Schedule 1299-I (R-07/24) Page 1 of 17

Illinois Department of Revenue

2023 Schedule 1299-I

Income Tax Credits Information and Worksheets

What’s New for 2023?

• Public Act 102-1053 created the Recovery and Mental Health income tax credit (

Credit

Code 0180) eective for tax years beginning on or

after January 1, 2023.

• Public Act 102-0700 increased the maximum K-12 Instructional Materials and Supplies credit (Credit Code 5740) amount allowed for

Form IL-1040 lers. For tax years beginning on or after January 1, 2023, the maximum credit allowed for a single taxpayer is $500 or

$1000 for taxpayers married, ling jointly.

• No new credits will be allowed for the:

• Agritourism Liability Insurance income tax credit (Credit Code 5440) for tax years ending after December 31, 2023; and

• Invest in Kids credit (Credit Code 5660) for tax years ending after December 31, 2023.

NOTE: These credits may still be carried forward according to their provisions. See each credit’s specic instructions for more information.

•

Public Act 103-0009

extended the following income tax credits

•

Historic Preservation tax credit (Credit Code 1030) until tax years ending on or before December 31, 2028; and

•

New Markets Development tax credit (Credit Code 5500) until tax years ending on or before June 30, 2031.

•

Public Act 103-0592

extended the following income tax credits

•

Adoption credit (Credit Code 5780) until tax years ending on or before December 31, 2029; and

•

Student-Assistance Contributions tax credit (Credit Code 5420) until tax years ending on or before December 31, 2029.

• Public Act 103-0268 created the Hydrogen Fuel Replacement tax credit eective for tax years ending on or after December 31, 2027.

• Public Act 103-0595

• created the Quantum Computing Campuses tax credit (Credit Code 5480) eective for tax years ending on or after June 26, 2024; and

• extended the Research and Development tax credit (Credit Code 5340) until tax years

ending on or before December 31, 2031.

General Information

If you earned any of the following income tax credits:

• TECH-PREP Youth Vocational Programs,

• Dependent Care Assistance Program,

• Film Production Services,

• Employee Child Care (Corporate lers only),

• Enterprise Zone Investment,

• Enterprise Zone Construction Jobs,

• High Impact Business Construction Jobs,

• High Impact Business Investment,

• REV Illinois Investment,

• Aordable Housing Donations,

• Economic Development for a Growing Economy (EDGE),

• New Construction EDGE,

• Research and Development,

• Wages Paid to Ex-Felons,

• Student-Assistance Contributions,

• Angel Investment,

• Quantum Computing Campuses,

• New Markets Development,

• River Edge Historic Preservation,

• River Edge Construction Jobs,

• Live Theater Production,

• Hospital,

• Invest in Kids,

• K-12 Instructional Materials and Supplies (Form IL-1040 lers),

• Adoption (Form IL-1040 lers),

• Data Center Construction Employment ,

• Historic Preservation,

• Apprenticeship Education Expense,

• Agritourism Liability Insurance,or

• Recovery and Mental Health,

Printed by the authority of the state of Illinois - electronic only - one copy.

Schedule 1299-I (R-07/24) Page 2 of 17

use the instructions and worksheets in this schedule to determine the amount of credit to list in

• Column E, Credit Earned or Carried, of Schedule 1299-C, Income Tax Subtractions and Credits (for individuals),

• Column E, Credit Amount Earned, of Schedule 1299-A, Tax Subtractions and Credits (for partnerships and S corporations), and

• Column F, Credit Amount Earned, of Schedule 1299-D, Income Tax Credits (for corporations and duciaries).

If you are ling an Illinois combined unitary return, complete one Illinois Schedule 1299-D or 1299-A for the entire unitary business group by

listing the credit by unitary member. See the specic Schedule 1299 instructions for more information.

Keep a copy of your worksheets or calculations and Schedule 1299-I in your records. You may be required to submit further information to

support your ling.

Follow the specic schedule instructions for how to enter your credits on your Schedule 1299-C, 1299-D or 1299-A.

What if I have more credits than space allows on the form?

For several credits, you may have more qualifying items than space provided. For any of these credits in which you exceed the allotted space

to calculate the credit, use a separate sheet in the same format and include the individual amounts from multiple sheets and the total from

the worksheet in these instructions on the line for each credit on Schedules 1299-C, 1299-D, or 1299-A. Do not enter the total on your

additional sheets.

For example, if you have more than three qualifying properties for the Enterprise Zone Investment credit, use an additional sheet in the

same format provided on the Enterprise Zone Investment credit Worksheet. Add the totals from the worksheet and the additional sheets

and enter the total on Schedules 1299-C or 1299-A, Column E, or Schedule 1299-D, Column F, for your Enterprise Zone Investment credit.

What if I received a distributive share of a credit?

If you received a distributive share of a credit, report the credit amount in Step 3, Column F of Schedules 1299-A and 1299-C and Step 3,

Column G of Schedule 1299-D per the specic Schedule 1299 instructions. Schedules K-1-P are required as support for any credit being

claimed that was distributed to the claiming entity by a partnership or S corporation.

Additionally, if you receive more than one Schedule K-1-P for any eligible credit, add the amounts from all Schedules K-1-P for that credit and

enter the total in

• Column F, Distributive Share Credit from K-1-P, on the corresponding line of Schedule 1299-A,

• Column F, Distributive Share or Transfer, on the corresponding line of Schedule 1299-C, or

• Column G, Distributive Share Credit from K-1-P, on the corresponding line of Schedule 1299-D

that you enter that credit code. If you le an Illinois combined unitary return, see specic unitary instructions and examples on the Schedule

1299-D or Schedule 1299-A Instructions.

How do I report a transferred credit?

If you received a transferred credit, report the transferred amount in Step 3, Column G of Schedule 1299-A, Step 3, Column F of

Schedule 1299-C, and Step 3, Column H of Schedule 1299-D per the specic Schedule 1299 instructions. Proof of the transferred credit is

required as support for any credit being claimed.

What must I attach to Schedule 1299?

ATTACH: Schedule K-1-P, Partner’s or Shareholder’s Share of Income, Deductions, Credits, and Recapture, if you are a partner in

a partnership or a shareholder in an S corporation, and you received a Schedule K-1-P from the partnership or S corporation showing an

amount of credit that you may claim on your Schedule 1299. In order to claim amounts reported to you on a Schedule K-1-P, the tax year

ending listed on the Schedule K-1-P you received must fall within your tax year.

Note: All income tax credits are distributable by partnerships and S corporations, except:

• TECH-PREP Youth Vocational Programs

• Dependent Care Assistance Program Tax

• Employee Child Care

• High Impact Business Investment

• K-12 Instructional Materials and Supplies

• Adoption

ATTACH: Certicates issued by the Department of Commerce and Economic Opportunity (DCEO) if

• you entered into an agreement with DCEO and DCEO issued a tax certicate to you indicating the name of the credit and the amount of

the credit allowed in this taxable year; or

• you purchased or had credit transferred to you from another business and the credit purchase or transfer was approved by DCEO, who

then issued you a tax certicate indicating the name of the credit and the amount of credit allowed in this taxable year.

Note: Any income tax credit administered by DCEO requires a copy of the certicate to claim the credit. Those income tax credits include:

• Film Production Services

• Economic Development for a Growing Economy (EDGE)

• New Markets Development

• Angel Investment

• Live Theater Production

• Data Center Construction Employment

• Apprenticeship Education Expense

Schedule 1299-I (R-07/24) Page 3 of 17

• Enterprise Zone Construction Jobs

• High Impact Business Construction Jobs

• New Construction EDGE

• River Edge Construction Jobs

• REV Illinois Investment

• Quantum Computing Campuses

See the DCEO website for a list of incentives (credits) and DCEO contact information.

ATTACH: Certicates issued by the Department of Natural Resources (DNR) if

• you entered into an agreement with DNR and

• DNR issued a tax certicate to you indicating the name of the credit and the amount of the credit allowed in this taxable year.

Note: Any income tax credit administered by DNR requires a copy of the certicate to claim the credit. Those income tax credits include:

• River Edge Historic Preservation

• Historic Preservation

See the DNR website for a list of credits and contact information.

ATTACH: Certicates issued by the Illinois Department of Agriculture (IDOA) if

• you applied for a tax certicate with IDOA and

• IDOA issued a tax certicate to you indicating the name of the credit and the amount of the credit allowed in this taxable year.

Note: Any income tax credit administered by IDOA requires a copy of the certicate to claim the credit. The income tax credit includes:

• Agritourism Liability Insurance

See the IDOA website for information about the credit and contact information.

ATTACH: Certicates issued by the Department of Human Services (DHS) if

• you applied for a tax certicate with DHS and

• DHS issued a tax certicate to you indicating the name of the credit and the amount of the credit allowed in this taxable year.

Note: Any income tax credit administered by DHS requires a copy of the certicate to claim the credit. The income tax credit includes:

• Recovery and Mental Health

See the DHS website for information about the credit and contact information.

ATTACH: Any other documents (including transfer of credit documentation) required by the Illinois Department of Revenue (IDOR)

and noted in these instructions or your Schedule 1299 instructions.

• If you claim the Aordable Housing Donations credit, you must attach a copy of proof of the credit issued by the Illinois Housing

Development Authority or the city of Chicago.

• If you transferred the Hospital credit, you must attach a written notice of the transfer that you issued to the transferee. If you claim the

Hospital credit because the credit was transferred to you, you must attach a copy of the written notice of the transfer that the seller or

donor sent to IDOR. See Specic Instructions for the required written notice information.

• If you claim the Adoption credit, you must attach federal Form 8839, Qualied Adoption Expenses.

