Structural Fiscal Policy in

Uruguay: A Proposal

Guillermo Le Fort

Inter-American

Development Bank

Fiscal and Municipal

Management Division

DISCUSSION PAPER

No. IDB-DP-298

July 2013

Structural F

i

scal Pol

i

cy

i

n Uruguay:

A Proposal

Gui

ll

ermo Le Fort

Inter-American Development Bank

2013

http://www.iadb.org

The opinions expressed in this publication are those of the authors and do not necessarily

reflect the views of the Inter-American Development Bank, its Board of Directors, or the

countries they represent.

The unauthorized commercial use of Bank documents is prohibited and may be punishable

under the Bank's policies and/or applicable laws.

Copyright © Inter-American Development Bank. All rights reserved; may be freely

reproduced for any non-commercial purpose.

2013

Abstract

*

This paper presents a design and simulation of a structural fiscal policy in

Uruguay. The design includes the derivation of a metric for the structural

balance that is most adequate for the country and the calculation of a

structural fiscal target. This target is associated to a goal for the net worth of

the public sector that ensures sustainability of the financial position of the

public sector, or at least reduces its historical vulnerabilities. The paper also

discusses the current situation in meeting the preconditions for the

establishment of a structural fiscal balance target, and makes some

recommendations on the policy reforms that appear to be needed to implement

a structural fiscal policy in Uruguay.

JEL Codes: E62, H60

Keywords: Fiscal Policy, Structural Fiscal Policy, Structural Balance,

Structural Fiscal Target

*

This report on a structural fiscal policy for Uruguay has been prepared at the request of the IDB and as part of

a larger effort that includes similar works for other countries in the region. The preparation of this report

included a five day visit to Montevideo in early March 2010, and has included a significant effort in compiling

and processing data under the efficient lead of Salvador Andino and the help from Agustina Sanguinetti from

Ceres. We are particularly grateful to Ernesto Talvi and his team from Ceres for helpful discussions and for

sharing with us their data set, and to the several current and former Uruguayan authorities who were kind

enough to share with me their views on the “optimal” design for fiscal policy. Finally, we acknowledge the

valuable comments of Teresa Ter-Minassian, Gustavo García, Antonio Fernández, and Alberto Barreix and

other seminar participants at the IDB.

2

INDEX

I.! Introduction ............................................................................................................................... 3!

II.! Uruguay Descriptive Statistics ................................................................................................. 5!

1.! Fiscal Revenues and Expenditures ........................................................................................... 5!

2.! Primary and Overall Fiscal Balances ...................................................................................... 9!

3.! Public Debt ............................................................................................................................. 10!

4.! Real GDP and Components .................................................................................................... 14!

5.! Volatility of Real GDP ............................................................................................................ 16!

6.! Volatility of Fiscal Revenues .................................................................................................. 18!

III.! Estimating and Projecting the Structural Fiscal Balance in Uruguay ................................... 21!

1.! Estimation of Trend or Structural GDP .................................................................................. 21!

2. Elasticities and the Structural Balance ..................................................................................... 27!

3. Fiscal Projections ..................................................................................................................... 34!

4. The Structural Fiscal Target ..................................................................................................... 35!

IV.!Preconditions and Recommendations for the Implementation of the Fiscal Rule .................. 42!

V. Uruguay Database .................................................................................................................... 50!

VI. Bibliography and References .................................................................................................. 51!

3

I. Introduction

The report for structural fiscal policy in Uruguay is divided in three parts. The first consists

of a presentation and interpretation of descriptive statistics for the Uruguayan fiscal accounts

and macroeconomic data. The time series were put into place compiling data from different

sources and ensuring its compatibility, but despite our best effort there are different

limitations, which may affect the results. First, the database was assembled with pieces of

data coming from several sources, which are considered individually reliable, however there

are no guarantees that the series are fully consistent. In addition, because of data gaps in the

series we had to use estimates for certain variables and parameters that could be inaccurate.

This is the case of depreciation, for which information was obtained from the World Penn

Tables, the weight of labor and capital in the Cobb Douglas production function, which was

estimated following academic work rather than statistics on functional income distribution.

Finally, the estimates of the elasticities of fiscal revenue with respect to actual and trend GDP

and the GDP gap are the result of regressing the aggregates, rather than building an estimate

from the aggregation of the elasticities of individual taxes and sources of income, owing to

data limitations.

The second part of the report presents a design and simulation of a structural fiscal

policy in Uruguay, including the derivation of a measurement for the structural balance that

is most adequate for the country and the calculation of a structural fiscal target. Considering

that the main source of volatility and deviations from trend of the fiscal revenue in Uruguay

is the GDP cycle, this second part presents an analytical framework for defining and

estimating trend GDP and the relevant structural fiscal variables, drawing from Chile’s

decade of experience in structural fiscal policy. Uruguay’s structural fiscal revenue was

estimated as a function of trend GDP, which was estimated on the basis of a Cobb Douglas

production function and time series on capital stock, labor force, unemployment, and total

factor productivity that go back to the 1960s.

The selection of the structural fiscal target was associated to a goal for the net worth

of the public sector that ensures sustainability of the financial position of the public sector, or

at least reduces its historical vulnerabilities. In the case of Uruguay, the goal for net worth is

more directly linked with the composition of the public debt in terms of currency of

denomination than with the level of debt. The ability to have a large portion of debt in

4

domestic currency is the main condition to minimize the financial vulnerabilities of the

public sector and ensure the conditions under which this debt is sustainable.

The third part of the report discusses the current situation in meeting the pre

conditions for the establishment of a structural fiscal balance target. The report makes some

recommendations on the policy reforms that appear to be needed to implement a structural

fiscal policy in Uruguay. That includes a budgeting process centralized in the ministry of

finance, and where the political discussions are focused on the composition of spending and

associated priorities rather than on the level of fiscal spending, which is defined by the

estimated structural revenue and the fiscal target. The level of total spending is defined by a

macroeconomic framework, the response of fiscal revenue to trend GDP and the target for

the structural fiscal balance. Finally, some important conditions for a successful structural

fiscal policy are discussed, including the need for further transparency of fiscal data, on

revenues and expenditures, as well as debt and contingent liabilities.

The final objective of introducing a structural fiscal policy in Uruguay is to improve

on the country’s macroeconomic resiliency, eliminating a major source of vulnerability to

macroeconomic and financial crisis. Creating fiscal institutions that may lead the definitions

associated to fiscal policy in consistency with macroeconomic stability would only attain this

objective. This would imply stabilizing the rate of growth of spending to avoid the forced

adjustments and eventually the economic crashes that result when the inter-temporal

restrictions are ignored.

5

II. Uruguay Descriptive Statistics

1. Fiscal Revenues and Expenditures

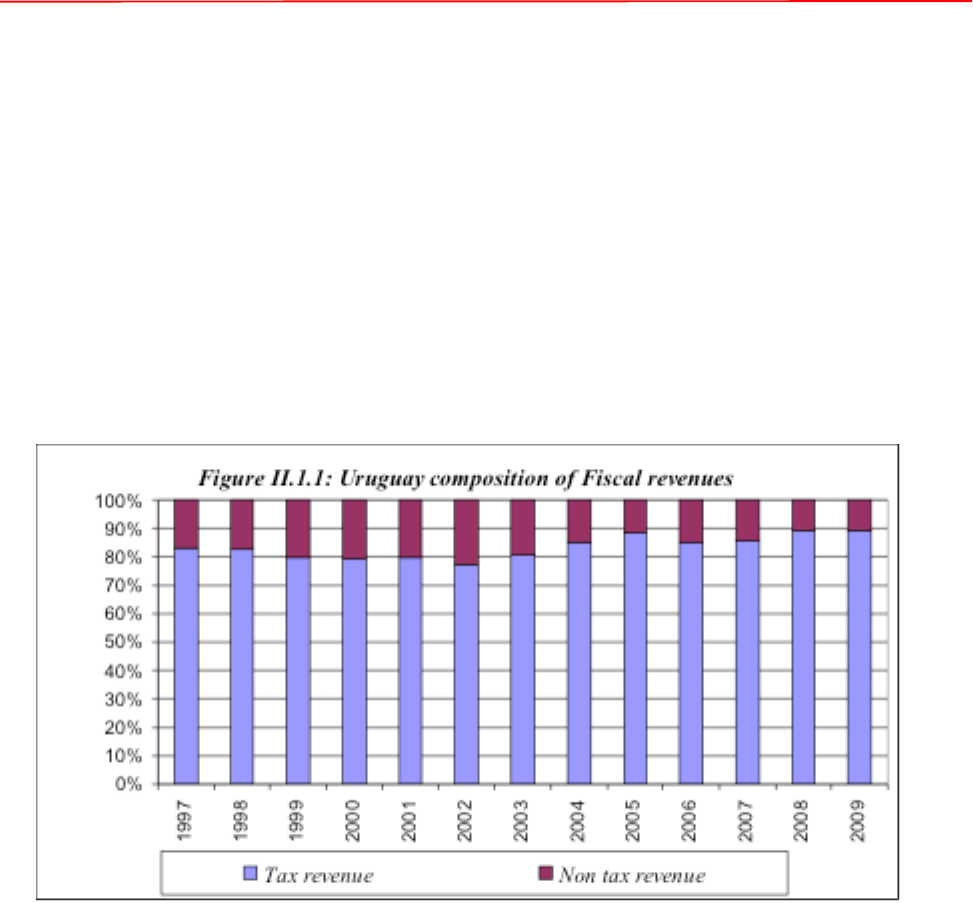

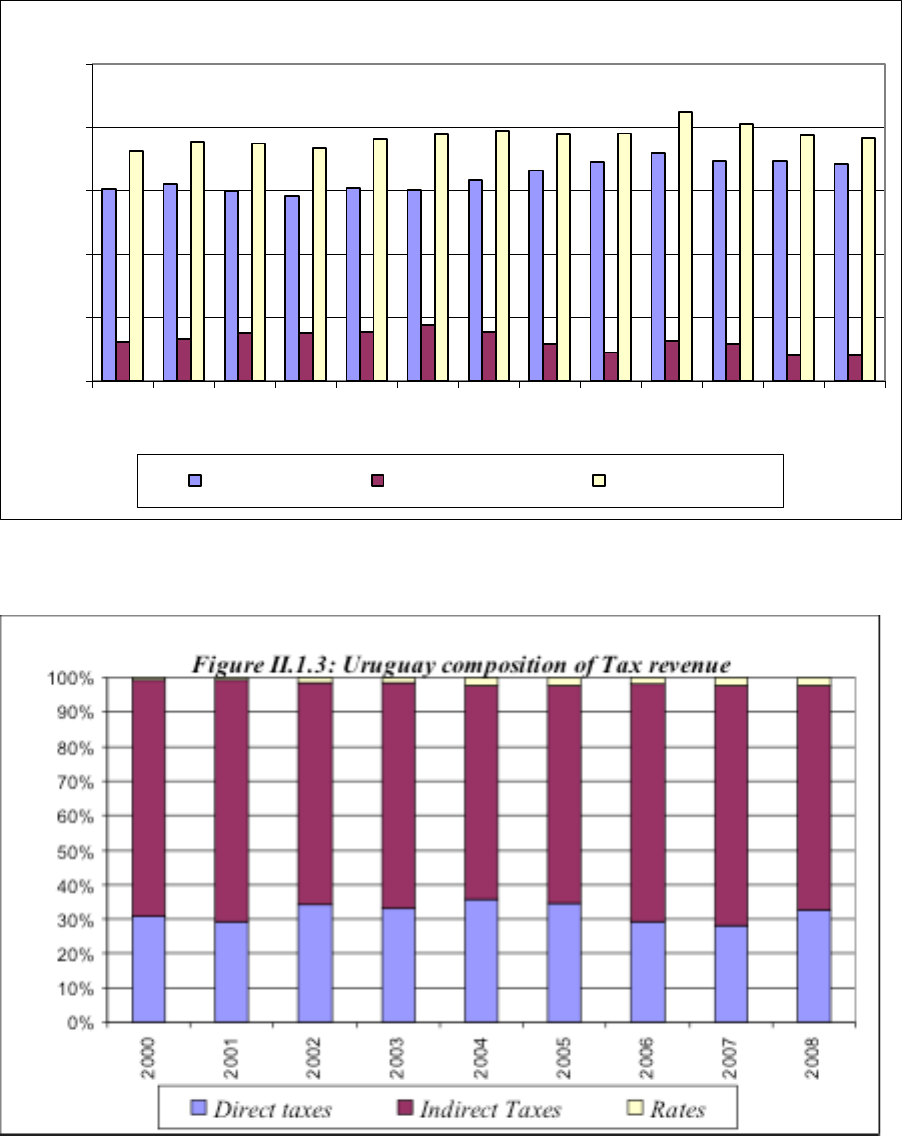

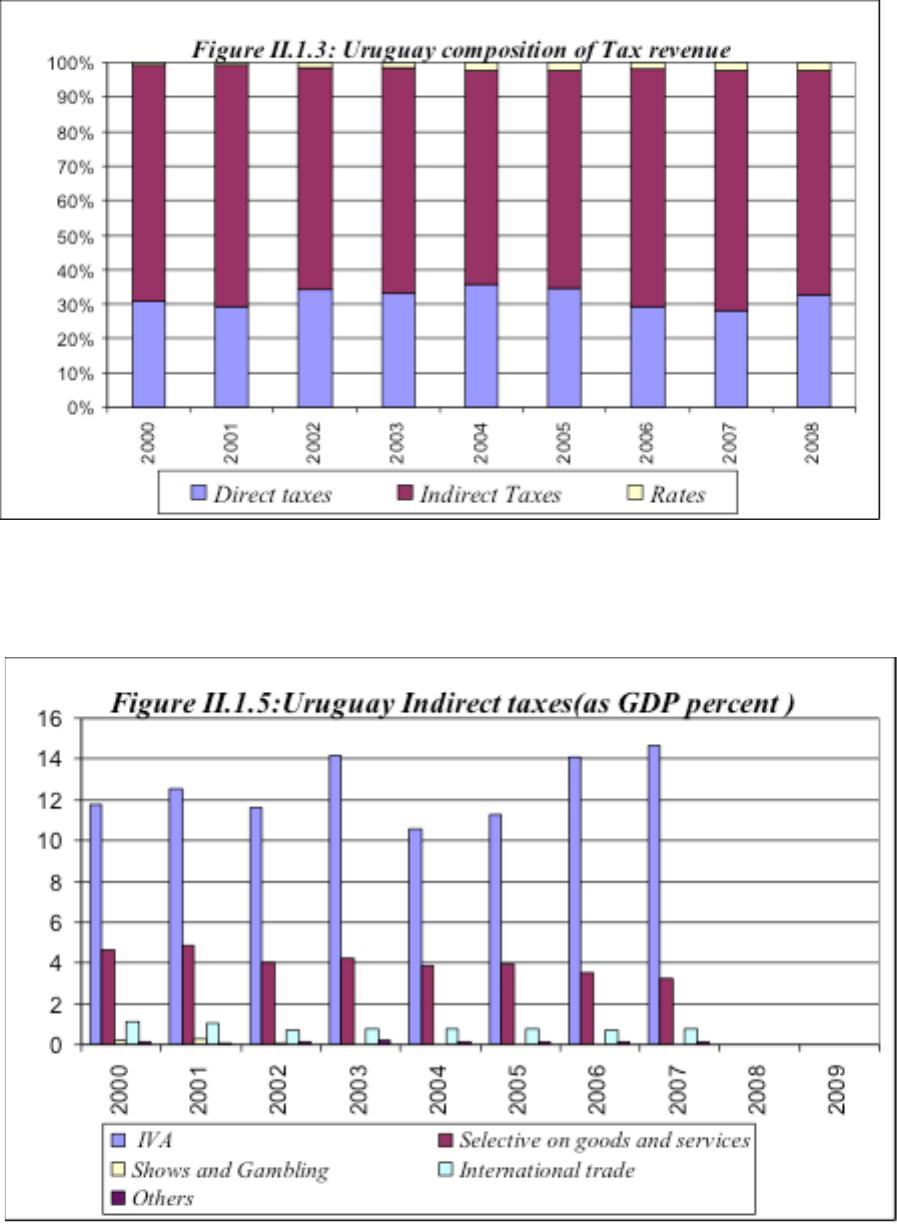

The main source of fiscal revenue in Uruguay is tax collections, which on average over the

last 10 years amounts for nearly 90 percent of total revenue, fluctuating around 16 percent of

GDP. Non-tax revenue contributes with an additional 3 percent of GDP to Uruguayan public

finances. Most of the tax revenues come from indirect taxes, and hence are associated to

domestic private spending. Indirect taxes represent an average of about 70 percent of total

revenue for the past 10 years. Indirect taxes are concentrated on taxes on goods and services,

and particularly the Value added tax, equivalent to 13 percent of GDP.

