UNUM LIFE INSURANCE COMPANY OF AMERICA

1

MD

Actuarial Memorandum

Group Long Term Care

May 2019

Maryland

PUBLIC

Form Number Description Certificate Issue Date

B.LTC, TQB.LTC

Long Term Care Indemnity Policy

October 1, 1992- June 1, 2018

GLTC95, TQGLTC95

Long Term Care Indemnity Policy

December 1, 1985 – June 1, 2018

These group long term care policy forms were actively marketed through 2004. Although

no longer actively marketed, new employees have been added after 2004 and can still be

added to existing inforce group policies.

These policy forms were originally priced prior to rate stability under the NAIC model regu-

lation, however certificates have been added after rate stability and new employees will

continue to be added. Therefore, this filing is being made according to rate stabilization re-

quirements consistent with the previous approved rate increase filings under SERFF num-

bers, U

NUM-128291722 in 2012, UNUM-129566116 in 2015, UNUM-130425131 in 2016, and UNUM-

130965778 in 2018.

These policy forms were marketed primarily to employers. In a few instances, policyholders

may be associations or other eligible groups permitted by state law. Therefore, the terms

“employer” and “employee” used in this Memorandum include “group policyholder” and “in-

sured.”

We respectfully request non-disclosure of this actuarial memorandum, if your Department

grants it.

1. Scope & Purpose

This actuarial memorandum has been prepared for the purpose of demonstrating that the loss

ratio requirements have been met in your state with respect to premium rate increases and

is not intended to be used for other purposes.

2. Benefit Description

Long Term Care Facility Benefit: Pays 100% of the daily maximum benefit.

Assisted Facility Benefit: Pays maximum of the Home and Community Care Benefits or 60%

of the Long Term Care Facility Daily Benefit.

Bed Reservation Benefit: up to 15 days per calendar year.

Respite Care Benefit: Provides temporary relief to primary informal caregiver from his or her

caregiving duties. The policy provides respite care benefits for up to 15 days each calendar

year.

UNUM LIFE INSURANCE COMPANY OF AMERICA

2

MD

Waiver of Premium: Premiums are waived after the insured satisfies the elimination period

and is receiving benefits.

Optional Benefits

• Home and Community Care Benefits: Pays 50%, 75% or 100% of the Long Term Care

Facility Daily Benefit. Includes adult day care and hospice care. A total home option

is also available that provides coverage for informal care.

• Accelerated Premium Payment Options

• Non-forfeiture

• Inflation Protection: Insured can select simple or compound 5% inflation protection.

A two times cap is also offered.

• Return of Premium at Death

3. Renewability

These are guaranteed renewable group long term care policies and certificates.

4. Applicability

This filing is applicable to inforce and new certificate holders. These policy forms are no

longer being sold in the market. The premium changes will apply to the base rates of the

policy. New certificates will be added at the rates applicable at the time they are issued and

subject to future applicable rate changes.

5. Actuarial Assumptions

Confidential

6. Trend Assumptions

As this is not medical insurance, we have not included any explicit medical cost trends in the

projections.

7. Marketing Method

Coverage under in-force group policies was offered through the worksite marketplace to meet

the needs of the employer and employees. Marketing was done through plan administrators

and employer sponsorship. This product is no longer marketed.

8. Underwriting Description

This product is subject to medical underwriting. Guarantee issue and modified medical under-

writing are available to active employees in an employer group where the plan offered meets

specified risk characteristics (e.g. minimum participation requirements, employer funding).

9. Premium Classes

The base policy premium rates vary by issue age, benefit period, inflation option, and home

care benefit percentage. Base premiums also vary by elimination period, the inclusion of a

reduced paid-up benefit and cognitive impairment for policy form B.LTC. Premium rates within

UNUM LIFE INSURANCE COMPANY OF AMERICA

3

MD

a specified group do not vary. Employees, spouses and other eligible participants will have the

same premium rates. Premium rates do not change when a participant ports their coverage.

10. Premium Modes

Available premium modes include annual, semi-annual, quarterly, monthly and monthly elec-

tronic funds transfer. Factor adjustments for modes other than annual are unchanged from

the initial rate filing.

11. Issue Ages

The issue ages are age 18 to 100.

12. Area Factors

Area factors within your state are not used for this product.