Failure to follow these instructions and attach required documentation will result in one or more of the following: a delay in the

processing of your return, the disallowance of the subtraction or credit, or the issuance of correspondence from IDOR. You also

may be required to submit further information to support your ling.

Should I round?

You must round the dollar amounts on Schedule 1299-I to whole-dollar amounts. To do this, you should

drop any amount less than 50 cents and increase any amount of 50 cents or more to the next higher dollar.

What if I need additional assistance or forms?

• For assistance, forms, or schedules, visit our website at tax.illinois.gov or scan the QR code

provided.

• Write us at:

ILLINOIS DEPARTMENT OF REVENUE

PO BOX 19001

SPRINGFIELD IL 62794-9001

• Call 1 800 732-8866 or 217 782-3336 (TTY at 1 800 544-5304).

• Visit a taxpayer assistance oce - 8:00 a.m. to 5:00 p.m. (Springeld oce) and 8:30 a.m. to 5:00 p.m. (all other oces), Monday

through Friday.

Specic Instructions

These instructions and worksheets are to be used to determine the amount of credit to list on your Schedule

• 1299-A, Column E for credits earned in the current year.

• 1299-C, Column E for credits earned in the current year and credits carried forward from past years. Use a separate line on

Schedule 1299-C for each tax year in which a credit was earned or is being carried.

• 1299-D, Column F for credits earned in the current year.

See the instructions for the specic Schedule 1299 you are ling for additional information.

Schedule 1299-I (R-07/24) Page 4 of 17

Each credit has a four-digit code used to identify it on Schedule 1299-C, 1299-D, or 1299-A. The rst digit of the code indicates how many

years the credit can be carried forward. For example, all credits that can be carried forward two years start with “2”. The remaining three digits

are the unique indicator for that specic code. Ten year carry forwards will use two digits for the year and two digits as the unique indicator.

Credit codes that start with “0” cannot be carried forward.

If you earn more than one of the same eligible credit code with the same expiration date, you should add the amounts from all of that credit

code when calculating the credit earned in the current year.

Credit Code Income Tax Credit Name

Active Credits

0160 Apprenticeship Education Expense

0180 Recovery and Mental Health

2000 TECH-PREP Youth Vocational Programs

2200 Dependent Care Assistance Program

5000 Film Production Services

5040 Employee Child Care (Corporate lers only)

5080 Enterprise Zone Investment

5120 Enterprise Zone Construction Jobs

5160 High Impact Business Construction Jobs

5220 High Impact Business Investment

5230 REV Illinois Investment

5260 Aordable Housing Donations

5300 Economic Development for a Growing Economy (EDGE)

5320 New Construction EDGE

5340 Research and Development

5380 Wages Paid to Ex-Felons

5420 Student-Assistance Contributions

5440 Agritourism Liability Insurance

5460 Angel Investment

5480 Quantum Computing Campuses

5500 New Markets Development

5540 River Edge Historic Preservation

5560 River Edge Construction Jobs

5580 Live Theater Production

5620 Hospital

5660 Invest in Kids

5740 K-12 Instructional Materials and Supplies (Form IL-1040 lers only)

5780 Adoption (Form IL-1040 lers only)

5820 Data Center Construction Employment

1030 Historic Preservation

Expired Credits, but can still be carried forward or distributed

5700 Natural Disaster (Credit earned in tax years beginning on or after January 1, 2017 and beginning prior to January 1, 2019).

Credit may not be used on returns for tax periods beginning after December 31, 2023.

1000 Historic Preservation (Credit earned in tax years ending on or before December 31, 2015). Credit may not be transferred,

carried forward, or distributed on returns for tax periods ending after December 31, 2025.

Tax Credits that can be used in the current year

Apprenticeship Education Expense (Credit Code 0160)

35 ILCS 5/231

For taxable years beginning on or after January 1, 2020, and beginning on or before January 1, 2025, the employer of one or more

qualifying apprentices shall be allowed a credit against income tax for qualied education expenses incurred on behalf of a qualifying

apprentice. This credit cannot be carried forward.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the Apprenticeship Education Expense tax credit (Code 0160) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P you received listing this credit to your Schedule 1299.

Schedule 1299-I (R-07/24) Page 5 of 17

Recovery and Mental Health (Credit Code 0180)

35 ILCS 5/233

For taxable years beginning on or after January 1, 2023, employers who employ eligible individuals in recovery from a substance use

disorder or mental illness in part-time and full-time positions within Illinois shall be allowed a credit against the qualied employer’s income tax

liability. This credit cannot be carried forward.

Contact DHS for more information.

Following the specic Schedule 1299 instructions, enter the Recovery and Mental Health tax credit (Code 0180) on Step 3 of:

Schedule 1299-A – credits from DHS certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DHS certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DHS certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DHS certicate and Schedule(s) K-1-P you received listing this credit to your Schedule

1299.

Tax Credits that can be carried for two years

TECH-PREP Youth Vocational Programs (Credit Code 2000)

35 ILCS 5/209

“Qualifying TECH-PREP programs” are those certied by the Illinois State Board of Education.

You may take this credit, for tax years ending on or after June 30, 1995, if

•

you are primarily engaged in manufacturing, and

•

you have direct payroll expenses for qualifying cooperative secondary school youth vocational programs in Illinois, or you pay for

personal services performed by a TECH-PREP student or instructor who would be subject to withholding if they were employed by you

and no other credit is claimed by the actual employer.

You may not take this credit for programs with national standards that have been or will be approved by the U.S. Department of Labor,

Bureau of Apprenticeship Training, or any federal agency succeeding to the responsibilities of that bureau.

Add the amount of direct payroll expenses for cooperative secondary school youth vocational programs and the amount paid to a

TECH-PREP student or instructor employed by you for personal services performed. Enter the total amount on the line below.

Multiply this amount by 20 percent (.20).

x .20 =

Following the specic Schedule 1299 instructions, enter the TECH-PREP Youth Vocational Programs tax credit (Code 2000) on Step 3 of:

Schedule 1299-C – credits from the line above in Column E.

Schedule 1299-D – credits from the line above in Column F.

This credit is not distributable or transferable.

Dependent Care Assistance Program (Credit Code 2200)

35 ILCS 5/210

You qualify for this credit, for tax years ending on or after June 30, 1995, if

•

you are primarily engaged in manufacturing, and

•

you have an on-site facility dependent care assistance program that is in Illinois and on the premises of your workplace.

Enter the amount of your expenses, reported under the IRC Section 129(d)(7), that were used for on-site dependent care on the line below.

Multiply this amount by 5 percent (.05).

x .05 =

Note: This credit cannot be claimed if the ve percent (.05) Employee Child Care Credit is claimed.

Total

Following the specic Schedule 1299 instructions, enter the Dependent Care Assistance Program tax credit (Code 2200) on Step 3 of:

Schedule 1299-C – credits from the total above in Column E.

Schedule 1299-D – credits from the total above in Column F.

This credit is not distributable or transferable.

Tax Credits that can be carried for ve years

Film Production Services (Credit Code 5000)

35 ILCS 5/213

For taxable years beginning on or after January 1, 2004 and prior to January 1, 2033, lm producers of qualied projects shall be allowed

a credit. For accredited productions commencing on or after January 1, 2009, this credit is equal to 30 percent of qualied expenditures

including Illinois production spending and Illinois labor, and an additional 15 percent on salaries paid to individuals who live in geographic

areas of high poverty or high unemployment.

To qualify for this credit you must have

• applied for and received a Tax Credit Certicate (indicating the amount of credit) from DCEO, or

• received a certicate from DCEO showing that a credit was transferred to you. A transfer of this credit may be made by the taxpayer

earning the credit within one year after the credit is awarded in accordance with rules adopted by DCEO.

Contact DCEO for more information.

Schedule 1299-I (R-07/24) Page 6 of 17

Following the specic Schedule 1299 instructions, enter the Film Production Services tax credit (Code 5000) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E, credits distributed to you in Column F, and credits transferred to you in

Column G.

Schedule 1299-C – credits from DCEO certicates in Column E, and credits distributed and transferred to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F, credits distributed to you in Column G, and credits transferred to you in

Column H.

Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Employee Child Care (Corporate lers only) (Credit Code 5040)

35 ILCS 5/210.5

“Start-up costs” include planning, site-preparation, construction, renovation, or acquisition of a child care facility.

You may take this credit if

•

you le Form IL-1120, or Form IL-990-T taxed as a corporation, and

•

you provide a child care facility, located in Illinois, for the children of your employees.

Note: You must keep records documenting all costs for which the credit is being claimed.

This is a two-part income tax credit.

Part One – For tax years ending on or after December 31, 2007, a credit of 30 percent (.30) of the “start-up costs” spent by you to provide a

child care facility for the children of your employees is allowed.

Enter the total amount of “start-up costs” to provide the child care facility. Multiply this amount by 30 percent (.30), and enter the result.

x .30 =

Part Two – For tax years ending on or after December 31, 2000, a credit of ve percent (.05) of the annual amount paid by you to provide the

child care facility for your employees’ children is allowed.

Enter the annual amount paid to provide the child care facility. Multiply this amount by ve percent (.05), and enter the result.

x .05 =

Note: The ve percent (.05) credit cannot be claimed if the Dependent Care Assistance Program Tax Credit is claimed.

Following the specic Schedule 1299 instructions, enter the Employee Child Care tax credit (Code 5040) total of Part One and Part Two in

Column F on Step 3 of Schedule 1299-D.

This credit is not distributable or transferable.