Source: LE&F, based in information of Contaduría general de Uruguay.

6

0

0.05

0.1

0.15

0.2

0.25

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Figure II.1.2: Uruguay Fiscal revenues (as GDP percent )

Tax revenue Non tax revenue Total revenue

Source: LE&F, based on information from Contaduría general de Uruguay.

S

Source: LE&F, based on information from Contaduría general de Uruguay.

7

Source: LE&F, based on information from Contaduría general de Uruguay.

Source: LE&F, based on information from Contaduría general de Uruguay.

8

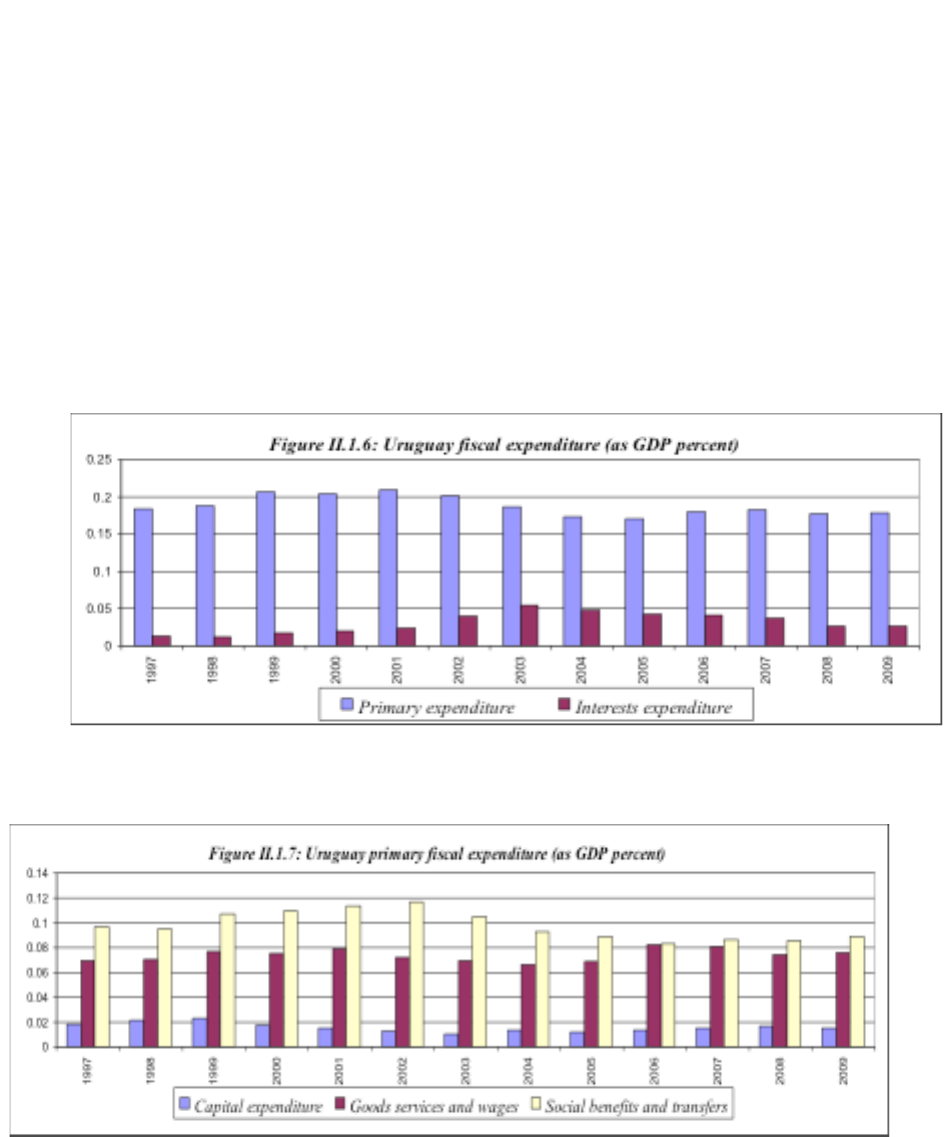

Primary fiscal expenditure expanded continuously reaching above 20 percent of GDP early

this decade, but has since declined converging towards 17 percent of GDP in the last few

years, while interest expenditure has risen from 2 percent of GDP to 5 percent of GDP over

the last decade. Operational expenditures represent the bulk of primary spending, about 90

percent of total, and capital represent the remaining 10 percent. In operational spending,

pension and other welfare benefits represent 40 percent of total expenditures and wages 20

percent. Finally, social benefits expenditure represent around 9 percent GDP while

expenditure on goods, services and wages close to 8 percent of GDP and both have remained

relatively stable over the last few years.

Source: LE&F, based on information from Banco Central de Uruguay.

Source: LE&F, based on information from Banco Central de Uruguay.

9

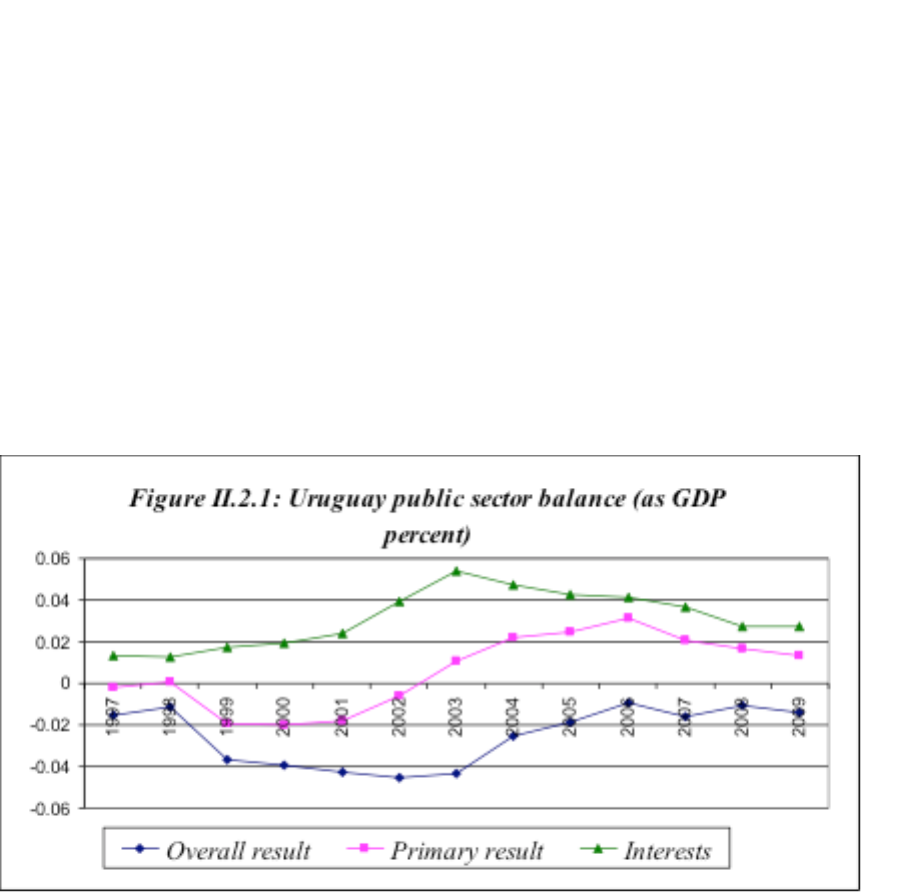

2. Primary and Overall Fiscal Balances

Uruguay’s primary fiscal balance went into deficit from 1999 to 2001 as the crisis ensued,

but with the adjustment and recovery begun in 2003 brought a succession of increasing

primary surpluses reaching up to 3 percent of GDP in 2006. Since then the primary surplus

has declined gradually just below 2 percent of GDP. Uruguay’s debt crisis resulted in a

sustained increase in interest expenditures, which reached a maximum of 5 percent of GDP

en 2003–2004. The adjustment, debt rescheduling and decline in international rates that

followed resulted in the continuous decline of interest spending to less than 3 percent of GDP

in 2009. The overall fiscal balance has remained in deficit throughout the decade, with a

significant improvement over the last few years when the overall balance stood at -1 percent

of GDP and the primary balance at a surplus just below 2 percent of GDP.

Source: LE&F, based on information from Banco Central de Uruguay.

10

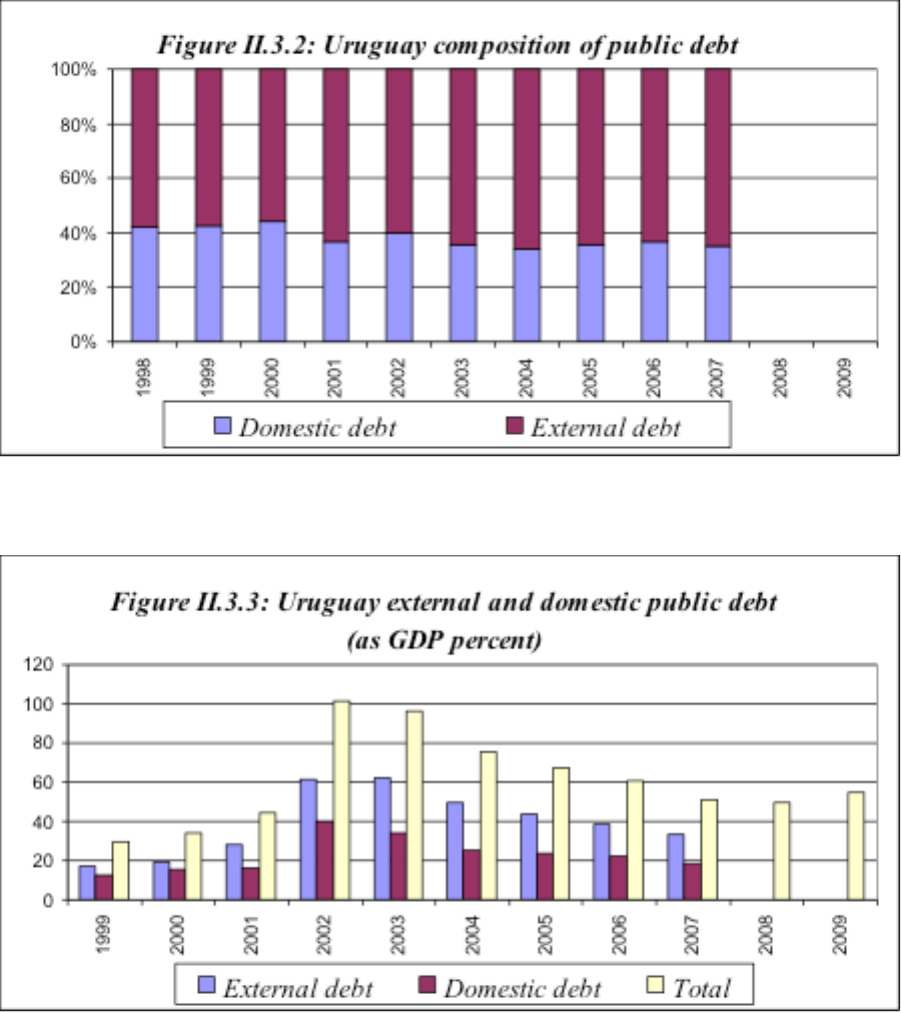

3. Public Debt

The financial crisis of 2002–2003 represented an explosion in the public debt, which

increased from less than 30 percent of GDP in 1999 to 100 percent of GDP by 2002.

Subsequently, with the rescheduling, recovery and adjustment, the public debt level has

gradually declined without reaching the pre crisis level; the debt ratio stood at about 50

percent of GDP in the period 2007–2009. The debt structure is characterized by an almost

even level of foreign and domestic debt, 60 percent and 40 percent of total debt, respectively.

External debt reached levels of over 60 percent of GDP in 2002 and 2003, and then

descended gradually to just over 30 percent in 2007. Domestic debt followed a similar

pattern, reaching levels of 40 percent in 2002 and falling gradually to just under 20 percent o

GDP in 2007.

0

20

40

60

80

100

120

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Figure II.3.1: Uruguay public debt (as GDP percent)

Source: LE&F, based on information from Contaduría general de Uruguay.

11

Source: LE&F, based on information from Contaduría general de Uruguay.

Source: LE&F, based on information from Contaduría general de Uruguay.

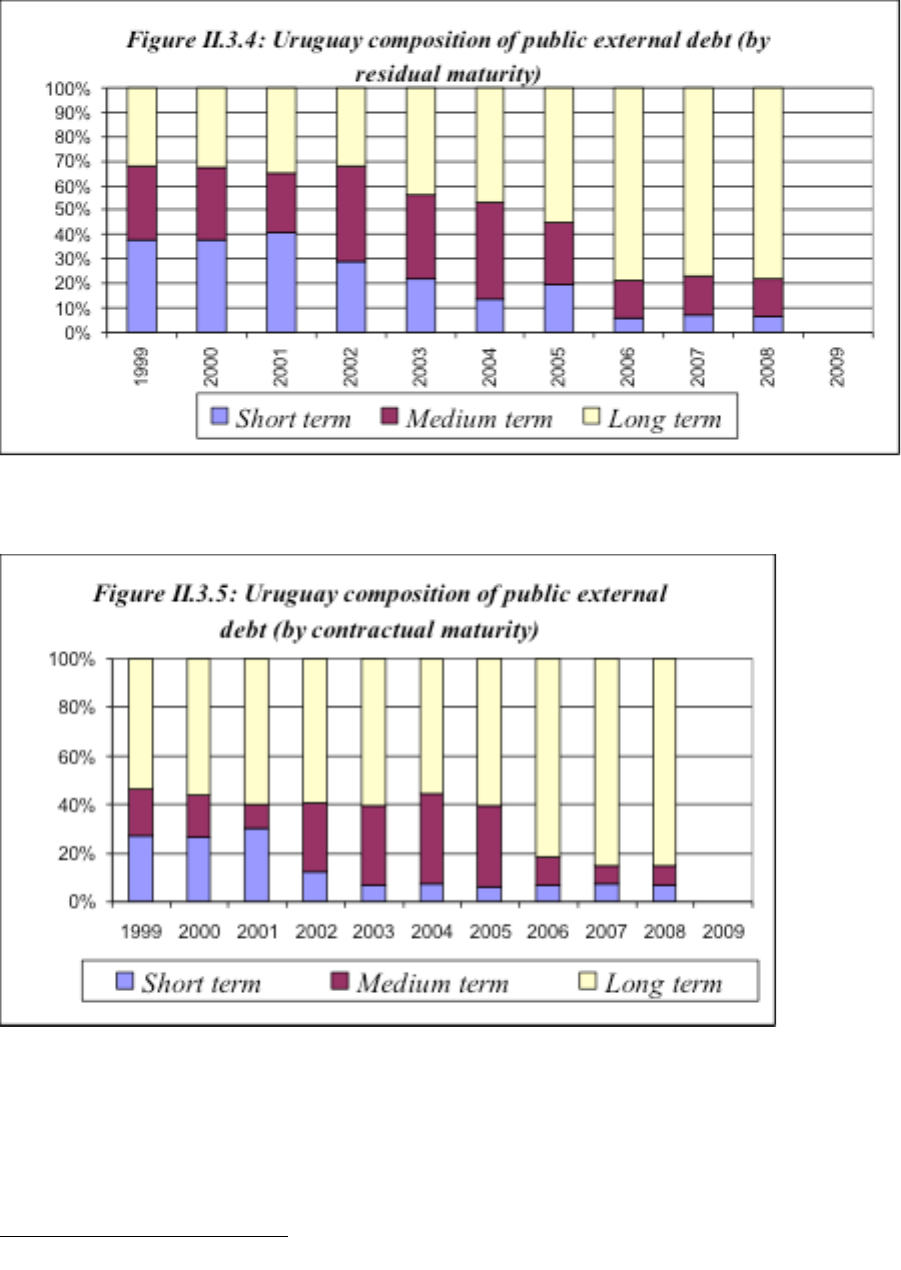

The composition of Uruguayan Public debt has improved over the last few years after the

crisis, the maturity of the debt has increased, the fixed interest rate has gained ground over

the flexible rate, and a lower percentage of debt is denominated in foreign currency. The

residual maturity of external debt instruments has increased over the last few years. Long-

12

term

1

instruments represent almost 80 percent of total in 2008 after being only 30 percent

earlier in the decade.

Source: LE&F, based on information from Contaduría general de Uruguay.

Source: LE&F, based on information from Ministerio de Economía y Finanzas of Uruguay.

1

Long term: more than 5 years; medium term: 1-5 years; short term: less than 1 year

13

Fixed interest rates debt has increased from 30 percent of total in 1999 to 60 percent of total

in 2008.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Figure II.3.6: Uruguay composition of public external

debt (by interest rate)

Fixed rate Libor BID BIRF Others variables Net deposits and other liabilities

c

Source: LE&F, based on information from Ministerio de Economía y Finanzas of Uruguay.

