HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-1

7.1 INTRODUCTION

This chapter applies to ownership transfers or sales [7 CFR 3560.406] of all or a

controlling interest in the project ownership.

During the term of a Rural Development (RD) loan, borrowers may determine that it is

in their best interest to transfer a project to another owner. Transfer of any RD project

requires RD’s prior approval. RD may approve a project transfer [7 CFR 3560.406 (b)] if that

project continues to further the objectives of the program, if the transaction is in the best

interest of Government and the tenants, and if RD’s security is protected.

The Agency's Transfer Application Process (TAP) strives to balance the needs of RD

and its customers. This chapter elaborates on Agency policies and defines thresholds to

accomplish this goal. The Agency review process relies on accurate information being timely

provided from all parties. This chapter outlines the requirements for project transfers and RD’s

procedures for reviewing and approving those transfers.

The programs covered by this Chapter and authorized by Title V of the Housing Act

of 1949 are as follows:

1. Section 515 Rural Rental Housing (RRH) that includes congregate housing, group

homes, and Rural Cooperative Housing as defined in §3560.11; and

2. Section 514 Farm Labor Housing (FLH) loans and Section 516 FLH grants for

farm-worker housing.

A transferee must meet the eligibility requirements found in HB-1-3560 for the

respective loan program type (RRH or FLH) as defined in 7 CFR§3560.55 and §3560.555,

including possessing the financial capacity and management experience to successfully own and

manage the project. After a transfer is authorized, the property should be financially and

operationally sustainable for the remaining term of the RD funding. The property should

provide adequate, affordable, decent, safe, and sanitary rental units for very low-, low-, and

moderate-income households in rural areas.

To protect RD’s security interests in a transfer, the RD underwriter must perform the

evaluations outlined in this chapter, taking into account the requirements in Chapters 4 and 5

of HB-1-3560 and considering the impact of the transaction on the tenants. While transfers

offer an opportunity to improve the quality of housing through improved maintenance,

rehabilitation, and/or better management, if not properly scrutinized, a transfer may increase the

risk of loan default or poorer housing conditions.

For purposes of this chapter, the term applicant, transferee, or purchaser is used to refer

to the entity that wishes to acquire the property, and borrower, transferor, or seller refers to the

current borrower, or the entity transferring the property.

For additional guidance on loan restructuring, see Chapter 11 of this Handbook. For a

list of documents to be submitted when requesting RD approval of a transfer, see Attachment

7-B-1, Transfer Application Documents.

CHAPTER 7: TRANSFER OF OWNERSHIP

7 CFR 3560.406

HB-3-3560

This page is intentionally left blank

7-2

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-3

SECTION 1: OVERVIEW

7.2 RD OBJECTIVES AND GUIDING PRINCIPLES

A.

Objectives

The key objective of this chapter is to ensure RD Multi-Family Housing (MFH)

projects continue to meet long-term program goals stated below by maintaining the

affordability of needed rental housing in rural areas. This chapter guides the Loan

Servicer/underwriter and the applicant in evaluating transfer requests to ensure the transaction

meets the best interests of the Government and the tenants by:

1. Improving and maintaining the long-term physical and financial viability of the

property;

2. Improving or maintaining the affordability of the property for RD-eligible tenants

and applicants;

3. Completing the transaction in a timely and efficient manner; and

4. Providing a framework for the timely and consistent review of the applicant’s

submission subject to the applicable program and statutory requirements.

B.

Responsibilities

RD relies on the ability of underwriter and loan originator (hereinafter used

interchangeably and in those cases they may be designated as a MFH specialist and may

further serve as the loan servicer) to complete the basic eligibility determinations concerning

both the applicant/borrower and the project to ensure the transaction complies with the

respective MFH program authorities described in current RD Handbooks, Code of Federal

Regulations (CFR), and statutory authorities. It is RD’s responsibility to fully evaluate the

proposal and determine when the transaction meets applicable Agency administrative and

program requirements. In those cases where the RD underwriter and RD loan servicer are

two different individuals, they will jointly be involved in processing the loan transfer and

share accountability for successfully completing the transfer by fulfilling the actions

described in this Chapter. All transfers and Multi-Family Housing Preservation and

Revitalization (MPR) Transactions must be in the best interests of the Government and

tenants. These transactions must demonstrate the extended viability/sustainability of the

project, the likelihood of full repayment under the terms being offered, and the probability of

providing and maintaining quality affordable housing over the long-term.

The Applicant is responsible for providing complete, timely and accurate information

and documentation throughout the transfer process to comply with all of the applicable

program policies, procedures, and regulations. The Loan Servicer is typically the initial point of

contract when a borrower decides to transfer their property and will determine if the transfer meets

these objectives subject to the applicable program and statutory requirements. If a transfer

does not meet each of these objectives, the Loan Servicer should work with the purchaser and

the seller in an effort to resolve issues of concern within the respective program limitations. If

the applicant contacts the RD underwriter who is not also the designated loan servicer, the

underwriter will inform the servicer and initiate the cooperative effort necessary to comply

HB-3-3560

with the process described in this Chapter. It is not RD’s role to assume any responsibility for

the individual business decisions of the borrower or applicant in ultimately determining the

course of action they propose. RD does not negotiate the terms of the transaction that are

between the buyer and seller.

C.

Guiding Principles

Agency underwriters will use the currently available underwriting analysis and guides

available at the RD intranet (SharePoint) https://mfhdemoteam.sc.egov.usda.gov/

ProgTracking/ default.aspx to document their MFH transfer and MPR decisions. Applicants

and borrowers may access these forms through the appropriate RD public websites

(http://www.rd.usda.gov/programs-services/multi-family-housing-direct-loans or

http://www.rd.usda.gov/programs-services/housing-preservation-revitalization-

demonstration-loans-grants).

The key parties to the transfer include the Seller, the Purchaser, the Agency (on behalf

of the tenants and as mortgagor), and any third-party funders (other lenders, tax credit

agencies, syndicators/investors, etc.). The different parties may have competing or

conflicting requirements, needs, and/or objectives and goals that must be recognized and

addressed early in the transfer process. RD is not responsible for reconciling conflicts

between buyers, seller or any other interested third parties. RD may, within its policy

constraints and to protect the interest of the Government and the tenants, offer alternatives for

conflict resolution.

An initial or preliminary conceptual meeting with the RD loan servicer, Seller, and

Purchaser should be arranged as early in the process as possible to evaluate the potential

suitability of the proposed transfer and formulate a mutually acceptable schedule for RD's

internal program analysis. This meeting can also identify potential problems or issues early in

the process that will need to be addressed before completing the transfer application.

When initiating the conceptual discussion, RD should recommend to applicants the

use of RD’s optional Preliminary Assessment Tool (PAT) or a suitable preliminary

assessment tool alternative offered by other parties, as a starting point to explore the

feasibility of the transaction. Using the PAT encourages all interested parties to contact the

RD servicing office as early as possible to discuss program requirements and conditions. The

PAT contains general instructions, basic underwriting thresholds and pertinent tips for RD

customers and staff to assist in preparing and evaluating proposals. The tool incorporates the

detailed instructions found in the applicable RD Handbooks, CFR, and other applicable

Agency and Departmental regulations. Additional instructions and suggestions are available

internally for Agency underwriters through the Agency SharePoint by drilling down to their

specific needs.

The RD website (http://www.rd.usda.gov/programs-services/multi-family-housing-

direct-loans) includes the PAT along with many of the other tools and additional program

information.

Using the information provided by the applicant, Loan Servicers should assess whether

the transfer request is consistent with the following guiding principles:

1. There is a continuing need for the property in the community. This should be

considered in lieu of prepayment of any existing RD direct loan MFH properties.

2. When the transaction is complete, the property will be in the hands of eligible

owners.

7-4

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-5

3. The transaction will address the immediate and long-term physical needs,

including accessibility issues identified in a Transition Plan as well as any other

fair housing requirements, and other needs of the property.

4. Any increased post-transaction rents will not displace existing tenants otherwise

meeting the RD eligibility requirements for continued occupancy.

5. Post-transaction basic rents will not exceed the lesser of conventional rents for

comparable units (CRCU), or the restricted rents as defined below in Paragraph D

1, unless an exception is allowed by the Agency. Low Income Housing Tax

Credits (LIHTC) rents are differentiated from CRCU and other restricted rents that

may be imposed by the applicant’s participation in other funding sources such as

HOME or individual State Housing Assistance programs. See Paragraph 7.7 B.

6. Any equity amount recognized by RD will be supported by a market value

appraisal meeting RD appraisal acceptability and underwriting requirements.

