ANNUAL REPORT

2022

Mrs. PHORK Hoeurng

Owner of Golden Yem

Enterprise

Annual Interest Rate from

5.50%

Entrepreneurs Scheme

(CWES)

Cambodia Women

Annual Interest Rate from

5.88%

Automation Scheme

(CDAS)

Cambodia Digital &

Mr. Song Khenglean

Owner of CSL Enterprise

Annual Interest Rate from

5.88%

SME Scheme (CSS)

Cambodia

Annual Interest Rate from

7.50%

Enterprise Scheme

(Unsecured Loan)

(CMES)

Cambodia Micro

Mrs. PHORK Hoeurng

Owner of Golden Yem

Enterprise

Annual Interest Rate from

5.50%

Entrepreneurs Scheme

(CWES)

Cambodia Women

Annual Interest Rate from

5.88%

Automation Scheme

(CDAS)

Cambodia Digital &

Mr. Song Khenglean

Owner of CSL Enterprise

Annual Interest Rate from

5.88%

SME Scheme (CSS)

Cambodia

Annual Interest Rate from

7.50%

Enterprise Scheme

(Unsecured Loan)

(CMES)

Cambodia Micro

The Best Partner Bank for Small and

Medium Enterprises in Cambodia

About SME Bank

Message from Chairman................................6

Message from CEO ..........................................8

About SME Bank ............................................10

Achievement Report in 2022 .................... 12

Branch Networks ............................................ 13

Corporate Milestones ................................... 14

Cash Management Partner ......................... 16

Partnerships ......................................................17

CONTENTS

Events

Annual Meeting 2022 .................................. 24

Employee Recognition

Program 2022 ................................................ 25

Key Highlights ................................................ 26

Memorandum of Understanding

(MoU) with Participating Financial

Institutions ....................................................... 30

Financial Statements

Financial Statements ................................... 47

Corporate Governance

Organizational Structure ............................. 31

The Board of Directors ............................... 34

Senior Management ..................................... 37

Corporate Governance ............................... 39

Board of Directors Meeting ......................40

Board Risk and Compliance

Committee .................................................. 41

Board Audit Committee ............................44

Board of Remuneration and

Nomination Committee (BRNC) .............46

Business Highlight

Co-Financing Scheme ................................. 19

The Direct Lending Scheme ...................... 21

Voice from Customers .................................22

MESSAGE FROM CHAIRMAN

SME Bank is a policy bank

established under the

wise leadership of Samdech

Akka Moha Sena Padei

Techo Hun Sen, Prime

Minister of the Kingdom of

Cambodia, to support

small and medium enterprises

aected by COVID-19 and

newly-established enterprises

in need of financial and

technical support.

6

Annual Report 2022 About SME Bank

SME Bank of Cambodia

On behalf of SME Bank of Cambodia (SME Bank) and

the Board of Directors, I am honored and pleased to

provide you with the bank’s annual report for fiscal

year 2022.

The growth of the global economy and trade remains

at a slow pace despite the decrease in the COVID-19

spread. However, the war between Russia and Ukraine

has prolonged, resulting in adverse impacts on the

economy of the United States, European Union, and

Southeast Asian countries.

The Cambodian economy began to recover in 2021

due to the support of various sectors; however,

Cambodia is still facing a lot of obstacles in restoring

its economy. Many SMEs have not been properly

operated since some owners have had insucient

budget, resources, supporting products, capital and

have faced an inflation. In this situation, the Royal

Government of Cambodia has set out a number of

policies and strategies to restore all sectors, such as

the Cambodia Digital Economy and Society Policy

Framework 2021-2035, the strategic framework and

programs for economic recovery in the context of

living with COVID-19 in a new normal for 2021-2023.

SME Bank is a policy bank established under the wise

leadership of Samdech Akka Moha Sena Padei Techo

Hun Sen, Prime Minister of the Kingdom of Cambodia,

to support small and medium enterprises aected by

COVID-19 and newly established enterprises, which

need financial and technical support. The Bank has

launched a number of financing schemes to support

small and medium enterprises to meet their needs by

oering favourable terms and low interest rates. As

of the end of 2022, SME Bank has financed 231 small

and medium enterprises (SMEs) through the direct

financing, including 62 female entrepreneurs and 169

male entrepreneurs with a total loan amount of

approximately USD 53.4 million and the loaning

through Co-Financing with participating financial

institutions, supporting a total of 3,037 enterprises,

equivalent to a total amount of approximately USD

380 million.

In line with the policies and programs for economic

recovery and to promote Cambodia’s economic

growth in living with COVID-19 in the new normal for

2021-2023 of the Royal Government of Cambodia,

SME Bank continues to implement and strive to

promote the growth of all small and medium

enterprises to contribute to the sustainable economic

growth.

As the Chairman of the Board, I am very pleased to

sincerely thank the relevant authorities for their tireless

eorts to support the Bank’s growth and development.

I also would like to sincerely thank our valued

customers for their trust in SME Bank, even during

the global epidemic. We are committed to being a

trusted partner and continue to finance all enterprises

that are still in need of finance to grow their businesses.

H.E. Dr. Phan Phalla

Secretary of State, Ministry of Economy and

Finance, and Chairman of the Board

7

Annual Report 2022About SME Bank

SME Bank of Cambodia

MESSAGE FROM CEO

Dear our valued customers and the public

Although the world has suered from the epidemics

and crisis that have caused adverse impacts on the

global and Cambodian economy, Small and Medium

Enterprise Bank of Cambodia Plc. (“SME Bank”)

continues its mission to support the growth and

development of small and medium enterprises in

Cambodia. SME Bank remains committed to providing

eective and ecient financing to business owners

who support the priority sectors to contribute to the

restoration and development of the Cambodian

economy in line with the strategic framework and the

programs for economic recovery and to promote

Cambodia’s economic growth in living with COVID-19

in the new normal for 2021-2023.

Since 2022, SME Bank has continued focusing on

widely expanding its distribution networks, such as:

(1). The Bank has relocated its head oce to the

SME Bank remains committed to

providing eective and ecient

financing to business owners

who support the priority sectors

to contribute to the restoration

and development of the

Cambodian economy in line with

the strategic framework and the

programs for economic recovery

and to promote Cambodia’s

economic growth in living with

COVID-19 in the new normal for

2021-2023.

8

Annual Report 2022 About SME Bank

SME Bank of Cambodia

“Business Development Centre” building of the

Ministry of Economy and Finance, which is more

spacious and has multiple institutions to support

entrepreneurs technically and financially, and develop

human resources, (2). SME Bank has ocially operated

two new branches, including Phsar Thmei Branch and

Battambang Provincial Branch, to ensure convenience

for small and medium enterprise owners who need

financial support, (3). SME Bank has also further

developed a number of business partners, including

business incubation associations, commercial banks,

payment services providers, financial technology

companies, as well as local and international public

institutions to expand the scope of services and move

it closer to the target customers. Furthermore, SME

Bank has set out a specific plan for the modernization

of information technology systems and the

development of digital platform infrastructures to

improve the customer service experiences more

eectively and eciently in line with the Cambodia

Digital Economy and Society Policy Framework 2021-

2035.

To accelerate the financing, SME Bank has revised

the definition of small and medium enterprises to suit

current socio-economic development and has

increased the maximum loan amount from USD

500,000 to USD 1,000,000 per customer. Furthermore,

SME Bank has launched unsecured financing and

overdraft schemes that oer additional options for

target enterprises in accordance with their objectives

and types of businesses.

As of 2022, SME Bank has achieved total assets of

USD 281 million, representing an increase of USD 131

million from 2021, in which the total loan balance is

USD 214 million. Meanwhile, in September 2022, SME

Bank successfully completed the second phase of the

SME Co-Financing Scheme, supporting a total of 1,992

enterprises, equivalent to a total of USD 240 million

(USD 120 million from the Royal Government of

Cambodia through the Ministry of Economy and

Finance and SME Bank, and the other USD 120 million

from participating financial institutions). Furthermore,

SME Bank has developed and launched a Co-Financing

Scheme to support and boost the recovery of the

tourism sector with a total amount of USD 150 million

(USD 75 million from the Royal Government of

Cambodia through the Ministry of Economy and

Finance and SME Bank, and the other USD 75 million

from participating financial institutions). As of

December 2022, there were a total of 291 enterprises,

using a total financing of USD 41.52 million, equivalent

to 27.68% of the total budget.

The major strategic plans for the following year

include: (1). Improve and develop products and

services to meet the needs of target customers, (2).

Continue to develop distribution networks such as

branches, business partners, the development of

digital platform technology infrastructures, which is

an extensive connection point and gets closer to the

target customers, (3). Develop human resources with

sucient knowledge and skills that ensure the work

eciency and transparency, and (4). Establish a better

risk management system and culture.

All these achievements are made with the financial

and technical support from the Ministry of Economy

and Finance, as well as the cooperation of the

competent authorities, in particular the National Bank

of Cambodia, which is the supervisory institution.

Furthermore, I would like to express my sincere

gratitude to our valued customers, Board of Directors,

management and employees, as well as our business

partners for always supporting SME Bank to achieve

the results in accordance with the plans, particularly

in 2022.

DR. LIM AUN

Chief Executive Ocer

and Board Member

9

Annual Report 2022About SME Bank

SME Bank of Cambodia

SME Bank has been established in the Cambodian

market for almost three years and was recognized

as the policy bank which provides aordable financial

services to SMEs in Cambodia by focusing on the

priority sectors including food processing,

manufacturing of consumer goods and spare parts,

research and development in information and

technology, manufacturing of medical equipment

and medicines, and other business supporting the

priority sectors. Currently, SME Bank of Cambodia is

focusing on implementing Co—Financing Schemes

with participating financial institutions (PFIs) and

direct lending schemes.

Small and Medium Enterprises (SMEs) are the vital

driver for economic growth in developing countries

like Cambodia. However, some SMEs are facing some

challenges accessing aordable financial services

due to collateral requirements and higher interest

rates. To better support this segment, the Royal

Government of Cambodia has established the SME

Bank of Cambodia (SME Bank).

SME Bank was ocially licensed as a commercial

bank by the National Bank of Cambodia (NBC) on

the 27th February 2020. With the technical and

financial guidance of the Ministry of Economy and

Finance (MEF), the bank’s strategic intent and

direction are coherent with the policies set by The

Royal Government of Cambodia, assuring reliable

and sustainable banking to all small and medium

enterprises.

ABOUT SME BANK

10

Annual Report 2022 About SME Bank

SME Bank of Cambodia

CORE VALUES

We will ingrain integrity

in our DNA to ensure a high

level of trust and reputation

in our business.

INTEGRITY

We consider all employees

as our core asset and will

respect, value and actively

engage them in all our

business dealings.

PEOPLE

We will be professional by

being accountable to all our

stakeholders and responsible in

discharging our duties.

ACCOUNTABILITY

As customers are the main

purpose for our existence we will

provide excellent and consistent

customer experience.

CUSTOMER

We strive for operational

excellence to ensure profitability,

growth and sustainability for all

our stakeholders.

EFFICIENCY

MISSION

VISION

To be the Best and Preferred

SME Bank in Cambodia, providing

aordable financing, easy

accessibility, technical support and

excellent customer experience.

To provide ecient and

sustainable financing and

commercial banking services

to support SMEs to promote

economic diversification

and exports in line with

government policy.

Annual Report 2022About SME

11Small and Medium Enterprise Bank of Cambodia Plc.

