NATIONAL SECURITY AGENCY

OFFICE OF THE INSPECTOR GENERAL

Audit of the Implementation of the

Coronavirus Aid, Relief, and Economic

Security (CARES) Act, Section 3610

AU-20-0008

26 May 2022

(Reissued with Administrative Revisions on 22 June 2022)

Audit of the Implementation of the CARES Act, Section 3610

Audit

of the Implementation of the CARES Act, Section 3610

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

ii

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .i

I. Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

II. Results of the Audit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

FINDING 1: NSA had signicant issues implementing the CARES Act, including

insucient invoice reviews. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3

III. Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Appendices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

APPENDIX A: About the Audit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

APPENDIX B: Abbreviations and Organizations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

APPENDIX C: CARES Act Sample Documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

1

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

I. INTRODUCTION

On 27 March 2020, Congress enacted the Coronavirus Aid, Relief, and Economic Security (CARES)

Act in response to the Coronavirus Disease 2019 (COVID-19) national emergency. The CARES Act

contains a number of provisions aimed at stabilizing the economy and helping affected households and

businesses. Section 3610 of the CARES Act permits federal agencies, under certain circumstances, to

modify terms of existing contracts or agreements, and to reimburse federal contractors’ compensation

due to COVID-19-related issues. CARES Section 3610 provides federal agencies the discretion

to reimburse paid leave to federal contractors confronted with the inability of their employees or

subcontractors to perform work at a federal government-approved work site due to facility closures,

government-directed denied access, or other restrictions when their job duties could not be performed

remotely.

1

Reimbursement under CARES Act, Section 3610 has several limitations, as described below:

• A contractor may only receive reimbursement if its employees or subcontractor employees:

- Cannot perform work at a government-owned, government-leased, contractor-

owned, or contractor-leased facility or site approved by the Federal Government

for contract performance due to COVID-related closures or other restrictions,

and

- Are unable to telework because their job duties cannot be performed remotely

during the public health emergency that was declared on 31 January 2020.

• Reimbursement is authorized:

- Only at the minimum applicable contract billing rate, and

- Not to exceed an average of 40 hours per week per employee.

2

• The Government must reduce the maximum reimbursement authorized by the amount of

credit the contractor is allowed pursuant to Division G of the Families First Coronavirus

Response Act (FFCRA) and any applicable credits the contractor is allowed.

3

• Reimbursement is contingent upon the availability of funds.

1

Government-directed denied access refers to NSA’s denied-access protocol that prevents affiliates with an increased risk

of having COVID-19 or individuals who are medically recommended to quarantine due to possible exposure to COVID19

from entering NSA spaces during the public health emergency.

2

The CARES Act states “not to exceed an average of 40 hours per week.” On 3 April 2020, the Office of the Director of

National Intelligence (ODNI) issued IC [Intelligence Community] Guiding Principles for the IC Acquisition & Procurement Community

on Implementation of the CARES Act, which states “not to exceed an average of 40 hours per week per employee.” On 9 April

2020, NSA issued Invoicing Information for Contractors under CARES Act, which states that “hours billed in cumulative shall not

exceed an average of 40 hours per week per obligated FTE [full time equivalent]. In cases where the FTE support level is less

than 40 hours per week, the hours billed shall not exceed the stated contractual hours per week.”

3

The FFCRA requires certain employers to provide employees with paid sick leave or expanded family and medical

leave for specific reasons related to COVID-19. Division G of the FFCRA allows tax credits to employers for COVID-19

paid leave.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

2

According to the Office of the Under Secretary of Defense, during the COVID-19 pandemic, many

Department of Defense (DoD) contractors were struggling to maintain a mission-ready workforce

due to work-site closures, personnel quarantines, and state and local restrictions on movement. The

Office of the Director of National Intelligence (ODNI) supported the immediate implementation of

Section 3610 of the CARES Act and encouraged Intelligence Community (IC) agencies to make full

use of the flexibility provided by the Act and other existing contracting tools to enable the maximum

number of contractor personnel to convert to staying home in a “ready state” during the national effort

to mitigate the spread of COVID-19.

4

As of 8 June 2021, NSA reported the amount of CARES invoices as totaling $917 million for a total

of 81,000 CARES hours.

B

See Appendix A, “About the Audit,” where the audit objective, scope, methodology, and criteria can

be found.

4

In the context of Section 3610 of the CARES Act, NSA defined “ready state” in communications to contractors as the

ability and willingness of a contractor employee to return to a place of performance that has been closed, or otherwise having

limited or reduced access due to conditions caused by the COVID-19 pandemic, within two hours after having been notified

by the Government through the contractor employee’s management.

B

Subsequent to issuance of this report, the Agency indicated to the OIG that the total number of 81,000 CARES hours

was incorrect. The Agency informed the OIG that the correct total for the time period was 6.4 million hours; however

the OIG has not independently verified the accuracy of this revised number. The hours were included in the report as

background information and are not a basis for or relevant to the audit’s findings or recommendations. Moreover, because

the invoiced amounts may include other indirect costs, it would not be possible to determine an hourly rate from these totals.

3

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

II. RESULTS OF THE AUDIT

The Agency did not perform sucient review of CARES invoices. This was due to

evolving guidelines, reduced contract oversight stang during the COVID-19 pandemic,

an overreliance on contractor-provided information, and the absence of clear and

comprehensive Contracting Ocer Representative (COR) oversight procedures for

CARES invoices. Insucient documentation and lack of COR oversight caused the OIG to

question more than $16.4 million, or 40 percent of the sampled CARES invoice charges.

As a result, the Agency has an increased risk of being overcharged for CARES paid leave

and of potential fraud by contractors, both of which could reduce the funds available for

mission requirements.

NSA notified contractors on 30 March 2020 that it was developing implementation guidance for the

CARES Act. The guidance notice provided to contractors on 31 March 2020 stated that “subject to

the availability of appropriations, contractors who are working under reduced manning at Agency

sites may be reimbursed . . . .” In addition, on 3 April 2020, the Agency published guidance on the

Acquisition Resource Center (ARC) website that stated that Section 3610 only applied if a contractor

employee was unable, due to COVID-19, to perform work because they were restricted from access

to the site where they are contractually assigned, and that telework by contractor personnel at private

residences was not permitted for any work charged to an Agency contract.

For any invoice payment, DoD Financial Management Regulation (FMR) 7000.14R, Volume 10,

Chapter 8, Section 0803, issued March 2020, states, “[a]s part of entitling and certifying a payment,

DoD Components must ensure that appropriate payment documentation is established and retained

to support payment of invoices and interest penalties. This documentation normally includes the

contract/purchase order, receipt/acceptance report, and a proper invoice.”

