CDP–WWF Temperature

Scoring Methodology

A temperature scoring method for

targets, corporates, and portfolios

Open-source methodology to translate

the ambition of corporate greenhouse gas

(GHG) emission reductions into

temperature scores for corporates and

investment portfolios

CDP Worldwide and WWF International

Version 1.5.

May, 2024

1

© CDP Worldwide and WWF International 2024

ABSTRACT

This methodology is an open-source method to enable the translation of corporate greenhouse

gas (GHG) emission reduction targets into temperature scores at a scope, company, and portfolio

level. The methodology allows generating temperature scores for individual scope level targets

(e.g., Scope 1, Scope 2, Scope 3). It also provides a protocol to aggregate scope level scores into

a common intuitive metric reflecting the ambition of the company’s GHG reduction targets. Finally,

the method defines a series of weighting options that enable Financial Institutions (FI) and others

to aggregate the temperature scores of companies in a portfolio to a portfolio temperature score.

This is an update (version 1.5) of the initial publication of the methodology, which was published

in 2020.

The methodology provides a public, transparent, and science-based protocol to assess the

ambition of corporates and portfolios based on the ambition of GHG reduction targets. It enables

users to assess the ambition of public GHG emission reduction targets and can help users

compare the relative ambition of one company’s target versus another. Likewise, the method

allows comparing different portfolio ambitions and FIs to calculate their own portfolio temperature

score, which is a key starting point for aligning the portfolio with long-term temperature goals such

as 1.5C.

2

© CDP Worldwide and WWF International 2024

CDP Worldwide and WWF International

About CDP

CDP is a global non-profit that runs the world’s environmental disclosure system for companies,

cities, states, and regions. Founded in 2000 and working with more than 740 financial institutions

with over US$136 trillion in assets, CDP pioneered using capital markets and corporate

procurement to motivate companies to disclose their environmental impacts, and to reduce

greenhouse gas emissions, safeguard water resources and protect forests. Over 24,000

organizations around the world disclosed data through CDP in 2023, with more than 23,000

companies – including listed companies worth two thirds of global market capitalisation – and over

1,100 cities, states, and regions. Fully TCFD aligned, CDP holds the largest environmental

database in the world, and CDP scores are widely used to drive investment and procurement

decisions towards a zero carbon, sustainable, and resilient economy. CDP is a founding member

of the Science Based Targets initiative, We Mean Business Coalition, The Investor Agenda, and

the Net Zero Asset Managers initiative.

Visit https://cdp.net/en or follow us @CDP to find out more.

About WWF

WWF is an independent conservation organization, with over 30 million followers and a global

network active in nearly 100 countries. Our mission is to stop the degradation of the planet's

natural environment and to build a future in which people live in harmony with nature, by

conserving the world's biological diversity, ensuring that the use of renewable natural resources

is sustainable, and promoting the reduction of pollution and wasteful consumption. Find out more

at panda.org.

3

© CDP Worldwide and WWF International 2024

KEY TERMINOLOGY

Carbon dioxide removal, or “CDR”: a process in which carbon dioxide (CO

2

) is removed from the

atmosphere by deliberate anthropogenic activities and durably stored in geological, terrestrial, or

ocean reservoirs, or in products

1

.

Compound Annual Reduction, or “CAR”: the annualized emissions reduction rate over a specific

period of time, as implied by climate scenarios and corporate GHG emissions reduction targets.

Default temperature score: default °C-value applied to companies in the absence of valid

climate target data (here: 3.4°C, derived from Climate Action Tracker’s “policies & action emission

scenario”).

Warming function: a linear regression model used to project the impact of GHG emissions

reduction rates on global warming by the end of the century.

Global climate models, simulations, and scenarios: Climate models are a mathematical

description of the earth’s climate system. Global coupled climate models include physical

principles of the atmosphere, ocean, land surface, and sea ice. The results from running global

climate models are referred to as model simulations. The scenarios are primarily derived from

Integrated Assessment Models (IAMs) and serve as boundary conditions for global climate

models. They describe possible future pathways, covering a wide range of assumptions regarding,

e.g., GHG emission trajectories, socio-economic trends, and technological developments. For

simplicity, we refer to the model simulations (based on different scenarios) as “scenarios”.

Temperature scores, or “TS”: a forward-looking metric that expresses the GHG emissions

reduction targets of a company, portfolio, or fund with the associated annual global mean surface

temperature rise.

Total GHG emissions: refer to the total of a company’s emission scope 1, scope 2, and scope 3

emissions. Scope 1 refers to direct emissions from sources that are owned or controlled by the

company, scope 2 refers to indirect emissions from purchased energy, and scope 3 refers to

indirect emissions (not included in scope 2) that occur upstream and downstream of a company’s

value chain. In the regression models, the GHG considered depend on the variable used for each

respective scope (see Chapter 4 for more details).

1

See IPCC_AR6_WGIII_Factsheet_CDR.pdf for further information.

4

© CDP Worldwide and WWF International 2024

Contents

1. Fundamentals ..................................................................................................................... 7

1.1. Understanding temperature scores .............................................................................. 7

1.2. What a temperature score does not cover ................................................................... 7

1.3. Warming Function versus Single Scenario ................................................................... 8

2. Key changes to the previous version ................................................................................... 9

3. Introduction and methodological overview..........................................................................10

4. Step 1: Create benchmarks ...............................................................................................12

4.1. Underlying data of linear regression models ...............................................................12

4.2. Linear regression models ............................................................................................13

4.2.1. Sector-specific variables and benchmarks ...........................................................15

4.2.2. Analysis for scenario selection .............................................................................17

4.2.3. Regression results ...............................................................................................19

5. Step 2a: Target validation ..................................................................................................22

5.1. Assigning a temperature score to disclosed targets ....................................................22

5.2. Target validation .........................................................................................................23

5.3. Default temperature score for companies without valid targets ...................................24

5.3.1. Purpose of a default temperature score ...............................................................24

5.3.2. Default score approaches ....................................................................................24

5.4. Temperature floor .......................................................................................................27

6. Step 2b: Company scoring .................................................................................................29

6.1. Target timeframe ........................................................................................................29

6.2. Target quality criteria ..................................................................................................30

6.3. Target criteria waterfall ...............................................................................................31

6.3.1. Target vintage ......................................................................................................32

6.3.2. Boundary coverage ..............................................................................................32

6.3.3. Target types .........................................................................................................33

6.3.4. Scope coverage ...................................................................................................34

6.3.5. Reduction ambition ..............................................................................................34

6.3.6. Target year ..........................................................................................................34

5

© CDP Worldwide and WWF International 2024

6.4. Multiple scope 3 targets ..............................................................................................35

6.4.1. Aggregation of multiple scope 3 temperature scores............................................36

6.5. Temperature score aggregation ..................................................................................37

6.6. Using temperature scores ...........................................................................................37

7. Step 3: Portfolio scoring .....................................................................................................39

7.1. Weighting objectives and principles ............................................................................39

7.2. Weighting options .......................................................................................................40

7.3. Weighting method assessment ...................................................................................43

7.4. Additional notes on the portfolio scoring ......................................................................46

8. Limitations and outlook ......................................................................................................47

8.1. Methodology limitations ..............................................................................................47

8.1.1. Linear regression model ......................................................................................47

8.1.2. Formula to compute annual reduction rates .........................................................48

8.1.3. Sector granularity .................................................................................................49

8.1.4. Climate target metric(s) ........................................................................................50

8.1.5. Forward- versus backward-looking assessment ...................................................50

8.1.6. Carbon credits and carbon offsets .......................................................................51

8.1.7. Assurance of GHG and GHG reduction target data..............................................51

8.2. Outlook: Next steps and future research .....................................................................51

9. Version control ...................................................................................................................53

9.1. Change log .................................................................................................................53

10. Consultation questions .......................................................................................................55

10.1. Step 2b .......................................................................................................................55

10.1.1. Should older targets be considered in the absence of recent target data? ........55

10.1.2. Should TS aggregation based on GHG weighting be conducted based on base

year or current year data? ..................................................................................................55

10.1.3. Aggregation when missing GHG data ...............................................................56

10.1.4. Weighting of multiple scope 3 targets ...............................................................56

10.1.5. Scoring of portfolios including targets using the CDP–WWF Temperature Score-

or Temperature Rating methodology ..................................................................................57

10.1.6. Do you agree with the scoring approach taken in Step 2b, Section 6.2.3.1. (see

“Target type exception”)? If not, what alternative suggestion do you have? .......................57

6

© CDP Worldwide and WWF International 2024

10.1.7. Do you agree with the general approach taken in Step 2b, Chapter 6 “Company

scoring”? 57

10.2. Step 1 .........................................................................................................................57

10.2.1. Do you agree with the approach taken in Step 1, “Create benchmarks”? ........57

10.3. Step 2a .......................................................................................................................57

10.3.1. Do you agree with the approach taken in Step 2a, Chapter 5 “Target validation”?

57

10.4. Step 3 .........................................................................................................................57

10.4.1. Do you agree with the approach taken in Step 3, Chapter 7 “Portfolio scoring”?

57

10.5. General questions .......................................................................................................57

10.5.1. Do you have suggestions for future research that could inform the next version of

the CDP–WWF Temperature Score methodology? ............................................................57

10.5.2. Do you have any other comments? ..................................................................57

11. References ........................................................................................................................58

12. Annex ................................................................................................................................60

Annex 1: Warming Function versus Single Scenario .............................................................60

Annex 2: Details of sector variables .......................................................................................62

Annex 3: Result of linear regression model ...........................................................................63

Annex 4: Calculation examples .............................................................................................69

Annex 5: Summary of required data for applying the Temperature Scoring method ..............73

Annex 6: Tables, figures, and equations ................................................................................76

Tables ................................................................................................................................76

Figures ...............................................................................................................................76

Equations ...........................................................................................................................77

7

© CDP Worldwide and WWF International 2024

1. Fundamentals

Given the diversity in climate target scopes, timeframes, and metrics used by companies across

various sectors, understanding, and comparing the adequacy of companies’ decarbonization

goals can be challenging. Initially published in October 2020, this methodology document was

designed to serve as a protocol for assessing and comparing the ambition of companies’ GHG

emissions reduction targets. The key audience of this methodology are Financial Institutions (FIs)

and large corporates wishing to assess, steer, and set targets on their scope 3 emissions as well

as data providers offering ITR metrics. Other users of this methodology include academia and civil

society, as well as supervisory authorities and regulators.

1.1. Understanding temperature scores

The first version of this method introduced a scoring methodology which translates diverse GHG

reduction targets into an intuitive metric expressed in projected warming by 2100. This metric,

sometimes referred to as an Implied Temperature Rise (ITR), can be used to compare the

ambition of different companies’ decarbonization goals as expressed in their public GHG

emissions reduction targets. Henceforth, this output metric will be referred to in this document as

a temperature score (TS).

These scores should not be interpreted like IPCC results (i.e., global climate projections) nor does

the metric predict a certain temperature outcome. Temperature scores instead allow a relative

comparison of climate ambition with respect to the temperature goals of the Paris Agreement. The

scores should be interpreted as follows: This company’s GHG reduction target implies an annual

reduction rate that is consistent with an ambition heading towards X°C – under the assumption

that all companies behave the same.

Users of TS can use this metric to engage with companies to set targets (or improve existing

ones), compare the ambition of corporate GHG emissions targets, measure the alignment of their

own scope 3, and set targets accordingly (e.g., at the portfolio level for FIs, or at the supply chain

level for large companies).

1.2. What a temperature score does not cover

Temperature scores are not intended to serve as a comprehensive metric summarising a

company’s climate transition performance or overall “green credentials”. Temperature scores do

not provide insights into a company’s operational or financial performance relative to these

ambitions, the current trajectory of the company’s historical GHG emissions, or the existence of a

credible climate transition plan to achieve these goals.

