Recursive Neyman Algorithm for Optimum Sample Allocation

under Box Constraints on Sample Sizes in Strata

Jacek Wesołowski

*

, Robert Wieczorkowski

†

, Wojciech Wójciak

‡

March 27, 2024

Abstract

The optimum sample allocation in stratified sampling is one of the basic issues of survey

methodology. It is a procedure of dividing the overall sample size into strata sample sizes in such a

way that for given sampling designs in strata the variance of the stratified π estimator of the

population total (or mean) for a given study variable assumes its minimum. In this work, we

consider the optimum allocation of a sample, under lower and upper bounds imposed jointly on

sample sizes in strata. We are concerned with the variance function of some generic form that, in

particular, covers the case of the simple random sampling without replacement in strata. The goal of

this paper is twofold. First, we establish (using the Karush-Kuhn-Tucker conditions) a generic form

of the optimal solution, the so-called optimality conditions. Second, based on the established

optimality conditions, we derive an efficient recursive algorithm, named RNABOX, which solves the

allocation problem under study. The RNABOX can be viewed as a generalization of the classical

recursive Neyman allocation algorithm, a popular tool for optimum allocation when only upper

bounds are imposed on sample strata-sizes. We implement RNABOX in R as a part of our package

stratallo which is available from the Comprehensive R Archive Network (CRAN) repository.

*

Programming, Coordination of Statistical Surveys and Registers Department, Statistics Poland, Aleja Niepodległo

´

sci

208, 00-925 Warsaw, Poland, and Faculty of Mathematics and Information Science, Warsaw University of Technology, ul.

Koszykowa 75, 00-662 Warsaw, Poland. E-mail: jacek.wesolowski@pw.edu.pl

†

Programming, Coordination of Statistical Surveys and Registers Department, Statistics Poland, Aleja Niepodległo

´

sci 208,

‡

Faculty of Mathematics and Information Science, Warsaw University of Technology, ul. Koszykowa 75, 00-662 Warsaw,

Poland. E-mail: wojciech.wojciak.dokt@pw.edu.pl

1

arXiv:2304.07034v4 [stat.ME] 26 Mar 2024

Key Words: Stratified sampling; Optimum allocation; Optimum allocation under box constraints;

Neyman allocation; Recursive Neyman algorithm.

1 Introduction

Let us consider a finite population U of size N. Suppose the parameter of interest is the population total

t of a variable y in U, i.e. t =

P

k∈U

y

k

, where y

k

denotes the value of y for population element k ∈ U.

To estimate t, we consider the stratified sampling with the π estimator. Under this well-known sampling

technique, population U is stratified, i.e. U =

S

h∈H

U

h

, where U

h

, h ∈ H, called strata, are disjoint

and non-empty, and H denotes a finite set of strata labels. The size of stratum U

h

is denoted N

h

, h ∈ H

and clearly

P

h∈H

N

h

= N . Probability samples s

h

⊆ U

h

of size n

h

≤ N

h

, h ∈ H, are selected

independently from each stratum according to chosen sampling designs which are often of the same

type across strata. The resulting total sample is of size n =

P

h∈H

n

h

≤ N. It is well known that the

stratified π estimator

ˆ

t

π

of t and its variance are expressed in terms of the first and second order inclusion

probabilities (see, e.g. Särndal, Swensson and Wretman, 1992, Result 3.7.1, p. 102). In particular, for

several important sampling designs

V ar(

ˆ

t

π

) =

X

h∈H

A

2

h

n

h

− B, (1.1)

where A

h

> 0, B do not depend on n

h

, h ∈ H. Among the most basic and common sampling designs

that give rise to the variance of the form (1.1) is the simple random sampling without replacement in

strata (abbreviated STSI). In this case, the stratified π estimator of t assumes the form

ˆ

t

π

=

X

h∈H

N

h

n

h

X

k∈s

h

y

k

, (1.2)

which yields in (1.1): A

h

= N

h

S

h

, where S

h

denotes stratum standard deviation of study variable y,

h ∈ H, and B =

P

h∈H

N

h

S

2

h

(see, e.g. Särndal et al., 1992, Result 3.7.2, p. 103).

The classical problem of optimum sample allocation is formulated as the determination of the

allocation vector n = (n

h

, h ∈ H) that minimizes the variance (1.1), subject to

P

h∈H

n

h

= n, for a

given n ≤ N (see, e.g. Särndal et al., 1992, Section 3.7.3, p. 104). In this paper, we are interested in the

classical optimum sample allocation problem with additional two-sided constraints imposed on sample

sizes in strata. We phrase this problem in the language of mathematical optimization as Problem 1.1.

2

Problem 1.1. Given a finite set H ̸= ∅ and numbers A

h

> 0, m

h

, M

h

, n, such that 0 < m

h

< M

h

≤

N

h

, h ∈ H and

P

h∈H

m

h

≤ n ≤

P

h∈H

M

h

,

minimize

x = (x

h

, h ∈H) ∈R

|H|

+

X

h∈H

A

2

h

x

h

(1.3)

subject to

X

h∈H

x

h

= n (1.4)

m

h

≤ x

h

≤ M

h

, h ∈ H. (1.5)

To emphasize the fact that the optimal solution to Problem 1.1 may not be an integer one, we denote

the optimization variable by x, not by n. The assumptions about n, m

h

, M

h

, h ∈ H, ensure that

Problem 1.1 is feasible.

The upper bounds imposed on x

h

, h ∈ H, are natural since for instance the solution with x

h

> N

h

for some h ∈ H is impossible. The lower bounds are necessary e.g. for estimation of population

strata variances S

2

h

, h ∈ H. They also appear when one treats strata as domains and assigns upper

bounds for variances of estimators of totals in domains. Such approach was considered e.g. in Choudhry,

Hidiroglou and Rao (2012), where apart of the upper bounds constraints x

h

≤ N

h

, h ∈ H, the additional

constraints

1

x

h

−

1

N

h

N

2

h

S

2

h

≤ R

h

, h ∈ H, where R

h

, h ∈ H, are given constants, have been imposed.

Obviously, the latter system of inequalities can be rewritten as lower bounds constraints of the form

x

h

≥ m

h

=

N

2

h

S

2

h

R

h

+N

h

S

2

h

, h ∈ H. The solution given in Choudhry et al. (2012) was obtained by the

procedure based on the Newton-Raphson algorithm, a general-purpose root-finding numerical method.

See also a related paper by Wright, Noble and Bailer (2007), where the optimum allocation problem

under the constraint of the equal precision for estimation of the strata means was considered.

It is convenient to introduce the following definition for feasible solutions of Problem 1.1.

Definition 1.1. Any vector x = (x

h

, h ∈ H) satisfying (1.4) and (1.5) will be called an allocation.

An allocation x = (x

h

, h ∈ H) is called a vertex one if and only if

x

h

=

m

h

, h ∈ L

M

h

, h ∈ U,

where L, U ⊆ H are such that L ∪ U = H and L ∩ U = ∅.

3

An allocation which is not a vertex one will be called a regular allocation.

The solution to Problem 1.1 will be called the optimum allocation.

Note that an optimum allocation may be of a vertex or of a regular form. The name vertex allocation

refers to the fact that in this case x is a vertex of the hyper-rectangle ×

h∈H

[m

h

, M

h

]. We note that

Problem 1.1 becomes trivial if n =

P

h∈H

m

h

or n =

P

h∈H

M

h

. In the former case, the solution is

x

∗

= (m

h

, h ∈ H), and in the latter x

∗

= (M

h

, h ∈ H). These two are boundary cases of the vertex

allocation. In real surveys with many strata, a vertex optimum allocation rather would not be expected.

Nevertheless, for completeness we also consider such a case in Theorem 3.1, which describes the form of

the optimum allocation vector. We also note that a regular optimum allocation x

∗

∈ ×

h∈H

(m

h

, M

h

) if

and only if it is the classical Tschuprow-Neyman allocation x

∗

= (A

h

n

P

v∈H

A

v

, h ∈ H) (see Neyman,

1934, Tschuprow, 1923).

The rest of this paper is structured as follows. Section 2 presents motivations for this research as well

as a brief review of the literature. In Section 3, we identify Problem 1.1 as a convex optimization problem

and then use the Karush-Kuhn-Tucker conditions to establish necessary and sufficient conditions for a

solution to optimization Problem 1.1. These conditions, called the optimality conditions, are presented

in Theorem 3.1. In Section 4, based on these optimality conditions, we introduce a new algorithm,

RNABOX, and prove that it solves Problem 1.1 (see Theorem 4.1). The name RNABOX refers to the fact

that this algorithm generalizes the recursive Neyman algorithm, denoted here RNA. The RNA is a well-

established allocation procedure, commonly used in everyday survey practice. It finds a solution to the

allocation Problem 2.1 (see below), which is a relaxed version of Problem 1.1. As we shall see in Section

4.4, a naive modification of the recursive Neyman approach, which works fine for the one-sided upper

bounds imposed on the sample strata sizes, does not give the correct solution in the case of two-sided

bounds. A more subtle approach is needed.

Finally, let us note that the implementation of RNABOX algorithm is available through our R package

stratallo (Wójciak, 2023b), which is published in CRAN repository (R Core Team, 2023).

4

2 Motivation and literature review

An abundant body of literature is devoted to the problem of optimum sample allocation, going back to

classical solution of Tschuprow (1923) and Neyman (1934), dedicated to STSI sampling without taking

inequality constraints (1.5) into account. In spite of this fact, a thorough analysis of the literature shows

that Problem 1.1 has not been completely understood yet and it suffers from the lack of fully satisfactory

algorithms.