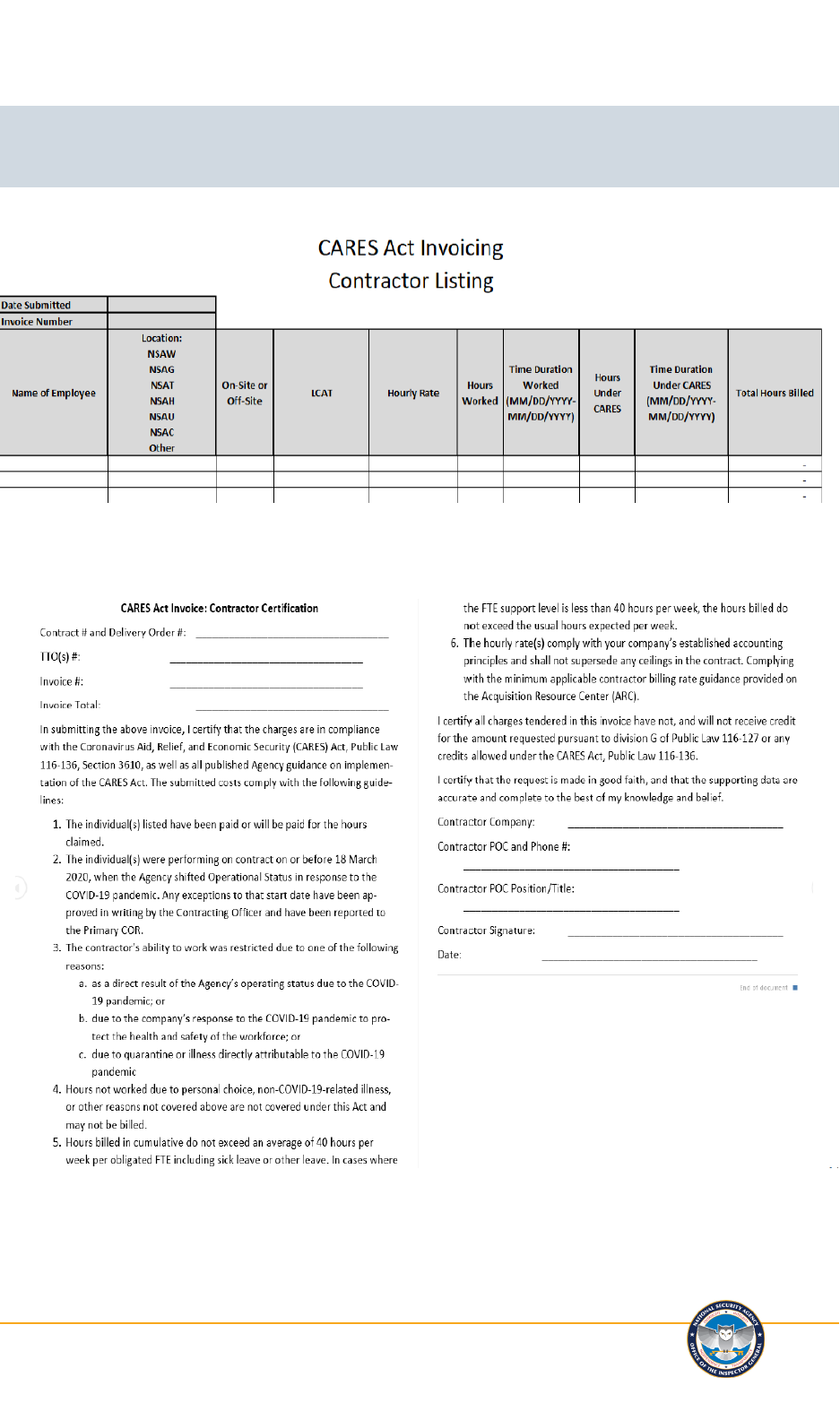

In addition to these documents, NSA required contractors to follow additional guidance and

submit CARES documentation to support reimbursement for paid leave. NSA provided CARES

invoicing guidelines and instructions to contractors on 9 April 2020. The invoice guidelines required

contractors to separately track all paid leave for COVID-19, by labor category, from actual hours

worked for all Cost-Reimbursement, Time and Materials, Labor Hour, and Fixed Price Level of Effort

contracts.

5

Invoices submitted for CARES reimbursement were to include “CARES” in the invoice

number to allow the Agency to track all invoices under the CARES Act. Vendors were required to

5

The CARES Act only applies to labor costs.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

4

submit separate invoices for hours worked and CARES paid leave. In addition to standard invoice

documentation, contractors were required to submit a completed and signed CARES Act Invoice

Contractor Certification Memo—which required the contractor to attest they were not receiving other

reimbursement for the same costs—and a completed CARES Hours Tracker Excel template.

6

The

CARES Hours Tracker is an Excel table that indicates both hours worked and CARES hours by

employee. The Hours Tracker also shows the work location, labor category, and hourly rate for each

employee. Templates for the additional documentation were provided via the ARC and Maryland

Procurement Office (MPO) websites. (See Appendix C for samples of the additional CARES invoice

documentation.)

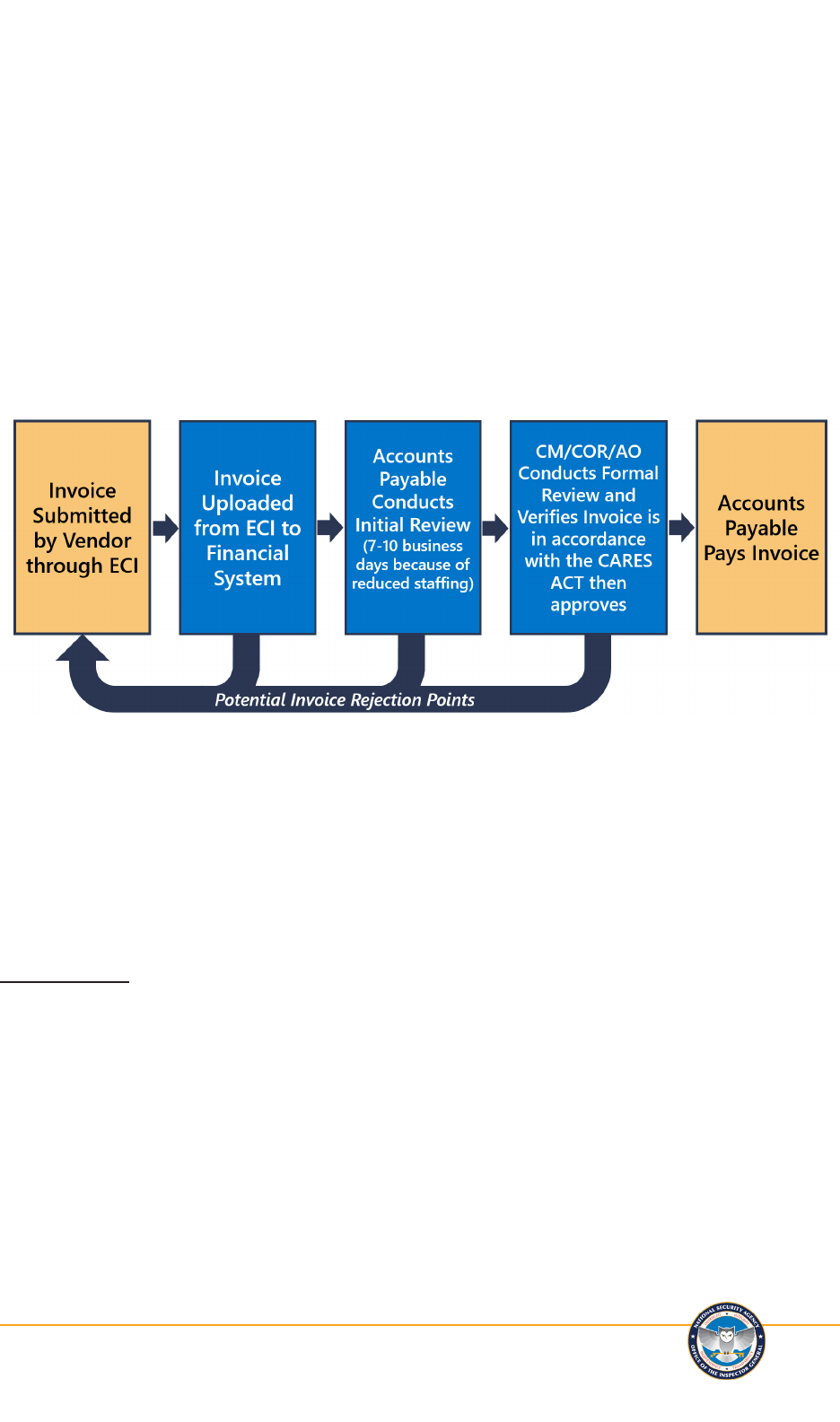

Invoices for CARES Act reimbursement followed the same invoice process as all regular invoices, as

shown in Figure 1.

