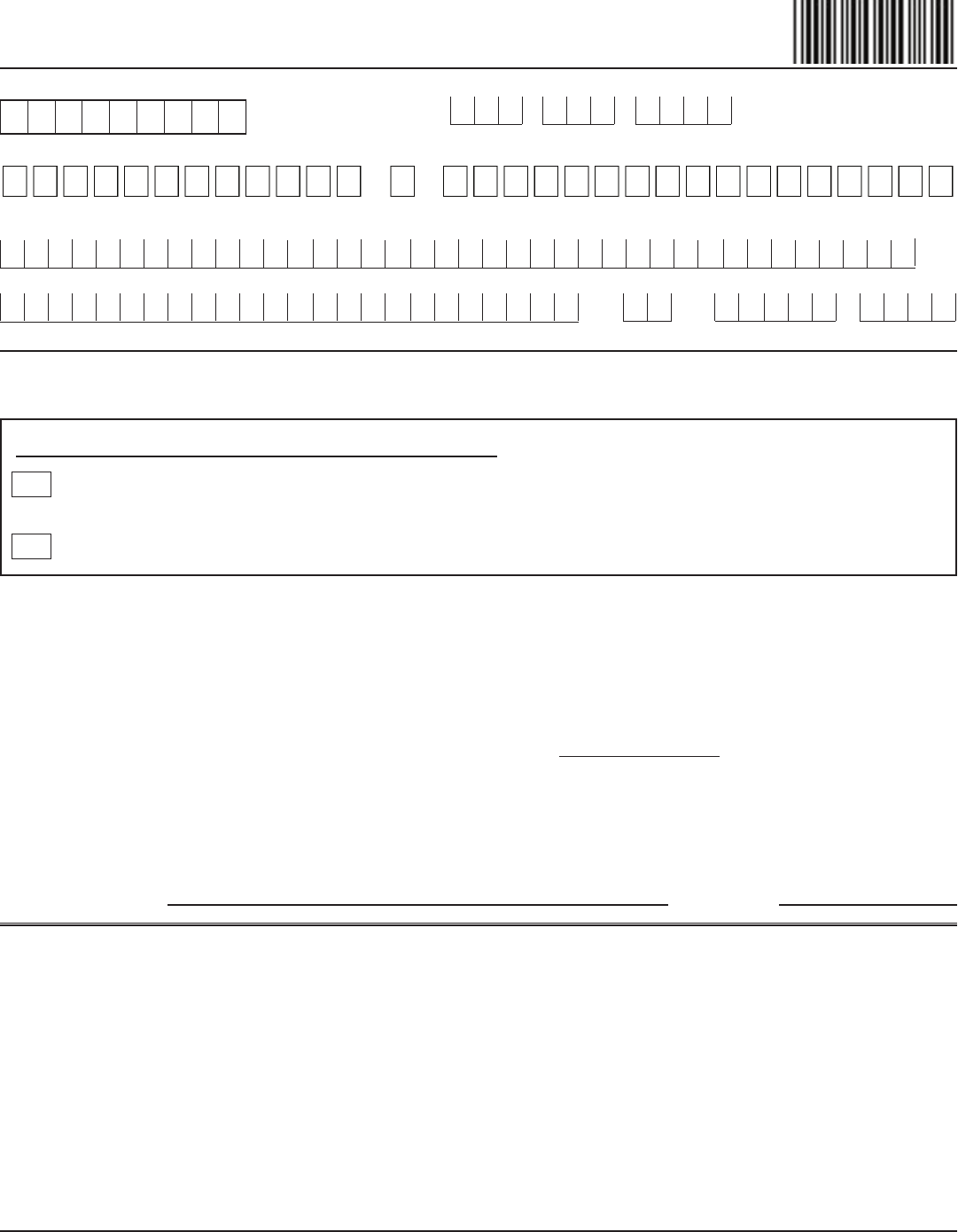

Application for Withdrawal of Accumulated

Contributions Package

This package contains

Frequently Asked Questions About Form 5

Special Tax Notice Regarding Your Rollover Options

Summary of Major Retirement Benefits

Application for Withdrawal of Accumulated Contributions (Form 5)

Trustee-to-Trustee Distribution Form for Rollovers (Form 193)

Application for Withdrawal of Accumulated

Contributions Package

This page intentionally left blank

Page 2 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

The Maryland State Retirement and Pension System

120 East Baltimore Street • Baltimore, MD 21202-6700

sra.maryland.gov

Frequently Asked Questions…

when filing the

Application for Withdrawal of Accumulated Contributions (Form 5)

Please review the following information in regard to applying to withdraw your accumulated

contributions. For retirement counseling call: 410-625-5555 or 1-800-492-5909.

Question: Do I need to have my former employer sign the Form 5?

Answer: If your termination date is less than six months from the date you complete the Form 5, you

must forward the form to your former employer. You should send to the attention of the

retirement coordinator or personnel office.

If your termination date is more than six months from the date you complete the Form 5, then

you may send the form directly to the Maryland State Retirement Agency.

Question: Does the Form 5 need to be notarized?

Answer: Yes. You must sign and date the form in the presence of a notary who will then affix the official

seal and complete the required information. Be sure the notary enters your name on the line

provided after “personally appeared” or the form will not be valid and no action will be taken.

By completing the Form 5, you are terminating your membership in the Maryland State

Retirement and Pension System and are forfeiting any right to a future benefit including

disability benefits. It is important that you acknowledge this forfeiture in the presence of a

notary.

Question: Do I need to complete the Trustee-to-Trustee Distribution Form for Rollovers (Form 193)?

Answer: If you choose Refund Choice 2 or 3 you must sign and complete page one of the Form 193.

Your financial institution must complete and return page two of the Form 193. The Form 193 is

not valid unless both sections are properly completed.

Some “eligible retirement plans” do not accept rollovers, some do not accept rollovers of after-

tax amounts and some may accept after-tax amounts if they separately account for the amount.

IRC Section 457(b) governmental plans and IRC Section 403(a) annuity plans do not accept

transfers of non-taxable amounts. Please check with the receiving plan as to whether or not

they can accept the rollover before sending the Form 193 to the Agency.

Non-Taxable amounts – these amounts have already been subject to federal tax. If that is the

only amount you wish refunded to you, write “NON-TAXABLE” on the line provided in Choice

#2.

Note: The non-taxable amount will be determined at the time of the refund.

Question: If I choose Refund Choice 2 or 3 will the refund check be mailed directly to the financial

institution accepting the rollover?

Answer: No. The refund check will be mailed to you at the address you provide on the Form 5. The

refund check will be payable to you and the financial institution and you are responsible for

delivering the check to the financial institution as soon as possible to complete the rollover.

Page 3 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

The Maryland State Retirement and Pension System

120 East Baltimore Street • Baltimore, MD 21202-6700

sra.maryland.gov

Question: How long will it take for me to get my refund?

Answer: Please allow up to 90 days from the latter of the receipt by the retirement agency of your last

payroll contribution (the last pay period from your resignation/termination) or the date of receipt

of the properly completed forms for processing.

Due to the volume of requests, the agency does not acknowledge receipt of withdrawal

requests. Requests for withdrawals are processed in the order received. If you are rolling over

your money, please inform the financial institution that it could take up to 90 days to receive the

money.

Question: Is there any way to expedite payment?

