__________________________________________________________

DoD

MILITARY RETIREMENT

TRUST FUND

Table of Contents

Overview ........................................................................................................................ 1

Principal Statements...................................................................................................... 11

Footnotes to the Principal Statements............................................................................ 19

Supplemental Financial and Management Information.................................................... 29

Audit Opinion ............................................................................................................... 33

Overview ______________________________________________ ___

___________________________________________________ Overview

1

DoD

MILITARY RETIREMENT

TRUST FUND

OVERVIEW

Overview ______________________________________________ ___

2

___________________________________________________ Overview

3

SUMMARY OF THE MILITARY RETIREMENT SYSTEM

As of September 30, 1998

Description of the Reporting Entity

The reporting entity is the Office of the Undersecretary of Defense for Personnel and Readiness,

one of whose missions is to oversee the accounting, investing, and reporting of the Military

Retirement Trust Fund (the Fund). In FY 1998, the Fund paid out approximately $31 billion in

benefits to military retirees and survivors. In addition to staff members of the reporting entity and

the DoD Office of the Actuary, hundreds of individuals at the DFAS Cleveland and Denver Pay

Centers are involved in making the benefit payments. The Fund receives income from three

sources: monthly normal cost payments from the Services to pay for the current year’s service

cost, annual payments from Treasury to amortize the unfunded liability, and investment income.

During FY 1998, the Fund received $10 billion in normal cost payments, a $15 billion unfunded

liability amortization payment, and $12 billion in investment income. No fund accounts have been

excluded by this statement. Because the Fund provides a service and not a product,

administrative costs are not ascertainable, and are therefore not calculated or reported.

Overview

The military retirement system applies to members of the Army, Navy, Marine Corps, and Air

Force. However, most of the provisions also apply to retirement systems for members of the

Coast Guard (administered by the Department of Transportation), officers of the Public Health

Service (administered by the Department of Health and Human Services), and officers of the

National Oceanic and Atmospheric Administration (administered by the Department of

Commerce). Only those members in plans administered by the Department of Defense are

included in this valuation.

The system is a funded, noncontributory defined benefit plan that includes nondisability retired

pay, disability retired pay, retired pay for reserve service, and survivor annuity programs. The

Service Secretaries approve immediate nondisability retired pay at any age with credit of at least

20 years of active-duty service. Reserve retirees must be 60 years old with 20 creditable years of

service before retired pay commences. There is no vesting before retirement.

There are three distinct nondisability benefit formulas related to three populations within the

military retirement system. Military personnel who first became members of the Armed Services

before September 8, 1980 have retired pay equal to (terminal basic pay) times (a multiplier). The

multiplier is equal to (2.5 percent) times (years of service) and is limited to 75 percent. If the

retiree first became a member of the Armed Services on or after September 8, 1980, the average

of the highest 36 months of basic pay is used instead of terminal basic pay. Members first

entering the Armed Services on or after August 1, 1986 are subject to a penalty if they retire with

less than 30 years of service; at age 62, their retired pay is recomputed without the penalty.

Overview ______________________________________________ ___

4

Retiree and survivor benefits are automatically adjusted annually to protect the purchasing power

of initial retired pay. The benefits associated with members first entering the Armed Services

before August 1, 1986 are adjusted annually by the percentage increase in the average Consumer

Price Index (CPI). This is commonly referred to as full CPI protection. Benefits associated with

members entering on or after August 1, 1986 are annually increased by the percentage change in

the CPI minus 1 percent. At the military member’s age 62, the benefits are restored to the

amount that would have been payable had full CPI protection been in effect. This restoral is in

combination with that described in the previous paragraph. However, after this restoral, partial

indexing (CPI minus 1 percent) continues for life.

Nondisability Retirement From Active Service

The current system allows voluntary retirement upon completion of at least 20 years of service at

any age, subject to Service Secretary approval. The military retiree receives immediate retired

pay calculated as (base pay) times (a multiplier). Base pay is equal to terminal basic pay if the

retiree first became a member of the Armed Services before September 8, 1980. It is equal to the

average of the highest 36 months of basic pay for all other members. The multiplier is equal to

(2.5 percent) times (years of service, rounded down to the nearest month) and is limited to 75

percent. Members first entering the Armed Services on or after August 1, 1986, and who retire

with less than 30 years of service receive a temporary penalty until age 62. The penalty reduces

the multiplier by one percentage point for each full year of service under 30. For example, the

multiplier for a 20-year retiree would be 40 percent (50 percent minus 10 percent). At age 62, the

retired pay is recomputed with the penalty removed.

In FY 1998, 1.33 million nondisability retirees from active duty were paid $25.77 billion.

Disability Retirement

A disabled military member is entitled to disability retired pay if the disability is at least 30 percent

(under a standard schedule of rating disabilities by the Veterans Administration) and either (1) the

member has eight years of service; (2) the disability results from active duty; or (3) the disability

occurred in the line of duty during a time of war or national emergency or certain other time

periods.

In disability retirement, the member receives retired pay equal to the larger of (1) the accrued

nondisability retirement benefit, or (2) base pay multiplied by the rated percent of disability. The

benefit cannot be more than 75 percent of base pay. Only the excess of (1) over (2) is subject to

Federal income taxes. Base pay is equal to terminal basic pay if the retiree first became a member

of the Armed Services before September 8, 1980. If the retiree first entered the Services on or

after September 8, 1980, base pay is equal to the average of the highest 36 months of basic pay.

___________________________________________________ Overview

5

Members whose disabilities may not be permanent are placed on a temporary-disability retired list

and receive disability retirement pay just as if they were permanently disabled. However, they

must be physically examined every 18 months for any change in disability. A final determination

must be made within five years. The temporary disability pay is calculated like the permanent

disability retired pay, except that it can be no less than 50 percent of base pay.

In FY 1998, 111,000 disability retirees were paid $1.43 billion.

Reserve Retirement

Members of the reserves may retire after 20 years of creditable service, the last eight of which

must be in a reserve component. However, reserve retired pay is not payable until age 60.

