D-101A (R. 12-17)

Who Must Pay Estimated Tax

Tax (including the Wisconsin alternative minimum tax) is required to be

paid on income as it is earned or constructively received. Withholding tax

and estimated tax are the two methods used to make those required tax

payments. Generally, if you work for wages, you have tax withheld from your

wages to prepay any tax which will be computed on your income tax return

for the year. If you have income from which tax is not withheld (for example,

interest, dividends, unemployment compensation, self-employment

income, taxable pensions, etc.), you must pay estimated tax to prepay any

tax which will be computed on your income tax return for the year.

You must pay Wisconsin estimated tax for 2018 if you expect to owe, after

subtracting your withholding and credits, at least $500 in tax for 2018 and

you expect your withholding to be less than the smallest of:

• 90% of the tax (including alternative minimum tax) shown on your 2018

income tax return.

• 100% of the tax (including alternative minimum tax) shown on your 2017

income tax return assuming the return covered 12 months. This does

not apply to trusts or estates that have 2018 taxable income of $20,000

or more. If your 2017 return was adjusted by the department or you filed

an amended return, use the tax from the latest adjusted or amended

return.

• 90% of the tax shown on your 2018 income tax return, computed by

annualizing your taxable income and alternative minimum taxable in-

come. (You may use Wisconsin Schedule U, Part IV, as a worksheet to

annualize income.)

Full-year residents, part-year residents, nonresidents, trusts, and estates

are subject to the estimated tax requirement. (Note: Trusts subject to tax

on unrelated business income should file on Form Corp-ES.)

You do not have to pay estimated tax if you were a full-year resident of

Wisconsin for 2017 and you had no tax liability for that 12-month period.

Estates and grantor trusts which are funded on account of a decedent’s

death are only required to make estimated tax payments for any tax year

ending two or more years after the decedent’s death.

You and your spouse may pay estimated tax either jointly or separately.

If joint payments are made, you and your spouse may still file separate

income tax returns for 2018. The estimated tax payments may be divided

between you and your spouse in any manner you choose. If separate pay-

ments are made, you and your spouse may file a joint income tax return

for 2018 and apply the separate estimated tax payments to the joint tax

liability. However, no part of the separate estimated tax payments may be

applied to a separate tax liability of the other spouse.

When to Pay Your Estimated Tax

Generally, you must make your first estimated tax payment by April 17,

2018. You may pay all your estimated tax at that time or in four equal

installments on or before April 17, 2018, June 15, 2018, September 17,

2018, and January 15, 2019. Exceptions to this general rule are as follows:

1. Other payment dates. In some cases such as an increase in income,

you may have to make your first estimated tax payment after April 17,

2018. The payment dates are then as follows:

If the requirement to pay Payment Of the estimated

estimated tax is met after: date is: tax due, pay:

March 31 and before June 1 ..June 15, 2018 .......1/2

May 31 and before Sept. 1 ...Sept. 17, 2018 ......3/4

August 31 ................Jan. 15, 2019 .......all

Any remaining payments should be 1/4 of your required annual

payment.

2. Your return as a payment. If you file your 2018 income tax return by

January 31, 2019, and pay the entire balance due, you do not have to

make your last payment of estimated tax due on January 15, 2019.

2018 Form 1‑ES Instructions – Estimated Income Tax for Individuals, Estates, and Trusts

3. Farmers and fishers. If at least two-thirds of your gross income (joint

gross income, if applicable) for 2017 or 2018 is from farming or fishing,

you may:

• pay your 2018 estimated tax in full by January 15, 2019; or

• file your 2018 income tax return on or before March 1, 2019, and

pay the total tax due. In this case, you need not make estimated

tax payments for 2018.

4. Fiscal year. If your return is filed on a fiscal year basis, your due dates

are the 15th day of the 4th, 6th, and 9th months of your current fiscal

year, and the 1st month of the following fiscal year. (Note: If any due

date falls on a Saturday, Sunday, or legal holiday, use the next busi-

ness day.)

