U.S. Department of the Interior

Office of Inspector General

AUDIT REPORT

ASSESSMENT AND COLLECTION OF

GROSS RECEIPTS TAXES,

DEPARTMENT OF REVENUE

AND TAXATION,

GOVERNMENT OF GUAM

REPORT NO. 98-I-570

JULY 1998

United States Department of the Interior

OFFICE OF INSPECTOR GENERAL

N-IN-GUA-003-97

Washington, D.C. 20240

Honorable Carl T.C. Gutierrez

Governor of Guam

O&e of the Governor

Agana, Guam 96910

Subject:

Audit Report on Assessment and Collection of Gross Receipts Taxes, Department

of Revenue and Taxation, Government of Guam (NO.

98-I-570)

Dear Governor Gutierrez:

This report presents the results of our review of gross receipts taxes at the Department of

Revenue and Taxation during fiscal years 1995, 1996, and 1997 (through

December 3

1,

1996). The objective of our audit was to determine whether the Government

of Guam effectively assessed and collected the gross receipts taxes applicable under Guam

laws and regulations.

Our audit disclosed that the Department of Revenue and Taxation did not ensure that all

delinquent gross receipts taxes were collected and did not use available sources of information

to identity businesses (taxpayers) that had not filed gross receipts tax returns. These

conditions occurred because the Department (1) had transferred Collection Branch personnel

to other divisions, which prevented the Collection Branch from initiating timely enforcement

actions to collect delinquent gross receipts taxes; (2) had not developed written procedures

for conducting an effective nonfiler identification program; (3) had not assigned a program

coordinator and personnel to conduct nonfiler identification programs; and (4) had not

entered income tax information into the Department’s automated income tax system to

provide a method for comparing income reported on income tax returns with income shown

on gross receipts tax returns. As a result, the Government of Guam lost gross receipts taxes

of $724,149 and risks losing additional taxes of at least $1.3 million if timely enforcement

actions are not taken. In addition, based on our limited testing of taxpayer information

sources on Guam, we identified 47 nonfilers who may have owed the Government of Guam

at least $972,486 in gross receipts taxes and related penalties and jnterest.

To correct these conditions, we recommended that you, as the Governor of Guam, require

the Director, Department of Revenue and Taxation, to (1) use all available enforcement

methods to collect delinquent gross receipts taxes, including seizures and sales of taxpayer

property; (2) consider returning the previously transferred personnel to the Collection Branch;

and (3) develop and implement a written plan and assign a program coordinator and personnel

to conduct nonfiler identification programs.

On April 8, 1998, we discussed the preliminary draft of this report with the Department’s

Director, the Tax Enforcement Administrator, and the Taxpayer Services Administrator, all

of whom expressed agreement with the findings and recommendations. In addition, the

Director stated that our report provided him “useful information” that he planned to use as

support for obtaining additional resources needed by the Department to carry out its tax

collection and enforcement activities.

On April 29, 1998, we transmitted a draft of this report to you, requesting your comments

by June 19, 1998. The June 22, 1998, response (Appendix 2) from the Acting Governor

indicated concurrence with all five of the recommendations. Based on the response, we

consider one recommendation resolved and implemented and one recommendations resolved

but not implemented, and we request additional information for three recommendations (see

Appendix 3).

The Inspector General Act, Public Law 95-452, Section S(a)(3), as amended, requires

semiannual reporting to the U.S. Congress on all audit reports issued, the monetary impact

of audit findings (Appendix l), actions taken to implement audit recommendations, and

identification of each significant recommendation on which corrective action has not been

taken.

In view of the above, please provide a response, as required by Public Law 97-357, to this

report by August 18, 1998. The response should be addressed to our Pacific Office, 415

Chalan San Antonio, Baltej Pavilion, Suite 306, Tamuning, Guam 96911. The response

should provide the information requested in Appendix 3.

We appreciate the assistance of the staff of the Department of Revenue and Taxation in the

conduct of our audit.

Sincerely,

$y?‘.

$u-&~

RichardbN. Reback

Acting Inspector General

cc:

Director, Department of Revenue and Taxation

Acting Director, Bureau of Budget and Management Research

CONTENTS

Page

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1

BACKGROUND ,...____..,._._...., ._ __....., ,....,...,....,

I

OBJECTIVE AND SCOPE .

1

PRIORAUDITCOVERAGE . . . . . . . . . . ..___.........__..__.._....

2

FINDINGS AND RECOMMENDATlONS

. . . . .

3

A. COLLECTION OF GROSS RECEIPTS TAXES

r .

3

B. NONFILER IDENTIFICATION PROGRAhi

. . . .

7

APPENDICES

1. CLASSIFICATION OF MONETARY AMOLXTS

. . . . . . . . . .

10

2. ACTLNG GOVERNOR OF GUAM RESPOXSE

.

11

3. STATUS OF AUDIT REPORT RECOMMEhBATIONS

. .

20

INTRODUCTION

BACKGROUND

The Department of Revenue and Taxation is responsible for enforcing all Guam tax laws,

including the gross receipts tax law. Title

11,

Chapter 26, of the Guam Code Annotated

provides the authority for imposing gross receipts taxes, and

Section 26202(a) of Chapter 26

states that businesses (referred to in this report as taxpayers) selling goods and services will

be taxed at a rate of 4 percent on the gross proceeds of sales.

The Director of Revenue and

Taxation is appointed by the Governor of Guam and confirmed by the Guam Legislature and

is responsible for managing the operations of the Department of Revenue and Taxation.

The Department of Revenue and Taxation has three branches that are responsible for

administering Guam’s gross receipts tax law: the Business Privilege Tax Branch and the

Accounting Branch, which are under the Taxpayer Service Division, and the Collection

Branch, which is under the Tax Enforcement Division. The Business Privilege Tax Branch

is responsible for receiving, processing, and verifying the accuracy of information on Monthly

Gross Receipts Tax Returns. The Accounting Branch is responsible for processing payments

of gross receipts taxes and assessing any gross receipts taxes that may be due the Government

of Guam. The Collection Branch is responsible for initiating collection actions to collect any

unpaid or past-due gross receipts taxes. During fiscal year 1997, the Business Privilege Tax

Branch (9 positions), the Accounting Branch (10 positions), and the Collection Branch (38

positions) were authorized a total of 57 full-time positions.

Revenue and Taxation’s records indicated that during fiscal years 1995, 1996, and 1997

(through December 3 1, 1996) the Business Privilege Tax Branch processed 448,288 gross

receipts tax returns with taxes totaling $389 million. During fiscal year 1996, gross receipts

tax revenues totaled $180 million, which is about 34 percent of the Government of Guam’s

total General Fund revenues. Gross receipts taxes receivable increased from $6.7 million at

the end of fiscal year 1994 to $14.9 million at the end of fiscal year 1996.

