Veterinarians

Preface

This publication is designed to help you understand California’s Sales and Use Tax Law as it applies to veterinary

practices, including clinics, hospitals, or centers operated by veterinarians. The term “veterinarian” is not limited to

individuals, but also includes any firm, partnership, joint venture, association, limited liability company, corporation,

syndicate, or any other group or combination acting as a unit to provide veterinary services.

If you cannot find the information you are looking for in this publication, please visit our website at www.cdtfa.ca.gov

or call our Customer Service Center at 1-800-400-7115 (CRS:711). Customer service representatives are available to

answer your questions Monday through Friday between 7:30 a.m. and 5:00 p.m. (Pacific time), except state holidays.

This publication complements publication 73, Your California Seller’s Permit, which includes general information

about obtaining a permit; using a resale certificate; collecting and reporting sales and use taxes; buying, selling,

or discontinuing a business; and keeping records. Please refer to our website or our For More Information section

for the complete list of California Department of Tax and Fee Administration (CDTFA) regulations and publications

referenced in this publication.

We welcome your suggestions for improving this or any other publication. If you would like to comment, please

provide your comments or suggestions directly to:

Audit and Information Section, MIC:44

California Department of Tax and Fee Administration

PO Box 942879

Sacramento, CA 94279-0044

Please note: This publication summarizes the law and applicable regulations in effect when the publication was

written, as noted on the cover. However, changes in the law or in regulations may have occurred since that time. If

there is a conflict between the text in this publication and the law, the law is controlling.

VETERINARIANS

|

APRIL 2022

Do You Make Retail Sales?

As a veterinarian, you commonly provide products including drugs, medicines, and pet supplies to your clients. This section

is intended to help you determine if any of your sales are considered retail sales, and whether you need a seller’s permit.

Information on reporting sales tax is found in the next section. Please refer to our website or our For More Information

section for CDTFA information and the complete list of regulations and publications referenced in this publication.

Are you a retailer, consumer, or both?

Retailer. If you make sales in your practice that qualify you as a retailer under the Sales and Use Tax Law, you must

obtain a seller’s permit, file tax returns, and pay tax on those sales. Using resale certificates, you may buy products

to resell. Your suppliers will not apply sales tax to purchases you make with a resale certificate.

Consumer. If you are considered a consumer (end user) for all of your transactions, you are generally not required

to obtain a seller’s permit or report sales tax to CDTFA. Your suppliers will generally apply tax when you purchase

products that you will consume in your practice. Under certain circumstances, you may be liable for reporting use

tax to CDTFA. (see Required registration to report use tax and Taxability of Purchases).

Most veterinarians are both. You may be considered a retailer in some instances and a consumer in others

(see table below). If this is the case, you will need to obtain a seller’s permit and report tax to CDTFA on your retail

sales. While you may use a resale certificate to purchase items you will resell, your suppliers should apply tax when

you purchase items you will consume in your practice.

Required registration to report use tax – how to register and le a return

California law requires a “qualified purchaser” to register with CDTFA and annually report and pay use tax directly to

us. You can register on our website at www.cdtfa.ca.gov, by selecting Register for a Permit. Once you have registered,

you may pay any use tax due by filing your return. You can also register to report use tax in person at any of our

offices. A “qualified purchaser” includes businesses with at least $100,000 in annual gross receipts from business

operations. Gross receipts are the total of all receipts from both in-state and out-of-state business operations. For

additional information see publication 126, Mandatory Use Tax Registration for Service Enterprises.

Which sales are retail sales?

To determine which of your sales are retail sales, CDTFA considers:

• The type of service, if any, provided with the product;

• Whether the product is a drug or medicine, or another type of product; and

• For products other than drugs or medicines, your billing method.

The table below shows the circumstances in which you are considered to be a retailer, and when you are a

consumer. It is important that you refer to the following pages for definitions of the terms found in the table.

Retail sales and products used by veterinarians

Item

Furnished without professional

services

Furnished with professional services

Separate charge Charge not separate

Drugs and medicines retailer consumer consumer

Other products retailer retailer consumer

VETERINARIANS

|

APRIL 2022

Professional services

Charges for your services are not subject to sales tax.

In defining retail sales by veterinarians, CDTFA looks at the relationship between the products you sell and

the services you provide. As you can see on the preceding table, providing a product to a customer without

professional services is generally considered a taxable retail sale. Yet, when the same product is provided with

professional services, you may be considered the consumer of the product. Therefore, it is important that you

understand how CDTFA defines professional services.