The primary purpose of this methodology’s TS is to assess a company’s climate target ambition

through a broad benchmark of climate scenarios. It is therefore suggested that temperature scores

are used as a comparative tool for assessing the climate ambition across multiple companies (e.g.,

within a supply chain or financial portfolio) or, on an aggregated level, of portfolios and supply

chains and that other complementary metrics are consulted to obtain a complete picture of a

8

© CDP Worldwide and WWF International 2024

company’s climate profile. Also, TS should not be used as a predictive tool for estimating a precise

degree of global warming.

1.3. Warming Function versus Single Scenario

To calculate a temperature score, this methodology benchmarks companies’ committed GHG

reduction ambition against a statistical regression model based on all vetted modelled scenarios

of the IPCC’s Sixth Assessment Report (AR6) (see Chapter 4). This approach is referred to as the

“Warming Function” and establishes a linear statistical relationship between the rates of GHG

emissions reduction and the projected temperature outcomes these scenarios imply by the end of

the century.

The Warming Function differs from a Single Scenario approach. A Single Scenario approach relies

on one single scenario and assumes that the future will unfold as per the selected single scenario’s

underlying assumptions. Because the Warming Function approach relies on multiple scenarios, it

reduces the scenario selection bias inherent to the Single Scenario approach. It also provides

greater comparability between implementations of the CDP–WWF method from different data

providers and users. This is as comparability between temperature scores using single scenario

approaches rely on the use of the same scenario for TC computation. However, the robustness

the CDP–WWF warming function provides is traded against less transparency on the effects of

the different assumptions underlying the input models and scenarios of a Warming Function on

the temperature scores. Another difference is that the Single Scenario approach, by using only

one scenario, can more easily allow for more granular, sector-specific analysis compared to this

methodology’s Warming Function. Further research and development are needed to allow the use

of more sector-specific warming functions, in addition to the sectors currently covered with their

own warming functions: steel, aluminium, cement, and power generation.

CDP and WWF have considered the different approaches and concluded that the robustness of

the warming function is preferable, despite its trade-offs, as it provides a more comprehensive,

comparable, and unbiased view of potential temperature outcomes.

Please refer to Annex 1: Warming Function versus Single Scenario for further details about the

rationale supporting that conclusion.

9

© CDP Worldwide and WWF International 2024

2. Key changes to the previous version

This version 1.5 of the CDP–WWF Temperature Scoring methodology (formerly known as CDP–

WWF Temperature Rating) marks the first update since its initial publication in October 2020

(version 1.0).

The primary objectives of this update revolve around refreshing this methodology’s benchmarks

with the latest climate science. It also implements adjustments and improvements on specific

aspects to ensure it remains relevant, fair, and effective. Finally, this version adds transparency

on methodological choices and implications through the presentation of additional analysis,

enhanced explanation, and dedicated sections.

Key changes introduced in this version include (please refer to the change log in Chapter 9 for

more details):

- Update of the input climate model simulations and scenarios of the linear regression

models by substituting the Intergovernmental Panel on Climate Change (IPCC) SR15

model simulations and corresponding scenarios with the IPCC’s AR6 set of climate

simulations with scenarios, including adjustments of scenario filtering decisions (see

Chapter 4 for more details).

- Revision of the calculation formula for the annual rate of GHG emissions reduction,

transitioning from a Linear Annual Reduction to a Compound Annual Reduction

approach (see Section 4.2 for more details).

- Introduction of a specific scope 2 benchmark relying on energy related variables. Scope

1 and scope 2 assessments are now carried out at the single scope level (see Section

4.2.1 for more details).

- Clarification and enhancement of the target selection process (“waterfall”) to prioritize

targets when a company reports multiple targets within the same scope category and

timeframe (see Section 6.3 for more details).

- Update of the target timeframe definition for short-, medium-, and long-term (see

Chapter 6 for more details).

- Update of the default score from 3.2°C to 3.4°C for companies without valid targets or

insufficient data disclosure, reflecting the latest projection based on real-world action and

current policies (see Section 5.3 for more details).

- Clarification on the best possible temperature score for a company, introducing a 1.5°C

temperature floor (see Section 5.4 for more details).

- Addition of a dedicated chapter detailing this methodology’s purpose and intended

outcomes (Chapter 1). Another new chapter focuses on the methodology’s key

limitations and a roadmap for further updates planned (Chapter 8). Finally, a

presentation of the rationale for relying on a warming function over single-scenario-

based benchmarks was added in Chapter 1 and in Annex 1: Warming Function versus

Single Scenario.

10

© CDP Worldwide and WWF International 2024

3. Introduction and methodological overview

Companies are directly responsible for a significant portion of global GHG emissions

(Intergovernmental Panel on Climate Change (IPCC) (Ed.), 2022). GHG emission reduction

targets are a partial but relatively crucial forward-looking marker of a company’s ambition to

mitigate its climate impact. In 2023, close to 5000 companies covering approximately 10 gigaton

(GT) of scope 1+2 GHG emissions, publicly reported GHG emissions targets through CDP (based

on CDP data 2023). However, assessing and comparing the ambition of corporate targets has

traditionally been complex as targets can be expressed with different metrics, over multiple

timeframes and cover various types of emission scopes.

The aim of a temperature score is to translate GHG emission targets into a single intuitive metric

that is linked to the long-term temperature projections associated with the ambition of the target.

In the initial publication of this methodology (version 1.0), a protocol for expressing (“scoring”)

climate targets in a temperature metric referring to projected warming by 2100, was presented.

This updated version builds on the original method and further develops that protocol.

The methodology is composed of three steps, represented in Figure 1:

Figure 1: Steps of the Temperature Scoring methodology

The benchmark creation step (Step 1, Chapter 4) consists in running linear regression models.

The outputs of these models are based on a warming function, derived from all vetted model-

based scenarios in the IPCC Sixth Assessment Report (AR6) Scenario Explorer and Database

2

hosted by the International Institute for Applied Systems Analysis (IIASA) (Byers et al., 2022).

The linear regression models allow the assessment of end-of-century temperature outcomes

expected from short, medium, and long-term projected changes in absolute GHG emissions or

GHG emissions intensity metrics. As such, the regression models are used to relate target

ambition (measured in committed rate of GHG emission reduction) to warming projections by the

end of the century (expressed in centigrade temperature change compared to preindustrial levels).

2

Accessible through this link: https://data.ece.iiasa.ac.at/ar6/#/login?redirect=%2Fworkspaces.

Create benchmarks:

IPCC scenarios and

linear regression

models for different

variables and

timeframes

Step 2a

Target validation:

Assess validity of

targets

Portfolio scoring:

Aggregation of multiple

company scores into

one portfolio score

Step 2b

Company scoring:

Select targets and

compute scope-level

and company-level

temperature scores

Step 1

Step 2 (Company-level assessment)

Step 2 (Company-level assessment)

2 (

Company-level assessmentStep 1assessment)

Step 3

11

© CDP Worldwide and WWF International 2024

As companies often have multiple climate targets, covering different emission scopes and

timeframes, and users may receive data from several sources, Step 2a (Chapter 5) defines the

process and criteria for validating the various company’s GHG reduction targets. This step can be

seen as an eligibility screening of targets allowed as input for temperature score computation. In

Step 2b (Chapter 6), scope-level targets are selected using the selection hierarchy (“waterfall”),

and scope-level temperature scores are calculated. Finally, these TS are then aggregated into

combined company-level scores. The target validation step (Step 2a) defines the minimum quality

criteria for determining the acceptability of a GHG emissions reduction target to be scored. The

company scoring step (Step 2b) specifies the process required to select target data to be used for

scoring and how to aggregate multiple targets to produce company-level scores.

The final step (Step 3, Chapter 7) is used to weight company scores when assessing an

aggregation of companies, such as a financial portfolio or a company value chain.

In addition to computing temperature scores for disclosed targets, the methodology also defines

an approach to address non-disclosing companies. Default scores are introduced, also to allow

TS aggregation for company-, portfolio- or supply chain-level TS (see Section 5.3 on default

scores).

12

© CDP Worldwide and WWF International 2024

4. Step 1: Create benchmarks

4.1. Underlying data of linear regression models

The linear regression models used in this methodology are based on underlying data from global

climate models with scenarios from the IPCC’s AR6 (see Section 4.2 for more information about

the linear regression models). The data is collected and downloaded from the AR6 Scenarios

Database hosted on a Scenario Explorer by the International Institute for Applied Systems

Analysis (IIASA), released in 2022 (Byers et al., 2022)

3

.

Climate models are a mathematical description of the earth’s climate system. Global coupled

climate models include physical principles of the atmosphere, ocean, land surface, and sea ice.

The results from running global climate models are referred to as model simulations. The

scenarios, on the other hand, are primarily derived from Integrated Assessment Models (IAMs)

and serve as boundary conditions for global climate models. They describe possible future

pathways, covering a wide range of assumptions regarding, e.g., GHG emission trajectories,

socio-economic trends, and technological developments. The AR6 Scenarios Database contains

a large number of model simulations with different scenarios which in turn could be classified into

categories based on the projected change in temperature by the end of this century and the

respective probability

4

. The IPCC undertook a vetting process for all model simulations and

scenarios reporting global data to ensure that key indicators such as GHG emissions and energy

are within reasonable ranges

5

(Intergovernmental Panel on Climate Change (IPCC) (Ed.), 2023).

In total, approximately 1,200 different model simulations and scenarios related to GHG emissions

passed this vetting process (Byers et al., 2022). To allow for higher reliability when generating the

linear regression models within this methodology, only model simulations with scenarios that

passed the IPCC’s vetting process are considered. For simplicity, we refer to the model

simulations (based on different scenarios) as “scenarios”.

3

Copyright 2022 IIASA, Publication date: 09/11/2022. Downloaded from this link:

https://data.ece.iiasa.ac.at/ar6/#/data-download.

4

Scenarios are classified into the following categories (C): C1: limit warming to 1.5°C (>50%) with no or

limited overshoot, C2: return warming to 1.5°C (>50%) after a high overshoot, C3: limit warming to 2°C

(>67%), C4: limit warming to 2°C (>50%), C5: limit warming to 2.5°C (>50%), C6: limit warming to 3°C

(>50%), C7: limit warming to 4°C (>50%), and C8: exceed warming of 4°C (>=50%).

5

For more information regarding the IPCC’s vetting process, please read Annex III: Scenarios and

Modelling Methods.

13

© CDP Worldwide and WWF International 2024

4.2. Linear regression models

The underlying data described in Section 4.2.1 is processed and modelled into linear regression

models in two R scripts: CDP–WWF_ITR_preparation_of_data.R and CDP–

WWF_ITR_Regression.R processes AR6 data from two different data file publications

6

, while the

linear regression models are created in CDP–WWF_ITR_Regression.R. The R scripts are open

source and are available upon publication of this methodology https://github.com/WWF-

Sweden/ITR-regression.

One linear regression model is created for each of the following variables and time horizon

7

.

