1

Discretionary Fiscal Policy as

a Stabilization Policy Tool:

What Do We Think Now That We Did Not

Think in 2007?

J. Bradford DeLong

Laura D. Tyson

1

U.C. Berkeley

DRAFT 1.21: April 5, 2013: 31 pp. 8166 words

ABSTRACT

Six years ago there was near-consensus among economists and

policymakers alike in support of Taylor's (2000) argument that aggregate

demand management was the near-exclusive domain of central banks.

Today central bankers like Federal Reserve Chair Bernanke (2013) are

actively asking for help by fiscal authorities. What caused this shift? In

part, the course of interest rates has made the costs of discretionary

expansionary fiscal policy lower than anyone would have believed. In

part, the benefits via Keynesian multiplier processes appear to have been

much larger than was presumed. And in large part monetary policy has

proven inadequate to the task without undertaking risky and untried non-

standard policy measures at a scale that has so far proven too large for

central banks to risk. Against this shift in the benefit-cost calculus toward

use of discretionary expansionary fiscal policy in the current conjuncture

we must set uncertain long-run costs of debt accumulation. These costs,

however, remain especially hard to analyze as they seem to substantially

consist of “unknown unknowns”.

1

We would like to thank Owen Zidar for excellent research assistance, and Olivier

Blanchard, Joe Gagnon, Yuriy Gorodnichenko, Carmen Reinhart, Christina Romer,

Robert Strom and Larry Summers for helpful conversations and observations.

2

II. What We Thought About Fiscal Policy Back in 2007

Six years ago, there was near-consensus among economists and

policymakers alike in support of John Taylor's (2000) argument that

aggregate demand management was the near-exclusive province of central

banks and monetary policy.

2

There was also near-consensus that the

expansionary stabilization policy tool of choice was the conventional open-

market operation: buying short-term government bonds for cash in order to

expand the money supply and so induce an increase in the pace of nominal

spending.

There were five powerful reasons for this near-consensus against the use of

discretionary fiscal policy

3

and for the use of monetary policy:

1. The problem of legislative confusion: Legislatures that were told that

expansionary policies which led to cyclical deficits in downturns were

good might have difficulty retaining the other important lesson that

structural deficits which led to perpetually rising debt-to-GDP ratios were

bad. Better, it was thought, to keep the legislative process focused on

“classical” considerations of the benefits and costs of spending programs

and taxation levels.

2. The problem of legislative process: Legislatures are, by design,

institutions that find it very difficult to make decisions quickly. Central

banks, by contrast, can move asset prices in an hour. Fiscal policies that

take effect this year as a result of decisions made by a legislature last year

based on information from two or three years ago would seem to

guarantee sub-optimal economic outcomes.

3. The problem of implementation: Public bureaucracies have limited

capacities to ramp-up or ramp-down their spending levels quickly without

incurring substantial waste. The larger the fiscal-policy intervention to

balance aggregate demand, the less likely the intervention would be well

timed, well designed and well executed.

2

John Taylor (2000), "Reassessing Discretionary Fiscal Policy", Journal of Economic

Perspectives 14:3 (Summer), pp. 21-36

<http://www.econ.ucdavis.edu/faculty/kdsalyer/lectures/ecn137/taylor_fiscal.pdf>.

3

There were no objections to "automatic stabilizers"--deficits produced by the natural

income elasticity of both tax and benefit structures.

3

4. The problem of rent-seeking: In a world where we fear that the

structure of government already leads to policies favoring too-many

politically-powerful winners at the expense of politically-weak losers, an

additional excuse to undertake fiscal projects and programs that would

not meet conventional societal benefit-cost tests is not welcome.

5. The problem of superfluity: Monetary policy was strong enough to do

the job. Fiscal policy was simply not necessary.

Of these, the fifth was most important.

The other four were political or institutional reasons for why the

discretionary portions of fiscal policy were not well adapted to a fiscal

stabilization role and instead should be set on “classical” principles. But

those arguments would not have been decisive save for the near-consensus

that central banks could, via monetary policy, direct the flow of nominal

spending in the economy to any pace they might desire. Under this

condition, no additional degrees of freedom of action were opened up by the

addition of discretionary fiscal policy.

This part of the near-consensus was backed by two lines of argument:

First, there was the observation that the failure to find robust evidence of

substantial non-wartime fiscal policy multipliers was a sign that central

banks were already engaging in full fiscal offset. According to this line of

thinking, central banks had in mind targets for the pace of nominal spending

and did not want their elbows joggled by fiscal policy actions. So the central

banks took steps to shift monetary policy to offset what would otherwise

have been the effects on the flow of demand from discretionary fiscal

policy.

4

The econometric failure to find substantial and robust multipliers

4

J. Bradford DeLong and Lawrence H. Summers (2012), "Fiscal Policy in a Depressed

Economy", Brookings Papers on Economic Activity. The belief that the Federal Reserve

under Alan Greenspan was and that financial markets believed the Federal Reserve

engaged in full fiscal offset was a key assumption behind Clinton Administration

justifications of its 1993 deficit-reduction program. See Laura D. Tyson et al. (1994),

Economic Report of the President 1994 (Washington, DC: GPO): “Lower federal

borrowing reduces interest rates directly, by reducing demand for credit. A more prudent

fiscal policy reduces the likelihood that the Federal Reserve will need to pursue a

restrictive monetary policy, and so reduces expected future short-term rates.” For a

contrasting view that fiscal-policy multipliers have in fact been large and that central

4

was thus interpreted as evidence not just that central banks could engage in

full fiscal offset but that they did--hence there was no point for an executive

and a legislature to try to affect the flow of aggregate demand via

discretionary fiscal policy.

Second, there was the theoretical belief that monetary policy could do the

job--even, in all likelihood, if nominal interest rates hit their zero lower

bound at which the elasticity of demand for cash was effectively unlimited.

As Professor Bernanke (1999)

5

wrote just before the millennium of Japan:

[L]iquidity trap or no, monetary policy retains considerable power….

Money… pays zero interest and has infinite maturity…. [I]f the price level

were truly independent of money issuance, then the monetary authorities

could use the money they create to acquire indefinite quantities of goods

and assets. This is manifestly impossible in equilibrium. Therefore money

issuance must ultimately raise the price level, even if nominal interest

rates are bounded at zero. This is an elementary argument… quite

corrosive of claims of monetary impotence…. [A] target in the 3-4% range

for inflation…. A nonstandard open-market operation… the purchase of…

long-term government bonds… at fair market value… [T]here is little

doubt that such operations, if aggressively pursued, would indeed have the

desired effect…. To claim that nonstandard open-market purchases would

have no effect is to claim that the central bank could acquire all of the real

and financial assets in the economy with no effect on prices or yields…

Yet in today's environment Federal Reserve Chair Bernanke (2013)

6

takes a

very different view:

7

that the Federal Reserve either does not have the power

to offset effects of discretionary fiscal policy on demand or sees large risks

in doing so, and in any event will not try to offset these effects:

Although monetary policy is working to promote a more robust recovery,

it cannot carry the entire burden…. The challenge for the Congress and the

banks have not been successfully engaged in full fiscal offset, see Christina Romer and

David Romer (2010), “The Macroeconomic Effects of Tax Changes: Estimates Based on

a New Measure of Fiscal Shocks” American Economic Review 100:3 (June), pp. 763-801

<http://goo.gl/h0wrC>.

5

Ben Bernanke (1999), "Japanese Monetary Policy: A Case of Self-Induced Paralysis?"

<http://www.princeton.edu/~pkrugman/bernanke_paralysis.pdf

>

6

Ben Bernanke (2013), "Semiannual Monetary Policy Report to Congress" (February 26)

<http://www.federalreserve.gov/newsevents/testimony/bernanke20130226a.htm

>.

7

Note that on April 5, 2013, the Bank of Japan in large part adopted Bernanke’s policy

recommendations of fourteen years before, embarking on a policy to double the monetary

base in two years in order to reflate the Japanese economy.

5

Administration is to put the federal budget on a sustainable long-run path

that promotes economic growth and stability without unnecessarily

impeding the current recovery…. [L]owering the deficit has been

concentrated in [the] near-term… which… could create a significant

headwind for the economic recovery… slow the pace of real GDP growth

by about 1-1/2 percentage points this year…

And Chairman Bernanke calls for a more expansionary fiscal policy posture

in the United States:

[T]he Congress and the Administration should consider replacing the

sharp, frontloaded spending cuts required by the sequestration with

policies that reduce the federal deficit more gradually…. Such an

approach could lessen the near-term fiscal headwinds facing the

recovery…

While Professor Bernanke believed that central banks had the tools, the

power, and the will to do what was necessary to support the level of

aggregate demand consistent with the economy’s productive potential--and

thus assistance from fiscal policy was superfluous--Chair Bernanke now

definitely asks for assistance from fiscal authorities in the form of delayed

long-run fiscal rebalancing.

