STATE OF MARYLAND

REGISTER OF WILLS

SAMPLE GUIDE

FOR FILING ACCOUNTS

Within nine months of the date of appointment, an initial account must be filed.

The following is an example of a First and Final Account. It should be used as a guide and checklist only.

All accounts must include the original signatures of all personal representatives and attorney for the estate,

if applicable.

THIS SAMPLE GUIDE IS APPLICABLE FOR A DATE OF DEATH ON OR AFTER JULY 1, 2010

UNLESS OTHERWISE NOTED

CONTACT THE REGISTER OF WILLS FOR GUIDANCE FOR A DATE OF DEATH

PRIOR TO JULY 1, 2010

Account Overview

The purpose of an account is to report all financial activity involving probate assets from the date of death of

the decedent to the end of the current accounting period. The initial account is due nine months after the date

of appointment of the personal representative.

There are two types of accounts, an interim account and a final account. With an interim account, not all estate

assets are distributed. After filing an interim account, the estate will remain open and each subsequent account

will be due six months from the approval of the prior account or nine months from the date the prior account

was filed, whichever occurs first, until the estate is closed by Court approval of the final account. With a final

account, all estate assets will be accounted for and upon the approval of the account, if no exceptions are

timely filed, the estate will close. No additional documents will be required by this office after the order

approving the final account becomes final.

You may prepay probate fees, and taxes due to this office; however, the probate fee will not be assessed until

after the filing of the first account. The inheritance tax will be assessed when distribution is shown in an

account. A bill will be sent to you from this office. This does not apply to non-probate inheritance tax which is

billed separately by this office. (See page 16 for calculation of the probate fee.)

Account Checklist

Before submitting your account, make sure the following items are completed and included:

0 Verification of the account signed by all personal representatives. (See page 13 and form on page 14.)

Note: If the personal representative is represented by an attorney, the attorney must sign the account

pursuant to Md. Rule 6-134(a).

0 Certificate of Service attesting to the fact that notice of the account has been sent to all interested

persons. Certificate must be signed by personal representative or attorney, if applicable. (See page 13

and form on page 14.)

0 Account includes Summary (page 1 of sample account) and Schedules 1 through 7 (pages 2 through

14 of sample account), and any supporting documentation.

Schedule 7 (page 12) is applicable only if the account is not a final account.

Note: The suggested format of the sample account is not required; however, your account must contain

the applicable information and documentation as described in the sample account.

0 The CLAIMS DOCKET at the Register of Wills Office has been reviewed prior to the estate closing to

verify all claims against the estate have been paid in full, settled, or formally disallowed. (See page 15

for overview of claims.)

0 Ensure that all figures balance. The sum of the beginning balance (Schedule 1); principal receipts

(Schedule 2); change in assets (Schedule 3); and income (Schedule 4) should equal the sum of the

disbursements (Schedule 5); distribution (Schedule 6) and, if applicable, balance retained for future

accounting (Schedule 7).

The following pages are an example of a First and Final Account, with explanation.

You may choose to follow this layout when preparing your account.

NOTE: INHERITANCE TAX RATES ARE DETERMINED BY THE DATE OF DEATH OF THE

DECEDENT AND THE RELATIONSHIP OF THE HEIR OR LEGATEE TO THE DECEDENT.

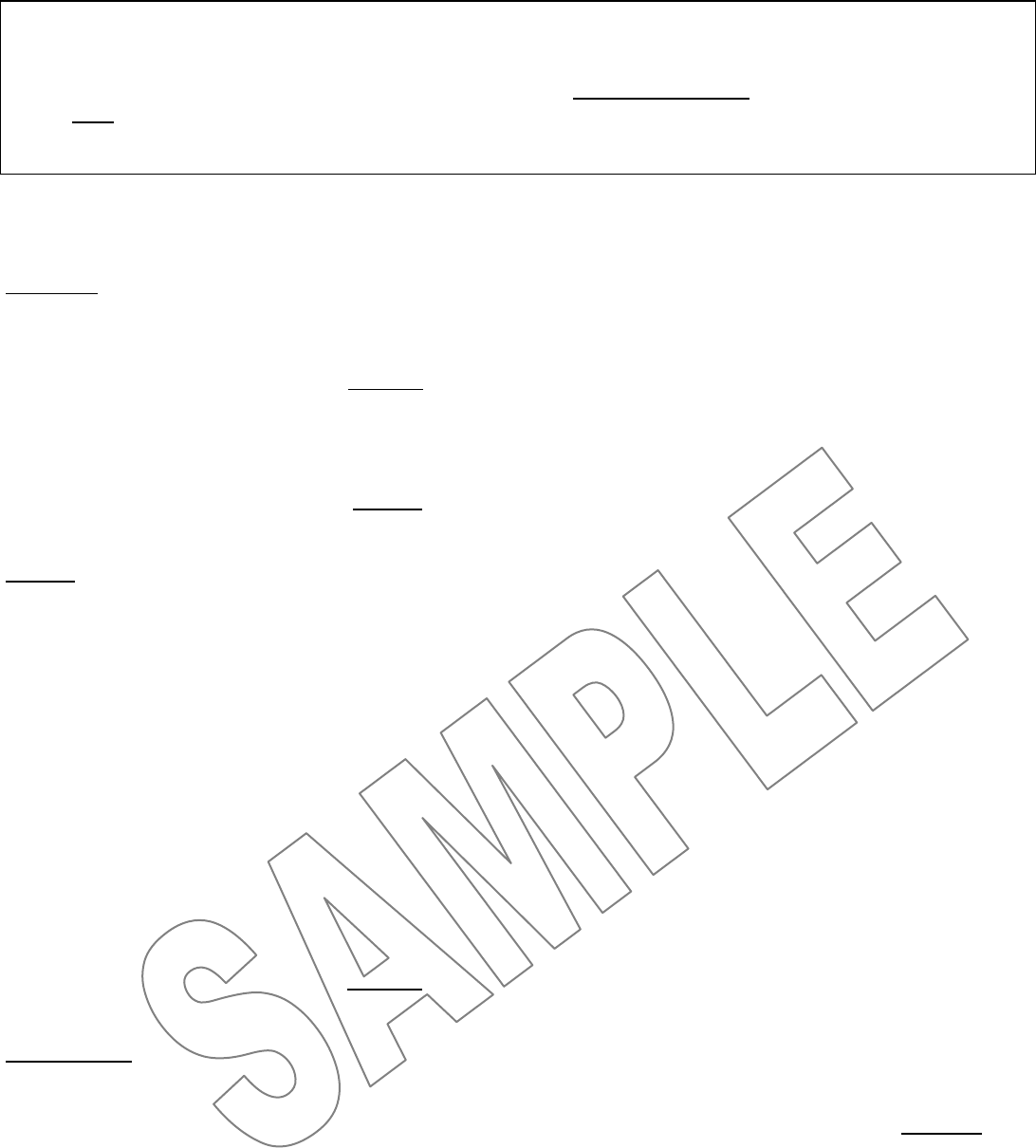

IN THE ORPHANS’ COURT FOR (_______________________________), MARYLAND

ESTATE OF (Decedent’s Name) ESTATE NO. W20000

Date of Death: January 1, 2015

FIRST AND FINAL ACCOUNT (or INTERIM ACCOUNT)