Retired pay is computed as (base pay) times (2.5 percent) times (years of service). If the reservist

was first a member of the Armed Services before September 8, 1980, base pay is defined as the

active duty basic pay in effect for the retiree’s grade and years of service at the time that retired

pay begins. If the reservist first became a member of the Armed Services on or after September 8,

1980, base pay is the average basic pay for the member’s grade in the last three years that he/she

was a member of the Armed Services. The years of service are determined by using a point

system, where 360 points convert to a year of service. Typically, a point is awarded for a day of

service or a drill attendance, with 15 points being awarded for a year’s membership in a reserve

component. A creditable year of service is one in which the member earned at least 50 points. A

member cannot retire without 20 creditable years, although points earned in non-creditable years

are used in the retirement calculation.

In FY 1998, 228,000 reserve retirees were paid $2.32 billion.

Survivor Benefits

Legislation originating in 1953 provided optional survivor benefits. It was later referred to as the

Retired Servicemen’s Family Protection Plan (RSFPP). The plan proved to be expensive and

inadequate since the survivor annuities were never adjusted for inflation and could not be more

than 50 percent of retired pay. RSFPP was designed to be self -supporting in the sense that the

present value of the reductions to retired pay equaled the present value of the survivor annuities.

On September 21, 1972, RSFPP was replaced by the Survivor Benefit Plan (SBP) for new

retirees. RSFPP still covers those servicemen retired before 1972 who did not convert to the new

plan and still pays survivor annuities.

Retired pay is reduced, before taxes, for the member’s cost of SBP. Total SBP costs are shared

by the Government and the retiree, so the reductions in retired pay are only a portion of the total

cost of the SBP program.

Overview ______________________________________________ ___

6

The SBP survivor annuity is initially 55 percent of the member’s base amount. The base amount

is elected by the member, but cannot be less than $300 or more than the member’s full retired pay.

If a penalty for service under 30 years is included in the calculation of retired pay, the maximum

base amount is equal to the full retired pay without the penalty.

The spouse’s annuity is considered a two-tier benefit because, at age 62, the annuity is reduced to

35 percent of the base amount. Prior to the enactment of the two-tier benefit, survivor annuities

were integrated with Social Security. SBP participants and active and reserve personnel with at

least 20 years of service on October 1, 1985 were grandfathered into the two-tier system. Their

survivors will be given the higher of the two annuities at age 62.

During FY 1987 the SBP program’s treatment of survivor remarriages changed. Prior to the

change, a surviving spouse remarrying before age 60 had the survivor annuity suspended. The

change lowered the age to 55. (If the remarriage ends in divorce or death, the annuity is

reinstated.)

Beginning in April 1992, retirees with base amounts equal to full retired pay could also elect a

supplemental annuity for their surviving spouses after age 62, in increments of 5 percent of the

base amount, up to a maximum 20 percent benefit. (The cost of this supplemental SBP benefit is

borne by retirees in the form of a reduction in retired pay over and above the usual 6.5 percent

reduction for SBP.)

Members who die on active duty with over 20 years of service are assumed to have retired on the

day they died and to have elected full SBP coverage for spouses and/or children.

SBP annuities are reduced by any VA survivor benefits and all premiums relating to the

reductions are returned to the survivor. Additionally, SBP annuities are annually increased with

cost-of-living adjustments (COLAs). These COLAs may be based on full or partial CPI increases,

depending on when the member first entered the Armed Services. If the member dies before age

62 and the survivor is subject to partial COLAs, the survivor’s annuity is increased (on the

member’s 62nd birthday) to the amount that would have been payable had full COLAs been in

effect. Partial COLAs continue annually thereafter.

For reserve retirees, the same set of retired pay reductions applies for survivor coverage after a

reservist turns 60 and begins to receive retired pay. A second set of optional reductions, under

the Reserve Component Survivor Benefit Plan, provides annuities to survivors of reservists who

die before age 60, but after attaining 20 years of service. The added cost of this coverage is borne

completely by reservists through deductions from retired pay and survivor annuities.

In FY 1998, 234,000 surviving families were paid $1.70 billion.

___________________________________________________ Overview

7

Temporary Early Retirement Authority (TERA)

The National Defense Authorization Act for FY 1993 (P.L. 102-484) grants temporary authority

for the military services to offer early retirements to members with more than 15 but less than 20

years of service. The retired pay is calculated in the usual way except that there is a reduction of

1 percent for every year below 20 years of service. Part or all of this reduction can be restored at

age 62 if the retired member works in a qualified public service job during the period from the

date of retirement to the date on which the retiree would have completed 20 years of service.

Unlike members who leave military service before 20 years with voluntary separation incentives

or special separation benefits, these early retirees are treated like regular military retirees for the

purposes of other retirement fringe benefits. This authority is scheduled to expire at the end of

FY 2001.

As of September 30, 1998, there were 52,000 TERA retirees receiving retired pay at an annual

rate of $615 million.

Cost-of-Living Increases

All nondisability retirement, disability retirement, and most survivor annuities are adjusted

annually for inflation. Cost-of-living adjustments (COLAs) are automatically scheduled to occur

every 12 months, on December 1st, to be reflected in checks issued at the beginning of January.

The “full” COLA effective December 1 is computed by calculating the percentage increase in the

CPI from the third quarter of the prior calendar year to the third quarter of the current calendar

year. The increase is based on the Urban Wage Earner and Clerical Worker Consumer Price

Index (CPI-W) and is rounded to the nearest tenth of one percent.

The benefits of retirees (and their survivors) first entering the Armed Services before August 1,

1986 are annually increased with the full COLA; all other benefits are annually increased with a

partial COLA equal to the full COLA minus 1 percent. A one-time restoral is given to a partial

COLA recipient on the first day of the month after the retiree’s 62nd birthday. At this time,

retired pay (or the survivor benefit if the retiree is deceased) is increased to the amount that would

have been payable had full COLAs been in effect. Annual partial COLAs continue after this

restoral.

Relationship with VA Benefits

The Department of Veterans Affairs (VA) provides compensation for Service-connected and

certain non-Service-connected disabilities. These VA benefits can be in place of (or in

combination with) DoD retired pay, but they are not additive. Since VA benefits are exempt from

Federal income taxes, it is sometimes to the advantage of a member to elect them.

Overview ______________________________________________ ___

8

Veterans Administration benefits also overlap survivor benefits through the Dependency and

Indemnity Compensation (DIC) program. DIC is payable to survivors of veterans who died from

Service-connected causes. Although an SBP annuity must be reduced by the amount of any DIC

benefit, all SBP premiums relating to the reduction in benefit are returned to the survivor.

