Chargeback, the onus is always on you, the merchant, to deliver the required supporting documentation

and prove the case in your favor.

This document provides information concerning the Chargeback process for the various card brands,

including Retrieval Requests. While all card brands have similarities in their chargeback processes, there

are also many differences By having a thorough understanding of the process and by working with your

Chargeback Analyst, you can make informed decisions about which Chargebacks to dispute and how to

do so successfully.

This book contains the following chapters:

• Visa (Pre-VCR) and MasterCard Chargeback Process

• Discover Chargeback Process

• American Express Chargeback Process

• Visa Claims Resolution Process

NOTE: The Worldpay eComm iQ Reporting and Analytics User Guide and the Worldpay eComm

Chargeback API Reference Guide contain additional information concerning the Chargeback

process and working Chargebacks in the system.

Introduction

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1 • API Release: 5.0

2

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

3

2

Visa (Pre-VCR) and MasterCard Chargeback

Process

The Chargeback processes for Visa and MasterCard are virtually identical through the resolution of the

First Chargeback. At that point, the processes diverge for Pre-Arbitration/Arbitration.

This chapter provides information about the Visa and MasterCard Chargeback process, including

Retrieval Requests. By having a thorough understanding of the process and by working with your

Chargeback Analyst, you can make informed decisions concerning which Chargebacks to dispute and

how to do so successfully.

The topics discussed in this chapter are:

• Retrieval Requests

• First Chargeback

• MasterCard Arbitration Chargeback

• Visa Arbitration Chargeback

NOTE: For information about the new Visa Claims Resolution process, which Visa plans on

introducing in April 14, 2018, please refer to Chapter 5, "Visa Claims Resolution Process".

NOTE: The Worldpay eCommerce iQ Reporting and Analytics User Guide and the Worldpay

eComm Chargeback API Reference Guide each contain additional information about the

Chargeback process and working Chargebacks using tools supplied by Worldpay.

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

4

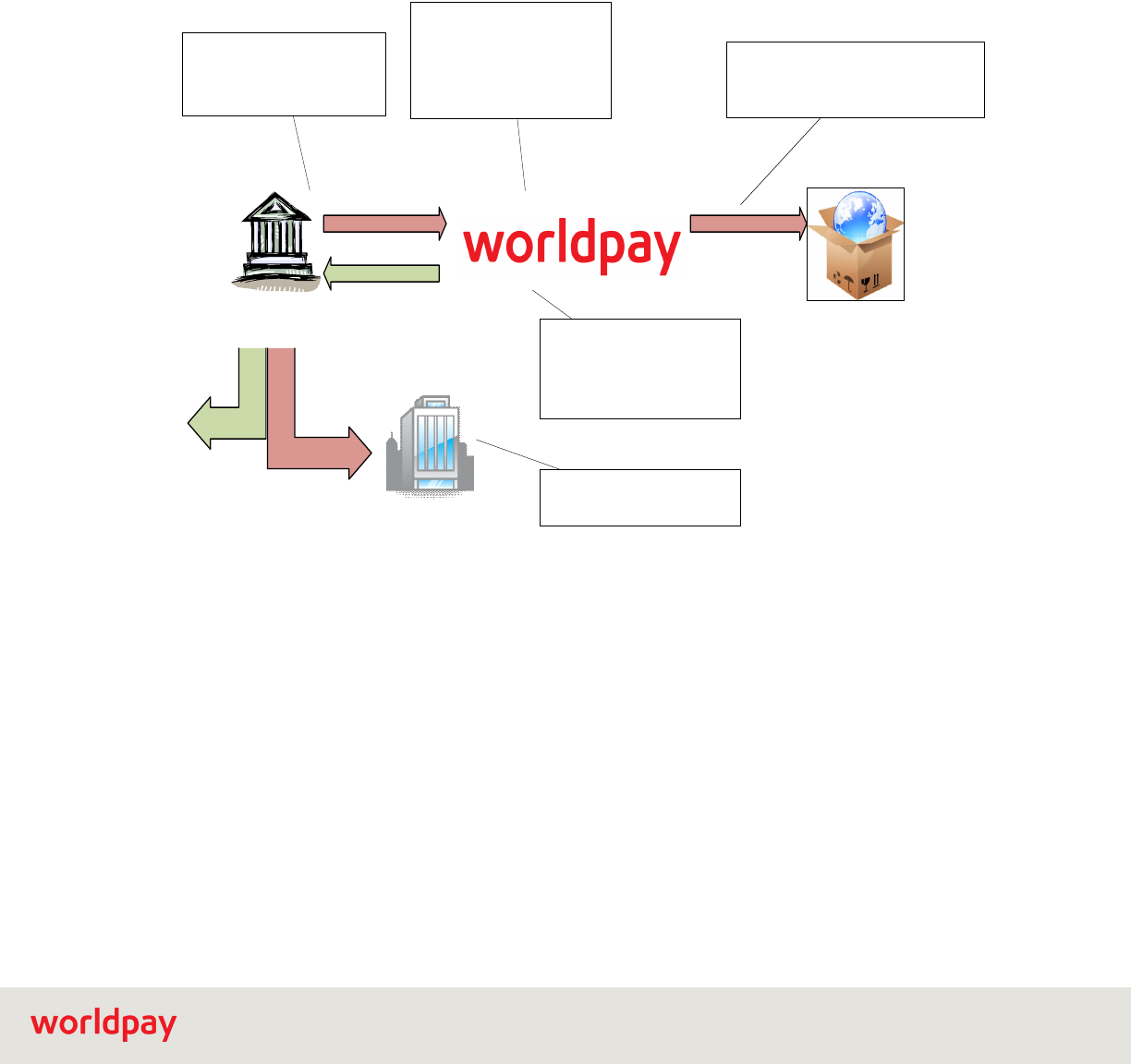

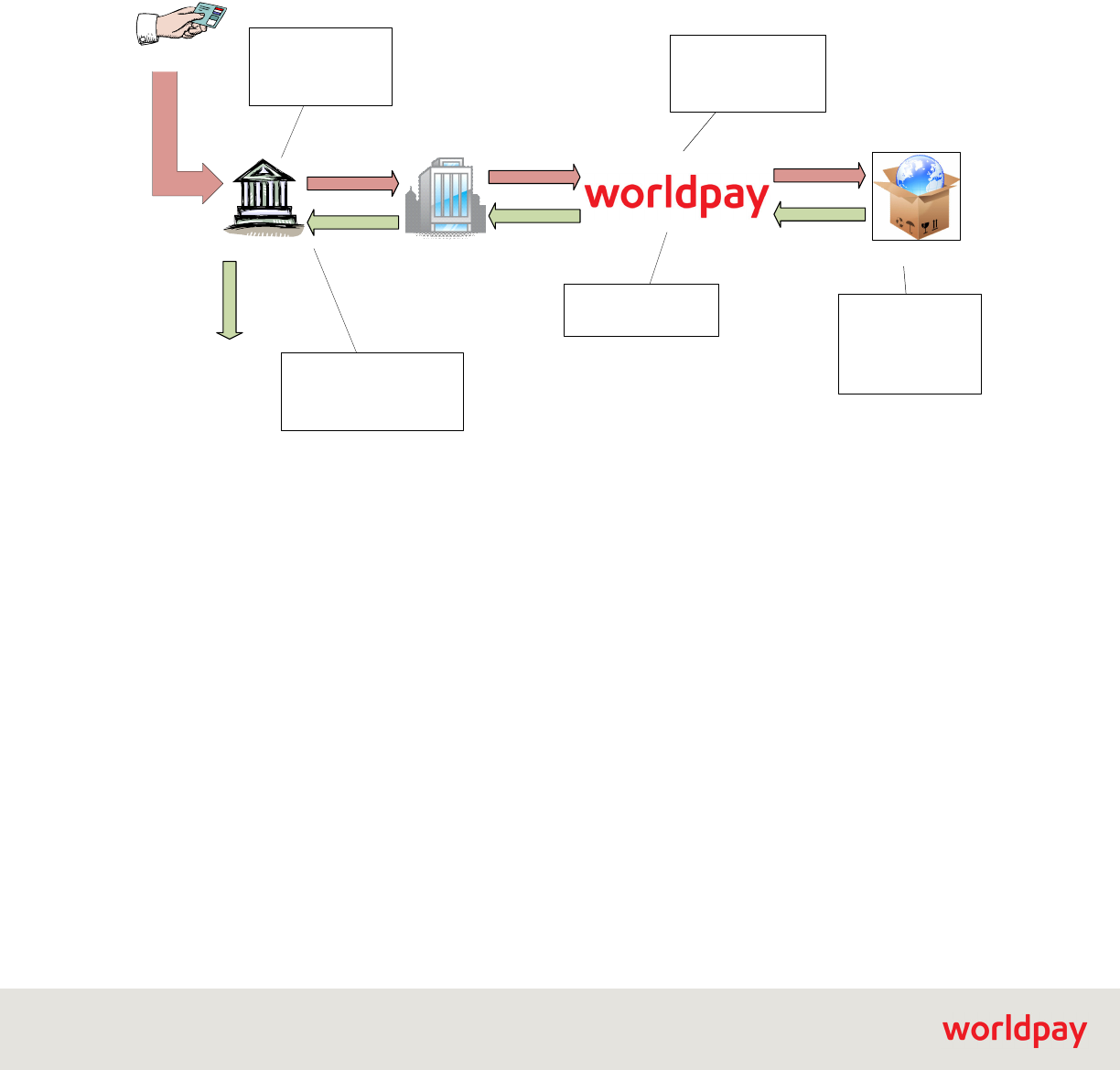

2.1 Retrieval Requests

A Retrieval Request is a request from the cardholder via their issuing bank for a sales draft or other sales

related information; although the request may be for fraud analysis. Retrieval Requests are sometimes

the first step taken by the issuing bank after receiving a cardholder’s complaint concerning a particular

charge on their account. The issuing bank makes the request after examining the complaint and deciding

that a resolution might be reached with additional information from the merchant. The Retrieval Request

includes a Retrieval Request Reason Code providing additional information concerning the cause of the

request and in some cases, the required documentation (see

Table 2-1 and Table 2-2).