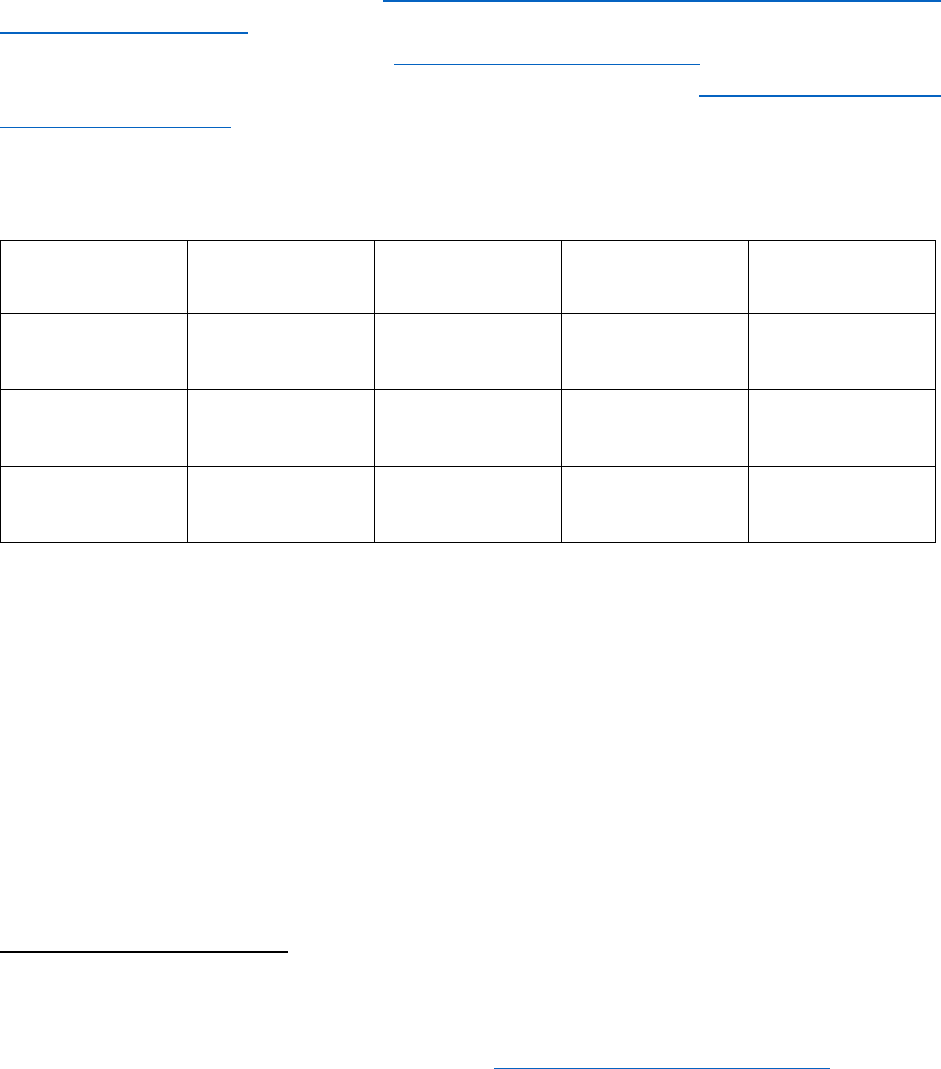

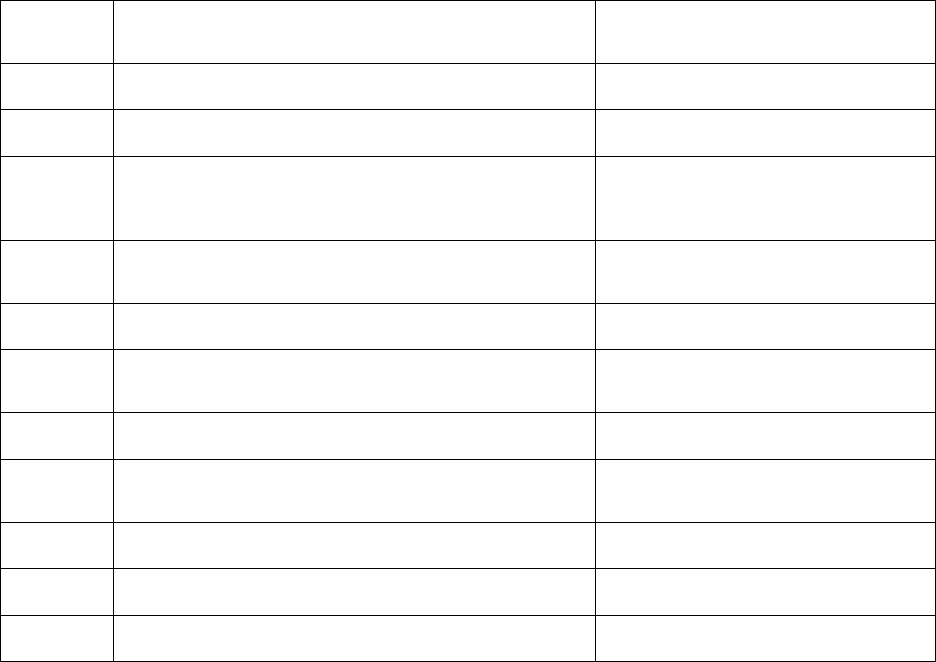

Table 1: Linear regression models associated with different time horizons and variables

Emissions | Kyoto

Gases

Emissions | CO

2

|

Energy | Supply

Emissions | CO

2

|

Energy and Industrial

Processes

Emissions | Kyoto

Gases /

GDP | PPP

Emissions| CO

2

|

Energy | Supply /

Secondary energy

Regression on 5-year

horizon

Regression on 5-year

horizon

Regression on 5-year

horizon

Regression on 5-year

horizon

Regression on 5-year

horizon

Regression on 10-year

horizon

Regression on 10-year

horizon

Regression on 10-year

horizon

Regression on 10-year

horizon

Regression on 10-year

horizon

Regression on 30y

horizon

Regression on 30-year

horizon

Regression on 30-year

horizon

Regression on 30-year

horizon

Regression on 30-year

horizon

This gives a total of 15 linear regression models that we refer to as benchmarks. The regression

coefficients are outlined in Table 3 in Section 4.2.3.

Equation 1: Linear regression formula

where:

= error term of the regression model.

= dependent variable, derived from MAGICC v7.5.3 (Model for Assessment

of Greenhouse Gas Induced Climate Change)

8

(Byers et al., 2022), and collected from the AR6 Scenario Database.

6

Two published data files are used: AR6_Scenarios_Database_World_v1.1 containing time series of different variables, and

AR6_Scenarios_Database_metadata_indicators_v1.1 containing metadata related to the climate models and scenarios. Copyright

2022 IIASA, Publication date: 09/11/2022. Downloaded from this link: https://data.ece.iiasa.ac.at/ar6/#/data-download.

7

Unique variables: Emissions|Kyoto Gases, Emissions|CO2|Energy|Supply, Emissions|CO2|Energy and

Industrial Processes, Emissions|CO2|Energy|Supply / Secondary energy and Emissions|Kyoto Gases /

GDP|PPP.

Three different time horizons: 5y, 10y and 30y.

8

Based on the variable AR6 climate diagnostics | Surface Temperature (GSAT) | MAGICCv7.5.3|50.0th

Percentile.

14

© CDP Worldwide and WWF International 2024

This variable is suitable for this methodology’s aim – to translate GHG emission reduction targets into a single common

and intuitive metric – as it returns a single unambiguous value expressed in projected temperature change in 2100.

= independent variable, is the annualized

reduction rate implied by the variable’s absolute change between two points in time, starting in 2020. This is expressed

as the compound annual reduction rate (CAR) for different time horizons – from five to 30 years (in five-year intervals).

Equation 2: Compound Annual Reduction Rate

where:

= compound annual reduction

= in the context of scenarios the year of reference is 2020. In the context of corporate targets, the year the

target was set.

= in the context of scenarios, the 5-year interval period after 2020 analyzed. In the context of corporate targets,

the year the target should be met.

= the percentage change of emissions between the base year and

end year (e.g., if the scenario’s GHG emission pathway shows a reduction in emissions by 50% between the two

periods, then the value should be −0.5). Note that when targeted reduction is 100%, the equation for CAR does not give

a meaningful value. Therefore, in the context of corporate targets, the method assigns the temperature floor (see Section

5.4) as the TS (see more under limitations in Section 8.1.2)

In this methodology, the time frames used for benchmarking targets are 5 years (short term), 10

years (medium term) and 30 years (long term). Year 2020 represents the base year. For example,

to run a regression model of projected temperature change in 2100 and GHG emissions’ evolution

in the next 30 years, the GHG emissions CAR from all scenarios’ emissions pathways between

2020 and 2050 are first calculated.

For an absolute reduction in emissions between two intervals, CAR will be negative as per the

formula above. To run the regression models the sign of CAR is flipped (a reduction in emissions

will be counted as a positive CAR) so that slopes in the regressions are negative and a reduction

in emissions can be more intuitively interpreted as an improvement in temperature outcomes when

calculating targets’ temperature scores. This transformation has no impact on the outcome of the

methodology and similar temperature scores would be observed without it, but it should be noted

if applying the regression coefficients provided in this paper.

15

© CDP Worldwide and WWF International 2024

Box 1: from Linear Annual Reduction (LAR) to Compound Annual Reduction (CAR).

The change in the annual reduction rate formula from linear annual reduction (LAR), used in the

initial publication of the methodology (version1.0), to compound annual reduction (CAR) has an

expected effect on the fit of the linear model as calculated by R

2

. LAR expresses changes in the

independent variable over the period in terms of percentage points (i.e., GHG emissions reduced

by two percentage points each year indicates that they are reduced from 100% to 98% to 96%

from a given baseline value), as opposed to annualized percentages with CAR (reduction of 2%

from the 2020 baseline value, and reduction of 2% from the 2021 value the following year, and so

on). LAR is normalized by nature with a significantly smaller variance, which mechanically

increases R

2

of the regressions, especially for long-time horizons. CAR represents a cumulative

reduction rate that is more accurately modelled by an exponential function as highlighted in Figure

2 (see Section 4.2.3). Investigating the possibility of using another statistical model will be subject

for a next update of this methodology.

The main reason for changing from LAR to CAR is to improve the interpretation of the model

results with respect to real economy changes in GHG emissions that are usually expressed in

annualized percentage changes as opposed to reduction in percentage points from a base year.

This change also incentivizes earlier action, as the CAR implies a higher absolute reduction in

GHG emissions in the short term given the higher baseline.

4.2.1. Sector-specific variables and benchmarks

Table 2 outlines which regression models that are used to benchmark sector specific targets in

this methodology. Some benchmarks are common across sectors and scopes.

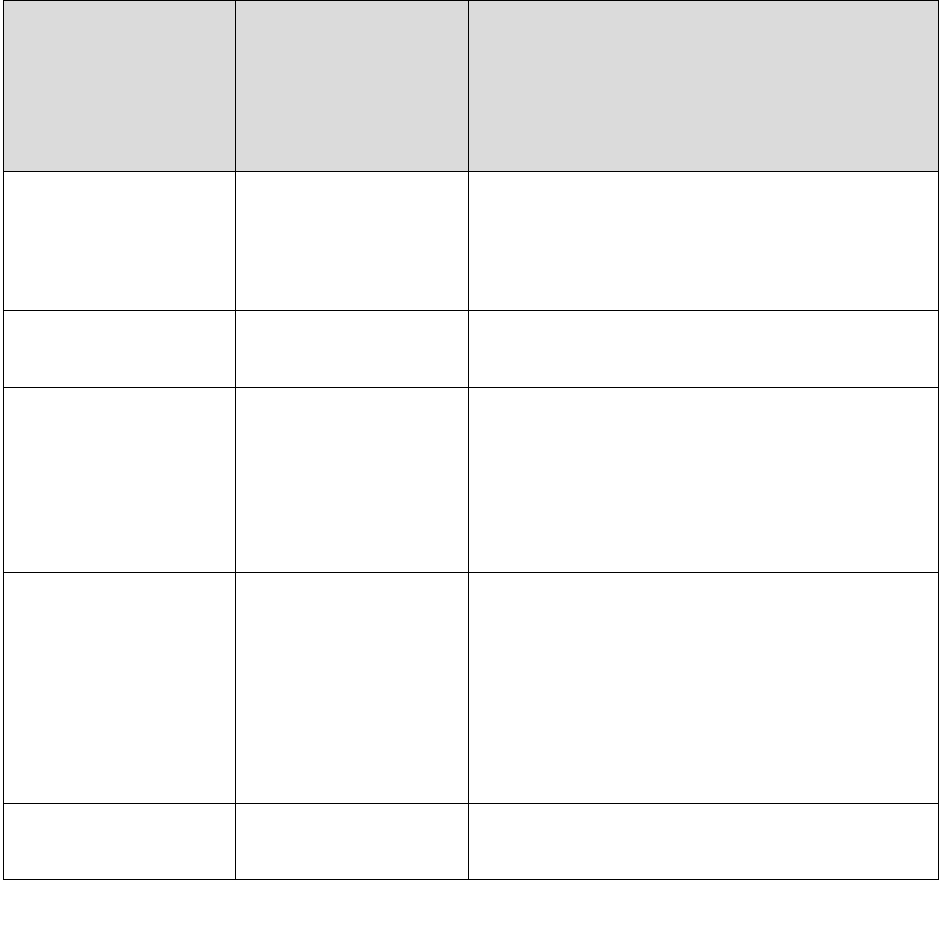

Table 2: Sector variables and associated linear regression models for each target type and scope category.