Below, we briefly review existing methods for solving Problem 1.1, including methods that provide

integer-valued solutions.

2.1 Not-necessarily integer-valued allocation

An approximate solution to Problem 1.1 can be achieved through generic methods of non-linear

programming (NLP) (see, e.g. the monograph Valliant, Dever and Kreuter, 2018, and references

therein). These methods have been involved in the problem of optimum sample allocation since solving

the allocation problem is equivalent to finding the extreme (namely, stationary points) of a certain

objective function over a feasible set. Knowing the (approximate) extreme of the objective function, one

can determine the (approximate, yet typically sufficiently accurate) sizes of samples allocated to

individual strata.

In a similar yet different approach adopted e.g. in Münnich, Sachs and Wagner (2012), Problem 1.1

is transformed into root-finding or fixed-point-finding problems (of some properly defined function) to

which the solution is obtained by general-purpose algorithms like e.g. bisection or regula falsi.

Algorithms used in both these approaches would in principle have infinitely many steps, and are

stopped by an arbitrary decision, typically related to the precision of the iterates. There are two main

weaknesses associated with this way of operating: failure of the method to converge or slow

convergence towards the optimal solution for some poor starting points. In other words, performance of

these algorithms may strongly depend on an initial choice of a starting point, and such a choice is

almost always somewhat hazardous. These and similar deficiencies are discussed in details in Appendix

A.2 in the context of the allocation methods described in Münnich et al. (2012). Another drawback of

the algorithms of this type is their sensitivity to finite precision arithmetic issues that can arise in case

5

when the stopping criterion is not expressed directly in terms of the allocation vector iterates (which is

often the case).

Contrary to that, in the recursive algorithms (we are concerned with), the optimal solution is always

found by recursive search of feasible candidates for the optimum allocation among subsets of H. Hence,

they stop always at the exact solution and after finitely many iterations (not exceeding the number of

strata + 1, as we will see for the case of RNABOX in the proof of Theorem 4.1). An important example of

such an algorithm, is the recursive Neyman algorithm, RNA, dedicated for Problem 2.1, a relaxed version

of Problem 1.1.

Problem 2.1. Given a finite set H ̸= ∅ and numbers A

h

> 0, M

h

, n > 0, such that 0 < M

h

≤ N

h

, h ∈

H and n ≤

P

h∈H

M

h

,

minimize

x = (x

h

, h ∈H) ∈R

|H|

+

X

h∈H

A

2

h

x

h

subject to

X

h∈H

x

h

= n

x

h

≤ M

h

, h ∈ H.

Although RNA is popular among practitioners, a formal proof of the fact that it gives the optimal

solution to Problem 2.1 has been given only recently in Wesołowski, Wieczorkowski and Wójciak (2022).

For other recursive approaches to Problem 2.1, see also e.g. Stenger and Gabler (2005), Kadane (2005).

To the best of our knowledge, the only non-integer recursive optimum allocation algorithm

described in the literature that is intended to solve Problem 1.1 is the noptcond procedure proposed by

Gabler, Ganninger and Münnich (2012). In contrary to RNABOX, this method in particular performs

strata sorting. Unfortunately, the allocation computed by noptcond may not yield the minimum of the

objective function (1.3); see Appendix A.1 for more details.

2.2 Integer-valued allocation

Integer-valued algorithms dedicated to Problem 1.1 are proposed in Friedrich, Münnich, de Vries and

Wagner (2015), Wright (2017, 2020). The multivariate version of the optimum sample allocation

problem under box constraints in which m

h

= m, h ∈ H, for a given constant m, is considered in the

paper of de Moura Brito, do Nascimento Silva, Silva Semaan and Maculan (2015). The proposed

6

procedure that solves that problem uses binary integer programming algorithm and can be applied to the

univariate case. See also Brito, Silva and Veiga (2017) for the R-implementation of this approach.

Integer-valued allocation methods proposed in these papers are precise (not approximate) and

theoretically sound. However, they are relatively slow, when compared with not-necessarily

integer-valued algorithms. For instance, at least for one-sided constraints, the integer-valued algorithm

capacity scaling of Friedrich et al. (2015) may be thousands of times slower than the RNA (see

Wesołowski et al., 2022, Section 4). This seems to be a major drawback of these methods as the

differences in variances of estimators based on integer-rounded non-integer optimum allocation and

integer optimum allocation are negligible as explained in Section 6. The computational efficiency is of

particular significance when the number of strata is large, see, e.g. application to the German census in

Burgard and Münnich (2012), and it becomes even more pronounced in iterative solutions to

stratification problems, when the number of iterations may count in millions (see, e.g. Baillargeon and

Rivest, 2011, Barcaroli, 2014, Gunning and Horgan, 2004, Khan, Nand and Ahmad, 2008, Lednicki and

Wieczorkowski, 2003).

Having all that said, the search for a new, universal, theoretically sound and computationally effective

recursive algorithms of optimum sample allocation under two-sided constraints on the sample strata-

sizes, is crucial both for theory and practice of survey sampling.

3 Optimality conditions

In this section we establish optimality conditions, that is, a general form of the solution to Problem 1.1.

As it will be seen in Section 4, these optimality conditions are crucial for the construction of RNABOX

algorithm.

Before we establish necessary and sufficient optimality conditions for a solution to optimization

Problem 1.1, we first define a set function s, which considerably simplifies notation and calculations.

Definition 3.1. Let H, n, A

h

> 0, m

h

, M

h

, h ∈ H be as in Problem 1.1 and let L, U ⊆ H be such

that L ∩ U = ∅, L ∪ U ⊊ H. The set function s is defined as

s(L, U) =

n −

P

h∈L

m

h

−

P

h∈U

M

h

P

h∈H\(L∪U)

A

h

. (3.1)

7

Below, we will introduce the x

(L, U)

vector for disjoint L, U ⊆ H. It appears that the solution of

the Problem 1.1 is necessarily of the form (3.2) with sets L and U defined implicitly through systems of

equations/inequalities established in Theorem 3.1.

Definition 3.2. Let H, n, A

h

> 0, m

h

, M

h

, h ∈ H be as in Problem 1.1, and let L, U ⊆ H be such

that L ∩ U = ∅. We define the vector x

(L, U)

= (x

(L, U)

h

, h ∈ H) as follows

x

(L, U)

h

=

m

h

, h ∈ L

M

h

, h ∈ U

A

h

s(L, U), h ∈ H \ (L ∪ U).

(3.2)

The following Theorem 3.1 characterizes the form of the optimal solution to Problem 1.1 and

therefore is one of the key results of this paper.

Theorem 3.1 (Optimality conditions). The optimization Problem 1.1 has a unique optimal solution.

Point x

∗

∈ R

|H|

+

is a solution to optimization Problem 1.1 if and only if x

∗

= x

(L

∗

, U

∗

)

, with disjoint

L

∗

, U

∗

⊆ H, such that one of the following two cases holds:

CASE I: L

∗

∪ U

∗

⊊ H and

L

∗

=

n

h ∈ H : s(L

∗

, U

∗

) ≤

m

h

A

h

o

,

U

∗

=

n

h ∈ H : s(L

∗

, U

∗

) ≥

M

h

A

h

o

.

(3.3)

CASE II: L

∗

∪ U

∗

= H and

max

h∈U

∗

M

h

A

h

≤ min

h∈L

∗

m

h

A

h

if U

∗

̸= ∅ and L

∗

̸= ∅,, (3.4)

X

h∈L

∗

m

h

+

X

h∈U

∗

M

h

= n. (3.5)

Remark 3.1. The optimum allocation x

∗

is a regular one in CASE I and a vertex one in CASE II.

The proof of Theorem 3.1 is given in Appendix B. Note that Theorem 3.1 describes the general

form of the optimum allocation up to specification of take-min and take-max strata sets L

∗

and U

∗

. The

question how to identify sets L

∗

and U

∗

that determine the optimal solution x

∗

= x

(L

∗

, U

∗

)

is the subject

of Section 4.

8

4 Recursive Neyman algorithm under box constraints

4.1 The RNABOX algorithm

In this section we introduce an algorithm solving Problem 1.1. In view of Theorem 3.1 its essential task is

to split the set of all strata labels H into three subsets of take-min (L

∗

), take-max (U

∗

), and take-Neyman

(H \ (L

∗

∪ U

∗

)). We call this new algorithm RNABOX since it generalizes existing algorithm RNA in

the sense that RNABOX solves optimum allocation problem with simultaneous lower and upper bounds,

while the RNA is dedicated for the problem with upper bounds only, i.e. for Problem 2.1. Moreover,

RNABOX uses RNA in one of its interim steps. We first recall RNA algorithm and then present RNABOX.

For more information on RNA, see Wesołowski et al. (2022, Section 2) or Särndal et al. (1992, Remark

12.7.1, p. 466).

Algorithm RNA

Input: H, (A

h

)

h∈H

, (M

h

)

h∈H

, n.

Require: A

h

> 0, M

h

> 0, h ∈ H, 0 < n ≤

P

h∈H

M

h

.

Step 1: Set U = ∅.

Step 2: Determine

e

U = {h ∈ H \ U : A

h

s(∅, U) ≥ M

h

}, where set function s is defined in (3.1).

Step 3: If

e

U = ∅, go to Step 4 . Otherwise, update U ← U ∪

e

U and go to Step 2 .

Step 4: Return x

∗

= (x

∗

h

, h ∈ H) with x

∗

h

=

M

h

, h ∈ U

A

h

s(∅, U), h ∈ H \ U.