Interrelationship with Other Federal Service

For retirement purposes, no credit is given for other Federal service, except where cross-service

transferability is allowed. Military service is generally creditable toward the Federal civilian

retirement systems if military retired pay is waived. However, a deposit (equal to a percentage of

post-1956 basic pay) must be made to the Civil Service Retirement Fund in order to receive

credit. Military service is not generally creditable under both systems (but is for reservists and

certain disability retirees). Retired regular officers employed by the Federal Government lose a

substantial portion of their retired pay while so employed, and all retired members are subject to a

combined ceiling equivalent to Level V of the Executive Schedule. The ceiling does not apply to

those who had retired before October 13, 1978 (or were under age 60 and eligible for Reserve

retirement on that date) and were continuously employed by the Federal Government since that

date.

Relationship of Retired Pay to Military Compensation

Basic pay is the only element of military compensation upon which retired pay is computed and

entitlement is determined. Basic pay is the principal element of military compensation that all

members receive, but it is not representative, for comparative purposes, of salary levels in the

public and private sectors. Reasonable comparisons can be made to regular military compensation

(RMC). RMC is the sum of (1) basic pay, (2) cash or in kind allowances (the housing allowance,

which varies by grade, location, and dependency status, and a subsistence allowance) and (3) the

tax advantages accruing to allowances because they are not subject to Federal income tax. Basic

pay represents approximately 72 percent of RMC for all retirement eligibles. For the 20-year

retiree, basic pay is approximately 69 percent of RMC. Consequently, a 20-year retiree may be

entitled to 50 percent of basic pay, but only 35 percent of RMC. For a 30-year retiree, the

corresponding entitlements are 75 percent of basic pay, but only 56 percent of RMC. These

relationships should be considered when military retired pay is compared to compensation under

other retirement systems.

Social Security Benefits

Many military members and their families receive monthly benefits indexed to the CPI from Social

Security. As full participants in the Social Security system, military personnel are in general

entitled to the same benefits and are subject to the same eligibility criteria and rules as other

employees. Details concerning the benefits are covered in other publications.

___________________________________________________ Overview

9

Beginning in 1946, Congress enacted a series of amendments to the Social Security Act that

extended some benefits to military personnel and their survivors. These “gratuitous” benefits

were reimbursed out of the general fund of the U.S. Treasury. The Servicemen’s and Veterans’

Survivor Benefits Act brought members of the military into the contributory Social Security

system effective January 1, 1957.

For the Old Age, Survivors, and Disability Insurance (OASDI) program, military members must

contribute the employee portion of the OASDI payroll tax, with the Federal Government

contributing the matching employer contribution. Only the basic pay of a military member

constitutes wages for social security purposes. One feature of OASDI unique to military

personnel grants a noncontributory wage credit of (i) $300 for each quarter between 1956 and

1978 in which such personnel received military wages and (ii) up to $1,200 per year after 1977

($100 of credit for each $300 of wages up to a maximum credit of $1,200). The purpose of this

credit is to take into account elements of compensation such as quarters and subsistence not

included in wages for social security benefit calculation purposes. Under the 1983 Social Security

amendments, the cost of the additional benefits resulting from the noncontributory wage credits

for past service was met by a lump sum payment from general revenues, while the cost for future

service will be met by payment of combined employer-employee tax on such credits as the service

occurs.

Members of the military are also required to pay the Hospital Insurance (HI) payroll tax, with the

Federal Government contributing the matching employer contribution. Medicare eligibility occurs

at age 65, or earlier if the employee is disabled. Entitlement to Medicare usually terminates

entitlement to benefits under TRICARE, DoD’s three-option managed health care program for

the military, although eligibility continues for medical care in military facilities on a space available

basis.

Performance Measures

During FY 1998, the Fund made disbursements to approximately two million retirees and

annuitants. All checks are sent out on a monthly basis.

While there are many ways to measure the funding progress of a pension plan, the ratio of assets

in the fund to the present value of future benefits for annuitants on the roll is commonly used.

Here is what this ratio has been for the last thirteen years:

a. September 30, 1998 = .34567

b. September 30, 1997 = .32200

c. September 30, 1996 = .31314

d. September 30, 1995 = .30375

e. September 30, 1994 = .30306

f. September 30, 1993 = .28314

g. September 30, 1992 = .27018

h. September 30, 1991 = .25127

Overview ______________________________________________ ___

10

i. September 30, 1990 = .21878

j. September 30, 1989 = .19549

k. September 30, 1988 = .16211

l. September 30, 1987 = .11431

m. September 30, 1986 = .07187

This demonstrates a consistent improvement in the strength of the Fund over time. This trend is

expected to continue in future years.

The weighted average yield of the Fund on September 30, 1998 was 8.2%.

Core Performance Measures

No operating costs are calculated for the Fund.

Limitations of the Financial Statements

These financial statements have been prepared to report the financial position and results of

operations for the Military Retirement Trust Fund pursuant to the requirements of the Chief

Financial Officers Act of 1990. While the statements have been prepared from the books and

records of the Military Retirement Trust Fund in accordance with the formats prescribed by the

Office of Management and Budget, the statements are different from the financial statements used

to monitor and control budgetary resources that are prepared from the same books and records.

These statements should be read with the realization that they are for a Federal entity, that

unfunded liabilities reported in the financial statements can not be liquidated without the

enactment of an appropriation, and that the payment of all liabilities other than for contracts can

be abrogated by DoD.