Professional services

Professional services are considered to include activities such as:

• Diagnosis, including examinations, x-rays, tests, etc.

• Treatment

• Surgery

• Administration of drugs

Example, product furnished with professional services: Based on your examination of a parrot and subsequent

tests, you determine that the bird has a respiratory infection. You provide your client with a liquid antibiotic

for the parrot, an action directly related to specific professional services—in this case, your examination, tests,

and diagnosis. As you can see in the table above, when you provide a drug or medicine with professional

services, you are considered the consumer of the drug, and the transaction is not a retail sale (see Drugs and

medicines, below).

Other services

Some services you provide are not considered to be professional services. Although you may, in connection with

the sale of a product to a customer, use your:

• General medical knowledge and experience to recommend the use of a particular drug or other product; or

• Provide advice to a customer regarding the use of a particular product.

These actions are not considered professional services.

Example: A customer comes into your office seeking an ointment for a minor cut on her horse. Advice you

provide regarding which ointment to buy, or how to use it, is not considered a professional service. The sale of

the ointment is a retail sale (see Retail sales and products used by veterinarians).

Drugs and medicines

You are generally considered the consumer of drugs and medicines (see definition below) you furnish with

related professional services. However, when you do not provide related professional services, furnishing drugs

or medicines to clients is considered a retail sale, and you are generally required to report sales tax based on the

product’s selling price.

Exemptions: If a drug or medicine will be administered to food animals (see Feed for food animals) or to animals

that will be sold by their owners in the regular course of business, the sale, use, or purchase of the drug or medicine

may not be taxable. This is true whether you are considered the retailer or consumer of the product. For more

information and a table showing when tax applies to transactions involving drugs and medicines, see Tax- exempt

sales of drugs and medicines.

Definition

Veterinary drugs and medicines are considered to be substances or preparations intended for the use in the

diagnosis, cure, mitigation, treatment, or prevention of disease in animals. They include:

VETERINARIANS

|

APRIL 2022

• Pills (other than vitamins)

• Capsules (other than vitamins)

• Liquid medications

• Injectable drugs

• Ointments

• Vaccines

• Intravenous fluids

• Medicated soaps (which are available only to veterinarians)

Please note: Supplies you use in your practice, such as dressings, sutures, splints, etc., are not considered drugs or

medicines. You are generally considered the consumer of those supplies.

Other products

As shown in the table on Retail sales and products used by veterinarians, sales of products other than drugs or

medicines, when furnished without related professional services, are generally considered retail sales. When these

products are provided with professional services, your billing method determines whether the transaction is

considered a retail sale (see below).

The following products are not considered veterinary drugs or medicines:

• Flea powder, spray, and dip; flea collars

• Leashes, leads, and collars

• Animal carrying cases

• Animal shampoo

• Grooming aids

• Pet foods, including prescription diet foods and artificial diets

• Vitamins

Billing methods and tax

You are considered the retailer of products other than veterinary drugs or medicines furnished with professional

services when you list a separate charge for those items on your bill. Tax is due on the sale of the products based on

their selling price. However, if you bill your client for a lump sum amount (services and products combined in one

charge), you are considered the consumer of those products rather than the retailer.

X-rays

You are considered the retailer of x-rays if you:

• Deliver x-rays to a client (for example - you hand them to your client), and

• Charge separately for them.

Tax would apply to your charges.

Boarding charges

You may board animals at your hospital or clinic in association with professional services or as a service to your

clients. Your charges for boarding are not subject to tax, whether they are itemized or included in a lump-sum

billing. However, you may be required to report tax on the sale of products furnished for a boarded animal, as

explained on the next page.

VETERINARIANS

|

APRIL 2022

• If your bill does not list separate charges for products furnished, you are considered the consumer of those

products and should not buy them with a resale certificate. If you do, you will owe use tax based on their

purchase price (see Use tax).

• If your bill includes separately stated charges for products furnished, you are considered the retailer of those

products and must report tax on your sales. Exception: If you provide professional services with boarding, you

are generally considered the consumer of drugs and medicines even when you charge separately for them

(see Drugs and medicines).

Questions?

If you’re not sure whether to report tax on a sale, please call our Customer Service Center at 1-800-400-7115 (CRS:711).

VETERINARIANS

|

APRIL 2022

Reporting Sales Tax

The retail sale of goods in California is generally subject to sales tax. This section describes sales tax reporting, including

information on credit sales. For more information, you may wish to obtain a copy of publication 73, Your California

Seller’s Permit. Please refer to our website or our For More Information section for CDTFA information and the complete

list of regulations and publications referenced in this publication.