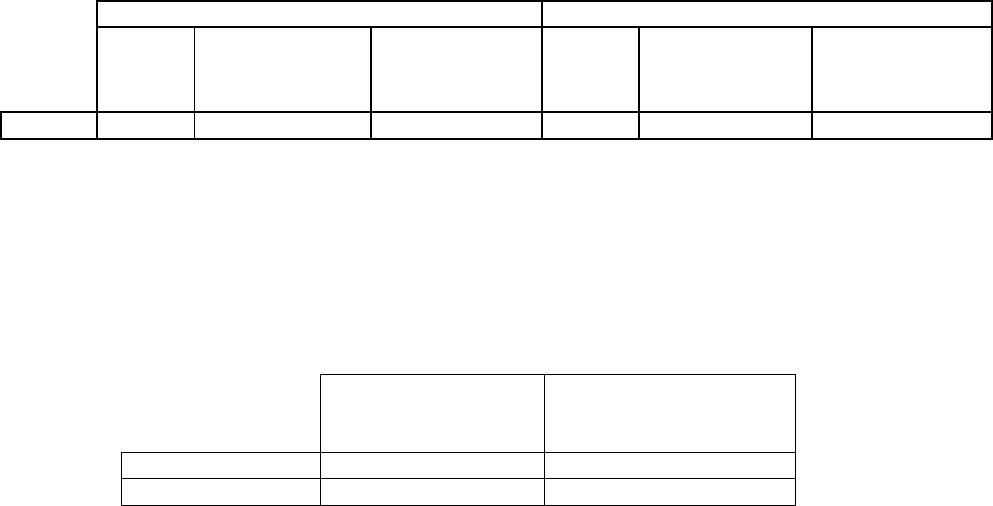

13. Average Annual Premium

The table below summarizes the average annual premium per policy before and after the

requested rate increase, both nationwide and in your state based on the proposed rate in-

creases in your state.

Nationwide

Maryland

Cur-

rent

With Approved

Rate Increases

After Proposed

Rate Increase

Cur-

rent

With Approved

Rate Increases

After Proposed

Rate Increase

Total

521

570

1,117

627

667

753

*The nationwide “After Proposed Increase” cell above represents the expected average nationwide

premium after implementing the remaining balance of our 2012 rate increase initiative of 75% plus

our proposed new 2019 initiative.