________________________________________ Principal Statements

11

DoD

MILITARY RETIREMENT

TRUST FUND

PRINCIPAL STATEMENTS

Principal Statements _______________________________________

12

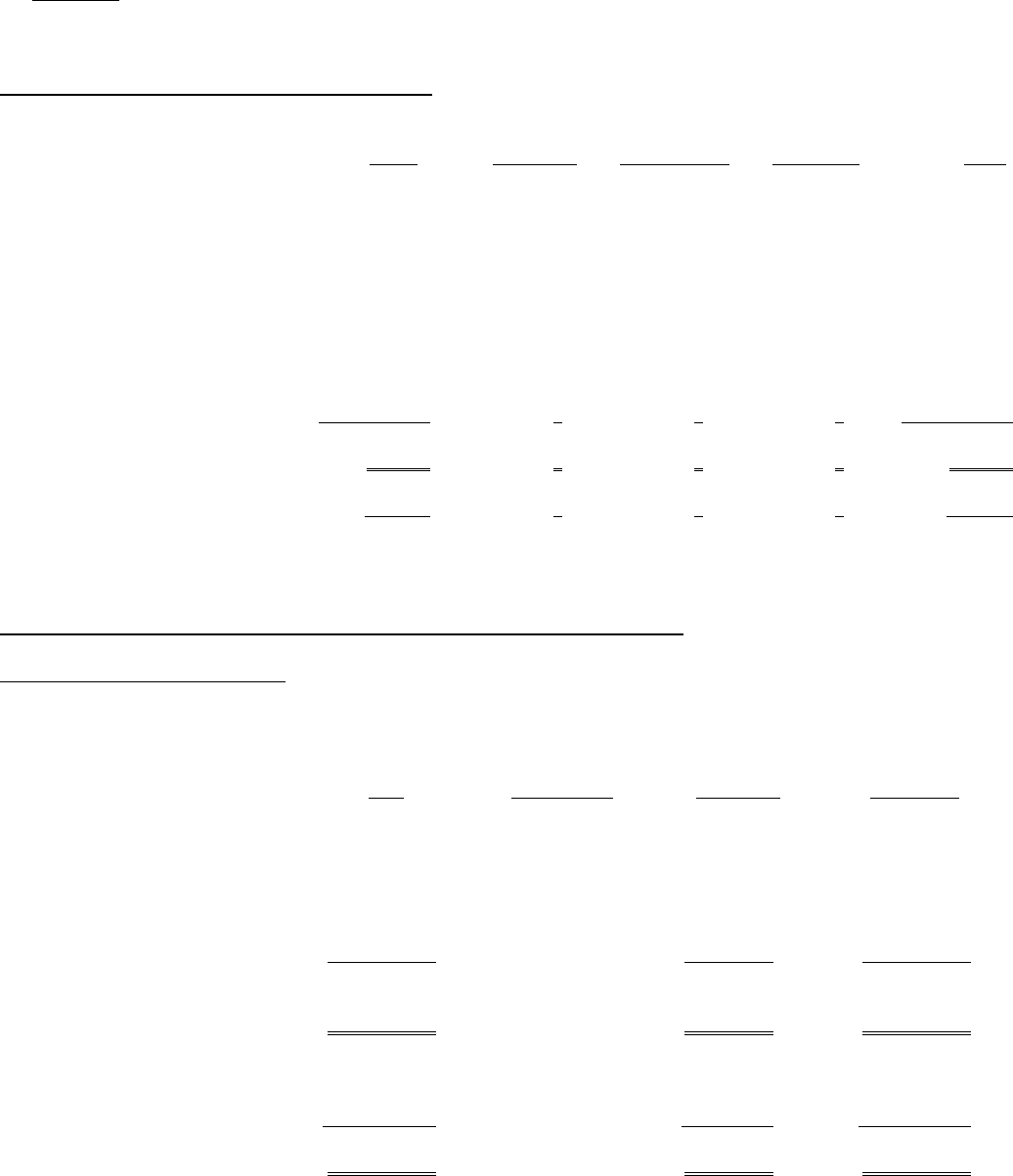

Principal Statements

Department of Defense

Military Retirement Trust Fund

BALANCE SHEET

As of September 30, 1998

($ in Thousands)

FY

1998

ASSETS

1. Entity Assets:

A. Intragovernmental

1. Fund Balance with Treasury (Note 2) $ 20,971

2. Investments, Net (Note 4) 149,855,263

3. Accounts Receivable, Net (Note 5) 0

4. Other Assets (Note 6) 0

B. Total Intragovernmental 149,876,234

C. Investments, Net (Note 4) 0

D. Accounts Receivable, Net (Note 5) 25,738

E. Loans Receivable and Related Foreclosed Property, Net (Note 7) 0

F. Cash and Other Monetary Assets (Note 3) 0

G. Inventory and Related Property, Net (Note 8) 0

H. General Property, Plant and Equipment, Net (Note 9) 0

I. Stewardship Assets (National Defense PP&E, etc.) N\A

J. Other Assets (Note 6) 0

K. Total Entity Assets 149,901,972

2. Non-Entity Assets:

A. Intragovernmental

1. Fund Balance with Treasury (Note 2) $ 0

2. Accounts Receivable, Net (Note 5) 0

3. Other Assets (Note 6) 0

B. Total Intragovernmental 0

C. Accounts Receivable, Net (Note 5) 0

D. Cash and Other Monetary Assets (Note 3) 0

E. Other Assets (Note 6) 0

F. Total Non-Entity Assets 0

3. Total Assets

$ 149,901,972

The accompanying notes are an integral part of these statements.

13

Principal Statements

Department of Defense

Military Retirement Trust Fund

BALANCE SHEET

As of September 30, 1998

($ in Thousands)

FY

1998

LIABILITIES

4. Liabilities Covered by Budgetary Resources:

A. Intragovernmental

1. Accounts Payable $ 0

2. Environmental Cleanup (Note 11) 0

3. Debt (Note 10) 0

4. Other Liabilities (Notes 11, 12, and 15) 0

B. Total Intragovernmental 0

C. Accounts Payable 0

D. Liabilities for Loan Guarantees 0

E. Military Retirement Benefits and Other Employment

Related Actuarial Liabilities (Note 13) 147,178,531

F. Environmental Cleanup (Note 11) 0

G. Other Liabilities (Notes 11, 12, and 15) 2,723,441

H. Total Liabilities Covered by Budgetary Resources 149,901,972

5. Liabilities Not Covered by Budgetary Resources:

A. Intragovernmental

1. Accounts Payable 0

2. Debt (Note 10) 0

3. Environmental Cleanup (Note 11) 0

4. Other Liabilities (Notes 11, 12, and 15) 0

B. Total Intragovernmental 0

C. Accounts Payable 0

D. Debt (Note 10) 0

E. Military Retirement Benefits and Other Employment

Related Actuarial Liabilities (Note 13) 497,145,173

F. Environmental Cleanup (Note 11) 0

G. Other Liabilities (Notes 11, 12, and 15) 127

H. Total Liabilities Not Covered by Budgetary Resources 497,145,300

6. Total Liabilities $ 647,047,272

NET POSITION

7. Unexpended Appropriations (Note 14) $ 0

8. Cumulative Results of Operations (497,145,300)

9. Total Net Position (497,145,300)

10. Total Liabilities and Net Position

$ 149,901,972

The accompanying notes are an integral part of these statements.