Sales tax reimbursement (including an amount for sales tax in your charges)

Although you are responsible to report and pay sales tax to CDTFA, the law allows you to collect “reimbursement”

from your customers for the sales tax you will owe on each retail sale. You may add the amount of tax due to the

price of the products you sell, being sure to itemize the tax on your invoice or receipts. Or, you may include it

in the price for the product. If you choose the latter method, you must post a visible sign stating, “All prices of

taxable items include sales tax reimbursement calculated to the nearest mill,” or include a similar statement on

your sales receipts.

Tax due with your sales and use tax return

You must report all of your sales on your sales and use tax return — including nontaxable sales, nontaxable charges

for professional services, and nontaxable boarding charges. The tax due with each return is based on your total

gross sales for the period less deductions for nontaxable receipts and other adjustments. (Some exemptions and

deductions common to veterinary practices are described in Exemptions and deductions.)

Reporting credit sales

Tax for an item sold on credit is due with the tax return for the reporting period in which you make the sale, even

though you may not receive full payment until a later date. Tax is due on the full selling price.

Example: You perform surgery on a horse in March and keep the animal at your clinic for two days for

observation. On your bill, you separately state a $50 charge for the horse’s feed (as explained in Boarding

charges, when related to professional services and listed as a separate charge, the sale of feed is generally

considered a taxable retail sale). Your client pays you $25, and agrees to pay the balance in future months.

Regardless of when you receive the balance due, the $50 selling price of the feed must be included on your

tax return for the reporting period that includes the month of March.

You may exclude amounts for insurance, interest, finance, and carrying charges from the taxable selling price you

report for a credit sale, provided you keep adequate and complete records itemizing those charges.

If you have reported tax on a transaction and do not receive payment from your customer, you may be able to claim

a bad debt deduction on your sales and use tax return. Please see Bad debt deductions.

Losses from robbery, theft, or shoplifting

You are required to pay tax on all of your taxable sales despite any loss of proceeds from them. As a result, you may

not take a deduction for a loss due to robbery, theft, or shoplifting.

Although you cannot deduct such losses, you must document them in your records. Acceptable forms of

documentation include police reports, insurance claims, reports from private investigating agencies, etc. It is

important that you be able to account for all of your inventory and income if your practice is audited.

VETERINARIANS

|

APRIL 2022

Exemptions and Deductions

Although you must report all of your sales on your sales and use tax return, you may deduct amounts included for

nontaxable sales or for other allowable deductions before you calculate the tax you owe. This section describes some

of the more common nontaxable sales and deductions that may apply in your practice. For more information, see

publication 73, Your California Seller’s Permit. You may also wish to obtain CDTFA publication 61, Sales and Use Tax:

Exemptions and Exclusions. Please refer to our website or our For More Information section for CDTFA information and

the complete list of regulations and publications referenced in this publication.

Recordkeeping

It is important that you maintain proper documentation for all tax-exempt sales and other deductions you claim

on your sales and use tax return. You should be sure to maintain resale and exemption certificates and indicate

purchasers’ names on corresponding sales invoices, and to maintain other information necessary to substantiate

each exemption or deduction.

Sales for resale

Sales you make to others for resale are not subject to tax, provided you obtain a valid resale certificate from the

purchaser. For more information on acceptance or use of resale certificates, see publication 73, Your California

Seller’s Permit, or Regulation 1668, Resale Certificates.

Sales of feed

Feed for food animals

Your sale or use of feed for food animals is not subject to tax. Food animals are considered to be those animals,

birds, or insects commonly used to produce food items that people eat, such as meat products, dairy products,

eggs, and honey. Examples include cattle, swine, chickens, sheep, goats, quail, ostriches, turkeys, and bees.

This tax exemption applies regardless of the method you use to bill your customer. Feed, for sales and use tax

purposes, includes products such as grain, hay, seed, and similar products. It does not include sand, charcoal,

granite grit, or sulfur.

In addition, your purchases of feed for food animals are not taxable. See Purchases of feed for food animals for

further information.

Exemption certicates

If you sell feed for food animals and that feed can also be used for nonfood animals, you may need to obtain a feed

exemption certificate from the purchaser (see Appendix). However, a certificate is not required for sales of:

• Two or fewer standard sacks of grain, and/or four or fewer bales of hay (for use as feed)

• Feed bearing a manufacturer’s label indicating that it is intended for food animals

Sales of feed for nonfood animals to be sold

The sale of feed for nonfood animals that will be sold by the purchaser in the regular course of business is not

subject to tax. In addition, feed sales to breeders who will sell their nonfood animals’ offspring in the regular course

of business are not taxable. You should obtain a feed exemption certificate from the purchaser to substantiate these

sales (see Appendix).

