Help to make the most

of your savings with

an Offset Mortgage

Your savings could help you reduce

your monthly mortgage payments

or mortgage term.

C M

Y K

PMS ???

PMS ???

PMS ???

PMS ???

COLOUR

COLOUR

JOB LOCATION:

PRINERGY 3

Non-printing

Colours

BAR_9910221_UK_0921.indd 1BAR_9910221_UK_0921.indd 1 15/09/2021 11:2515/09/2021 11:25

2

|

Offset Mortgages Guide Offset Mortgages Guide

|

3

What is an Offset Mortgage? How the Barclays Offset Mortgage works

Very simply described, an Offset Mortgage is a way of using the credit balances

in your Barclays savings and Barclays current accounts to help reduce the

mortgage balance you are charged interest on.

By linking your savings to your mortgage, you can

make your money work harder.

Any savings and current accounts you choose to

link to an Offset Mortgage will not earn interest,

but the more you hold in them, the more mortgage

interest you will save. As interest is calculated daily^,

even savings held for a few days will reduce the

mortgage interest charged. You can still have

instant access to your savings whenever you want

as they are not part of the mortgage loan.

Secure and trusted brand

Barclays is one of the UK’s leading mortgage

providers and one of the first to introduce Offset

Mortgages to the UK so you can be confident in

your choice.

What interest rate will I pay?

All Barclays Offset Mortgages are tracker mortgages

and so the interest rate is variable. Most of our

trackers change in line with the Bank of England

Base Rate (BEBR)** which is a variable rate set by

the Bank of England. Current rates are available

online, on the telephone, or you can find out more

from a Barclays Mortgage Advisor.

** The Bank of England Base Rate is a variable rate which can go up

or down.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS

ON YOUR MORTGAGE.

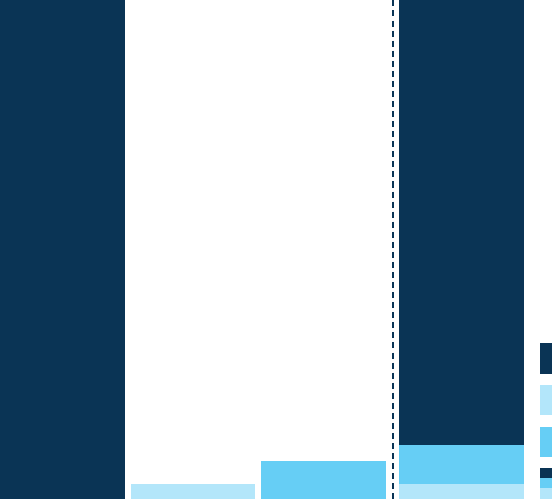

If you have a mortgage of £120,000 and have

£10,000 in linked Barclays savings and current

accounts, by offsetting you will only be charged

mortgage interest on the £110,000 difference.

You can choose to regularly overpay each month,

without incurring early repayment charges,

by making your contractual monthly payment.

The interest saved will gradually reduce the

mortgage balance and, therefore, the term of

the mortgage or you can pay less each month.

£120,000

£2,500

£7,50 0

^Deposits and withdrawals made over non-working days or after cut-off times on working days are calculated from the next working day.

Our working days are generally Monday to Friday except public holidays. Different types of payment instructions have different cut-off times,

which are the latest time on any day that we can start processing a payment. You can find out the cut-off times by asking us in branch or on the

phone.

BAR_9910221_UK_0921.indd 2BAR_9910221_UK_0921.indd 2 20/09/2021 16:1820/09/2021 16:18

2

|

Offset Mortgages Guide Offset Mortgages Guide

|

3

What is an Offset Mortgage? How the Barclays Offset Mortgage works

Very simply described, an Offset Mortgage is a way of using the credit balances

in your Barclays savings and Barclays current accounts to help reduce the

mortgage balance you are charged interest on.

Secure and trusted brand

Barclays is one of the UK’s leading mortgage

providers and one of the first to introduce Offset

Mortgages to the UK so you can be confident in

your choice.

What interest rate will I pay?

All Barclays Offset Mortgages are tracker mortgages

and so the interest rate is variable. Most of our

trackers change in line with the Bank of England

Base Rate (BEBR) which is a variable rate set by the

Bank of England. Current rates are available online,

on the telephone, or you can find out more from a

Barclays Mortgage Advisor.

