STATE OF CALIFORNIA

CALIFORNIA DEBT LIMIT ALLOCATION COMMITTEE

915 CAPITOL MALL, ROOM 311

SACRAMENTO, CA 95814

TELEPHONE: (916) 653-3255

FAX: (916) 653-6827

www.treasurer.ca.gov/cdlac

Jeree Glasser-Hedrick

Executive Director

Background

Localities and certain state agencies can apply to the California Debt Limit Allocation Committee (CDLAC) for

authority to issue Mortgage Credit Certificates (MCC) to low- and moderate-income first-time homebuyers, or to

low- and moderate-income families purchasing a home in a federally-defined target area (Qualified Census Tract).

What is a Mortgage Credit Certificate?

An MCC provides eligible borrowers with a federal income tax credit based on a specified percentage of the

mortgage interest paid each year. The tax credit is a dollar-for-dollar reduction in the homebuyer’s federal tax

liability that increases the household income available to qualify for a mortgage loan and to make monthly

mortgage payments. MCCs can be used with many fixed- or adjustable-rate mortgages, but cannot be used with

tax-exempt bond financed programs.

Who is eligible to receive a Mortgage Credit Certificate?

• Occupancy: Home must be owner-occupied for the life of the MCC.

• Income Limits: Household income cannot exceed 115% of the Area Median Income, unless the household is

purchasing a home in a federally-defined target area or high cost area.

• Purchase Price Limits: Home price cannot exceed 90% of the average area purchase price over the past 12

months, unless the home is located in a federally-defined target area.

• First-Time Homebuyer: Household must not have owned a home for three years prior to application, unless

the household is purchasing a home in a federally-defined target area.

How do Mortgage Credit Certificates work?

Most often, the participating lender or broker originating the loan that the MCC is attached to submits eligibility

information to the locality for approval when the mortgage loan is packaged for credit review. The MCC benefit

can equal 15% - 20% of mortgage interest as determined by the locality for their program. It can be redeemed

annually on the homebuyer’s federal taxes or proportionately each month on their paycheck by increasing their

withholdings. Since the amount of interest paid declines as the amount of principal paid increases, the MCC

benefit declines each year; however, the remaining 80% - 85% of the interest is still eligible for the standard

mortgage interest tax deduction.

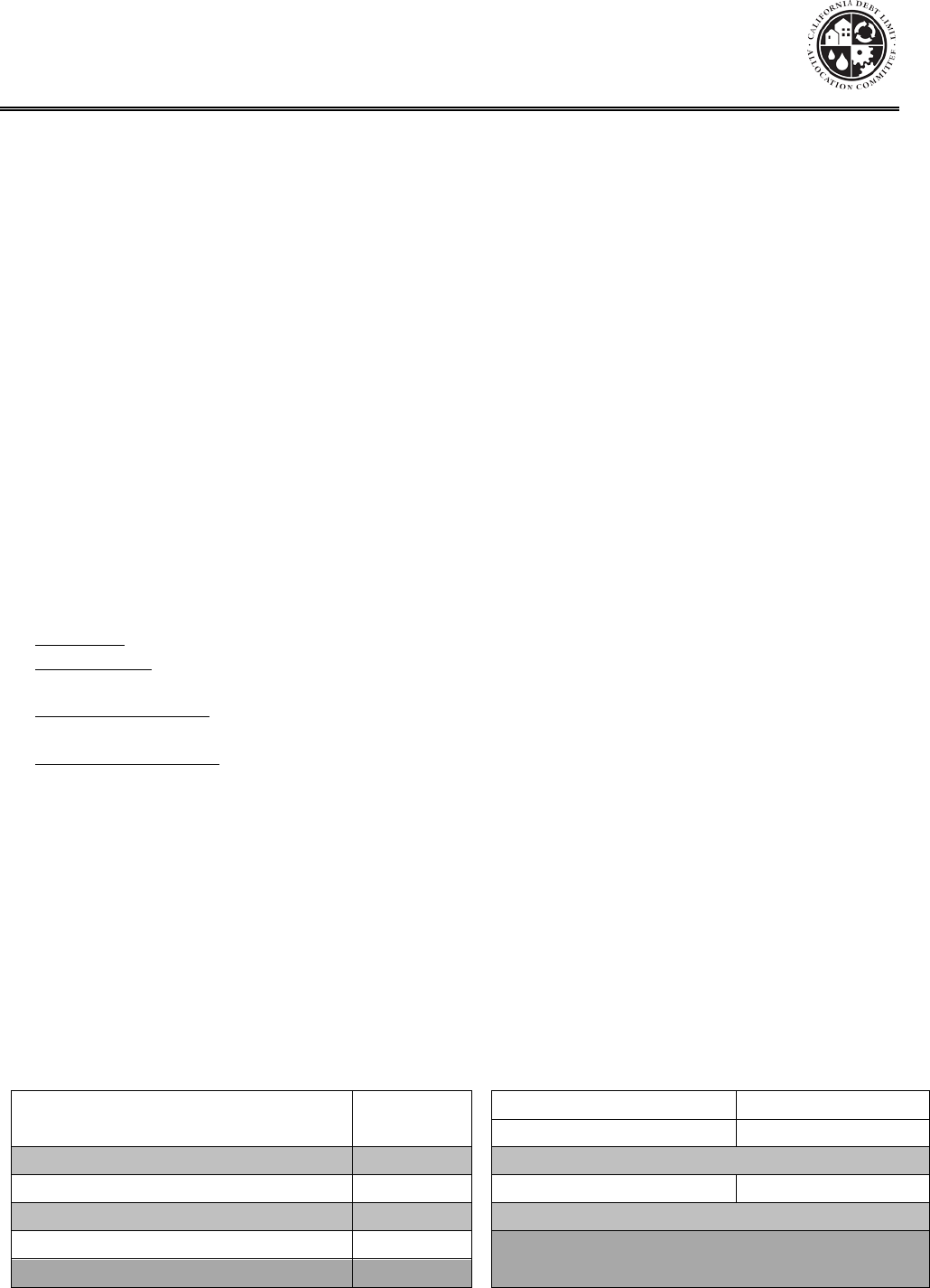

For example, a 15% tax credit on a $360,000 home loan with a 30-year term will yield a total tax savings of

$54,000 in addition to most of the standard deductions, as demonstrated below.

30-Year Tax Savings from MCC

Purchase Price

$400,000

Year 1 Tax Credit Value

$2,955

Minus 10% Down Payment

$40,000

Year 10 Tax Credit Value

$2,420

Loan Amount

$360,000

Total saved on taxes to date = $29,000

Multiplied by Interest Rate

5.50%

Year 20 Tax Credit Value

$1,499

Annual Interest Payment

$19,800

Total saved on taxes to date = $49,000

Multiplied by Tax Credit Percentage

15%

Total saved at the end of 30 years = $54,000 plus

most of the standard interest deduction.

Year 1 MCC Value

$2,955

MEMBERS

John Chiang, Chairman

State Treasurer

Edmund G. Brown Jr.

Governor

Betty T. Yee

State Controller