Enterprise Zone Investment (Credit Code 5080)

35 ILCS 5/201(f)

“Qualied property” is property that

•

is tangible, whether new or used, including buildings and structural components of buildings;

•

is depreciable according to Internal Revenue Code (IRC) Section 167;

•

has a useful life of four or more years as of the date placed in service in Illinois; and

•

is acquired by purchase as dened in IRC Section 179(d).

Qualied property can be new or used but does not qualify for the Enterprise Zone Credit if it was previously used in Illinois in a manner that

qualied for that credit or for the Replacement Tax Investment Credit on Form IL-477, Replacement Tax Investment Credits. Qualied property

includes buildings and structural components of buildings that are real property. It does not include land or improvements to real property that are not

a structural component of a building, such as landscaping, sewer lines, local access roads, fencing, parking lots, and other appurtenances.

Any improvement or addition made on or after the date the enterprise zone or river edge redevelopment zone was designated, or on or after the

date the business was designated as a high impact business, is considered to be qualied property to the extent that the improvement or addition

increases the adjusted basis of the property previously placed in service in Illinois and otherwise meets the requirements of qualied property.

For taxable years ending on or after July 1, 2006, you may take this credit if you

•

placed qualied property in service in an Illinois enterprise zone within the tax year,

•

placed it in service on or after the date the zone was ocially designated as an enterprise zone, and

•

continued to use the qualied property on the last day of your tax year.

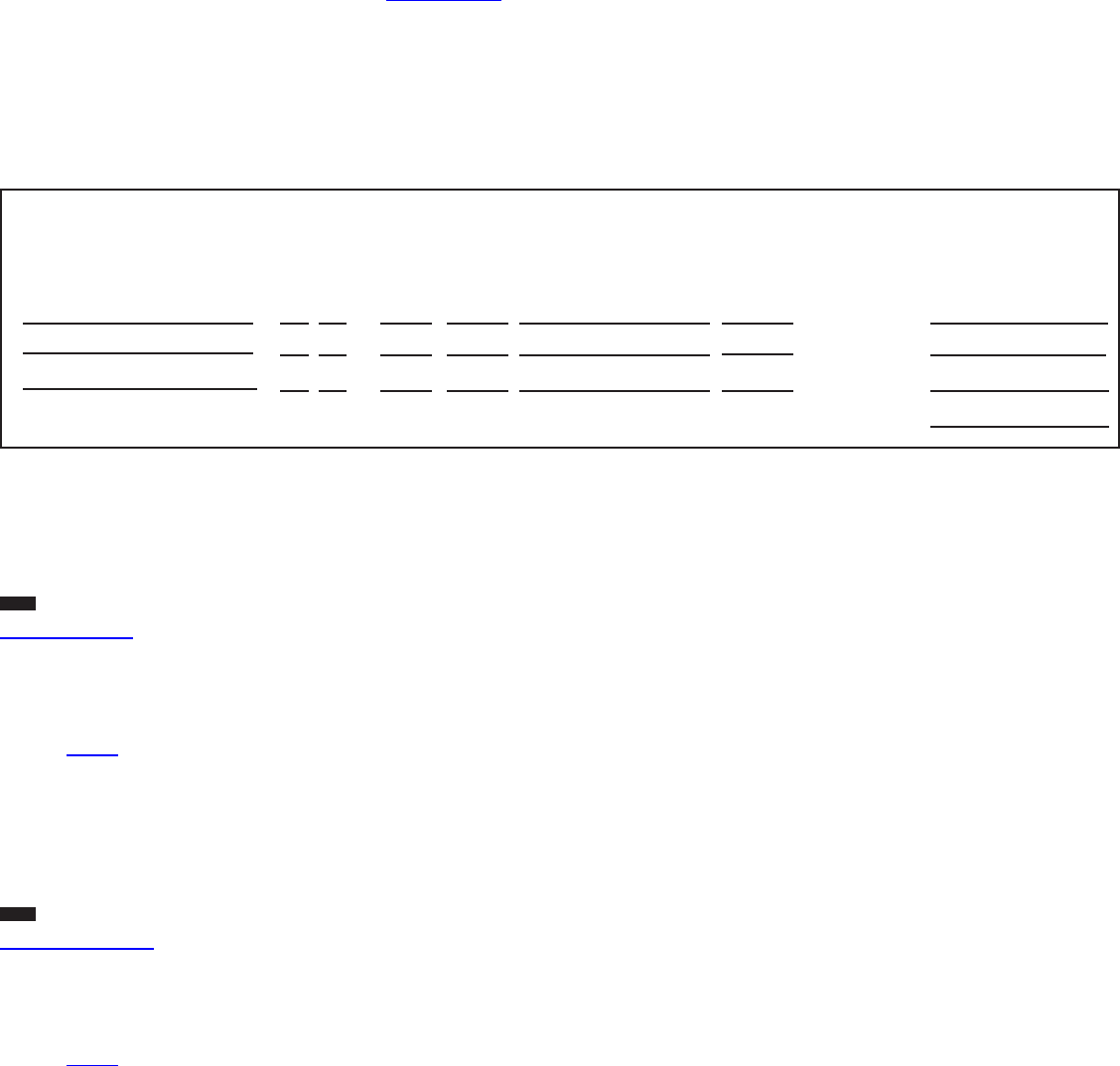

Using the worksheet below and these instructions, gure your Enterprise Zone Investment credit to enter on your Schedule 1299.

Column A – Describe each item of qualied property you placed in service in an Illinois enterprise zone.

Column B – Enter the month and year each item of qualied property was placed in service in Illinois. An item is placed in service on the

earlier of

•

the date the item is placed in a condition or state of readiness and availability for its specically assigned function, or

•

the date the depreciation period of the item begins. (Generally, this will be the same date the item is placed in service for purposes of the

federal depreciation deduction.)

Column C – If you are using the federal accelerated cost recovery system (ACRS) to depreciate the property, enter the ACRS class assigned

to each item of qualied property. Property assigned to an ACRS class of less than four years is not qualied.

If you are not using the ACRS method to depreciate the property, enter the useful life assigned to the property for federal depreciation

purposes. The useful life of the property when placed in service must be four or more years to qualify.

Schedule 1299-I (R-07/24) Page 7 of 17

Column D – Indicate whether each item of qualied property is new or used. If the property was previously used, enter the abbreviation of the

state where the property was located. If you are ling Schedule 1299-D or 1299-A and the property was previously used in Illinois, but not in

a manner that qualied for this credit or for the Replacement Tax Investment Credit on Form IL-477, maintain a statement in your records to

provide upon request.

Column E – Enter the name of the enterprise zone in which the property is used.

Note: Qualied enterprise zones are listed on the DCEO website.

Column F – For each item of property, enter the basis used to gure the depreciation deduction for federal income tax purposes. Generally,

the basis will be the purchase price, plus any capital expenditures, minus any rebates and IRC Section 179 deductions. The basis is not

reduced by depreciation, including bonus depreciation, except depreciation you were allowed to claim before the date you placed it in service

in Illinois, or in an Illinois enterprise or river edge redevelopment zone.

Column G – If you placed property in service in an enterprise zone, the credit rate is .005.

Column H – Multiply each entry in Column F by the amount in Column G, and enter the result in Column H.

Line 4 – Follow the instructions on the worksheet.