Answer: No. Withdrawal requests are processed in the order that they are received.

Question: Will my refund be sent direct deposit?

Answer: No. You will receive a paper check mailed to the address you provide on the Form 5.

If you move before the refund has been processed, notify the agency in writing of your new

address, including a full signature and social security number or date of birth. You can mail the

change of address to the Retirement Agency.

Question: Are taxes withheld from my refund?

Answer: If you select Refund Choice 1, “entire amount refunded,” or Refund Choice 2, refund a

designated amount, then the agency is required to withhold a minimum of 20% of any taxable

amount paid to you for federal taxes, and if you are a Maryland resident, the agency is required

to withhold 7.75% of any taxable amount for Maryland state taxes.

If you select Refund Choice 3, “entire amount transferred to an eligible retirement plan,” then the

agency will not withhold any amount for federal or Maryland state taxes.

If you have any questions about your specific tax situation, consult your financial advisor, CPA

or the Internal Revenue Service. The retirement agency cannot advise you on tax issues.

Question: Do I need to complete IRS Form W-4R?

Answer: Only complete and return Form W-4R if you are not rolling over all of your payment to another

qualified retirement plan and you want to have more than 20% of your payment withheld for

federal taxes.

Question: Where do I send the completed forms?

Answer: Return the completed forms to:

Maryland State Retirement Agency

120 E. Baltimore Street

Baltimore, MD 21202-6700

Page 4 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Page 1 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

SPECIAL TAX NOTICE REGARDING YOUR ROLLOVER OPTIONS

You are receiving this notice because all or a portion of a payment you are receiving from the Maryland State Retirement

and Pension System (the "Plan") is eligible to be rolled over to an IRA or an employer plan. This notice is intended to help

you decide whether to do such a rollover.

Rules that apply to most payments from a plan are described in the "General Information About Rollovers" section. Special

rules that only apply in certain circumstances are described in the "Special Rules and Options" section.

GENERAL INFORMATION ABOUT ROLLOVERS

How can a rollover affect my taxes?

You will be taxed on a payment from the Plan if you do not roll it over. If you are under age 59½ and do not do a rollover,

you will also have to pay a 10% additional income tax on early distributions (generally, distributions made before age 59½),

unless an exception applies. However, if you do a rollover, you will not have to pay tax until you receive payments later

and the 10% additional income tax will not apply if those payments are made after you are age 59½ (or if an exception to

the 10% additional income tax applies).

What types of retirement accounts and plans may accept my rollover?

You may roll over the payment to either an IRA (an individual retirement account or individual retirement annuity) or an

employer plan (a tax-qualified plan, section 403(b) plan, or governmental section 457(b) plan) that will accept the rollover.

The rules of the IRA or employer plan that holds the rollover will determine your investment options, fees, and rights to

payment from the IRA or employer plan. Further, the amount rolled over will become subject to the tax rules that apply to

the IRA or employer plan.

How do I do a rollover?

There are two ways to do a rollover. You can do either a direct rollover or a 60-day rollover.

If you do a direct rollover, the Plan will make the payment payable to your IRA or an employer plan for your benefit.

However, the payment may be mailed to you for delivery to your IRA or employer plan. You should contact the IRA sponsor

or the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit into an IRA or eligible employer plan that

will accept it. Generally, you will have 60 days after you receive the payment to make the deposit. If you do not do a direct

rollover, the Plan is required to withhold 20% of the payment for federal income taxes. In addition, the Plan is required to

withhold 7.75% for Maryland residents. This means that, in order to roll over the entire payment in a 60-day rollover, you

must use other funds to make up for the 20% withheld. If you do not roll over the entire amount of the payment, the portion

not rolled over will be taxed and will be subject to the 10% additional income tax on early distributions if you are under age

59 ½ (unless an exception applies).

How much may I roll over?

If you wish to do a rollover, you may roll over all or part of the amount eligible for rollover. Any payment from the Plan is

eligible for rollover, except:

• Certain payments spread over a period of at least 10 years or over your life or life expectancy (or the joint lives or

joint life expectancies of you and your beneficiary);

• Required minimum distributions after age 70½ (if you were born before July 1, 1949), after age 72 (if you were

born after June 30, 1949), or after death; and

• Corrective distributions of contributions that exceed tax law limitations.

The Plan administrator or the payor can tell you what portion of a payment is eligible for rollover.

Page 5 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Page 2 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

If I don't do a rollover, will I have to pay the 10% additional income tax on early distributions?

If you are under age 59½, you will have to pay the 10% additional income tax on early distributions for any payment from

the Plan (including amounts withheld for income tax) that you do not roll over, unless one of the exceptions listed below

applies. This tax applies to the part of the distribution that you must include in income and is in addition to the regular

income tax on the payment not rolled over.

The 10% additional income tax does not apply to the following payments from the Plan:

• Payments made after you separate from service if you will be at least age 55 in the year of the separation;

• Payments that start after you separate from service if paid at least annually in equal or close to equal amounts over

your life or life expectancy (or the joint lives or joint life expectancies of you and your beneficiary);

• Payments from a governmental plan made after you separate from service if you are a qualified public safety

employee and you will be at least age 50 in the year of the separation;

• Payments made due to disability;

• Payments after your death;

• Corrective distributions of contributions that exceed tax law limitations;

• Payments made directly to the government to satisfy a federal tax levy;

• Payments made under an eligible domestic relations order (EDRO) to an alternate payee who is a former spouse

of the member;

• Payments up to the amount of your deductible medical expenses (without regard to whether you itemize deductions

for the taxable year);

• Certain payments made while you are on active duty if you were a member of a reserve component called to duty

after September 11, 2001 for more than 179 days; and

• Payments excepted from the additional income tax by federal legislation relating to certain emergencies and

disasters.

If I do a rollover to an IRA, will the 10% additional income tax apply to early distributions from the IRA?

If you receive a payment from an IRA when you are under age 59 ½, you will have to pay the 10% additional income tax

on early distributions on the part of the distribution that you must include in income, unless an exception applies. In general,

the exceptions to the 10% additional income tax for early distributions from an IRA are the same as the exceptions listed

above for early distributions from a plan. However, there are a few differences for payments from an IRA, including:

• The exception for payments made after you separate from service if you will be at least age 55 in the year of the

separation (or age 50 for qualified public safety employees) does not apply;

• The exception for EDROs does not apply (although a special rule applies under which, as part of a divorce or

separation agreement, a tax-free transfer may be made directly to an IRA of a spouse or former spouse); and

• The exception for payments made at least annually in equal or close to equal amounts over a specified period applies

without regard to whether you have had a separation from service.

Additional ex

ceptions apply for paym

ents from an IRA, including:

• Payments for qualified higher education expenses;

• Payments up to $10,000 used in a qualified first-time home purchase; and

• Payments for health insurance premiums after you have received unemployment compensation for 12 consecutive

weeks (or would have been eligible to receive unemployment compensation but for self-employed status).

Will I owe State income taxes?

If you do not do a rollover, the Plan is required to withhold 7.75% for Maryland residents. This notice does not address any

other State or local income tax rules (including withholding rules).