VETERINARIANS

|

APRIL 2022

Tax-exempt sales of drugs and medicines

Under certain circumstances, your sale or use of a veterinary drug or medicine is not taxable. The product must be

sold for the prevention or control of disease in food animals (see Drugs and medicines), or in animals that will be

sold by the purchaser in the regular course of business. For animals that will be sold, the drug or medicine must be

intended for administration as an additive to feed or water rather than for direct administration. The table below

summarizes how tax applies to the sale or use of drugs and medicines.

Type of Animal

Drug or Medicine Administered

in Feed or Water Directly

1

Food Animal Nontaxable Nontaxable

Nonfood animal if it or its

offspring will be sold in the

regular course of business

Nontaxable

Taxable

Other nonfood animal Taxable Taxable

1

Oral, hypodermic, external, or topical application, including injections, implants, drenches, repellents, and

pour-ons.

Supporting documentation

When you make a nontaxable sale of drugs or medicine, your sale should be supported by a drug exemption

certificate completed by the purchaser. A sample certificate is shown (see Appendix).

Note: These rules also apply to your purchases of drugs and medicines (see Purchases of drugs and medicines).

Tax-paid purchases resold prior to use

If you pay an amount for sales or use tax on the purchase of an item and then resell the item before using it, you can

take a deduction on your tax return. When you report the sale, you may deduct your cost for the item, not including

any applicable tax, under “Cost of Tax-Paid Purchases Resold Prior to Use.” If you do not take the deduction, you may

pay more tax than you owe.

Example: You purchase a case of prescription diet dog food for $20. Since you intend to use the dog food in

a way that qualifies you as its consumer, your supplier applies tax to your purchase. Later, a customer comes

into your practice with a prescription for diet dog food from another veterinarian. You sell the customer the

case of dog food for $35 without providing any related professional services. The transaction is considered a

retail sale.

You are required to report the $35 sale on your sales and use tax return (included in your gross receipts) and

to pay sales tax on the transaction. However, since sales tax was applied to your initial dog food purchase,

you can take a $20 deduction (your cost, not including tax) on your return, under “Cost of Tax-Paid Purchases

Resold Prior to Use.”

Cash discounts on taxable sales

A cash discount on a retail sale is not subject to sales tax. For example, if you sell a dog kennel for $350 less a ten

percent discount ($35), tax would be due on $315, the total amount you received in connection with the sale

($350 price – $35 discount = $315). Your invoice or receipt should clearly list the original price, amount of discount,

amount subject to tax, and the amount of tax applicable to the sale. Please see publication 113, Coupons, Discounts

and Rebates, for additional information.

VETERINARIANS

|

APRIL 2022

Bad debt deductions

If you reported tax on a sale and have been unable to collect payment from your customer, you may claim a

deduction for the bad debt. Bad debts may take the form of:

• Checks returned unpaid by the purchaser’s bank which you have determined to be uncollectible; or

• Accounts from charge or credit sales found worthless.

You must charge off the bad debts for income tax purposes or charge them off in accordance with generally

accepted accounting principles.

You should claim the deduction on the return filed for the period in which you found the account worthless and

wrote it off. Your deduction cannot include the amount of tax that applied to the sale, or any other nontaxable

charges included in your total loss. (When you calculate your deduction, please be sure to deduct tax from the total

loss at the rate in effect when the sale was made.) You cannot deduct amounts you paid to collect the funds due.

If you later collect the money due for a bad debt (including worthless checks), any amount you previously claimed

as a deduction must be reported as a taxable sale.

Note: Since there are many rules governing deductions for bad debt losses, see Regulation 1642, Bad Debts.

Professional services and boarding charges

Charges for professional services and boarding charges that do not include taxable sales of products are not subject

to tax. Receipts from these services included in “Total (gross) sales” on your sales and use tax return should be

deducted under “Other” deductions before you calculate the tax you owe.

VETERINARIANS

|

APRIL 2022

Taxability of Purchases

Tax generally applies to your purchases of items you will consume in your practice. However, if you use a resale certificate

to purchase merchandise you will resell, tax will not apply to the transaction. If you purchase property for resale but use

it for another purpose, you may be required to pay use tax to CDTFA. This section describes common situations in which

sales or use tax may apply to your purchases. Also refer to Required registration to report use tax.

