Contents

A handy checklist for you

> See page 4

A

Your adventure

starts here

> See page 6

B

How we cover pre-existing

medical conditions

> See page 29

C

How we cover

pregnancy

> See page 35

D

What is and isn’t covered

> See page 36

E

General exclusions —

things we never cover

> See page 80

F

Definitions — words

with specific meanings

> See page 91

2

As part of our commitment to you, this document meets the WriteMark

Plain Language Standard. The WriteMark is a quality mark awarded to

documents that achieve a high standard of plain language.

Welcome to Southern Cross Travel Insurance. This document explains

what your policy covers, the limits to that cover, the terms and

conditions of your policy, and your responsibilities.

Southern Cross Benefits Limited is the insurer of this policy

Southern Cross Benefits Limited, trading as Southern Cross Travel Insurance (SCTI), is the insurer

of this policy.

Our financial strength rating is A (Strong)

Standard & Poor’s (Australia) Pty Ltd has given Southern Cross Benefits Limited an A (Strong) financial

strength rating.

The rating scale is:

• AAA (Extremely Strong)

• AA (Very Strong)

• A (Strong)

• BBB (Good)

• BB (Marginal)

• B (Weak)

• CCC (Very Weak)

• CC (Extremely Weak)

• SD or D (Selective Default or Default)

• R (Regulatory Supervision)

• NR (Not Rated).

Ratings from ‘AA’ to ‘CCC’ may be modified with a plus (+) or minus (-) sign to show relative

standing within the major rating categories. Full details of the rating scale are available at

www.standardandpoors.com. Standard & Poor’s (Australia) Pty Ltd is an approved agency

under the Insurance (Prudential Supervision) Act 2010.

3

Your travel insurance policy document Introduction

A handy checklist for you

If you have questions about how to apply, your cover, or how to claim

Get in touch by phone or email

Phone from New Zealand: 0800 800 571

Phone from overseas: +64 9 979 6593

Email: info@scti.co.nz

> We record all customer calls. This helps us with sta training and if we need to check the

details of any calls.

Before you buy

Make sure it’s safe to travel to your destination

You need to check two things to make sure it’s safe to travel at the time you purchase your policy.

• Check your destinations on www.safetravel.govt.nz. If a destination has a travel advisory of

‘Do not travel’ or ‘Avoid non-essential travel’, your cover will be affected

• Check if the destinations you’re visiting have been in the news. If you book travel to somewhere

that’s been in the news for things that have already happened like natural events, your policy

may not cover you

> See ‘Make sure it’s safe to travel’, page 27.

Before you go

How to buy a policy

You can buy a policy online at: www.scti.co.nz. Alternatively, you can call us on 0800 800 571.

Double-check the information in your policy documents

With so much to plan, it can be easy to overlook mistakes.

We recommend you double check:

• your latest Certificate of Insurance, including your medical assessment

• any special conditions we may have sent you (including any Endorsement to your policy) before

your journey.

Make sure it’s safe to travel to your destinations

You need to check two things before you start your journey (or each journey on an Annual Multi-Trip Policy).

• Check your destinations again on www.safetravel.govt.nz. If a destination has a travel advisory

of ‘Do not travel’ or ‘Avoid non-essential travel’, your cover will be affected

• Check again to see if the places you’re visiting have been in the news. If you travel to somewhere

that’s been in the news for things that have already happened like natural events, your policy

may not cover you

> See ‘Make sure it’s safe to travel’, page 27.

TravelCare

4

Tell us if you may need to cancel or delay your journey

If something unexpected happens and you may need to delay or cancel your journey, you must

do the following.

• Tell us as soon as possible as it may affect your cover

• Tell your service providers, such as your transport provider, hotel, and tour operator, as soon as possible

> See ‘D.2 Cancelling or changing your journey before you leave’, page 43.

Tell us about any health changes

Tell us if the health of anyone listed on your Certificate of Insurance changes — no matter how big

or small the change – so that we can tell you whether we’ll offer you cover for the health changes.

> See ‘Tell us about changes to your health’, page 27.

Make sure you have your policy details handy

You may need to check your policy or tell us your policy number while you’re away. To help you do this,

you could:

• take a printout of your policy with you

• keep the email we sent you that includes your policy information

• text yourself the policy number and the Southern Cross Emergency Assistance number: +64 9 359 1600.

While you’re away

If any of your belongings are lost, stolen or damaged

You must tell the relevant authority, such as the local police, hotel security, or airline, and get

a written report on the incident as soon as you can.

If your belongings were in the care of a service provider, such as a transport provider, hotel,

or tour operator, file a claim with them first.

> See ‘D.4 Baggage and personal items’, page 56

If you are admitted to hospital, need surgery, or need medical treatment

you expect to cost over $2,000

• You or someone acting on your behalf must ask Southern Cross Emergency Assistance for prior approval.

• Phone: +64 9 359 1600 (open 24 hours a day, 7 days a week).

If you need minor medical attention

• If treatment is minor, pay the medical provider then make a claim for assessment.

> Remember – keep all receipts and any medical or dental notes.

If you need to cut your journey short or change your journey

• If you’re in an emergency and need help rearranging your journey, call Southern Cross

Emergency Assistance.

• Phone: +64 9 359 1600 (open 24 hours a day, 7 days a week).

> Only use this number for emergencies, not for general queries or claims queries.

5

Your travel insurance policy document Introduction

Your policy is a contract of insurance between you and us that

consists of all the following.

• This policy wording

• Your latest Certificate of Insurance – which includes your

medical assessment

• Any special terms and conditions we’ve sent you, including any

Endorsement to your policy, that confirm any addition to or

variation of your policy

Read this policy carefully — check it’s right for you

Make sure you read your whole policy so you can travel with peace of mind. As with all insurance

contracts, there are limits to your cover. In particular, please make sure you understand:

• who can get cover on page 7

• what your policy covers on page 8

• the limits to your cover, and the terms and conditions, on page 9

• your responsibilities on page 22

• the general exclusions on page 80

• the losses we don’t cover under each section.

We’ve designed this policy to cover you when you’re travelling overseas on an international journey

for any of the following reasons.

• A holiday

• A visit to friends and family

• Non-manual work, such as working in an office, attending a trade fair at a conference centre,

or going to a training course or business meeting

If you have any questions, call us on 0800 800 571.

A.

Your adventure

starts here

Some words in this policy have specific meanings

If a word or phrase is in italics, it has a specific meaning.

In addition to the words in italics, the following words also have specific meanings:

• ‘we’, ‘us’, and ‘our’ means Southern Cross Travel Insurance

• ‘you’, ‘your’, and ‘yourself’ means the insured people named on your Certificate of Insurance.

To improve the readability of this document, these words have not been put in italics.

> You can find the specific meanings of other defined words under ‘F. Definitions — words with

specific meanings’, page 91.

Headings in this document don’t aect your cover

The headings in this document are to help you find relevant information. They don’t affect the

meaning or interpretation of any cover under this policy.

We use examples to help explain parts of your cover

When we use an example in this policy, it is to help you understand a particular concept, or how

particular parts of your cover work. Other terms and conditions may apply when you make a claim,

and the examples don’t make up all the situations that may apply.

Who can get cover under this policy

You can only get cover under this policy if you meet all the criteria below.

• You live in New Zealand permanently

• You’re eligible for funding for all public health and disability services in New Zealand

• You haven’t already left New Zealand when you buy this policy

• You’re travelling on your journey to a destination outside of New Zealand

• You will return to New Zealand after finishing your journey, or each journey if you are buying an

Annual Multi-Trip Policy

• You haven’t been refused cover, had an insurance claim declined, or had an insurance policy

cancelled or voided, because of fraud

• You have a New Zealand bank account

• You have access to an email address so we can contact you about your policy

When you buy this policy, you confirm that you meet these criteria at the date your insurance was

issued, and will keep meeting the criteria until the date your insurance ends.

If you don’t meet all these criteria at the date your insurance was issued, we treat your policy as void

from that date, and don’t cover any claims.

You must meet all the criteria for the entire period of insurance. If you stop meeting any of the criteria

at any time, your policy will immediately end. From that date, we have no liability for any further claims,

costs, or losses.

