Page 0 of 41

Lodgers’ Tax Best

Practices Handbook

This handbook’s purpose is to provide best practices, unification, standardization, and an overall framework

on how to best collect, enforce, and administer these funds by empowering stakeholders and to position

tourism leaders to make optimal marketing and promotion decisions that advance their destinations and

the industry.

White Sands National

Park

Page 1 of 41

TABLE OF CONTENTS —

1. Executive Summary

a. Purpose

b. Guiding Principals

c. Development Process

2. The Path of Lodgers’ Tax

a. Collection: Lodging Businesses

b. Submission: NM Department of Finance Administration (DFA) — Local Government Division

c. Governance & Administration: Local Governments

i. Calculating How Lodgers’ Tax Can Be Spent

ii. Other Allowable Uses of Lodgers’ Tax Proceeds

iii. Accountability

d. Oversight & Transparency: Lodgers’ Tax Advisory Boards

e. Disbursement: Lodgers’ Tax Funds Administrators

i. Industry Statistics to Have on Hand

ii. Determination of Applicable Use & Funding Requests

1. Understand Use Provisions

2. Understand Other Definitions

3. Develop a Strategic Process for Funds Use

4. Statutory Requirements & Best Practice Recommendations

iii. Measure the Return on Investment & Economic Impact

3. Additional Stakeholders

4. Additional Tourism Development Financing Mechanisms

5. Overview of the Short-term Rental Market

a. Creating Effective Short-term Rental Policies

i. Assessment

ii. Policy Objectives

iii. Regulatory Approaches

b. Monitoring, Compliance & Enforcement

c. Resources

6. Descriptions & Definitions

7. Resource Appendix

Disclaimer Statement

The information provided in this document does not, and is not intended to, constitute legal advice. All

information, content, and materials referenced in this document are for general informational purposes only

and should not be considered legal advice of any kind. Readers of this document should contact an individual

attorney to obtain advice with respect to any particular legal matter related to the New Mexico Tax Code or

any local Lodgers' Tax statutes. No reader or user of this document should act or refrain from acting on the

basis of information contained in the document. Only your individual attorney can provide assurances that

the information contained herein — and your interpretation of it — is applicable or appropriate to your

particular situation. Use of this document, or any of the resources contained herein, does not create an

attorney-client relationship between the reader or user and the NMHA. References are provided for

informational purposes only and are subject to change at the discretion of NMHA. The information contained

in this document is also subject to changes based on legislative action.

Page 2 of 41

Executive Summary:

Hospitality and tourism is a leading economic driver for the State of New Mexico (second only to oil/gas)

contributing $693 million in state and local tax revenue in 2018. Tourism had its largest economic impact in

state history for a seventh straight year, injecting $7.1 billion into New Mexico’s economy and supporting

nearly 102,000 jobs in 2019. 1–in–12 New Mexico jobs are supported by visitor spending and tourism

sustained 8.5% of all jobs in 2018 (source: NMTD Annual Report—2018).

Due to the importance and impact of tourism to New Mexico’s economy, it is critical that tourism funding is

used the way it was intended. To continue to attract visitors to New Mexico, effective marketing and

promotion is necessary. Lodgers’ Tax is a crucial funding mechanism that allows local municipalities to

further promote their destinations and drive visitation to their tourism economies.

The Lodger’s Tax Best Practices Handbook was designed with six stakeholder

groups in mind, with each having an essential role in the collection,

enforcement, and administration of Lodgers’ Tax.

1. Lodging Businesses

2. Local Government

3. Destination Marketing Organization (DMO) /Lodgers’ Tax Administrators

4. Lodgers’ Tax Advisory Boards

5. Event Organizers

6. New Mexico Department of Finance Administration — Local Government Division

Purpose of This Handbook:

This handbook’s’ purpose is to provide best practices, unification, standardization, and an overall framework

on how to best collect, enforce, and administer these funds to grow the tourism economy by providing

guidance and empowering stakeholders and to position tourism leaders to make optimal marketing and

promotion decisions that advance their destinations and the industry.

Furthermore, the state Lodgers’ Tax statute (also referred to as Occupancy Tax) was established in 1969 for

the purpose of allowing municipalities the option to create local Lodgers’ Tax ordinances to collect tax for

the primary purpose of marketing and promoting their destination to tourists. The local ordinances and

administration of the Lodgers’ Tax must be executed within the context of the state statute. Lodgers’ Tax is

an international funding model that has successfully increased tourism and furthered local tourism

economies.

www.newmexicohospitality.org - Lodgers’ Tax Manual Resources – Lodgers’ Tax Statute

Guiding Principles -

1. Sharply focus on the ultimate intent of Lodgers’ Tax which is to grow the tourism economy

2. Grow tourism through promotion and development

3. Increase tourism employment

4. Nurture fiscal stewardship

Page 3 of 41

Hospitality and tourism

contributed

$693 million

in state and local tax

revenue in 2018.

Ski New Mexico

Page 4 of 41

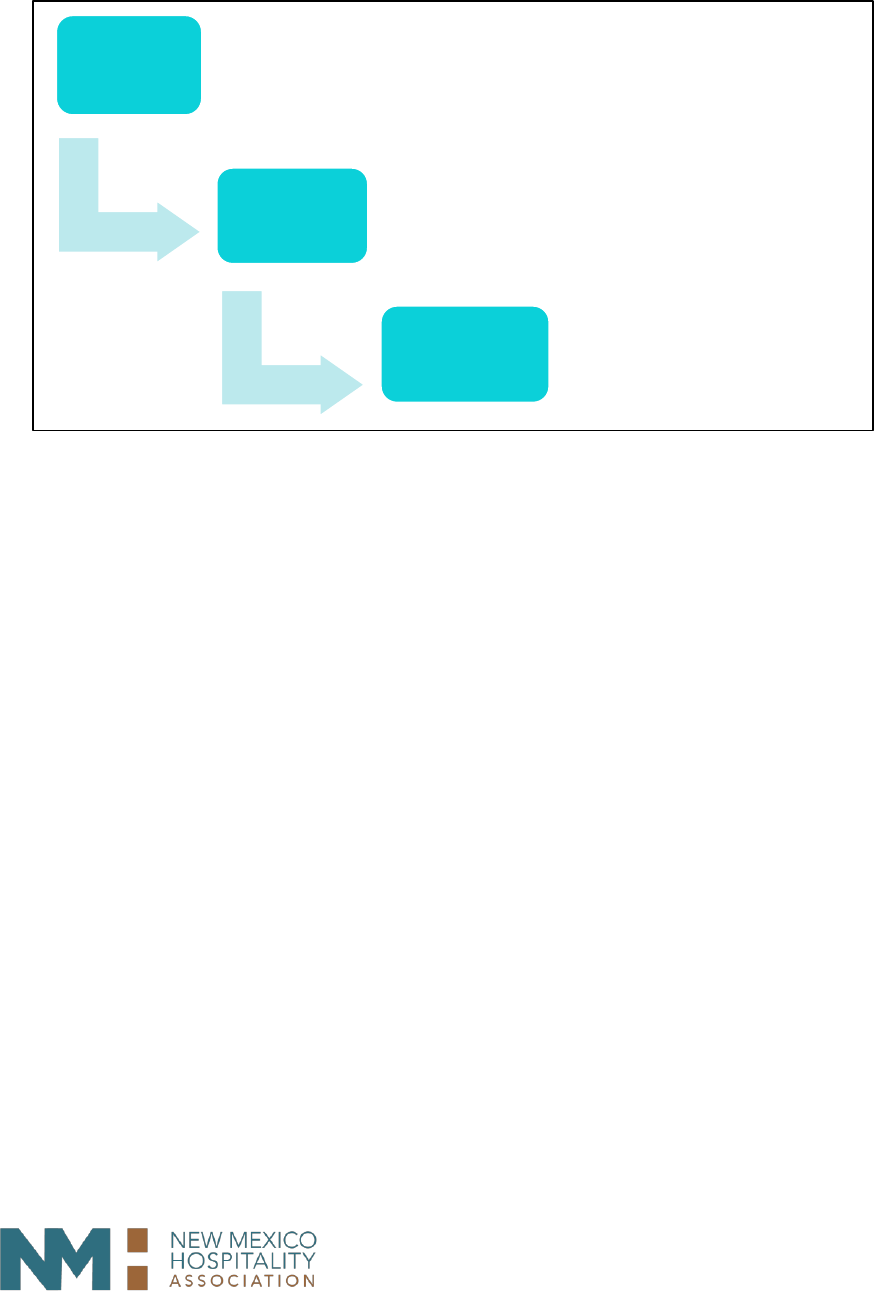

Development Process:

New Mexico Hospitality Association led three phases of development for the Lodgers’ Tax Best Practices

Handbook.

In the fall of 2019, NMHA conducted a survey of statewide municipalities and counties administration of

Lodgers’ Tax. The results clearly illustrated the common challenges throughout the state, and the feedback

from the tourism industry affirmed the need for a comprehensive Lodgers’ Tax resource that addressed the

industry’s needs:

• To establish uniformity and standardization criteria for collection, expenditure, and administrative

practices;

• To compile resources to provide guidance;

• To provide guidance on the technological advancements that have created disrupters and/or altered

the tourism industry as well as the marketing/promotion industry; and

• To provide guidance on the online booking platforms, online marketplace platforms and/or short-

term rental markets, as commonly termed, that are now a major global tourism player. These

properties have historically and largely operated with very little oversight, creating a lack of parity

with traditional lodging businesses.

The remaining information, resources and guidance that follows, aligns with the Path of Lodgers’ Tax Funds

graphic on the next page. This is designed for the purpose of simplicity and flows with the Lodgers’ Tax

statute from a process standpoint.