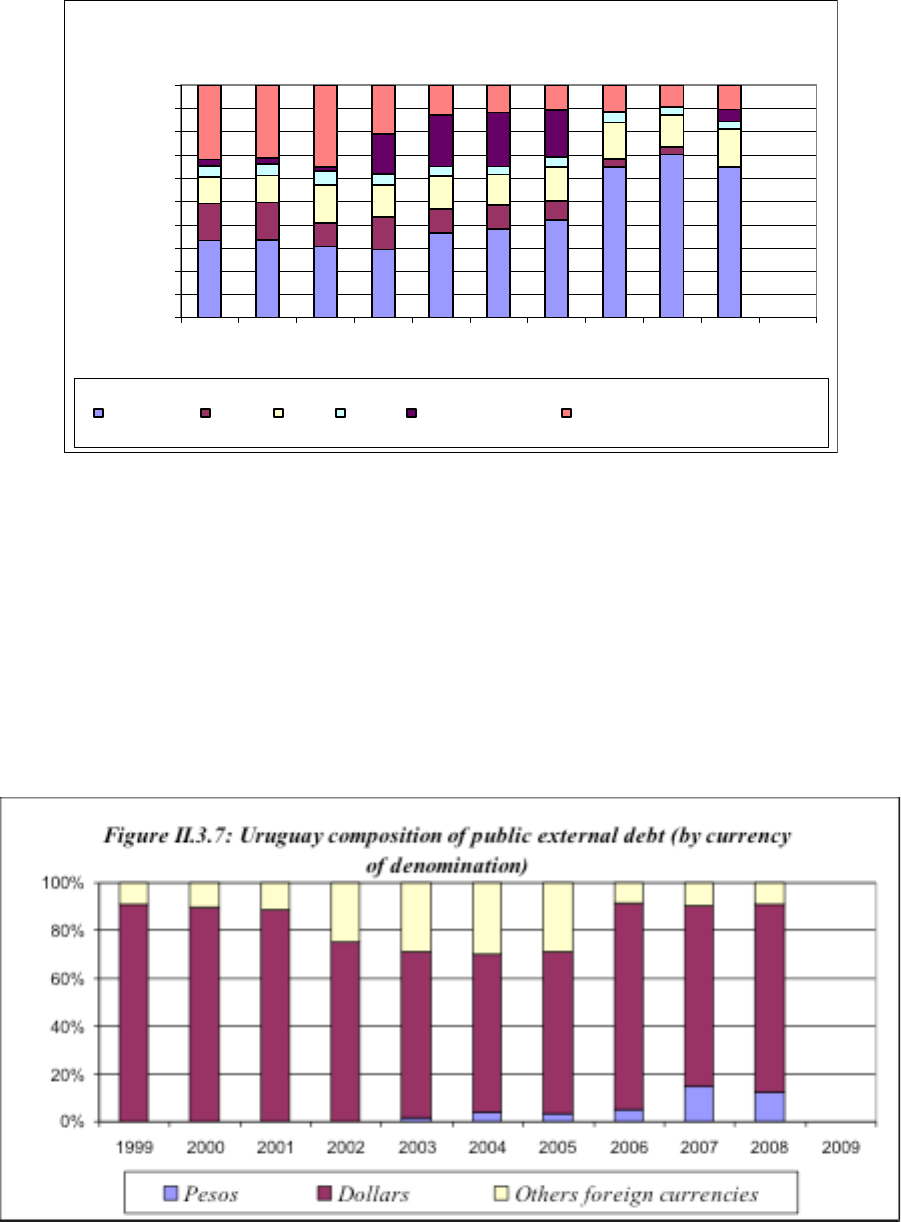

Currency composition: Foreign debt is denominated mostly in dollars, but it has declined

from around 90 percent of total in 1999 to less than 80 percent in 2008. A significant portion

of domestic debt is also denominated in US dollars, but its importance is declining, Actually,

in 2009, 30 percent of total debt is denominated in domestic currency, either nominal or

adjustable by the CPI inflation rate.

Source: LE&F, based on information from Ministerio de Economía y Finanzas de Uruguay

14

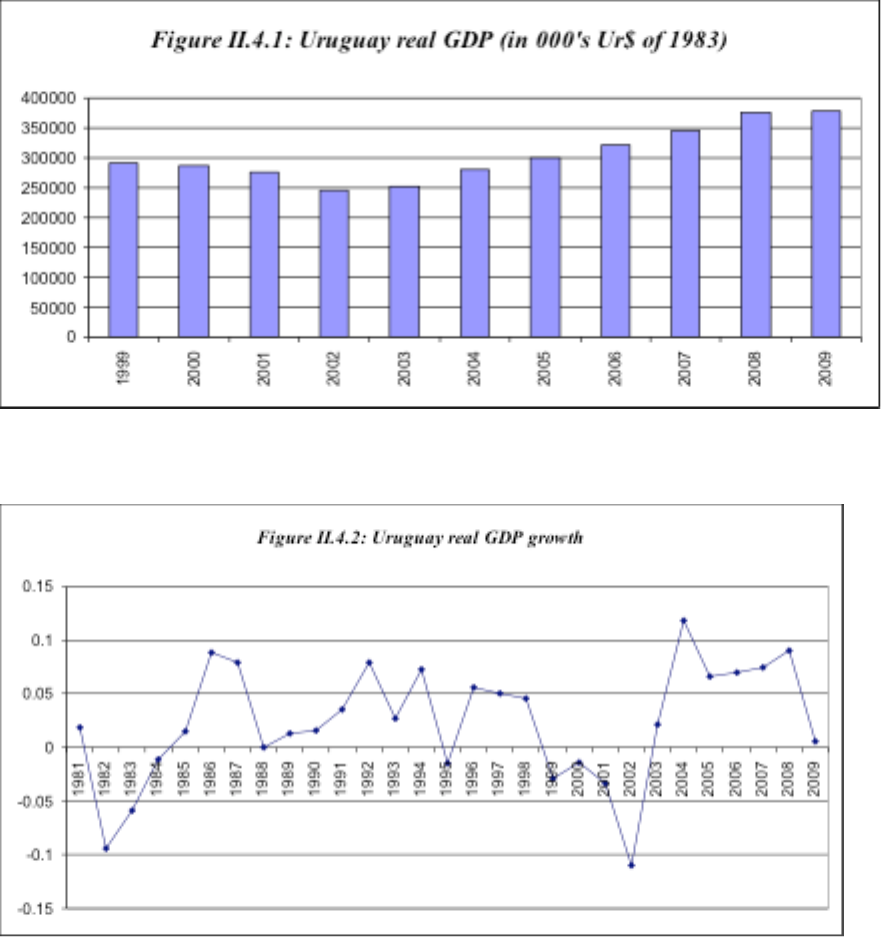

4. Real GDP and Components

As it is well known, Uruguay experienced another financial crisis and a major recession

earlier in this decade mostly as a result of contagion from the financial crisis of Argentina

through a very vulnerable domestic financial system. The recovery that was evident in the

data from 2004 on has been quite strong, with an annual GDP growth rate that averaged

around 8 percent per year in 2004-2008, but has since then declined to almost 0 in 2009,

partly as a result of the effects of the sub prime crisis in Uruguay’s international markets.

Source: LE&F, based on information from Banco Central de Uruguay.

Source: LE&F, based on information from Banco Central de Uruguay.

15

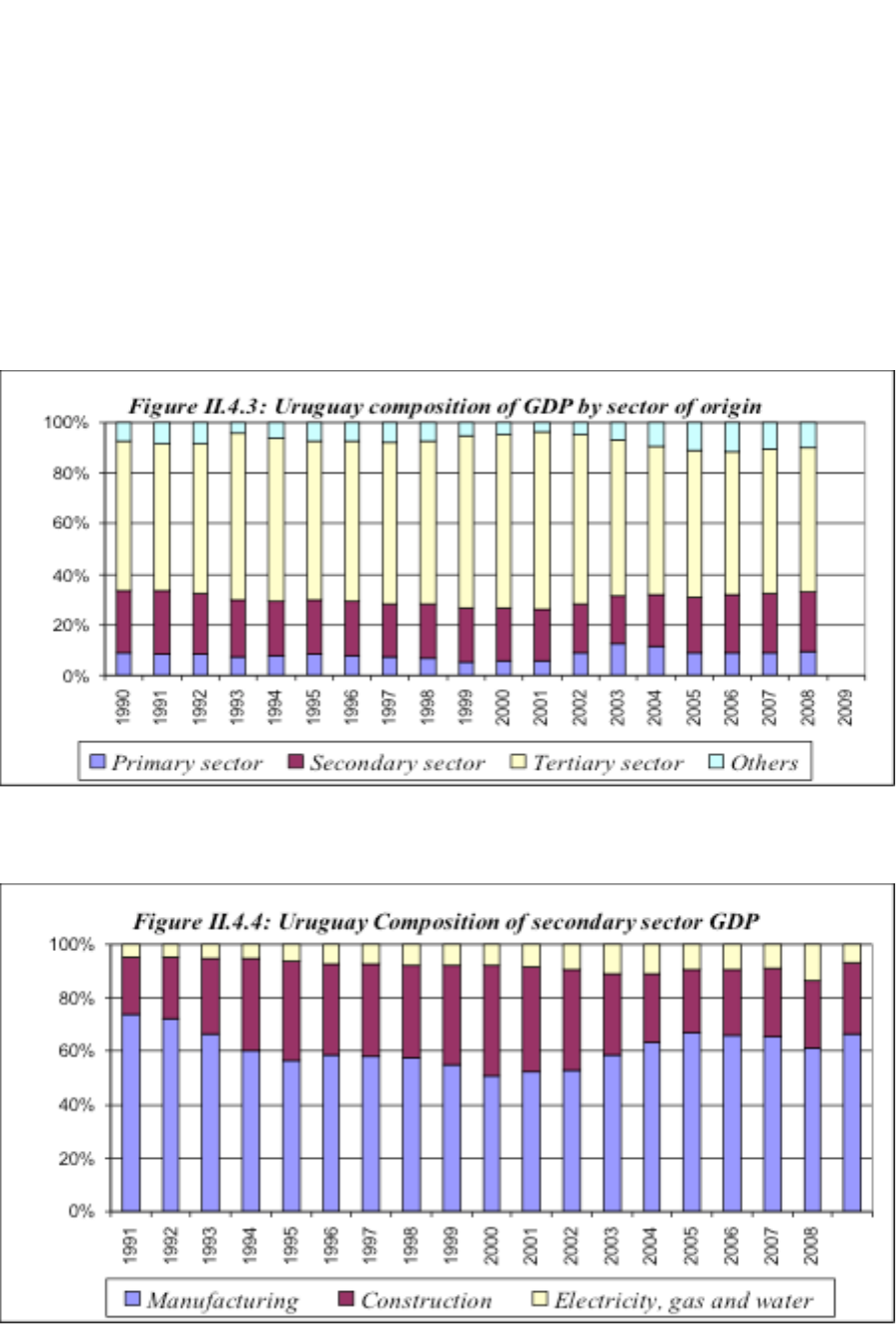

The composition of Uruguay’s GDP shows a certain bias towards services, with the tertiary

sector representing close to 60 percent of total GDP. Services like financing, insurance, real

estate and renting accounts for 1/3 of this total, business services other third, and community,

social and personal services the remaining. The secondary sector represents approximately 20

percent of GDP, with manufacturing, construction and electricity accounting for 70 percent,

20 percent and 10 percent of this total, respectively. Despite its agricultural export base, the

primary sector in Uruguay is about 10 percent of GDP, with agriculture representing over 80

percent of primary sector activity.

Source: LE&F, based on information from UN ECLAC.

Source: LE&F, based on information from UN ECLAC.

16

Source: LE&F, based on information from UN ECLAC.

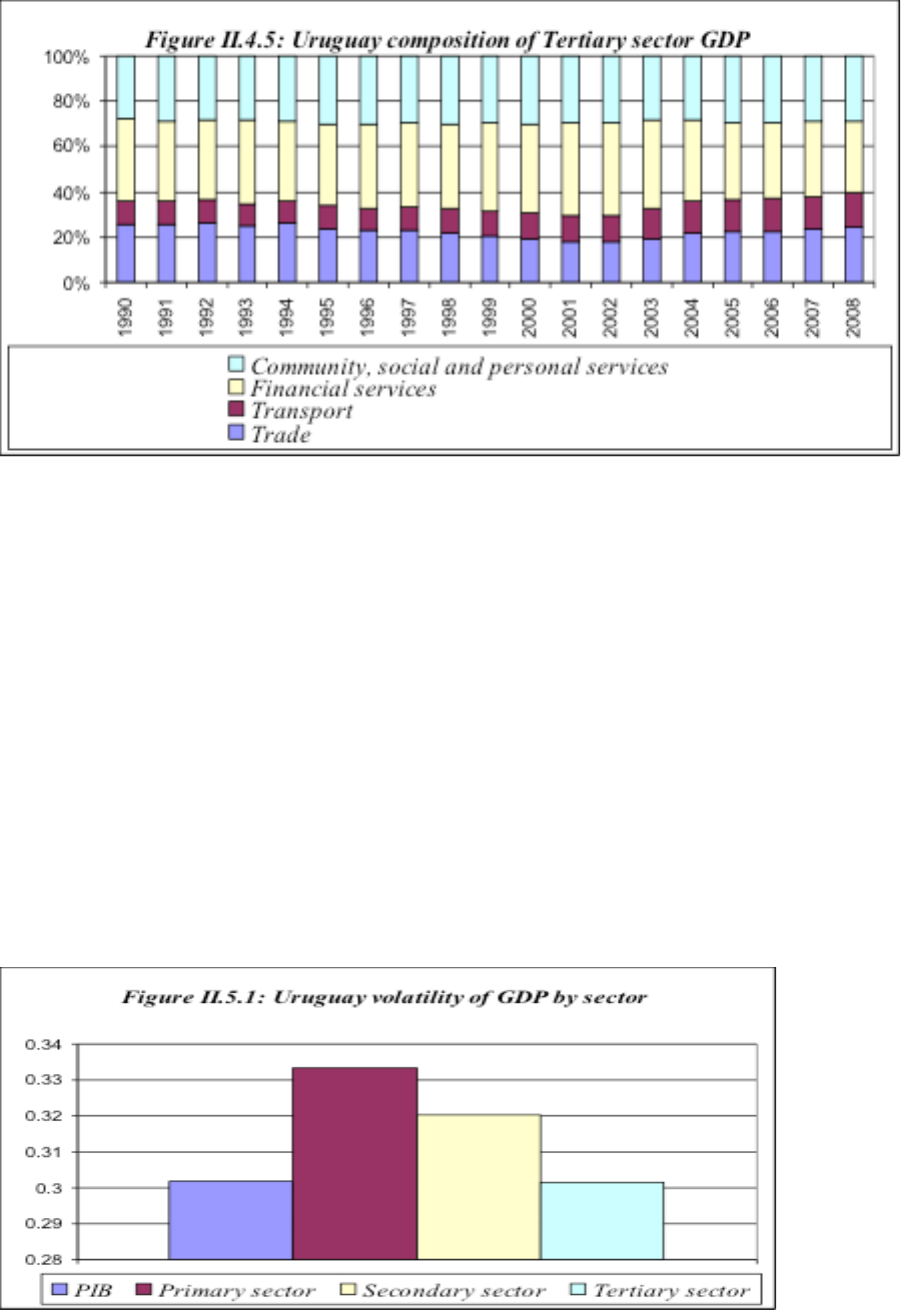

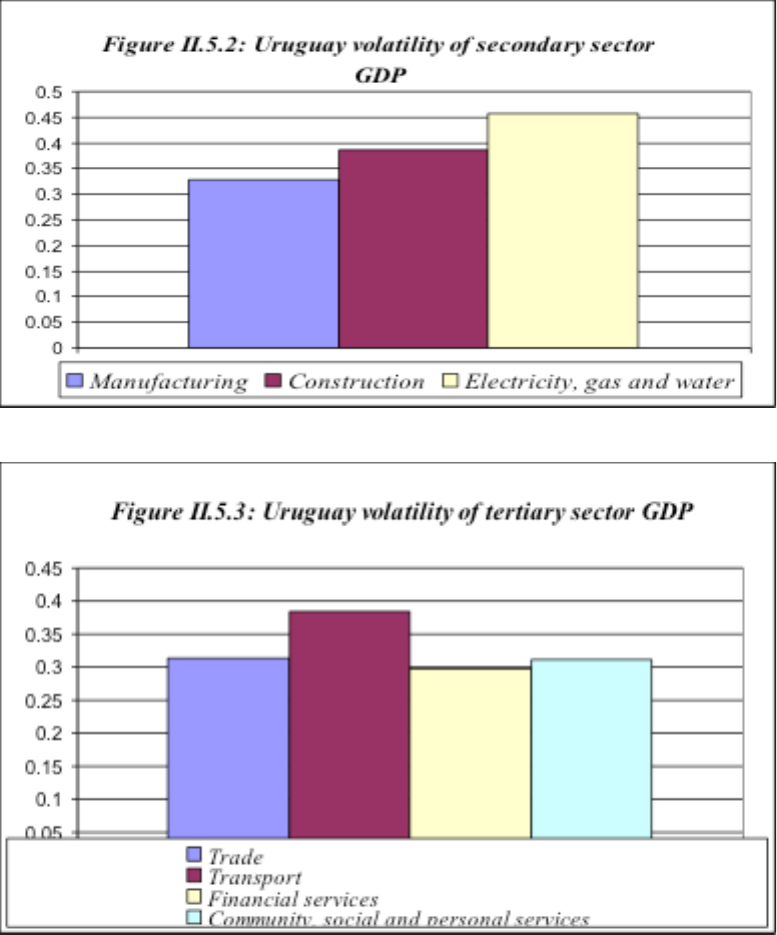

5. Volatility of Real GDP

In order to measure the variability of GDP, we use the coefficient of variation for total GDP

and its main sectors of origin. The primary sector presents the highest volatility, with a

coefficient of 0.33, higher than total GDP, 0.30. By individual sectors, electricity is the most

volatile, even more than agriculture. To a large extent the volatility of electricity is the result

of the weather, given that the value added of hydro-electrical generation, highly dependent on

rainfall, is much higher than that of thermo electrical generation. The rainfall changes the

composition of electrical generation and with that sectorial GDP.