We note that in real life applications numbers (A

h

)

h∈H

are typically unknown and therefore their

estimates (

ˆ

A

h

)

h∈H

are used instead in the input of the algorithms.

Theorem 4.1 is the main theoretical result of this paper and its proof is given in Appendix C.

Theorem 4.1. The RNABOX algorithm provides the optimal solution to Problem 1.1.

4.2 An example of performance of RNABOX

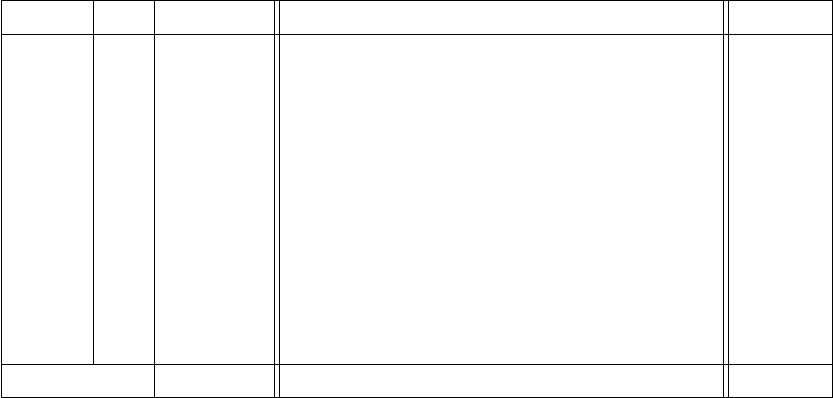

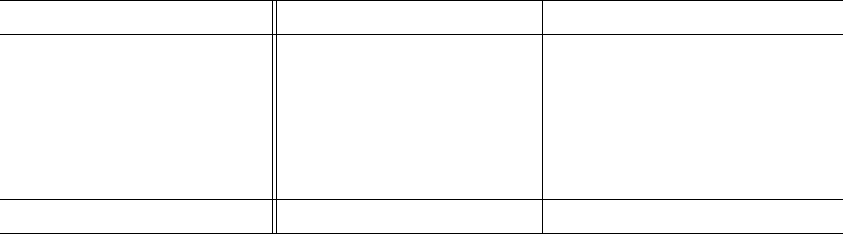

We demonstrate the operational behaviour of RNABOX algorithm for an artificial population with 10

strata and for total sample size n = 5110, as shown in Table 4.1.

9

Algorithm RNABOX

Input: H, (A

h

)

h∈H

, (m

h

)

h∈H

, (M

h

)

h∈H

, n.

Require: A

h

> 0, 0 < m

h

< M

h

, h ∈ H,

P

h∈H

m

h

≤ n ≤

P

h∈H

M

h

.

Step 1: Set L = ∅.

Step 2: Run RNA[H, (A

h

)

h∈H

, (M

h

)

h∈H

, n] to obtain (x

∗∗

h

, h ∈ H).

Let U = {h ∈ H : x

∗∗

h

= M

h

}.

Step 3: Determine

e

L = {h ∈ H \ U : x

∗∗

h

≤ m

h

}.

Step 4: If

e

L = ∅ go to Step 5. Otherwise, update n ← n −

P

h∈

e

L

m

h

, H ← H \

e

L, L ← L ∪

e

L and go to

Step 2.

Step 5: Return x

∗

= (x

∗

h

, h ∈ L ∪ H) with x

∗

h

=

m

h

, h ∈ L

x

∗∗

h

, h ∈ H.

For this example, RNABOX stops after 6 iterations with take-min strata set L

∗

= {1, 2, 4, 6, 7, 9, 10},

take-max strata set U

∗

= {8} and take-Neyman strata set H \ (L

∗

∪ U

∗

) = {3, 5} (see column L

6

/U

6

).

The optimum allocation is a regular one and it is given in column x

∗

of Table 4.1. The corresponding

value of the objective function (1.3) is 441591.5. The details of interim allocations of strata to sets L, U

at each of 6 iterations of the algorithm are given in columns L

1

/U

1

- L

6

/U

6

.

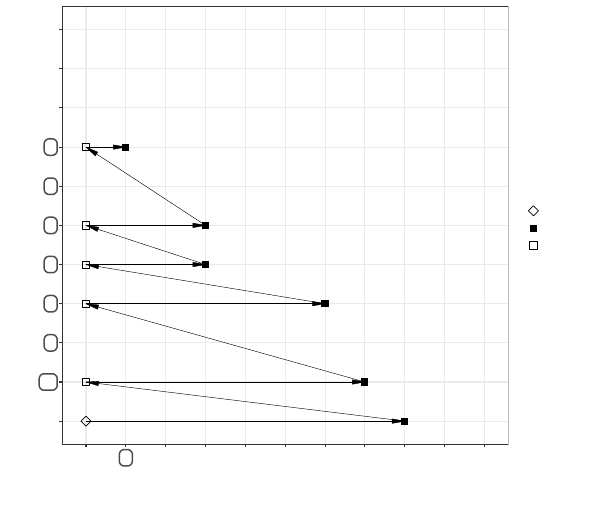

Results summarized in Table 4.1 are presented graphically in Fig. 4.1. The σ(H) axis corresponds

to strata assigned to set U, while τ(H) is for L. For the sake of clear presentation, the values on σ(H)

axis are ordered non-increasingly in

A

h

M

h

, h ∈ H, which gives

A

8

M

8

≥

A

5

M

5

≥

A

3

M

3

≥ . . . ≥

A

10

M

10

, while for

τ(H) axis the strata are ordered non-decreasingly in

A

h

m

h

, h ∈ H, which gives

A

10

m

10

≤

A

1

m

1

≤

A

2

m

2

≤ . . . ≤

A

8

m

8

. Squares in Fig. 4.1 represent assignments of strata into sets L or U, such that the corresponding

coordinate is the value of the last element (follow the respective axis) in the set. For example, ■ at

coordinate 6 on σ(H) axis means that in this iteration of the algorithm (iteration no. 3) we have U =

{8, 5, 3, 7, 4, 6}, while □ at coordinate 6 on τ(H) axis means that in this iteration (no. 5) we get L =

{10, 1, 2, 9, 6}. Directions indicated by the arrows correspond to the order in which the sets L and U are

built as the algorithm iterates. Numbers above the squares are the values of set function s(L, U) for L

and U with elements indicated by the coordinates of a given square. For example, for ■ at coordinates

(8, 7), we have s({10, 1, 2, 9, 6, 4, 7}, {8}) = 0.0622.

10

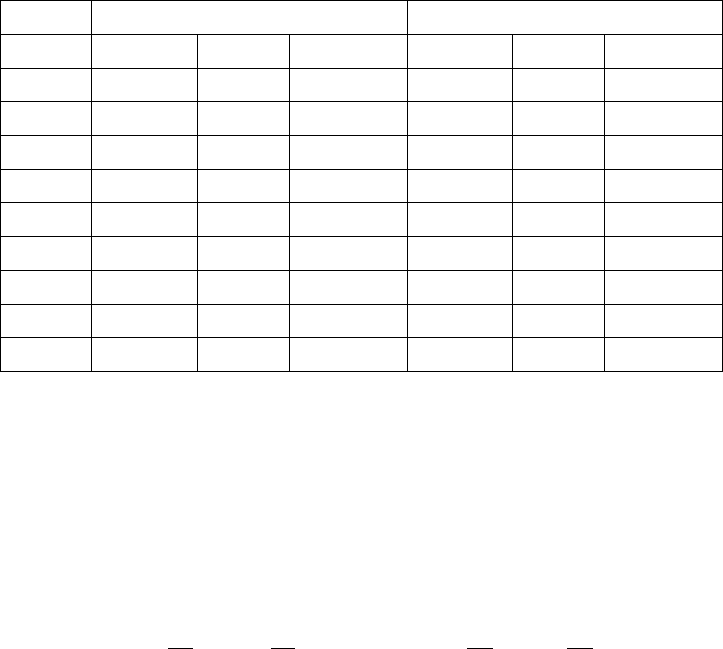

Table 4.1: An example of RNABOX performance for a population with 10 strata and total sample size

n = 5110. Columns L

r

/U

r

, r = 1, . . . , 6, represent the content of sets L, U respectively, in the r-th

iteration of the RNABOX (between Step 3 and Step 4): symbols □ or ■ indicate that the stratum with label

h is in L

r

or U

r

, respectively.