Phase

One

• Industry Survey

• Industry Roundtables

• Convene Task Force

Phase

Two

• Membership Feedback on Draft

• State and National Stakeholder

Feedback on Draft

Phase

Three

• Membership Approval

• Stakeholder Endorsements

• Publish

Page 5 of 41

Page 6 of 41

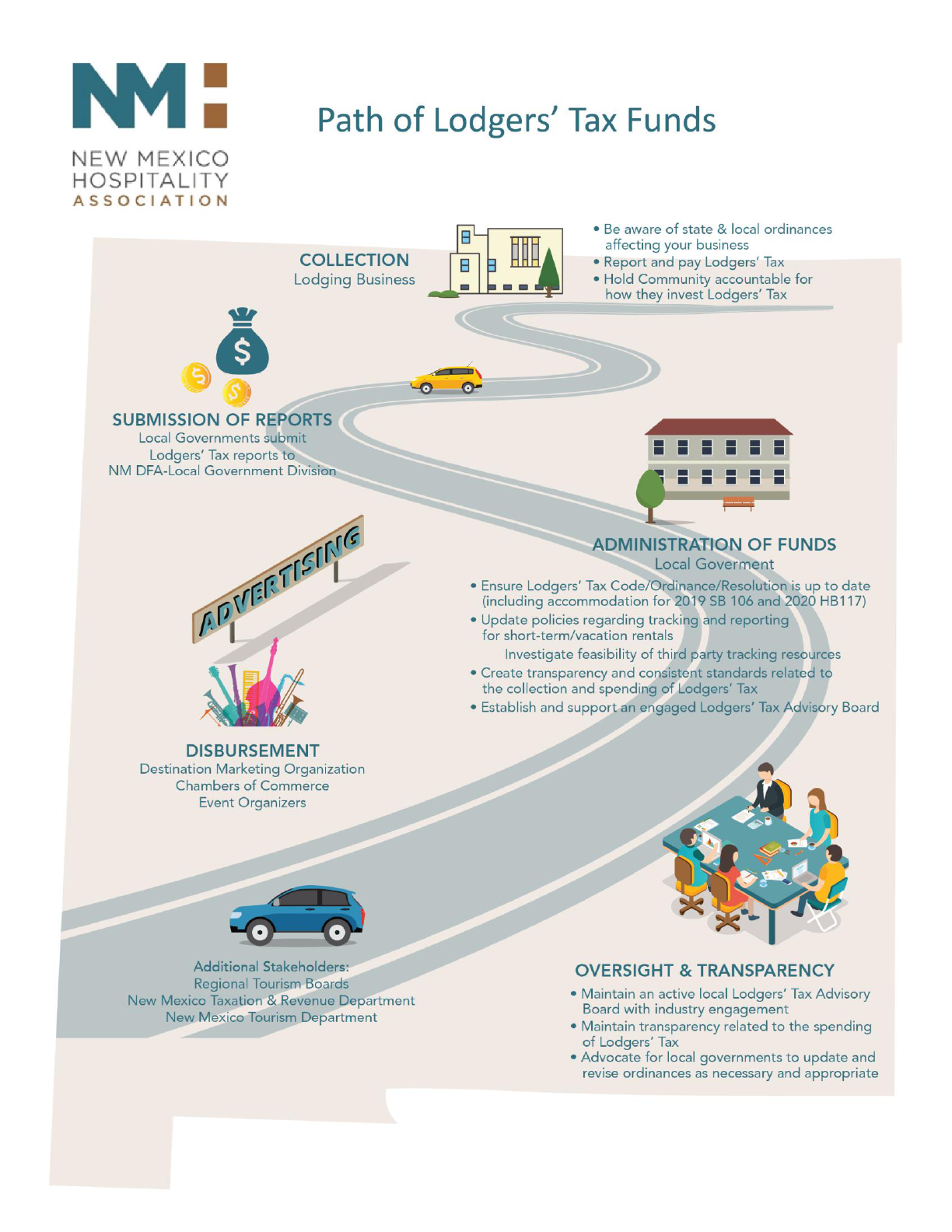

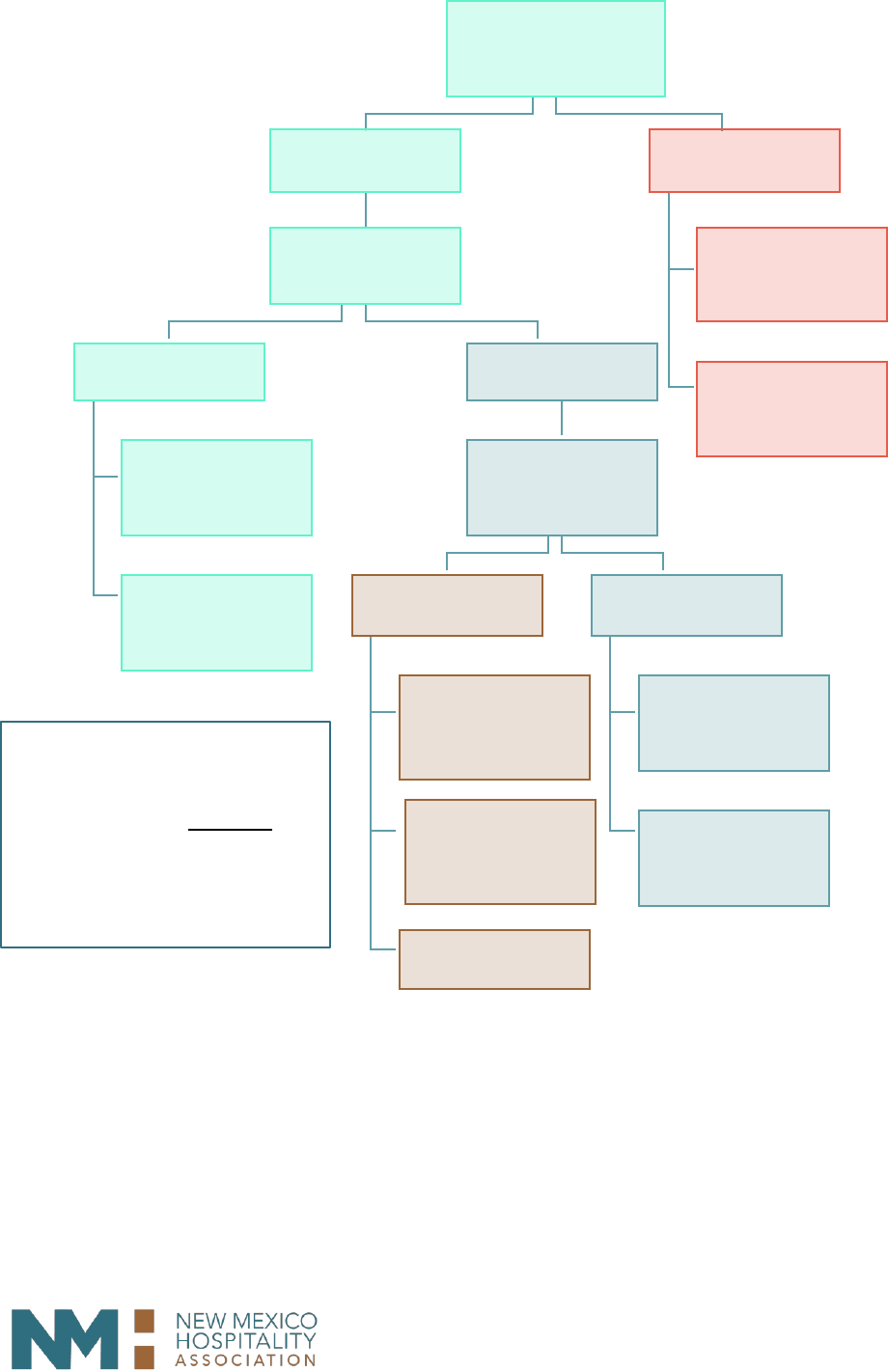

Path of Lodgers’ Tax Funds:

Collection, administration, and enforcement are the three general aspects relating to Lodgers’ Tax and

understanding the various roles of stakeholder groups, lends itself to these best practices.

COLLECTION: Lodging Businesses

Lodging Businesses are entities engaged in providing overnight accommodations and

services to tourists.

• Be aware of state and local ordinances affecting your business.

• Lodger’s Tax is to be collected for each night of a stay of 30 days or less and

on days 1 through 30 of an extended stay.

• Report Lodgers’ Tax to your local Lodgers’ Tax Administrator.

• Be prepared for an annual audit by your local government.

• Make sure the industry is actively represented on the Lodgers’ Tax Advisory Board.

• Hold your community accountable for how they invest Lodgers’ Tax-

▪ Monitor reports and advocate local governments to ensure Lodgers’ Tax is used for

intended purposes and hold municipalities, administrators, and event organizers

accountable for results

SUBMISSION OF REPORTS: New Mexico

Department of Finance Administration —

Local Government Division

Collects and posts Lodgers’ Tax as reported by local municipalities. Reports are due from local governments

to DFA – Local Government Division, within 30 days following the quarter ending report. Example: Fiscal

year Q1 (July-Sept) revenue and expense activity report is due to DFA-LGD by October 31.

http://www.nmdfa.state.nm.us/bfb-forms.aspx

Pursuant to Statute 3-38-15D(2), this formula applies to a municipality not located in a class A county, or a

county which is not a class A county, that is imposing an occupancy tax of more than 2%.

http://www.nmdfa.state.nm.us/County_Classifications.aspx

http://nmdfa.state.nm.us/Financial_Distribution.aspx

Page 7 of 41

GOVERNANCE & ADMINISTRATION OF

FUNDS: Local Governments

For these purposes, Local Governments are defined as elective and appointive

entities and agencies in political geographic areas (counties or municipalities) that regulate and administer

activities engaged in lodging, services, and products provided to tourists. In fiscal year 2018, New Mexico

Lodgers’ Tax was over $53,000,000 according to New Mexico’s Department of Finance Administration —

Local Government Division.

• Every local governing body must ensure their Lodgers’ Tax Code/Ordinance/ Resolution is up to date

with the current Statute.

The local ordinance should include, at minimum:

• Definitions

• Declaration of % to be collected based on the size of the community (See Figure #1)

• Requirements for collecting tax from lodgers

• Requirements for quarterly reporting

• Policy and Procedures on how funds will be used

• Policy and Procedures on how ordinance will be enforced

• Short-term rental platforms are now required to pay Lodgers’ Tax — this is outlined in PART 2.