OBJECTIVE AND SCOPE

The audit objective was to determine whether the Government of Guam effectively assessed

and collected the gross receipts taxes applicable under Guam laws and regulations.

The scope

of the audit covered Revenue and Taxation’s assessment and collection of gross receipts taxes

that occurred during fiscal years 1995, 1996, and 1997 (through December 3 1, 1996).

However, by letter of April 1, 1997, the Inspector General amended the scope of the audit

to include a review of income tax returns and any other records that were necessary to

complete the audit of gross receipts taxes.

Our audit was conducted at Revenue and Taxation’s offices from January to September 1997.

In addition, we obtained information relating to gross receipts taxes from offtcials at the

1

Department of Administration, the Guam Housing and Urban Renewal Authority, the Guam

Legislature, and the Guam Finance Commission. In addition, we visited ofIicials of the

Contracting Services Office at Andersen Air Force Base on Guam to obtain information

related to payments made to contractors that perform work for the military.

The audit was made, as applicable, in accordance with the “Government Auditing Standards,”

issued by the Comptroller General of the United States. Accordingly, we included such tests

of records and other auditing procedures that were considered necessary under the

circumstances.

As part of the audit, we evaluated the system of internal controls relating to processing gross

receipts tax returns, assessing and collecting gross receipts taxes, maintaining taxpayer case

files, and operating nonfiler identification programs to the extent that we considered necessary

to accomplish our audit objective. We found that the Department had adequately assessed

gross receipts tax returns filed by taxpayers. However, significant internal control weaknesses

were identified in the areas of collecting gross receipts taxes, maintaining taxpayer case tiles,

and conducting a nonfiler identification program. These weaknesses are discussed in the

Findings and Recommendations section of this report. Our recommendations, if implemented,

should improve the internal controls in these areas.

PRIOR AUDIT COVERAGE

During the past 5 years, neither the Genera! Accounting Office nor the Office of Inspector

General had audited the Government of Guam’s assessment and collection of gross receipts

taxes. However, on May 2, 1989, the Office of Inspector General issued the report “Gross

Receipts Tax Billing and Collection Practices, Department of Revenue and Taxation,

Government of Guam” (No. 89-70). The report noted deficiencies in tax operations that

resulted in (1) the loss of $118,000 because the 3-year statute of limitation had expired on

various tax cases and (2) the risk of loss of $628,000 in unbilled and undocumented taxes and

$3 million in uncollected delinquent taxes.

In addition, an independent public accounting firm issued single audit reports on the

Department of Revenue and Taxation’s operations for each of fiscal years 1994, 1995, and

1996. These reports showed that (1) account balances were not reconciled at Revenue and

Taxation and at the Department of Administration for checks which were returned by banks

for insufficient funds, (2) about 85 percent of receivables for these checks were more than

120 days past due, (3) the allowance for doubtful accounts could not be verified, and (4)

abatements of taxes receivable were generally not reported to the Department of

Administration.

2

FINDINGS AND RECOMMENDATIONS

A. COLLECTION OF GROSS RECEIPTS TAXES

The Department of Revenue and Taxation did not ensure that delinquent gross receipts taxes

were collected or collected in a timely manner. Title

11,

Chapters

15

and 26, of the Guam

Code Annotated provides time frames for initiating enforcement actions to collect delinquent

gross receipts taxes. However, Collection Branch personnel said that they were not alu-ays

able to initiate enforcement actions in a timely manner because the Collection Branch did not

have a sufficient number of revenue officers to manage the delinquent taxpayer caseload.

As

a result, during fiscal years 1995, 1996, and 1997 (through December 3 1, 1996): the

Government of Guam lost gross receipts tax revenues of at least $724,149 and may be at risk

of losing another $1.3 million of delinquent gross receipts taxes if timely enforcement actions

are not taken.

Enforcement Practices

Title 11, Chapter 15, Section 15 10 1 (a), of the Guam Code Annotated states that “in all cases

ofunpaid gross receipts taxes, demand for payment shall be made in writing within thirty (30)

days of filing unpaid gross receipts tax returns, and liens and levies shall be filed on such

unpaid amounts not later than sixty (60) days of filing unpaid gross receipts tax returns.”

Also, Section 15 102(a) states,

“Repayment may be made over a period of sixty (60) months

or less.” However, Section 15 102(d) states, “Upon default of the delinquent taxpayer in all

or all [sic] of the agreement terms and conditions, the entire amount owed shall be

immediately due and payable, and collection procedures shall be immediately instituted against

the defaulting taxpayer’s property or properties unless the Director of Revenue and Taxation,

on his discretion, finds that the default was excusable, and the taxpayer promptly (within 30

days) cures the default.” In addition, Title 11, Chapter 26, Section 26205, of the Guam Code

Annotated states, “The statute of limitations for collections of unpaid taxes due on gross

receipts tax returns shall be seven (7) years after the return is filed.” Finally, Chapter 15,

Section 15 10 1 (b), “Collection of Delinquent Taxes,”

states, “Nothing herein shall affect the

power of the Department of Revenue and Taxation to levy, seize and sell property at public

auction.” However, we found that Revenue and Taxation did not always comply with these

requirements.

Based on Revenue and Taxation’s December 3 1, 1996, Collection Branch Monthly Activity

Report, the Collection Branch had an outstanding inventory of 5,206 demand for payment

notices that had been issued to 1,415 delinquent taxpayers who owed gross receipts taxes

totaling $14.9 million.

Of the 1,415 taxpayer case files, we selected a judgmental sample of

129 taxpayer case files, which contained 1,007 payment notices totaling about $3.3 million,

to determine whether Revenue and Taxation had complied with statutory requirements for

collecting the delinquent taxes. Of the 129 delinquent taxpayer case files selected for review,

Revenue and Taxation was not able either to locate case files or to produce complete case

3

tiles for 35 taxpayers who owed taxes of $145,465. Therefore, based on our review of the

94 available case tiles, we found that Revenue and Taxation generally issued notices to

delinquent taxpayers within the 30-day period prescribed by the Guam Code and had followed

statutory requirements for collecting delinquent taxes from 30 taxpayers who owed taxes of

$1.2 million.

However, Revenue and Taxation (1) did not comply with statutory

requirements for using liens and levies and enforcing payment agreements against 54

delinquent taxpayers who owed taxes of $1.3 million and (2) did not use available

enforcement actions to collect delinquent taxes from 10 other taxpayers, which resulted in the

loss of gross receipts taxes of $724,149.