of _ (Personal Representative)__

(or Successor Personal Representative or Special Administrator)

for the period beginning January 1, 2015

1

and ending October 31, 2015

2

SUMMARY OF TRANSACTIONS RECEIPTS

DISBURSEMENTS

Total Beginning Balance

from SCHEDULE 1 $ 617,806.59

Total Miscellaneous Principal Receipts

from SCHEDULE 2 9,727.75

Total Changes In Assets

from SCHEDULE 3 16,966.06

Total Income

from SCHEDULE 4 7,801.61

Total Disbursements

from SCHEDULE 5 $ 58,550.76

Total Distributions and Inheritance Tax

from SCHEDULE 6 593,751.25

Total Balance Retained For Future Accounting

from SCHEDULE 7 -0-

TOTALS $ 652,302.01 $ 652,302.01

1

1

When filing the First and Final Account (or First Account if not a final), the accounting period begins as of the date of

death.

2

The deadline for filing the First Account is 9 months after date of appointment of the personal representative. In this

example the personal representative was appointed February 15, 2015. The deadline for filing the account is

November 15, 2015.

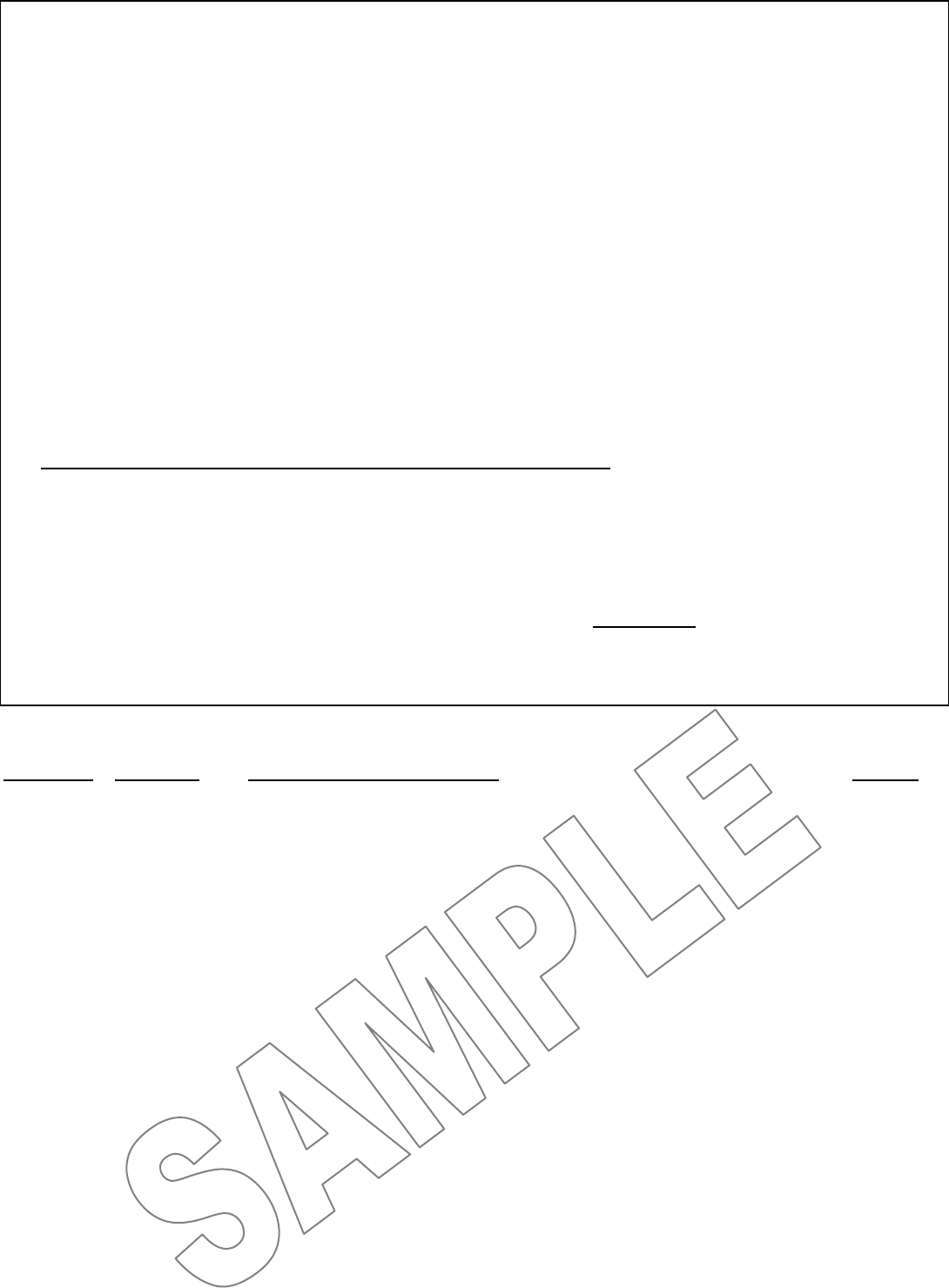

The Summary Page provides an overview of the entire account. A supporting schedule for each

figure reported on the summary page is included.

Schedule 1 of a First Account reflects the date of death value of the assets solely owned by the decedent,

or held as a tenant in common, as reported on all Inventories filed with this office. If the first account is not also

a final account, the subsequent account will reflect the balance of the assets retained from the previous

account as itemized on Schedule 7 of the previous account.

SCHEDULE 1 - Beginning Balance

ASSETS PER INVENTORY (or assets carried forward from prior account)

Schedule

A Real Property

405 Main St., Rockville, MD $325,000.00

5764 Frederick Rd., Gaithersburg, MD 98,000.00

B Leasehold -0-

C Tangible Personal Property 3,400.00

D Corporate Stocks 59,812.00

E Bonds, Notes, Mortgages, Debts 98,283.44

F Bank Accounts, Savings & Loan Accounts, Cash 22,311.15

G All Other Interests 11,000.00

TOTAL $617,806.59

2

Schedule 2 includes all miscellaneous collections not otherwise reported by Schedule 1 (beginning

balance), Schedule 3 (changes in assets) or Schedule 4 (income earned on probate assets after date of

death).