Your travel insurance policy document Section A

7

What your policy covers

Your policy covers a wide range of losses that are caused by unexpected events. See the table

on page 9 for a summary of those losses.

An unexpected event is something that happens during your period of insurance and is all

the following.

• Sudden, unforeseeable, or unintended

• Outside of your control

• Something you could not have reasonably expected or avoided

Examples of events that are not unexpected include events that have been in the news or a weather

report before the date your insurance starts, like a storm that’s on its way or severe floods. These

would not be unexpected events. A reasonably well-informed person would have seen that these

events could cause problems for travellers.

This policy covers cruises travelling internationally

This policy automatically covers you while you’re on a cruise ship if all the following apply.

• You travel as a fare-paying passenger

• The cruise is run by a company that’s licensed to operate a passenger carrying service, or is

a tour operator

• On your journey, the cruise is travelling to an overseas destination (including international waters)

This policy doesn’t cover domestic cruises

This policy won’t cover you if you’re travelling on a cruise that stays only in New Zealand

waters.

This policy covers travel on charter vessels overseas

Your policy includes cover for travel while you’re a passenger on a charter vessel overseas if both:

• the charter vessel is crewed

• you only travel within coastal or inland waters.

Some terms have specific definitions

When we use the following term, we mean the definition we give here.

Coastal waters

In this policy, ‘coastal waters’ means waters that are within 12 nautical miles (22.2 km) from

the coast of your overseas destination.

TravelCare

8

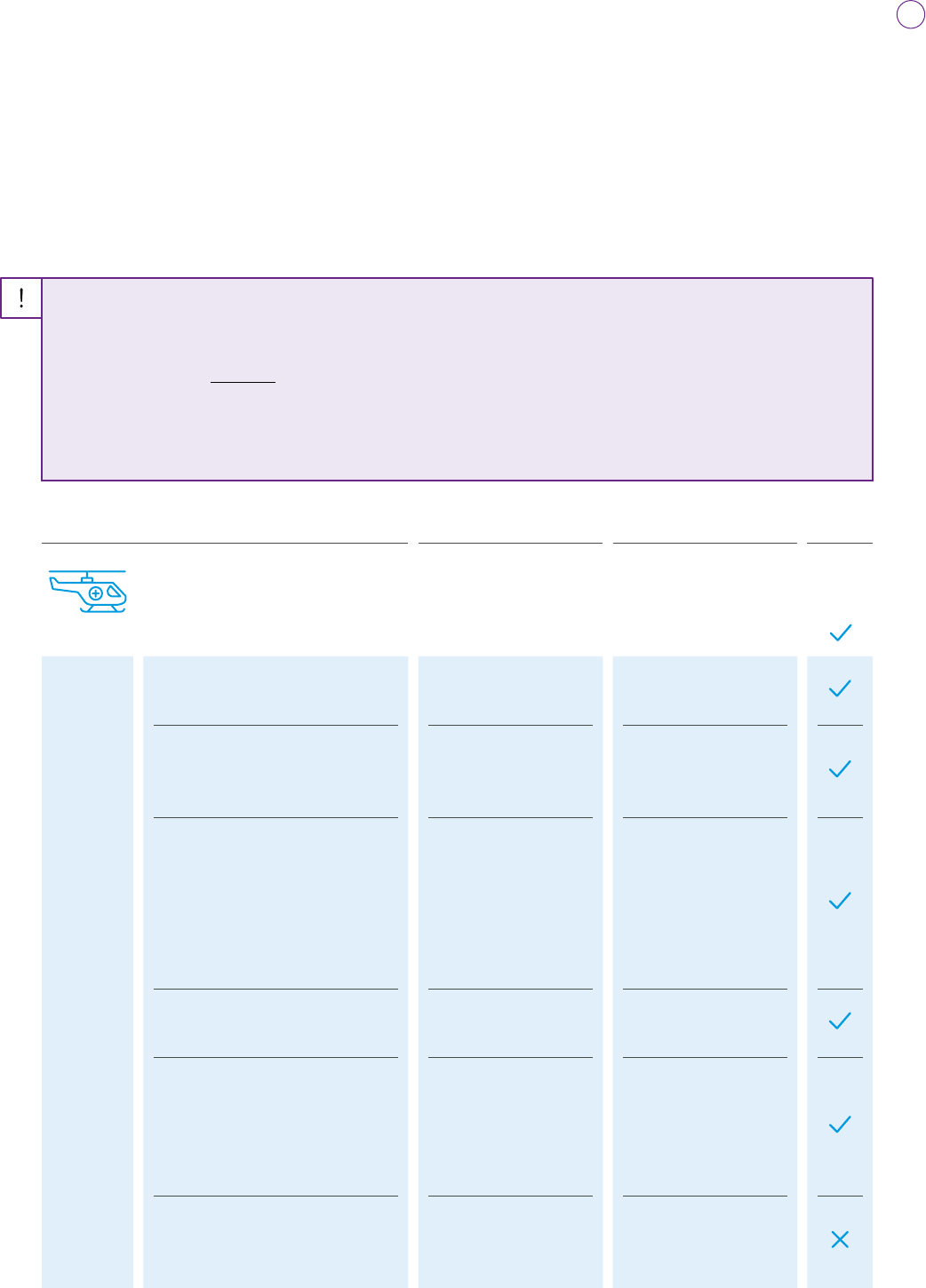

A summary of your cover

The table below summarises the losses this policy covers — use it to help you decide if this policy is

right for you. But it’s just a summary, so you’ll need to read the rest of this document to understand

what you are — and are not — covered for.

All amounts in this policy are in New Zealand dollars and include Goods and Services Tax (GST) and

other duties.

Points to note before you read this table

An excess is the first part of the claim for which you are responsible.

> Learn more on page 15.

We base age-related benefits on your age at the date your insurance starts.

Conditions, exclusions, limits and sub-limits apply.

D.1 Individual cover Family cover Excess

Benefit Medical and evacuation Unlimited Unlimited

Sublimit

D.1.1 Directly or indirectly

related to terrorism

$100,000

for each journey

$100,000

for each journey

D.1.2 Emergency dental

treatment

$750

for each person

for each journey

$750

for each person

for each journey

D.1.3 Cash allowance

while in hospital (after

72 hours)

$100

for each complete

24-hour period

$3,000

for each person

for each journey

$100

for each complete

24-hour period

$3,000

for each person

for each journey

D.1.4 Extra travel and

accommodation

Unlimited Unlimited

D.1.5 Accompanying

person (if you’re in

hospital for more than

10 days and travelling

alone)

$5,000

for each journey

$5,000

for each journey

D.1.6 Funeral expenses

or return of a loved

one’s mortal remains

$15,000

for each

deceased person

$15,000

for each

deceased person

Your travel insurance policy document Section A

9

D.2 Individual cover Family cover Excess

Benefit

Cancelling or changing your

journey before you leave

$2,500 to

unlimited

$5,000 to

unlimited

Sublimit

D.2 Any claim for frequent

flyer points

$2,500 to

$5,000

for each journey

$5,000

for each journey

D.2 Any claim relating to

the existing condition

of a relevant person

$2,500

for each person

$5,000

for each journey

$2,500

for each person

$5,000

for each journey

D.2.1 Cancelling or changing

your journey

$2,500 to

unlimited cover

for each journey

$5,000 to

unlimited cover

for each journey

D.2.2 Delayed journey to

a special event

$2,500 to

$3,000

for each person

$6,000

for each journey

$2,500 to

$3,000

for each person

$6,000

for each journey

D.3 Individual cover Family cover Excess

Benefit

Changes to your journey

once you have left $50,000 $100,000

Sublimit

D.3 Any claim for frequent

flyer points

$5,000

for each journey

$5,000

for each journey

D.3 Any claim relating to

the existing condition

of a relevant person

$2,500

for each person

$5,000

for each journey

$2,500

for each person

$5,000

for each journey

D.3.1 Travel interruption $30,000

for each journey

$30,000

for each journey

D.3 .2 Cutting your

journey short

$50,000

for each journey

$100,000

for each journey

D.3.3 Delayed journey

to a special event

$3,000

for each person

$6,000

for each journey

$3,000

for each person

$6,000

for each journey

TravelCare

10

D.4 Individual cover Family cover Excess

Benefit

Baggage and

personal items $25,000 $50,000

Sublimit

D.4.1 Unspecified

jewellery (or pair or

set) and watches

Depreciation applies

$2,500

for all items for

each journey

$2,500

for all items for

each journey

D.4.1 Unspecified

laptops, personal

computers, tablets,

cameras (including

related accessories

Depreciation applies

$3,000

for each item

$10,000

for all items for

each journey

$3,000

for each item

$10,000

for all items for

each journey

D.4.1 Other unspecified

items (or pair or set

of items) including

related accessories

Depreciation applies

$1,500

for each item

$1,500

for each item

D.4.2 Specified items

(or a pair or set)

including related

accessories (in each

case inclusive of

accessories as a set

of equipment items)

