1

Supply/Availability of Wholesale Funds for MFIs in Nepal:

Challenges and Problems

A draft paper prepared for the Microfinance Summit Nepal 2010

(14-16 February, 2010)

Kathmandu, Nepal

By

Nirdhan Utthan Bank Ltd.

Siddharthnagar, Rupandehi

February, 2010.

2

Supply/Availability of Wholesale Funds for MFIs in Nepal:

Challenges and Problems

Abstract

This paper intends to explore different aspects of supply of wholesale funds and the threat of

drying up the resources and probably the sustainable solution: saving mobilization from the

general public.Study finds Nepalese microfinance institutions are getting wholesale funding from

commercial sources under deprived sector lending scheme and from specialized wholesale

institutions. The deprived sector lending provision has played a very big role to promote and

develop microfinance industry. Since the scope of deprived sector is being made broader,

available funding under deprived sector lending scheme is diverted to Youth Self Employment

programme, funding for growing Nepalese microfinance sector is getting drier slowly. MFIs are

in rush to catch the scarce resources and the cost of fund is increasing. In this context, public

deposit could be the last resort to microfinance institutions, however, deposit mobilization is not

so easy task. Besides mobilizing deposit from the public deprived sector lending scheme is

needed for MFIs for many years to come. NRB needs to permit MFIs setting stringent criteria

and limits to mobilize deposits from the public.

3

1.0 Background

Microfinance is often defined as financial services for poor and low income clients. It is a

package of financial services for individuals, families or entrepreneurs excluded from traditional

or commercial financial system. It is the broad range of financial services such as loans, deposits,

payment services, money transfer and micro insurance to poor and low income households and

their microenterprises.

More broadly, microfinance refers to a movement that envisions a world in which poor and low

income households have permanent access to a range of high quality financial services to finance

their income- generating activities, stabilize consumption, and protect against risks. These

services are not limited to credit, but include savings, insurance and remittances.

In Nepal, micro finance institutions (MFIs) are working as regulated micro finance development

banks (MFDBS),not-for-profit organizations as financial intermediary non-governmental

organizations (FINGOs), Savings and Credit Cooperatives (SACCOS), and self-help groups. The

microfinance business is becoming a for-profit business with strong social motives. The

institutional sustainability and professionalism are getting importance in microfinance field

nowadays. Since the microfinance institutions mobilize savings only from the members, they

lack sufficient funding for on-lending. The common sources of financing are the equity, savings,

borrowings and grants.

1.1 Objectives

The broad objective of the paper is to explore different aspects of wholesale funding and

challenges due to the drying up resources and recommend the probable solution. To achieve this

goal following specific objectives were analyzed:

• An overview on current pattern of financing mix,

• Analysis of supply and use of current funding,

• Analysis of growth trend and demand forecasting

• Analysis of expected supply and the gap

• Analysis of probable sources to meet the gap.

1.2 Methodology

This paper is prepared based on analysis of secondary data from various sources. Various

literature were studied . Among them the major are the annual reports of Nepal Rastra Bank

(NRB), Rural Microfinance Development Centre (RMDC), Sana Kisan Bikas Bank Ltd.

(SKBBL) and many Microfinance Development Banks (MFDBs). Besides annual reports and

other publications of MFDBs, FINGOS, SACCOS were studied. Legal documents like Bank and

4

Financial Institution Act, 2006, various circular and directives, policies of NRB were studied.

The websites of NRB, RMDC, SKBBL, MIFAN, GON/DOC were visited to get needed

information. Growth trend was analyzed to forecast the demand. The supply side was analyzed

by reviewing the available funds under deprived sector lending scheme as well as wholesale

lending scheme.

2.0 Review of Literature

As per NRB’s licensing policy the microfinance development banks which fall under Class “D”

financial institution as per Bank and Financial Institution Act, 2006 needs to have at least Rs. 10

million as paid-up capital to operate in 3 districts, Rs. 20 million to operate in 10 districts, Rs 60

million to operate in a region and Rs. 100 million to operate at national level. Out of their paid

up capital at least 30 percent should be sold to general public. FINGOS and SACCOS are

allowed to work in one district at the beginning and later their working districts are added after

complying the directives from NRB. They must maintain positive net worth.

In Nepal, MFIs are allowed to mobilize savings only from their members/ clients. They cannot

accept deposit from the general public. Most MFDBs are adopting mandatory and voluntary

saving schemes. Under mandatory savings the clients need to deposit certain amount in their

regular meetings and certain percentage of loan amount (ranging 3 to 5 percent) is also deducted

and deposited in the same account. Under voluntary savings, the clients can deposit any amount

they can. Some MFIs are mobilizing savings in the form of contractual savings like pension

savings Chimmek Bikas Bank Ltd. and others. Generally, the saving balances finance about one-

third of their loan portfolio.