9

Sector

10

Target

type

Scope 1 benchmarks:

AR6 regression

model variable

Scope 2 benchmarks:

AR6 regression

model variable

Scope 3 benchmarks:

AR6 regression

model variable

All sectors

(except for the

ones listed below)

Absolute

Emissions | Kyoto

Gases

Emissions | CO

2

|

Energy | Supply

Emissions | Kyoto

Gases

Intensity

Emissions | Kyoto

Gases /

GDP | PPP

Emissions | CO

2

|

Energy | Supply /

Secondary energy

Emissions | Kyoto

Gases /

GDP | PPP

9

Some of the variables in the table are expressed in CO2 rather than CO2e or Kyoto Gases. However, this

is the nature of the specific AR6 variable, and CO2 is considered the best proxy for CO2e/Kyoto Gases in

this methodology.

10

In this paper, sectors are defined following the CDP-Activity classification system.

16

© CDP Worldwide and WWF International 2024

Power

Generation

Absolute

Emissions | CO

2

|

Energy | Supply

The regression model

for all sectors applies

The regression model

for all sectors applies

Intensity

Emissions| CO

2

|

Energy | Supply /

Secondary energy

The regression model

for all sectors applies

The regression model

for all sectors applies

Cement/

Steel/

Aluminium

Absolute

Emissions | CO

2

|

Energy and Industrial

Processes

The regression model

for all sectors applies

The regression model

for all sectors applies

Intensity

The regression model

for all sectors applies

The regression model

for all sectors applies

The regression model

for all sectors applies

These are used to assess corporate GHG targets according to their type (using absolute or

intensity metrics), sectors (All sectors, Power Generation, and Cement/Steel/Aluminium), and

emission scope category (scope 1, 2, and 3). The sector variables used to benchmark absolute

targets are directly available from the AR6 Scenario Database. The intensity variables are

calculated from AR6 scenarios data for the purpose of this methodology (this calculation is

included as part of the CDP_WWF_ITR_Regression.R script mentioned in Section 4.2).

The benchmarks are selected and allocated to a sector based on a combination of criteria: data

availability, suitability of the AR6 variable to proxy the specific sector emissions, and the fit of the

linear regression model when using this benchmark.

The following updates are introduced in this methodology compared to the initial version (1.0):

- A specific benchmark for scope 2 targets based on the following variables to proxy indirect

emissions from energy consumption: Emissions | CO

2

| Energy | Supply, and Secondary

energy output for the intensity targets

11

. This change relies on the assumption that energy

consumption’s absolute emissions and intensity should follow a similar path as the supply

of energy. This benchmark is now also used to assess Power Generation scope 1 targets.

Previously, one common benchmark is used to assess both scope 1 and scope 2 targets

for all sectors, and the Power Generation scope 1 emissions are assessed according to a

different benchmark

12

.

- The sector-specific benchmark for Primary Energy is removed in this methodology since

the variable used in the initial version (version 1.0) is considered too generic and

11

These two variables are related to GHG emissions from fuel combustion and fugitive emissions from

fuels: electricity and heat production and distribution, other energy conversion (e.g. refineries, synthetic fuel

production, solid fuel processing) including pipeline transportation fugitive emissions from fuels and

emissions from transport and storage (Byers et al., 2022).

12

The variable Emissions | CO

2

| Energy and Industrial Processes is used for absolute targets and

Emissions | CO

2

| Energy | Supply | Electricity / Secondary Energy | Electricity for intensity targets

17

© CDP Worldwide and WWF International 2024

alternative suitable variables yielded low linear fits in regression models. Therefor the “all

sectors” benchmarks are now used to assess companies’ targets in the fossil fuel sector.

See Annex0 for a more detailed description of the variables. Future updates of this methodology

aim to conduct further research to inform the possible inclusion of additional sector specific

regression models.

4.2.2. Analysis for scenario selection

In this version of the methodology, all scenarios that passed the vetting process from the IPCC

are selected to feed into the linear regression models. After conducting analysis on the potential

impact of excluding certain scenarios based on additional considerations detailed below, the

overall conclusion is not to perform any exclusionary filters.

In the initial publication of this methodology (version 1.0), the IPCC’s SR15

13

scenarios were first

filtered before the linear regression models were generated. This was done by creating different

scenario sets that matched normative and precautionary preferences concerning overshoot and

the level of plausible carbon dioxide removal (CDR above 10 Gt CO

2

/year considered as not

plausible)

14

,

15

. Baseline scenarios, i.e., scenarios where no deliberate mitigation action was taken,

were also removed from the initial SR15 dataset. Besides these normative, precautionary

preferences, the best model fit over medium- and long-term horizons

16

was the basis for selecting

and applying scenario set 4 in the version 1.0 methodology. This scenario set applied a CDR limit

to maximum 10 Gt CO

2

/year as well as excluding baseline scenarios.

When applying a similar CDR-related precautionary consideration to the AR6 dataset, the results

are contradictory to the ones using data from the SR15. While intuitively, excluding scenarios

based on high CDR (defined as >10 Gt CO

2

/year) is expected to increase the GHG emission

reduction ambition

17

reflected in the regression models, the opposite outcome was found. After

investigation, the potential reasons identified are the following: firstly, and most significantly, the

underlying dataset of AR6 is fundamentally different compared to the one of SR15 (e.g., different

report purpose, other and updated climate models and scenarios are used, etc.), hence why

similar normative precautionary preferences and filter options will not necessarily lead to

13

Global Warming of 1.5°C, IPCC Special Report on the impacts of global warming of 1.5°C above pre-

industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the

global response to the threat of climate change, sustainable development, and efforts to eradicate poverty.

Accessible through this link: Download Report — Global Warming of 1.5 ºC (ipcc.ch).

14

56 unique scenario sets were generated in the initial methodology (version 1.0).

15

For more information about the scenario filtering process of the initial methodology (version 1.0), please

review https://www.cdp.net/en/investor/temperature-ratings/CDP–WWF-temperature-ratings-methodology

16

Represented by R^2.

17

The ambition is defined as the GHG emission annual reduction rate required to reach 1.5°C warming in

2100 based on the regression coefficients. The lower estimate rate, then the lower the ambition.

18

© CDP Worldwide and WWF International 2024

regression outcomes as in the initial methodology. Secondly, in AR6, the levels of yearly CDR

tend to be high and increase by the end of the century compared to the first half. This is also the

case for scenarios with an ambitious GHG emissions reduction rate that project to limit warming

to 1.5°C by the end of the century. As a result, excluding scenarios based on such CDR criteria

(i.e., CDR>10 Gt CO

2

/year) also means excluding ambitious 1.5°C-scenarios, leading to an overall

decrease of the GHG emission reduction ambition reflected in the linear regression models (rather

than in an increase). Following these findings, no CDR filter is applied to the AR6 dataset.

Further analysis shows that excluding baseline scenarios from the AR6 dataset has no significant

impact on the annual GHG emission reduction ambition reflected in the regression models. This

insight, in combination with the possibility that these baseline scenarios are potential future

trajectories of the world’s development, leads to the conclusion to keep baseline scenarios in the

dataset used to derive the benchmarks.

Additional analysis to inform the filter choices was conducted. The effect on the projected

temperature change at the end of the century (dependent variable in the linear regression models)

and the annual GHG emissions reduction rate (independent variable in the linear regression

models) was tested for two additional filters: 1) the exclusion of scenarios with a GHG emission

peak year before year 2024, and 2) outlier analysis using statistical analysis of Cook’s D, leverage,

and residuals.

The results from filter test 1) shows that the GHG emission reduction ambition significantly

decreases from a short time frame perspective. However, the effect is less noticeable in the longer

term. One possible explanation for this outcome could be that very few scenarios with a projected

1.5°C temperature outcome by the end of the century

18

assume a peak year of GHG emissions

after 2020. Thus, removing scenarios based on such condition will decrease the overall GHG

emissions reduction ambition, leading to steeper regression lines. In addition, as demonstrated in

the linear regression models (see Figure 2 in Section 4.2.3) the variability of the scenarios’ GHG

emission reduction is, in general, larger in the shorter time frames compared to the longer time

frames, which could explain why the effect is less noticeable in the longer term. This result leads

to the conclusion not to remove any scenarios from the dataset based on the results from filter

test 1.

The outlier analysis (filter test 2) highlights that the number of scenarios considered as outliers

according to the three approaches (Cook’s D, leverage, and residuals) is limited. The result also

shows that no scenario alone is deemed to influence the linear regression model to a significant

extent, and hence, no scenario is removed from the data set based on the results from filter test

2.

18

Scenarios classified as Category 1: limit warming to 1.5°C (>50%) with no or limited overshoot, and

Category 2: return warming to 1.5°C (>50%) after a high overshoot.

19

© CDP Worldwide and WWF International 2024

The overall conclusion from the scenario selection analysis is that the vetting process from IPCC

is considered sufficient criteria for selecting scenarios for the linear regression models in this

methodology. As a result, the linear regression models computed and used in this methodology

include all scenarios that passed the IPCC’s vetting process.

