Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>Please refer to the last page of the report on Restrictions

on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors, Expert Investors or

Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

Refer to Important Disclosures at the end of this report

BUY

Senco Gold

‘Gold’en opportunity – At a bargain; initiate with BUY

Retail Initiating Coverage September 20, 2023

TARGET PRICE (Rs) : 630

Senco Gold boasts of being one of the top-2 as regards revenue share in the

~Rs800bn eastern market, abetted by strongest brand accessibility vs peers, in

terms of product, price & penetration. Growth headroom is huge, as its market

share is still at a mid-single-digit in the East, and focused efforts are afoot to

capitalize on non-East prospects. Better access to capital, upbeat franchisee

interest and shift to organized should drive a strong revenue-led EPS CAGR of

>20% for Senco in FY23-26E. Growth would be backed by near-equal input from

new stores and SSG. Senco follows hygiene practices for sourcing/hedging gold

(50% stated policy), thus reducing the commodity’s volatility risk. Unit metrics

are better than/in line with peers’ (ex TTAN) and should further improve with

rise in franchisee mix. Despite similar growth prospects, Senco’s 19x 1-yr fwd

P/E is at a major discount to peer valuations, offering scope for rerating. We

initiate coverage on Senco with BUY and TP of Rs630/share (20x Sep-25E EPS).

Senco Gold: Financial Snapshot (Consolidated)

Y/E Mar (Rs mn)

FY22

FY23

FY24E

FY25E

FY26E

Revenue

35,346

40,774

50,147

59,955

71,240

EBITDA

2,772

3,166

3,522

4,421

5,462

Adj. PAT

1,291

1,585

1,680

2,146

2,718

Adj. EPS (Rs)

19.4

22.9

21.6

27.6

35.0

EBITDA margin (%)

7.8

7.8

7.0

7.4

7.7

EBITDA growth (%)

58.1

14.2

11.2

25.5

23.6

Adj. EPS growth (%)

110.0

18.0

(5.6)

27.8

26.6

RoE (%)

19.4

19.0

14.5

14.6

16.0

RoIC (%)

17.3

15.5

14.2

15.3

16.0

P/E (x)

24.4

20.7

21.9

17.1

13.5

EV/EBITDA (x)

12.9

12.0

11.4

9.3

7.8

P/B (x)

4.3

3.5

2.7

2.3

2.0

FCFF yield (%)

(1.8)

(3.1)

1.1

0.4

1.0

Source: Senco RHP document (historicals), Emkay Research (projections)

Low share in its stronghold East and focused non-East entry offer huge growth

runway: Senco is #2 in the East (Emkay: a Rs800bn market), given deepest penetration

in West Bengal (85 stores in 55 cities vs a 15-30-city presence for peers). Senco’s

unrivalled reach in WB is enabled by its effective franchisee partnerships, where peers

lack proficiency. Its East market share still being low at mid-single digit, Senco’s ahead-

of-the-curve investments in brand/franchisees are aiding extension into the adjoining

states of Bihar, Assam, Orissa and Jharkhand, and the Northeast. Also, Senco’s focus on

non-East (mainly Delhi-NCR/UP for now) will supplement its expansion in core eastern

areas. We expect the East and non-East to jointly add 60stores for Senco in FY23-26E,

on a base of 136 stores (12% store CAGR over FY23-26E vs. 8% CAGR over FY20-23).

Light-weight strengths ensure best accessibility; focus on new retail formats

for catering to affluent/GenZ customers: Senco’s basic offering entails a <10gm

product in most categories which facilitates it to offer a similar look at lower grammage

than peers. Leveraging its multi-decadal liaison with karigars (experts in making light-

weight items), Senco offers best-in-class accessibility, which has assisted it to permeate

deeper into tier-2/3 cities. Further, Senco is expanding its customer base via the D’Signia

and Everlite store formats, targeting affluent/GenZ customers (4-5% of FY23 sales).

Senco’s return ratios in line with or better than most organized players’

While Senco logs 13-14% RoE in COCO (company-owned company-operated) stores,

returns in FOFO (franchisee-owned franchisee-operated) stores are much higher, on nil

inventory investment. Versus peers, Senco’s return is aligned with Kalyan’s/better than

most listed jewelry retailers’. Senco’s margin surpasses peers’, albeit rev/store is lesser,

on low per-capita in the East; but this gets adjusted, on lower inventory need at stores.

Big valuation gap; candidate for huge rerating, on earnings delivery certainty

We expect Senco to clock ~20% PAT CAGR over FY23-26E which is in line with some

best-performing sector players’. Despite similar growth prospects, Senco trades at ~40%

discount to Kalyan Jewelers. While Kalyan has relatively better brand strength for faster

Pan-India expansion, we believe such a steep discount is unwarranted and provides

scope for re-rating, as Senco delivers on our expectations going ahead.

Target Price – 12M

Sep-24

Change in TP (%)

NA

Current Reco.

BUY

Previous Reco.

NA

Upside/(Downside) (%)

33.1

CMP (18-Sep-23) (Rs)

473.4

Stock Data

Ticker

52-week High (Rs)

490

52-week Low (Rs)

358

Shares outstanding (mn)

77.7

Market-cap (Rs bn)

37

Market-cap (USD mn)

441

Net-debt, FY24E (Rs mn)

3,284

ADTV-3M (mn shares)

-

ADTV-3M (Rs mn)

-

ADTV-3M (USD mn)

-

Free float (%)

15.0

Nifty-50

20,133

INR/USD

83.3

Shareholding, Jul-23

Promoters (%)

68.5

FPIs/MFs (%)

3.0/8.1

Price Performance

(%)

1M

3M

12M

Absolute

16.3

-

-

Rel. to Nifty

11.5

-

-

1-Year share price trend (Rs)

Devanshu Bansal

devanshu.bansal@emkayglobal.com

+91 22 6612 1385

Bhavika Choudhary

bhavika.choudhary@emkayglobal.com

+91 22 6624 2431

10

18

26

34

42

50

300

340

380

420

460

500

Jul-23 Jul-23 Aug-23Aug-23Aug-23Sep-23Sep-23

%Rs

SENCO IN EQUITY (LHS) Rel to Nifty (RHS)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |2

Story in Charts

Exhibit 1: The category (i.e. gold jewelry) has shown resilience, despite a spate of regulatory interventions and the Covid-19 pandemic

FY16

FY23

FY26E

FY36E

FY16-23

FY23-26E

FY26-36E

CAGR (%)

Gold rate (USD/Troy Ounce)

1,160

1,800

2,025

2,721

6.5

4.0

3.0

INR-USD currency

64

79

88

131

3.0

4.0

4.0

Gold rate (INR/10gm)

23,915

45,512

57,587

1,14,560

9.6

8.2

7.1

India Custom Duty (%)

10%

15%

15%

15%

Gold Imports (ton)

857

774

774

774

-1.4

0.0

0.0

Total Imports - Value (Rs trn)

2.3

4.1

5.1

10.2

8.7

8.2

7.1

Gold exchange incremental sales mix (%)

8%

12%

13%

19%

0.5

0.4

0.5

Studded incremental sales mix (%)

4%

8%

11%

17%

0.5

0.9

0.5

Brand/Design incremental sales mix (%)

4%

8%

9%

16%

0.5

0.5

0.6

Total Gold Jewelry consumption (Rs trn)

2.6

5.2

7.0

16.3

10.3

10.1

8.8

Source: World Gold Council (WGC), Emkay Research; Note: The WGC follows calendar-year reporting (FY16 is CY15 and so on, for WGC numbers)