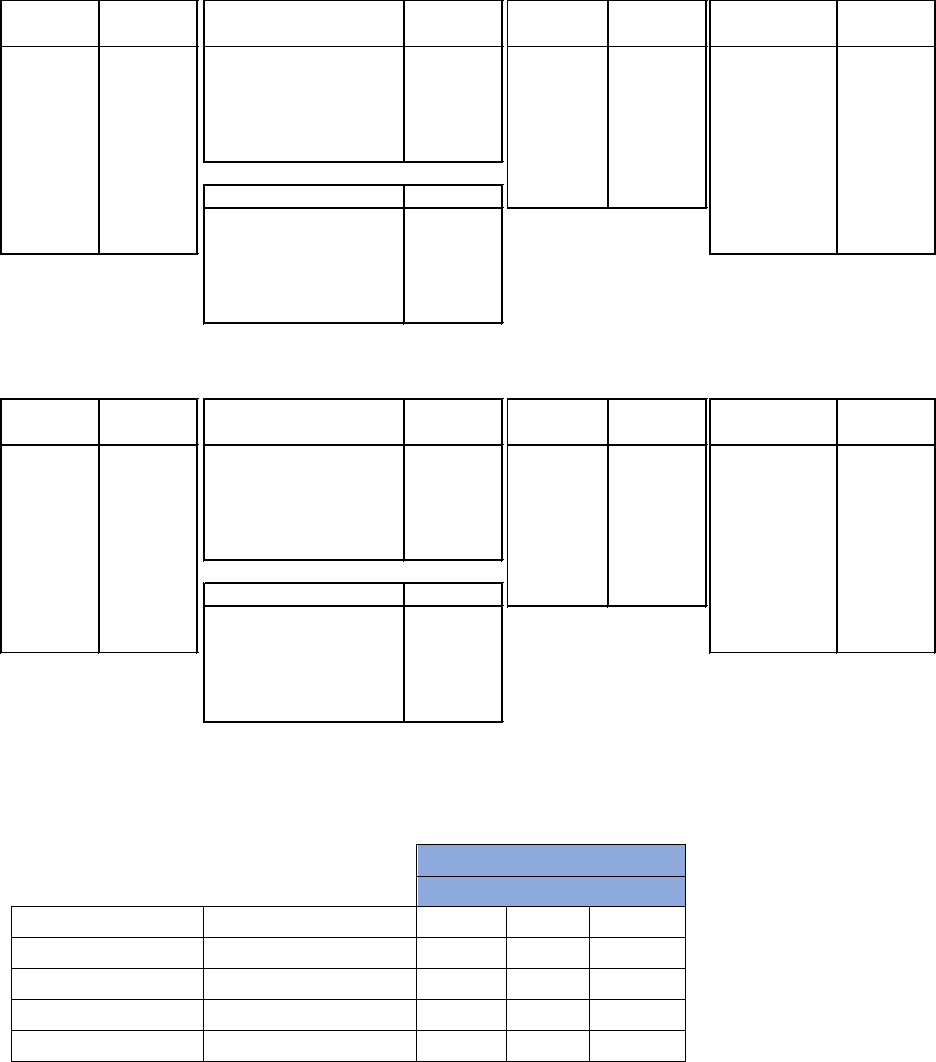

14. Number of Certificateholders

The table below summarizes the number of premium-paying policies inforce and their annu-

alized premium as of 6/30/2018.

Number of Policies

Annualized Premium

Maryland

9,247

6,171,643

Nationwide

489,757

279,234,412

15. Distribution of Business

The table below summarizes, as of 6/30/2018, the distribution of insureds by several charac-

teristics.

This information below is based on national inforce business.

UNUM LIFE INSURANCE COMPANY OF AMERICA

4

MD

The information below is based on Maryland inforce business.

16. History of Previous Rate Revisions

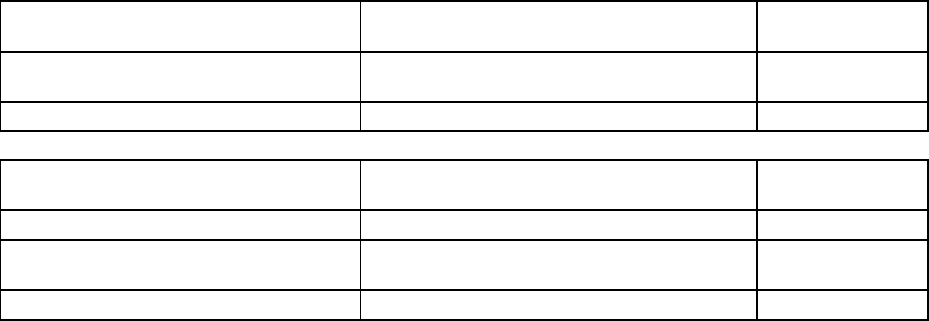

The following average rate increases were previously approved in your state.

Policy Form Series

B.LTC &GLTC95

Rate Increase

SERFF Number

Year

Month

Amount

1st Increase

UNUM-128291722

2012

11

15%

2nd Increase

UNUM-129566116

2015

4

15%

3rd Increase

UNUM-130425131

2016

3

15%

4th Increase

UNUM-130965778

2018

1

5.2%

Please see Exhibit 3 for historical filings and the current filing status of rate increases in

other states.