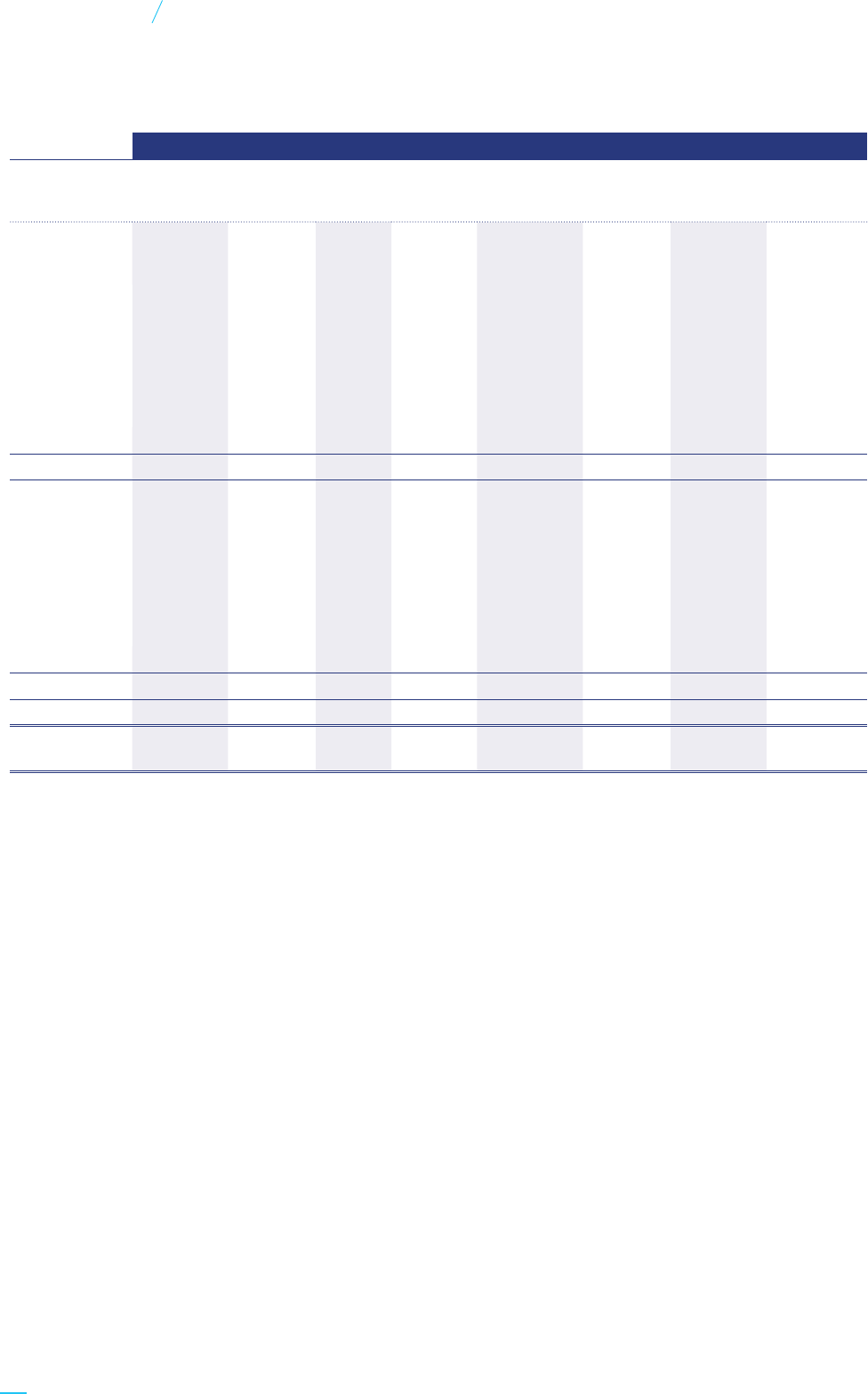

No of

Customers

Loan

Outstanding

Total Assets

No of Sta

No of Women

SMEs

Loan Outstanding in

The Priority Sectors

Branch Networks

Business Partners

+3,200

+138

3

10

+24%

+51%

Bank Equity

(in USD Millions)

Total Assets

(in USD Millions)

2020 2021 2022 2020 2021 2022

100

148

199

100

150

281

USD

+214

USD

+281

ACHIEVEMENT REPORT IN 2022

12

Annual Report 2022 About SME Bank

SME Bank of Cambodia

No 30, St. Pasteur corner

Prey Nokor Street, Sangkat Phsar

Thmei Ti Muoy, Khan Daun Penh,

Phnom Penh, Cambodia.

Phsar Thmei Branch

MEF Business

Development Center,

Ground and 20

th

Floor,

OCIC Street, Khan Chraoy

Chongvar, Phnom Penh,

Cambodia.

Head Oce

No. 161 & 162, National Road No. 5,

Group 6, Phum Rumchek 5, Sangkat

Rottanak, Krong Battambang,

Battambang Province, Cambodia.

Battambang Provincial Branch

BRANCH NETWORKS

13

Annual Report 2022About SME Bank

SME Bank of Cambodia

Obtained the Commercial Bank License

on February 27

th

, 2020

Launched the first phase of the

SME Co-Financing Scheme, with a

total amount of USD 100 million

in collaboration with 33 participating

financial institutions and completed

it in October 2020;

Launched the direct financing scheme,

including:

• Cambodia SME Scheme (CSS)

• Cambodia Digital and Automation

Scheme (CDAS)

• Cambodia Women Entrepreneurs

Scheme (CWES)

• Cambodia Recovery Support

Scheme (CRSS)

Achieved total assets of

over USD 100 million.

2020 2021

2022

“SME Bank of the

Year – Cambodia”

awarded from the Asian

Banking & Finance

Memorandum of Understanding

in promoting SMEs with the

FASMEC, KE, and BanhJi FinTech

Co., Ltd. etc.

Launched the second phase

of the SME Co-Financing

Scheme, with a total amount

of USD 240 in collaboration

with 28 participating

financial institutions and

financed 981 enterprises to

achieve total assets of

over USD 150 million.

Launched a Co-Financing Scheme to support and boost

the recovery of the tourism sector with

a total

amount of USD 150 million

in collaboration

with 24 participating financial institutions

Became a member of the Fast Payment service of the

National Bank of Cambodia to enable customers to transfer

money via the bank quickly;

Launched the Cambodia Micro Entreprise Scheme (CMES),

an Unsecured Loan;

Launched two more new branches, including Phsar Thmei

and Battambang Provincial branches;

Developed business partnerships with five additional

SME associations to promote direct lending to target

customers, including CEO Master Club of Life Education

Co., Ltd., Young Entrepreneurs Association of Cambodia

(YEAC), AgriBee (Cambodia) Plc., Cambodian Water

Supply Association, and Cambodia Food Manufacture

Association;

Achieved total asset of

over USD 281 million.

CORPORATE MILESTONES

14

Annual Report 2022 About SME Bank

SME Bank of Cambodia

Obtained the Commercial Bank License

on February 27

th

, 2020

Launched the first phase of the

SME Co-Financing Scheme, with a

total amount of USD 100 million

in collaboration with 33 participating

financial institutions and completed

it in October 2020;

Launched the direct financing scheme,

including:

• Cambodia SME Scheme (CSS)

• Cambodia Digital and Automation

Scheme (CDAS)

• Cambodia Women Entrepreneurs

Scheme (CWES)

• Cambodia Recovery Support

Scheme (CRSS)

Achieved total assets of

over USD 100 million.

2020 2021

2022

“SME Bank of the

Year – Cambodia”

awarded from the Asian

Banking & Finance

Memorandum of Understanding

in promoting SMEs with the

FASMEC, KE, and BanhJi FinTech

Co., Ltd. etc.

Launched the second phase

of the SME Co-Financing

Scheme, with a total amount

of USD 240 in collaboration

with 28 participating

financial institutions and

financed 981 enterprises to

achieve total assets of

over USD 150 million.

Launched a Co-Financing Scheme to support and boost

the recovery of the tourism sector with

a total

amount of USD 150 million

in collaboration

with 24 participating financial institutions

Became a member of the Fast Payment service of the

National Bank of Cambodia to enable customers to transfer

money via the bank quickly;

Launched the Cambodia Micro Entreprise Scheme (CMES),

an Unsecured Loan;

Launched two more new branches, including Phsar Thmei

and Battambang Provincial branches;

Developed business partnerships with five additional

SME associations to promote direct lending to target

customers, including CEO Master Club of Life Education

Co., Ltd., Young Entrepreneurs Association of Cambodia

(YEAC), AgriBee (Cambodia) Plc., Cambodian Water

Supply Association, and Cambodia Food Manufacture

Association;

Achieved total asset of

over USD 281 million.

15

Annual Report 2022About SME Bank

SME Bank of Cambodia

SME Bank aims to promote financing to small and medium enterprises in various provinces and cities of

Cambodia. SME Bank’s branch network is currently limited and IT infrastructure is also limited and under

development its capacity. To improve the customer experience, SME Bank has engaged some financial

institutions to facilitate the bill payment through their available networks.

SME Bank has signed a Memorandum Of Understanding with ABA Bank and TrueMoney Cambodia to ocially

launch bill payment through its ABA Mobile and more than 11K TrueMoney agents across the country and the

TrueMoney Wallet. This collaboration will provide a secured and convenient financial services experience.

CASH MANAGEMENT PARTNERS

16

Annual Report 2022 About SME Bank

SME Bank of Cambodia

PARTNERSHIPS

17

Annual Report 2022About SME Bank

SME Bank of Cambodia

In 2022, despite the slowdown in global economic growth,

the SME Bank of Cambodia could increase loan net growth

by 93%, from USD 111 million in 2021, to USD 214 million in

2022. The loan net growth was mainly contributed by two

schemes, consisting of Co-Financing Scheme and Direct

Lending Scheme. The Co-Financing scheme increased by

58% USD 96 million in 2021, compared to USD 152 million

in 2022. Moreover, Direct Lending Scheme has a significant

growth from USD 4 million in 2021 to 53 million in 2022.

Additionally, as a bank’s aspiration to financing SME in food

processing and manufacturing, as well as other priority

sectors, SME Bank has proactively provided direct lending

loans to SME in processing and manufacturing sector for

46% of total loan outstanding in 2022 via Cambodia SME

Scheme (CSS), Cambodia Women Entrepreneur Scheme

(CWES), Cambodia Digital & Automation Scheme (CDAS),

Cambodia Micro Enterprise Scheme (CMES).

Business Highlight

18

Annual Report 2022

SME Bank of Cambodia

Business Highlight

The Tourism Recovery Co-Financing Scheme (TRCS)

is a part of the support for the implementation of the

“Strategic Framework and Program for Economic

Recovery in the Context of Living with Covid-19 in a

New Normal for 2021-2023”.

To promote tourism recovery, the Royal Government

has decided to implement this scheme to address

the lack of financing support for tourism-related

businesses.

TRCS will support (a) re-operating the business, (b)

improving and modernizing, and (c) strengthening

and diversifying tourism services to prepare for

national and international tourists in the post-covid-19

crisis.

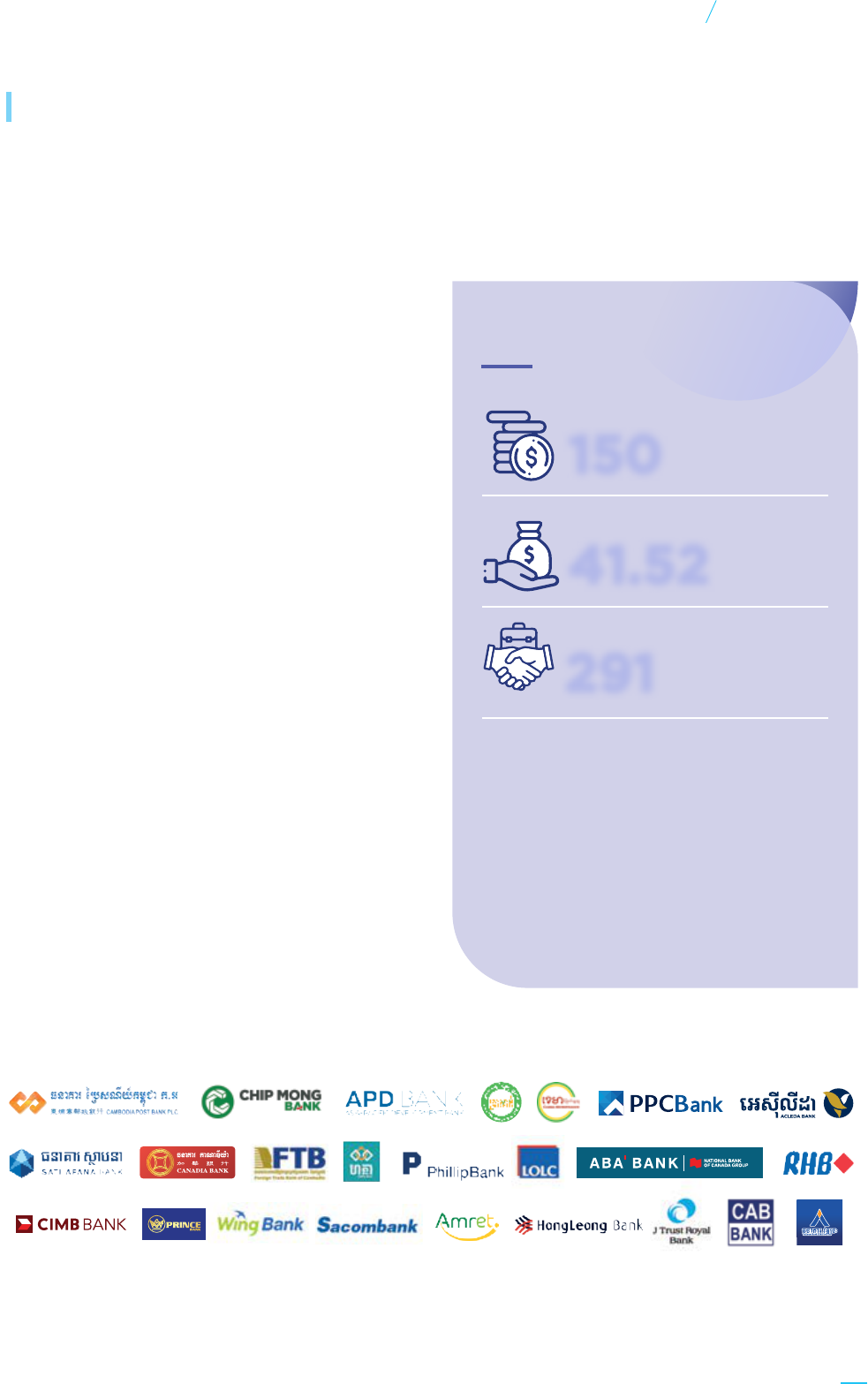

TRCS was initiated in July 2022, with a total

commitment budget of USD 150M, which co-financed

between the government of Cambodia and PFIs.