7. The RD-recognized Seller's Equity will consider the Market Value reflected in the

RD-approved appraisal (See Paragraph 7.7 B) less the unpaid balance of the

outstanding RD Loans on the Property and any other amortizing debt or other real

estate secured liens outstanding at the time of transfer as determined appropriate

by the Agency. If any new loans will be placed on the property at the time of

transfer that will cause the total real estate debt to exceed the RD security value,

an exception may be made for payment of a Seller’s Equity on a case-by-case

basis with RD Headquarters (HQ) Multi-Family Housing Preservation and Direct

Loan Division (PDLD) approval.

8. An Exit Incentive (EI) can be paid to the Seller if the following tests are met:

a. The present RD-accepted market value appraisal does not indicate any equity

exists in the property as is;

b. All threshold items in Paragraph 7.2 C of this handbook are met;

c. The total amount paid as EI is available from tax credits or other soft dollars

(RD funds will not be used to fund EI);

d. All New Loans are used for eligible RD MFH program purposes; and

e. All RD Direct Loans together with any RD authorized senior or superior debt,

such as may be incurred when the RD direct loans have been subordinated or

were previously issued in a junior lien position, post transfer will be less than

the Security Value determined by RD.

9. The Seller’s Equity and any EI may not both be paid on the same transfer. When

an EI is proposed, the RD HQ must review the PAT before RD issues a letter of

support for the buyer to obtain tax credits. RD must also review the settlement

statement pre- and post-closing to verify the amounts that may ultimately be

released at closing, and confirm no more than the amount authorized has been

allowed.

10. The PDLD concurs with the equity loan amounts and the new Return-To-Owner

(RTO) being authorized when it exceeds the seller’s originally authorized return,

and coordinates the approval of all waivers for unique and non-recurring

HB-3-3560

7-6

circumstances that fall outside of the normal transaction principles, RD HQ

approvals, or revitalization-related policy issues.

11. RD encourages the use of third-party resources to secure adequate funding to

successfully complete transfers and associated revitalization efforts. Such

resources include Low Income Housing Tax Credits (LIHTC), grants, and

participating lenders adhering to established RD MFH policies and programs,

including Section 538, Guaranteed Rural Rental Housing (GRRH) loans. Lenders

include Federally-regulated and insured institutions; State-regulated, chartered,

and insured institutions; and other national, state, regional, or local governmental

agencies specifically authorized to make loans and/or grants for multi-family

housing purposes authorized under the authorities accorded to USDA.

12. Post-transaction basic rents will not exceed the lesser of Conventional Rents for

Conventional Units (CRCU) or the restricted rents as defined below in Paragraph

C 1, unless an exception is allowable or the rents are 100 percent Project-Based

Section 8 with evidence from HUD that the current rents will be carried forward to

the new borrower without anticipating any reduction for the remaining term of the

Housing Assistance Payments Contract (HAP) contract. See Paragraph 7.7 B.

13. Each transfer will result in computation of a new Return-to-Owner (RTO) for the

new owner. Currently the RD RRH program allows the project owner to

potentially earn its maximum return based on original loan terms and/or prior

modification authorized by the Agency. A new RTO will replace the previous

owner's return amount in underwriting and future operating budgets for the longest

remaining term of any RD direct MFH loan on the property assumed, incurred or

modified as part of the transfer transaction.

For transfers, the following conditions are considered in determining when any

tax-credit equity, projected-deferred developer fees, or other program adjustments

will be used to establish the maximum total RTO the new owner may be allowed:

a. Rehabilitation costs eligible for the RD Section 515 Program purposes less all

outstanding and new RD direct loans, together with any RD authorized senior

or superior debt such as may be incurred when the RD direct loans have been

subordinated or were previously issued in a junior lien position must not exceed

the RD-determined Security Value;

b. The new maximum projected RTO at the time of transfer approval based on the

Agency underwriting analysis of Net Operating Income (NOI) less debt service

for all loans (without agency debt deferral);

c. NOI for payment of RTO should provide for the Debt Service Coverage Ratio

(DSCR) of 1.15 (when RD-recognized new equity has been provided), and will

be based upon the projected post-rehabilitation operating budget with rents not

exceeding the lesser of CRCU or, if applicable, the LIHTC rents required by

the tax credit application process or any other restricted rents as approved

during RD underwriting;

HB-3-3560

d. The budget must reflect the lesser of the Agency’s 5 percent of O&M and

historical vacancy plus 2 percent (not to exceed maximum of 10 percent for 16

or more units, or 15 percent for fewer than 16 units), or the industry standard of

5 percent vacancy;

e. There must be a demonstrated ability to repay any deferred developer’s fee from

the NOI proposed by the applicant at the time of RD underwriting approval for

the remaining term of the RD loan using the rents approved for the transaction

(See Paragraph 7.2 B); and

f. Each transfer request received by RD will be tracked by Agency underwriters

and loan servicers throughout the transfer process in the electronic monitoring

and tracking system prescribed by RD HQ.

D.

Preliminary Transfer Thresholds

RD adopted the following thresholds and policies for evaluating MFH transfer

feasibility to promote consistency in RD underwriting for MFH transfer transactions; and

balance the needs of the Agency, customers, and the project to maintain affordability for

eligible tenants under the RD programs. The transferee should complete a preliminary

assessment using these standards early in the transfer process and discuss it with the RD

office responsible for servicing the account. Careful analysis by all parties involved can

identify the general issues that will need to be resolved as the transfer application is

completed and submitted for formal review. Acceptance of the preliminary analysis by RD

does not constitute final approval of any transfer proposal by RD or any other third-party

funder. Thresholds RD considers include:

1. Post-Transfer Rents. Post-transfer rents should not exceed the restricted rents of

the LIHTC, HOME Program (if applicable), or CRCU (as defined in existing RD

regulations), whichever is less. The term Restricted Rents for the purpose of this

review will be the rent restrictions of LIHTC, HOME, or other Rent Restricting

Program(s) that will be placed on the property upon completion of the transfer.

Post-transfer rents on properties with 100 percent Project-Based Section 8 will not

exceed the maximum rents authorized under the HAP contract. No rent increase

beyond the current basic rents is authorized prior to completion of the planned

rehabilitation.

2. Rents Cash Flow in Proposed Operations. Proposed rents must be sufficient to

meet all projected expenses including a reasonable allowance for operations and

incidentals, and are typically included in the estimated individual operating

expense line items. The allowance may be expressed as a percentage of total

operating expenses and the resulting planned amount is reflected in the amount

shown as net cash on the RD operating budget, Form RD 3560-7, Part I, Line 30.

The minimum combined allowance for operating expenses and vacancy/bad debt

loss must not fall below the equivalent industry standard of 5 percent vacancy loss

or the applicable amount specified in #3 below. Net operating income (NOI) must

also be sufficient to meet the general industry minimum standard of 1.15 Debt

Service Coverage Ratio (DSCR) for all amortizing debt being placed on the

property in the initial underwriting review and authorization determination based

on the first year of typical operations (rents, O&M, etc.). If third-party lenders

(02-04-05) SPECIAL PN 7-

7

Revised (01 06-17) PN 492

HB-3-3560

7-8

specifically require DSCR in excess of the minimum, such rate should be used for

RD underwriting analysis during the initial three operating years. See also # 9

below.

3. Vacancy/Bad Debt Loss. The maximum allowance for vacancy and bad debt is 10

percent (for 16 or more units) and 15 percent (for fewer than 16 units) unless

otherwise specified by terms of any supplemental Notice of Solicitation of

Applications (NOSA) for which the transaction has been submitted. The

minimum allowance is the lesser of the historical average of collected rents for the

most recent three years plus 2 percent for bad debt, or the Restricted Rent

Program/Lender requirement when specified. If the budgeted allowance is less

than historical average plus 2 percent, it will be considered a failure to meet the

required threshold unless extenuating circumstances can be supported and

documented to RD’s satisfaction.

4. Operating Expenses. The minimum amount of operating expenses required per

unit is the greater of any specified by the Restricted Rent Program (LIHTC,

HOME, etc.) or the third-party lender (if applicable). Generally, project

maintenance costs are reduced as a result of the proposed rehab and generate a net

reduction. However, any reduction must be reasonable. No more than a 10 percent

change or variance in total project post-transfer closing operating expenses based

on historical actual averages will be accepted for underwriting without an adequate

justification acceptable to RD.

5. General Operating Account Minimum Requirement. The project’s General

Operating Account (GOA) must be equal to 20 percent total operating expense as

underwritten at the time of transfer (excluding the required prorated tax and

insurance escrow), and there must not be any outstanding accounts payable

exceeding 30 days. If this requirement cannot be achieved through normal project

operations as reflected in the underwritten typical year budget, the transfer

development budget must include an additional cash deposit to the GOA from

non-debt, LIHTC or the applicant’s non-project resources. Any additional

required deposit (not from normal operations) made by the applicant must be

documented to the Agency at the time of transfer. The applicant may recoup the

additional required cash deposit to the GOA between the second and seventh year

of operation in accordance with HB-2-3560 Chapter 4, Section 1, 4.3.