$10,000

for each item

$15,000

for all items for

each journey

$10,000

for each item

$15,000

for all items for

each journey

D.4.3 Baggage delay

during your journey

$1,000

for each person

$5,000

for each journey

$1,000

for each person

$5,000

for each journey

D.4.4 Essential

medication

$500

for each person

$500

for each journey

$500

for each person

$500

for each journey

D.5 Individual cover Family cover Excess

Benefit

Cash, bank cards, travel

documents and passports $1,000 $2,000

Sublimit

D.5 Cash $500

for each journey

$500

for each journey

Your travel insurance policy document Section A

11

D.6 Individual cover Family cover Excess

Benefit

Personal

accident

$25,000

(16–80 years)

$50,000

(16–80 years)

Sublimit

D.6.1 Loss of income $6,500

for each injured

person ($500

for each week)

$13,000

for each journey

$6,500

for each injured

person ($500

for each week)

$13,000

for each journey

D.6 .2 Total permanent

disablement

$25,000

for each journey

$50,000

for each journey

D.6.3 Loss of life $25,000

for each journey

$25,000

for each journey

D.7 Individual cover Family cover Excess

Benefit

Personal

liability

$1,000,000

for each journey

$1,000,000

for each journey

D.8 Individual cover Family cover Excess

Benefit

Rental vehicle

excess

$5,000

for each journey

$5,000

for each journey

D.9

Moped and

motorbike cover

See ‘D.9 Optional:

Moped and

motorbike cover’,

page 76

See ‘D.9 Optional:

Moped and

motorbike cover’,

page 76

D.10

Skiing and

snowboarding cover

See ‘D.10

Optional: Skiing

and snowboarding

cover’, page 78

See ‘D.10

Optional: Skiing

and snowboarding

cover’, page 78

You can increase the amount of cover you have for your journey

This policy provides cover if you need to cancel or change your travel arrangements before leaving

on your journey because of an unexpected event. When you buy this policy, you’re covered for the

following amounts.

• $2,500 for each journey – if you buy Individual cover

• $5,000 for each journey – if you buy Family cover

TravelCare

12

When you buy this policy, you can choose to increase your cover up to an unlimited amount under

‘D.2 Cancelling or changing your journey before you leave’ on page 43. Think carefully before you

decide how much cover you need. To help you decide, make notes on what you’ve paid, or will have to

pay before you leave, for the travel, accommodation, event tickets and tours you’ve booked.

For example, if you chose a limit of $5,000 for each journey, but spend $15,000 on your journey,

the most you can claim is $5,000 if you have to cancel that journey.

You can add extra cover for specific items

This policy covers you for personal items you take with you but haven’t told us about. We call these

‘unspecified’ items. When we pay your claim for an unspecified item, we only pay up to the benefit

limits in the table on page 57.

You can increase the benefit limit for more valuable personal items by asking us to cover them as

̒specified̕ items. We’ve made it easy for you to specify items — from watches and jewellery to laptops

and mobile phones. Learn more about cover for specified items on page 59.

There are some items we never cover

Before you specify an item or decide if you want to take it with you, make sure it isn’t something we

would never cover.

> See ‘D.4.5 Other losses we won’t cover’, page 63 and ‘E. General exclusions — things we

never cover’, page 80.

Depreciation may apply to claims for your personal items

When you claim for a personal item, we may subtract the value the item has lost over time

(depreciation). The table below shows how we apply depreciation to items.

Type of personal item

Does

depreciation

apply?

Unspecified items

Specified items Specified items where you can’t provide proof of

ownership and value, as shown on page 59

Any other specified items where you can

provide proof of ownership and value, as shown

on page 59

Your travel insurance policy document Section A

13

Check you’re not already covered under another policy

We won’t cover you for claims, costs, losses or liabilities if you have another insurance policy that

already covers you. We won’t contribute to any claim under any other policy. This applies to any

section you claim under in this policy.

Check any other insurance policies you have before you add extra cover for your specified items.

You can remove cover for your specified items and get a premium refund:

• before the date your journey starts, if you have a Single Trip Policy

• before the date your insurance starts, if you have an Annual Multi-Trip Policy.

You can add cover for skiing and snowboarding

This policy does not automatically cover you for skiing or snowboarding. However, you can add this

cover when you apply. Even if you add this cover, you will need to follow some conditions.

> Learn more about cover for skiing and snowboarding on page 78.

You can add cover for riding mopeds and motorbikes

This policy does not automatically cover you while riding a moped or motorbike – this includes you

driving or being a passenger. However, you can add cover when you apply. Even if you add this cover,

you need to follow some conditions.

> Learn more about cover for moped and motorbikes on page 76.

Choose the destinations you’re travelling to

When you buy your policy, you must tell us which destinations you want to cover – including any transit

stops where you’ll leave the airport.

You don’t have to list:

• when it includes travel through New Zealand waters – see ‘This policy covers cruises travelling

internationally’ on page 8

• transit stops, when they’re less than 24 hours and you’ll stay in the airport – you’re automatically

covered in those airports.

We won’t cover you for events outside of the airport in a destination that isn’t listed on your

Certificate of Insurance.

If you have a Single Trip Policy, you can change the destinations you have cover for before you set off

on your journey. However, once you’ve departed on your journey, you can only add new destinations.

If you have an Annual Multi-Trip Policy, you can change the destinations before the date your

insurance starts. However, after the date your insurance starts, you can only add new destinations.

Some destinations may be free to add cover for. We may charge an additional premium for other

destinations.

To change the destinations you have cover for, or if you’re unsure which destinations you’ll be

travelling to, please call us on 0800 800 571 or email us at: [email protected]

TravelCare

14

Choose your excess

An excess is the first part of the claim, for which you are responsible. If an excess applies to a claim,

we subtract that excess from the amount we pay.

When you apply for your policy, you can choose whether to have an excess. Your premium may be

higher if you choose to not have an excess.

We only subtract one excess for each unexpected event. So, if an unexpected event means you need

to claim under more than one section of this policy, we only subtract one excess. However, if more

than one unexpected event affects you, we subtract an excess for each event.

You won’t pay an excess on the following benefits:

• ‘D.1.6 Funeral expenses or returning mortal remains’ (page 42)

• ‘D.6 Personal accident’ (page 69)

• ‘D.7 Personal liability’ (page 72)

• ‘D.8 Rental vehicle excess’ (page 74).

How we work out what you need to pay for your policy

Your premium is the amount you must pay for your policy. We tell you how much your premium is

when you apply for your policy. We base the premium on several things, including:

• whether you want to cover a single journey or many separate journeys across the year (see page 17)

• if you chose an Annual Multi-Trip Policy, the maximum trip duration you select

• the number of adults, children, and non-dependent children you want cover for, and how old they are

• which destinations you’re travelling to

• how long you want cover for

• what excess you’ve selected

• whether you’ve increased the amount of cover you have under ‘D.2 Cancelling or changing your

journey before you leave’ (see page 43)

• whether you’ve added any specified items, and the value of those items (see page 59)

• whether you’ve added cover for skiing and snowboarding (see page 78)

• whether you’ve added cover for moped and motorbikes (see page 76)

• whether you’ve added cover for any pre-existing medical conditions (see page 31).

Your premium includes government duties and taxes, including Goods and Services Tax (GST),

if applicable.

This policy covers dependent children for free

We cover your dependent children for free while they’re with you on your journey.

A dependent child can be any of the following.

• Your child, stepchild, or foster child

• Your grandchild

• Your niece or nephew

Your travel insurance policy document Section A

15

For a child to be dependent, they must also meet all the following criteria.