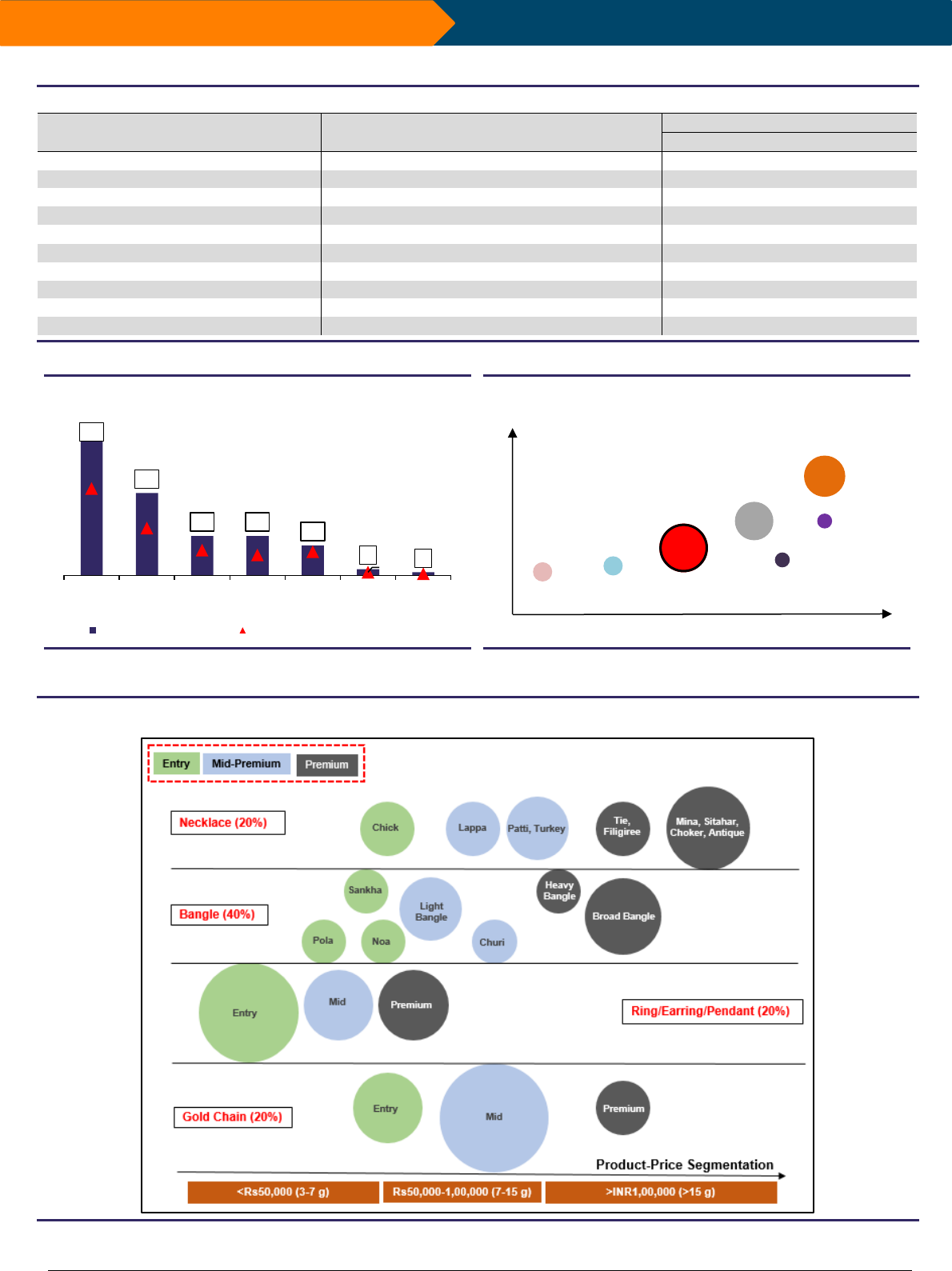

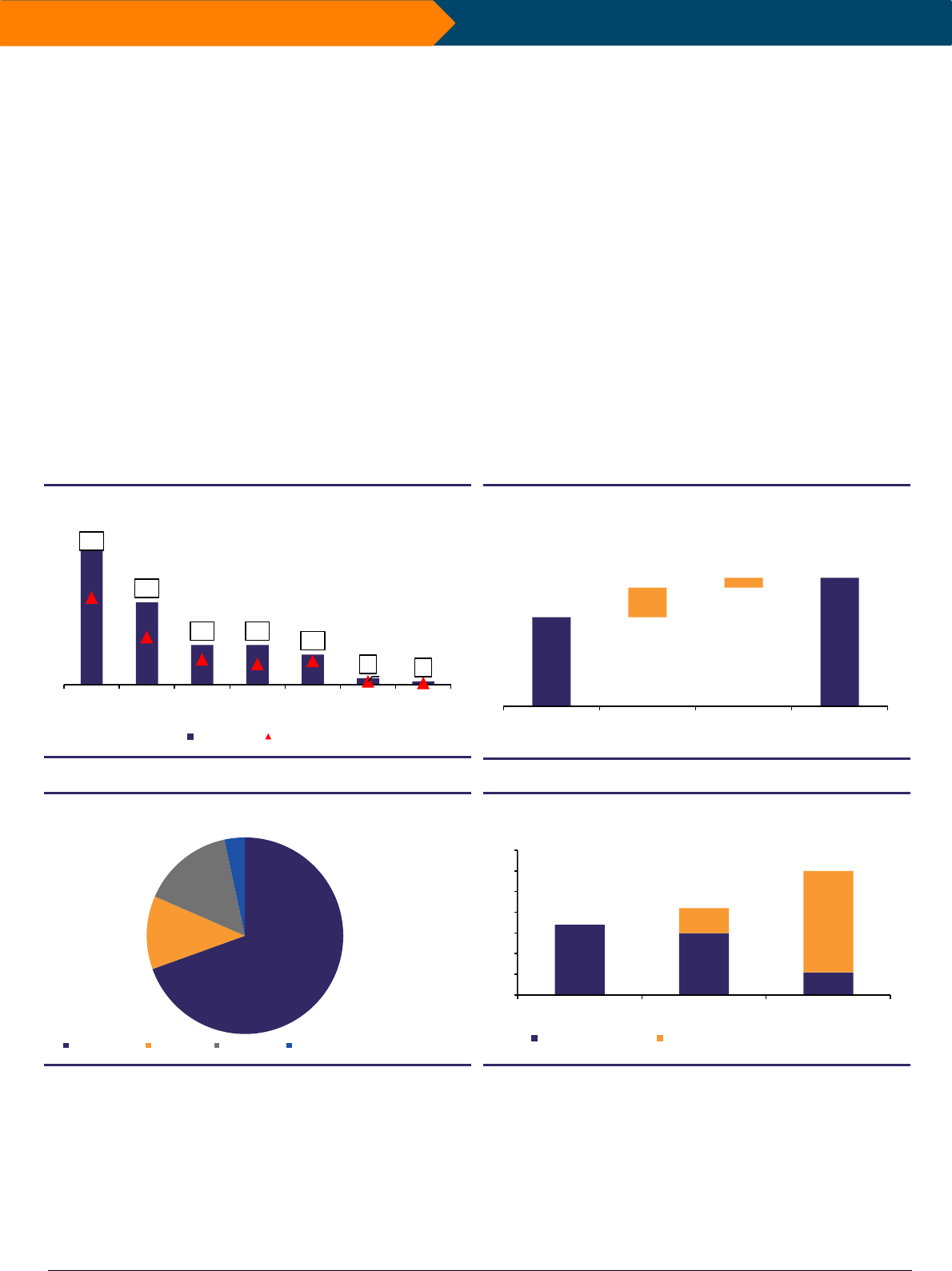

Exhibit 2: Senco leads the pack in the East, given its penetration

being the deepest among peers in the West Bengal market

Source: Store locators (Company websites), Emkay Research

Exhibit 3: The East is a Rs800bn market, with Tanishq/Senco/PC

Chandra commanding dominant shares

Source: Emkay Research, Note: The size of the bubble in the chart

represents the ballpark market share (%) in West Bengal

Exhibit 4: Senco focuses on maintaining superior brand accessibility, via light-weight product offerings, customer engagement, purity and

branding initiatives

Source: Emkay Research (channel checks); Note: Size of the bubble represents the ballpark value share of an article within its category for Senco

85

52

25 25

19

4

2

55

30

16

13

15

2

1

Senco PC

Chandra

Anjali Tanishq MPJ Kalyan Malabar

Number of stores Number of cities, West Bengal

Tanishq

Kalyan

PC

Chandra

Malabar

Senco

MPJ

Anjali

Design Language (bsed on grammage)

Making Charges

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |3

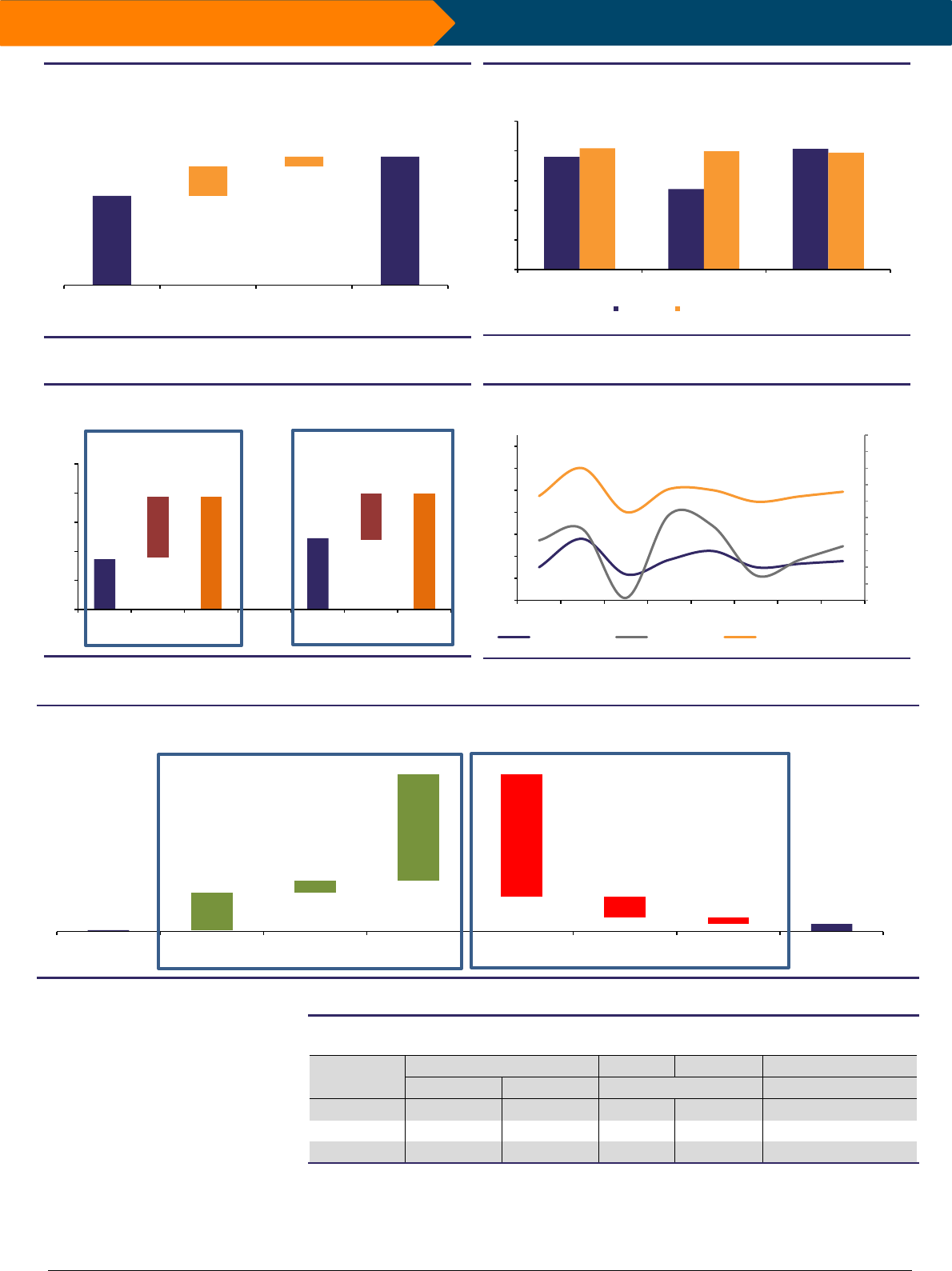

Exhibit 5: We expect network expansion to accelerate, with 60 new

store additions over FY23-26, on a base of 136 stores

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 6: We expect revenue/EBITDA/PAT CAGR of ~20% over

FY23-26E, largely led by topline growth and stable margins

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 7: We expect the topline CAGR of 20% to be supported by

the 8%/12% SSG/store-addition CAGR, respectively

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 8: We expect ROE to recover to the mid-teens, on margin

recovery and utilization of balance-sheet cash

Source: Senco RHP document (Historicals), Emkay Research (Projections)

Exhibit 9: Senco will require Rs10bn growth capital to open 45 COCO stores over FY23-26; of these, 80% would be serviced by internal

accruals

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 10: Senco currently trades at ~40% discount to Kalyan, despite both having similar

revenue growth prospects

Company (%)

FY23-26E CAGR

FY23

FY26

1-Yr fwd P/E (x)

Revenue

PAT

ROE

(Sep-24E EPS)

TTAN

18.0

18.5

30.9

26.5

74

KALYAN

23.0

31.4

11.9

16.2

33

SENCO

20.4

19.7

16.8

14.9

19

Source: Bloomberg estimates (Kalyan), Emkay Research

136

196

45

15

FY23 Store

Count

COCO additions

(FY23-26)

FOFO additions

(FY23-26)

FY26 Store

Count

19

14

20

20

20

20

0

5

10

15

20

25

Revenue EBITDA PAT

FY20-23 FY23-26E, CAGR (%)

9

10

19

12

8

20

0

5

10

15

20

25

Store

CAGR

SSG

CAGR

Revenue

CAGR

Store

CAGR

SSG

CAGR

Revenue

CAGR

FY20-23 (%)

FY23-26E (%)

13.0

15.6

12.4

13.7

14.5

13.0

13.3

13.6

15.4

16.5

10.2

17.8

16.8

12.2

13.7

14.9

6.3

8.0

5.3

6.7

6.7

6.0

6.3

6.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

10

12

14

16

18

20

22

24

FY19 FY20 FY21 FY22 FY23 FY24E FY25E FY26E

Gross (LHS, %) RoE (LHS, %) Pre-IndAS EBITDA (RHS, %)

0.1

0.6

2.7

0.8

7.5

8.7

1.5

0.5

Cash (FY23) Equity Raise (FY24) Debt Raise (FY23-

26)

CFO (before WC

changes)

WC Investments

(FY23-26)

Capex (FY23-26) Dividend (FY23-26) Cash (FY26)

Sources of Funds (Rs bn)

Usage of Funds (Rs bn)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |4

Table of contents

■ Jewelry Retail: Value appreciation and cultural significance provide natural

tailwinds, offer relatively more resilience .......................................................... 5

■ Differentiated product, improved capital access and first-mover advantage

should help to accelerate growth ....................................................................... 7

Senco’s strength in light-weight offerings makes it the most accessible brand .............. 8

Skewed EBO penetration provides a long growth runway ............................................ 10

Unit Metrics: Increase in Franchisee mix should drive RoE improvement .................. 11

Gold appreciation is a big SSG lever; attractive schemes to help drive faster growth .. 12

Peer Comparison: Strong growth delivery; returns profile matches Kalyan’s ............ 13

Follows hygiene practices for sourcing; stated policy of 50% hedging Gold exposure . 15

Jewelry purchase schemes: Cheaper source of capital ................................................. 16

■ Financials: Accelerated expansion and strong SSG to drive >20% PAT CAGR .... 17

Expect stable working capital on strong plans for non-East expansion ......................... 18

Internal accruals to service 80% of the required growth capital over FY23-26E ........... 18

■ Valuations: Trading at steep discount to peers; Consistent delivery on our

expectations provides scope for re-rating .......................................................... 19

■ Potential upsides and downsides ....................................................................... 20

■ Appendix ........................................................................................................... 21

■ Key Financials ................................................................................................... 23

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |5

Jewelry Retail: Value appreciation and cultural significance

provide natural tailwinds, offer relatively more resilience

India’s love for ‘gold’ is clearly evident in its positon as the second-largest importer of gold

globally, only marginally behind China. The category’s resilience is also demonstrated by the

jewelry category leading other discretionary categories, with 175% recovery in FY23 (over

FY20; pre-pandemic) and 10% CAGR over FY16-23, despite a glut of unfavorable regulatory

changes and gold-price volatility (refer Exhibit 11-12). The better recovery is a result of strong

cultural significance of gold in Indian weddings/festive seasons and the associated investment

value in times of uncertainty. Basis such growth drivers, we expect continued strong CAGR of

9-10% for Indian jewelry retail over the next decade as well.

More importantly, shift towards organized retail has accelerated, with: 1) improved access to

growth capital (equity/gold-metal-loans) and franchisee investments for organized players; 2)

loss of profit avenues for unorganized players with regulatory curbs on under-carat-age/price

arbitrage, with implementation of GST/hallmarking; and 3) increase in urbanization/women-

workforce-participation, which is driving higher spends on studded jewelry and better designs

(higher making charges).

Exhibit 11: The category (i.e. gold jewelry) has shown resilience, despite a spate of regulatory interventions

FY16

FY23

FY26E

FY36E

FY16-23

FY23-26E

FY26-36E

CAGR (%)

Gold rate (USD/Troy Ounce)

1,160

1,800

2,025

2,721

6.5

4.0

3.0

INR-USD currency

64

79

88

131

3.0

4.0

4.0

Gold rate (INR/10gm)

23,915

45,512

57,587

1,14,560

9.6

8.2

7.1

India Custom Duty (%)

10%

15%

15%

15%

Gold Imports (ton)

857

774

774

774

-1.4

0.0

0.0

Total Imports - Value (Rs trn)

2.3

4.1

5.1

10.2

8.7

8.2

7.1

Gold exchange incremental sales mix (%)

8%

12%

13%

19%

0.5

0.4

0.5

Studded incremental sales mix (%)

4%

8%

11%

17%

0.5

0.9

0.5

Brand/Design incremental sales mix (%)

4%

8%

9%

16%

0.5

0.5

0.6

Total Gold Jewelry consumption (Rs trn)

2.6

5.2

7.0

16.3

10.3

10.1

8.8

Source: World Gold Council, Emkay Research; Note: WGC follows calendar-year reporting (FY16 is CY15 and so on, for WGC numbers)

Exhibit 12: Jewelry retailers have seen a relatively higher recovery than other discretionary categories (over pre-pandemic levels; FY20)

Source: Company, Emkay Research

Organized players are also expanding faster than the overall industry, with increasing

willingness of third-party retailers to invest and participate in the strong growth journey of

organized watch retail. Strong brand recall is crucial for gaining traction with franchisees.