Source: LE&F, based on information from UN ECLAC .

17

Source: LE&F, based on information from UN ECLAC.

Source: LE&F, based on information from UN ECLAC.

18

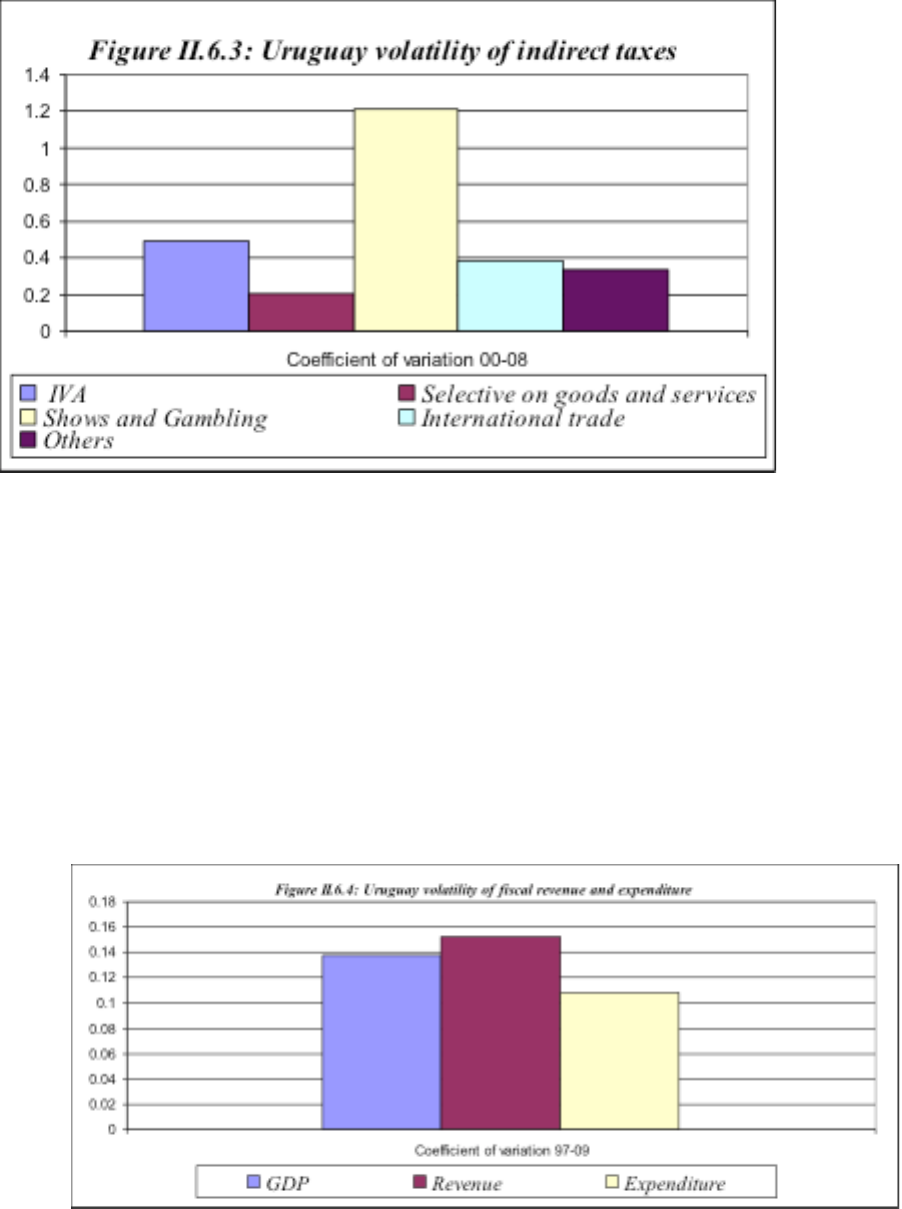

6. Volatility of Fiscal Revenues

Fiscal revenue is more volatile than fiscal expenditure. In turn, tax revenues are more volatile

than non-tax revenue. The revenue form the Value Added Tax (VAT) presents a slightly

higher volatility than total GDP, probably reflecting that the volatility of domestic demand is

higher than that of GDP, and that the VAT exemptions for exports imply that the VAT tax

base is domestic demand rather than output.

Source: LE&F, based on information from Contaduría general de Uruguay.

Source: LE&F, based on information from Contaduría general de Uruguay.

19

Source:

LE&F, based on information from Contaduría general de Uruguay.

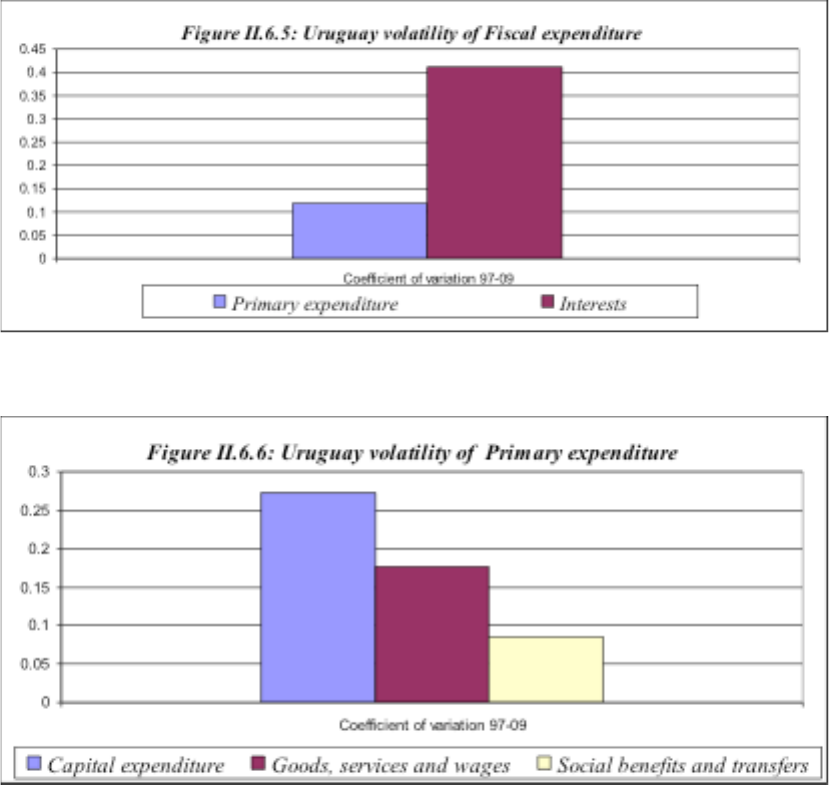

Interest expenditure is more volatile than primary expenditure, and within this item, both

spending on goods and services and capital spending have a volatility higher than that of

social spending which seems quite protected by policies from the ups and downs of domestic

activity and fiscal revenue. While the volatility of interest expenditure seems to reflect the

volatility of the exchange rate and of international interest rates, the volatility of capital

expenditure is residual, that is reflects the efforts of conforming the fiscal balance to

available resources.

Source: LE&F, based on information from Contaduría general de Uruguay.

20

Source: LE&F, based on information from Contaduría general de Uruguay.

Source: LE&F, based on information from Contaduría general de Uruguay.

21

III. Estimating and Projecting the Structural Fiscal Balance in Uruguay

Uruguay is an open economy that exports a variety of agricultural commodities, including

meat, rice, wool, leather and others. However, its degree of specialization is lower than that

of other Latin American countries where the main export item plays a significant role in the

generation of fiscal revenue. That is the case of oil in Venezuela, Ecuador and Trinidad and

Tobago, or of Copper in Chile and Peru. A combination of a tax structure focused on

domestic spending and the relative export diversification of Uruguay implies that the

volatility of total fiscal revenue is mostly associated to the cycle of GDP, and not to the

evolution of the price, cost and export of some of the agricultural commodities exported. The

methodology to estimate structural fiscal revenue will then focus in the estimation of trend

and transitory GDP and their effects on fiscal revenue and the fiscal balance. To the extent

that the information is available, we will follow the procedures identified by the OECD in a

similar way as it has been implemented by the Chilean government over the last decade.

1. Estimation of Trend or Structural GDP

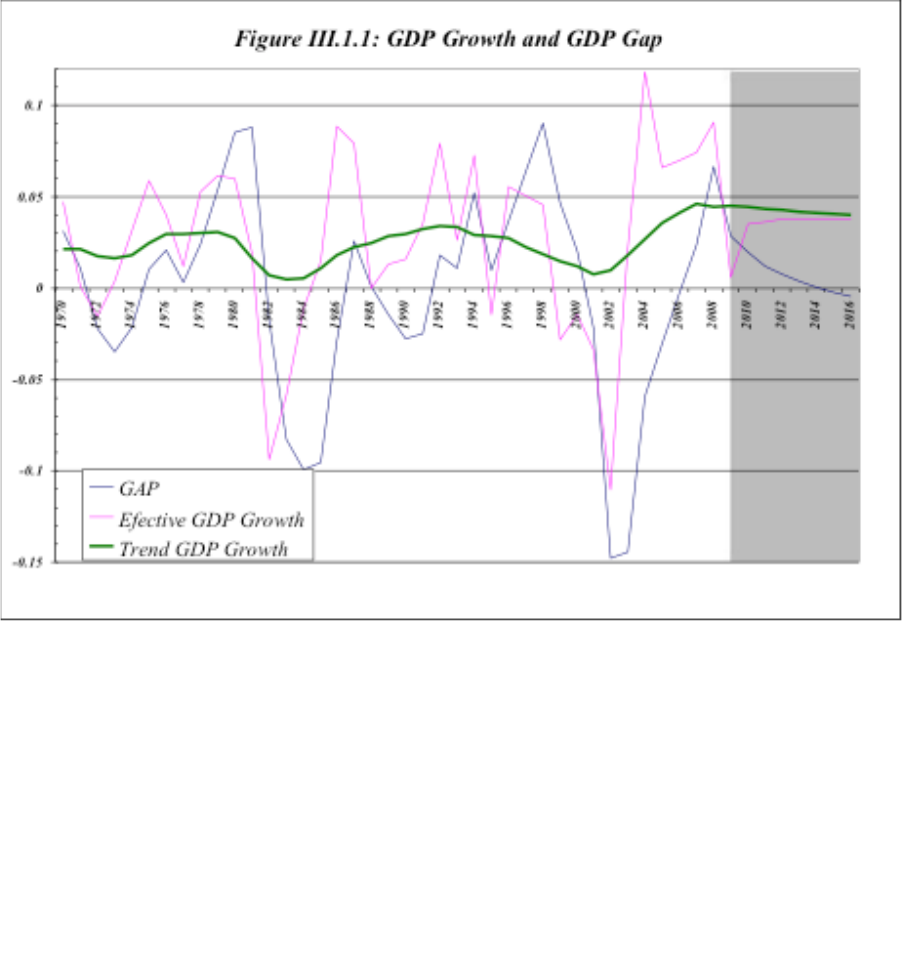

Real GDP (y) can be analytically decomposed in a permanent (Yp) and a transitory

component (Ytran). The log of transitory GDP, also called the GDP gap, is positive in

expansionary periods, negative during slow downs and recessions and cero during neutral or

normal periods, besides its mean is also cero.

Y

t

tran

t

P

tt

tran

t

P

tt

gapyyyyyy ==−+= logloglog;logloglog

Permanent GDP is estimated from a Cobb Douglas production function with constant returns

to scale, where A is total factor productivity, K capital, N effective labor and a the share of

capital in total income. The superscript P is used to represent the permanent or trend

component of the corresponding variable, total factor productivity, capital stock, and

effective labor. In selecting the capital and labor shares we use the results of previous works,

Theoduloz (2006), where a is a constant estimated equal to 0.27

2

.

P

t

P

t

P

t

P

t

P

t

P

t

PP

t

NKAy

NKAy

log)1(logloglog

;)()(

)1(

αα

αα

−++=

=

−

2

Ideally, alpha should be obtained from the national income accounts, considering it represents the share of

capital in the functional distribution of national income. Such source of data is not available in Uruguay.

22

Source: LE&F, based on information from ECLAC, INE and CERES.

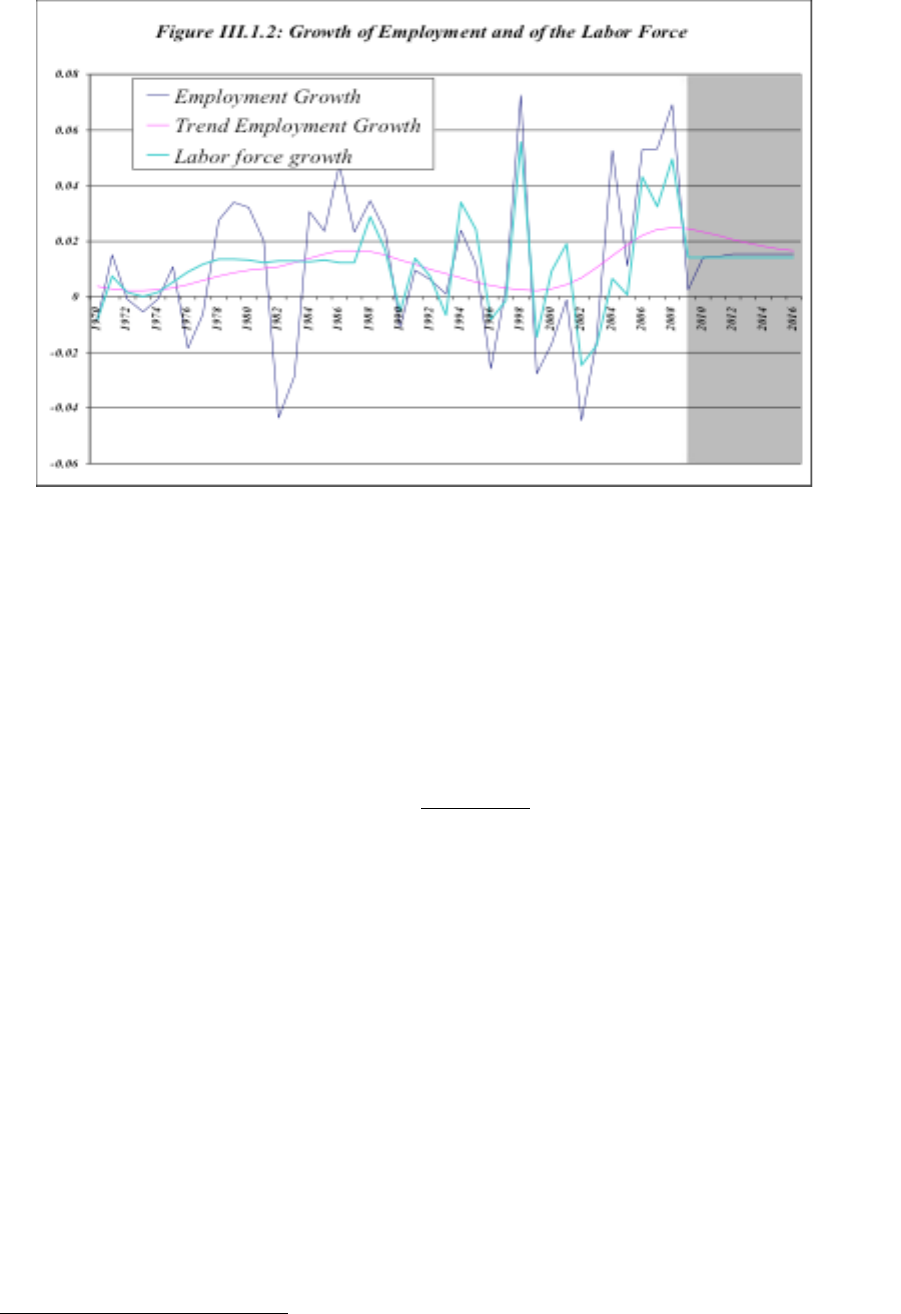

Effective employment (N) can be defined as the total hours of effective work, and calculated

multiplying the number of employed workers (N#) by the average number of hours worked

(h) and by the average years of schooling (s). The series on the number of workers N# was

obtained from the ECLAC and INE for the period 1970-2009. Unfortunately the series on

average number of hours worked and average years of schooling of the labor force are not

available, thus we have assumed value 1 for all observations of both variables.