As of December 2022, 24 PFIs joint the TRCS scheme.

The scheme has been financed to about 291 enterprises

(50 hotels, 97 guesthouses, 120 restaurants, and 51

Supplies of Products and Services supporting the

tourism sector) with the disbursed amount of

approximately USD 41.52M.

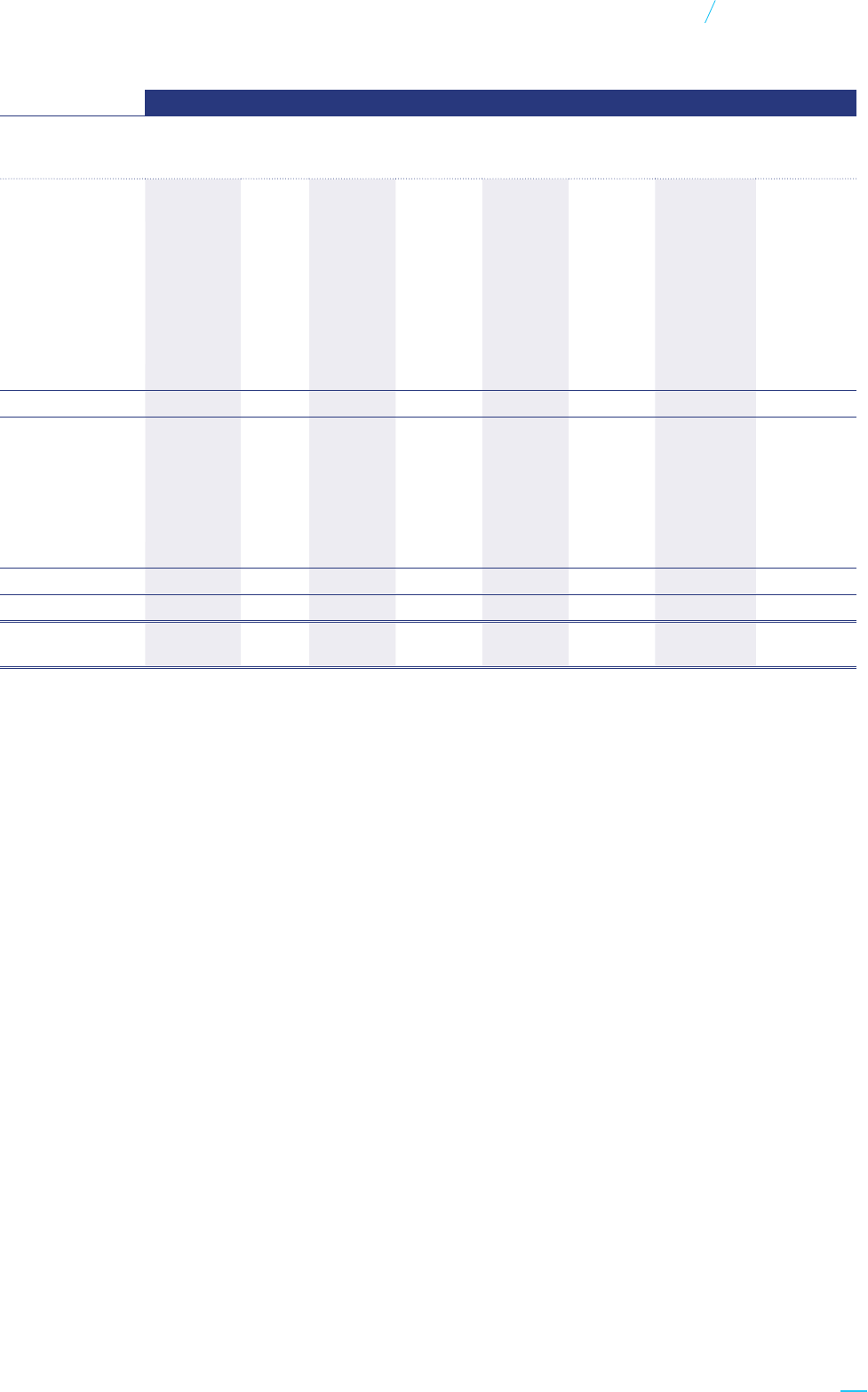

Tourism Recovery Co-financing Scheme (TRCS)

Commitment Fund

Disbursed Amount

No of

Customer

Hotel Guest

House

Restuarant

in USD

Millions

in USD

Millions

150

41.52

26% 28%

Supply of Products and

Service Supporting

Tourism Sector

No of Women

SMEs

14% 43%

32%

291

Performance Update

CO-FINANCING SCHEME

19

Annual Report 2022

SME Bank of Cambodia

Business Highlight

The SME Co-Financing Scheme II (the “SCFS II”) has

assisted SMEs that have been negatively impacted

by Covid-19 to restart their businesses, aligning with

RGC’s During and Post Covid-10 Recovery Plan and

so as to contribute to the economic recovery.

SCFS II was initiated in August 2021, with a total

commitment budget of USD 240 million, which

Co-Financing between SME Bank and 32 PFIs. The

scheme was completed on the 22nd August 2022 by

providing financing to 1992 SMEs including the priority

sector at 42%, the normal sector at 58%, and female

entrepreneurs at 30%.

SME Co-financing Scheme II (SCFS II)

Commitment Fund

Disbursed Amount

No of

Customer

Priorities

Sector

Normal

Sector

No of Women

SMEs

in USD

Millions

in USD

Millions

240

239.97

42% 58% 30%

1,992

Achievement

20

Annual Report 2022

SME Bank of Cambodia

Business Highlight

SME Bank has operated according to its mission to

support the government policies, especially providing

access to finance to SMEs in the priority sector. The

bank has initiated four types of direct lending schemes

namely the Cambodia SME Scheme (CSS), the

Cambodia Women Entrepreneur Scheme (CWES),

the Cambodia Digital & Automation Scheme (CDAS),

the Cambodia Micro Enterprise Scheme (CMES) in

2021, and proactively provided financing support to

231 entrepreneurs with loan outstanding of USD 53M

as of 31st December 2022. 69% of the loan outstanding

was provided to the priority sector, and 46% of the

loan outstanding was provided to processing and

manufacturing of agricultural products.

THE DIRECT LENDING SCHEME

21

Annual Report 2022

SME Bank of Cambodia

Business Highlight

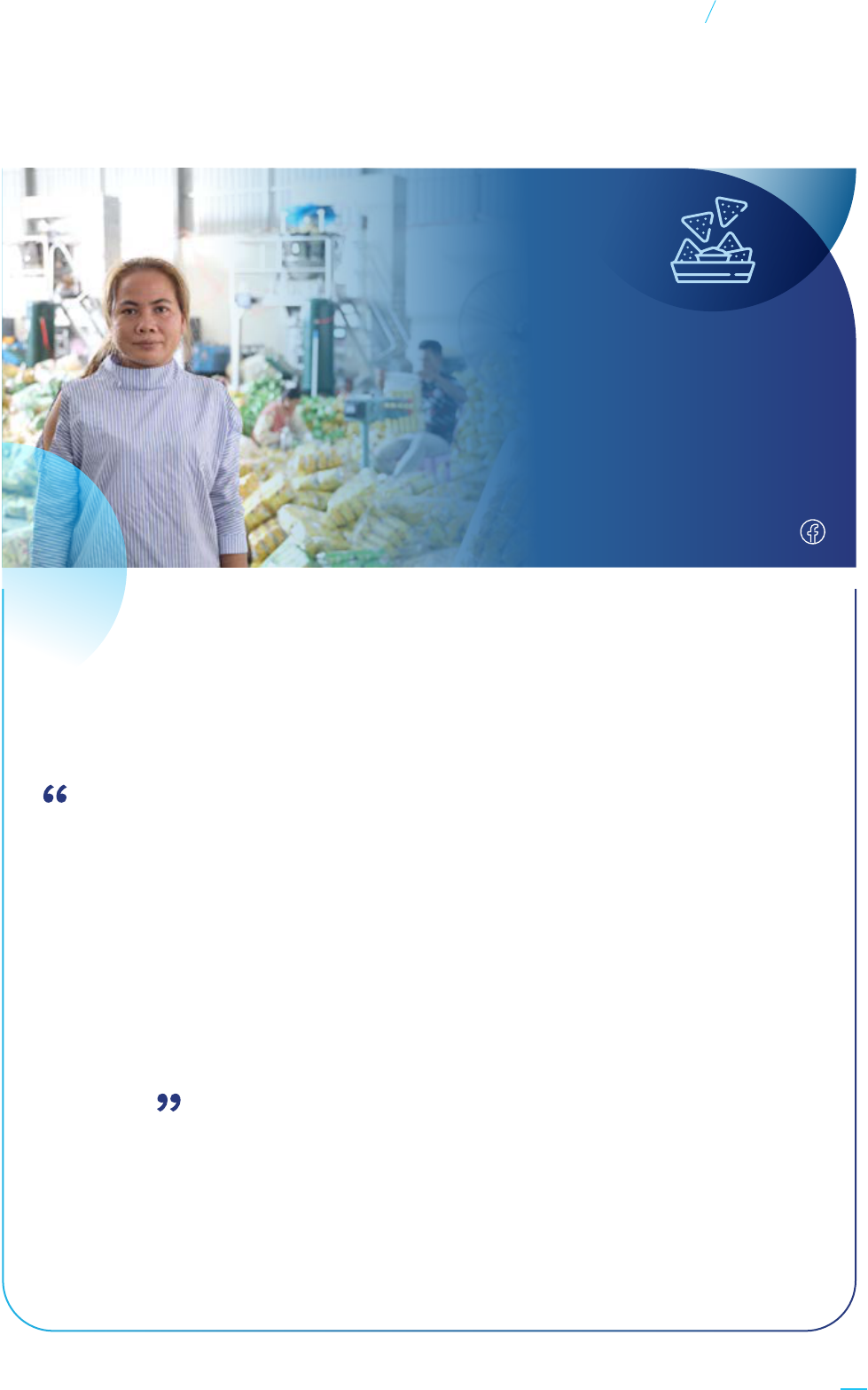

Mr. SOK Khenglean

Owner of CSL Enterprise

As a manufacturer and supplier of

packaged food made from fruits,

grains and spices in Sangkat Teuk Thla,

Khan Sen Sok, Phnom Penh

https://cslsnack.com/en/products

My enterprise started operating in 2017 with only a few products,

observing the market demand as well as the support of new food

packages and groceries by more and more customers; then in

2021, I decided to create more new products including packaged

foods made from cashew nuts, mangoes, bananas, taro and logan,

plus grocery such as mung beans, soybeans, red beans, dried

chilli, and ground peppers, etc.

To achieve this goal, it requires me to have some capital to invest,

such as buying better quality machines and working capital to

buy raw materials. As a solution, I applied for a loan from SME

Bank of Cambodia to purchase more machines and expand the

warehouse to stock raw materials.

In fact, after receiving capital from the bank, my business has

run better because the products of my enterprise can meet the

needs of customers in a timely manner with good quality. The

growth of my orders has been increasing by major supermarkets

such as Aeon Mall, Lucky Mall, Makro Market, Thai Huot Market,

Bayon Market and many depots across the country.

I am very happy and satisfied with the bank that has financed

me with the most reasonable interest rate that I have been able

to repay during the process of expanding my business.

Without the

financial support of

the SME Bank of

Cambodia,

the processing and

development of

local products or

raw materials

into value-added or

finished products

would not have been

done smoothly.

VOICE FROM CUSTOMERS

22

Annual Report 2022

SME Bank of Cambodia

Business Highlight

Initially, my business ran with only one product line which

was natural tea bag products. As I have been planning to

expand my business, I decided to create four more types of

snacks packaging by adding many different flavours to fulfil

the market demand.

Due to the lack of capital to purchase machines and equipment

for making snacks as well as natural tea, I decided to apply

for a loan from SME Bank to purchase more machines, relocate

the warehouse to a bigger place and stock more ingredients

for making snacks and natural tea.

My craft is running smoothly and growing remarkably due to

the orders from many wholesale customers and supermarkets

such as: Aeon Mall, Lucky Supermarket, Makro Mall, Thai Huot

Supermarket, Bayon Supermarket, and nationwide distribution

depots. My business started with only ten employees, but

now I can employ more than 30 employees, which is 300%

increase compared to the time before receiving a loan from

SME Bank.

I have applied for a SME Bank loan through a friend with a

similar business who has also applied for a SME Bank loan,

and I am so grateful that SME Bank has a financing scheme

designed specifically for female entrepreneurs with a

favourable interest rate to support my business. I highly

recommend to female entrepreneurs who need more fund

to expand their businesses, please visit and apply a loan from

SME Bank.

SME Bank does not

only provide financial

services to food

processing

enterprises, but also

provides and

encourages

businesswomen

honestly and

sincerely.