What caused this shift? And how far does this shift extend? What do we now

think are the limits on the appropriate stabilization policy role of

discretionary fiscal policy?

III. The Evolution of Thinking on Discretionary Fiscal Policy as

Stabilization Policy, 2007-2013

Looking back, thought on discretionary fiscal policy as stabilization policy

has only gradually shifted away from the near-consensus rejection of any

appropriate role six years ago. Six distinct stages in the evolution of thinking

can be seen.

First, with the reduction of short-term nominal policy interest rates to zero

toward the end of 2008, there came recognition that conventional open-

market operations were not powerful enough to accomplish the desired

stabilization of aggregate demand. This recognition led to another: that

discretionary fiscal policy might have an appropriate stabilization role, but

6

this role would be limited to a period of at most two years, until

deleveraging, rebalancing, and price adjustment proceeded far enough to

bring an end to the liquidity trap and an exit from the zero lower bound on

short-term nominal interest rates.

By mid-2009, however, events had moved on to a second stage produced by

the slow recognition that the financial shock was larger than anticipated and

deleveraging and price adjustment slower than anticipated. The consequence

was that exit from the liquidity trap would come not in 2010 but

considerably later, and this raised the question of whether expansionary

discretionary fiscal policy might have a medium-run rather than merely a

short-run role to play.

The medium-run limit on expansionary fiscal policy had always been that it

would trigger the crowding-out of investment spending. An increase in bond

issues that raised the supply of government debt would lower the price of

both government debt and private debt, and so crowd-out the private

investment projects that private debt would normally finance. Unless there

was strong confidence that the central bank would act on interest rates in a

timely way to prevent such crowding-out from taking place, this channel

had, in the general consensus, always made any medium-run stabilization

policy role for expansionary discretionary fiscal policy unwise.

However, no interest rate increases occurred in much of Europe, including

the UK, in North America, or in Japan. For the most credit-worthy

sovereigns, even extraordinary rates of increase in sovereign debts did not

call forth any rise in long-term rates. There was no crowding-out of private

investment: rather the reverse.

Nevertheless, during this second stage of thinking there were questions as to

whether “non-standard” monetary and banking policy measures—

quantitative easing, relaxation of medium-term inflation targets, nominal

GDP level targeting, loan guarantees, and bank recapitalizations—might be

superior to discretionary fiscal policy and obviate the need for it.

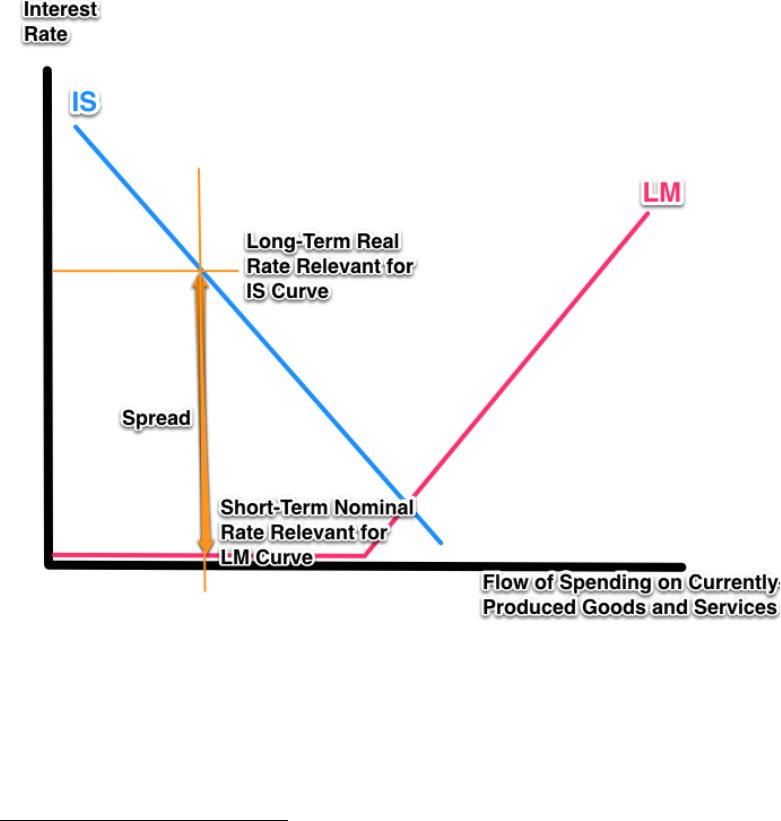

A framework for analyzing these first-round issues can be found in a four-

commodity model of John Hicks (1937), in which the commodities are:

money, safe short-term bonds, risky long-term bonds, and spending on

7

currently-produced goods and services.

8

In this framework there are four

variables to be determined: the short-term safe nominal interest rate that

clears the supply and demand for money balances according to the “LM”

Irving Fisher quantity theory, the long-term risky real interest rate that clears

the supply and demand for bonds according to the “IS” Knut Wicksell

savings-investment equation, the spread between the interest rate relevant

for the “LM” curve and the interest rate relevant for the “IS” curve, and the

flow of spending on currently-produced goods and services.

Figure 1: An Augmented Hicks Diagram

In this framework, the OECD economy as of late 2009 was characterized by

(a) a very low short-term safe nominal interest rate relevant for money

demand and money supply in the “LM” curve, (b) a rather high long-term

8

Olivier Blanchard stresses the importance of moving from a three-commodity to a four-

commodity version of the Hicksian (1937) general-equilibrium framework. See Tim

Besley, et al. (2013), “What should economists and policymakers learn from the financial

crisis?” (London School of Economics video) <http://goo.gl/9TG4K>.

8

risky real interest rate relevant for the determination of savings, investment,

and the flow of spending in the “IS” curve, (c) an unusually high spread

between the interest rates relevant for the “IS” and the “LM” curves

produced by low forecast inflation and the greatly diminished risk-bearing

capacity of financial intermediaries in a context of heightened perceived

risk, and (d) a reduced flow of spending on currently-produced goods and

services.

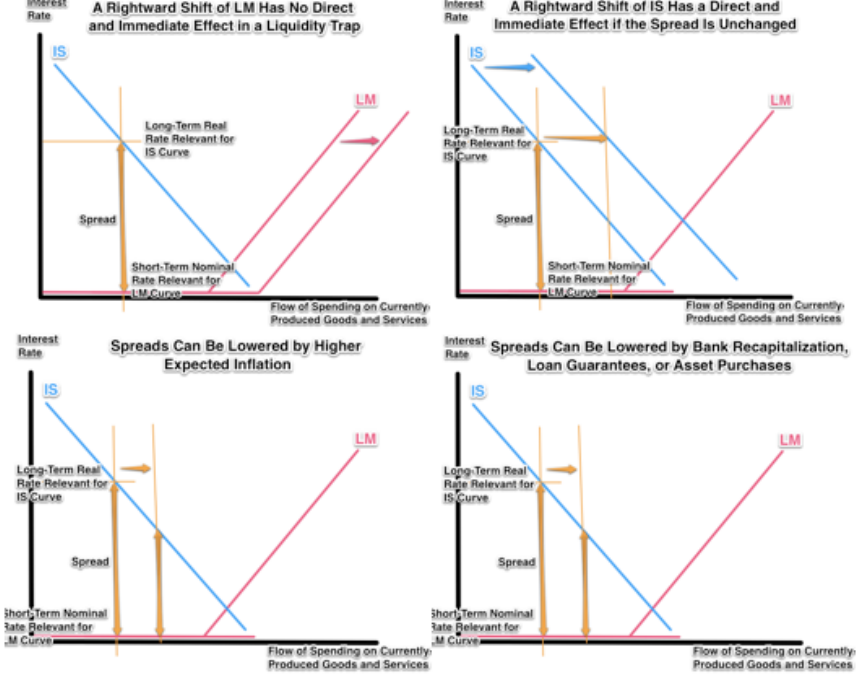

Figure 2: Policies in the Augmented Hicks Diagram

Restoring the flow of spending to a pace consistent with normal levels of

employment could, in theory at least, be achieved by a number of different

policy tools. The obvious tool was monetary expansion to shift the quantity-

theory money-market supply and demand “LM” curve to the right. However,

the fact that the short-term safe nominal interest rate was at its zero lower

bound meant that a further rightward shift of the “LM” curve would have no

direct and immediate effect on the system’s current state. The next obvious

9

tool was fiscal expansion: shifting the IS curve to the right, with the hope of

having a direct and immediate positive effect on spending and employment,

which would naturally occur on the absence of a steep sudden rise in the

interest-rate spread.