Note the following:

1. If the receipt represents a refund, in whole or in part, of a payment that was made during the

administration of the estate, include that information in the description of the receipt. See example below

of the “partial refund of fiduciary income tax.”

2. An adjustment for a payment made by the decedent or the estate in advance of a real estate sale, such

as pre-paid county property taxes shown on the Closing Disclosure form, Line F.04, is reported on

Schedule 2.

If the estate is subject to inheritance tax, also note the following:

1. The portion of the income receipt accruing, or earned, before the date on which a decedent dies is

designated as principal. For example, regular quarterly dividends earned prior to death are considered

principal, even if the payment of the dividends is not made until after the date of death. The principal

portion is shown on Schedule 2. (A principal receipt reported on Schedule 2 is subject to inheritance tax if

it passes to a person not exempt from tax according to Tax-General § 7-203.)

2. The dividends earned after death are considered income and reported on Schedule 4. (An income receipt

reported on Schedule 4 is exempt from inheritance tax even if it passes to a person otherwise subject to

inheritance tax.)

SCHEDULE 2 - Miscellaneous Principal Receipts

01/31/15 Final payment of accrued salary $ 2,350.00

01/31/15 Accrued vacation pay 1,275.00

02/01/15 Insurance policy payable to estate

RMD Insurance Company 5,000.00

02/14/15 Refund – Washington Sun Newspaper 6.20

02/26/15 Reimbursement - Blue Cross/Blue Shield Insurance 111.62

05/07/15 Adjustment for pre-paid property tax on sale of

405 Main Street - per Closing Disclosure form 910.04

10/15/15 Partial refund of fiduciary income tax – payment of tax 74.89

shown as expense on Schedule 5 ___________

TOTAL $ 9,727.75

All sums deposited in estate money market account #0000004321

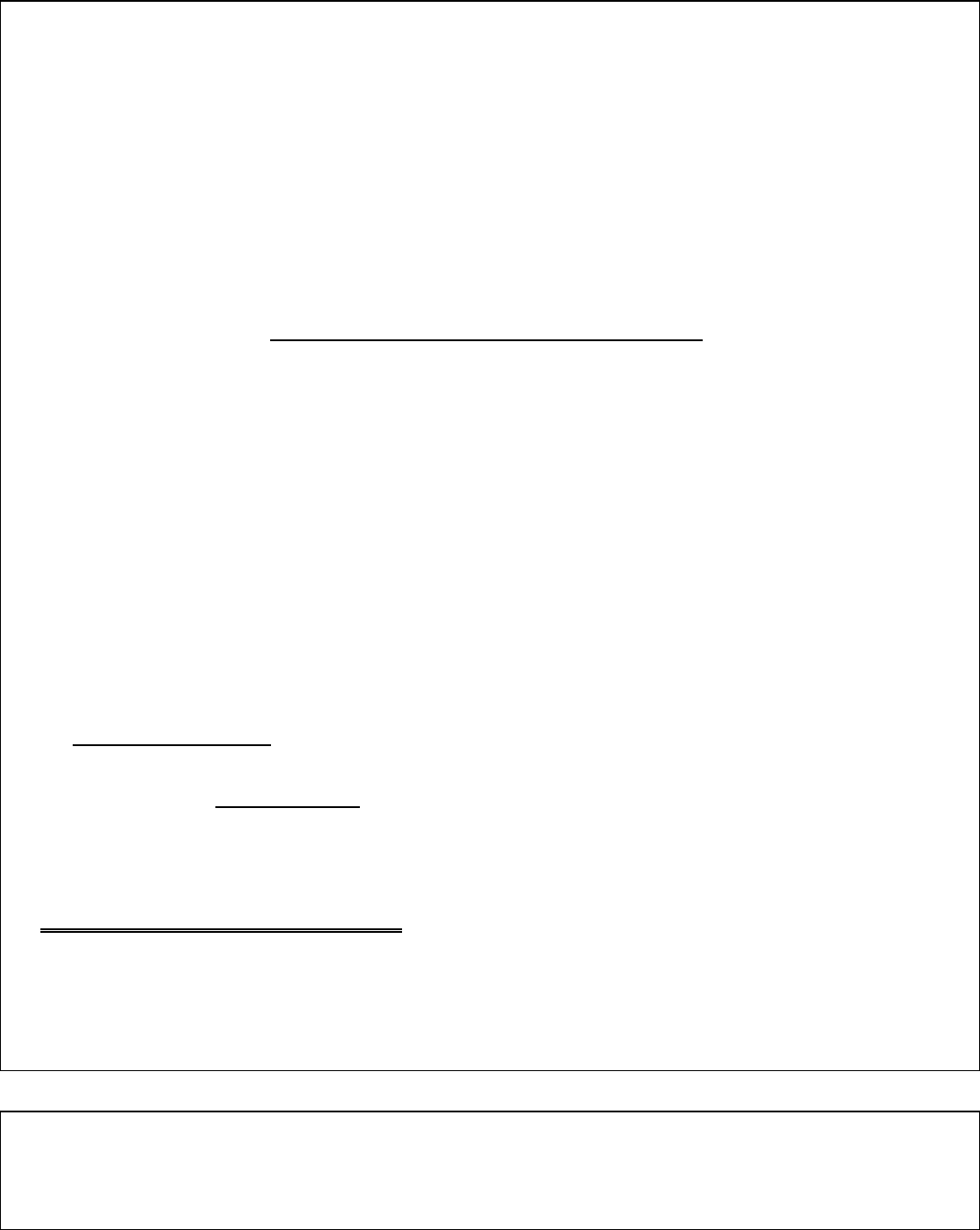

3

Schedule 3 is a summary of changes in assets including sales, redemptions, transfers, purchases,

adjustments to inventory values, stock splits, changes of corporate names, etc.

Any gain or loss realized from a transaction is to be shown on this schedule. For example, when real

property is sold, the gain or loss is calculated based on the difference in the inventory value and the contract

sales price. (See example below.) Provide a copy of the Closing Disclosure form.

A gain or loss due to market fluctuation should not be included on this schedule unless it has been

approved by the court pursuant to Estates and Trusts § 7-204.

Documentation of transactions such as the sale of tangible personal property or securities may be

required. Examples of documentation include a bill of sale and broker’s statement.

EFFECTIVE FOR DECEDENTS DYING ON OR AFTER JANUARY 1, 1998: The inheritance tax is not

assessed on a gain realized on the sale of a probate asset. Additionally, the inheritance tax is not reduced by a

loss realized on the sale of a probate asset. The inheritance tax is based on the value of the asset as reported

in the Inventory. However, realized gains/losses are subject to accounting by a personal representative.