14

Principal Statements

Department of Defense

Military Retirement Trust Fund

STATEMENT OF NET COST

For the period ending September 30, 1998

($ in Thousands)

FY

1998

1. Program Costs

A. Intragovernmental $ 0

B. With the Public 33,842,108

C. Total Program Cost 33,842,108

D. Less: Earned Revenues (37,771,030)

E. Net Program Costs $ (3,928,922)

2. Costs Not Assigned to Programs 0

3. Less: Earned Revenues Not Attributable to Programs 0

4. Deferred Maintenance (Note 17) 0

5. Net Cost of Operations

$ (3,928,922)

Additional information included in Note 16.

The accompanying notes are an integral part of these statements.

15

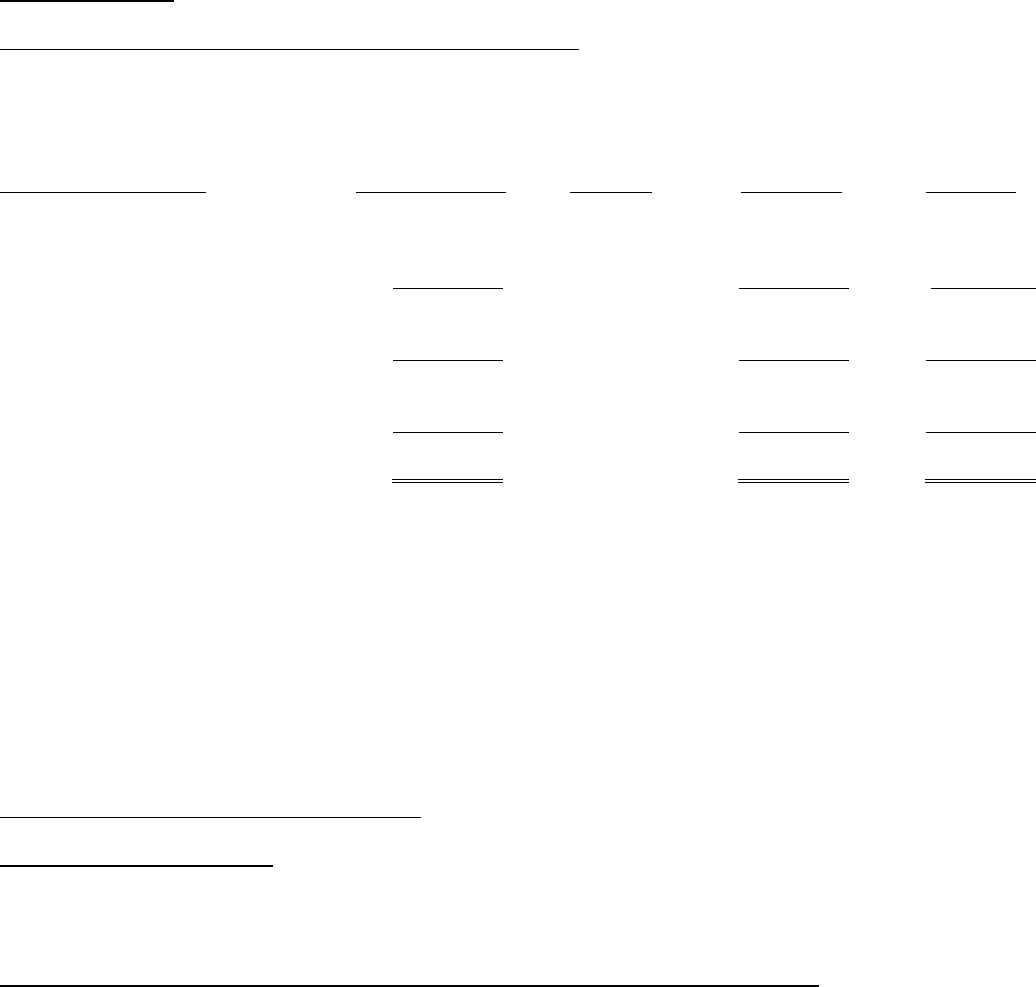

Principal Statements

Department of Defense

Military Retirement Trust Fund

STATEMENT OF CHANGES IN NET POSITION

For the period ending September 30, 1998

($ in Thousands)

FY

1998

1. Net Cost of Operations $ (3,928,922)

2. Financing Sources (Other than Exchange Revenues):

A. Appropriations Used 0

B. Taxes (and Other Non-exchange Revenue) 0

C. Donations (Non-exchange Revenue) 0

D. Imputed Financing 0

E. Transfers-In 0

F. Transfers-Out 0

3. Net Results of Operations (Line 2 less Line 1) 3,928,922

4. Prior Period Adjustments (Note 18) 0

5. Net Change in Cumulative Results of Operations 3,928,922

6. Increase (Decrease) in Unexpended Appropriations 0

7. Change in Net Position 3,928,922

8. Net Position-Beginning of Period (501,074,222)

9. Net Position-End of Period

$ (497,145,300)

Additional information included in Note 18.

The accompanying notes are an integral part of these statements.

16

Principal Statements

Department of Defense

Military Retirement Trust Fund

STATEMENT OF BUDGETARY RESOURCES

For the period ending September 30, 1998

($ in Thousands)

FY

1998

BUDGETARY RESOURCES

1. Budget Authority $ 37,773,868

2. Unobligated Balance - Beginning 136,412,829

of Period

3. Net Transfers Prior-Year Balance, Actual (+/-) 0

4. Spending Authority from Offsetting Collections 0

5. Adjustments 0

6. Total Budgetary Resources $ 174,186,697

STATUS OF BUDGETARY RESOURCES

7. Obligations Incurred $ 31,233,467

8. Unobligated Balances - Available 142,953,230

9. Unobligated Balances - Not Available 0

10. Total Status of Budgetary Resources $ 174,186,697

OUTLAYS

11. Obligations Incurred $ 31,233,467

12. Less: Spending Authority From Offsetting 0

Collections & Adjustments

13. Obligated Balance, Net - Beginning of Period 2,606,084

14. Obligated Balance Transferred, Net 0

15. Less: Obligated Balance, Net - End of Period (2,697,703)

16. Total Outlays $ 31,141,848

Additional information included in Note 19.