Across major organized players, franchisees form 20-45% of the overall store network.

Exhibit 13: Strong organized brands have access to franchisee capital; expansion is asset-light

Source: Company (Senco, Kalyan); Emkay Research (channel checks for TTAN)

113

115

166

203

131

147

165

169

171

105

114

118

121

168

243

132

139

168

186

193

BATA

RELAXO

METRO

CAMPUS

JUBI

WESTLIFE

DEVYANI

SAPPHIRE

BK India

TCNSBR

ARVIND

SHOP

VMART

ABFRL

TRENT

TBZ

KALYAN

SENCO

THANGAMAYIL

TTAN

Footwear: 132

Jewelry: 173

Apparel: 154

QSR: 149

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |6

Gold price increase is a natural tailwind for jewelry industry: Jewelry industry has seen

10% CAGR over FY16-23, largely led by realization growth, as volume has largely remained

stable over many years now. We believe stable volume is a function of a strong increase in

gold price which is resulting in a volume squeeze by consumers to protect their wallets.

Incrementally, value addition in the form of higher studded mix and better designs (making

charges) has added 150-200bps to industry growth. Going ahead, we expect continued strong

trends for the industry, driven by a high single-digit industry growth and growing share of

studded/high-margin purchases, on improved urbanization and higher per-capita income.

Exhibit 14: Gold price increase and long-term INR depreciation are

natural growth drivers for the category

Source: WGC, Emkay Research; Note: FY16 is CY15 and so on, for WGC

numbers

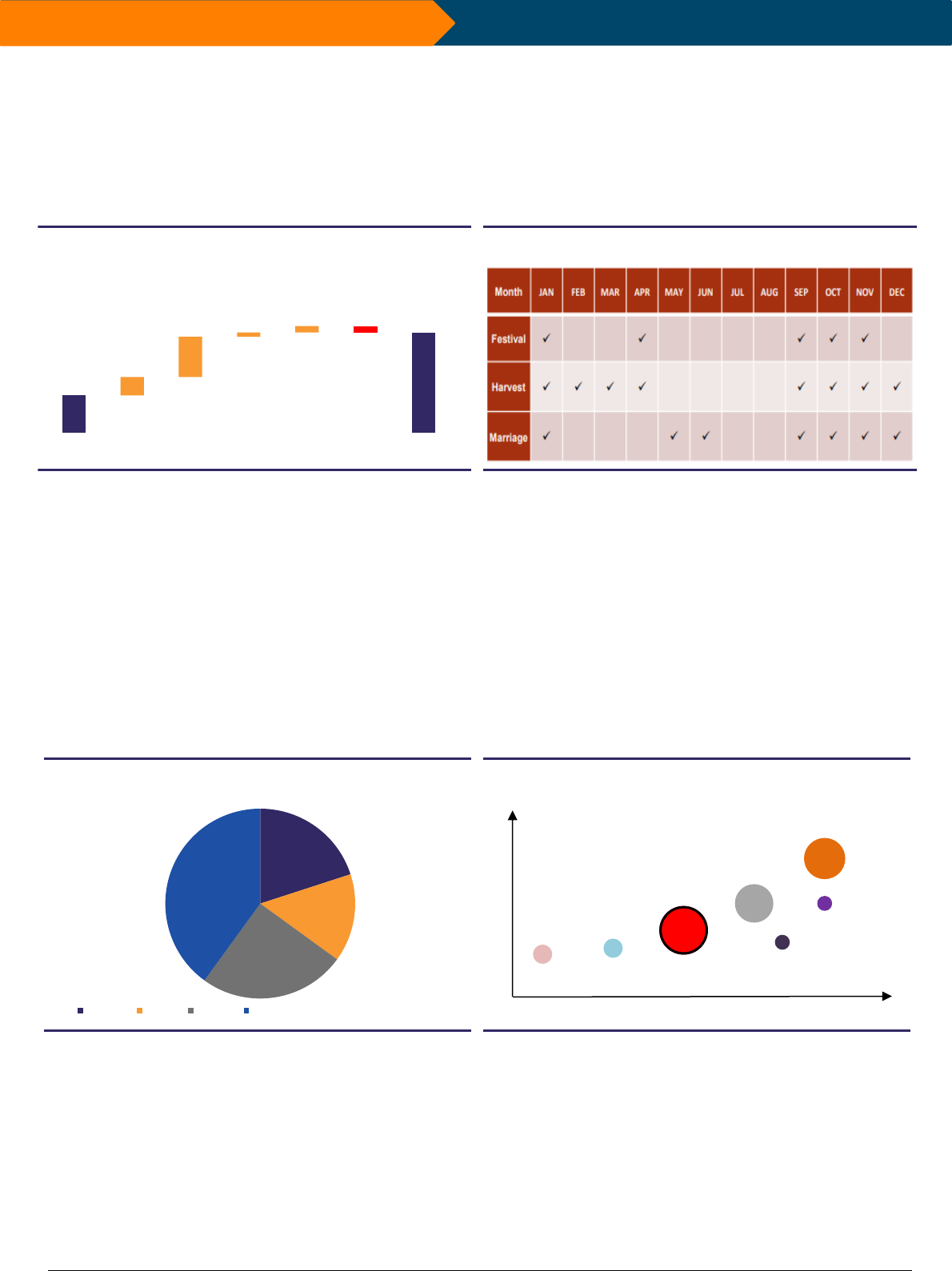

Exhibit 15: Demand is seasonal, with Q3 being the strongest quarter,

followed by Q1/Q4; Q2 is the weakest quarter

Source: Thangamayil investor PPT, Emkay Research

Low per-capita in East India provides long-term growth potential; Senco commands

dominant share among organized players: Among regions, South India leads with 40%

share, the North and West follow with 20-25% share, while the East lags with the lowest share

of 15%. Salience across regions depends on per-capita income across regions. Among

rural/urban regions, Rural in East India logs significantly lower per-capita consumption vs the

national average. However, this provides scope for continued growth with potential increase in

per-capita income of these regions going ahead. Among the top-7 organized jewelry chains in

the region, Senco, PC Chandra and Tanishq command the majority share. Regional players like

MPJ Jewelers and Anjali Jewelers are relatively less aggressive on the growth front, while

Kalyan/Malabar are starting to test the waters in East India. Jewelry is a seasonal business

with high salience towards festive/wedding/harvest periods. Among quarters, Q3 is the

strongest, followed by Q1, Q4 and Q2 in that order.

Exhibit 16: Lower per-capita income drives lower mix for East

India; longevity of growth is high, with expected rise in per-capita

Source: Senco RHP document, Emkay Research

Exhibit 17: The East is a Rs800-bn market, with Senco/PC

Chandra/Tanishq commanding leadership shares

Source: Emkay Research, Note: The size of the bubble in the chart

represents the ballpark market share (%) in West Bengal

Hallmarking/GST implementation a fortunate turn for organized players: Regulatory

changes over the past few years have plugged key bad practices or profit avenues for

unorganized players, thereby accelerating the shift towards organized players. Unorganized

players have always benefited from under-caratage, aiding in ‘making charges’ staying below

organized players’ and gaining traction with consumers. However, with implementation of

hallmarking (HUID), unorganized players have to compensate the under-caratage loss by

increasing their making charges, resulting in a level-playing field for all players. Similarly, GST

implementation has curbed price arbitrage enjoyed by unorganized players, again accelerating

the market-share shift towards organized players.

100

110

3

6

1

1

INR/USD

Designs/

Studded

Custom

Duty

Gold

price

Volumes

Components of Indian Jewelry category growth (FY16-23)

-1

20%

15%

25%

40%

North East West South, Region wise value market share

Tanishq

Kalyan

PC

Chandra

Malabar

Senco

MPJ

Anjali

Design Language (bsed on grammage)

Making Charges

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |7

Differentiated product, improved capital access and

first-mover advantage should help to accelerate growth

Senco Gold is part of select and elite group of organized jewelers, who have seen faster and

consistent growth over the last decade (~15% CAGR for Senco over FY16-23 vs. 10-11%

growth for the industry). The 15% revenue CAGR has been led by ~8% CAGR in store additions,

with the remaining through a healthy growth in average revenue per store (or SSG). Despite

the higher base, we expect Senco to deliver earnings CAGR of >20% over FY23-26E, with

accelerated expansion through IPO proceeds (12% store-addition CAGR vs. 8% historically).

At present, RoE is in mid-teens which should gradually track an improving trend with increase

in franchisee mix and better inventory turns on consumers adapting to elevated gold prices.

Senco as a brand stands out in terms of its light-weight jewelry with a heavy look which ensures

the best affordability for the emerging middle-class consumer. Sourcing, merchandising and

marketing are the company’s key moats that ensure product differentiation, micro-market-

based assortment, and help it to on-board new consumers with attractive offers and celebrity

endorsements. Going ahead, Senco’s focus is to leverage its strong brand equity for expansion

through franchisees in eastern India and strengthen its brand in non-eastern regions via

company-owned stores initially.

Exhibit 18: IPO proceeds, product differentiation (light-weight jewelry) and accelerated organized shift should help to deliver >20% growth

over FY23-26E vs. 15% over FY16-23

FY16

FY23

FY26E

FY36E

FY16-23

FY23-26E

FY26-36E

CAGR (%)

Gold rate (USD/Troy Ounce)

1,160

1,800

2,025

2,721

6.5

4.0

3.0

INR-USD currency rate

64

79

88

131

3.0

4.0

4.0

Gold rate (INR/10g)

23,915

45,512

57,587

1,14,560

9.6

8.2

7.1

India Custom Duty (%)

10%

15%

15%

15%

Gold Imports (ton)

857

774

774

774

-1.4

0.0

0.0

Total Imports - Value (Rs trn)

2.3

4.1

5.1

10.2

8.7

8.2

7.1

[A] Gold exchange incremental sales mix (%)

8%

12%

13%

19%

[B] Studded incremental sales mix (%)

4%

8%

11%

17%

[C] Brand/Design incremental sales mix (%)

4%

8%

9%

16%

Total Gold Jewelry consumption (Rs trn)

2.6

5.2

7.0

16.3

10.3

10.1

8.8

Total Gold Jewelry consumption (East India, Rs bn)

787

1,196

3,716

15.0

12.0

Senco - Revenue (East India, Rs bn)

33

57

260

19.8

16.3

Market Share

4.2%

4.8%

7.0%

Total Gold Jewelry consumption (other regions, Rs bn)

4,457

5,794

12,546

9.1

8.0

Senco – Revenue (other regions, Rs bn)

6

11

125

19.7

28.0

Market Share (%)

0.1%

0.2%

1.0%

Senco Gold (other segments, Rs bn)

1.2

3.2

13.0

39.8

15.0

Total Revenue - Senco Gold (Rs bn)

15.3

40.8

71.2

398.5

15.0

20.4

18.8

Source: World Gold Council, Kalyan/Senco Gold RHP Document, Emkay Research; Note: WGC follows calendar-year reporting (FY16 is CY15 and so on)

Exhibit 19: Senco is part of the elite group of jewelers that have seen faster and consistent growth over the last decade

Source: MCA, Company, Emkay Research; Note: Revenue includes export revenue across players; Malabar topline includes wholesale revenue as well

92

68

87

15 58 13 59

98

17

300

191

243

35

103

22

82

108

18

22

19

19

15

10

10

6

2

2

0

5

10

15

20

25

0

50

100

150

200

250

300

350

Malabar GRT Titan

(Jewelry)

Senco Gold Joyalukkas Thangamayil Lalithaa Kalyan TBZ

FY16 Revenue (Rsbn) FY22 Revenue (Rsbn) Revenue CAGR (%)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |8

Senco’s strength in light-weight offerings makes it the most accessible brand for

middle-class consumers in East India:

1) Product: Senco leverages its multi-decadal relationship with karigars (in Kolkata) to

offer relatively light-weight ornaments with a heavy-look. This helps Senco to

differentiate itself from players who offer heavier jewelry (higher grammage). From a

category perspective, presence is across categories, with major contributors being

necklaces, bangles, rings/pendants and gold chains. Senco scores well on customer

trust, as the brand has improved its ranking from the fourth most-trusted jewelry

brand in 2017 (TRA’s Brand Trust Report) to the second 2nd most-trusted jewelry

brand since 2020.

2) Pricing: Merchandise at stores is localized, with focus on addressing the entire

middle-class of the local catchment through its light-weight jewelry. For all categories,

Senco starts off with a <10gm offering, through which it is able to offer a similar look

with 15-20% lower grammage than peers (channel checks). In other words, key focus

is on maintaining superior brand accessibility and generating higher footfalls, albeit at

lower ticket size vs. peers (Rs60-70K ticket size vs. Rs80-125K for TTAN, Kalyan).

