© 2021 Thrivent | For financial professional use only.

1

Thrivent Traditional

Long-Term Care Insurance

Product Guide

Introduction 2

General Overview 3

Target Market and Suitability 4

Basic Product Overview 5

Contract Provisions

• Issue Ages

• Risk Classes

• Premium Payment Types

• Premium Modes

• Rate Guarantee

• Dividends

6

Couples Discount 8

Features and Benefits Overview 9

Base Contract Features and Benefits

• Waiver of Premium

• Contingent Nonforfeiture Benefit–

Lifetime Pay Contracts

• Contingent Nonforfeiture Benefit–

Limited Pay Contracts

• Alternate Care Benefit

• Bed Reservation

• Care Coordinator Services

10

Ancillary Benefits

• Respite Care Benefit

• Equipment/Home Modification Benefit

• Caregiver Training

• International Care Benefit

13

Basic Building Blocks

• Elimination Period

• Benefit Multiplier

• Maximum Monthly Benefit

• Available Benefit

15

Benefit Increase Options

• Flexible Increase Benefit

• Annual Increase Benefit

• Comparing the Benefit

Increase Options

17

Optional Riders

• Waiver of Elimination Period for Home

Care and Adult Day Care

• Cash Benefit

• Return of Premium Upon Death

• Shared Care Benefit

• Survivorship Benefit

• Nonforfeiture Benefit

22

Optional Riders Compatibility Chart 28

Qualifying for Benefits 29

Payment of Benefits 31

Other Important Information 32

Underwriting 33

Suitability 33

Administrative Questions 34

Long-Term Care Insurance

Partnership Information

35

Long-Term Care Insurance Taxation 36

Conversions and Replacements 37

1035 Exchange Overview 38

Appendix A: Tables for Substantial

Premium Rate Increases

39

Table of Contents

© 2021 Thrivent | For financial professional use only.

2

Thrivent Traditional Long-Term Care Insurance

Thrivent Traditional Long-Term Care Insurance is a

comprehensive product that can help clients and

prospects pay for qualified long-term care expenses and

protect income and savings from being redirected to pay

for care.

Thrivent Traditional Long-Term Care Insurance covers

services and care in a variety of settings, from home

care to facility care, giving the insured flexibility to

receive the level of care he or she needs in a location

he or she may prefer.

Full Impact of Long-Term Care Needs

On January 1, 2011, the first of 76 million baby boomers

started to turn 65, a transition that is reported to continue

at a rate of more than 10,000 people per day, every day,

for the next 18 years.

1

By 2050, the number of individuals using paid long-term

care services in any setting (e.g., at home, residential

care such as assisted living, or skilled nursing facilities)

will likely double from 13 million in 2000, to 27 million

people. This estimate is influenced by growth in the

population of older people in need of care.

2

Why Thrivent Traditional Long-Term Care Insurance?

We believe long-term care is an event, not a product.

You may never experience the need for it, but if you do,

the people you love will experience consequences—

emotional, physical and financial.

It’s critical to make an extended care plan (whether you

believe you’ll need it or not). With a strategy in place, your

family won’t have to make hasty, emotional decisions that

too often damage family relationships.

Long-term care insurance is a way to fund the choices

you specify in your strategy (where/how you’ll receive

care, your family’s involvement, how you’ll pay for care).

Caregiving can have a devastating emotional effect on a

family. Care coordination services handle the business

details, so you can focus on being a family.

As a financial professional, you can help guide your

clients throughout their long-term care planning

decisions, as part of an ongoing overall financial strategy.

1

“Combination Insurance Products: What Do Consumers Really Want?” Pokorski, Robert M.D. LIMRA’s MarketFacts Quarterly/Number 1, 2011.

2

U.S. Department of Health and Human Services, and U.S. Department of Labor. The future supply of long-term care workers in relation to the aging

baby boom generation: Report to Congress. Washington, D.C.: Office of the Assistant Secretary for Planning and Evaluation, 2003.

http://aspe.hhs.gov/daltcp/reports/ltcwork.pdf (Jan. 20. 2005)

Introduction

© 2021 Thrivent | For financial professional use only.

3

What Is Long-Term Care?

Long-term care is a range of services and support that

may be needed to meet health or personal needs over a

long period of time. Most long-term care is not medical

care, but rather assistance with the basic personal tasks

of everyday life, called “activities of daily living,” such as:

• Bathing

• Dressing

• Using the toilet

• Transferring (to or from bed or chair)

• Caring for incontinence

• Eating

Many different services help people with chronic

conditions overcome limitations that keep them from

being independent. Long-term care is different from

traditional medical care. Long-term care helps a person

live as he or she does now. However, it may not help to

improve or correct medical conditions.

Long-term care services that help with activities of

daily living may include home health care, respite care,

hospice care, adult day care, care in a nursing home and

care in an assisted living facility. Long-term care may also

include care management services, which will evaluate

needs and coordinate and monitor the delivery of long-

term care services.

Who May Need Long-Term Care?

The need for long-term care may begin gradually

and progress as more and more help is needed with

activities of daily living, such as bathing, dressing,

household chores, meal preparation or managing

money. Or long-term care may be needed suddenly

after a major illness, such as a stroke or heart attack.

It may also be needed due to injuries sustained in an

accident. If care is needed, a stay at a care facility or

home health care services may be necessary—for

months, years or the rest of a person’s life.

What Can Long-Term Care Insurance Do for Clients

and Prospects?

Long-term care insurance can help clients

and prospects:

• Stay at home longer.

• Pay for qualified long-term care expenses

and protect income and savings from

being reallocated to pay for care.

• Receive help with activities of daily living. For example:

– An occupational therapist may be needed to

provide instruction on how to use adaptive

equipment (such as a reacher, sock aid or

long-handled shoe horn) or alternate ways to

perform daily activities.

– A home health aide may help with showers,

general hygiene and setting up daily medications.

– A nurse may be needed to periodically provide

assistance with insulin shots, blood thinners,

routine vital sign checks or wound care.

– A speech therapist might teach techniques to help

a person swallow more effectively if an individual

is experiencing problems eating or drinking.

General Overview

© 2021 Thrivent | For financial professional use only.

4

Target Market

• Preretired

– Ages 45-65.

– Working and saving.

• Goals include:

– Protecting his or her income and savings.

– Paying for long-term care expenses without

depleting savings or redirecting current income.

– Having choices and control over who provides

care and where.

– Making decisions today to preserve/ensure

options and independence in the future.

Secondary Markets

• Women

– The vast majority of those needing care are women.

– Most informal caregivers are women.

• Sandwich generation

– This generation is trying to manage helping their

parents and raising their children.

– They recognize that their parents may not have

planned and may not be able to financially

obtain coverage.

– They may be willing to purchase coverage on

their parents so they can manage their care

instead of provide it.

• Business owners

– Appeal as a key person.

– Potential tax advantages.

Suitability

A person should consider buying long-term care

insurance if he or she:

• Has significant savings and income.

• Wants to protect some of the assets and income.

• Can pay premiums, including possible future

premium increases, without financial difficulty.

• Wants to stay independent of the support of others.

• Wants the flexibility to choose care in the setting

that he or she will be most comfortable in.

A person should not buy long-term care insurance

if he or she:

• Cannot afford the premiums.

• Has limited assets, savings or income.

• Only has a single source of income from a

Social Security benefit or Supplemental

Security Income (SSI).

• Often has trouble paying for utilities, food,

medicine or other important needs.

• Is on Medicaid.