** The Bank of England Base Rate is a variable rate which can go up

or down.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS

ON YOUR MORTGAGE.

If you have a mortgage of £120,000 and have

£10,000 in linked Barclays savings and current

accounts, by offsetting you will only be charged

mortgage interest on the £110,000 difference.

You can choose to regularly overpay each month,

without incurring early repayment charges,

by making your contractual monthly payment.

The interest saved will gradually reduce the

mortgage balance and, therefore, the term of

the mortgage or you can pay less each month.

To save even more interest you can also make

adhoc overpayments on your mortgage at any

time if it suits you.

Some charges may apply so please refer to your

offer letter and Terms and Conditions.

Depending on how much you can offset over the

course of the mortgage, you could save thousands

of pounds in interest payments.

~

No interest is payable on funds during the period when used in the

offset arrangement.

£120,000

£2,500

£7,50 0

Standard

Mortgage

Current

Account

~

Savings

Account

~

Offset

Mortgage

£2,500

£7,50 0

^Deposits and withdrawals made over non-working days or after cut-off times on working days are calculated from the next working day.

Our working days are generally Monday to Friday except public holidays. Different types of payment instructions have different cut-off times,

which are the latest time on any day that we can start processing a payment. You can find out the cut-off times by asking us in branch or on the

phone.

BAR_9910221_UK_0921.indd 3BAR_9910221_UK_0921.indd 3 15/09/2021 11:2515/09/2021 11:25

4

|

Offset Mortgages Guide Offset Mortgages Guide

|

5

Why choose a Barclays Offset Mortgage?

Offsetting can make sense whatever

the level of interest rates

By offsetting with Barclays, you are effectively

getting interest on your savings at the full mortgage

rate. For example, if rates are low and affecting the

returns you get on your savings accounts, you may

find your savings work harder for you with an Offset

Mortgage. This is because mortgage interest rates

are usually higher than the rates you can get on

your savings accounts.

For example, if your mortgage rate was 6%, your

savings and current account balances would be

offsetting the mortgage interest at that rate.

We calculate interest daily^ – so your

money works harder

Anything you put in your Barclays linked savings

or current accounts reduces the interest charged

on your mortgage, the following month.

The more you have in your Barclays linked

accounts, the more interest you save on your

mortgage. So you may want to consider

transferring money held in other savings

accounts to your Barclays linked accounts.

You can choose from many eligible

accounts, and view and manage

them online

Many Barclays current and instant access savings

accounts are eligible to be offset as well as all

How does it work?

You can use the mortgage interest you save by offsetting in one of two

ways: later, by reducing the term of your mortgage or now, by reducing

your monthly mortgage payments.

It’s designed to work around you – rather than change the way you deal with

your finances. And because it’s a mortgage from Barclays, you know you’re

in safe and expert hands. Let’s look at some of the special features of a Barclays

Offset Mortgage:

Taking the benefit later

– ‘term reduction’

This could be ideal if you want to pay off your

mortgage early. You make your regular monthly

mortgage payment but the mortgage interest you

save is used to reduce the balance each month and

pay off your mortgage earlier – this could be days,

months or even years earlier, depending on how

much is offset against your mortgage.

Taking the benefit now

– ‘payment reduction’

Payment reduction could be ideal if you want to

reduce your monthly expenditure. The mortgage

interest you save one month is used to reduce your

monthly mortgage payment in the following month.

Your monthly payments will therefore depend on

the credit balance in your linked savings and current

accounts during the previous month.

So you can either keep payments the same and pay off your mortgage earlier or pay a reduced monthly

mortgage payment each month. Whichever you choose, you won’t receive interest on your savings as a

result but you’ll still have access to your funds when you need them. A Barclays Offset Mortgage really does

give you the opportunity to manage your money as it suits you.

Linking your Current and Savings

Accounts

In order to help you get the best out of your Offset

Mortgage we will automatically link any eligible

savings and current accounts held in your sole

or joint names.

Please note that the offset accounts have to be

in the same names as the mortgage or in the

sole name of one of the parties to the mortgage

– we will not link joint savings accounts to sole

account mortgages.

Details of these accounts and the balances that

have been offset each month will appear on your

offset statement.

If there are any accounts that you do not want us

to automatically link against your Offset mortgage

please call 0800 022 4022* and speak to the Offset

Linking Team.