Page 6 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Page 3 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

SPECIAL RULES AND OPTIONS

If your payment includes after-tax contributions

After-tax contributions included in a payment are not taxed. If you receive a partial payment of your total benefit, an

allocable portion of your after-tax contributions is included in the payment, so you cannot take a payment of only after-tax

contributions. However, if you have pre-1987 after-tax contributions maintained in a separate account, a special rule may

apply to determine whether the after-tax contributions are included in the payment. In addition, special rules apply when

you do a rollover, as described below.

You may roll over to an IRA a payment that includes after-tax contributions through either a direct rollover or a 60-day

rollover. You must keep track of the aggregate amount of the after-tax contributions in all of your IRAs (in order to

determine your taxable income for later payments from the IRAs). If you do a direct rollover of only a portion of the amount

paid from the Plan and at the same time the rest is paid to you, the portion rolled over consists first of the amount that would

be taxable if not rolled over. For example, assume you are receiving a distribution of $12,000, of which $2,000 is after-tax

contributions. In this case, if you directly roll over $10,000 to an IRA that is not a Roth IRA, no amount is taxable because

the $2,000 amount not rolled over is treated as being after-tax contributions. If you do a direct rollover of the entire amount

paid from the Plan to two or more destinations at the same time, you can choose which destination receives the after-tax

contributions.

Similarly, if you do a 60-day rollover to an IRA of only a portion of a payment made to you, the portion rolled over consists

first of the amount that would be taxable if not rolled over. For example, assume you are receiving a distribution of $12,000,

of which $2,000 is after-tax contributions, and no part of the distribution is directly rolled over. In this case, if you roll over

$10,000 to an IRA that is not a Roth IRA in a 60-day rollover, no amount is taxable because the $2,000 amount not rolled

over is treated as being after-tax contributions.

You may roll over to an employer plan all of a payment that includes after-tax contributions, but only through a direct

rollover (and only if the receiving plan separately accounts for after-tax contributions and is not a governmental section

457(b) plan). You can do a 60-day rollover to an employer plan of part of a payment that includes after-tax contributions,

but only up to the amount of the payment that would be taxable if not rolled over.

If you miss the 60-day rollover deadline

Generally, the 60-day rollover deadline cannot be extended. However, the IRS has the limited authority to waive the deadline

under certain extraordinary circumstances, such as when external events prevented you from completing the rollover by the

60-day rollover deadline. Under certain circumstances, you may claim eligibility for a waiver of the 60-day rollover deadline

by making a written self-certification. Otherwise, to apply for a waiver from the IRS, you must file a private letter ruling

request with the IRS. Private letter ruling requests require the payment of a nonrefundable user fee. For more information,

see IRS Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs).

If you were born on or before January 1, 1936

If you were born on or before January 1, 1936 and receive a lump sum distribution that you do not roll over, special rules

for calculating the amount of the tax on the payment might apply to you. For more information, see IRS Publication 575,

Pension and Annuity Income.

If you are an eligible retired public safety officer and your payment is used to pay for health coverage or qualified

long-term care insurance

If you retired as a public safety officer, and your retirement was by reason of disability or was after normal retirement age,

you can exclude from your taxable income Plan payments paid directly as premiums to an accident or health plan (or a

qualified long-term care insurance contract) that your employer maintains for you, your spouse, or your dependents, up to

a maximum of $3,000 annually. For this purpose, a public safety officer is a law enforcement officer, firefighter, chaplain,

or member of a rescue squad or ambulance crew.

Page 7 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Page 4 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

If you roll over your payment to a Roth IRA

If you roll over a payment from the Plan to a Roth IRA, a special rule applies under which the amount of the payment rolled

over (reduced by any after-tax amounts) will be taxed. In general, the 10% additional income tax on early distributions will

not apply. However, if you take the amount rolled over out of the Roth IRA within the 5-year period that begins on January

1 of the year of the rollover, the 10% additional income tax will apply (unless an exception applies).

If you roll over the payment to a Roth IRA, later payments from the Roth IRA that are qualified distributions will not be

taxed (including earnings after the rollover). A qualified distribution from a Roth IRA is a payment made after you are age

59½ (or after your death or disability, or as a qualified first-time homebuyer distribution of up to $10,000) and after you

have had a Roth IRA for at least 5 years. In applying this 5-year rule, you count from January 1 of the year for which your

first contribution was made to a Roth IRA. Payments from the Roth IRA that are not qualified distributions will be taxed to

the extent of earnings after the rollover, including the 10% additional income tax on early distributions (unless an exception

applies). You do not have to take required minimum distributions from a Roth IRA during your lifetime. For more

information, see IRS Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs), and IRS Publication

590-B, Distributions from Individual Retirement Arrangements (IRAs).

If you are not a Plan member

Payments after death of the member. If you receive a distribution after the member’s death that you do not roll over, the

distribution generally will be taxed in the same manner described elsewhere in this notice. However, the 10% additional

income tax on early distributions and the special rules for public safety officers do not apply, and the special rule described

under the section "If you were born on or before January 1, 1936" applies only if the deceased member was born on or

before January 1, 1936.

If you are a surviving spouse. If you receive a payment from the Plan as the surviving spouse of a deceased member, you

have the same rollover options that the member would have had, as described elsewhere in this notice. In addition, if you

choose to do a rollover to an IRA, you may treat the IRA as your own or as an inherited IRA.

An IRA you treat as your own is treated like any other IRA of yours, so that payments made to you before you are age 59½

will be subject to the 10% additional income tax on early distributions (unless an exception applies) and required minimum

distributions from your IRA do not have to start until after you are age 70½ (if you were born before July 1, 1949) or age

72 (if you were born after June 30, 1949).

If you treat the IRA as an inherited IRA, payments from the IRA will not be subject to the 10% additional income tax on

early distributions. However, if the member had started taking required minimum distributions, you will have to receive

required minimum distributions from the inherited IRA. If the member had not started taking required minimum

distributions from the Plan, you will not have to start receiving required minimum distributions from the inherited IRA until

the year the member would have been age 70 ½ (if the participant was born before July 1, 1949) or age 72 (if the participant

was born after June 30, 1949).

If you are a surviving beneficiary other than a spouse. If you receive a payment from the Plan because of the member's

death and you are a designated beneficiary other than a surviving spouse, the only rollover option you have is to do a direct

rollover to an inherited IRA. Payments from the inherited IRA will not be subject to the 10% additional income tax on early

distributions. You will have to receive required minimum distributions from the inherited IRA.

Payments under an EDRO. If you are the spouse or former spouse of the member who receives a payment from the Plan

under an EDRO, you generally have the same options and the same tax treatment that the member would have (for example,

you may roll over the payment to your own IRA or an eligible employer plan that will accept it). However, payments under

the EDRO will not be subject to the 10% additional income tax on early distributions.

Page 8 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Page 5 of 5 Special Tax Notice Regarding Your Rollover Options (REV. 12/20)

If you are a nonresident alien

If you are a nonresident alien and you do not do a direct rollover to a U.S. IRA or U.S. employer plan, instead of withholding

20%, the Plan is generally required to withhold 30% of the payment for federal income taxes. If the amount withheld exceeds

the amount of tax you owe (as may happen if you do a 60-day rollover), you may request an income tax refund by filing

Form 1040NR and attaching your Form 1042-S. See Form W-8BEN for claiming that you are entitled to a reduced rate of

withholding under an income tax treaty. For more information, see also IRS Publication 519, U.S. Tax Guide for Aliens,

and IRS Publication 515, Withholding of Tax on Nonresident Aliens and Foreign Entities.