There are several long-term care insurance options

available to clients, including stand-alone long-term

care insurance (like this product), annuities with a

long-term care insurance rider, and life insurance

with a long-term care insurance rider. Each type of

coverage has unique characteristics and features,

and—as a result—it is difficult to make “apples-to-

apples” comparisons.

Stand-alone long-term care insurance may have a

larger benefit over a longer period of time. This type of

insurance is also pure insurance.

You can help clients understand the differences and

develop insights about which type of coverage may

be appropriate for their specific situation. Consider

clients’ overall financial situations and use available

illustrations to highlight the unique product features.

(Additional suitability information on page 33.)

Target Market and Suitability

© 2021 Thrivent | For financial professional use only.

5

Thrivent Traditional Long-Term Care Insurance is intended

to be federally tax-qualified long-term care insurance

pursuant to the Internal Revenue Code 7702B(b).

It is a comprehensive long-term care insurance product,

with coverage that includes home health care, residential

care facilities and adult day care.

Basic Product Overview*

Thrivent Traditional Long-Term Care Insurance Benefits

The benefits below are available after the elimination period has been satisfied and are subject to

the maximum monthly benefit and available benefit. Benefits may vary by state.

Home Health Care

Home health care benefits are qualified long-term care services if they are:

• Necessary to enable the insured to continue to live safely in his or her own residence; and

• Are provided by an employee of a home health agency or other trained personnel in the insured’s

residence. Note: Although family members may be taking care of the insured, family/informal

caregivers cannot bill for services to be reimbursed.

Home care services include:

• Homemaker services.

• Home health aide services.

• Skilled nursing services.

• Nutritional and dietary services.

• Physical, occupational, speech and respiratory therapy.

• Hospice care services.

Homemaker services include the following services when an impairment does not permit a person to

perform them and an informal caregiver is not available:

• Routine housecleaning.

• Preparing meals.

• Laundry.

• Shopping for essentials.

Residential Care

Facility

Residential care facility benefits include nursing homes, assisted living facilities and hospice care.

Residential care facilities do not include any facility that is primarily:

• A clinic, hospital or sanatorium.

• A subacute care or rehabilitation hospital.

• A sheltered living accommodation, a residence home or a similar living arrangement.

• A home or facility that operates primarily for the treatment of alcoholism, drug addiction or

a mental or nervous disorder.

Adult Day Care

Facility

Adult day care benefits provide care and companionship, outside the home, to small groups of adults

(typically six or more) who are chronically ill and need assistance or supervision during the day.

The program offers relief to family members or caregivers and allows them the freedom to go to work,

handle personal business or just relax knowing their loved one is well cared for and safe.

*Refer to individual state contracts for unique contractual definitions/terms.

© 2021 Thrivent | For financial professional use only.

6

Contract Provisions

Feature Details Additional Information

Issue Ages

18 to 79

The age used for the contract is the applicant’s age as of 30 days prior to the

application date.

Example: The applicant’s birthday is on Nov. 10 and she turned 60. She applies

for a long-term care insurance contract on Nov. 28. In this case, her contract age

would be 59 years old, even though her actual age is 60 (30 days prior to Nov. 28

she was 59 years old).

“Saving Age” is not allowed, other than as described above.

Risk Classes

Preferred

Preferred—90% of standard.

Standard

Class 1

Class 2

Class 1—125% of standard.

Class 2—150% of standard.

Gender-distinct pricing (except for Montana).

Premium Payment

Types

Lifetime Pay

10 Pay

This is not a cash accumulation product; no cash value is accumulated with

limited pay or lifetime pay.

Underwriting does not vary based on the premium payment type.

Changes to the premium payment type:

• May change from limited pay to lifetime pay after issue.

– Not subject to underwriting.

– Premium calculated based on the original issue age.

• May NOT change from lifetime pay to limited pay after issue.

• May NOT add/increase any other benefits or riders when a limited pay

premium mode is elected.

– If the insured wants to add or increase benefits or riders, he or she

must go through underwriting and buy a new contract.

Premium Modes

Monthly EFT

Quarterly

Semiannually

Annually

Paying the premium more often than annually will result in higher premiums.

© 2021 Thrivent | For financial professional use only.

7

Contract Provisions (continued)

Feature Details Additional Information

Rate Guarantee

Five year rate

guarantee

The rate guarantee is for five years from the issue date, and applies to the

entire contract, including any flexible increase benefit increases that occur

during that time. The new premium associated with the flexible increase

benefit would be guaranteed for the remaining years of the original five-year

rate guarantee.

Example of the rate guarantee with the flexible increase benefit:

A contract has an issue date of 1/1/13 and an original maximum monthly

benefit of $2,000 and a $550 annual premium. The rate guarantee is in effect

until 1/1/18.

On 1/1/14, the insured accepts a flexible increase offer. The new maximum

monthly benefit is $2,100 and the premium is $585. The new premium of

$585 is guaranteed until 1/1/18 (five years from the original issue date of

the contract).

On 1/1/15, the insured declines the flexible increase offer. The premium

remains $585, guaranteed to 1/1/18.

On 1/1/16, the insured accepts another flexible increase offer. The new

maximum monthly benefit is $2,205 and the premium is $630. The new

premium of $630 is guaranteed until 1/1/18.

Dividends

Eligible for

dividends

Dividends are not guaranteed.

Dividends, if payable, will be applied on an annual basis.

The only available dividend option is to reduce the premium.

• If the dividend exceeds the premium, the amount in excess will be

accumulated and applied toward future premiums.

• Accumulated dividends will earn 3.5% interest until used to pay any

future premiums.

• If the dividend is less than the premium, the balance will be billed.

• Upon termination of the contract, any remaining accumulated dividends

will be paid to the insured or insured’s estate, but only to the extent

that they do not exceed the sum of premiums paid by the insured and

applied to the contract.

– The sum of premiums paid does not include premiums waived or

reduced by dividends.

All distributions of dividends will be taxable and require a 1099.

© 2021 Thrivent | For financial professional use only.

8

Who Qualifies for the Couples Discount?

The couples discount is available to:

• Married couples.

• State partners/civil unions/domestic partners that are

named in a valid certificate or license by the state.

• Two individuals living together for at least

three years in a committed relationship as

partners or family members AND:

– Are committed to sharing expenses.

– Are not married.

– If related, must belong to the same generation

(such as siblings).

Why Do ‘Couples’ Receive a Discount?

In general, research has shown that individuals in a

committed relationship (such as spouses, partners or

family members who live together) provide each other

with informal care when it is needed. They tend to use

fewer paid care services, and if paid care services

are used, they tend to be used later in the process

compared to single people who are in a similar situation.

Having a spouse or partner to assist with care can

make a significant difference in the type of care needed

and where it is received. Care provided in the insured’s

home is typically less expensive than residential care,

thus potentially resulting in lower claim amounts being

paid over time.

Couples Discount

Two Available Discounts

1

Discount Details Additional Information

20% Couples

Discount

2

• Both individuals apply and

are approved for coverage,

or

• One individual has existing

coverage issued by Thrivent,

AAL or LB, and the other

is applying for Thrivent

Traditional Long-Term Care

Insurance coverage.

• When one insured dies or if the couple divorces

or separates:

– Discount remains for life.

– No changes to coverage.

• Marriage/remarriage (or meets the eligibility rules for the

couples discount outlined above):

– Discount may be applied after issue if insured marries

or remarries and the new spouse buys a contract.

5% Couples

Discount

3

• Both individuals apply but only

one is approved for coverage; or

• Only one individual applies.

• Discount may be applied after issue if the insured

marries or remarries (or meets the eligibility rules

for the couples discount outlined above).

• Do not need to submit two applications to qualify

for 5% discount.