Mrs. PHORK Hoeung

Owner of Golden Yem

Tea and snack jacks producer

in Sangkat Choam Chao, Khan Po

Senchey district, Phnom Penh

Golden Yem

23

Annual Report 2022

SME Bank of Cambodia

Business Highlight

Annual Meeting 2022

SME Bank has organized the annual meeting with the participation of

sta at all levels, the management of the Bank, as well as his excellency

chairman and members of the Board of Directors. This annual meeting

was held at Sokha Hotel, Preah Sihanouk Province, on Friday afternoon,

February 4, 2023. In this meeting, SME bank provided an overview of

the Bank’s performance in 2022, emphasizing the fruitful results that

reflect the Bank’s growth as well as the new strategic plan that will be

implemented in the coming year of 2023 in line with the vision of the

Royal Government of the Kingdom of Cambodia.

EVENTS

24

Annual Report 2022

SME Bank of Cambodia

Events

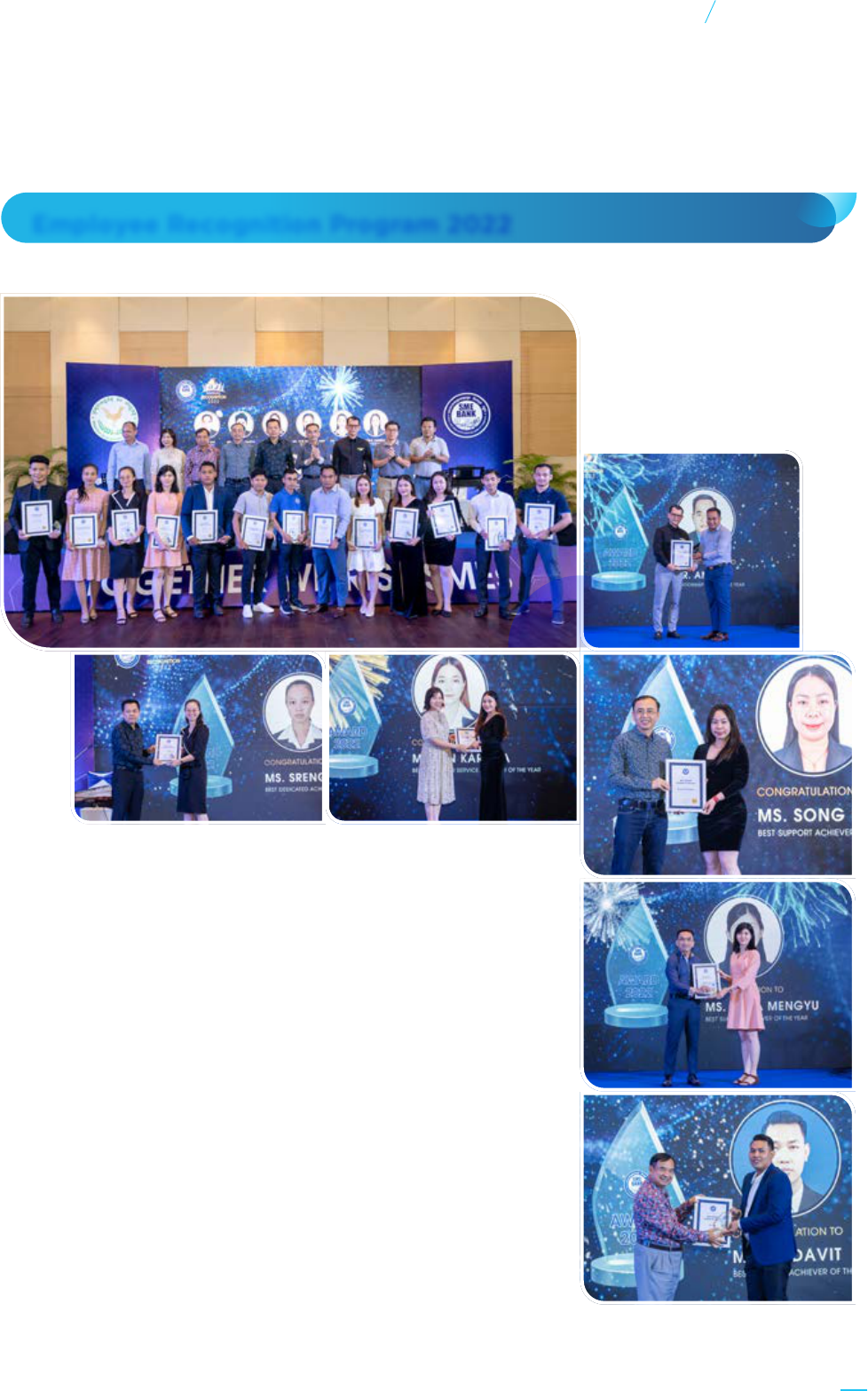

Employee Recognition Program 2022

SME Bank also organized the employee recognition ceremony in 2022

for top-performing employees who have actively contributed to the

Bank’s growth. This employee recognition ceremony was held in the

evening of February 4, 2023, at Sokha Hotel in Preah Sihanouk Province.

The Department of Human Resources organized this program based

on the procedure of selecting candidates from all branches and oces

and then discussing and seeking approval from the senior management

of the Bank. This program is designed to recognize outstanding

employees, encourage those who strive to achieve high results, foster

a high-performing culture, and reward top-performing employees with

value. The Bank identified 12 (twelve) award winners of the year who

received congratulations, trophies, and the cash award of 1,000,000

(one million) KHR. The Board of Directors and the senior management

personally presented the trophies and prizes to all the award winners.

25

Annual Report 2022

SME Bank of Cambodia

Events

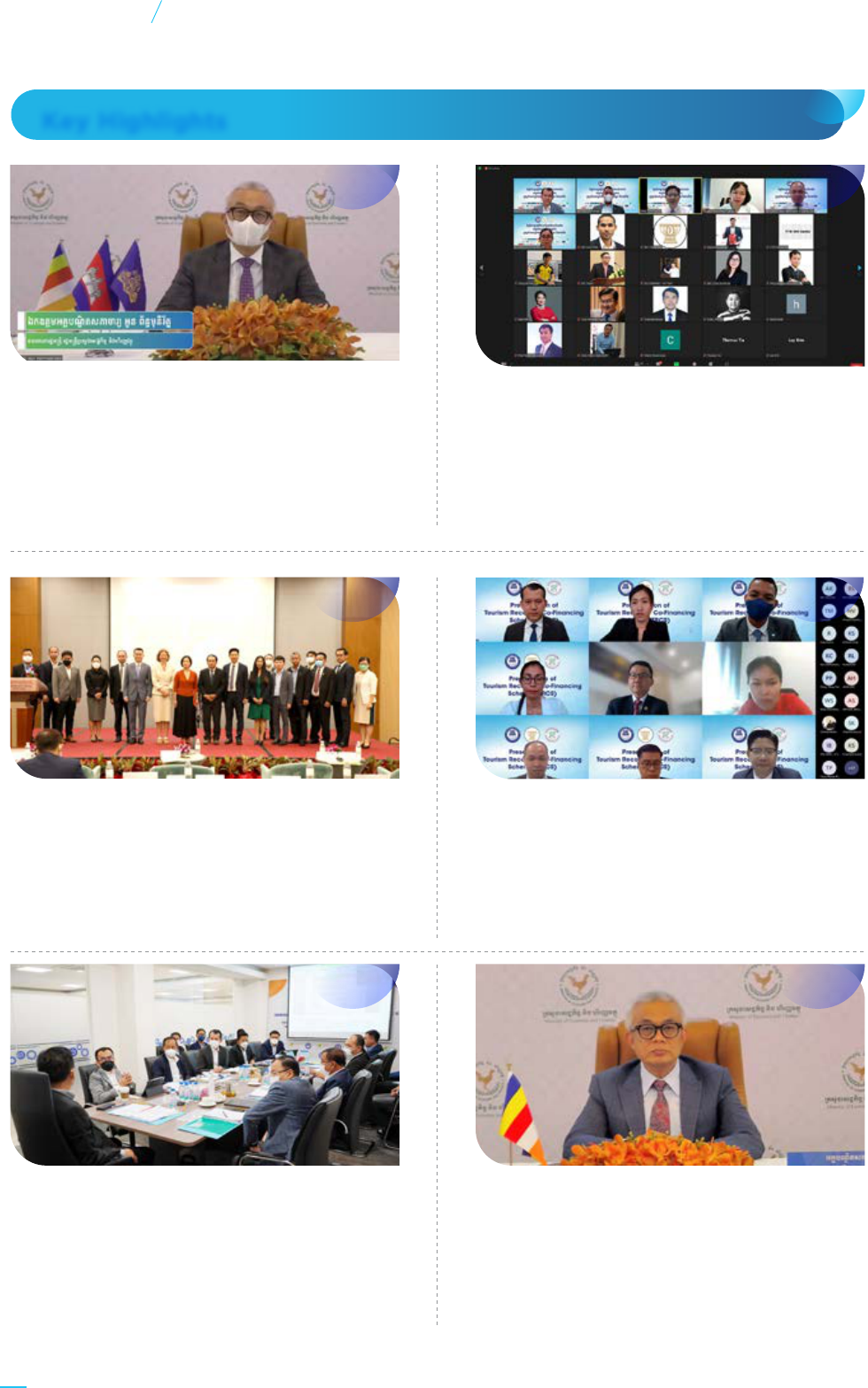

The virtual discussion forum on

“the Presentation of Tourism Recovery

Co-Financing Scheme”

April 20, 2022

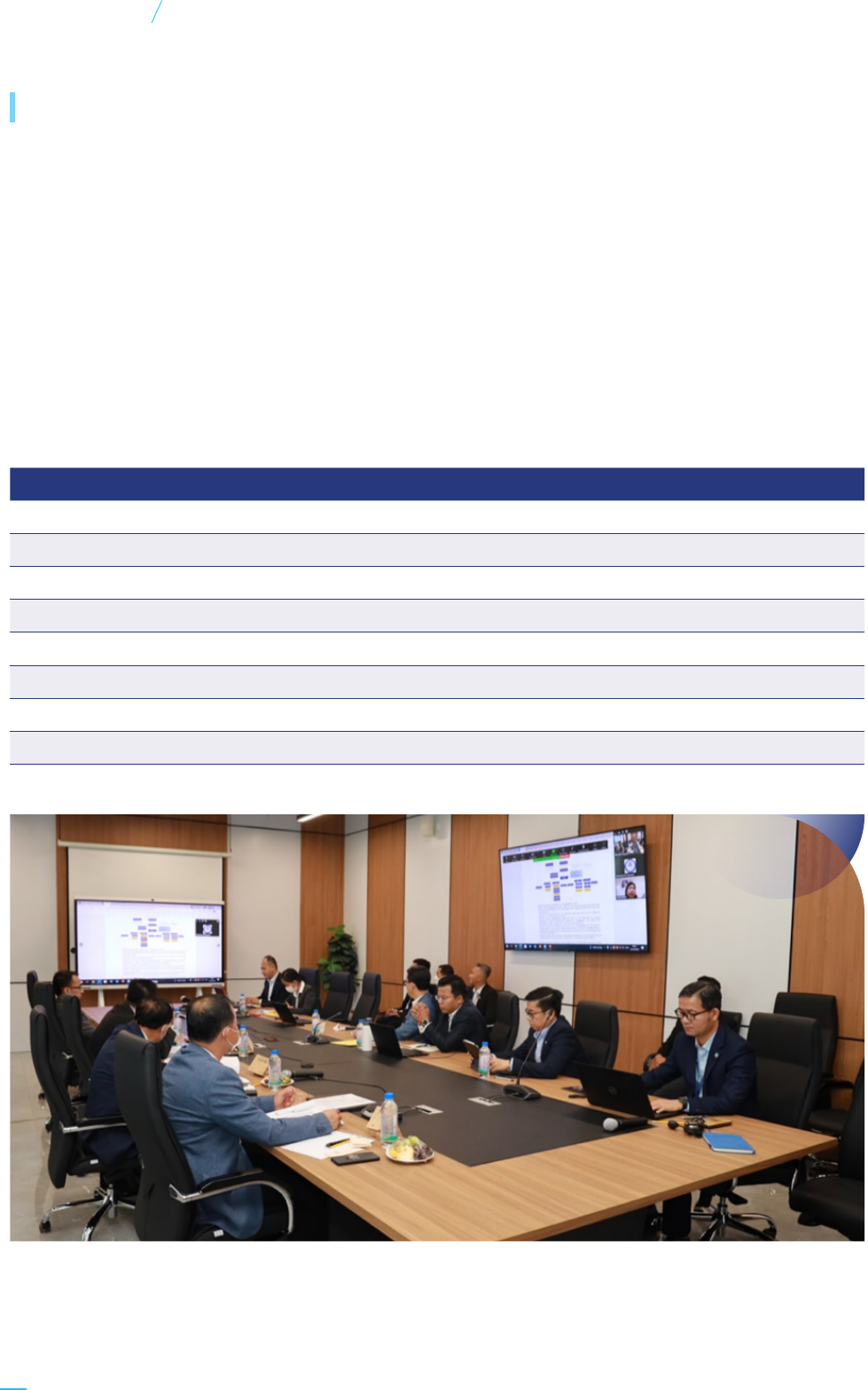

10th Board of Directors Meeting

April 21, 2022 at the SME Bank’s Head Oce

Key Highlights

The Dissemination Ceremony on

“the Additional Fund Allocation for Small and

Medium Enterprise Bank of Cambodia and

Agricultural and Rural Development Bank”