6. Tenant Protection. RD does not permit the intentional displacement of any

existing RD-eligible tenant because of the planned transfer, as long as the tenant

remains eligible under RD regulations and the terms of the RD-approved lease.

For projects not having full Rental Assistance (RA) and for all non-RA assisted

revenue units where the transfer results in a rent increase, the applicant must agree

to protect currently eligible tenants affected by the rent increase as long as the

tenant resides in the project. All tenant protection costs must be included in the

Sources and Uses analysis used in RD underwriting for the full amount needed to

fund the initial two-year minimum period following the transfer closing for

transfer underwriting purposes. NOTE: This does not limit the total cost of tenant

protections the transferee may ultimately be responsible for and is solely to aid in

completing the initial transfer underwriting analysis using the PAT. The applicant

will establish a specific cash escrow set-aside for this purpose at the time of

closing, and is responsible for providing, from non-project resources, any future

HB-3-3560

tenant subsidy or protections necessary to maintain cash flows if the project does

not have or fails to secure 100 percent RA, or other tenant subsidy necessary to

meet LIHTC or other third-party tenant rent restrictions.

7. Capital Needs Assessment (CNA) Funding & Reserve Deposit. The minimum

requirement per unit is the greater of any Restricted Rent Program (LIHTC,

HOME, etc.) requirement, or third-party lender (if applicable) requirement that

will be placed on the property upon completion of the transfer. The Reserve

Account ending balance forecast must be positive for all 20 years of CNA.

8. New Loans for RD Section 515 Eligible Purposes. Any new loans placed on the

property must be for Section 515 RRH-eligible loan purposes only, as defined in 7

CFR 3560.53. The Agency will analyze Federal Government and other assistance

provided to any MFH project to establish the maximum loan amount and to assure

that the assistance is not more than the minimum necessary to make the housing

affordable, decent, safe, and sanitary to potential tenants [7 CFR 3560.63(d)]. Any

prohibited uses of loan funds as defined in 7 CFR 3560.54 must be paid from non-

debt sources. However, projects using a RD Section 538 Guaranteed Rural Rental

Housing (GRRH) loan may be allowed additional debt for purposes eligible under

the GRRH regulations.

9. Debt Service Coverage Ratio (DSCR). RD underwriting will include annual

trending increases of revenue at 2 percent and expenses at 3 percent (including

reserve) for each of the first 15 years. For transfer underwriting and analysis, the

project at a minimum must meet an initial DSCR of 1.15 through year 3, and may

project subsequent DSCRs of 1.1 in years 4 and 5, and 1.0 for the remaining years

solely for the purposes of the RD initial transfer analysis. Third-party lenders may

require higher DSCR for their individual underwriting approval requirements. If

so, the DSCR required by the third-party lenders should be used in the RD

underwriting analysis during the initial 3 operating years.

10. Loan-to-Value. Upon completion of all planned rehabilitation/repairs and

approved development, all Debts must be secured within the Prospective As-

Improved Security Value as defined by RD in 7 CFR 3560, §3560.63. RD

determines Security Value and includes the intangible benefits afforded by the

interest credit subsidy of the RD loans, and the benefits of other favorable

financing resulting from other Federal, state or local government instrumentality

direct or authorized intermediary lending programs such as HOME, Preservation

Revolving Loan Fund (PRLF), and Section 538 GRRH loans being made at

below-market rates and terms, as permitted by RD regulations. Security Value

does not include any non-amortizing or deferred loans or grants regardless of the

source; or any federal, state or local LHITC and Historic tax credits or the

investment value thereof.

11. Loan Terms of Third-Party Debt. No balloon payment from any third-party debt

is allowed prior to the expiration of the minimum RD Loan Term (30 years for

RRH transfers and 33 years for FLH transfers), unless the Lender provides a

written agreement, acceptable to the Agency, to extend the scheduled maturity on

terms that do not require rents above comparable rents for comparable units

(CRCU) through the term of the RD loan.

(02-04-05) SPECIAL PN 7-

9

Revised (01 06-17) PN 492

HB-3-3560

7-10

12. Sources and Uses Must Balance. Sufficient funds must be available for all

proposed rehabilitation, acquisition costs, and uses to meet the terms of the

proposed transaction. Funds must be adequate to address repairs needed

immediately, including all health and safety, fair housing and accessibility issues.

13. These may be included as part of the up-front rehabilitation that is being paid by

third-party funds. Applicants must be able to fund any projected shortfalls from

resources other than the project or project income.

7.3 KEY ANALYTICAL CONCEPTS

In evaluating all the components of a transfer request, the Loan Servicer and the

Applicant need to determine if the transfer meets RD’s objectives by collecting the

information necessary to form the analytical foundation for Agency processing and

authorization of the proposal.

Using a preliminary analytical process and the processes provided in this Handbook,

the Loan Servicer and underwriter should be able to answer, and document the proposed terms

and conditions that will ultimately serve as part of the basis for approving the transfer request.

Formal final approval will only be granted upon submission and acceptance of all required

documentation in its totality, and the Agency's completion of the internal analytical analysis

tools as prescribed. RD underwriting considers the applicant's capacity to pay the loan,

provide sufficient capital to meet the transfer requirements, demonstrate the character

necessary to meet operational ownership and management requirements, provide and

maintain the project collateral, and meet the anticipated conditions necessary to close the

transaction and complete any required construction needs.

Applicants must have both sufficient experience and the financial capacity for the

development and ownership of the proposed property transfer. Applicants are required to

submit appropriate documentation to assist RD underwriters and approval officials evaluate

and establish reasonable expectations to assure the terms and conditions of the respective

assistance can be followed and carried in meeting the purposes intended. Applicants,

including any affiliated entities sharing an identity of interest with the applicant (i.e.,

management, contractors, etc.), must be in compliance on all or any other Agency-financed

projects that they may own or provide decision-making and operational authority over. Any

noncompliance issues must

have been cured or be in compliance with a workout agreement

approved by the RD for at least 6 consecutive months as of the date that the initial application

is due unless an exception is authorized by HQ.

Newly formed applicant entities, may not have the ability to demonstrate creditworthiness

and financial capacity to meet basic program eligibility determinations. RD underwriters and

approval officials may then look at the individual key principals the applicant identifies with the

organization, decision making and operational authority controlling the applicant organization or

entity as necessary.

All Principals will be identified and analyzed with respect to their capacity of credit,

experience and financial histories. Regulatory standards established in the Code of Federal

Regulations (24 C.F.R.) Part 200 Subpart H Participation and Compliance requirements determine

the appropriate review of previous participation in multifamily insured programs based upon their

past performance as well as other aspects of their records.

42 U.S. Code § 1441

HB-3-3560

These considerations are generally categorized in each of the following areas:

A.

Eligibility

The Loan Servicer must establish applicant eligibility in the same manner as during the

loan origination process, including an in depth evaluation of the applicant and the individual

principals of the applicant entity and any sub-entity. These requirements set the basic

standards for all borrowers including:

1. Analysis of financial capacity (such as balance sheets for all principals, including the

individual key principals involved in the organization, decision-making and

operational authority that may control the applicant and any sub-applicant entities

involved

);

2. Credit worthiness of all principals (such as credit reports, contingent obligations,

payment history, etc.);

3.

Experience

(such

as

previous

participation

certificates,

CAIVRs,

SAMs,

etc.);

4. Incidence of ongoing or chronic adverse actions in other projects or business

transactions;

5. Satisfactory explanation of all insufficient, incomplete, or negative factors identified in

the eligibility review; and,

6. Simultaneously, completion of the planned transfer must sufficiently determine a

continued need for affordable housing with adequate demand for continued use of the

project by tenants meeting the RD eligibility requirements. When necessary to establish

the continued need for a property, the loan underwriter may require additional

documentation acceptable to RD that there is an actual need for the project considering

any other existing or planned affordable housing in the market area.

Note: RD needs and LIHTC needs may not always serve the same market, and may

have different demands and concerns as affordable housing. Reviewers must ensure that RD

funds will be used in accordance with the program’s statutory requirements. The project’s

eligibility as documented during the loan transfer process requires the loan servicer to confirm

that the project will remain eligible after the transfer.

B.

Feasibility

The Loan Servicer must determine if the proposed transfer is feasible. This

feasibility determination requires an in-depth financial analysis of project operations, sources

and uses of funds, and potential for future success. See Paragraph 7.23.

C.