3

1

All discounts are subject to eligibility rules as explained in this Product Guide.

2

For MT: 25% Couples Discount.

3

For MT: 10% Couples Discount.

© 2021 Thrivent | For financial professional use only.

9

Features and Benefits Overview

*CA Rider: Waiver of Elimination Period for Home and Community-Based Care.

Thrivent Traditional Long-Term Care Insurance is a

comprehensive product with many built-in features, as

well as optional riders to customize the plan according

to the client’s or prospect’s personal needs.

It may be helpful to think about the coverage in four

buckets: base contract benefits and features, basic

building blocks, inflation protection and optional riders.

• Base contract benefits and features are

built into the base contract. A few examples

include ancillary benefits, bed reservation,

care coordination and waiver of premium.

• The basic building blocks are the required

choices an individual must make when

designing his or her personal long-term

care insurance contract. They include:

– Maximum monthly benefit amount.

– Benefit multiplier.

– Available benefit.

– Elimination period.

• We offer two benefit increase options to help keep

pace with inflation and the rising costs of care:

– Flexible Increase Benefit.

› 5% compound

– Annual Increase Benefit.

› 1% compound

› 2% compound

› 3% compound

› 5% compound

• Optional riders are typically the last choices to

be made. They are available for an additional

cost and customize the long-term care insurance

contract to meet an individual’s specific wants

and needs. The optional riders are:

– Waiver of Elimination Period for Home Care

and Adult Day Care.*

– Cash Benefit.

– Return of Premium Upon Death.

– Shared Care Benefit.

– Survivorship Benefit.

– Nonforfeiture Benefit.

© 2021 Thrivent | For financial professional use only.

10

Base Contract Features and Benefits

Waiver of Premium

This benefit states that premiums will be waived once the elimination period is satisfied as long as

the insured continues to be benefit-eligible. Once the insured is no longer benefit-eligible and no

longer receiving services, the waiver of premium benefit will end and premium payments will resume.

If the insured becomes eligible for benefits again, the waiver of premium benefit will apply again.

Additional Information:

• Ancillary benefits do not trigger waiver of premium.

• Double waiver of premium is included if the insured has the shared care benefit rider.

– This will waive the premium for both individuals even if only one insured is receiving benefits.

• Limited Pay Contracts:

– If the contract goes on waiver for a limited pay contract, it does not change the number of

years the premium will be paid.

Example: The payment type selected on a contract is 10 years. If the individual pays the premium

for five years and then goes on premium waiver for two years and then recovers, he or she would

need to pay the remaining three years of premium payments.

Contingent

Nonforfeiture

Benefit—

Lifetime Pay

Contracts

This benefit states that if the contingent nonforfeiture benefit is triggered, the coverage will continue as

paid-up coverage. If the benefit is triggered by premium default, the paid-up coverage will be effective

on the date the grace period ends. Otherwise, paid-up coverage will be effective the date of the

insured’s notice to cancel the contract.

• Benefits will be paid subject to all of the conditions and limitations of this contract.

• Maximum monthly benefit and elimination period will be the same as were in effect

at the time of lapse.

• No increases will be provided under any increase benefit rider on or after the date paid-up

coverage becomes effective.

• All riders on this contract will terminate on the date paid-up coverage becomes effective.

• The available benefit under the paid-up coverage may be used for all care and services

covered under the terms of the contract.

• The available benefit will be reduced by the amounts that are paid under the paid-up coverage.

• Paid-up coverage will terminate on the date the available benefit reaches zero.

The paid-up coverage will have an available benefit equal to the lesser of:

1. The nonforfeiture credit.

2. The available benefit in effect immediately before the date paid-up coverage becomes effective.

The nonforfeiture credit is equal to the greater of:

1. The total of all premiums paid for the contract.

2. The maximum monthly benefit in effect on the date paid-up coverage becomes effective.

Premiums paid by the insured do not include premiums waived by Thrivent or reduced by dividends.

The Contingent Nonforfeiture Benefit will be triggered if:

1. Thrivent increases the premium rates;

2. The new premium represents a substantial increase in premium;* and

3. Within 120 days after the due date of the new premium if either:

a. The contract terminates due to premium default; or

b. The insured gives notice to cancel the contract. The date of notice is the date Thrivent

receives it or, if later, the date the insured specifies.

*A substantial premium increase is an increase that results in a cumulative percentage increase in premiums

since the contract’s date of issue that equals or exceeds the percentages shown in Appendix A.

Base Contract Features and Benefits

© 2021 Thrivent | For financial professional use only.

11

Base Contract Features and Benefits Continued

Contingent

Nonforfeiture

Benefit—

Limited Pay

Contracts

This benefit states that if the contract has a limited premium payment period, and the contingent

nonforfeiture benefit is triggered, the coverage will continue as paid-up coverage with reduced benefit

maximums. If the benefit is triggered by premium default, the paid-up coverage will be effective on the

date the grace period ends. Otherwise paid-up coverage will be effective the date of the insured’s

notice to cancel the contract.

• Benefits will be paid subject to all of the conditions and limitations of the contract.

• No increases will be provided under any increase benefit rider on or after the date paid-up

coverage becomes effective.

• All riders on the contract will terminate on the date paid-up coverage becomes effective.

• The available benefit under the paid-up coverage may be used for all care and services

covered under the terms of the contract.

• The available benefit will be reduced by the amounts that are paid under the paid-up coverage.

• Paid-up coverage will terminate on the date the available benefit reaches zero.

The contract’s remaining available benefit, maximum monthly benefit and ancillary benefit limits will be

reduced to amounts equal to:

90% of the amounts in eect prior to termination

x

# of months premiums were paid/# of months in the premium paying period

=

Paid-up benefit amount

Premiums paid by the insured do not include premiums waived by Thrivent or reduced by dividends.

The Limited Premium Payment Period Contingent Nonforfeiture Benefit will be triggered if:

1. Thrivent increases the premium rates,

2. The new premium represents a substantial premium,*

3. Prior to the due date of the increased premium, premiums have been paid for

at least 40% of the number of months in the premium payment period, and

4. Within 120 days after the due date of the new premium if either:

a. The contract terminates due to premium default, or

b. The insured gives notice to cancel the contract. The date of notice is the

date Thrivent receives it or, if later, the date the insured specifies.

*A substantial premium increase is an increase that results in a cumulative percentage increase in premiums

since the contract’s date of issue that equals or exceeds the percentages shown in Appendix A.

© 2021 Thrivent | For financial professional use only.

12

Base Contract Features and Benefits Continued

Alternate Care

Benefit

Allowing for an alternate care benefit helps ensure that individuals have access to emerging services

that may develop over time, but are not currently identified or available.

This allows the insured to qualify for benefits not specifically listed elsewhere in the contract.

Alternate care that is not normally covered by the contract may be covered if:

• Thrivent and the insured have a written agreement that describes how the services will be covered.

• The alternate care is prescribed in a plan of care document.

– The care is a cost-effective alternative.

– The plan pays expenses up to the maximum monthly benefit.

– Care is subject to the elimination period and available benefit.

Benefits will be paid according to the terms of the contract (e.g., maximum monthly benefit, available

benefit). No benefits will be paid for alternate services provided prior to the date of the agreement.

Bed Reservation

This feature provides a benefit for bed reservation for temporary absences of up to 60 days per

calendar year.

This means that if the insured is in a residential care facility and temporarily leaves (e.g., to go to

the hospital or attend a family event), the charges incurred to hold a space to enable the insured

to return to that facility will be covered.

If the elimination period has not yet ended, the crediting of days toward the elimination period

will not be interrupted by a temporary absence as described above.