;# shNN

ttt

××=

23

Source: LE&F, based on information from ECLAC and INE.

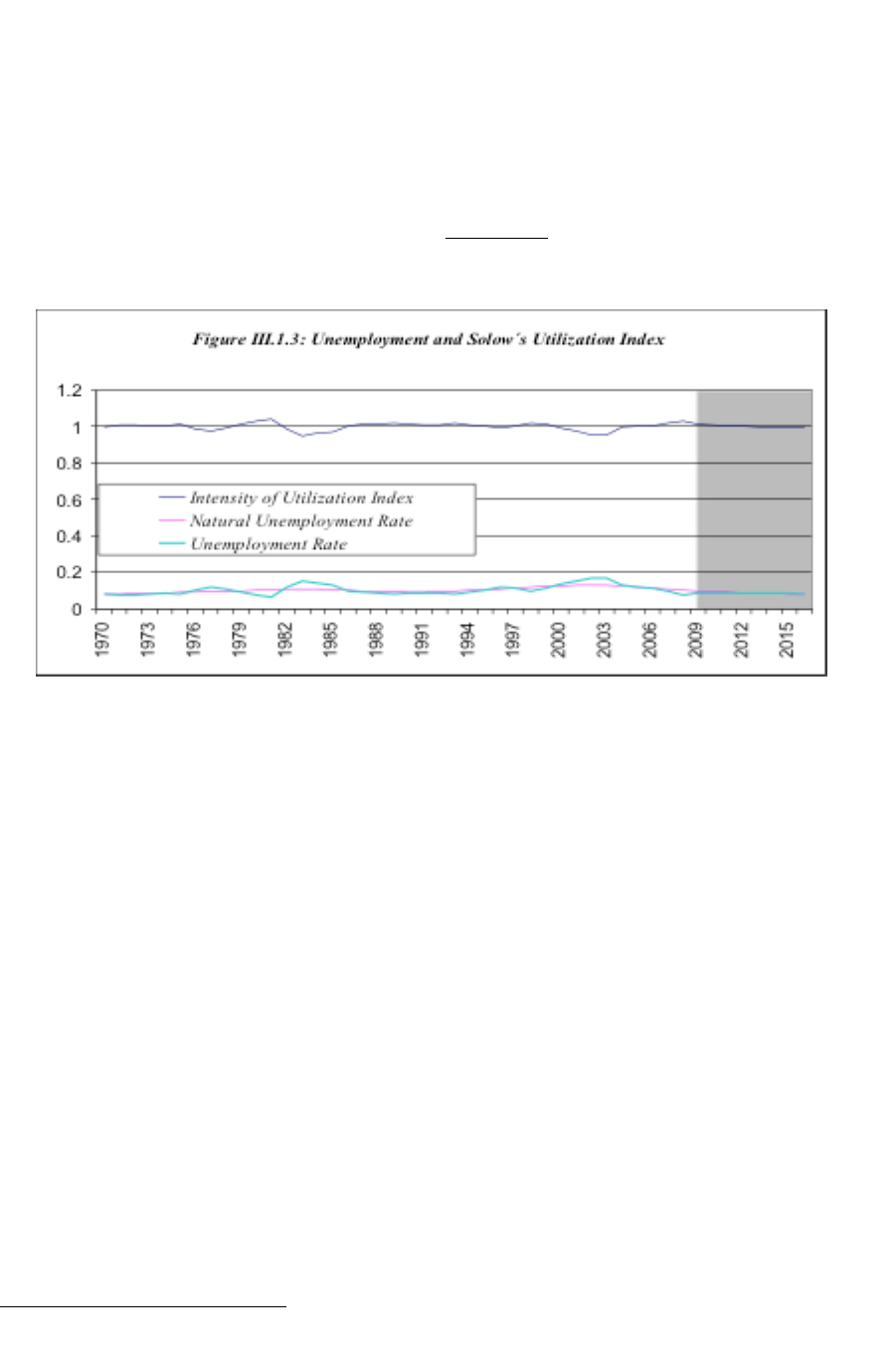

The degree of utilization of Labor and capital is derived from the unemployment rate (U)

which is defined as the difference between the labor force (L) and the number of people

employed N#, as a percent of the labor force

3

. Trend or natural unemployment is obtained

applying a HP filter to the unemployment rate series

4

.

)(

#

t

P

t

t

tt

t

UHPfilte rU

L

NL

U

=

−

=

The trend value of effective employment is obtained applying a Hodrick and Prescott filter

(HP filter) to the series of labor force L, and multiplying it for one minus the natural

unemployment rate. Over the last years and with the recovery from the debt crisis, the rate of

growth of trend employment has increased reaching a maximum slightly above 2 percent per

year. Given the demographic projections the trend growth rate of employment will be

gradually declining below 2 percent over the next decade.

)1()(

P

tt

P

t

ULHPfilterN −×=

3

The source of the series on the labor force and employment is ECLAC and INE

4

The OECD recommendation is to use a lambda value of 100 for obtaining the trend unemployment rate, where

lambda is the HP filter parameter.

24

The Solow index of the intensity of use is defined on the basis of the regular and natural

unemployment ratios, so that the index value is 1 when the unemployment rate is equal to the

natural unemployment rate and less than one when effective unemployment is above the

natural rate.

)1(

)1(

P

t

t

t

U

U

S

−

−

=

Source: LE&F, based on information from ECLAC and INE.

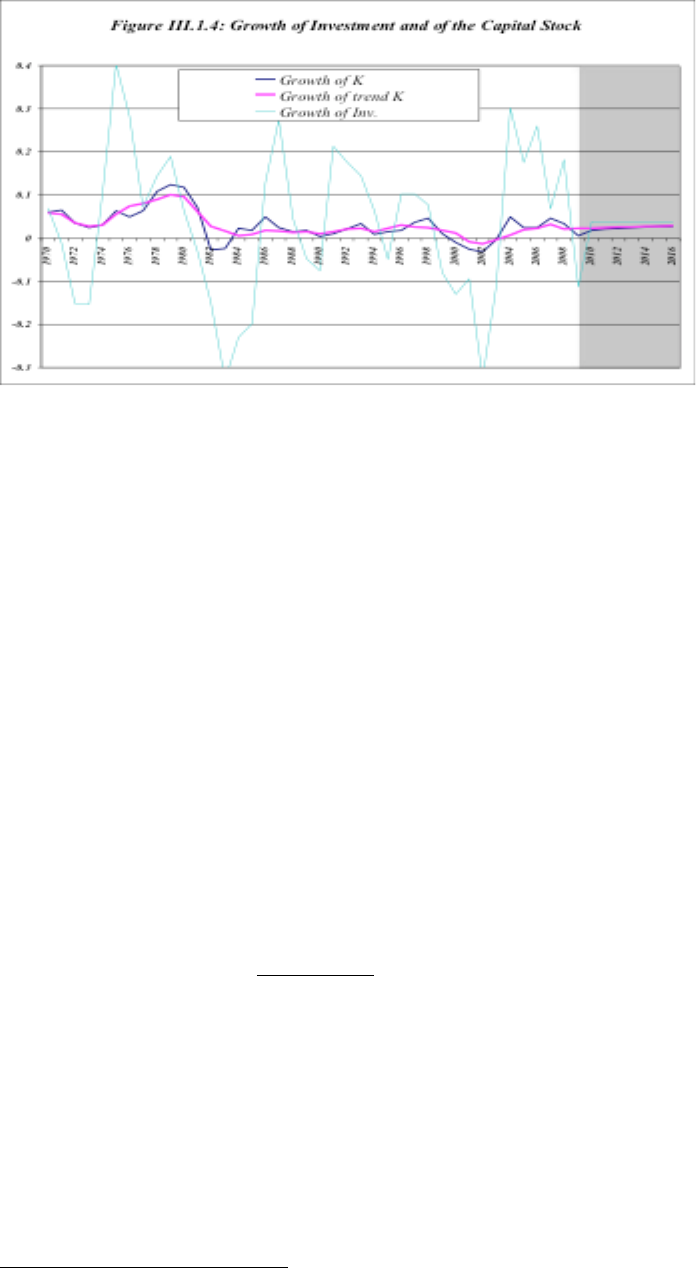

The estimation of the capital stock is based on the regular inventory accumulation equation,

where K is the capital stock, I is investment, defined as the fixed gross capital formation, and

d is the depreciation rate. The series on gross capital formation was obtained from the

ECLACC and CERES, and the depreciation rate was obtained from World Penn extended

table. The initial value for the capital stock implies a capital labor ratio equal to 1.6 in 1970.

5

On the basis of an estimated growth rate of Gross Capital formation of less than 4 percent

over the next few years, the trend growth rate of the capital stock remains slightly below 3

percent, implying a continuous decline in the capital-output ratio.

t

P

t

P

t

IKK +−=

−

)1(

1

δ

5

The initial estimate of the capital stock (1970) was obtained from the data on fixed capital formation and

depreciation using a regular inventory methodology see Haindl and Fuentes (1986).

25

Source: LE&F, based on information from ECLAC and CERES.

The estimation of the effective capital stock K is obtained by correcting the trend capital

stock K by the Solow intensity of use (S):

t

P

tt

SKK ×=

Finally, total factor productivity TFP is derived as a residual using the production function

and effective data on GDP, capital, adjusted by the intensity of use, and effective

employment. To obtain the permanent or trend total factor productivity we applied the

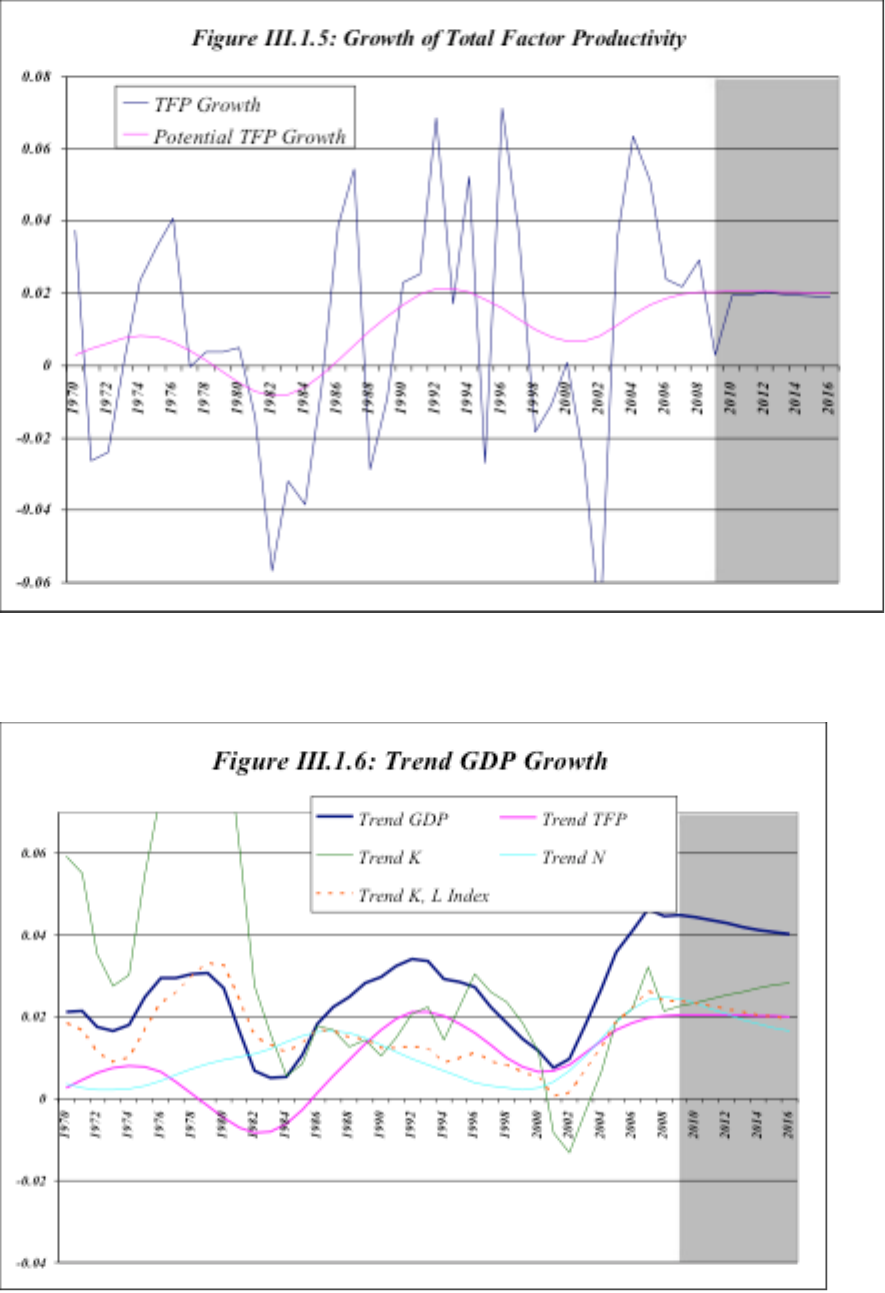

Hodrick and Prescott filter to the TFP series. Surprisingly enough, trend productivity growth

not only has increased to about 2 percent per year, but also is projected to remain at that

expansionary rate over the next few years.

6

tttt

tt

t

t

NKyA

NK

y

A

log)1(logloglog

;

)1(

αα

αα

−−−=

=

−

)(

t

P

t

AHPfilterA =

6

We have used the IMF WEO projections for real GDP growth through 2016, and assumed that the investment

to GDP ratio will continue at its average value of the last five years, thus deriving a gross capital formation

estimate. To project employment we assume that the unemployment rate will converge to the last observation of

the natural unemployment rate and considered that the labor force would increase with the working age

population.

26

Source: LE&F, based on information from ECLAC and CERES.

Source: LE&F, based on information from Banco Central de Uruguay.

27

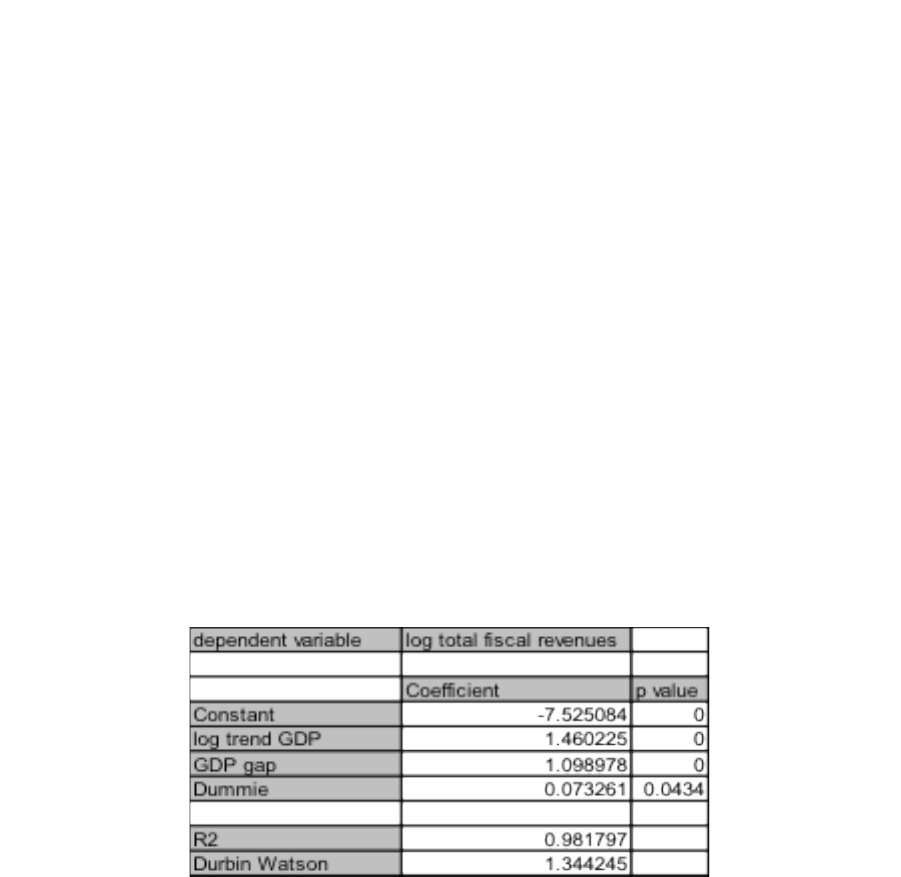

The results indicate that over the last few years, the growth of trend GDP in Uruguay has

been accelerating reaching a rate slightly above 4 percent per year. Growth has then

stabilized but our projections indicate a convergence of trend GDP growth to about 4 percent

during the second decade of the 21st century. The forecasted rate of expansion for trend GDP

is significantly above its historical value, with ups and downs around 2 percent, and could be

affected by the recent recovery. The assumptions used for future GDP, labor force and gross

capital investment growth are subject to discussion and for that reason should be derived

from the opinions of several experts on the Uruguayan economy, and revised annually.