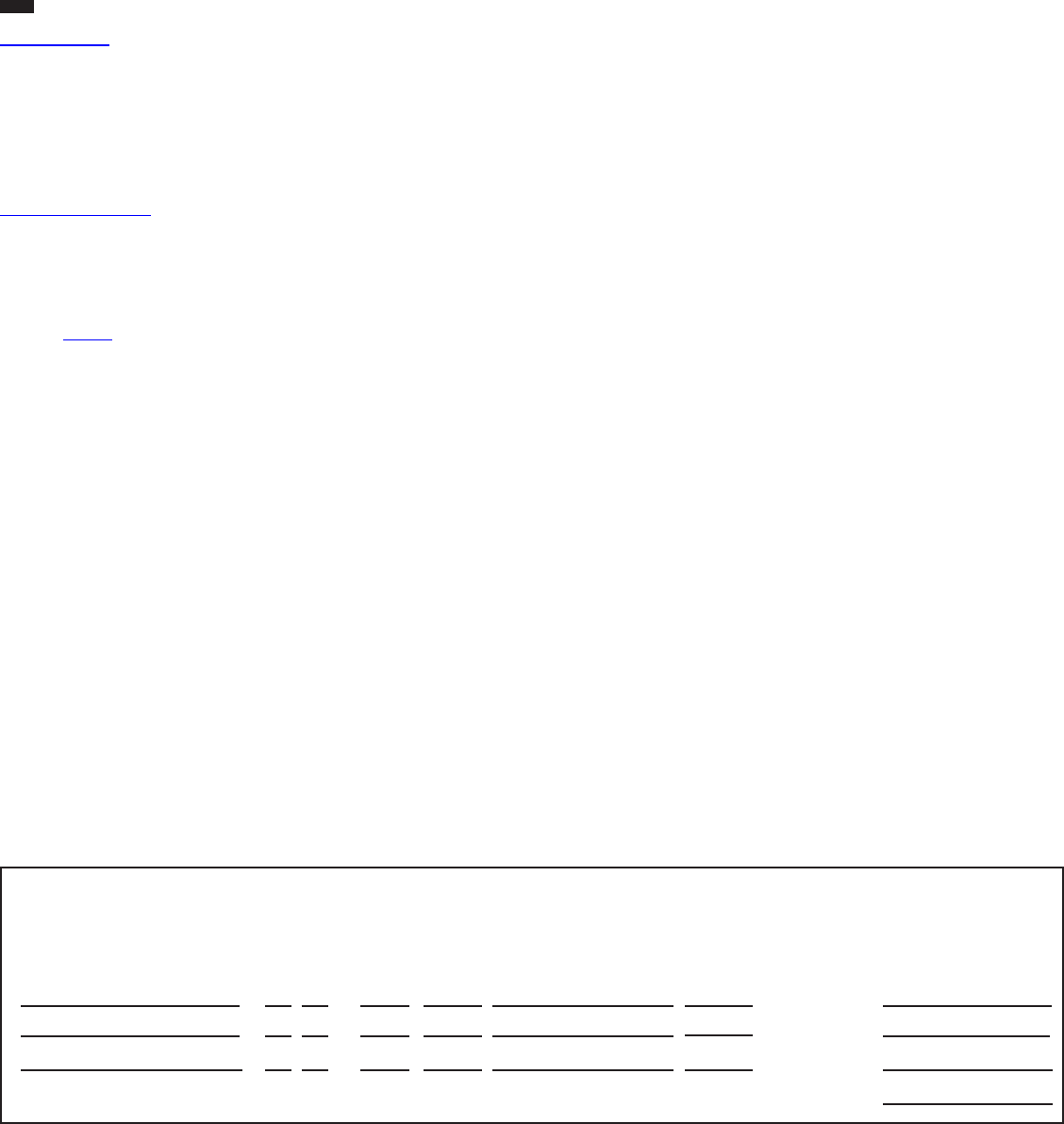

Enterprise Zone Investment Worksheet

A B C D E F G H

Description of Date placed in ACRS New/Used Name of zone Basis Rate Column F x Column G

qualied property service in Illinois class (see instr.)

Month Year

1

/

.005 1

2

/

.005 2

3

/

.005 3

4 Total Column H, Lines 1 through 3. 4

Following the specic Schedule 1299 instructions, enter the Enterprise Zone Investment tax credit (Code 5080) on Step 3 of:

Schedule 1299-A – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from Line 4 above in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Enterprise Zone Construction Jobs (Credit Code 5120)

35 ILCS 5/201(f)

For taxable years beginning on or after January 1, 2021, a taxpayer who has been awarded a credit certicate by DCEO is entitled

to a credit. The amount of the credit shall be 50 percent (75 percent if the project is located in an underserved area) of the amount of

the incremental income tax attributable to Enterprise Zone construction jobs credit employees employed in the course of completing an

Enterprise Zone construction jobs project. To qualify for the credit, you must have applied for and received a tax credit certicate from DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the Enterprise Zone Construction Jobs tax credit (Code 5120) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

High Impact Business Construction Jobs (Credit Code 5160)

35 ILCS 5/201(h-5)

For taxable years beginning on or after January 1, 2021, a taxpayer who has been awarded a credit certicate by DCEO is entitled to

a credit. The amount of the credit shall be 50 percent (75 percent if the project is located in an underserved area) of the amount of the

incremental income tax attributable to High Impact Business construction jobs credit employees employed in the course of completing a High

Impact Business construction jobs project. To qualify for the credit, you must have applied for and received a tax credit certicate from DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the High Impact Business Construction Jobs tax credit (Code 5160) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Schedule 1299-I (R-07/24) Page 8 of 17

High Impact Business Investment (Credit Code 5220)

35 ILCS 5/201(h)

“Qualied property” is property that

•

is tangible, whether new or used, including buildings and structural components of buildings;

•

is depreciable according to Internal Revenue Code (IRC) Section 167;

•

has a useful life of four or more years as of the date placed in service in Illinois; and

•

is acquired by purchase as dened in IRC Section 179(d).

Qualied property, whether new or used, includes buildings and structural components of buildings that are real property. It does not include land

or improvements to real property that are not a structural component of a building, such as landscaping, sewer lines, local access roads, fencing,

parking lots, and other appurtenances.

Any improvement or addition made on or after the date the business was designated as a high impact business, is considered to be qualied

property to the extent that the improvement or addition increases the adjusted basis of the property previously placed in service in Illinois and

otherwise meets the requirements of qualied property.

For tax years ending on or after December 31, 1987, you may take this credit if

•

your business has been designated as a high impact business,

•

you placed qualied property in service on or after the date the business was designated as a high impact business and on or before the

last day of your current tax year, and

•

you continued to use the qualied property on the last day of your tax year.

You may not take this credit

•

if the property is eligible for the Enterprise Zone Investment credit.

•

until the minimum investments in qualied property required under Section 5.5 of the Illinois Enterprise Zone Act have been satised.

You should take the credit applicable to the minimum investments in the tax year in which the minimum investments were completed. Credit

for additional investments (beyond the minimum investments) is available only in the year the qualied property is placed in service.

Using the worksheet on Page 8 and these instructions, gure your High Impact Business Investment credit to enter on your Schedule 1299.

Lines 1 through 3 – For each qualied property that you are claiming a credit:

Column A – Describe each item of qualied property placed in service in Illinois.

Column B – Enter the month and year each item of qualied property was placed in service in Illinois. An item is placed in service on the

earlier of

•

the date the item is placed in a condition or state of readiness and availability for its specically assigned function, or

•

the date the depreciation period of the item begins. (Generally, this will be the same date the item is placed in service for purposes of the

federal depreciation deduction.)

Column C – If you are using the federal accelerated cost recovery system (ACRS) to depreciate the property, enter the ACRS class assigned

to each item of qualied property. Property assigned to an ACRS class of less than four years is not qualied.

If you are not using the ACRS method to depreciate the property, enter the useful life assigned to the property for federal depreciation

purposes. The useful life of the property when placed in service must be four or more years to qualify.

Column D – Indicate whether each item of qualied property is new or used. If the property was previously used, enter the abbreviation of

the state where the property was located. In addition, if the property was previously used in Illinois, but not in a manner that qualied for this

credit or for the Replacement Tax Investment Credit on Form IL-477, maintain a statement in your records to provide upon request.

Column E – For each item of property, enter the basis used to gure the depreciation deduction for federal income tax purposes. Generally,

the basis will be the purchase price, plus any capital expenditures, minus any rebates and IRC Section 179 deductions. The basis is not

reduced by depreciation, including bonus depreciation, except depreciation you were allowed to claim before the date you placed it in service

in Illinois, or in an Illinois enterprise or river edge redevelopment zone.

Column F – Multiply each entry in Column E by .5 percent (.005) and enter the result in Column F.

Line 4 - Follow the instructions on the worksheet.

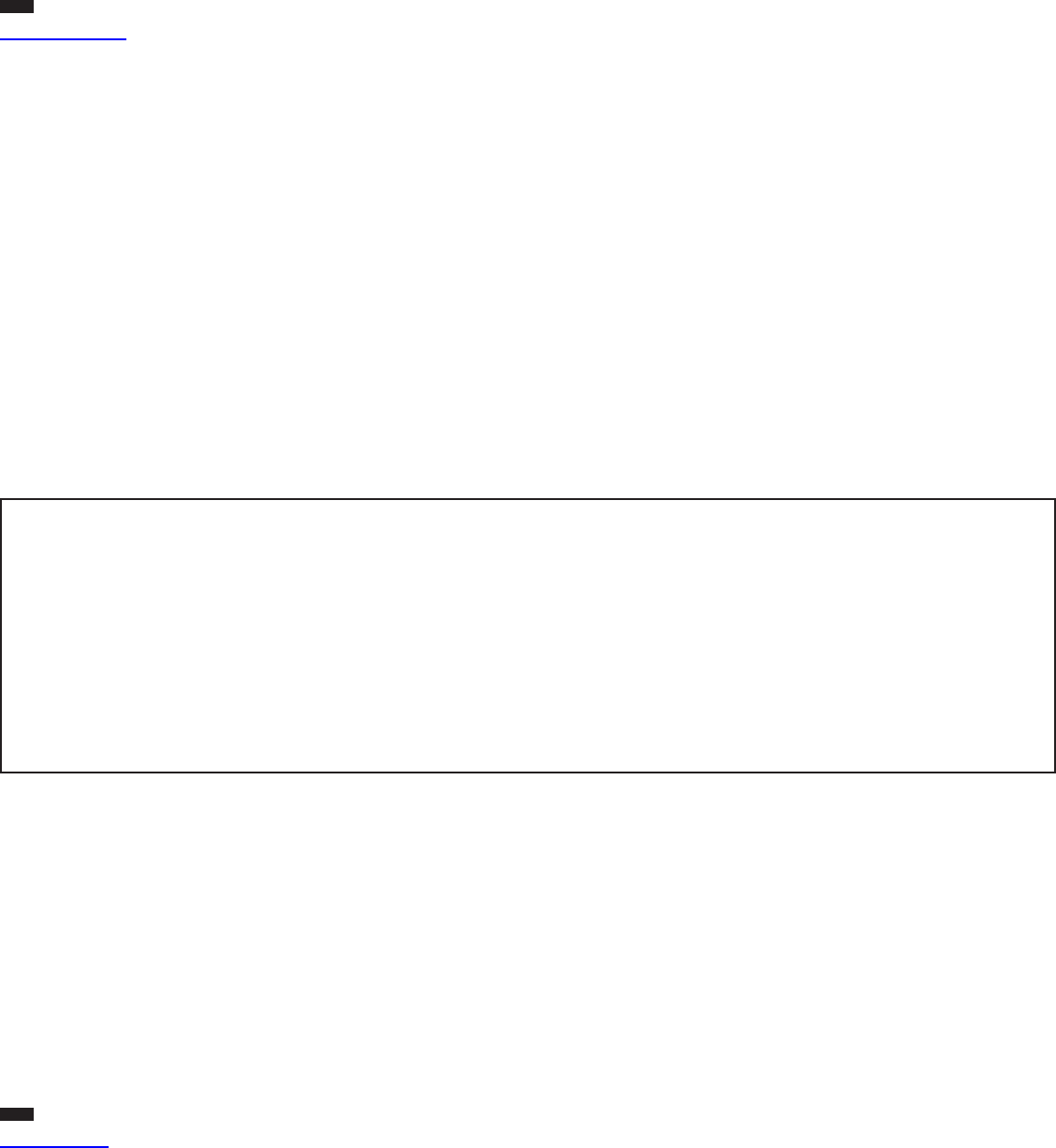

High Impact Business Investment Worksheet

A B C D E F

Description of Date placed in ACRS New/Used Basis Column E x .5% (.005)

qualied property service in Illinois class (see instructions)

Month Year

1_______________________ _____ / _____ _______________ _______________ _______________ 1 _________________

2_______________________ _____ / _____ _______________ _______________ _______________ 2 _________________

3_______________________ _____ / _____ _______________ _______________ _______________ 3 _________________

4 Total Column F, Lines 1 through 3. 4

Following the specic Schedule 1299 instructions, enter the High Impact Business Investment tax credit (Code 5220) on Step 3 of:

Schedule 1299-C – credits from Line 4 above in Column E.