But there was also the possibility of policies to reduce the interest-rate

spread, thus having a direct and immediate positive effect on the economy

without requiring immediate increases in fiscal deficits. A credible

commitment to a higher medium-term inflation rate would reduce the

spread—for the interest rate relevant to the “IS” curve is a real rate, while

the interest rate relevant to the “LM” curve is a nominal rate. Such a

commitment might be accomplished via quantitative easing as a pledge that

monetary expansion would be maintained even after the economy had exited

the zero-lower bound. A reduction in risk, either through central bank

purchases of risky assets via quantitative easing or through loan guarantees

would also reduce the spread. And an increase in the risk-bearing capacity of

the financial sector via banking-sector recapitalization would reduce the

spread as well.

Thus by mid-2010 the debate over the medium-run role of expansionary

discretionary fiscal policy had moved to the recurrent fear that fiscal

expansion would increase the interest-rate spread. Most of the developed

countries face a long-term fiscal dilemma. Aging populations require greater

pension and health-care expenditures, a great deal of which will inevitably

land on governments. An ongoing shift in economic structure towards an

increasing share of GDP devoted to education and to health care promises a

larger share of government spending in GDP as well—for the four major

sectors of the economy that have never been successfully privatized are

infrastructure, national defense, and the twins of health care and education.

Governments have no consistent and coherent plans for dealing with this

long-term projected rise in government spending as a share of GDP. In such

a policy environment, a short-term move further away from what would be

seen as fiscal prudence might increase perceptions of risk and increase

spreads. Thus expansionary fiscal policy might prove to be

counterproductive, if the rise in spreads overbalanced whatever rightward

shift in the “IS” curve fiscal expansion accomplished.

In the absence of European fiscal union and with the commitment of the

European Central Bank to support the government bond markets of

peripheral European countries unclear, these third-stage considerations

10

moved from theory to reality as large budget deficits in southern European

countries triggered runs on national government bond markets and a sharp

increase in interest-rate spreads. It became clear that successful

expansionary fiscal policy required a central bank willing to support the

relevant government bond market and, behind it, a credit-worthy sovereign

to support the central bank—or required backing of a non-credit-worthy

sovereign by a credit-worthy sovereign. Thus among the developed

countries, expansionary discretionary fiscal policy came to be a policy

option limited to Japan, the United States and Canada, Great Britain,

Germany, the IMF, and possibly France—and to other economies only

insofar as they could draw on those credit-worthy sovereigns for backing.

But would those credit-worthy sovereigns remain credit-worthy?

By mid-2011 the debate had moved on to stage four. There was an

acknowledgement that the limit on fiscal expansion and spending—for the

most credit-worthy sovereigns, at least—was not that further deficit

spending would lead to crowding-out and fail to boost output and

employment now, but would rather that it would entail unwarranted risks of

long-term inflation should electorates prove unwilling to tax themselves to

properly amortize the debt. Delaying fiscal consolidation in these

circumstances might not be counterproductive in the short-run or the

medium-run, but it would elevate risks in the long-run when the electorates

of the credit-worthy sovereigns would be presented with the bills that had

been incurred in their name.

Stages five and six in the evolution of thinking about fiscal policy occurred

between mid-2011 and mid-2012. Stage five was the slow recognition that

the collapse of private-sector risk tolerance was not being reversed.

Banking-sector recapitalization and central bank and Treasury backstops did

not lead to a revival of the credit channel’s willingness to assume risk and

encourage enterprise. There was growing recognition that merely

recapitalizing the banking system does not restore the trust of private savers

in financial intermediaries and the functioning of the credit channel and that

at least for the medium term private savers' demands for the debt of credit-

worthy sovereigns will be much larger than had previously been thought

possible. These developments encouraged some economists and

policymakers to consider whether governments could create alternative

savings vehicles that private-sector savers would trust as low risk without

having a large adverse effect on government's long-term balance sheet.

11

It seemed as if demand for safe nominal assets was sufficiently elevated that

only credit-worthy sovereigns could possibly provide the safe assets the

private sector wanted to hold in sufficient quantity to allow for rebalancing

near full employment.

And stage six was the recognition that the fiscal stakes both in the short-run

and the long-run were larger than had been recognized. The IMF’s revisiting

of the cross-European experience led it to conclude that the open-economy

policy-relevant fiscal multipliers in 2009-2011 had been not 0.5 but 1.5—

which implies that the closed-economy policy-relevant fiscal multipliers not

for individual countries but for Europe or for North America as a whole

were in all likelihood close to if not greater than 2.5. And revisions of long-

run forecast growth trajectories raised the possibility that continued slack

demand was having a significant negative influence not just on short-run

output but on long-run growth, raising the possibility that premature fiscal

austerity was both reducing employment and production today and also

worsening long-term fiscal dilemmas if austerity reduced the denominator of

the debt-to-annual-GDP ratio by a greater fraction than it reduced the

numerator.

And that is where we stand today. In the context of central banks that believe

they lack the power and certainly lack the will to use non-standard

expansionary monetary policy to rapidly rebalance economies to attain full

employment and low inflation, expansionary fiscal policy thus acquires a

stabilization policy role. The question is how large a role. And that requires

assessing the benefits and the risks from expansionary fiscal policy.

IV. The Current Benefits of Expansionary Fiscal Policy, as

Undertaken by Credit-Worthy Sovereigns

Overview: It is important to focus on the problems of the OECD. The

problems are twofold: first, the presence of an extraordinary amount of

economic waste in the form of idle resources, both labor and capital; second,

the OECD economies are failing to prepare for the shift of resources into

larger old-age pensions and more medical care that the combination of

population aging and evolving technology will bring.

But, while it would be desirable to have a policy in place that would address

12

the second problem—and while policies in place to deal with the second

problem might pay dividends in terms of greater confidence and reduced

uncertainty —the second problem is not a current problem. It can be fixed

gradually over time in the future. The current gap between actual and

potential output, by contrast, represents a pure and tragic waste of productive

and human potential that cannot be undone if not fixed now. As long as

there is underutilized capacity, discretionary fiscal policy in the form of

temporary tax cuts and temporary increases in government spending, can

boost aggregate demand and help close the gap between actual and potential

output, provided there is no offsetting monetary policy response. According

to the Federal Reserve, this is the case in the US for the foreseeable future.

Under these circumstances, consistent with traditional Keynesian theory,

recent research confirms

9

that fiscal policy multipliers appear significantly

larger than in “normal” conditions when the economy is operating near

capacity, resources are tight, and monetary policy is not at or near the zero

interest rate bound.

Using a variety of statistical techniques, researchers have reached the

following conclusions about fiscal policy multipliers.

The size of multipliers is state-dependent and nonlinear: multipliers

vary over the business cycle, are significantly larger during downturns

than during expansions, and significantly larger overall than

previously thought.

10

The size of multipliers depends on what the current monetary policy

9

With the exception of Michael Owyang, Valerie Ramey, and Sarah Zubairy (2013),

“Are Government Spending Multipliers Greater During Periods of Slack? Evidence from

20th Century Historical Data” (Cambridge: NBER Working Paper 18769)

<http://goo.gl/cGh3P

>

10

See Alan J. Auerbach and Yuriy Gorodnichenko (2012) "Measuring the Output

Responses to Fiscal Policy," American Economic Journal: Economic Policy 4:2 (May),

pp. 1-27; Alan Auerbach and Yuriy Gorodnichenko (2013), “Fiscal Multipliers in

Recession and Expansion”, in Fiscal Policy after the Financial Crisis (Chicago:

University of Chicago Press) <http://www.nber.org/papers/w17447>; and Olivier

Blanchard and Daniel Leigh (2013), “Growth Forecast Errors and Fiscal Multipliers”

(Washington, DC: IMF Working Paper 13/1)

<http://www.imf.org/external/pubs/ft/wp/2013/wp1301.pdf>.

13

régime is.

11

When a government confronts borrowing constraints as a result of high

public debt, multipliers are smaller.

12

Multipliers are larger when private actors are credit-constrained. Under

these circumstances, consumption depends more on current income

than on expected future income and investment depends more on

current profits than on expected future profits.

13

Estimates of multipliers with credit-constrained hand-to-mouth

consumers are 50% larger than estimates under normal credit

conditions.

14

11

See J. Bradford DeLong and Lawrence H. Summers (2012), “Fiscal Policy in a

Depressed Economy”, Brookings Papers on Economic Activity 2012:1; J. Bradford

DeLong (2013), “The Full Fiscal Offset Principle”

<http://delong.typepad.com/sdj/2013/02/the-full-fiscal-offset-principle-away-from-the-

zero-lower-bound-that-is-or-why-one-would-expect-the-multiplier-to-be-zer.html>.