General principles and methods

Generally, you should use a resale certificate to purchase items you will sell at retail, and pay sales tax reimbursement

to your suppliers or use tax on purchases of items you will consume. However, it may be difficult for you to apply this to

all of your purchases, since you may both resell and consume certain products you buy for your practice.

You may find it helpful to adopt one of the following purchasing methods and use it consistently in your practice.

If you rarely make retail sales

If you rarely make retail sales, you may prefer not to use a resale certificate when making purchases for your

practice. If you do resell items, you may be able to take a “tax-paid purchases resold prior to use” deduction

(explained in Tax-Paid Purchases Resold Prior to Use).

If you ordinarily make retail sales of each item you purchase

If you sell some of each product you purchase, you may wish to buy all of those products using a resale certificate.

You will report sales tax on items you sell at retail, and use tax on the cost of items you consume in your practice.

You should report that cost under “Purchases Subject to Use Tax” on your sales and use tax return

(see Items you consume when tax not paid on purchase). Use tax is explained in more detail below.

If you can determine which products you will sell and which you will consume

If you can readily determine which products you buy to sell at retail, and which products you buy to consume, you

should use a resale certificate when purchasing items you will resell. You should pay tax reimbursement to your

suppliers when purchasing products you will consume.

Use tax

In certain circumstances, use tax applies to the purchase price of items you buy. For example, if you purchase an

item without paying an amount for California tax and then use the item for a purpose other than resale, your

purchase is subject to use tax. The use tax rate is the same as the sales tax rate for your location. You should report

purchases subject to use tax on the line of that same name (usually line 2) of your sales and use tax return.

The following sections describe typical situations in which use tax applies to your purchases.

Merchandise purchased for resale

You must report use tax to CDTFA if you purchase merchandise with a resale certificate and then use the

merchandise for other business or personal purposes. Taxable uses include:

• Use of products as a consumer (see Are you a retailer, consumer, or both?).

• Donations (donations to certain charitable organizations may be tax-exempt. Please call our Customer Service

Center at 1-800-400-7115 (CRS:711) for further information.

• Gifts to friends, employees, and others.

• Personal use.

Please note: If you know at the time you make a purchase that you will not resell the merchandise you are buying,

you may not use a resale certificate for that transaction.

VETERINARIANS

|

APRIL 2022

Items used for demonstration and display

Merchandise you use exclusively for demonstration and display while it is for sale is not subject to use tax. Sales tax

applies when the item is sold.

If you use a demonstration or display item for any additional purpose, including personal use, the purchase price

must be reported under “Purchases Subject to Use Tax” on your return. Again, sales tax applies to the subsequent

retail sale of the merchandise. For more information, see Regulation 1669, Demonstration, Display, and Use of

Property Held for Resale—General. Please refer to our website or our For More Information section for CDTFA

information and the complete list of regulations and publications referenced in this publication.

Purchases from out-of-state retailers

In general, if you purchase taxable merchandise from a retailer located outside the state without paying California

tax, and use the merchandise for a purpose other than for resale (including use as a consumer), the purchase is

subject to use tax and must be reported to CDTFA.

Credit against use tax liability for payment of another state’s tax. If you were required to pay, and did pay,

another state’s sales tax on a purchase, you may take a credit against your use tax liability by:

• Reporting the amount of the purchase under “Purchases Subject to Use Tax,” and

• Deducting the amount of tax paid under “Sales or Use Tax Paid to Other States” on your return. You can claim a

credit up to the amount of California use tax due.

Please note: You may not claim this credit against your sales tax liability for purchases you resell.

Some out-of-state retailers are authorized to collect and pay California use tax. If your receipt indicates that the retailer

collect the correct amount of California use tax from you. You do not need to report the purchase on your return.

Items you consume when tax not paid on purchase

If you purchase merchandise without payment of California tax and consume the items in your practice rather than

resell them, you must report use tax on your purchase. This holds true whether you buy the product using a resale

certificate or from an out-of-state supplier who does not collect California use tax (see Purchases from out-of-state

retailers, above).

Example: You spend $250 on equine vaccine for use in your large animal practice, knowing that you will sell

some of the vaccine on an over-the-counter basis and use some of it in connection with professional services.

Since you intend to resell some of the vaccine, you provide your supplier with a resale certificate and the

supplier does not apply tax to your purchase.