Other special rules

If a payment is one in a series of payments for less than 10 years, your choice whether to do a direct rollover will apply to

all later payments in the series (unless you make a different choice for later payments).

If your payments for the year are less than $200, the Plan is not required to allow you to do a direct rollover and is not

required to withhold federal income taxes. However, you may do a 60-day rollover.

You may have special rollover rights if you recently served in the U.S. Armed Forces. For more information on special

rollover rights related to the U.S. Armed Forces, see IRS Publication 3, Armed Forces' Tax Guide. You also may have

special rollover rights if you were affected by a federally declared disaster (or similar event), or if you received a distribution

on account of a disaster. For more information on special rollover rights related to disaster relief, see the IRS website at

www.irs.gov.

FOR MORE INFORMATION

You may wish to consult with the Plan administrator or a professional tax advisor, before taking a payment from the Plan.

Also, you can find more detailed information on the federal tax treatment of payments from employer plans in: IRS Publi-

cation 575, Pension and Annuity Income; IRS Publication 590-A, Contributions to Individual Retirement Arrangements

(IRAs); IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs); and IRS Publication 571,

Tax-Sheltered Annuity Plans (403(b) Plans). These publications are available from a local IRS office, on the web at

www.irs.gov, or by calling 1-800-TAX-FORM.

The State Retirement Agency strongly urges you to consult with a qualified tax advisor, the Internal Revenue Ser-

vice, or a Certified Public Accountant regarding the tax consequences of your distribution as it relates to your spe-

cific tax situation.

Page 9 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Application for Withdrawal of Accumulated

Contributions Package

This page intentionally left blank

Page 10 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

IMPORTANT: PLEASE READ “SUMMARY OF MAJOR RETIREMENT BENEFITS”

BENEFITS SYSTEMS

Non-Contributory /Contributory

Pension System

Alternate Contributory

Pension Selection Plan – enrolled

before 7/1/2011

Reformed Contributory Pension

Benefit – Enrolled on or after July

1, 2011

Retirement System – Note:

Bifurcated members are in the

Retirement System but receive a

combination benefit from both the

Retirement & applicable Pension System

Service

Retirement

Eligibility

Formula

Members enrolled prior to 7/1/2011:

Age 62 with at least 5 years of eligibility

service, OR

Age 63 with at least 4 years of eligibility

service, OR

Age 64 with at least 3 years of eligibility

service, OR

Age 65 or older with at least 2 years of

eligibility service, OR

At least 30 years of eligibility service

regardless of age.

Members enrolled 7/1/2011 or later:

See Reformed Contributory Pension

section

Non-Contributory Pension: .8% of

average final compensation up to Social

Security integration level, plus 1.5% of

average final compensation in excess of

the Social Security Integration Level,

times creditable service.

Contributory Pension: 1.2% of average

final compensation times service credit as

of June 30, 1998, plus 1.4% of average

final compensation times creditable

service earned after June 30, 1998.

Age 62 with at least 5 years of eligibility

service, OR

Age 63 with at least 4 years of eligibility

service, OR

Age 64 with at least 3 years of eligibility

service, OR

Age 65 or older with at least 2 years of

eligibility service, OR

At least 30 years of eligibility service

regardless of age.

1.2% of average final compensation

times creditable service as of June 30,

1998, plus 1.8% of average final

compensation after June 30, 1998.

Age 65 with at least 10 years of

eligibility service, OR

Rule of 90 (sum of age and eligibility

service equal 90).

1.5% of average final compensation

times creditable service.

At least age 60, regardless of creditable

service, OR

At least 30 years of creditable service,

regardless of age.

1.8% of average final compensation

times creditable service.

Page 11 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

BENEFITS SYSTEMS

Non-Contributory /Contributory

Pension System

Alternate Contributory

Pension Selection Plan – enrolled

before 7/1/2011

Reformed Contributory Pension

Benefit – Enrolled on or after July

1, 2011

Retirement System – Note:

Bifurcated members are in the

Retirement System but receive a

combination benefit from both the

Retirement & applicable Pension System

Early

Retirement

Eligibility

Early

Retirement

Formula

Member enrolled prior to 7/1/2011:

At least age 55 with at least 15 years of

eligibility service.

Member enrolled 7/1/2011 or later:

At least age 60 with at least 15 years of

eligibility service

Member enrolled prior to 7/1/2011:

Same as service retirement formula, but

reduced .005 times the number of months

to age 62. Maximum reduction of 42%.

Member enrolled 7/1/2011 and later:

Same as service retirement formula, but

reduced .005 times the number of months

to age 65. Maximum reduction of 30%.

At least age 55 with at least 15 years of

eligibility service.

Same as service retirement formula, but

reduced .005 times the number of months

to age 62. Maximum reduction of 42%.

For members who earn service credit on a

ten month basis, the reduction is .006 for

each month prior to age 62.

At least age 60 with at least 15 years of

eligibility service.

Same as service retirement formula, but

reduced .005 times the number of months

to age 65. Maximum reduction of 30%.

For members who earn service credit on a

ten month basis, the reduction is .006 for

each month prior to age 65.

At least 25 years of creditable service.

Same as service retirement formula, but

reduced .005 times the lesser of the

number of months to age 60 or 30 years

of service. For members who earn service

credit on a ten month basis, the reduction

is .006 for each month prior to 30 years.

Vested Service

Retirement

Eligibility

Formula

Member enrolled prior to 7/1/2011:

At least 5 years of eligibility service.

Member enrolled 7/1/2011 or later:

At least 10 years of eligibility service.

Member enrolled prior to 7/1/2011:

Same as service formula with benefits

beginning at age 62, OR an early service

retirement if eligible.

Member enrolled 7/1/2011 or later:

Same as service formula with benefits

beginning at age 65, OR an early service

retirement if eligible.

At least 5 years of eligibility service.

Same as service formula with benefits

beginning at age 62, OR an early service

retirement if eligible.

At least 10 years of eligibility service.

Same as service formula with benefits

beginning at age 65, OR an early service

retirement if eligible.

At least 5 years of eligibility service.

Same as service formula with benefits

beginning at age 60.

Page 12 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

BENEFITS SYSTEMS

Non-Contributory /Contributory

Pension System

Alternate Contributory

Pension Selection Plan – enrolled

before 7/1/2011

Reformed Contributory Pension

Benefit – Enrolled on or after July

1, 2011

Retirement System – Note:

Bifurcated members are in the

Retirement System but receive a

combination benefit from both the

Retirement & applicable Pension System

Ordinary

Disability

Retirement

Eligibility

Formula

Permanently disabled after 5 years of

eligibility service.

Member enrolled prior to 7/1/2011:

Same as service retirement formula using

creditable service projected to age 62.

Member enrolled prior to 7/1/2011:

Same as service retirement formula using

creditable service projected to age 65.

Permanently disabled after 5 years of

eligibility service.

Same as service retirement formula using

creditable service projected to age 62.

Permanently disabled after 5 years of

eligibility service.

Same as service retirement formula using

creditable service projected to age 65.

Permanently disabled after 5 years of

eligibility service.

Same as service retirement formula with

a minimum of 25% of average final

compensation or a formula using

creditable service projected to age 60.

Accidental

Disability

Retirement

Eligibility

Accidental

Disability

Retirement

Formula

Permanently and totally disabled by an

accident in the performance of duty.