February 14, 2022

Participation in a panel discussion on

“Understanding How to Access Financing”

at the program launch on “Access to Finance”

April 01, 2022 at Olympia City Hotel

The virtual discussion forum on “the Additional

Budget for SME Co-Financing Scheme Phase II”

February 22, 2022

Launching Ceremony of

“Tourism Recovery Co-Financing Scheme”

May 17, 2022

26

Annual Report 2022

SME Bank of Cambodia

Events

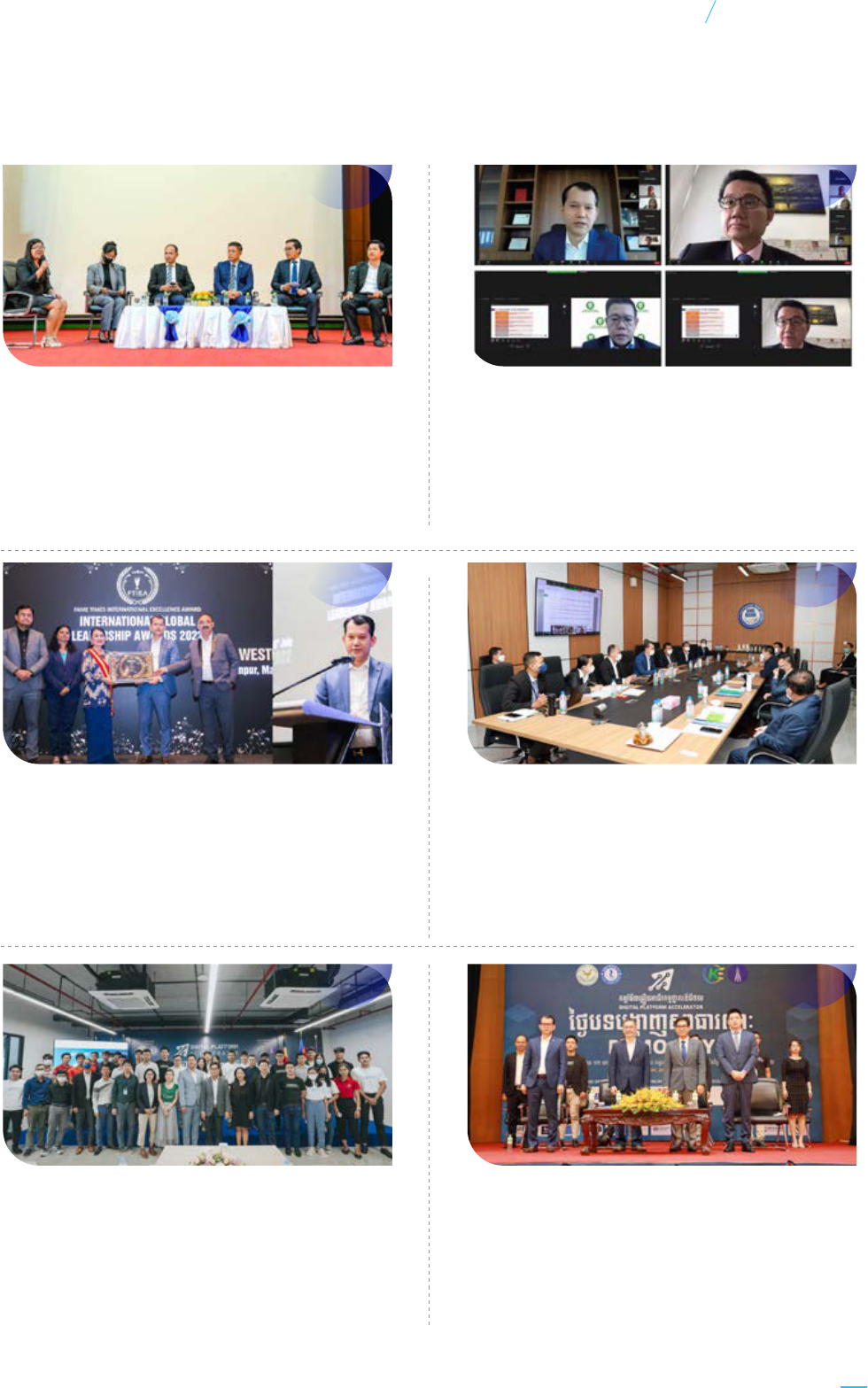

Dr. Lim Aun Receives an International

Global Leadership Awards 2022 in

Management

July 30, 2022 at Westin Hotel in Kuala Lumpur,

Malaysia

11th Board of Directors Meeting

August 4, 2022 at the SME Bank’s Head Oce

Participation in the demo day of the

“Digital Platform Accelerator”

August 24, 2022 at Cambodia-Japan

Cooperation Center (CJCC)

Participation in the launching ceremony

of the “Digital Platform Accelerator”

August 24, 2022 at the Techo Startup Center’s

Oce

Participation in discussion forum on

“Access to Finance and Market for

Women’s Business Growth”

June 16, 2022 at the Cambodia-Japan

Cooperation Centre (CJCC)

The virtual discussion forum on “The

implementation of Tourism Recovery

Co-Financing Scheme”

July 21, 2022

27

Annual Report 2022

SME Bank of Cambodia

Events

Organized the “Strategy Workshop”

to set the Bank’s business strategies plan for

2023-2025

September 30, 2022 at Hyatt Regency Hotel

Phnom Penh

Participation in the Cambodian Women

Entrepreneur’s Day on “MSMEs access to

Finance on digital Era”

December 09, 2022 at Sofitel Phnom Penh

Phokeetra Hotel

Participation in “the 4th CEO Gathering & 2nd

SMEs and Financial Institutions Night”

October 07, 2022 at Olympia City Hotel

Discussion on “ Tourism Recovery Co-Financing

Scheme Progress Update”

September 27, 2022 at the SME Bank’s Head

Oce

Induction Training

Septemeber 27 - 30, 2022 at the SME Bank’s

Head Oce

Seminar on “SME Access to Finance for

Developing Global Market”

October 4, 2022 at the SME Bank’s Head Oce

28

Annual Report 2022

SME Bank of Cambodia

Events

Co-sponsored on “the Cambodia Tech Expo

2022 (CTX 2022)”

November 11 - 13, 2022 at Koh Pich Convention

and Exhibition Center

Press Conference on “the Achievements of SME

Co-Financing Scheme”

December 05, 2022 at Raes Le Royal Hotel

12th Board of Directors Meeting

October 24, 2022 at the SME Bank’s Head Oce

29

Annual Report 2022

SME Bank of Cambodia

Events

Signing Ceremony of Memorandum of

Understanding (MoU) between SME Bank and

Cambodia Asia Bank Ltd., to implement the

Tourism Recovery Co-Financing Scheme

October 04, 2022

Signing Ceremony of Memorandum of

Understanding (MoU) between SME Bank and

J-Trust Royal Bank Ltd., to implement the

Tourism Recovery Co-Financing Scheme

October 26, 2022

Signing Ceremony of Memorandum of

Understanding (MoU) between SME Bank

and LOLC (Cambodia) Microfinance Institution

Plc., to implement the SME Co-Financing

Scheme Phase II

April 12, 2022

Signing Ceremony of Memorandum of

Understanding (MoU) between SME Bank and

Amret Microfinance Institution Ltd., to

implement the Tourism Recovery Co-Financing

Scheme

September 05, 2022

Signing Ceremony of Memorandum of

Understanding (MoU) between SME Bank and

Cambodia Asia Bank Ltd., to implement the

SME Co-Financing Scheme Phase II

May 03, 2022

Signing Ceremony of Memorandum of

Understanding (MoU) between SME Bank and

Maybank (Cambodia) Plc., to implement the

SME Co-Financing Scheme Phase II

April 19, 2022

Internal

Audit Dept.

Finance &

Planning Dept.

Chief Finance

Ocer

Chief Operating

Ocer

Deputy CEO

(Vacant)

Procurement

Committee

State

Controller

Board

of Directors

Board

Audit

Committee

Board Risk

and Compliance

Committee

Procurement

Unit

Chief Executive

Ocer

Chief

Technology

Ocer

Chief

Risk Ocer

Treasury Unit

Operation

Dept.

Marketing

Dept.

Technology

System Dept.

Executive Committee

Risk Management Committee

Credit Committee

Assets & Liabilities Committee

Disciplinary Committee

IT Security

Unit

Risk

Management

Dept.

ESG Unit

Direct Sale

Dept.

Property &

Admin Unit

Business

Development

Dept.

Legal &

Secretariat Dept.

Human Resource

Dept.

Information

System Dept.

Credit

Management

Dept.

Compliance

Dept.

Branches

MINISTRY

OF

ECONOMY &

FINANCE

Board Remuneration

and Nomination

Committee

Memorandum of Understanding (MoU) with

Participating Financial Institutions

30

Annual Report 2022

SME Bank of Cambodia

Events

Internal

Audit Dept.

Finance &

Planning Dept.

Chief Finance

Ocer

Chief Operating

Ocer

Deputy CEO

(Vacant)

Procurement

Committee

State

Controller

Board

of Directors

Board

Audit

Committee

Board Risk

and Compliance

Committee

Procurement

Unit

Chief Executive

Ocer

Chief

Technology

Ocer

Chief

Risk Ocer

Treasury Unit

Operation

Dept.

Marketing

Dept.

Technology

System Dept.

Executive Committee

Risk Management Committee

Credit Committee

Assets & Liabilities Committee

Disciplinary Committee

IT Security

Unit

Risk

Management

Dept.

ESG Unit

Direct Sale

Dept.

Property &

Admin Unit

Business

Development

Dept.

Legal &

Secretariat Dept.

Human Resource

Dept.

Information

System Dept.

Credit

Management

Dept.

Compliance

Dept.

Branches

MINISTRY

OF

ECONOMY &

FINANCE

Board Remuneration

and Nomination

Committee

ORGANIZATIONAL STRUCTURE

31

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

THE BOARD OF DIRECTORS

SENIOR MANAGEMENT

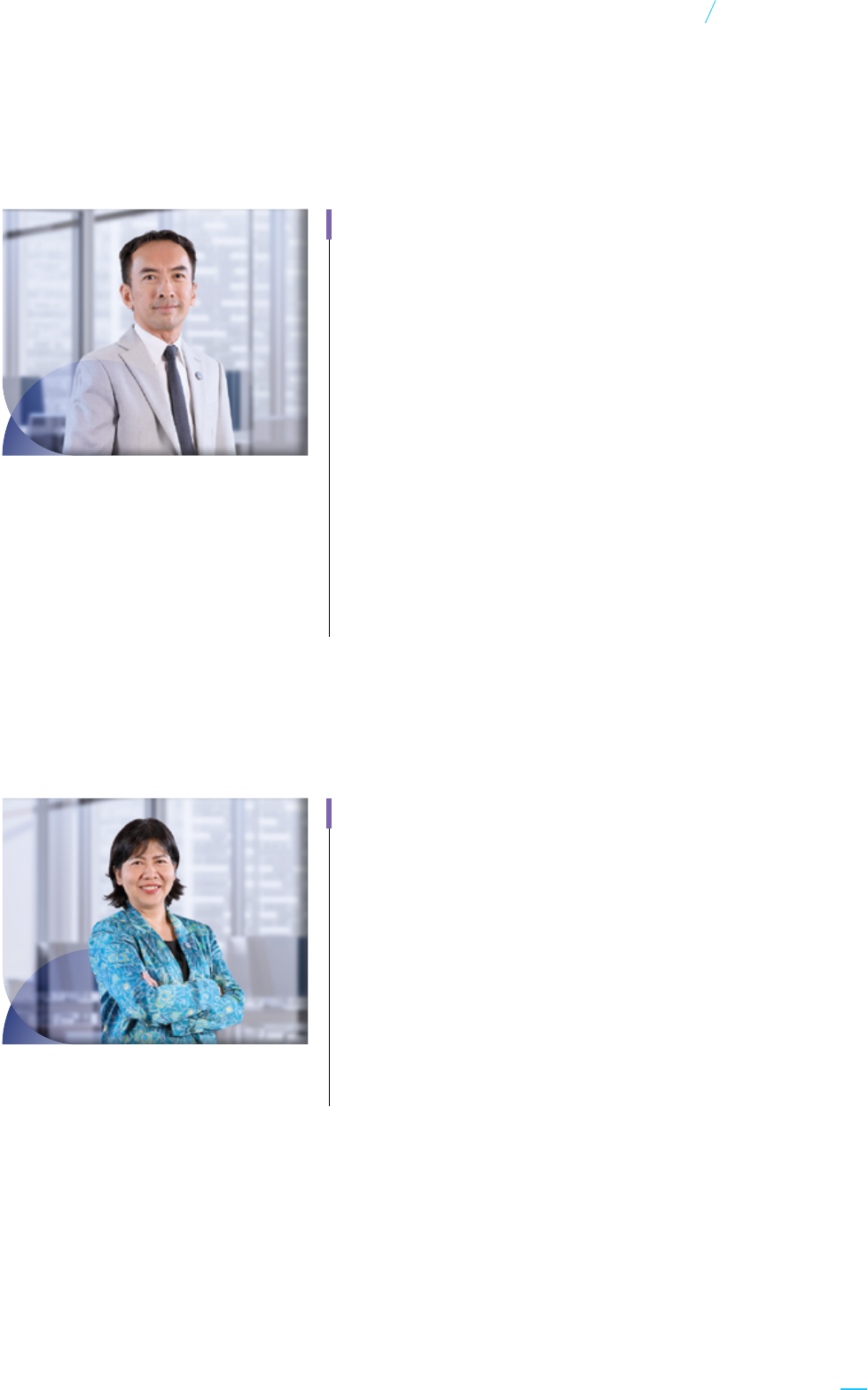

H.E. Dr. PHAN Phalla has joined the Ministry of Economy and

Finance and the Supreme National Economic Council since 2004.