As per article 47 sub-article (7) (j) of Bank and Financial Institution Act, 2006 the class “D”

microfinance development banks can collect and pay back savings with interest or without

interest subject to limit prescribed by Nepal Ratra Bank (NRB).

The main source of wholesale funding is the commercial banks. They provide wholesale funding

to MFIs under deprived sector lending scheme. As per NRB directives, deprived sector lending is

the directed mandatory lending under which commercial banks (class “A” financial institutions)

need to lend at least 3 percent of their portfolio to deprived sector, the same is 1.5 percent for

class “B” development banks and 1.5 percent for class “C” finance companies. To lend under

deprived sector, a financial institution can disburse small loans directly. NRB has given option to

lend to MFIs or invest in the equity of such MFIs.

5

3.0 Data Presentation and Analysis

3.1 Savings to Loan ratio

MFIs are characterized with low capital base, little saving mobilization-about one-third of loan

portfolio, and small or no grants.

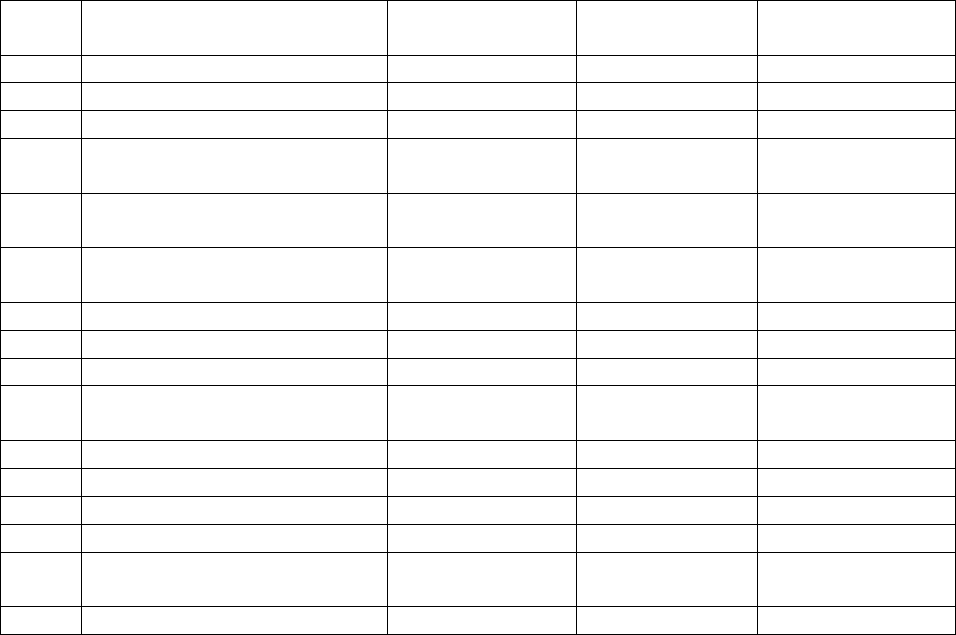

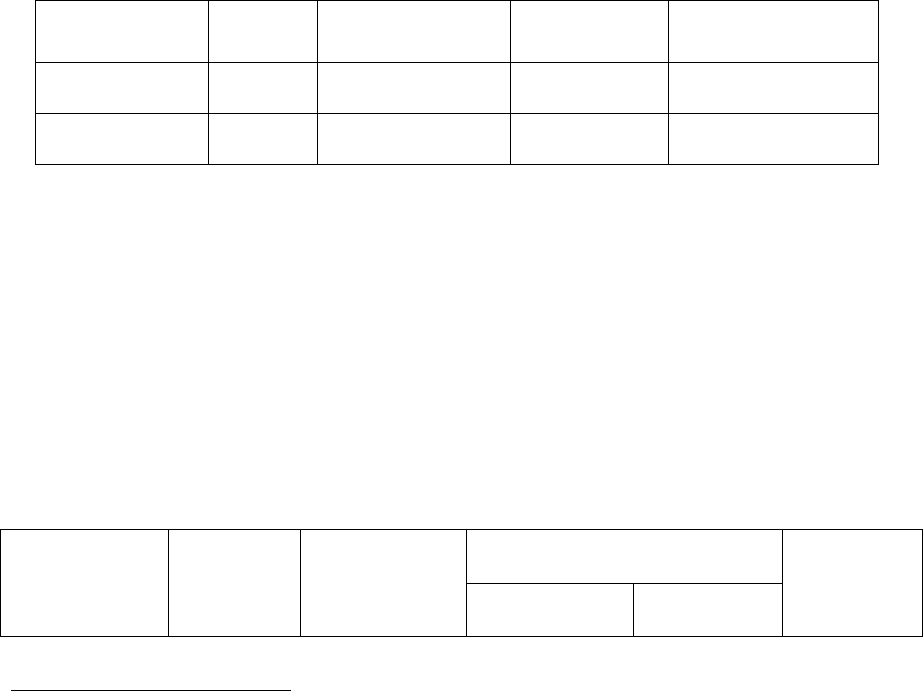

Table 1

The loan portfolio and savings of few MFIs as of 31 Ashad, 2066 (15 July, 2009)

(Amount in Rs.’000)

S. No.

Name of MFIs Gross Loan

Portfolio

Savings Savings/loan ratio

1 Nirdhan Utthan Bank Ltd. 1,118,639

336,825

30.11%

2 Chhimek Bikas Bank Ltd. 894,178

416,398

46.56%

3 Swawlamban Bikas Bank Ltd.

699,699

327,407

46.76%

4 Paschimanchal Grameen

Bikas Bank

596,639

162,175

27.18%