“Local Multiplier” studies, that examine disparate output responses to disparate fiscal

stimulus in sub-regions of a currency union—and that thus keep monetary and financial

conditions constant as the degree of fiscal impetus shifts—do show much larger

multipliers than do studies that do not control for how the central bank’s reaction function

leads monetary policy to shift as the fiscal impetus shifts. See Juan Carlos Suarez Serrato

and Philippe Wingender (2010), “Estimating Local Fiscal Multipliers” (Berkeley, CA:

U.C. Berkeley) <http://ceg.berkeley.edu/students_9_2583495006.pdf>; Gabriel

Chodorow-Reich et al. (2011), “Does State Fiscal Relief During Recessions Increase

Employment? Evidence from the American Recovery and Reinvestment Act” (Berkeley,

CA: U.C. Berkeley) <http://econgrads.berkeley.edu/gabecr/files/2011/05/Does-State-

Fiscal-Relief-During-Recessions-Increase-Employment-August-20114.pdf>; Brock

Mendel (2012), “The Local Multiplier: Theory and Evidence” (Cambridge, MA: Harvard

University); and many others.

12

See Giancarlo Corsetti, Andre Meier, and Gernot J. Müller (2012), “What Determines

Government Spending Multipliers?” (Washington DC: IMF Working Paper 12/150) <

http://www.imf.org/external/pubs/ft/wp/2012/wp12150.pdf>

13

See Giancarlo Corsetti, Andre Meier, and Gernot J. Müller (2012), “What Determines

Government Spending Multipliers?” (Washington DC: IMF Working Paper 12/150) <

http://www.imf.org/external/pubs/ft/wp/2012/wp12150.pdf>; Atif Mian and Amir Sufi

(2010), “Household Leverage and the Recession of 2007-09”, IMF Economic Review

58:1, pp. 74–117; Gauti Eggertsson and Paul Krugman (2012), “Debt, Deleveraging, and

the Liquidity Trap: A Fisher-Minsky-Koo Approach”, The Quarterly Journal of

Economics, 1469–1513. <http://qje.oxfordjournals.org/content/127/3/1469.full.pdf>.

14

See Atif Mian and Amir Sufi (2010), “Household Leverage and the Recession of 2007-

09”, IMF Economic Review 58:1, pp. 74–117.

14

Opinion is divided on the relative size of the multipliers for government

spending and for taxes. Keynesian models assume that the multipliers

for government spending are larger, and most macroeconomic models

of the US economy, including those used by the CBO and by private

forecasters are consistent with this assumption. But some academic

research indicates that the multipliers for tax policies are larger than

previously thought

15

and some preliminary research suggests that they

may be larger than the multipliers for government spending under

some circumstances.

16

The multipliers for changes in government spending vary for different

kinds of government spending.

The multipliers for changes in government taxes vary for different

kinds of taxes.

17

The size of the multiplier varies across countries, so fiscal policies

should be tailored to specific country conditions.

Multipliers are smaller in small, open economies than in large

economies.

Countries operating with fixed exchange rate systems have larger

multipliers than countries with flexible exchange rate systems.

Cross-border multiplier effects can be significant. Fiscal stimulus in

one country is likely to have economically and statistically significant

effects on output in countries with the effects depending on the

15

Mertens and Ravn (2013) “Reconciliation of SVAR and Narrative Estimates of Tax

Multipliers”

<http://www.economics.cornell.edu/km426/papers/Reconciliation_revision.pdf>

16

Alberto Alesina, Carlo Favero and Francesco Giavazzi (2012) "The Output Effect of

Fiscal Consolidations"

<http://didattica.unibocconi.it/mypage/upload/48751_20120830_023720_THEOUTPUT

OFFISCALCONSOLIDATIONS.PDF> and Andrew Jalil (2012) “Comparing Tax and

Spending Multipliers: It’s All About Controlling for Monetary Policy”

<http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2139855>

17

See Christina Romer et al. (2010), Economic Impact of the Recovery and Reinvestment

Act of 2009: Fourth Quarterly Report (Washington, DC: Government Printing Office).

15

intensity of trade between the countries and their overall openness to

trade. The strength of the spillovers also depends on the conditions in

the recipient country and the source country, with large multipliers

when both economies are in recessionary conditions.

Conventional Keynesian Multiplier Analysis: For the US, fiscal

multipliers appear to vary from near 0, complete crowding-out, in normal

circumstances to about 2.5 during recessions. Based on their own economic

models and the models of other public and private forecasters, the

Congressional Budget Office uses a broad range of multipliers that vary over

both business cycle conditions and types of fiscal measures.

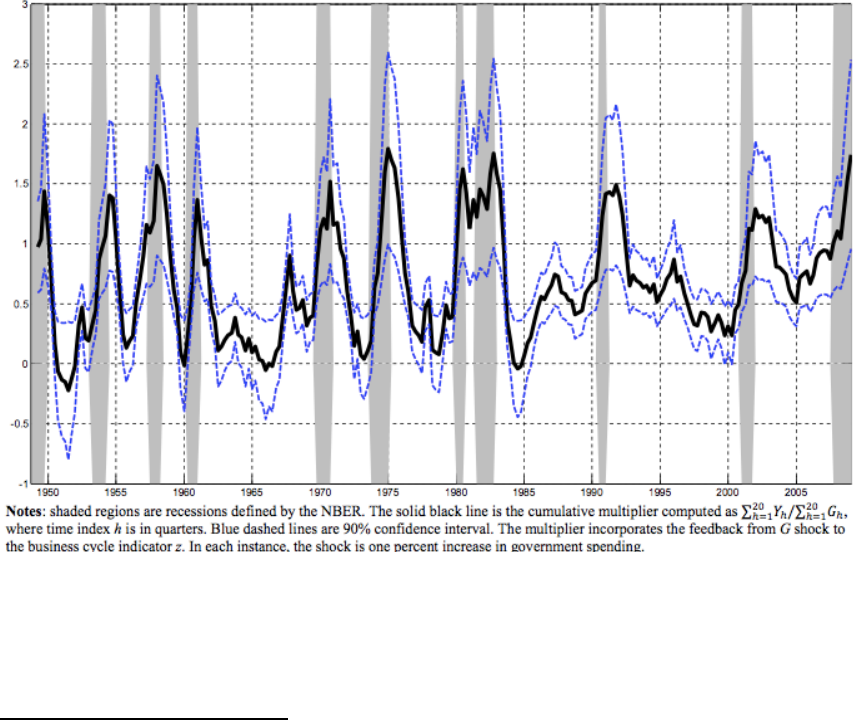

Figure 3: Auerbach and Gorodnichenko Time-Varying

Government Spending Multipliers

18

In its most recent publication assessing the effects of the 2009 economic

stimulus package (the ARRA bill), the CBO used the following range of

18

Source: Figure 5 of Alan J. Auerbach and Yuriy Gorodnichenko (2012) "Measuring the

Output Responses to Fiscal Policy," American Economic Journal: Economic Policy 4:2

(May), pp. 1-27.

16

multipliers for different components of the package. These multipliers show

the effects on output of a particular fiscal policy over four quarters, staring

the quarter in which the first direct effect on demand occurs in response to

that policy. The size of these multipliers is based on the assumption that

there was no monetary policy offset between 2009 and 2013. The CBO uses

a range for the size of multipliers and their effects on output and

employment to reflect differences in the size of multipliers from different

sources and based on different modeling techniques.

19

Under more normal conditions, when the economy is close to potential and

away from the zero nominal lower bound, the Federal Reserve attempts to

offset the effects of discretionary fiscal policy on aggregate demand. Then

both the low and the high ends of the range for multipliers used by the CBO

are about one-third smaller, reflecting the CBO assumption that roughly

two-thirds of the effects of discretionary fiscal policies on aggregate demand

are “crowded out” under normal economic conditions.

Within spending, direct government purchases of goods and services have

the largest multipliers. Both government consumption spending and

government investment spending have positive effects on output but the

multiplier for the latter is much stronger, especially so in normal conditions

when the multiplier for government consumption spending is considerably

lower.

Government investment spending on programs like infrastructure and

research boosts the economy’s potential growth and capacity both directly

and indirectly by encouraging complementary private investment. Although

the CBO notes that government investment spending offsets some of the

possible “crowding out” of private investment that results from an increase

in government debt in the future, the CBO does not include this effect in its

multiplier estimates. The CBO estimates that government investment

spending amounted to about 20%-25% of the 2009 stimulus.

20

In general, tax cuts and transfer payments appear most effective when aimed

19

Congressional Budget Office (2013), Estimated Impact of the American Recovery and

Reinvestment Act on Employment and Economic Output from October 2012 Through

December 2012 (Washington, DC: Government Printing Office); Congressional Budget

Office (2012), CBO’s Multipliers <http://goo.gl/2DqPw>.