He has been actively involved in the development of the Financial

Management Information System (FMIS) project, the Public

Financial Management Reform Program (PFMRP), the preparation

of national and sectoral strategies, revenue collection strategies,

management, and Macroeconomic analysis, development of

strategic framework and programs to restore and promote

Cambodia’s economic growth in living with COVID-19 in the new

normal path for 2021-2023, etc.

He is currently a member of the Supreme National Economic

Council, a board member of the Sihanoukville Autonomous Port,

the Secretary-General of the Economic and Financial Policy

Committee, the Secretary of State of the Ministry of Economy

and Finance, and the Chairman of SME Bank of Cambodia. He

holds a PhD in Economics from Australia.

H.E. Dr. PHAN Phalla

Secretary of State, Ministry of

Economy and Finance, and

Chairman of the Board

H.E. SON Seng Huot is the Secretary of State of the Ministry of

Industry, Science, Technology, and Innovation, he has a lot of

experience, before 2013, he was a director of Phnom Penh

Department of Industry, Mines and Energy. From 2013 to 2014,

He was the Deputy Director General of the Department of Small

and Medium Enterprise and Handicrafts at the Ministry of Industry

and Handicraft. From 2014 to the present, He is the Secretary of

State of the Ministry of Industry, Science, Technology, and

Innovation in charge of the General Department of Small and

Medium Enterprise and Handicrafts and the Department of

Industrial Aairs of the General Department of Industry.

He graduated from Vietnam with Small and Medium Enterprise

Management Skills and One Village One Product Management

Skills from Japan. He underwent short-term training courses on

small and medium enterprise management from Singapore and

Korea. He holds a master’s degree in public administration from

Asia Europe University.

H.E. SON Seng Huot

Board Member

THE BOARD OF DIRECTORS

34

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

H.E. TEP Phiyorin is currently the Under Secretary of State at the

Ministry of Economy and Finance. In the past, he was the Director

General of the General Department of Policy. He also served as

an advisor to the Executive Director of the World Bank Group,

based in Washington D.C. the United States. He joined the Ministry

of Economy and Finance in 1999 as a Budget Ocer, and since

then he has held several positions in the Ministry of Economy

and Finance, including the Director of the Oce of Macroeconomics,

Deputy Head of Department, and Head of the Department of

Economic Policy and Public Finance.

He holds a degree in Public Economics and Finance from the

University of Birmingham in the United Kingdom and in Economics

from the Kharkov State University of Economics in Ukraine. He

is currently responsible for monitoring macroeconomic

development, policy monitoring, and analysis of development

issues. He is also in charge of the macroeconomic framework,

and medium-term taxes, and advises on economics, finance, and

the public management sector as well.

H.E. TEP Phiyorin

Board Member

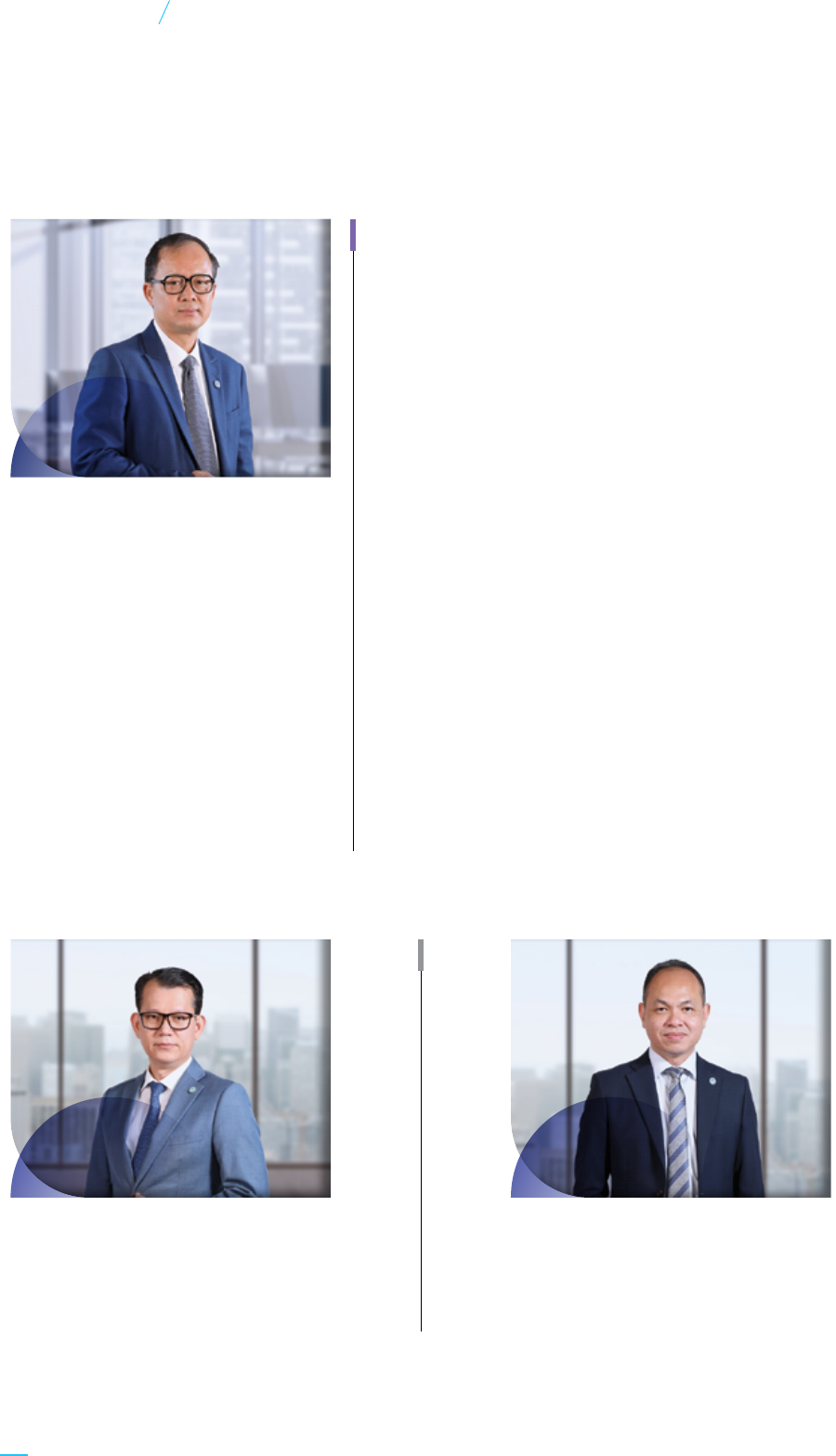

Mrs. CHHORN Dalis has been appointed as an Independent Board

Member of SME Bank of Cambodia in 2020. She has more than

20 years of experience as an accountant and leads small and

medium enterprises in various fields, including agro-industry and

clean water.

She holds a Master of Business Administration from the Asian

Institute of Technology in Thailand and a Master of International

Finance from Ceram Sophia Antipolis in France in 2002.

Mrs. CHHORN Dalis

Independent Board Member

35

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

Dr. LIM Aun

Chief Executive Officer and Board

Member

Mr. NEAV Sokun

Chief Operating Officer

and Board Member

H.E. CHAN Sok Ty is currently the Royal Government of Cambodia

Delegate in charge of the CEO of Green Trade Company of the

Ministry of Commerce, with the same status as the Secretary of

State and Board Member of SME Bank of Cambodia.

He is a member of the Food Reserve System Management

Committee of Cambodia (ប.ស.ប.ក), which is responsible for

managing the Royal Government’s Food Reserve System.

He was also the Director General of Domestic Trade of the Ministry

of Commerce; he has been the Director of Accelerating Inclusive

Markets for Smallholders Project (AIMS).

His Excellency joined the Ministry of Commerce in 1997 as an

Ocer of the Laboratory Oce of the General Department of

CamControl, and since then he has also held various positions in

the Ministry of Commerce, including Chong Ty Deputy Branch

Manager, Deputy Head of Department and Deputy Director

General of the General Department of International Trade, Acting

Director General of the General Department of Trade Promotion

of the Ministry of Commerce.

H.E. CHAN Sok Ty graduated with a degree in Food Chemistry

Engineering from the Institute of Technology of Cambodia and

a master’s degree in agriculture from the University of Tokyo,

Japan.

H.E. CHAN Sok Ty

Board Member

36

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

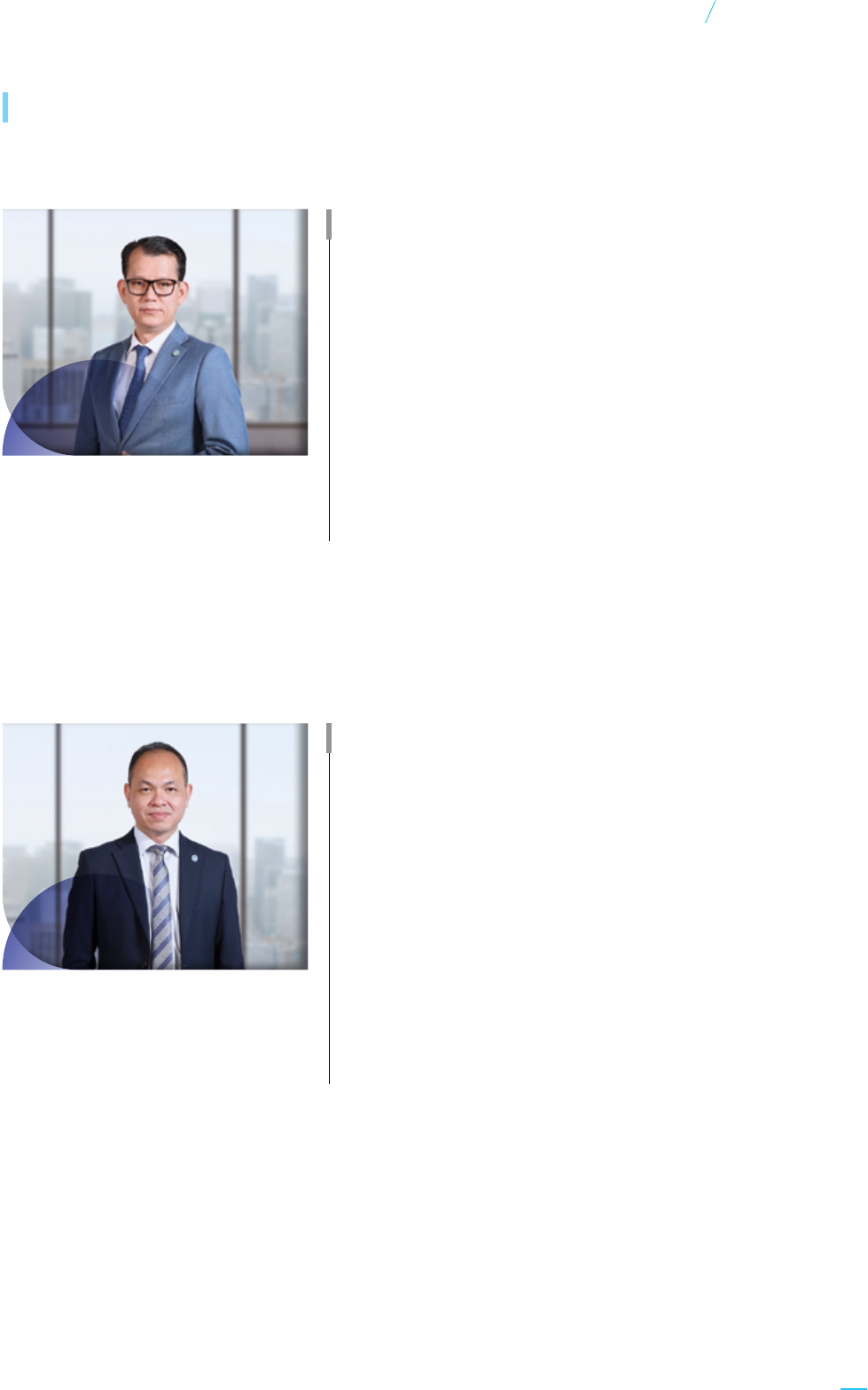

Dr. LIM Aun has more than 25 years of experience in the field of

banking and international auditing companies. Before joining

SME Bank of Cambodia, from 1997 to 2021, he served as a Senior

Auditor at KPMG in Cambodia and Malaysia, a Deputy General

Manager at Vattanac Bank, and lastly, a Chief Executive Ocer

at Sathapana Bank.

He was appointed as a Chief Executive Ocer and a Board

Member of SME Bank of Cambodia by the Royal Government in

August 2021.