Schedule 1299-D – credits from Line 4 above in Column F.

This credit is not distributable or transferable.

Schedule 1299-I (R-07/24) Page 9 of 17

Reimagining Energy and Vehicles (REV) Illinois Investment (Credit Code 5230)

35 ILCS 5/237

“Qualied property” is property that

(1) is tangible, whether new or used, including buildings and structural components of buildings;

(2) is depreciable pursuant to Section 167 of the Internal Revenue Code, except that “3-year property” as dened in Section 168(c)(2)(A)

of that Code is not eligible for the credit provided by this Section;

(3) is acquired by purchase as dened in Section 179(d) of the Internal Revenue Code;

(4) is used at the site of the REV Illinois Project by the taxpayer; and

(5) has not been previously used in Illinois in such a manner and by such a person as would qualify for the credit.

Public Act 102-0669 provides for tax years beginning on or after November 16, 2021, a credit for taxpayers against the tax imposed by

subsections (a) and (b) of Section 201 for investment in qualied property which is placed in service at the site of a REV Illinois Project subject

to an agreement between the taxpayer and DCEO pursuant to the Reimagining Energy and Vehicles in Illinois Act. The credit is equal to 0.5

percent of the basis for the property. The credit is only available in the taxable year in which the property is put into service. Any taxpayer

qualifying for the REV Illinois Investment Tax Credit shall not be eligible for either the investment tax credits in Section 201(e), (f), or (h) of the

Illinois Income Tax Act. The credit is nonrefundable, but may be carried forward for ve years.

Contact DCEO for more information.

Using the worksheet below and these instructions, gure your REV Illinois Investment credit to enter on your Schedule 1299.

Column A – Describe each item of qualied property you placed in service in a REV Illinois Project.

Column B – Enter the month and year each item of qualied property was placed in service in Illinois. An item is placed in service on the

earlier of

• the date the item is placed in a condition or state of readiness and availability for its specically assigned function, or

•

the date the depreciation period of the item begins. (Generally, this will be the same date the item is placed in service for purposes of the

federal depreciation deduction.)

Column C – If you are using the federal accelerated cost recovery system (ACRS) to depreciate the property, enter the ACRS class assigned

to each item of qualied property. Property assigned to an ACRS class of less than four years is not qualied.

If you are not using the ACRS method to depreciate the property, enter the useful life assigned to the property for federal depreciation

purposes. The useful life of the property when placed in service must be four or more years to qualify.

Column D – Indicate whether each item of qualied property is new or used. If the property was previously used, enter the abbreviation of the

state where the property was located. If you are ling Schedule 1299-D or 1299-A and the property was previously used in Illinois, but not in

a manner that qualied for this credit or for the Replacement Tax Investment Credit on Form IL-477, maintain a statement in your records to

provide upon request.

Column E – Enter the location of the REV Illinois Project in which the property is used.

Column F – For each item of property, enter the basis used to gure the depreciation deduction for federal income tax purposes. Generally,

the basis will be the purchase price, plus any capital expenditures, minus any rebates and IRC Section 179 deductions. The basis is not

reduced by depreciation, including bonus depreciation, except depreciation you were allowed to claim before the date you placed it in service

in Illinois, or in an Illinois enterprise or river edge redevelopment zone or in the location of a REV Illinois Project.

Column G – If you placed property in service in a REV Illinois Project, the credit rate is .005.

Column H – Multiply each entry in Column F by the amount in Column G, and enter the result in Column H.

Line 4 – Follow the instructions on the worksheet.

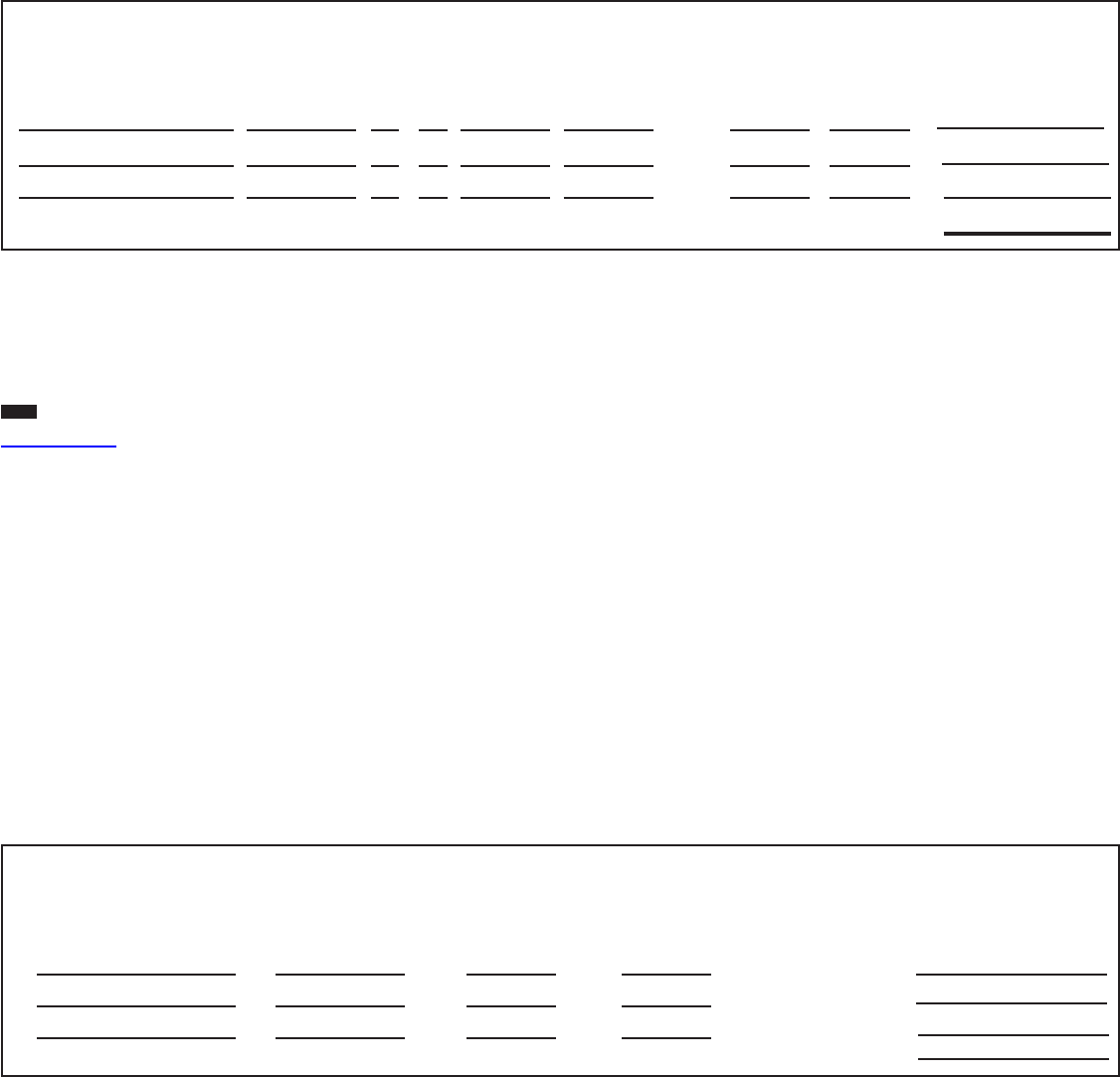

REV Illinois Investment Credit Worksheet

A B C D E F G H

Description of Date placed ACRS New/Used Location of REV Basis Rate Column F x Column G

qualied property in service in class (see instr.) Illinois Project

Illinois

Month Year

1 / .005 1

2 / .005 2

3 / .005 3

4 Total Column H, Lines 1 through 3. 4

Following the specic Schedule 1299 instructions, enter the REV Illinois Investment tax credit (Code 5230) on Step 3 of:

Schedule 1299-A – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from Line 4 above in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Schedule 1299-I (R-07/24) Page 10 of 17

Aordable Housing Donations (Credit Code 5260)

35 ILCS 5/214

You may take this credit if

• you have made a donation under Section 7.28 of the Illinois Housing Development Act for the development of aordable housing in

Illinois,

• you made the donation in a tax year ending on or after December 31, 2001, through a tax year ending on or before

December 31, 2026, and

• you were issued an Illinois Aordable Housing Tax Credit certicate from Illinois Housing Development Authority (IHDA) or the City of

Chicago’s Department of Housing and Economic Development,

• you received Schedule(s) K-1-P distributing this credit to you by a pass-through entity, or

• you received a transfer of credit meeting the following criteria:

• Under IITA Section 214(c), the credit allowed under this Section may be transferred: A) to the purchaser of land that has been

designated solely for aordable housing projects in accordance with the Illinois Housing Development Act; or B) to another donor who

has also made a donation in accordance with Section 7.28 of the Illinois Housing Development Act.