h A

h

m

h

M

h

L

1

/U

1

L

2

/U

2

L

3

/U

3

L

4

/U

4

L

5

/U

5

L

6

/U

6

x

∗

1 2700 750 900 □ □ □ □ 750

2 2000 450 500 ■ □ □ □ □ 450

3 4200 250 300 ■ ■ ■ ■ ■ 261.08

4 4400 350 400 ■ ■ ■ □ 350

5 3200 150 200 ■ ■ ■ ■ ■ 198.92

6 6000 550 600 ■ ■ ■ □ □ 550

7 8400 650 700 ■ ■ ■ □ 650

8 1900 50 100 ■ ■ ■ ■ ■ ■ 100

9 5400 850 900 ■ ■ □ □ □ 850

10 2000 950 1000 □ □ □ □ □ 950

SUM 5000 5600 0/8 1/7 3/6 4/3 5/3 7/1 5110

We would like to point out that regardless of the population and other allocation parameters chosen,

the graph illustrating the operations of RNABOX algorithm will always have a shape similar to that of the

right half of a Christmas tree with the top cut off when U

r

∗

̸= ∅. This property results from that fact that

L

r

⊊ L

r+1

(see (C.1)) and U

r

⊇ U

r+1

(see (C.16)) for r = 1, . . . , r

∗

− 1, r

∗

≥ 2. For the population

given in Table 4.1, we clearly see that L

1

= ∅ ⊊ L

2

= {10} ⊊ L

3

= {10, 1, 2} ⊊ L

4

= {10, 1, 2, 9} ⊊

L

5

= {10, 1, 2, 9, 6} ⊊ L

6

= L

∗

= {10, 1, 2, 9, 6, 4, 7} and U

1

= {8, 5, 3, 7, 4, 6, 9, 2} ⊃ U

2

=

{8, 5, 3, 7, 4, 6, 9} ⊃ U

3

= {8, 5, 3, 7, 4, 6} ⊃ U

4

= {8, 5, 3} = U

5

⊃ U

6

= U

∗

= {8}. Moreover,

regardless of the population and other allocation parameters chosen, subsequent values of set function

s, which are placed at the ends of branches of the Christmas tree, above ■, form a non-increasing

sequence while moving upwards. This fact follows directly from Lemma C.3. For the example allocation

illustrated in Fig. 4.1, we have s(L

1

, U

1

) = 0.3 > s(L

2

, U

2

) = 0.204 > s(L

3

, U

3

) = 0.122 >

s(L

4

, U

4

) = 0.0803 > s(L

5

, U

5

) = 0.075 > s(L

6

, U

6

) = 0.0622 (note that L

1

= ∅). The same

property appears for values of s related to the trunk of the Christmas tree, placed above □. In this case,

this property is due to (C.2), (C.15) and (C.1). For allocation in Fig. 4.1, we have s(L

1

, ∅) = 0.127 >

11

Figure 4.1: Assignments of strata into set L (take-min) and set U (take-max) in RNABOX algorithm for an

example of population as given in Table 4.1 and total sample size n = 5110. The σ(H) axis corresponds

to strata assigned to set U, while τ (H) is for L. Squares represent assignments of strata to L (□) or U

(■) such that the coordinate corresponding to a given square is the value of the last element (following

the order of strata, σ or τ, associated to the respective axis) in the set.

0.127 0.3

0.109 0.204

0.0884 0.122

0.0751 0.0803

0.0706 0.075

0.0602 0.0622

0

10

1

2

9

6

4

7

3

5

8

0 8 5 3 7 4 6 9 2 1 10

σ(W)

τ(W)

Init

U (take−max)

L (take−min)

s(L

2

, ∅) = 0.109 > s(L

3

, ∅) = 0.0884 > s(L

4

, ∅) = 0.0751 > s(L

5

, ∅) = 0.0706 > s(L

6

, ∅) =

0.0602.

4.3 Possible modifications and improvements

4.3.1 Alternatives for RNA in Step 2

The RNABOX algorithm uses RNA in its Step 2. However, it is not hard to see that any algorithm dedicated

to Problem 2.1 (like for instance SGA by Stenger and Gabler, 2005 or COMA by Wesołowski et al., 2022)

could be used instead. We chose RNA as it allows to keep RNABOX free of any strata sorting.

12

4.3.2 A twin version of RNABOX

Let us observe that the order in which L and U are computed in the algorithm could be interchanged.

Such a change, implies that the RNA used in Step 2 of the RNABOX, should be replaced by its twin

version, the LRNA, that solves optimum allocation problem under one-sided lower bounds. The LRNA is

described in details in Wójciak (2023a).

Algorithm LRNA

Input: H, (A

h

)

h∈H

, (m

h

)

h∈H

, n.

Require: A

h

> 0, m

h

> 0, h ∈ H, n ≥

P

h∈H

m

h

.

Step 1: Let L = ∅.

Step 2: Determine

e

L = {h ∈ H \ L : A

h

s(L, ∅) ≤ m

h

}, where set function s is defined in (3.1).

Step 3: If

e

L = ∅, go to Step 4 . Otherwise, update L ← L ∪

e

L and go to Step 2 .

Step 4: Return x

∗

= (x

∗

h

, h ∈ H) with x

∗

h

=

m

h

, h ∈ L

A

h

s(L, ∅), h ∈ H \ L.

Taking into account the observation above, Step 2 and Step 3 of RNABOX would read:

Step 2: Run LRNA[H, (A

h

)

h∈H

, (m

h

)

h∈H

, n] to obtain (x

∗∗

h

, h ∈ H).

Let L = {h ∈ H : x

∗∗

h

= m

h

}.

Step 3: Determine

e

U = {h ∈ H \ L : x

∗∗

h

≥ M

h

}.

The remaining steps should be adjusted accordingly.

4.3.3 Using prior information in RNA at Step 2

In view of Lemma C.2, using the notation introduced in Appendix C.1, in Step 2 of RNABOX, for r

∗

≥ 2

we have

U

r

= {h ∈ H \ L

r

: x

∗∗

h

= M

h

} ⊆ U

r−1

, r = 2, . . . , r

∗

.

This suggests that the domain of discourse for U

r

could be shrunk from H \ L

r

to U

r−1

⊆ H \ L

r

, i.e.

U

r

= {h ∈ U

r−1

: x

∗∗

h

= M

h

}, r = 2, . . . , r

∗

. (4.1)

Given the above observation and the fact that from the implementation point of view set U

r

is determined

internally by RNA, it is tempting to consider modification of RNA such that it makes use of the domain of

13

discourse U

r−1

for set U

r

. This domain could be specified as an additional input parameter, say J ⊆ H,

and then Step 2 of RNA algorithm would read:

Step 2: Determine

e

U = {h ∈ J \ U : A

h

s(∅, U) ≥ M

h

}.

From RNABOX perspective, this new input parameter of RNA should be set to J = H for the first

iteration, and then J = U

r−1

for subsequent iterations r = 2, . . . , r

∗

≥ 2 (if any).

4.4 On a naive extension of the one-sided RNA

By the analogy to the one-sided constraint case, one would expect that the optimum allocation problem

under two-sided constraints (1.5) is of the form (3.2) and hence it could be solved with the naive

modification of RNA as defined below.

Algorithm Naive modification of RNA

Input: H, (A

h

)

h∈H

, (m

h

)

h∈H

, (M

h

)

h∈H

, n.

Require: A

h

> 0, 0 < m

h

< M

h

, h ∈ H,

P

h∈H

m

h

≤ n ≤

P

h∈H

M

h

.

Step 1: Set L = ∅, U = ∅.

Step 2: Determine

e

U = {h ∈ H \ (L ∪ U) : A

h

s(L, U) ≥ M

h

}, where set function s is defined in (3.1).

Step 3: Determine

e

L = {h ∈ H \ (L ∪ U) : A

h

s(L, U) ≤ m

h

}.

Step 4: If

e

L ∪

e

U = ∅ go to Step 5. Otherwise, update L ← L ∪

e

L, U ← U ∪

e

U and go to Step 2.

Step 5: Return x

∗

= (x

∗

h

, h ∈ H) with x

∗

h

=

m

h

, h ∈ L

M

h

, h ∈ U

A

h

s(L, U), h ∈ H \ (L ∪ U).

This is however not true and the basic reason behind is that sequence (s(L

r

, U

r

))

r

∗

r=1

(where r

denotes iteration index, and L

r

and U

r

are taken after Step 3 and before Step 4), typically fluctuates. Thus,

it may happen that (C.13) - (C.15) are not met for U

r

,

e

L

r

defined by the above naive algorithm for some

r = 1, . . . , r

∗

≥ 1. Consequently, optimality conditions stated in Theorem 3.1 may not hold. To

illustrate this fact, consider an example of population as given in Table 4.2. For this population, a naive

version of the recursive Neyman stops in the second iteration and it gives allocation x with L = {3}

and U = {2, 5}, while the optimum choice is x

∗

with L

∗

= {3} and U

∗

= {5}. For non-optimum

allocation x, we have s({3}, {2, 5}) = 0.0714 ≱ 0.25 =

A

2

M

2

, i.e. U does not follow (3.3). Note that the

14

Table 4.2: Example population with 5 strata and the results of naive recursive Neyman sample allocation

(columns x and L/U/H \ (L ∪ U)) for total sample size n = 1489. Lower and upper bounds imposed

on strata sample sizes are given in columns m

h

and M

h

respectively. The optimum allocation with

corresponding strata sets are given in the last two columns. Squares in cells indicate that the allocation

for stratum h ∈ H = {1, . . . , 5} is of type take-min (□) or take-max (■).

h A

h

m

h

M

h

x L/U/H \ (L ∪ U) x

∗

L

∗

/U

∗

/H \ (L

∗

∪ U

∗

)

1 420 24 420 30 54.44

2 352 15 88 88 ■ 45.63

3 2689 1344 2689

1344 □ 1344 □

4 308 8 308 22 39.93

5 130 3 5 5 ■ 5 ■

SUM 1394 3510 1489 1/2/2 1489 1/1/3

allocation x is feasible in this case (it may not be in general), yet is not a minimizer of the objective

function (1.3) as f(x) = 20360 − B, and f(x

∗

) = 17091 − B, where B is some constant. Thus, it

appears that in the case of two-sided constraints, one needs a more subtle modification of RNA

procedure that lies in a proper update of the pair (L

r

, U

r

) in each iteration r = 1, . . . , r

∗

≥ 1 of the

algorithm, such as e.g. in RNABOX.