Care Coordinator

Services

If the insured would like to use the services of a care coordinator, Thrivent will identify someone in the

area. The insured is not required to use care coordinator services in order to use his or her insurance

benefits. Expenses for care coordinator services will not be reimbursed from the contract coverage but

rather are covered separately by Thrivent. A care coordinator can help develop the insured’s required

plan of care, which will be used to administer benefits.

A care coordinator is a health care professional with training and expertise in case management.

Services provided by a care coordinator include:

• Performing a comprehensive care needs assessment.

• Developing, implementing and coordinating a plan of care.

• Identifying the services needed.

• Locating local caregivers and care facilities.

• Monitoring ongoing care.

© 2021 Thrivent | For financial professional use only.

13

Ancillary Benefits

Ancillary Benefits*

Ancillary benefits include:

• Respite care.

• Equipment/home modification.

• Caregiver training.

• International care benefit.

These benefits are not subject to the elimination period or the maximum monthly benefit.

In addition, the benefits do not satisfy the elimination period. Ancillary benefits that are paid

will reduce the total available benefit amount.

Each ancillary benefit has its own separate benefit limit. The benefit limits are tied directly to

the maximum monthly benefit. If the maximum monthly benefit increases or decreases, so do

the ancillary benefit limits.

Ancillary benefits = 2x maximum monthly benefit.

Example: The insured has a $5,000 maximum monthly benefit amount, a 60-month benefit

multiplier and the 5% compound annual increase benefit. The available benefit is $300,000

($5,000 x 60 = $300,000).

The ancillary benefit limits would be $10,000 when the contract is issued (2 x $5,000 = $10,000).

After the first contract anniversary when the 5% compound annual increase benefit is applied, the

maximum monthly benefit would be $5,250 and the available benefit would be $315,000. Thus, the

ancillary benefit limits would be $10,500.

If $2,000 is paid for respite care in the second contract year, the available benefit amount would be

reduced to $313,000 ($315,000 - $2,000 = $313,000). The remaining respite care benefit for that

contract year would be $8,500 ($10,500 - $2,000 = $8,500).

*For CA: Referred to as Supplemental Benefits. Respite care is the only ancillary benefit that is available each

calendar year. Equipment/home modification, caregiver training and the international care benefit are lifetime limits.

Respite Care Benefit

Respite care is designed to provide an opportunity for an informal caregiver to have some

needed time off by providing alternative care for the insured.

Respite care means qualified long-term care services are designed to:

• Relieve an informal caregiver.

• Provide on a short-term basis, in a residential care facility, an adult day care facility,

or in a person’s home as home care services.

• Are received in a week where no days are credited toward the elimination period.

– The insured must decide if the days go toward the elimination period or toward

respite care benefits (cannot do both in the same week).

Benefit = 2x current maximum monthly benefit amount each calendar year.

© 2021 Thrivent | For financial professional use only.

14

Ancillary Benefits Continued

Equipment/Home

Modification Benefit

Equipment/home modifications are safety-related alterations to the home. Equipment or home

modifications must be specified in the plan of care and be necessary according to the insured’s

condition to be covered.

Special equipment means:

• Therapeutic equipment such as a hospital bed, wheelchair, crutches or walker.

• Safety-related equipment such as a medical alert system.

• Any other medical equipment that is specified in the insured’s plan of care.

Home modifications are:

• Home safety checks to evaluate the insured’s home to determine if it is a physically

safe environment for the insured and provide recommendations for home modifications.

• Accessibility changes to an insured’s home such as a ramp, chairlift or alterations to

accommodate a wheelchair.

• Safety-related changes to an insured’s home such as installation of grab bars or railings.

• Any other changes to an insured’s home that are specified in his or her plan of care.

Benefit = 2x current maximum monthly benefit amount (lifetime limit).

Caregiver Training

Benefit

The caregiver training benefit allows a qualified health care professional to provide training

that is specific to the needs of the insured so that an informal caregiver can care for that person.

An informal caregiver does not receive compensation for providing care.

Benefit = 2x current maximum monthly benefit amount (lifetime limit).

International Care

Benefit

The international care benefit provides a nominal benefit if covered services are received outside of the

United States, its territories and possessions.

The international care benefit can be used for:

• Nursing home care.

• Assisted living care.

• Home health care.

• Hospice care.

The insured must provide appropriate documentation in English to receive payment.

This documentation includes:

• Certification from a U.S.-licensed health care practitioner that the insured is chronically ill and

received care for the covered expense for which the insured is submitting notice of claim.

• Properly completed claim forms and proof that the insured is receiving covered care

(in the form of fully itemized bills).

• Copy of an airline ticket or other proof acceptable that the insured is outside of the country.

• Copies of medical records which Thrivent deems necessary to support the insured’s claim.

The benefit is paid in U.S. dollars to the insured.

The benefit will not cover expenses incurred in countries where payment would violate economic,

financial or trade sanctions imposed by the U.S. or United Nations.

Benefit = 2x current maximum monthly benefit amount (lifetime limit).

Cash Benefit Rider does not pay when receiving international care.

© 2021 Thrivent | For financial professional use only.

15

Basic Building Blocks

The basic building blocks are the required choices

individuals must make when you are helping design

his or her long-term care insurance and include:

• Elimination period.

• Benefit multiplier.

• Maximum monthly benefit.

• Available benefit.

Basic

Building Block

Details Additional Information

Elimination Period

30, 90 or 180 days*

The elimination period is the time when the insured must pay for

covered services before the insurance begins paying benefits.

Calendar days:

• One day of service in a week receives credit for full week

(seven days).

• Calendar week begins on Sunday and ends Saturday.

The elimination period needs to be satisfied only once while

the contract is in force.

Changes to the elimination period:

• Decreases—Changing to a longer elimination period after issue.

– Subject to the current issue minimums.

– Future premium will be recalculated based on the

decreased coverage and the original issue age.

– Cannot decrease coverage during or after a claim period

has occurred.

• Increases—Changing to a shorter elimination period after issue.

– Subject to underwriting at attained age.

Note: Zero-day elimination is an option for the home care and

adult day care benefit only if the optional waiver of elimination

period for home care and adult day care rider is selected.

Benefit Multiplier

24, 36, 48, 60 or 96 months

The benefit multiplier is a factor based on time (expressed in

months) that is used to determine the insured’s available benefit

or pool of money.

Changes to the benefit multiplier:

• Decreases—Can be decreased after issue.

• Increases—Can be increased after issue.

– Subject to evidence of insurability.

Example: If the insured selects a $5,000 maximum monthly

benefit and a 60-month benefit multiplier, the total available

benefit is $300,000 for long-term care expenses, regardless of

how long it takes to use the benefits.

• $5,000 x 60 = $300,000

If the insured uses the maximum every month, benefits will last

approximately five years. Benefit increase options, which are

discussed later in the guide, would extend the time frame that

the benefit would be paid. If less than the maximum is used, the

available benefit will last longer than five years.

*CT: 180 days Elimination Period is not available.

© 2021 Thrivent | For financial professional use only.

16

Basic Building Blocks Continued

Basic

Building Block

Details Additional Information

Maximum Monthly

Benefit

$1,500–$15,000

(Increments of $100)

The maximum monthly benefit amount is the limit on the amount the

contract would pay, each month, during a claim period for qualified

expenses. The elimination period must be met and there must be a

remaining available benefit.

Changes to the maximum monthly benefit:

• Decreases—Can be decreased after issue.

• Increases—Can be increased after issue.

– Subject to evidence of insurability.

Examples:

• If expenses in a given month during a claim period exceed the

contract’s benefit amount, the expenses would be reimbursed

up to the maximum monthly benefit amount and reduce the total

available benefit.