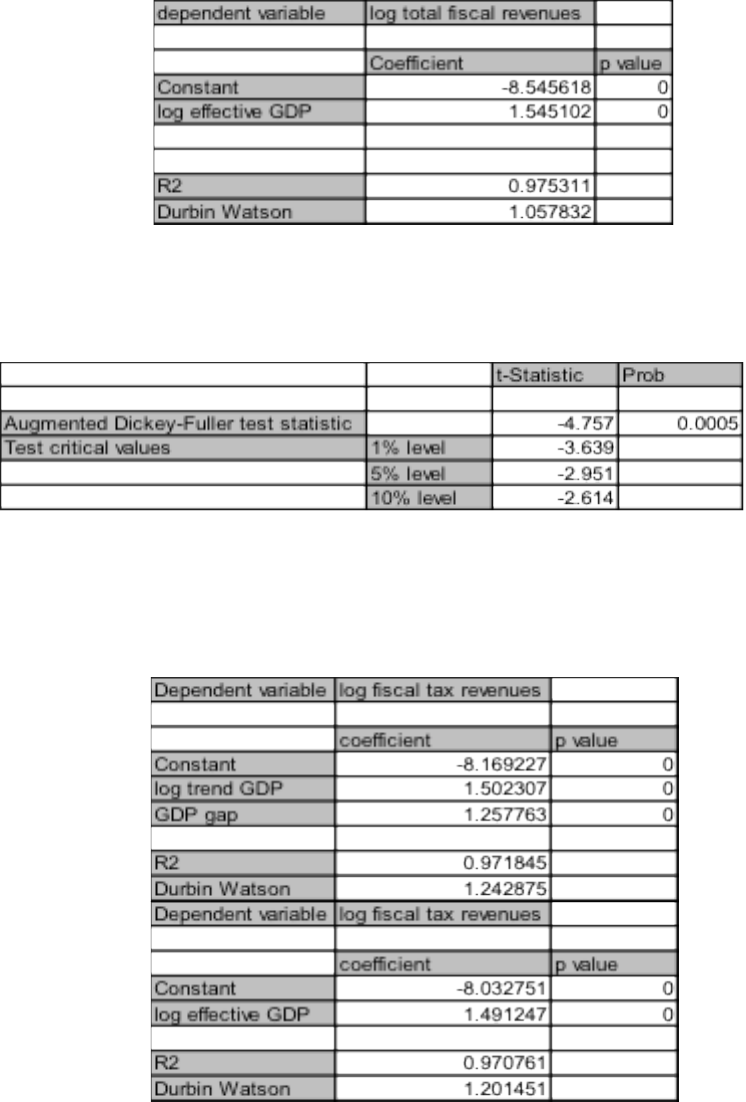

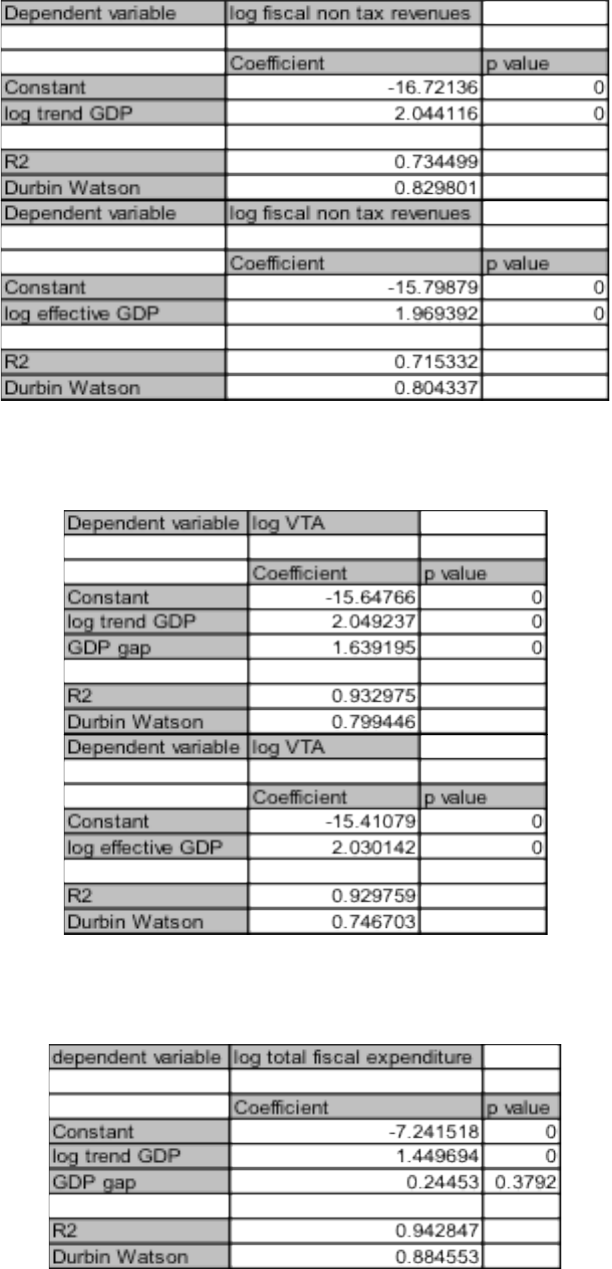

2. Elasticities and the Structural Balance

The estimation of the structural fiscal balance requires the estimation of a stable relationship

between fiscal revenue and its components with trend GDP and the GDP gap. The elasticity

of fiscal revenue with respect to trend GDP is going to play a pivotal role in determining the

value of the structural revenue and the structural balance. The estimated regression is of the

following form,

tt

y

t

P

tt

DgapyT

εββββ

++++=

1997

3210

loglog

Where T represents the real fiscal revenue, total or components, Yp the permanent GDP, gap

y the GDP gap and D1997 a qualitative variable to represent the structural break that

represents the policy reaction that resulted in a structural break in the level of Public sector

revenue in Uruguay.

Table III.2.1: Regressions for Total Fiscal Revenue and GDP

28

Source: LE&F, based on information from ECLAC and CERES.

Table III.2.1.i: Co-integration Analysis (residual test)

Source: LE&F, based on information from ECLAC and CERES.

Table III.2.2: Regressions for Tax Revenue and GDP

Source: LE&F, based on information from ECLAC and CERES.

29

Table III.2.3: Regressions for Non-tax Fiscal revenue and GDP

Source: LE&F, based on information from ECLAC and CERES.

Table III.2.4: Regressions for the VAT and GDP

Source: LE&F, based on information from ECLAC and CERES.

Table III.2.5: Regressions for Fiscal Expenditure and GDP

30

Source: LE&F, based on information from ECLAC and CERES.

The results of the estimation indicate that the elasticity of revenues to trend GDP is

somewhat greater than one in which the structural break is in general significant. Moreover,

both fiscal revenues and fiscal expenditures present a pro cyclical response to GDP, given the

positive and significant elasticity of revenue and expenditure with respect to the GDP gap.

7

Conceptually, the structural fiscal balance is the one that would have existed if GDP

were at its trend level. Correspondingly the structural fiscal revenue is the revenue that would

have been obtained under a zero gap. Then the structural fiscal balance is defined as the

difference between the total structural fiscal revenue and the total fiscal expenditure. The

estimation of the total structural revenue can be obtained using the estimated regression for

total revenue, and assuming a zero gap:

Thus the structural fiscal balance is

t

P

tt

GTSFB −=

Government revenue (T) has a permanent (TP) and a transitory (Ttran) component

tran

t

P

tt

TTT +=

Which can be expressed as a percent of GDP in lower case letters:

tran

t

P

tt

ttt +=

The primary fiscal balance is obtained by excluding the interest expenditures. The structural

primary balance, psb, is derived subtracting the transitory revenue.

7

In addition, the regular co-integration analysis was carried out for the fiscal revenues and tax equation, and it

was obtained that the residuals of the main regression (Table III.2.1) are stationary, so that these variables co-

integrate among themselves.

31

tranD

ttt

tranD

t

DP

tt

tpsbpgttpfb

,,

+=−+=

The structural fiscal balance (sfb) can be obtained subtracting from the primary surplus the

interest expenditure.

ttt

P

tt

igpsigpgtsfb −=−−=

*

The actual fiscal balance (fb) is the structural balance plus the transitory revenue, which can

be positive or negative. Any positive transitory revenue is to be saved in the form of a larger

fiscal balance, and any negative transitory revenue dis-saved through a smaller fb or larger

deficit.

tran

tttt

tran

t

P

tt

tsfbigpgttfb +=−−+=

In the case of Uruguay, permanent and transitory fiscal revenue stems from the business

cycle that gives rise to fluctuations in the domestic revenue (DT). The ups and downs in GDP

result in ups and downs in domestic revenue (DT):

t

P

tt

P

tt

YYYDT

εβββ

+−++= ]log[logloglog

210

Where bo, b1 and b2 are parameters to be estimated and e represent the disturbances of the

domestic revenue equation. In some specifications used by the OECD b2 is considered equal

to cero, however we consider that excluding the gap from this equation may bias the estimate

for the elasticity with respect to trend GDP. We can distinguish permanent or structural

revenue from transitory revenue.

P

ttt

P

tt

tran

t

P

t

P

t

DTDTYYDT

YDT

loglog]log[lo glog

loglog

2

10

−=+−=

+=

εβ

ββ

Presenting revenue in percent of GDP

32

t

P

tt

tran

t

P

tt

tran

t

tt

P

tt

tran

t

t

P

t

P

t

Y

DTDT

dt

DTDTDT

YYYdt

YYdt

−

=

−=

+−−=

−+=

εβ

ββ

log]log[loglog

logloglog

2

10

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0.04

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

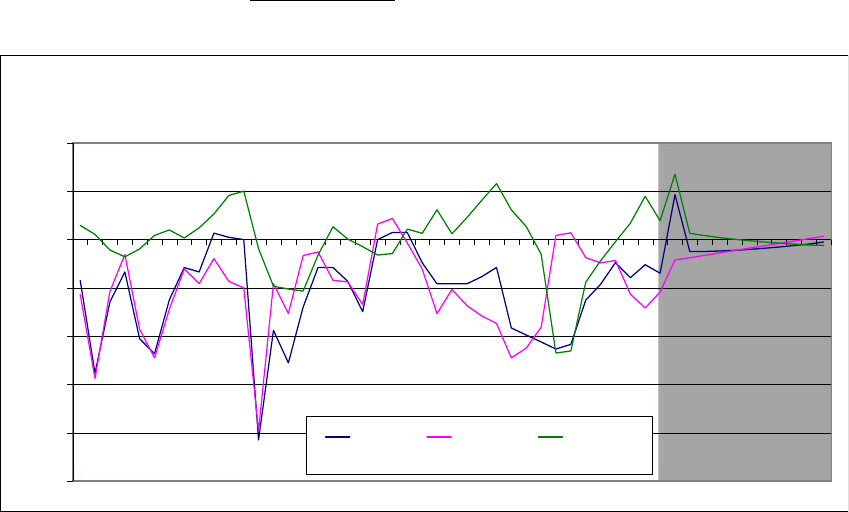

Figure III.2.1: Fiscal balance evolution (as GDP percent)

Effective

balance

Structural

balance

Cyclical

component

Source: LE&F, based on information from ECLAC and CERES.

Our estimates indicate that Uruguay’s total structural fiscal balance has remained in deficit

almost continuously, exception made for a brief period of zero structural balance in the early

1990s. The debt crisis of 1982 had implied a large widening of the structural fiscal deficit and

a continuous adjustment effort followed, reaching its peak results in terms of fiscal

consolidation in 1989-1992. From then on a sustained deterioration in the structural fiscal

balance took the deficit to a new local maximum of 4 percent of GDP in the years of the turn

of the century (1999-2002). The adjustment that followed the last debt crisis once again

reduced the structural fiscal deficit to 1 percent of GDP for a few years, but the structural

deficit has recently widened to about 2 percent of GDP in 2009. Despite the improvements in

public finances of the last 5 years by no means Uruguay is out of the woods, as it has

happened before the debt level may again rise to critical levels unless a structural fiscal

policy committed with the reduction of the vulnerabilities of the public finances is

33

implemented. That would require a return of the fiscal balance or slight surplus similar to the

one carried out during the early 1990s.

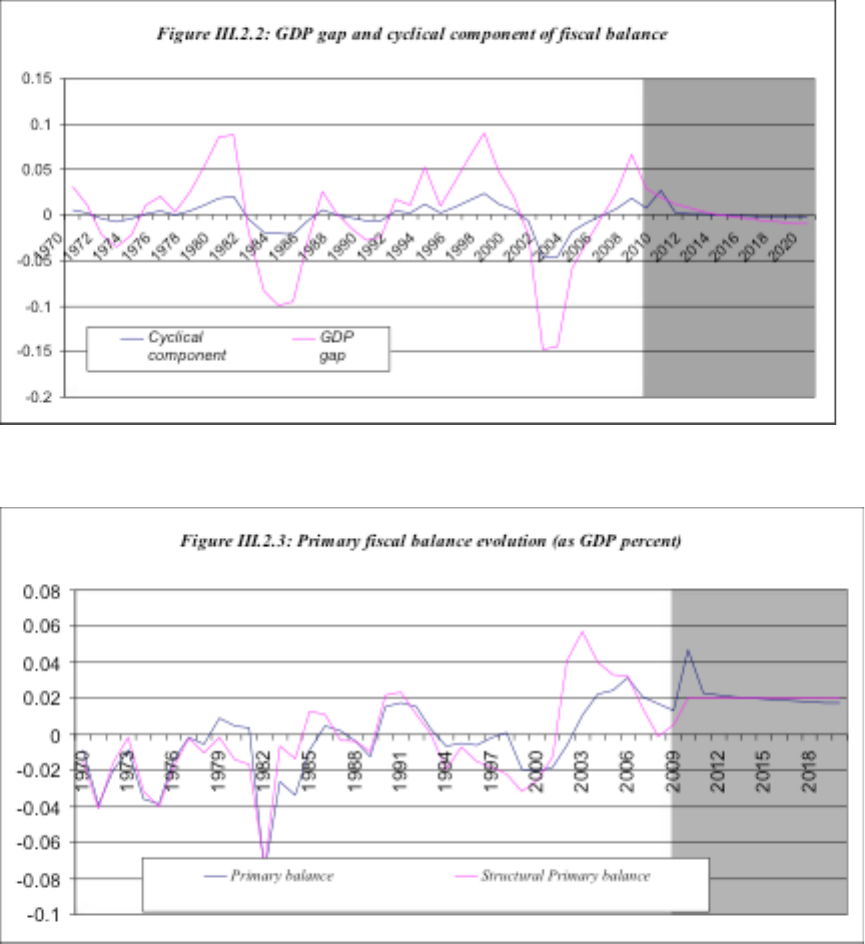

Source: LE&F, based on information from ECLAC and CERES.

Source: LE&F, based on information from ECLAC and CERES.

The structural primary balance in Uruguay has fluctuated around 0 with some periods of deep

deficits and a few years of sustained surpluses. The deficit periods are associated with the

debt crisis of 1982 and the debt crisis of 2002; actually a succession of primary deficit

preceded the last debt crisis. The most notable surplus periods are two, the first stabilization

effort of the early 1990s that resulted in a sustained reduction on the inflation rate. The

second is the recent adjustment that followed the debt crisis of 2002 generating large

34

structural primary surpluses, of up to 4 percent of GDP in the period 2004-2007. However,

since then the structural primary surplus has fallen below 1 percent of GDP in 2008 and

2009.