How to Use Form 1‑ES

1. If you have a preprinted voucher, make any corrections necessary

to your name and address by lining out the incorrect information and

printing in the correct information. To obtain personalized Form 1-ES

vouchers, visit the department's website at revenue.wi.gov/Pages/

Form/2018-TaxForms.aspx or call (608) 266-1961.

2. Complete the “2018 Estimated Income Tax Worksheet” on page 2 of

these instructions. Use your 2017 tax return as a guide, but be sure to

consider any law changes for 2018. Law changes are published in the

Wisconsin Tax Bulletin, which is available on the Internet at: revenue.

wi.gov/Pages/ISE/wtb-Home.aspx.

3. Fill in the amount from line 14 of the worksheet on the “Amount of

Payment” line on Form 1-ES.

4. Enclose, but do not staple or attach, your check or money order with

Form 1-ES. Make your remittance payable to the Wisconsin Depart-

ment of Revenue and mail to the address shown on Form 1-ES.

To pay online, go to the department's website at:

https://tap.revenue.wi.gov/pay. This is a free service.

To pay by credit card, call 1-800-2PAY-TAX (1-800-272-9829) or visit

officialpayments.com. There will be a 2.5% fee charged for this service.

If you need help, contact our Customer Service Bureau at (608) 266-2486

or visit any Department of Revenue office.

How to Amend Your Estimated Tax Payments

If you have a substantial increase or decrease in your estimated tax liability,

your estimated tax payments should be amended.

1. Recompute your estimated tax liability on the “2018 Estimated Income

Tax Worksheet.” Include any estimated tax payments already made

for 2018 on line 10 of the worksheet.

2. Determine the amount of each remaining installment due:

• If all 4 installments are being amended, fill in 1/4 of line 11 of the

worksheet on each payment voucher.

• If 3 installments are being amended, fill in 1/2 of line 11 on the first

amended voucher and 1/4 of line 11 on each of the last two vouchers.

• If 2 installments are being amended, fill in 3/4 of line 11 on the first

amended voucher and 1/4 of line 11 on the last voucher.

• If only the last installment is being amended, fill in all of line 11 on

the voucher filed.

Interest Charge for Failure to Pay Estimated Tax

If you are required to pay estimated tax and you do not, or you underpay

any installment, you are subject to interest on the underpayment amount

when you file your 2018 return. Wisconsin Schedule U is used to compute

the interest due. The Schedule U instructions provide information on

exceptions to the interest charge.

D-101A (R. 12-17)