^Deposits and withdrawals made over non-working days or after cut-off times on working days are calculated from the next working day. Our

working days are generally Monday to Friday except public holidays. Different types of payment instructions have different cut-off times, which are

the latest time on any day that we can start processing a payment. You can find out the cut-off times by asking us in branch or on the phone.

BAR_9910221_UK_0921.indd 4BAR_9910221_UK_0921.indd 4 15/09/2021 11:2515/09/2021 11:25

4

|

Offset Mortgages Guide Offset Mortgages Guide

|

5

Why choose a Barclays Offset Mortgage?

Offsetting can make sense whatever

the level of interest rates

By offsetting with Barclays, you are effectively

getting interest on your savings at the full mortgage

rate. For example, if rates are low and affecting the

returns you get on your savings accounts, you may

find your savings work harder for you with an Offset

Mortgage. This is because mortgage interest rates

are usually higher than the rates you can get on

your savings accounts.

For example, if your mortgage rate was 6%, your

savings and current account balances would be

offsetting the mortgage interest at that rate.

We calculate interest daily^ – so your

money works harder

Anything you put in your Barclays linked savings

or current accounts reduces the interest charged

on your mortgage, the following month.

The more you have in your Barclays linked

accounts, the more interest you save on your

mortgage. So you may want to consider

transferring money held in other savings

accounts to your Barclays linked accounts.

You can choose from many eligible

accounts, and view and manage

them online

Many Barclays current and instant access savings

accounts are eligible to be offset as well as all

Barclays Mini Cash ISAs. You can see all your

accounts online, alongside your mortgage account,

and make transfers between accounts when

it suits you.

You keep any historical cash

ISA allowances

If you’ve saved money in a cash ISA, you can offset

this. If in the future you don’t want to offset your

ISA accounts, you will not have lost your historical

tax-free cash ISA capital allowance.

You may wish to check whether offsetting your

cash ISA is right for you; this may depend on

your personal circumstances and requirements

as well as the interest rates payable on your cash

ISA accounts.

Offsetting may be tax efficient

As no interest is earned on your Barclays linked

Current and Savings Accounts, there is no tax to

pay on savings interest received. This may be

particularly efficient if you’re a higher rate tax payer.

How to save even more

We let you overpay as much as you like, whenever

you are able. However, fees may apply when you

repay your mortgage in full

†

.

†

Your mortgage product may require the payment of an early

repayment charge on early redemption (either fully or in part).

Details are available on request by calling 0800 022 4022*

or by reference to your original mortgage offer.

How does it work?

You can use the mortgage interest you save by offsetting in one of two

ways: later, by reducing the term of your mortgage or now, by reducing

your monthly mortgage payments.

It’s designed to work around you – rather than change the way you deal with

your finances. And because it’s a mortgage from Barclays, you know you’re

in safe and expert hands. Let’s look at some of the special features of a Barclays

Offset Mortgage:

Taking the benefit now

– ‘payment reduction’

Payment reduction could be ideal if you want to

reduce your monthly expenditure. The mortgage

interest you save one month is used to reduce your

monthly mortgage payment in the following month.

Your monthly payments will therefore depend on

the credit balance in your linked savings and current

accounts during the previous month.

So you can either keep payments the same and pay off your mortgage earlier or pay a reduced monthly

mortgage payment each month. Whichever you choose, you won’t receive interest on your savings as a

result but you’ll still have access to your funds when you need them. A Barclays Offset Mortgage really does

give you the opportunity to manage your money as it suits you.

^Deposits and withdrawals made over non-working days or after cut-off times on working days are calculated from the next working day. Our

working days are generally Monday to Friday except public holidays. Different types of payment instructions have different cut-off times, which are

the latest time on any day that we can start processing a payment. You can find out the cut-off times by asking us in branch or on the phone.

BAR_9910221_UK_0921.indd 5BAR_9910221_UK_0921.indd 5 15/09/2021 11:2515/09/2021 11:25

6

|

Offset Mortgages Guide Offset Mortgages Guide

|

7

Mortgage Current Account

An added feature of your Offset Mortgage is a Mortgage Current Account.

The Mortgage Current Account is linked to your mortgage and can be

used just like a normal current account.

The advantages of using the

Mortgage Current Account

Any credit balance in the account offsets the

mortgage balance, just like the linked savings.