2/3 of average final compensation plus

accumulated contributions paid as an

annuity.

Permanently and totally disabled by an

accident in the performance of duty.

2/3 of average final compensation plus

accumulated contributions paid as an

annuity.

Permanently and totally disabled by an

accident in the performance of duty.

2/3 of average final compensation plus

accumulated contributions paid as an

annuity.

Permanently and totally disabled by an

accident in the performance of duty.

2/3 of average final compensation plus

accumulated contributions paid as an

annuity.

Page 13 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

BENEFITS SYSTEMS

Non-Contributory /Contributory

Pension System

Alternate Contributory

Pension Selection Plan – enrolled

before 7/1/2011

Reformed Contributory Pension

Benefit – Enrolled on or after July

1, 2011

Retirement System – Note:

Bifurcated members are in the

Retirement System but receive a

combination benefit from both the

Retirement & applicable Pension System

Cost-of-Living

Adjustment to

Retirement

Benefit

Eligibility

Formula

Retired at least 1 year as of July 1

st

.

Member enrolled prior to 7/1/2011:

Any annual adjustment based on changes

in the Consumer Price Index. Any annual

adjustment limited to a maximum of 3%

of the initial/current (for non-

Contributory/Contributory plan)

retirement benefit for service credit

earned by 7/1/2011. Service after

7/1/2011 earns adjustment capped at

2.5% if assumed rate of return for

investments in prior calendar year is met

otherwise 1% if investment target not

met.

Member enrolled 7/1/2011 or later:

Any annual adjustment based on

Consumer Price Index. Limited to 2.5%

if assumed rate of return for investments

is prior calendar year met otherwise 1% if

investment target not met.

Retired at least 1 year as of July 1

st

.

Any annual adjustment based on changes

in the Consumer Price Index. Any annual

adjustment limited to a maximum of 3%

of the current retirement benefit for

service credit earned by 7/1/2011.

Service after 7/1/2011 earns adjustment

capped at 2.5% if assumed rate of return

for investments in prior calendar year is

met otherwise 1% if investment target not

met.

Retired at least 1 year as of July 1

st

.

Any annual adjustment based on

Consumer Price Index. Capped at 2.5% if

assumed rate of return for investments is

prior calendar year met otherwise 1% if

investment target not met.

Retired at least 1 year as of July 1

st

.

Any annual adjustment based on

Consumer Price Index. Unlimited annual

adjustment for Plan A; maximum of 5%

for Plan B; and a combination for Plan C

based upon previous and current plans of

participation.

Death Benefits –

If you die before

retirement while

actively employed

or while on an

approved leave of

absence and you

have at least one

year of eligibility.

Beneficiary may

receive:

(1) a single payment of your accumulated

contributions plus your annual salary.

If your sole primary beneficiary is your

spouse, the spouse may choose a monthly

allowance instead of the above benefit, if

you: (1) were eligible to retire; or (2) had

25 years of eligibility service, or (3) were

age 55 or older and had at least 15 years

of eligibility service.

If you are killed in the line of duty,

different benefits are paid to your eligible

spouse, minor children, or dependent

parent.

(1) a single payment of your accumulated

contributions plus your annual salary.

If your sole primary beneficiary is your

spouse, the spouse may choose a monthly

allowance instead of the above benefit, if

you: (1) were eligible to retire; or (2) had

25 years of eligibility service, or (3) were

age 55 or older and had at least 15 years

of eligibility service.

If you are killed in the line of duty,

different benefits are paid to your eligible

spouse, minor children, or dependent

parent.

(1) a single payment of your

accumulated contributions plus your

annual salary.

If your sole primary beneficiary is your

spouse, the spouse may choose a monthly

allowance instead of the above benefit, if

you: (1) were eligible to retire; or (2) had

25 years of eligibility service, or (3) were

age 55 or older and had at least 15 years

of eligibility service.

If you are killed in the line of duty,

different benefits are paid to your eligible

spouse, minor children, or dependent

parent.

(1) a single payment of your accumulated

contributions plus your annual salary.

If your sole primary beneficiary is your

spouse, the spouse may choose a monthly

allowance instead of the above benefit, if

you: (1) were eligible to retire; or (2) had

25 years of creditable service, or (3) were

age 55 or older and had at least 15 years

of creditable service.

If you are killed in the line of duty,

different benefits are paid to your eligible

spouse, minor children, or dependent

parent.

Page 14 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

PUBLIC SAFETY PLANS

STATE POLICE RETIREMENT SYSTEM

1. Service Retirement: at age 50, or with 22 years (25 years for members enrolled 7/1/2011 or later) of eligibility service.

2. Vested Retirement: at age 50 if you have at least 5 years (10 years for members enrolled 7/1/2011 or later) of eligibility service.

3. Ordinary Disability Retirement: If you are permanently incapacitated with at least 5 years of eligibility service, regardless of age.

4. Special Disability Retirement: If you are permanently incapacitated in the performance of duty, regardless of age or creditable service.

5. Cost-of-Living Adjustment to Retirement Benefit: Must be retired at least one year as of July 1. Any annual adjustment based on changes in the Consumer Price Index. Any annual

adjustment unlimited for service credit earned by 7/1/2011. Service after 7/1/2011 earns adjustment capped at 2.5% if assumed rate of return for investments in prior calendar year is met

otherwise 1% if investment target not met.

CORRECTIONAL OFFICERS’ RETIREMENT SYSTEM

1. Service Retirement: at age 55 OR have 20 years of eligibility service, the last 5 years of which must be as a member in one of the classifications listed above.

2. Vested Retirement: at age 55 (60 for security attendants at Clifton T. Perkins Hospital Center who separated employment before July 1, 2016) if you have at least 5 years (10 years for

members enrolled 7/1/2011 or later) of eligibility service.

3. Ordinary Disability Retirement: If you are permanently incapacitated with at least 5 years of eligibility service, regardless of age.

4. Accidental Disability Retirement: If you are permanently incapacitated in the performance of duty, regardless of age or creditable service.

5. Cost-of-Living Adjustment to Retirement Benefit: Must be retired at least one year as of July 1. Any annual adjustment based on changes in the Consumer Price Index. Any annual

adjustment unlimited for service credit earned by 7/1/2011. Service after 7/1/2011 earns adjustment capped at 2.5% if assumed rate of return for investments in prior calendar year is met

otherwise 1% if investment target not met.

LAW ENFORCEMENT OFFICERS’ PENSION PLAN

1. Service Retirement: at age 50 or with 25 years of eligibility service.

2. Vested Retirement: at age 50 with at least 5 years (10 years for members enrolled 7/1/2011 or later) of eligibility service.

3. Ordinary Disability Retirement: If you are permanently incapacitated with at least 5 years of eligibility service, regardless of age.

4. Accidental Disability Retirement: If you are permanently incapacitated in the performance of duty, regardless of age or creditable service.

5. Cost-of-Living Adjustment to Retirement Benefit: Must be retired at least one year as of July 1. Any annual adjustment based on changes in the Consumer Price Index. Any annual

adjustment limited to a maximum of 3% of the current retirement benefit for service credit earned by 7/1/2011. Service after 7/1/2011 earns adjustment capped at 2.5% if assumed rate of

return for investments in prior calendar year is met otherwise 1% if investment target not met.