3) Promotion: With focus on light-weight jewelry, Senco invests in both, ATL and BTL

avenues of marketing, to garner the required footfalls. The company spends ~2% of

sales earnings in ads/marketing, with focus on top-of-the-funnel marketing, to gain

new consumers. In addition to its mass-marketing initiatives with celebrity brand

ambassadors (Kiara Advani, Sourav Ganguly and Vidya Balan), Senco makes

extensive efforts in store-level marketing initiatives, such as cross-marketing with

other retailing formats, specific event-based schemes in housing societies/tourist

hotspots and strong engagement with local influencers/regional celebrities.

4) Placement: Senco largely distributes its products through the Senco-branded EBOs

(both COCO/FOFO). The company has presence in 85 cities via 142 stores, of which

80 are in the COCO format with the remaining in the FOFO format. Focus is to have

presence in metro/tier-1 cities through COCO stores and penetrate deeper into Tier-

2/3/4 cities via the asset-light FOFO model. Jewelry is sold to franchisees on an

outright basis, with Senco retaining 1/3rd margin and distributing the balance to

franchisees. Franchisee return on mature stores is healthy, in the 15-20% range, in

addition to the long-term appreciation of the gold inventory.

Exhibit 20: Senco focuses on maintaining superior brand accessibility, via light-weight product offerings, customer engagement, purity and

branding initiatives

Source: Emkay Research (channel checks); Note: The size of the bubble represents ball-park value share of an article within its category for Senco

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |9

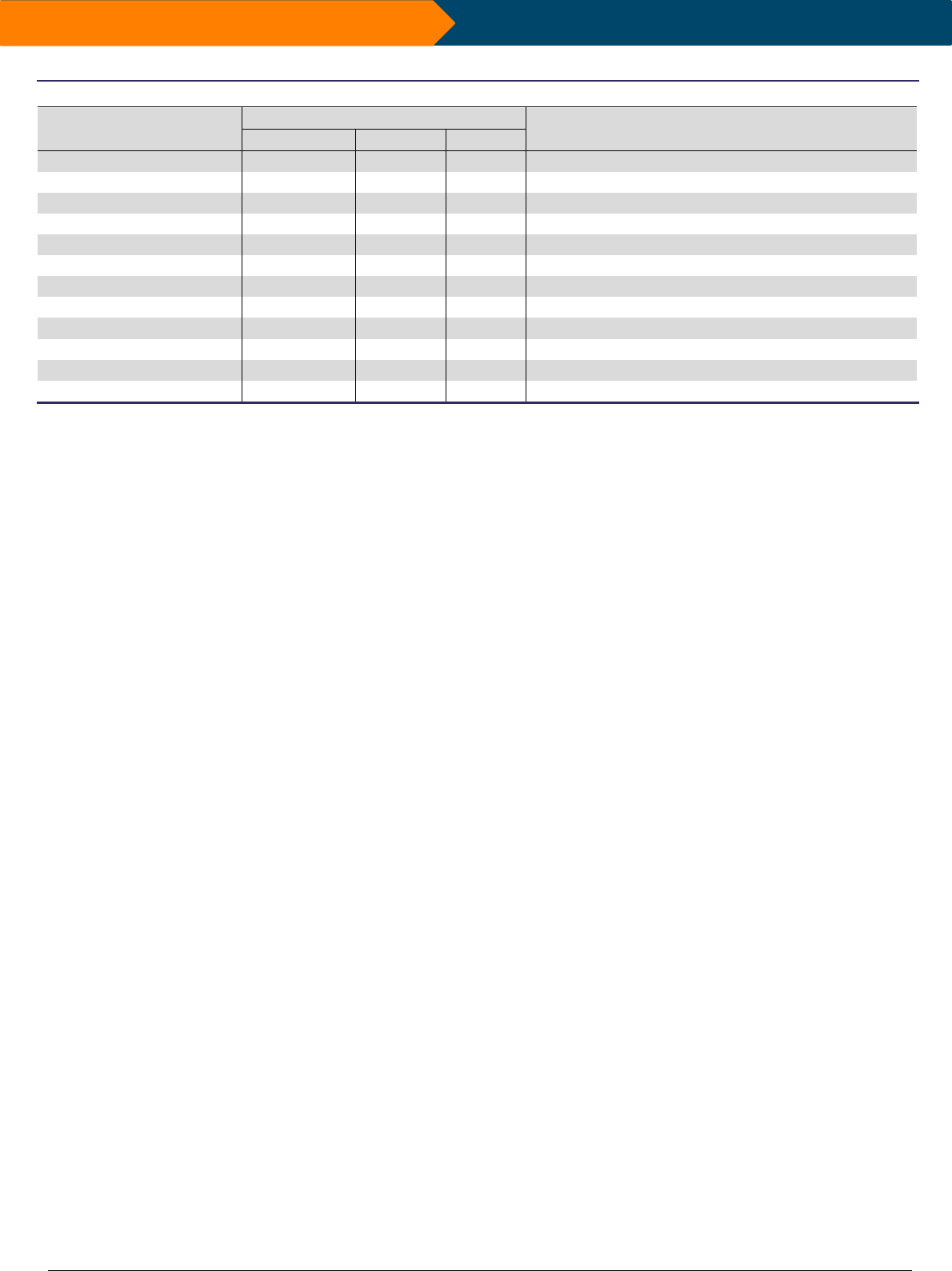

Exhibit 21: Channel checks suggest differing merchandise across stores in Kolkata, based on clientele in the local catchment area

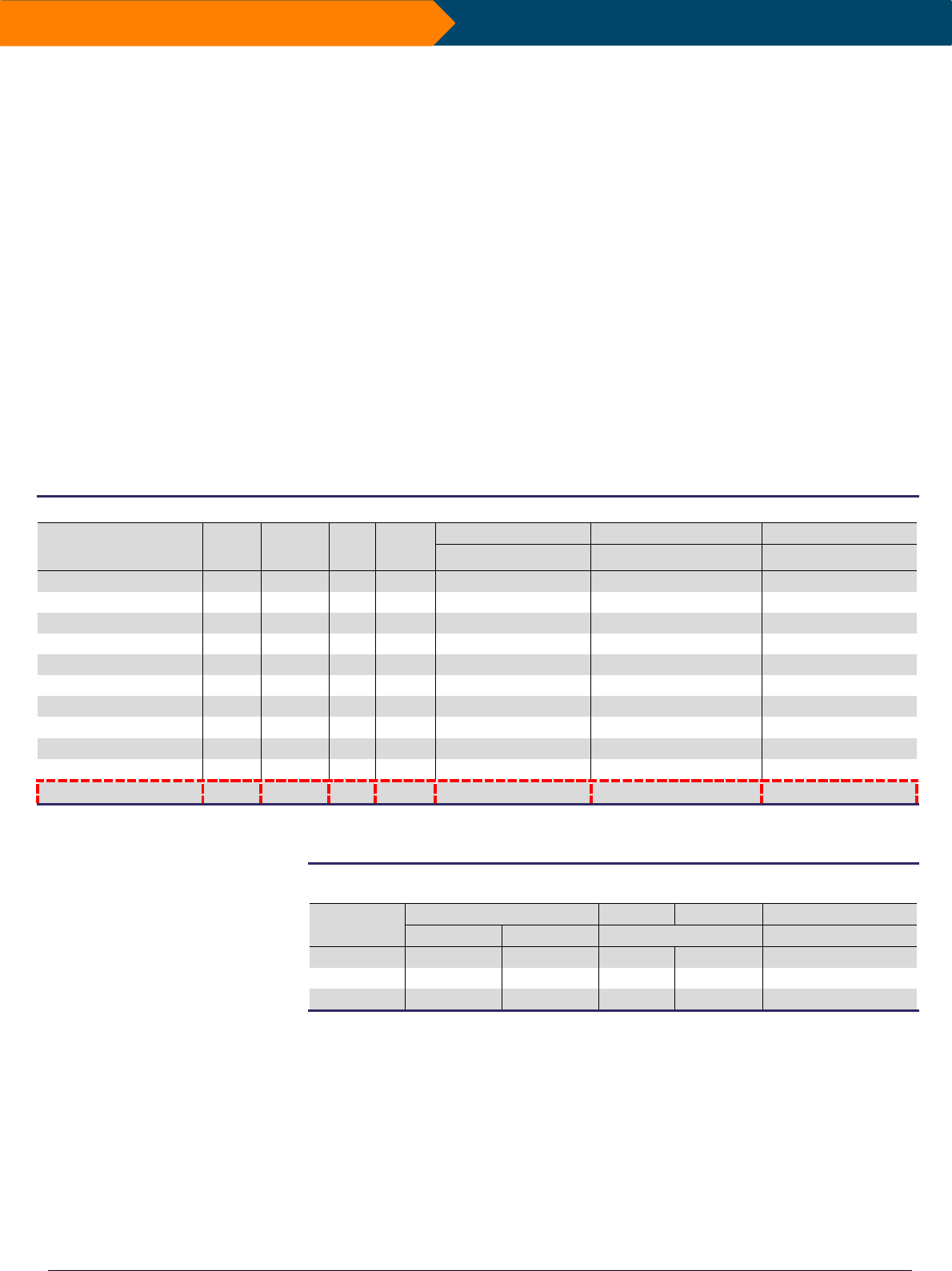

Store-level metrics

Kolkata stores

Remarks

Camac Street

Baguihati

Moulali

Store Size (sqft)

5,500

12,000

5,000

Avg. Ticket Size (ATS, Rs)

95,000

66,000

80,000

ATS differs, based on sales mix (studded/regular/wedding)

Avg. Daily Footfalls (x)

20

65

50

Conversion (%)

75

80

80

Conversions are broadly similar across stores

No. of bill cuts/month (x)

450

1,550

1,200

Bill-cuts differ, based on assortment at stores

Revenue (Rs mn)

500

1,250

1,150

Studded Mix (%)

25

15

5

Stores are targeting different mix, based on micro-markets

Gross Profit (Rs mn)

110

213

151

Gross margin (%)

22

17

13

Gross margins are different based on studded mix at stores

EBITDA (Rs mn)

50

186

129

EBITDA margin (%)

10

15

11

Inventory (Rs mn)

450

350

300

Inventory differs across stores, based on demand in markets

Source: Emkay Research (channel checks)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

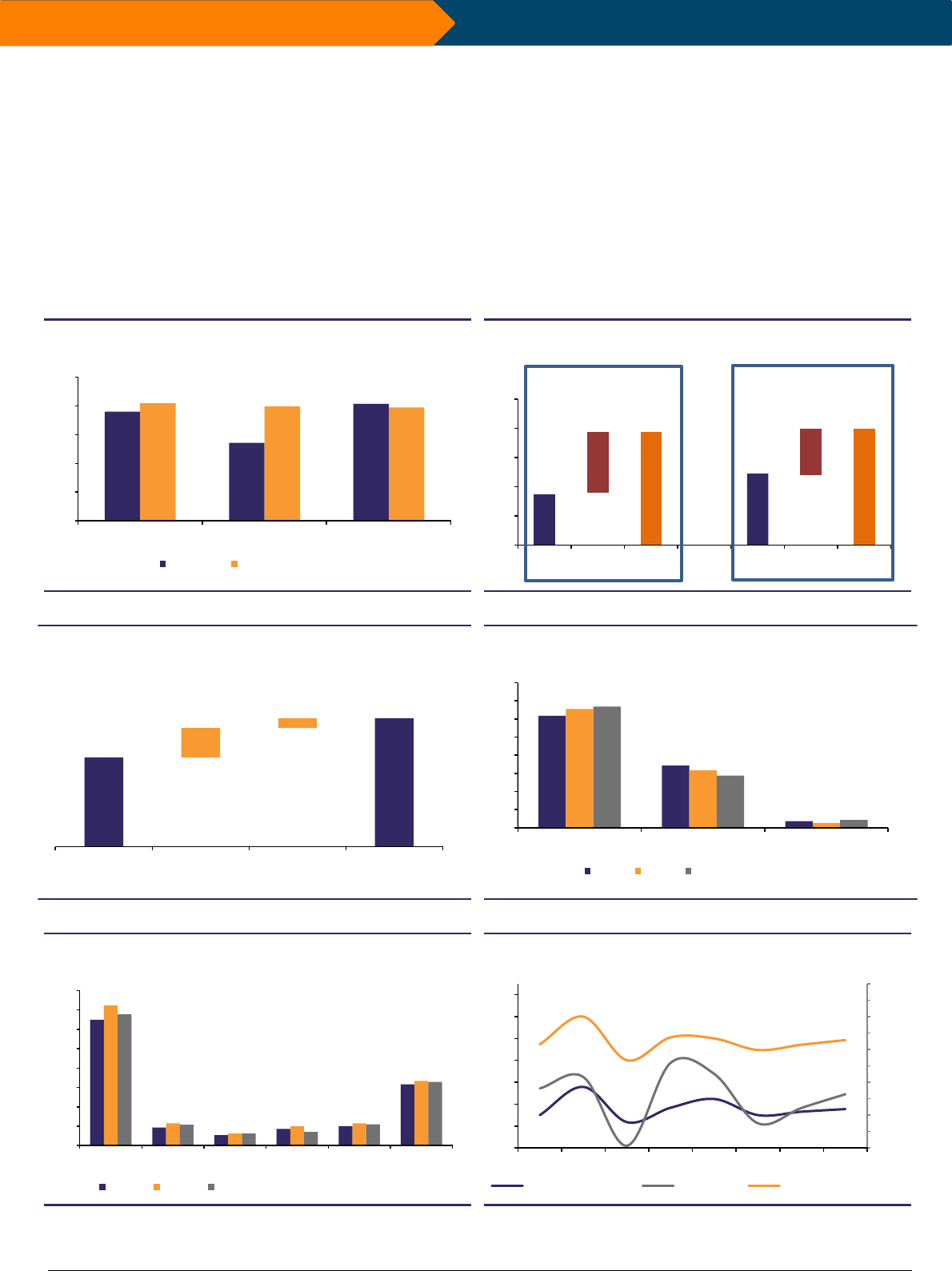

September 20, 2023 |10

Skewed EBO penetration provides a long growth runway: Senco boasts of garnering one

of the top-2 revenue shares in the eastern market, which contributes >80% to its overall

revenue. Our analysis suggests that the East is an ~Rs800bn market (~15% of overall India

market), wherein Senco has a mid-single-digit market share. Senco has strong brand strength

in the West Bengal market which has helped it to penetrate deeper with the help of franchisees.