7

The OIG judgmentally sampled 25 CARES invoices with a period of service from 27 March through

31 August 2020 totaling $37.9 million.

8 9

Based on review of only the supporting documentation, the

OIG had questions or concerns with all but two invoices; these questions and concerns related to:

1. Questionable contractors billed: employees on invoices who were not listed on the

Electronic Contractor Position Roster Log (eCPRL) or who were listed as pending or

de-sponsored,

10 11

6

According to Business Management & Acquisition (BM&A), NSA participated in ODNI biweekly sessions with other

IC agencies to discuss the implementation of the CARES Act and share processes among participants. For example, the

group shared the process of having the vendor self-certify that they did not receive other COVID-19 relief.

7

The Electronic Commerce Interface (ECI) is used by contractors to submit electronic invoices to the Agency. Contract

Managers (CM) are responsible for contract monitoring, mission communication, and requisition tracking. Acceptance

Officer (AO) is an individual named by the Contracting Officer to verify receipt of supplies or simple services and approve

invoices for those actions.

8

The total number of CARES invoices submitted to the Agency from 27 March through 31 August 2020 was 2,145.

9

The OIG did not reach out to contractors to determine whether the questionable costs were true errors or complete

further review of invoices to determine the specific amount of error. If Agency personnel were unable to sufficiently justify

or explain the hours/rates on an invoice, we deemed the entire invoice questionable for purposes of this audit.

10

The eCPRL is an electronic contractor position log used to identify all cleared contractors associated with NSA

contracts.

11

“Pending” refers to individuals who require some type of Agency action to be in an active or approved status on the

eCPRL. “De-sponsored” refers to individuals who no longer require access to NSA.

5

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

2. Questionable differences: differences between e-invoices and CARES Hours Trackers,

3. Questionable billing rates: questionable hourly rates,

4. Questionable hours: hours in excess of 40 hours per week average, and

5. Questionable timeframe: hours billed outside CARES period.

Questionable contractors billed. The Agency’s Notice to Contractors Regarding COVID-19 Update,

issued 20 April 2020, stated that “only costs incurred on or after 27 March 2020 are reimbursable

under Section 3610 of the CARES Act.” In addition, Business Management & Acquisition’s (BM&A)

COVID-19 Invoicing Guidelines, issued 17 April 2020, stated that “the individual must be approved

to work on the contract by the COR or Contracting Officer (CO) prior to the contractor invoicing

for COVID-19 related expenses.”

12

We compared the individuals billed on CARES invoices to the

eCPRL for the contracts in our sample to determine whether the employee was active on the contract

prior to billing CARES leave and within the CARES period. We identified 10 invoices on which some

employees were either not listed on the eCPRL or were listed as pending, de-sponsored, or inactive

during the period of service on the invoice. For 2 of the 10 invoices, the CORs were unable to provide

additional documentation to support that the contractor was approved to work on the contract prior

to the invoice period:

• For one invoice, an individual billed on the CARES invoice was listed as pending on the

eCPRL as of July 2019. The COR stated that this individual was approved to work on the

contract as of July 2019 but could not provide documentation to support that statement and

could not explain why the eCPRL showed the individual as pending.

• The other invoice had an individual listed on the eCPRL as de-sponsored as of

27 March 2020 (the beginning of the CARES period) but billed 16.5 CARES leave hours

for a total of $2,355. As a result of our interview, the COR requested an explanation from

the contractor, who, upon review, admitted that the hours were billed in error and should

be credited to NSA on a future invoice.

Questionable differences. In addition to standard invoice documentation, the Agency required

contractors to submit a completed CARES Hours Tracker, as described above. We identified 13 of

the 25 invoices in which the e-invoice did not agree with the CARES Hours Tracker. As illustrated in

Figure 2, for 7 of the 13, or 54 percent of the invoices, the CORs were able to provide explanations of

the differences that the OIG determined were sufficient. For example, one COR stated the difference

was due to the contractor failing to update the hourly rates on the Hours Tracker. The contract

transitioned from one option year to the next and the labor rates changed; however, the e-invoice and

the Hours Tracker were using different rates. After further review of the contract and invoice, the OIG

determined that the documentation supported the COR’s explanation. For 6 of the 13 invoices, the

CORs were unable to sufficiently explain to the OIG the differences between the e-invoices and the

CARES Hours Trackers. For example, one COR stated that they relied on the vendor for the hours

and did not note the difference in the documentation.

12

The BM&A COVID-19 Guidelines were updated multiple times as the Agency received additional guidance. We are

including the date of issuance throughout the report for reference.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