Improve or Maintain Risk Levels

The Loan Servicer must consider any financial and operational risk factors in the

transfer that conflict with the respective MFH loan program origination and servicing

principles.

(02-04-05) SPECIAL PN 7-

11

Revised (01 06-17) PN 492

HB-3-3560

7-12

7.4 DEFINITIONS

As used in this chapter, the following definitions apply to ownership transfers or sales

of all or a controlling interest in the project ownership as addressed in 7 CFR 3560.406.

A.

Transfer

A transfer occurs whenever there is a change in a project’s ownership that:

1. Places title to the property in the hands of a new owner;

2. A new owner assumes all liability for the debt; or

3. There is a change in the legal entity owning the project, such that the transferee

is commonly considered a distinct and separate legal entity from the original

borrower (including, without limitation, a change resulting in a new Internal

Revenue Service Tax ID number), or 100 percent of a borrower entity's

ownership interests will be transferred within a 12-month period (7 CFR

3560.405 (a)).

Changes in membership within the ownership entity such as the admission of non-

controlling members do not constitute a transfer, but do require RD involvement as discussed

in Chapter 5 of this Handbook. A change in ownership due to the death or involuntary

incapacitation of a joint owner, beneficiary of a trust owner, or in membership within the

ownership entity such as a general partner interest being sold or bequeathed may not

constitute a transfer as long as the incoming member meets RD eligibility requirements, and

the State Director requests authorization on a case-by-case basis from RD HQ. The change

must be appropriately documented without any change in the currently authorized RTO for

the project; additional debt, liability, or encumbrance of the RD loan security; or change of

project type or purpose. RD HQ will review the status of the project's current physical and

operational condition and may waive any other provision of this chapter for these cases only

when the RD approval official determines that such ownership change is in the best interests

of the government and the tenants. Borrowers may request to transfer their project to another

entity in which the members are involved in both the transferring and the assuming entities,

provided the new entity be legally organized, discloses all Identity-of-Interest situations, and

meets applicable RD eligibility requirements. (See also Paragraphs 7.5 and 7.16 E.)

A proposed transfer to an IRS-approved intermediary for purposes of a Section 1031

exchange is a transfer for purposes of this chapter.

If the transfer being proposed is part of an Agency incentive offer as described in

Chapter 15 of this Handbook as part of a prepayment incentive offer, a complete transfer

application package must be submitted as described herein unless all of the following

conditions are being met:

1. No additional sources of funding are being brought into the transaction and the

new owner does not request any RTO consideration other than those approved

as part of the Agency incentive offer;

2. There are also no existing physical, operational or financial needs, or

deficiencies that must be addressed to ensure the continued success of the

project in meeting the MFH program mission; and

HB-3-3560

3. The State Office has consulted with PDLD and determines an exception to this

Chapter is in the best interests of the government and the tenants.

B.

Non-Program Transfers [7 CFR 3560.406 (l)]

This chapter does not apply to non-program transfers, as discussed in Chapter 5 of this

Handbook. However, such a transfer or sale will only be considered when it is determined by

RD to be in the best interest of the Federal Government and the objectives of the original loan

can no longer be met.

C.

Underwriting

Underwriting as used in this Chapter refers to the process of determining the financial

and operational feasibility of the project, applicant eligibility, environmental compliance, and

fair housing compliance of a proposed transaction based on the specific requirements

specified in this Chapter, Agency Handbooks and guidance, and/or applicable Notice of

Funding Availability (NOFA), and/or Notice of Solicitation of Applications (NOSA). The

specific aspects of the transaction process such as determining applicant eligibility, assessing

environmental compliance, or evaluating fair housing compliance are more fully addressed in

the current RD Handbooks and Regulations, and supplemented from time to time with other

published guidance available on the RD website.

D.

Related Definitions

The following are definitions for certain related terms used in this Chapter.

• Acceptable Appraisal. The Agency will use appraisals to determine whether the

security offered by an applicant or borrower is adequate to secure a loan, or

determine appropriate servicing or preservation decisions. Appraisals used for

Agency decision-making must be current unless the Agency and the applicant or

borrower mutually agree to the use of an appraisal that is not current. A current

appraisal is an appraisal with an effective date that is not more than one year old

per §3560.752. All MFH appraisals that were not written by an Agency appraiser

will be reviewed by an Agency appraiser who will write and file a technical

review report that complies with the Uniform Standards of Professional Appraisal

Practice (USPAP) Standard 3, and Agency requirements as prescribed in

Handbook 1, 3560.

• Corporation. A corporation is any entity that has filed Articles of Incorporation in

one of the 50 States, the District of Columbia, or the various territories of the

United States including American Samoa, Federated States of Micronesia, Guam,

Midway Islands, Northern Mariana Islands, Puerto Rico, Republic of Palau,

Republic of the Marshall Islands, or the U.S. Virgin Islands. Corporations include

for both profit and non-profit entities.

• Debt Deferral. A deferral of an existing RD debt. Agency debt deferral is subject

to appropriations and may be offered to a transfer applicant selected for

participation under the terms of an outstanding MPR Program NOSA. This

deferral includes the deferment of the monthly principal and interest payments

with a balloon payment at the end of the deferral period. A debt deferral

agreement will be required for the debts assumed eligible for deferral at the time

of closing.

(02-04-05) SPECIAL PN 7-

13

Revised (01 06-17) PN 492

HB-3-3560

7-14

• Equity. Equity is the amount of the RD-accepted market value that exceeds the

total of all currently outstanding RD direct loans and any other parity, or senior

debts approved by RD, or to which RD has an outstanding subordination.

• Exit Incentive. An Exit Incentive is an amount of incentive compensation

determined by RD that may be paid to the selling borrower to facilitate

transferring the property to an eligible buyer when there is no equity as determined

by the RD-accepted market value used in the underwriting analysis. See also 7.2 C

8 for mandatory applicable Guiding Principles.

• Identity-of-Interest. A relationship between applicants, borrowers, grantees,

management agents, or suppliers of materials or services described under, but not

limited to, any of the following conditions (7CFR 3560.102 (g)):

1. There is a financial interest between the applicant, borrower, grantee and a

management agent or the supplying entity;

2. One or more of the officers, directors, stockholders, or partners of the applicant,

borrower, or management agent is also an officer, director, stockholder, or

partner of the supplying entity;

3. An officer, director, stockholder, or partner of the applicant, borrower, or

management agent has a 10 percent or more financial interest in the supplying

entity;

4. The supplying entity has or will advance funds to an applicant, borrower, or

management agent;

5. The supplying entity provides or pays on behalf of the applicant, borrower, or

management agent the cost of any materials or services in connection with

obligations under the management plan or management agreement;

6. The supplying entity takes stock or a financial interest in the applicant,

borrower, or management agent as part of the consideration to be paid them; or

7. There exists or come into being any side deals, agreements, contracts or

understandings entered into thereby altering, amending, or canceling any of the

management plan, management agreement documents, organization

documents, or other legal documents pertaining to the property by the Agency.

See 7 CFR 3560.11.

• Key Principle. A key principle is the party or parties involved in the organization,

decision-making and operational authority that may control the applicant and any sub-

applicant entities involved

and includes the actual individual(s) of any sub-entity

(i.e., other organizations, partnerships, etc.) which cannot demonstrate financial

ability, creditworthiness or experience in the name of the transferee or identified

sub-entity, to mitigate any creditworthiness, financial capacity and/or experience in

the transferee’s own right or may not have equal strength with respect to all of the

eligibility criteria.

• Non-Equity Compensation. Non-equity compensation is a payment to the Seller,

from the buyer when no equity exists in the property. This payment should come

from non-loan funds and must not affect project rents at any time during the term of

the RD direct loan or any modification thereof. See Paragraph 7.8 D.

• Portfolio Transaction. A portfolio transfer transaction is a transaction involving

multiple projects within one State being acquired by a single purchaser.

• RD Funds. RD funds include, for example, a subsequent Section 515 loan or a

Section 538 loan.

HB-3-3560

• Security Value. The security value is the property value established by RD which

is the lesser of the total development cost [exclusive of any developer's fee as

provided by §3560.63 (d)(2)]or the housing project's security value as determined

by an appraisal conducted in accordance with Subpart P of this part, minus any

prior or parity liens on the housing project.

• Third-Party Funding. Third-party funding involves sources of funds other than

RD funds and the purchaser’s personal funds. The third-party funding is provided

by other recognized third-party funding sources as described in 7 CFR 3565.102.

Tax credit equity, HOME funds, and Community Development Block Grant

(CDBG) funds are a few examples of third-party funding.

• Transferee. The transferee is the person or entity acquiring the RD-financed

property. In this Chapter, the term is used interchangeably with the terms

purchaser or buyer.