4.2.3. Regression results

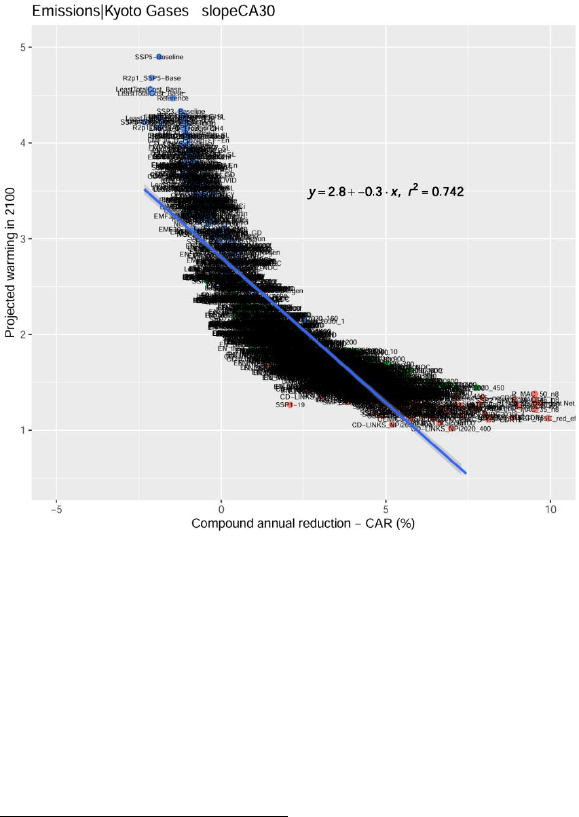

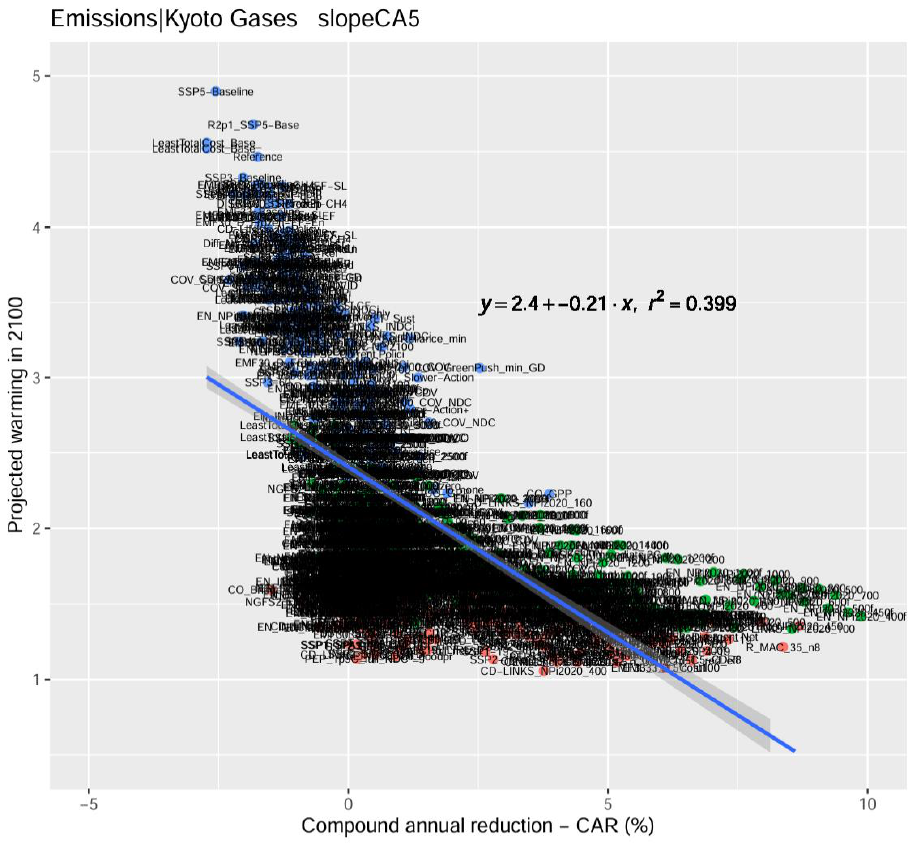

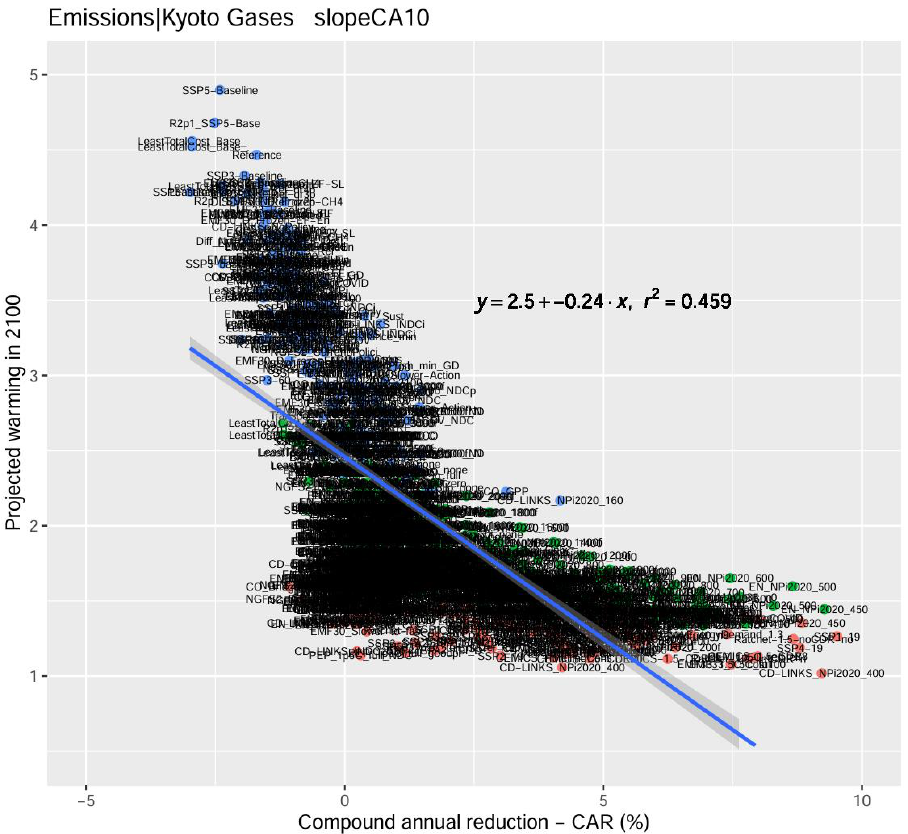

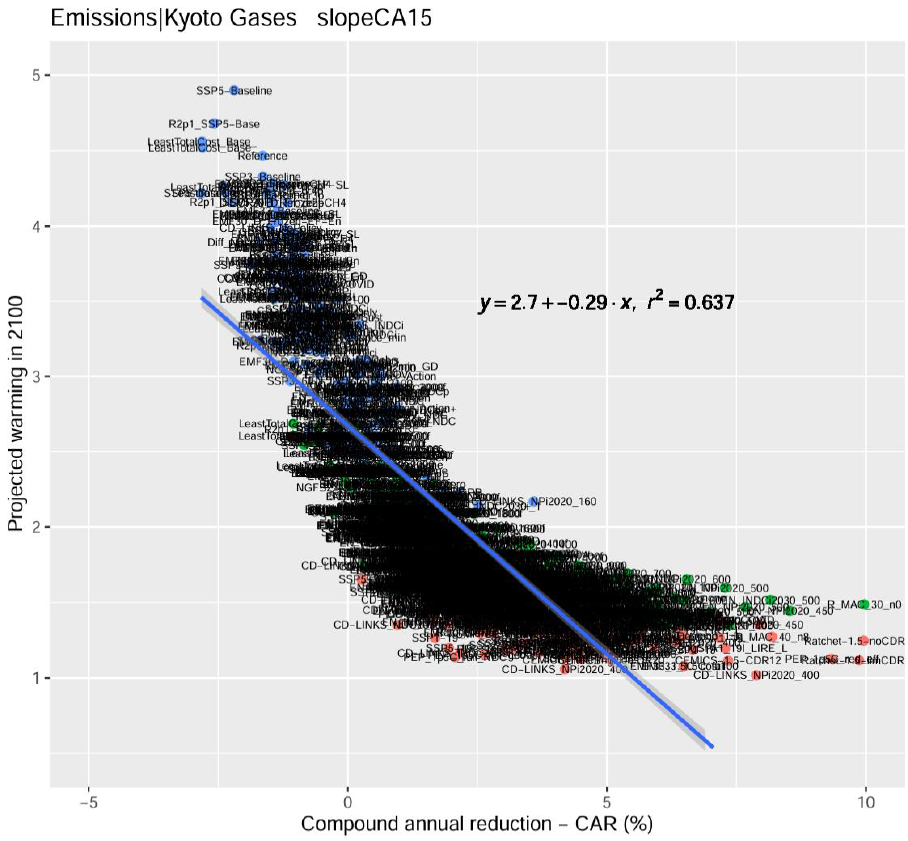

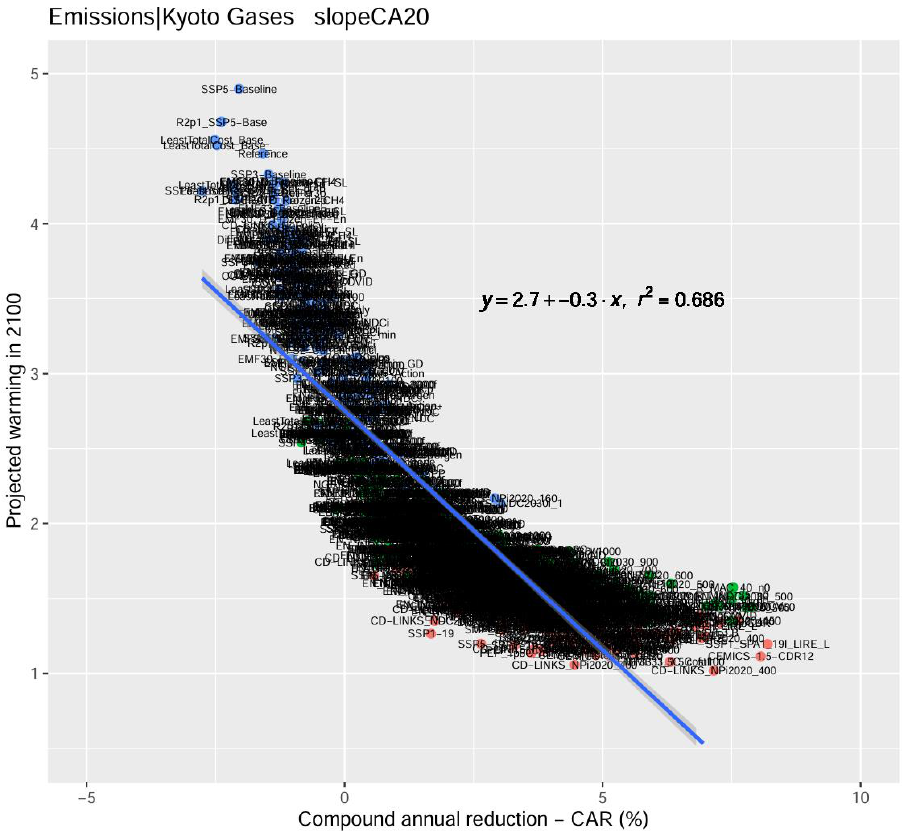

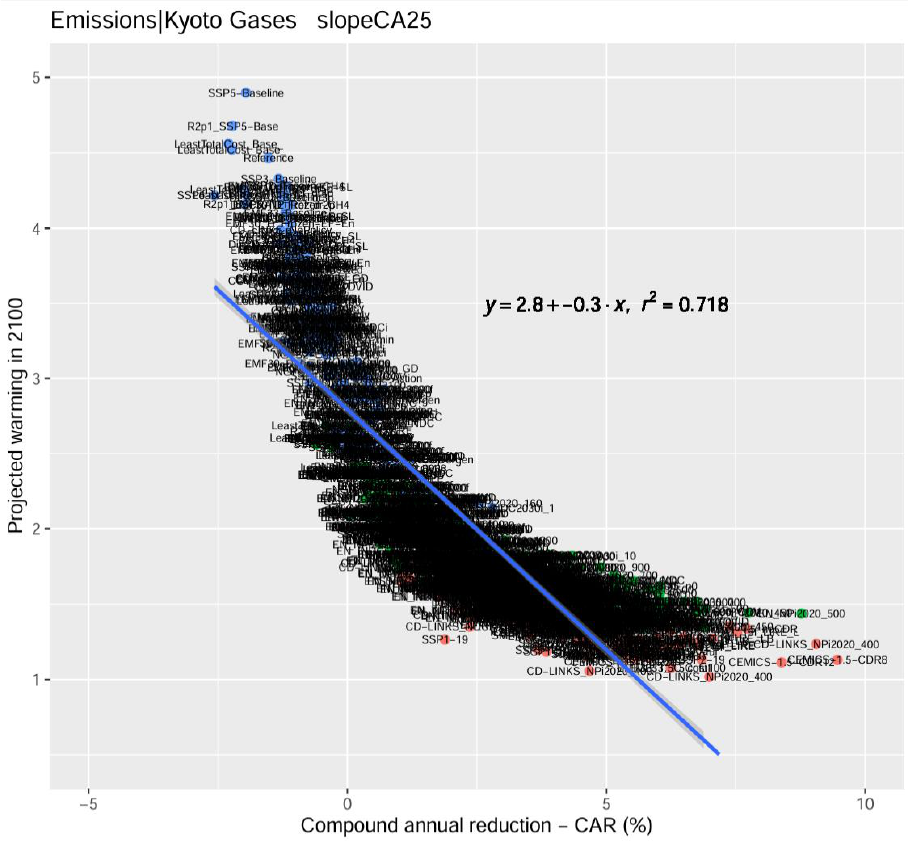

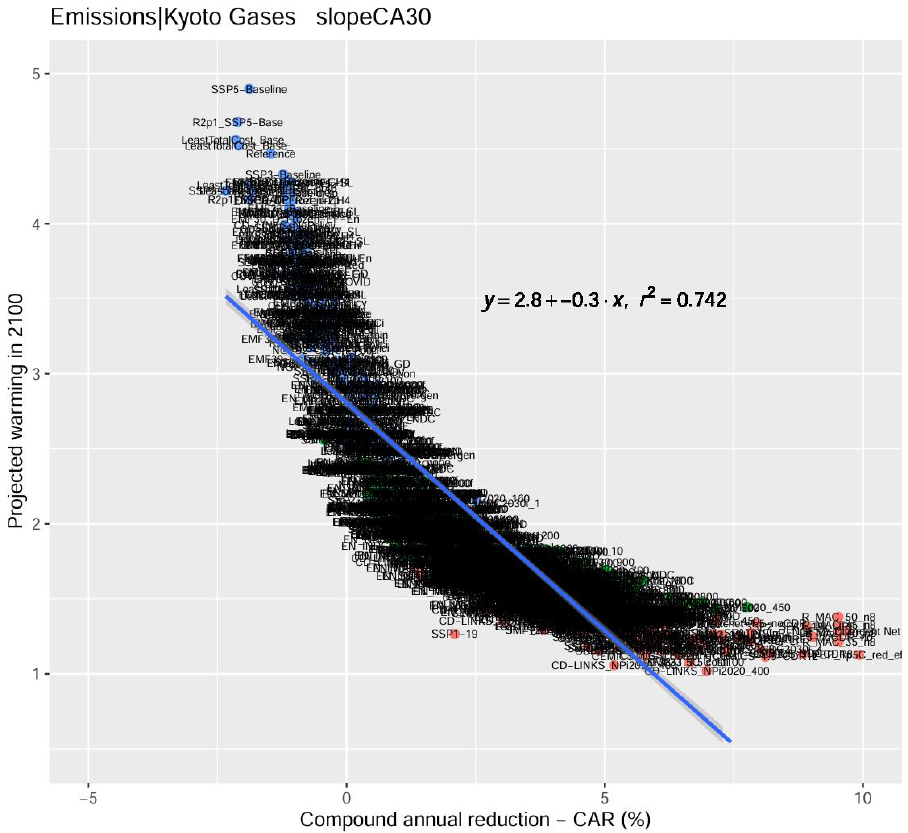

Figure 2 provides an illustration of the linear regression model applied to the variable Emissions |

Kyoto Gases on the 30-year horizon

19

. The remaining linear regression results for different time

horizons are found in Annex 3: Result of linear regression model.

Figure 2: Example of the result of the linear regression model for Emissions | Kyoto Gases for a 30-year time horizon

Table 2 summarizes the details of the linear regression models for 5-, 10- and 30-year horizons

representing short-, medium- and long-term targets, for each variable used in this methodology.

The fit of the regression line, represented by R

2

,

and the intercept increase as the time horizon

increases (intercept of 2.4, R

2

of 0.40 for 5 years; intercept of 2.8, R

2

of 0.74 for 30 years). This is

logical since the degree of variability between scenarios decreases over longer horizon and the

range of possible annualized reduction rates leading to a given temperature outcome is lower for

19

Time horizons used in this methodology: 5-year (short term), 10-year (medium term), and 30-year (long

term). Base year is 2020.

20

© CDP Worldwide and WWF International 2024

longer time horizons. In addition, no action (zero year-on-year reduction) will lead to higher

temperature outcomes if observed over longer time horizons.

Compared to the initial methodology (version 1.0) where the scenarios were grouped into different

scenario sets based on the filtering process (see Section 4.2.2), this methodology only contains

one scenario set including all the vetted scenarios from the IPCC AR6 database (see Section

4.2.24.2.2).

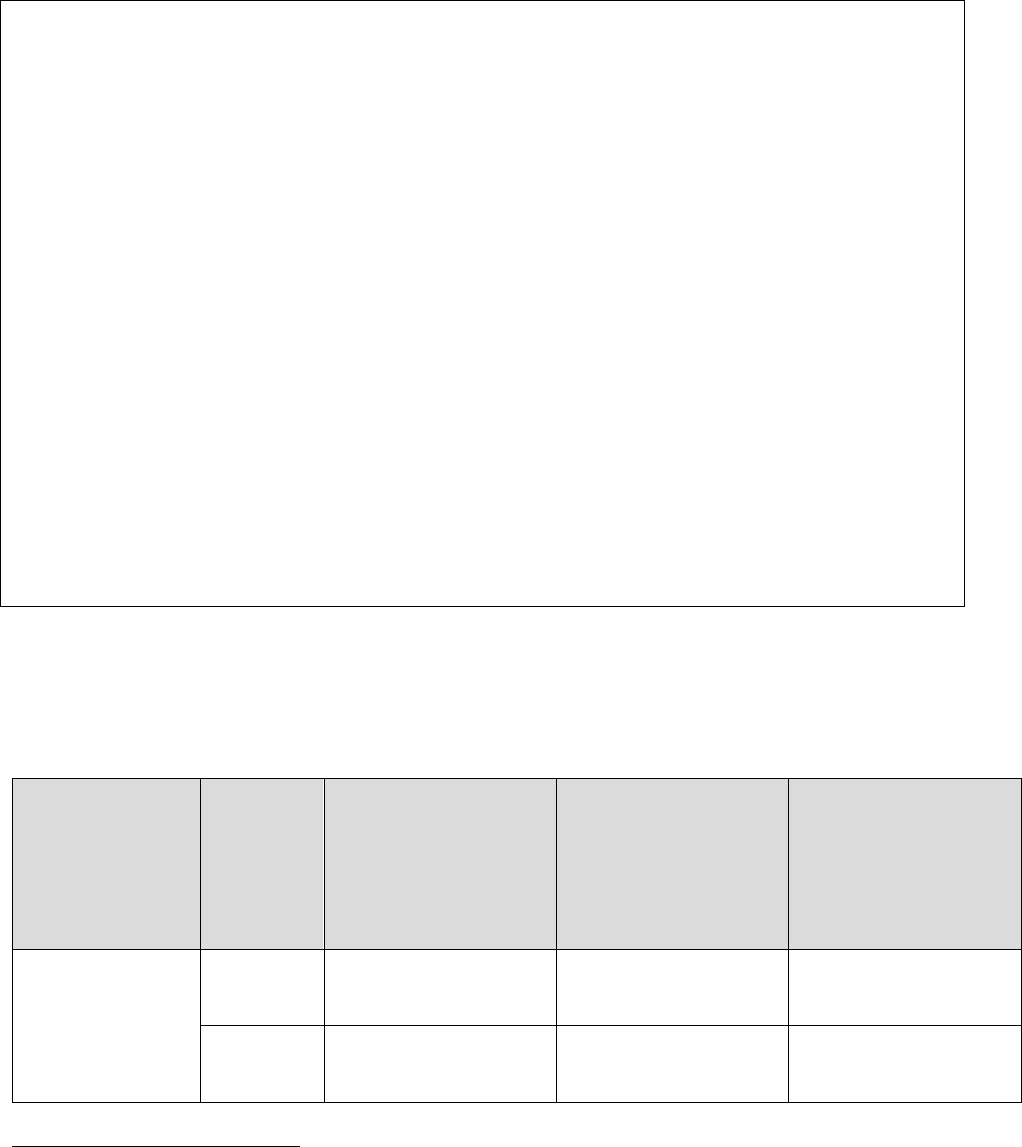

Table 3: Summary of linear regression results (note that rounding differences may occur).

Regression

model

variable

5-year horizon

10-year horizon

30-year horizon

Sample

size

Intercept

Slope

R

2

Sample

size

Intercept

Slope

R

2

Sample

size

Intercept

Slope

R

2

Emissions |

Kyoto Gases

1,115

2.40

−0.21

0.40

1,115

2.46

−0.24

0.46

1,112

2.81

−0.30

0.74

Emissions | CO

2

| Energy |

Supply

1,160

2.35

−0.12

0.32

1,156

2.40

−0.11

0.36

851

2.85

−0.15

0.63

Emissions | CO

2

| Energy and

Industrial

Processes

1,171

2.27

−0.22

0.37

1,170

2.33

−0.24

0.43

1,155

2.58

−0.19

0.56

Emissions |

Kyoto Gases /

GDP | PPP

986

3.13

−0.21

0.38

986

3.21

−0.23

0.44

983

3.57

−0.30

0.70

Emissions| CO

2

|

Energy | Supply

/ Secondary

energy

764

2.19

−0.08

0.15

764

2.22

−0.07

0.17

575

2.61

−0.11

0.41

To calculate the temperature score of a company’s climate target, the target is first mapped to the

most representative benchmark available in the methodology (see Table 2). Depending on the

target’s time-horizon, the appropriate regression parameters (see Table 3) can be applied

according to the following formula:

Equation 3: Temperature Score

where:

= intercept of the regression model for a given time horizon and variable

21

© CDP Worldwide and WWF International 2024