• They must be under 21 years old at the date your insurance was issued.

• If they are 18 years old or over, they must:

– be unmarried

– not be in full-time employment

– be financially dependent on at least one adult listed on your Certificate of Insurance (a child

is not financially dependent if you’re only covering their finances while on the journey).

This policy doesn’t automatically cover pre-existing medical conditions (see page 29) and

specified items (see page 59). So, if your dependent children need cover for these, you may need

to pay an extra premium.

You’ll need to pay a premium for non-dependent children

We charge a premium for any children travelling who aren’t dependent children. Examples of

non-dependent children include children who aren’t related to any of the adults your policy covers,

such as your child’s friend. Children travelling without any adults are non-dependent children and

we charge them a premium.

Non-dependent children travelling without an adult each need their own separate policy.

You’ll have Individual or Family cover on your journey

We have two types of cover under this policy – Individual and Family cover. We’ll automatically select

your cover type when you confirm the number and type of travellers on your policy.

Individual cover Family cover

Applies to any:

• one non-dependent child

• one adult

• one adult and any dependent children.

Two or more children travelling

without an adult must have separate

‘Individual’ policies.

Applies to either:

• two adults

• two adults and any dependent children.

With Family cover on an Annual Multi-Trip

Policy, the following criteria apply.

• Adults can travel independently

• Dependent children are only covered if

travelling with an adult who’s covered by

the policy

As two adults are covered under Family cover, some benefits have higher maximum cover for each

journey – see page 9.

TravelCare

16

Choose a Single Trip Policy or an Annual Multi-Trip Policy

You can choose one of our two policies.

• The Single Trip Policy covers you for a single return journey overseas, for up to 12 months

• The Annual Multi-Trip Policy covers you for an unlimited number of overseas return journeys

(up to a maximum trip duration for each journey) in a 12-month period

With a Single Trip Policy, the journey, including any policy extension we agree to, can’t be longer

than 12 months in total from the date your journey starts.

Select your travel dates with a Single Trip Policy

With a Single Trip Policy, you select the dates you will depart and return to New Zealand. You don’t

need to choose when your cover starts because it starts on the day you buy it.

> Learn how your cover starts and stops on page 20.

Select when you’d like your cover to start with an Annual Multi-Trip Policy

With an Annual Multi-Trip Policy, you’ll need to choose when you want your cover to start. If you want

your cover to start as soon as you buy your policy, select today’s date.

Your 12 months of cover begins on the date you choose for your cover to start.

If you choose to start your cover after the day you buy your policy, you won’t have any cover until the

date you chose. For example, you won’t have cancellation cover for any events that happen before the

date your insurance starts.

> Learn how your cover starts and stops on page 20.

With an Annual Multi-Trip Policy, you’ll have to select a maximum trip duration

If you choose an Annual Multi-Trip Policy, you’ll have to choose the maximum length of cover you want

for each journey – we call this the ‘maximum trip duration’.

You can choose a maximum trip duration of 30, 60, or 90 days. If you want to go on a journey that’s

longer than 90 days, the Single Trip Policy may be a better option.

Day one of your maximum trip duration is the day you start each journey. If you’ve chosen 30 days as

your maximum trip duration, but take a 35-day journey, the policy won’t cover you for the last 5 days.

So, choose your maximum trip duration carefully.

> If you’re planning a journey that’s longer than your maximum trip duration, get in touch to

discuss your options.

Your travel insurance policy document Section A

17

We may decide to offer you different cover, or refuse cover

When you apply for your policy, we can decide how and when to offer cover. We may decide to not

offer you cover, or to offer you cover on different terms and conditions — even if you’ve had a policy

with us before.

We may send you special terms and conditions in any of the following.

• Your Certificate of Insurance – which includes your medical assessment

• Any Endorsement to your policy

If we do send you special terms and conditions, your cover will be determined by both:

• the terms and conditions in this policy

• the special terms and conditions we send you.

We email your policy documents when we accept your application

If we accept your application, we send you an email that confirms your cover. The email will include:

• a copy of this policy

• your Certificate of Insurance and medical assessment, which set out:

– details of your policy

– details of your medical cover and your answers to the medical questions

• any special conditions that apply to your policy (including any Endorsement to your policy).

These documents form your insurance contract.

We usually contact you by email

We send emails to the main policyholder using the email address you give us.

We use email to send you any important documents. If you don’t want to share these important

documents with the main policyholder, you’ll need to buy a separate policy.

When we make decisions and set timeframes, we use the dates we send an email rather than the date

it was delivered or received.

If you don’t receive an email you’re expecting, please check your junk mail first, then contact us.

TravelCare

18

If you’re the main policyholder

If you’re the main policyholder, you’re responsible for:

• passing on any information we send you to the people named on your Certificate of Insurance

• any information you give us about people named on your Certificate of Insurance.

> See ‘Give us accurate and complete information’, page 22.

For our records, if we contact the main policyholder, we’ve contacted everyone named on your

Certificate of Insurance.

We keep your information private

Our privacy statement explains when and how we collect, hold, use, and disclose your personal

information. You can find our privacy statement at: www.scti.co.nz/privacy

For example, we use the information about you to:

• decide whether we can cover you

• decide how much you should pay for cover

• process any claims.

We won’t rent or sell your personal information to other companies.

If you would like to access or correct your personal information, please email us at: in[email protected]

You have a 14-day free look period

If you cancel your policy within 14 days of buying it, you can get a full refund if you meet all the

criteria below.

• You tell us you want to cancel within 14 days of buying your policy

• You haven’t started your journey

• You haven’t made a claim, and don’t intend to make a claim

Tell us you want to cancel by calling 0800 800 571 or emailing us at: info@scti.co.nz

Refunds if you cancel after the 14-day free look period

If you cancel your Single Trip Policy after the 14-day free look period, you can get a full refund,

but you’ll need to pay a $35 cancellation fee and meet all the criteria below.

• You haven’t started your journey (you can’t cancel your policy after the date your journey starts)

• You haven’t made a claim or intend to make a claim

If you cancel your Annual Multi-Trip Policy after the 14-day free look period, you can get a full refund

if you meet the criteria below. You don’t have to pay a cancellation fee.

• Your cover hasn’t started (you can’t cancel your policy after the date your insurance starts)

• You haven’t made a claim or intend to make a claim

Tell us you want to cancel by calling 0800 800 571 or emailing us at: info@scti.co.nz

Your travel insurance policy document Section A

19

When your cover starts and stops

When you buy your policy, you select the dates relevant to your cover. You can’t buy this policy if

you’ve already started your journey.

Cancellation cover begins on your date your insurance starts

From the date your insurance starts, you have cover under ‘D.2 Cancelling or changing your journey

before you leave’ (see page 43).

The date your insurance starts is different depending on whether you have the Single Trip Policy or

Annual Multi-Trip Policy. See the table below for details.

Single Trip Policy Annual Multi-Trip Policy

You don’t need to choose when your cover

starts. The date your insurance starts is the

date and time you buy your policy.

You must choose the date your insurance

starts. It can be the date you buy your policy

or any other date before the start of your

first journey.

Your cover begins on the date you choose

as the date your insurance starts.

The rest of the cover kicks in under the other sections when you start

your journey

How your cover starts under the other sections is different depending on whether you have the

Single Trip Policy or Annual Multi-Trip Policy. See the table below for details.

Single Trip Policy Annual Multi-Trip Policy

The rest of your cover starts when you leave

on your journey.

The rest of your cover starts when you leave

on each journey.

When you return from your journey your full

cover stops. This means between journeys

you only have cover under ‘D.2 Cancelling or

changing your journey before you leave’

(see page 43).