• If expenses in a given month during a claim period are less than the

contract’s maximum monthly benefit amount, the expenses would be

reimbursed, and the unused portion of the maximum monthly benefit

amount would remain in the total available benefit. The total available

benefit would be reduced only by the amount reimbursed.

– The unused maximum monthly benefit does not increase the

following month’s maximum monthly benefit amount. It does help

the pool of money last longer.

• The chart below shows how a hypothetical claim may be paid

based on a $5,000 maximum monthly benefit and total available

benefit of $300,000.

Long-term

care expense

incurred

Actual amount paid

from long-term care

insurance contract

Available

Benefit

January $2,500 $2,500 $2 97, 50 0

February $3,000 $3,000 $294,500

March $5,000 $5,000 $289,500

April $5,200 $5,000 $284,500

May $4,800 $4,800 $279,700

Available Benefit

The available benefit is the total pool of money available during the

insured’s lifetime to pay for qualified long-term care expenses.

Example:

The maximum monthly benefit amount selected is $5,000. The benefit

multiplier selected is 60 months. So, the available benefit is $300,000.

$5,000 x 60 = $300,000

This amount will increase if the contract has an annual increase

benefit or the flexible increase benefit (and does not decline an

increase offer).

The available benefit is decreased when covered expenses

are reimbursed.

Monthly

Benefit

Benefit

Multiplier

Available

Benefit

© 2021 Thrivent | For financial professional use only.

17

Benefit Increase Options

If you’ve seen recent cost-of-care projections, you know

long-term care expenses are likely to be higher in the

future than they are today. Benefit increase options help

protect against the rising costs of long-term care by

helping the insureds to customize their plans to meet

their current and potential future needs for increased

coverage. Choosing a benefit increase option can be one

of the most important additions a prospective insured

includes in long-term care insurance planning.

Thrivent offers two types of benefit increase options:

• Flexible Increase Benefit (FIB).

• Annual Increase Benefit (AIB).

Benefit increase options:

• Can be added to individual and shared care contracts.

• Cannot be selected together on a contract—

can only have one or the other.

• Both options are available on preferred,

standard, class 1 and class 2 contracts.

Let’s take a closer look at how these options work.

Flexible Increase Benefit (FIB)

Details

Issue ages: 18 to 70

The flexible increase benefit includes an automatic claim increase benefit.

How It Works

Provides an opportunity to increase the maximum monthly benefit and current remaining

available benefit on the contract anniversary by 5% compounded annually. Ancillary benefits

will also increase accordingly.

• Without evidence of insurability.

• All-or-nothing offer each year (5% increase or 0% increase).

The increase will be automatic unless the insured opts out when he or she receives the

annual notification letter.

• Premiums will increase with each offer accepted and premiums will be based on the insured’s

age at the time of the increase.

• Premiums will remain unchanged if the insured does not accept the increase.

Automatic increases will occur if the insured is on claim.

• The insured can decline automatic increases while on claim, but it may not be in

his or her best interest.

• If the insured recovers, he or she will have to pay the increased premium amount

associated with the new coverage.

• If the new premium associated with the automatic increases is not affordable to the insured,

the insured can decrease coverage.

If three consecutive offers are declined, no future increase offers will be extended. However, the rider

will remain on the contract since the insured is still eligible for the automatic claim increases.

Additional

Information

This benefit is not available with:

• 10-pay contracts.

• Survivorship Benefit Rider.

Flexible increase benefit increases occur automatically on the contract anniversary.

A notification letter will be sent prior to the contract anniversary.

Changes

Changes:

• If the flexible increase benefit is dropped after issue, the previous increases will be maintained,

and the future premium will be recalculated without the flexible increase benefit rider load/premium.

• Flexible increase benefit can be added after issue.

– Evidence of insurability will be required.

© 2021 Thrivent | For financial professional use only.

18

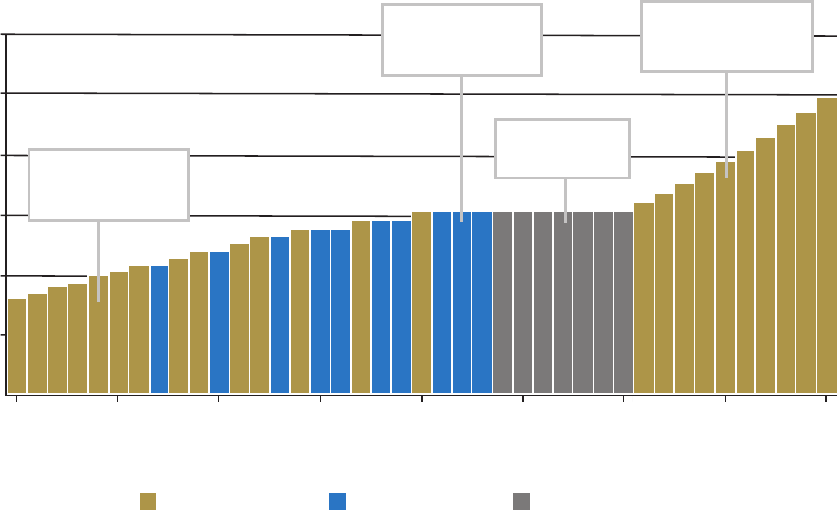

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$0

50

55

60

65

70

75 80 85 90

Age

Increase Accepted

Increase Declined

Increase Not Oered

Maximum Monthly Benefit

No increases

oered

Increases resume

when receiving

benefits

Three consecutive

declines

Most increases

accepted

Let’s look at a hypothetical example using the flexible

increase benefit:

Mary, at age 50, purchased Thrivent Long-Term Care

Insurance, choosing the optional flexible increase

benefit rider to help manage her budget. Having the

option to accept or decline the premium increases

was important to her, especially during the years when

her children needed help paying for college. Mary

also knew that in preparing for the future, she wanted

the maximum monthly benefit amount to increase over

time; with a goal to accept increases until her maximum

monthly benefit amount reached at least $15,000.

Over the next 20 years, Mary accepted 13 annual

increase offers, and declined seven. However, she didn’t

decline the offer in three consecutive years, which meant

her flexible increase benefit was offered each year.

When she reached age 70, Mary decided her maximum

monthly benefit of $15,000 was adequate to meet her

needs and declined all future increases. After Mary

declined the increase offer three years in a row, she

was not offered any future increases.

At age 80, Mary’s health declined, and she needed

assistance with daily activities. She began to receive

qualified long-term care services at home according

to her Plan of Care. After meeting her elimination

period, her long-term care insurance benefits started.

Now that Mary is on claim, the flexible increase

benefit rider automatically increases her maximum

monthly benefit and available benefit by 5%,

compounded annually, and will continue to do

so each year while she is receiving care.

Mary doesn’t have to worry about paying premiums

during this time since the premium waiver benefit is

a standard benefit included with her insurance.

Flexible Increase Benefit

Hypothetical Example

Flexible Increase Benefit

© 2021 Thrivent | For financial professional use only.

19

Annual Increase Benefit (AIB)

Details

Issue ages: 18 to 79

How It Works

If the insured chooses this benefit rider, the maximum monthly benefit, available benefit (pool of money)

and ancillary benefits will automatically increase annually on the rider anniversary, depending on the

level selected.

Premiums, however, will remain level over time. That’s because the cost of future increases is

automatically built into the premium. As a result, this benefit may be appropriate for people who want

the convenience of making one decision and not having to decide each year or prefer a level premium

for budgeting purposes.