He holds a PhD in Business Administration from France.

Dr. LIM Aun

Chief Executive Officer

and Board Member

Mr. NEAV Sokun has more than 20 years of experience in the

banking and financial sector. He has started his career in finance

since 2003. He has held various senior positions including Branch

Manager, Credit Executive, and Branch Manager with some big

Banks. In August 2021, he joined the SME Bank of Cambodia as

a Chief Operating Ocer, being responsible for managing the

processes and operations of the Business Department, Operations

Department, Marketing Department, Business Development

Department, Administration, and branches.

He holds a master’s degree in business administration from Norton

University and a Bachelor of Arts in English from Build Bright

University. He has also received certifications in management

and leadership training from many countries, including Italy, India,

and Vietnam.

Mr. NEAV Sokun

Chief Operating Officer

and Board Member

SENIOR MANAGEMENT

37

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

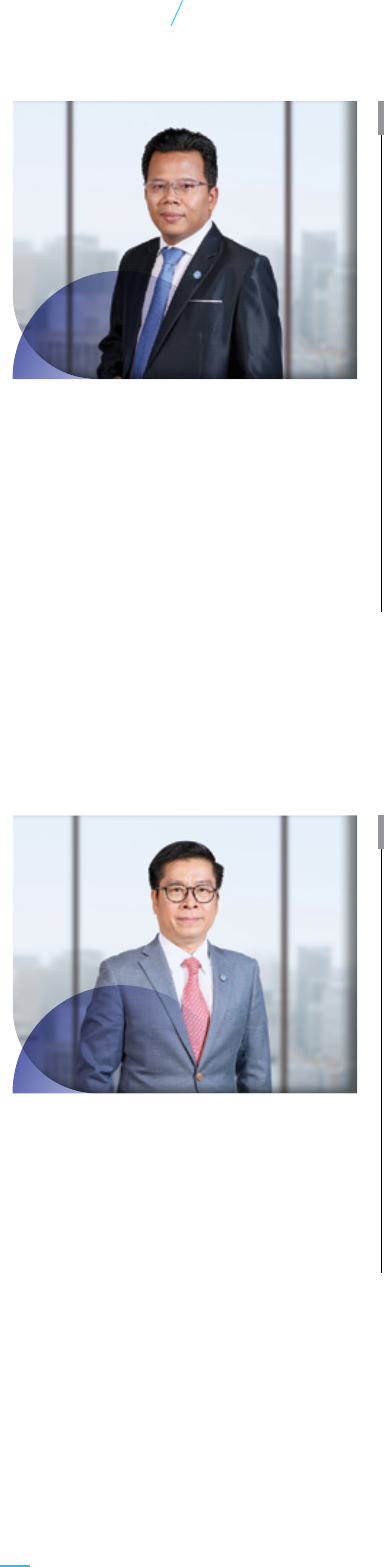

Mr. DEN Davuth joined the SME Bank of Cambodia in July 2021

with key responsibilities to execute Bank’s IT strategy, business

process re-engineering initiatives, and strengthen IT governance

and control.

He started his career in 2005 with a local bank in the Information

Technology Department. In 2010 he was among the pioneer team

to set up a bank, one of the biggest regional banks in Cambodia,

where he headed the Information Technology and Operations

departments. From 2018-2019, he drove a project team to set up

a new IT and Digital Banking infrastructure for a new local bank.

From 2020-2021, he became the Chief Technology and Information

Ocer at Sathapana Bank.

He graduated with a bachelor’s degree in computer science and

engineering from the Royal University of Phnom Penh in 2004,

a bachelor’s degree in public communication from the Institute

of Foreign Languages in 2009 and received his Management and

Leadership certificate from Nanyang Technological University in

2013.

Mr. DEN Davuth

Chief Technology Officer

Mr. OEUR Vibol has more than 18 years of experience in the

banking sector. He started his career at one of the leading local

banks in 2004 with experience in numerous roles in accounting

and finance. In 2010, he moved to one of the regional banks as

a pioneer in setting up the bank, where he had an opportunity

to expand his professional experience in accounting, finance, and

risk management. In his last role as Head of Risk Analytics and

Management, his main responsibilities were developing and

implementing risk management frameworks and policies to suit

operations and regulations.

In August 2020, he joined SME Bank as a Chief Risk Ocer to

oversee risk management functions, including but not limited to

credit, operational, liquidity, and market risks.

He graduated from the National University of Management with

a degree in Accounting and Finance and participated in numerous

courses in accounting, finance, risk management, and leadership.

Mr. OEUR Vibol

Chief Risk Management

38

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

The Bank has a strong governance structure through the

technical and financial guidance of the Ministry of Economy

and Finance with further supervision from the National

Bank of Cambodia. The bank is managed by the Chairman

and Members of the Board appointed by the Sub-Decree

of the Royal Government of Cambodia.

The Bank operates on the basis of the principles, regulations,

procedures, validation and evaluation mechanisms

established by the management and other relevant

departments within the Bank and approved by the Board

of Directors.

Corporate Governance

39

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

The Board of Directors (The Board) has seven members, with two Executive Directors and five Non-Executive

Directors. The Board is responsible for setting the goal and overseeing the overall management and aairs

of the Bank in accordance with the Royal Government of Cambodia’s policy direction. It is primarily accountable

to the Ministry of Economic and Finance (sole shareholder) for the proper conduct of the business of the

Bank. The Bank has established three Board-level committees which are under the direct control of the Board,

(1) Board Risk and Compliance Committee, (2) Board Nomination and Remuneration Committee, and (3)

Board Audit Committee. The Bank also has five executive Committees under the supervision of the Chief

Executive Ocer; they are 1) Executive Committee, 2). Risk Management Committee, 3). Asset and Liability

Management Committee, 4). Credit Committee, and 5). Procurement Committee.

A total of four Board meetings were held in 2022 and the Directors’ attendance at the meetings are as follows:

No. Directors Composition

1 H.E Dr. Phan Phalla Chairman

2 H.E Tep Phiyorin Member

3 H.E Son Senghout Member

4 H.E Chan Sokty Member

5 Dr. Lim Aun Member

6 Mrs. Chhorn Dalis Member

7 Mr. Neav Sokun Member

8 H.E Dr. Kong Marry State Controller

BOARD OF DIRECTORS MEETING

40

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

The Board appoints the Board Risk and Compliance Committee (BRCC) and comprises three Non-Executive

Directors. BRCC’s responsibility is authorized by the Board to ensure that the integrated risk management

functions within the Bank are eectively discharged.

The BRCC oversees credit, liquidity, market, and operational risks including a review of strategic risks, policies,

guidelines, assessment methodology, and risk management report. The BRCC reports to the Board of Directors

on all risk and compliance matters of the Bank.

A total of seven BRCC meetings were held in 2022 and the Directors’ attendance at the meetings is as follows:

No. Directors Composition

1 H.E. Tep Phiyorin Chairman / Non-Executive Director

2 H.E. Song Seng Huot

Member / Independent Non-Executive Director

3 Mrs. Chhorn Dalis Independent Non-Executive Director

The terms of reference of the Board Risk and

Compliance Committee are as follows:

› Risk Management

• To review, formulate and recommend policies for

the Board’s approval;

• To review and consider the adequacy of risk

management policies and frameworks, identifying,

measuring, monitoring, and controlling risk and

the extent to which these are operating eectively;

• To ensure infrastructure, resources and systems

are in place for risk management i.e., to ensure

that the sta are responsible for implementing

risk management systems performing those duties

independently of the Bank’s risk-taking activities;

• To review management’s periodic reports on risk

exposure, risk portfolio composition, risk rating

systems, risk appetite, stress testing, and risk

management activities;

• To review and approve risk-taking activities as

delegated;

• To establish and keep under review any sub-

committee.

› Compliance

• Discuss compliance, anti-money laundering, and

combating the financing of the terrorism risk, and

ensure the risks are resolved eectively and

eciently;

• Review and comply with all regulations and

policies on anti-money laundering and combating

the financing of the terrorism and all necessary

amendments to the compliance;

• Receive and review, at least annually, a report on

anti-money laundering and combating the

financing of terrorism crime produced by the

Compliance Ocer and any specific actions taken

by senior management concerning the report;

• Review reports from Compliance Ocer on the

arrangements established by management for

ensuring adherence to internal compliance policies,

procedures, and compliance with specific laws

and regulations, as required by the Committee or

required by laws and regulations;

• Review and advise on the fundamental activities

that are required by the Board of Directors.

BOARD RISK AND

COMPLIANCE COMMITTEE

41

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

Key Matters Reviewed/Deliberated/

Approved

Throughout the financial year ended 2022, BRCC has

committed to ensuring the Bank’s structure remained

resilient against multiple stressors, most notably

post-pandemic recovery strategies, and unexpected

economic shocks. Other matters discussed are set

out below:

• Discussed Risk Management Report;

• Discussed Compliance and Regulatory Compliance

Risk Report;

• Discussed compliance, anti-money laundering,

and combating the financing of the terrorism risk;

• Discussed the Bank’s Business Continuity

Management (BCP);

• Reviewed and endorsed Deviation Approval for

Loan Application;

• Reviewed and endorsed Finance and Accounting

Policy;

• Reviewed and approved on Finance’s Delegated

Authority;

• Reviewed and endorsed Credit Delegated

Approving Authority;

• Reviewed and endorsed Pricing Delegated

Authority for KHR Loan;

• Reviewed and endorsed Sale Channels Strategy;

• Reviewed and endorsed Business Partnership for

Bill Payment Services;

• Reviewed and endorsed Revised TRCS Schemes

Features;

• Reviewed and endorsed the Approved Property

Developers for sta Housing Loans;

• Reviewed and endorsed Opening Bank Account

and Delegated Authorized Signatories;

• Reviewed and endorsed Account Opening

Proposal – Wing

• Approved Risk Management Division’s and

Compliance Department’s Terms of Reference;

• Approved on AML/CFT Procedure;

• Approved Updating Credit Loss Rate;

• Approved Bill Payment Operations Manual;

• Approved Stress Test Scenario Result and Analysis

for Position as of November 2022;

› Risk Management Division

Risk Management plays a vital role in the banking business and is even more crucial during challenging business

environments. The role of Risk Management has also been broadened, and a strong risk culture needs to be

embedded into business units to ensure adequate risk transparency for the sustainable growth of the Bank.

Risk Management functions works independently and closely with all relevant business units to ensure the

understanding of risk culture and awareness.

Overall, Risk Management is responsible for administrating the day-to-day risk management functions as well

as the monitoring and control of the Bank’s risk exposures with regular reporting to the Risk Management

Committee and the Board Risk and Compliance Committee (BRCC).

42

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

Key Roles of Risk Management:

Credit Risk

Credit Risk is the possibility of losses due to a borrower or market counterparty failing

to perform its contractual obligations to the Bank.

The Credit Management is under the Risk Division, which is responsible for Credit Risk,

including reviewing key risk strategies, policies, guidelines, risk assessment approaches,

and risk reports. The Credit Management Department also provides an independent

evaluation of credit applications before submissions for decisions. Credit management

is also responsible for reviewing and monitoring the Bank’s loan portfolio and any

credit-related limit/threshold. Besides credit evaluation, Credit Management has also

covered the scope for Credit Quality Control and Loan Monitoring and Recovery to

strengthen the Bank’s asset quality and its long-term sustainability.

Liquidity

Risk

Liquidity Risk is the risk that the Bank does not have sucient financial resources

available to fund increases in assets or to meet its obligations as they come without

incurring unacceptable losses.

The Bank must maintain sucient liquidity at all times so that its cash flow positions

and/or liquefiable assets are readily available to meet financial and regulatory obligations

under BAU and stress conditions.

Liquidity risk undertaken by the Bank is governed by an established liquidity risk

appetite that defines the risk-taking level that the Bank is willing to accept in pursuit

of its strategic and business objectives.

Risk Management is responsible for monitoring the Bank’s liquidity risk profile and

reports regularly to the Risk Management Committee and the BRCC to manage its

liquidity position to meet its daily operational needs and regulatory requirements.

Market Risk

Market Risk is defined as fluctuations in the value of financial instruments due to

changes in market risk factors such as interest rates, currency exchange rates, credit

spreads, equity prices, commodities prices, and their associated volatility.

Operational

Risk

Operational Risk refers to the risk of loss resulting from inadequate or failed internal

processes, people and systems or external events. One of the key requirements of a

robust risk management structure is having eective Operational Risk Management

tools to identify comprehensively, measure, monitor, control, and report the entity’s

operational risk exposures.

43

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

The Board Audit Committee (“BAC”) is appointed by the Board. Board Audit Committee has composed of

four members who are Non-Executive Directors to provide oversight of the internal audit, financial statements,

internal control system, and risk management framework to ensure compliance with regulatory requirements

in the Bank. A total of eight Board Audit Committee meetings were held in 2022 at the meetings are as follows:

No. Directors Composition

1 Mrs. CHHORN Dalis Chairwoman

2 H.E. TEP Phiyorin Member

3 H.E. SON Senghuot Member

4 H.E. CHAN Sokty Member

The Board Audit Committee performs the

roles and responsibilities as follows:

• Ensure the information provided to the Public and

the National Bank of Cambodia is accurate and

reliable.