TravelCare

20

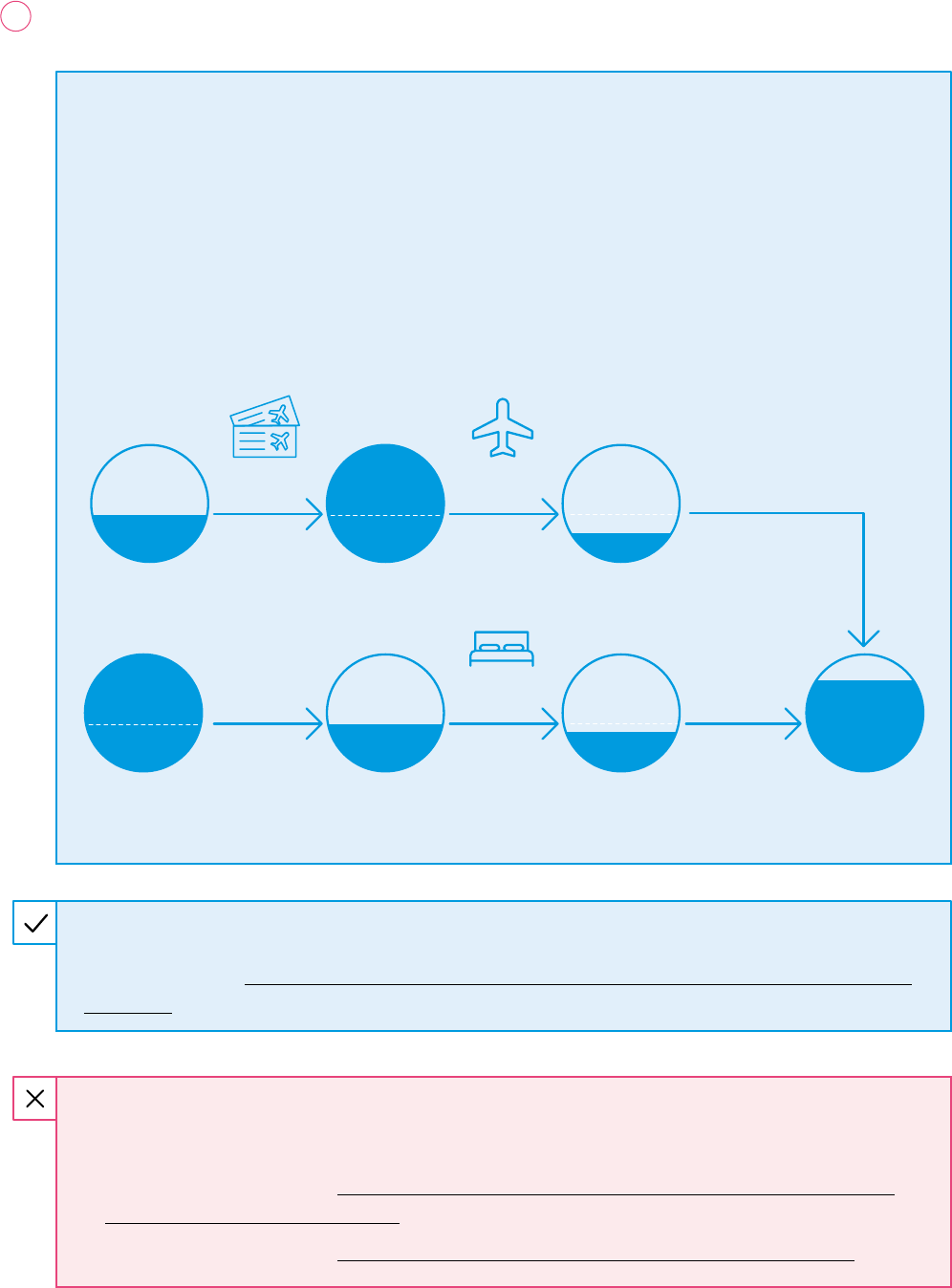

When cover for your journey ends

If you change your plans and return to New Zealand early or stay overseas longer make sure you know

when your cover for your journey ends. This is different depending on whether you have the Single Trip

Policy or Annual Multi-Trip Policy. See the table below for details.

Single Trip Policy Annual Multi-Trip Policy

Cover for your journey ends at whichever

is earliest:

• on the date and time you return to

New Zealand

• on the date your insurance ends.

Cover for your journey ends at whichever

is the earliest:

• on the date and time you return to

New Zealand

• on the last day you selected as your

maximum trip duration

• on the date your insurance ends.

For example, on a Single Trip Policy if you return to New Zealand early, cover for your journey stops

at the date and time you arrive back. If you stay overseas longer, your cover stops on the date your

insurance ends.

When cover for your policy ends

Cover under your policy ends on the date your insurance ends.

When we will — and won’t — extend your cover

This part of the policy explains the circumstances where we can extend your policy.

We extend your cover at no charge if an unexpected event means you

can’t return home

If an unexpected event that we cover stops you from returning to New Zealand, we can extend your

cover at no charge if you call us at 0800 800 571 or email us at: in[email protected]

When you contact us, we’ll tell you in writing when your extended cover will end. This will form part of

your insurance contract.

To keep getting cover, you must go along with any arrangements we make to get you back to

New Zealand. If this is related to a medical event, you must return to New Zealand once we, or our

medical team, say you’re fine to travel.

Your cover stops if you decide to continue your journey or don’t follow our arrangements.

Remember, if you have an Annual Multi-Trip Policy, let us know if your health has changed before you

start your next journey. We can tell you whether we’ll offer you cover for the health changes for any

future journey under your policy.

> See ‘Tell us about changes to your health’ (page 27).

Your travel insurance policy document Section A

21

You can ask us to extend your Single Trip Policy cover for an extra charge

You can ask us to extend your cover if all the following apply.

• You have a Single Trip Policy

• You are still overseas

• You haven’t reached the date your insurance ends

• Your length of cover (including the extension) is no more than 12 months

If we agree to extend your cover, you’ll need to pay an extra premium. We won’t extend your policy

if your insurance has already ended.

Tell us if you need to extend your cover by calling 0800 800 571 or emailing us at: [email protected]

Extensions won’t cover unexpected events that have already happened

If we offer to extend your cover for an extra premium, the extension won’t cover any unexpected

events that happened during the original period we were covering you.

Making other changes to your policy

You can ask us to change your policy. We decide whether to make any changes you ask for.

If we agree to make a change, we’ll:

• tell you if you need to pay an extra premium

• tell you if we need to revise your policy or send you a new one

• email you to confirm the change and include your changed or new insurance documents.

The changes only take effect when we have sent the email confirming the change and we’ve

received any extra premium.

If you return to New Zealand early, we won’t shorten your policy or refund any premium.

Your responsibilities

As a condition of your cover, you must meet the following responsibilities. These responsibilities

apply to all sections of this policy.

You must be reasonably careful

We expect you to take reasonable care to avoid or minimise a loss, and to take extra care of more

valuable items.

Give us accurate and complete information

You must be honest and fair with us. All the information we get from you, or anyone acting on your

behalf, about this policy and any claim must be honest, accurate and complete.

TravelCare

22

What we can do if you don’t meet your responsibilities

If you don’t meet the responsibilities above, we may:

• refuse to issue a policy

• decline any claim

• reduce our liability for any claim

• recover any amount we’ve already paid you for claims

• cancel this policy

• void this policy — this means treating your policy as though it never existed

• we may refuse to insure you in the future.

If we decide to cancel your policy:

• we’ll do it by email

• we won’t cover you or anyone listed on your Certificate of Insurance from the cancellation date

in the email

• we may keep the premium you’ve paid for the policy

• we may refuse to insure you in the future.

If we decide to void your policy:

• we’ll do it by email

• we’ll treat the policy as if it had never existed, and won’t cover you or anyone listed on your

Certificate of Insurance

• we’ll return the premium you paid for the policy

• you’ll have to refund any amount we’ve already paid you for claims, if we ask

• we may refuse to insure you in the future.

Claiming and the claims process

It’s stressful when things go wrong on a journey, so we’ve made it as straightforward as possible to

make a claim. It’s important that you tell us as soon as you become aware of any circumstances that

may result in a claim.

Making your claim

You can make a claim online at: www.scti.co.nz/claims. Follow the prompts and upload your

supporting documents. To avoid delays, make sure you have your supporting documents ready.

When you make your claim, we may ask you to complete an authorisation form. You must complete

this form and return to us before we can assess your claim.

If you have any questions about making a claim, call us on 0800 800 571.

Your travel insurance policy document Section A

23

You can only claim for the same standard of travel and accommodation

If your plans change, you may have to book new flights or accommodation. If this happens, you can

only claim for travel or accommodation that’s the same standard you originally booked. For example,

if you booked premium economy seats, we won’t cover an upgrade to business class.