Senco has presence in >55 cities vs. 13-30 cities for PC Chandra/Tanishq/MPJ/Anjali; presence

of other brands like Kalyan/Malabar is much lower. We expect Senco to leverage its ahead-of-

the-curve investments and continue growing strongly in the eastern region, given that market

share is still low here. Also, initial signs have been encouraging in the non-eastern regions of

Delhi-NCR/Uttar Pradesh, with stores reporting 15-20% studded mix (vs. overall mix of 10%).

Success in new regions, coupled with expansion in the East, provides a long growth runway for

Senco. Given improved access to capital, we expect Senco to increase the pace of store

additions, with 60 adds over FY23-26E on a base of 136 stores.

Franchisee model well established for Senco: Senco definitely scores higher in terms of

franchisee relationship/experience when compared with most jewelers (ex-TTAN). Of the

overall network of 136 stores (FY23-end), Senco has 61 franchise stores that contribute ~35%

to overall revenue. Most franchisees have >2 stores, highlighting long-term relationships and

satisfied franchisees. With strong brand strength in eastern India, franchisees are primarily

located in West Bengal, with inroads made in states like Orissa, Assam, Bihar and Jharkhand.

Exhibit 22: Senco leads the pack in the East, with relatively much

deeper penetration in the West Bengal market

Source: Store locators (Company websites), Emkay Research

Exhibit 23: We expect network expansion to accelerate, with 60

new additions over FY23-26, on a base of 136 stores

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 24: Majority of Senco Gold’s revenue, at ~80%, is reaped

from East India currently

Source: Senco RHP document, Emkay Research

Exhibit 25: Senco has penetrated deeper into Tier-1/Tier-2 cities,

via the franchisee route

Source: Company, Emkay Research

85

52

25 25

19

4

2

55

30

16

13

15

2

1

Senco PC

Chandra

Anjali Tanishq MPJ Kalyan Malabar

Stores (x) Cities (x)

136

196

45

15

FY23 Store

Count

COCO additions

(FY23-26)

FOFO additions

(FY23-26)

FY26 Store

Count

70

12

15

3

West Bengal Rest-East Rest-India Others , Revenue split (FY23, %)

34

30

11

12

49

0

10

20

30

40

50

60

70

Metro Tier 1 Tier 2

Company owned Franchisee owned, No. of stores (x)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |11

Increase in Franchisee mix should drive RoE improvement: Senco’s modus operandi is

to build its brand in Metros/Tier-1 cities, and then improve brand penetration through

franchisee-led expansion (asset-light) in adjacent Tier-2/3 cities. While COCO stores generate

a decent RoE of 13-14%, FOFO stores log much higher RoE, of 40-50%, due to lower invested

capital (Emkay estimate: Rs15mn for a FOFO store vs. Rs220mn for a COCO store). Working

Capital (WC) is relatively higher for the business, as the category requires larger stores holding

significant amount of high-value inventory (gold, gems and other precious metals), thereby

driving relatively-lower RoE compared with other retail formats. The format also has multiple

categories (necklace, bangles, rings and chains), requiring multiple designs to gain traction

with consumers. A significant increase in gold prices has led to incommensurate increase in

store-level revenues (vs. store inventory levels), leading to lower inventory turns in the short

term. However, RoE should further improve, as customers get accustomed to the elevated gold

rates as well as with increase in franchisee mix in the overall business. Notably, historical RoE

for Senco was higher due to inventory gains related to steep increase in diamond prices, which

are expected to normalize in coming years.

Exhibit 26: Channel-wise Unit Metrics

(Rs mn)

COCO stores

FOFO stores

Unit metrics

FY23

FY24E

FY26E

FY23

FY24E

FY26E

Revenue

368

393

421

239

279

324

Gross margin (incl. Job work; %)

18.5

17.1

17.5

6.8

5.5

5.8

Store running expenses, % of sales

5.9

5.8

5.9

0.2

0.2

0.2

Store EBITDA margin (%)

12.6

11.3

11.5

6.6

5.3

5.6

HO Costs (Ad/Employee), % of sales

3.2

2.8

2.7

5.0

4.0

3.5

EBITDA

34

34

37

4

4

7

EBITDA Margin (%)

9.3

8.5

8.8

1.6

1.3

2.1

Depreciation

2

3

3

EBIT

32

31

35

3.9

3.6

6.8

Interest Expense

8

9

8

1.1

1.3

1.4

Other Income

4

4

4

PBT

28

27

30

2.8

2.3

5.3

Tax

7

7

8

0.7

0.6

1.4

PAT

20.9

19.6

22.2

2.1

1.7

3.9

PAT margin (%)

5.7

5.0

5.3

0.9

0.6

1.2

Working Capital

183

184

189

11

12

18

Capex - Gross Assets

29

31

32

Total Invested Capital

212

216

221

11

12

18

Gross Debt

67

62

50

9

9

8

Equity

145

154

171

2

3

10

RoE* (%)

14.4

12.8

13.0

115.7

56.3

39.7

Source: Company (historicals), Emkay Research (projections); Note: RoE here will differ from the reported

RoE, as it is being calculated on gross assets (for capex) and pre-IndAS numbers

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |12

Natural gold appreciation is a big SSG lever; attractive schemes to help drive the

organized shift faster: We expect Senco to deliver strong SSG of 9-10% in the medium term,

helped by natural appreciation in gold prices, premiumization (products with higher making

charges/studded) and volume growth enabled by shift towards organized. Shift to organized

players is enabled by attractive schemes, hallmarking, skilled employees and improved

availability of capital for organized players (equity/Gold Metal Loans/franchisees). Key ATL

initiatives undertaken by Senco to drive this shift include rationalization of gold prices, event-

based schemes on Gold exchange (Zero deduction) and strong IRRs on Gold deposit schemes

(Suvarna Yojana). Among BTL initiatives, Senco does cross-marketing with other retail formats

(like Pantaloons) and proactive reach out to customers in local catchments/tourist hotspots.

Further, Senco is expanding its customer base via the D’Signia and Everlite store formats,

targeting affluent/GenZ customers (4-5% of FY23 sales). Filling of key portfolio gaps should

also drive a strong SSG for Senco.

Exhibit 27: Senco offers attractive exchange offers (nil deduction) from time to time; such offers

help customers during an elevated gold-price environment

Source: Social marketing handles, Emkay Research

Exhibit 28: Senco undertakes ATL activities (celebrity endorsements)

to create desire & aspiration in consumers’ minds

Source: Social marketing handles, Emkay Research

Exhibit 29: Event-specific offers are targeted to accelerate shift

towards organized players

Source: Social marketing handles, Emkay Research

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |13

Peer Comparison

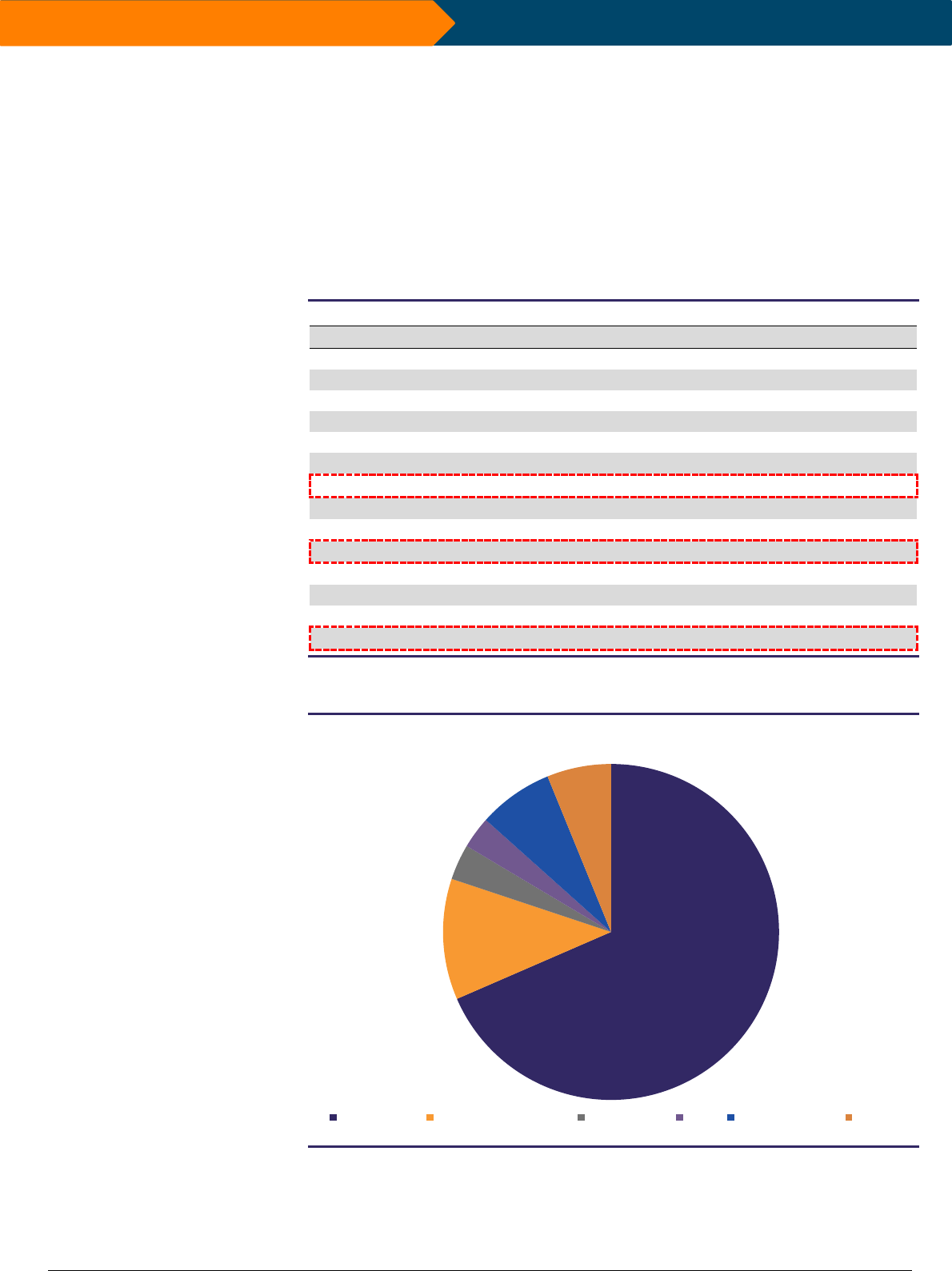

Strong growth delivery; returns profile matches Kalyan’s, is better than others’:

Senco comes with a heritage of strong growth performance and has delivered a strong ~19%

revenue CAGR over FY20-23. Given that preference is relatively higher for high-margin hand-

made jewelry in eastern India, margin for Senco is better vs. South-based jewelers like

Thangamayil/Kalyan. However, revenue/store is relatively lower for Senco due to lower per-

capita consumption in eastern India (200g/wedding vs. 300-350g/wedding in southern India).

But the same gets adjusted with the lower inventory requirement at the store level. Better

margins help Senco to still command a better ROCE profile vs. peers (ex-TTAN). TTAN clearly

enjoys best profitability/return ratios among jewelry retailers, on account of 2-3x margins,

helped by stronger brand and higher studded mix. In addition to the superior margins, TTAN’s

superior brand strength helps it to enjoy better traction among franchisees and attain deeper

penetration with presence in 251 cities through 423 stores.

Senco’s focus remains on improving studded mix: Studded mix is lower at 10-15% for

most jewelry retailers compared with 25-30% for TTAN/Kalyan. In our view, Senco’s studded

mix has, so far, been lower due to higher mix of plain gold jewelry in the eastern market.

However, studded mix should increase with increase in mix of non-eastern markets in overall

revenue, as Senco is already seeing higher studded mix at 15-20% in markets like Delhi.