Of the 54 delinquent taxpayers that had a total of $1.3 million of past-due taxes, we

determined that Revenue and Taxation had not filed any liens and/or levies against the

property of 20 taxpayers that owed taxes of $219,882 and had not filed liens and/or levies

timely against the property of 24 taxpayers that owed taxes of $694,182. Furthermore, we

found that for five taxpayers that owed delinquent taxes of $179,679, Revenue and Taxation

had not initiated followup collection actions subsequent to filing liens and/or levies against

the taxpayers’ property to ensure that the Government of Guam’s interests in the delinquent

gross receipts taxes were protected. As a result, Re\-enue and Taxation had not collected

delinquent taxes of $1.1 million from these 49 taxpayers.

We also found that Revenue and Taxation did not follow statutory requirements when

enforcing payment agreements with five delinquent taxpayers who owed $234,134. In one

instance, we determined that Revenue and Taxation had entered into a payment agreement

with a delinquent taxpayer who owed taxes of $60,192. However, the payment agreement

allowed the taxpayer to extend payments over a 363-month period, which exceeded the

60-month payment period allowed by law. In addition, we found that four taxpayers, who

owed taxes of $173,942, had defaulted on their payment agreements with Revenue and

Taxation. However, Revenue and Taxation had not taken any action to seize and sell

taxpayer assets to collect the delinquent taxes from these four taxpayers in accordance with

Title 11, Chapter 15, Section 15 10 l(b), of the Guam Code.

Based on our review of the remaining 10 delinquent taxpayer case files, we also determined

that the Government of Guam lost gross receipts tax revenues of at least $724,149 because

Revenue and Taxation had not used available enforcement actions, such as seizures and sales

of property, to collect the delinquent taxes. Specifically, we found that Revenue and Taxation

had not collected delinquent taxes of $40,545 from five taxpayers before expiration of the

7-year statute of limitations.

In addition, we determined that the Government of Guam lost

delinquent taxes of $158,940 because three taxpayers declared bankruptcy and Revenue and

Taxation had not taken adequate steps, such as securing a claim against the taxpayers’ assets,

to protect the Government’s interests. Finally, we found that Revenue and Taxation had

written off delinquent gross receipts taxes of $524,664 from two taxpayers because one

taxpayer had departed Guam and the other taxpayer no longer had any assets to seize.

Based on Revenue and Taxation’s budget documents for fiscal year 1997, we determined that

the Collection Branch was authorized a staff of 38 employees (35 revenue officers, 2 tax

auditors, and 1 support staff). Ofthe 38 employees, we found that the Collection Branch had

4

seven vacancies (6 revenue officers and

1

support stat?) and that 12 of its 29 revenue officers

had been reassigned by a former Director to cover shortages of staff in other Revenue and

Taxation divisions. Therefore, during our audit, the Collection Branch had a staff of 19

employees, According to the Administrator of the Tax Enforcement Division, the shortage

of staff in the Collection Branch had negatively impacted the ability of the Collection Branch

to initiate timely collection actions against delinquent taxpayers. The Administrator also

stated that the Collection Branch would be able to reduce the backlog of delinquent taxpayer

cases (I,4 15 taxpayers as of December 3 1, 1996) if some of the reassigned employees were

returned to the Branch and the seven vacancies were filled. Finally, Collection Branch

personnel and the Acting Collection Branch Supervisor stated that the insufficient numbers

of staff had prevented the Collection Branch from properly managing its delinquent taxpayer

caseload.

We also discussed with the Tax Enforcement Administrator the possibility of using seizures

and sales of property to collect delinquent gross receipts taxes, The Tax Enforcement

Administrator stated that he did not want to use seizures and sales of property because he

believed that enforcement tools such as liens and levies were as effective as the use of seizures

and sales of property. However, during the exit conference on April 8, 1998, the Tax

Enforcement Administrator stated that seizures and sales of property should be used only as

a “last resort” to collect delinquent taxes.

Nevertheless, we believe that by delaying

enforcement actions against delinquent taxpayers, including the use of seizures and sales of

property, Revenue and Taxation risks the loss not only of additional gross receipts tax

revenues as a result of the expiration of the statute of limitations but also the opportunity to

collect tax revenues from taxpayers who may declare bankruptcy or leave Guam.

In addition,

we believe that the number of delinquent tax cases (1,415 taxpayers as of December 3 1,

1996) could be reduced if Revenue and Taxation aggressively pursued the collection of

delinquent gross receipts taxes through the use of seizures and sales of property.

Finally, as noted previously, Revenue and Taxation was unable to locate 35 (27 percent) of

the 129 delinquent taxpayer case files that we selected for review. Therefore, we believe that

Revenue and Taxation should develop written procedures to ensure that taxpayer case files

maintained by the Collection Branch are safeguarded and can be located when needed by the

revenue officers.

Recommendations

We recommend that the Governor of Guam require the Director, Department of Revenue and

Taxation, to:

1. Instruct the Tax Enforcement Administrator to comply with established procedures

for collecting delinquent gross receipts taxes, including the use of seizures and sales of

taxpayer property.

2. Provide the necessary resources to ensure that the Collection Branch reduces its

backlog of delinquent taxpayer cases and collects delinquent gross receipts taxes in a timely

manner.

5

3. Develop and implement written procedures and establish a records management

system to ensure that the Collection Branch controls and safeguards taxpayer case files.

Governor of Guam Response and Office of Inspector General Reply

The June 22, 1998, response (Appendix 2) to the draft report from the Acting Governor of

Guam concurred with all three recommendations and indicated that corrective actions would

be taken. Based on the response, we consider Recommendation

1

resolved and implemented

and request additional information for Recommendations 2 and 3 (see Appendix 3).

6

B. NONFILER IDENTIFICATION PROGRAM

The Department of Revenue and Taxation did not use available information sources to

identify potential nonfilers of gross receipts taxes. Guam Public Law 19- 10, Section 19,

authorized Revenue and Taxation to use various sources of information, such as the Guam

Telephone Directory, the Guam Waterworks Authority’s water connection records, and the

Guam Housing and Urban Renewal Authority’s and Guam Housing Corporation’s listings of

landlords, to identify potential nonfilers. However, Revenue and Taxation had not

(1)

developed a written plan, including specific goals and objectives, to serve as a basis for

conducting an effective nonfiler identification program; (2) assigned sufficient personnel and

a program coordinator to conduct a nonfiler identification program; and (3) ensured that all

income tax return information was entered into Revenue and Taxation’s automated income

tax system to provide a method for comparing income reported on individual and/or

corporate income tax returns with income shown on gross receipts tax returns. As a result,

based on our limited testing of alternative sources of taxpayer information, we estimated that

gross receipts taxes and related penalties and interest of at least $972,486 may not have been

paid by nonfilers during calendar years 1995 and 1996.