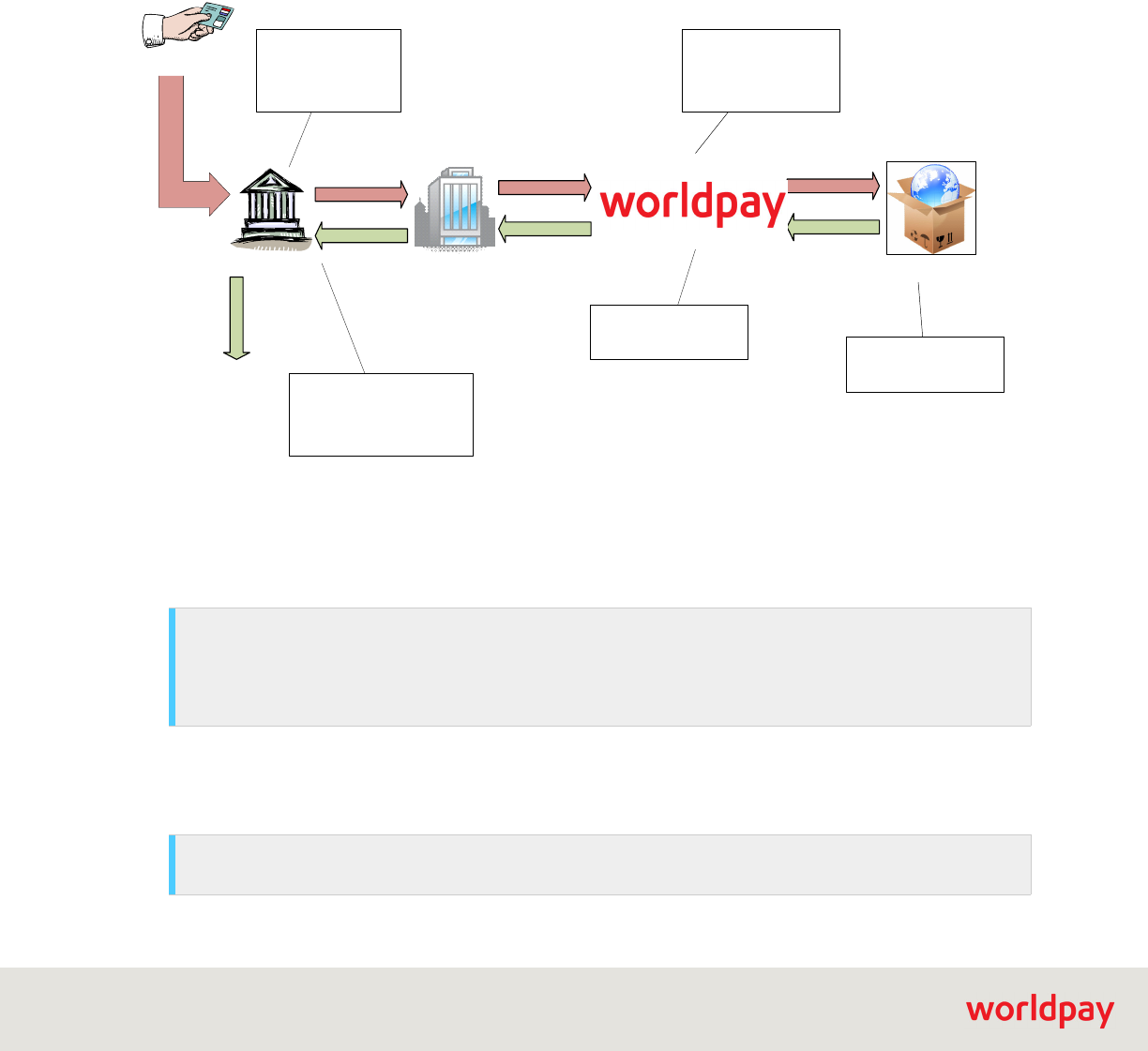

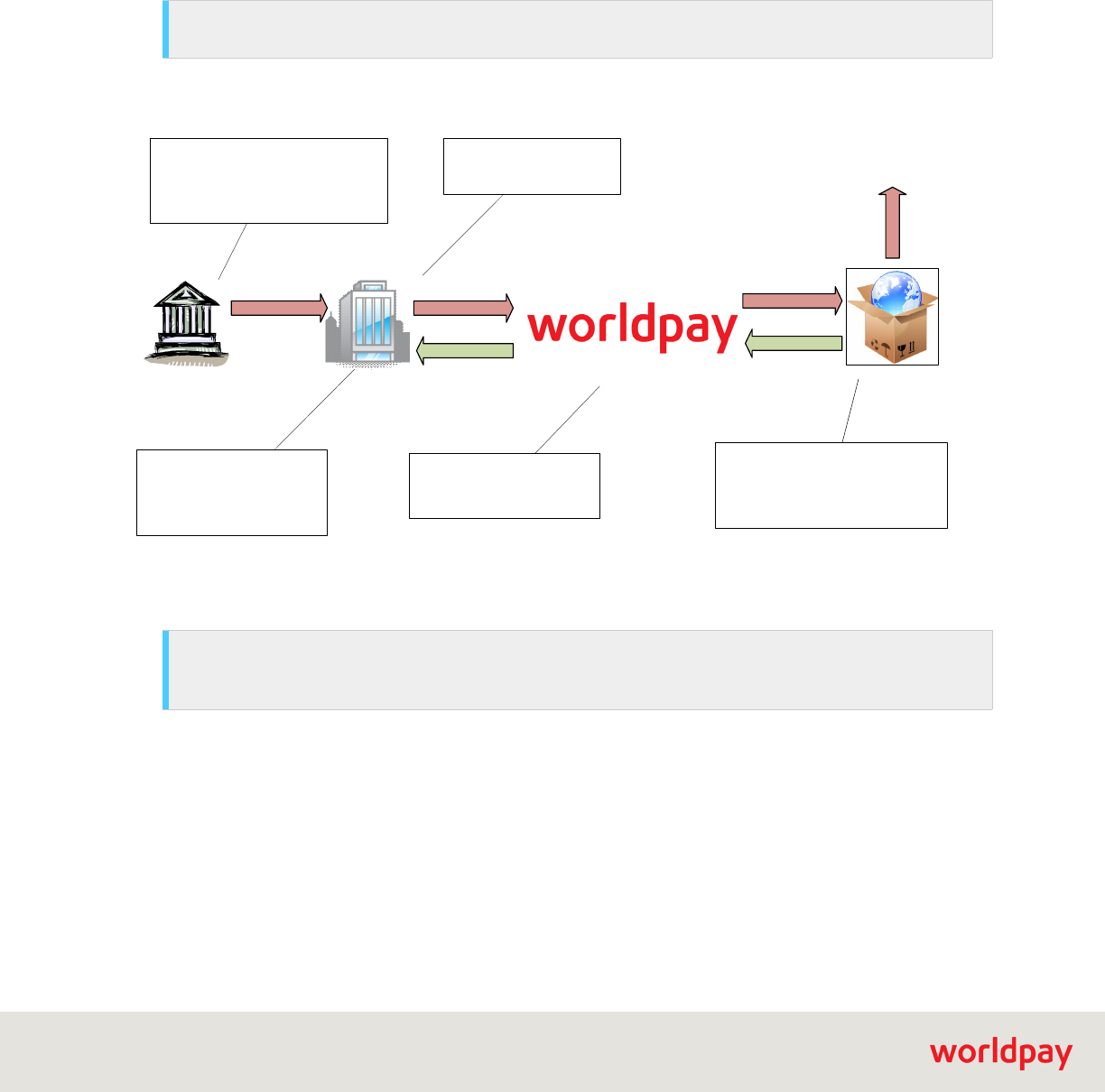

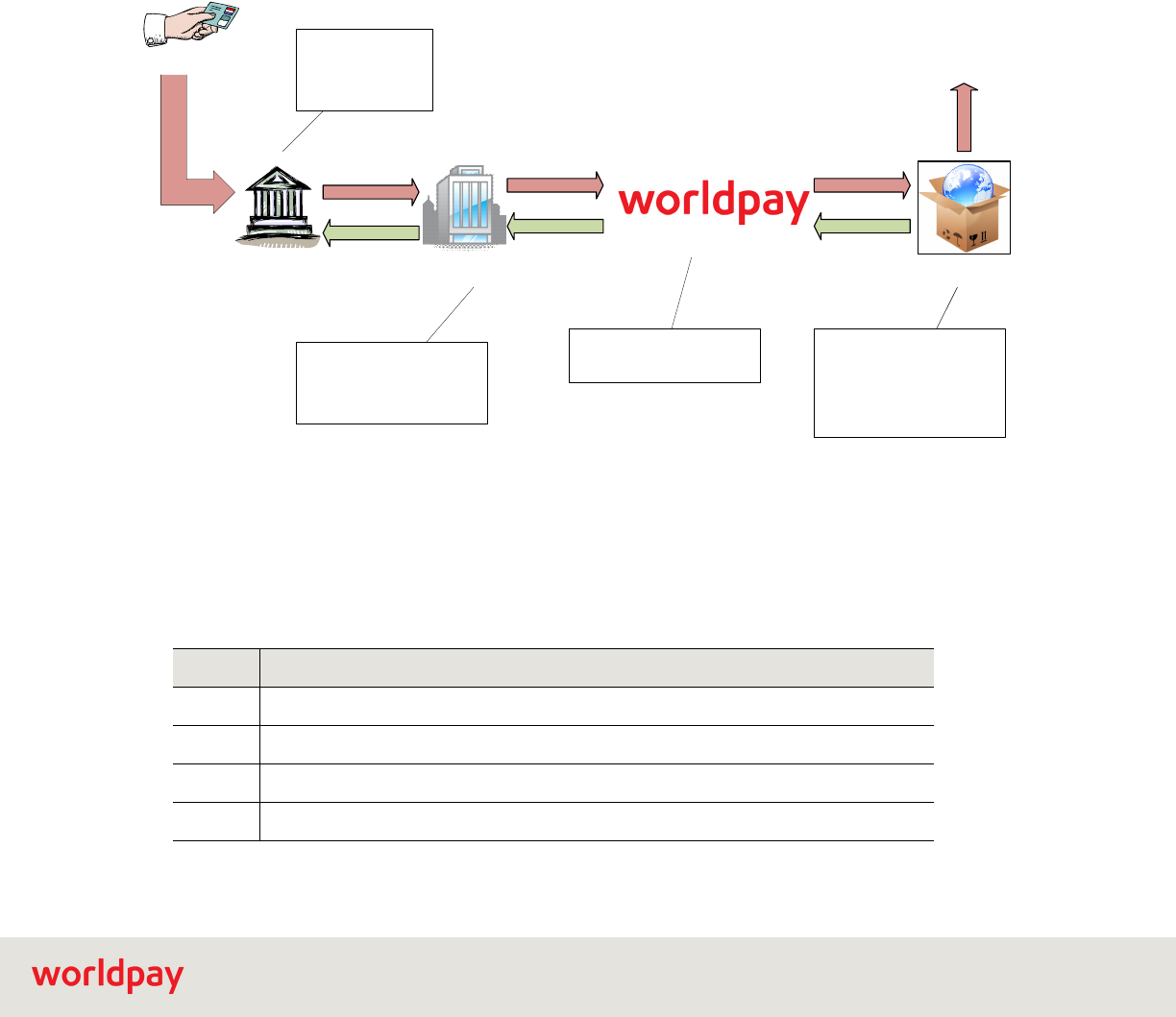

FIGURE 2-1 Retrieval Request Cycle

You should take action as soon as you receive the Retrieval Request. As with any other part of the

Chargeback process, there is a set time limit for you to respond. For a Retrieval Request you have twenty

(20) days to submit the required information to Worldpay for processing and forwarding to the issuer. If

you do not respond in that time frame, the Retrieval Request almost always becomes a Chargeback.

Typically, you must supply records that contain the following information (Worldpay supplies the bold

items from the deposit record):

NOTE: Failure to respond to a Retrieval Request for a MasterCard transaction may result in a

Chargeback with a 4801 Reason Code, for which you will not have dispute rights.

Visa allows you to dispute a Chargeback even if it resulted from a failure to respond to a Retrieval

Request.

NOTE: Visa requires you to maintain the sales data for a minimum of 12 months after the sale

transaction, while the MasterCard requirement is 18 months.

Cardholder

Issuing Bank

Card Assn.

Merchant

Transaction validated

– process ends

If satisfied by the supplied

documentation, the process ends

here. If unsatisfied, the Issuer

initiates a First Chargeback

The Issuer initiates the

process after receiving a

query/complaint from the

cardholder or unilaterally.

Worldpay reviews the

submitted documentation

and responds to the Issuer.

Upon arrival at Worldpay an

automated process

forwards the Retrieval

Request to the Merchant

Queue.

The merchant has 20 days

to respond by submitting

the required documentation.