• Ensure the internal auditors regularly audit the

accounting methods, records, and financial

statements to meet the expectations of the

regulations and the Board.

• Evaluate, check, and approve the internal audit

policies, procedures, and annual internal audit

plans, mainly whether the system measuring,

monitoring, and risk management are consistent

and recommended on audit findings.

• Assist the Board in overseeing the implementation

of accounting policies, preparing accurate and

sucient reports, and ensuring the eectiveness

of internal control.

• Ensure corrective action between the internal

auditor and senior management to comply with

the target response.

Results of the Board Audit Committee’s

performance achievement in 2022:

• Reviewed and advised on internal audit findings,

and special audit findings;

• Discussed the KPIs for the Internal Audit team,

budgeting, and stang manpower;

• Reviewed the implementation following

recommendations from the Internal Audit

Department and the Board of Audit Committee;

• Reviewed and endorsed on External Auditor

selection before the Board of Director approved;

• Conducted meeting between senior management

with External Auditors on findings;

• Reviewed and endorsed on Annual Audit Report

2021 before the Board of Director for submitted

to CAFIU;

• Reviewed and approved Internal Control Report

2021 for submitted to NBC and CAFIU

• Reviewed training course for internal auditors;

• Reviewed and approved Annual Internal Audit

Plan for 2022;

• Evaluated annual performance of the Head Internal

Audit.

BOARD AUDIT COMMITTEE

44

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

The Internal Audit Department is responsible for

regularly evaluating, checking, and monitoring the

implementation of the Bank’s internal control system

and governance to ensure the Bank’s vision and main

objectives’ eectiveness. To ensure the transparency

and independence of the audit work, the internal

auditors must report directly to the Board Audit

Committee and indirectly to the Chief Executive

Ocer on certain administrative matters.

Internal Audit’s Key Roles:

• Manage audit work, coordinate, review, and report

on the internal audit’s work, and provide the Audit

Standards, criteria, and requirements of the

internal audit.

• Plan, manage, and monitor the daily work activities

of the Internal Audit Department and develop and

maintain eective and ecient customers and

sta.

• Ensure that Bank’s management and employees

fully implement all internal policies and procedures.

• Introduce management to the impact of risks

related to new products and services or activities

and plans to mitigate risks.

• Prepare and update an internal risk-based audit

plan for evaluating the eectiveness of risk

management and report the internal audit report

to the Board Audit Committee.

• Ensure the management has responded and acted

on the internal audit report and implemented the

recommendation by the target date. Perform other

tasks as assigned by the Board Audit Committee.

• Assist the Board Audit Committee and the Board

of Directors in fulfilling their responsibilities for

properly implementing accounting policies,

reports, adequacy, and eectiveness of internal

control.

45

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

The Board of Remuneration and Nomination (BRNC) Committee is appointed by the Board of Directors. The

Board of Remuneration and Nomination Committee consists of 1 (one) executive director and 4 (four) non-

executive directors to ensure that the Remuneration Policy is consistent with the long-term objectives and

corporate values of the SME Bank and reasonable in the light of the SME Bank’s objectives, compensation for

a similar function in other banks and financial institutions, and other relevant factors with due regard to the

interests of the shareholders and to the financial and commercial needs of the SME Bank. There were 5 (five)

meetings held in 2022 with the participation of members as follows:

No. Directors Composition

1 H.E. SON Senghuot Chairman

2 H.E. TEP Phiyorin Member

3 H.E. CHAN Sokty Member

4 Mrs. CHHORN Dalis Member

5 Mr. NEAV Sokun Member

The BRNC performs the roles and

responsibilities as follows:

• Cover all aspects of remuneration, including but

not limited to Directors’ fees, salaries, allowances,

expenses, consultancy fees (where applicable)

and benefits in kind; and

• Recommend the remuneration of the Directors

of the SME Bank to the Board of Director.

• Recommend to the Board the performance targets

and incentive plan (including bonus and any other

scheme designed to encourage long-term

corporate value creation) for the SME Bank

Managements, the Head of Internal Audit, and the

Compliance Manager for the coming year.

• Review the adequacy and form of compensation

to the SME Bank Managements and Key Managers

to ensure that it is realistically commensurate with

the responsibilities and risks involved in being an

eective member of the management team.

• Review and guide the evaluation of the

eectiveness of the Board and the Board

committee at least once per year.

• Review and update the relevant policies and

procedures at least once a year for BOD’s approval.

Results of the Board of Remuneration and

Nomination Committee in 2022:

• Reviewed and advised on the Annual salary

increment of 2022 and special salary increments

before the Board of Director approved

• Reviewed and advised on Sales incentive scheme

before the Board of Director approved

• Reviewed and advised on revise SME bank’s

management restructure before the Board of

Director approved

• Reviewed and approved on Employee performance

evaluation form of 2022

• Reviewed and approved on Provision of training

to employees

• Reviewed on defining employee performance

evaluation criteria

• Reviewed and advised on Code of Conduct before

the Board of Director approved

• Reviewed and evaluated the extension of

employment contract of a C-level sta

• Reviewed and approved on employee recognition

program

BOARD OF REMUNERATION AND

NOMINATION COMMITTEE (BRNC)

46

Annual Report 2022

SME Bank of Cambodia

Corporate Governance

FINANCIAL

STATEMENTS

The Board of Directors of Small and Medium Enterprise Bank of Cambodia Plc. (“the Bank”) presents its report

and the Bank’s financial statements as at 31 December 2022 and for the year then ended.

THE BANK

The Bank was incorporated in the Kingdom of Cambodia as a state-owned company organized under Law

on the General Statute of Public Enterprise with the registration certificate Co. 0001 M/2020 issued by the

Ministry of Commerce on 13 January 2020. The Bank is under technical and financial supervision of Ministry

of Economy and Finance (“MEF”).

The Bank obtained its banking license from the National Bank of Cambodia (“NBC”) on 27 February 2020 to

operate as a commercial bank with a permanent validity.

The Bank’s principal business activities are provisions of financing and commercial banking services to support

small and medium enterprises in the Kingdom of Cambodia.

The Bank’s registered oce address is located at MEF Business Development Center, #S, OCIC Street, Phum

Kien Khleang, Sangkat Chraoy Chongvar, Khan Chraoy Chongvar, Phnom Penh, Cambodia.

FINANCIAL RESULT

The Bank’s financial performance for the year is set out in the statement of comprehensive income.

DIVIDENDS

No dividend was declared or paid, and the Board of Directors does not recommend any dividend to be paid

for the year.

EXPECTED CREDIT LOSSES ON LOANS AND ADVANCES

Before the financial statements of the Bank were prepared, the Board of Directors took reasonable steps to

ascertain that action had been taken in relation to writing o of bad loans or recognition of allowance for

expected credit losses and satisfied themselves that all known bad loans had been written o and that adequate

allowance had been made for expected credit losses on loans and advances.

At the date of this report and based on the best of knowledge, the Board of Directors is not aware of any

circumstances which would render the amount written o for bad loans or the amount of the allowance for

expected credit losses in the financial statements of the Bank inadequate to any material extent.

REPORT OF THE BOARD

OF DIRECTORS

48

Annual Report 2022

SME Bank of Cambodia

Financial Statements

ASSETS

Before the financial statements of the Bank were prepared, the Board of Directors ascertained that management

took reasonable steps to ensure that any assets, which were unlikely to be realized in the ordinary course of

business at their values as shown in the accounting records of the Bank had been written down to amounts

which they might be expected to realize.

At the date of this report and based on the best of knowledge, the Board of Directors is not aware of any

circumstances which would render the values attributed to the assets in the financial statements of the Bank

misleading in any material respect.

VALUATION METHODS

At the date of this report, the Board of Directors is not aware of any circumstances that have arisen which

render adherence to the existing method of valuation of assets and liabilities in the financial statements of

the Bank misleading or inappropriate.

CONTINGENT AND OTHER LIABILITIES

At the date of this report, there is:

(a) no charge on the assets of the Bank which has arisen since the end of the financial year which secures

the liabilities of any other person; and

(b) no contingent liability in respect of the Bank that has arisen since the end of the financial year other

than in the ordinary course of its business operations.

No contingent or other liability of the Bank has become enforceable, or is likely to become enforceable within

the period of 12 months after the end of the financial year which, in the opinion of the Board of Directors, will

or may have a material eect on the ability of the Bank to meet its obligations as and when they fall due.

CHANGE OF CIRCUMSTANCES

At the date of this report, the Board of Directors is not aware of any circumstances, not otherwise dealt with

in this report or the financial statements of the Bank, which would render any amount stated in the financial

statements misleading.

ITEMS OF AN UNUSUAL NATURE

The result of the operation of the Bank for the year was not, in the opinion of the Board of Directors, substantially

aected by any item, transaction or event of a material and unusual nature.

There has not arisen in the interval between the end of the financial year and the date of this report any item,

transaction or event of a material and unusual nature likely, in the opinion of the Board of Directors, which

aect substantially the financial performance of the Bank for the year in which this report is made.

49

Annual Report 2022

SME Bank of Cambodia

Financial Statements

EVENTS AFTER END OF THE REPORTING PERIOD

At the date of this report, to the best knowledge of the Board of Directors, there have been no significant

events occurring after end of the reporting period which would require adjustments or disclosures to be made

in the financial statements.

THE BOARD OF DIRECTORS

The members of the Board of Directors holding oce during the year and at the date of this report are:

Name Position

H.E. Dr. Phan Phalla Secretary of State, Ministry of Economy and Finance

and Chairman of the Board of Directors

H.E. Tep Phiyorin Member

H.E. Chan Sokty Member

H.E. Son Seng Huot Member

Mrs. Chhorn Dalis Member

Dr. Lim Aun Chief Executive Ocer and Member

Mr. Neav Sokun Chief Operating Ocer and Member (Appointed on 1 February 2022)

AUDITOR

Ernst & Young (Cambodia) Ltd. is the auditor of the Bank.

DIRECTORS’ INTERESTS

No directors held any interest in the equity of the Bank. No arrangement existed to which the Bank is a party

with object of enabling the members to obtain an interest in the Bank or in any corporate body.

DIRECTORS’ BENEFITS

During and at the end of the year, no arrangement existed to which the Bank was a party with the objective

of enabling the directors of the Bank to acquire benefits by means of the acquisition of shares in or debentures

of the Bank or any other body corporate.

During the financial year, no director of the Bank has received or become entitled to receive any benefit by

reason of a contract made by the Bank or a related corporation with a firm of which the director is a member,

or with a company in which the director has substantial financial interest other than as disclosed in the financial

statements.

50

Annual Report 2022

SME Bank of Cambodia

Financial Statements

RESPONSIBILITIES OF THE BOARD OF DIRECTORS IN RESPECT OF

THE FINANCIAL STATEMENTS

The Board of Directors is responsible for ascertaining that the financial statements give a true and fair view

of the financial position of the Bank as at 31 December 2022, and its financial performance and its cash flows

for the year then ended. The Board of Directors oversees preparation of these financial statements by

management who is required to:

• adopt appropriate accounting policies which are supported by reasonable and prudent judgments and

estimates and then apply them consistently;

•

comply with the disclosure requirements of Cambodian International Financial Reporting Standards

(“CIFRSs”), or if there have been any departures in the interest of fair true and fair presentation, ensure

that these have been appropriately disclosed, explained and quantified in the financial statements;

•

oversee the Bank’s financial reporting process and maintains adequate accounting records and an eective

system of internal controls;

• assess the Bank’s ability to continue as a going concern, disclosing, as applicable, matters related to going

concern and using the going concern basis of accounting unless management either intends to liquidate

the Bank or to cease operations, or has no realistic alternative but to do so; and

• eectively control and direct eectively the Bank in all material decisions aecting the operations and

performance and ascertain that such have been properly reflected in the financial statements.

The Board of Directors confirms that they have fulfilled and complied with the above responsibilities in

preparing the financial statements.

APPROVAL OF THE FINANCIAL STATEMENTS

We hereby approve the accompanying financial statements which give a true and fair view of the financial

position of the Bank as at 31 December 2022, and its financial performances and its cash flows for the year

then ended in accordance with CIFRSs.

On behalf of the Board of Directors:

H.E. Dr. Phan Phalla

Secretary of State of Ministry of Economy and Finance

and Chairman of the Board of Directors

Phnom Penh, Kingdom of Cambodia

22 March 2023

Dr. Lim Aun

Chief Executive Ocer and Member

51

Annual Report 2022

SME Bank of Cambodia

Financial Statements

To: The Shareholder of Small and Medium Enterprise Bank of Cambodia Plc.

Opinion

We have audited the accompanying financial statements of Small and Medium Enterprise Bank of Cambodia

Plc. (“the Bank”) which comprise the statement of financial position as at 31 December 2022, and the statement

of comprehensive income, statement of changes in equity and statement of cash flows for the year then

ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements give a true and fair view of the financial position of the

Bank as at 31 December 2022, and its financial performance and its cash flows for the year then ended in

accordance with Cambodian International Financial Reporting Standards (“CIFRSs”).

Basis for Opinion

We conducted our audit in accordance with Cambodian International Standards on Auditing (“CISAs”). Our

responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of