Issue Age %

Inflation T ype

%

Benefit

Period

%

Attained Age %

<40 37.3% Compound Uncapped 15.4% 2 7.4% <40 17.2%

40-44 13.6% Simple Uncapped 8.9% 3 55.4% 40-44 7.9%

45-49 14.7% Compound Capped 1.3% 4 2.2% 45- 49 9.9%

50-54 14.7% Simple Capped 11.4% 5 5.1% 50-54 10.9%

55-59 11.5% No Inflation 63.0% 6 22.3% 55-59 13.0%

60-64 5.9% 10 0.2% 60- 64 13.4%

65-69 1.7%

Eliminat ion Period %

Lifetime 7.4% 65- 69 11.5%

70-74 0.4% 0 0.1% 70-74 8.9%

75+ 0.1% 30 0.9% 75+ 7.2%

60 3.7%

90 92.8%

100+ 2.4%

Issue Age % Inflation T ype %

Benefit

Period

% Attained Age %

<40

31.0% Compound Uncapped 32.3% 2 4.3% <40 12.7%

40-44 11.6% Simple Uncapped 0.2% 3 67.0% 40-44 5.9%

45-49 14.7% Compound Capped 0.0% 4 0.0% 45- 49 6.9%

50-54 16.9% Simple Capped 1.0% 5 4.4% 50- 54 9.4%

55-59 15.0% No Inflation 66.6% 6 19.5% 55-59 12.0%

60-64 7.6% 10 0.0% 60- 64 13.6%

65-69 2.4%

Eliminat ion Period % Lifetime 4.8% 65- 69 14.4%

70-74 0.6% 0 0.2%

70-74 13.2%

75+ 0.1% 30 10.8% 75+ 11.9%

60 0.5%

90 88.4%

100+ 0.1%

UNUM LIFE INSURANCE COMPANY OF AMERICA

5

MD

17. Requested Rate Increase

Per guidance form the Maryland Insurance Administration, the Company is limiting its request

to 15% on voluntary and employer funded policies with compound uncapped, 15% on volun-

tary policies with capped inflation, and 6.8% on policies with no inflation. This is an average

aggregate rate increase request of 9.5% per insured, that varies by inflation coverage.

The anticipated full rate increase needed is outlined below.

Employer Funded (Non-Vol-

untary)

Rate Increase Needed

Number of

Insureds

Compound Uncapped Inflation

15% for 6 years and 9.5% for 1

year

761

No Inflation

6.8% for 1 year

4,381

Voluntary (100% Employee

Paid)

Rate Increase Needed

Number of

Insureds

Compound Uncapped Inflation

15% for 9 years

2,229

Compound and Simple Capped

Inflation

15% for 4 years

89

No Inflation

6.8% for 1 year

1,787

“Employer Funded” indicates that some portion of the premium is paid by the employer where

all employees or sub-class of employees are provided some level of employer-paid base cov-

erage. “Voluntary” indicates that 100% of the premiums are paid by the employee.

“Capped Inflation” refers to 5% annual inflation growth until the monthly benefit doubles.

18. Reserves

Active life reserves have not been used in this rate increase demonstration. Statutory claim

reserves as of 06/30/2018 have been discounted to the date of incurrals of each respective

claim and included in the historical incurred claims. Incurred But Not Reported claim re-

serves as of 06/30/2018 have also been allocated to the expected calendar year of incurrals

and included in historical incurred claims and runoff in the projected experience.

19. Past and Future Projected Policy Experience and Demonstration of Satisfac-

tion of Loss Ratio Requirements

Confidential

20. Cost of Waiting

Confidential

21. Proposed Effective Date

The rate increase will apply to policies on their policy anniversary date following a 60-day

policyholder notification period.

22. Similar Forms

There are no similar forms currently marketed by the company.

UNUM LIFE INSURANCE COMPANY OF AMERICA

6

MD

23. Actuarial Certification

I am a Fellow of the Society of Actuaries and a Member of the American Academy of Actuar-

ies. I meet the Academy’s qualification standards for rendering this opinion and am familiar

with the requirements for filing long-term care insurance premiums and filing for increases

in long-term care insurance premiums.

To the best of my knowledge, this rate filing is in compliance with the applicable laws and

regulations of this state. This memorandum has been prepared in conformity with all appli-

cable Actuarial Standards of Practice including ASOP Number 8.

I certify that renewal premium rate schedules are not greater than new business premium

rates schedules except for differences attributable to benefits. Unum is no longer writing any

new group long term care employer policies.

I have taken into consideration the policy design, underwriting, and claims adjudication

practices.

To the best of my knowledge, the premium rate increase requests outlined in Section 17 of

this memorandum are necessary to certify that the premium rate schedules are sufficient to

cover anticipated cost under moderately adverse experience, if the underlying assumptions

are realized and the premium rates schedules are reasonably expected to be sustainable

over the life of the policies with no further premium rate schedule increases anticipated.

Emerging experience will continue be monitored to assess future rate increase needs.

Ronald L. Lucas, F.S.A., M.A.A.A.

Vice President, Long Term Care Pricing

Unum

2211 Congress St.

Portland, ME 04122

Ph: 207-575-3895

Email: rlucas@Unum.com