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

5

• Cardholder’s name

• Cardholder’s account number

• Card expiration date

• Merchant name

• Merchant Address (either physical address or web address for ecommerce merchants)

• Date of sale

• Amount of sale

• Authorization code

• AVS code

• Description of purchased item

• Ship to address

• Proof of delivery

TABLE 2-1 Visa Retrieval Request Codes and Descriptions

Code Message

28 Request for Copy Bearing Signature

30 Cardholder Request Due to Dispute

32 Copy Request because original lost in transit

33 Legal Process or fraud analysis request

34 (if Domestic) Repeat Request for Copy

or

(if International) Legal Process Request

35 Written cardholder request for original due to inadequate copy of mail/phone order or

recurring transaction receipts

36 Legal Process request for original

38 Paper/Handwriting analysis request

39 Repeat Request for original copy

40 Arbitration Request

TABLE 2-2 MasterCard Retrieval Request Codes and Descriptions

Code Message

6321 Cardholder does not recognize the transaction

6323 Request for Copy

6341 Fraud Investigation

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

6

6342 Potential Chargeback or Compliance Documentation

TABLE 2-2 MasterCard Retrieval Request Codes and Descriptions (Continued)

Code Message

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

7

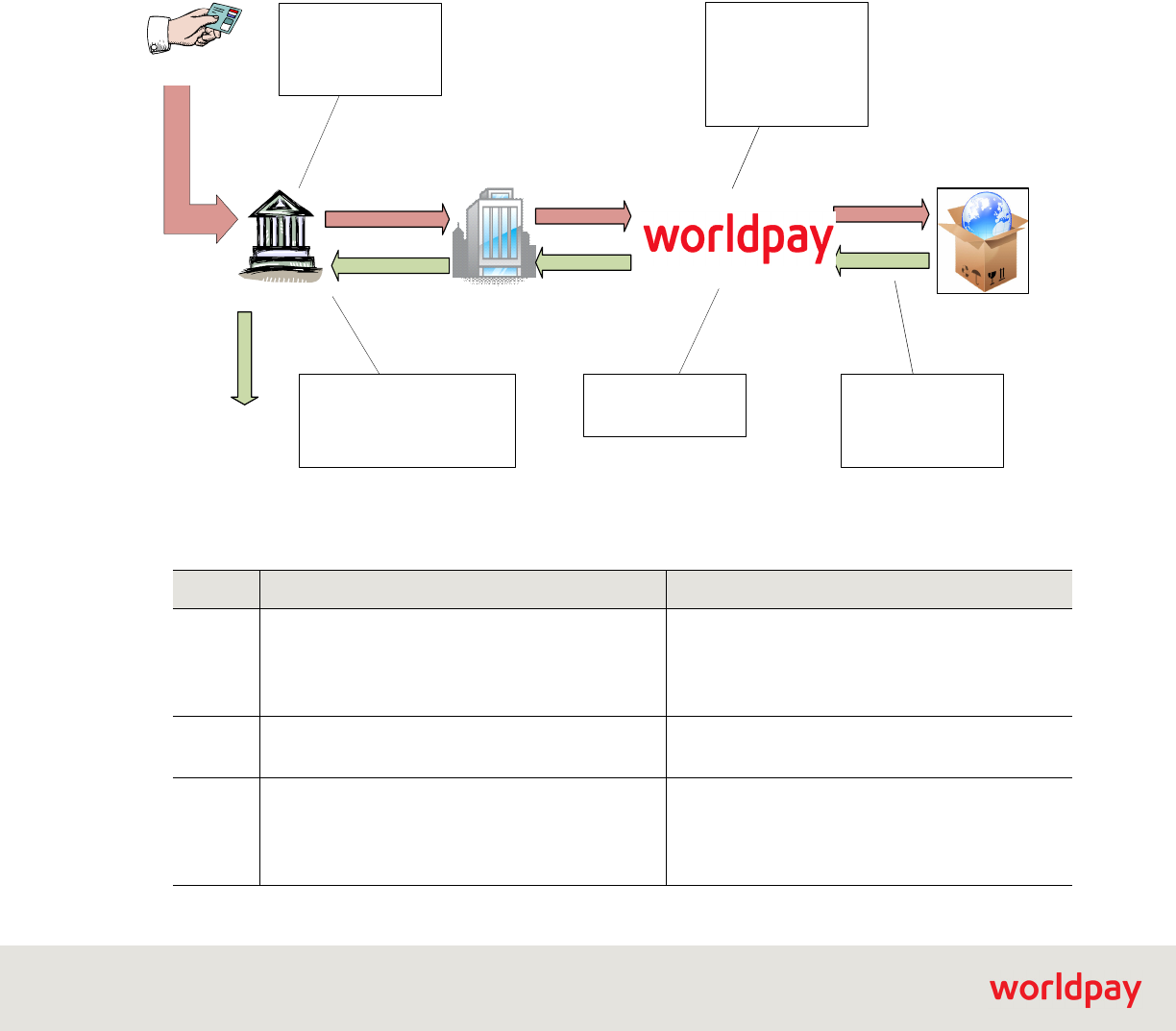

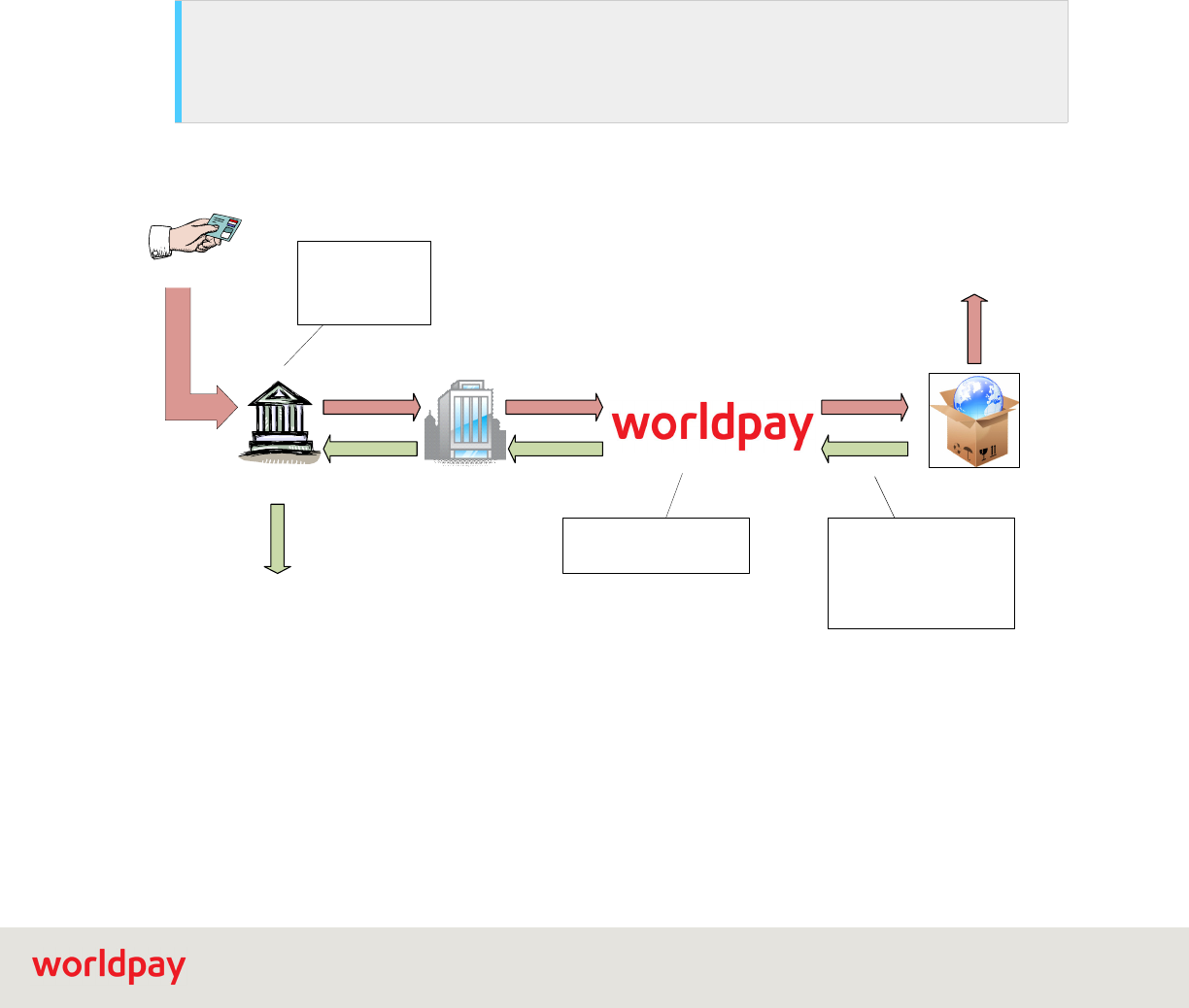

2.2 First Chargeback

The issuing bank initiates a First Chargeback on behalf of the cardholder by sending notification to

Worldpay explaining the dispute. After Worldpay receives the chargeback, we assign it to you for review

by moving it from the Vantiv Queue to the Merchant Queue. At the time the chargeback moves to the

Merchant Queue, your merchant account is debited for the amount of the chargeback.

You review the chargeback and, based upon the reason code, decide whether to represent the

transaction (dispute the chargeback) or to accept the chargeback. If you decide to accept the chargeback,

you move the chargeback into the Merchant Assumed Queue using the Merchant Accept Liability activity.

If you elect to represent the transaction, you attach supporting documentation and move the chargeback

to the Vantiv Outgoing Queue using the Merchant Represent activity. You must respond within 30 days.

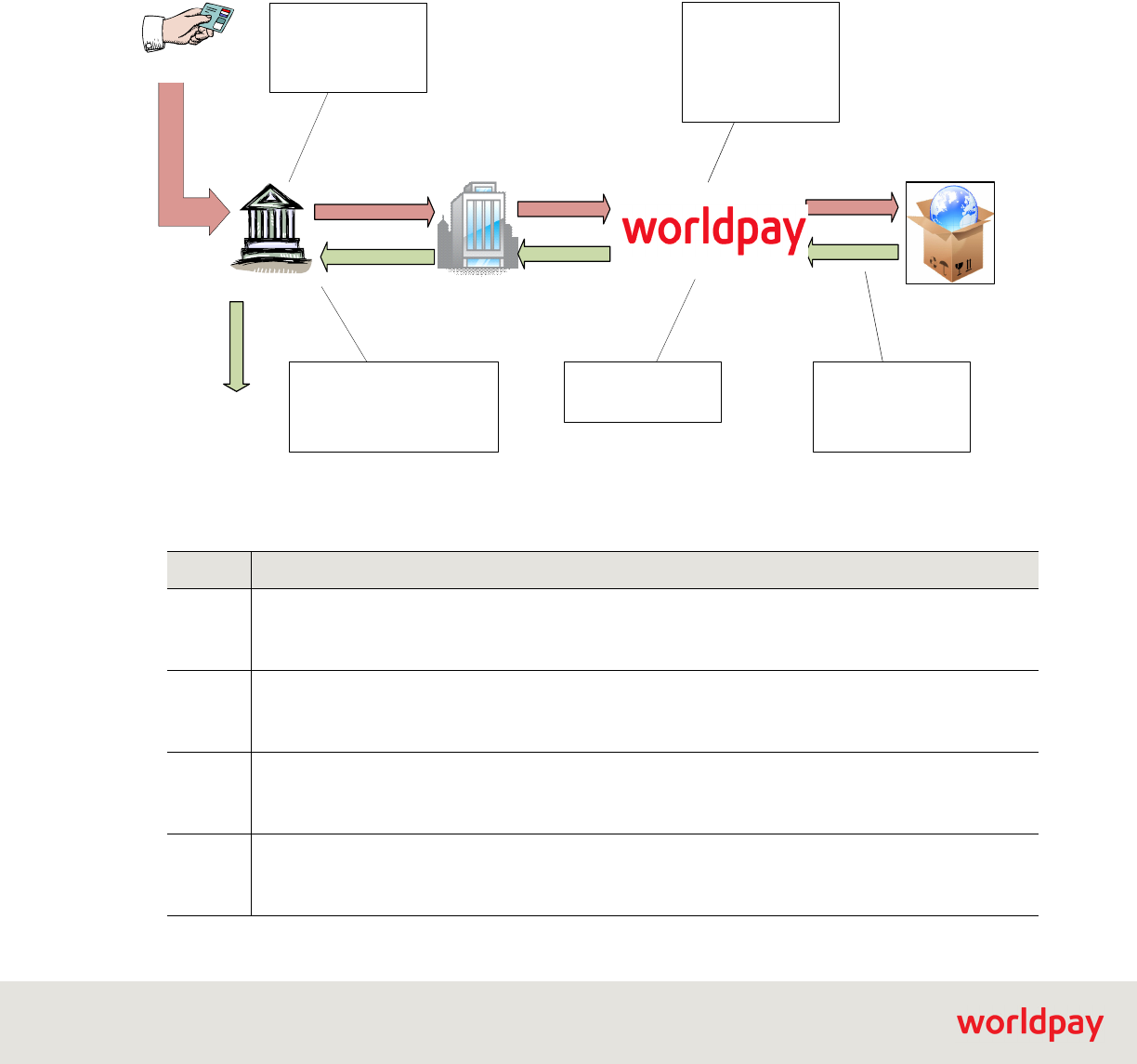

FIGURE 2-2 First Chargeback Cycle

Once the chargeback moves to the Vantiv Outgoing Queue, the Chargeback Analyst prepares the

response, verifying that all required fields are complete, and submits it through the card network back to

the Issuing bank. Upon the representment, when you move the chargeback from the Merchant Queue to

the Vantiv Outgoing Queue, your merchant account is credited the representment amount.