5 Numerical results

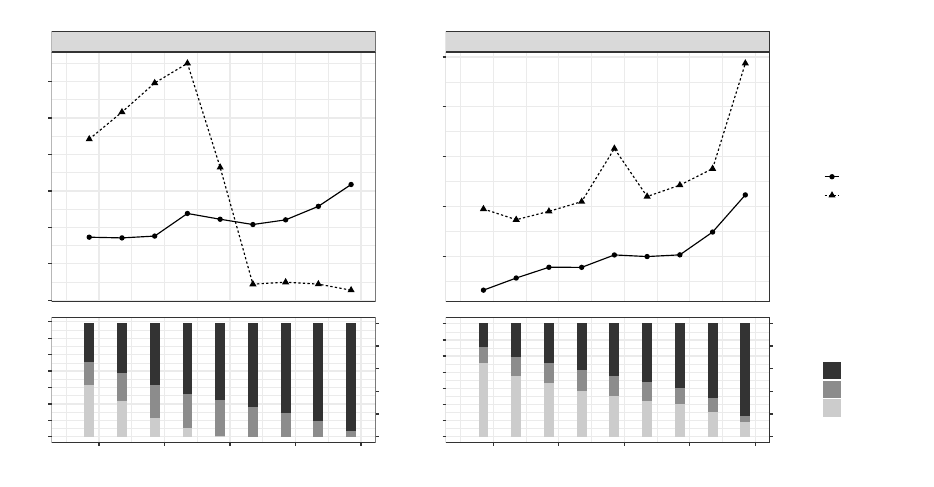

In simulations, using R Statistical Software (R Core Team, 2023) and microbenchmark R package

(Mersmann, 2021), we compared the computational efficiency of RNABOX algorithm with the

efficiency of the fixed-point iteration algorithm (FPIA) of Münnich et al. (2012). The latter one is

known to be an efficient algorithm dedicated to Problem 1.1 and therefore we used it as a benchmark.

The comparison was not intended to verify theoretical computational complexity, but was rather

concerned with quantitative results regarding computational efficiency for the specific implementations

of both algorithms.

To compare the performance of the algorithms we used the STSI sampling for several artificially

created populations. Here, we chose to report on simulation for two such populations with 691 and 703

15

strata, results of which are representative for the remaining ones. These two populations were constructed

by iteratively binding K sets of numbers, where K equals 100 (for the first population) and 200 (for the

second population). Each set, labelled by i = 1, . . . , K, contains 10000 random numbers generated

independently from log-normal distribution with parameters µ = 0 and σ = log(1 + i). For every set

i = 1, . . . , K, strata boundaries were determined by the geometric stratification method of Gunning and

Horgan (2004) with parameter 10 being the number of strata and targeted coefficient of variation equal

to 0.05. This stratification method is implemented in the R package stratification, developed by

Rivest and Baillargeon (2022) and described in Baillargeon and Rivest (2011). For more details, see the

R code with the experiments, which is placed in our GitHub repository (see Wieczorkowski, Wesołowski

and Wójciak, 2023).

Results of these simulations are illustrated in Fig. 5.1. From Fig. 5.1 we see that, while for majority

of the cases the FPIA is slightly faster than RNABOX, the running times of both of these algorithms are

generally comparable. The gain in the execution time of the FPIA results from the fact that it typically

runs through a smaller number of sets L, U ⊂ H (according to (A.6)), than RNABOX in order to find the

optimal L

∗

and U

∗

. Although this approach usually gives correct results (as in the simulations reported

in this section), it may happen that the FPIA misses the optimal sets L

∗

, U

∗

⊊ H. In such a case, FPIA

does not converge, as explained in Appendix A.2. Nevertheless, we emphasize that this situation rarely

happens in practice.

6 Concluding comments

In this paper we considered Problem 1.1 of optimum sample allocation under box constraints. The main

result of this work is the mathematically precise formulation of necessary and sufficient conditions for the

solution to Problem 1.1, given in Theorem 3.1, as well as the development of the new recursive algorithm,

termed RNABOX, that solves Problem 1.1. The optimality conditions are fundamental to analysis of the

optimization problem. They constitute trustworthy underlay for development of effective algorithms

and can be used as a baseline for any future search of new algorithms solving Problem 1.1. Essential

properties of RNABOX algorithm, that distinguish it from other existing algorithms and approaches to

the Problem 1.1, are:

16

Figure 5.1: Running times of FPIA and RNABOX for two artificial populations. Top graphs show the

empirical median of execution times (calculated from 100 repetitions) for different total sample sizes.

Numbers in brackets are the numbers of iterations of a given algorithm. In the case of RNABOX, it is

a vector with number of iterations of the RNA (see Step 2 of RNABOX) for each iteration of RNABOX.

Thus, the length of this vector is equal to the number of iterations of RNABOX. Counts of take-min,

take-Neyman, and take-max strata are shown on bottom graphs.

(6)

(5,5,6)

(6)

(6,6,6)

(6)

(7,6,6)

(7)

(7,7,7)

(7)

(7,7)

(7)

(7)

(7)

(7)

(8)

(8)

(9)

(9)

691 strata, N = 990403

40

60

80

100

120

140

160

Median Time [microseconds]

(5)

(6,5,5,5)

(6)

(6,6,6)

(7)

(7,6,6)

(7)

(7,7,7)

(8)

(8,8,8,8)

(8)

(7,8,8)

(8)

(9,8,8)

(10)

(9,10,10)

(12)

(12,12,12,12)

703 strata, N = 991226

100

150

200

250

300

Algorithm

FPIA

RNABOX

0.2 0.4 0.6 0.8 1.0

0

100

200

300

400

500

600

700

0%

20%

40%

60%

80%

100%

Total sample size (as fraction of N)

Number of strata

0.2 0.4 0.6 0.8 1.0

0

100

200

300

400

500

600

700

0%

20%

40%

60%

80%

100%

Total sample size (as fraction of N)

Strata Set

take−max

take−Neyman

take−min

1. Universality: RNABOX provides optimal solution to every instance of feasible Problem 1.1

(including the case of a vertex optimum allocation).

2. No initialization issues: RNABOX does not require any initializations, pre-tests or whatsoever that

could have an impact on the final results of the algorithm. This, in turn, takes places e.g. in case

of NLP methods.

3. No sorting: RNABOX does not perform any ordering of strata.

4. Computational efficiency: RNABOX running time is comparable to that of FPIA (which is probably

the fastest previously known optimum allocation algorithm for the problem considered).

17

5. Directness: RNABOX computes important quantities (including RNA internals) via formulas that

are expressed directly in terms of the allocation vector x

(L, U)

(see Definition 3.2). This reduces the

risk of finite precision arithmetic issues, comparing to the algorithms that base their key operations

on some interim variables on which the optimum allocation depends, as is the case of e.g. the NLP-

based method.

6. Recursive nature: RNABOX repeatedly applies allocation Step 2 and Step 3 to step-wise reduced set

of strata, i.e. "smaller" versions of the same problem. This translates to clarity of the routines and

a natural way of thinking about the allocation problem.

7. Generalization: RNABOX, from the perspective of its construction, is a generalization of the

popular RNA algorithm that solves Problem 2.1 of optimum sample allocation under one-sided

bounds on sample strata sizes.

Finally, we would like to note that Problem 1.1 considered in this paper is not an integer-valued

allocation problem, while the sample sizes in strata should be of course natural numbers. On the other

hand, the integer-valued optimum allocation algorithms are relatively slow and hence might be inefficient

in some applications, as already noted in Section 2. If the speed of an algorithm is of concern and non-

necessarily integer-valued allocation algorithm is chosen (e.g. RNABOX), the natural remedy is to round

the non-integer optimum allocation provided by that algorithm. Altogether, such procedure is still much

faster than integer-valued allocation algorithms. However, a simple rounding of the non-integer solution

does not, in general, yield the minimum of the objective function, and may even lead to an infeasible

solution, as noted in Friedrich et al. (2015, Section 1, p. 3). Since infeasibility can in fact arise only

from violating constraint (1.4), it can be easily avoided by using a rounding method of Cont and Heidari

(2014) that preserves the integer sum of positive numbers. Moreover, all numerical experiments that we

carried out, show that the values of the objective function obtained for non-integer optimum allocation

before and after rounding and for the integer optimum allocation are practically indistinguishable. See

Table 6.1 for the exact numbers.

The above observations suggest that fast, not-necessarily integer-valued allocation algorithms, with

properly rounded results, may be a good and reasonable alternative to slower integer algorithms when

speed of an algorithm is crucial.

18

Table 6.1: For populations used in simulations in Section 5, V

int

and V denote values of variance (1.1)

computed for integer optimum allocations and non-integer optimum allocations, respectively. Variances

V

round

are computed for rounded non-integer optimum allocations (with the rounding method of Cont

and Heidari (2014)).