• Persons or entities not subject to the tax imposed by IITA Section 201(a) and (b) and who made a donation under Section 7.28 of the

Illinois Housing Development Act are entitled to a credit as described in this Section and may transfer that credit as provided in this

subsection (c). (IITA Section 214(a))

• Transfer of the credit shall be made pursuant to 47 Ill. Adm. Code 355.309.

• Transfer may be made of all or of any portion of the credit allowable to the transferor. However, any portion of a credit that has already

been used to reduce the tax of a transferor may not be transferred.

The credit is 50 percent (.50) of the total amount of your donation to qualied aordable housing projects or the total amount of the credit that

was distributed or transferred to you.

Following the specic Schedule 1299 instructions, enter the Aordable Housing Donations tax credit (Code 5260) on Step 3 of:

Schedule 1299-A – credits earned from IHDA or City of Chicago certicates in Column E, credits distributed to you in Column F, and credits

transferred to you in Column G.

Schedule 1299-C – credits earned from IHDA or City of Chicago certicates in Column E, and credits distributed and transferred to you in

Column F.

Schedule 1299-D – credits earned from IHDA or City of Chicago certicates in Column F, credits distributed to you in Column G, and credits

transferred to you in Column H.

Attach the IHDA or City of Chicago certicates, any Schedule(s) K-1-P received listing this credit, and any transfer documentation to support

the credit claimed to your Schedule 1299.

Economic Development for a Growing Economy (EDGE) (Credit Code 5300)

35 ILCS 5/211

You may take this credit if

•

you have entered into an agreement with DCEO, either under the Economic Development for a Growing Economy Tax Credit Act or the

Corporate Headquarters Relocation Act, between January 1, 1999, and June 30, 2027, and

•

you meet the conditions stated in your agreement with DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the Economic Development for a Growing Economy (EDGE) tax credit (Code 5300)

on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

New Construction EDGE (Credit Code 5320)

35 ILCS 10/5-51

For taxable years beginning on or after January 1, 2021, a taxpayer who has been awarded a credit certicate by DCEO is entitled to a

credit. The amount of the credit shall be 50% (75% if the project is located in an underserved area) of the amount of the incremental income

tax attributable to New Construction EDGE credit employees employed in the course of completing a New Construction EDGE project. To

qualify for the credit, you must have applied for and received a tax credit certicate from DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the New Construction EDGE tax credit (Code 5320) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Schedule 1299-I (R-07/24) Page 11 of 17

Research and Development (Credit Code 5340)

35 ILCS 5/201(k)

A taxpayer is entitled to take this credit for tax years ending on or after December 31, 2004 and ending prior to January 1, 2032.

(Qualifying expenses must be from research activities conducted in Illinois.)

“Qualifying expenses” are expenditures qualifying under IRC Section 41 that are attributable to research in Illinois, including certain

payments to qualied organizations for basic research in Illinois.

“Qualifying expenses for increasing research activities in Illinois” are the excess of qualifying expenses incurred for the current tax year

over qualifying expenses incurred for the base period.

“Base period” is the three tax periods immediately preceding the current year.

“Qualied research” is research or experimental activities that create or improve a function, performance, reliability, or quality. Research

must be performed in Illinois and be of a technical nature and be intended to be useful in the development of a new or improved business

component held for sale, lease, license, or use by you in your business.

You may take this credit if you have certain qualifying expenses for increasing qualied research activities in Illinois. You may not take this

credit for the following types of activities:

• research conducted after the beginning of commercial production;

• research adapting an existing product or process to a particular customer’s need;

• duplication of an existing product or process;

• surveys or studies;

• research relating to certain internal-use computer software;

• research conducted outside Illinois;

• research in the social sciences, arts, or humanities; or

• research funded by another person (or government entity).

Using the worksheet and instructions below, gure your Illinois qualifying expenses to enter on the Research and Development Worksheet on

your Schedule 1299-C or 1299-A, Step 2 or Schedule 1299-D, Step 1.

Research and Development Worksheet

(Qualifying expenses must be from research activities conducted in Illinois.)

A B

Enter the following:

Base period avg. expenses This year’s expenses

1 Illinois wages for qualied services. See instructions below. 1 ___________________ ___________________

2 Illinois cost of supplies 2 ___________________ ___________________

3 Illinois rental or lease costs of computers 3 ___________________ ___________________

4 65% (.65) of Illinois contract expenses 4 ___________________ ___________________

5 Illinois basic research payments to qualied organizations (corporations only) 5 ___________________ ___________________

6 Add Lines 1 through 5 of each column. Total Illinois qualifying expenses. 6 ___________________ ___________________

Lines 1 through 5 – Follow the instructions below to determine the amount to enter in Column A and Column B.

Column A – Enter the yearly average of the base period qualied expenses resulting from activities that were conducted in Illinois.

If you were not doing business in Illinois during one or more of the tax years included in the base period, use “0” as the factor for that tax

year when computing the yearly average base period qualied expenses.

If you were doing business in Illinois for less than an entire year during any tax year in the base period, the qualifying expenses

(Lines 1 through 5) for that year must be annualized as follows: (qualied expenses x number of days taxable by Illinois) ÷ (365).

Column B – Enter the current year qualied expenses resulting from activities that were conducted in the State of Illinois.

Line 6 – Add Lines 1 through 5 of each column. Transfer the amount on Line 6 in both columns to the Research and Development Worksheet

on Schedule 1299-C or 1299-A, Step 2 or Schedule 1299-D, Step 1. Follow the instructions on your Schedule 1299 to determine the amount

to enter as the Research and Development tax credit (Code 5340) on Step 3 of:

Schedule 1299-A – credits from Step 2 in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from Step 2 in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from Step 1 in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach any Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Wages Paid to Ex-Felons (Credit Code 5380)

35 ILCS 5/216

“Qualied wages” means wages you paid during the one-year period beginning with the date an ex-oender begins working for you. Only

wages that are subject to unemployment tax under IRC Section 3306 qualify. This includes amounts in excess of the maximum taxable wage.

Wages paid during any period for which you received federally funded payments for on-the-job training for the ex-oender do not qualify.

A “qualied ex-oender” means an Illinois resident who

• has been convicted of any crime in this State or of any oense in any other jurisdiction, other than an oense or attempted oense that

would subject a person to registration under the Sex Oender Registration Act;

• was sentenced to a period of incarceration in an Illinois adult correctional center; and

• was hired by you within three years after being released from the adult correctional center.

Schedule 1299-I (R-07/24) Page 12 of 17

For tax years beginning on or after January 1, 2007, the Credit for Wages Paid to Ex-Felons is 5 percent (.05) of qualied wages paid

during the taxable year to an employee who is a qualied ex-oender. The total credits for all tax years for wages paid to a particular

ex-oender may not exceed $1500.

Using the worksheet and these instructions, gure your Wages Paid to Ex-Felons credit to enter on your Schedule 1299.

Lines 1 through 3 – For each ex-oender for whom you are claiming a credit:

Column A – Enter the name of the qualied ex-oender.

Column B – Enter the Social Security number of the qualied ex-oender.

Column C – Enter the date you hired the qualied ex-oender.

Column D – Enter the amount of qualied wages you paid to this ex-oender during the taxable year. Do not include any wages paid more

than one year after the date of hiring.

Column E – Multiply the amount in Column D by 5 percent (.05).

Column G – If you claimed a Wages Paid to Ex-Felons credit for this ex-oender in the prior year, enter the total amount of credit claimed.

Otherwise, enter “0”.

Column H – Subtract the amount in Column G from Column F. This amount cannot be less than zero.

Column I – Enter the amount from Column E or Column H, whichever is less.

Line 4 – Follow the instructions on the worksheet.

Wages Paid to Ex-Felons Worksheet

A B C D E F G H I

Date Qualied Col. D Max credit Prior Col. F minus Enter the lesser of

Name SSN hired wages x 5% (.05) amount credit Col. G Column E or H

1

/

$1,500 1

2

/

$1,500 2

3

/

$1,500 3

4 Add Column I, Lines 1 through 3.

4

Following the specic Schedule 1299 instructions, enter the Wages Paid to Ex-Felons tax credit (Code 5380) on Step 3 of:

Schedule 1299-A – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from Line 4 above in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach any Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Student-Assistance Contributions (Credit Code 5420)

35 ILCS 5/218

“Qualied Illinois prepaid tuition programs” include:

• Illinois Bright Start College Savings Program,

• Illinois Bright Directions College Savings Program,

• College Illinois Prepaid Tuition Program.

For taxable years ending on or after December 31, 2009, and on or before December 31, 2029, if you are an employer who makes a

matching contribution to a qualied Illinois prepaid tuition program on behalf of your employees, you are entitled to a credit of 25 percent (.25)

of the contribution for each employee or $500 per employee, whichever is less.

Using the worksheet and instructions, gure your Student-Assistance Contributions credit to enter in your Schedule 1299.

Lines 1 through 3 – For each employee for whom you made a matching contribution:

Column A – Enter the name of the employee.

Column B – Enter the Social Security number of the employee.

Column C – Enter the amount of the matching contribution you made.

Column D – Multiply the amount in Column C by 25 percent (.25).

Column F – Enter the amount from Column D or the amount from Column E, whichever is less.

Line 4 – Follow the instructions on the worksheet.