6

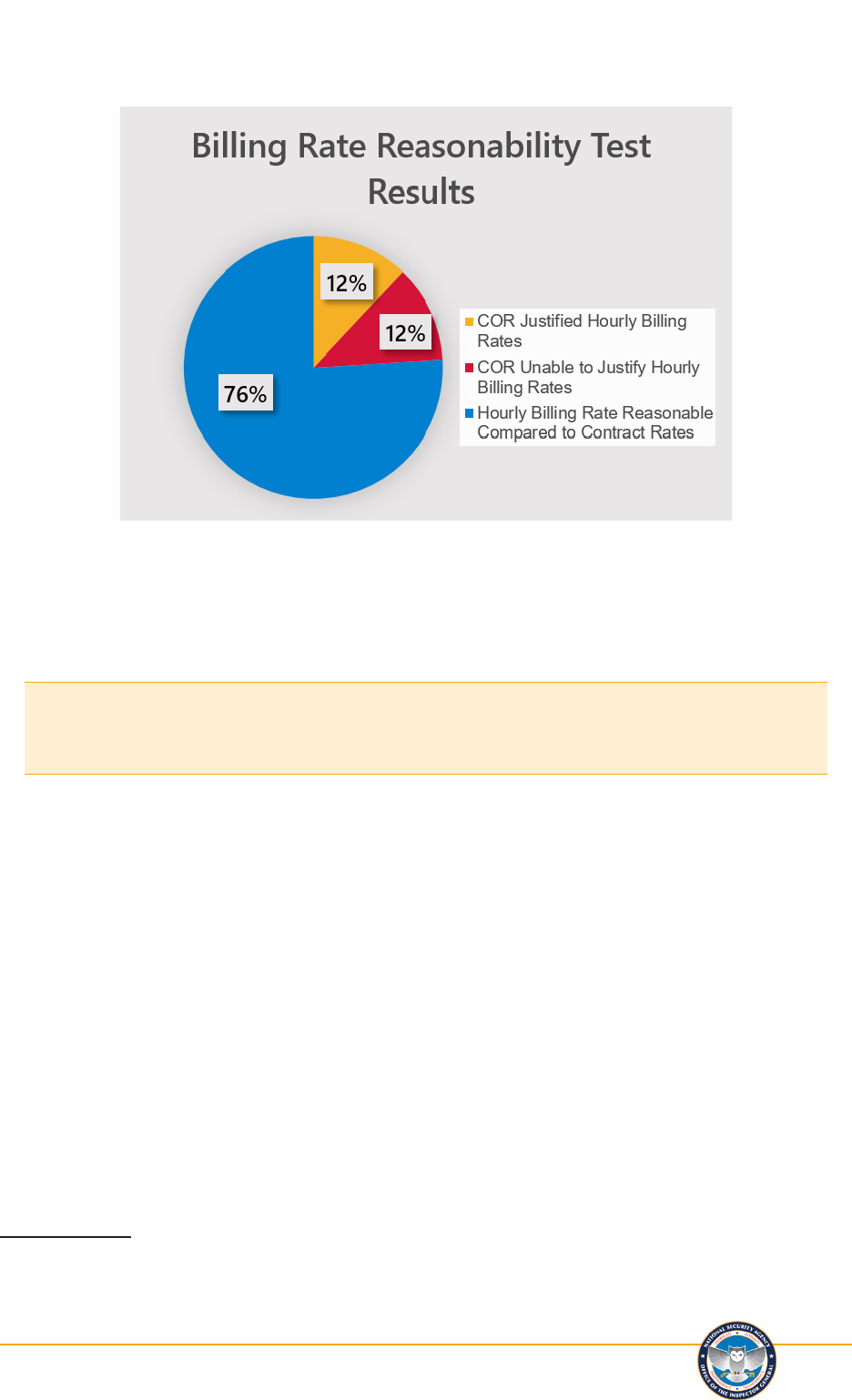

Questionable billing rates. The CARES Act allowed agencies to “reimburse at the minimum

applicable contract billing rates.” According to BM&A’s COVID-19 Invoicing Guidelines, issued

17 April 2020, “the rate charged must be the minimum applicable contract billing rate for the location

where the work would have been performed (excluding profit/fee).”

13

We compared the hourly rates

per the contracts to the hourly rates billed on CARES invoices by labor category to determine whether

the rates charged were in accordance with the CARES Act, Section 3610. We identified 3 of the 25, or

12 percent of the invoices where the hourly rates billed on the CARES invoices exceeded the contract

rate. However, the CORs were able to justify the hourly rates billed on these invoices. These three

invoices were from cost contracts in which the rates varied from the stated contract rates. The CORs

were knowledgeable about the rate differences and noted that the CARES rates were lower than the

non-CARES rates, and the fee, if applicable, was separate, demonstrating that they had performed a

review of the rates. However, we also identified another three, or 12 percent of the invoices in which

we were unable to verify the hourly rates based on the documentation. The CORs were unable to

provide explanations to justify the hourly rates billed on these invoices. Two of the three invoices were

Firm-Fixed Price Level of Effort contracts. The labor rates billed agreed with the labor rates on the

contracts; however, the CORs stated that they were unsure if profit/fee was included in these rates.

For example, one contract manager stated that they thought some profit was built into the contract rate

but was not sure of the exact percentage or amount. The results of our analysis of the 25 invoices is

depicted in Figure 3 as follows:

13

In April 2020, a decision was made and communicated that profit/fee could not be reimbursed. See further discussion

in footnote 17.

7

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

As a result of our audit inquiry, the COR for one invoice reviewed the CARES billing to date for the

contractor and determined that there were fees included in the billing rates. In December 2021, the

Agency recovered $43,000 related to these mischarges.

In December 2021, the Agency recovered $43,000 related to [CARES

invoice] mischarges.

Questionable hours. The CARES Act, as implemented through ODNI guidance, states that

reimbursement is authorized not to exceed an average of 40 hours per week per employee. BM&A’s

COVID-19 Invoicing Guidelines, issued 17 April 2020, states that “hours billed in cumulative shall not

exceed an average of 40 hours per week per obligated FTE [full time equivalent] including sick leave

or other leave.” We reviewed invoice documentation to determine whether the hours billed exceeded

an average of 40 hours per week in accordance with the CARES Act and Agency guidance.

We identified two invoices in which the hours exceeded an average of 40 hours per week.

14

One invoice

had a period of service (POS) from 27 March through 7 June 2020. We determined there were 50

work days in that POS (excluding the government holiday) for an estimated total of 400 hours. There

were two individuals whose total hours per the CARES Hours Tracker were 472 hours and 432 hours

during this period, respectively. The COR was unable to provide an explanation for the hours. In

addition, the vendor provided an additional spreadsheet that broke out the CARES hours by month.

However, the CARES hours by month exceeded the possible work hours in the month for 12 out of 29

employees. The COR was unable to explain the CARES hours and admitted that this issue was not

noted or discussed with the COR-Technical (COR-T). The COR for another invoice stated that their

14

Since the CARES invoices did not provide details showing hours per week, we used the assumption that a 40-hour

work week equates to 8 hours per day. Eight hours was multiplied by the number of work days in the period of service (POS)

to get an estimate of the number of hours that would be reasonable for that POS.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

8

review included ensuring that individuals were not charging more than 180 hours total as that was the

typical hours for this vendor’s invoices. However, the OIG determined that for the sampled invoice,

the COR did not question why 73 of 444 (16 percent) employees billed more than 200 total hours and

2 of those billed more than 200 CARES hours.

Questionable timeframe. The CARES Act states that a contractor may receive reimbursement if its

employees or subcontractor employees cannot perform work due to COVID-related closures or other

restrictions, as laid out in the introduction of this report. Although the CARES Act was extended

past 30 September 2020, CARES invoices should have been minimal after that point. We identified

28 invoices with a POS outside the CARES period or with no POS. We judgmentally selected 20 of

these invoices and identified 2 with questionable costs for a total of $738,000:

• One invoice for $11,000 had a POS beginning 16 March 2020, and the number of hours

billed was excessive for the CARES period, which should have started 27 March. The COR

stated that there were multiple changes to the guidelines going on at the time of this invoice

and that this was an oversight.