The accompanying notes are an integral part of these statements.

17

Principal Statements

Department of Defense

Military Retirement Trust Fund

STATEMENT OF FINANCING

For the period ending September 30, 1998

($ in Thousands)

FY

1998

1. OBLIGATIONS AND NONBUDGETARY RESOURCES:

A. Obligations Incurred $ 31,233,467

B. Less: Spending Authority for Offsetting Collections

and Adjustments 0

C. Donations Not in the Entity's Budget 0

D. Financing Imputed for Cost Subsidies

0

E. Transfers-In (Out)

0

F. Exchange Revenue Not in the Entity's Budget (37,771,030)

G. Other 0

H. Total Obligations as Adjusted and Nonbudgetary

Resources $ (6,537,563)

2. RESOURCES THAT DO NOT FUND NET COST OF OPERATIONS:

A. Change in Amount of Goods, Services, and

Benefits Ordered but Not Yet Received or Provided 0

B. Costs Capitalized on the Balance Sheet 0

C. Financing Sources That Fund Costs of Prior Periods 0

D. Other 0

E. Total Resources That Do Not Fund Net Costs of

Operations 0

3. COSTS THAT DO NOT REQUIRE RESOURCES:

A. Depreciation & Amortization 0

B. Revaluation of Assets & Liabilities 0

C. Other 0

D. Total Costs That Do Not Require Resources 0

4. Financing Sources Yet to be Provided 2,608,641

5. Net Cost of Operations

$ (3,928,922)

Additional information included in Note 20.

The accompanying notes are an integral part of these statements.

18

__________________________________________________________ Footnotes

19

DoD

MILITARY RETIREMENT

TRUST FUND

FOOTNOTES

TO THE

PRINCIPAL STATEMENTS

Footnotes __________________________________________________________

20

__________________________________________________________ Footnotes

21

NOTES TO THE DOD MILITARY RETIREMENT TRUST FUND PRINCIPAL STATEMENTS

AS OF SEPTEMBER 30, 1998

NOTE 1. SIGNIFICANT ACCOUNTING POLICIES

A. Basis of Presentation. The Department of Defense (DoD) Military Retirement Trust Fund was authorized by Public Law (PL)

# 98-94 for the accumulation of funds to finance the liabilities of the DoD under military retirement and survivor benefit programs.

These financial statements have been prepared to meet the requirements of the Chief Financial Officers (CFO) Act of 1990 and other

appropriate legislation. They have been prepared from the books and records of Reporting Division A, Office of the Assistant Deputy

Director for Reporting, Accounting Directorate, Defense Finance and Accounting Service, in accordance with the requirements of the

Office of Management and Budget (OMB) Bulletin No. 97-01, as amended, “Form and Content of Agency Financial Statements,” and

subsequent issues.

The program is funded by:

(1) Annual unfunded liability payment from Treasury.

(2) Monthly Service contributions as a percentage of base pay.

(3) Interest on investments.

B. Basis of Accounting. Under the authority of the CFO Act of 1990, the Federal Accounting Standards Advisory Board (FASAB)

was established to recommend Federal accounting standards to the Secretary of the Treasury, the Director of the Office of

Management and Budget and the Comptroller General, co-principals of the Joint Financial Management Improvement Program

(JFMIP). The Statement of Federal Financial Accounting Standards (SFFAS) have been issued by the Director of OMB and the

Comptroller General, some of with deferred effective dates. In the event the SFFAS’s do not address transactions, the following

hierarchy provides sources of accounting principles for the Federal Government: (1) Individual standards agreed to by the Director of

OMB, the Comptroller General and the Secretary of the Treasury and published by OMB and the General Accounting Office (GAO);

(2) Interpretations related to the SFFAS’s issued by OMB in accordance with the procedures contained in OMB Circular A-134,

“Financial Accounting Principles and Standards;” (3) Requirements contained in OMB’s Form and Content Bulletin in effect for the

reporting period covered by the financial statements; and (4) Accounting principles published by other authoritative standard-setting

bodies and other authoritative sources. This hierarchy is a comprehensive basis of accounting other than generally accepted

accounting principles.

To comply with the CFO Act, Military Retirement Trust Fund financial statements are presented in conformity with OMB Bulletin 97-

01, Form and Content of Agency Financial Statements. This represents a fundamental change in presentation from the prior year. In

fiscal year 1997, the financial statements were prepared in accordance with the requirements of the OMB Bulletin 94-01 and the

effective provisions of OMB Bulletin 97-01. As a result, fiscal year 1998 is the transition year, and accordingly, the financial

statements do not contain comparative information. Differences in the basis of presentation include form and content changes to

existing statements and the following new statements:

• Statement of Net Cost

• Statement of Budgetary Resources

• Statement of Financing

C. Investments in U.S. Government Securities. Intragovernmental securities represent nonmarketable securities issued by the United

States Treasury’s Bureau of Public Debt. These securities are redeemable at market value exclusively through the Federal Investment

Branch. These nonmarketable market-based Treasury securities are not traded on any securities exchange, but mirror the prices of

marketable securities with similar terms. Investments are recorded at amortized cost on the Balance Sheet.

D. Actuarial Information. The Military Retirement Trust Fund financial statements present the unfunded actuarial liability

determined as of the end of the fiscal year based on population information as of the beginning of the year and updated using accepted

actuarial techniques. The “projected benefit obligation” method is used as required by the Statement of Federal Financial Accounting

Standards (SFFAS) No. 5, “Accounting for Liabilities of the Federal Government.”

Footnotes __________________________________________________________

22

E. Estimates. The preparation of financial statements requires management to make estimates and assumptions that affect amounts

reported in the financial statements and accompanying notes. Such estimates and assumptions could change in the future as more

information becomes known, which could inpact the amounts reported and disclosed herein.