The Issuing bank has 45 days after the representment to issue an Arbitration Chargeback, in the case of

MasterCard, or request Pre-Arbitration/Arbitration in the case of Visa. This action by the Issuing bank, if

taken, generates a new case in the system.

Cardholder

Issuing Bank

Card Assn.

Merchant

The Merchant may assume

liability and end the process.

Transaction validated

– process ends

Merchant credited

Representment

amount

If satisfied by the representment,

the process ends here. If

unsatisfied, the Issuer escalates

to the next stage which varies

depending upon if this is a Visa

or MasterCard transaction.

The Issuer initiates the

First Chargeback after

receiving a complaint

from the cardholder or

unilaterally.

Worldpay reviews the

Representment and support

documentation and responds to

the Issuer.

If the merchant elects to

represent the transaction, they

attach the required supporting

documentation to the case and

submit it to Worldpay.

Merchant debited

chargeback amount

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

8

TABLE 2-3 Visa Chargeback Reason Codes and Descriptions

Code Message Necessary Action

30 Services Not Rendered or Merchandise Not

Received

Note: Also see Changes to Visa Dispute

Resolution Process on page 13.

Provide proof that cardholder/authorized

representative received

merchandise/services, or provide statement

indicating merchant did not receive returned

merchandise, or provide proof that a credit

was processed.

41 Cancelled Recurring Transaction Provide proof that charge was within

preauthorize range of amounts and provide

proof that you sent the cardholder

notification 10 days in advance of charge

and no response was received back denying

consent for charge to be posted, or provide

proof that a credit was processed.

53 Not as Described or Defective Merchandise

Note: Also see Changes to Visa Dispute

Resolution Process on page 13.

Provide proof that you fixed any deficiency

that led to the chargeback, or that the items

were as described, or provide proof that a

credit was processed.

57 Fraudulent Multiple Transactions Provide proof that multiple fraudulent

transactions did not occur and multiple

transactions were authorized by cardholder,

or provide proof that a credit was processed.

62 Counterfeit Transaction Provide proof that the

account-number-verifying Terminal at the

member/merchant outlet could not read the

magnetic stripe, or that the authorization

record contains a POS entry mode code of

“90” or “05” or a valid online card

authentication cryptogram, or provide proof

that a credit was processed.

70 Account Number on Exception File Provide proof that the account number was

not listed on the Exception file with a “pick

up” response at 8PM PST on the date

preceding the transaction date, or that

Account Number Verification or

Authorization was obtained, or that the

transaction was Chip-initiated and

authorized offline, or provide proof that a

credit was processed.

71 Declined Authorization Provide proof that valid authorization was

obtained on the transaction date, or that

transaction date is different, or transaction

was Chip-initiated and authorized offline, or

provide proof that a credit was processed.

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

9

72 No Authorization Provide proof authorization was obtained on

the transaction date, or Authorization for a

Mail/Phone Order or Electronic Commerce

Transaction was obtained within 7 calendar

days prior to the Transaction Date and

merchandise was shipped or delivered, or

provide proof that a credit was processed.

73 Expired Card Provide proof that card was not expired on

the Transaction Date, or that Merchant

obtained Authorization, or that transaction

was Chip-initiated and authorized offline, or

provide proof that a credit was processed.

74 Late Presentment Provide proof that the transaction was not

processed more than 30 days after the

actual transaction date, or provide proof that

a credit was processed.

75 Cardholder Does Not Recognize

Transaction

Provide documentation to assist cardholder

in recognizing the transaction

(membership/order and ship information), or

provide proof that a credit was processed.

76 Incorrect Transaction Code Provide proof the transaction was processed

properly (purchase was not intended to be a

credit), or provide proof that a credit was

processed.

77 Non-Matching Account Number Provide proof that the card number is

correct, or Authorization was obtained from

Issuer, the Issuer's Authorizing Processor,

or Stand-In-Processing, or provide proof that

a credit was processed.

80 Incorrect Transaction Amount or Account

Number

Provide proof that the transaction receipt is

correct or was not altered, or that cardholder

agreed to altered amount, or for MOTO

merchants that account number is correct

and authorization was obtained, or provide

proof that a credit was processed.

81 Fraudulent Transaction - Card Present

Environment

Note: Also see Changes to Visa Dispute

Resolution Process on page 13.

Provide proof that the transaction receipt

contains both a signature (or PIN) and an

imprint, or provide proof that a credit was

processed.

82 Duplicate Processing Provide proof that two different transactions

were processed, or provide proof that a

credit was processed.

TABLE 2-3 Visa Chargeback Reason Codes and Descriptions (Continued)

Code Message Necessary Action

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

10

83 Fraudulent Transaction - Card Absent

Environment

Note: Also see Changes to Visa Dispute

Resolution Process on page 13.

Provide proof that merchandise or a service

was ordered through a Mail/Phone Order or

Electronic Commerce Transaction, AND it

was shipped/delivered, AND Acquirer

received a “U” or “Y” AVS response

(address + 5 or 9 zip matched), AND

merchandise was delivered to this same

AVS address; or CVV2 code was U and the

presences indicator was 1, 2 or 9, or provide

proof that a credit was processed.

85 Credit Not Processed Provide statement that returned goods were

not received, or proof of proper disclosure of

refund policies at the time of the

Transaction, AND proof that

merchandise/services were delivered to

cardholder, or provide proof that a credit

was processed.

86 Paid By Other Means Provide proof that merchandise or services

were not paid for by an alternate means, or

provide proof that a credit was processed.

90 Services Not rendered - ATM or Visa Travel

Money

Provide proof that cardholder received

funds, or provide proof that a credit was

processed.

93 Risk Identification Service Provide proof that issuer already charged

back the transaction for another reason, or

provide proof that a credit was processed.

96 Transaction Exceeds Limited Amount Provide proof that transaction type was not

for a Self-Service or Limited-Amount

Terminal, or that transaction was less than

the allowed amount, or provide proof that a

credit was processed.

TABLE 2-4 MasterCard Chargeback Reason Codes and Descriptions

Code Message Necessary Action

4801 Requested Transaction Data Not Received No dispute rights. You must accept the

Chargeback.

If you fulfilled the Retrieval Request, or you

processed a credit previously, please

contact your Chargeback Analyst to discuss

options.

TABLE 2-3 Visa Chargeback Reason Codes and Descriptions (Continued)

Code Message Necessary Action

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

11

4802 Requested/Required Information Illegible or

Missing

Provide the missing or illegible information

requested, or proof that a credit was

processed.

4807 Warning Bulletin Filed Provide proof of valid authorization, proof

that the account was not on the warning

bulletin list on date of transaction, or proof

that a credit was processed.

4808 Authorization Related Provide proof of valid authorization, or proof

that the transaction date was incorrect

(supply corrected one), or proof that a credit

was processed.

4812 Account Number Not on File Provide proof that this is a valid card

number, or bill the corrected account number

and accept the chargeback, or contact the

cardholder for a new form of payment and

accept the chargeback, or proof that a credit

was processed.

4831 Transaction Amount Differs Provide proof that the transaction amount is

correct, that you had cardholder permission

to increase debit, or proof that a credit was

processed.

4834 Point of Interaction Errors Provide proof that the transactions are

separate/different transactions, or proof that

a credit was processed.

4835 Card Not Valid or Expired Provide proof of a valid Authorization from

Issuer or MasterCard, or proof that a credit

was processed.

4837 No Cardholder Authorization Provide proof that you have a positive AVS

(address +5 or 9 zip match) and that you

shipped to this same AVS approved

address, or that issuer did not respond to

your CVC2 request (response U), or proof

that a credit was processed.

4840 Fraudulent Processing of Transactions Provide proof that you are processing

multiple transaction to the card with

cardholder permission along with a letter

explaining the charges, or proof that a credit

was processed.

4841 Cancelled Recurring Transaction Provide proof that this is not a recurring

charge but may instead be an installment

billing, or proof that a credit was processed.

TABLE 2-4 MasterCard Chargeback Reason Codes and Descriptions (Continued)

Code Message Necessary Action

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

12

4842 Late Presentment Provide proof that the transaction date was

originally submitted incorrectly and provide

incorrect and corrected dates, or proof that a

credit was processed.

4846 Correct Transaction Currency Code Not

Provided

Provide proof that the correct transaction

amount and currency code were submitted,

or proof that a credit was processed.

4847 Exceeds Floor Limit, Not Authorized and

Fraudulent Transaction

Provide proof that the full transaction amount

was authorized by issuer or MasterCard, that

partial transaction amount was authorized

(only dispute partial amount), or proof that a

credit was processed.

4849 Questionable Merchant Activity Provide proof that the card acceptor was not

listed on the MasterCard Global Security

Bulletin at time of transaction, or proof that a

credit was processed.

4850 Credit Posted as a Purchase Provide proof that the transaction should

have been processed as a purchase and not

a credit, or proof that a credit was

processed.

4853 Cardholder Disputes Provide proof that you fixed any deficiency

that led to the chargeback, that the items

were as described, or proof that a credit was

processed.

4854 Cardholder Dispute - Not Elsewhere

Classified (US only)

Provide proof that contradicts the issuers

supporting documentation, or proof that a

credit was processed.

4855 Non-receipt of Merchandise Provide signed proof that the cardholder or

person that the cardholder authorized

received the merchandise, proof that the

cardholder picked the merchandise up at

your location, or proof that a credit was

processed.

4857 Card-Activated Telephone Transaction Provide proof that the transaction is not a

Card-Activated Telephone transaction, or

proof that a credit was processed.

4859 Services Not Rendered Provide proof that the services were

rendered; or that the cardholder was advised

of the no-show policy, or proof that a credit

was processed.

TABLE 2-4 MasterCard Chargeback Reason Codes and Descriptions (Continued)

Code Message Necessary Action

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

13

2.2.1 Changes to Visa Dispute Resolution Process

As of April 20, 2013, Visa allows merchants to provide additional types of compelling evidence for certain

Chargeback Reason Codes to try to prove the cardholder participated in the transaction, received the

goods or services, or benefited from the transaction. This only applies to the following Chargeback

Reason Codes: 30, 53, 81, and 83.

4860 Credit Not Processed Provide a statement that you did not agree

to credit cardholder, have not received

merchandise back or a cancellation of

services request, or that the cancellation

policy was disclosed to the cardholder at

point of interaction (provide policy), or proof

that a credit was processed.

4863 Cardholder Does Not Recognize - Potential

Fraud

Provide documentation showing dates and

information about service agreement, order

information, proof of delivery, contract, and

any other information that will assist

cardholder in identifying the transaction, or

proof that a credit was processed.

4870 Chip Liability Shift Provide documentation showing that the

liability shift does not apply because the

transaction was completed with chip, the

chargeback was invalid for other reasons,

such as the that terminal was a hybrid, or by

showing that the card involved was not a

hybrid card.

4871 Chip Liability Shift - Lost/Stolen/NRI

TABLE 2-5 Allowable Compelling Evidence

Chargeback Reason

Codes Allowable Compelling Evidence

30, 53, 81, and 83 Evidence, such as photographs or emails, to prove a link between the person

receiving the merchandise and the cardholder, or to prove that the cardholder

disputing the transaction is in possession of the merchandise.