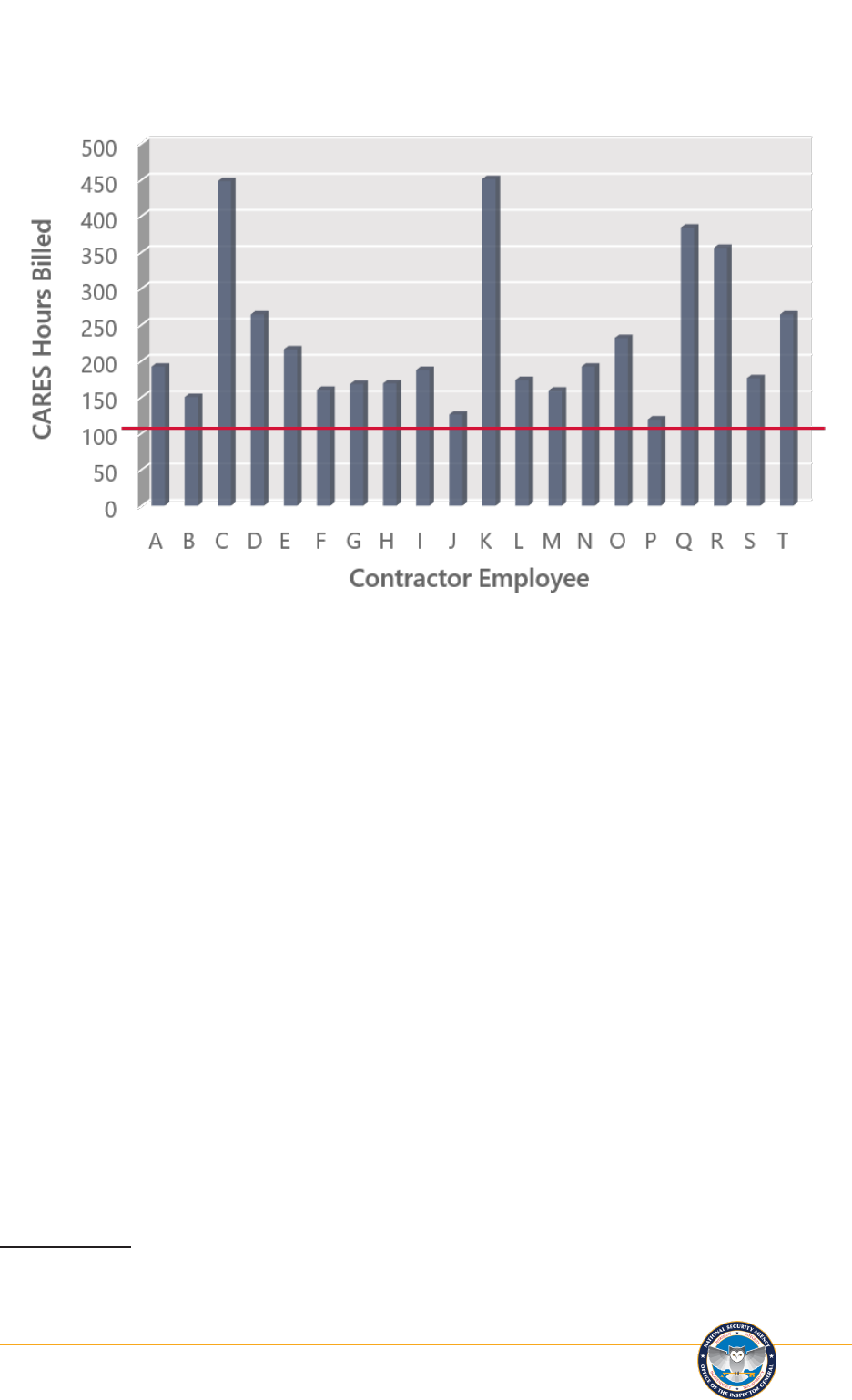

• Another invoice for $727,000 had a POS from 15 August through 25 September 2020. Given

the contractor’s work schedule during that timeframe, the OIG would expect that there were

approximately 14 work days in the POS for this invoice, which equates to approximately

112 hours per individual contractor. Twenty individuals billed CARES hours in excess of

112 hours, including two individuals with CARES hours in excess of 440 hours (see Figure

4 below). In addition, no (non-CARES) hours worked were reported. The COR did not

explain how they determined the accuracy of the CARES hours. The COR stated that they

were not familiar with this contract, but they had been reviewing invoices for someone who

was on extended COVID leave. The COR believed the excess hours were due to back hours

from subcontractors that bill later than the original invoice. Even though the invoice POS

was August through September, the invoice backup documentation provided by the COR

showed hours from March through September as all CARES hours. Since the invoice POS

included a period in which the contractor employees should have been working alternate

weeks, yet the invoice documentation showed no hours worked, it is unclear how the COR

monitored which employees were entitled to CARES leave and which were required to

report to work in order to ensure the accuracy of the invoice.

9

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

For the 25 invoices with concerns in our sample, the OIG interviewed the 22 CORs who approved the

CARES invoices, and based on our review of the available documentation and those interviews, we

questioned a total of $16,442,669, representing approximately 40 percent of the sample reviewed.

15

After discussions with CORs, the OIG identified the following problems with the process that may

have led to the more than $16 million in questionable costs related to the CARES invoices.

Guidance Constantly Evolving. The dynamic and prolonged nature of COVID-19 caused Section

3610 guidance to be continuously updated. From the time the CARES Act was passed on 27 March

2020, the implementation guidance was being updated and clarified through as late as December

2020. There were at least 10 memoranda issued by the Office of the Secretary of Defense, ODNI,

and the Office of Management and Budget (OMB) and over 25 ARC guidance documents, with each

providing additional clarification for agencies to implement the CARES Act. NSA management

tracked the changing guidelines and issued announcements to contractors and contracting personnel

through the ARC and internal NSA websites. Although 80 percent of the CORs interviewed stated that

the guidance they received from management regarding CARES invoices was helpful, the changing

guidance increased the risk for invoicing errors.

In addition, the required CARES invoice documentation was updated to reflect changes in guidance

that resulted in at least six versions of the Certification Memo and four versions of the CARES Hours

Tracker spreadsheet. Invoices were being submitted at the same time guidance was changing, making

15

Twenty-five questionable invoices are the result of 23 invoices from the original sample of CARES invoices from 27

March through 31 August 2020 and 2 questionable invoices from the sample of CARES invoices outside the CARES period.

(See Appendix A for more information on the two samples.)

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

10

it difficult for CORs and contractors to ensure they were using the most up-to-date guidance and

documentation. For example, due to unspecific initial guidance from OMB and DoD, the start date

for occurrence of labor costs reimbursable under Section 3610 was initially declared in a 9 April 2020

ARC announcement as 31 January 2020; however, due to evolving OMB guidance, the start date was

changed to 27 March 2020 just one week later.

16

Additionally, there was initial confusion regarding

whether fee/profit could be included in a Section 3610 reimbursement request.

17

Reduced Staffing to Review Increased Number of Invoices During COVID-19 Pandemic. During

the COVID-19 pandemic, the Agency developed procedures where other CORs would review invoices

in the event the primary/assigned COR was not available to review invoices. In addition to reduced

staffing of Agency personnel, there was also an increase in the number of invoices submitted because

contractors were required to submit separate invoices for CARES leave hours and actual work

performed in order to properly track CARES spending.

BM&A’s COVID-19 Invoicing Guidelines, issued 29 April 2020, stated that “designated BCMO [Business

and Contract Management Office] POCs [points of contact] will research invoices to determine if the

primary or alternate COR is [available]. For invoices without a present COR, the BCMO POCs shall

obtain reasonable knowledge and reasonable verification of all invoices.” The guidelines also stated

that “individuals approving invoices, other than regularly assigned CORs/AOs [Acceptance Officers],

will document the steps taken to gain reasonable verification in a Word document and attach to the

invoice in FACTS along with any supporting documentation utilized.”

18

Our sample did not contain

any invoices that were approved by someone other than an assigned COR. Fourteen of the 25 were

not approved by the primary COR but did have an assigned COR approval. Therefore, none of the

sample invoices had any additional documentation to support the verification of the sampled invoices.