20

Congressional Budget Office (2009), “H.R. 1: The American Reinvestment and

Recovery Act of 2009” <http://www.cbo.gov/publication/41756>

17

at households that have the highest marginal propensity to consume. Rising

income inequality is a problem facing the US and many other developed

countries. “Progressive” discretionary fiscal policies that are targeted

toward lower-income groups not only have larger multipliers but also

address this problem Tax cuts aimed at businesses should focus on

additional or marginal investment incentives. Changes in corporate taxes

that affect after-tax profits—like a cut in the corporate tax rate—have

smaller multipliers than changes in corporate taxes that affect after-tax-

returns to new investment—like a temporary investment tax credit. Increases

in disposable incomes, either through transfer payments or tax breaks, are

more likely to boost spending in lower-income households than in higher-

income households. New research in the US finds that tax cuts for lower

income groups have larger multipliers and larger effects on employment

than comparable changes for higher income groups.

21

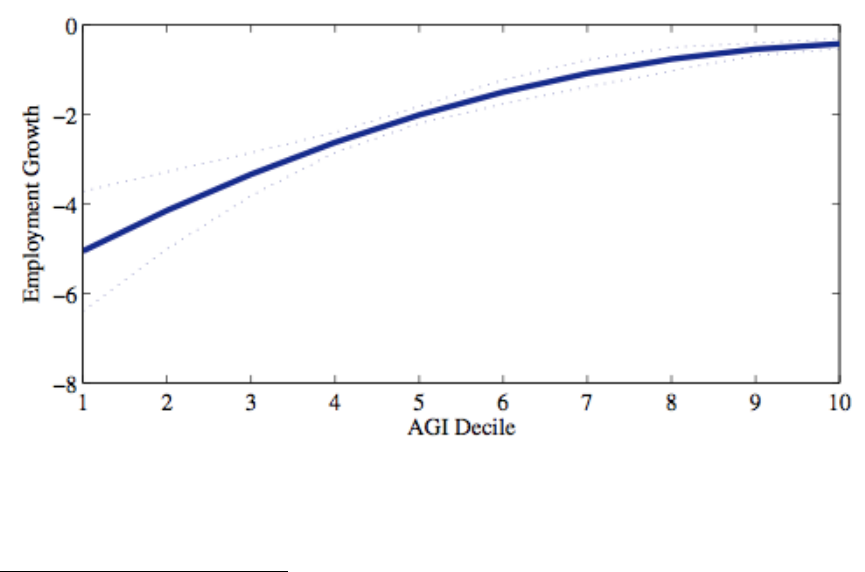

Figure 4: Zidar Estimates of Employment Effects of Stimulus

Ranked by AGI Decile

22

When the economy is operating far below potential and unemployment is

high, there is also a strong case for targeted fiscal measures to increase labor

21

Owen Zidar (2013), “Tax Cuts for Whom? Heterogeneous Effects of Income Tax

Changes on Growth & Employment”

<http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2112482>

22

Owen Zidar (2013), “Tax Cuts for Whom? Heterogeneous Effects of Income Tax

Changes on Growth & Employment”

<http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2112482>

18

demand. These measures include credits to small and medium sized

companies, tax credits for additions to payrolls, reductions in non-wage

labor costs and funds to support active labor market policies like job training

and assistance programs. The so-called “Jobs Package” proposed by

President Obama in the fall of 2010

23

as a second fiscal stimulus package

contained several targeted measures. Private forecasters estimated that this

package would boosted private job creation by 1 million jobs over two years,

but most of the package was not passed by the Congress. The temporary

employer payroll tax, which would have strengthened labor demand, was not

enacted and the temporary employee payroll tax, which was passed, affected

labor demand only indirectly through additional consumption spending.

In addition to focusing on particular income groups or particular goals like

infrastructure investment or labor demand, fiscal policy can also be targeted

to specific regions. Recent US research confirms that the multipliers for

federal spending in hard-hit states are considerably larger than economy-

wide multipliers and can deliver strong employment effects per dollar of

federal spending.

24

Compared to discretionary fiscal policy that can be targeted by income

group, by purpose and by region, discretionary monetary policy is a blunt

instrument. The low interest rate policy and the QE policies of the Federal

Reserve have been aimed at strengthening aggregate demand by keeping

long-term interest rates low and boosting the value of stocks and other

financial assets. These policies, however, have been criticized by some for

disproportionately benefitting high-income earners who own a large share of

these assets,

25

and by others for inducing banks and private investors to take

23

See Barack Obama (2010), “H. Doc. 112-53 - The ‘American Jobs Act of 2011’

Legislative Proposal” <http://www.gpo.gov/fdsys/pkg/CDOC-112hdoc53/content-

detail.html>

24

See Juan Carlos Suarez Serrato and Philippe Wingender (2010), “Estimating Local

Fiscal Multipliers” (Berkeley, CA: U.C. Berkeley)

<http://ceg.berkeley.edu/students_9_2583495006.pdf>; Gabriel Chodorow-Reich et al.

(2011), “Does State Fiscal Relief During Recessions Increase Employment? Evidence

from the American Recovery and Reinvestment Act” (Berkeley, CA: U.C. Berkeley)

<http://econgrads.berkeley.edu/gabecr/files/2011/05/Does-State-Fiscal-Relief-During-

Recessions-Increase-Employment-August-20114.pdf>.

25

See “Yves Smith” (2009-2013), “Naked Capitalism”

<http://www.nakedcapitalism.com>, passim.

19

on yet another round of poorly-understood and poorly-managed tail risk.

26

Safe Assets and Deleveraging Issues: As time passes and as the OECD

economies continue to remain with relative levels of activity and

employment far below normal, there has been increasing attention paid to

perspectives that argue that standard models are not serving analysis well.

Richard Koo has is a prominent and vocal critic of the relevance of these

models to current circumstances.

27

Neither standard monetarist models, with

their mechanical and predictable quantity-theoretic links between liquid

balances on the one hand and spending on the other, nor standard Keynes-

Wicksell savings-investment balance models with mechanical and

predictable propensity-to-spend links between income flows on the one hand

and spending on the other, appear to be capturing reality in an adequate

fashion.

Stepping back to the beginning of macroeconomics in 1829, we have John

Stuart Mill’s insight

28

that downward pressure on spending that pushed

production and employment below normal relative levels was driven by a

perceived shortage of financial assets: excess demand (at full employment)

for financial assets entailed, by what would become known as Walras’s Law,

led to excess supply (at full employment) of currently-produced goods,

services, and labor. To the extent that the excess demand for safe assets took

the form of excess demand for the liquid circulating medium, individuals

could add to their accumulations by simply cutting spending below

income—but while an individual could cut spending below income, the

community could not. Restoring normal activity required then the injection

of enough liquid money to balance demand and supply for liquidity at full

employment. This is the insight underpinning Irving Fisher’s original brand

26

See Jeremy Stein (2013), “Overheating in Credit Markets: Origins, Measurement, and

Policy Responses”

<http://www.federalreserve.gov/newsevents/speech/stein20130207a.htm>

27

See Richard Koo (2003), Balance-Sheet Recession: Japan's Struggle with Uncharted

Economics and its Global Implications (New York: John Wiley); Richard Koo (2009),

The Holy Grail of Macroeconomics: Lessons from Japan’s Great Recession (New York:

John Wiley); Richard Koo (2011), “Learning Wrong Lessons from the Crisis in Greece”

(New York: INET).

28

John Stuart Mill (1829, pub. 1844), “Of the Influence of Consumption on Production”,

Essays on Some Unsettled Questions in Political Economy (London: Longmans, Green).

20

of quantity-theoretic monetarism.

29

Similarly, should the shortage of supply for financial assets take the form of

a shortage of financial vehicles to convey wealth from the present to the

future—should, in Wicksellian

30

terms, ex ante savings be greater than

investment—individual savers will use liquid money as a proxy substitute

financial savings vehicle and so attempt to depress their spending (at full

employment) below their income. This requirement that supply and demand

for financial savings vehicles balance at full employment is, as Hicks (1937)

says, really “the [Keynesian] multiplier equation, which performs such queer

tricks.”

31

But as Koo argues, what if the problem is not a shortage relative to demand

at full employment of liquid money or of financial savings vehicles, but

rather a shortage of safe assets—or rather as assets perceived as safe?

Economic agents will be anxious to cut their spending below their income

and use extra cash as a proxy safe asset in order to boost the safe-asset

component of their portfolios, and will continue to do so until an extended

period of deleveraging has reduced risk and restored the economy’s relative

balance of assets between those perceived to be risky and those perceived to

be safe to what private savers require. This is the essence of a balance-sheet

recession, and neither expansionary monetary policy (to the extent that it

simply swaps the safe asset of cash for the safe asset of short-term

government securities) nor expansionary fiscal policy (unless it is conducted

on such a scale as not merely to affect income flows but rather the perceived

riskiness of the entire stock of financial assets) will have much effect.