30, 81, and 83 For a card-not-present (CNP) transaction, when the merchandise is picked up

at the merchant location, any of the following:

• Cardholder signature on the pick-up form

• Copy of identification presented by the cardholder

• Details of identification presented by the cardholder

TABLE 2-4 MasterCard Chargeback Reason Codes and Descriptions (Continued)

Code Message Necessary Action

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

14

30, 81, and 83 For a CNP transaction in which the merchandise is delivered, documentation

that the item was delivered to the same physical address for which the

merchant received an AVS match of "Y" or "M" (evidence of delivery and time

delivered).

A signature is not required as evidence of delivery.

30, 81, and 83 For ecommerce transactions representing the sale of digital goods

downloaded from a website, one or more of the following:

• Purchaser's IP address

• Purchaser's email address

• Description of the goods downloaded

• Date and time goods were downloaded

• Proof that the merchant's website was accessed for services after the

transaction date

30, 81, and 83 For transactions in which merchandise was delivered to a business address,

evidence that the merchandise was delivered and that, at the time of delivery,

the cardholder was an employee of the company at that address (e.g.,

confirmation that the cardholder was listed in the company directory or had an

email address with the company's domain name).

A signature is not required as evidence of delivery.

30, 81, and 83 For a Mail Order/Phone Order transaction, a signed order form.

30, 81, and 83 For passenger transport transactions, any of the following:

• Proof that the ticket was received at the cardholder's billing address

• Evidence that the boarding pass was scanned at the gate

• Details of frequent flyer miles claimed, including address and telephone

number, that established a link to the cardholder

• Evidence of additional transactions related to the original transaction, such

as purchase of seat upgrades, payment for extra baggage or purchases

made on board the aircraft

81 and 83 For CNP transactions, evidence that the transaction uses data such as IP

address, email address, physical address and telephone number that had

been used in a previous, undisputed transaction.

81 and 83 Evidence that the transaction was completed by a member of the cardholder's

household.

TABLE 2-5 Allowable Compelling Evidence (Continued)

Chargeback Reason

Codes

Allowable Compelling Evidence

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

15

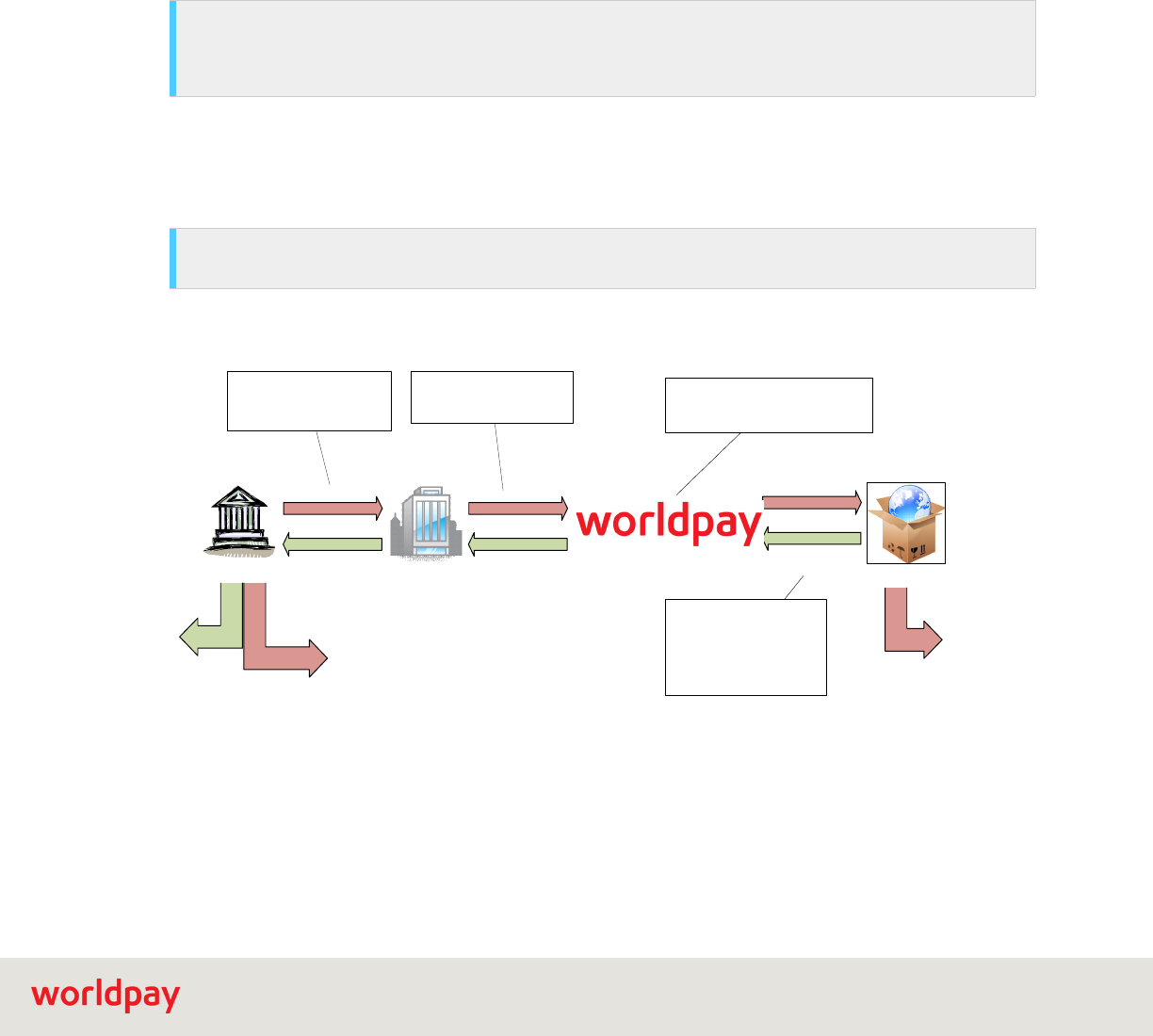

2.3 MasterCard Arbitration Chargeback

After the First Chargeback cycle the process differs between MasterCard and Visa. With a MasterCard

transaction the process for a Arbitration Chargeback is similar to a First Chargeback. The Issuing bank

submits the Arbitration Chargeback within 30 days of the representment, along with an explanation of

what additional documentation you must supply in order to pursue the case further. Once again, your

merchant account is debited the amount of the chargeback.

You must decide whether or not to assume the Arbitration Chargeback. If you decide to pursue the case,

you must submit new supporting documentation to prove the validity of the transaction within 35 days of

receiving the Arbitration Chargeback and use the Merchant Requests Arbitration action to move the case

to the Merchant Arbitrate Queue. The Chargeback Analyst determines if the case should go to Arbitration

or if Pre-arbitration (member mediation) and moves the case to the Pre-Arbitrate Queue or Arbitrate

Queue as appropriate.

FIGURE 2-3 MasterCard Arbitration Chargeback Cycle

Pre-arbitration is a review process that occurs within the MasterCard MasterCom system between the

Issuing bank and Worldpay without the involvement of the association. During this time, the case remains

in the Pre-Arbitrate Queue. The Issuing bank has the option of refusing to participate in the review of the

case. If the bank declines the case, your merchant account is debited the transaction amount.

If the results of Pre-arbitration are unfavorable, you can still bring the case to Arbitration; however, doing

so is potentially expensive. For MasterCard, there is an initial Filing Fee of $150 and a Review Fee of

$250. The loser of the Arbitration decision is liable for both fees. It is also possible for MasterCard to

NOTE: Current rules prohibit Dispute Resolution Management from reviewing merchant

documentation in an arbitration case that should have been presented in chargeback cycles unless

a change of code occurred with the arbitration chargeback. As of 19 April 2013, in specific

scenarios, merchants will be allowed to submit documentation with an arbitration case filing. By

making this change, MasterCard is providing merchants with the ability to review progressive

documentation from the cardholder in response to the second presentment, and provide further

insight into the reason why the transaction should be the issuer’s responsibility.

Issuing Bank

Card Assn.

Merchant

Merchant Assumes Liability –

process ends

If the case goes to Arbitration, a

MasterCard committee makes

the final decision.

The Issuer initiates the Arbitration

Chargeback after determining

that the Representment does not

prove the validity of the charge.

Worldpay reviews the new

information and determines

whether to seek Pre-arbitration

or file an Arbitration case.

The merchant has two options:

Assume Liability

Request Pre-Arbitration/Arbitration

To proceed with the dispute, the

merchant must present new information.

Merchant debited

disputed amount

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

16

charge a $100 fee for each Technical Error associated with the case. MasterCard can assess Technical

Error Fees against either party, win or lose.

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

17

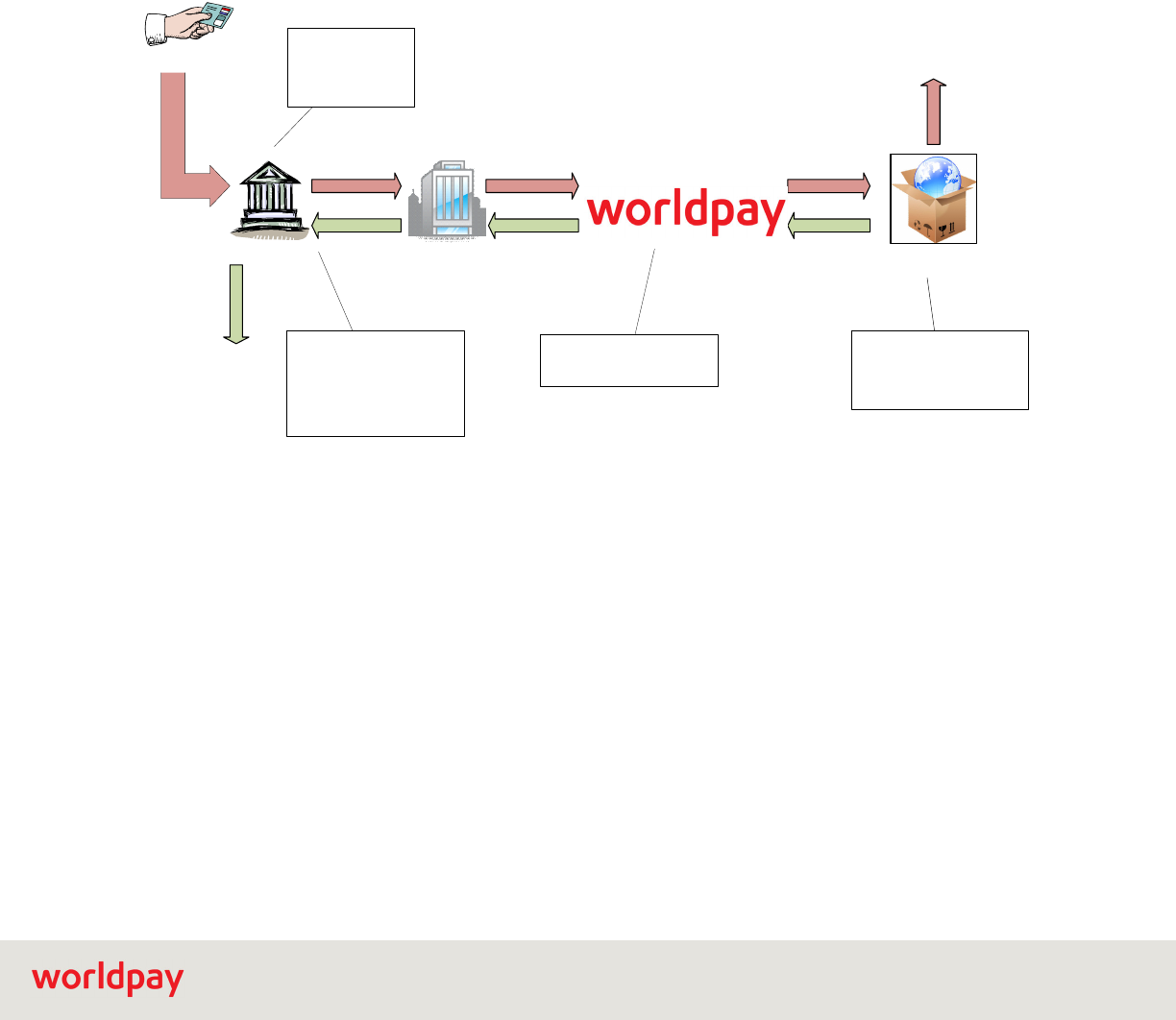

2.4 Visa Arbitration Chargeback

The primary difference between the MasterCard system and the Visa system for Pre-Arbitration and

Arbitration is that the decision to escalate the case resides with the Issuing bank and not the merchant. If

the Issuing bank does not agree with the merchant’s representment, they have two options:

• file a Pre-Arbitration case in the Visa ROL system

• send the case directly to Arbitration

FIGURE 2-4 Visa Pre-Arbitration/Arbitration

If the Issuer files a Pre-Arbitration case, Worldpay reviews the case and responds on behalf of the

merchant. If Worldpay accepts the case, the merchant is debited the disputed amount. If Worldpay

declines the case, the Issuer has the option of filing with Visa for Arbitration. At that point, you have the

option to withdraw from Arbitration, but are liable for a $250 fee.