• In 2019, Senate Bill 106 (SB106) was passed, removing the 3-room exemption and making it easier

for communities to track short-term/vacation rentals and collect applicable taxes.

https://legiscan.com/NM/bill/SB106/2019

• In 2020 House Bill 117 (HB117) was passed, amending the Act to alter certain exemptions and

changing the allowable uses of occupancy tax revenue to allow some communities to extend

Lodgers’ Tax to rentals longer than 30 days. https://legiscan.com/NM/bill/HB117/2020

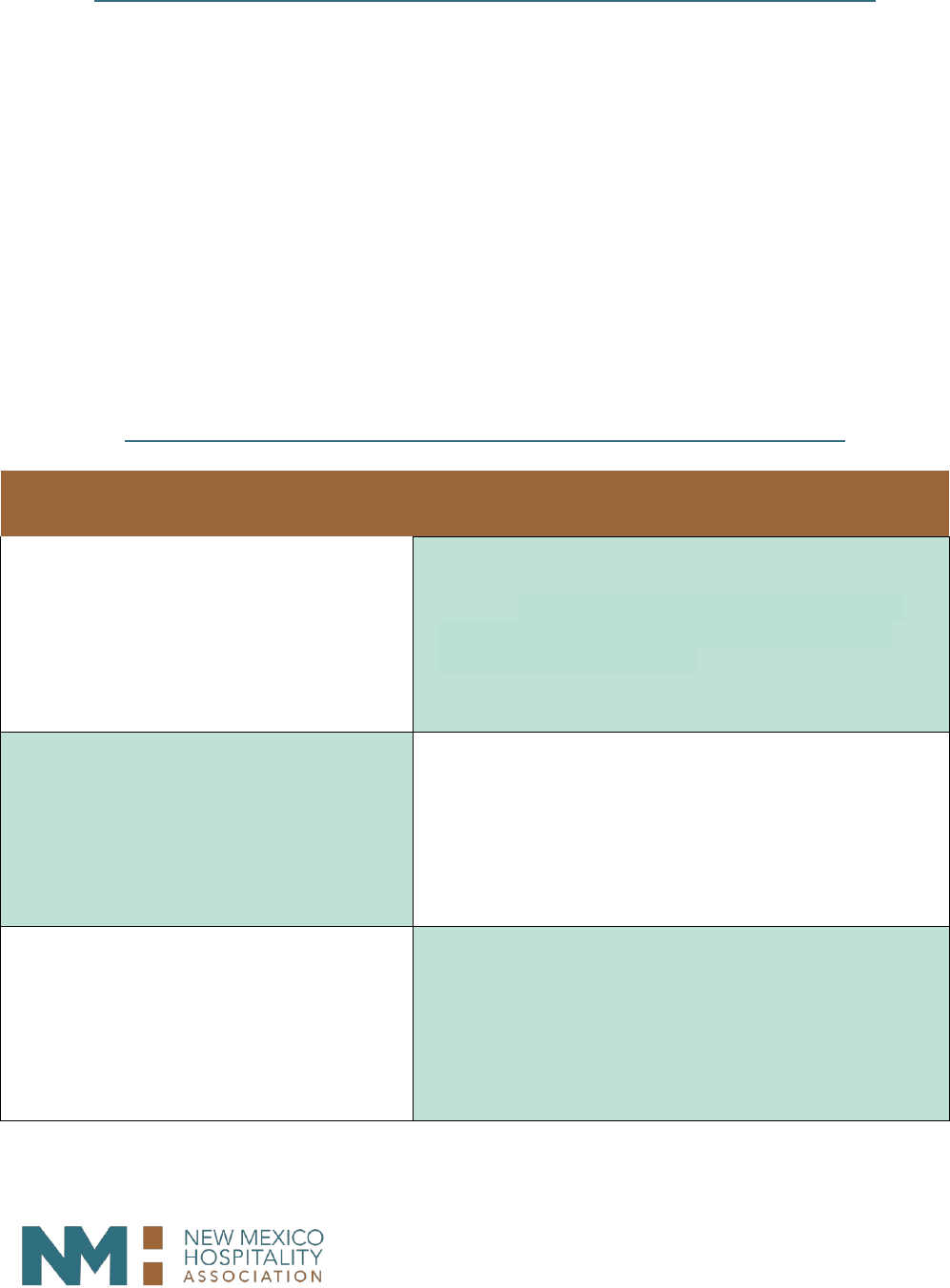

Calculating How Lodgers’ Tax Funds Can Be Spent (Restrictions) -

New Mexico’s Lodgers’ Tax Act has a very specific formula to determine the absolute minimum amount of

Lodgers’ Tax proceeds that must be spent on marketing and promotion. There are other restrictions for the

remaining proceeds; however, all Lodgers’ Tax proceeds must be used with the intent to grow the tourism

economy. This formula is outlined in section 3-38-15-D of the Lodgers’ Tax Act or check here:

https://law.justia.com/codes/new-mexico/2018/chapter-3/article-38/section-3-38-15/

Dependent upon the city’s or county’s classification, there are different requirements for the percent of

funds that must be used for marketing and promotion. To determine a municipality’s restrictions and/or

confirm a city and/or county’s classification see Figure #2. The flowchart illustrates how to calculate the

Lodgers’ Tax restriction rate.

*Examples for all items can be found in the Resource Appendix on Page 37.