5 Madhyamanchal Grameen

Bikas Bank

451,921

142,075

31.43%

6 Nerude Laghu Bitta Bikas

Bank

309,956

102,250

32.98%

7 FORWARD (FINGO) 302,420

117,413

38.82%

8 CSD (FINGO) 290,691

158,129

54.39%

9 Jeevan Bikas Samaj, (FINGO)

315,954

122,766

38.85%

10 Muktinath Bikas Bank

(Class B Dev. Bank)

75,231

21,040

27.96

11 Sahara Cooperative, Jhapa 300,743

115,529

38.41%

12 Karnali Cooperative 69,854

29,307

41.95%

13 Manushi (FINGO) 62,020

31,260

50.40%

14 UNYC, Bardiya, (FINGO) 26,498

11,776

44.44%

15 Baudha Cooperative

Surkhet

15,205

10,138

66.67%

16 Sana Kisan Cooperative 81,178

57,683

71.05%

Source: Grameen Laghubitta, Vol.29, 2066 Ashad, RMDC.

The saving to loan ratio in these institutions varies from 27.18 percent to 71.05 percent, however,

we can conclude that their savings are not enough to meet their on-lending funds.

3.2 Sources and Uses of Funds

Financing in MFIs is matched with borrowed money which they receive from commercial banks

under deprived sector lending scheme. Commercial banks, Rural Microfinance Development

Centre Ltd. (RMDC), Sana Kisan Bikas Bank Ltd. (SKBBL), Nepal Rastra Bank- Rural Self-

6

Reliance Fund (RSRF) are the major sources of wholesale funding to MFIs in Nepal. Some MFIs

have received wholesale funding from multilateral funding projects like Third Livestock

Development Project (TLDP), Poverty Alleviation Project in Western Terai (PAPWT), and

Community Ground Irrigation Sector Project (CGISP). Few MFIs have/had received funding

from foreign institutions like Grameen Trust, Bangladesh.