If the case goes to Arbitration, a Visa committee issues a binding decision with the losing party paying the

Filing Fee of $250 and a Review Fee of $250. As with MasterCard, Technical Error Fees ($100 for each

technical violation of the Visa USA Inc. Operating Regulations) may also be assessed at the discretion of

Visa.

Issuing Bank

Card Assn.

Merchant

If Worldpay declines the case,

the Issuer can go to arbitration.

If the Issuer requests Arbitration,

you can still withdraw, but must

pay a $250 fee.

The Issuer can either file a Pre-

Arbitration case in the Visa ROL

system, or go straight to

Arbitration.

Chargeback Analyst reviews the

Pre-Arbitration case and

responds on behalf of the

merchant. Cases do not appear

in the Worldpay system

Pre-Arbitration

If Worldpay accepts the Pre-Arbitration

case, a new case is established in the

system and your merchant account is

debited the pre-arbitration amount.

If the case goes to Arbitration, a

Visa committee makes the final

decision.

Arbitration

Issuer Accepts

Visa (Pre-VCR) and MasterCard Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

18

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

19

3

Discover Chargeback Process

While the overall process for Discover Chargebacks is similar to both Visa and MasterCard there are

several differences. This section will discuss the entire Discover process, highlighting the differences

where applicable.

The sections of this chapter are:

• Discover Retrieval Requests

• Discover Chargeback

• Discover Pre-Arbitration

• Discover Arbitration

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

20

3.1 Discover Retrieval Requests

A Discover Ticket Retrieval Request is similar to a Retrieval Request used in the Visa and MasterCard

processes. It is a request by Discover for documentation regarding a transaction where the Cardholder or

Issuer believes that the underlying Card Transaction is invalid and seeks compelling evidence from the

Acquirer or Merchant supporting the validity of the transaction. Discover may have initiated the request on

its own behalf or on behalf of a Cardholder. As with any other part of the Chargeback process, there is a

set time limit for you to respond. You have twenty (20) days to submit the required information to

Worldpay for processing and forwarding to the Discover. For Reason Codes 6005, 6021, 6029, and

6041(see

Table 3-1), failure to respond will likely result in a Chargeback for which you do not have

representment rights.

FIGURE 3-1 Discover Retrieval Requests

TABLE 3-1 Discover Retrieval Request Codes and Descriptions

Code Message Description

6005 Transaction Documentation Request Due to

Cardholder Dispute

The Cardholder/Issuer requests a copy of

the transaction documentation for a

transaction that the Cardholder alleges is

invalid.

6021 Transaction Documentation Request The Cardholder/Issuer requests a copy of

the transaction documentation.

6029 Transaction Documentation Request - T & E The Cardholder/Issuer requests a copy of

the transaction documentation for a

transaction submitted by the merchant in the

travel or entertainment industry.

Cardholder

Issuing Bank

Discover

Merchant

Transaction validated

– process ends

If satisfied by the supplied

documentation, the process ends

here. If unsatisfied, the Issuer initiates

a Chargeback.

The Issuer initiates the

process after receiving a

query/complaint from the

cardholder or unilaterally.

Worldpay reviews the

submitted documentation

and responds to the Issuer.

Upon arrival at Worldpay an

automated process

forwards the Retrieval

Request to the Merchant

Queue. This is true for

either type.

The merchant has 20 days

to respond by submitting

the requested/required

documentation.

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

21

6040 Good Faith Investigation The Cardholder/Issuer challenges the

validity of a transaction after the expiration of

the standard Dispute initiation time frame.

6041 Transaction Documentation Request for

Fraud Analysis

The Issuer requests a copy of the

transaction documentation in connection with

a fraud investigation.

TABLE 3-1 Discover Retrieval Request Codes and Descriptions (Continued)

Code Message Description

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

22

3.2 Discover Chargeback

From a process flow standpoint, the Discover Chargeback and Representment process is virtually

identical to that of Visa or MasterCard. Typically, the issuing bank initiates a First Chargeback on behalf

of the cardholder by sending notification to Worldpay explaining the dispute. After Worldpay receives the

chargeback, we assign it to you for review by moving it from the Vantiv Queue to the Merchant Queue.

At this point, you review the chargeback and decide whether to represent the transaction (dispute the

chargeback) or to accept the chargeback. If you decide to accept the chargeback, you move the

chargeback into the Merchant Assumed Queue using the Merchant Accept Liability activity. If you elect to

represent the transaction, you attach supporting documentation and move the chargeback to the Vantiv

Outgoing Queue using the Merchant Represent activity. You must respond within 35 days.

FIGURE 3-2 Discover Chargeback and Representment Cycle

Once the chargeback moves to the Vantiv Outgoing Queue, the Chargeback Analyst prepares the

response, verifying that all required fields are complete, and submits it through the card network back to

the Issuing bank.

If the Issuing bank disagrees with your Representment Request or the Representment request decision

made by Discover, it has 30 days after the Representment to issue a Pre-Arbitration Inquiry. This action

by the Issuing bank, if taken, generates a new case in the system.

NOTE: The Discover Network may issue a Chargeback unilaterally for failure to comply with

Operating Regulations based upon the response to the Dispute Retrieval Request

Cardholder

Issuing Bank

Discover

Network

Merchant

The Merchant may assume

liability and end the process.

Merchant credited

Representment

amount

Discover renders a decision.

The losing party can escalate to

the next stage – PreArbitration

for Issuer, or Arbitration for

Merchant.

The Issuer initiates the

First Chargeback after

receiving a complaint

from the cardholder or

unilaterally.

Worldpay reviews the

Representment and support

documentation and responds to

the Issuer.

If the merchant elects to

represent the transaction, they

attach the required supporting

documentation to the case and

submit it to Worldpay.

In some cases, Discover may

initiate a Representment.

Merchant debited

chargeback amount

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

23

TABLE 3-2 Discover Chargeback Codes and Descriptions

Code Message

4502 Illegible Sales Data

4534 Duplicate Processing

4541 Recurring Payments

4542 Late Presentation

4550 Credit/Debit Posted Incorrectly

4553 Cardholder Disputes Quality of Goods or Services

4554 Not Classified

4586 Altered Amount

4753 Invalid Cardholder Number

4755 Non-Receipt of Goods or Services

4757 Violation of Operating Regulations

4863 Authorization Noncompliance

7001 Fraud - Card Present Transaction

7030 Fraud - Card Not Present Transaction

8002 Credit Not Processed.

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

24

3.3 Discover Pre-Arbitration

In the Discover system, if the Issuer does not agree with the Merchant Representment or the

Representment decision rendered by Discover, the Issuer can initiate a Pre-Arbitration Inquiry. Issuers

must submit Pre-Arbitration Inquiries through the Discover Network Dispute System or another approved

Dispute resolution system within twenty (20) days of the Representment/Representment decision. The

Issuer may not request Dispute Arbitration prior to close date of the Pre-Arbitration Inquiry.

FIGURE 3-3 Discover Pre-Arbitration Cycle

You have ten (10) days from the date of the Pre-Arbitration Inquiry Dispute Notice to respond and supply

any additional documentation in opposition to the Pre-Arbitration Inquiry.

NOTE: In some cases and with Discover Network’s consent, the Issuer may change the Reason

Code assigned to a Dispute prior to initiating a Pre-Arbitration Inquiry.

NOTE: The issuer may withdraw a Pre-Arbitration Inquiry at any time prior to Discover issuing the

decision. Upon withdrawal, the case ends and the issuer cannot re-initiate a Pre-Arbitration Inquiry

or initiate a Dispute Arbitration for the case.

Issuing Bank

Discover

Network

Merchant

Merchant Assumes Liability –

process ends

Discover renders a decision

based upon the Merchant

response. Either party can

escalate to Arbitration if they do

not agree with the decision.

The Issuer can file a Pre-Arbitration

Inquiry case in the Discover Network

Dispute system if they disagree with the

Representment/Representment decision.

Worldpay reviews the new

information and submits it to

Discover.

As with a Chargeback, the merchant has

two options:

Assume Liability

Send Supporting documentation

Merchant debited

disputed amount

Discover can allow the Issuer

to change the Reason Code

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

25

3.4 Discover Arbitration

The discover Arbitration process can be initiated by either the Issuer or the Merchant. The Issuer can

initiate Arbitration only if they do not agree with the decision from the Pre-Arbitration process. The

Merchant can initiate Arbitration if they do not agree either with the Representment decision or the results

of the Pre-Arbitration Inquiry. In either case, no money movement takes place until the Discover Network

issues a a decision, or one party, Issuer or Merchant, decides to accept liability. You have thirty-five (35)

days to respond to an Issuer initiated Arbitration case.

Based upon the decision, the disputed funds either remains with the winning party or moves to the

winning party. For example, if the Issuer initiates the process because they lost the Pre-Arbitration

decision and then loses the Arbitration, the money which is in the Merchant account based upon the

Pre-Arbitration decision, remains in the Merchant account. If the Issuer wins the Arbitration decision, the

money moves to the Issuer. In either case the Arbitration fees are paid by the losing party.

Discover Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

26

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

27

4

American Express Chargeback Process

While the overall process for American Express Chargebacks is similar to the other card brands, there are

several differences. This section will discuss the entire American Express process, highlighting the

differences where applicable.

The sections of this chapter are:

• American Express Inquiry

• American Express Chargeback

American Express Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

28

4.1 American Express Inquiry

An American Express Inquiry is similar to a Retrieval Request used in the Visa and MasterCard

processes. It is a request by AmEx for documentation regarding a transaction where the Cardmember

believes that the underlying card transaction is invalid and seeks compelling evidence from the Acquirer

or Merchant supporting the validity of the transaction. As with any other part of the Chargeback process,

there is a set time limit for you to respond. You have ten (10) days to submit the required information to

Worldpay for processing and forwarding to American Express.

FIGURE 4-1 American Express Inquiry

TABLE 4-1 American Express Retrieval Request Codes and Descriptions

Code Description

004 The Cardmember/Issuer requests delivery of goods/services ordered, but not received.

Please provide the service, ship the goods, or provide Proof of Delivery or proof of services

rendered.

021 The Cardmember claims the goods/services were canceled /expired, or the cardholder has

been unsuccessful in an attempt to cancel the goods/services. Please issue credit or contract

signed by the cardholder and discontinue future billings.

024 The Cardmember claims the goods received are damaged or defective and requests return

authorization. If a return is not permitted, please provide a copy of your return or refund

policy.

059 The Cardmember requests repair or replacement of damaged or defective goods received.

Please provide return instructions and make appropriate repairs, or provide a copy of your

return/replacement policy and explain why the goods cannot be repaired/replaced.

Cardholder

Issuing Bank

Discover

Merchant

Transaction validated

– process ends

If satisfied by the supplied

documentation, the process ends

here. If unsatisfied, the Issuer initiates

a Chargeback.