Four choices are available (compounded annually):

• 1% • 2% • 3% • 5%

Changes

• If the annual increase benefit is dropped after issue, the previous annual increases will be

maintained and the future premium will be recalculated based on the current amount of

maximum monthly benefit coverage (including increases) at the original issue age without the

annual increase benefit rider.

• The compound annual increase benefit can be decreased after issue.

– Allowed decreases include:

› Changing from a higher percent AIB to a lower percent AIB (for example: 5% to 3%, 2%,

or 1% AIB; 3% to 2% or 1% AIB, or 2% to 1% AIB).

– No evidence of insurability required.

› Changing from either AIB (5%, 3%, 2% or 1%) to FIB.

– No evidence of insurability required.

• The compound annual increase benefit can be added or increased after issue.

– Evidence of insurability will be required.

– Allowed additions and increases include:

› Changing from no annual increase benefit to 1%, 2%, 3% or 5%.

› Changing from a lower percent AIB to a higher percent AIB (1% to 2%, 3% or 5% AIB; 2% to

3% or 5% AIB; 3% to 5% AIB).

› Changing from FIB to AIB.

© 2021 Thrivent | For financial professional use only.

20

Let’s look at a hypothetical example using the 5%

annual increase benefit.

At age 50, Sue purchases Thrivent Long-Term

Care Insurance with a maximum monthly benefit

amount of $5,700 and a 5% annual increase benefit,

compounded annually. Her desired goal is to have

a maximum monthly benefit of $15,000 when she

reaches age 70.

As you can see from the chart below, Sue’s annual

premiums of $9,638 remain level over time, although

her monthly benefit increases 5% annually.

At age 70, Sue’s maximum monthly benefit has

reached $15,124, and at age 80—when she needs

residential care—her maximum monthly benefit has

grown to $24,635.

Annual Increase Benefit

Hypothetical Example*

*Based on a 5% Annual Increase Benefit (compounded annually), $9,638 annual premium, goal to reach a maximum monthly

benefit of $15,000 by age 70, issue age 50, standard risk class, ignores any other riders and premium discounts that may be

applicable. No changes are made to the contract throughout the years illustrated and no claims are paid. Premiums may increase

after the initial five year rate guarantee.

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$0

$12,000

$10,000

$8,000

$6,000

$4,000

$2,000

$0

50 55 60 65 70 75 80

Age

Maximum Monthly Benefit

Annual Premium

AIB Monthly Benefit AIB Premium

Annual Increase Benefit

© 2021 Thrivent | For financial professional use only.

21

• 50-year-old female insured with standard risk

class, no couples discount or additional riders.

• 90-day elimination period with

60-month benefit multiplier.

• Goal is to have approximately $15,000

maximum monthly benefit by age 70.

• Annual increase benefit contract (5%).

– Maximum monthly benefit amount begins at $5,700.

– Annual premium is $9,638.

• Flexible increase benefit contract.

– Maximum monthly benefit amount begins at $8,000.

– Annual premium is $3,256.

– 7 of 20 increases are declined between the

ages of 50 and 70.

– No increases accepted after age 70.

Comparing the Benefit Increase Options

Flexible Increase Benefit Annual Increase Benefit

• Flexible.

• Benefits and premium increase automatically

each year unless declined.

• For people who prefer a lower initial premium.

• For people who prefer a level premium.

• Convenience of making the decision once

instead of each year.

The graph below shows a comparison of the maximum

monthly benefit and premium between the flexible

increase benefit and the annual increase benefit.

This hypothetical comparison is based on the previous

examples used for the flexible increase benefit and the

annual increase benefit:

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$0

$12,000

$10,000

$8,000

$6,000

$4,000

$2,000

$0

50 55 60 65 70 75 80

Age

Maximum Monthly Benefit

Annual Premium

AIB Monthly Benefit FIB Monthly Benefit AIB Premium FIB Premium

© 2021 Thrivent | For financial professional use only.

22

Optional riders are typically the final choices to be made. They are available for an

additional cost and help customize the long-term care insurance contract to meet

the individual’s specific wants and needs.

The available riders are:

• Waiver of Elimination Period for Home Care and Adult Day Care.*

• Cash Benefit.

• Return of Premium Upon Death.

• Shared Care Benefit.

• Survivorship Benefit.

• Nonforfeiture Benefit.

Optional Riders

*CA Rider: Waiver of Elimination Period for Home and Community-Based Care.

Waiver of Elimination Period for Home Care and Adult Day Care*

Description

The rider allows the insured to receive home health care and adult day care services on day one—

effectively a zero-day elimination period—specifically for at-home care.

How It Works

The coverage days received under this benefit will be applied toward meeting the elimination period

(so when facility care is needed, the elimination period doesn’t “start over”).

Even though the elimination period is waived, the premium will not be waived until the

elimination period is met.

Additional Details

Available on individual and shared care contracts.

Restriction: This rider is NOT available with the 180-day elimination period.

Changes

• Can be dropped after issue.

• Can be added after issue.

• Subject to evidence of insurability.

Cash Benefit

Description

The cash benefit is a rider that provides additional cash payments above the maximum monthly benefit,

regardless of whether the insured is receiving home care or facility care. It provides the insured with

added flexibility to pay for services that are not typically covered.

How It Works

If the insured is receiving home care services:

• An additional amount equal to 15% of the maximum monthly benefit would be paid

as a cash payment.

If the insured is receiving facility care:

• The cash benefit is equal to 10% of the maximum monthly benefit.

The insured must meet the elimination period and receive at least five days of care per calendar month

to receive the benefit.

The cash benefit is not payable for international care.

Additional Details

Available on individual and shared care contracts.

This benefit is a separate benefit and does not reduce the available benefit.

Elimination period must be met before this benefit will be paid.

If home care and facility care services are paid in the same month, the higher percentage will be paid.

Benefits received may be taxable.

Changes

• Can be dropped after issue.

• Can be added after issue.

– Subject to evidence of insurability.

© 2021 Thrivent | For financial professional use only.

23

Optional Riders Continued

Return of Premium Upon Death

Description

This rider returns the premiums paid to the insured’s estate at the time of death.

How It Works

The rider must be in force for 10 years before a death occurs to be eligible for payment.

Payment = Premiums paid for the base contract and riders less

Any accumulated dividends paid upon death and the sum of any benefit payments that

were paid on the contract, including ancillary benefits.

If the benefits paid exceed premiums paid, then no return of premium is paid.

To pay the benefit under this rider, Thrivent requires:

• Rider must be active; and

• Proof of death; and

• Written notice from a representative of the insured’s estate that no expenses eligible for

payment are outstanding.

Additional Details

Restriction: Only available on individual contracts; not available with shared care contracts.

The sum of premiums paid does not include premiums waived or reduced by dividends.

May have tax implications for the estate.

Changes

• Can be dropped after issue.

• Can NOT be added after issue.

Shared Care Benefit

Description

This rider is for couples who purchase identical Thrivent Long-Term Care Insurance. It’s designed to

provide couples with extra flexibility in their long-term care planning.

How It Works

“Benefit partner” is the term used to identify the two people in a shared care benefit agreement.

The shared care benefit links two individual contracts together. If an insured uses his or her entire

available benefit, then he or she can start drawing from the benefit partner’s remaining available benefit.

• An insured does not need to satisfy a new elimination period to use his or her benefit partner’s

benefits since he or she already met the elimination period under his or her own contract.

• If one insured qualifies for the waiver of premium, neither benefit partner will have to pay premiums.

The joint waiver of premium benefit automatically kicks in.

• If an insured uses all of his or her benefit partner’s benefits, the benefit partner not on claim

can elect to purchase an additional 24-month benefit for his or her use only (without additional

underwriting). This is called the residual benefit.