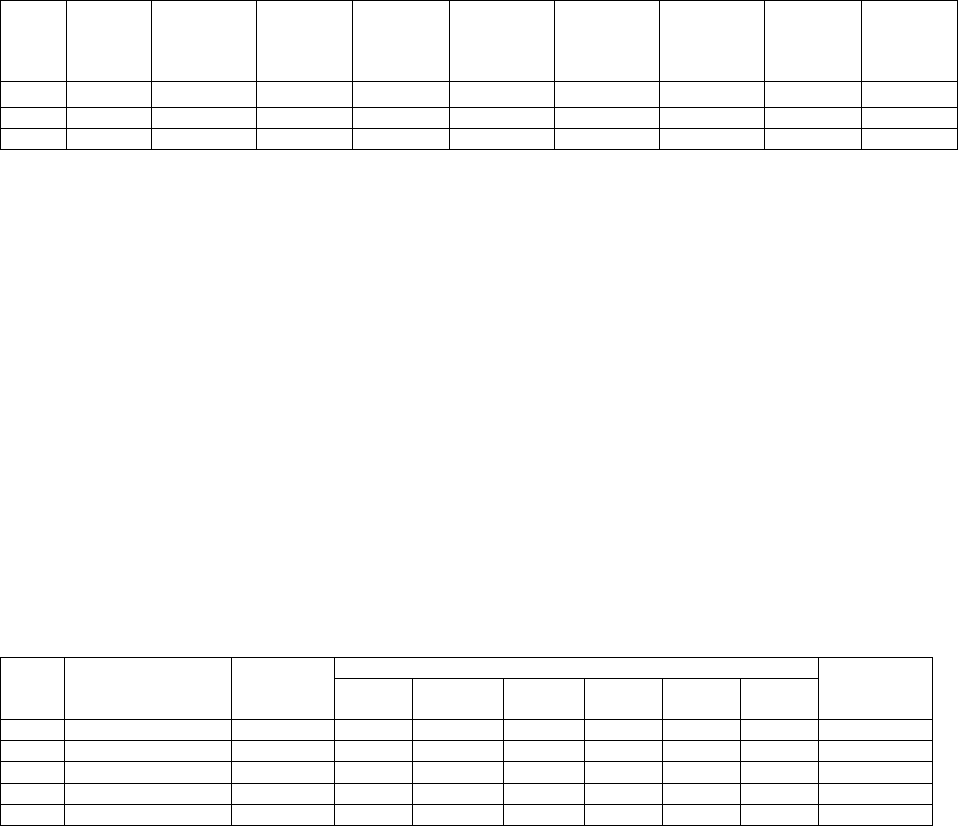

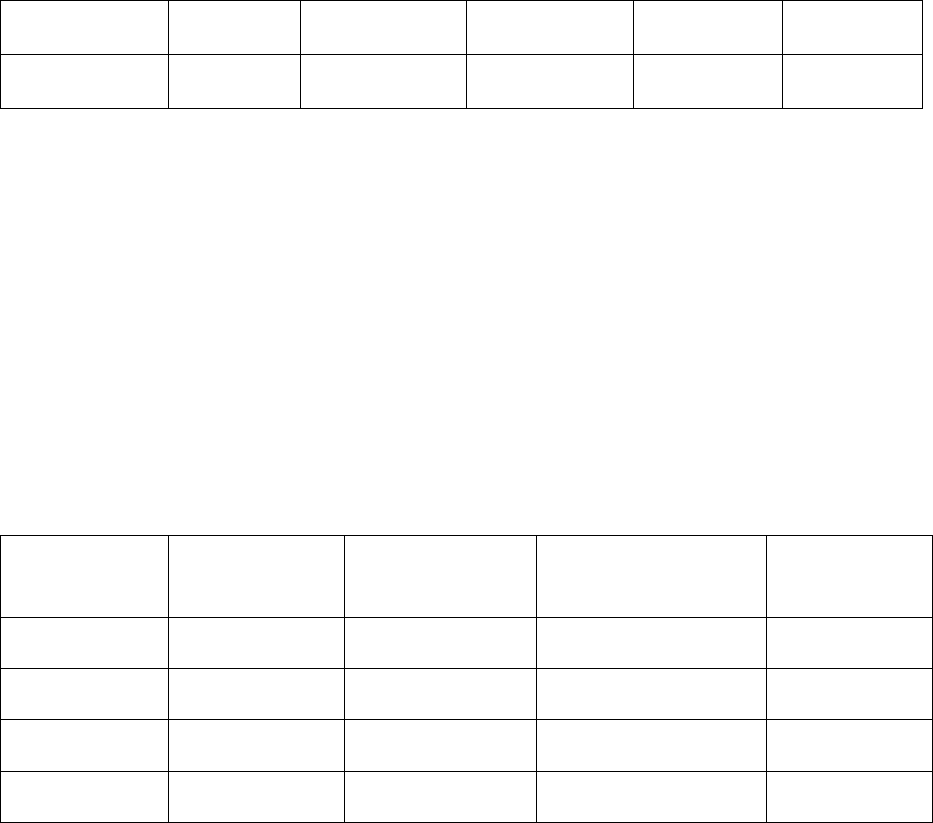

Table 2

Sources and Uses of Funds of Class D MFDBs

(Amount in Rs. ‘000)

S.No. FY Capital Members’

savings

Borrowin

gs from

Commerci

al Banks

Borrowing

from other

Financial

institutions

Borrowing

from others

Total

Resources

Total

Loans and

Advances

Surplus

Amount

1 2006/07 1,118,500 1,384,161 3,892,613 1,999,300 1,449,781 9,844,355 5,780,600 4,063,755

2 2007/08 1,257,900 1,425,053 3,821,713 3,370,607 1,609,953 14,485,226 7,078,200 7,407,026

3 2008/09 1,450,176 2,030,612 6,141,530 953,677 1,809,103 12,385,098 8,231,287 4,153,811

Source: NRB

From the financing mix of these MFIs, the borrowing is the most critical component of

financing. It covers about 76 percentage of total resource mobilization. The members’ savings

comes next followed by equity. Till the FY 2008/09, MFIs are enjoying surplus resources.