The Issuer initiates the

process after receiving a

query/complaint from the

cardholder or unilaterally.

Worldpay reviews the

submitted documentation

and responds to the Issuer.

Upon arrival at Worldpay an

automated process

forwards the Retrieval

Request to the Merchant

Queue. This is true for

either type.

The merchant has 20 days

to respond by submitting

the requested/required

documentation.

American Express Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

29

061 The Cardmember claims the referenced Credit should have been submitted as a Charge.

Please submit the Charge or provide an explanation of why a Credit was issued.

062 The Cardmember claims the referenced Charge should have been submitted as a Credit.

Please issue the Credit or provide support and itemization for the Charge and an explanation

of why Credit is not due.

063 The Cardmember requests replacement for goods or services that were not as described by

your Establishment, or credit for the goods or services as the Cardmember was dissatisfied

with the quality.

127 The Cardmember claims not to recognize the Charge. Please provide support and

itemization. In addition, if the Charge relates to shipped goods, please include a Proof of

Delivery with the full delivery address. If this documentation is not available, please issue

Credit.

147 The Cardmember claims the Charge will be paid by their insurance company. Please provide

a copy of the following documentation: itemized rental agreement, itemized repair bill, and

acknowledgment of responsibility signed by the Card Holder

154 The Cardmember claims the goods/services were canceled and/or refused. Please issue

Credit or provide Proof of Delivery, proof the cardholder was made aware of your

cancellation policy and an explanation why Credit is not due.

155 The Cardmember has requested Credit for the goods/services that were not received from

your Establishment. Please issue Credit or provide Proof of Delivery, or a copy of the signed

purchase agreement indicating the cancellation policy and an explanation why Credit is not

due.

158 The Cardmember has requested Credit for the goods that were returned to your

Establishment. Please issue a Credit or explain why a Credit is not due along with a copy of

your return policy.

169 The Cardmember has requested Credit for a Charge you submitted in an invalid currency.

Please issue a Credit or explain why a Credit is not due.

170 The Cardmember has requested Credit for a canceled lodging reservation or a Credit for a

CARDeposit was not received by the cardholder. Please issue the Credit or provide a copy of

your cancellation policy and an explanation of why Credit is not due.

173 The Cardmember requests Credit from your Establishment for a duplicate billing. If your

records show this is correct, issue a Credit. If Credit is not due, provide support and

itemization of both charges and explain fully in the space below.

175 The Cardmember claims that a Credit was expected, but has not appeared on his/her

account. Please issue a Credit or supply support for the Charge and an explanation of why a

Credit is not due.

176 The Cardmember claims not to recognize the Card Not Present Charge(s). Please issue the

Credit or provide support and itemization for the Charge and an explanation of why Credit is

not due.

177 The Cardmember claims this charge was unauthorized. Please issue the Credit or provide

support for the Charge and an explanation of why Credit is not due.

TABLE 4-1 American Express Retrieval Request Codes and Descriptions (Continued)

Code Description

American Express Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

30

193 The Cardmember claims the Charge incurred at you Establishment is fraudulent. For a Card

Present Charge, provide a copy of the Charge record and an imprint of the card, if one was

taken. For a Card Not Present Charge, provide a copy of the Charge record (or Substitute

Charge Record), any contract, or other details associated with the purchase and Proof of

Delivery (where applicable) with full shipping address.

680 The Cardmember claims the Charge amount you submitted differs from the amount the card

member agreed to pay. Please issue the Credit or explain why Credit is not due.

684 The Cardmember claims the Charge was paid by another form of payment. Please issue the

Credit or provide proof that the Cardmember’s payment by other means was not related to

the Disputed Charge or that you have no record of the Cardmember’s other payment.

691 The Cardmember is not disputing the Charge, but is requesting support and itemization.

Please provide this requested documentation.

693 The Cardmember has questioned the Charge for damages/theft or loss. Please issue the

Credit or provide a copy of the following documentation: itemized rental agreement, itemized

documentation to support the Charge, and acknowledgment of responsibility signed by the

Cardmember.

S02 We have reviewed the response(s) you sent in for the charge(s) in question and will not be

debiting your account. Thank you for your timely response to our inquiry.

S03 Support received.

TABLE 4-1 American Express Retrieval Request Codes and Descriptions (Continued)

Code Description

American Express Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

31

4.2 American Express Chargeback

From a process flow standpoint, the American Express Chargeback and Reversal Request process is

similar to that of Visa or MasterCard. Typically, American Express initiates a Chargeback on behalf of the

cardholder by sending notification to Worldpay explaining the dispute. After Worldpay receives the

Chargeback, we assign it to you for review by moving it from the Vantiv Queue to the Merchant Queue.

At this point, you review the chargeback and decide whether to submit a Reversal Request (dispute the

chargeback) or to accept the chargeback. If you decide to accept the chargeback, you move the

chargeback into the Merchant Assumed Queue using the Merchant Accept Liability activity. If you elect to

represent the transaction, you attach supporting documentation and move the chargeback to the Vantiv

Outgoing Queue using the Merchant Represent activity. You must respond within 7 days.

FIGURE 4-2 AmEx Chargeback and Dispute Charge Cycle

Once the chargeback moves to the Vantiv Outgoing Queue, the Chargeback Analyst prepares the

response, verifying the completeness of all required fields, and submits it electronically to AmEx.

American Express reviews your Reversal Request and supporting documentation. AmEx then issues a

decision; either the Chargeback stands, or they issue a Chargeback Reversal.

TABLE 4-2 American Express Chargeback Codes and Descriptions

Code Message

A01 Charge Amount Exceeds Authorization Amount

A02 No Valid Authorization

A08 Authorization Approval Expired

F10 Missing Imprint (requires Inquiry prior to Chargeback)

Cardholder

Issuing Bank

Discover

Network

Merchant

The Merchant may assume

liability and end the process.

Merchant credited

Representment

amount

Discover renders a decision.

The losing party can escalate to

the next stage – PreArbitration

for Issuer, or Arbitration for

Merchant.

The Issuer initiates the

First Chargeback after

receiving a complaint

from the cardholder or

unilaterally.

Worldpay reviews the

Representment and support

documentation and responds to

the Issuer.

If the merchant elects to

represent the transaction, they

attach the required supporting

documentation to the case and

submit it to Worldpay.

In some cases, Discover may

initiate a Representment.

Merchant debited

chargeback amount

American Express Chargeback Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

32

F22 Expired or Not Yet Valid Card

F24 No Card Member Authorization (requires Inquiry prior to Chargeback)

F29 Card Not Present

F30 EMV Counterfeit

C02 Credit (or partial credit) Not Processed

C04 Goods/Services Returned/Refused

C05 Goods/Services Cancelled

C08 Goods/Services Not received

C14 Paid by Other Means

C18 “No Show” or CARDeposit Cancelled

C28 Cancelled Recurring Billing

C31 Goods/Services Not as Described

C32 Goods/Services Damaged or Defective

M10 Vehicle Rental - Capital Damages

M49 Vehicle Rental - Theft or Loss of Use

P01 Unassigned Card Number

P03 Credit Processed as Charge

P04 Charge Processed as Credit

P05 Incorrect Charge Amount

P07 Late Submission

P08 Duplicate Charge

P22 Nonmatching Card Number

P23 Currency Discrepancy

R03 Insufficient Reply (requires Inquiry prior to Chargeback)

R13 No Reply (requires Inquiry prior to Chargeback)

M01 chargeback Authorization (requires Inquiry prior to Chargeback)

FR2 Fraud Full Recourse Program

FR4 Immediate Chargeback Program

FR6 Partial Immediate Chargeback Program

TABLE 4-2 American Express Chargeback Codes and Descriptions

Code Message

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

33

5

Visa Claims Resolution Process

Beginning in April 2018 Visa disputes (formerly known as chargebacks) will follow the new Visa Claims

Resolution process. Visa designed VCR to simplify the handling of disputes, improve efficiency, and

shorten the overall chargeback process. The new system also acts to block disputes that do not meet

certain criteria. For example. Visa would block the introduction of a fraud dispute when there was a

previous report of fraud on the account, but the issuing bank approved an authorization after the reported

fraud. Visa estimates a reduction of as much as 14% in First Chargebacks you receive.

As part of the simplification, Visa separates disputes into one of two workflows: Allocation and

Collaboration.

Visa further simplified chargebacks by consolidating the chargeback reason codes into one of four

categories: Fraud (10), Authorization (11), Processing Errors (12), and Consumer Disputes (13). The

Allocation process typically covers all Fraud and Authorization disputes, while the Collaborative process

covers Processing Errors and Consumer Disputes other than fraud. This acts to reduce complexity, while

still providing you the same level of, if not more, data to help you understand the dispute.

The sections of this chapter are:

• Retrieval Request

• Collaboration Workflow

• Allocation Workflow

NOTE: As of April 14, 2018, all new Visa Chargebacks will use the new VCR system. Existing

chargebacks introduced prior to this date will continue to follow the old methodology (see Chapter 2,

"Visa (Pre-VCR) and MasterCard Chargeback Process").