If you can’t book the same standard of flights or accommodation, you must get our permission before

you book a higher standard.

You have responsibilities at claim time

You’re responsible for doing certain things described in this section before and after you claim,

and after we accept your claim. These responsibilities apply to any section you claim under.

Before you claim

You must do all the following before you make a claim.

Tell us as soon as possible

Make a claim as soon as possible.

Prevent any further loss

You must take all reasonable steps to prevent further loss or liability. For example, you would not be

taking all reasonable steps to prevent further loss if you:

• Knew you couldn’t make your journey, but couldn’t get a refund or credit because you cancelled

too late.

• Continued to pay towards your journey when you knew you had a change in your health that later

affects your ability to travel.

• Received medical treatment in a private hospital in a country where you could have received free

or subsidised medical treatment under the public health system.

Get written reports for medical events

For minor medical events, you pay the costs yourself and submit a claim for assessment. Get a

medical report from your medical professional and a copy of any prescriptions you’re given.

You’ll need to submit these with your claim along with your receipts for the payments.

For major medical events, we’ll work with you or the hospital to get the information we need to

decide cover, so it’s important that you call Southern Cross Emergency Assistance as soon as

you can on +64 9 359 1600.

Get written reports for lost, stolen or damaged items

If your items are lost, stolen or damaged, you must report it to the relevant authorities, such as the

police or your airline operator as soon as possible, and get a written report from them. If you don’t

report lost or stolen items to the relevant authorities, we won’t pay your claim.

For any claims relating to a lost or stolen mobile phone or device with phone capabilities, you must

block the International Mobile Equipment Identity (IMEI) number. You must also send us proof

that this IMEI number has been blocked, or confirmation from your provider confirming that it can’t

be blocked.

TravelCare

24

Claim refunds, credits, payments, or compensation from anyone else, if you can

You must seek refunds, credits, payments, or compensation from other parties for the loss you’re

claiming. For example:

• an airline might give you a refund or a credit,

• your credit card provider might give you a refund

• you may be able to claim against a hotel, a transport provider (an airline, ferry operator, or bus

company), or travel and tour operator.

If we accept your claim, we’ll pay the difference between your cover and any other refunds, credits,

payments, or compensation you’ve received.

Both of the following must apply.

• You’ve got any other refunds, credits, payments, or compensation for the loss

• Your claims against anyone else have been decided

We will ask you to prove that you can’t get a refund, credits, payments, or compensation for any costs

you’re claiming.

If you have other insurance, we won’t pay your claim.

Preserve anything that is part of the claim

Don’t destroy, dispose of or have repaired anything that is or could be part of the claim.

Once you have claimed

You must do all the following once you’ve made a claim.

Follow our instructions

Do what we ask you to do and give us the information and help that we need. We may decide to not

pay your claim if you don’t do what we, or Southern Cross Emergency Assistance, ask you to do.

Provide us with proof to support your claim

Send us proof to support your claim. Each benefit requires specific evidence that’s needed to prove

your claim. You’ll need to refer to the benefit you’re claiming under to understand what you need to

send to us.

Give us necessary documents and authority to act

Give us all necessary documents and authority so that we can deal with your claim. For a claim under

‘D.7 Personal liability’, you must let us take over, and conduct in your name, the defence or settlement

of any claim, and give us full discretion in the handling of any legal proceedings.

If someone is claiming against you, refer them to us

If someone is making a claim against you, don’t admit any liability. Instead, let us know about the

situation and follow our advice.

Your travel insurance policy document Section A

25

Once we’ve accepted your claim

You must do all the following once we’ve accepted your claim.

Help us recover money from someone else, if we ask

We have the right to take action to get money back from a person or company that caused a loss

you’ve claimed for under your policy.

We’ll pay for any action and may:

• act in your name to get money back from other parties

• take over defending an action that other parties are carrying out against you

• defend and settle any claim against you.

You must not start any action against other parties without our written permission. ‘Action’ includes

incurring expenses and negotiating, paying, settling, or agreeing on compensation.

You must help us by:

• answering our questions and giving us any information we ask for

• cooperating with us and anyone else we appoint to help us recover the money.

If we pay you for a damaged item, send it to us

Where we pay your claim for a damaged item, it becomes ours. If we ask, you must send it to us,

at our cost.

Tell us if your lost or stolen property is recovered

If any lost or stolen items that you claimed for are found, you must tell us. Then we’ll decide whether

you must give us the recovered items, or refund any money we paid you for them.

What we can do if you don’t meet your responsibilities

If you don’t meet the responsibilities under this section ‘You have responsibilities at claim time’,

we may:

• decline any claim

• reduce our liability for any claim

• recover any amount we’ve already paid you for claims

• cancel this policy

• refuse to insure you in the future.

If we cancel your policy:

• we’ll do it by email

• we won’t cover you or anyone listed on your Certificate of Insurance from the cancellation date

in the email

• we may keep the premium you’ve paid for the policy

• we may refuse to insure you in the future.

TravelCare

26

Some advice before you go

Make sure it’s safe to travel

You must make sure it’s still safe to travel to your destinations by checking for travel advisories on the

SafeTravel website www.safetravel.govt.nz

Your policy may be affected if the travel advisory on the SafeTravel website is ‘Do not travel’ or ‘Avoid

non-essential travel’.

You need to check this when you buy your insurance, again before you start your journey, and before

leaving for each new destination.

The table below shows how travel advisories affect your policy.

Type of travel advisory Eect on your policy

A travel advisory that affects just

part of a country

You won’t be covered for events in that part of the

country that relate to that travel advisory.

A travel advisory that affects the

whole country

You won’t be covered for events anywhere in that country

that relate to that travel advisory.

Multiple travel advisories may apply to a country. For example, Ministry of Foreign Affairs and Trade

(MFAT) may issue an entire country with a travel advisory because of kidnapping threats. In addition,

a city in that country may be experiencing civil riots which results in MFAT issuing a partial travel

advisory to that specific area.

Your cover may be impacted if you buy your policy, then your destination is given a travel advisory

before you leave for that destination, including if you are already overseas at the time the travel

advisory is issued.

To find out how you are covered if a travel advisory changes for a destination on your journey, call us

on 0800 800 571.

Tell us about changes to your health

This policy doesn’t automatically cover changes to your health after the date your insurance was

issued other than where you qualify for cover under ‘D.2 Cancelling or changing your journey before

you leave’ (page 43).

However, if you contact us to complete a medical assessment, we may be able to offer you cover for

these changes.

Your travel insurance policy document Section A

27

Contact us if you want to make a complaint

If you’re unhappy with any part of your insurance, or the service we’ve provided, please let us know.

We take complaints seriously and do our best to resolve them.

You can call us on 0800 800 571, or email us at: [email protected]

If we can’t resolve your problem after you first contact us, we’ll ask you to follow our internal complaint

process — see: www.scti.co.nz/complaints

If you’re not satisfied with the result of your complaint, you can take it to the independent Insurance

& Financial Services Ombudsman Scheme. You can find out more about the Ombudsman Scheme

at: www.ifso.nz

We have a vulnerable customer policy

You can access our vulnerable customer statement (including how we support customers in a family

violence situation) on our website at: www.scti.co.nz/vulnerable

New Zealand law applies

Any legal disputes about this policy will be decided under New Zealand law.

TravelCare

28

This section applies to any claim under this policy. It explains how and

when we can cover:

• illnesses, injuries, and health symptoms that you knew about when

you applied for your policy — we call these pre-existing medical

conditions

• changes to your pre-existing medical conditions after you buy

your policy

• any new illness, injury, or health symptom that you discover after

the date your insurance was issued and before the date your

journey starts.

> The terms and conditions in this section apply when you a make claim under

‘D. What is and isn’t covered’ (see page 36).

Section B

29

Your travel insurance policy document

B.

How we cover

pre-existing

medical conditions

Pre-existing medical conditions

We don’t automatically cover any pre-existing medical condition

The policy doesn’t automatically cover your pre-existing medical conditions. However,

if you complete a medical assessment, we may be able to offer you cover for your

pre-existing medical conditions.