SCHEDULE 3 - Changes in Assets

Including Gains and Losses

01/15/15 Bank accounts reported on inventory closed and $ -0-

transferred to estate money market account at

Rockville Nat’l Bank – estate acct. #0000004321

03/08/15 GMAC Note redeemed at $100,000.00

Inventory value 98,283.44

Gain 1,716.56

Proceeds deposited in estate acct. #0000004321

05/07/15 405 Main Street sold for (contract sales price)

1

338,500.00

Inventory value

325,000.00

Gain 13,500.00

Proceeds deposited in estate acct. #0000004321

06/10/15 Office Building Partnership

Inventory value 11,000.00

Capital distribution received and deposited

to estate acct. #0000004321 5,000.00

Carrying value 6,000.00

Net Gain or Loss -0-

07/31/15 ABC Corp. - 1000 shares sold at 32,499.00

Inventory value 30,125.00

Gain 2,374.00

Proceeds deposited in estate acct. #0000004321

07/31/15 XYZ Corp. - 500 shares - Inventory value 29,687.00

Sold at 29,062.50

Loss (624.50)

Proceeds deposited in estate acct. #0000004321

TOTAL $ 16,966.06

4

1

Expenses in connection with the sale of the real property are reported on Schedule 5.

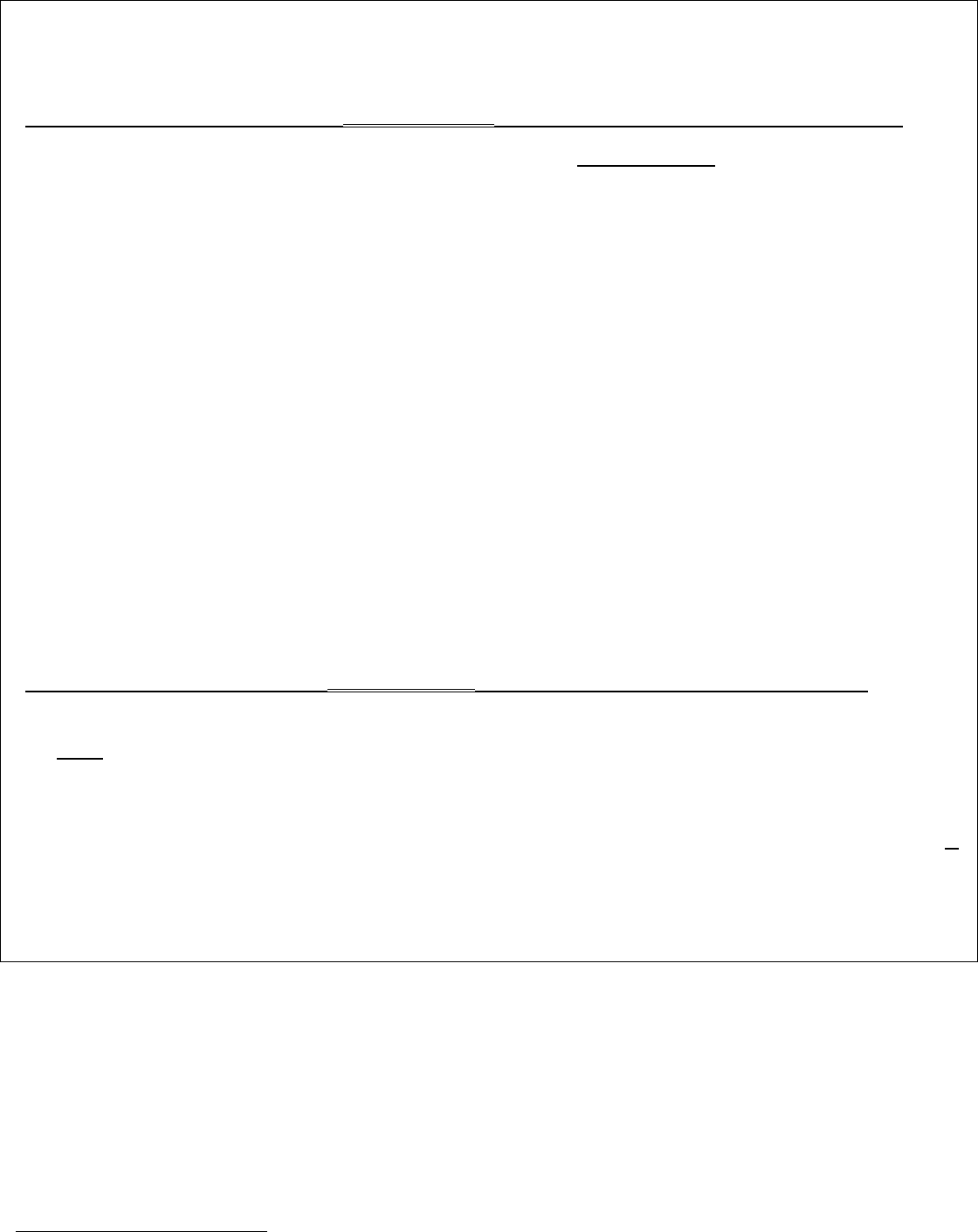

Schedule 4 is an itemization of all income earned on estate assets since the date of death (or during the

accounting period if not a first account). Set forth the source, date and amount of each receipt.

EFFECTIVE FOR DECEDENTS DYING ON OR AFTER JANUARY 1, 1998: Income earned on probate

assets after the date of death is not subject to inheritance tax, but is subject to accounting by a personal

representative. Tax-General § 7-203(j)

SCHEDULE 4 – Income

Dividends

ABC Corp. 01/31/15 $490.00

04/30/15 490.00

07/31/15 490.00

$ 1,470.00

XYZ Corp. 01/31/15 150.00

04/30/15 150.00

07/31/15 150.00

450.00

Interest

02/15/16 - Estate Bank Account

interest earned through 09/01/15 220.45

03/08/16 - GMAC NOTE

interest earned from 01/02/15 - 03/08/15 2,698.75

Rockville National Bank - estate money market - acct. #0000004321

01/31/15 23.20

02/28/15 75.67

03/31/15 165.29

04/30/15 198.16

05/31/15 210.47

06/30/15 257.62

07/31/15 272.50

08/31/15 306.50

09/30/15 326.00 1,835.41

Other Income

08/31/15 - Income distribution (profit earned) on Office Bldg. Partnership

from 01/01/15 – 08/01/15 ____1,127.00

TOTAL $ 7,801.61

5

Schedule 5 includes all disbursements made by the personal representative during administration of the

estate or during the accounting period if the account is not a First and Final Account.