Page 8 of 41

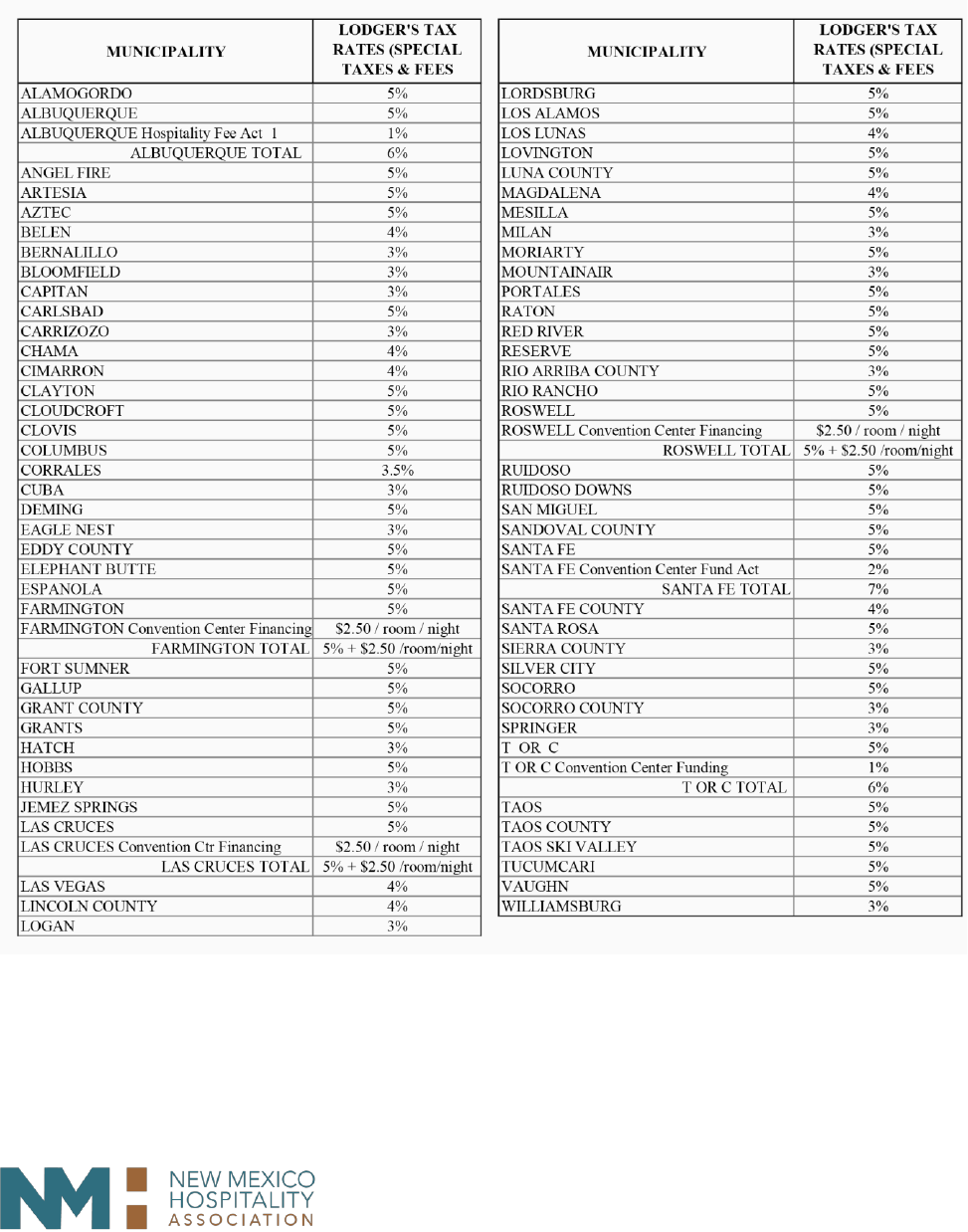

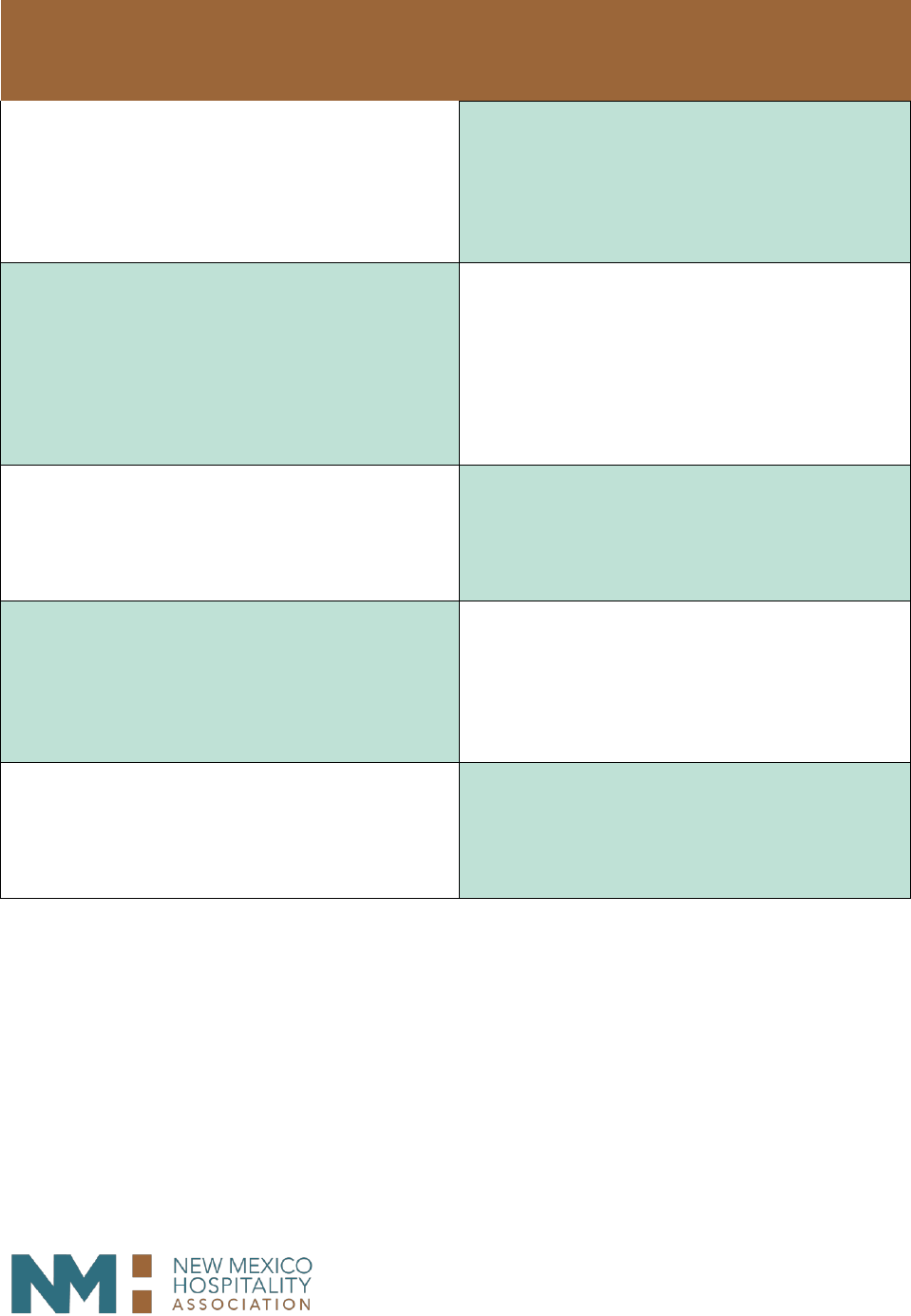

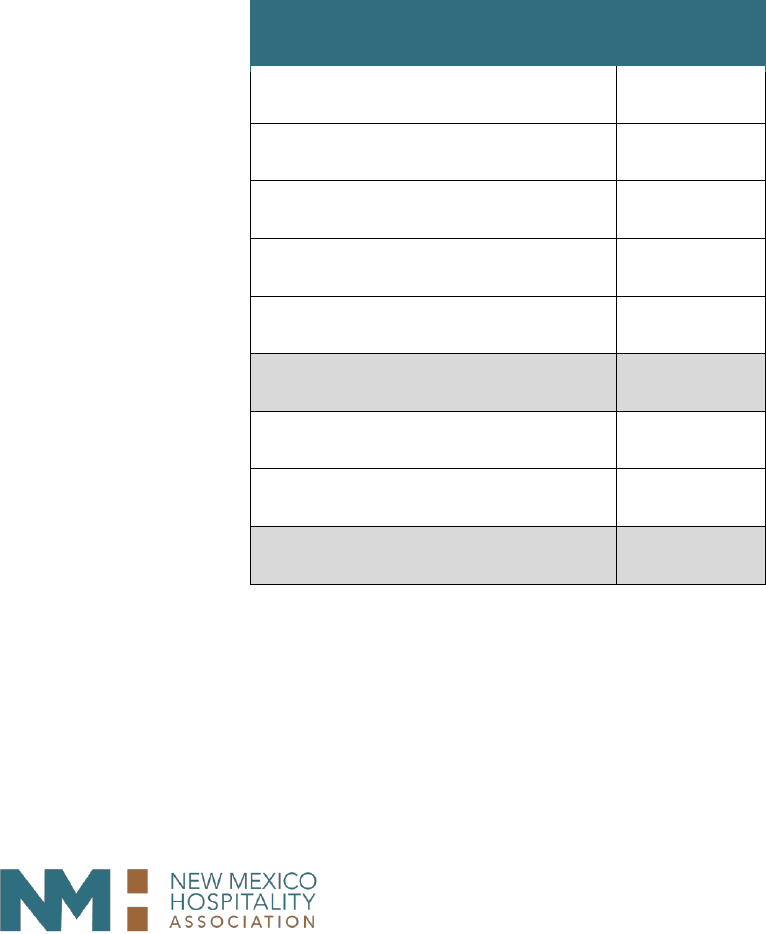

Figure

#

1: Lodgers’ Tax Rates for New Mexico

Municipalities & Counties

Page 9 of 41

Figure #2: Lodgers’ Tax Restriction Rate Formula and Flowchart

After calculating the absolute minimum amount of Lodgers’ Tax proceeds that must be spent on marketing

and promotion, it is important to note that spending as much Lodgers’ Tax funds as possible on marketing

and promotion is most beneficial to grow tourism, increase visitation, increase visitor spend and create jobs.

Sunrise Springs Spa Resort

Is the tax rate

more than 2%?

Yes

Class A County?

Yes

At least 1/2 of

proceeds must be

for marketing.

$100,000*1/2 =

$50,000

No

Is the tax rate

more than 3%?

Yes

At least 1/2 of

proceeds of 1st

3% must be for

marketing.

At least 1/4 of

proceeds in excess of

3% must be for

marketing.

See "the formula"

No

At least 1/2 of

proceeds must be

for marketing.

$100,000 * 1/2 =

$50,000

No

At least 1/4 of

proceeds must be

for marketing.

$100,000*1/4 =

$25,000

FORMULA: [(3% / tax rate) *

proceeds] * ½ + [(tax rate – 3%)

* proceeds * ¼] = minimum

amount of lodgers’ tax proceeds

to be spent on

marketing/promotion.

Page 10 of 41

Other Allowable Uses of Lodgers’ Tax Proceeds -

The statute recognizes that there are costs associated with the collection, administration, and management

of the Lodgers’ Tax process as well as the creation and maintenance of the tourism infrastructure.

Accordingly, subject to the limitations contained in Section 3-38-15 NMSA 1978 a municipality or county

imposing a Lodgers’ Tax may, once the required minimum amount of Lodgers’ Tax proceeds that must be

spent on marketing and promotion has been met, use the proceeds from Lodgers’ Tax to defray costs of:

https://law.justia.com/codes/new-mexico/2018/chapter-3/article-38/section-3-38-15/

• Collecting and otherwise administering the occupancy tax, including the performance of audits

required by the Lodgers’ Tax Act pursuant to guidelines issued by the Department of Finance &

Administration – Local Government Division;

• Establishing, operating, purchasing, constructing, otherwise acquiring, reconstructing, extending,

improving, equipping, furnishing or acquiring real property or any interest in real property for the

site or grounds for tourist-related facilities and attractions or tourist-related transportation systems

of the municipality or the county in which the municipality is located;

• The principal of and interest on any prior redemption premiums due in connection with and any

other charges pertaining to revenue bonds authorized by Section 3-38-23 or 3-38-24 NMSA 1978

https://law.justia.com/codes/new-mexico/2011/chapter3/article38/section3-38-23/

https://law.justia.com/codes/new-mexico/2011/chapter3/article38/section3/38-24/

• Providing police and fire protection and sanitation service for tourist-related facilities, attractions

and events located in the respective municipality or county;

• Providing a required minimum revenue guarantee for air service to the municipality or county to

increase the ability of tourists to easily access the municipality's or county's tourist-related facilities,

attractions and events; or

• Contracting for the management of programs and activities funded with revenue from the Lodgers’

Tax (Section 3-38-21 NMSA 1978 - https://law.justia.com/codes/new-mexico/2006/nmrc/jd_3-38-

21-26ab.html). Funds provided to the contracting person or governmental agency shall be

maintained in a separate account established for that purpose and shall not be commingled with

any other money. The contractor may spend Lodgers’ Tax funds on day-to-day operations, supplies,

salaries, office rental, travel expenses and other administrative costs only if those administrative

costs are incurred directly for the purpose of managing the programs and activities funded with

revenue from the Lodgers’ Tax.

• Any combination of the foregoing purposes or transactions stated in this section, but for no other

municipal or county purpose.

Page 11 of 41

Exemptions (Cannot Tax) -

The Lodgers’ Tax does not apply in the following situations:

• If a renter/vendee is using the premises as their permanent residence of over thirty (30) days and has

entered into a written agreement for use of the taxable premises;

• If the rent paid by a vendee is less than two dollars ($2.00) per day;

• Lodging accommodations at institutions of the federal government, the state or any political subdivision

thereof;

• Lodging accommodations at religious, charitable, educational or philanthropic institutions, including

accommodations at summer camps operated by such institutions;

• Clinics, hospitals or other medical facilities; or

• Privately owned and operated convalescent homes or homes for the aged, infirm, indigent or chronically

ill.

Vendor & Municipality Accountability:

Vendor Accountability –

Per the Lodgers’ Tax Statute, every vendor providing lodging within a county or municipality that imposes a

lodgers’ tax is responsible for collecting and reporting that tax. If the county or municipality collects more

than $250,000 in lodgers’ tax revenue, the governing body must conduct random audits of vendors to

confirm compliance. The audit requirements are to be outlined in the local Lodgers’ Tax ordinance (3.38.20)

and should specify:

• the times, place and method for the payment of the occupancy tax proceeds to the municipality or

county;

• the accounts and other records to be maintained in connection with the occupancy tax;

• a procedure for making refunds and resolving disputes relating to the occupancy tax, including

exemptions pertaining thereto;

• the procedure for preservation and destruction of records and their inspection and investigation;

• vendor audit requirements;

• applicable civil and criminal penalties; and

• a procedure of liens, distraint and sales to satisfy such liens.

https://codes.findlaw.com/nm/chapter-3-municipalities/nm-st-sect-3-38-20.html

*Note: Most local ordinances include confidentiality language regarding the results of Lodgers’ Tax Audits.

( Sample language — It is unlawful for any employee of the City to reveal to any individual, other than

another employee of the City, any information contained in the return or audit of any taxpayer, including

vendors subject to the Lodgers' Tax Act, except to a court of competent jurisdiction in response to an order

thereof in an action related to taxes to which the City is a party, and in which information sought is material

to the inquiry; to the taxpayer himself or to his authorized representative; and in such manner, for statistical

purpose, the information revealed is not identified as applicable to any individual taxpayer.)

Page 12 of 41

Municipality Accountability –

As previously mentioned, every municipality is required to file Lodgers’ Tax reports with DFA – Local

Government Division. Lodgers’ Tax Reports can be accessed at:

http://www.nmdfa.state.nm.us/Financial_Distribution.aspx

Every municipality is also required to have an annual audit. The Office of the State Auditor in accordance

with the Audit Act, §§12-6-1 to 12-6-14, NMSA 1978, is tasked with thoroughly examining and

auditing the financial affairs of every agency and political subdivision of the state that receives or expends

public money from whatever source derived, including counties and municipalities.

Annual audit reports can be viewed at: https://www.saonm.org/auditing/audit-report-search/

Moreover, the Office of the State Auditor maintains a hotline that allows the public to report allegations

financial fraud, waste or abuse. This tool allows individuals to report 24 hours a day, seven

days a week either on the record or anonymously. Reports may be made through

https://secure.ethicspoint.com/domain/media/en/gui/58852/index.html or by calling 1-866-OSA-FRAUD

(1-866-672-3728).