So, if you don’t hold a current account with

Barclays, you could consider having your salary

paid into your Barclays Mortgage Current Account.

It will then offset the mortgage balance, as long

as the account remains in credit.

Is an Offset Mortgage right for you?

If you are interested in an Offset Mortgage or would like more information after reading this booklet, please

make an appointment to see a Barclays Mortgage Adviser in one or our branches, or call 0845 677 9993*.

If you have savings or a little left over each month, an Offset Mortgage could

suit you. That applies whether you’re remortgaging or buying a new home.

Your Situation The Benefits of an Offset Mortgage

An Offset Mortgage could be particularly useful if:

You want to save now, as well as pay off

your mortgage faster

Your savings could work efficiently until you need

them – and at the same time you could either

reduce your monthly payments or the term of

your mortgage

You want to save regularly towards your annual

tax bill

You want to be able to dip in and out of your

savings as you need them

You are self-employed or in a job where your

income is variable and may consist of additional

payments, such as bonuses or commission

As interest is calculated daily any regular monthly

overpayments or any bulk payments to your offset

accounts will start to save mortgage interest

immediately

You have other sources of income such as rent

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS

ON YOUR MORTGAGE.

BAR_9910221_UK_0921.indd 6BAR_9910221_UK_0921.indd 6 15/09/2021 11:2515/09/2021 11:25

6

|

Offset Mortgages Guide Offset Mortgages Guide

|

7

Mortgage Current Account

An added feature of your Offset Mortgage is a Mortgage Current Account.

The Mortgage Current Account is linked to your mortgage and can be

used just like a normal current account.

The advantages of using the

Mortgage Current Account

Any credit balance in the account offsets the

mortgage balance, just like the linked savings.

So, if you don’t hold a current account with

Barclays, you could consider having your salary

paid into your Barclays Mortgage Current Account.

It will then offset the mortgage balance, as long

as the account remains in credit.

Makes paying in and out easy

You can use your cheque book and debit card

to make payments from your mortgage current

account. You can also manage the account online

or by telephone to view statements, set up standing

orders or manage regular payments.

Is an Offset Mortgage right for you?

If you are interested in an Offset Mortgage or would like more information after reading this booklet, please

make an appointment to see a Barclays Mortgage Adviser in one or our branches, or call 0845 677 9993*.

If you have savings or a little left over each month, an Offset Mortgage could

suit you. That applies whether you’re remortgaging or buying a new home.

Your Situation The Benefits of an Offset Mortgage

An Offset Mortgage could be particularly useful if:

You want to save now, as well as pay off

your mortgage faster

Your savings could work efficiently until you need

them – and at the same time you could either

reduce your monthly payments or the term of

your mortgage

You want to save regularly towards your annual

tax bill

You want to be able to dip in and out of your

savings as you need them

You are self-employed or in a job where your

income is variable and may consist of additional

payments, such as bonuses or commission

As interest is calculated daily any regular monthly

overpayments or any bulk payments to your offset

accounts will start to save mortgage interest

immediately

You have other sources of income such as rent

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS

ON YOUR MORTGAGE.

BAR_9910221_UK_0921.indd 7BAR_9910221_UK_0921.indd 7 15/09/2021 11:2515/09/2021 11:25

8

|

Offset Mortgages Guide Offset Mortgages Guide

|

9

What will I pay in the month after

my mortgage completes?

In the first full month after your mortgage

completes, the payment you will have to make

is a full contractual monthly payment plus any

mortgage interest carried forward from the

month when your mortgage completed.

Your first monthly payment will be reduced by the

Offset Benefit you have earned by the end of the

month when your mortgage completes. This is

because each monthly payment is reduced by

the amount of Offset Benefit that you have earned

in the previous month.

What will I pay each month thereafter?

Each of the following monthly payments will be

reduced by the Offset Benefit earned during the

previous month. If the total balance held in your

offset accounts fluctuates during the month, this

will be reflected in the following month’s payment.

If I choose ‘payment reduction’ and

have exactly the same in savings

as I have on my mortgage, will I pay

or receive any interest?