OTHER RETIREMENT SYSTEMS

JUDGES’ RETIREMENT SYSTEM

1. For an individual who was a member of the Judges’ Retirement System on or before June 30, 2012:

a. A Retirement Allowance if: (1) You are at least age 60 regardless of the years of creditable service as a judge or (2) You resign because of an incapacitating illness regardless of age

or years of creditable service as a judge.

b. A Vested Retirement Allowance: At age 60 if you leave your accumulated contributions on deposit with the Maryland State Retirement Agency.

2. For an individual who was a member of the Judges’ Retirement System on or after July 1, 2012:

a. A Retirement Allowance if: (1) You are at least age 60 and have at least five years of eligibility service or (2) You resign because of an incapacitating illness regardless of age or

years of creditable service as a judge.

b. A Vested Retirement Allowance: At age 60 if you have at least five years of eligibility service and if you leave your accumulated contributions on deposit with the Maryland State

Retirement Agency.

LEGISLATIVE PENSION SYSTEM - For members of the Legislative Pension System, please call the Maryland State Retirement Agency for information.

If you wish to apply for one of the benefits, contact your employer’s retirement coordinator or a retirement benefits specialist at 410-625-5555 or toll-free at 1-800-

492-5909 for the appropriate form or for additional information. Keep this information for your records.

Page 15 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Application for Withdrawal of Accumulated

Contributions Package

This page intentionally left blank

Page 16 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

MARYLAND STATE RETIREMENT AGENCY

120 EAST BALTIMORE STREET

BALTIMORE, MARYLAND 21202-6700

APPLICATION FOR WITHDRAWAL

OF ACCUMULATED CONTRIBUTIONS

RETIREMENT USE ONLY Form 5 (REV. 8/23)

Purpose of this form: This form is used by an individual to request a withdrawal of his or her balance of

accumulated contributions from the Maryland State Retirement and Pension System (System). An individual

is eligible to request a withdrawal only if he or she has resigned or has been terminated from the position

which made the person eligible to participate in the System. If you have not resigned your position or you

have not been terminated from your position you are not eligible to withdraw your balance of accumulated

contributions from the System.

INSTRUCTIONS

Please print in ink, using one space per letter or •

number and skip a space between words.

The top portion of this form (Section I) is to be •

completed by the person who is applying to with-

draw his or her balance of accumulated contribu-

tions from the System.

Your signature on this form must be notarized. •

Do not sign on the Member’s Signature line until

you are in the presence of a Notary Public who

can notarize your signature.

If your resignation/termination date is less than •

six months from the date that you are completing

and submitting this form, a representative from

your former employer’s human resources depart-

ment must complete the bottom portion of the

form (Section II), titled “To be completed by the

Retirement Coordinator,” before you submit the

completed form to the Retirement Agency.

If you choose Refund Choice No. 1 you do not •

need to complete the Form 193 Trustee-to-

Trustee Distribution Form for Rollovers.

If you choose Refund Choice No. 2 or Refund •

Choice No. 3 a completed copy of the Form 193

Trustee-to-Trustee Distribution Form for

Rollovers must be submitted with this form.

Please allow up to 90 days from the latter of the •

Retirement Agency’s receipt of your payroll con-

tribution (the last pay period from your resigna-

tion/termination) or the receipt of your properly

completed forms for the Retirement Agency to

process your request.

Refunds are paid by paper checks which are •

mailed to the address that you provide on this

form. Note: Even if you requested to roll over all

or a portion of your refund, all checks are mailed

to you at the address provided on this form.

The Retirement Agency will withhold federal •

taxes equal to 20% and Maryland state taxes

(only if you are a Maryland resident) equal to

7.75% of the taxable refund amount not rolled

over to another qualified retirement plan.

If you need additional assistance to complete this •

form, you may call 410-625-5555 or toll-free 1-

800-492-5909.

The original, completed form must be returned to •

the Maryland State Retirement Agency, 120 E.

Baltimore Street, Baltimore, Maryland 21202-

6700.

Please note: If you fax your completed forms to

the Retirement Agency, the Notary seal on Form

5 must be visible by Agency staff.

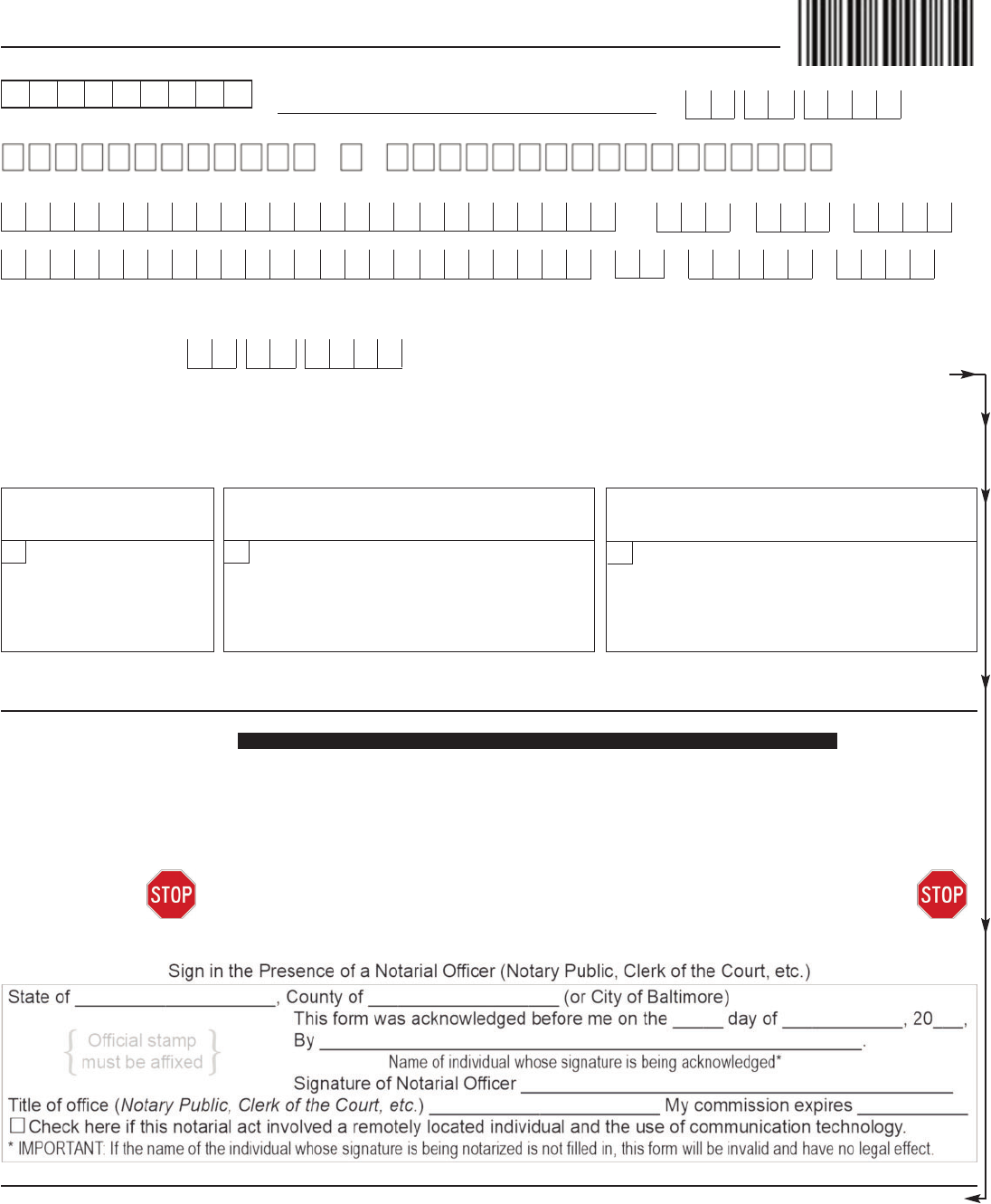

FORM 5 (REV. 8/23) Page 1 of 2

Page 17 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

NAME

First Initial Last

Number and Street

Retirement Coordinator Signature Date Telephone Number

Name of the Employing Agency at Resignation/Termination

Daytime Telephone Number

A rollover of after-tax amounts is only permitted to an IRA or as a direct rollover to a 401(a) plan or 403(b) annuity that agrees to separately account for the after-