OVERSIGHT & TRANSPARENCY:

Lodgers’ Tax Advisory Boards

As outlined in the Lodgers’ Tax Act [3-38-13 through 3-38-24 NMSA 1978], the

mayor or county commission chair of every municipality or county that

imposes an occupancy tax shall appoint a five-member advisory board that

consists of:

• Two members who are owners or operators of lodgings subject to

the Occupancy Tax within the municipality or county,

• Two members who are owners or operators of industries located within the municipality or county

that primarily provide services or products to tourists; and

• One member who is a resident of the municipality and represents the general public.

The advisory board’s Involvement may vary depending on the nature of each community or county tourism

management structure; however typically the advisory board shall:

• Advise the respective governing bodies on the expenditure of funds authorized by Section 3-38-15

NMSA 1978 for advertising, publicizing and promoting tourist attractions and facilities in the

respective counties and municipalities; and

• Submit to the mayor and council or county commission recommendations for the expenditures of

funds authorized pursuant to the Lodgers’ Tax Act for advertising, publicizing and promoting tourist-

related attractions, facilities and events in the respective counties and municipalities.

Lodgers’ Tax Advisory Boards are subject to the New Mexico Open Meetings Act:

https://www.nmag.gov/uploads/files/Publications/ComplianceGuides/Open%20Meetings%20Act%20Co

mpliance%20Guide%202015.pdf

Page 13 of 41

For detailed information on a municipality’s Lodgers’ Tax Advisory Board, you can research the codified

ordinances for that particular community or county — the clerk, general counsel or executive leadership of

the community or county are also good resources.

DISBURSEMENT:

Lodgers’ Tax Administrators

Destination Marketing Organizations (DMO) (sometimes known as Convention Visitors

Bureaus or CVBs) promote the long-term development and marketing of the destination,

serving those attractions and activities of tourist related services and products for the

purpose of driving visitation to that destination. Chambers of Commerce in communities without a DMO or

CVB, may serve in that capacity as might Event Organizers contracted to organize, promote and operate

fairs, festivals, meetings and conferences and other group events which draw visitors and tourism to the

destination.

BEST PRACTICE: Industry Statistics to Always

Have on Hand

Knowing that differing interpretations of existing law and/or a lack of awareness of Lodgers’ Tax

requirements can occur when new leadership comes on board, which can be new elected officials, new

Lodgers’ Tax Advisory Board members, or a new Municipal Administrator, it is important to be proactive in

educating and communicating the value, importance, process and policy — data and statistics are effective

talking points and can be used to gain support. Consider having on hand current information specific to the

community or county that highlights areas such as:

• the economic impact of the hotel/tourism industry on the State's economy and on your specific city

or region;

• employment numbers by the visitor industry-hotels, restaurants, bars, retail, transportation,

amusement and recreation sectors;

• where visitors stay (with friends and relatives, in short- term rentals, at hotels, in apartments, etc.)

• what visitors spend on transportation, retail, lodging, meals, etc.;

• occupancy, average daily rate, and actual demand history for your community;

• any other numerical support for the statistics from other credible sources; and

• portray this information on a pie chart to show that there are many others and larger beneficiaries

of the tourist dollar

DISBURSEMENT: Determination of Applicable

Use & Funding Requests

While all Lodgers’ Tax funds are intended to support tourism growth with an emphasis on increasing

day trips and marketable overnight visits, there is a portion of the proceeds that are

required

to be

used to specifically

advertise, publicize and promote tourist-related attractions, facilities and events

which is calculated using the provided formula on page 9. The remaining funds may be utilized for

$$$

Page 14 of 41

several tourism related expenditures with the intent to increase Day Trips and Marketable Overnight

Trips.

https://codes.findlaw.com/nm/chapter-3-municipalities/nm-st-sect-3-38-15.html

STEP ONE: Understand the use provisions:

Component #1: Define “tourism related events”

“Tourism-related events” means events that are

planned for, promoted to and attended by tourists

(3-38-14.I).

https://codes.findlaw.com/nm/chapter-3-municipalities/nm-st-sect-3-38-14.html

Component #2: Define the term ‘tourist.’

“Tourist” means a person who travels for the purpose of business, pleasure or culture to a municipality

or county imposing an occupancy tax (3-38-14.H).

https://codes.findlaw.com/nm/chapter-3-municipalities/nm-st-sect-3-38-14.html

•

The key word is travel and New Mexico Tourism Department best practices define a tourist as “one

that travels *60 miles or more from their residence”

*Note that 60 miles is the preferred standard, but in rural New Mexico that is not always

applicable.

Component #3:

Define “planned for, promoted to, and attended by”

•

The term

“planned for”

suggests that the event must be specifically produced with the intent to

attract tourists. This component of the definition will quickly disqualify many events that are

produced for the citizens of a municipality.

•

The term

“promoted to”

suggests that the event must be promoted specifically to tourists. To be

considered a tourist, a person must travel for the purpose of business, pleasure or culture;

therefore, the event must be promoted outside of the given municipality where the event is to be

located, which means the media purchased must target media markets outside of the municipality.

Best practices suggest that the event should be promoted outside at least a 60-mile radius.

•

The term

“attended by”

suggests that tourists must actually be at the event to qualify as a tourism-

related event. It is critical to track where event attendees are from so event planners and Lodgers’

Tax administrators know if tourists actually attended the event.

Component #4: Statutory Definition of “tourism-related facilities and attractions”

“tourist-related facilities and attractions” means facilities and attractions that are intended to be used by

or visited by tourists (3-38-14.J)

https://codes.findlaw.com/nm/chapter-3-municipalities/nm-st-sect-3-38-14.html

Common examples include natural and cultural sites, historical places, monuments, zoos and game

reserves, aquaria, museums and art galleries, gardens, architectural structures, theme parks, sports

facilities, festivals and events, and wildlife.

Page 15 of 41

STEP TWO: Understand other definitions for use provisions

While the Lodgers’ Tax Statute does not define all terms and terminology, it is important to utilize standard

definitions when evaluating Lodgers’ Tax requests and determining the use of Lodgers’ Tax funds. Some

standard terms include:

• Marketing

• Advertising

• Publicizing

• Promotion

• Marketable Overnight Trips

These terms are defined in the Definitions Section beginning on Page 34. (Definition Sources: American

Marketing Association, US Travel Association, UNWTO – United Nations World Tourism Organization).

STEP THREE: Develop a strategic process for funds use

TIPS

Identify ways for the project to produce

or convert visitation into “heads in

beds”. Include or request a plan that sets

a goal to ensure a percentage of visitors

stay at lodging properties that collect

lodgers’ tax

Consider the development of a community marketing

strategy or tourism development strategy so that all

requests roll up to the overall goals and objectives.

Consider involving the lodging properties

for rate and occupancy benefits during

shoulder or peak seasons.

Identify and require each project to outline the priority

to reach visitors in specific markets and that the

approach meets the 60-mile radius threshold

Identify the planned promotional

activities (type of media, geographic

reach of media, special publications)

Leverage additional community support that meets the

projects needs while at the same time pledges a

portion of lodgers’ tax funds (in-kind,

business/corporate support, etc.)

Page 16 of 41

Present information in a consistent

fashion — ensure data listed in one area

of an application matches other

references

Consider hosting a workshop to explain lodgers’ tax as

an economic driver to stakeholders and lodgers’ tax

fund requestors so they understand the standardized

process. Other workshops can be held to educate on

who should be paying lodgers’ tax and what it does.

Establish methods for tracking

attendance, lodging, and other data.

(Samples are provided in the Resource

Appendix)

Make sure the economic impact figures are accurate

and have data to reinforce. Develop or utilize an

impact analysis sheet.

(A sample is provided in the Resource Appendix)

Establish methods to evaluate program

success to quantify and quality Return on

Investment (ROI) and/or Economic

Impact.

Make sure you demonstrate how your project serves

the community brand

Page 17 of 41

STEP FOUR: Consider these Statutory Requirements and Best

Practice Recommendations

Visitors’

Centers

Debt service for

convention

centers

Marketing and/or

operations of

convention centers

Event

Centers

Advertising, publicizing, and

promoting events, facilities,

and tourist attractions that

draw visitors from at least a

60 mile radius; acquiring,

constructing, and

maintaining tourist

attractions and recreational

facilities

Destination Marketing

Organizations and/or

Chambers of

Commerce

Expenses related to

the administration of

Lodgers’ Tax funds

Special use

allocations for

marketing

Cultural facilities,

nonprofits,

cultural arts

Special Events that

place “heads in

beds”

Transit, solid waste,

police and fire safety

overtime in support of

tourism activity

Page 18 of 41

Acceptable Advertising Uses of

Lodgers Tax

Alternative Uses

A wine festival that promotes the event to

the defined tourist and is attended by

the defined tourist (outside a 60-mile radius).

Utilization of Lodgers’ Tax to sponsor a Wedding

Expo where hotels and other wedding vendors

participate in a trade show and the local

community attends to seek out their favorite

vendors for their upcoming wedding.

A marketing campaign to promote a

community asset or event, with a direct focus

on a specific drive or fly market audience, that

has an overnight stay (or multiple) component,

and an ancillary spend component.

A marketing campaign for niche print

publications or to enthusiasts, such as RV’ers,

to visit a destination or attend an event that

does is either not a high valued traveler,

and/or does not have a conversion factor:

overnight lodging

Print, digital, social, and out of home media

uses. Media buy in a targeted drive market in

another state. The media buy is to promote

destination (i.e. street car wrap, trolley signage)

A marketing or promotion campaign touting

assets that limits the travelers experience to only

a day trip.

Travel and Adventure Tradeshow branded booth

signage or shows in target market that consumers

are attending. The ROI is brand impressions.

An event, attraction or product in which the

marketing, promotion or advertising is not

beyond the 60-mile radius, which generates a

better ROI of new /increased visitors and

new/increased spend.

Targeted ads in multimedia platform for a

seasonal event during shoulder season that is

focused on overnight or multiple night stays

(“heads in beds”)

Design and production of a banner, sign, or

product that does not drive the consumer to a

call to action like ancillary spend or overnight or

multiple night stay.