We won’t cover undiagnosed pre-existing medical conditions at all

We won’t cover undiagnosed pre-existing medical conditions. For example, if you’re

experiencing stomach pains but the medical professionals don’t know why, or you’re

awaiting test results, we won’t cover those symptoms.

What we consider a pre-existing medical condition

A pre-existing medical condition is any illness, injury, or health symptom to which all the

following apply.

• You know about it, or a reasonable person should have known about it prior to the date your

insurance was issued.

• In the 3 years before the date your insurance was issued, any of the following applied.

– You sought or received medical help

– Someone recommended you seek or receive medical help

– A reasonable person would have sought or received medical help

– You were waiting for medical help

In this definition, ‘medical help’ means any of the following.

– Advice from a health professional

– Tests, investigations, or specialist consultations

– Care, treatment, or medical attention, including surgery

– Medication or a script for medication

An illness, injury or health symptom doesn’t need a confirmed medical diagnosis to count as

a pre-existing medical condition.

30

TravelCare

We treat pregnancy complications as pre-existing medical conditions

If you have had any pregnancy complications in the 3 years before the date your insurance was issued,

we consider these complications to be pre-existing medical conditions. If you experience those same

complications, we won’t automatically cover you, so if you want cover, you should apply.

Examples of pregnancy complications include:

• pre-eclampsia

• recurrent miscarriage (that is, three or more consecutive miscarriages)

• small for date baby

• postnatal depression.

We may be able to cover you for pre-existing medical conditions

If you complete a medical assessment, we may be able to offer you cover for your pre-existing

medical conditions.

Changes to health

We don’t automatically cover changes to your health other than under

‘D.2 Cancelling or changing your journey before you leave’

This policy doesn’t automatically cover changes to your health other than under

‘D.2 Cancelling or changing your journey before you leave’ (see page 43).

If there’s a change to your health before your journey, we may cover you under ‘D.2 Cancelling or

changing your journey before you leave’ (see page 43), even if we can’t cover that condition on

your journey.

We only cover you under ‘D.2 Cancelling or changing your journey before you leave’ (see page 43)

if medical advice states that you are not medically fit to travel on your journey as it was originally

arranged.

Unless you contact us and we confirm otherwise, we won’t cover any payments you make after

you become aware, or a reasonable person would have been aware, of any changes to your health.

We won’t cover undiagnosed changes to your health at all

We won’t cover undiagnosed changes to your health. For example, if you’re experiencing

stomach pains but the medical professionals don’t know why, or you’re awaiting test results,

we won’t cover those symptoms.

Section B

31

Your travel insurance policy document

What we consider to be changes to health

A change to your health before you travel is any new illness, injury or health symptom, or change

to a covered condition, to which all of the following apply:

• It occurs between the date your insurance was issued and the date your journey starts.

For Annual Multi-Trip Policies, the date your journey starts applies to each journey you start.

• You know about it, or a reasonable person should know about it.

• Any of the following apply:

– you seek or receive medical help

– someone recommends you seek or receive medical help

– a reasonable person would seek or receive medical help

– you are waiting for medical help

In this definition, ‘medical help’ means any of the following:

– advice from a health professional

– tests, investigations or specialist consultations

– care, treatment, or medical attention, including surgery

– medication or a script for medication

A new illness, injury or health symptom, or change to a covered condition doesn’t need a confirmed

medical diagnosis to count as a change to your health.

Changes to a covered condition include any change in the prognosis, treatment or medication

(including dose).

We may be able to cover you for changes to your health before you travel

If you contact us to complete a medical assessment, we may be able to offer you cover for these

changes to your health.

Before you travel, we recommend getting your doctor to check for any new health conditions or

symptoms you or anyone traveling may have. If your doctor tells you or anyone traveling of any new

illness, injury, health symptom, or change to a covered condition before the date your journey starts,

contact us to see if we can offer cover.

How to apply to cover your pre-existing medical condition,

or changes to your health, under section D

To apply for cover for your pre-existing medical condition or changes to your health you must both:

• complete the medical assessment when you apply for cover

• tell us about all your pre-existing medical conditions or changes to your health when you complete

the medical assessment.

We need to know the name of the health condition or health symptom of your pre-existing medical

condition or changes to your health when you apply. If you’re unsure, check with your doctor first. If

you don’t tell us about all your pre-existing medical condition or changes to your health it could affect

your cover when you submit a claim.

32

TravelCare

You must tell us about all your pre-existing medical conditions

or changes to your health, not just some

If you choose to tell us about one pre-existing medical condition or changes to your health, you must

tell us about all your pre-existing medical conditions or changes to your health when you apply for

cover and complete the medical assessment.

If you don’t tell us about any pre-existing medical conditions

or changes to your health, we won’t cover them

If you don’t tell us about your pre-existing medical conditions, we won’t cover anything related

to them.

If you don’t tell us about changes to your health, we will only provide the cover available under

‘D.2 Cancelling or changing your journey before you leave’ (page 43).

Call us about your pre-existing medical condition or change

to your health, if you’re unsure

Making sure you have the right cover for your health is important to us. If you have any questions,

call us on 0800 800 571.

You can accept or decline our oer to cover you for a pre-existing

medical condition or change to your health

If we offer to cover any of your pre-existing medical conditions or change to your health which you tell

us about in your medical assessment, you can choose to accept or decline our offer.

If you accept our oer, you may need to pay an extra premium

You may need to pay an extra premium if you accept our offer. When we receive that premium,

we send you an email confirming the pre-existing medical conditions or change to your health we

have agreed to cover. Your medical assessment will list them as covered conditions.

If you decline our oer, we won’t cover your pre-existing medical conditions

You won’t need to pay any extra premium if you decline our offer. We’ll send you an email confirming

that we’re not covering your pre-existing medical conditions or change to your health. Your medical

assessment will list these as excluded conditions. We won’t cover any claims for anything related to

your excluded pre-existing medical conditions or change to your health.

We may be unable to cover your condition

If we’re unable to cover your pre-existing medical conditions or change to your health, we’ll send you

an email confirming this. Your medical assessment will list those pre-existing medical conditions or

change to your health as excluded conditions.

We won’t pay any claims for anything related to your excluded pre-existing medical conditions or

change to your health.

Section B

33

Your travel insurance policy document

We won’t cover changes or cancellations for expected medical procedures

— even if they’re for covered conditions

If you need to claim because of a medical procedure you were on a waiting list for or scheduled to

receive before the date your insurance was issued, we won’t cover you under:

• ‘D.2 Cancelling or changing your journey before you leave’ (page 43)

• ‘D.3 Changes to your journey once you have left’ (page 49).

This exclusion applies even if the condition you are having the medical procedure for is listed on your

medical assessment as a covered condition.

We may cover journey changes caused by the ill-health of someone

important to you

A relevant person is a person who’s important to you but isn’t named on your Certificate of Insurance

and is one of the following.

• A member of your immediate family

• Your travel companion

• A person directly related to the primary purpose of your journey

Points to note

Take the health of any relevant people into account when you plan your journey and choose

your cover. We only provide limited cover for changes or cancellations caused by sudden

unexpected changes in a relevant person’s health.

You can make a claim under ‘D.2 Cancelling or changing your journey before you leave’ on page 43,

or ‘D.3 Changes to your journey once you have left’ on page 49, if the health of a relevant person

unexpectedly gets worse, resulting in any of the following.

• Their death

• Their admission to a public or private hospital, for inpatient care as part of non-elective treatment

• A doctor recommending their admission to a public or private hospital for inpatient care as part of

non-elective treatment

• Their admission to end-stage palliative care

• A doctor recommending their admission to end-stage palliative care

• Their diagnosis of a terminal condition

• Their diagnosis of a condition that needs radiotherapy or chemotherapy

The relevant person must also not be over 85 years old before the date your insurance was issued.

34

TravelCare

This section explains how we cover pregnancy under section D.

We cover you for costs or losses related to pregnancy

This policy automatically covers pregnancy up until the 24th week of gestation (the first 23 weeks

and 6 days). Gestational age is measured in weeks and days from the first day of your last menstrual

period or from staging ultrasound. We provide this cover for a single pregnancy, a multiple pregnancy

(such as twins or triplets) and a pregnancy through fertility treatment, as long as the pregnancy had no

complications before you bought your policy.