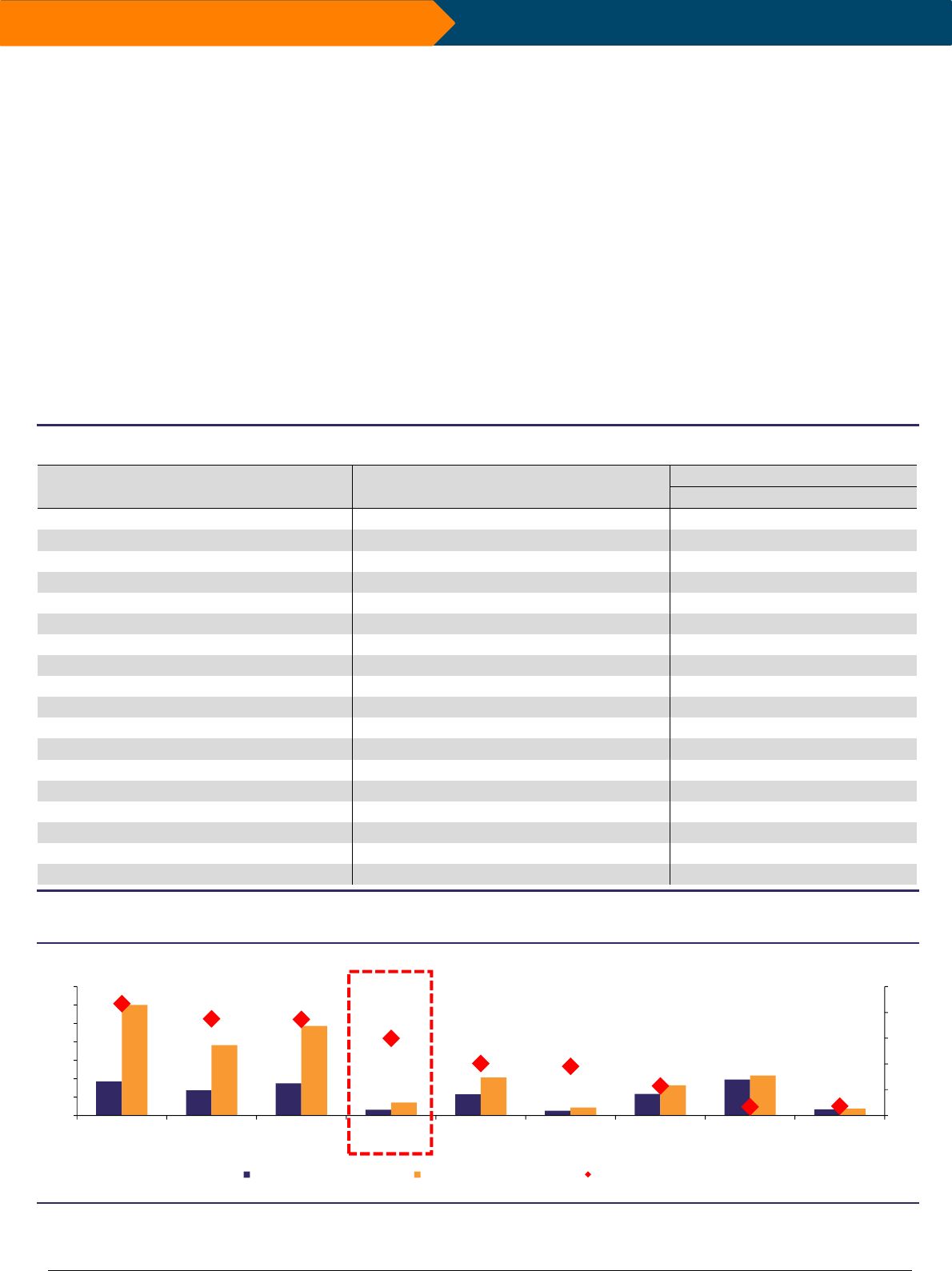

Exhibit 30: Comparison across key parameters for listed jewelry retailers

Company name

TTAN*

Senco

Thangamayil

KALYAN

TBZ

P&L Comparison

Revenue CAGR (3Y; %)

22

19

23

12

10

Brand Strength

Franchisee Arrangement

Number of Stores (FY23-end)

423

136

53

149**

32

Avg. Bill Size (Rs)

120K

65K

NA***

75K

125K

Revenue/Store (Rs mn)

900

375

750

850

780

Studded Mix

30%

11-12%

10%

27-28%

20%

Gross margin

27-29%

17-18%

9-10%

15-16%

12-14%

Store EBITDA margin

22-23%

10%

4-5%

8-9%

5-6%

Depreciation (Rs mn)

4.0

2.5

4.0

4.5

5.0

EBIT margin

22%

9%

3%

7%

4%

Balance Sheet Comparison

WC/Store (Rs mn)#

360

180

180

300

300

Capex/Store (Rs mn)

40

25

40

45

50

Invested Capital/Store (Rs mn)

400

205

220

345

350

Store ROCE

50%

17%

12%

18%

10%

DuPont Analysis

Net Profit margin

IC turnover

Leverage

Overall

Source: Emkay Research (channel checks); Note: *TTAN metrics are indicative of COCO stores and based on channel checks; **India store count for Kalyan,

***Data not available, #WC/Store includes Gold metal loan and other deposits/margin money

.

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |14

Exhibit 31: The East market has relatively lower per-capita consumption currently, thus providing

scope for continued growth in the region

Source: Kalyan RHP document

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |15

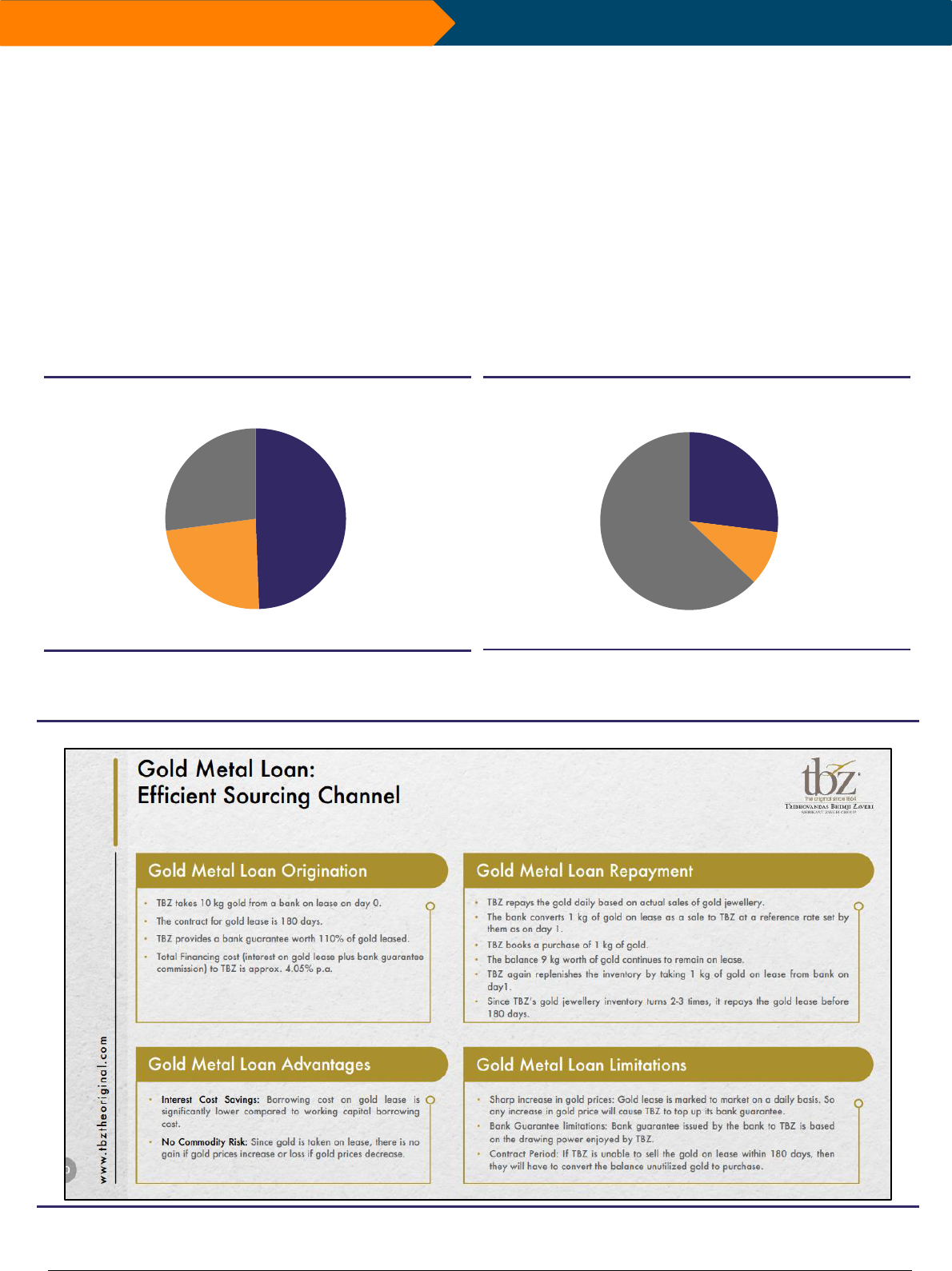

Follows hygiene practices for sourcing; stated policy of 50% hedging Gold exposure:

Sourcing of Gold inventory (~80% of total inventory) is mainly through: i) gold metal loans

(50%); ii) bullion dealers/trading agents (25%), and iii) gold exchange programs (25%). Senco

has credit limit of ~Rs20bn, 75% of which is for gold-metal loans (30% consortium and rest

outside consortium) and the balance is for cash-credit (CC)/WC demand loan (WCDL)/Letter of

credit (SBLC). Notably, non-consortium loans require 110% margin. However, in our view, a

non-consortium loan is still a better way to fund growth (compared with equity), as rate of

interest on margin money is higher than the cost of interest on gold metal loan.

Gold-metal loans a natural source of hedging: As of FY23-end, Senco has availed credit

facility of Rs11.6bn, of which ~Rs6bn is gold-metal-loan (~50% of gold inventory and ~35%

of overall inventory), with the remaining used for CC/WCDL/SBLC. Gold metal loans act as a

natural hedge against gold price volatility, as purchase price is fixed on the day of gold sale to

consumers, thereby protecting 50% of gold inventory from price volatility. While the stated

policy asks for 50% hedging, Senco hedges 80-90% in its normal business routine, by entering

into forward contracts/hedges on the rest of the inventory.

Exhibit 32: Almost 50% sourcing of gold is hedged through Gold-

metal-loans

Source: Company, Emkay Research

Exhibit 33: Mix of sales channels for Senco

Source: Emkay Research

Exhibit 34: Process for sourcing through Gold metal loans (GML; interest rate for GML sourcing is 3-3.5% for Senco Gold)

Source: TBZ investor presentation, Emkay research

Gold Metal

Loan, 49%

Bullion/

Trading

Jewelry,

24%

Gold

exchange,

27%

Annual Gold Sourcing (%)

Gold

Exchange,

27%

Jewelry Purchase

Schemes, 10%

Spot Sales,

63%

Annual Sales Mix (%)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |16

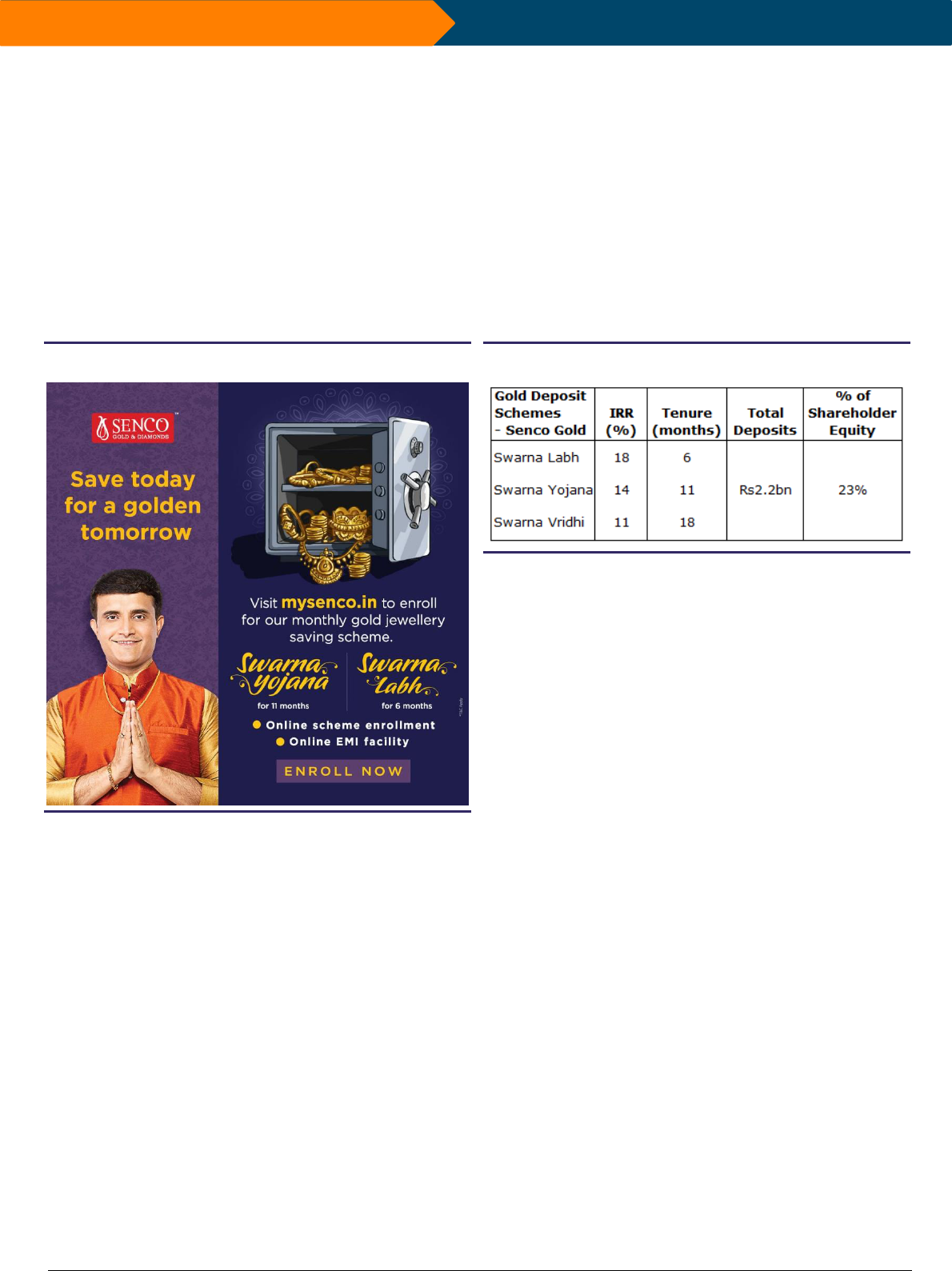

Jewelry purchase schemes: Cheaper source of capital; share increase provides scope

for RoE improvement

In our view, Gold deposit schemes are a relatively cheaper source of capital, albeit the amount

of overall deposit that can be raised from consumers is restricted to 25% of overall shareholder

equity via regulations. Along with working-capital funding, such schemes also help to increase

the frequency of purchase as they guarantee attractive IRRs to consumers. Though guaranteed