tax amounts. Any employer pick-up contributions transferred under payment choices 2 or 3 lose their post tax status for Maryland income tax purposes. Mandatory

federal income tax withholding is at the rate of 20% on the taxable amount paid to you.

PLEASE READ THE FREQUENTLY ASKED QUESTIONS AND SPECIAL TAX NOTICE BEFORE SELECTING YOUR CHOICE. CHECK ONE:

RETIREMENT COORDINATOR COMPLETES THIS SECTION EMPLOYING AGENCY NAME: ______________________________________

This member’s resignation/termination date is: ______________ This member’s pay period ending date is: ______________

I certify that the above information regarding resignation/termination date is true and accurate to the best of my knowledge and that I am authorized to

certify this information by my employer.

____________________________________________ _________________ _(______)____________________________

Signature and Certification: I apply for the withdrawal of my accumulated contributions with interest earned and thereby terminate my membership in the Maryland

State Retirement and Pensions System and forfeit any further right to receive a future benefit, including disability retirement benefits. I have read and under-

stand the Summary of Major Retirement Benefits. By signing below

, I certify the following:

1) the information I have provided herein is correct;

2) as of the date of this application, I have separated from my employment with all employers that participate in the System; and

3) I have received the IRS Safe Harbor explanation titled Special Tax Notice Regarding Your Rollover Options (“Special Tax Notice”), have had an opportunity to

review the Special Tax Notice with my tax advisor, accountant, attorney, or the IRS, and understand my options with respect to receipt of a distribution from the System

at this time. I understand that I have at least 30 days to review the Special Tax Notice and consider whether or not to have my payment rolled over. I further understand

that, if I complete and submit this form prior to the end of the 30-day period for reviewing the Special Tax Notice, I have waived my right to the 30-day period to review

the Special Tax Notice.

SOCIAL SECURITY NUMBER

HOME ADDRESS

City State ZIP Code

Email address: ________________________________________________

-

- -

Refund $__________________ to me. Balance transferred to

an “eligible retirement plan” (Traditional IRA, 401(a) plan,

403(a) or (b) annuity, 408A Roth IRA or 457(b) governmental

plan.) (If transferring to a 457(b) governmental plan or 403(a)

annuity plan, the minimum payable to me is the non-taxable

amount, if any.)

REFUND CHOICE NO. 2

(Complete Form 193)

Entire amount transferred to an “eligible retirement

plan” (Traditional IRA, 401(a) plan, 403(a) or (b)

annuity, 408A Roth IRA or 457(b) governmental

plan.) Both 457(b) governmental plans and 403(a)

annuity plans prohibit a rollover of non-taxable

funds from this plan.)

Entire amount refunded

to me.

REFUND CHOICE NO. 1

(Do Not Complete Form 193)

REFUND CHOICE NO. 3

(Complete Form 193)

Member’s Signature ____________________________________________________________________ Date ______________________

Month Day Year

DATE OF BIRTH

- -

Are you a resident of Maryland? No ___ Yes ___ (For Maryland residents, State income tax withholding of 7.75% will be withheld from the taxable amount paid to you.)

Resignation/Termination Date:

Have you submitted a claim for disability? No ___ Yes ___ If Yes, know that by completing and submitting this form, you are forfeiting all rights to a future benefit,

including disability, and your disability claim will be terminated.

Are you transferring to a State Agency, County Board of Education, or Participating Governmental Unit? No ___ Yes ___

If yes, give name of new employing agency ________________________________________________________________

Mo. Day Yr.

- -

If date entered is less than six months from date this form is signed, return completed

form to your former employer’s retirement coordinator to complete bottom section.

SECTION I — To be completed by the Withdrawal Applicant

SECTION II — To be completed by the Retirement Coordinator

FORM 5 (REV. 8/23) Page 2 of 2

Do Not Sign This Form Until You Are in the Presence of a Notary Public.