= slope of the regression model for a given time horizon and variable

= compound annual reduction of the variable over time horizon implied by the target set by the company.

Using the formula expressed above, if CAR is 0 (i.e., the company’s absolute reduction of

emissions over the next 10 years is zero) then the projected temperature outcome of the target

will amount to the intercept of the linear regression.

The next section provides further details on the validation and assessment of targets (Step 2).

22

© CDP Worldwide and WWF International 2024

5. Step 2a: Target validation

5.1. Assigning a temperature score to disclosed targets

The methodology assumes that there is a linear relationship between the change in common

climate target metrics (e.g., absolute or intensity GHG emissions) for a specific timeframe and the

projected global warming in 2100. This assumption is applied for corporate targets, for target

horizons set out in the Section 4.2. Limitations to this assumption of linearity are covered in Section

8.1.1.

The first step in assigning temperature scores to disclosed corporate GHG targets is to assess

which types of targets could be adequately matched to a scenario variable, and consequently,

which associated linear regression model should be applied. Disclosed corporate GHG targets

refer to either absolute GHG reduction targets and/or GHG intensity reduction targets. Table 2 in

Section 4.2.1 shows the sector variables and the associated linear regression model applicable in

this methodology. Table 4 showcases examples of climate target wording applicable for the

respective variables.

Table 4: Target class, wording, and scenario variables

Target Class

Example of target wording

AR6 benchmark variable

Absolute GHG reduction

targets

Company X commits to reduce

absolute scope 1 GHG emissions

60% by 2030 from a 2022 base

year.

Company X commits to reduce

absolute scope 2 GHG emissions

60% by 2030 from a 2022 base

year.

Company X commits to reduce

absolute scope 3 emissions GHG

with 50% by 2030 from a 2022

base year.

• Emissions | Kyoto Gases

• Emissions | CO

2

| Energy | Supply

• Emissions | CO

2

| Energy and

Industrial Processes

GHG economic intensity

target

Company X commits to reduce

scope 1 GHG emissions 60% per

unit of added value by 2030 from

a 2022 base year.

Company X commits to reduce

scope 2 GHG emissions 60% per

unit of added value by 2030 from

a 2022 base year.

Company X commits to reduce

scope 3 GHG emissions 50% per

unit of added value by 2030 from

a 2022 base year.

• Emissions | Kyoto Gases / GDP |

PPP

• Emissions | CO

2

| Energy | Supply /

Secondary energy

23

© CDP Worldwide and WWF International 2024

The second step is to convert the corporate target into a corresponding annual reduction rate to match the format of the

independent variable of the regression models. These annualized reduction rates are calculated using the formula for

CAR (see Equation 2 in Section 4.2)4.2. As per

Equation 3, the CAR of a target is used in the linear equation specified by the model’s parameters

to convert the target’s ambition into a temperature score. For example, an absolute GHG reduction

target of 30% between the base year 2020 and the target year 2035, mapped to the scenario

variable Emissions | Kyoto Gases, would result in a compound annual reduction rate of 2.3%.