NOTE 2. FUND BALANCES WITH TREASURY:

($ in Thousands)

Trust Revolving Appropriated Other Fund

Funds Funds Funds Types Total

A. Entity Fund and Account Balances:

Unobligated Balance Available

Available $142,953,231 0 0 0 $142,953,231

Restricted 0 0 0 0 0

Reserve for Anticipated 0 0 0 0 0

Obligated Balance, Net 2,697,703 0 0 0 2,697,703

Unfunded Contract Authority 0 0 0 0 0

Unused Borrowing Authority 0 0 0 0 0

Other (145,629,963) 0 0 0 (145,629,963)

Total Entity Treasury Balance $20,971 0 0 0 $20,971

B. Non-Entity Fund and Account Balance 0 0 0 0 0

C. Other Information: Securities are redeemed to cover expenses. “Other” represents the value of investments, net; as discussed in

Note 4.A.

NOTE 3. CASH, FOREIGN CURRENCY AND OTHER MONETARY ASSETS: Not applicable

NOTE 4. INVESTMENTS, NET:

($ in Thousands)

(1) (2) (3) (4)

Amortized

Amortization Premium/ Investments

Cost Method (Discount) Net

A. Intragovernmental

Securities:

(1) Marketable 0 0 0

(2) Non-Marketable

Par Value 0 0 0

(3) Non-Marketable

Market Based $153,401,460 Effective Interest $7,771,497 $145,629,963

Subtotal $153,401,460 $7,771,497 $145,629,963

(4) Accrued Interest 4,225,300 4,225,300

Total $157,626,760 $7,771,497 $149,855,263

B. Other Securities:

Not applicable 0 0 0

Subtotal 0 0 0

C. Total $157,626,760 $7,771,497 $149,855,263

__________________________________________________________ Footnotes

23

D. Other Information: The Market Value of comparable Treasury securities as of September 30, 1998, is $173,616,650. The

calculated yields match up with yields in published security tables of U.S. Treasury securities.

NOTE 5. ACCOUNTS RECEIVABLE, NET:

($ in Thousands)

(1) (2) (3)

Allowance for

Gross Amount Estimated Net Amount

Due Uncollectibles Due

A. Entity Receivables:

Intragovernmental 0 0 0

With the Public $25,738 0 $25,738

B. Non-Entity Receivables:

Intragovernmental 0 0 0

With the Public 0 0 0

C. Allowance Method Used: Not applicable

D. Other Information: Accounts Receivable With the Public represents Refunds Receivable of overpayments of benefits.

NOTE 6. OTHER ASSETS: Not applicable

NOTE 7. DIRECT LOANS AND LOAN GUARANTEES, NON-FEDERAL BORROWERS: Not applicable

NOTE 8. INVENTORY AND RELATED PROPERTY: Not applicable

NOTE 9. GENERAL PROPERTY, PLANT, AND EQUIPMENT (PP&E), NET: Not applicable

NOTE 10. DEBT: Not applicable

NOTE 11.B. OTHER LIABILITIES:

($ in Thousands)

1. Other Liabilities Covered by Budgetary Resources

Noncurrent Current

Liability Liability Total

(a) Intragovernmental: Not applicable

(b) With the Public

(1) Accrued Funded Payroll and Benefits 0 0 0

(2) Advances from Others 0 0 0

(3) Deferred Credits 0 0 0

(4) Deposit Funds and Suspense Accounts 0 0 0

(5) Other Liabilities 0 $2,723,441 $2,723,441

Total 0 $2,723,441 $2,723,441

2. Other Information: Accrued entitlement benefits for military retirees and survivors.

3. Other Liabilities Not Covered by Budgetary Resources: Not Applicable

Footnotes __________________________________________________________

24

NOTE 12. LEASES: Not applicable

NOTE 13. PENSIONS AND OTHER ACTUARIAL LIABILITIES:

($ in Thousands)

(1) (2) (3) (4)

Actuarial Present Assumed Assets Unfunded

Value of Projected Interest Available to Actuarial

Major Program Activities Plan Benefits Rate (%) Pay Benefits Liability

A. Pension and Health Benefits

1. Military Retirement Pensions $644,323,704 6.5 $147,178,531 $497,145,173

2. Military Retirement Health Benefits 0 0 0

B. Insurance/Annuity Programs:

1. Not Applicable 0 0 0

C. Other:

1. Not Applicable 0 0 0

D. Total Lines A+B+C: $644,323,704 $147,178,531 $497,145,173

E. Other Information:

1. Actuarial Cost Method Used: Aggregate entry-age normal method.

2. Assumptions: The Military Retirement System is a single-employer, defined benefit plan. Administrative costs are not borne by

the Trust Fund. Projected revenues, authorized by PL 98-94, will be paid into the Fund at the beginning of each fiscal year by the

Secretary of the Treasury as certified by the Secretary of Defense. This permanent, indefinite appropriation, determined by the

Board of Actuaries, represents the amortization of the unfunded liability for service performed prior to October 1, 1984, as well as

the amortization of unfunded liabilities resulting from gains and losses since then. The annual interest rate is assumed to be 6.5%.

The long-term inflation rate is assumed to be 3.5%; the long-term annual salary increase is assumed to be 4.0%. For fiscal years

1998 and 1999, the actual inflation rates of 2.1% and 1.3%, and the actual salary increases of 2.8% and 3.6% were used. Other

assumptions, such as mortality and retirement rates, are developed from actual experience.

NOTE 14. UNEXPENDED APPROPRIATIONS: Not applicable

NOTE 15. CONTINGENCIES :

($ in Thousands)

This represents the Death Payment Contingency of $127; Not Covered by Budgetary Resources.

NOTE 16. FOOTNOTE DISCLOSURES RELATED TO THE STATEMENT OF NET COST :

($ in Thousands)

The amount of $33,842,108 shown on Line l.C. of the Statement of Net Cost is different than that of Line 11 on the Statement of

Budgetary Resources. The amount of $31,233,467 on Line 11 does not include the net changes in Actuarial Liabilities of $2,608,632

and Death Payment Contingencies of $9. Line 1.D., Earned Revenues, consists of Service Contributions as a percentage of base pay of

$10,420,687; the Annual Unfunded Liability Payment of $15,119,000, and Interest on Investments of $12,231,343.