3.3. Sources of Wholesale Funding

3.3.1 Deprived Sector Lending from Commercial Sources: The main source of wholesale

funding is the commercial banks. They provide wholesale funding to MFIs under deprived sector

lending scheme.

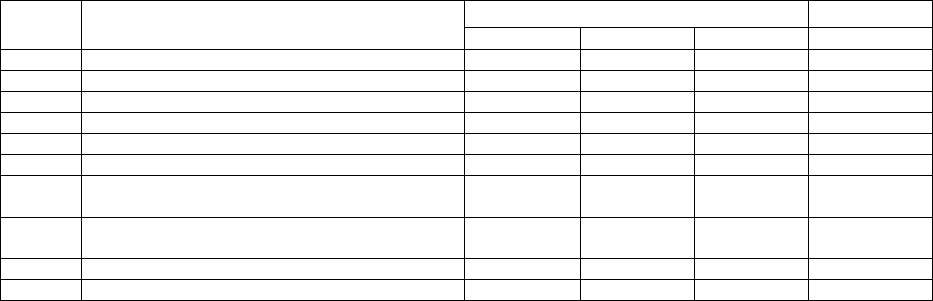

Table 3

Status of deprived sector lending from commercial banks, development banks and finance

companies as of Ashad Last, 2066 (Mid- July 2009)

(Amount in Rs. ‘000)

Indirect Lending S.

No.

Types of Financial

Institutions

Direct

Lending to

Clients

Share Class D

MFDBs

Coop,

FINGOs

YSEP Foreign

Emp.

Other

Total

1 Commercial Banks 3,474,447 470,430 7,324,691 918,325 939,210 131,282 155,273 13,413,568

2 Development Banks 583,672 4,500 132,857 0 2,615 1,608 0 725,207

3 Finance Companies 640,008 2,925 11,226 0 5,723 0 0 659,882

Total 4,698,082 477,855 7,468,774 918,235 947,548 132,890 155,273 14,798,657

31.75% 3.23% 50.47% 6.20% 6.40% 0.90% 1.05%

Source: NRB

These financial institutions have channelized their 50 percent of their deprived sector portfolio

through class “D” microfinance development banks.

7

3.3.2 Specialized Wholesale Institutions

3.3.2.1 RMDC: Rural Microfinance Development Centre Ltd. (RMDC) is an apex wholesale –

lending organization of microfinance. Besides, it also works for promotion and development of

microfinance in the country. It promotes financially viable and sustainable MFIs by providing

necessary financial and technical support to potential institutions. It makes due diligence before

disbursing loan to particular MFI.

Table 4

Results of Financing from RMDC.

Results Particulars Unit

Mid-July ‘06 Mid-July ‘07 Mid-July ‘08

Disbursed

Rs. million

298.24

961.07

525.02

Repaid

Rs. million

123.22

326.88

405.64

Total Outstanding

Rs. million

500.85

1,135.04

1,254.42

Source: RMDC Annual Report 2007-08.

3.3.2..2 SKBBL: Sana Kisan Bikas Bank Ltd. (SKBBL) is a specialized wholesale micro-

financing development bank established with the aim of promoting and strengthening grassroots

level Small Farmer Cooperatives Ltd. (SFCLs) in particular and similar other microfinance

intermediaries in general. The bank provide short and medium term wholesale credit or refinance

to SFCLs and other similar grassroots level financial intermediaries.

Table 5

Results of Financing from SKBBL

Results Particulars Unit

Mid-July ‘07 Mid-July ‘08

Disbursed

Rs. million

697.48

912.33

Repaid

Rs. million

657.264

846.38

Total Outstanding

Rs. million

1,327.04

1,445.42

Source: SKBBL 7

th

Annual Report 2064/65.

3.3.3 Rural Self-Reliance Fund (RSRF): To increase the income and render employment

opportunities for the deprived people in the rural areas, the Government of Nepal has established

RSRF in 1991 with seed capital of Rs. 20 million and added another 20 million in 2004/05. NRB

has provided additional money from its profit to this fund in different periods. RSRF provides

8

the wholesale credit for on-lending purpose to deprived people through MFIs, cooperatives,

FINGOs.

Table 6

Results of Financing from RSRF

Description Mid- July 2007 Mid- July 2008

Loan Disbursement:

No. of Districts

No. of MFIs

No. of Beneficiary families

Loan Disbursed (Rs. in million)

Loan Collected (Rs. in million)

Outstanding loan (Rs. in million)

48

277

12,228

132.6

81.2

51.4

50

334

14,862

193.4

102.3

91.1

Source: NRB, Annual Report 2064/65.