► ► ► ► ► This form MUST be signed and notarized in order to be valid. ◄ ◄ ◄ ◄ ◄

Page 18 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

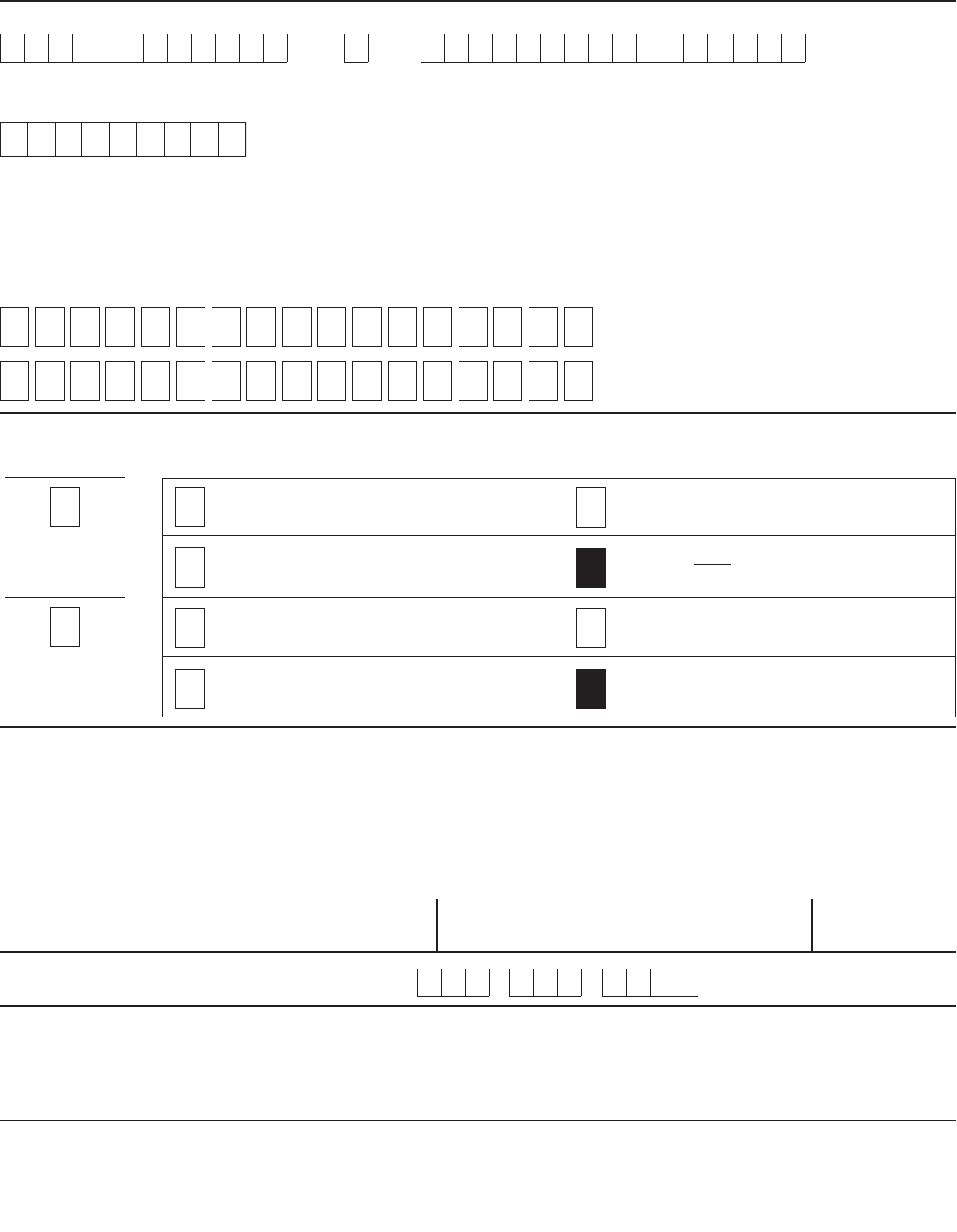

MARYLAND STATE RETIREMENT AGENCY

120 EAST BALTIMORE STREET

BALTIMORE, MARYLAND 21202-6700

TRUSTEE-TO-TRUSTEE DISTRIBUTION FORM

FOR ROLLOVERS

RETIREMENT USE ONLY Form 193 (REV. 8/23)

Purpose of this form: This form is used by an individual applying to receive a lump sum payment from the

Maryland State Retirement Agency and who wants to rollover all or a portion of the payment to another quali-

fied retirement plan.

Instructions

Section I of this form is to be completed by the •

individual (the Payee) who is applying to receive

the lump sum payment from the Retirement

Agency.

Section II of this form is to be completed by a •

representative of the financial institution who will

be accepting the rollover.

Please print in ink, using one space per letter or •

number and skipping a space between words.

Keep a copy of the completed form for your •

records.

If you need additional assistance, please contact •

a retirement benefits specialist at 410-625-5555

or toll-free 1-800-492-5909.

The completed form must be returned to the •

Maryland State Retirement Agency, 120 E.

Baltimore Street, Baltimore, Maryland 21202-

6700.

FORM 193 (8/23) Page 1 of 3

Page 19 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

Based on the payment option I selected, I direct the SRA to do the following:

SECTION I — To be completed by the Payee

NEXT PAGE ALSO MUST BE COMPLETED

AND

The account balance will be made payable to your designated IRA or Eligible Employer Plan. (Note: distributions to a

457(b) governmental plan or a 403(a) annuity may not exceed the taxable amount.)

I understand the Agency may issue two checks to me: one payable to my order for an amount I elect to receive and the

other payable to the order of both me and the IRA or Eligible Employer Plan that is to receive my rollover distribution. I

understand that I am responsible for delivering the check for my rollover distribution directly to the IRA or Eligible

Employer Plan for processing within 60 days after I receive the check, and I agree to do so.

SRA will not process more than one trustee-to-trustee distribution. Thus, if you want to move funds between IRA’s and/or

Eligible Employer Plans, contact the IRA or Eligible Employer Plan to which you are making the direct rollover to deter-

mine whether transfers are allowable.

I understand and agree to the above distribution conditions.

PAYEE (Signature): DATE:

Check [ ] only one option to indicate payment selection.

Pay to me my designated flat dollar refund amount of $___________________.

OR

Pay to me all federal “NON-TAXABLE” funds to be determined at time of payment.

NAME

First Initial Last

Number and Street

SOCIAL SECURITY NUMBER DAYTIME PHONE NUMBER

HOME ADDRESS

City State ZIP Code

-

-

-

Ext. _____________

For help in completing this form, please view the training video on the Retirement Agency’s website at sra.maryland.gov.

If you need additional

assistance, telephone a retirement benefits specialist at 410-625-5555 or toll-free at 1-800-492-5909.

FORM 193 (8/23) Page 2 of 3

P

Page 20 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)

I confirm that the payee, account number and title are correct. Further, I confirm that the plan designated by the payee is

(or is intended to be) an IRA, or an Eligible Employer Plan which includes a plan qualified under section 401(a) of the

Internal Revenue Code, including a 401(k) plan, profit sharing plan, defined benefit plan, stock bonus plan, and money pur-

chase plan; a section 403(a) annuity plan; a section 403(b) tax sheltered annuity; or an eligible section 457(b) plan main-

tained by a governmental employer (governmental 457 plan), that the plan designated may accept such payment (including

any after-tax contributions, if applicable) and that I am authorized to act on behalf of the designated plan and will accept

the direct rollover for the payee and account for it as required by the Internal Revenue Code.

PRINT OR TYPE REPRESENTATIVE’S NAME SIGNATURE OF REPRESENTATIVE DATE

REPRESENTATIVE’S AREA CODE/TELEPHONE:

PLEASE READ THIS CAREFULLY: All information on this form, including the individual’s Social Security num-

ber, is required. The information is confidential and will be used only to process payment data from the Maryland

State Retirement Agency to the financial institution and its agent. Failure to provide the requested information

may prevent or delay release or payment.

For help in completing this form, please view the training video on the Retirement Agency’s website at sra.maryland.gov. If you

need additional assistance, telephone a retirement benefits specialist at 410-625-5555 or toll-free at 1-800-492-5909.

FORM 193 (8/23) Page 3 of 3

The arrangement selected by the Payee is: (Check [ ] one):

DEPOSITOR ACCOUNT TITLE: In order to properly prepare the check, the Retirement Agency needs the name of the

financial institution/account into which the check will be made payable. Enter in the spaces below this information, up to

34 characters. The check payable to your designated financial institution/account will carry the notation “DIRECT

ROLLOVER,” and will contain the name for the individual indicated in Section I. For IRA’s, the check will read payable to:

[Information Below] as trustee of IND. RET. ACCT of [Payee in Section I]. For Eligible Employer Plans, the check will read

payable to: [Information Below] FBO [Payee in Section I].

Qualified plan under §401(a), including

a 401(k) plan

§403(a) qualified annuity

§403(b) tax sheltered annuity

§457(b) governmental plan

Check indicates plan separately accounts

for after-tax contributions and earnings

Plan may NOT accept after-tax contribu-

tions from a 401(a) qualified plan

Check indicates plan separately accounts

for after-tax contributions and earnings

Plan may not accept after-tax contributions

Traditional IRA Eligible Employer Plan

SECTION II — To be completed by a representative of

the financial institution that will accept the rollover

Roth IRA

Check [ ] Box to Affirm that Plan Separately

Accounts for After-Tax Contributions & Earnings

PAYEE’S NAME

First Initial Last

PAYEE’S SOCIAL SECURITY NUMBER

-

-

P

P

Page 21 of 21

Application for Withdrawal of Accumulated Contributions Package (REV. 8/23)