Identification of Nonfilers

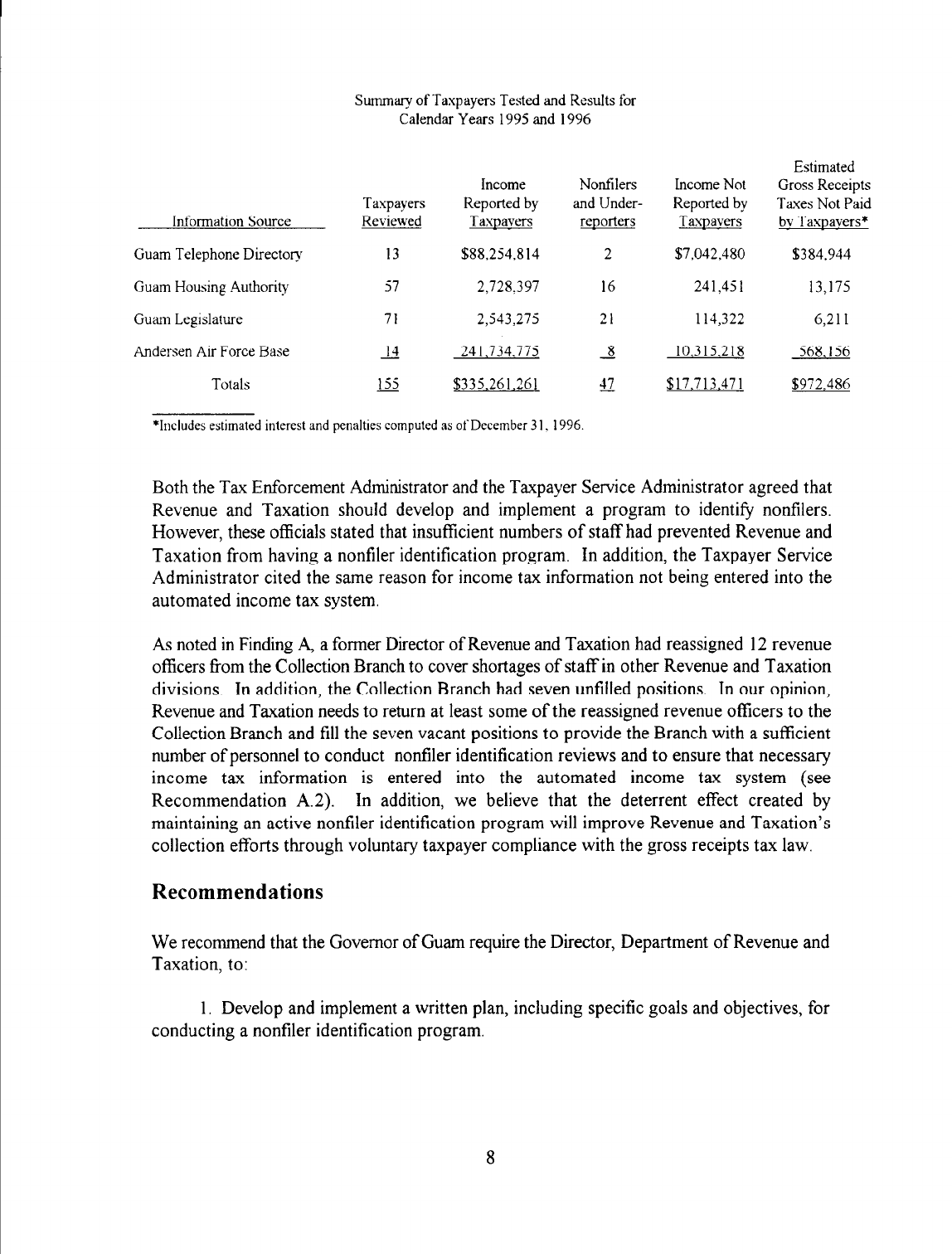

We tested several alternative sources of taxpayer information that Revenue and Taxation

could use to identify potential nonfilers, including the Guam Telephone Directory, the Guam

Housing and Urban Renewal Authority’s listing of Section 8 (Federal Housing Assistance)

Program landlords, the Guam Legislature’s logbook of personal services contracts, and the

military construction and service contract records at Andersen Air Force Base. From these

sources, we selected 155 taxpayers to determine whether they had filed gross receipts tax

returns during calendar years 1995 and 1996. In addition, for the taxpayers selected for

review from the Guam Housing Authority’s listing, the Legislature’s contract logbook, and

the Air Force Base’s contract records, we compared the amount of taxpayer income shown

in these records with the amount of income reported on gross receipts tax returns to

determine whether all income had been reported by the taxpayers during calendar years 1995

and 1996. Based on our review of the information obtained for the 155 taxpayers, we

determined that 108 taxpayers had filed gross receipts tax returns and had apparently reported

all of their income. However, we found that the remaining 47 taxpayers’ either had not filed

gross receipts tax returns or had underreported their income, of which both actions resulted

in the nonpayment of gross receipts taxes estimated at $972,486, as shown in the following

table:

‘On February 5, 1996, we provided a list of the 47 taxpayers to Revenue and Taxation’s Director so that

Revenue and Taxation could determine why the 47 taxpayers either had not filed gross receipts tax returns or

had underreported income. If appropriate, actions should be taken to collect the amounts due.

7

Summary of Taxpayers Tested and Results for

Calendar Years 1995 and 1996

Income Nonfilers

Taxpayers Reported by and Under-

Information Source Reviewed Tasnavers renorters

Guam Telephone Directory

13 $88,254,814 2

Guam Housing .4uthority

57

2,728,397 16

Guam Legislature

71

2,543,275 21

Andcrsen Air Force Rase

JJ

241.734.775

8

Totals Ijj $335.261.2ti

g

*Includes estimated interest and penalties

computed as

ofDecember 31.

1996.

Income Not

Reported by

Taxpavers

$7,042,480

241,451

114,322

lo.315218

$17.713,471

Estimated

Gross Receipts

Taxes Not Paid

bv Taspavers*

$384,944

13,175

62 1

1

568,156

$972,486

Both the Tax Enforcement Administrator and the Taxpayer Service Administrator agreed that

Revenue and Taxation should develop and implement a program to identify nonfilers.

However, these officials stated that insufficient numbers of staff had prevented Revenue and

Taxation from having a nonfiler identification program. In addition, the Taxpayer Service

Administrator cited the same reason for income tax information not being entered into the

automated income tax system.