3.4 Demand Analysis

3.4.1 Demand of on-lending funds to MFDBs

The microfinance clients, the loan portfolio outstanding, and savings are in increasing trend.

Table 7

Borrowings needed for On-lending to MFDBs

(Amount in Rs. thousand)

Actual Projected Indicator/ Year

2006/07 2007/08 2008/09 2009/10 2010/11

No. of Members

409,113 501,059 561,624 658,678 772,504

No. of Loan clients

339,048 394,711 441,711 504,268 575,685

Loan Portfolio

5,780,600 7,087,200 8,231,287 9,795,232 11,656,326

Savings

1,384,161 1,425,053 2,030,612 2396,122

2,755,540

Equity

1,118,500

1257,900 1,450,176 1,645,950 1,859,923

External Resource

Needed

3,277,939 4,404,247 4,750,499 5,753,160 7,040,863

Source: MFDBs and NRB

From the table, the loan outstanding in MFDBs is growing rapidly and it is expected to reach to

Rs.

9,795,232

thousand in Mid- July 2010. The savings mobilized from the members would be

9

only Rs.

2396,122

thousand, equity Rs.

1,645,950

thousand indicating a gap of on-lending fund

by Rs.

5,753,160

thousand at the same date.

3.4.2 Demand of On-lending fund to FINGOs

25 FINGOs licensed from NRB are serving 329,755 poor clients and they have total loan

outstanding of Rs. 2,183,221 thousand and saving of Rs. 864,283 thousand as of Mid- July

2009.

1

Table 8

Demand of On-lending fund for FINGOs

2

(Amount in Rs. Thousand)

Time line Members

Loan Outstanding Savings Borrowings needed

Mid- July 2009 329,755 2,183,221 864,283 1,318,938

Mid- July 2010 362,731 2,401,546 950,7132 1,450,833

Source: MIFAN

3.4.3 Demand of on-lending fund for Cooperatives

The demand of on-lending funds to SACCOS is also in increasing trend. As per Department of

Cooperatives, there are 5,162 SACCOS with membership of 714,516 as of Chaitra end 2065

(Mid- April 2009)

3

.

Table 9

Demand of On-lending fund for SACCOS

4

(Amount in Rs. Thousand)

Available Resources Time line No. of

Members

Total Loan

Amount

Savings Equity

Resource

Needed

1

Source: Microfinance Association of Nepal (MIFAN).

2

Since FINGOs are not for profit organization, they have little equity, therefore ignored while

calculating the demand of on-lending funds.

3

Source: Department of Cooperatives, GON.

4

Due to lack of reliable data on cooperatives engaged microfinance business, all these 5,162

SACCOS are assumed as MFIs as their loan outstanding per member is Rs. 28.165 thousand,

and the projection is made taking 10 percent growth .

10

Mid- Apr 2009 714,516

20,124,886

16,247,310

2,191,126

1,686,450

Mid- Jul 2010 785,968

22,137,386

17,872,050

2,410,240

1,855,096

Source: Department of Cooperatives, GON

3.4.4 Total demand for MFIs

MFIs need funding not only for on-lending, rather for operating expenses, capital expenditure

and to keep mandatory reserves and provisions. Besides, they need to maintain funds enough to

meet at least three months demand because they cannot get the money as and when needed.

From the above analysis, the demand of funding for MFIs in FY 2009/10 seems to be Rs.

11,323,861 thousand besides the savings mobilized from clients and their equity.

Table 10

Demand of funding for MFIs in FY 2009/10

(Amount in Rs. Thousand)

Types of MFIs Expected No. of

Clients

Funds needed for

On-lending

Funding needed for

additional 3 months

Total Funds

needed

MFDBs 658,678

5,753,160

1,438,290

7,191,450

FINGOs 362,731

1,450,833

362,708

1,813,541

SACCOS 785,968

1,855,096

463,774

2,318,870

TOTAL 1,807,377

9,059,089

2,264,742

11,323,861

3.5 Supply Analysis

On the supply side, almost all private sector commercial banks are providing wholesale lending

to MFIs rather than channeling small loans to individual clients under deprived sector lending.

The development banks and finance companies are also asked to direct some of their lending

towards deprived sector, this has increased the supply of wholesale funding, however, their

portfolio being smaller compared to commercial banks.