During our interviews, one COR-T stated that they approved most of the non-CARES invoices for the

contract but felt that they were in a position to do that since they understand the nature of the work.

However, the COR-T stated they were unsure of the requirements for approving the CARES invoices

and would rather have not approved those invoices. They were asked to approve the CARES invoices

because they were working at the time the invoice needed approval. Another COR stated that there

was a two-to-three week delay between Accounts Payable receiving an invoice and sending the invoice

to the COR for review, so they felt their primary responsibility was ensuring the invoice was approved

or rejected as soon as it hit their queue.

19

Adequate review of CARES invoices requires knowledge of

16

See NSA CARES Act FAQs [Frequently Asked Questions], Revised, issued 14 April 2020; OMB M-20-22, Preserving the

Resilience of the Federal Contracting Base in the Fight Against the Coronavirus Disease 2019, issued 17 April 2020; the ARC COVID-

19 Invoice Guidelines, issued 17 April 2020; and ARC-Revised CARES Act Implementation Guidance, issued 20 April 2020.

17

An ARC announcement dated 9 April 2020 stated that “the minimum applicable billing rate may be fully loaded, and

inclusive of fee. Award fees will be calculated according to the applicable award fee plan.” However, on that same day, 9

April 2020, a Secretary of Defense memorandum stated that no contractor profit or fee is to be reimbursed. On 14 April

2020, an NSA CARES FAQs document announced the following revision: “In accordance with DPC [Defense Pricing and

Contracting] guidelines, profit/fee cannot be included.” On 22 April 2020, an ARC NSA CARES FAQs document noted

questions from contractors regarding fee/profit and requested assistance in removal of fee/profit from invoices, indicating

there was still confusion regarding fee/profit.

18

FACTS is the fully integrated financial management system that provides support to a variety of financial and business

functions.

19

According to Accounts Payable, the maximum number of days for receiving and sending an invoice to the COR for

review was 14 calendar days.

11

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

the contract, invoice details, and CARES requirements; therefore, reduced staffing increased the risk

that an error or mischarge on the invoice would not be caught.

Overreliance on Contractor-Provided Support. The OIG Audit of Cost-Reimbursement Contracts

(AU19-0010), issued 1 July 2021 (unclassified version released 20 October 2021), found that there was

an overreliance on contractor-provided reports. CORs were relying on contractor-provided monthly

reports to perform a cost review of invoices; however, in instances where the monthly reports did not

reconcile to the invoice amount, the CORs did not take steps to validate the difference. The OIG

found similar overreliance related to CARES supporting documentation.

Four of 20 (20 percent) of the CORs we interviewed stated that they relied on either the contractor’s

word or contractor-provided documents to verify the accuracy of the CARES invoices. In addition, two

CORs stated that they received no information from Occupational Health, Environmental and Safety

Services (OHESS) regarding those contractors who were on denied access due to testing COVID-

19 positive or being a close contact. Therefore, they were not able to verify that those individuals

were on denied access and relied on representations from the contractor. The CORs were under

the impression that information should have come from OHESS. However, according to BM&A

leadership interviewed by the OIG, they, along with the Office of the General Counsel, decided the

contractor Certification Memo was sufficient given the limitations on support the Agency could

request due to concerns about the dissemination of personally identifiable information and personal

medical information.

In addition, the Agency relied on self-certification by the contractor (discussed in the “Potential Fraud”

section of this report) that no other COVID-19 relief was received. Without an independent review or

determination as to the accuracy of contractor-provided documentation, there is an increased risk the

Agency was overcharged for CARES paid leave.

Absence of Clear and Comprehensive COR Oversight Procedures. Throughout April 2020, BM&A’s

evolving guidelines included the invoice verification process for government personnel. While the

guidance stated what costs are allowable under CARES and that no invoice will be paid if the COR

cannot obtain reasonable verification that the goods or services were received, the verification steps do

not include the COR determination that the CARES invoice amount was accurate. The verification

steps for reviewing invoices submitted under CARES ultimately included:

• Reviewing dates of the paid leave charges (27 March 2020 or later),

• Confirming the Excel document and certification statement were submitted as required,

and

• Ensuring that profit/fee is not included in charges.

These steps do not include instructions on how to verify the accuracy of the CARES hours or total

claim amounts submitted. In addition, the CARES Hours Tracker included the hourly rate per

individual and the number of hours but did not calculate total dollars. Based on our interviews with

CORs, they claim this made it difficult to compare the Hours Tracker to the e-invoice, and many CORs

did not notice there was a difference in amounts between the e-invoice and the Hours Tracker (see the

“Questionable Differences” section of this report for more detail). We asked the Contracting office

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

12

what type of review the COR was expected to perform to determine whether the hours and amount of

the invoice were accurate. They stated that the CORs are expected to perform a comparative analysis

to validate the number of hours from previous periods as well as the projection for the subject invoice

period. However, this type of analysis was not included in any invoice guidelines provided to the

CORs.

Previously Identified Inadequate COR Oversight. The Audit of Cost-Reimbursement Contracts

(AU19-0010) demonstrated that the Agency had inadequate oversight of the actual costs of cost-

reimbursement contracts due to vague and ineffective COR roles, responsibilities, and oversight

procedures. As a result, the OIG recommended that the Agency develop written procedures

documenting the COR process, including a standard governance structure and standard communication

processes among CORs to support the primary COR function. The OIG also recommended that

the Agency include invoice review responsibilities for all types of CORs and expressly address how

invoices are reviewed for accuracy and completeness (including rates and factors that comprise costs).

This recommendation, when implemented, should address the CARES invoice review deficiencies

identified by the OIG in this audit; therefore, we will not be making a separate recommendation in this

report. The recommendation is repeated below:

RECOMMENDATION AU-19-0010-1 [from the Audit of Cost-Reimbursement

Contracts (AU-19-0010)]

There were more than 2,000 CARES invoices rejected by NSA through October 2020. Accounts

Payable rejected the majority of the invoices due to incomplete or inaccurate supporting documentation;

however, we identified six invoices that were rejected by CORs:

• Four contractor employees charged CARES leave but the respective CORs determined that

the contractors were not in a “ready state.” Some examples under this category included

one contractor who had not yet been issued a badge and, therefore, could not access the

work site, and one contractor who had a health condition that qualified them as high risk

under COVID19.

• One COR stated that they rejected the invoice because the contractor billed for CARES

leave when the contractor was not scheduled to work.

• Another COR stated that the contractor billed hours past 26 September 2020 with no valid

reason for denied access.

13

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

In addition, CORs rejected another 86 invoices because the invoice period was outside of the CARES

time period, and 157 invoices were rejected because of either inaccurate or disputed billing or hours.

The majority, 75 percent, of COR rejections appeared to occur in June 2020 or later, which may

indicate that the reviews were improving as the guidance became clearer and/or more invoices were

reviewed. However, since the COR process is manual and not comprehensive or standardized, not

all CORs perform the same level of detailed review and there are not standards in place to ensure the

continuity of any improvement in this area.

OMB Memorandum 20-22 states:

The federal government’s aggressive response to COVID-19 included an unprecedented

economic relief package, including multiple mechanisms to support federal contractors and

their employees. To ensure relief achieves its desired impact and federal funds are not being

used to make multiple payments for the same purpose, agencies should take the following steps:

a) maintain mission focus and evaluate use of Section 3610 in the broader context of all

strategies to promote contractor resiliency;

b) follow restrictions in Section 3610;

c) work with the contractor to secure necessary documentation to support reimbursement

and prevent duplication of payment; and

d) track use of Section 3610.