This is known as 100% offset, and in theory it

would mean you pay no interest on your mortgage

and receive no interest on your savings. In reality

there would be slight anomalies. The monthly

mortgage payment is calculated as 1/12th of the

annual interest plus any capital repayment due

(i.e. each ‘month’ is 30.4 days) whereas the Offset

Benefit is based on the actual number of days

in the calendar month. For example, the mortgage

payment for March would be for 30.4 days less

the Offset Benefit earned during the 28 days of

February and there would, therefore, be a small

amount to pay.

How many people can be part

of an Offset Mortgage?

Offset mortgages can be offered to one or

two applicants.

Which accounts can I use to offset?

Many Barclays current and instant access savings

accounts are eligible to be offset as well as all

Barclays Mini Cash ISAs. With the exception of

Cash ISAs we will automatically link all eligible

savings and current accounts. However, you cannot

offset Bonds. Check with your Mortgage Adviser

if your Barclays accounts are eligible to be offset.

If you don’t have a suitable Barclays account,

we can open one for you.

Can I offset accounts in individual

names on a joint mortgage?

Yes, you can offset the savings or current accounts

of an individual as long as they are named on the

mortgage. Please be aware that eligible accounts

in a sole name will automatically be linked to the

offset mortgage, and account and balance details

for both joint and individual accounts will appear

on the monthly Offset statement.

How and when do I choose which

accounts to offset?

You can open additional savings accounts at any

time before your mortgage completes if you wish

to keep your savings in different accounts. We will

link all eligible savings and current accounts to

your mortgage when it completes but not your

Cash ISAs. You will receive a letter confirming the

accounts that have been offset and you can contact

us if you wish to open new accounts or to offset any

Cash ISAs.

If you decide that there are accounts that you

would prefer were not automatically offset against

your Offset mortgage, please call 0800 022 4022*

and speak to the Offset Linking Team.

Will I get credit interest on my savings?

No, from the day your mortgage completes and

your Offset Arrangement is set up, your linked

savings will stop earning interest.The total balance

of your offset accounts will instead be used to

reduce the mortgage balance that interest is

calculated on. The interest you save every month

is known as your Offset Benefit.

How can an Offset Mortgage reduce

the length of my mortgage?

If you choose ‘term reduction’, we’ll collect your full

monthly mortgage payment, and the interest saved

from offsetting your savings (your Offset Benefit)

will be used to reduce the capital part of your

mortgage, thus helping to pay it off sooner.

If I choose to reduce my monthly

payments, how will I know what I’m

paying each month?

We’ll send you an Offset statement at the end of

each month showing a daily breakdown of the

Offset Benefit you have earned from any accounts

you have linked to your mortgage. This statement

will also show the monthly payment that we will

collect by direct debit in the following month.

What will my payment be in the month

my mortgage completes?

As your mortgage can complete at any time during

the month we will not collect your first payment

until the following month. However, you will begin

to earn Offset Benefit on the total balances in the

accounts that you have linked to your mortgage.

Your questions answered

BAR_9910221_UK_0921.indd 8BAR_9910221_UK_0921.indd 8 15/09/2021 11:2515/09/2021 11:25

8

|

Offset Mortgages Guide Offset Mortgages Guide

|

9

What will I pay in the month after

my mortgage completes?

In the first full month after your mortgage

completes, the payment you will have to make

is a full contractual monthly payment plus any

mortgage interest carried forward from the

month when your mortgage completed.

Your first monthly payment will be reduced by the

Offset Benefit you have earned by the end of the

month when your mortgage completes. This is

because each monthly payment is reduced by

the amount of Offset Benefit that you have earned

in the previous month.

What will I pay each month thereafter?

Each of the following monthly payments will be

reduced by the Offset Benefit earned during the

previous month. If the total balance held in your

offset accounts fluctuates during the month, this

will be reflected in the following month’s payment.

If I choose ‘payment reduction’ and

have exactly the same in savings

as I have on my mortgage, will I pay

or receive any interest?

This is known as 100% offset, and in theory it

would mean you pay no interest on your mortgage

and receive no interest on your savings. In reality

there would be slight anomalies. The monthly

mortgage payment is calculated as 1/12th of the

annual interest plus any capital repayment due

(i.e. each ‘month’ is 30.4 days) whereas the Offset

Benefit is based on the actual number of days

in the calendar month. For example, the mortgage

payment for March would be for 30.4 days less

the Offset Benefit earned during the 28 days of

February and there would, therefore, be a small

amount to pay.

What happens if I have more in savings

balances than I have outstanding on

my mortgage?