IRRs are in the 12-15% range, in terms of purchase values across players (10-12-month

schemes), it is to be noted that companies are incurring only associated COGS (80-85% of

purchase value), thereby making it a relatively cheaper source of capital.

Senco has three deposit schemes: Swarna Labh, Swarna Yojana and Swarna Vridhi, which call

for monthly instalments for 6/11/18 months and provide IRR of 18%/14%/11% to consumers,

in terms of purchase value. Lower tenure schemes provide higher IRR as it increases the

frequency of deposits and also helps to raise more capital to fund growth.

Exhibit 35: Jewelry purchase schemes are a cheaper source of

capital and improve the frequency of purchase by customers

Source: Social marketing platforms, Emkay Research

Exhibit 36: Senco provides an IRR of 18%/14%/11% to

consumers, in terms of purchase value

Source: Company website, Emkay Research; Note: Discount given is equal

to IRR on purchase value, and is over & above the prevailing discount

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |17

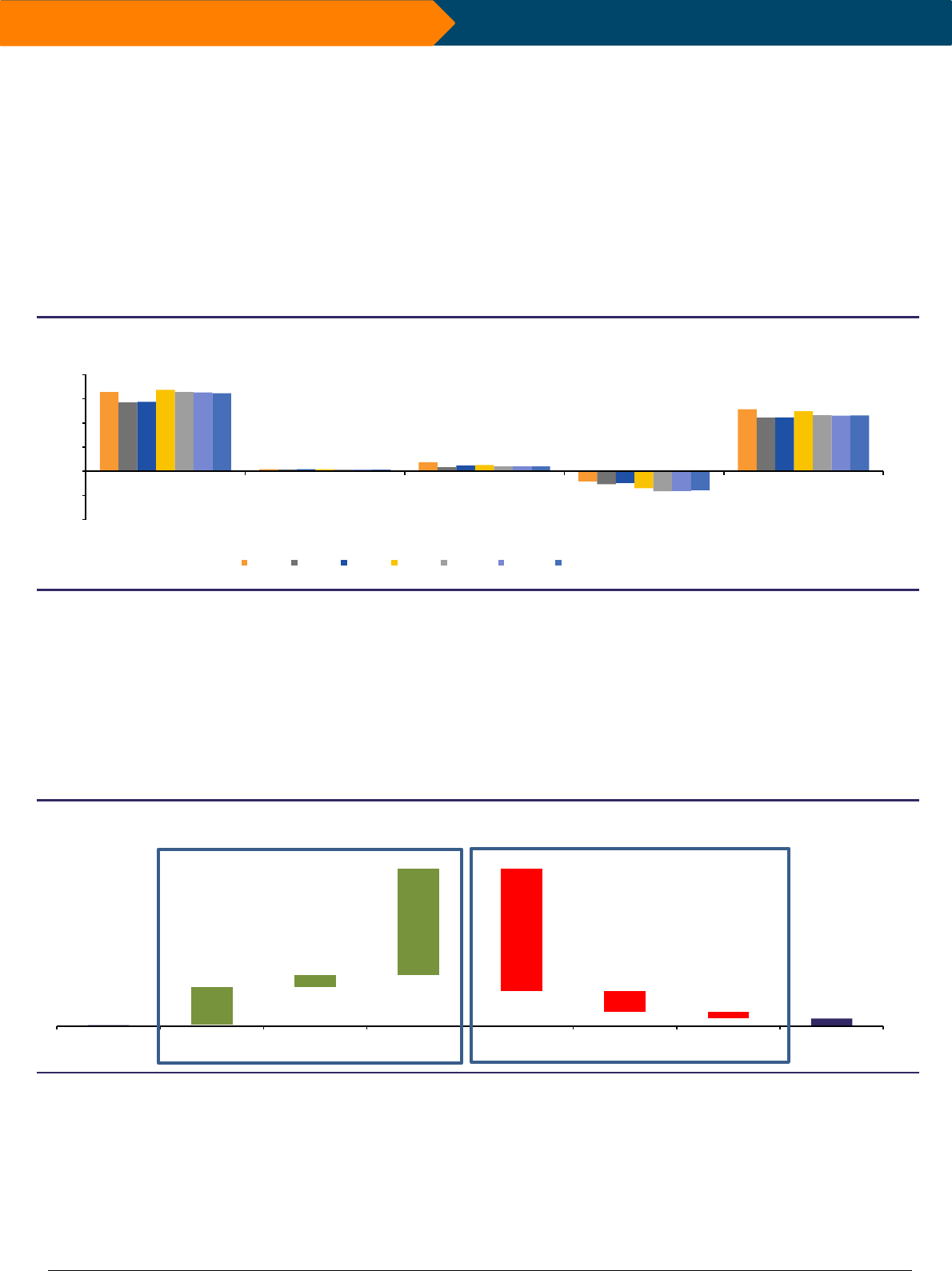

Financials: Accelerated expansion and strong SSG to

drive >20% PAT CAGR

Given significant consumption thrust towards organized retailers (trust, service, marketing),

Senco’s focus remains on revenue growth vs. margin gains or working capital reduction in the

near future. Our investment thesis on Senco rests on ~20% revenue/EBITDA/PAT CAGR in the

medium term, enabled by strong SSG, in a high single-digit, and healthy network expansion

of 12% every year. After an initial dip in margin/RoE, on account of aggressive schemes to

recruit new customers, absence of diamond-inventory gains in FY24 (vs. FY23) and equity-led

expansion, we expect margins/RoE to continue on an improving trend thereafter, aided by

operating leverage and utilization of balance-sheet cash. With majority expansion through

capital-intensive COCO stores (Rs200mn/store) over FY23-26E, free-cash-flow-to-equity

(FCFE) is expected to remain negative over this period, post which there should be a significant

improvement in cash flows.

Exhibit 37: We expect revenue/EBITDA/PAT CAGR of ~20% over

FY23-26E, largely led by topline growth and stable margins

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 38: We expect topline CAGR of 20% to be supported by

9%/12% SSG/store addition CAGR

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 39: Expect expansion to be led by capital-intensive COCO

stores over FY23-26E, post which FOFO additions should pick-up

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 40: Higher COCO additions should drive continued improvement

in revenue mix for this channel over FY23-26

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 41: Operating leverage to help margin recovery despite

lower gross margin, on absence of any one-off in FY24

Source: Senco RHP document (historicals), Emkay Research (projections)

Exhibit 42: We expect ROE to recover to the mid-teens, on margin

recovery and utilization of balance-sheet cash

Source: Senco RHP document (historicals), Emkay Research (projections)

19

14

20

20

20

20

0

5

10

15

20

25

Revenue EBITDA PAT

FY20-23 FY23-26E, CAGR (%)

9

10

19

12

8 20

0

5

10

15

20

25

Store

CAGR

SSG

CAGR

Revenue

CAGR

Store

CAGR

SSG

CAGR

Revenue

CAGR

FY20-23 (%)

FY23-26E (%)

136

196

45

15

FY23 Store

Count

COCO additions

(FY23-26)

FOFO additions

(FY23-26)

FY26 Store

Count

62

34

4

65

32

3

67

29

4

0

10

20

30

40

50

60

70

80

Owned Store Franchisee Store Others

FY20 FY23 FY26E, Rev. mix (%)

13.0

1.9

1.1

1.7

2.0

6.3

14.5

2.3

1.2

2.0

2.3

6.7

13.6

2.2

1.2

1.4

2.2

6.6

0

2

4

6

8

10

12

14

16

Gross (%) Employee (%) Rent (%) Ad (%) Others (%) EBITDA (%)

FY19 FY23 FY26E, (% of sales; Pre-IndAS116)

13.0

15.6

12.4

13.7

14.5

13.0

13.3

13.6

15.4

16.5

10.2

17.8

16.8

12.2

13.7

14.9

6.3

8.0

5.3

6.7

6.7

6.0

6.3

6.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

10

12

14

16

18

20

22

24

FY19 FY20 FY21 FY22 FY23 FY24E FY25E FY26E

Gross Margin (LHS, %) RoE (LHS, %) EBITDA Margin (RHS, %)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |18

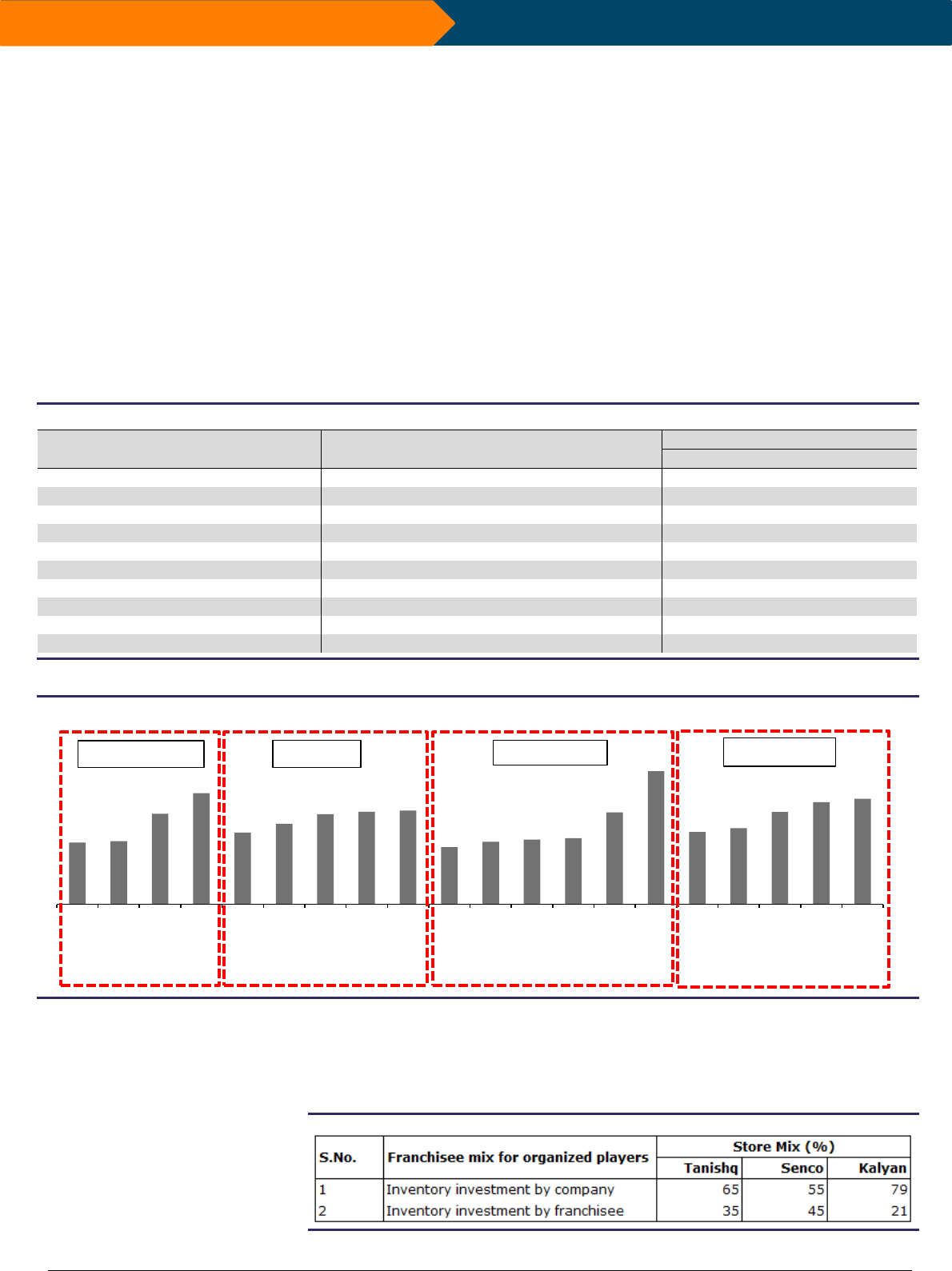

Expect stable working capital on strong plans for non-East expansion: Working capital

is the most crucial investment in the jewelry business and forms >90% of invested capital for

Senco. However, the inventory liquidation risk is relatively lower, as the WC constituents

(gold/other precious metals) are readily monetizable and Senco hedges ~80% of overall gold

inventory to remain protected from the volatility in gold prices. Notably, the stated policy is

to hedge >50% of overall gold inventory, but the company hedges 80-90% as a

normal business practice. Typically, a COCO store requires WC investment of Rs200mn,

which is a combination of Rs250mn inventory (Store + Head Office), Rs50-60mn deposits

(margin/GML) and credits from gold deposit schemes (Rs30mn)/gold metal loans (Rs90mn).