Visa Claims Resolution Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

34

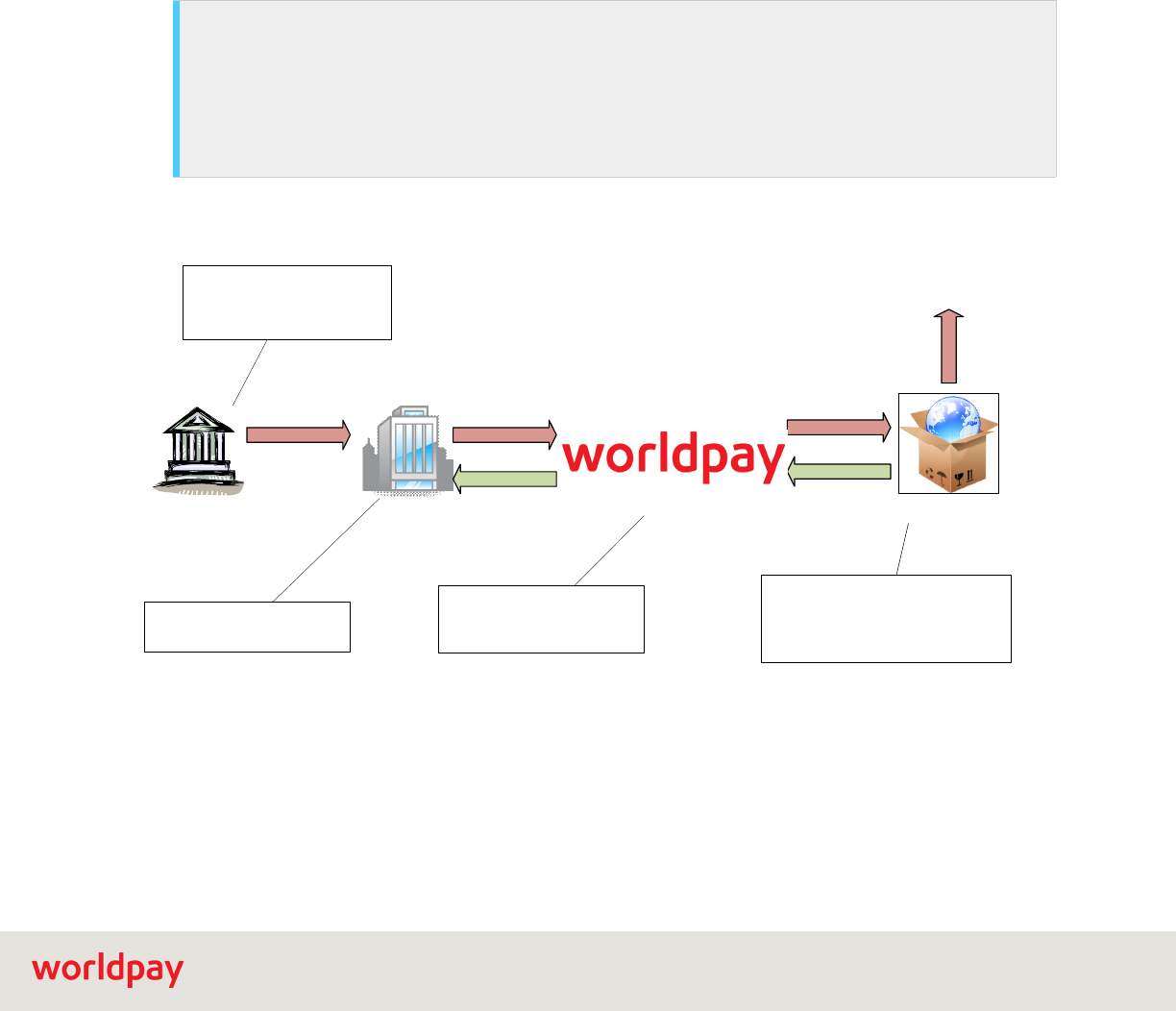

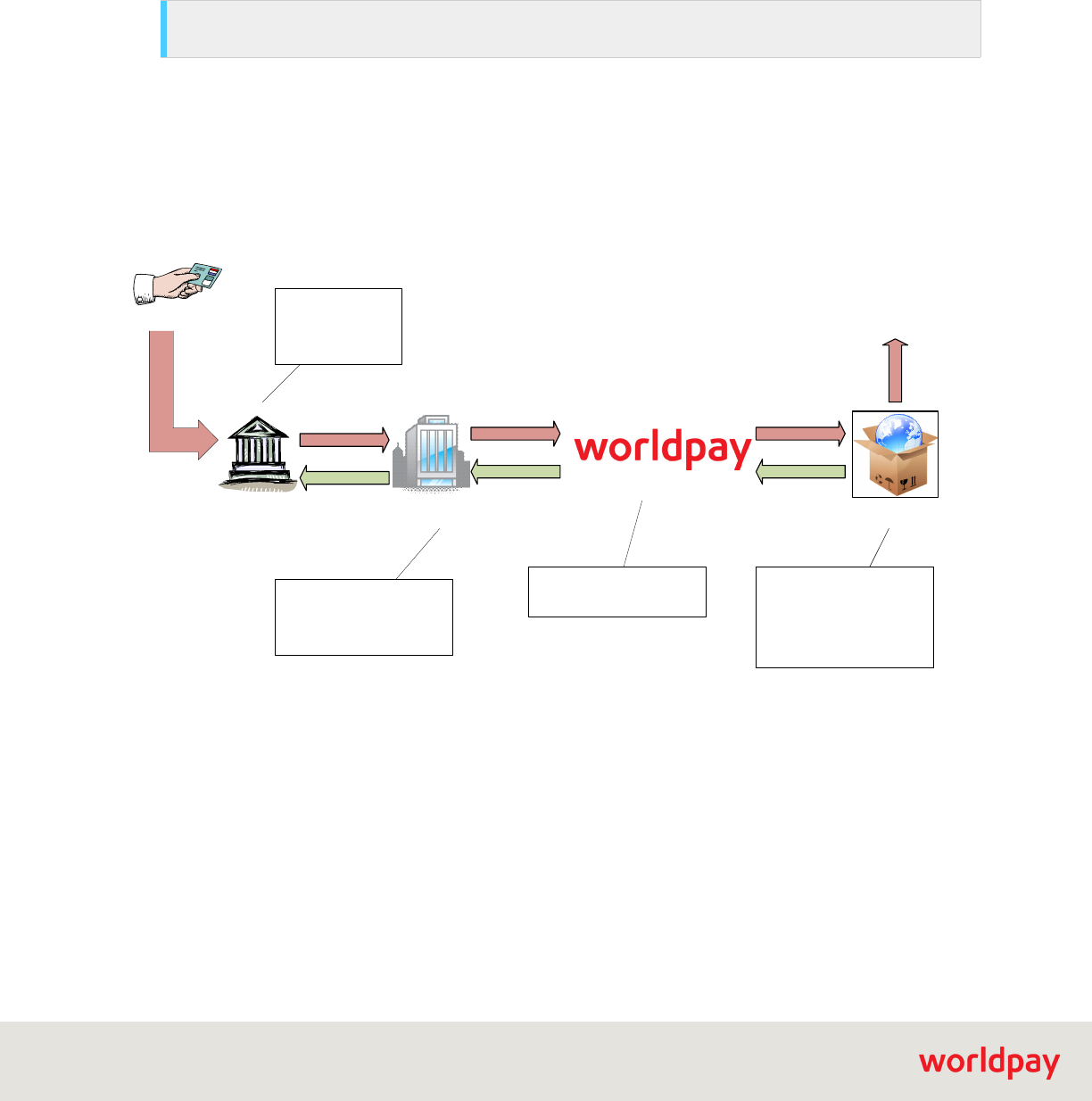

5.1 Retrieval Request

Worldpay eComm has not changed the handling of Retrieval Request with the introduction of the Visa

Claims Resolution. The Retrieval Request is your opportunity to submit supplemental information to an

issuer in support of the transaction prior to the introduction of a dispute. Typically, the consumer contacts

their bank, either because they do not recognize the purchase, or recognize the purchase, but had some

issue with the transaction.

FIGURE 5-1 Retrieval Request Process

If you respond with the necessary information to demonstrate the legitimacy of the transaction, the

process stops here. If you fail to respond to a Retrieval Request, or if you do not submit the required

information, the issuing bank will likely introduce a dispute.

Cardholder

Issuing Bank

Visa

Merchant

Transaction validated

– process ends

If satisfied by the supplied

documentation, the process ends

here. If unsatisfied, the Issuer

initiates a Dispute.

The Issuer initiates the

process after receiving a

query/complaint from the

cardholder or unilaterally.

Worldpay reviews the

submitted documentation

and responds to the Issuer.

Upon arrival at Worldpay an

automated process

forwards the Retrieval

Request to the Merchant

Queue.

The merchant responds

by submitting the

required documentation,

as soon as possible. This

could include: Additional

Data, Credit info, or both.

Visa Claims Resolution Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

35

5.2 Collaboration Workflow

The Collaboration workflow involves disputes due to either processing errors or consumer disputes. Other

than the categories of disputes, this workflow is very similar to the existing Visa Chargeback workflow.

The issuing bank initiates a Dispute on behalf of the cardholder by sending notification to Worldpay

explaining the dispute. After Worldpay receives the dispute, we assign it to you for review by moving it

from the Vantiv Queue to the Merchant Queue. At the time the dispute moves to the Merchant Queue,

Worldpay debits your merchant account for the amount of the dispute.

You review the dispute and decide whether to accept or respond to the dispute. If you decide to accept

the chargeback, you move the chargeback into the Merchant Assumed Queue using the Merchant Accept

Liability activity. The optimal way to respond to the dispute (represent), if you choose to do so is via iQ. In

iQ you complete the questionnaire and attach supporting documentation. Your response goes directly to

Visa. You must respond within 20 days.

FIGURE 5-2 Collaboration Workflow Overview

Once the dispute moves to the Vantiv Outgoing Queue, the Chargeback Analyst prepares the response,

verifying that all required fields are complete, and submits it through the card network back to the Issuing

bank. Upon your response, when you move the dispute from the Merchant Queue to the Vantiv Outgoing

Queue, Worldpay credits your merchant account the representment amount.

The Issuing bank has 30 days after your response to accept the response or to issue their own

Pre-Arbitration response. This action by the Issuing bank, if taken, generates a new case in the system.

No money movement occurs when the issuer initiates a Pre-Arbitration case.

NOTE: If you respond to the Dispute using the Chargeback API, A Worldpay eComm Chargeback

Analyst completes the required questionnaire on your behalf.

Although Visa allows 30 days for a response, the Worldpay eComm Operations team reserves 10

days to resolve, on your behalf, any potential problems relating to the dispute.

Cardholder

Issuing Bank

Visa

Merchant

The Merchant may assume

liability and end the process.

The Issuer initiates the

Chargeback for

Processing Error or

Consumer Dispute.

Worldpay reviews the response

and support documentation and

responds to the Issuer.

If the merchant elects to respond

to the dispute, they attach the

required supporting

documentation to the case,

complete the questionnaire (in

iQ), and submit it to Worldpay.

If satisfied by the dispute

response, the process ends

here. If unsatisfied, the Issuer

escalates to the next stage :

Pre-Arbitration.

Visa Claims Resolution Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

36

You have the same options on a Pre-Arbitration case as the initial dispute. That is, you can accept

liability, or you can decline liability (partial or full) within 20 days. If you accept liability, the case ends and

Worldpay moves the disputed funds from your account back to the issuer. If you decline, the issuer can

accept your decline (you win), or request Arbitration. The issuer’s request for Arbitration must occur within

10 days. If the issuer request Arbitration, Visa makes the final decision. The results are one of the

following: ARBITRATION_WON, ARBITRATION_LOST, or ARBITRATION_SPLIT. Any required money

movement occurs after the final Visa decision.

5.2.1 Dispute Reason Codes - Collaboration Workflow

The following table provides information about the Dispute Reason Codes applicable to the Collaboration

Workflow.

TABLE 5-1 Collaboration Workflow Dispute Reason Codes

Category Code Description Old Code

Processing

Error

12.1 Late Presentment

RC 74 - Late Presentment

RC 76 - Incorrect Transaction Code

RC 77 - Non-Matching Account Number

RC 80 - Incorrect Transaction Amount or

Account Number

RC 82 - Duplicate Processing

RC 86 - Paid By Other Means

12.2 Incorrect Transaction Code

12.3 Incorrect Currency

12.4 Incorrect Account Number

12.5 Incorrect Amount

12.6.1 Duplicate Processing

12.6.2 Paid by Other Means

12.7 Invalid Data

Consumer

Dispute

13.1 Merchandise/Services Not

Received

RC 30 - Services Not Rendered or Merchandise

Not Received

RC41 - Cancelled Recurring Transaction

RC53 - Not as Described or Defective

Merchandise

RC85 - Credit Not Processed

RC90 - Non-receipt of Cash or Load Transaction

Value at ATM

13.2 Cancelled Recurring

Transaction

13.3 Not as Described/Defective

13.4 Counterfeit Merchandise

13.5 Misrepresentation

13.6 Credit Not Processed

13.7 Cancelled/Returned

Merchandise or Service

13.8 Original Credit Not

Accepted

13.9 Non-Receipt of Cash or

Load Transaction Value

Visa Claims Resolution Process

© 2020 Worldpay, Inc.. All rights reserved.

cnpAPI Reference Guide V3.1

37

5.3 Allocation Workflow

The Allocation workflow involves disputes due to either fraud or authorization issues. Because of the

nature of these disputes and the fact that Visa blocks any that meet certain criteria (for example, fraud on

3DS authorized transaction, dispute introduced too late, or already refunded), the workflow assumes the

merchant will accept liability for most Allocation disputes. This results in a shorter flow.

In this workflow, the Issuer introduces the dispute which Visa reviews and categorizes. Unlike the

collaborative workflow, if you elect to fight the dispute, you do so by requesting Pre-Arbitration, providing

the evidence necessary to win and completing the Visa Questionnaire in iQ. This evidence must

constitute definitive proof that the dispute is invalid. You must request the Pre-Arbitration within 20 days of

receiving the dispute and the Issuer must respond within 30 days.

If the Issuer accepts your argument, the disputed funds move back to your account. If they do not, you

have 7 days to request Arbitration. The Visa Arbitration ruling is final. The results are one of the following:

ARBITRATION_WON, ARBITRATION_LOST, or ARBITRATION_SPLIT.

FIGURE 5-3 Allocation Workflow Overview

5.3.1 Dispute Reason Codes - Allocation Workflow

The following table provides information about the Dispute Reason Codes applicable to the Allocation

Workflow.

NOTE: In the Allocation Workflow, there are no funds movement when requesting Pre-Arbitration.

Although Visa allows 30 days for you to request Pre-Arbitration, the Worldpay eComm Operations