- 2 -

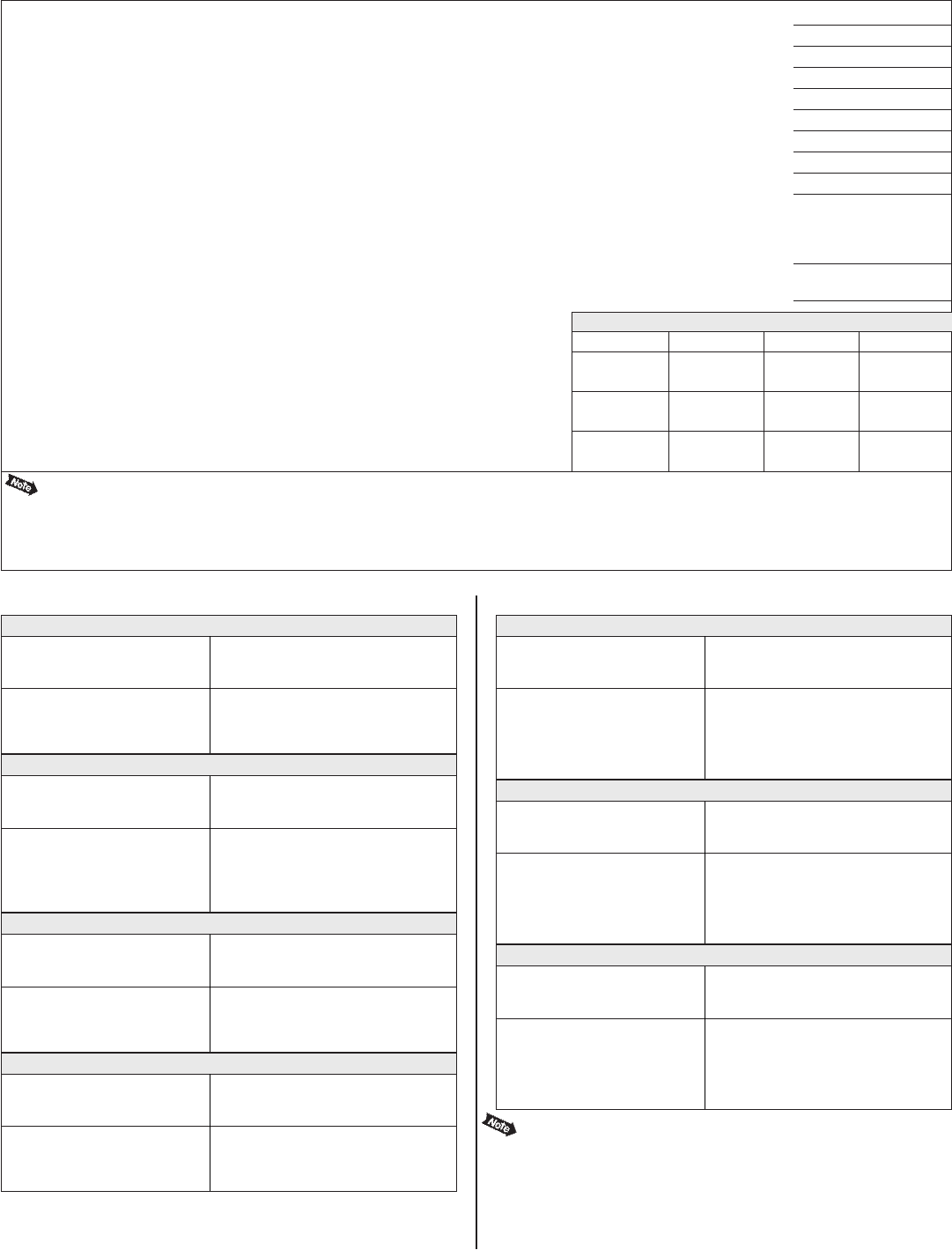

1. Fill in the amount of Wisconsin income you expect in 2018. Use your 2017 tax return as a guide ............ 1. .

2. Wisconsin standard deduction and exemptions (see standard deduction schedules below)* ................. 2. .

3. Estimated taxable income (subtract line 2 from line 1) .............................................. 3. .

4. Estimated tax (see tax rate schedules below) ..................................................... 4. .

5. Estimated credits (see instructions provided with your 2017 tax return for descriptions of credits) ............ 5. .

6. Subtract line 5 from line 4 ................................................................... 6. .

7. Estimated Wisconsin alternative minimum tax .................................................... 7. .

8. Add lines 6 and 7 .......................................................................... 8. .

9. Required annual payment. Fill in amount of line 8 that you are required to pay . . . . . . . . . . . . . . . . . . . . . . . . . . . 9. .

Caution: Generally, if you do not prepay at least 90% of your 2018 tax liability or 100% of your 2017 tax, whichever is smaller,

you may be subject to interest on the underpayment amount. To avoid this, be sure your estimate is as accurate as possible.

If you are unsure of your estimate, you may want to pay more than 90% of the amount you have shown on line 8.

10. Wisconsin income tax withheld and estimated to be withheld during 2018 .............................. 10. .

11. Balance (subtract line 10 from line 9). (Note: If line 8 less line 10 is less than $500, you are not required to

make estimated tax payments.) ................................................................ 11. .

12. If four installments are due, enter in each column 1/4 of the amount on line 11.

If less than four installments are due, use the instructions for other payment dates

under “When to Pay Your Estimated Tax” ...............................

13. Apply overpayment carried forward from your 2017 tax return

(applyrsttoAprilandcarryremaindertoJune,etc.) ......................