The CARES Act requires the amount of reimbursement for paid leave to be reduced by the amount

of credit a contractor has received from other COVID-19 relief programs, such as the Family First

Coronavirus Relief Act (FFCRA) and the Paycheck Protection Program (PPP). However, the CARES

Act does not specify how agencies should vet whether a contractor received other COVID19 relief.

NSA created the Certification Memo for vendors to attest that they have not received and will not

receive credit for the hours for which they are requesting reimbursement. The memo requires vendors

to notify NSA if they do get credit after the fact to ensure the Government is able to recover improper

payments.

The PPP, managed by the Small Business Administration (SBA), provides loans to small businesses as

an incentive to keep their workers on payroll. If businesses meet certain requirements, they are eligible

for PPP loan forgiveness through the SBA. The OIG obtained the SBA PPP loan data for the period

of April through August 2020. We matched the vendors on the PPP loan data to the entire population

of Agency CARES invoices. We identified a number of vendors whose name and address matched

exactly in both data sets.

The SBA also provided other COVID-19 relief in the form of Economic Injury Disaster Recovery Loans

(EIDLs) and EIDL Advances. EIDLs provided relief for small businesses who were experiencing a

temporary loss of revenue in terms of a fixed interest rate loan with a 30-year term and 1-year deferred

payments. EIDL Advances were provided to businesses that were in low-income communities and

had a 30-percent reduction in revenue over an eight-week period up to a maximum of $15,000 and did

not have to be repaid. We matched the vendors on the EIDL data (both advances and loans) to the

entire population of Agency CARES invoices. We identified a number of matches on the business

name for the EIDL Advance data. While it is possible that the vendors used the PPP loans and EIDLs

and EIDL Advances for non-NSA employees, it does raise concerns about the contractor potentially

double dipping. This information was provided to the OIG Office of Investigations for further review.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

14

In addition, contractors were eligible for COVID-19 relief through the FFCRA, Division G, which

provided tax credits to employers for paid sick and paid family and medical leave related to COVID19.

Division G allowed employers a credit against the Social Security Tax imposed (both employer and

employee portions) for each calendar quarter in an amount equal to 100 percent of the qualified sick

leave wages paid by the employer, subject to limitations. Without extensive interagency coordination,

the Agency and the OIG cannot conduct an analysis of tax credits to verify whether any NSA

contractors took advantage of these credits or potentially received duplicative payments as a result.

Because the Agency did not receive separate CARES funding to reimburse contractors for paid leave

and, therefore, had to use current contract funding to pay approximately $900 million in CARES

invoices, the OIG inquired as to how the Agency tracked CARES spending and assessed impacts on

mission and contract completion. We found the following:

Tracking CARES Spending. ODNI requested each agency to aggregate their total expenses incurred

attributed to the CARES Act. Resource Data Analytics was responsible for tracking CARES spending

for the Agency. Resource Data Analytics aggregated the CARES invoices by manually pulling each

CARES Hours Tracker spreadsheet to compile hours, and dollar amounts were pulled from FACTS.

Resource Data Analytics maintained a report of the CARES invoice data from March 2020. As of

8 June 2021, BM&A leadership reported to ODNI, and others, that the amount of CARES invoices

totaled $917 million for 81,000 CARES hours.

C

According to BM&A leadership, NSA has a higher

CARES cost than other IC agencies given that the nature of the work does not allow for many telework

opportunities. NSA reconstituted earlier than some other IC agencies, which, according to BM&A,

helped mitigate CARES Act costs.

Assessing Mission Impact. BM&A leadership stated that the NSA Director and Deputy Director

were aware of the potential for mission impacts due to the implementation of the CARES Act, but

made the decision that health and safety and maintaining a cleared contract workforce was worth

the risk. According to BM&A, the Agency was tracking and reporting CARES Act spending as well

as COVID-19 mission impacts. BM&A told the OIG that program managers worked to minimize

program impacts through requirement trade-offs, schedule delays, implementation of unclassified

telework, exhaustion of contract reserve funding, or recalling certain contractors early. BM&A

leadership stated that the greater mission impacts were due to other COVID-19 restrictions, such as

travel restrictions and deployment delays, rather than Section 3610 paid leave.

Additionally, NSA provided regular COVID-19 impacts to the Under Secretary of Defense as input

into their Defense Intelligence Enterprise COVID-19 Mission Impacts and reported the total monthly CARES

Act expenses to the IC Chief Financial Officer beginning in June 2020.

C

Subsequent to issuance of this report, the Agency indicated to the OIG that the total number of 81,000 CARES hours

was incorrect. The Agency informed the OIG that the correct total for the time period was 6.4 million hours; however

the OIG has not independently verified the accuracy of this revised number. The hours were included in the report as

background information and are not a basis for or relevant to the audit’s findings or recommendations. Moreover, because

the invoiced amounts may include other indirect costs, it would not be possible to determine an hourly rate from these totals.

15

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

Because of insufficient review of CARES Act invoices, the Agency may have incorrectly reimbursed

contractors for paid leave. Insufficient documentation and lack of COR oversight led the OIG to

question approximately 40 percent of the CARES invoices that we reviewed. Moreover, because the

Agency did not receive separate CARES funding, it used current contract funding, which, extrapolated

to the full amount of CARES invoices, could impact current and future contract work and mission

requirements.

RECOMMENDATION AU-20-0008-1

RECOMMENDATION AU-20-0008-2

RECOMMENDATION AU-20-0008-3

RECOMMENDATION AU-20-0008-4

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

16

III. RECOMMENDATIONS

RECOMMENDATION AU-20-0008-1

Perform a thorough review of OIG-sampled CARES invoices with questionable costs, and request

additional contractor documentation necessary to determine accuracy of CARES hours, rates, and

contractor status. If any charges are not allowed, recover as appropriate.

Page: 15

AGREE. The Primary CORs will perform a review of the OIG-sampled CARES invoices to determine

accuracy of CARES hours, rates, and contractor status. If any charges are not allowed, recover as

appropriate.

Implementing Organization: Business Contract Management Groups

OIG Analysis: The action planned meets the intent of the recommendation.

RECOMMENDATION AU-20-0008-2

For invoice 146201-CARES (contact 19-C-0057), ensure credit was received for the hours that the

contractor admitted to billing in error.

Page: 15

AGREE. A credit, in the amount of $2,355.92, was received on 7 February 2022 and approved on

1 March 2022.

Implementing Organization: Cybersecurity & Enterprise Discovery and Information and Intelligence

Analysis Contract Management.

OIG Analysis: CLOSED. Corrective action was taken before report publication and has been verified

by the OIG as sufficient to meet the intent of the recommendation.

RECOMMENDATION AU-20-0008-3

Perform a risk assessment of all CARES invoices and processes to determine, at a minimum, the

nature and extent of testing required to sufficiently identify unsupported payments.

Page: 15

17

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

AGREE. A risk assessment of all CARES invoices and processes to determine the extent of testing

required to identify unsupported payments will be conducted.

Implementing Organization: Business Contract Management Groups

OIG Analysis: The action planned meets the intent of the recommendation.