You administer one-half of the vaccine to horses you see on ranch visits, a use connected with professional

services. Since you are considered to be the consumer of vaccine provided with professional services rather

than its retailer (see table Retail sales and products used by veterinarians), you must report use tax on the

portion of the vaccine you use in this way. In this case, one-half of your original purchase cost, or $125. (You

must report sales tax on equine vaccine sales not connected with your professional services, based on your

selling price.)

Partial exemption for agriculture-related purchases

Purchases of certain supplies, equipment and machinery, liquefied petroleum gas (LPG), feed, and veterinary drugs

by veterinarians used primarily or exclusively in assisting farmers, ranchers, or other growers may be exempt from

the state general fund portion of the sales and use tax, currently 5.25 percent. To receive the partial exemption,

veterinarians must provide a partial exemption certificate to retailers. For more information, see Regulation 1533,

Liquefied Petroleum Gas, Regulation 1533.1, Farm Equipment and Machinery, and publication 66, Agricultural Industry.

VETERINARIANS

|

APRIL 2022

Please note: The rate for the general fund portion of the sales tax has been lower in the past and may change again

after the date of this publication. You must use the rate in effect at the time your sale occurs. Information on tax rate

changes is available at our website or from our Customer Service Center.

Business supplies and equipment

Purchases of items used in your business, such as display fixtures, equipment, instruments, bookkeeping materials,

and maintenance materials, are subject to sales or use tax. Tax also applies to your purchases of supplies used in

your practice, such as disinfectant, dressings, suture materials, and similar items. If bought from an out-of-state

seller who does not charge California use tax, you must report the purchase on your return, under “Purchases

Subject to Use Tax.” The subsequent retail sale of these items would be subject to sales tax.

Purchases of feed for food animals

Purchases of feed for food animals (see Sales of feed) are not subject to tax. This holds true whether you later sell

the feed at retail or consume it in your practice. You should provide your supplier with a completed feed exemption

certificate at the time of purchase (see Exemption certificates). A sample certificate is found in the Appendix.

Purchases of drugs and medicines

As with sales of drugs and medicines, some of your drug and medicine purchases may not be subject to tax. For

information regarding how tax applies to transactions involving drugs and medicines, see the text and table on Tax-

exempt sales of drugs and medicines. You should provide your supplier with a drug exemption certificate when you

make qualifying nontaxable purchases of drugs and medicines (see Appendix).

VETERINARIANS

|

APRIL 2022

Appendix: Exemption Certicates

Feed exemption certicate

For information on feed exemption certificates, see Exemptions and Deductions and Purchases of feed for food

animals.

Drug exemption certicate

For information on drug exemption certificates, see Tax-exempt sales of drugs and medicines and Purchases of

drugs and medicines.

Please note: There is no required form for exemption certificates. Other forms are acceptable provided they contain

all of the information shown here. While CDTFA does not provide blank certificates, you may reproduce the ones on

this page.