As noted in Finding A, a former Director of Revenue and Taxation had reassigned 12 revenue

officers from the Collection Branch to cover shortages of staff in other Revenue and Taxation

divisions In addition, the Collection Branch had seven unfilled positions. In our opinion,

Revenue and Taxation needs to return at least some of the reassigned revenue officers to the

Collection Branch and fill the seven vacant positions to provide the Branch with a sufficient

number of personnel to conduct nonfiler identification reviews and to ensure that necessary

income tax information is entered into the automated income tax system (see

Recommendation A.2). In addition, we believe that the deterrent effect created by

maintaining an active nonfiler identification program will improve Revenue and Taxation’s

collection efforts through voluntary taxpayer compliance with the gross receipts tax law.

Recommendations

We recommend that the Governor of Guam require the Director, Department of Revenue and

Taxation, to:

1.

Develop and implement a written plan, including specific goals and objectives, for

conducting a nonfiler identification program.

8

2. Initiate a review to determine why the 47 taxpayers either had not filed gross

receipts tax returns or had underreported income. If this review determines that additional

taxes are due, actions should be taken to collect the amounts due.

Governor of Guam Response and Office of Inspector General Reply

The June 22, 1998, response (Appendix 2) to the draft report from the Acting Governor of

Guam concurred with the two recommendations and indicated that corrective actions would

be taken. Based on the response, we consider Recommendation

1

resolved but not

implemented. Accordingly, the recommendation will be referred to the Assistant Secretary

for Policy, Management and Budget for tracking of implementation. Also based on the

response, additional information is requested for Recommendation 2 (see Appendix 3).

9

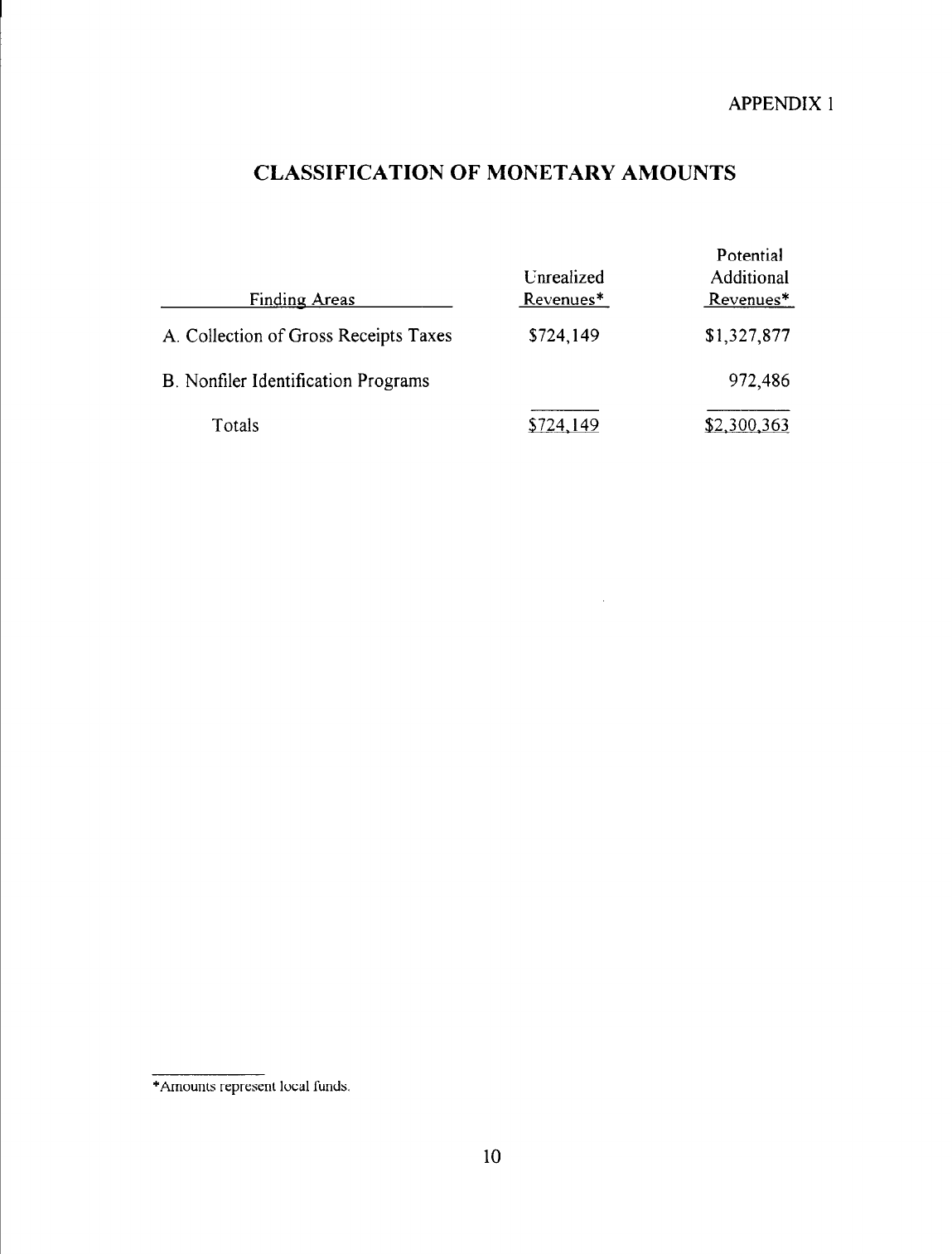

APPENDIX 1

CLASSIFICATION OF MONETARY AMOUNTS

Finding Areas

A. Collection of Gross Receipts Taxes

Unrealized

Revenues*

5724,149

B. Nonfiler Identification Programs

Potential

Additional

Revenues*

$1,327,877

972,486

Totals

$724,149

$2,300,363

*Amounts represent local funds

10

APPESDIX 2

?age 1 of 9

UFISINAN I MAGA’WiI

TERITORION GUAM

JUN 221998

Mr. Robert J. Williams

Acting Inspector General

Office of the Inspector General

United States Department of the Interior

Washington, D.C. 20240

Dear Mr. Williams:

Enclosed is the Department of Revenue and Taxation’s response and the action plans

in regard to the Inspector General’s Audit Report on “Assessment and Collection of

Gross Receipt Taxes” (Assignment No. N-IN-GUA-003-97).

Should you have any questions or comments, please write to me.