Student-Assistance Contributions Worksheet

A B C D E F

Qualied Column C Max credit Enter the lesser

Name SSN contribution amount x 25% (.25) amount of Column D or E

1 $500 1

2

$500 2

3

$500 3

4 Add Column F, Lines 1 through 3. 4

Schedule 1299-I (R-07/24) Page 13 of 17

Following the specic Schedule 1299 instructions, enter the Student-Assistance Contributions tax credit (Code 5420) on Step 3 of:

Schedule 1299-A – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from Line 4 above in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from Line 4 above in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach any Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Agritourism Liability Insurance (Credit Code 5440)

35 ILCS 5/232

For tax years beginning on or after January 1, 2022, and ending on or before December 31, 2023, an Agritourism Liability Insurance

credit may be claimed in an amount equal to the lesser of 100% of the liability insurance premiums paid during the taxable year or $1,000. To

qualify for the credit, you must have applied for and received a tax credit certicate from IDOA.

Contact IDOA for more information.

Following the specic Schedule 1299 instructions, enter the Agritourism Liability Insurance tax credit (Code 5440) on Step 3 of:

Schedule 1299-A – credits from IDOA certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from IDOA certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from IDOA certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every IDOA certicate and Schedule(s) K-1-P received listing this credit to your

Schedule 1299.

Angel Investment (Credit Code 5460)

35 ILCS 5/220

For tax years beginning on or after January 1, 2011, and ending on or before December 31, 2026, an Angel Investment credit may be

claimed in an amount equal to:

• 25 percent (.25) of an investment made directly in a qualied new business, or

• 35 percent (.35) of an investment made directly in a qualied new business venture in which:

• the new business is a minority-owned business, a women-owned business, or a business owned a person with a disability (as those

terms are used and dened in the Business Enterprise for Minorities, Women, and Persons with Disabilities Act); or

• the principal place of the business is located in a county with a population of not more than 250,000.

To qualify for the credit, you must have applied for and received a tax credit certicate from DCEO. Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the Angel Investment tax credit (Code 5460) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Quantum Computing Campuses (Credit Code 5480)

35 ILCS 5/241

For tax years ending on or after June 26, 2024, a taxpayer who has been awarded a credit by DCEO is entitled to a credit against the taxes

imposed under subsections (a) and (b) of Section 201 of the IITA. The amount of the credit shall be 20% of the wages paid by the taxpayer

during the taxable year to a full-time or part-time employee of a construction contractor employed in the construction of an eligible facility

located on a quantum computing campus. To qualify for the credit, you must have applied for and received a tax credit certicate from DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the Quantum Computing Campuses credit (Code 5480) on Step 3 of:

Schedule 1299-A – credits from the DCEO certicate in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from the DCEO certicate in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from the DCEO certicate in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your

Schedule 1299.

New Markets Development (Credit Code 5500)

20 ILCS 663/1 et. seq.

The New Markets Development credit is allowed for qualied investments made in a community development entity in tax years beginning

on or after December 31, 2008 and ending before July 1, 2031. Credits are allowed on the second anniversary of the investment and the

next four anniversaries. To qualify for this credit, you must have applied for and received a tax credit certicate from DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the New Markets Development tax credit (Code 5500) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Schedule 1299-I (R-07/24) Page 14 of 17

River Edge Historic Preservation (Credit Code 5540)

35 ILCS 5/221

For tax years beginning on or after January 1, 2012, and ending prior to January 1, 2027, the River Edge Historic Preservation credit is

available for projects located in river edge redevelopment zones. The credit is awarded by the Department of Natural Resources (DNR). To

qualify for this credit, you must have applied for and received a tax credit certicate from DNR.

Contact DNR for more information.

Following the specic Schedule 1299 instructions, enter the River Edge Historic Preservation tax credit (Code 5540) on Step 3 of:

Schedule 1299-A – credits from DNR certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DNR certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DNR certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DNR certicate and Schedule(s) K-1-P received listing this credit to your

Schedule 1299.

River Edge Construction Jobs (Credit Code 5560)

35 ILCS 5/221

For taxable years beginning on or after January 1, 2021, and ending prior to January 1, 2027, a taxpayer who has been awarded a credit

certicate by DCEO is entitled to a credit. The amount of the credit shall be 50% (75% if the project is located in an underserved area) of the

amount of the incremental income tax attributable to River Edge construction job employees employed in the course of completing a River

Edge construction job project. To qualify for the credit, you must have applied for and received a tax credit certicate from DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the River Edge Construction Jobs tax credit (Code 5560) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from DCEO certicates in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F and credits distributed to you in Column G.

This credit is not transferable. Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Live Theater Production (Credit Code 5580)

35 ILCS 5/222

For tax years beginning on or after January 1, 2012, and beginning prior to January 1, 2027, the Live Theater Production credit is

awarded based on applications approved through DCEO.

To qualify for this credit, you must have

• applied for and received a tax credit certicate from DCEO, or

• received a certicate from DCEO showing that a credit was transferred to you. A transfer of the tax credit may be made by the taxpayer

earning the credit within one year after the credit is awarded in accordance with rules adopted by DCEO.

Contact DCEO for more information.

Following the specic Schedule 1299 instructions, enter the Live Theater Production tax credit (Code 5580) on Step 3 of:

Schedule 1299-A – credits from DCEO certicates in Column E, credits distributed to you in Column F, and credits transferred to you in

Column G.

Schedule 1299-C – credits from DCEO certicates in Column E, and credits distributed and transferred to you in Column F.

Schedule 1299-D – credits from DCEO certicates in Column F, credits distributed to you in Column G, and credits transferred to you in

Column H.

Attach a copy of every DCEO certicate and Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Hospital (Credit Code 5620)

35 ILCS 5/223

For tax years ending on or after December 31, 2012, and ending on or before December 31, 2027, the Hospital credit is available to the

owner of a hospital that

• is licensed under the Hospital Licensing Act, and

• is not exempt from federal income taxes under the Internal Revenue Code.

The credit is an amount equal to the lesser of the amount of real property taxes paid on Illinois property used for hospital purposes during

the prior tax year or the cost of free or discounted services provided during the current tax year at Illinois locations in accordance with the

hospital’s charitable nancial assistance policy, measured at cost.

The Hospital credit may be transferred, either by selling or donating the credit,

• by the taxpayer who originally earned the credit, and

• only if the transfer occurs within one year after the due date of the transferor’s return for the period in which the credit is earned.

The taxpayer transferring the credit must attach to their Schedule 1299-C,1299-D, or 1299-A a copy of the written notice of the transfer stating

the intent to sell or donate the credit, including the amount of credit to be transferred, the date of the transfer, and the name, address, and the

Federal Employer Identication Number (FEIN) or Social Security Number (SSN) of the recipient. A copy of this notice must also be provided

to the recipient of the credit who in turn should attach a copy of the notice to their Schedule 1299-C, 1299-D or 1299-A when ling their

return. If you transfer the credit after your original return has been submitted, you must submit an amended return and all aected supporting

documents to report the transfer.

Schedule 1299-I (R-07/24) Page 15 of 17

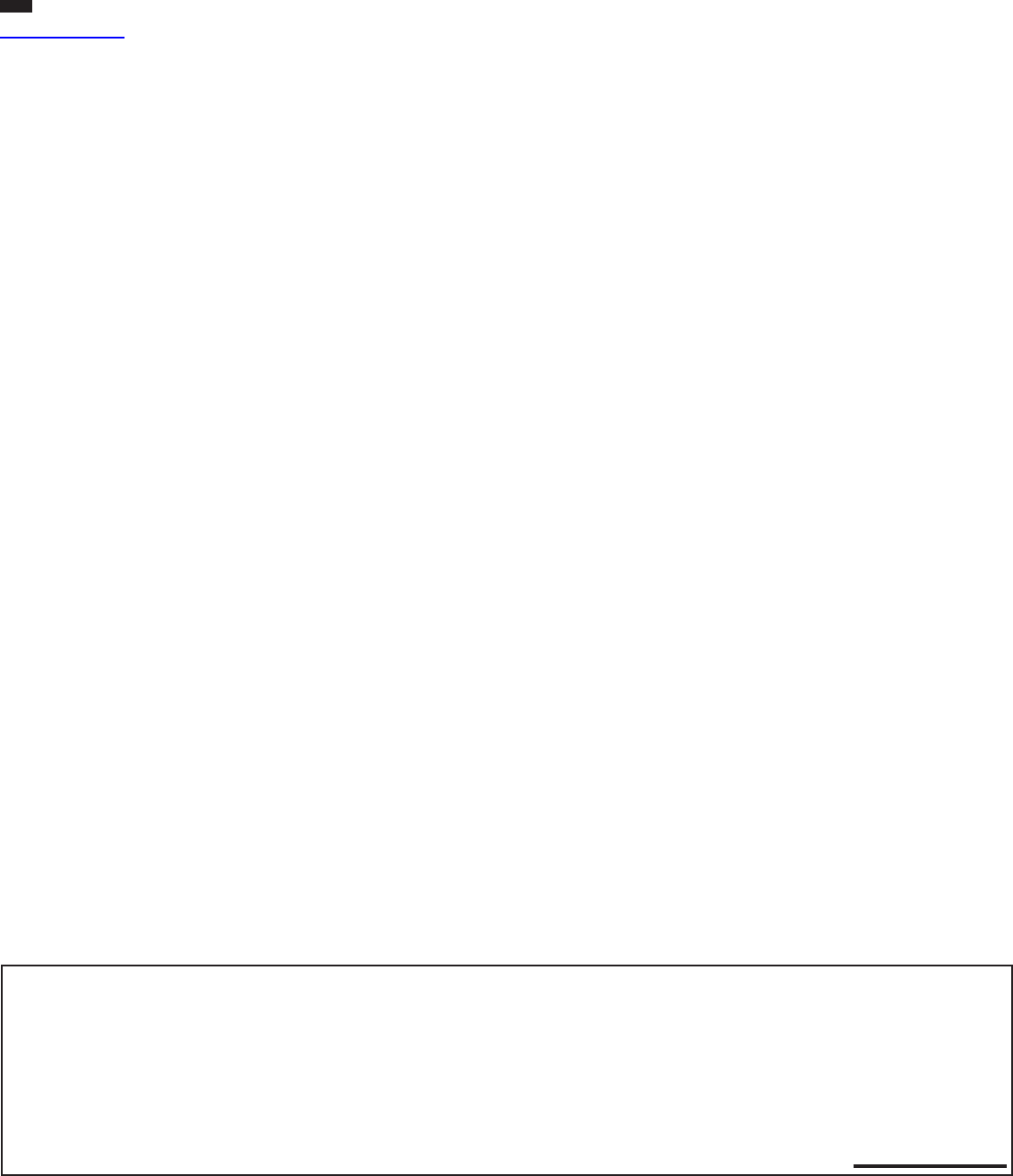

Use the worksheet below to gure your Hospital credit.