Page 19 of 41

DISBURSEMENT: Measure the Return on Investment

(ROI) and Economic Impact

Tourism generates, directly and indirectly, an increase in economic activity of the places visited (and

beyond), mainly due to demand for goods and services produced and provided at the destination. Tourism’s

direct impacts are measured in “economic contribution”. The following graphic provides a visual roadmap:

Page 20 of 41

Lodgers’ Tax is shared by both lodging providers and their guests. Maintaining a competitive overall travel

tax rate is essential for tourism growth and development.

Leveraging the current momentum and making every potential marketing dollar work harder and smarter is

imperative. Lodgers’ Tax is a powerful marketing and promotion funding mechanism that can drive

economic vibrancy in local communities. Every community has a vested interest and responsibility to

safeguard their Lodgers’ Tax fund and work tirelessly to make this fund achieve its full potential. All Lodgers’

Tax stakeholder groups have a deep obligation to each other, to their community and their fellow New

Mexicans; someone’s job depends on it.

Marketing Return on Investment (MROI):

Understanding of MROI (marketing return on investment, aka ROMI or return on marketing investment) in a

general sense would be beneficial. There are various tools that provide either a flat metric/algorithm that

can be applied to any kind of marketing spend and there are those that can quantify something that is

channel-specific (like how TV broadcast metrics are different from social-media marketing metrics).

Following are a few universal resources to understand the importance of calculating, measuring and

evaluating the effectiveness of marketing spend.

• New Mexico Tourism Dept Co-Op Marketing Grant Program builds a community’s marketing

capability through media consultations and technical assistance that provides measurable results

and performance reporting to demonstrate the impact to your destination, attraction or event.

https://www.newmexico.org/industry/work-together/grants/co-op-marketing/

• Harvard Business Review:

• https://hbr.org/2017/07/a-refresher-on-marketing-roi

• A white paper from Deloitte:

https://www2.deloitte.com/content/dam/Deloitte/us/Documents/CMO/cmo-mroi-defined.pdf

Return on Investment:

Return on Investment (ROI) research is key to understanding the effects of tourism marketing on visitor

spending and demand. Return on investment in tourism measures the direct impact of specific marketing

materials on consumers’ decisions to visit a particular destination. In most ROI studies, travelers who would

have visited a destination without marketing (ie, repeat visitors, travelers visiting friends and family, and

business travelers) are excluded from the sample, leaving only persuadable consumers. These consumers

are then asked to recall specific marketing and to provide data on their travel habits. When this sample is

extrapolated to the population level, an estimate of directly influenced trips and spending can be

established. This allows destination marketing organizations to determine what kinds of advertisements

work best with which populations, allowing for a smarter expenditure of funds and ultimately a more

efficient marketing campaign with a greater return in trips and spending.

Page 21 of 41

Economic Analysis:

As mentioned before, tourism generates economic activity directly, indirectly and through induced means

in the places visited (and beyond), mainly due to demand for goods and services that needs to be

produced and provided. In the economic analysis of tourism, one may distinguish between tourism’s

‘economic contribution’ which refers to the direct effect of tourism and is measurable and tourism’s

‘economic impact’ which is a much broader concept encapsulating the direct, indirect and induced

financial effects of tourism and which must be estimated by applying models. Economic impact studies

aim to quantify economic benefits, that is, the net increase in the wealth of residents resulting from

tourism, measured in monetary terms, over and above the levels that would exist in its absence.

Economic analysis allows communities to understand the specific contributions of visitor spending

compared to local resident spending. This can provide communities with an understanding of where

tourism dollars are going and how money flows through local economies, allowing for targeted economic

development. Economic analysis can also serve as a tool for advocacy, both for improving resident

sentiment and for allocation of funding.

Examples for ROI, Economic Impact Analysis and Report Types are in the Resource Guide on Page 37 and at

www.newmexicohospitality.org – Lodgers’ Tax Resources – Economic Impact Tools

Additional Stakeholders:

• Regional Tourism Boards: Six regional marketing boards created by the NM Tourism Department

charged with monitoring and coordinating local and regional marketing efforts to support and

enhance the department’s mission to drive visitation to the state

https://www.newmexico.org/industry/work-together/partnership-opportunities/regional-

marketing-boards/

• New Mexico Taxation & Revenue Department: As of July 1, 2019, online sales and marketplace

services are subject to New Mexico Gross Receipts Tax. For more information, go to:

http://www.tax.newmexico.gov/

• New Mexico Tourism Department: Municipalities and events can expand the impact of their

Lodgers’ Tax dollars through collaboration with the Tourism Department through the New Mexico

True Co-Op Marketing Program. For more information, go to: https://www.newmexico.org

Page 22 of 41

Additional Tourism Development

Financing Mechanisms:

Currently, twelve counties and sixty-two cities impose Lodgers’ Tax in New Mexico, and there are six (6)

special hospitality or convention fees.

HOSPITALITY FEE – Albuquerque (3-38A-1 through 3-38A-12 -https://law.justia.com/codes/new-

mexico/2013/chapter-3/article-38a/ )

CONVENTION CENTER FINANCING ACT – Las Cruces, Farmington, Roswell, Truth or Consequences (3-38A-1

through 3-38A12 - https://law.justia.com/codes/new-mexico/2013/chapter-3/article-38a/ )

CONFERENCE & CONVENTION CENTER FINANCING ACT – Santa Fe (5-14-1 through 5-14-15 -

https://law.justia.com/codes/new-mexico/2006/nmrc/jd_5-14-1-3b45.html )

TAX INCREMENT DEVELOPMENT DISTRICTS (TIDD) – Mechanisms to support economic development and

job creation by providing gross receipts tax financing and property tax financing for public infrastructure -

Sections 5-15-2 NMSA 1978 - https://law.justia.com/codes/new-mexico/2006/nmrc/jd_5-15-2-3b85.html

Page 23 of 41

Short-term rental platforms

are now required to pay

Lodgers’ Tax.

The industry must continue to monitor new

entrants into the hospitality arena and ensure

that statues and policies adapt to maintain level

playing fields and ensure that tax revenue is

collected. An updated report on the impact of

short-term rentals in New Mexico is available at

www.newmexicohospitality.org

Pecos River Cabins

Page 24 of 41

PART 2 -

Overview of the Short-term Rental Market:

Local governments across the state are focused on finding ways to manage the rapid growth of home-

sharing and short-term rental properties in their communities This involves balancing the rights of private

citizens to generate revenue with the impact on the surrounding communities and ensuring parity between

private lodging options and the traditional lodging community.

It is apparent that this market disruptor generates both positive and negative aspects for a community;

however, it’s imperative that local governments adopt sensible and enforceable regulation that maintain

level playing fields and ensure tax revenue is collected. The industry must continue to monitor new entrants

into the hospitality arena and ensure that statues and policies adapt.

Short-term rental platforms are now required to pay Lodgers’ Tax. In 2019, Senate Bill 106 was passed

removing the 3-room exemption and making it easier for communities to track short-term/vacation rentals

and collect applicable taxes. https://legiscan.com/NM/text/SB106/2019

At times when a community or state is faced with a declining revenue base, sources of revenue from non-

voters (i.e. visitors) will be as popular as ever. Due to the importance and impact of tourism to New

Mexico’s economy, it is critical that tourism funding is used the way it was intended — to continue to attract

visitors to New Mexico and grow the tourism economy. Marketing and promotion is a necessity for that and

everyone benefits from an economically healthy and attractive tourism industry.

Short-term Rental Impact in New Mexico:

With recent technology disruptions and online booking agents, the short-term rental market is

now a major global tourism player. These properties largely operate in the dark without collecting tax (Gross

Receipts Tax and Lodgers’ Tax) or complying with public safety regulations and licensing. As a best practice,

research was needed to establish a baseline and provide guidance for the policy development.

The New Mexico Hospitality Association updated an audit and fiscal impact analysis of short-term rentals in

the State of New Mexico that was previously conducted in 2017 (research compiled in December 2016). The

purpose of the update was to identify the number of active short-term rentals in the state, compare the

2019 market to the 2017 short-term rental market, and identify the additional estimated revenue that will

be generated since the loophole exempting rental units with three rooms or less is no longer in effect as of

January 1, 2020.

• The scope of the audit included every community and county in New Mexico and the purpose was

to identify the number of active short-term rental properties and the potential gross receipts and

lodgers’ taxes that could be generated from these properties.

• In 2017, Southwest Planning and Marketing identified a total 4,076 of short-term rental properties,

of which 3,587 were taxable (after removal of the 3-room exemption).

• As of December 2019, the number of short-term rentals is estimated to be 5,659, all of which will be

taxable beginning on January 1, 2020. If the exemption had not been removed, the total estimated

number of taxable properties would have been 4,981.

• Please note that there is currently no way to capture all short-term rentals, so all numbers related to

this issue are conservative estimates.

Page 25 of 41

Using an average annual conservative occupancy scenario for short-term rentals of 40% to determine the

estimated fiscal impact of short-term rentals as of January 1, 2020 resulted in an estimated $7.1 million

generated annually in lodgers’ tax to communities and counties and $11.5 million generated annually in

gross receipts tax (GRT) (total estimated taxes of $18.6 million).

For contrast purposes, had the 3-room exemption not been removed, just $6.0 million would be generated

in lodgers’ tax and $9.8 million in GRT (total estimated taxes of $15.9 million) from these short-term rentals.

Findings:

5,659 total active short-term rentals were identified and an estimated total of 12,008 active available short-

term rental room nights were for rent in New Mexico as of December 2019. Average room rates, average

number of bedrooms per property, individual property gross receipts tax (GRT), and individual property

lodgers’ tax rates were used to determine the potential revenue generated in New Mexico from short-term

rentals. Assuming all rooms are occupied 100% of the time, total potential estimated tax revenue generated

from these short-term rentals effective January 1, 2020 is $46.5 million based on a total estimated gross

revenue of $354.0 million.

All Properties – 100% Occupancy

Number of Properties

5,659

Average Number of Bedrooms

2.1

Number of Bedrooms

12,008

Available Room Nights (365 days)

4,383,054

Average Statewide Rate per Room

$81

Total Revenue

$353,965,007

Lodger's Tax (Avg. 5.0%)

$17,658,127

GRT (Avg. 8.2%)

$28,856,374

Total Taxes Generated

$46,514,501

Page 26 of 41

Creating Effective Short-term Rental Policies:

Many communities in NM are developing stand alone or separate policies and procedures for this platform

and an increasing number of municipalities are looking for the best way to regulate short-term rentals. Each

community must design a regulation and oversight system that works for their needs.

Part 1 of this handbook outlines the process within the Lodgers’ Tax Act for compliance, enforcement and

administration of Lodger’s Tax. As such, that material remains relevant in this platform and can be

duplicated with the same steps for the Short-term Rental policy and process.