• Transferor. The transferor is the person or entity selling the RD-financed

property. In this chapter, the term is used interchangeably with the terms borrower

or seller.

7.5 CONDITIONS FOR TRANSFERS

A.

Conditions When a Transfer May Occur

Transfer applications, documenting in writing one of more of the following

conditions, will generally be considered for further processing:

• The transfer facilitates the physical and financial revitalization of the property;

• The transfer is needed to remove a hardship to the current borrower that was

caused by circumstances beyond the borrower’s control (circumstances

constituting ‘hardship’ are discussed below);

• The transfer is a result of a court order requiring the division of security property;

• The transfer is being requested as an alternative to prepayment;

• The transfer will do no harm to RD or the current and future eligible tenants; or

• Other circumstances exist which make the transfer in the best interest of the

Government.

Typically, RD will not consider a transfer if the borrower has owned the property for

fewer than five years. However, if the State Director determines that a hardship is present,

the transfer may occur without prejudice to the borrower.

Examples of hardship include, but are not limited to:

• Serious Illness or death of the borrower;

(02-04-05) SPECIAL PN 7-

15

Revised (01 06-17) PN 492

HB-3-3560

• Serious financial difficulties beyond a borrower’s control that cause the borrower

to shut down the business operation; or

• Inability of the borrower to obtain necessary credit on terms that would facilitate

refinancing the debt and allow for operation of the project at affordable rents, if

the outstanding loans are eligible for prepayment.

NOTE: RD will pursue appropriate administrative and/or civil remedies with respect

to transfers that occur without prior RD approval. RD considers these transfers to be

unauthorized sales. An unauthorized sale also constitutes a default on the RD loan [7 CFR

3560, subpart J].

B.

Types of Transfers

There are many different characteristics and circumstances that may be present in a

transfer. All transfer applications, unless otherwise specifically exempted in RD Regulations,

will comply with the eligibility requirements based on the type of project and the nature of the

transferee for the respective RD MFH program. These requirements are more fully described

in the applicable sections of HB 1-3560.

If any project being transferred is currently subject to an RD-approved Workout Plan

and an Identity-of-Interest as defined by RD regulations, the transferee must be in compliance

with the workout plan in place and on schedule. In addition, the purchaser (transferee) must

be in compliance with RD regulations or have a RD-approved workout plan in place and on

schedule with respect to any other RD properties owned.

For a list of documents to be submitted when requesting RD approval of a transfer, see

Attachment 7-B-1, Transfer Application Documents.

C.

Coordination between RD Headquarters and State Offices

Some transfers raise complex issues and require close coordination between the

borrower, the purchaser, and the Agency. However, simple transfers can be quickly and

easily addressed between the borrower, purchaser, and the Agency. For example, a simple

transfer of title to a purchaser with proven capacity, or transfer of a project without regulatory

compliance issues that does not require a rent increase or new funding from RD, would

proceed rapidly from application to approval to closing under the authority of the Loan

Servicer, with a final approval from the State Director as permitted by this Chapter up to the

amounts specified in RD Instruction 1901-A. Compliance issues could include issues with

the physical or financial condition of the property, poor management, or noncompliance with

civil rights and accessibility laws.

In transfers where the State Director’s approval limit is exceeded or requires

additional concurrence (e.g. where a rent increase or a policy waiver is necessary) and

authorization by RD HQ, the State Director will submit the request together with their

recommendation, appropriate documentation and sufficient underwriting documentation as

specified by Agency policy and procedures to MPDL prior to approval. Upon completion of

the HQ review, the State Director will be provided with the appropriate concurrence and

guidance memorandum authorizing the terms/conditions for the continued final processing,

formal approval or denial of the transaction at the State Director level.

7-16

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-17

MFH Transfer and MPR underwriting is used to authorize the transaction and approve

the terms leading to approval. Often underwriting transactions becomes intertwined among

the aspects and requirements crossing multiple interdisciplinary divisions within the Rural

Housing Service (RHS). To minimize potential confusion for borrowers and applicants, and

to ensure consistent application of pertinent RHS requirements, underwriters must coordinate

loan making (direct and guaranteed when applicable) and servicing expectations when

evaluating the proposed MFH transaction. Responsibility for successfully completing any

MFH underwriting requires ongoing coordination of Preservation and Direct Loan Division

(PDLD) loan making; Guaranteed Loan Division (GLD) guaranteed loan participation, and

Portfolio Management Division (PMD) loan servicing efforts.

7.6 PROCESSING A TRANSFER REQUEST

The Loan Servicer will coordinate the review process to meet the processing

guidelines by completing all of the steps below to move through the process of receiving a

transfer application, evaluating the transaction, and closing the transfer. These steps are listed

in Exhibit 7-1, Key Steps to Conduct a Transfer, and may be used to as a preliminary

checklist for discussion with the applicant.