Hospital Worksheet

1 Enter the amount of real property taxes paid during the tax year on Illinois real property used for

hospital purposes during the prior tax year. 1

2 Enter the cost of free or discounted services provided at Illinois locations during the tax year pursuant

to the hospital’s charitable nancial assistance policy, measured at cost. 2

3 Enter the lesser of Line 1 or Line 2. This is your Hospital credit before transfers. 3

4 Enter any amount of the credit from Line 3 you have transferred or intend to transfer and attach a written

notice of the transfer. 4

5 Subtract Line 4 from Line 3. 5

Following the specic Schedule 1299 instructions, enter the Hospital tax credit (Code 5620) on Step 3 of:

Schedule 1299-A – credits from Line 5 above in Column E, credits distributed to you in Column F, and credits transferred to you in Column G.

Schedule 1299-C – credits from Line 5 above in Column E, and credits distributed and transferred to you in Column F.

Schedule 1299-D – credits from Line 5 above in Column F, credits distributed to you in Column G, and credits transferred to you in Column H.

Attach any transfer documentation and any Schedule(s) K-1-P received listing this credit to your Schedule 1299.

Invest in Kids (Credit Code 5660)

35 ILCS 5/224

For taxable years beginning on or after January 1, 2018, and ending before January 1, 2024, you are eligible for this credit if you made

a qualied contribution to one or more Scholarship Granting Organizations (SGO) during the taxable year and did not claim any portion of the

contribution as a federal tax deduction.

For each Certicate of Receipt (COR) you receive from the SGO(s), enter the total amount from the COR on the line below. Multiply this amount

by 75 percent (.75).

x .75 =

Each COR you receive must be entered on a separate line of Schedule 1299. Use the formula above to determine the amount to enter as the

Invest in Kids tax credit (Code 5660) on Step 3 of:

Schedule 1299-A – credits from the line above in Column E and credits distributed to you in Column F.

Schedule 1299-C – credits from the line above in Column E and credits distributed to you in Column F.

Schedule 1299-D – credits from the line above in Column F and credits distributed to you in Column G.

This credit is not transferable. Do not attach a copy of your COR to Schedule 1299-D, 1299-C or 1299-A; however, you must maintain the

copy in your records in the event the Department requests to see the copy. Attach Schedule(s) K-1-P received listing this credit to your

Schedule 1299.

Note: Remember to enter the Certicate Number in the correct column.

K-12 Instructional Materials and Supplies (Credit Code 5740) (Form IL-1040 lers only)

35 ILCS 5/225

For tax years beginning on and after January 1, 2017, the K-12 Instructional Materials and Supplies credit is available to eligible educators

for qualied expenses paid during the taxable year. For taxable years beginning on or after January 1, 2023, eligible educators can claim a

credit up to $500 for qualied expenses paid in the current taxable year. If married, ling jointly, and both taxpayers were eligible educators,

the maximum credit is $1000.

DEFINITIONS

“Eligible educator” is a kindergarten through twelfth grade teacher, instructor, counselor, principal, or aide in a qualied K-12 school for at

least 900 hours during a school year.

“Materials and supplies” are instructional materials or supplies designated for classroom use in any qualied school.

“Qualied expenses” include ordinary and necessary expenses paid in connection with books, supplies (including nonathletic supplies for

courses of instruction in health or physical education), equipment (including computer equipment, software, and services), and other materials

used in the classroom. An ordinary expense is one that is common and accepted in your educational eld. A necessary expense is one that is

helpful and appropriate for your profession as an educator. An expense does not have to be required to be considered necessary.

NOTE: Qualied expenses do not include expenses paid for instruction in a home school.

“Qualied school” is a public school or non-public school located in Illinois.

Note: Home schools are not qualied schools.

Using the worksheet on Schedule 1299-C and the instructions below gure your K-12 Instructional Materials and Supplies credit.

If you are an eligible educator and you paid amounts for instructional materials and supplies during the taxable year, complete all lines in

Column A. If you le a joint return, and your spouse is an eligible educator who paid amounts for instructional materials and supplies during

the taxable year, complete all lines in Column B.

Line 11a - Enter the Professional Educator License number, if applicable. If not applicable, enter “N/A”.

Line 11b - Enter the name of the Illinois school where the taxpayer or spouse was employed as a teacher, instructor, counselor, principal, or

aide for at least 900 hours during the school year.

Schedule 1299-I (R-07/24) Page 16 of 17

Line 11c - Enter the total qualied expenses paid during the taxable year for instructional materials and supplies used in classroom-based

instruction at the school entered on Line 11b.

Line 11d - Enter the lesser of the amount on Line 11c or the maximum credit. The maximum credit amount allowed for each column is $500.

Line 12 - Add Line 11d, Columns A and B, and enter the result. Enter this amount in Column E on Schedule 1299-C, Step 3, on the line that

you enter “5” in Column A and Credit Code 5740 in Column B.

This credit is not distributable or transferable.

Adoption (Credit Code 5780) (Form IL-1040 lers only)

35 ILCS 5/227

For tax years ending on or after December 31, 2018, and on or before December 31, 2029, if you have qualied adoption expenses in the

course of adopting an eligible child, you are entitled to the Adoption credit in the amount equal to the amount of the federal adoption tax credit

received subject to the limitations detailed in Part 2. DO NOT include any federal carryover when determining the amount of federal adoption

tax credit received. An eligible child is any individual who has not attained age 18, or is physically or mentally incapable of caring for himself

or herself. The credit is allowed

•

in the case of any expense paid or incurred before the taxable year in which the adoption becomes nal, for the taxable year following

the taxable year during which the adoption expense is paid or incurred, or

•

in the case of an expense paid or incurred during or after the taxable year in which the adoption becomes nal, for the taxable year in

which such expense is paid or incurred.

No credit will be allowed for any expense for which funds are received from any Federal, State or local program. Spouses ling a joint return

are considered one taxpayer. For nonresidents and part-year residents, the amount of credit shall be in proportion to the amount of income

attributable to this state.

Using the worksheet on Schedule 1299-C, Step 2, and the instructions below, gure your Adoption credit. Attach additional pages in the same

format, if you are claiming the Adoption credit for more than three children.

Part 1 - Adopted Child Information - For each eligible child you are adopting or have adopted and are claiming qualifying adoption

expenses, enter the name, identifying number (Social Security number, ITIN, etc.), birth date (month and year) and check the appropriate

box(es)

•

if the adopted child is an Illinois resident at the time the expenses are paid or incurred.

•

if the adoption is nal during this tax year.

Part 2 - Figure Your Credit - The total amount of qualied adoption expenses allowed as a credit shall not exceed $2,000 ($1,000 in the

case of married ling separate return). However, the credit allowed increases to $5,000 ($2,500 in the case of a married ling separate return)

if the adoption is of an eligible child who is at least one year old and resides in Illinois at the time the expenses are paid or incurred.

Note: When qualied adoption expenses are reported over multiple tax years for the adoption of the same child, any amount of Illinois

Adoption credit previously received for this child must be included on your Schedule 1299-C, Part 2, Line 16b, Adoption Credit worksheet.

Your total adoption credit for all tax years may not exceed the maximum allowable credit for the adoption of that child.

Line a - Enter the maximum credit allowed based on the above description.

Line b - Enter the amount of any adoption credit previously claimed on an Illinois return for the same child. The maximum credit on Line a

is for the entire adoption of that child, no matter how many years the adoption takes to complete.

Line c - Follow the directions on the worksheet.

Line d - Enter the qualied adoption expense you paid or incurred (usually, Line 5 of federal Form 8839, Qualied Adoption Expenses)

where qualied adoption expense means any reasonable and necessary adoption fees, court costs, attorney fees, and other expenses

which are

•

directly related to, and the principal purpose of which is, the legal adoption of an eligible child by the taxpayer,

•

not incurred in violation of State or Federal law or in carrying out any surrogate parenting arrangement,

•

not expenses in connection with the adoption by an individual of a child who is the child of such individual’s spouse, and

•

not reimbursed under an employer program or otherwise.

Line e - Follow the directions on the worksheet.

Line f - Total all columns of Line e and enter the result here.

Line g - Follow the directions on the worksheet.

Line h - Follow the directions on the worksheet. Enter the total in Column E of your Schedule 1299-C, Step 3, on the line that you enter “5”

in Column A and Credit Code 5780 in Column B.