Allowable expenses include payments of the following: reasonable funeral expenses (see page 15); family

allowance (see page 15); debts due by the decedent which had not been paid as of date of death; unpaid

expenses of last illness; bond premium; publication cost; bank service charges; federal estate taxes; Maryland

estate taxes (see page 19); fiduciary income taxes (see page 19); expenses incurred from a sale, transfer or

redemption of an asset; court costs and probate fee (see page 16); fees to the attorney for the estate and

personal representative’s commission (CAUTION - payment of fees or commissions may not be made until

approved by court order or consents are filed. See pages 17 and 18.) See page 18 regarding the proposed

payment to the personal representative or attorney of record for a claimed debt existing prior to the death of

the decedent.

Maintenance expenses, including utilities, generated by non-income producing real property, are generally

not allowed beyond the time for filing claims (6 months after date of death). When sale of the real property is

directed by the Will or becomes essential in order to pay claims and expenses, necessary maintenance

expenses may be considered. Mortgage payments will be allowed. Credit for any outstanding mortgage

balance at the time of distribution will be allowed to offset inheritance tax. (If the property produces a

reasonable amount of rental income, maintenance expenses may be allowed beyond the claims period of six

months after the date of death.)

Closing Disclosure forms for real property sales must be submitted.

Vouchers (such as copies of cancelled checks, invoices, or bank statements) to support disbursements or

other transactions may be requested by the auditor. Copies of the estate bank account statements may also be

requested by the auditor.

Documentation evidencing payment in full of a claim filed against the estate may be required.

Note: When a provision in the Will directs the inheritance tax on non-probate property (reported on the

Information Report) be paid out of the residuary (probate) estate, the tax on the non-probate property is

calculated at the rate of 11.11111%. The inheritance tax is considered an expense of the estate and is

reported as a expense on Schedule 5.

SCHEDULE 5 – Disbursements

Check No.

Date Paid

Payee and nature of expense

Amount

101

01/03/15

Rockville Funeral Home

$ 10,223.16

102

01/03/15

Rockville Cemetery

995.00

n/a

01/15/15

Money Market check printing charges –

charged to estate account #000004321

18.00

103

01/15/15

Mary Doe, reimburse for funeral expense paid to Rev. Jones

100.00

104

02/28/15

PEPCO - Main Street property - administration expense

119.00

105

02/28/15

Local paper for publication of Notice to Creditors

60.00

106

02/28/15

Bond Company, Inc. – Estate Bond

100.00

107

02/28/15

Dr. Smith – expense of last illness

145.00

108

109

03/15/15

03/15/15

Rockville Hospital – expense of last illness

X-Ray Techs. – expense of last illness

Balance Forward

795.00

23.00

$ 12,578.16

6

Check No.

Date Paid

Payee and Nature of Expense

Balance Forward

$ 12,578.16

110

03/15/15

Visa Credit Card - debt of decedent

253.00

111

03/30/15

Local Store Credit Card - debt of decedent

52.00

112

03/30/15

PEPCO - Main Street property - administration expense

155.00

113

03/30/15

Rockville Fuel Oil - Main St. property - admin. expense

115.00

114

04/15/15

WSSC - Main Street property - administration expense

23.00

115

04/15/15

Appraiser’s Inc. – appraisal of real property

600.00

116

04/15/15

Bill’s Appraisal Service – appraisal of tangible personal property

100.00

117

04/15/15

Mary Doe, spouse - family allowance

10,000.00

1

118

04/15/15

James Doe, minor child of decedent, c/o Mary Doe, parent

5,000.00

119

04/30/15

PEPCO - Main Street property - administration expense

63.36

120

04/30/15

Rockville Fuel Oil - Main St. property - admin. expense

127.00

121

05/07/15

PEPCO - Main St. property - admin. expense (final bill)

4.00

n/a

05/07/15

Expenses of sale of Main Street property -

per attached Closing Disclosure form

Realtor’s commission $ 10,155.00

Loan origination fee 1,246.50

Title search 95.00

Document preparation 75.00

Courier fee 35.00

Payoff of mortgage loan 12,782.47

24,388.97

n/a

07/03/15

Local stockbroker’s fee for sale of stock - per broker’s statement

316.27

122

08/01/15

IRS - Fiduciary Income Tax - administration expense

505.00

123

08/05/15

Clerk of Circuit Court–recording deed-Frederick Rd. real property

20.00

124

11/15/15

Register of Wills for Montgomery County - probate fee ($750) paid

herewith

750.00

n/a

to be paid

Attorney’s Fee - subject to Court approval

(Petition and proposed order filed.)

3,500.00

TOTAL DISBURSEMENTS

7

$ 58,550.76

1

For date of death prior to October 1, 2013, see page 15 (Family Allowance) for the applicable allowance for a surviving

spouse and minor child of the decedent.

Schedule 6 includes all distributions to the beneficiaries of the estate, which were made during the

accounting period. Also includes all proposed distributions (distributions that will be made within 30 days after

the order approving the account becomes final). Itemize the assets distributed or proposed to be distributed

pursuant to the terms of the Last Will and Testament or the laws of intestate succession.

If the decedent died without a Will, distribution must be in accordance with the laws of intestate succession

established by the Estates and Trusts Article of the Annotated Code of Maryland, Title 3, Subtitle 1. See How

Will My Estate Be Distributed If I Die Without A Will on page 20.

Authority for Maryland Inheritance Tax is established by

Title 7 of the Tax-General Article, Annotated Code of Maryland

INHERITANCE TAX EXEMPTIONS (TAX-GENERAL § 7-203)

for Date of Death On or After JULY 1, 2010:

The inheritance tax does not apply to the receipt of property that passes from a decedent to or for the use of:

(1) a grandparent of the decedent;

(2) a parent of the decedent (“parent” includes a stepparent or former stepparent);

(3) a surviving spouse of the decedent (“surviving spouse” means a surviving spouse who has not remarried);

(4) a child of the decedent or a lineal descendant of a child of the decedent (“child” includes a stepchild or

former stepchild);

(5) a spouse of a child of the decedent or a spouse of a lineal descendant of a child of the decedent;

(6) a surviving spouse of a deceased child of the decedent or of a deceased lineal descendant of a child of the

decedent who was married to the child or lineal descendant of the child at the time of the child’s or lineal

descendant’s death;

(7) a brother or sister of the decedent; or

(8) a corporation, partnership, or limited liability company if all of its stockholders, partners, or members

consist of individuals specified in items 1 through 7 above.