We expect working capital to normalize to ~115 days over FY23-26E, led by the recent

moderation in gold prices and other operational efficiencies. Post FY26, working capital should

remain on an improving trend, led by an asset-light franchisee-led expansion.

Exhibit 43: We expect WC to remain stable at ~115 days over FY24-26E, post a reduction in inventory days in FY24 due to the recent

correction in gold prices

Source: Senco RHP (historicals), Emkay (projections), *Please note ‘other net Assets’ include Gold metal loans and other deposits/margin money

Internal accruals to service 80% of the required growth capital over FY23-26E: Given

focus on brand creation through company-owned stores in new territories in the North and East

India, we expect initial expansion to be through capital-intensive company-owned stores

(COCO model; Rs200-220mn investment per store). Post establishment of a strong brand in

new territories, we expect further expansion to be driven by asset-light franchisee stores (FOFO

model), significantly aiding free-cash-flows for the company. We expect Senco to open 45

COCO stores over FY23-26E, which will entail capex/working capital investment of ~Rs10bn.

We expect internal accruals to service 80% of the required growth capital, while the balance

20% should be serviced by the recent equity capital raise.

Exhibit 44: Senco will require Rs10bn growth capital to open 45 COCO stores over FY23-26, of which 80% would be serviced by internal

accruals

Source: Senco RHP document (historicals), Emkay Research (projections)

164

4

19

-21

128

143

4

8

-27

111

144

4

12

-24

112

169

4

13

-35

125

164

4

10

-41

116

163

3

10

-41

116

161

3

10

-39

116

(100)

(50)

0

50

100

150

200

Inventory days Receivables days Payables days Other net Assets days WC days

FY20 FY21 FY22 FY23 FY24E FY25E FY26E (Number of Days)

0.1

0.6

2.7

0.8

7.5

8.7

1.5

0.5

Cash (FY23) Equity Raise (FY24) Debt Raise (FY23-

26)

CFO (before WC

changes)

WC Investments

(FY23-26)

Capex (FY23-26) Dividend (FY23-26) Cash (FY26)

Sources of Funds (Rs bn)

Usage of Funds (Rs bn)

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |19

Valuations: Trading at steep discount to peers; Consistent

delivery on our expectations provides scope for re-rating

We expect Senco to deliver ~20% revenue/PAT CAGR over FY23-26E which is in line with that

of some of the best-performing companies in our coverage universe. PAT CAGR would largely

be led by revenue growth, along with our expectation of stable EBITDA margin. Medium-term

growth prospects are also healthy, as scope to increase market share remains healthy in the

current geography of operations and focus efforts are afoot to expand in the adjacent regions

of the Northeast (Assam, Tripura), East (Bihar/Jharkhand/Orissa) and North (Delhi-NCR/UP).

We expect the high-teens earnings CAGR to continue over FY26-36E as well.

We believe RoE would recover to mid-teen levels post the near-term moderation, due to

normalization of gross margin on absence of diamond inventory gains. However, the RoE should

keep inching up with increase in franchisee mix, improvement in asset turns with customers

adapting to the elevated gold prices and increase in mix of jewelry purchase schemes.

Despite similar growth prospects, Senco is trading at ~40% discount to Kalyan Jewelers. While

Kalyan has relatively better brand strength for faster Pan-India expansion, we believe such a

steep discount is unwarranted and provides scope for re-rating, as Senco delivers on our

expectations going ahead. Given the recent listing and higher revenue concentration from

eastern markets currently, we are conservatively valuing the company at 20x Sep-25E EPS

and recommend BUY on the stock, with Sep-24E TP of Rs630/share.

Exhibit 45: Economic peer comparison

Company name

Price

(Rs)

Mcap

(Rs bn)

Reco

Target

Price

(Rs)

EPS (Rs)

P/E (x)

EV/EBITDA (x)*

FY23E

FY24E

FY25E

FY23E

FY24E

FY25E

FY23E

FY24E

FY25E

Titan Company

3,340

2,965

Hold

3,000

39.8

50.3

61.3

83.8

66.4

54.5

56.6

45.4

37.4

Varun Beverages

912

1,185

Buy

970

16.0

19.8

24.9

56.9

46.0

36.6

32.8

27.3

23.0

Page Industries

40,326

450

Sell

37,100

519.8

678.9

818.3

77.6

59.4

49.3

49.3

38.8

32.7

Jubilant FoodWorks

539

356

Sell

420

6.0

8.8

11.0

89.7

61.1

49.0

28.1

21.9

18.5

Devyani International

210

254

Hold

180

1.5

2.8

3.9

139.2

75.4

53.9

33.2

24.8

19.3

ABFRL

226

214

Hold

215

-5.3

-3.7

-2.2

-42.6

-60.9

-101.0

16.0

10.8

8.5

Westlife Development

980

153

Buy

1,035

10.4

12.9

17.1

94.5

76.1

57.1

31.0

26.2

21.4

Sapphire Foods

1,453

93

Hold

1,400

22.6

32.6

44.1

64.3

44.5

32.9

16.5

12.1

9.7

Go Fashion

1,361

74

Buy

1,430

19.4

26.4

34.0

70.2

51.5

40.0

27.1

20.7

16.5

Ethos

1,712

40

Buy

1,770

31.8

46.1

57.7

53.8

37.1

29.7

25.6

18.1

14.6

Senco Gold

473

37

Buy

630

21.6

27.6

35.0

21.9

17.1

13.5

11.7

9.3

7.5

Source: Company, Emkay Research; *Post IndAS-116 EBITDA

Exhibit 46: Senco currently trades at ~40% discount to Kalyan, despite similar revenue growth

prospects

Company (%)

FY23-26E CAGR

FY23

FY26

1-Yr fwd P/E (x)

Revenue

PAT

ROE

(Sep-24E EPS)

TTAN

18.0

18.5

30.9

26.5

74

KALYAN

23.0

31.4

11.9

16.2

33

SENCO

20.4

19.7

16.8

14.9

19

Source: Bloomberg estimates (Kalyan), Emkay Research

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |20

Potential upsides

Case-1: Improvement in credit rating and higher gold deposits can help to

increase access to low-cost capital and improve ROE: The cost and availability of

capital (gold metal loans/WCDL/CC/SBLC) depend on the assigned credit ratings by credit

agencies. Senco’s fund-based working capital facilities have been assigned a rating of

‘ICRA A’ with a stable outlook for long-term facilities and a rating of ‘ICRA A2+’ for short-

term facilities. An improvement in these ratings can lead to reduction in cost of capital,

thereby helping to improve the profit growth and ROE for Senco, in our view.

Case-2: Better margin/WC performance should help Senco to get re-rated: Given

expansion in the non-East regions through COCO stores, our FY23-26E margin is

conservative over FY23-26E. WC forms a significant part of the capital invested in the

business (~90%). We are not building-in any significant moderation in WC in our

estimates, and a better performance can significantly improve the RoE for Senco. Decline

in gold prices remains a big lever for WC reduction in the business.

Potential downsides

Case-3: Senco is venturing into new geographies of operations which may

require higher-than-expected time and investments: Senco is venturing into non-

eastern geographies to replicate its success in East India. While we are reasonably

confident of long-term success, given high share of unorganized players, an increase in

organized competition can delay the expected growth or can require more investments.

Case-4: Increase in Custom Duty: We have seen regulatory interventions like increase

in custom duty to reduce the fiscal deficit, in an uncertain macro environment. Such

actions push up the gold price, thereby weakening the demand environment for a short

period of time. While the GoI may chose this route for short-term fiscal disciplines, we do

not see risk of sustained increase in custom duty, as such actions lead to more incentives

for flow of smuggled gold into the country.

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |21

Appendix

Senco Gold is a Pan-India retail jewelry player with a history of more than five decades and

has a fourth-generation entrepreneur in the jewelry industry as the Promoter. It is the largest

organized jewelry retail player in the eastern region of India, based on number of stores. The

company primarily sells gold and diamond jewelry as well as jewelry made of silver, platinum

and precious & semi-precious stones and other metals. Other offerings include costume

jewelry, gold & silver coins, and utensils made of silver. Company offers a large variety of

designs of handcrafted jewelry, most of which are designed and manufactured in-house by own

designers, in close collaboration with skilled local craftsmen (generally termed karigars) in

Kolkata and across the country. Machine-made light weight jewelry in gold and diamonds is

also manufactured at Company’s manufacturing facility.

Exhibit 47: Senco Gold’s major events and milestones over the years

Year

Description

1994

Company incorporated by merging the existing proprietary and partnership

2000

Opened the first franchisee in Durgapur (West Bengal)

2002

Largest showroom with an area of ~8,000sqft launched in Kolkata (Moulali), West Bengal

2010

Adopted franchisee route to expand outside WB by opening first showroom in Assam

2012

Opened first showroom in Jharkhand under the franchisee model

2013

Entered northern region by opening the Lajpat Nagar showroom in Delhi

2014

Total number of showrooms cross 50; revenue crosses INR10bn

2015

Raises INR800mn equity from SAIF Partners India IV limited (now Elevation Capital)

2016

Entered southern region by opening a showroom in Bangalore; introduced the Everlite brand

2018

Revenue crossed INR20bn

2020

Crossed the 100-showrooms mark; launched 2 D'Signia showrooms targeting the elite class

2021

Awarded the second most-trusted jewelry brand by TRA and ET Trusted Brands

2022

Raises INR750mn equity from OIJIF II

2023

Revenue crossed INR40bn; listed on the NSE and BSE

Source: Company

Exhibit 48: Shareholding pattern

Source: Company, Emkay Research

Promoters,

68.5

Saif Partners

(PE), 11.6

OIJIF (PE), 3.4

FIIs, 3.1

Mutual

Funds,

7.2

Others

, 6.2

Promoters Saif Partners (PE) OIJIF (PE) FIIs Mutual Funds Others

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |22

Exhibit 49: A brief about Senco Gold’s key management team

Name

Designation

Description

Ranjana Sen

Chairperson

Ranjana Sen, aged 64 years, is the Chairperson and Whole Time Director of the Company. She holds a bachelor’s degree

in arts from the University of Calcutta. She has been associated with the Company since its incorporation and has over

29 years of experience in the jewelry industry

Suvankar Sen

Managing

Director/Chief

Executive

officer

Suvankar Sen, aged 39 years, is a Whole Time Director designated as MD and CEO of the Company. He holds a degree

in bachelors of Science with Honors in Economics from St. Xavier’s College, University of Calcutta. He also holds a post-

graduate diploma in business management from the Institute of Management Technology, Ghaziabad. He has been

associated with the Company since 2005 and has over 17 years of experience in the jewelry industry

Sanjay Banka

Chief Financial

Officer

Sanjay Banka has been associated with the Company since December 21, 2020. He is a fellow member of the ICAI and

ICSI. He is also a member of All India Management Association and Chartered Institute of Securities and Investment,

United Kingdom. He has over 20 years of experience in the field of banking, corporate finance, company secretary,

business strategy, M&A, taxation, IT implementation and treasury

Surendra Gupta

Company

Secretary &

Compliance

Officer

Surendra Gupta heads the secretarial department and joined Senco on May 22, 2013. He holds a bachelors’ degree in

commerce from the University of Calcutta and a L.L.B. degree from Magadh University. Further, he holds a degree in

master of Business laws from National Law School of India University. He is a member of the Institute of Company

Secretaries of India. He has over eight years of experience in the jewelry industry

Source: Senco Gold RHP document

Exhibit 50: Senco has invested to build a solid senior management employee base, to deliver a strong growth trajectory

Source: Senco RHP document

This report is intended for [email protected] use and downloaded at 09/21/2023 11:48 AM

Senco Gold (SENCO IN)

India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com and Bloomberg EMKAY<GO>.Please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research

analyses may only be distributed to Institutional Investors, Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore.

September 20, 2023 |23

Senco Gold : Consolidated Financials and Valuations

Profit & Loss

Y/E Mar (Rs mn)

FY22