HB-3-3560

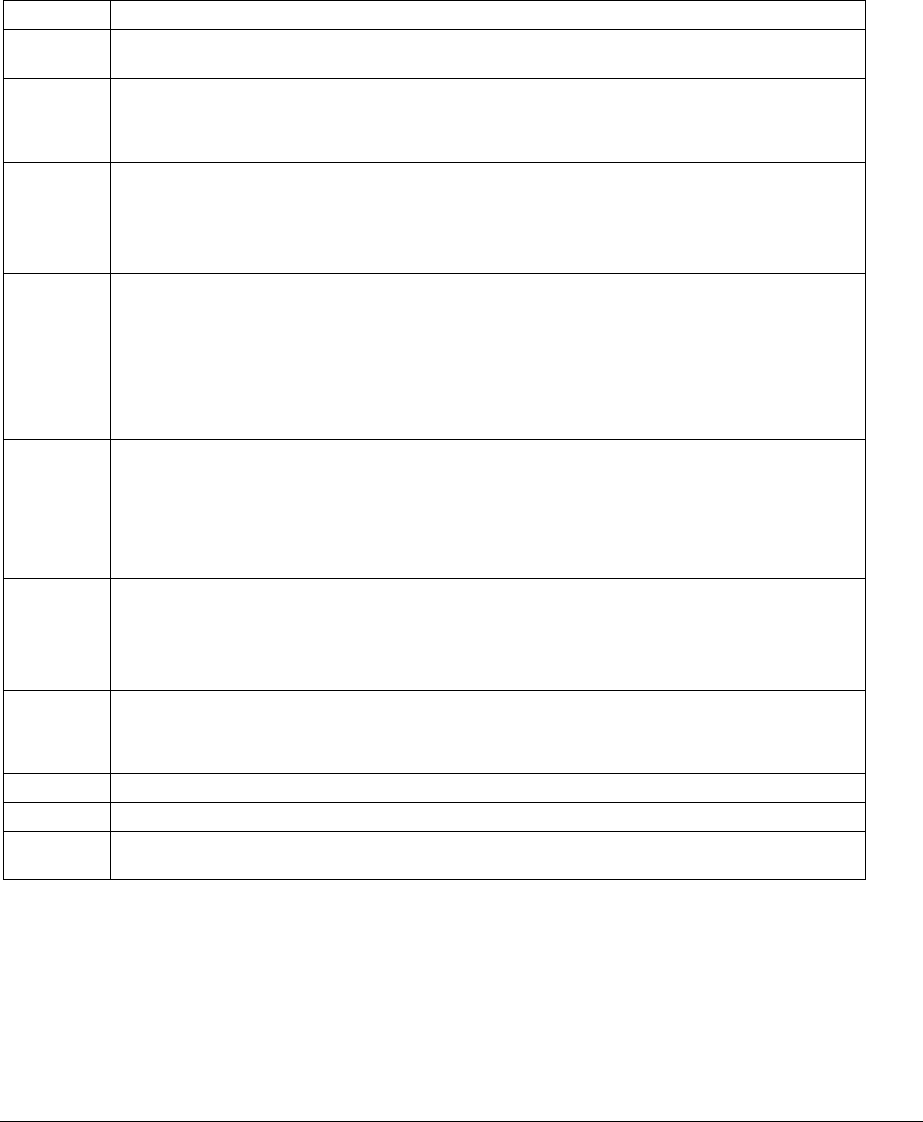

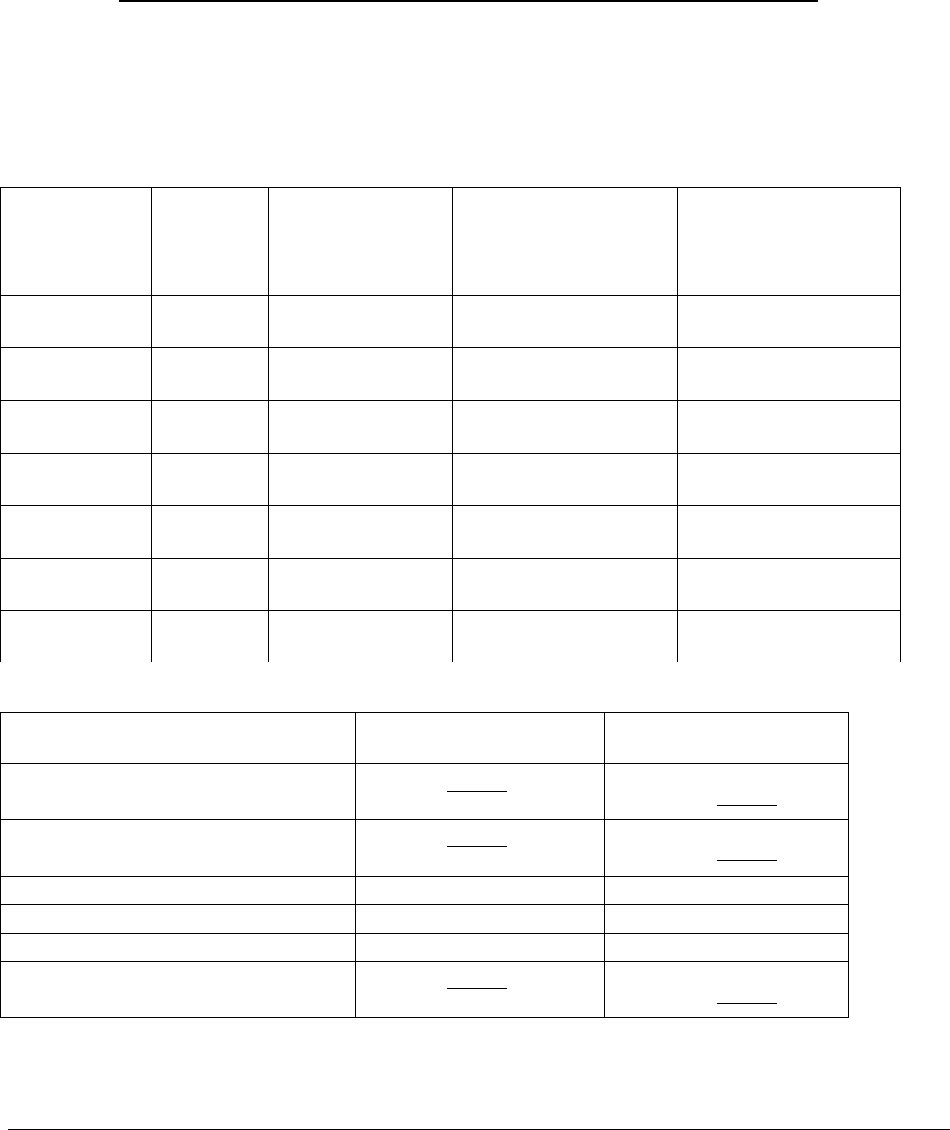

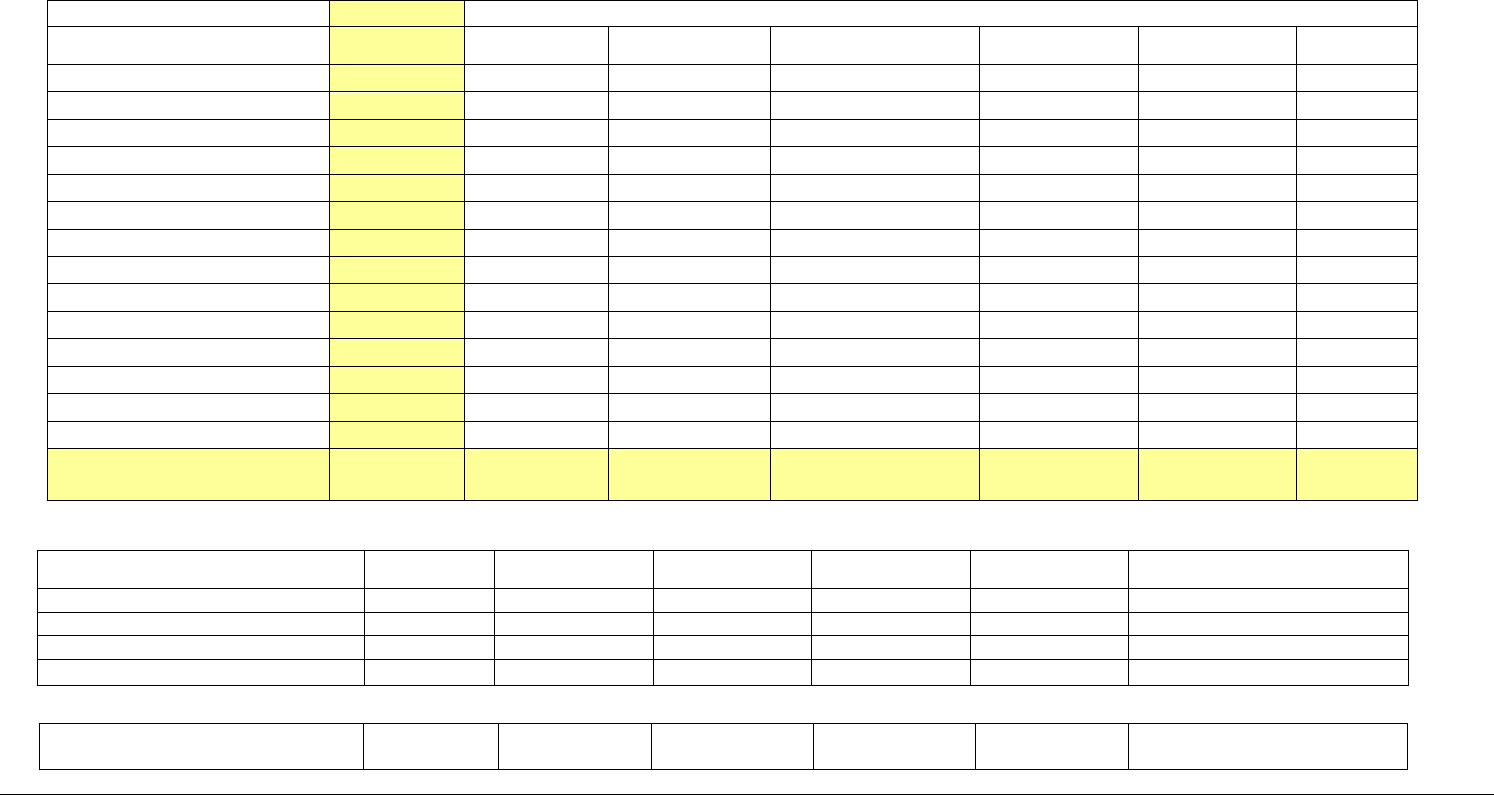

Exhibit 7-1

Key Steps to Conduct a Transfer

Step

Action

1

Applicant completes Preliminary Analysis and schedules Initial

Consultation with designated RD Loan Servicer

2

Initial Consultation with Applicant, Seller, and other key participants

having significant roles in the transaction such as other lenders, grantors,

etc.

3

Application Provided by Applicant preliminary review starts; RD

completeness review of application completed within 14 business days.

Incomplete applications will be returned to applicant and processing does

not begin until the complete application is received.

4

Request Underwriter Review - Detailed review by Underwriter commences

and processing starts. Status updates provided to applicant within every 30

business days the application is in process at RD. If additional clarification

or other materials are needed, the application will be considered incomplete

and it well be returned to the applicant for resolution. Unsatisfactory

submissions will be returned as incomplete or rejected.

5

Submit application to RD HQ for Authorization. Upon completion of the

Underwriter’s detailed review, the application will be submitted to HQ.

Within 10 business days, HQ determines if the transfer may be authorized.

If the transfer requires additional information from the applicant, the

application is returned to the state office for continued processing.

6

Agency Decision - Communicate to Applicant within 45 business days

(single property) / 75 days (multiple properties) - Processing for approval is

limited to the periods shown and does not include delays beyond the

underwriter’s immediate control.

7

Prepare Approval Conditions for Signature of Applicant - Within 15

business days of Agency Decision written approval conditions sent to

applicant for acceptance

8

Coordinate Closing Instructions and OGC Loan Document Approval.

9

Schedule and Close Transfer.

10

Complete post-closing review and verification that approval and closing

conditions have been met.

A.

Key Steps to Process a Transfer

1. Applicant completes Preliminary Analysis and schedules Initial Consultation with

designated RD Loan Servicer.