Guiding Principles -

1. Sharply focus on the ultimate intent of Lodgers’ Tax to grow the tourism economy

2. Grow tourism through promotion and development

3. Increase tourism employment

4. Nurture fiscal stewardship

5. Ensure that short-term rentals are taxed in the same way as traditional lodging providers to ensure a

level playing field

6. Develop policy and procedures that minimize public safety risks, noise, trash, zoning, parking, and

affordable housing concerns often associated with short-term rentals

Assess the Situation:

The Resource Appendix will include examples from various New Mexico communities, specific to this

platform. Before beginning the formal process, it is prudent to evaluate the situation within your

community to effectively implement the policy and to monitor, enforce and administer this evolving market

for Lodgers’ Tax revenue purposes:

• Are you enforcing laws already on the books?

• Has your community or county expressed an interest in implementing solutions that do not

overly regulate businesses — what are those collective suggestions?

• What is the economic impact to the municipality from rental activity (lodging tax revenue,

rental and restaurant activity, attractions, direct jobs, related service jobs, home service

providers, landscapers, realtors, professional services, etc.)?

• What is the impact on property values?

• What is the cost of monitoring/enforcement?

If the economic impact from rental activity in your community or county has

not been measured, this is the most responsible place to start. Regulating

activity without understanding the adverse consequences can result in legal

challenges/lawsuits and high non-compliance rates. Studies can be

commissioned by service providers in this arena.

Page 27 of 41

• What kind of short-term rental activity do you have?

• What is your current planning strategy for the activity in the community or county?

• If there are complaints from residents regarding existing short-term rentals, which type of

short-term rental is causing the most issues or complaints? And what types of complaints

are you receiving? How many?

• Can any of the identified problems be resolved by working directly with

owners/management without new ordinances/regulations? If facing complaints from

constituents, how many formal complaints are there? Have you engaged the police

department/zoning/other departments in identifying responses to complaints?

Start with Explicit Policy Objectives:

• There is no “one size fits all” approach that will work for all communities. Local regulations should

be adopted to fit the local circumstances in a practical and cost-effective manner.

• Once clear and concrete policy objectives have been formulated, take the time to understand what

information can be used for code enforcement purposes, in a cost-effective manner.

• Consider policy objectives that factor in community or county aspects, like for an urban community

with a shortage of affordable housing, or for an area with ample housing availability and a struggling

downtown, as examples.

• Ensure your community or county has the budget, monitoring systems, and workforce to monitor

and enforce regulations

• Establish a reporting module and metric model. Track compliance rate, tax revenue changes, etc.

Metrics are important to reflect the value and impact behind the policy.

• Look at options for entering into Voluntary Collection Agreements

KEEP IT SIMPLE:

• Adopt policies that are not complicated, hard to understand or comply

with and enforce

• Factor in the investment of time and money for enforcement

• Set goals and benchmark.

Page 28 of 41

Ideas for Regulatory Approaches:

As mentioned earlier, the first step to creating effective short-term rental regulation is to set clear and

concrete policy objectives. Once this has been accomplished, it is now time to establish regulatory levers

that are practical, cost effective, and align with the direction a community or county has determined is its

best governance model. Example approaches follow.

Objective

Best Approach(es)

Deficit Approach(es)

Give options to utilize homes as

short-term rentals

Adopting a formal annual

permitting requirement and a

process for revoking permits

from “trouble properties”.

Establishing unclear rules to

comply with and unclear defined

criteria for non-compliance and

enforcement action.

Ensure there are provisions so that

pseudo hotels do not occur while

still providing options for

homeowners to generate extra

income as a short-term rental

Adopting a formal permit

process requiring residency

verification, much like schools

do.

Not stipulating residency

requirements clearly in the

permitting process

Ensure homes are not turned into

“party houses"

Adopting a formal permit

requiring limitations based on

fire code. Require that this be

included on agreements and

booking platforms. While not

bullet proof, it may deter

abuse.

Not stipulating what types of uses

are disallowed will be ineffective

and likely result in

misinterpretation and/or abuse.

Minimize potential parking problems

for the neighbors of short-term

rental properties

Adopting a formal permit

requiring limitations based on

fire code. Require that this be

included on agreements and

booking platforms.

Not stipulating what types of uses

are disallowed will be ineffective

and likely result in

misinterpretation and/or abuse.

Minimize public safety risks and

possible noise and trash problems

Adopting a formal permit

process requiring

• All property owners must

provide the customer

with a copy of local

ordinances, or

• Require the property

owner to identify an

emergency contact that

will be responsible for

taking immediate

corrective action, or

• establish a 24/7 hotline

Not stipulating what is required or

disallowed will be ineffective and

likely result in misinterpretation

and/or abuse.

Page 29 of 41

to allow neighbors and

other citizens to easily

report non-emergency

issues

Ensure that no long-term rental

properties are converted to short-

term rentals to the detriment of

long-term renters in the community

Adopting a residency

requirement for permit

holders to mitigate absentee

landlords from converting

long-term rental properties

into short-term rentals.

Not stipulating residency

requirements clearly in the

permitting process

Ensure that residential

neighborhoods are not inadvertently

turned into tourist areas to the

detriment of permanent residents

Setting specific quotas and/or

including in, or adopting,

permanent residency

requirements for permit

holders

Adopting a complete ban on short-

term rentals, unless such a ban is

heavily enforced.

Ensure the physical safety of short-

term renters

Adopting a safety inspection

requirement as part of the

permit approval process that

outlines minimum levels.

Adopting a complete ban on short-

term rentals, unless such a ban is

heavily enforced.

Ensure any regulation of short-term

rentals does not negatively affect

property values or create other

unexpected negative long-term side-

effects

Adopting regulation that

automatically expires after a

certain amount of time (i.e. 2–

5 years) to ensure that the

rules and processes that are

adopted now are evaluated as

the market and technology

evolves over time.

Adopting regulation that does not

contain a catalyst for evaluating its

effectiveness and side-effects

down the line.

Page 30 of 41

Monitoring, Compliance & Enforcement:

Many New Mexico communities are utilizing third party resources for tracking short-term/vacation rental

activity. These services help municipalities understand the scale and scope of the impact of short-term

rentals in their community to enact regulations that minimize noise, trash, parking and traffic problems, as

well as the negative impacts on housing affordability and neighborhood character.

It is imperative to know the limitations of public data that can be used to monitor and enforce, as well as the

resources that are available to aid in that collection of data or information. Once ordinances are updated

and adopted, these companies can also help manage all of the registration, permitting, address

identification, compliance monitoring, enforcement, outreach, tax collection and complaint processes.

Be aware that the online marketplace platforms have built-in functionality that specifically prevents

information gathering — this is known as “permit sounding”. These platforms do not willingly or

cooperatively offer the data necessary to enforce, and as a word of caution, some have refused to share and

have sued cities for requesting detailed data. It is best to work with your community general counsel on the

appropriate approach on these matters.

Monitoring -

• Expect to invest some level of staff time and/or other resources in compliance monitoring and

enforcement.

• Manually monitoring 100’s or 1000s of short-term rental properties within a specific jurisdiction is

practically impossible without sophisticated databases as property listings are constantly added,

changed or removed.

• Require short-term rental permit holders to maintain books and records for a minimum of 3 years so

that it is possible to obtain the information necessary to conduct inspections or audits as required.

Compliance -

• To implement any type of effective short-term rental best practices it’s important to understand the

technological needs and capacity needs to do this cost effectively.

• Rental property listings are spread across dozens (or hundreds) of different home sharing websites,

with new sites popping up all the time (Airbnb and HomeAway are only a small portion of the total

market).

• Address data is hidden from property listings making it time-consuming or impossible to identify the

exact properties and owners based just on the information available on the home-sharing websites

• The listing websites most often disallow property owners from including permit data on their

listings, making it impossible to quickly identify unpermitted properties.

• There is no manual way to find out how often individual properties are rented and for how much,

and it is therefore very difficult to precisely calculate the amount of taxes owed by an individual

property owner.

Enforcement -

Adopt fine structures that adequately incentivize short-term landlords to comply with the adopted

regulation. Ideally the fines should be proportionate to the economic gains that potential violators can

realize from breaking the rules, and fines should be ratcheted up for repeat violators.

Page 31 of 41

Fine Structure Considerations:

1. Any violation enforcement costs can be constructed to reimburse the local government and other

participating agencies their full investigative costs, pay all back-owed taxes, and remit all illegally

obtained short-term rental revenue proceeds to the local government

2. Any unpaid fine will be subject to interest from the date on which the fine became due and payable

to the local government until the date of payment.

3. The fine schedule is in addition to, and not in lieu of, all other legal remedies, criminal or civil, which

may be pursued.

Draft a Roadmap:

Once the community or county has identified and addressed any outstanding current issues and the

economic considerations of the current state of affairs regarding short-term Rentals, that information can

assist in the development of the roadmap — with the end goal of this information contributing to the

development of a final ordinance. Apply these questions to the roadmap development.

1. How will properties be identified and tracked (internal process or third-party service)?

2. Does a Voluntary Collection Agreement work for the municipality?

3. Application Process – What Department(s) Oversee(s)?

4. Fee Structure

5. Inspection Fees

6. Structural/General Safety

7. Fire

8. Neighborhood Impact (parking, traffic, noise, density, etc.)

9. Registration Fees (one time or annual?)

10. Affordable Housing Fees

11. Penalty/Fees for Non-compliance

12. How will properties be notified of ordinance requirements?

13. What department(s) will be responsible for monitoring/enforcement?

14. How will penalties for non-compliance be assessed/enforced?

15. How often will the ordinance policies/systems be assessed and re-evaluated?

Next Steps:

Once the Short-term Rental Roadmap is complete, it will serve as the outline for the development of your

Short-term Rental Ordinance or Resolution.

To present your Ordinance or Resolution for adoption, follow the steps outlined on page 7, in the section

titled GOVERNANCE & ADMINISTRATION OF FUNDS.

Follow the steps indicated for Ordinance or Resolution adoption according to your local governing body’s

polices regarding posting and publication.

Once the Ordinance or Resolution is adopted, Lodgers’ Tax collection now applies; therefore, the

compliance, enforcement and administration of Lodger’s Tax follows the steps outlined in Sections 2(c)

through 2(e) in the handbook.

This section can serve as a stand-alone mini handbook specifically for the short-term rental platform, and

will include all the resources and sample documents from the Resource Appendix, in the digital form.