Applying the Emissions | Kyoto Gases linear equation for the long-term timeframe (corresponding

to the 2035 target year), this target’s ambition would translate to a 2.1°C temperature score

(calculated as 2.81 − 0.30 * 2.3).

5.2. Target validation

All targets are subjected to a validation procedure to assure their usefulness in generating

company-level temperature scores. The method also attempts to split targets covering multiple

scopes into single-scope targets. The target validation process checks that each target is

accompanied by the data required to calculate temperature scores in later steps.

The following criteria need to be met for a target to be valid:

1) The scope coverage of the target, any single scope or combination of scopes 1, 2, or 3.

2) Target type must be absolute or intensity with valid metric.

3) Target progress < 100% on the date the relevant target was first published.

4) Base year < target year.

5) Target year ≥ current year.

6) Base year GHG data must be available for the emission scope of the target, i.e., scope

1 GHG data for a scope 1 target, etc.

7) Boundary coverage of the target is required for the emission scope(s) of the target, for

instance, 60% of the scope 1 emissions. If this number is missing, the value will be set

to zero.

8) Target reduction ambition must not be negative.

Targets which do not meet the criteria are removed from further calculation.

Temperature scores are calculated on the most disaggregated level of targets that the provided

data allows. A scope 1+2+3 target is split into one scope 1+2 target and one scope 3 target, and

a scope 1+2 target (including those split from a scope 1+2+3 target) will be split into one scope 1

target and one scope 2 target. Targets for the three scopes will then be scored separately and a

combined score will later be calculated in the target aggregation procedure, see Section 6.5. It

should be noted, however, that temperature scores are aggregated using the company’s current

GHG emissions. Therefore, the presence of current GHG data must be verified before a scope

1+2 target is split. If the data is missing, the scope 1+2 target is kept and scored using the provided

target data.

When splitting a valid scope 1+2 target, the scope 1 target is assigned the scope 1 boundary

coverage from the original target and the scope 2 target is assigned the scope 2 boundary

24

© CDP Worldwide and WWF International 2024

coverage from the original target. Both targets are assigned the reduction ambition of the original

target.

The procedure for splitting targets thus means that a target covering scopes 1+2+3 ideally results

in three targets for the individual scopes, where each target consists of its respective boundary

coverage and the reduction ambition from the original target. However, even if current GHG data

is missing, a scope 1+2+3 target will be split into a scope 1+2 target and a scope 3 target for

separate scoring. For the scope 1+2 target the boundary coverage is calculated as follows:

Equation 4: Boundary coverage

where bc = boundary coverage

The reduction ambition is copied from the original scope 1+2+3 target. The resulting scope 3 target

keeps the scope 3 boundary coverage and the target reduction ambition from the original target.

Note that if reduction ambition is missing or has a value of zero, the TS will be calculated as the

intercept of the applicable regression function.

Finally, the boundary coverage is used to adjust each target’s reduction ambition according to the

procedure described in Section 6.3.2.

5.3. Default temperature score for companies without valid targets

5.3.1. Purpose of a default temperature score

The purpose of assigning a default temperature score is to provide a means for scoring a full

portfolio or value chain although some portfolio constituents lack publicly disclosed targets or fail

to meet specific criteria for target coverage or quality.

In instances where companies do not have valid targets, it is assumed that they are following a

business-as-usual trajectory, as they have not publicly articulated their GHG emissions reduction

strategies through GHG targets. Therefore, default scores represent the anticipated business-as-

usual GHG emissions trajectory. In essence, the default score reflects the pathway expected to

be followed if companies continue operating under existing governmental policies, and thus

adhering to the minimum requirements of current regulation.

5.3.2. Default score approaches

Business-as-usual trajectories can be defined at a company, sector, and/or economy-wide level.

This version 1.5 of the methodology still focuses on uniform default scores at an economy-wide

level but will aim to provide more sectoral granularity in version 2.0 (see Section 8.2). While

economy-wide default scores assume the company’s temperature score is aligned with that of the

global economy, sector-specific approaches define business as usual pathways at a sector level

and assume the company’s trajectory is consistent with that of the sector.

25

© CDP Worldwide and WWF International 2024

5.3.2.1. Economy-wide default scores

An economy-wide default score applies the score uniformly to all companies, regardless of sector

or current performance.

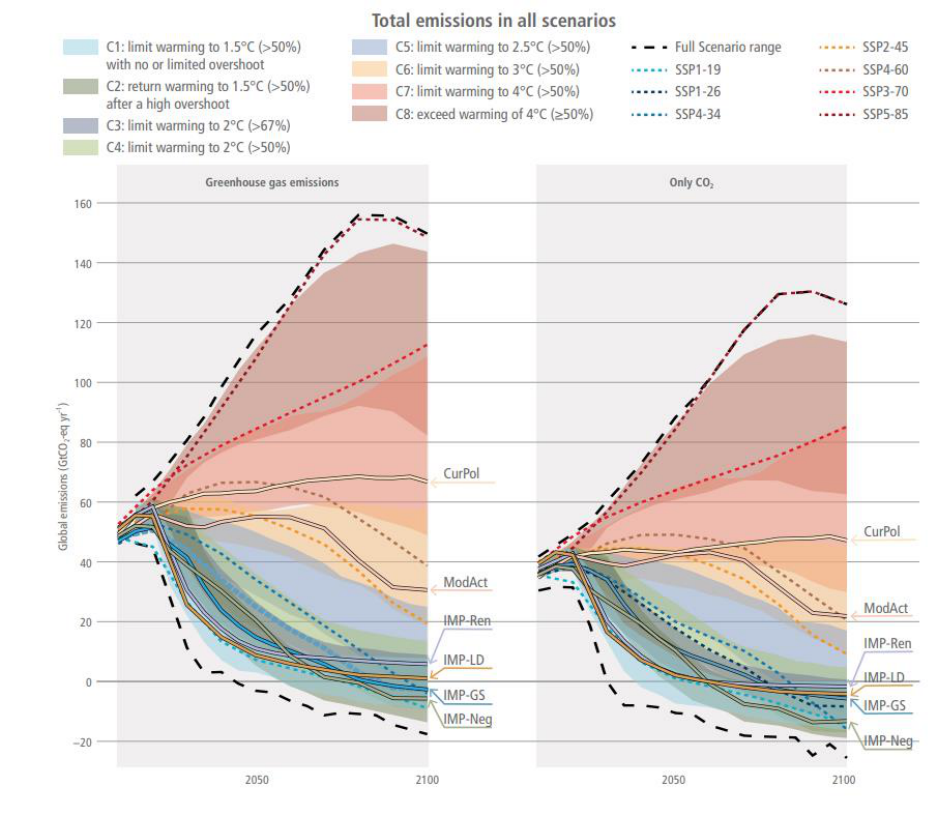

The first version of this methodology relied on the December 2019 end-of-century warming

projections from the Climate Action Tracker (“CAT”) to establish a 3.2°C economy-wide default

score. At the time, this value corresponded to the upper bound of the range of median

temperatures expected from the continuation of current policies being implemented by

governments (i.e., real-world action based on current policies).

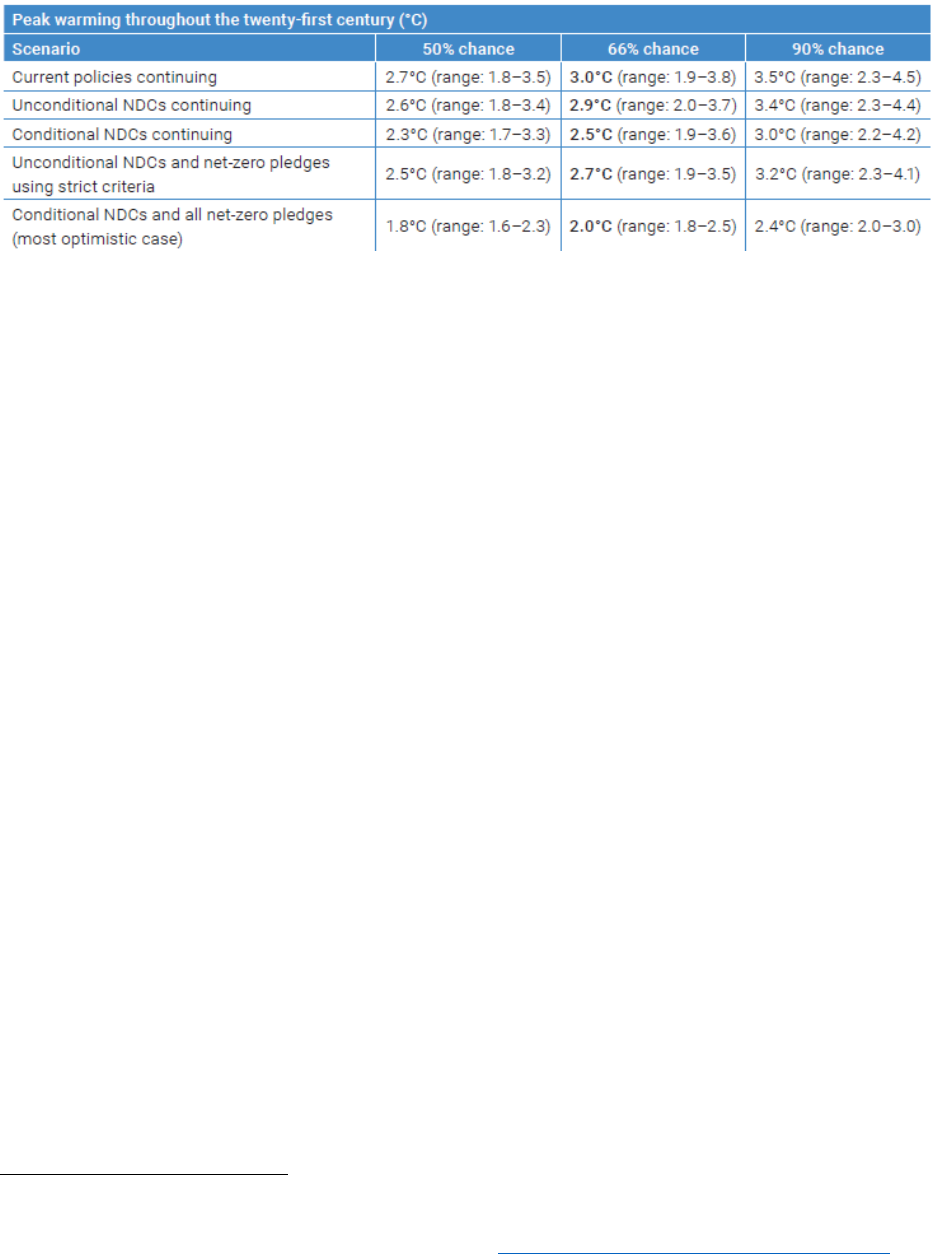

Using the same source (updated in December 2023, see Figure 3) and the same “policies & action”

projections, a range of warming between 2.2°C and 3.4°C is expected by the end of the century,

with a median projection of 2.7°C (50% probability).

26

© CDP Worldwide and WWF International 2024

Figure 3: Summary and breakdown of 2100 warming projections based on a range of future scenarios (Source: Climate

Action Tracker, December 2023)

This aligns with the conclusions of the 2023 UNEP Emissions Gap Report (United Nations

Environment Programme, 2023), which finds that a continuation of the level of mitigation effort

under current governmental policies would result in a warming of 2.7°C at the end of the century

(range: 1.8–3.5°C, with a 50% probability).

27

© CDP Worldwide and WWF International 2024

Table 5: End-of-century warming projections based on a range of future scenarios (UNEP Emissions Gap Report, 2023)

When presenting temperature estimates with a 66% probability, CAT’s median projections of

3.0°C also align with the UNEP Emissions Gap Report’s warming estimates.