14. Installment amount (subtract line 13 from line 12).

Fill in here and on the “Amount of Payment” line on Form 1-ES ..............

April17 June15 Sept.17 Jan.15

Installments

*Nonresidents and part-year residents must prorate the tax brackets

(amountsappearinginthersttwocolumnsofthe2018TaxRateSchedules)

based on the ratio of their Wisconsin income to their federal adjusted gross

income. For example, for a single individual the tax brackets are $11,450,

$11,450,and$229,250.Assumingtheindividualhasaratioof20%,therst

$2,290 ($11,450 x .20) is taxed at 4%, the next $2,290 ($11,450 x .20) is taxed

at 5.84%, and the next $45,850 ($229,250 x .20) is taxed at 6.27%. Taxable

income over $50,430 ($252,150 x .20)is taxed at 7.65%.

*Individuals Yourexemptionsare$700foryourself,$700foryourspouseiflingajointreturn,and$700foreachdependent.Add$250tothe

totalifyouare65yearsofageoroverand,iflingajointreturn,add$250ifyourspouseis65yearsofageorover.(Exception:Ifyouareclaimedas

a dependent on someone else’s return, you do not qualify for an exemption.) Estates and Trusts Fill in -0- on line 2. Nonresidents and part-year

residents prorate the standard deduction as follows: (1) Figure your standard deduction using your federal adjusted gross income instead of your Wisconsin

income, and (2) prorate using the ratio of Wisconsin income to federal adjusted gross income. Exemptions must also be prorated using the same ratio.

2018 Tax Rate Schedules for Full‑Year Residents*

2018 Estimated Income Tax Worksheet – Keep for your records – Do not file

2018 Standard Deduction

$ 0 830 $ 15,249 $ 10,580

15,249 103,417 10,580 less 12% ....... $ 15,250

103,417 or over 0

Schedule for Single Taxpayers

but of the

over – not over – amount over –

If Wisconsin income is: The 2018 Standard

Deduction is:

Schedule for Head of Household

$ 50 30 $ 15,249 $ 13,660

15,249 44,541 13,660 less 22.515% $ 15,250

44,541 103,417 10,580 less 12% .......... 15,250

103,417 or over 0

but of the

over – not over – amount over –

If Wisconsin income is: The 2018 Standard

Deduction is:

Schedule for Married Filing Jointly

but of the

over – not over – amount over –

If Wisconsin income is: The 2018 Standard

Deduction is:

$ 50 30 $ 22,009 $ 19,580

22,009 121,009 19,580 less 19.778% $ 22,010

121,009 or over 0

Schedule for Married Filing Separately

but of the

over – not over – amount over –

If Wisconsin income is: The 2018 Standard

Deduction is:

$50 830 $ 10,449 $ 9,300

10,449 57,472 9,300 less 19.778% $ 10,450

57,472 or over 0

Schedule A

– Single, Head of Household, Estates and Trusts

but of the

over – not over – amount over –

If taxable income is: The 2018

Gross Tax is:

$ 0 30 $ 11,450 $ 4.00% ...... $ 0

11,450 22,900 458.00 + 5.84% ............11,450

22,900 252,150 1,126.68 + 6.27% ........... 22,900

252,150 or over 15,500.66 + 7.65% ......... 252,150

Schedule B

– Married Filing Jointly

$50 830 $ 15,270 $ 4.00%........$ 0

15,270 30,540 610.80 + 5.84%.............15,270

30,540 336,200 1,502.57 + 6.27%.............30,540

336,200 or over 20,667.45 + 7.65%...........336,200

but of the

over – not over – amount over –

If taxable income is: The 2018

Gross Tax is:

Schedule C

– Married Filing Separately

$50 830 $ 7,630 $ 4.00%........$ 0

7,630 15,270 305.20 + 5.84%...............7,630

15,270 168,100 751.38 + 6.27%.............15,270

168,100 or over 10,333.82 + 7.65%...........168,100

but of the

over – not over – amount over –

If taxable income is: The 2018

Gross Tax is: