NBER WORKING PAPER SERIES

MARKET DESIGN, HUMAN BEHAVIOR, AND MANAGEMENT

Yan Chen

Peter Cramton

John A. List

Axel Ockenfels

Working Paper 26873

http://www.nber.org/papers/w26873

NATIONAL BUREAU OF ECONOMIC RESEARCH

1050 Massachusetts Avenue

Cambridge, MA 02138

March 2020

Chen acknowledges financial support from the National Science Foundation via grant numbers

SES-1620319 and 1838994. Cramton and Ockenfels acknowledge funding by the European

Research Council (ERC) under the European Union’s Horizon 2020 research and innovation

program under grant agreement No 741409, as well as by the German Research Foundation

(DFG) under Germany´s Excellence Strategy (EXC 2126/1– 390838866). The views expressed

herein are those of the authors and do not necessarily reflect the views of the National Bureau of

Economic Research.

NBER working papers are circulated for discussion and comment purposes. They have not been

peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies

official NBER publications.

© 2020 by Yan Chen, Peter Cramton, John A. List, and Axel Ockenfels. All rights reserved.

Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission

provided that full credit, including © notice, is given to the source.

Market Design, Human Behavior, and Management

Yan Chen, Peter Cramton, John A. List, and Axel Ockenfels

NBER Working Paper No. 26873

March 2020

JEL No. C91,C93,D4,D47,D9

ABSTRACT

We review past research and discuss future directions on how the vibrant research areas of market

design and behavioral economics have influenced and will continue to impact the science and

practice of management in both the private and public sectors. Using examples from various

auction markets, reputation and feedback systems in online markets, matching markets in

education, and labor markets, we demonstrate that combining market design theory, behavioral

insights, and experimental methods can lead to fruitful implementation of superior market designs

in practice.

Yan Chen

School of Information

University of Michigan

105 South State Street

Ann Arbor, Mich 48109

United States

Peter Cramton

Department of Economics

University of Cologne

D-50923 Köln

Germany

John A. List

Department of Economics

University of Chicago

1126 East 59th

Chicago, IL 60637

and NBER

Axel Ockenfels

Department of Economics

University of Cologne

D-50923 Köln

Germany

1

Market Design, Human Behavior and Management

Yan Chen

a

, Peter Cramton

b

, John A. List

c

, and Axel Ockenfels

d

March 12, 2020

We review past research and discuss future directions on how the vibrant research

areas of market design and behavioral economics have influenced and will continue to

impact the science and practice of management in both the private and public sectors.

Using examples from various auction markets, reputation and feedback systems in

online markets, matching markets in education, and labor markets, we demonstrate

that combining market design theory, behavioral insights, and experimental methods

can lead to fruitful implementation of superior market designs in practice.

1 Introduction

Since the 1990s, economic research has played an increasingly important role in the practical

organization and design of markets. The phrase market design includes “the design not only of

marketplaces but also of other economic environments, institutions and allocation rules” (Roth 2015).

Prominent examples of market design include the auctions for spectrum, electricity, and other

commodities; tradable permit systems for pollution abatement and other environmental regulations;

online auctions; online reputation and feedback systems; financial markets; labor market

clearinghouses; formal procedures for student assignment to public schools or colleges; centralized

systems for the allocation of organs; and other related matching and trading processes. In many of

these cases, theoretical, experimental and empirical research have complemented each other and

influenced the design of market institutions.

In the process of bringing a theoretical idea or result to practice, the research strategy is often to

observe the performance of the new market design in the context of the simple situations that can

be created in a laboratory and assess its performance relative to what it was created to do and

relative to the theory upon which its creation rests. For this reason, laboratory experiments are often

a

School of Information, University of Michigan, 105 S. State St., Ann Arbor, MI 48109-1285; Department of

Economics, School of Economics and Management, Tsinghua University, Beijing 100084, China; e-mail:

yanchen@umich.edu

. Chen acknowledges financial support from the National Science Foundation via grant

numbers SES-1620319 and 1838994.

b

Department of Economics: Market Design, University of Cologne, Albertus Magnus Platz, 50923 Köln,

Germany; e-mail: pcra[email protected]

.

c

The Kenneth C. Griffin Department of Economics, The University of Chicago, 1126 E. 59th Street, Chicago,

Illinois 60637; e-mail: jlist@uchicago.edu

.

d

Department of Economics, University of Cologne, Albertus Magnus Platz, 50923 Köln, Germany; e-mail:

ockenfels@uni-koeln.de

.

Cramton and Ockenfels acknowledge funding by the European Research Council (ERC) under the European

Union’s Horizon 2020 research and innovation program under grant agreement No 741409, as well as by the

German Research Foundation (DFG) under Germany´s Excellence Strategy (EXC 2126/1– 390838866).

2

compared to a wind tunnel. For the rest of this section, we will briefly review several important

papers published in Management Science related to market design and human behavior.

At the theoretical level, the most important tool for market design is game theory. In the first 20

years after von Neuman and Morgenstern published their seminal book, Theory of Games and

Economic Behavior, game theory largely remained an academic pastime, primarily because of the

technical difficulties of modeling games of incomplete information that underlies almost all economic

environments of interests (Morris 2019). Between 1967 and 1968, John Harsanyi published three

path-breaking papers in Management Science, where he successfully argued that we can incorporate

any incomplete information without loss of generality as the interim stage of some suitably

constructed model of asymmetric information, and extended Nash’s concept of an equilibrium point

to games of incomplete information (Harsanyi 1967, 1968a, 1968b). One of the many important

results from these papers was the concept of a “type” that summarizes the relevant characteristics

of a particular player. These three papers provided economists with the much-needed tools for

studying asymmetric information problems in strategic interactions (Gul 1997).

The first applied area of economics that embraced game theory was industrial organization,

which generated many interesting insights on bargaining, contract design, pricing and other practical

problems which influenced the theory and practice of management. Game theory has since

contributed considerably to virtually all applied theoretical research in economics and political

science. Harsanyi’s three Management Science papers are broadly considered the precursor to the

game theory takeover of economic theory (Morris 2019). Primarily for his contributions in formalizing

games of incomplete information, John Harsanyi, together with John Nash and Reinhardt Selten,

received The Bank of Sweden Prize in Economic Science in Memory of Alfred Nobel in 1994 (Nobel

Foundation a).

In addition to theoretical foundations for market design, Management Science has also published

a sequence of influential papers on human behavior. Here we highlight two such papers by

researchers pivotal in the creation of the now vibrant field of behavioral economics. The first paper

is due to Kahneman and Lovallo (1993), who study choice under uncertainty by focusing on “isolation

errors,” whereby people tend to treat risky prospects separately rather than together. In their first

“prospect theory” paper, Kahneman and Tversky (1979) raised two central aspects of choice under

uncertainty: the role of loss aversion and the probability weighting function. Isolation errors as the

third component in risky choice is “something whose centrality to understanding risk attitudes

researchers have only begun to fully appreciate” (Rabin 2003). In this paper, Kahneman and Lovallo

not only presented experimental results demonstrating the prevalence of isolation errors, but also

applied it extensively in the context of managerial decision-making to explain, for example, the

pervasiveness of small-scale insurance policies, such as extended warranties on consumer products,

and the equity premium puzzle (Benartzi and Thaler 1995). “For having integrated insights from

psychological research into economic science, especially concerning human judgment and decision-

making under uncertainty,” Daniel Kahneman shared the 2002 Nobel Prize in Economics (Nobel

Foundation b).

3

A second paper highlighted here is by Thaler and Johnson (1990), who investigate how risk-taking

is affected by prior gains and losses. They present experimental data supporting the “house money

effect” whereby decision makers become more risk seeking in the presence of a prior gain, and

“break-even effects” whereby, in the presence of prior losses, outcomes which offer a chance to

break even are especially attractive. Summarizing these empirical regularities, they propose an

editing rule to describe how decision makers frame such problems. For having built “a bridge

between the economic and psychological analyses of individual decision-making” and for his

instrumental role “in creating the new and rapidly expanding field of behavioral economics,” Richard

Thaler received the Nobel Prize in Economics in 2017 (Nobel Foundation c).

Finally, Management Science has published a sequence of papers on market design which

combines theoretical insights with laboratory experiments to shed light on new market designs. Here

we highlight Katok and Roth (2004) who investigate in the laboratory the performance of two auction

formats for selling multiple homogenous objects, the ascending auctions used in eBay and the

descending auctions best known for its use in the flower auctions in the Netherlands. The authors

design three environments that include synergies and potentially subject bidders to the exposure

problem and the free-riding problem. They find that the descending auctions perform well across

environments, while the eBay ascending auction better avoids the free-riding problem. These findings

have significant implications for market design for procurement and privatization. One year later, in

2005, Management Science published a special issue on Electronic Markets (Volume 51, Issue 3),

which includes foundational auction design papers by various economists and computer scientists.

Alvin Roth, together with Lloyd Shapley, received the 2012 Nobel Prize in Economics “for the theory

of stable allocations and the practice of market design” (Nobel Foundation d).

As demonstrated in the above examples, Management Science has published foundational

work in game theory, human behavior and market design. Compared to mechanism design, which

focuses on the use of game theory to understand how to efficiently design institutions, markets, and

contracts respecting individual incentives, market design deals with a similar question but recognizes

that theory can only go so far because many people are not (traditionally) rational or a necessary

assumption of the theory means that critical things are left out. In the auction literature, the Vickrey

-Clarke-Groves mechanism (Vickrey 1961, Clarke 1971, Groves 1973) is the output of the mechanism

design approach whereas ascending package bidding auctions are the output of the market design

approach. Market design at its best takes the insights from game theory, behavioral economics,

experiments and field data to come up with practical institutional designs that have a real chance of

improving existing institutions. Specifically, market design has a few distinguishing features

compared to mechanism design. First, the objective of market design is to find institutions that work

better. Second, market design emphasizes areas of inquiry where theory is relatively silent or

underdeveloped. Lastly, market design should result in new (hopefully applied) mechanisms.

For the rest of the paper, we will survey several market design challenges and solutions, including

strategic timing in auction and financial markets (Section 2), reputation and feedback system design

4

in online markets (Section 3), matching market design in education (Section 4), and the design of

labor markets (Section 5). Finally, Section 6 concludes.

2 Strategic timing in markets

While economic theory simplifies auctions and often does not worry about strategic timing in

markets, it is an important concern in market design

. In matching markets, Roth and his coauthors

analyze and develop mechanisms that address problems arising from incentives to act earlier than

others (Roth 1990, 1991, Mongell and Roth 1991, Roth and Xing 1994, Roth and Peranson 1999, Kagel

and Roth 2000, Chen and Sönmez 2006, Roth 2008 provides a survey). Competition for people and

positions in various job markets led to earlier and earlier dates of appointment, to the point that

students were being hired before useful information about their performance was available, and

before the students themselves could develop informed career preferences. Roth designed and

helped implement successful centralized matching algorithms to stabilize such markets (Roth 2002,

and Roth and Wilson 2019 provide an account of the history of market design and of recent

developments).

Yet, timing is also an important aspect of strategic behavior in auction markets. As we show in

this section, a strategy called “sniping” (bidding as early or as late as possible to gain an advantage)

is prevalent in many auction market environments, hampering the efficiency of trade. Sniping has

probably been first observed in candle auctions, which were used starting about 1490 (Cassady 1967).

In modern markets, market design solutions that can help mitigate sniping are often available. First,

we show that sniping is widespread on consumer-to-consumer (C2C) online markets like eBay yet can

be largely mitigated by changing the rule by which the auctions end. We then sketch how sniping

arises in spectrum auctions and can be addressed by activity rules designed to promote better price

discovery. Finally, we describe the race for speed in financial markets, why it arises, and how it can

make traders worse off and create inefficiencies and market instabilities. Here, too, innovative

market design solutions are available.

2.1 Online auctions

Many auctions, including online auctions for consumer goods, are often run in continuous time.

1

The

simplest rule for ending such auctions is a fixed end time (a “hard close”), as employed by eBay. A

striking property of bidding on eBay is that a substantial fraction of bidders submits their bids in the

closing seconds of an auction, which is called “sniping”, just before the hard close. Bidding is different

on other platforms such as those formerly run by Amazon, which operated under otherwise similar

rules. Amazon auctions were automatically extended if necessary past the scheduled end time until 10

minutes passed without a bid (a “soft close”).

1

This section is an adjusted and updated, and much shortened, version of Ockenfels and Roth’s (2013) account

of the literature on sniping in auctions for consumer goods. To simplify our exposition, we will use the present

tense when we talk about Amazon auctions in this section, although Amazon shut down its auction platform

many years ago.

5

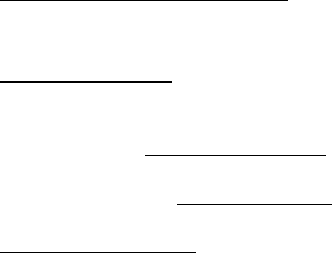

Based on a study by Roth and Ockenfels (2002), Figure 1 shows the empirical cumulative probability

distributions of the timing of the last bid in each auction for a sample of 480 eBay and Amazon auctions

of antiques and computers with a total of 2,279 bidders. The timing of bids in Amazon is defined with

respect to the initially scheduled deadline, which differs from the actual closing time if a bid comes in

later than ten minutes before the initial end time (only very few bids came in after the initially

scheduled deadline, so we drop those observations for simplicity).

Figure 1. Cumulative distributions over time of eBay auctions’ last bids

(reproduced from Roth and Ockenfels 2002)

Figure 1 shows that there is significantly more late bidding on eBay than on Amazon. For instance,

40 percent of eBay-Computers auctions and 59 percent of eBay-Antiques auctions in the sample have

last bids in the last 5 minutes, compared to about 3 percent of both Amazon computer and Amazon

antiques auctions that have last bids in the last five minutes before the initially scheduled deadline

or later. The pattern repeats in the last minute and even in the last ten seconds. This suggests that

changes in the ending rules of auctions can strongly affect bidding behavior. While the Roth and

Ockenfels (2002) study was one of the earliest on eBay, and the data were collected by hand, more

recent studies of eBay referenced below use millions of auctions as data and mostly confirm the

results.

Sniping on eBay is not easily explained by simple textbook auction analyses. The reason is that

there is no time dimension in sealed-bid auctions, and dynamic auctions are typically modeled as

clock auctions, where “price clocks” – instead of the bidding itself – determine the pace of the

bidding. Moreover, eBay asks the bidders to submit maximum bids (called “proxy bids”). Because

eBay’s bidding agent will bid up to the maximum bid only when some other bidder has bid as high or

higher, if the bidder has submitted the highest proxy bid, he wins at the “lowest possible price” of

one increment above the next highest bid. Thus, similar to the second-price sealed-bid auction, at

the end of the auction a proxy bid wins only if it is the highest proxy bid, and the final price is the

minimum increment above the second highest submitted proxy bid, regardless of the timing of the

bid. This suggests that there is no reason to bid late. Yet, proxy bidding does not necessarily remove

the incentives for sniping on eBay. Sniping can avoid bidding wars with incremental bidders, with like-

minded late bidders, and with uninformed bidders who look to others’ bids to determine the value

of an item (see the series of papers by Roth and Ockenfels (2002), Ockenfels and Roth (2006, 2013),

30%

40%

50%

60%

70%

80%

90%

100%

60 55 50 45 40 35 30 25 20 15 10 5 0

minutes before auction ends

% of submitted last bids

eBay-Computers eBay-Antiques

Amazon-Computers Amazon-Antiques

6

that offers game theoretic analyses for late and incremental bidding strategies, field evidence for

strategic late bidding).

For example, sniping can be the best response to the late bidding strategies of like-minded

bidders. In 2000, Hal Varian explained the underlying idea in a New York Times column titled “Online

Users as Laboratory Rats” as follows: Suppose you are willing to pay up to $10 for a pez dispenser,

and there is only one other potential bidder who you believe also has a willingness to pay of about

$10. If both of you submit your value early, you will end up with a second highest submitted proxy

bid of about $10 implying a price of about $10. Thus, regardless of whether you win or not, your

earnings would be close to zero. Now consider a strategy that calls for a bidder to bid $10 at the very

last minute and not to bid earlier, unless the other bidder bids earlier. If the other bidder bids earlier,

the strategy calls for a bidder to respond by promptly bidding his true value. If both bidders follow

this strategy and mutually delay their bids until the last minute, both bidders have positive expected

profits, because there is a positive probability that one of the last-minute bids will not be successfully

transmitted (Roth and Ockenfels 2002); in which case the winner only has to pay the (small) minimum

bid. However, if a bidder deviates from this strategy and bids early, his expected earnings are

(approximately) zero because of the early price war triggered by the early bid. Thus, with sniping,

expected bidder profits will be higher and seller revenue lower than when everyone bids true values

early. That is, sniping can be an equilibrium strategy even with private values and even if there is a

risk that the snipe does not make it to eBay in time, before the auction closes.

When values are interdependent, there are additional strategic reasons to bid late in auctions,

because the bids of others can then carry valuable information about the item’s value that can

provoke a bidder to increase his willingness to pay. This creates incentives to bid late, because by

bidding late, less informed bidders can incorporate into their bids the information they have gathered

from the earlier bids of others, and experts can avoid giving information to others through their own

early bids (Bajari and Hortaçsu 2004, Ockenfels and Roth 2006, Hossain 2008).

Finally, last minute bidding can also be a best reply to incremental bidding. To see why, suppose

you believe that your competitor starts with a bid well below his maximum willingness to pay and is

then prepared to raise his proxy bid whenever he is outbid, as long as the price is below his willingness

to pay. Last-minute bids can be a best response to this kind of incremental bidding because bidding

near the deadline of the auction would not give the incremental bidder enough time to respond to

being outbid. By bidding at the last moment, you might win the auction at the incremental bidder’s

initial, low bid, even when the incremental bidder’s willingness to pay exceeds your willingness to

pay. Non-strategic reasons for incremental bidding include that bidders may not be aware of eBay’s

proxy system and thus behave as if they bid in an ascending (English) auction, ‘endowment effect’

(Roth and Ockenfels 2002, Wolf et al. 2005 and Cotton 2009), ‘auction fever’ (Heyman et al. 2004),

escalation of commitment and competitive arousal (Ku et al. 2005), uncertainty over one’s own

private valuation (Rasmusen 2006), or an unwillingness to reveal one’s valuation (Rothkopf et al.

1990). Strategic reasons include shill bidding by confederates of the seller to push up the price beyond

7

the second-highest maximum bid (Engelberg and Williams 2009), and a strategic response to the

multiplicity of listings of similar objects (Anwar et al. 2006, Peters and Severinov 2006).

Amazon auctions are automatically extended if necessary past the scheduled end time until ten

minutes have passed without a bid. Although the risks of last-minute bidding remain, the strategic

advantages of last-minute bidding are eliminated or severely attenuated in Amazon-style auctions,

because no matter how late a bid was placed, other bidders will have time to respond. Thus, on

Amazon, an attentive incremental bidder, for example, can respond whenever a bid is placed. As a

result, the advantage that sniping confers in an auction with a fixed deadline is eliminated or greatly

attenuated in an Amazon-style auction with an automatic extension (Ockenfels and Roth 2006,

Malaga et al. 2010). Indeed, Figure 1 suggests that late bidding arises in large part from the rational

response of the bidders to the strategic environment. Moreover, more experienced bidders on eBay

bid later than less experienced bidders, while experience in Amazon has the opposite effect (Ariely

et al. 2005, Ockenfels and Roth 2006, Wilcox 2000). In addition, since significantly more late bidding

is found in antiques auctions than in computer auctions on eBay, but not on Amazon, behavior

responds to the strategic incentives created by the possession of information, in a way that interacts

with the rules of the auction.

Laboratory experiments conducted by Ariely et al. (2005) replicate the major field findings in a

controlled laboratory private-value setting in which the only difference between auctions is the

ending rule. Moreover, the laboratory Amazon condition turns out to be more efficient and to yield

higher revenues than the other conditions; the field evidence on efficiency and revenues from various

auction platforms is, however, somewhat more mixed (Glover and Raviv 2012, Gray and Reiley 2013,

Cao et al. 2019, Brown and Morgan 2009, Houser and Wooders 2005, Elfenbein and McManus 2010

and Carpenter et al. 2011). Backus et al. (2015) find another harmful impact of sniping based on eBay

field data: being sniped discourages new bidders from returning to bid again – they are between 4

and 18 percent less likely to return to the platform.

The next subsections describe two other important examples for sniping in markets, examples in

which traders are – unlike on eBay – most sophisticated and in which very different solutions to

address sniping have been devised.

2.2 Spectrum auctions

Spectrum auctions have been used by governments to assign and price spectrum for 25 years.

2

The

development and implementation of innovative spectrum auction formats is among the greatest

successes of market design. Over the years, many design issues have surfaced. Like on eBay (which

was founded in 1995, around the same time when spectrum auctions started to become popular),

2

This section is mostly based on Cramton (2013). Because of space restrictions, we cannot discuss issues

related to package bidding here, although they are an important part of the auction design literature (Cramton

et al. 2006, Milgrom 2017) – with important papers published in Management Science, such as Pekec and

Rothkopf (2003), Kwasnica et al. (2005), Goetzendorff et al. (2015). In this context, some early papers also

addressed strategic timing, such as Rassenti et al. (1982) and Banks et al. (1989).

8

one important challenge is to address incentives bidders may have to withhold expressing true

demands until late in the auction, and thereby undermine price discovery.

The workhorse for spectrum auctions since 1994 has been the simultaneous ascending auction,

which is a simple generalization of the English auction to multiple items in which all items are

auctioned simultaneously. Thus, unlike Sotheby’s or Christie’s auctions in which the items are

auctioned in sequence, here all the items are auctioned at the same time: Each item has a price that

is associated with it. Over a sequence of rounds, bidders are asked to raise the bid on any items that

they find attractive, and the auctioneer identifies the provisional winner for each item at the end of

every round. The process continues until nobody is willing to bid any higher – which is related to

Amazon’s soft close auction.

3

This process was originally proposed by Preston McAfee, Paul Milgrom,

and Robert Wilson for the FCC spectrum auctions.

Although these auctions end with a soft close, bidders may want to hold back, not pushing up

prices on those objects they value most and concealing their private information until the end of an

auction. One motivation for this strategy stems from an aggregate budget constraint. It may be easier

to push a competitor aside late in the auction when the competitor has already committed its budget

in other markets. A second motivation is a desire to better understand prices before committing to a

specific portfolio of spectrum assets.

Sniping, however, slows the auction down and prevents price discovery.

4

Yet good price discovery

is essential in realizing the benefits of complex, dynamic auctions. One reason is that there is much

uncertainty about what the objects being sold are worth. The bidders typically can only develop a

crude valuation model. They need the benefit of some collective market insights, which can be

revealed in a dynamic auction process to improve their bidding. If the price discovery process works

well, the bidders gradually have their sights focused on the most relevant part of the price space.

Focusing bidder decisions on what is relevant is probably the biggest source of benefit from the

dynamic process (although this benefit is often ignored by economists, because economists typically

assume that bidders fully understand their valuation models, when in practice bidders almost never

have a completely specified valuation model). For such reasons price discovery is a public good and

thus sniping – free-riding on others’ efforts to find market prices – is a reasonable strategy if not

prevented by auction design.

The standard solution in spectrum auction design is an “activity rule”. The activity rule requires a

bidder to be active (that is to be the current high bidder or to submit new bids) on a predetermined

quantity of spectrum licenses. If a bidder falls short of the required activity level, the quantity of

3

Klemperer (1998, 2002) proposes an ending rule for spectrum auctions that is somewhat closer to eBay’s hard

close, namely a hybrid of the ascending, soft-close auction format and the sealed-bid format, which he calls

“Anglo-Dutch”. The idea is that the early bidding is like in the simultaneous ascending auction, but bidders can

make final sealed-bids at the end of the auction. Klemperer argues that this kind of hard-close can discourage

collusion in the dynamic phase of the auction, because the last-minute round allows bidders to renege on any

deals without fear of retaliation, and because the final bids induce some uncertainty about the winner, this can

also attract entrants. Such concerns are not relevant for the choice of eBay’s hard-close ending rule in their

single-object auctions, though.

4

Studies on eBay reveal that bidders do not bid truthfully early in the auction, but that much of the price

discovery is done only in the closing seconds of the auction (e.g., Ariely et al. 2005).

9

licenses it is eligible to buy shrinks. Thus, bidders are prevented from holding back. The activity rule

avoids late bidding and controls the pace of auctions by creating pressure on bidders to bid actively

from the start. Milgrom and Wilson

designed an activity rule that was applied to the U.S. spectrum

auctions (McAfee and McMillan 1996, Milgrom 2004). Nearly all high-stake auctions, such as the FCC

spectrum auctions, have an activity rule.

The exact design of the activity rule depends on the auction environment. More complex auctions

require more complex activity rules. Too strong activity rules might force bidders to bid for less than

their true demands, and too weak activity rules will inevitably lead to late bidding. For a single-object

spectrum auction, a reasonable activity rule would require that no bidder can re-enter after exiting

the auction. In an eBay-like auction, for instance, the activity rule would imply that all bidders, right

at the start, submit their maximum willingness to pay as a proxy bid. No bidder could enter the

auction once it started or re-enter once the bidder exited. (This, of course, would be incompatible

with the flexibility needed on C2C auction platforms, but it is compatible with spectrum auctions

where there are discrete rounds that follow a daily schedule.) For a multi-unit auction of a single

product, the activity rule would require that one cannot increase demand as price increases. For

many related products, an aggregate quantity rule is needed, which requires that bidders are active

on a particular fraction of current “eligibility” or the eligibility is reduced.

5

In more complex auctions,

such as combinatorial clock auctions, state-of-the-art revealed preference rules can make sure that,

as prices increase, bidders can only shift toward packages that become relatively cheaper (Ausubel

et al. 2006, Ausubel and Baranov 2019).

What happens without an activity rule can be observed in spectrum auctions such as the Italy 4G

auction, which did not have an activity rule. As a result, bidders held back demand, slowing the

auction and limiting price discovery. Eventually, the auction lasted 470 rounds. That said, Germany’s

recent 5G auction, in 2019, lasted 497 rounds and thus set a new world record with respect to number

of rounds in a simultaneous ascending auction. Here, the flaw was not the activity rule, but the fact

that it would take many rounds to get a one increment increase in price, because Germany used the

traditional simultaneous ascending auction with bidding on individual lots, rather than a modern

clock auction, which has prices increase by a bid increment in each round for any product with excess

demand (see Cramton and Ockenfels 2017 for an analysis of the German spectrum auction design).

Measures to address sniping cannot be analyzed in isolation but must be closely connected to other

details of the rules, such as pricing rules and increment rules to be fully effective.

2.3 Financial markets

Markets for financial securities are another important example where market design has a profound

impact on the incentives for sniping and speed in markets. Unlike in spectrum auctions, the problem

5

Here, each lot corresponds to a specific quantity of spectrum, measured in either MHzPop or in “eligibility

points”. The bidder starts with an initial eligibility based on the bidder’s initial deposit. To maintain this level of

eligibility in future rounds, the bidder needs to bid on a sufficiently large quantity of spectrum in the current

round, where “sufficiently large” is stated as some percentage, typically between 80% and 100% of the bidder’s

current eligibility. If the bidder bids on a smaller quantity, the bidder’s eligibility is reduced in future rounds.

10

is not that bids tend to be held back, but rather a never-ending arms race for ever faster trading.

Because trading is continuous and equally attractive orders are processed in the order they arrive,

speed is crucial in this format. This limits the performance of these markets (e.g., Budish et al. 2019).

As before, the problem can be viewed with the lens of market design. This reveals a solution as

presented in Budish et al. (2015), which we describe below.

The root of the problem is a fundamental flaw in today’s markets: continuous-time trading.

Continuous-time trading means that it is possible to buy or sell securities at any instant, where instant

is measured in billionths of seconds – the speed of today’s computers. Thus, the solution is for trading

to occur in discrete time. Instead of trading at any instant, trading occurs, say, once per second.

Orders arriving in the same second are batched together without any priority for orders that arrive a

bit earlier, and all trades occur at the same price where supply and demand cross. The key is that the

trading interval should be short as perceived by humans, but long for a computer.

But what exactly is wrong with continuous trading? Is trading as fast as possible not just good for

price discovery and healthy competition, as probably suggested by our discussion of the need for

activity rules in spectrum auctions? The answer boils down to a combination of two market failures.

The first market failure is that in times of algorithmic trading, continuous markets do not and cannot,

work as they should in continuous time. Equivalent securities with prices that move in lockstep at

human time intervals have moments of significant divergence at high frequencies. This creates what

economists call technical arbitrage opportunities: the kinds of opportunities that are not supposed

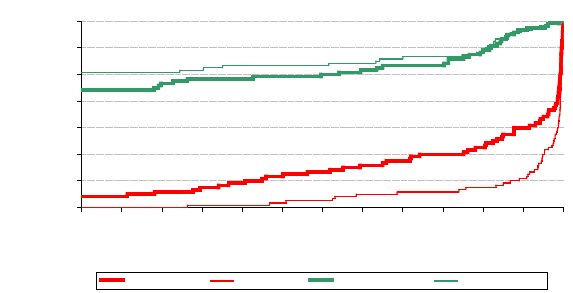

to exist if the market is working properly. For example, the price of the S&P 500 futures contract in

Chicago (ES) and the S&P 500 EFT in New York (SPY) should move in perfect lockstep, and to the

human eye they do (Figure 2 left panel). But, when we zoom in to high frequency, there are hundreds

of opportunities a day to make nearly riskless money – buy low in New York and sell high in Chicago,

or vice versa (Figure 2 right panel). This adds up to about $75 million a year for high frequency traders

– and this is just one pair of securities. There are hundreds of other pairs just like it, and, in our

fragmented US equities markets, trades that are even simpler: if a stock jumps up on NASDAQ, buy

it low on NYSE.

11

Figure 2. S&P 500 index in Chicago (ES) and New York (SPY) minute-by-minute (left panel) and

millisecond-by-millisecond (right panel). The securities move in lockstep on human time scale but

are uncorrelated on a millisecond time scale. (Reproduced from Budish et al. 2015)

The second market failure is that these technical arbitrage opportunities – which are a prize to

whichever trader snaps them up the fastest – create a never-ending arms race for speed. This fight

for the prize is why there are investments like the $300 million high-speed cable between New York

and Chicago – and why that cable is already obsolete. This is why there are armies of physics and

computer science PhDs devoted to shaving millionths or billionths of seconds off trading times. This

is also why there are exchanges renting colocation services and high-speed data feeds – that is their

way of getting a piece of the prize. Here is a simple way to think about it: continuous-time trading

creates a $10 billion prize, and then high-frequency traders, exchanges, and broker-dealers all

scramble to get their piece.

Ultimately the prize comes out of the pockets of investors. The reason is that the technical

arbitrage opportunities harm liquidity – it is harder to provide quotes to investors if one is constantly

worried that prices will change and one’s stale quotes will get picked off before one can revise them.

So, markets are less liquid than they should be. And for institutional investors this means trading large

blocks of stock is costlier.

Discrete time directly addresses both market failures. With discrete time, one cannot make

money from exploiting pricing discrepancies that many traders see at the same time – just by acting

a billionth of a second faster. This stops the arms race for speed. Unhealthy competition for speed is

transformed into productive price competition. Trades occur at the right price – the consensus of the

market – rather than at stale quotes. High-frequency traders still will be able to make money, but

only if they take actual risk, provide liquidity, or are smarter than the rest of the market – know

something that the rest of the market does not. One no longer can make money just from being the

fastest to respond to some commonly observed event.

Discrete time also makes computational sense. Continuous trading implicitly assumes that

computers and communications are infinitely fast. Computers and communications are fast but not

infinitely so. Discrete time respects these limits. Tiny speed discrepancies between the direct feeds

and public feeds of exchange data are critical with continuous time. This issue goes away with discrete

time.

Continuous time breeds constant change and heightened complexity, making markets vulnerable

to instability. Discrete time simplifies markets and allows both traders and exchanges to focus on

improvements that make trading smarter and safer.

Which market design works in the financial sector to address sniping is the topic of many current

discussions. Discrete time has seen limited implementation and alternative design solutions have

been proposed. For example, in 2016, the U.S. Securities and Exchange Commission approved the

Investors Exchange (IEX) to operate as a public securities exchange. A primary goal of the IEX market,

which was founded in 2012 to provide an alternative trading system with delayed messaging (Aldrich

12

and Friedman 2018) is to reduce potential advantages of high-frequency trading firms. Another

alternative is randomization of order priority as employed by Electronic Broking Services (EBS), the

largest currency exchange in the world. Asymmetric speed bumps – delaying sniping orders but not

order cancelations – are now common. Other innovative methods such as flow trading are also being

studied (Kyle and Lee 2017, Budish et al. 2020).

2.4 Future directions: Economic and algorithmic design, and the pace of price discovery

There are many opportunities and important challenges in auction and market design (for surveys

see Bichler and Goeree 2017, Cramton et al. 2006, Milgrom 2004, 2019, Klemperer 2004, Greiner et

al. 2012). Many of those opportunities and challenges follow from the fact that most digital platforms

allow market engineers much control over the design, implementation, and operation of markets

regarding pricing, demand and supply expression, information feedback, timing of transaction, and

many other market features. Moreover, economic and algorithmic design is increasingly asked to

address social concerns that go beyond economic efficiency, such as privacy and fairness. Exciting

work at the interface of economics and computer science attests to these developments (examples

include Bichler et al. 2010, Kearns and Roth 2019, Milgrom 2017, Parkes and Seuken 2020; see also

the next sections). As a result, market and algorithmic design is shaping virtually all facets of economic

and social interaction in many areas: online marketplaces, financial exchanges, the sharing economy

and platforms of social exchange.

In this section we show that controlling the pace of price discovery is one of the pressing topics

in this new era of market design. Interestingly, this was not anticipated by auction theory, but rather

inspired by practical challenges, low market performance and failed design attempts. Analyses of

spectrum, online and financial markets demonstrate that sniping can often be explained by

equilibrium predictions. Much of the late bidding in C2C online auctions such as eBay, on the other

hand, is often best explained by a strategic response to naïve, incremental bidding, yet it can also

arise at equilibrium in both private- and common-value auctions.

6

Indeed, the effect of the fixed

deadline is likely as large as it is because it rewards late bidding both when other bidders are

sophisticated and when they are not. Market design must sometimes consider not only the

equilibrium behavior that we might expect experienced and sophisticated players eventually to

exhibit, but also how the design affects behavior of inexperienced participants, as well as the

interaction between sophisticated and unsophisticated human players and algorithmic bidding-

agents.

Yet, unlike in spectrum and online auctions, which have experimented with various auction

architectures both in the laboratory and the field,

7

there is not much conclusive and clean causal

6

Ely and Hossain (2009) suggest from their field experiment that the availability of closely substitutable

auctions on eBay may reduce the overall benefit of sniping.

7

Another auction context where much has been learned from laboratory human-subject research is the

practical design of procurement auctions, with much research published in Management Science (Chaturvedi et

al. 2014, Fugger et al. 2015, Davis et al. 2011, 2014, Engelbrecht-Wiggans and Katok 2008, and Katok and Roth

2004).

13

empirical evidence yet that reveals the relative performance of financial market institutions and that

can guide market design for financial securities – despite the fact that policy makers worldwide are

already taking actions intended to discourage high frequency trading. Zhang and Riordan (2011),

Brogaard et al. (2014), Menkveld and Zoican (2014), Benos and Sagade (2016), and Benos et al.

(2017), among others, provide evidence for the costs of aggressive sniping. However, this literature

comes from minor variants of the standard financial market design, and thus offers no direct evidence

about the costs and benefits of other platforms, engineered to eliminate the dilemma, as in Budish

et al. (2015) and Aquilina et al. (2020). Moreover, even though there are three decades of studying

financial markets in the laboratory (for surveys on experimental research in financial markets see

Friedman and Rust 1993, Friedman 2010, and Noussair and Tucker 2013), aside from particular

episodes such as the “Flash Crash” (Aldrich et al. 2016), little is known about the impact of sniping in

times of financial stress as opposed to normal times (but see Jagannathan 2019 for a step in this

direction). However, Aldrich and López Vargas (2019) recently conducted a laboratory market design

study on high-frequency trading that suggests that, relative to the continuous double auction, the

frequent batch auction exhibits less predatory trading behavior, lower investments in low-latency

communication technology, lower transaction costs, and lower volatility in market spreads and

liquidity. More studies on how financial market design affects sniping, market stability and market

resiliency are necessary.

Also, many other markets, as they move to real-time interaction, already see or will likely see

similar problems, and thus require new clever market design solutions. As an example, think about

electricity market design, where we are just starting to observe similar issues. One of the reasons is

the increasing share of intermittent renewables, which puts enormous stress on the system and

increases the risk of outages, so that both, improved investment incentives for reserve generation

capacity (Cramton and Ockenfels 2012, Cramton et al. 2013) and more liquid real-time trading is

needed. Yet, because the trend towards algorithmic trading in continuous electricity markets will also

lead to a wasteful race for speed, this is posing serious threats to the efficiency and reliability of these

markets (Neuhoff et al. 2016). Moreover, compared to financial markets, things tend to be more

complicated in electricity markets because of complementarities in electricity production (Wilson

2002 and Cramton 2017). For instance, the race for speed in electricity trading hampers efficient

pricing of transmission, which is often done on a first-come-first-serve basis in intraday trading. Also,

a race for speed complicates the formulation and consideration of multi-dimensional bids, which

consider the non-convex cost structure of electricity production.

Another interesting example for the relevance of timing in markets is auction design for

continuous sponsored search in the Internet, where other undesired bidding timing phenomenon

have been observed, such as bidding cycles with automated bidding agents, as well as various

attempts to address those (Edelman and Ostrovsky 2007, Edelman et al. 2007, Varian 2007, 2009,

Athey and Ellison 2011, Levin 2013 provides a survey). Clearly, taming sniping and improving price

formation will remain a critical aspect of market performance in modern market environments.

14

Technology gives market designers an unprecedented ability to design and operate markets to

better achieve objectives. One might expect rapid marketplace innovation as a result. Yet progress is

often slowed from the inertia of the status quo. Research is needed that improves our understanding

of why innovation is difficult and how barriers of innovation may be overcome (see Budish et al. 2019

for a study of these challenges in financial markets). Too often market inefficiencies stem not from a

lack of knowledge on how to fix the problem but from barriers to adopting the needed innovation.

3 Reputation and feedback system design in online markets

The astonishing success of online market platforms such as eBay, Amazon, Uber, and Airbnb can be

attributed to the ease in which one side of the market can find a match on the other market side, as

well as to the fact that they provide reliable information about the trustworthiness of the trading

partner. All markets require some minimum amount of trust, yet this is a particular challenge for

online markets and sharing platforms, where trades are typically with strangers, geographically

dispersed, and executed sequentially. To incentivize trustworthiness, most online platforms employ

a reputation-based ‘feedback system’, enabling traders to publicly post information about past

transaction partners. These systems have been, and are being, engineered based on conceptual

insights from game theory and behavioral sciences, and with the help of laboratory and field studies

(surveys include Dellarocas 2003, Bar-Isaac and Tadelis 2008, Greiner and Ockenfels 2009, Ockenfels

and Resnick 2012, Bolton and Ockenfels 2012, Tadelis 2016, Gutt et al. 2019).

3.1 A case study in engineering trust

One major challenge of all feedback-based reputation systems is to get people to cooperate with the

platform and leave feedback about their transaction partner. Feedback information is largely a public

good, helping other traders to manage the risks involved in trusting an unknown transaction partner,

so economists would tend to predict low participation rates. Yet, in the field data by Bolton, Greiner

and Ockenfels (2013), about 70% of the eBay traders, sellers and buyers alike, leave feedback (a

number consistent with other research). It turns out that the key driver of provision of feedback, as

well as the source of various distortions in feedback information identified in the literature, is

reciprocity. More specifically, much of the feedback patterns we see can be organized by connecting

them to two of the most fundamental research findings on the patterns of human cooperation in the

last decades: altruistic punishment promotes cooperation, and counter-punishment hampers

cooperation (Ostrom et al. 1992, Fehr and Gächter 2000a, 2002, Nikiforakis 2008, Mussweiler and

Ockenfels 2013, Balafoutas et al. 2014). A natural way to (altruistically) punish a trader on an Internet

platform who is not behaving according to what is perceived to be the social or trading norm, is to

leave negative feedback. This way, a propensity to altruistically punish norm-violators creates an

incentive to be trustworthy. However, punishments can often be counter-punished, which is known

to reduce the effectiveness of punishment to promote cooperation. Indeed, by retaliating a negative

feedback with a negative one, counter-punishment may spoil the reputation of the altruistic

punisher, which in turn may deter altruistic punishment in the first place. As a result, the potential of

15

counter-punishment can hamper the effectiveness of reputation mechanisms and thus the

performance of markets.

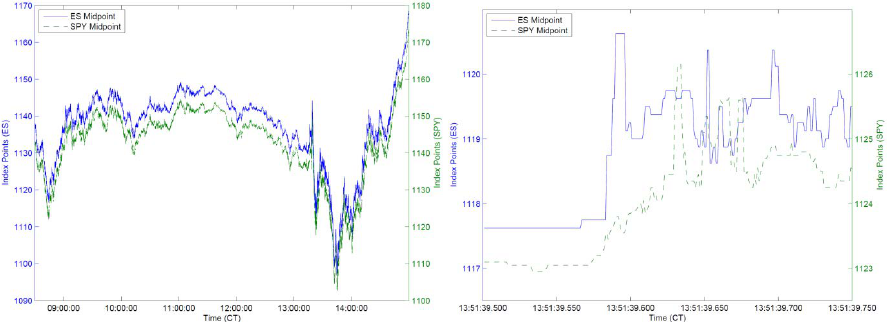

To illustrate the close analogy between (counter-) punishment in the behavioral science literature

and giving feedback in the Internet, look at the figure below, which is taken from Bolton et al. (2013).

It shows the timing of feedback given on eBay by the buyer and the seller in hundreds of thousands

of transactions. Most transactions either end with mutually positive (green dots), or with mutually

negative feedback (red dots). Transactions with mutually positive feedback are all over the place

(although a closer look at the data in Bolton et al. reveals that there is lots of reciprocity: many traders

give ‘kind’ feedback in reciprocal response to ‘kind’ feedback). Transactions with mutual negative

feedback, on the other hand, are highly clustered just below the diagonal. This means that many

sellers, who are punished with a negative feedback from their buyers, respond immediately by

counter-punishing with a negative feedback. Clearly, feedback giving is not independent. The

tightness and sequence in timing rather strongly suggest that sellers reciprocate positive feedback

and ‘retaliate’ negative feedback. Seller retaliation also explains why more than 70% of cases in which

the buyer gives problematic feedback and the seller gives positive feedback (blue dots in Figure 2),

involve the buyer giving second – the buyer going first would involve a high risk of retaliation.

Observations in which only the seller gives problematic feedback (yellow dots) are rare and have their

mass below the 45-degree line.

Figure 3. Reciprocity in feedback giving (reproduced from Bolton et al. 2013)

There are benefits and costs of reciprocity in feedback giving. A benefit of reciprocal positive

feedback, for both the individual traders involved and the larger system, is that it helps getting

mutually beneficial trades recorded. But in the form of seller retaliation, reciprocal feedback imposes

costs both on the buyers retaliated against and potentially on the larger system (because traders

16

might not be willing to leave negative feedback out of fear that it will be retaliated). This would bias

feedback information to be overly positive and therefore less informative in identifying problem

sellers. Indeed, on eBay, almost all feedback is positive. Using internal eBay data, Nosko and Tadelis

(2015) find that traders’ positive feedback percentage is 99.3% with a median of 100%. The concern

is also supported by Dellarocas and Wood (2008) who examine the information hidden in the cases

where feedback is not given. They estimate, under some auxiliary assumptions, that buyers are at

least mildly dissatisfied in about 21% of all eBay transactions, far higher than the levels suggested by

the reported feedback. They argue that many buyers do not submit feedback at all because of the

potential risk of retaliation. Controlled laboratory evidence in Bolton et al. (2013) supports the notion

that counter-punishment in feedback giving reduces the effectiveness of reputation building and

market performance.

Yet, online reputation systems can be designed to address flaws in the system. Bolton et al. (2013)

demonstrate that reciprocity can be guided by changing the way feedback information flows through

the market system, leading to more accurate reputation information, more trust and more efficient

trade. Specifically, their data show that, compared to the simple two-sided feedback system

traditionally implemented by eBay, where buyers leave feedback on sellers and vice versa, both blind

and one-sided feedback significantly reduce the scope for retaliation, which in turn increase the

informativeness of the feedback presented to buyers. The result is in line with game theory,

behavioral science, laboratory and field research on social behavior and reputation building (such as

the line of research by Bolton et al. 2004, 2005, Bolton and Ockenfels 2009, 2014), and with field data

collected across various market platforms. Indeed, the idea of making altruistic punishment easy but

counter-punishment difficult explains important features of today’s running reputational feedback

systems. For instance, eBay supplemented their old two-sided feedback system with a one-sided

system (called “detailed seller rating”). Based on research by Bolton et al. (2013), the one-sidedness

was designed so that feedback cannot be retaliated by sellers. Airbnb, also inspired by the line of

behavioral research described above and their own experimental findings, created a blind feedback

system, where transaction partners cannot see the others’ feedback until they left their own. This,

too, makes it impossible to retaliate negative feedback (although a recent study finds the effect to

be small on Airbnb; Fradkin et al. 2019). Uber, on the other hand, makes it hard for passengers to

identify a specific feedback giver, which is another way of making it difficult to retaliate negative

feedback. Finally, eBay changed its systems again in 2008 so that sellers can only leave positive

feedback, which was meant to eliminate the scope for counter-punishment.

3.2 Future directions: Incentivizing, filtering and de-biasing human judgment

There are still important gaps in our knowledge, and much more experimenting is needed to further

improve trustworthiness and cooperation in online markets. For instance, because eBay’s 2008

feedback system removes counter-punishment by sellers, buyers welcomed the new design (Klein et

al. 2016). But there are several indications that many sellers are unhappy with the new system. The

reason is that by removing the option to counter-punish, the new system also removes the option to

17

punish buyers, and thus mitigates buyers’ incentives to cooperate. To the extent that there is scope

for moral hazard on the buyer side, this creates an imbalance of punishment (and thus bargaining)

power between buyers and sellers. Thus, the overall effect of removing the sellers’ punishment

option on cooperation and market performance is probably more ambiguous than the Klein et al.

study (2016) suggests. From a broader perspective, the question how the rules affecting the scope

for punishment and counter-punishment in interactions with two-sided moral hazard should be

shaped largely remains an open one.

More recent attempts to incentivize, filter, and de-bias human judgment involve financial

compensation for feedback information (see Li 2010, Li and Xiao 2014, and Li et al. 2016 for case

studies on Alibaba, Cabral and Li 2015 for field experiments on eBay, and Burtch et al. 2018), plans

to rely more on big behavioral data and artificial intelligence to better predict future behavior

(Milgrom and Tadelis 2018, Masterov et al. 2015, Luca and Zervas 2016), and on blockchain

technology to better verify and audit transaction attributes (Catalini and Gans 2019).

Another pressing question in reputation design is whether and how traders can modify already

submitted feedback information. One example is whether traders should be allowed to remove an

initially given negative feedback if the dispute could later be resolved. Many platforms, including

eBay.com, etsy.com, discogs.com, ricardo.ch, tradingpost.com.au, trademe.co.nz,

mercadolibre.com, and listia.com, have or had a system that withdraws negative feedback from both

traders’ reputation profiles – if and only if both traders agree. Among other things, this option is

thought to incentivize conflict resolution. However, Bolton et al. (2018) have shown both,

theoretically and empirically, that this system is flawed in that it creates incentives to distrust,

escalating conflict instead of resolving it. The reason is that the system allows traders to use counter-

punishment to protect untrustworthy behavior: If I counter-punish a negative feedback that I

received, my opponent will more likely agree to remove that negative feedback (because otherwise

his reputation will be spoiled, too). However, there is a lack of research that can guide the design of

rules to integrate effective dispute resolution and informative reputation building systems (but see

Ockenfels and Resnick 2012 and Bolton et al. 2019).

There is also a lack of knowledge regarding feedback giving, content and usage in credence good

markets, such as markets for medical, financial or technical repair services. One major difference to

the kind of online markets we have discussed so far is that consumers are often persistently unable

to identify the quality of service that fits their needs best. This poses new challenges to designing

effective and behaviorally robust mechanisms that promote trust and trustworthiness in these

markets (Balafoutas et al. 2013, 2017, Dulleck et al. 2011, Kerschbamer et al. 2016, 2019).

We finally emphasize that research on “engineering trust” in online markets has been inspired by

practical design problems. Indeed, standard reputation theory did hardly anticipate the kinds of

problems that online markets face when implementing reputation systems. Theory often assumes

that reputation information is perfectly accurate and complete. Under these conditions, we can

expect to see perfect reputation building, and perfect trust, among market actors (Wilson 1985,

Bolton et al. 2011), and there is no scope for an engineering literature that guides attempts to

18

effectively promote the provision of informative feedback in practice. On the other hand, behavioral

research and experimental studies turned out to be useful in organizing the relevant patterns

observed in the field. A desirable next step is to learn from such observations and develop new

analytical models of the relevant institutional details and behavioral complexities in the field. For

instance, while there has been much progress in modeling social behavior in the last two decades,

including models of fairness and reciprocity (see Cooper and Kagel 2016 for an overview), as well as

theoretical mechanism design implications of social preferences (Bierbrauer et al. 2017), no social

preferences model captures the relevant punishment and counter-punishment patterns within an

equilibrium framework (Engel 2014 and Dhami 2016 survey the literature). There is also

comparatively little research on the psychological and social determinants of the production of

reputation information, connecting the fundamental behavioral science literature on punishment

and the practical market design literature on feedback giving. Interesting variables include the role

of comparison processes for feedback giving and punishment (Chen et al. 2010, 2019, Mussweiler

and Ockenfels 2013), social identity and discrimination (Chen and Li 2009, Cui et al. 2019, Kim et al.

2019, Bolton et al. forthcoming), and uncertainty (Ambrus and Greiner 2012, Bolton et al. 2019).

4 Matching markets in education

While auction markets use prices to coordinate demand and supply, most of the centralized matching

markets take agents’ reported preferences as inputs and feed them into various matching algorithms to

determine who gets what. Matching theory has been applied to many important design and

management problems in both the private and public sectors, such as school choice, college

admissions, course allocation and entry-level labor markets. The practical design application of

matching theory starts with the redesign of the National Residence Matching Program (Roth and

Peranson 1997), and has since evolved into a research program that addresses practical market design

problems using game theory, laboratory and field experiments, as well as computation methods (Roth

2002).

In what follows, we provide three examples of how a combination of economic theory and

laboratory experiments inform the implementation of better education policies and management

practices.

4.1 Re-design school choice mechanisms

School choice has been a widely debated education policy across the world, affecting the education

experiences and labor market outcomes for millions of students each year.

8

The past two decades

have witnessed major innovations in this domain. For example, shortly after Abdulkadiroğlu and

Sönmez (2003) was published, New York City high schools replaced their allocation mechanism with

a capped version of the student-proposing deferred acceptance (DA) mechanism (Gale and Shapley

8

This section is based on, and partly taken from, the school choice literature review in Chen et al. (2018) and

Chen and Kesten (2019).

19

1962), a less manipulable and more stable mechanism advocated by matching theorists involved in

the design process (Abdulkadiroğlu et al. 2005a). In 2005, the Boston Public School Committee voted

to replace its Boston immediate acceptance school choice mechanism (IA) with DA (Abdulkadiroğlu

et al. 2005b) after IA was shown to be vulnerable to strategic manipulation both theoretically

(Abdulkadiroğlu and Sönmez 2003, Ergin and Sönmez 2006) and experimentally (Chen and Sönmez

2006). In this case, experimental data helped make the case for DA in Boston’s decision to switch

from IA in 2005 (Abdulkadiroğlu et al. 2005b).

Within school choice research, matching mechanisms that have received significant scholarly

attention include the Gale-Shapley Deferred Acceptance mechanism (Gale and Shapley 1962), the

Boston Immediate Acceptance mechanism (Abdulkadiroğlu and Sönmez 2003), the Top-Trading-

Cycles (TTC) mechanism (Abdulkadiroğlu and Sönmez 2003), and variants of the serial dictatorship

mechanism (Pathak and Sönmez 2013). Indeed, the question of which mechanism best meets the

goals of a school choice plan has been at the center of intensive research as well as ongoing policy

discussions (Abdulkadiroğlu and Sönmez 2003, Ergin and Sönmez 2006, Abdulkadiroğlu et al. 2011).

We first briefly introduce the school choice mechanisms, summarize their theoretical properties,

and performance in the laboratory and field when applicable. We then discuss the major school

choice reforms around the world concerning the abandonment or adoption of some of these

mechanisms.

Our first mechanism, IA, is the most common school choice mechanism observed in practice in

China, the United Kingdom and the United States. Its outcome can be calculated via an algorithm that

puts a lot of emphasis on a student’s reported top choice. In the first step of the algorithm, each

school only considers students who have listed it as their top choice, and sorts them in priority order.

Each school admits those with the highest priority and rejects the rest. Those rejected enter the

second step of the algorithm, and so on. The algorithm terminates when there are no students left

to assign or no school seats remain. Importantly, note that the assignments in each step are final.

We will use a simple example to illustrate the incentive problems created by this algorithm.

Consider a fictional student, Anna, who applies to elementary schools under the IA algorithm. There

are three public elementary schools in her school district, Angell, Burns Park and King. Anna lives in

the Burns Park district, which gives her high priority at Burns Park, and low priority elsewhere. Her

top choice is Angell. Her second choice is Burns Park, and her third choice is King. If Anna ranks her

preferences truthfully but does not get into Angell (likely because she has lower priority there), her

application will be sent to Burns Park. However, if all Burns Park seats are filled in the first round,

Anna loses her priority advantage, and is assigned to her last choice, King. In this case, we say Anna

has justified envy as she is not assigned to Burns Park, but she prefers Burns Park to her assignment,

and she has a higher priority than some student who is assigned to Burns Park.

If she plays it safe and list Burns Park as her top choice, she is guaranteed a seat at Burns Park, a

better outcome than being assigned to King. Based on this feature, an important critique of IA is that

it gives students strong incentives for gaming through misreported preferences. That is, a student

who has high priority for a school under IA may lose her priority advantage for that school if she does

20

not list it as her first choice. Consequently, IA forces students to make hard and potentially costly

choices, which leads to a high-stakes game among participants with different levels of strategic

sophistication. This has been observed in the laboratory among financially motivated subjects (Chen

and Sönmez 2006), as well as in the field, using naturally occurring data from Boston (Pathak and

Sönmez 2008). Recognition of these deficiencies of IA has lead Boston and many other cities in the

United States to abandon IA and replace it with DA.

Outside of the United States, variants of IA have been used as a school choice mechanism in China,

France, and the United Kingdom. In China, to equalize access to school resources across students of

different socioeconomic backgrounds, the Chinese government abandoned the previous merit-based

middle school admissions mechanism in 1998, and replaced it with an open enrollment school choice

mechanism where parents rank schools and schools select students using IA (Lai et al. 2009). Since

then, students applying for middle schools are prioritized based on their residence, whereas those

applying for high schools are prioritized based on their municipal-wide exam scores. Using public

middle school admissions data from Beijing Eastern City District, He (2014) investigates parents’

behavior and finds that parents are overcautious in that they play “safe” strategies too often.

Combining survey data, middle school choice data and High School Entrance Exam test scores from

Beijing, Lai et al. (2009) find that children of parents who made mistakes in middle school selection

were admitted to lower quality schools and achieved lower test scores on the High School Entrance

Exam three years later. Despite these problems, IA continues to be used as the major school choice

mechanism in China.

Our second mechanism is the student-proposing deferred acceptance mechanism (Gale and

Shapley 1962), which has played a central role in the school choice reforms in Boston and New York

City (Abdulkadiroğlu et al. 2005a,b), as well as in Finland, Ghana, Paris (Fack et al. 2019), Romania,

Singapore and Turkey. The outcome of this mechanism can be calculated via the deferred acceptance

(DA) algorithm. In the first step of the algorithm, each school also only considers students who have

listed it as their top choice, and sorts them in priority order. Each school put those with the highest

priority tentatively on hold and rejects the rest. Those rejected apply to their second-choice school,

which resorts those on hold from the previous round and the newcomers based on their priority, put

those with the highest priority on hold and reject the rest, and so on. The algorithm terminates when

each student is tentatively retained at some school. Note that, in DA, assignments made at each step

are temporary, until the last step. This feature contributes to the desirable properties of DA in terms

of incentives and stability.

Consider our fictional student Anna’s brother, Marco, who applies to elementary schools under

the DA algorithm. He lists his choices in the true order of his preferences, which are the same as his

sister’s: Angell, Burns Park, and King. If Marco does not get into Angell either, his application will be

sent to Burns Park. The algorithm then resorts everyone retained from the first round together with

the newcomers based on their priorities. As Marco does not lose his priority advantage, he is assigned

to Burns Park. Therefore, truth telling does not hurt Marco, and may sometime make him strictly

better off.

21

To summarize, one advantage of DA is that it is strategy-proof (Roth 1982, Dubins and Freedman

1981). That is, when students can list as many choices as they want, DA allows them to safely rank

schools in true order of preferences. They won’t lose a place just because someone else applies

earlier in the algorithm. A second advantage of DA is that it produces the stable matching that is most

favorable to each student. In other words, when the algorithm finishes, there will not be any student

and any school that are not matched with each other but that would both prefer to be. Although its

outcome is not necessarily Pareto efficient, it is constrained efficient among the stable mechanisms.

In many laboratory experiments testing DA, researchers find that it remains the mechanism that

achieves the highest proportion of stable allocations. Depending on the size of the match, the

proportion of students revealing their preferences truthfully varies between 47% to over 80%

(Hakimov and Kübler 2019). In addition to Boston and New York City, variants of DA have been

implemented in Amsterdam, Denver, Hungary, Paris, New Orleans and Taiwan.

In the trade-off between elimination of justified envy and Pareto efficiency, DA gives up Pareto

efficiency. The Top Trading Cycles mechanism (TTC), on the other hand, gives up elimination of

justified envy, but is Pareto efficient.

In each round of the TTC algorithm, each student points to her favorite school among schools that

remain, whereas each school points to the applicant who has the highest priority at that school

among the remaining applicants. A cycle of students and schools pointing at each other is called a

“top trading cycle”. Every student in a cycle is assigned to the school she is pointing to. These students

as well as their assignments are removed from the allocation process. School capacity is updated. The

algorithm terminates when each student is assigned a school seat or all school seats are assigned.

The TTC mechanism is not only Pareto efficient, but also strategy-proof. In the lab, however,

without prompting from the experimenters, sometime up to one-third of the subjects manipulate

their preferences (Chen and Sönmez 2006).

In theory, TTC has an efficiency advantage over IA as well as DA: The outcome of IA is Pareto

efficient if participants reveal their preferences truthfully. Any efficiency loss in IA is a consequence

of preference manipulation. DA, on the other hand, is strategy-proof, but elimination of justified envy

and Pareto efficiency are not compatible. Since DA Pareto dominates any other mechanism that

eliminates justified envy, any efficiency loss in DA is a consequence of this incompatibility.

In practice, the only public school district which implemented TTC as its school choice mechanism

is the New Orleans Recovery School District (RSD). However, one year after its implementation, the

RSD switched to DA, citing the difficulty to explain TTC to parents as well as the lack of stability as

main reasons for the switch. Using data from New Orleans, Abdulkadiroğlu et al. (2017) find that the

switch to DA had little impact on the overall aggregate rank distribution of choices received by

applicants; however, no student is involved in a blocking pair as a result of the switch. Based on the

revealed preferences of officials in both the Boston and New Orleans public schools, one cannot help

but notice that they seem to put more weight on stability, guaranteed by DA, compared to efficiency,

guaranteed by TTC. The lack of stability might create blocking pairs, which might lead to legal

challenges to the school district.

22

Lastly, in the fall of 2009, without the involvement of market design researchers, Chicago Public

Schools decided to replace its highly manipulable matching algorithm for exam schools, a variant of IA,

with a less manipulable mechanism, a capped version of the serial dictatorship (Pathak and Sönmez

2013).

In sum, market design in the school choice domain is considered a success story, with many active

research projects investigating school choice mechanisms around the world. In many cases,

researchers are directly involved in the design of better matching algorithms, whereas in other cases,

officials from public school districts abandon problematic matching algorithms in favor of less

manipulable ones.