Sincerely,

Enclosures

11

Post

Office

60x2950. Agana. Guam 96910 9 (671)472-8931

l

Fax (671)477tUAM

APPEYDIX 2

Page

2

of 9

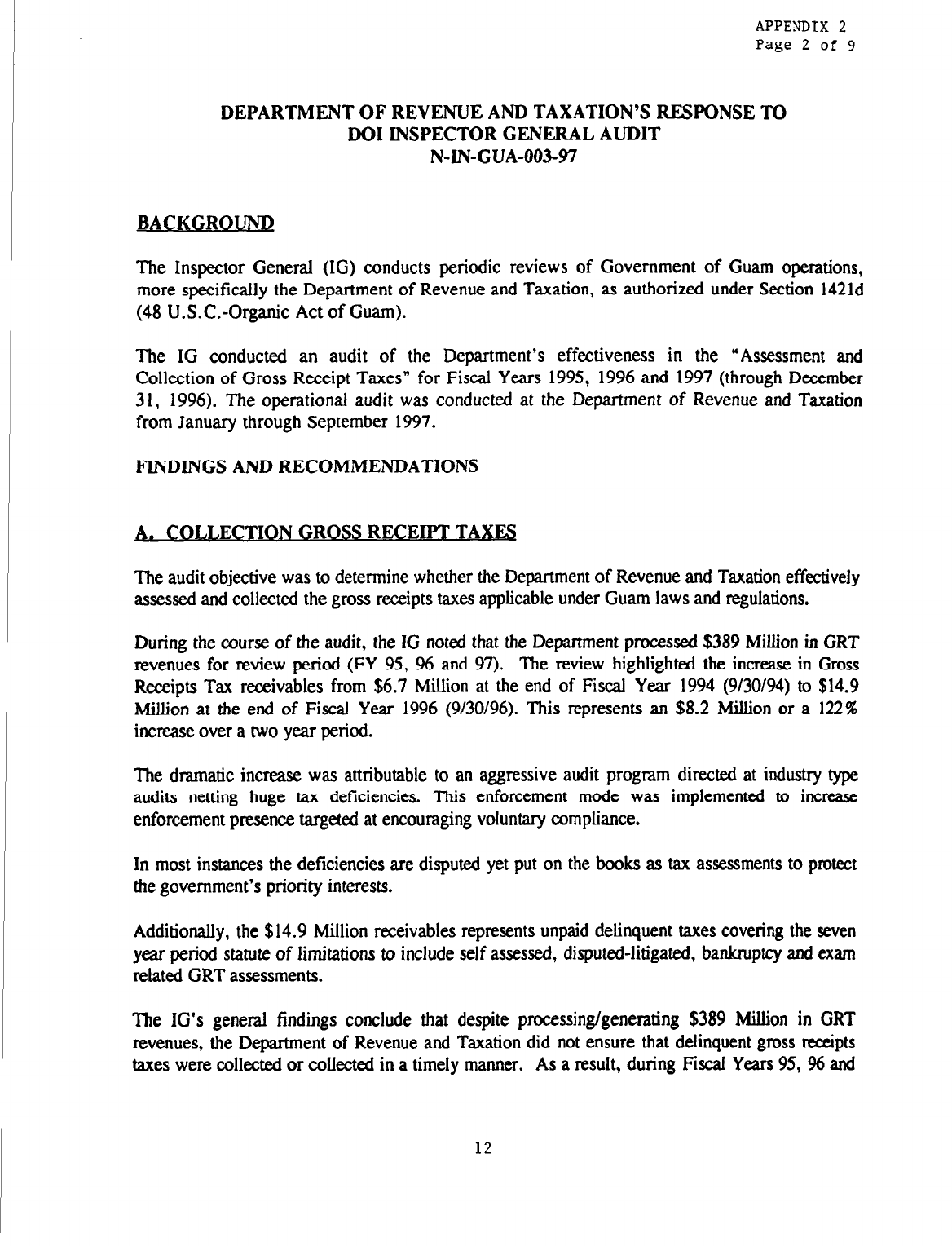

DEPARTMENT OF REVENUE AND TAXATION’S RESPONSE TO

DOI INSPECTOR GENERAL

AUDIT

N-IN-GUA-00347

BACKGROI JND

The Inspector General (IG) conducts periodic reviews of Government of Guam operations,

more specifically the Department of Revenue and Taxation, as authorized under Section 1421d

(48 U.S.C.-Organic Act of Guam).

The IG conducted an audit of the Department’s effectiveness in the “Assessment and

Collection of Gross Receipt Taxes” for Fiscal Years 1995, 1996 and 1997 (through December

31, 1996). The operational audit was conducted at the Department of Revenue and Taxation

from January through September 1997.

FINDINGS AND RECOMMENDATIONS

The audit objective was to determine whether the Department of Revenue and Taxation effectively

assessed and collected the gross receipts taxes applicable under Guam laws and regulations.

During the course of the audit, the IG noted that the Department processed $389 Million in GRT

revenues for review period (FY 95, 96 and 97). The review highlighted the increase in Gross

Receipts Tax receivables from

$6.7 Million at the end of Fiscal Year 1994 (g/30/94) to $14.9

Million at the end of Fiscal Year 1996 (9130196). This represents an $8.2 MilIion or a 122%

increase over a two year period.

The dramatic increase was attributable to an aggressive audit program directed at industry type

audits netting huge tax deficiencies. This enforcement mode was implemented to increase

enforcement presence targeted at encouraging voluntary compliance.

In most instances the deficiencies are disputed yet put on the books as tax assessments to protect

the government’s priority interests.

Additionally, the $14.9 Million receivables represents unpaid delinquent taxes covering the seven

year period statute of limitations to include self assessed, disputed-litigated, bankruptcy and exam

related GRT assessments.

The IG’s general findings conclude that despite processing/generating $389 Million in GRT

revenues, the Department of Revenue and Taxation did not ensure that delinquent gross receipts

taxes were collected or collected in a timeIy manner. As a result, during FiscaI Years 95, % and

12

APPENDIX 2

Page 3 of 9

97 the Government of Guam lost gross receipts tax revenues of at least $724,149 and may be at

risk of losing another $1.3 Million of delinquent taxes if timely enforcement actions are not taken.

With the findings and recommendations analyzed, the Department of Revenue and Taxation shall

implement the recommended courses of action.

The IG recommends the following be implemented to strengthen the collections operations:

1.

Instruct the Tax Enforcement Administrator to comply with established procedures

for collecting gross receipts taxes, including the use of seizures and sales of taxpayer property.

Response:

Attached please find a copy of a memo dated June 17, 1998, instructing the Tax

Enforcement Administrator and Collection Branch personnel to follow established collection

procedures and as warranted, utilize seizures and sales of property to collect delinquent taxes.

2.

Provide the necessary resources to ensure that the Collection Branch reduces its

backlog of delinquent taxpayer cases and collects delinquent gross receipts taxes in a timely

manner.