RECOMMENDATION AU-20-0008-4

Based on the results of Recommendation AU-20-0008-3, perform a review of CARES invoices to

ensure accuracy of CARES hours, billing rates, and contractor COVID-19 status, and, if necessary,

recover costs from inaccurate billing.

Page: 15

AGREE. Based on the results of recommendation AU-20-0008-3, the Primary CORs will review the

CARES invoices to ensure the accuracy of CARES hours, billing rates, and contractor COVID-19

status and, if necessary, recover costs from inaccurate billing.

Implementing Organization: Business Contract Management Groups and Office of Contracting

OIG Analysis: The action planned meets the intent of the recommendation.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

18

APPENDICES

The objective of this audit was to determine whether NSA economically, effectively, and efficiently

implemented Section 3610 of the CARES Act.

Fieldwork for this audit was conducted from July 2020 through July 2021. The scope of the audit was

CARES Act requests for reimbursement and payments.

We reviewed written processes, procedures, and other documentation for adequate controls. We

conducted interviews of personnel in Accounts Payable, Contracting, BM&A leadership, and CORs

across multiple directorates who are responsible for or have specified roles in CARES Act, Section 3610

reimbursement.

We performed data analytics of the CARES invoices to include:

• A review of vendors submitting both CARES and non-CARES invoices for the same time

period,

• A comparison of historical vendor payments to CARES invoices, and

• A search for CARES invoices for goods-only contracts.

We conducted this performance audit in accordance with generally accepted government auditing

standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate

evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives.

We believe that the evidence obtained provides a reasonable basis for our findings and conclusions

based on our audit objectives.

We received a population of CARES Act reimbursement payments from 27 March 2020 through

31 August 2020 from the Contracting office.

20

We selected a random sample of contracts from each of

the six contract types (i.e., Time & Materials, Cost Plus Fixed Fee, Cost, Cost Plus Award Fee, Labor

Hour, Firm-fixed Price). The number of contracts we randomly selected from each contract type was

judgmental based on the number of invoices for a total of 25 sampled invoices totaling approximately

20

There were a total of 2,145 CARES invoices submitted to the Agency from 27 March 2020 through 31 August 2020.

19

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

$37.9 million. We also judgmentally selected an additional 20 invoices, totaling $3.23 million, from

a population of CARES invoices with a POS prior to 31 March 2020 or after 30 September 2020

(the initial CARES period). For each invoice, we reviewed supporting documentation, including the

CARES Act invoice and backup documentation, signed Certification Memo, CARES Hours Tracker

spreadsheet, and COR approvals. We also met with CORs responsible for reviewing and approving

CARES invoices.

We used computer-processed data from FACTS to select a population of CARES invoices. We used

data from the eCPRL tool and COR tool to assist our review of the invoices. We did not attempt to

assess the completeness of FACTS, the eCPRL tool, or the COR tool because it was not relevant to

the context of our audit. Our testwork involved tracing invoices from the FACTS population to source

documents. In addition, any inconsistencies or issues noted with the eCPRL or COR tools were

followed up by interviews with CORs.

There was no previous OIG coverage of this topic.

Public Law 116-136, Coronavirus Aid, Relief, and Economic Security Act, Section 3610, issued

27 March 2020, permits federal agencies, under certain circumstances, to modify terms of existing

contracts or agreements and to reimburse federal contractors’ compensation due to COVID-19 related

issues.

Defense Federal Acquisition Regulation Supplement 231.205-79(a)(1)(i), CARES Act Section

3610 Implementation, issued 8 April 2020, provides a framework for CARES Act, Section 3610

implementation.

Office of Management and Budget Memo M-20-18, Managing Federal Contract Performance Issues

Associated with the Novel Coronavirus, issued 20 March 2020, identifies steps to help ensure the safety of

federal contractors while maintaining continued contract performance in support of agency missions,

wherever possible.

Office of Management and Budget Memo M-20-22, Preserving the Resilience of the Federal Contracting

Base in the Fight Against the Coronavirus Disease 2019, issued 17 April 2020, provides supplemental

guidance for the implementation of CARES Act, Section 3610.

Office of Management and Budget Memo M-20-27, Additional Guidance on Federal Contracting

Resiliency in the Fight Against the Coronavirus Disease, issued 14 July 2020, provides additional guidance

that further addresses the resiliency of the federal acquisition workforce and federal contractors who

support agency missions.

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

20

Office of the Under Secretary of Defense Memo 2020-00013, Class Deviation – CARES Act Section

3610 Implementation, issued 8 April 2020, provides a framework for CARES Act, Section 3610

implementation.

Office of the Under Secretary of Defense Memo, Implementation Guidance for Section 3610 of the CARES

Act, issued 9 April 2020, provides supplemental guidance for the implementation of the CARES Act,

Section 3610.

Office of the Under Secretary of Defense Memo, Assessment of Other COVID-19 Related Impacts and

Costs, issued 2 July 2020, provides guidance on the assessment of costs and delays due to COVID-19.

Office of the Director of National Intelligence for Enterprise Capacity, IC Guiding Principles for

the IC Acquisition & Procurement Community on Implementation of the CARES Act, issued 3 April 2020,

provides the IC community with guiding principles to address procurement issues during pandemic

mitigation.

NSA/CSS Policy Manual 4-19, Health and Safety of the Workforce, issued 30 October 2020, establishes

standards and procedures to ensure the health and safety of NSA/CSS affiliates and contractors who

have been exposed to or are in danger of being exposed to a communicable disease in the event of a

declared public health emergency.

NSA/CSS COVID-19 webpage provides continuously updated guidance for NSA contractors.

As part of the audit, we assessed the internal control environment as outlined in NSA/CSS

Policy 73, Managers’ Internal Control Program, issued 17 October 2016. We focused on internal controls

when assessing processes and procedures for the implementation of CARES Act, Section 3610. We

reviewed the vulnerability and process assessment for Accounts Payable. We did not identify any

significant control deficiencies pertaining to this audit. Through interviews, reviews of procedures,

and testing, we assessed the control environment, risk assessment, control activities, information and

communication, and monitoring, and found there is a lack of controls to ensure the accuracy of

CARES reimbursement payments.

21

AU-20-0008

Audit of the Implementation of the CARES Act, Section 3610

IC

AO Acceptance Officer

ARC Acquisition Resource Center

BCMO Business and Contract Management Office

BM&A Business Management & Acquisition

CARES Coronavirus Aid, Relief, and Economic Security

CO Contracting Officer

COR Contracting Officer Representative

COR-T Contracting Officer Representative - Technical

COVID-19 Coronavirus Disease 2019

CSS Central Security Service

DoD Department of Defense

ECI Electronic Commerce Interface

eCPRL Electronic Contractor Position Roster Log

EIDL Economic Injury Disaster Recovery Loan

FFCRA Family First Coronavirus Relief Act

FMR Financial Management Regulation

FTE Full time equivalent

Intelligence Community

MPO Maryland Procurement Office

NSA National Security Agency

ODNI Office of the Director of National Intelligence

OHESS Occupational Health, Environmental and Safety Services

OIG Office of the Inspector General

OMB Office of Management and Budget

POC Point of contact

POS Period of service

PPP Paycheck Protection Program

SBA Small Business Administration

Audit of the Implementation of the CARES Act, Section 3610

AU-20-0008

22

OFFICE OF THE INSPECTOR GENERAL

How to Reach Us

HOTLINE