> For details on how we cover you, see ‘D.1 Cover for medical and evacuation’ (page 36),

‘D.2 Cancelling or changing your journey before you leave’ (page 43), and ‘D.3 Changes to

your journey once you have left’ (page 49).

We will cover the following medical expenses related to pregnancy:

• childbirth up until the 24th week (the first 23 weeks and 6 days)

• neo-natal care of the new-born child up until the date and time you return to New Zealand.

We won’t cover any pregnancy after the 24th week of gestation.

Section B

35

Your travel insurance policy document

C.

How we cover

pregnancy

This section explains the details of your policy: when you are covered

and when you are not.

Cover for medical and evacuation

This section explains cover for medical treatment and evacuation because of an unexpected event

on your journey.

When you need to check with us before you start medical treatment

You need to let us know about major, but not minor, treatment.

Contact us if you need serious, or expensive medical treatment

You may not be able make a claim if you don’t get our approval first. You, or someone acting for

you, must contact Southern Cross Emergency Assistance as soon as possible if you need serious

medical attention.

You must get our approval if you:

• are admitted to hospital

• need surgery

• expect your medical and related expenses to be more than $2,000.

D.1

36

TravelCare

D.

What is and

isn’t covered

You don’t need to get our approval for minor medical treatment

If you need to see a medical professional or get minor medical treatment that’s under $2,000,

you should pay for it and submit a claim for assessment.

Don’t forget to keep all receipts, bills, medical reports and any other documents that could

support your claim.

We are not responsible for standards of medical care

Some overseas countries may have lower medical standards and services than New Zealand.

We are not responsible for the standard of any medical services you get while you are overseas.

D.1.1 Medical and evacuation

We’ll cover your actual and reasonable medical expenses if you need medical treatment because

of an unexpected event during your journey.

If we have confirmed that your medical expenses are covered, and you are deemed medically fit to

travel by Southern Cross Emergency Assistance, we can pay to:

• repatriate you to New Zealand

• evacuate you to another country that we choose for further treatment.

If you need medical evacuation, or repatriation to New Zealand, because of an unexpected event

during your journey, we’ll cover:

• your medical evacuation costs if we need to move you to another location for necessary

medical treatment

• your repatriation costs to bring you back to New Zealand.

We only cover you if one of the following applies.

• Your policy covers your medical treatment

• Your policy would cover your medical treatment, but a public health service already covers it

Your claim must meet the conditions of cover below.

We subtract an excess from claims we pay under this section.

Section D

37

Your travel insurance policy document

Conditions of cover

We only cover your claims if you follow any instructions we make to evacuate you to another

medical facility or repatriate you to New Zealand. We will only ever ask to do this if you are

medically fit to travel.

We won’t cover any further medical treatment after the date and time we would have moved

you, if you refuse to be evacuated or repatriated.

The following conditions also apply to all claims under this section.

• You must, in our opinion, be medically fit to travel with or without an upgrade to your

travel arrangements

• We’ll decide whether to medically evacuate you or repatriate you to New Zealand. This

includes when, where, and how we’ll do it

• If we have to repatriate you to New Zealand, we’ll try to use your original return ticket.

If we can’t re-book the ticket, you must try to get a refund and return it to us. If the refund

is more than the cost of returning you to New Zealand, you keep the difference between

the cost and the refund

• If you don’t hold a return ticket to New Zealand, we’ll deduct the cost of a one-way fare to

New Zealand from any payment made under this section of the policy. The cost will be a

one-way economy fare from your original carrier for the return route we use, as published

on the date we finalise your claim. You must give us the full itinerary that you got from your

transport providers so that we can confirm your flight details with your carrier

• If we cover the cost of your repatriation to New Zealand, there is no cover for any unused

pre-paid costs of your original return travel arrangements to New Zealand

What we won’t cover

We won’t cover any claims, costs or losses directly or indirectly arising from, related to

or associated with the following.

• Specialist consultations, investigations or treatment without a referral from a general

practitioner or family doctor where referral services are available

• Check-ups or treatment when there were no symptoms, illness or injury under

investigation

• Self-prescribed (over-the-counter) treatments or medication that is available without

a prescription

• Preventative treatment (including but not limited to contraception and vaccines)

• Fertility treatment

• Medical expenses incurred directly or indirectly due to a treatment error by a medical

provider

• Medical treatment in New Zealand, unless provided on a cruise ship which is travelling

internationally – see page 8

• Anything excluded under ‘E. General exclusions — things we never cover’ (page 80)

38

TravelCare

D.1.2 Your cover for emergency dental treatment

We cover you if you require emergency dental treatment because of an unexpected event during

your journey.

Your claim must meet the conditions of cover below.

We pay up to $750 for each person for each journey.

We subtract an excess from claims we pay under this section.

Conditions of cover

We will only cover emergency dental treatment if it is for at least one of the following.

• To relieve sudden and acute pain to teeth

• Where your natural teeth, replacement teeth or dentures have been damaged during your

journey as a result of an injury

You must also get a report from the treating dentist that confirms the reason for and details

of the emergency dental treatment.

What we won’t cover

We won’t cover any claims, costs or losses directly or indirectly arising from, related to

or associated with the following.

• Check-ups or preventative treatment

• Dental treatment in New Zealand, unless provided on a cruise ship which is travelling

internationally – see page 8

• Self-prescribed (over-the-counter) treatments or medication that is available without

a prescription

• Dental expenses incurred directly or indirectly due to a treatment error by a dental provider

• Anything excluded under ‘E. General exclusions — things we never cover’ (page 80)

Section D

39

Your travel insurance policy document

D.1.3 Cash allowance whilst in hospital

We’ll pay you a cash allowance if you need to stay in hospital for more than 72 consecutive hours

because of an unexpected event during your journey.

Your claim must meet the conditions of cover below.

We pay you $100 a day for each complete 24-hour period you’re in hospital. We pay up to $3,000

for each person.

We subtract an excess from claims we pay under this section.

Conditions of cover

We only cover you if one of the following applies.

• Your policy covers your medical treatment

• Your policy would cover your medical treatment, but a public health service already covers it

What we won’t cover

We won’t cover claims for anything excluded under ‘E. General exclusions — things we never

cover’ (page 80).

D.1.4 Extra travel and accommodation costs if you’re unable to travel

We’ll cover extra travel and accommodation costs if you fall ill or get injured because of an

unexpected event during your journey, and we don’t consider you medically fit to travel.

Your claim must meet the conditions of cover below.

We’ll cover you and any other person on your Certificate of Insurance for your reasonable actual

costs of:

• extra accommodation and meals that you were not expecting to pay for

• necessary travel within the area you’re staying in, for example to hospital or medical appointments.

We subtract an excess from claims we pay under this section.

40

TravelCare

Conditions of cover

We’ll only cover you if we’ve confirmed that your policy covers your unexpected event.

• We cover you under this benefit during the period you are not medically fit to travel and

whilst you incur additional accommodation or travel expenses.

• If during this period you have losses relating to pre-paid unused accommodation or travel,

we will consider these losses under section ‘D.3 Changes to your journey once you have

left’ (page 49). We will take into account the amount we have paid under this benefit,

and will only cover any losses over and above this amount.

• Once you are declared medically fit to travel, we will cover the cost of additional travel to

return you to New Zealand under this benefit.

• If we agree to you continuing on your journey, we consider the losses related to amending

your journey under Section ‘D.3 Changes to your journey once you have left’ (page 49).

What we won’t cover

We won’t cover claims for anything excluded under ‘E. General exclusions — things we never

cover’ (page 80).

D.1.5 Accompanying person

If you’re travelling alone and are admitted to hospital for more than 10 days because of an unexpected

event during your journey, we’ll arrange for someone to travel to where you’re getting medical

treatment. You can choose who comes to you, as long as they’re coming from New Zealand.

Your claim must meet the conditions of cover below.

We cover your accompanying person’s reasonable costs of travel (a return economy flight and

transfers), accommodation, and meals.

We pay up to $5,000 for each person.

We subtract an excess from claims we pay under this section.

Conditions of cover

We only cover you if one of the following applies.

• Your policy covers your medical treatment

• Your policy would cover your medical treatment, but a public health service already covers it

What we won’t cover