691 strata (N = 990403) 703 strata (N = 991226)

fraction f n = f · N V/V

int

V

round

/V

int

n = f · N V/V

int

V

round

/V

int

0.1 99040 0.999997 1.000000 99123 0.999997 1.00000

0.2 198081 0.999999 1.000000 198245 0.999999 1.00000

0.3 297121 0.999999 1.000000 297368 0.999999 1.00000

0.4 396161 0.999999 1.000000 396490 0.999999 1.00000

0.5 495202 0.999999 1.000000 495613 0.999999 1.00000

0.6 594242 0.999999 1.000000 594736 0.999999 1.00000

0.7 693282 1.000000 1.000000 693858 0.999998 1.00000

0.8 792322 1.000000 1.000000 792981 0.999995 1.00000

0.9 891363 1.000000 1.000000 892103 0.999759 1.00000

A Appendix: On the existing allocation algorithms by GGM and MSW

A.1 Necessary vs. sufficient optimality conditions and the noptcond function of GGM

Problem 1.1 has been considered in Gabler et al. (2012) (GGM in the sequel). Theorem 1 in that paper

announces that there exist disjoint sets L, U ⊂ H with L

c

= H \ L, U

c

= H \ U, such that

max

h∈L

A

h

m

h

< min

h∈L

c

A

h

m

h

and max

h∈U

c

A

h

M

h

< min

h∈U

A

h

M

h

, (A.1)

and, if the allocation x = (x

h

, h ∈ H) is of the form (3.2) with L and U as above, then x is an optimum

allocation. An explanation on how to construct sets L and U is essentially given in the first part of the

proof of Theorem 1, p. 154-155, or it can be read out from the noptcond function. The noptcond is

a function in R language (see R Core Team, 2023) that was defined in Sec. 3 of GGM and it aims to

find an optimum sample allocation based on results of Theorem 1, as the authors pointed out. However,

as it will be explained here, (3.2) and (A.1) together, are in fact necessary but not sufficient conditions

for optimality of the allocation x. In a consequence, the noptcond function may not give an optimum

allocation.

19

By Theorem 3.1, CASE I, a regular allocation x is an optimum allocation if and only if it is of the

form (3.2) with disjoint sets L, U ⊊ H, L ∪ U ⊊ H, L

c

= H \ L, U

c

= H \ U such that the following

inequalities hold true:

max

h∈L

A

h

m

h

≤

1

s(L, U)

< min

h∈L

c

A

h

m

h

, (A.2)

max

h∈U

c

A

h

M

h

<

1

s(L, U)

≤ min

h∈U

A

h

M

h

. (A.3)

Clearly, (A.2) implies the first inequality in (A.1), and (A.3) implies the second one. Converse

implications do not necessary hold, and therefore sufficiency of condition (3.2) with (A.1) for Problem

1.1 is not guaranteed. In others words, (3.2) and (A.1) alone, lead to a feasible solution (i.e. the one that

does not violate any of the constraints (1.4) - (1.5)), which, at the same time, might not be a minimizer

of the objective function (1.3).

The proof of Theorem 1 in GGM gives an explicit, but somewhat informal algorithm that finds sets

L and U which define allocation (3.2). Sets L and U determined by this algorithm meet inequalities (4)

and (5) in GGM, which are necessary and sufficient conditions for an optimal (regular) solution. This

fact was noted by the authors, but unfortunately (4) and (5) are not given in the formulation of Theorem

1. Presumably, this was due to authors’ statement that (4) and (5) follow from (3.2) and (A.1): "From the

definition of L1, L2 in Eq. 3 we have ...", while in fact to conclude (4) and (5) the authors additionally

rely on the algorithm constructed at the beginning of the proof. Note that conditions (4) and (5) are the

same as those given in Theorem 3.1 for a regular solution (CASE I). Moreover, it is a matter of simple

observation to see that the allocation found by the algorithm described in the proof of Theorem 1 in GGM,

meets also optimality conditions (3.4) and (3.5) established in Theorem 3.1 for vertex solutions (CASE

II). Hence, the allocation computed by the algorithm embedded in the proof of the GGM’s Theorem 1 is

indeed an optimal one, though the formal statement of Theorem 1 is not correct.

Unfortunately, the noptcond function does not fully follow the algorithm from the proof of Theorem

1 of GGM. Consequently, the optimality of a solution computed by noptcond is not guaranteed. This can

be illustrated by a simple numerical Example A.1, which follows Wójciak (2019, Example 3.9).

Example A.1. Consider the allocation for an example population as given in Table A.1.

20

Table A.1: Two allocations for an example population with two strata: non-optimum x

noptcond

with

L = {1}, U = ∅, and optimum x

∗

with L

∗

= ∅, U

∗

= {1}. Set function s is defined in (3.1).

h A

h

m

h

M

h

A

h

m

h

A

h

M

h

s

−1

({1}, ∅) s

−1

(∅, {1}) x

noptcond

x

∗

1 2000 30 50 66.67 40

23.08 27.27

30 50

2 3000 40 200 75 15 130 110

The solution returned by noptcond function is equal to x = (30, 130), while the optimum allocation

is x

∗

= (50, 110). The reason for this is that conditions (A.2), (A.3) are never examined by the noptcond,

and for this particular example we have

A

1

m

1

= 66.67 ≰ 23.08 =

1

s(L, U)

as well as

A

1

M

1

= 40 ≮ 23.08 =

1

s(L, U)

, i.e. (A.2), (A.3) are clearly not met. A simple adjustment can be made to noptcond function so

that it provides the optimal solution to Problem 1.1. That is, a feasible candidate solution that is found

(note that this candidate is of the form x = (x

v

, v ∈ H \ (L ∪ U)) with x

v

= A

v

s(L, U)), should

additionally be checked against the condition

max

h∈L

A

h

m

h

≤

A

v

x

v

≤ min

h∈U

A

h

M

h

, v ∈ H \ (L ∪ U). (A.4)

We finally note that the table given in Section 4 of GGM on p. 160, that illustrates how noptcond

operates, is incorrect as some of the numbers given do not correspond to what noptcond internally

computes, e.g. for each row of this table, the allocation should sum up to n = 20, but it does not.

A.2 Fixed-point iteration of MSW

Theorem 1 of Münnich et al. (2012) (referred to by MSW in the sequel) provides another solution to

Problem 1.1 that is based on results partially similar to those stated in Theorem 3.1. Specifically, it states

that the allocation vector x = (x

h

, h ∈ H) can be expressed as a function x : R

+

→ R

|H|

+

of λ, defined

as follows

x

h

(λ) =

M

h

, h ∈ J

λ

M

:=

n

h ∈ H : λ ≤

A

2

h

M

2

h

o

A

h

√

λ

, h ∈ J

λ

:=

n

h ∈ H :

A

2

h

M

2

h

< λ <

A

2

h

m

2

h

o

m

h

, h ∈ J

λ

m

:=

n

h ∈ H : λ ≥

A

2

h

m

2

h

o

,

21

and the optimum allocation x

∗

is obtained for λ = λ

∗

, where λ

∗

is the solution of the equation:

˜g(λ) :=

X

h∈H

x

h

(λ) − n = 0. (A.5)

Here, we note that the optimum allocation x

∗

obtained is of the form x

(L, U)

, as given in (3.2), with

L = J

λ

∗

m

and U = J

λ

∗

M

. Since ˜g is continuous but not differentiable, equation (A.5) has to be solved by

a root-finding methods which only require continuity. In MSW, the following methods were proposed:

bisection, secan and regula falsi in few different versions. The authors reported that despite the fact that

some theoretical requirements for these methods are not satisfied by the function ˜g (e.g. it is not convex

while regula falsi applies to convex functions), typically the numerical results are satisfactory. However

this is only true when the values of the initial parameters are from the proper range, which is not known

a priori.

As these algorithms might be relatively slow (see Table 1 in MSW), the authors of MSW proposed

an alternative method. It is based on the observation that (A.5) is equivalent to

λ = ϕ(λ) :=

1

s

2

(J

λ

m

, J

λ

M

)

,

where set function s is as in (3.1) (see Appendix A, Lemma 2 in MSW). Note that ϕ is well-defined only

if J

λ

m

∪ J

λ

M

⊊ H. The authors note that the optimal λ

∗

is a fixed-point of the function ϕ : R

+

→ R

+

.

This clever observation was translated to an efficient optimum allocation fixed-point iteration algorithm,

FPIA, that was defined on page 442 in MSW. Having acknowledged its computational efficiency as well

as the fact that typically it gives the correct optimum allocation, the following two minor issues related

to FPIA can be noted:

• The FPIA is adequate only for allocation problems for which an optimum allocation is of a regular

type (according to Definition 1.1), as for vertex allocation J

λ

∗

m

∪ J

λ

∗

M

= H and therefore ϕ is not

well-defined for such λ

∗

.

• The FPIA strongly depends on the choice of initial value λ

0

of the parameter λ. If λ

0

is not chosen

from the proper range (not known a priori), two distinct undesirable scenarios can occur: the FPIA

may get blocked, or it may not converge.

To outline the blocking scenario which may happen even in case of a regular optimum allocation, let

I :=

λ ∈

min

h∈H

A

2

h

m

2

h

, max

h∈H

A

2

h

M

2

h

: s(J

λ

m

, J

λ

M

) = 0

,

22

and note that I ̸= ∅ is possible. If FPIA encounters λ

k

∈ I ̸= ∅ at some k = 0, 1, . . ., then the crucial

step of FPIA, i.e.:

λ

k+1

:=

1

s

2

J

λ

k

m

, J

λ

k

M

, (A.6)

yields λ

k+1

=

1

0

, which is undefined. Numerical Example A.2 illustrates this scenario.

Example A.2. Consider allocation for a population given in Table A.2. Initial value λ

0

= 6861.36 ∈

I = [2304, 6922.24] and therefore FPIA gets blocked since λ

1

=

1

0

is undefined.