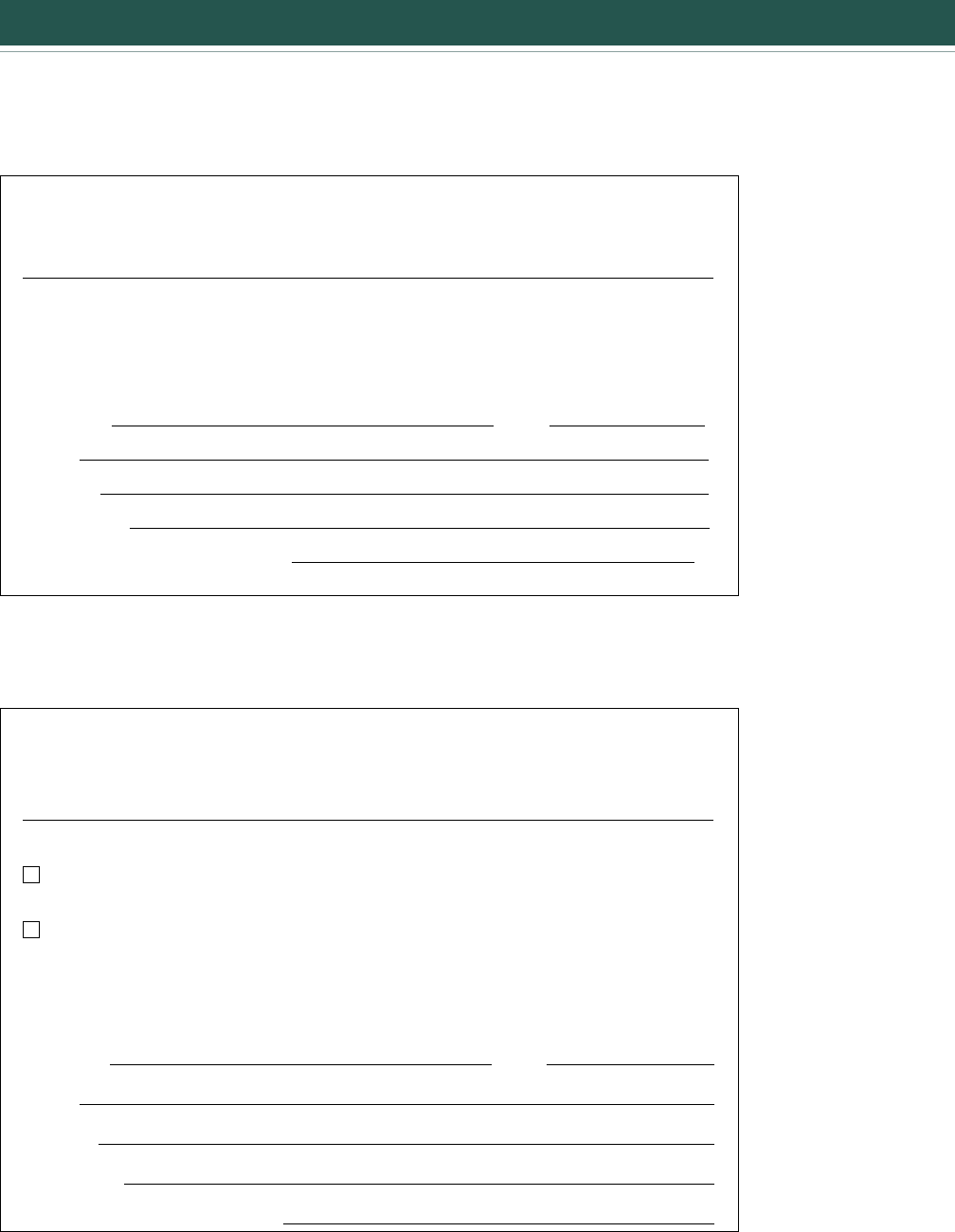

FEED EXEMPTION CERTIFICATE

“I hereby certify that all of the feed which I shall purchase from

will be purchased for use as feed for food animals or for nonfood animals which are

being sold in the regular course of business. This certificate shall be considered

a part of each order which I give unless such order shall otherwise specify. This

certificate shall be good until revoked in writing.”

Signature Date

Name

Address

Occupation

Seller’s Permit Number (if any)

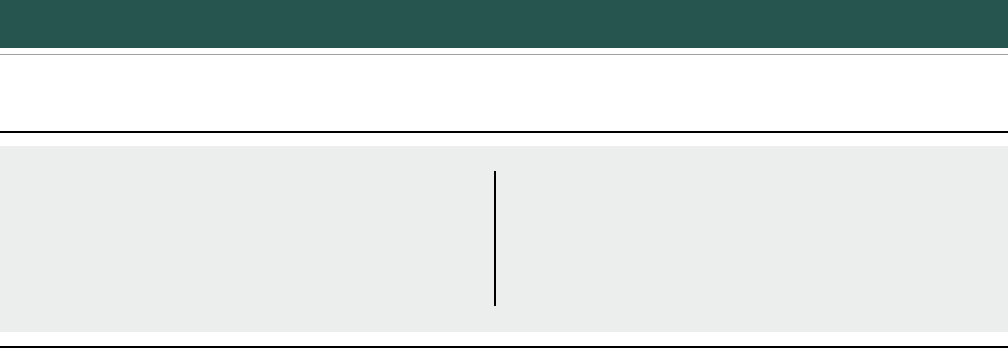

DRUG EXEMPTION CERTIFICATE

“I hereby certify that the drugs or medicines which I shall purchase from

will be purchased

as an additive to feed or drinking water for food animals or for nonfood animals

being held for sale in the regular course of business, or

for administration directly to a food animal.

This certificate shall be considered a part of each order which I shall give unless

such order shall otherwise specify. This certificate shall be good until revoked

in writing.”

Signature Date

Name

Address

Occupation

Seller’s Permit Number (if any)

VETERINARIANS

|

APRIL 2022

INTERNET

www.cdtfa.ca.gov

You can visit our website for additional information—such as laws, regulations, forms, publications, industry guides,

and policy manuals—that will help you understand how the law applies to your business.