1

• Other than reducing the contract’s available benefit, payment of benefits to the benefit partner will

not affect the other insured’s eligibility for benefits under his or her contract.

• Both insureds may be on claim at the same time.

1

In Arizona and Connecticut, each person must retain 24 months of benefits in the pool for the contract owner’s sole purpose.

The additional 24-month benefit is not available for purchase.

© 2021 Thrivent | For financial professional use only.

24

Optional Riders Continued

Shared Care Benefit—Continued

Additional Details

Both contracts MUST have identical coverage, issue dates and benefits, including:

• Elimination period

• Benefit multiplier

• Maximum monthly benefit

• Benefit increase options

• Riders

• Premium payment type

(lifetime pay or limited pay)

For contracts with the flexible increase benefit rider:

• Benefit partners must either accept or decline the increase offers together—the maximum

monthly benefit amounts must be identical at all times.

• If one insured is on claim and the other insured is not, both individuals will get the automatic

increase associated with the flexible increase benefit.

– If the insured that is on claim recovers, both individuals will need to pay for

the increases that occurred while on claim.

– If the premium associated with the increase in coverage is not manageable, the benefit

partners are allowed to drop their coverage amounts (benefits must remain identical).

Restrictions: The shared care benefit is not available with the return of premium upon death rider.

Residual Benefit

As mentioned above the residual benefit is available to a contract owner when his or her benefit

partner has used all the benefits from both contracts. The benefit partner not on claim can elect

to purchase an additional 24-month benefit for his or her use only.

The new available benefit will be the current maximum monthly benefit on the date of termination

with a benefit multiplier of 24 months.

• No evidence of insurability is required.

• The new premium will be based on the insured’s attained age.

• Available through age 85.

Eligibility for the residual benefit:

• Insured that is applying for the benefit has not had any days credited to

his or her elimination period.

• Insured that is applying has not been eligible to be certified as chronically ill in the

two years before the application date for the residual benefit.

Who can elect the

shared care benefit?

The shared care benefit rider is available to:

• Married couples.

• State partners/civil unions/domestic partners that are named in a valid certificate or

license by the state.

• Two individuals living together for three consecutive years in a committed relationship

as partners or family members AND:

– Are committed to sharing expenses.

– Are not married.

– If related, must belong to the same generation (such as siblings).

© 2021 Thrivent | For financial professional use only.

25

Optional Riders Continued

Shared Care Benefit—Continued

Death, Divorce

or Separation

Death

• Surviving benefit partner’s contract will be automatically increased by the remainder of the

deceased’s available benefit.

• Shared care rider will terminate.

• The new premium calculation will be the surviving contract holder’s original premium

(with the couples discount still in place) less the premium for the shared care rider.

There is no charge for the increased available benefit.

Example:

Divorce or Separation

Upon divorce or separation, this rider is only terminated if one of the benefit partners cancels the rider.

Otherwise, the rider will continue.

Remarriage/New Partner/New Committed Relationship

(See page 24 for who is eligible to elect the shared care benefit.)

The insured cannot add a new spouse, partner or family member to this coverage (the rider cannot

be added after issue).

Changes

• Can be dropped after issue.

• Can NOT be added after issue.

• Contract changes cannot be made that create unequal benefits while maintaining the shared

care benefit rider.

– Example: If benefit partner A wants to drop his or her maximum monthly benefit from

$5,000 to $3,000, then benefit partner B must do the same.

• If a contract change is made that creates an unequal benefit, the shared care benefit rider

will be terminated.

$500,000 total shared

pool of money at time

of initial purchase

Death occurs:

Person A dies without using

any long-term care benefits

Person B now has the sum

of both pools for covered

long-term care expenses

A B

$250,000 $250,000

A B

$250,000 $250,000

B

$500,000

Let’s take a look at how the shared care benefit rider

would work:

In the example below, Paul and Mary have identical

Thrivent Traditional Long-Term Care Insurance plans

without the shared care benefit rider.

Now, let’s take a look at the options Paul and Mary have

available to them when they purchase identical Thrivent

Traditional Long-Term Care Insurance with the shared

care benefit rider:

Paul Mary

Maximum Monthly Benefit

$6,000

Maximum Monthly Benefit

$6,000

Benefit Multiplier

60 months

Benefit Multiplier

60 months

Total Available Benefit is $360,000 each

Paul Mary

Maximum Monthly Benefit

$6,000

Maximum Monthly Benefit

$6,000

Benefit Multiplier

60 months

Benefit Multiplier

60 months

Total Available Benefit

$360,000

Total Available Benefit

$360,000

Total Available Benefit is $720,000,

which is available to Paul and/or Mary

© 2021 Thrivent | For financial professional use only.

26

Optional Riders Continued

Survivorship Benefit

Description

This rider states if two individuals (benefit partners) have in-force contracts and riders for 10 years

and one individual dies, the surviving benefit partner’s contract will become paid up.

How It Works

If two individuals have in-force contracts with the survivorship rider on both of their contracts

(naming each other as the benefit partner), then upon the death of one insured, the surviving

benefit partner’s contract will become paid up.

• If either benefit partner dies before 10 years, then no benefit will be paid.

• No benefits can have been paid during the first 10 years in force.

Additional

Information

The survivorship benefit is available to individuals who qualify for the couples discount

(see below for eligibility).

The insured’s contracts do not need to be identical, but they both have to have the rider and be

named as the benefit partner on the other insured’s contract.

Restriction: This rider is not available with:

• 10-pay contracts.

• FIB Rider.

Who is eligible for

this rider?

The survivorship benefit rider is available to:

• Married couples.

• State partners/civil unions/domestic partners that are named in a valid certificate or

license by the state.

• Two individuals living together for three consecutive years in a committed relationship as

partners or family members AND:

– Are committed to sharing expenses.

– Are not married.

– If related, must belong to the same generation (such as siblings).

Divorce

Upon divorce/separation, the rider is terminated if one of the insureds cancels the rider;

otherwise the rider will continue.

Changes

• Can be dropped after issue.

• Can NOT be added after issue.

© 2021 Thrivent | For financial professional use only.

27

Optional Riders Continued

Nonforfeiture Benefit

Description

This rider provides an option for the long-term care benefits to continue as reduced paid-up

insurance if the insured chooses to terminate his or her contract for any reason. The contract

must be in force for a minimum of three years before this benefit can be triggered.

How It Works

The amount of paid-up coverage will be equal to the lesser of:

• The nonforfeiture credit (see below); and

• The available benefit in effect immediately before the date paid-up coverage becomes effective.*

The nonforfeiture credit is equal to the greater of:

• The total premiums paid for the contract; and

• The maximum monthly benefit in effect on the date the paid-up coverage becomes effective.

Premiums paid by the insured do not include premiums waived by Thrivent or reduced by dividends.

The shortened benefit period is NOT reduced by any benefit payments paid prior to the date of lapse

but is subject to the remaining available benefit.

The same maximum monthly benefit amount, elimination period and other limits

(except available benefit) remain that were in effect at the time of lapse.

All optional riders will terminate on the date paid-up insurance becomes effective.

*For CA: Three times the maximum monthly benefit in effect on the date the paid-up coverage becomes effective.

Additional

Information

Available on individual and shared care contracts.

If this rider is selected, the insured may also have a contingent nonforfeiture option available BUT

the insured can only be paid under one of the nonforfeiture options. The insured may choose which

nonforfeiture benefit he or she would like to receive if more than one is triggered.

Changes

• Can be dropped after issue.

• Can NOT be added after issue.

© 2021 Thrivent | For financial professional use only.