Response:

The effectiveness of the Department of Revenue and Taxation’s enforcement program is

predicated on the resources allocated to the Tax Enforcement Program.

Despite an ever increasing taxpayer base and collateral demand for services, the budgetary

resources allocate to the tax enforcement program has either remained level or been reduced

consistent with the financial and economic condition of the Government of Guam. This condition

has progressively worsen as the Departmental budget reflects an allocation lower than pre FY 95

budget authorizations ($1.75 to 2.5 Million lower).

On paper (The FY 97 Budget), Collection Branch was authorized a staff of 38 employees

(35 Revenue Officers, 2 Tax Auditors, and 1 Support Staff). As of the review period the IG

confirmed that only 19 employees, or a 50% compliment, manned the collections branch function.

The 50% understaffing was attributed to 7 vacancies and 12 Revenue Officers reassigned by the

previous Director to cover shortages in other areas of operations.

To correct this, as of mid 1997 internal reassignments were affected to transfer most, if

not all, Revenue Officers back to the tax area and hire 3 entry level Revenue Officers from the

collections branch vacancies.

Additionally, the Department will continue to request funding for the vacancies and that

the collections branch allocations be exempted from budget constraints (hiring freezes).

APPEYDIX 2

Page 4 of 9

3.

Develop and implement written procedures and establish a records management

systems to ensure that the Collection Branch controls and safeguards taxpayer case files.

Response:

Attached please find a copy of a memorandum dated June 17, 1998 to the Administrator,

Tax Enforcement Programs, directing him to

develop and implement procedures for a records

management systems within the Collection Branch.

B. NONFILER IDENTIFICATION PROGRAM

The ICI audit findings conclude that the Department did not use available information sources

to identify non-filers which resulted in potential nonpayment loss of gross receipt taxes of at

least $972,486.

Revenue and Taxation had not (1) developed a written plan, including specific goals and

objectives, to serve a basis for conducting an effective non-filer identification program; (2)

assigned sufficient personnel and a program coordinator to conduct a non-filer program; and

(3) ensured that all income tax return information was entered in Revenue and Taxation’s

automated system.

The Department conducts

such non-filer review (as mandated by Guam Public Law 19-10) of

gross receipt tax returns filed to ensure taxpayers whom are required to file do so prior to the

renewal of the business licenses, the program is currently limited to only the Department’s

automated systems.

The IG recommends the following be implemented:

1.

Develop and implement a written plan, including specific goals and objectives,

for conducting a nonfiler identification program.

Response:

Attached please find a copy of a memo dated June 17, 1998 instructing the Tax

Enforcement Administrator and Taxpayer Service Administrator to develop for implementation

a Gross Receipt non-filer program.

2. Initiate a review to determine why the 47 taxpayers either had not filed gross

receipt tax returns or had underreported income.

If this review determines that additional taxes

are due, action should be taken to collect the amounts due

3

14

APPENDIX 2

Page 5 of 9

Response:

The review of the 47 taxpayers is being conducted and the Tax Enforcement

Administrator is monitoring the findings and actions.

Attached is a copy of a memo dated

June

17, 1998 to Tax Enforcement Administrator.

4

15

APPENDIX 2

CARL T.C. GUTIERREZ. Govern

Wage

6 of 9

DEPARTMENT OF

MADELEINE

Z.

BORDALLO, Lleutonan~ Govwnor

REVENUE AND TAXATION

GOVERNMENT OF GUAM

JOSEPH T. DUENAS. Dirrdor CARL E. TORitES. Deputy DimcIm

JUN 17 1998

MEMORANDUM

To:

Administrator, Tax Enforcement Division

From:

Director

Subject:

IG Report-Collections Procedures

Effective immediately, you are hereby directed to adhere to the established procedures for

collecting delinquent gross receipt taxes, including the use of seizures and sales of taxpayer

property when warranted.

Please instruct all employees of the Collection Branch to adhere to the established procedure so

as to affect timely collection of delinquent GRT assessments.

Qr;b

JOSEPH T. DUENAS

P. 0. Box 23607,

GMF,

Guam

96921 -

Tel:

(671) 475-1801

- Fax: (671)

472-2643

16

APPENDIX 2

Page 7 of 9

CARL T.C. GUTIERREZ, Govomor

DEPARTMENT OF

MADELEINE 2. BORDALLO, Lieutenant Govomor

REVENUE AND TAXATION

GOVERNMENT OF GUAM

JOSEPH T. DUENAS DIrector CARL k TORIUS, Dcpvtr DIrector

MEMORANDUM

To:

Administrator, Tax Enforcement Division

From:

Director

Subject:

Procedures for a Records Management System

You are hereby directed to develop procedures for a records management system for the

Collections Branch.

Please coordinate with all affected operational areas to facilitate the implementation of said

system so as to ensure that the collections Branch controls and safeguards taxpayer case files.

Refer to IG Report No. N-IN-GUA-003-97 for additional guidance on this matter.

JOSEPH T. DUENAS

P. 0. Box

23607.

GMF, Guam

96921-

Tel:

(671) 475-1801

-

Fax:

(671) 472-2643

17

APPENDIX 2

Page 8 of 9

CARL T.C. GUTIERREZ, Govomor

DEPARTMENT OF

MADELEINE 2. BORDALLO, Lhtonant Govm

REVENUE AND TAXATION

GOVERNMENT OF GUAM

JOSEPH T. DUENAS, DlmcIw CARL

L

TORRES, Deputy Dir&or

MEMORANDUM

To:

Administrator, Tax Enforcement Division

Administrator, Taxpayer Service Division

From:

Director

Subject:

Non-Filer Program for Gross Receipt Taxes

You are hereby directed to develop for implementation a Gross Receipt non-filer program.

This

program should include goals and objectives.

A draft of this plan must be submitted to my office within sixty days.

If you have any questions,

please let me know.

JOSEPH T. DUENAS

P. 0. Box 23607,

GMF, Guam

96921 - Tel: (671)

475-1801 -

Fax: (67l) 472-2643

18

APPENDIX 2

Page 9 of 9

CARL T.C. GUTIEFtREZ, Govomor

DEPARTMENT OF

MADELEINE 2. BORDALLO, Lieutonwtt Govomor

REVENUE AND TAXATION

GOVERNMENT OF GUAM

JOSSPH T. DIJENAS. Dk+r(w

CARL

L TORRID, aprtr Mm&r

JUN

17’7933

MEMOFtANDUM

To:

Administrator, Tax Enforcement Division

From:

Director

Subject:

IG Audit Recommendation

DO1 Audit N-IN-GUA-003-97

After reviewing results of the IG audit findings of “Assessment and Collections Gross Receipts

Taxes”, you are hereby instructed to provide me periodic status updates of the 47 taxpayers cited

as either had not filed gross receipt tax returns or had under-reported income.