Additionally, inheritance tax does not apply:

(1) if a charitable organization is exempt under Section 501(c)(3) of the Internal Revenue Code, or on certain

transfers which are deductible under § 2055 of the Internal Revenue Code;

(2) to the receipt of the family allowance to the surviving spouse and minor child of a decedent under Estates

and Trusts § 3-201;

(3) to the receipt of property that passes from a decedent to any one (1) person if the total value of the

property does not exceed $1,000.00;

(4) For date of death after January 1, 1998, distribution of income, including gains and losses, accrued on

probate assets after the decedent’s date of death must be reported, but is not subject to inheritance tax.

(See Schedules 3 and 4, and Example 3 on page 11)

(5) Real property that is subject to a perpetual conservation easement for the use of farming purposes only

and passes to a niece or nephew of the decedent.

NOTE: For a date of death occurring BEFORE JULY 1, 2010, contact the Register of Wills for applicable

inheritance tax exemptions.

Pursuant to the Estates and Trusts §§ 7-101(b) and 9-104, assets shall be distributed in kind to the extent

possible and within the time for filing the first account. See Schedule 7 if final distribution is not possible.

8

SCHEDULE 6 - Distribution and Inheritance Tax (continued)

Calculation of inheritance tax on a specific bequest that passes to a person not exempt from tax:

· If the Will contains a sufficient tax clause

1

, inheritance tax on a specific bequest is not subtracted from the

bequest. The tax is calculated on the total amount of the bequest at the rate of 11.11111%. For example, if

a legatee

2

receives a specific bequest of $10,000, the legatee receives the full amount of the bequest

($10,000) and an inheritance tax of $1,111.11 (10,000 x 11.11111%) is paid by the personal representative

out of the “rest and residue” or “residuary” of the estate. (The inheritance tax is considered an “expense” of

the estate.)

· Absent a tax clause, the specific bequest must be reduced by the inheritance tax at the appropriate rate of

10%. (A specific bequest of $10,000 is reduced by an inheritance tax of $1,000 ($10,000 x 10%); thereby

reducing the distribution to the legatee to $9,000.) The inheritance tax of $1,000 is paid by the personal

representative to the register.

Note: When the Will directs that a legatee under the Will is to receive a bequest of a specific item of property,

such as real property or a particular stock, the personal representative is to determine the amount of net

principal receipts (portion subject to inheritance tax) and income receipts (portion exempt from inheritance tax)

in connection with that specific bequest and is to distribute same to the legatee who is to receive the specific

property. For example, if the Will directs that a specific stock be distributed to a particular person, the dividends

earned on that stock after the date of death are included in the distribution to that person. Another example is

real property. If a person is to receive a specific piece of real property, any rental income and any expenses

incurred after the date of death in connection with that property is allocated or assigned to that legatee. See

E&T § 15-503.

Calculation of inheritance tax on residuary estate that passes to person not exempt from tax:

· When a partial distribution of the residuary estate is reflected in an interim account and inheritance tax

is not withheld from the partial distribution, the higher rate (11.11111%) is applied to the actual amount

received by the beneficiary. (The tax is considered an expense of the estate. If the tax is not shown in the

account when the distribution is reported, the tax may be shown in a subsequent account.)

· When a partial distribution of the residuary estate is reflected in an interim account and the inheritance tax is

withheld from the partial distribution, the tax rate of 10% is applicable.

· The inheritance tax on the final distribution of the residuary estate is always calculated at the rate of 10%.

9

1

A “tax clause” is a provision in a Will that directs the source for payment of the inheritance tax. Used here, a sufficient tax

clause designates the “rest and residue” or “residuary” estate as the source for payment. (The “rest and residue” of the

estate are the assets remaining after the payment of all debts, expenses and specific bequests.)

2

A “legatee” is a person who would receive any property disposed of by a Will.

SCHEDULE 6 – Distribution and Inheritance Tax (continued)

EXAMPLE 1

In the following, the distribution includes a specific bequest of $2,000 to the decedent’s nephew, Bob Smith.

As a nephew, he is subject to inheritance tax. The Will does not contain a tax clause directing the

inheritance tax to be paid from the residuary estate. Therefore, the specific bequest to Bob Smith is reduced by

the inheritance tax of $200 ($2,000 x 10% = $200).

Available Balance for Distribution:

Sum of Schedules 1, 2, 3 & 4, $593,751.25

minus Schedule 5

St. Joseph’s Church – per Item III of Will

Tax exempt under IRS Code 501(c)(3) $ 1,000.00

Paid by check #124 on 9/15/15

Bob Smith, Nephew – per Item V of Will $ 2,000.00

Subject to Inheritance Tax at 10% ( 200.00)

Paid to Register of Wills 200.00

Paid to Bob Smith by check #126 on 9/15/15 1,800.00

John Doe, Jr., Brother – per Item IV of Will 35,000.00

Exempt from Inheritance Tax

Paid by check #125 on 9/15/15 35,000.00

Mary Doe, Spouse – per Item IX of Will 98,000.00

Real Property – 5674 Frederick Rd

Exempt from Inheritance Tax 98,000.00

Deed Recorded 9/15/15

Mary Doe, Spouse – per Item X of Will

Exempt from Inheritance Tax

Rest and Residue of Estate consisting of

Personal property – distributed 7/4/15 3,400.00 3,400.00

Partnership – distributed 7/30/15 6,000.00 6,000.00

Cash balance to be distributed

upon approval of this account 448,351.25 448,351.25

TOTAL DISTRIBUTIONS AND INHERITANCE TAX $ 593,751.25

Summary of total fees and inheritance tax due to Register of Wills

and paid herewith by check #124

Probate fee/costs per Schedule 5 $ 750.00

Collateral Inheritance Tax at 10% 200.00

TOTAL PAID $ 950.00

10

Schedule 6 – Distribution and Inheritance Tax (continued)

EXAMPLE 2

When the Will contains a tax clause directing the inheritance tax to be paid from the residuary estate, the

distribution of the specific bequest of $2,000 to the decedent’s nephew, Bob Smith, is shown as follows:

Bob Smith, Nephew – per Item V of Will $ 2,000.00

Subject to Collateral Inheritance Tax at 11.11111% 222.22

Paid to Register of Wills 222.22

Paid to Bob Smith 2,000.00

Bob receives the total amount of the bequest ($2,000) and the inheritance tax ($222.22) is paid by the personal

representative from the estate. It is “as if” Bob receives an additional bequest in the amount of $222.22, paid

on his behalf by the estate. As a result, the value of the estate available for distribution to the residuary legatee

is reduced by the payment of inheritance tax on the specific bequest.