In this framework, if it provides an insightful way of looking at the situation,

the source of the depressed condition of the OECD economy lies in (a) the

increased demand by wealthholders for the safe-asset component of their

portfolios coupled with (b) the disappearance of $8 trillion of private

structured products, mortgage-backed securities, and the ex-France ex-

Germany sovereign debt of the Eurozone from the category of assets

previously thought to be safe.

29

See Irving Fisher (2011), The Purchasing Power of Money (New York: Macmillan).

30

Knut Wicksell (1907), “The Influence of the Rate of Interest on Prices”, Economic

Journal 17.

31

John Hicks (1937), “Mr. Keynes and the ‘Classics’: A Suggested Interpretation”,

Econometrica 5:2 (April).

21

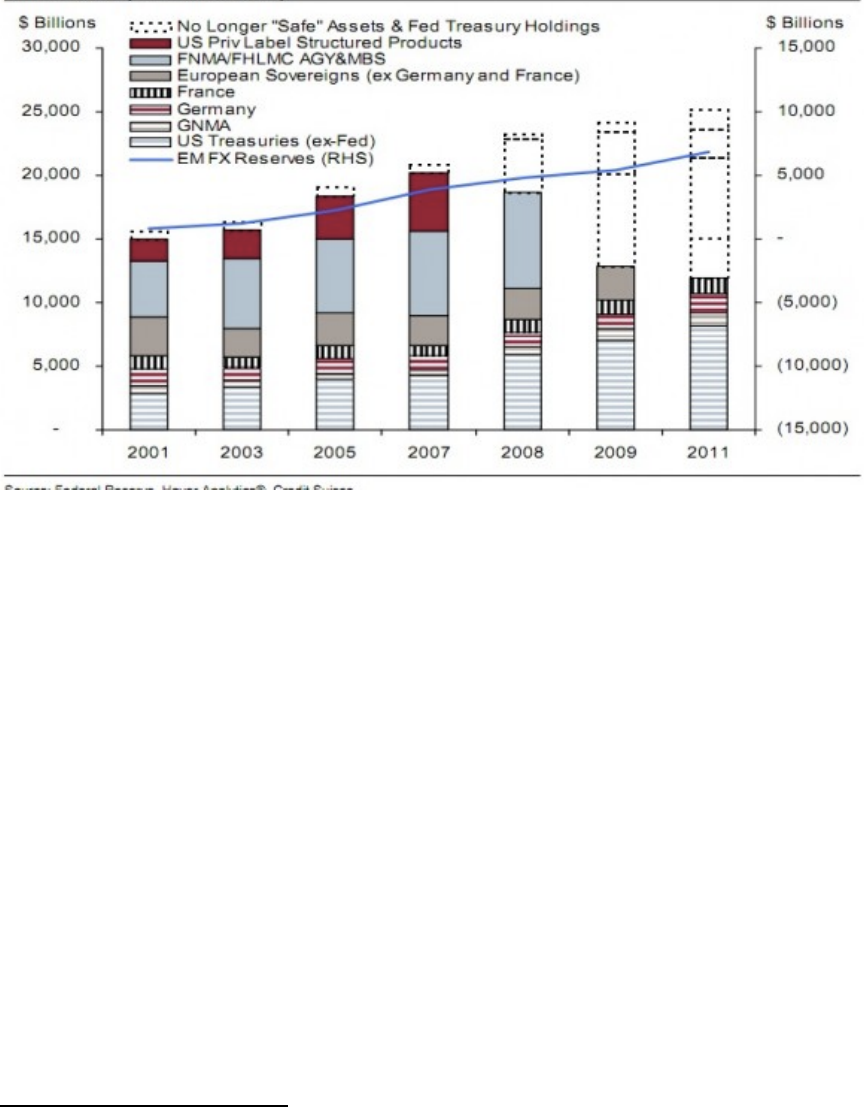

Figure 5: Credit Suisse Estimates of the Shrinking Universe of

Assets Perceived as Safe

32

Filling in this safe-assets gap via conventional bond issues would require

that credit-worthy sovereigns increase their debts relative to baseline by

some $10 trillion—and that they do so without cracking their own status as

issuers of assets perceived to be safe. The large required scale raises the

possibility that a better policy than expansionary fiscal policy would be for

credit-worthy sovereigns to focus on transforming private liabilities into safe

assets by taking on tail risk—through banking and credit market policies not

through fiscal policy.

Hysteresis: Longer-Run Benefits of Expansionary Fiscal Policy on

Output?: In recent testimonies and speeches, Fed Chair Ben Bernanke and

Vice-Chair Janet Yellen have warned that the longer the economy operates

below potential, with an elevated unemployment rate, the greater the danger

that a cyclical unemployment problem becomes a structural one. In

Bernanke’s words:

32

Cardiff Garcia (2011), “The Unwanted Mutant Offspring of the Most Important Chart

in the World”, FT Alphaville <http://ftalphaville.ft.com/2011/07/15/623881/the-aaa-

bubble/>

22

High unemployment has substantial costs, including not only the hardship

faced by the unemployed and their families, but also the harm done to the

vitality and productive potential of the economy as a whole.

In Yellen’s words, the persistence of long-term unemployment—which is

40% of total unemployment—is of “great concern” because individuals out

of work for extended periods become less employable as their skills erode

and their attachment to the labor force weakens. Even when the economy

recovers to capacity, these workers may not be able or willing to find jobs.

In the United States, the aging of the baby-boom generation and growing

wealth currently impart a slow downward trend of between 0.1 and 0.2

percentage points per year to the labor-force participation rate. The business

cycle also imposes its imprint on participation: when the employment-to-

population ratio falls by 0.3 percentage points relative to trend, the labor

force participation rate falls by 0.1 percentage point. The collapse of

retirement savings in 2008-9 with declines in asset values and housing

equity, however, was a countervailing force working to postpone retirement

and raise labor-force participation. These factors would lead an observer to

anticipate that today the U.S. labor-force participation rate would be roughly

65%. But it is lower: 63.5%,

33

lower than at any time since the 1970s, before

the feminist revolution had opened American female employment

opportunities. Even with a constant labor-force participation rate, and even

with strongly impaired balance sheets leading households to postpone

retirement, labor-force participation in the United States has been falling

since 2009 at 0.5 percentage points per year.

How much of this decline will be reversed when the economy normalizes?

How much of it reflects a permanent transformation of what was cyclical

into structural unemployment?

34

Such concerns reflect a broader concern that the longer the economy

operates far below its capacity, the slower the growth of its future capacity

as a result of the erosion of worker skills, foregone investment, and

33

63.3% as of the March 2013 CPS survey week.

34

Attempts to find any non-cyclical cause of the acceleration in the decline in labor-force

participation have been strikingly unsuccessful. See Robert Moffitt (2012), “The U.S.

Employment-Population Reversal in the 2000s: Facts and Explanations”, Brookings

Papers on Economic Activity 2012:2 <http://ideas.repec.org/p/nbr/nberwo/18520.html>

23

diminished risk taking and entrepreneurship. As the recovery continues to

be slow and partial, the CBO and other forecasters have been sharply

revising downward their estimates of the long-run growth potential of the

U.S. economy,

35

concluding that the financial crash, the recession, and slow

recovery have significantly reduced this potential. Private investment

plummeted to new lows as a share of GDP during the recession. It had yet to

recover to its previous peak. Also sharply off is the rate of new business

formation. In his typical colorful language, John Maynard Keynes warned

that a time of unutilized resources was one strongly unfavorable to creative

destruction, entrepreneurship, and growth: “ the game of hazard which the

entrepreneur plays is [then] furnished with many zeroes…”

36

How large is the effect of a persistent output gap on future potential output

and growth? DeLong and Summers draw on the work of Oulton and

Sebastia-Barriel, and note that with even a modest “hysteresis coefficient” of

well below 0.2, the long-term real government borrowing rate is sufficiently

low that each additional dollar of discretionary fiscal spending more than

pays for itself, as the combination of low US Treasury borrowing rates,

positive fiscal multiplier effects, and modest hysteresis effects renders fiscal

expansion self-financing. Under these conditions, it is austerity right now

rather than fiscal expansion that threatens to raise the long-run debt-to-

annual-GDP ratio by lowering its denominator by more than it lowers its

numerator.

37

V. Costs and Risks of Discretionary Fiscal Policy

In the wake of the 2008 financial crisis, and the resulting deep recession and

slow recovery, government debt in the US and other advanced industrial

35

See J. Bradford DeLong and Lawrence H. Summers (2012), “Fiscal Policy in a

Depressed Economy”, Brookings Papers on Economic Activity 2012:1. They argue that

the pattern of forecast revisions by the consensus of forecasters appears to take a one year

output gap maintained for one year to be a associated with a long-run decline in potential

output of 0.2 percentage points,. There is not enough information in the Post-World War

II data sample for any econometric estimation to be convincing.