11

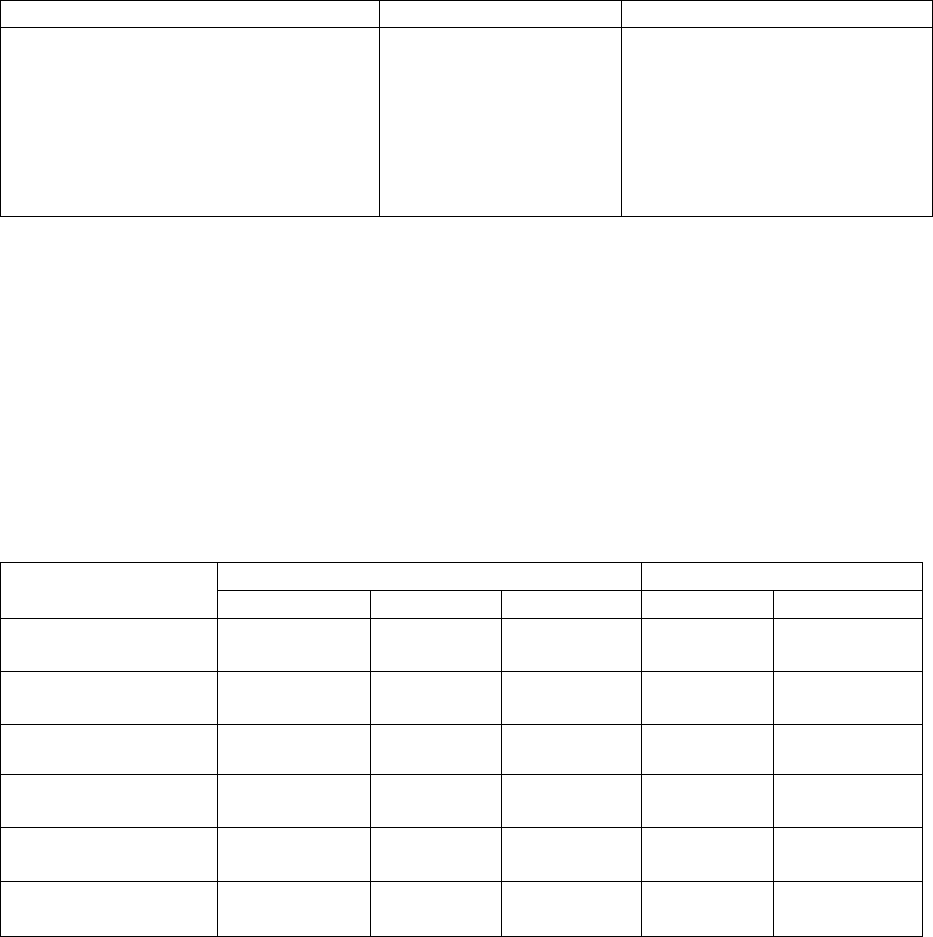

Table 11

Status of Loan Disbursement of Commercial Banks, Development Banks and Finance

Companies and available funding under Deprived Sector Lending

4 (Amount in Rs. thousand)

Actual Projected S. No.

Types of Financial Institutions

2006/07 2007/08 2008/09 2009/10

1 Commercial Banks: Total Loan 215,978,400 292,500,400 382,082,290 476,838,697

Deprived Sector loan 7,213,325 9,670,417 12,869,333 14,305,160

2 Development Banks: Total Loan 11,930,334 21,533,633 39,425,641 57,163,236

Deprived Sector loan 724,137 1,143,264

3 Finance Companies: Total Loan 21,085,294 36,902,652 51,165,790 69,263,129

Deprived Sector loan

4 Total Amount available under Deprived sector

lending scheme

7,213,325 9,670,417 14,253,352 16,487,372

5 Funding towards YSEP Fund (1/3 of DSL

Funding)

5,495,790

6 Amount for Direct Lending to clients (32 %) 5,275,956

7

Remained Amount for MFIs 5,715,626

Source: NRB

The total available funds under deprived sector lending is Rs. 16,487,372 thousand, out of this

one-third i.e. Rs. 5,495,790 thousand goes under YSEP and rest Rs. 10,991,582 thousand will be

available for direct lending from these institutions as well as lending through MFIs. As per last

year’s trend 32 % of the total DSL fund will be channelized by banks and financial institutions to

their customers directly. Rs. 5,715,626 thousand only is remained for channeling through MFIs.

12

4.0 Findings, Conclusion and Recommendations

4.1 Drying up resources and increasing cost of funds

From the demand analysis, the expected demand for MFIs in FY 2009/10 is expected to be Rs.

10,352,454 thousand whereas the available supply under DLS scheme is 5,715,626 thousand

after excluding the provisions for YSEP and directly lending from banks and finance companies.

Wholesale institutions like RMDC, SKBBL and RSRF have not enough money to meet the gap.