__________________________________________________________ Footnotes

25

NOTE 16G: BENEFIT PROGRAM EXPENSE:

($ in Thousands)

DoD Military Retirement Trust Fund

For the year ended September 30, 1998

1. Service Cost $10,420,687

2. Period Interest on the Benefit Liability $41,045,712

3. Prior (or Past) Service Cost 0

4. Period Actuarial (Gains) or Losses ($17,624,300)

NOTE 16H: GROSS COST AND EARNED REVENUE BY BUDGET FUNCTIONAL CLASSIFICATION:

($ in Thousands)

Budget

Function Gross Earned Net

Code Cost Revenue Cost

A. Department of Defense Military: Not Applicable

B. Water Resources by US Army Corps of

Engineers: Not Applicable

C. Pollution Control and Abatement by US

Army Corps of Engineers: Not Applicable

D. Federal Employee Retirement and Disability

by DoD Military Retirement Trust Fund 602 $33,842,108 $37,771,030 ($3,928,922)

E. Veterans Education, Training, and Rehabilitation

by Department of Defense Education Benefits

Trust Fund: Not Applicable __________ __________ __________

Total $33,842,108 $37,771,030 ($3,928,922)

NOTE 17. DEFERRED MAINTENANCE ON PROPERTY, PLANT, AND EQUIPMENT: Not applicable

NOTE 18. FOOTNOTE DISCLOSURES RELATED TO THE STATEMENT OF CHANGES IN NET POSITION: Not

applicable

NOTE 19. FOOTNOTE DISCLOSURES RELATED TO THE STATEMENT OF BUDGETARY RESOURCES: Not

applicable

NOTE 20. FOOTNOTE DISCLOSURES RELATED TO THE STATEMENT OF FINANCING :

($ in Thousands)

Guidance from OMB (Circular No. A-34), requires Revenue and Financing Sources designated as “available” to be placed on Line

1.A. of the Report on Budget Execution. The difference between line 1. A. of the Report on Budget Execution and the amount shown

on Line 1.F. of the Statement of Financing is ($2,839). The difference is due to the decrease in Accrued Interest Receivable, which is

explained in Note 22. Line 4. “Financing Sources Yet to be Provided” has a balance of $2,608,641 that is made up of the net changes

in the Actuarial Liability of $2,608,632 and the Death Payment Contingency of $9.

NOTE 21. FOOTNOTE DISCLOSURES RELATED TO THE STATEMENT OF CUSTODIAL ACTIVITY: Not applicable

Footnotes __________________________________________________________

26

NOTE 22. INTER-AGENCY ELIMINATIONS:

($ in Thousands)

DoD Military Retirement Trust Fund Column A Column B Column C

Accounts Unearned

Receivable With Revenue With Revenue From

Other Federal Other Federal Other Federal

Entities Entities Entities

Part A. DoD Eliminations of Seller Activity With Other

Federal Agencies Arrayed by DoD Entities N/A $12,234,182 N/A

Total N/A $12,234,182 N/A

Part B. DoD Eliminations of Seller Activity Arrayed By

Other Federal Agencies

Department of the Treasury (TI 20) N/A $12,234,182 N/A

Total N/A $12,234,182 N/A

Other Information: For securities purchased on October 1, 1986, and subsequent, discount and premium are amortized through

account 97X8097.2, Earnings on Investments. The amortization of discount and premium for securities purchased prior to October 1,

1986, is reported to Treasury by changing the Preclosing Unexpended Balance for account 97X8097.941 on report FMS 2108. Gains

and losses on securities sold are also reported through account 97X8097.2. A total of $12,357,964 was reported to account 97X8097.2

during fiscal year 1998. Amortization of ($123,782) was reported to Treasury via the FMS 2108. These two amounts equal

$12,234,182 as reported in Column B, above.

The Statement of Financing, Line 1.F., shows Exchange Revenue Not in the Entity’s Budget totaling $37,771,030. The Report on

Budget Execution, Line 1, shows $37,773,869. The difference of $2,839 is attributable to a decrease in Accrued Interest Receivable as

shown below:

Interest collected (cash) $13,593,437

Amortized Premium (1,427,882)

Amortized Discount 68,627

Subtotal $12,234,182

Decrease in Accrued Interest Receivable (2,839)

Total Interest $12,231,343

NOTE 23. OTHER DISCLOSURES:

($ in Thousands)

Net Pension Expense: The net pension expense for the actuarial accrued liability is developed in the table below.

A. Beginning of Year Accrued Liability $641,715,072

B. Normal Cost Liability 10,420,687

C. Plan Amendment Liability 0

D. Benefit Outlays (31,233,467)

E. Interest on Pension Liability 41,045,712

F. Actuarial Loss (Gain) (17,624,300)

G. End-of-Year Accrued Liability (A+B+C+D+E+F) $644,323,704

H. Net Change in Actuarial Liabilities (B+C+D+E+F) $ 2,608,632

Other Information: The interest on the pension liability (Line E) is calculated as a full year of interest on the beginning-of-

year accrued liability (Line A) and one-half year of interest on the normal cost liability and the benefit outlays (Lines B and D). A bill

__________________________________________________________ Footnotes

27

has been introduced in the U.S. Congress to improve pay and retirement equity for members of the Armed Forces. The proposed

legislation would increase basic pay rates, enhance retirement options, and provide certain other benefits. No effect has been given in

the accompanying financial statements for the impact of the proposed legislation.

Footnotes __________________________________________________________

28

_______________________________________________ Supplemental

29

DoD

MILITARY RETIREMENT

TRUST FUND

SUPPLEMENTAL FINANCIAL

AND

MANAGEMENT INFORMATION

Supplemental _______________________________________________

30

_______________________________________________ Supplemental

31

TABLE 1

MILITARY RETIREMENT SYSTEM

ACTUARIAL STATUS INFORMATION

SEPTEMBER 30, 1998

($ in thousands)

Sept 30, 1998

1. Present value of future benefits

a. Annuitants now on roll $425,783,099

b. Non-retired reservists $26,138,048

c. Active duty personnel

1

$272,972,526

d. Total $724,893,673

2. Present value of future normal cost contributions $80,569,969

3. Actuarial accrued liability $644,323,704

4. Assets

2

$147,178,531

5. Unfunded accrued liability $497,145,173

________________________________

1

The future benefits of active duty personnel who are projected to retire as reservists are

counted on line 1-b.

2

The assets available to pay benefits are determined using the amortized cost method (book

value) of valuation.

Supplemental _______________________________________________

32

_______________________________________________ Audit Opinion

33

DoD

MILITARY RETIREMENT

TRUST FUND

AUDIT OPINION

Audit Opinion _______________________________________________

34