36

See John Maynard Keynes (1936), The General Theory of Employment, Interest and

Money (London: Macmillan), ch. 24.

37

Nicholas Oulton and María Sebastiá-Barriel (2013), “Long and Short-Term Effects of

the Financial Crisis on Labour Productivity, Capital and Output” (London: Bank of

England Working Paper 470)

<http://www.bankofengland.co.uk/publications/Documents/workingpapers/wp470.pdf>

24

countries has increased sharply. The dramatic increase in the debt to GDP

ratios in the developed countries is consistent with previous financial crises

after which public sector debt soars as government revenues contract and

government spending increases to offset the collapse of private sector

demand and to stabilize the financial sector often by absorbing private sector

losses.

The surge of public debt since 2007 has triggered concerns about the risks

associated with high levels of public debt. There appear to be four distinct

risks:

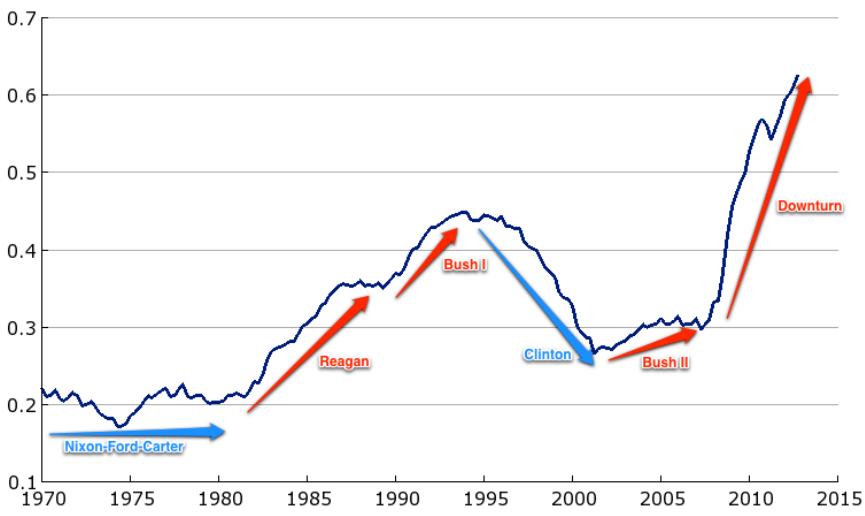

Figure 6: The Course of U.S. Debt Held by the Public to Annual

GDP

First, large and rising government debt weakens market confidence in the

creditworthiness of sovereign borrowers and heightens the risk of financial

crises emanating in the markets for public sector debt. History shows,

however, that most large financial crises begin in the private sector not the

public sector. Over time, it appears that private sector credit booms and the

resulting buildup of private sector debts, not excessive government spending

and the buildup of public sector debts, pose the main risk to financial

25

stability in advanced industrial countries.

38

Second, when the output gap has closed and economies are operating at their

potential levels, government debt crowds out private debt and private

investment. This in turn reduces the private capital stock and the economy’s

productivity growth and wage growth. The main macroeconomic channel

through which crowding out occurs is an increase in both short-term and

long-term interest rates, as private sector borrowing competes with public

sector borrowing for scarce capital and as central banks adjust short-term

interest rates to contain inflation and offset expansionary fiscal policies.

Crowding out also occurs through other channels such as an increase in

taxes that may be necessary to provide the government with revenues to

service its debt and cover its other spending commitments. Additional taxes

impose deadweight losses on the economy and the composition of these

taxes can have additional crowding-out effects on incentives for saving,

investment and labor.

Third, large and rising public debt creates uncertainties about the course of

future fiscal policies that could undermine private sector confidence and

spending. Expected increases in future tax rates, for example, could

discourage investment and weaken worker incentives. The uncertainty

argument is a variant of the “crowding out” argument, allowing for the

possibility that the expectations of future policy changes necessitated by a

high and rising public debt “crowd out” private sector spending long before

the economy is operating at capacity and reduce the economy’s future

potential growth rate.

There is no evidence of the “uncertainty crowding out” effects in the interest

rates or other financial market indicators in the US and many other

developed countries with large and rising public debt to GDP ratios. Indeed,

recent evidence points in the opposite direction, with a negative correlation

between near-term growth and CDS spreads on public debt. In some

countries, large deficit reduction or fiscal consolidation packages adopted to

boost market confidence have aggravated market concerns about slow

growth and led to increased spreads on government debt.

39

38

See Jorda, Schularick, & Taylor (2013), “Sovereigns versus Banks: Credit, Crises,

and Consequences”

39

Carlo Cottarelli and Laura Jaramillo (2012), “Walking Hand in Hand: Fiscal Policy

and Growth in Advanced Economies” (Washington, DC: IMF Working Paper 12/137

<http://www.imf.org/external/pubs/ft/wp/2012/wp12137.pdf>

26

Fourth, large and rising public debt reduces budgetary flexibility or the

“fiscal space” for governments to deal with unexpected adverse shocks or

emergencies, and to finance spending on desired goals without jeopardizing

fiscal sustainability or economic stability in the future.

The most analyzed and quantifiable of these four risks is the traditional

crowding-out risk. It is also the one on which most economists agree. But

since the US and most other advanced industrial countries with high and

rising public debt burdens are still far from capacity, there is little sign of

crowding out effects, or uncertainty/confidence effects, in interest rates—

which are the major channel through which they operate. Chairman

Bernanke (2013) recently pointed out that long-term interest rates have been

falling, not rising, in the US, the UK, Japan, Germany and Canada. All of

these countries had high and rising debt to GDP ratios between 2009 and the

end of 2012, yet long-term interest rates declined both in nominal and in real

terms along similar paths, with highly correlated movements during this

period.

40

Moreover, these rates are now at or near all-time lows of around 2% in

nominal terms and about 0% in real terms despite public debt to GDP ratios

that are at peacetime highs.

Why are long-term interest rates so low? Why do investors appear to be

unconcerned about the public debt trends in these countries? The answer is

that markets expect slow growth and low returns to investment for the next

decade, as a result of both the slow cyclical recovery and the resulting

slowdown in future potential growth rates. Consistent with this slow growth

expectation, markets anticipate that inflation will remain subdued and that

central banks will continue to keep short-term nominal interest rates at very

low levels. Under these conditions, markets believe that the crowding out

risks of high government debt during the next decade will remain low for the

foreseeable future.

41

40

Ben Bernanke (2013), “Long-Term Interest Rates” (Washington DC: Federal Reserve)

<http://www.federalreserve.gov/newsevents/speech/bernanke20130301a.htm>

41

Standard quadratic yield-curve estimation predicts that if the U.S. Treasury issued a

consol, it would currently carry a nominal coupon of 3.5%/year. The thirty-year inflation-

protected TIPS currently has the same duration as a nominal consol would: its real yield

is 0.56%/year. Since one of these securities is non-existent—hence present in zero

volume—and the other is a small part of the debt, these interest rates speak to market

27

What of the risks that interest rates will normalize or super normalize in the

near future and impose high costs. Recently, Martin Feldstein

42

argued that

the model scenario involves a 3 percentage point rise in real Treasury yields

over the next five years, with a consequent unhedged 31% loss on ten-year

Treasuries and on those other portions of their portfolios with equivalent

duration. While individual firms can hedge this risk, the economy as a whole

cannot—and the past six years have not impressed anybody with the ability

of highly-leveraged money-center banks to find clients who understand and

can afford to bear such risks.

43

Whether even the money-center banks can

know whether their capital is large enough to absorb their share of such

losses is something that would require that banks have greater understanding

and control of their derivatives books than they have in the past. And as

Treasury debt continues to mount, banks’ exposure to interest rate risk is

likely to mount as well.

That being said, a more common perspective than Feldstein’s is the belief

that a super-normalization of interest rates in the near-term is very unlikely.

As Carmen Reinhart and Belen Sbrancia point out,

44

OECD governments

have enormous regulatory tools to force their banking sectors to hold

government debt on whatever terms governments wish—and governments

have never been shy about using such tools. Should the interest rate

environment change, the probable future would involve not spiking interest

rates and rapidly accumulating public debt but rather “financial repression”

of some form.

That future of “financial repression”, however, should it come to pass, might

well be one in which debt accumulation imposes substantial costs in terms of

reduced economic growth. Several recent studies have found a negative

forecasts of risk-neutral interest rate expectations and not to market fears or to the cost of

downside risks.

42

Martin Feldstein (2013), “When Interest Rates Rise”, Project Syndicate

<http://www.project-syndicate.org/commentary/higher-interest-rates-and-financial-

stability-by-martin-feldstein>

43

As current UBS Chair Axel Weber said: “while [a bank’s] treasury department was

reporting that it bought all these high-yielding products, its credit department was

reporting that it had securitized and sold off all its risk.”