You can also verify seller’s permit numbers on our website (see Verify a Permit, License, or Account).

Multilingual versions of publications are available on our website at www.cdtfa.ca.gov/formspubs/pubs.htm.

Another good resource—especially for starting businesses—is the California Tax Service Center at www.taxes.ca.gov.

TAX INFORMATION BULLETIN

The quarterly Tax Information Bulletin (TIB) includes articles on the application of law to specific types of

transactions, announcements about new and revised publications, and other articles of interest. You can find

current TIBs on our website at www.cdtfa.ca.gov/taxes-and-fees/tax-bulletins.htm. Sign up for our CDTFA updates

email list and receive notification when the latest issue of the TIB has been posted to our website.

FREE CLASSES AND SEMINARS

We offer free online basic sales and use tax classes including a tutorial on how to file your tax returns. Some classes are

offered in multiple languages. If you would like further information on specific classes, please call your local office.

WRITTEN TAX ADVICE

For your protection, it is best to get tax advice in writing. You may be relieved of tax, penalty, or interest charges that

are due on a transaction if we determine that we gave you incorrect written advice regarding the transaction and

that you reasonably relied on that advice in failing to pay the proper amount of tax. For this relief to apply, a request

for advice must be in writing, identify the taxpayer to whom the advice applies, and fully describe the facts and

circumstances of the transaction.

For written advice on general tax and fee information, please visit our website at www.cdtfa.ca.gov/email to email

your request.

You may also send your request in a letter. For general sales and use tax information, including the California

Lumber Products Assessment, or Prepaid Mobile Telephony Services (MTS) Surcharge, send your request to:

Audit and Information Section, MIC:44, California Department of Tax and Fee Administration, P.O. Box 942879,

Sacramento, CA 94279-0044.

For written advice on all other special tax and fee programs, send your request to: Program Administration Branch,

MIC:31, California Department of Tax and Fee Administration, P.O. Box 942879, Sacramento, CA 94279-0031.

TAXPAYERS’ RIGHTS ADVOCATE

If you would like to know more about your rights as a taxpayer or if you have not been able to resolve a problem

through normal channels (for example, by speaking to a supervisor), please see publication 70, Understanding Your

Rights as a California Taxpayer, or contact the Taxpayers’ Rights Advocate Office for help at 1-888-324-2798. Their fax

number is 1-916-323-3319.

If you prefer, you can write to: Taxpayers’ Rights Advocate, MIC:70, California Department of Tax and Fee Administration,

P.O. Box 942879, Sacramento, CA 94279-0070.

FOR MORE INFORMATION

For additional information or assistance, please take advantage of the resources listed below.

CUSTOMER SERVICE CENTER

1-800-400-7115 (CRS:711)

Customer service representatives are available

Monday through Friday from 7:30 a.m. to 5:00 p.m.

(Pacific time), except state holidays. In addition to

English, assistance is available in other languages.

OFFICES

Please visit our website at

www.cdtfa.ca.gov/office-locations.htm

for a complete listing of our office locations. If you

cannot access this page, please contact our

Customer Service Center at 1-800-400-7115 (CRS:711).

Regulations, forms, publications, and industry guides

Lists vary by publication

Selected regulations, forms, publications, and industry guides that may interest you are listed below.

Spanish versions of certain publications are also available online.

Regulations

1506 Miscellaneous Service Enterprises

1533 Liquefied Petroleum Gas

1533.1 Farm Equipment and Machinery

1587 Animal Life and Feed

1641 Credit Sales and Repossessions

1642 Bad Debts

1654 Barter, Exchange, “Trade-ins” and Foreign Currency Transactions

1655 Returns, Defects and Replacements

1667 Exemption Certificates

1668 Resale Certificates

1669 Demonstration, Display and Use of Property Held For Resale-General

1698 Records

1700 Reimbursement for Sales Tax

1821 Forword—District Taxes

Publications

44 District Taxes (Sales and Use Taxes)

51 Resource Guide to Tax Products and Services for Small Businesses

58A How to Inspect and Correct Your Records

61 Sales and Use Taxes: Exemptions and Exclusions

70 Understanding Your Rights as a California Taxpayer

73 Your California Seller’s Permit

74 Closing Out Your Account

75 Interest, Penalties, and Collection Cost Recovery Fee

76 Audits

103 Sales for Resale

113 Coupons, Discounts, and Rebates

126 Mandatory Use Tax Registration for Service Enterprises