The applicant will complete the preliminary feasibility analysis and submit it to

the Loan servicer or other designated State Office reviewer for the Agency's

consideration within five business days of its receipt. If this preliminary

7-18

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-19

feasibility analysis has used the RD Preliminary Assessment Tool (PAT) and

the analysis appears to meet Agency thresholds or provides sufficient

explanation to indicate preliminary feasibility, an initial consultation will be

scheduled with the applicant, seller, and other participants as appropriate.

2. Initial Consultation with Applicant and Interested Parties.

The initial consultation will establish a common understanding of the transfer

process, timelines, terms, limitations, responsibilities, and conditions all parties

will be required to agree to that will affect the transfer being proposed. In

addition to the specific transfer requirements contained in the respective MFH

program authorities, additional discussion will further clarify the minimum

acceptable requirements for each of the following topics. Items to be discussed

include:

a. Identification of the transfer applicant and its principal entities or

individuals

• Type of entity must be legally recognized and authorized to conduct

business operations for the proposed transaction under applicable state

governing laws, rules, regulations, licensing, etc.;

• List of all individual sponsors, registered agents, key principals,

controlling members, and any board members and officers based on the

type of entity; and

• Identification of the applicant’s principal ownership interests and all

Identity-of-Interests among participants including buyer, seller, contractor,

management, lender, etc.

b. Eligibility requirements ( 7CFR 3560.55), including

• Creditworthiness of the sponsors, the borrower entity if formed, and its

principals should be verified with an appropriate commercial credit report,

• Applicant's experience record must be documented for the principals,

controlling members, officers, etc.

• Project limitations and restrictions to include discussion of any

outstanding or potential use restrictions that currently exist or will be

imposed based on the terms, financing, or other participants in the

proposed transaction; this includes existing LIHTC and any other

restrictions outstanding on the property.

• Financing plans, participants, roles, amounts, terms, and conditions

necessary to secure funding will be discussed.

• See HB1-3560, Chapters 2 and 4 for additional specific program eligibility

requirements.

c. Site control

• Applicant must have enforceable site control throughout the transfer

process. Adequately describe real estate and any other personal property,

chattels, equipment, movable property and business property that is not

real property, money or investments belonging to the project being

HB-3-3560

7-20

acquired in compliance with state laws and practices. Applicant should

consult with his or her own appropriate legal counsel as necessary to

ensure adequacy and proper enforceability of the purchase agreement.

• Price and terms must be clearly defined

• See also Handbook 1-3560, Chapter 7 for additional eligibility

requirements.

d. Appraisal requirements

• Only appraisals acceptable to RD will be used for transfer underwriting.

Third-party appraisals may not be sufficient for RD use unless they

comply with Agency requirements in form, timeliness, and sufficiency.

See HB1-3560, Chapter 7.

• Applicants should discuss RD appraisal requirements including the

statement of work prior to engaging an appraiser.

• Appraisals prepared for any other participants or lenders may not satisfy

RD Statement of Work requirements, and may require the applicant to

incur additional appraisal costs.

e. Capital Needs Assessment requirements

• RD requires a current CNA meeting Agency requirement for all transfers.

• CNA guidelines are available on the RD public website at:

http://www.rd.usda.gov/programs-services/multi-family-housing-direct-

loans

f. Scope of Work

• All planned repairs, replacements, and other development must comply

with RD requirements as required in RD Instruction 1924-A, regardless of

funding source.

• To coordinate construction and satisfy transfer requirements, applicants,

their contractors, and any technical staff should discuss the details of the

Scope of Work being planned to ensure the requirements of each

participating funder is addressed.

g. Applicant’s Feasibility Analysis

• Verify that all parties to the transaction have been identified, and that lines

of communication can be extended to ensure that full disclosure of the

planned transaction will be forthcoming.

• Remind the applicant that it is his or her responsibility to provide adequate

and accurate information in a timely manner to move forward with the

transfer request.

• Be available to discuss deficiencies in the application, and demonstrate a

willingness to consider appropriate compromise with the participants and

lenders when evaluating the best interests of the Government and the

tenants.

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-21

• Remember a transfer request is a business and financial decision being

made by the buyer and seller to request RD permission to effect the

transfer under the rules, regulations, and policies that have been

prescribed.

h. Provide a general Letter of Support based upon agreements being proposed.

• The applicant's delivery of a completed self-analysis of their transfer

proposal using the PAT, does not guarantee final approval of the transfer

request.

• However, this analysis should present a reasonable approximation that a

final transfer application adhering to the fundamental assumptions that

have been presented would, upon the completion of the full transfer

process, likely lead to an RD transfer authorization subject to the

regulations then in effect.

3. Application Provided by Applicant.

The Loan Servicer will record all transfer applications into the MFH Transfer

Tracking System in SharePoint at:

https://mfh.usda.net/Admin/Lists/Transfer%20Tracking/AllItems.aspx and

annotate Multi-family Information System (MFIS) with an appropriate

servicing action as designated by RD HQ upon receipt from the applicant. The

Servicing Office receiving the application will establish a transferee account in

MFH records based on the information provided by entering the M1AA, M5A

and M5B into AMAS to establish the transferee.

All transfer applications received will be reviewed within 14 business days of

receipt for completeness, and provide appropriate notification to applicant.

Applicants established in the tracking and servicing monitoring system will

also be updated to include appropriate comments and follow up actions so long

as the transfer application remains active. If the application is incomplete, it

will immediately be returned to applicant. However, minor errors or

administrative omissions should not prevent determination of application’s

eligibility or feasibility.

Internal Agency reviews will commence upon determining the application is

sufficiently complete to begin processing the PAT. To ensure that the

processing guideline goals can be met, the Loan Servicer will typically

schedule simultaneous reviews by one or more staff members:

• The State Office review of the CNA;

• The required on-site inspection, and completion of the analytical template;

and

• Coordinate all other requests for reviews.

The goal is to complete the full evaluation of the complete application(s) is:

• 45 business days if one property is involved, or

• 75 business days if two or more properties are involved.

The complete application submitted by the applicant will be evaluated based on

the application materials provided by the applicant and a review of Agency

records, including AMAS and MFIS information for the project being

HB-3-3560

7-22

transferred, the applicant, and the other key principals involved in the

transaction. The Loan Servicer must demonstrate in the case file that the

transfer application sufficiently addresses the issues of eligibility, compliance,

feasibility, and risk as discussed in this chapter in each of the following broad

categories.

a. Evaluate the Transferee

Transferees must meet the basic applicant eligibility for the respective loan

program (RRH or FLH) currently financing the property. These

requirements are presented in more detail in HB 1-3560.

• Analyze creditworthiness of the sponsors, the borrower entity if formed,

and its principles; order a commercial credit report for the applicant

entity, any parent organization, affiliate, subsidiary, and all principals.

A comprehensive commercial credit report will be order by RD for all

transferees, including any key principles as defined in 7.4 C of this

handbook.

• Analyze program organization requirements for all applicant entities'

ability to meet the organizational formation and operating

requirements/restrictions within the state in which the project is

located, including representations regarding felony conviction and tax

delinquency status for a corporation. Use Form AD-3030, for

corporations to verify the corporation does not that have felony

convictions within the past 24 months, or have unpaid Federal tax

delinquencies.

• Require current financial statements from all entities and principals.

• Analyze the applicant's experience record and resumes from principals.

• Review Form RD 1944-37, Previous Participation Certification(s) for all

principles.

• Order CAIVRS, SAM, and Credit Reports.

• Request initial Organizational Document review from OGC.

b. Evaluate the Property

Each property being transferred must be evaluated to determine if, upon

closing the transaction, the property will continue to meet the respective

loan program purposes, including:

• Evidence of continuing project need;

• Rents and occupancy; CRCU and other rent limitations;

• Property feasibility/adequacy of repair and rehabilitation, and method of

construction; and,

• Reasonableness of costs for planned development.

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-23

c. Evaluate the Project

The transfer further encompasses a number of other Agency requirements

and conditions that become the complete project. This includes the

following items necessary to satisfy the commitments imposed by other

applicable Federal laws and regulations.

• Environmental Review (typically categorical exclusion);

• Evidence of third-party funding availability, including rates and terms;

• Coordination with other third-party participants in place;

• Request of Reviews by PSS and OGC; and,

• Civil Rights Impact Analysis.

d. Compile all information necessary to complete underwriting analytical

analysis using the RD PAT.

e. Notify the applicant of any deficiencies, and require corrections before

considering the application to be complete for processing. Applications

not corrected within 30 days will be withdrawn and returned to the

applicant for resubmission when the outstanding issues are resolved.

PAT contains general instructions, basic underwriting thresholds, and

pertinent tips for RD customers and staff to assist in preparing and

evaluating proposals. The tool supplements the more detailed instructions

found in the applicable RD Handbooks, CFR, and regulations. Additional

instructions and suggestions are available internally for Agency

underwriters through the Agency SharePoint.