Page 32 of 41

Short-term Rental Resources:

Statute:

In 2019, SB 106 was passed, removing the 3-room exemption and making it easier for communities to track

short-term/vacation rentals and collect applicable taxes https://legiscan.com/NM/text/SB106/2019.

Examples of recently updated ordinances for reference:

https://www.cabq.gov/dfa/treasury/taxes-and-fees/lodgers-tax-ordinance

https://www.santafenm.gov/documents__forms

https://www.taosgov.com/427/Short-Term-Rentals

Helpful Hints for Updating Lodgers’ Tax Policies

(provided by the City of Albuquerque):

www.newmexicohospitality.org

Update ordinances regarding tracking and reporting for short-

term/vacation rentals:

https://www.taosgov.com/427/Short-Term-Rentals

https://www.santafenm.gov/documents__forms

Third Party resources for tracking short-term/vacation rental activity:

These services can help manage all of the registration, permitting, address identification, compliance

monitoring, enforcement, outreach, tax collection and complaint processes.

https://hostcompliance.com/ (Currently used by Taos)

https://www.harmari.com/ (Currently used by Santa Fe)

*No party, entity, or agency associated with this handbook endorses any particular software service.

Page 33 of 41

Descriptions

& Definitions

The Gila River

Page 34 of 41

Descriptions & Definitions:

Advertising

Advertising is a one-way communication whose purpose is to inform potential customers about products

and services and how to obtain them.

Day Trips

For the purpose of tourism, the term Day Trip refers to a person traveling from their residence with a plan to

return to their residence within the same day. This may include a family from Los Alamos who are traveling

to Rio Rancho for their son’s soccer tournament. Another example is a group of NMSU students traveling to

Elephant Butte to spend the day boating on the lake. During winter, a common day trip is heading to the

mountains for a day of skiing. These examples show the importance of in-state travel, but Day Trips also

come from our neighboring states and Mexico.

Economic Impact

The effect that an event, policy change, or market trend will have on economic factors such as tax revenue,

consumer confidence, or unemployment.

Marketable Overnight Trips

Marketable Overnight Trips are defined as travel that is influenced by marketing efforts and do not include

visitors whose main purpose in taking a trip is to visit friends and family or for business trips, and the visitor

stays overnight. This is a desirable type of tourist because, as research commissioned by New Mexico

Tourism Department shows, out-of-state visitors spend much more per person and bring new money into

the state.

Marketing

The activity, set of institutions, and processes for creating, communicating, delivering, and exchanging

offerings that have value for customers, clients, partners, and society at large.

Online Travel Agency (OTA)

Online companies whose websites allow consumers to book various travel related services directly via

Internet. They are 3rd party agents reselling trips, hotels, cars, flights, vacation packages etc. provided or

organized by others.

Promotion

Promotion involves disseminating information about a product, product line, brand, or company. It is

designed to raise customer awareness of a product or brand, generating sales, and creating brand loyalty.

Publicizing

Publicity (publicizing) is to make something widely known – give out publicity about (a product, person, or

company) for advertising or promotional purposes.

Return on Investment

A performance measure used to evaluate the efficiency of an investment or compare the efficiency, or

revenue generated, of a number of different investments. ROI tries to directly measure the amount of

return on a particular investment, relative to the investment’s cost.

Page 35 of 41

Shared Economy

An economic model defined as a peer-to-peer (P2P) based activity of acquiring, providing, or sharing access

to goods and services that is often facilitated by a community-based on-line platform.

Short-Term Rental

A short-term vacation rental (also called a vacation rental or STR) is most often defined as a rental of a

residential dwelling unit or accessory building for periods of less than 31 consecutive days. In some

communities, short-term rental housing may be referred to as vacation rentals, transient rentals, short-term

vacation rentals or resort dwelling units.

Tourist-Related Attractions, Facilities and Events

A tourist attraction, facility or event is a place of interest where tourists visit, typically for its inherent or an

exhibited natural or cultural value, historical significance, natural or built beauty, offering leisure and

amusement. The most important characteristic of a tourist attraction, facility or event is that it is

“consumed” at the destination, rather than at the tourist‘s home. This means that in order to consume the

product, the client must first travel to it.

Voluntary Collection Agreement

An agreement between a company like Short-term rental platforms and a state or local government that

pertains to the collection of lodging taxes.

Page 36 of 41

Resource

Appendix

Sitting Bull Falls

Page 37 of 41

Lodgers’ Tax Resource Appendix:

Where to report Lodgers’ Tax:

Report Lodgers’ Tax - http://www.nmdfa.state.nm.us/Financial_Distribution.aspx

Use of Lodgers’ Tax:

https://law.justia.com/codes/new-mexico/2018/chapter-3/article-38/section-3-38-15/

Recent Lodgers’ Tax Legislation:

New Mexico Senate Bill 106: https://legiscan.com/NM/text/SB106/2019.

New Mexico House Bill 117: https://legiscan.com/NM/text/HB117/2020

Examples of Updated Lodgers’ Tax Ordinances and Policies:

https://www.cabq.gov/dfa/treasury/taxes-and-fees/lodgers-tax-ordinance

https://www.santafenm.gov/documents__forms

https://www.taosgov.com/427/Short-Term-Rentals

Sample of Lodger’s Tax Reports/Event Applications:

https:// roswell-nm.gov/DocumentCenter/View/7340/Nov-2019-Lodgers-Tax-Report

https://roswell-nm.gov/AgendaCenter/ViewFile/Minutes/_08202019-1621

https://roswell-nm.gov/1030/Lodgers-TaxSpecial-Events

https://www.gallupnm.gov/DocumentCenter/View/3269/Lodgers-Tax-FY-20--REFILLABLE-PDF

Lodgers’ Tax Advisory Boards:

http://www.townofsilvercity.org/r/legal_notes/Ord%201213%20%20Lodgers%20Tax%20Adviso

ry%20Board.pdf

https://www.nmag.gov/uploads/files/Publications/ComplianceGuides/Open%20Meetings%20Act

%20Compliance%20Guide%202015.pdf

Third Party Short-Term Rental Monitoring Resources:

https://hostcompliance.com/ (Used by Taos)

https://www.harmari.com/ (Used by Santa Fe)

Page 38 of 41

Partner Resources:

New Mexico Municipal League: https://nmml.org/

New Mexico Association of Counties: https://www.nmcounties.org/

Regional Marketing Boards: https://www.newmexico.org/industry/work-together/partnership-

opportunities/regionalmarketing-boards/

New Mexico Taxation & Revenue: http://www.tax.newmexico.gov/

New Mexico Tourism Department: https://newmexico.org

General Resources & Information:

HOSPITALITY FEE – Albuquerque (3-38A-1 through 3-38A-12 -https://law.justia.com/codes/newmexico/

2013/chapter-3/article-38a/)

CONVENTION CENTER FINANCING ACT – Las Cruces, Farmington, Roswell, Truth or Consequences (3-38A-1

through 3-38A12 - https://law.justia.com/codes/new-mexico/2013/chapter-3/article-38a/

CONFERENCE & CONVENTION CENTER FINANCING ACT – Santa Fe (5-14-1 through 5-14-15 -

https://law.justia.com/codes/new-mexico/2006/nmrc/jd_5-14-1-3b45.html )

TAX INCREMENT DEVELOPMENT DISTRICTS (TIDD) – Mechanisms to support economic development and

job creation by providing gross receipts tax financing and property tax financing for public infrastructure

(Sections 5-15-2 NMSA 1978 - https://law.justia.com/codes/new-mexico/2006/nmrc/jd_5-15-2-

3b85.html)

Hotel Valuation Services Report: https://www.hvs.com/article/8607-2019-hvs-lodging-tax-report-usa ),

New Mexico Hospitality Association Resources:

2019 Short-Term Rental Impact Report

2020 Lodgers’ Tax Policy Survey Summary

Helpful Hints for Updating Lodgers’ Tax Policies (provided by the City of Albuquerque)

New Mexico Main Street Lodgers’ Tax Report (2016)

US Travel Association

www.newmexicohospitality.org

Page 1 of 41

New Mexico Hospitality

Association is the state’s

No.1 Resource

for travel, tourism and

lodging stakeholders.

Page 2 of 41

New Mexico Hospitality Association is the state’s number one

resource for travel, tourism and lodging stakeholders. It is a

privately funded nonprofit that is focused on serving its

members and all segments of the hospitality industry through three distinct functions.

First, the association unites the industry to influence public policy. The association takes positions

and advocates for legislation and policy that align with five core principles: build the tourism

industry, promote the tourism industry, foster a business-friendly environment for tourism,

increase opportunities for tourism development, and preserve tourism resources and funding

mechanisms. As Lodgers’ Tax is a critical funding mechanism for the industry, the association took

the leadership role in the development of the Lodgers’ Tax Best Practices Handbook.

Second, the association creates and administers educational programming to further develop the

industry’s workforce. This includes two statewide annual conferences, a pilot apprentice program

designed specifically for the hospitality industry, and a student scholarship program. The Lodgers’

Tax Best Practices Handbook provides another educational resource that will be integrated into the

association’s overall educational programming to ensure the workforce has access.

Thirdly, New Mexico Hospitality Association provides platforms of collaboration to tackle and solve

various challenges. The Lodgers’ Tax Best Practices Handbook is an example of that collaborative

system. The association identified the need for a manual and convened a group of tourism leaders

to develop a comprehensive solution. Through the spirit of collaboration, the association is able to

provide another resource to the industry.

The association delivers decades of combined experience to lead public policy and workforce

development strategy for a more prosperous economy. The association represents member

interests at the state and national level, cultivates professional development, and targets

opportunity to incubate and foster long-term job and wealth creation statewide. The association’s

members are true investors and are playing a crucial role in growing tourism and New Mexico’s

economy.

Page 3 of 41

Thanks

Thank you to the following partners who played a vital role in the development of this manual:

Jennifer Lazarz – City of Gallup

Noah Trujillo – Visit Rio Rancho

Will Maguire – Ambience Hospitality

Debbie Edwards – Artesia Chamber of Commerce

Dora Dominguez – Sandoval County

Karina Armijo – Town of Taos

Synthia Jaramillo – City of Albuquerque

Judith Newby – Village of Corrales

Valerie Lind – Visit Albuquerque

Steven Rose – The Blake at Taos Ski Valley

Barbara Rudolf – Sunny505

Tania Armenta – Visit Albuquerque

Randy Randall – Tourism Santa Fe

Jason Weaks – NMHA Lobbyist

Kim Skinner – Sierra County

Lisa Boeke – City of Carlsbad

Rachelle Howell – Southwest Planning & Marketing

The New Mexico Tourism Department

{kind=link}