EXAMPLE 3

Applicable for a date of death on or after January 1, 1998: The inheritance tax does not apply to the receipt of

property that is income, including gains and losses, accrued on probate assets after the date of death of the

decedent. Tax-General § 7-203(j)

Therefore, only the principal portion of the distribution to a collateral

1

heir or legatee is subject to

inheritance tax. The Changes in Assets (Schedule 3) and Income (Schedule 4) are tax exempt.

An additional calculation is needed to determine the correct inheritance tax.

The example below illustrates the inheritance tax on the final distribution of the residuary estate to an

heir or legatee subject to inheritance tax.

The decedent left a Will directing distribution of the total available balance for distribution (Schedule 6) to a

legatee not exempt from inheritance tax OR the decedent did not leave a Will and the total balance is

distributed to an heir not exempt from inheritance tax.

Available Balance for Distribution:

(sum of Schedules 1, 2, 3 & 4, $593,751.25

minus Schedule 5)

Consisting of:

Principal $ 568,983.58

(sum of Schedules 1 and 2, minus Schedule 5)

Income and Changes in Assets

2

24,767.67

(sum of Schedules 3 and 4) _________

Total 593,751.25

To Bob Smith, Nephew – final distribution

Principal (subject to inheritance tax) 568,983.58

Less Inheritance Tax at 10% (568,988.58 x 10%) ( 56,898.36)

Net Principal to Nephew 512,085.22

Income/Changes (tax exempt) to Nephew 24,767.67

Inheritance tax to Register of Wills 56,898.36

Total $ 593,751.25

11

1

A collateral heir or legatee is a person not exempted from inheritance tax by Tax-General § 7-203.

2

When the sale of an asset of the estate results in a gain to the value of the estate, the gain does not increase the

taxable estate (principal). When the sale results in a loss, the taxable estate is not reduced by the loss.

Tax-General § 7-203(j)

Schedule 7 is an itemization of the assets retained by the personal representative and is required with any

account which is not a Final Account. A sufficient explanation of why assets must be retained is required.

Include the explanation at the end of Schedule 7.

SUBSEQUENT ACCOUNTS ARE REQUIRED TO BE FILED AT REGULAR INTERVALS OF THE FIRST TO

OCCUR: Six months from the order approving the prior account or nine months after the prior account was

filed, until the estate is closed by court approval of the final account. See Md. Rule 6-417.

SCHEDULE 7 - Assets Retained for Future Accounting

Value at end

Description of Asset(s): of accounting period:

$

TOTAL BALANCE FORWARD: $

EXPLAIN WHY IT IS NECESSARY TO RETAIN ASSETS AND KEEP THE ESTATE OPEN.

NOTE: Estates and Trusts § 7-101 requires, in part, that a personal representative settle and distribute an

estate as expeditiously and with as little sacrifice of value as is reasonable.

Unless good cause is shown, a personal representative is required to distribute all assets within the time for

rendering the First Account (within 9 months from date of appointment as personal representative).

Upon the filing of multiple interim accounts, the Court may require that a Petition and Order for Authority to

Retain Assets be submitted. If good cause for delayed closing of the estate is not shown, the Court may issue

an order for the personal representative to appear before the Court to show cause why the final account should

not be filed and the estate closed.

12

VE

RIFICATION AND CERTIFICATE OF SERVICE

Each account filed by the personal representative must include the following:

• VERIFICATION OF ACCOUNT Md. Rule 6-417(b)(9) Form on page 14

Statement by each personal representative that the account, or affidavit in lieu of account,

1

is true and

complete for the period covered by the account.

Note: If the personal representative is represented by an attorney, the attorney must also sign the account

pursuant to Md. Rule 6-134(a).

• CERTIFICATE OF SERVICE OF NOTICE REQUIREMENTS Md. Rule 6-417(d) Form on page 14

At the time the account or affidavit in lieu of account is filed, the personal representative must serve notice

on each interested person who has not waived notice.

The certificate of service is the personal representative’s certification of compliance with the notice

requirements (described below). The certificate of service contains the name and address of each

interested person upon whom notice was served. Service of the notice may be made by personal delivery

or by mail, postage prepaid.

The notice shall state:

(1) that an account or affidavit has been filed;

(2) that the recipient may file exceptions with the court within 20 days after the court’s order approving the

account is docketed;

(3) that further information can be obtained by reviewing the estate file in the office of the Register of Wills

or by contacting the personal representative or the attorney;

(4) that upon request the personal representative shall furnish a copy of the account or affidavit to any

person who is given notice, and

(5) that distribution under the account as approved by the court will be made within 30 days after the order

of court approving the account becomes final.

2

13

1

An affidavit in lieu of account is applicable if an estate has had no assets during an accounting period. Md. Rule 6-417(c)

2

If no exceptions to the account are filed within 20 days after entry of the order approving the account, the order of the

court becomes final (Md. Rule 6-417(g)). Within 30 days after the 20 day period has passed, distribution as reported in the

account must be made.

Estate of ______________________________ Estate No: _______________________

VERIFICATION OF ACCOUNT

MD RULE 6-417(b)(9)

I DO SOLEMNLY AFFIRM UNDER THE PENALTIES OF PERJURY THAT THE CONTENTS OF THE

FOREGOING DOCUMENT (ACCOUNT OF PERSONAL REPRESENTATIVE) ARE TRUE TO THE BEST OF

MY KNOWLEDGE, INFORMATION AND BELIEF.

_____________________________________ ________________________________

Attorney for the Estate Personal Representative

(Signature required if applicable) (Signature required)

CERTIFICATE OF SERVICE

MD RULE 6-417(d)

I HEREBY CERTIFY that on the _______ day of _______________________. ________ I delivered or

mailed, postage prepaid, a notice to all interested persons listed below or listed by attachment, a notice stating:

(1) that an account or affidavit in lieu of account has been filed; (2) that the recipient may file exceptions with

the Court within 20 days after the Court’s Order approving the account is docketed; (3) that further information

can be obtained by reviewing the estate file in the office of the Register of Wills or by contacting the personal

representative or the attorney; (4) that upon request the personal representative shall furnish a copy of the

account or affidavit to any interested person who was given notice; and (5) that distribution under the account

as approved by the Court will be made within 30 days after the Order of Court approving the account becomes

final.

Interested persons names and addresses:

______________________________________ ___________________________________

Attorney for the Estate Personal Representative

(Signature required if applicable) (Signature required)

______________________________________ ____________________________________

Address Address

______________________________________ _____________________________________

______________________________________ _____________________________________

Telephone number Telephone number

14

FUNERAL EXPENSES

(Estates and Trusts § 8-106)

A Petition for Funeral Expenses (Form 1130; see page 21) is required if the following applies:

1. The decedent died without a Will, the estate is solvent and the total funeral expenses exceed $15,000.

(For an estate opened prior to October 1, 2015 contact the Register of Wills for applicable funeral

allowance.)