4. Request Underwriter Review.

MFH Transfer underwriting is used to authorize the transaction and the future

servicing requirements upon closing. Responsibility for successfully

completing any MFH underwriting relies on the ongoing coordination of loan

making and loan servicing efforts. The underwriting review relies on the

expertise of the RD staff currently servicing the loan, and the invaluable input

and insights each can offer on the project, the market, the borrower, and the

applicant. An on-going RD team effort involving both the underwriting staff

and servicing is required to deliver a project that will be sustainable for eligible

tenants over the life of the RD loan.

The underwriter must have the ability to complete the basic eligibility

determinations concerning both the applicant/borrower and the project to

HB-3-3560

ensure the transaction complies with the respective MFH program authorities

described in current RD Handbooks, CFR, and statutory authorities.

The Underwriter will import the CNA, appraisal information, and all other

third-party sources and uses into the PAT (available at the RD intranet

SharePoint https://mfh.usda.net/default.aspx) to document the MFH transfer.

All transfers, including those utilizing any MPR tools, must be in the best

interests of the Government and tenants. These transactions must demonstrate

the extended viability and sustainability of the project, the likelihood of full

repayment under the terms being offered, and the potential to succeed in

providing and maintaining quality housing over the long-term. It is not the

Agency’s role to assume any responsibility for the individual business

decisions of the borrower or applicant in ultimately determining the course of

action they propose.

Each component in every transaction will be evaluated and analyzed on its

individual merits. Common sense consideration of pertinent present and

historical conditions, as well as recognition of justifiable future impacts, must

all be used to judge the project’s potential to succeed over the term of

financing being proposed.

Key considerations may include questions such as:

• Is the project needed?

• Is the applicant eligible?

• Is the project eligible? Is there a present and continuing need for the project

in its market area?

• Is the project economically feasible? Does the transaction cash flow use a

reasonable operating budget comparable to other similar affordable

properties in the market area?

• Will the project be and remain affordable upon completion of the

transaction?

• Are the RD-eligible project construction and operating costs reasonable?

• Are the Agency’s interests secure?

• Is the transaction in the best interests of the Government and the tenants?

• Does the proposal offer adequate property and asset management to meet

RD requirements into the future based on the information presented?

The terms and conditions of the transaction presented by the applicant must

reasonably address the issues that determine the potential for success. This

includes substantiating any future tenant subsidies that may be necessary to

ensure success of planned operations. All parties need to recognize that the

transactional costs and fees proposed may adversely limit the amount of funds

needed for repairs, replacements, and improvements and become detrimental to

7-24

HB-3-3560

(02-04-05) SPECIAL PN

Revised (01-06-17) PN 492

7-25

the Agency transfer requirements and thresholds. Ultimately, any allowable

costs will pass to the tenants through rent increases, but tenant subsidies such

as Rental Assistance (RA) are not guaranteed beyond their current expiration.

Tenants who do not receive RA will be impacted directly by any rent increase,

which they may not be able to afford.

Agency underwriters must use the most current underwriting tools and

guidance such as those in the PAT available at the RD intranet (SharePoint)

https://mfh.usda.net/ProgTracking/default.aspx to document the MFH transfer

and MPR decisions.

Applicants and borrowers may access these forms through the appropriate RD

public websites (http://www.rd.usda.gov/programs-services/multi-family-

housing-direct-loans or http://www.rd.usda.gov/programs-services/housing-

preservation-revitalization-demonstration-loans-grants).

At this point, the Underwriter will complete the final underwriting analysis to

determine full feasibility and terms for the transaction. The Underwriter will

normally conclude this analysis within 45 days (for a single property) or 75

days (for multiple properties) from the date that the complete application(s) has

(have) been received. The Underwriter will evaluate the application for overall

compliance, risk to the Agency, and impact to the tenants.

If the terms of the transfer do not meet Agency requirements, the Underwriter

will communicate to the Loan Servicer that the assumptions used in the

application are not reasonable and the application will rejected. The Loan

Servicer will communicate to the applicant the Agency’s decision and follow

the applicable requirements of RD Instruction 2033-A for file retention.

If the terms of the transfer meet the Agency’s requirements, the Underwriter

will communicate to the Loan Servicer that the assumptions used in the

application are reasonable and the application will proceed. The Loan Servicer

will communicate to the applicant the Agency’s decision to continue

processing the transfer application.

The Loan Servicer will provide the applicant with a status update within 30

business days of receipt of the application.

5. Submit to RD HQ for Concurrence and Authorization for approval by the State

Director.

When the underwriter has completed the underwriting analysis using the

information and materials supplied by the Loan Servicer, the transfer

underwriting analytical tool or PAT, and appropriate supporting information,

the application will be signed by the State Director and submitted for

authorization by the RD HQ Office. The submission will include the

underwriter’s recommended conditions and estimated closing date.

HB-3-3560

7-26

6. Agency Decision.

RD HQ will review the underwriter's package and recommendations. Upon

acceptance of the information, a letter authorizing the State Director to

formally approve the specific transfer pursuant to program regulations,

funding, etc. will be provided to the State Director within 15 business days.

7. Prepare Approval Conditions for Signature of Applicant.

Within 15 business days of the date the authorization is signed by the RD HQ

Office designate, the State Director will notify the applicant of the specific

approval conditions. The Applicant will signify acceptance of approval

conditions by endorsing and returning the duplicate set of the State Director's

approval letter.

8. Coordinate Closing Instructions and Loan Document Approval from OGC.

The Loan Servicer will coordinate closing instructions and any necessary loan

document approval with OGC and the closing agent within the closing

timeframe authorized in the transfer approval letter. The Loan Servicer will

also establish the new buyer's account in AMAS and MFIS within the

timeframes established in the accounting system, and input necessary budgets,

worksheets, etc. as required by the AMAS tips.

9. Schedule and Close Transfer.

The designated closing agent will coordinate the delivery of the RD closing

documents, complete the scheduled closing as directed and deliver the

necessary documentation to RD to properly evidence closing, recording, etc.

10. Complete post-closing review and verification.

The Loan Servicer will finalize the buyer's account in AMAS and MFIS to

ensure the transaction complies with all of the applicable loan and operational

conditions authorized for the transaction.

B.

Procedure for Incomplete Transfer Requests

If at any point, the Loan Servicer determines that additional information is required

from the purchaser in order to complete processing, the Loan Servicer will notify the

purchaser in writing as follows:

• Explain the deficiency and describe what additional information is needed and

the timeframe for submitting the additional information.

• RD’s timeframe for processing the transfer request may be extended for not more

than 30 business days beginning with the date of the notice to the applicant.

• If the information is not submitted within the extension period, RD will consider

the transfer request to have been withdrawn and return the application.

HB-3-3560

C.

Denial of Transfer Request

The Loan Servicer may issue a denial of the transfer request at any point during the

process. Appeal rights should be given for denials as submitted. Grounds for denial include,

without limitation:

1. Eligibility issues as determined by the specific program regulations for RRH

and LH, and this Handbook:

•

Ineligible transferee; or

•

Ineligible project.

2. Feasibility issues, such as:

• CNA does not meet RD requirements;

• The proposed transfer does not address the property’s physical needs;

• The appraisal submitted does not meet RD requirements;

• The proposed transfer does not address all compliance issues;

• Proposed Operations and Maintenance (O&M) expenses are not adequate

for the project’s long-term viability;

• Proposed net operating income (NOI) is not sufficient to meet the general

industry standard of 1.15 debt service coverage ratio (DSCR) through year

three for all amortizing debt that is being placed on the property with the

proposed transfer transaction;

• Proposed rents exceed the lesser of CRCU or restricted rents unless an

exception is allowable under the regulation; or

• Proposed rents are not adequate to support the property’s long-term

viability.

3. Financial issues, such as:

• The proposed transfer would not bring all loan accounts current;

• The taxes and insurance account will not be adequately funded, with all

outstanding bills paid; and

• The security deposit account will not be fully funded.

4. The proposed management is not acceptable as required in 7 CFR 3560.102

and further described in RD HB 2-3560.

5. The proposed transfer will not correct all outstanding findings sufficiently to

allow re-classification of the property to an acceptable level. In some cases

(02-04-05) SPECIAL PN 7-

27

Revised (01 06-17) PN 492

HB-3-3560

7-28

the agreement to transfer ownership may be considered part of an

acceptable workout plan for MFIS entry together when any further servicing

actions determined appropriate to meet the best interests of the government

and the tenants. Some transfer requests may be unacceptable as submitted

but could be acceptable with specific modifications. At any point during the

process, the Loan Servicer may inform the applicant accordingly, using the

procedure in paragraph 7.6 B. Incomplete transfer requests not corrected