3. Fiscal Projections

In the fiscal projections exercise we assume an active policy scenario in which a structural

fiscal policy is implemented. Primary government expenditure as a percent of GDP (pg) is

budgeted on the basis of permanent revenue (tP) and the fiscal target for the primary balance

(ps*). Interest spending (ig) is predetermined by debt contracts, added to primary spending

we obtain total government expenditure (g).

*

pstpg

P

tt

−=

t

P

tttt

igpstigpgg +−=+=

*

To define the budget for primary expenditure (pg) it is necessary first to estimate the

structural fiscal revenue (tP) and then to set the fiscal target for the primary structural balance

ps*. The future structural fiscal revenue is to be obtained from the estimation of the future

trend GDP, for that purpose we use the estimated elasticity of fiscal revenue with respect to

trend GDP.

P

t

P

t

YDT

1101

loglog

++

+=

ββ

The future value of trend income has to be estimated on the basis of the production function,

using projected future values for trend productivity (Ap), trend Capital stock (Kp) and trend

employment (Np).

P

t

P

t

P

t

P

t

NKAy

1111

log)1(logloglog

++++

−++=

αα

)(

11 ++

=

t

P

t

AHPfilterA

Trend productivity can be obtained applying an HP filter to the series of actual and projected

productivity. For that purpose projections of A through 2020 were used.

itititit

NKyA

++++

−−−= log)1(logloglog

αα

35

For consistency the projected values for total factor productivity (A) should be obtained as a

residual from the projections of GDP, Capital and Labor.

11

)1(

++

+−=

t

P

t

P

t

IKK

δ

Trend capital is equal to total capital and the projections for K can be obtained on the basis of

the inventory equation and projections for gross capital formation. Again we projected the

capital stock adjusted for the intensity of use through 2020.

)1()(

11

P

tt

P

t

ULHPfilterN −×=

++

Finally, the projection of trend employment requires the projection of the trend labor force,

and of the trend unemployment rate. Summing up, projections through 2020 were used for

GDP, gross capital formation, labor force and the unemployment rate. From there the

budgeting process can derive trend GDP and thus the trend fiscal revenue. Given the target

for the structural balance, the budgeted primary fiscal expenditure is to be obtained. In this

exercise we used the WEO projections for GDP growth through 2016 and assumed a stable

growth rate afterwards at the level of the last observation. Investment was projected assuming

that the last five-year average for the investment GDP ratio will prevail in the future. Finally,

the projected expansion of the working age population was used to project labor force, and

the stabilization of the unemployment rate at the natural rate value was used to derive

effective employment.

4. The Structural Fiscal Target

The proposed structural fiscal target has to be derived for the structural primary balance. The

target for the structural primary balance should be defined so as to provide fiscal

sustainability by meeting certain goals for the relevant definition of the public sector net

financial wealth (B). The fiscal balance represents the change in financial wealth. It is equal

to the primary balance and net interest, where i is the nominal interest rate.

36

tttttt

IGPFBIGPGTFB −=−−=

111 −−−

+=+−=−

ttttttt

iBPSiBPGTBB

We can define the wealth equation for the primary surplus:

1

)1(

−

++=

ttt

BiPSB

Defining the variables as a percent of GDP, where p is inflation and l real GDP growth, and r

the real interest rate.

1

1

1

)1)(1(

)1(

)1(

−

−

−

++

+

+=×++=

t

tt

t

t

t

t

tttt

b

i

psb

Y

Y

bipsbb

πλ

11

)1(

)1(

)1(

−−

++=

+

+

+=

tttt

t

t

tt

bpsbb

r

psbb

ψ

λ

The idea is to find a permanent target for the primary structural surplus psb*, which we will

assume to be constant. In addition we will assume constant real interest rate and constant

growth rate, so that the wealth equation is transformed to:

1

)1(

−

++=

tt

bpsbb

ψ

Where the discount factor is:

)1(

)1(

)1(

λ

ψ

+

+

=+

r

Developing the wealth equation for future periods:

1

2

1

)1()]1(1[)1(

−+

++++=++=

ttt

bpsbbpsbb

ψψψ

1

32

2

)1(])1()1(1[

−+

++++++=

tt

bpsbb

ψψψ

37

1

1

0

]1[]1[

+

−

=

+

+++=

∑

N

t

j

N

j

Nt

bpsbb

ψψ

The value for the targeted psb* depends on the initial wealth level b(t-1), the discount factor,

the target for the wealth level b(t+N), and the number of periods to reach the target (N). If the

fiscal target were set to keep constant the wealth to GDP ratio at its initial level b(t-1), then

*

0

1

1

]1[

])1(1[

psb

b

j

N

j

N

t

=

+

+−

∑

=

+

−

ψ

ψ

Otherwise, a given target for the wealth to GDP ratio at a given horizon of N years into the

future b(t+N) would give the general result for the annual structural fiscal target.

*

0

1

1

*

]1[

]1[

psb

bb

j

N

j

N

tNt

=

+

+−

∑

=

+

−+

ψ

ψ

To calculate the fiscal target and as shown in the above equation, there are several

information requirements. First about debt or public sector wealth, including actual, in the

last period available, and targeted debt, second about the discount factor for which we need

the real interest rate and the real growth rate, and, finally, the horizon in which the debt target

is to be met. The debt information was obtained from the central bank of Uruguay; the

growth rate used is that obtained previously as the projected potential growth rate of the

economy. We recognize that different views are possible regarding the future growth of the

Uruguayan economy, our estimate of 4 percent sustained real GDP growth may seem high

for historical standards in this country

8

. However, the trend growth rate will be endogenous

to the policies implemented which can easily reduce or increase the sustained growth rate

through their effect on productivity growth, i.e. incentives for innovation, capital stock

8

Using the WEO projections for economic activity, and under assumptions for investment, working age

population and productivity growth rates

38

growth, i.e. incentives on savings and investment, and labor growth, incentives on migration

of the qualified labor force. Different views may exist about the future trend GDP growth of

the Uruguayan economy, and the views may change over time.

Given that Uruguay is a debtor country, we estimate the relevant real interest rate on

the basis of an indicator for the real return on global assets and a representative risk spread

for Uruguay. The real global rate of return in the long run is estimated on the basis of the

average annual growth rate of JPM Global Bond and MSCI all countries indices, both in real

terms. We assume an equal weight for both indices to represent a global portfolio and its

historical average real return in the long run of it is to be considered the global real interest

rate that will prevail in the future. Our estimation indicates a global long run real interest rate

of 4.65 percent. However that is not the relevant rate for the Uruguayan public sector that

borrows at that rate plus a risk spread. To estimate the relevant Uruguayan spread we

compare the actual returns of the Uruguayan debt (actual real interest rates) with the historic

global rate of return, yielding an average spread of 1.1 percent. Thus the Uruguayan log run

real interest rate on debt was estimated at 5.75 percent.

Again, as in the case of the real growth rate, the estimate for the interest rate of the

Uruguayan debt over the long term is subject to discussions and different views. The one

presented is our best guess with the information and expertise available, but the spread of he

Uruguayan debt is endogenous and in the future will reflect the risk that markets give to its

repayment. A virtuous cycle of lower deficit, lower debt, and lower spread is possible, but

also is possible a vicious one of higher deficit, debt and spread. A repeated assessment of the

debt risk is required to estimate the future values of the spread.

Given that it is not possible to determine a single horizon and a single debt target that

would be appropriate for Uruguay we present a table considering a range of possibilities for a

given value of the discount ratio psi, which was estimated at 1.549 percent. For the time

horizon we consider a wide range from 5 to 50 years, considering as a minimum the period of

one Uruguayan government, and as a maximum the period of ten governments. To set a

target for such a long period, a very solid political consensus should be developed to back the

structural fiscal policy. For the future public wealth target we also considered a relatively

large range of options, from -50 percent of GDP similar to the existing level of public debt, to

+10 percent of GDP similar to the public sector wealth accumulated by Chile at the end of

2009, before the earthquake.

39

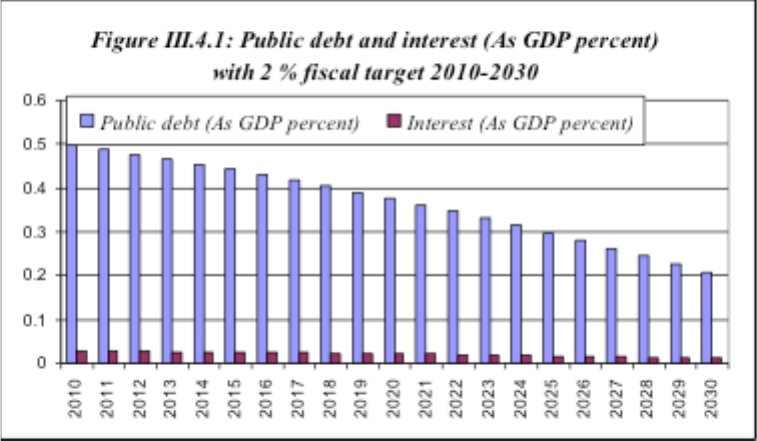

Table III.4.1: Fiscal targets for the primary balance as percent of GDP

Source: LE&F, based on information from ECLAC and CERES.

As is evident in Table III.4.1, the longer the time horizon to fulfill the fiscal target, the

lower is the required primary balance target. On the other hand, the more demanding is the

wealth target, the higher is the required primary balance. To attain a wealth target of -50

percent of GDP, that is a net debt level equivalent to 50 percent of GDP and similar to the

existing starting point, a sustained 1 percent (0.8 percent -0.9 percent) of GDP of structural

primary fiscal surplus is required regardless of the time horizon considered. That would be

the lowest possible primary balance target consistent with debt sustainability: one to conserve

the existing public debt level. On the other extreme, attaining a public sector wealth goal of

10 percent of GDP

9

in a 10 years horizon would require a sustained structural primary

surplus of almost 6 percent of GDP, and achieving the same goal in twice the time horizon

(20 years) would require a surplus slightly above half the previous, 3.3 percent of GDP.

From inspection the fiscal target cannot be less that a sustained primary surplus of 1

percent of GDP. However a desirable target ought to be higher than that one that only

maintains the wealth level at the actual one. Currently in Uruguay, 70 percent of the debt is

denominated in foreign currency, despite all the efforts applied by the authorities to change

debt denomination from US dollars to the unit indexed to GDP. Thus, an exchange rate shock

would increase the debt ratio very significantly. Under a real exchange rate shock of a 50

percent real depreciation, the debt to GDP ratio would jump from 49 percent of GDP to 66

percent of GDP even if the total fiscal balance is zero. A debt ratio of 66 percent of GDP is

already in the vulnerability zone, and is higher than the debt level that Uruguay had before

the last crisis.

A 50 percent increase of the real exchange rate is not unlikely considering the

country’s vulnerabilities as presented in the history of this variable in Uruguay. Moreover,

several analysts consider that currently the real exchange rate is 25 percent to 35 percent

overvalued as compared to its long-term equilibrium. If the debt ratio were to be reduced to

9

Similar to the wealth level of the Chilean public sector at the end of 2009.

40

20 percent of GDP it would be possible to concentrate the debt reduction (30 percent of

GDP) in eliminating debt denominated in foreign currency. Under those conditions of

reduced share of foreign currency debt and lower debt level, even if the domestic currency

debt cannot be increased, a similar 50 percent real exchange rate shock would increase the

debt ratio only marginally, from 20 percent to 22 percent of GDP.

Our recommendation would be to set the debt goal in 20 percent of GDP (-20 percent

public sector wealth) and to give a total of 20 years to attain the debt goal. Under those

conditions the target for the structural primary fiscal balance would be a surplus of 2.0

percent of GDP. It can be verified on Table III.4.1 that a similar fiscal target would be

obtained to achieve the goal of a -40 percent of GDP fiscal wealth in more than 5 and less

than 10 years. Despite the recommendation, setting the fiscal target ought to be one of the

elements of the new institutional framework for fiscal policy in Uruguay.

Source: LE&F simulations.

41

Source: LE&F simulations.

Introducing a structural fiscal policy in Uruguay would not just be a tool to reduce the

cyclical fluctuations of fiscal expenditure, which are significant but no extreme so as to

justify the effort to build a complex political commitment. The increasing vulnerability of the

fiscal position and risk of repeating yet another episode of fiscal insolvency and financial

crisis are considered sufficient motivation. No individual government or political group in the

country can carry by itself the costs of initiating a long term fiscal consolidation knowing that

all its efforts of reducing debt and deficits may reduce its chances to remain in power an open

the possibility to other political group to run an expenditure binge in the future. Fiscal

consolidation should be part of a concerted effort, a national policy built on the basis of

permanent institutions that would give guarantees of a sustained effort that would yield

benefits to all.

42

IV. Preconditions and Recommendations for the Implementation of the

Fiscal Rule

The structural fiscal policy is based upon a national agreement on the importance of a rules

based fiscal policy, which is expressed in a policy framework used in the definition of the

budget with an explicit target for the structural primary balance derived from a medium-term

debt goal and projections for the structural or trend fiscal revenue derived from a

macroeconomic framework. The structural fiscal target, the debt goal and the macroeconomic

framework for fiscal policy are political decisions that should be defined democratically, but

with the technical backing of a group of experts. Besides, fiscal accounts, including revenues,

expenditure, assets and liabilities and their components must be fully transparent and public,

so that the compliance or noncompliance with the fiscal target is information known by all.

1. Improving the Budgetary Process

One of the characteristics of fiscal policy in Uruguay is its decentralized nature and the lack

of a macroeconomic framework in the definition of the five-year budget and for its annual

revisions. The budget process in Uruguay can be characterized as a process of aggregation in

which individual entities either present their own budget proposal to Congress or lobby in

both chambers so as to modify the budget presented by the Ministry of Finance. The MEF

has to fight against the pressure of political interests, congressmen and often other Ministries

in an effort to trim down the budget coming out from that process so as to limit the departure

from the expenditure level originally proposed. Some times the support of the President of

the Republic allows the MEF to cut down to size the proposed budget resulting from the

interaction of Congress and interest groups, others the final budget is not much different from

the expression of will of the individual public sector entities. At the end of the aggregation

process the size of the budget as well as its composition are the result of the political game

played by Congress, the individual interests and the MEF. In a democratic setting that would

be appropriate for the budget composition, the budget size should obey a rational application

of an inter-temporal budget constraint for the Public Sector and not a political game.

At the heart of this decentralized and aggregative budget process is the idea that

expenditures can be financed generically from “general government revenue” or from a

deficit. Consequently, Congress can add to the budget by stating that the additional

expenditures are going to be financed by one of this “generic sources”. The application of a

structural fiscal policy requires setting up a macroeconomic framework that represents the

43

inter-temporal budget constraint. Under that idea, the MEF should define an initial budget

proposal, which is to be developed on the basis of a macroeconomic framework that

considers a projected level for the government revenue and the target for the structural

balance in similar fashion as the one presented in the previous section. For that, the rules of

the budget process should be modified.

10

The budget discussion should be developed on the

basis of that initial proposal, and the modifications by Congress may consider reallocating

expenditure from item to item, or increasing expenditure. However, in this latter case the

initiative should also include an increase in government revenue (some tax measure or sale of

assets) that the MEF considers sufficient to cover the added expenditure. In short the budget

discussion would consist in the selection and application of priorities to decide the

composition of government expenditures and only under exceptional circumstances would

also include initiatives to increase the level of total expenditure, and if that is the case it

would not modify the projected fiscal balance.

The budget should set up an authorization to spend in well-defined items, including

some contingencies to be defined later. In addition to the spending level and composition, the

budget should set a level of projected revenue, projected fiscal balance, and the uses and

sources of any additional financing or financing needs. The additional financing or financing

needs may arise from the deviations in the level of actual government revenue from the one

projected in the budget. An authorization to issue debt up to certain amount could take care

of the financing needs that may arise if there is a short fall in the projected revenue.

Contributions to a sovereign “debt reduction” fund may be consider for the allocation of an

unexpected fiscal surplus. The sovereign fund should consider a limited number of low risk

assets in which to be invested, including the purchase of Uruguayan public debt.

2. Setting the Macroeconomic Framework for Fiscal Policy

The structural fiscal framework requires a number of macroeconomic variables that are

required to setup the target for the annual structural primary balance, those are a goal for

public sector wealth, and the number of years needed to achieve that goal. Besides the

framework also requires the projections for the macroeconomic variables needed to estimate

10

Mr. Ignacio de Posadas, a well-respected lawyer and former Minister of Finance and Senator, believes that an

interpretative law can be used to improve fiscal discipline. In essence Mr. de Posadas proposal considers that

every spending initiative has to be financed by genuine resources, which are defined as well identified sources

of government revenue and not just general resources or deficit financing.