44

See Carmen M. Reinhart M. Belen Sbrancia (2011), The Liquidation of Government

Debt” (Cambridge: NBER Working Paper 16893)

<http://www.imf.org/external/np/seminars/eng/2011/res2/pdf/crbs.pdf>

28

relationship between public debt to GDP ratios and economic growth.

45

These studies establish correlation, not causality, between high and rising

debt to GDP ratios and actual or potential economic growth. Some of these

studies identify a threshold value for the debt to GDP ratio of 80%-90%

beyond which higher ratios have a significant effect on growth.

46

Crowding

out of private investment and future productivity growth is the major

channel through which higher debt is presumed to impede growth. Italy and

Japan, with debt to GDP ratios beyond these thresholds and with slow

productivity growth, are often cited as examples of the deleterious effects of

sustained crowding out over time.

Since the publication of the Reinhart and Rogoff results, politicians and

policy makers in many countries have focused on the 90% threshold, and

have suggested that 90% is a tipping point beyond which economic growth

falls sharply or the odds of a sovereign debt crisis rise dramatically.

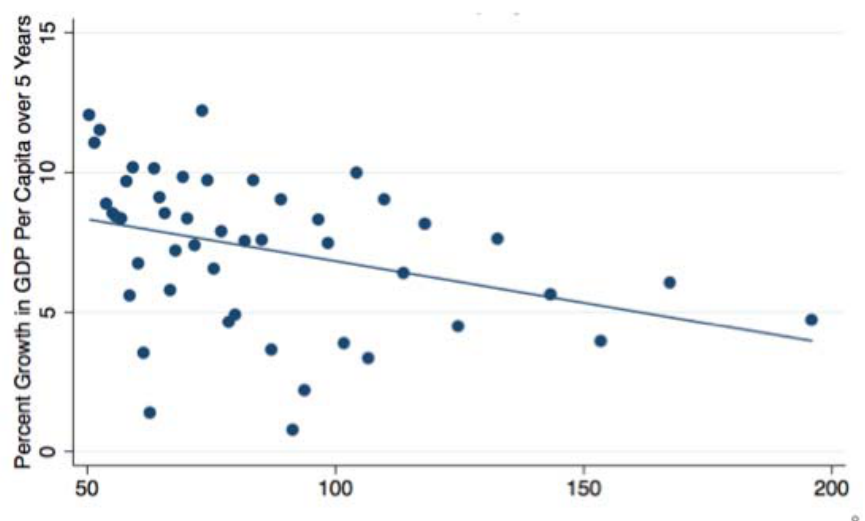

We question whether the Reinhart-Rogoff data support a tipping point

interpretation. We find that countries with public debt-to-annual-GDP ratios

over 90% for a five-year period do indeed grow less rapidly in per capita

GDP terms over the next five years. Consistent with Kumar and Woo

(2010), there is no sign of a threshold break at 90%.

Interpreting this correlation is not straightforward. Surely cases in which

high debt accumulation does lead to substantially-elevated interest rates are

ones in which we would expect growth to slow, but that tells us little about

45

See Manmohan S. Kumar and Jaejoon Woo (2010), “Public Debt and Growth”

(Washington DC: IMF Working Paper 10/174)

<http://www.imf.org/external/pubs/ft/wp/2010/wp10174.pdf>; Carmen Reinhart and

Kenneth Rogoff (2010), “Growth in a Time of Debt” (Cambridge, MA: NBER Working

Paper No. 15639 <http://www.nber.org/papers/w15639>; Carmen Reinhart, Vincent

Reinhart, and Kenneth Rogoff (2012), “Debt Overhangs, Past and Present” (Cambridge,

MA: NBER Working Paper No. 18015 <http://www.nber.org/papers/w18015>; Cristina

Checherita and Philipp Rother (2010), “The Impact of High and Growing Government

Debt on Economic Growth: An Empirical Investigation for the Euro Area” (ECB

Working Paper 1237); and Stephen G Cecchetti, M S Mohanty and Fabrizio Zampolli

(2011), “The Real Effects of Debt” <http://www.bis.org/publ/othp16.pdf>.

46

Some, however, argue that the threshold is considerably higher. See Alexandru Minea

and Antoine Parent (2012), “Is High Public Debt Always Harmful to Economic Growth?

Reinhart and Rogoff and Some Complex Nonlinearities” (Paris: Association Francaise de

Cliometrie Working Paper 8) <http://www.cliometrie.org/images/wp/AFC_WP_08-

2012.pdf>

29

the consequences of high debt-to-annual-GDP accompanied by low interest

rates. Moreover, the debt-to-annual-GDP ratio has both a numerator and a

denominator: it can be elevated either by rapid debt accumulation or slow

past growth, and we would expect slow past growth to forecast slow future

growth as well. The effects are modest: raising debt-to-annual-GDP from

50% to 150% is associated with a growth reduction on the order of 0.6

percentage points per year. Controlling for country effects reduces the

estimated magnitude of the effect on growth by more than half. Such a post-

crisis growth-rate reduction is not obviously a cost that overwhelms the

benefits of restoring normal employment and output levels more rapidly, if

expansionary fiscal policies are indeed able to do so.

Figure 7: Public Debt Burdens and Subsequent Growth: No

Threshold Effect

Federal Reserve Chair Ben Bernanke recently summarized the evidence as

indicating that:

Neither experience nor economic theory clearly indicates the threshold at

which government debt begins to endanger prosperity and economic

stability.

We agree. The question of whether and how much growth reduction is

30

entailed in the future by rapid debt accumulation now is one that is

absolutely key to making good policy, and yet one that is very poorly

understood by economists. This time, it really is different: more research is

definitely necessary.

VI. Policy Challenges and Tradeoffs

Policy makers face tough decisions in difficult and uncharted circumstances.

With low inflation, interest rates at zero lower bound, a promise of

continued monetary accommodation, and low and stable inflationary

expectations, there is a strong case for additional expansionary discretionary

fiscal policies to strengthen the recovery in countries like the US whose

governments can borrow at or near historically low long-term interest rates.

The possibility that the slow recovery will depress future potential output

growth through hysteresis effects makes the case even more compelling,

particularly for additional government investment spending on infrastructure

and research and on targeted policies to strengthen the skills of the

workforce.

But there are risks—albeit shadowy and poorly-understood ones

The US and other creditworthy countries must also confront the long-run

dangers and costs of elevated and rising public debt levels. The policy

challenge is to get the balance right. More discretionary fiscal support now

means a stronger recovery, given the large multipliers that exist under

current conditions, but a larger government debt and its attendant risks in the

future. More deficit reduction now would curb the growth of government

debt, but would slow the pace of recovery.

US policymakers right now are erring right now on the side of too much

fiscal contraction now and too little planning for long-term budget balance.

Federal Reserve Chair Bernanke has warned that monetary policy “cannot

carry the burden of ensuring a speedier recovery to economic health.” In a

recent speech William Dudley, the President of the Federal Reserve Bank of

New York, warned that “ We have the opposite of what we need now”—too

much fiscal retrenchment now, without a credible plan to stabilize and

reduce the debt to GDP ratio in the long term. As a result of recent fiscal

actions, fiscal drag will be about 1.34% of GDP in 2013. Federal Reserve

31

Vice Cahir Janet Yellen has pointed out that while recoveries from previous

postwar recessions in the US have been aided by expansionary discretionary

fiscal policy, the current recovery from the longest and deepest recession

since the Great Depression has been slowed by fiscal austerity. In the

meantime, as a result of deep political and ideological divisions about the

size and the purpose of government, US policymakers have not agreed on

any long-term plan that grapples with the major drivers of the long-term debt

problem: the aging of the population, the rising per capita cost of health care

and insufficient revenues.

As a result of the excessively front-loaded fiscal measures already taken, the

debt to GDP ratio in the US should stabilize at around 75% over the next

decade. Soon thereafter, however, the debt to GDP ratio will start to climb

again to unsustainable levels.

The prudent course for the U.S. at least, therefore, appears to be to, as long

as asset prices maintain their current configuration, postpone deficit

reduction and in fact to seek to pull spending forward in time from the future

into the underemployed present, while pushing taxes back in time from the

present into the presumably fully-employed future, all the while continuing

to call for the adoption of long-term plans to properly fund the social

insurance state.

But such a policy program may require sudden adjustment should interest

rates spike, should financial repression policies prove suddenly necessary, or

should more and better information emerge about the long-run costs of debt

accumulation. And a political system that cannot get its act together to plan

for fiscal balance over the long-run future is unlikely to be able to response

in order to reorient policy quickly should any of the risks involved in

policies that entail rapid debt accumulation in the present be presented, and

when these bills are presented it may well come as a substantial surprise.