If you have any questions, please see me.

97-J-

JOSEPH T. DUENAS

P. 0.

Box

23607,

GMF,

Guam 96921-

Tel:

(67l) 47~1801-

Fax:

(67l) 472-2643

19

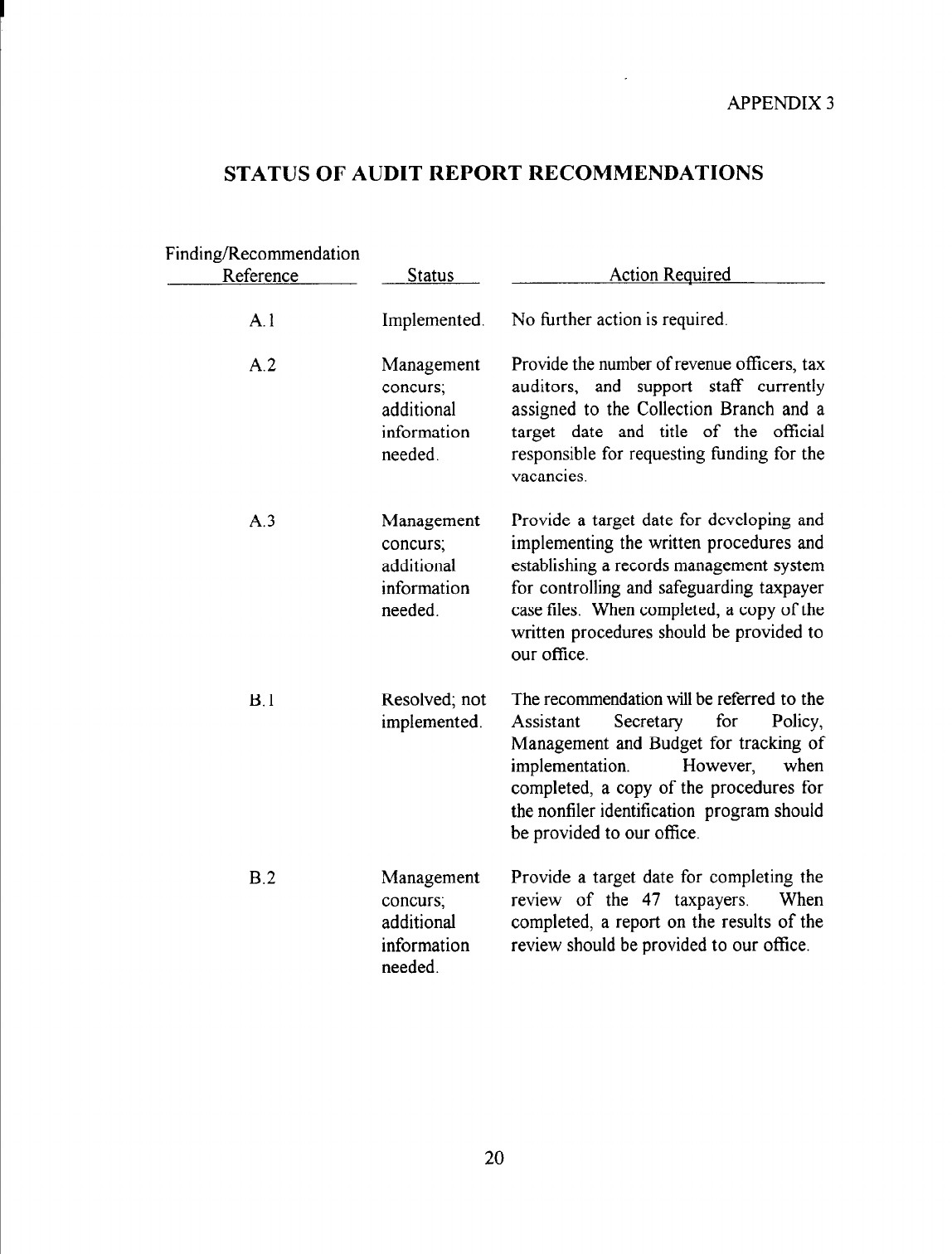

APPENDIX 3

STATUS OF AUDIT REPORT RECOMMENDATIONS

Finding/Recommendation

Reference

Status

A. 1

Implemented.

No tkther action is required.

A.2

Management

concurs;

additional

information

needed.

A.3

B.l

B.2

Management

concurs;

additional

information

needed.

Resolved; not

implemented.

Management

concurs;

additional

information

needed.

Action Reauired

Provide the number of revenue officers, tax

auditors, and support staff currently

assigned to the Collection Branch and a

target date and title of the official

responsible for requesting funding for the

vacancies.

Provide a target date for developing and

implementing the written procedures and

establishing a records management system

for controlling and safeguarding taxpayer

case files. When completed, a copy of the

written procedures should be provided to

our office.

The recommendation will be referred to the

Assistant Secretary

for Policy,

Management and Budget for tracking of

implementation. However, when

completed, a copy of the procedures for

the nonfiler identification program should

be provided to our office.

Provide a target date for completing the

review of the 47 taxpayers

When

completed, a report on the results of the

review should be provided to our offke.

20

I

’

ILLEGAL OR WASTEFUL ACTIVITIES

SHOULD BE REPORTED TO

THE OFFICE OF INSPECTOR GENERAL BY:

Sending written documents to:

Calling:

Within the Continental United States

U.S. Department of the Interior

Office of Inspector General

1849 C Street, N.W.

Mail Stop 5341

Washington, D. C. 20240

Our 24-hour

Telephone HOTLINE

l-800-424-508 1 or

(202) 208-5300

TDD for hearing impaired

(202) 208-2420 or

l-800-354-0996

Outside the Continental United States

Caribbean Retion

U.S. Department of the Interior

Office of Inspector General

Eastern Division - investigations

4040 Fairfax Drive

Suite 303

Arlington, Virginia 22201

(703) 235-9221

North Pacific Region

U.S.

Department of the Interior

Office of Inspector General

North Pacific Region

415 Chalan San Antonio

Baltej Pavilion, Suite 306

Tamuning , Guam 969 11

(67 1) 647-605 1

Toll Free INumbers:

l-800-424-5081

TDD l-800-354-0996

FlVCommercial Numbers:

(202) 208-5300

TDD (202) 208-2320

HOTLINE

1849 C Street, N.W.

&&lad Stop 5341

Washington. D.C. 20240