44

the fiscal target and the structural fiscal balance, the long term real interest rate relevant for

Uruguayan debt, and trend GDP growth.

In one extreme it would be possible that the technicians at the Ministry of Finance

(MEF) could carry out all the estimations by themselves under the guidance of the current

Minister. However, that would not be representative of a national and permanent policy

framework, since the structural policy would be entirely under the control of the current

administration. A better possibility would be to limit the action of the technicians of the MEF

by giving them certain parameters on which to base their work. The fiscal target and

macroeconomic projections for trend GDP growth and the real interest rate relevant for

Uruguayan debt could be agreed by a technical commission of 5 members. All of them

should be reputed economists, that would be nominated by the government with the approval

of the Senate and that would represent the different points of views on fiscal policy. They

would give to the government once every 5 years a target for the primary balance, supported

on a goal for the fiscal wealth, a time horizon to attain such goal, and estimates on the long

term relevant real interest rate and the long-term growth rate of GDP for Uruguay.

The technical commission would also give to the MEF annually their projections for

the next five years on real GDP, real gross capital formation, labor- force and unemployment

rate. On the basis of that macroeconomic framework and on the fiscal target, the MEF would

present its estimates for structural revenue and the annual expenditure budget, or the annual

revisions to the five-year budget used in Uruguay.

In case the technical commission cannot come to agreement on the values of certain

variables, each member would present his or hers individual estimate in the Committee

meeting. The committee should present to the MEF a summarized minute of the result of its

deliberations, the value and the way that the fiscal target was calculated, the points of

agreement and the divergences. The MEF would calculate the median value of the variable

excluding the two extremes from the calculation, and complete all the other technical

procedures to obtain the projected trend GPD and structural revenue. The MEF should

present to the parliament and the public a technical report explaining the methodology and

results obtained in the estimation of the structural revenue and of the structural balance, and

of the advance to meet the fiscal wealth goal, including at least:

• The determination of structural fiscal revenue and the projections of trend GDP in

which they are based. Those projections are generated by a group of fiscal experts,

representing different views on this matter.

45

• The fiscal target chosen and the real interest rates and growth rates estimates, based

on a comprehensive study done by the experts, that clearly states the consequences of

such target on fiscal wealth or fiscal debt over time, and the risks involved.

3. Dealing with the Embedded Procyclicality of Expenditure

In many countries fiscal expenditure presents a procyclical bias that result in a faster rate of

growth in real expenditure during the expansionary phase of the business cycle or when the

GDP gap is positive. It is to be expected that this procyclical bias will be eliminated when a

structural fiscal policy is introduced, then the growth of real expenditure would be stable

during the business cycle. The procyclical bias often result from a budgeting process that

starts from the forecasting of next year’s actual fiscal revenue, which in itself is a pro cyclical

variable, and the definition of expenditure on the basis of forecasted revenue. By using the

forecast of structural rather that actual fiscal revenue to define expenditure that procyclical

bias is eliminated.

However in Uruguay there are further complications to eliminate the cyclicality of

fiscal expenditure since the procyclical bias is generated at least in part from some

institutional characteristics of the social security system. According to the law, the value in

Uruguayan pesos of pension benefits is indexed to the economy wide wages and salaries.

Consequently, social security spending, which represents a large portion of total fiscal

expenditure, tends to increase faster during the expansionary phase of the cycle when wages

and salaries increase in real terms. That procyclical characteristic of a large portion of total

expenditure will not disappear by the introduction of a structural fiscal policy, and

consequently, the rest of expenditure will have to follow a counter cyclical bias to allow that

total expenditure is cyclically neutral. Considering that public sector wages and salaries in

effect follow a similar path, it is possible that the flexible portion of fiscal expenditure in

Uruguay is much reduced, imposing a significant rigidity to the introduction of a structural

fiscal policy. In effect only capital expenditure can be managed with flexibility.

The rigidity of current expenditure in Uruguay may require different sources of

flexibility to carry out a structural fiscal policy. One possible source of flexibility could be a

counter cyclical public investment policy and a pro cyclical tax rate. That is, during the

expansionary phase of the cycle when current fiscal expenditure by institutional design

becomes excessive and procyclical, then capital expenditure should contract to a minimum to

allow meeting the structural target on the fiscal balance.

46

If the flexibility of public investment were not enough, meeting the structural fiscal

target may require an additional source of flexibility in some tax rates, for example in the

VAT rate. This would provide additional fiscal revenue during the expansionary phase

helping to meet the fiscal target without investment cuts and even when current expenditure

is expanding faster. On the other hand the tax increase may help in softening the procyclical

impulse of public expenditure. In a similar fashion during the contractionary phase of the

cycle, public investment may take the slack generated by the lower growth rate in current

expenditure, and in addition tax rates may be lowered. During a relatively normal phase of

the cycle tax rates would return to its regular level. The changes in the VAT rate may

represent some practical problems and be a source of additional macroeconomic volatility. If

that is the view the only source of fiscal flexibility would be that of discretionary capital

expenditure.

The success in implementing variables taxes, that is, to raise taxes when expansionary

shocks occur and lower them when a contractionary shock occur, will depend on many

factors identified in the interesting paper of Kaufman (2000). The paper argues that the

existence of variable taxes increase welfare as long as two conditions are met: There are

restrictions on credit, and on the other side that tax distortions in the labor market are low

(especially the income tax). It is reasonable to expect that in Uruguay there are important

credit constraints as in may other developing countries. On the other hand it is difficult to

quantify the distorting effects of taxes in the Uruguayan labor market. In this sense a

variables tax policy in the Uruguayan economy may be positive in this context.

Notwithstanding, it is also necessary to analyze the direct costs involved in such a step, as is

the case of recurrent changes in prices, with the subsequent influence in the inflation, which

in a country with history inflation as in Uruguay can be very dangerous. At the same time it

must consider potential lags in economic activity; such changes may be injurious to the cycle.

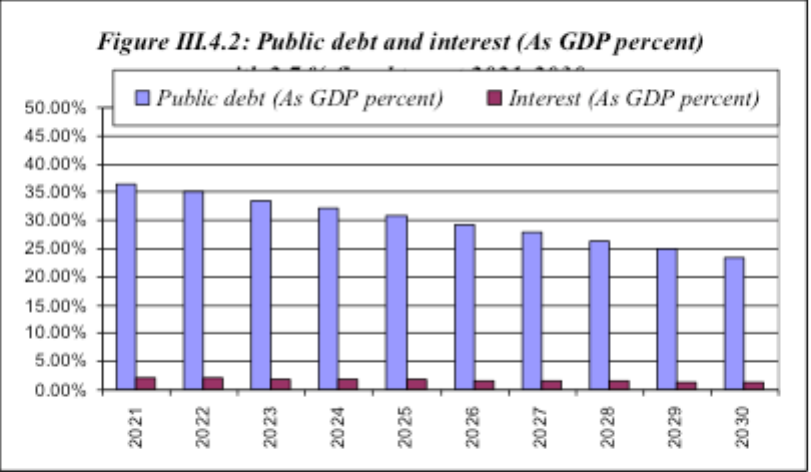

4. Sustainability Path of Fiscal Policy in the Medium and Long Term

The recommended target for the structural primary fiscal balance of 2.0 percent of GDP

should be enough to generate a sustainability path for fiscal policy in the medium and long

run. Even some of the other target levels considered would also generate a sustainable fiscal

path although subject to some additional vulnerability. A 1 percent of GDP primary balance

would stabilize debt around 50 percent of GDP. Looking at Figure II.3.1 we note that from

1999 to 2001 the level of Uruguayan public debt was about 30 percent of GDP. However, the

47

crisis in Argentina in 2001 generated several shocks that resulted in an explosion in the level

of public debt that rose to more than 100 percent of GDP in the following years. The debt

increasing shocks include the exchange rate depreciation, the increase in refinancing costs,

the drop in real GDP due to the recession and the financial assistance given by the public

sector to the financial system. Other measures may take care of the exposure to the recession

and the financial system needs of assistance. However, the exposure to the exchange rate and

refinancing cost shocks depends directly on the level of debt. In that regard, debt levels of

around 50 percent of GDP are still insufficient to reduce vulnerabilities, and it would be

highly advisable to continue to lower that percentage even below the pre-crisis levels

mentioned above.

A primary structural balance of 2 percent of GDP would not be very different form

what has already been achieved over the last years. In that sense the introduction of a

structural fiscal policy with that target level would not represent a large shift in fiscal policy

but taking an explicit commitment with the policy being developed would eliminate the risk

of going down the slippery slope of increasing deficit like in past episodes. Such action

would reduce uncertainty about the future course of fiscal policy and may end up generating

significant benefits. Lower uncertainty would reduce the level financial spreads and the

refinancing cost, allowing for improvements in debt composition, more long-term debt and

more domestic currency debt, and a faster reduction in the debt level.

5. Information and Fiscal Transparency

A national fiscal policy should be backed by the availability of data on public sector

operations and assets and liabilities that is of good quality, consistent and plenty of details,

and that is opportunely distributed. Data shortcomings in Uruguay are significant, the series

cover a relatively short period; fiscal data is collected on a cash rather than accrual basis, and

consequently lacks consistency with national accounts and with data on assets and liabilities.

Fiscal transparency requires a very significant effort in the compilation and development of

fiscal statistics, which should encompass data on fiscal operations, revenues and expenditures

on an accrual basis, aggregate and by institutions, and data on the assets and liabilities

changes and positions that are resulting from such operations.

Transparency also requires that all fiscal operations are covered by the statistics. In

this regards operations by the National Development Corporation or by firms fully owned by

48

Public Enterprises should be consolidated into the fiscal accounts. Moreover, a serious effort

should be carried out to quantify all the contingent liabilities of the public sector, including

the guarantees given to private debt.

49

Annex Table 1: Estimates of Trend GDP and GDP Gap

1961 2.98% 2.82% 2.84%

1962 -1.65% 2.33% -2.30%

1963 -2.46% 1.32% 0.51%

1964 -1.30% 0.87% 2.04%

1965 -0.88% 0.77% 1.20%

1966 1.61% 0.81% 3.35%

1967 -3.81% 1.24% -4.10%

1968 -3.55% 1.34% 1.60%

1969 0.60% 1.76% 6.07%

1970 3.10% 2.12% 4.71%

1971 1.10% 2.15% 0.12%

1972 -2.20% 1.75% -1.55%

1973 -3.48% 1.66% 0.36%

1974 -2.18% 1.81% 3.14%

1975 1.06% 2.49% 5.86%

1976 2.06% 2.95% 3.98%

1977 0.31% 2.96% 1.17%

1978 2.44% 3.04% 5.26%

1979 5.40% 3.07% 6.17%

1980 8.55% 2.72% 6.00%

1981 8.80% 1.64% 1.90%

1982 -1.75% 0.69% -9.39%

1983 -8.28% 0.51% -5.85%

1984 -9.93% 0.55% -1.09%

1985 -9.54% 1.08% 1.48%

1986 -2.86% 1.82% 8.86%

1987 2.56% 2.24% 7.93%

1988 0.08% 2.49% -0.01%

1989 -1.44% 2.84% 1.29%

1990 -2.78% 2.97% 1.59%

1991 -2.49% 3.23% 3.54%

1992 1.78% 3.42% 7.93%

1993 1.09% 3.37% 2.66%

1994 5.23% 2.93% 7.28%

1995 0.96% 2.85% -1.45%

1996 3.70% 2.73% 5.58%

1997 6.40% 2.25% 5.05%

1998 9.01% 1.84% 4.54%

1999 4.68% 1.46% -2.85%

2000 2.05% 1.18% -1.44%

2001 -2.15% 0.76% -3.39%

2002 -14.81 % 0.97% -11.03%

2003 -14.44 % 1.80% 2.17%

2004 -5.92% 2.69% 11.82%

2005 -3.03% 3.59% 6.62%

2006 -0.28% 4.09% 7.00%

2007 2.34% 4.64% 7.42%

2008 6.64% 4.47% 9.06%

2009 2.85% 4.49% 0.60%

2010 1.95% 4.44% 3.50%

2011 1.21% 4.37% 3.60%

2012 0.74% 4.28% 3.80%

2013 0.36% 4.20% 3.80%

2014 0.04% 4.13% 3.80%

2015 -0.22% 4.07% 3.80%

2016 -0.43% 4.02% 3.80%

2017 -0.61% 3.99% 3.80%

2018 -0.77% 3.96% 3.80%

2019 -0.90% 3.94% 3.80%

2020 -0.94% 3.84% 3.80%

Avg. 60-20 -0.22% 2.58% 2.59%

50

V. Uruguay Database

Primera parte.xls

Segunda parte.xls

51

VI. Bibliography and References

Anderson Barry and Minarik Joseph (2006), Design Choices for Fiscal Policy Rules, OECD

Journal on Budgeting.

Banco Central de Uruguay, Informe al poder ejecutivo 2008, 2007, 2006, 2005, 2004, 2003,

2002, 2001, 2000.

Bertino Magdalena y Bertino Reto (2004), Más de un siglo de deuda pública uruguaya:

una historia de ida y vuelta. The Nordic Journal of Latin American and Caribbean

Studies, Vol. 34: 1-2, Estocolmo, Suecia.

Bezdek Vladimír, Dybzak Kamil and Kreejdl Aleš (2007), Cyclically Adjusted Fiscal

Balance OECD and ESCB Methods, Czech Journal of Economics and Finance.

Borchardt Michael, Rial Isabel y Sarmiento Adolfo (1998), Sostenibilidad de la política

fiscal en Uruguay. Estudios CERES.

De Brun Julio (1988), Deuda pública y función de consumo. Terceras jornadas anuales de

Economía, Banco central de Uruguay.

Dos Reis Laura, Manasse Paolo y Panizza Ugo (2007), Targeting the Structural Balance.

BID Working Paper #598

Engel Eduardo, Marcel Mario y Meller Patricio (2007), Meta de superávit estructural:

elementos para su análisis. Direccion de presupuestos Chile.

Fedelino Annalisa, Ivanova Anna and Horton Mark (2009), Computing Cyclically adjusted

balances and automatics stabilizers. Fiscal Affairs department, IMF.

Franken Helmut, Le Fort Guillermo y Parrado Eric (2006), Business cycle responses and

the resilience of the Chilean economy, External Vulnerability and Preventive

Policies. Banco Central de Chile.

Ford Benjamin (2005), Structural fiscal indicators: an overview. Economic Roundup

Giorno Claude, Richardson Pete, Roseveare Deborah and van den Noord Paul (1995),

Estimating potential output, output gaps and structural budget balances. OCDE

economics department working papers no. 152

Girouard Nathalie and André Cristophe (2005) Measuring Cyclically adjusted budget

balances for OECD countries. OECD Economics department, working paper 434.

Hagemann Robert (1999), The structural budget balance the IMF methodology. IMF

Working paper

52

Le Fort Guillermo (2006), Política Fiscal con Meta Estructural en la experiencia chilena.

Presentado en la Segunda Reunión Anual del Grupo Latinoamericano de Especialistas

en Manejo de Deuda Pública (LAC Debt Group) Cartagena, Colombia

Mailhos Jorge A. y Sosa Sebastián (2000), El Comportamiento Cíclico de la Política Fiscal

en Uruguay. Estudios CERES.

Marcel Mario, Tokman Marcelo, Valdés Rodrigo y Benavides Paula (2001), Balance fiscal:

La base para la nueva regla de política fiscal chilena. Economía Chilena

Marcel Mario, Tokman Marcelo, Valdés Rodrigo y Benavides Paula (2001), Balance

estructural del gobierno central: Metodología y estimaciones para Chile 1987-

2000. Dirección de presupuestos, Ministerio de Hacienda, Chile.

Marcel Mario (2009), La Regla De Balance Estructural En Chile Diez Años, Diez

Lecciones. CIEPLAN.

Ministerio de Finanzas de Dinamarca (2008) ,Danish Fiscal Policy in 2009 in view of the

European Economic Recovery Plan (Addendum to Denmark’s Convergence

Programme 2008)

Price Robert and Nluller Patrice, Structural Budget indicators and the interpretation of

fiscal policy stance in OECD economies.

Rodríguez Jorge, Tokman Carla and Vega Alejandra (2007), Structural Balance Policy in

Chile. OECD Journal on Budgeting

Schick Allen (2005), Sustainable Budget Policy: Concepts and Approaches. OECD

Journal on Budgeting

Ter-Minassian Teresa (2009), Preconditions for a successful introduction of structural

fiscal balance-based rules in Latin America and the Caribbean: a framework

paper.

Theoduloz Tania (2006), El producto potencial en la economía uruguaya. Estudios

CERES.

World Economics Outlook 2009, 2008, 2007. IMF.