This indicates the supply of funds for MFIs is getting drier. MFIs are now in rush to catch the

scarce resources, and feeling difficult to get it and paying higher rate of interest (currently 7-9%)

than they have paid earlier (4-6%). The current financial crisis has further made MFIs position

very hard, they have either to increase the interest to its clients or squeeze their business, both

options being very painful. This will adversely affect the growth of microfinance industry.

Because of scarcity of resources and increasing cost of funds, MFIs may think twice to expand

their services in the remote and high hills which will further push the poor people living in

remote area further back.

Besides, the provision of mandatory deprived sector lending schemes, the evolution and growth

of wholesale funding agencies like RMDC, SKBBL and RSRF have made a significant

contribution for the growth of microfinance industry in Nepal. This has created a big financial

market among the poor households. Microfinance institutions are serving the un-served and

under- served people. Despite the contribution, recent directives from NRB has widened the

scope of deprived sector lending, commercial banks have option to establish subsidiary company

focusing on small loans, they can lend to micro hydro projects, hospitals, low cost housing and

many more, keeping the resources to MFIs drier. If this goes on continually without alternative

provisions to MFIs, they will be compelled to be consolidated and they hesitate to expand the

services which will jeopardize the whole effort of providing access to financial services to poor.

MFIs will be compelled to reduce their lending and incur losses. They may hesitate to expand

their services to under- served and un-served people and region.

4.2 Conclusion and Recommendation

4.2.1 Deposit mobilization from the public for sustainability.

Due to prudential regulations from NRB, many MFDBs are emerging professionally as very big

institutions, they have enough capital, professional management, good governance practices.

Similarly, many of them have wide branch network and well managed computer based

management information system. NRB, now, needs to come up with policy to allow MFIs to

mobilize deposit from the general public of course with stringent criteria for the safety of public

deposit. The criteria can be set in the area of capital adequacy, core capital and saving

mobilization limits, good governance, etc. However, even after allowing MFDBs to accept the

public deposit, the provision of deprived sector lending remains to be the most important sources

of funding for MFIs in many years to come.

13

At the beginning, collecting deposit from the public may cost more for MFIs than getting

wholesale funding from commercial banks, but deposit is the only way that makes MFIs

sustainable in the long -run. Most Nepalese microfinance institutions are moving towards

achieving operating and financial self-sufficiency. They have professional management with

competent human resources, and they are applying the best practices of microfinance. This has

increased the clients outreach, branch network and have created a faith among rural poor people

which will help them to mobilize savings from public.

Commercial banks like Rastriya Banijya Bank, Nepal Bank Ltd, Agriculture Development Bank

have closed their many rural branch offices during insurgency, and they are hesitant to re-

establish these branch offices in rural areas. MFIs like Nirdhan Utthan Bank Ltd. having the 4

th

biggest branch network in the country, can serve the missing middle for their need of financial

services to deposit their saving. This enables their access to formal financial services.

4.2.2 Government’s Role

Government has so far played conducive role by enacting the laws recognizing microfinance as

financial business, however, it is treating MFDBs as commercial organization and charging the

highest corporate tax on its profit. If the tax rate could be lowered, the amount so saved can be

used to provide services to more poor people. Government could also provide support to MFIs as

grant in planned manner to expand their services in remote and un-served areas of the country.

However, such grant should be linked with performance.

4.2.3 International Sources

Besides, the deprived sector lending, deposit mobilization, lending from wholesale funds, MFIs

should also search international sources of financing. Social investors in the developed countries

are interested to provide financing to the poor people in developing countries like Nepal. The

web based financing is increasing its stake in microfinance sector. KIVA has increased its

wholesale funding business in many countries and it is interested to enter into Nepalese market.

WEAL/GoodReturn, Energy in Common (EIC) are also interested to provide wholesale funding

to Nepalese MFIs. Whether NRB should come up with little more enabling policy to invite such

international funds for Nepalese MFIs. Funding from international sources is not easy because of

higher rate of interest and the risks of currency devaluation.

14

References

1. Annual Report 2064/65: NRB.

2. Annual Report 2007-08: RMDC.

3. 7

th

Annual Report 2064/65: SKBBL.

4. Annual Reports of Various MFDBs like NUBL, CBBL, PGBBL, DBBL, SBBL,etc.

5. Bank and Financial Institution Act, 2006

6. Grameen Laghubitta: Vol. 29, 2066 Ashad, RMDC.

7. Microfinance Association Nepal: An Outlook April 2009: MIFAN

8. Nepal Rastra Bank Act, 2058

9. Licensing Policy NRB

10. Unified Directives 2066/67: NRB

11. Various circulars from NRB

Websites visited

1. nrb.org.np

2. rmdcnepal.com

3. moac.gov.np

4. skbbl.com.np