Table A.2: Details of FPIA performance for a population with four strata. Here, λ

0

=

1

s

2

(∅, ∅)

, λ

1

=

1

s

2

(J

λ

0

m

, J

λ

0

M

)

, λ

∗

=

1

s

2

(J

λ

∗

m

, J

λ

∗

M

)

. Squares in cells indicate assignment of stratum h ∈ H = {1, 2, 3, 4} to

J

λ

m

(□) or J

λ

M

(■) for a given λ.

population FPIA optimum allocation

h A

h

m

h

M

h

A

2

h

m

2

h

A

2

h

M

2

h

J

λ

0

m

/J

λ

0

M

J

λ

1

m

/J

λ

1

M

J

λ

∗

m

/J

λ

∗

M

x

∗

1 4160 5 50 692224 6922.24 ■

-

44.35

2 240 5 50 2304 23.04 □ □ 5

3 530 5 50 11236 112.36 5.65

4 40 5 50 64 0.64 □ □ 5

total sample size n = 60 λ

0

= 6861.36 λ

1

=

1

0

λ

∗

= 8798.44

Figure A.1 shows the graphs of the functions g and ϕ for the problem considered in this example.

23

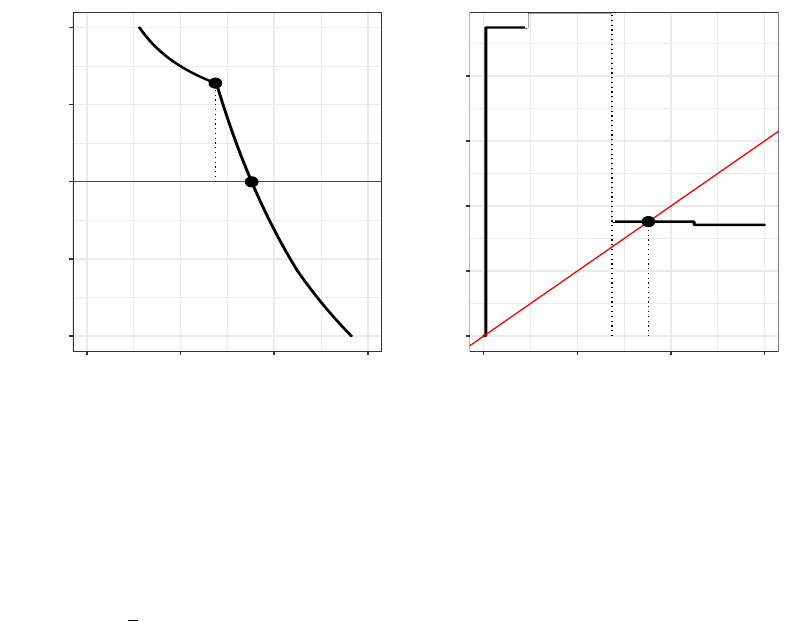

Figure A.1: Functions g and ϕ for Example A.2 of the allocation problem for which the FPIA gets

blocked.

λ

0

λ

∗

−10

−5

0

5

10

0 5000 10000 15000

λ

g(λ)

λ

0

λ

∗

0

5000

10000

15000

20000

0 5000 10000 15000

λ

φ(λ)

These graphs show that g is not differentiable, and ϕ has jump discontinuities. Moreover, there is an

interval I = [2304, 6922.24], such that ϕ is not well-defined on I.

We note that a simple remedy to avoid the blocking scenario in the case of a regular allocation is to

change λ to λ

new

=

1

λ

, with a corresponding redefinition of all the objects in the original algorithm.

The next Example A.3 illustrates a situation when FPIA does not converge.

Example A.3. Consider a population given in Table A.3. Initial value of λ

0

= 695.64 causes lack of

convergence of the FPIA due to oscillations:

λ

k

=

1444, k = 1, 3, 5, . . .

739.84, k = 2, 4, 6, . . . .

24

Table A.3: Details of FPIA performance for a population with four strata. Here, λ

0

=

1

s

2

(∅, ∅)

, λ

k+1

is as

in (A.6), and λ

∗

=

1

s

2

(J

λ

∗

m

, J

λ

∗

M

)

. Squares in cells indicate assignment of stratum h ∈ H = {1, 2, 3, 4} to

J

λ

m

(□) or J

λ

M

(■) for a given λ.

population FPIA optimum allocation

h A

h

m

h

M

h

A

2

h

m

2

h

A

2

h

M

2

h

J

λ

0

m

/J

λ

0

M

J

λ

1

m

/J

λ

1

M

J

λ

2

m

/J

λ

2

M

· · · J

λ

∗

m

/J

λ

∗

M

x

∗

1 380 10 50 1444 57.76 □

· · ·

13.1

2 140 10 50 196 7.84 □ □ □ □ 10

3 230 10 50 529 21.16 □ □ □ □ 10

4 1360 10 50 18496 739.84 ■ ■ 46.9

total sample size n = 80 λ

0

= 695.64 λ

1

= 1444 λ

2

= 739.84 · · · λ

∗

= 841

Figure A.2 shows the graphs of the functions g and ϕ for the problem considered in this example.

Figure A.2: Functions g and ϕ for Example A.2 of the allocation problem for which the FPIA does not

converge.

λ

0

λ

∗

λ

1

λ

2

−15

−10

−5

0

5

10

800 1200 1600

λ

g(λ)

λ

0

λ

∗

λ

1

λ

2

0

500

1000

1500

0 500 1000 1500

λ

φ(λ)

The issue of determining a proper starting point λ

0

was considered in MSW, with a recommendation

to choose λ

0

=

1

s

2

(∅, ∅)

. Alternatively, in case when

1

s

2

(∅, ∅)

is not close enough to the optimal λ

∗

(which

is not known a priori), MSW suggests to first run several iterations of a root finding algorithm to get the

starting point λ

0

for the FPIA.

25

B Appendix: Proof of Theorem 3.1

Remark B.1. Problem 1.1 is a convex optimization problem as its objective function f : R

|H|

+

→ R

+

,

f(x) =

X

h∈H

A

2

h

x

h

, (B.1)

and inequality constraint functions g

m

h

: R

|H|

+

→ R, g

M

h

: R

|H|

+

→ R,

g

m

h

(x) = m

h

− x

h

, h ∈ H, (B.2)

g

M

h

(x) = x

h

− M

h

, h ∈ H, (B.3)

are convex functions, whilst the equality constraint function w : R

|H|

+

→ R,

w(x) =

X

h∈H

x

h

− n

is affine. More specifically, Problem 1.1 is a convex optimization problem of a particular type in which

inequality constraint functions (B.2) - (B.3) are affine. See Appendix E for the definition of the convex

optimization problem.

Proof of Theorem 3.1. We first prove that Problem 1.1 has a unique solution. The optimization Problem

1.1 is feasible since requirements m

h

< M

h

, h ∈ H, and

P

h∈H

m

h

≤ n ≤

P

h∈H

M

h

ensure that

the feasible set F := {x ∈ R

|H|

+

: (1.4) - (1.5) are all satisfied} is non-empty. The objective function

(1.3) attains its minimum on F since it is a continuous function and F is closed and bounded. Finally,

uniqueness of the solution is due to strict convexity of the objective function on F .

As explained in Remark B.1, Problem 1.1 is a convex optimization problem in which the inequality

constraint functions g

m

h

, g

M

h

, h ∈ H are affine. The optimal solution for such a problem can be identified

through the Karush-Kuhn-Tucker (KKT) conditions, in which case they are not only necessary but also

sufficient; for further references, see Appendix E.

The gradients of the objective function (B.1) and constraint functions (B.2) - (B.3) are as follows:

∇f(x) = (−

A

2

h

x

2

h

, h ∈ H), ∇w(x) = 1, ∇g

m

h

(x) = −∇g

M

h

(x) = −1

h

, h ∈ H,

where, 1

is a vector with all entries 1 and 1

h

is a vector with all entries 0 except the entry with the label

26

h, which is 1. Hence, the KKT conditions (E.2) for Problem 1.1 assume the form

−

A

2

h

(x

∗

h

)

2

+ λ − µ

m

h

+ µ

M

h

= 0, h ∈ H, (B.4)

X

h∈H

x

∗

h

− n = 0, (B.5)

m

h

≤ x

∗

h

≤ M

h

, h ∈ H, (B.6)

µ

m

h

(m

h

− x

∗

h

) = 0, h ∈ H, (B.7)

µ

M

h

(x

∗

h

− M

h

) = 0, h ∈ H. (B.8)

To prove Theorem 3.1, it suffices to show that for x

∗

= x

(L

∗

, U

∗

)

with L

∗

, U

∗

satisfying conditions of

CASE I or CASE II, there exist λ ∈ R and µ

m

h

, µ

M

h

≥ 0, h ∈ H, such that (B.4) - (B.8) hold. It should

also be noted that the requirement m

h

< M

h

, h ∈ H, guarantees that L

∗

and U

∗

defined in (3.3) and

(3.4) are disjoint. Therefore, x

(L

∗

, U

∗

)

is well-defined according to Definition 3.2.

CASE I: Take x

∗

= x

(L

∗

, U

∗

)

with L

∗

and U

∗

as in (3.3). Then, (B.5) is clearly met after referring to

(3.2) and (3.1), while (B.6) follows directly from (3.2) and (3.3), since (3.3) for h ∈ H \ (L

∗

∪ U

∗

)

specifically implies m

h

< A

h

s(L

∗

, U

∗

) < M

h

. Take λ =

1

s

2

(L

∗

, U

∗

)

and

µ

m

h

=

λ −

A

2

h

m

2

h

, h ∈ L

∗

0, h ∈ H \ L

∗

,

µ

M

h

=

A

2

h

M

2

h

− λ, h ∈ U

∗

0, h ∈ H \ U

∗

.

(B.9)

Note that (3.3) along with requirement n ≥

P

h∈H

m

h

(the latter needed if U

∗

= ∅) ensure

s(L

∗

, U

∗

) > 0, whilst (3.3) alone implies µ

m

h

, µ

M

h

≥ 0, h ∈ H. After referring to (3.2), it is a

matter of simple algebra to verify (B.4), (B.7) and (B.8) for λ, µ

m

h

, µ

M

h

, h ∈ H defined above.