28

Optional Riders Compatibility Chart

This chart shows the allowable combinations of the optional riders and

limited pay period options.

Annual Increase

Benefit

— No Yes Yes Yes Yes Yes Yes Yes

Flexible Increase

Benefit

No — Yes Yes Yes Yes No Yes No

Nonforfeiture

Benefit

Yes Yes — Yes Yes Yes Yes Yes Yes

Return of

Premium Upon

Death

Yes Yes Yes — Yes Yes Yes No Yes

Cash Benefit

Yes Yes Yes Yes — Yes Yes Yes Yes

Waiver of

Elimination

Period for Home

Care and Adult

Day Care*

Yes Yes Yes Yes Yes — Yes Yes Yes

Survivorship

Benefit

Yes No Yes Yes Yes Yes — Yes No

Shared Care

Benefit

Yes Yes Yes No Yes Yes Yes — Yes

Limited Pay

Period—10 Pay

Yes No Yes Yes Yes Yes No Yes —

Annual Increase

Benefit

Nonforfeiture Benefit

Cash Benefit

Survivorship Benefit

Flexible Increase

Benefit

Return of Premium

Upon Death

Waiver of Elimination

Period for Home Care

and Adult Day Care*

Shared Care Benefit

Limited Pay Period—

10 Pay

*The Waiver of Elimination Period for Home Care and Adult Day Care is not available with the 180-day elimination period.

CA Rider: Waiver of Elimination Period for Home and Community-Based Care.

Note: The Flexible Increase Benefit is available with the Shared Care Benefit. However, both contract owners must accept or decline

their offers at the same time. The coverage must be identical, otherwise, the Shared Care Benefit rider will terminate.

© 2021 Thrivent | For financial professional use only.

29

Qualifying for Benefits

Eligibility for the Payment of Benefits

To be eligible for benefits under the long-term care

insurance contract, all of the following conditions must

be met:

1. Insured is chronically ill and receives qualified

long-term care services;

2. For benefits subject to the elimination period, the

services are received after that period has ended; and

3. Coverage is not listed under the exclusions

(see page 32 for exclusions list).

What does it mean to be chronically ill?

On any given day, an insured is chronically ill if a licensed

health care practitioner has, within the 12-month period

preceding that day, certified in writing that he or she has:

1. A physical impairment that is expected to last at least

90 days, or

2. A cognitive impairment.

A physical impairment is an impairment that prevents a

person from performing two or more activities of daily

living without the substantial assistance of another person.

Substantial assistance means hands-on assistance or

standby assistance.

Activities of daily living include:

1. Bathing. Washing oneself in a tub or shower,

including getting in or out of the tub or shower, or

by sponge bath.

2. Continence. Maintaining control of bowel and bladder

functions or, if unable to do so, taking care of the

personal hygiene associated with incontinence,

including caring for a catheter or colostomy bag.

3. Dressing. Putting on and taking off all items

of clothing and any necessary braces, fasteners

or prostheses.

4. Eating. Feeding oneself by getting food into the

body from a receptacle (such as a plate, cup or table)

or, if necessary, by feeding tube or intravenously.

Eating does not include preparing meals.

5. Transferring. Moving into or out of a bed, chair

or wheelchair.

6. Using the Toilet. Getting to and from the toilet,

transferring on and off the toilet and performing

the associated personal hygiene.

A cognitive impairment is an impairment of the mind that:

1. Is comparable to (and includes) Alzheimer’s disease

and similar forms of irreversible dementia;

2. Is measured by clinical evidence and standardized

tests; and

3. Results in the need for continual supervision.

© 2021 Thrivent | For financial professional use only.

30

Qualifying for Benefits Continued

What are Qualified Long-Term Care Services?

Qualified long-term care services are:

• Required because the insured is chronically ill; and

• Provided pursuant to a plan of care.

What is a plan of care? Why is it required?

A plan of care is a written document that:

1. Is prepared and signed by a licensed health

care practitioner in accordance with accepted

standards of practice;

2. Prescribes qualified long-term care services

that are consistent with an assessment of the

insured’s impairment; and

3. Includes services or treatment that could not

be omitted without adversely affecting the

insured’s health.

Thrivent retains the right to discuss the plan of care

with the licensed health care practitioner who prepared

it. Thrivent may also verify that the plan of care is

appropriate and consistent with generally accepted

standards of care for a person who is chronically ill. The

plan of care must be updated as the insured’s needs

change. Thrivent must receive a copy of the plan of

care upon its completion and each time it is updated.

Thrivent retains the right to request periodic updates not

more often than once every 30 days. Thrivent will make a

copy of the current plan of care available to the insured’s

doctor, when requested. The insured may only have one

plan of care in effect at any time.

Is there a benefit or service available to help the

insured with this process?

Yes. Care Coordination Services are available to the

insured if he or she would like assistance.

The Care Coordination Benefit, if the insured chooses to

use it, pays for a care coordinator to help the insured and

his or her family:

• Perform a comprehensive care needs assessment.

• Identify the services needed.

• Locate local caregivers and facilities.

• Assist in developing, implementing and

coordinating the insured’s plan of care.

• Monitor the insured’s ongoing care.

There is no cost to the insured for the services provided

by a care coordinator referred by Thrivent. In addition,

these services are not subject to the elimination period.

© 2021 Thrivent | For financial professional use only.

31

Payment of Benefits

Payment of Benefits/Claims Process

This is a brief outline of the claims process:

1. Contact Thrivent’s Claims department.

• A notice of claim must be submitted to

Thrivent at our Service Center within 30

days after a covered loss starts or as soon

after this as reasonably possible.

• An acknowledgement letter will be sent to

the insured and the financial professional

upon receipt of the request for benefits.

• A claims representative will review the health

status, physician’s assessment of care needs,

the contract and its available benefits and

services, and the credentials of the health

care provider or facility providing the care.

• When all the information has been received and

reviewed, a letter explaining the claim decision

and next steps will be sent to the insured.

• If a decision cannot be made, a letter explaining

the reason for the delay will be sent to the insured.

2. Contact care coordinator services.

3. Ongoing claim review.

4. Reimbursement for services.

Benefits will be paid to the insured or to the health care

provider to whom the insured has assigned benefits.

Any benefits payable to the insured that are unpaid at his

or her time of death will be paid to his or her estate.

The insured is eligible for reimbursement up to the

maximum monthly benefit, subject to the available benefit.

The insured can receive payment for multiple benefit

services in one day.

Coordination With Other Coverage

If an expense covered under this contract is also covered

by other contracts or a rider issued by Thrivent (or a

predecessor organization), the amount payable for that

expense under this contract will be reduced by the sum

of the amounts that are paid for that expense under the

other coverage.

Coordination of benefits will be determined on multiple

contracts based on the issue date, beginning with the

earliest issued contract paying benefits first.

Coordination of benefits provision applies to: Arizona,

California, District of Columbia, Delaware, Hawaii, Indiana,

Montana and South Dakota.

Medicare Non-Duplication

Medicare non-duplication applies. This means that the

long-term care contract will not pay benefits for expenses

which are reimbursable under Medicare or would be

reimbursable under Medicare but for the application of a

deductible or coinsurance amount.

© 2021 Thrivent | For financial professional use only.

32

Other Important Information

Right to Cancel

The insured is provided a 30-day period upon receipt of the contract to review and/or rescind the

contract. If the insured cancels during this initial 30 days, all premiums paid will be refunded.

Unintentional Lapse

A feature that allows the insured to name someone to be notified if coverage is about to lapse

because the premium has not been paid. This could be a relative, friend or professional such

as a lawyer or accountant.

Grace Period