Because of the way interest is calculated on an

Offset Mortgage, you wouldn’t receive any credit

interest on the surplus savings.

Can I withdraw an account from the

offset arrangement?

Yes. Simply let us know which account you no

longer wish to offset and we can arrange this for

you. Alternatively, you can remove the account

yourself if you are registered for Online Banking.

Any account you choose to withdraw from the

Offset Arrangement will continue to operate under

the terms and conditions of the particular product.

You will start earning interest (if applicable) on any

credit balance held in that account and it will no

longer be included in the interest calculation

for the mortgage. You can return any eligible

account to the Offset Arrangement at any time.

Will I get credit interest on my savings?

No, from the day your mortgage completes and

your Offset Arrangement is set up, your linked

savings will stop earning interest.The total balance

of your offset accounts will instead be used to

reduce the mortgage balance that interest is

calculated on. The interest you save every month

is known as your Offset Benefit.

How can an Offset Mortgage reduce

the length of my mortgage?

If you choose ‘term reduction’, we’ll collect your full

monthly mortgage payment, and the interest saved

from offsetting your savings (your Offset Benefit)

will be used to reduce the capital part of your

mortgage, thus helping to pay it off sooner.

If I choose to reduce my monthly

payments, how will I know what I’m

paying each month?

We’ll send you an Offset statement at the end of

each month showing a daily breakdown of the

Offset Benefit you have earned from any accounts

you have linked to your mortgage. This statement

will also show the monthly payment that we will

collect by direct debit in the following month.

What will my payment be in the month

my mortgage completes?

As your mortgage can complete at any time during

the month we will not collect your first payment

until the following month. However, you will begin

to earn Offset Benefit on the total balances in the

accounts that you have linked to your mortgage.

Your questions answered

BAR_9910221_UK_0921.indd 9BAR_9910221_UK_0921.indd 9 15/09/2021 11:2515/09/2021 11:25

10

|

Offset Mortgages Guide Offset Mortgages Guide

|

11

Would you like more information?

New Offset Enquiry

If you are interested in an Offset Mortgage or

would like more information after reading this

booklet, please make an appointment to see a

Mortgage Adviser in one of our branches, or call

0845 677 9993* to speak to a mortgage specialist.

Existing Offset Customers

If you already have an Offset Mortgage and have

any queries about which accounts you can offset,

please contact us on 0800 022 4022* and speak

to the ‘Offset Linking Team’.

You can also find more information about Offset Mortgages at

barclays.co.uk

BAR_9910221_UK_0921.indd 10BAR_9910221_UK_0921.indd 10 15/09/2021 11:2515/09/2021 11:25

10

|

Offset Mortgages Guide Offset Mortgages Guide

|

11

Would you like more information?

Existing Offset Customers

If you already have an Offset Mortgage and have

any queries about which accounts you can offset,

please contact us on 0800 022 4022* and speak

to the ‘Offset Linking Team’.

You can also find more information about Offset Mortgages at

barclays.co.uk

Let’s talk it through

|

in branch

|

0845 677 9993

*

|

barclays.co.uk

BAR_9910221_UK_0921.indd 11BAR_9910221_UK_0921.indd 11 15/09/2021 11:2515/09/2021 11:25

Your feedback

If you have a complaint about any aspect of our service then we would like to hear from you. You can

contact us by phone, in person, or in writing, either by post or e-mail. Details of our complaints handling

procedures are available on request from any branch, Barclays Group Information line on 0800 400 100*,

or barclays.co.uk.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS

ON YOUR MORTGAGE

You can request this in Braille, large print or audio. For information

about all of our accessibility services or ways to contact us, visit

barclays.co.uk/accessibility

Call monitoring and charges information

*Calls to 0800 numbers are free if made from a UK landline and international calls are charged at local rate,

mobile costs may vary – please check with your telecoms provider. Calls may be recorded so that we can

monitor the quality of our service and for security purposes.

Barclays Bank UK PLC. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and

the Prudential Regulation Authority (Financial Services Register No. 759676). Registered in England. Registered No. 9740322.

Registered Office: 1 Churchill Place, London E14 5HP.

Item ref: 9910221_UK Created: 09/21

BAR_9910221_UK_0921.indd 12BAR_9910221_UK_0921.indd 12 15/09/2021 11:2515/09/2021 11:25