This updated version of the methodology uses a 3.4°C value (i.e., the upper bound of the range

of temperature outcomes from CAT’s “policies & action” projections) to derive temperature scores

for companies with no valid forward-looking targets. This implies that these companies are

expected to decarbonize along a 3.4°C pathway, consistent with global policies implemented to

ensure the reduction of GHG emissions at this rate.

While it could be argued that the ambition of current policies has improved somewhat over recent

years (as reflected in the UNEP Emissions Gap Report 2023’s projections, for instance), their

impact at the company level remains uncertain. Bearing in mind the purpose and objectives of the

default temperature score outlined in Section 5.3.1, the shift from 3.2°C to 3.4°C in this version

aims primarily at reinforcing the continued need for a conservative approach when considering

companies without valid targets.

Chapter 8 outlines the plan for future methodological development, where we aim to provide more

granular and sector specific default scores for companies with no valid GHG emission reduction

targets.

5.4. Temperature floor

The best score applicable to a company’s climate ambition under this methodology is 1.5°C (i.e.,

in the case where a calculated score results in a temperature that is lower than 1.5°C, the applied

score shall be 1.5°C).

The reasoning behind flooring all temperature scores to 1.5°C is grounded in the prevailing

scientific consensus

20

which, at the time of drafting this version of the methodology, remains that

1.5°C represents the lower bound of feasible outcomes within the most optimistic climate

scenarios. In addition, this aligns with the conclusions of the Climate Action Tracker’s latest

20

Intergovernmental Panel on Climate Change (2021) – AR6 Synthesis Report: Climate Change 2023

29

© CDP Worldwide and WWF International 2024

6. Step 2b: Company scoring

Companies set targets across different timeframes, emissions scopes, and units. Target data is

also often collected from several sources and a target database may include multiple targets for

the same company, scope, and timeframe. This section describes how the method selects and

prioritizes which relevant valid targets to be scored.

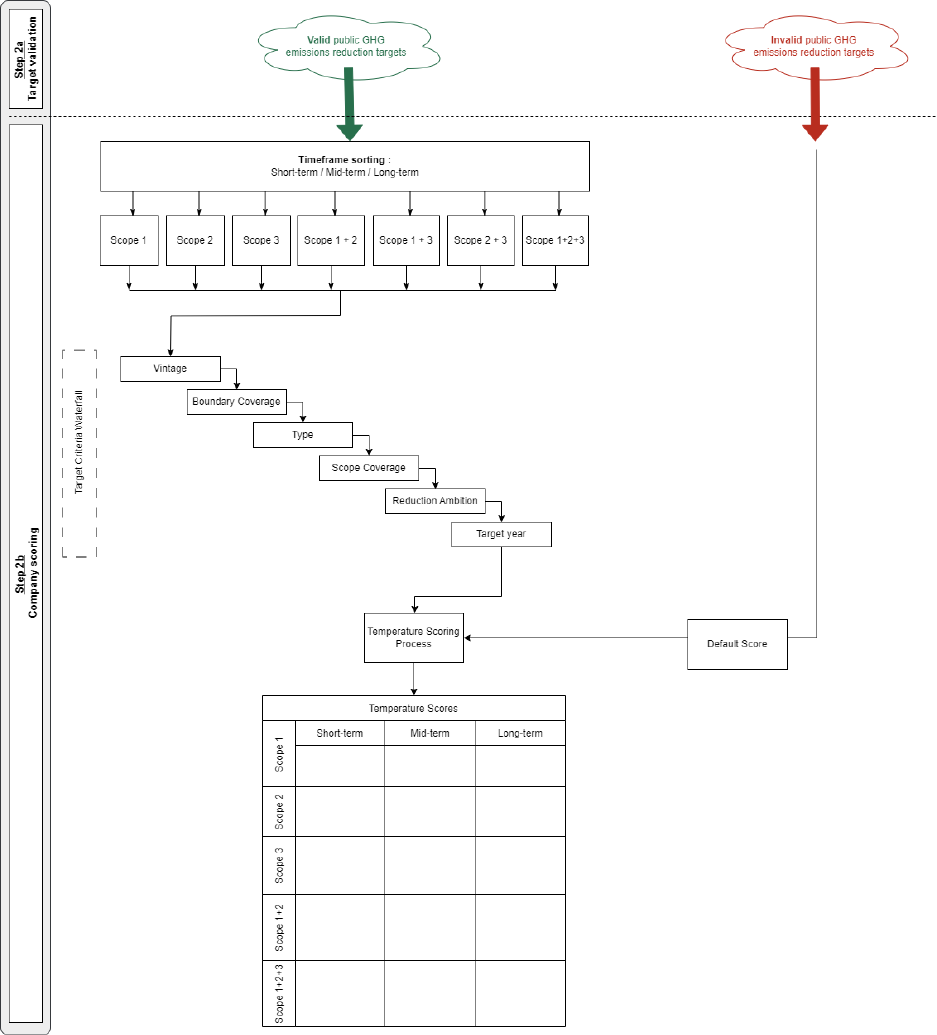

6.1. Target timeframe

The timeframe sorting first defines the range of target timeframes as applied in this methodology.

Targets are scored depending on which year the target ends in relation to the current year. The

target timeframes are divided into the following three buckets:

- Short-term: targets ending in up to 5 years from the current year, e.g., −2029 (current

year 2024)

- Mid-term: target ending 5–10 years from the current year, e.g., 2030–2034 (current year

2024)

- Long-term: target ending in more than 10 years from the current year, e.g., 2035–2050

(current year 2024)

Targets can then be scored across these three different timeframes, providing insights on the

short-, medium-, and long-term ambition of companies’ GHG emissions reduction targets.

Target timeframe also defines how long a target is used for scoring in a target timeframe bucket,

i.e., when a mid-term target becomes a short-term target and for how long a target is considered

as valid for scoring by this methodology. For instance, targets with end dates during the calendar

year (CY) 2024 would be valid throughout 2024 and would become invalid on January 1, 2025. A

mid-term target with an end date during CY 2030 would become a short-term target on January

1, 2026, as mid-term targets are defined as targets with 5–10 years left to run. There are

exceptions to this rule set out in Section 6.3.6.1 below.

Figure 4 displays a summary of the company protocol steps, including the waterfall, leading to the

output of a matrix of temperature scores for each timeframe and scope combination.

30

© CDP Worldwide and WWF International 2024

Figure 4: Step 2b – generating temperature scores at a company level, based on valid publicly disclosed targets or a

default approach for companies with no valid targets.

6.2. Target quality criteria

Targets are classified in terms of seven key criteria, presented in Table 6. Key requirements for

valid targets across these seven key criteria are further detailed in the different paragraphs of this

31

© CDP Worldwide and WWF International 2024

section. A description of how these criteria are prioritized in the selection process is provided in

Section 6.3.

Table 6: Target quality criteria

Criteria

Description

Target vintage

Defines the age of the target, based on the date the target was last

publicly communicated.

Boundary coverage

Within a given GHG emissions scope, companies define how much of

that scope will be included in the boundary of the target, e.g., 50% of

scope 1 or 95% of combined scope 1+2 is covered by the target.

Target Type

Defines whether the target ambition is based on an absolute or

intensity GHG emissions reduction.

Target scope

coverage

Defines the GHG emissions scope(s) covered by the target. Targets

can be set across individual or combined GHG emission scopes, as

defined in the GHG Protocol (World Business Council for Sustainable

Development & World Resources Institute, 2015), e.g., scope 1,

scope 2, scope 3, scope 1+2, scope 1+2+3, etc.

Reduction ambition

Defines the GHG emissions reduction ambition over the target

duration, e.g., absolute emission reduction of 30% by 2030.

Target timeframe

Classifies targets according to the duration between the current year

and the target end date. Targets can cover different timeframes.

Target progress

Describes the rate of achievement at the time the target was first

published. To be scored, target achievement has to be less than

100% at the time the target is published.

6.3. Target criteria waterfall

As mentioned in the introduction to this and displayed in Figure 4, a company’s targets are sorted

by scope coverage and according to three timeframes.

Some target quality criteria may be conflicting. Therefore, the method has established a waterfall

for these criteria, to determine which criteria should take precedence and be used for scoring.

For instance, companies may be reporting multiple targets within the same scope and timeframe,

e.g., two mid-term targets covering scope 1+2, covering different parts of their operation. Further,

users of this method may use different databases to collect target and emissions data which may

be updated with different frequencies, resulting in a combined user database with multiple targets

that may be conflicting. The below waterfall approach is used to select a single target for each

timeframe and scope category for scoring.

32

© CDP Worldwide and WWF International 2024

Table 7: Target waterfall criteria

Rank

Criteria

Priority

1

Vintage

More recently published targets

2

Boundary coverage

Highest coverage

3

Type

1) Absolute

2) Intensity

3) Other

4

Scope coverage

Prefer single scope S1, S2, and S3 targets before combined

scope targets that cannot be broken down into single scope

components.

5

Reduction ambition

Higher reduction ambition preferred

6

Timeframe

Longer-term targets are preferred within each timeframe

bucket (i.e., short-, medium-, long-term). If there are several

targets with same target year the more recent base year is

preferred.

6.3.1. Target vintage

A company’s latest statement of emission reduction ambition is preferred to older communicated

targets. Thus, a target to reduce GHG emissions by 30% by 2030 that was communicated last

month will take priority and be scored, instead of a target of 40% GHG emissions reduction by

2032 communicated last year, ceteris paribus. If the latest statement date is not available, the

method uses the target start year.

6.3.2. Boundary coverage

How much of companies’ emissions are covered in the GHG emissions reduction target, i.e., the

boundary coverage, often differ between companies and targets. Therefore, the ambition of the

target is normalized with the boundary coverage of the target. The boundary coverage of a target

can be expressed in percentage terms (e.g., 80% of the company’s scope 1 emissions in the base

year) or in emissions terms (e.g., 800,000 tons of scope 1 emissions out of a total 1,000,000 tons

of scope 1 emissions in the base year, i.e., 80%).

For combined GHG emissions scope targets, e.g., targets covering more than one scope, the

boundary coverage of the target is defined as the weighted average of the boundary coverage of

each of the scopes included in the target, using base year GHG as weights.

For all targets with less than 100% boundary coverage, the ambition of the target is adjusted by

the boundary coverage percentage. For instance, consider an absolute target of 30% reduction in

scope 1 and 2 GHG emissions, but that this target only covers 20% of the company’s scope 1 and

2 emissions. The ambition would then be adjusted to 6% (30% × 20% = 6%).

Without the quantified boundary coverage data, the method assumes 0% boundary coverage.

Given the adjustment to ambition is done based on the level of boundary coverage, as explained

33

© CDP Worldwide and WWF International 2024

above, any reduction ambition without boundary coverage data will be reduced to 0%. The

temperature score will then become the intercept of the regression.

6.3.3. Target types

Only GHG emission reduction targets are currently acceptable for scoring, i.e., absolute and

intensity GHG targets. Other targets, such as procurement, renewable electricity targets, or

engagement are currently not scored (see exception in Section 6.3.3.1). Long-term ambitious or

aspirational targets that are not quantitative (e.g., climate neutral/net-zero in 2050) are not scored

currently as these types of targets are difficult to objectively translate to a rate of change.

GHG emission reduction target types can broadly be divided into absolute and intensity targets.

All types of absolute targets based on GHG emissions and intensity targets based on GHG

reductions per unit of X are valid for scoring in the method, such as:

- Physical intensity targets: based on GHG emissions per unit of production – e.g. CO2eq /

kWh for Power Generation

- Economic intensity targets: based on GEVA (GHG emissions per unit of value added) or

revenue.

- Intensity targets where the conversion to absolute GHG emissions is disclosed.

6.3.3.1. Target type exception

The exception to this rule is scope 3 targets set using the CDP–WWF Temperature Rating method

version 1.0 or CDP–WWF Temperature Scoring method version 1.5 (this method).