CASE II: Take x

∗

= x

(L

∗

, U

∗

)

with L

∗

, U

∗

satisfying (3.4) and (3.5). Then, condition (B.5) becomes

(3.5), while (B.6) is trivially met due to (3.2). Assume that L

∗

̸= ∅ and U

∗

̸= ∅ (for empty L

∗

or U

∗

,

(B.4), (B.7) and (B.8) are trivially met). Take an arbitrary ˜s > 0 such that

˜s ∈

max

h∈U

∗

M

h

A

h

, min

h∈L

∗

m

h

A

h

. (B.10)

Note that (3.4) ensures that the interval above is well-defined. Let λ =

1

˜s

2

and µ

m

h

, µ

M

h

, h ∈ H be as

in (B.9). Note that (B.10) ensures that µ

m

h

, µ

M

h

≥ 0 for all h ∈ H. Then it is easy to check, similarly

as in CASE I, that (B.4), (B.7) and (B.8) are satisfied.

27

C Appendix: Auxiliary lemmas and proof of Theorem 4.1

C.1 Notation

Throughout the Appendix C, by U

r

, L

r

,

e

L

r

, we denote sets U, L,

e

L respectively, as they are in the r-th

iteration of RNABOX algorithm after Step 3 and before Step 4. The iteration index r takes on values from

set {1, . . . , r

∗

}, where r

∗

≥ 1 indicates the final iteration of the algorithm. Under this notation, we have

L

1

= ∅ and in general, for subsequent iterations, if any (i.e. if r

∗

≥ 2), we get

L

r

= L

r−1

∪

e

L

r−1

=

r−1

[

i=1

e

L

i

, r = 2, . . . , r

∗

. (C.1)

As RNABOX iterates, objects denoted by symbols n and H are being modified. However, in this

Appendix C, whenever we refer to n and H, they always denote the unmodified total sample size and the

set of strata labels as in the input of RNABOX. In particular, this is also related to set function s (defined

in (3.1)) which depends on n and H.

For convenient notation, for any A ⊆ H and any set of real numbers z

h

, h ∈ A, we denote

z

A

=

X

h∈A

z

h

.

C.2 Auxiliary remarks and lemmas

We start with a lemma describing important monotonicity properties of function s.

Lemma C.1. Let A ⊆ B ⊆ H and C ⊆ D ⊆ H.

1. If B ∪ D ⊊ H and B ∩ D = ∅, then

s(A, C) ≥ s(B, D) ⇔ s(A, C)(A

B\A

+ A

D\C

) ≤ m

B\A

+ M

D\C.

(C.2)

2. If A ∪ D ⊊ H, A ∩ D = ∅, B ∪ C ⊊ H, B ∩ C = ∅, then

s(A, D) ≥ s(B, C) ⇔ s(A, D)(A

B\A

− A

D\C

) ≤ m

B\A

− M

D\C.

(C.3)

28

Proof. Clearly, for any α ∈ R, β ∈ R, δ ∈ R, γ > 0, γ + δ > 0, we have

α+β

γ+δ

≥

α

γ

⇔

α+β

γ+δ

δ ≤ β. (C.4)

To prove (C.2), take

α = n − m

B

− M

D

β = m

B\A

+ M

D\C

γ = A

H

− A

B∪D

δ = A

B\A

+ A

D\C

.

Then,

α

γ

= s(B, D),

α+β

γ+δ

= s(A, C), and hence (C.2) holds as an immediate consequence of (C.4).

Similarly for (C.3), take

α = n − m

B

− M

C

β = m

B\A

− M

D\C

γ = A

H

− A

B∪C

δ = A

B\A

− A

D\C

,

and note that γ + δ = A

H

− A

B∪C

+ A

B\A

− A

D\C

= A

H

− A

B

− A

C

+ A

B

− A

A

− A

D

+ A

C

=

A

H

−A

A∪D

> 0 due to the assumptions made for A, D, B, C, and A

h

> 0, h ∈ H. Then,

α

γ

= s(B, C),

α+β

γ+δ

= s(A, D), and hence (C.3) holds as an immediate consequence of (C.4).

The remark below describes some relations between sets L

r

and U

r

, r = 1, . . . , r

∗

≥ 1, appearing in

RNABOX algorithm. These relations are particularly important for understanding computations involving

the set function s (recall, that it is defined only for such two disjoint sets, the union of which is a proper

subset of H).

Remark C.1. For r

∗

≥ 1,

L

r

∩ U

r

= ∅, r = 1, . . . , r

∗

, (C.5)

and for r

∗

≥ 2,

L

r

∪ U

r

⊊ H, r = 1, . . . , r

∗

− 1. (C.6)

Moreover, let x

∗

be as in Step 5 of RNABOX algorithm. Then, for r

∗

≥ 1,

L

r

∗

∪ U

r

∗

⊊ H ⇔ x

∗

is a regular allocation, (C.7)

and

L

r

∗

∪ U

r

∗

= H ⇔ x

∗

is a vertex allocation. (C.8)

29

Proof. From the definition of set U in Step 2 of RNABOX, for r

∗

≥ 1,

U

r

⊆ H \ L

r

, r = 1, . . . , r

∗

, (C.9)

which proves (C.5). Following (C.1), for r

∗

≥ 2,

L

r

=

r−1

[

i=1

e

L

i

⊆ H, r = 2, . . . , r

∗

, (C.10)

where the inclusion is due to definition of set

e

L in Step 3 of RNABOX, i.e.

e

L

r

⊆ H \ (L

r

∪ U

r

) for

r = 1, . . . , r

∗

. Inclusions (C.9), (C.10) with L

1

= ∅ imply

L

r

∪ U

r

⊆ H, r = 1, . . . , r

∗

≥ 1. (C.11)

Given that r

∗

≥ 2, Step 4 of the algorithm ensures that set

e

L

r

⊆ H \ (L

r

∪ U

r

) is non-empty for

r = 1, . . . , r

∗

−1, which implies L

r

∪U

r

̸= H. This fact combined with (C.11) gives (C.6). Equivalences

(C.7) and (C.8) hold trivially after referring to Definition 1.1 of regular and vertex allocations.

The following two remarks summarize some important facts arising from Step 2 of RNABOX

algorithm. These facts will serve as starting points for most of the proofs presented in this section.

Remark C.2. In each iteration r = 1, . . . , r

∗

≥ 1, of RNABOX algorithm, a vector (x

∗∗

h

, h ∈ H \ L

r

)

obtained in Step 2, has the elements of the form

x

∗∗

h

=

M

h

, h ∈ U

r

⊆ H \ L

r

A

h

s(L

r

, U

r

) < M

h

, h ∈ H \ (L

r

∪ U

r

),

(C.12)

where the set function s is defined in (3.1). Equation (C.12) is a direct consequence of Theorem D.1.

Remark C.3. Remark C.2 together with Theorem D.1, for r

∗

≥ 2 yield

U

r

= {h ∈ H \ L

r

: A

h

s(L

r

, U

r

) ≥ M

h

}, r = 1, . . . , r

∗

− 1,(C.13)

whilst for r

∗

≥ 1,

U

r

∗

= {h ∈ H \ L

r

∗

: A

h

s(L

r

∗

, U

r

∗

) ≥ M

h

}, (C.14)

if and only if x

∗

(computed at Step 5 of RNABOX algorithm) is: a regular allocation or a vertex allocation

with L

r

∗

= H.

30

Moreover, for r

∗

≥ 1,

e

L

r

= {h ∈ H \ (L

r

∪ U

r

) : A

h

s(L

r

, U

r

) ≤ m

h

}, r = 1, . . . , r

∗

. (C.15)

Note that in Remark C.3, function s is well-defined due to Remark C.1. The need to limit the scope

of (C.14) to regular allocations only, is dictated by the fact that in the case of a vertex allocation we have

L

r

∗

∪ U

r

∗

= H (see (C.8)) and therefore s(L

r

∗

, U

r

∗

) is not well-defined.

Lemma C.2 and Lemma C.3 reveal certain monotonicity properties of sequence (U

r

)

r

∗

r=1

and

sequence (s(L

r

, U

r

))

r

∗

r=1

, respectively. These properties will play a crucial role in proving Theorem

4.1.

Lemma C.2. Sequence (U

r

)

r

∗

r=1

is non-increasing, that is, for r

∗

≥ 2,

U

r

⊇ U

r+1

, r = 1, . . . , r

∗

− 1. (C.16)

Proof. Let r

∗

≥ 2 and r = 1, . . . , r

∗

− 1. Then, by (C.6), L

r

∪ U

r

⊊ H. Following (C.13), the domain

of discourse for U

r

is H \ L

r

, and in fact it is H \ (L

r

∪

e

L

r

) = H \ L

r+1

, since U

r

̸⊂

e

L

r

as ensured

by Step 3 of RNABOX. That is, both U

r

and U

r+1

have essentially the same domain of discourse, which is

H \ L

r+1

. Given this fact and the form of the set-builder predicate in (C.13) - (C.14) as well as equality

U

r

∗

= H\L

r

∗

for the case when x

∗

is a vertex allocation (for which (C.14) does not apply), we conclude

that only one of the following two distinct cases is possible: U

r

⊇ U

r+1

or U

r

⊊ U

r+1

.

The proof is by contradiction, that is, assume that (C.16) does not hold. Therefore, in view of the

above observation, there exists r ∈ {1, . . . , r

∗

− 1} such that U

r

⊊ U

r+1