2. The decedent died with a Will, the estate is solvent but the Will does not specify payment of unlimited

funeral expenses or payment without Order of Court and the expenses exceed $15,000. (For an estate

opened prior to October 1, 2015 contact the Register of Wills for applicable funeral allowance.)

_____________________

__________________________________________________________________

FAMILY ALLOWANCE

(Estates and Trusts § 3-201)

For date of death on or after October 1, 2013, a surviving spouse of a decedent is entitled to an

allowance of $10,000 for personal use. An allowance of $5,000 for the use of each unmarried child of the

decedent who has not attained the age of 18 years at the time of the death of the decedent shall be paid by

the personal representative to the guardian of the minor. If there is no guardian, payment may be made to the

parent or grandparent with whom the minor resides, or deposited in a financial institution as provided in

Estates & Trusts § 13-501(b).

For a date of death July 1, 1991 through September 30, 2013, the allowance for the surviving spouse of

the decedent is $5,000 for personal use. An allowance of $2,500 for the use of each unmarried child of the

decedent who has not attained the age of 18 years at the time of the death of the decedent shall be paid by the

personal representative in the manner described in the paragraph above.

For a date of death prior to July 1, 1991, contact the Register of Wills for applicable family allowance.

CLAIMS

(Estates and Trusts §§ 8-107, 8-108)

Upon the expiration of 6 months from the date of the decedent’s death, the personal representative

shall pay the claims allowed against the estate in order of priority prescribed in Estates and Trusts § 8-105.

If a personal representative intends to disallow, in whole or in part, a claim that has been presented

within the appropriate time and in the form prescribed in Estates and Trusts § 8-104(b) or (c), the personal

representative must mail notice to the claimant stating:

(1) that the claim has been disallowed in whole or in a stated amount; or

(2) that the personal representative will petition the court to determine whether the claim should be

allowed.

Notice of Disallowance Form 1129

15

Audit/SampleAccount2020.dot

rev 1/2020

PROBATE FEES

(Estates and Trusts § 2-206)

Effective for decedents dying on or after July 1, 1989, the probate fees for regular estates are reflected

by the following schedule. Fees are due at the time of filing the First Account and may be altered by the filing of

subsequent accounts until the estate is closed. The fees are computed on the gross estate which is the sum of

Schedules 1, 2, 3 and 4.

VALUE OF GROSS ESTATE

AT LEAST BUT LESS THAN FEE

$ - 0 - $ 50,000.00 $ 0.00

50,000.00 100,000.00 100.00

100,000.00 500,000.00 200.00

500,000.00 1,000,000.00 1,000.00

1,000,000.00 2,500,000.00 2,000.00

2,500,000.00 5,000,000.00 5,000.00

5,000,000.00 7,500,000.00 7,500.00

7,500,000.00 10,000,000.00 10,000.00

10,000,000.00 ------------ 10,000.00 plus .02% of

excess over

$10,000,000.00

This section only applies to estates opened before October 1, 2022

VALUE OF GROSS ESTATE

AT LEAST BUT LESS THAN FEE

$ - 0 - $ 10,000.00 $ 50.00

10,000.00 20,000.00 100.00

20,000.00 50,000.00 150.00

50,000.00 75,000.00 200.00

75,000.00 100,000.00 300.00

100,000.00 250,000.00 400.00

250,000.00 500,000.00 500.00

500,000.00 750,000.00 750.00

750,000.00 1,000,000.00 1,000.00

1,000,000.00 2,000,000.00 1,500.00

2,000,000.00 5,000,000.00 2,500.00

5,000,000.00 ------------ 2,500.00 plus .02% of

excess over

$5,000,000.00

For a date of death prior to July 1, 1989, contact the Register of Wills office for a calculation of court costs and

tax on commission.

16

PERSONAL REPRESENTATIVE’S COMMISSIONS AND/OR ATTORNEY’S FEES

Unless the will provides a larger amount, the maximum commission of a personal representative is

established by Estates and Trusts § 7-601 at the rate of 9% of the first $20,000.00, plus 3.6% of the excess

over $20,000.00 of the gross estate (applicable for estates of decedents dying on or after January 1, 1992).

Except as noted below, a Petition for Personal Representative’s Commissions and/or Attorney’s Fees,

Notice of Petition and proposed Order must be submitted for consideration by the court. Commissions and/or

attorney’s fees cannot be paid from estate assets until approved by court order.

Effective for decedent’s dying on or after January 1, 1998, payment of commissions to a personal

representative and/or fees to the attorney for the estate may be made without court approval if:

(1) Each creditor, who has filed a claim that is still open, and all interested persons consent in

writing to the payment;

(2) The combined sum of the payments of commissions and attorney’s fees does not exceed

the amounts provided in Estates and Trusts § 7-601; and

(3) The signed written consent form states the amounts of the payments and is filed with the

Register of Wills.

Consent to Compensation for Personal Representative and/or Attorney Form 1138

(Form on page 22)

Subject to Court Approval See Md. Rule 6-416(a)

1. When a petition for the allowance of attorney's fees or personal representative's commissions is

is required, it shall be verified and shall state:

(a) the amount of all fees or commissions previously allowed;

(b) the amount of fees or commissions that the petitioner reasonably estimates will be requested in the

future;

(c) the amount of fees or commissions currently requested;

(d) the basis for the current request in reasonable detail; and

(e) that the notice requirement (below) has been given.

2. The personal representative shall serve on each unpaid creditor who has filed a claim and on each

interested person a copy of the petition accompanied by a notice in the following form:

NOTICE OF PETITION FOR ATTORNEY’S FEES OR PERSONAL REPRESENTATIVE’S

COMMISSIONS

You are hereby notified that a petition for allowance of attorney’s fees or personal representative’s

commissions has been filed. You have 20 days after service of the petition within which to file written

exceptions and to request a hearing.

(Form for Notice and Certificate of Service on page 23)

3. Any exception to the petition must be filed with the court within 20 days after service of the petition and

notice and include the grounds therefore in reasonable detail. A copy of the exception must be served on

the personal representative.

4. If timely exceptions are not filed, the order of the court allowing the attorney's fees and/or personal

representative's commissions becomes final. Upon the filing of timely exceptions, the court shall set the

matter for hearing and notify the personal representative and other persons that the court deems

appropriate of the date, time, place, and purpose of the hearing.

17

PERSONAL REPRESENTATIVE’S COMMISSIONS AND/OR ATTORNEY’S FEES (continued)

NOTE: When extraordinary circumstances exist and the combined personal representative’s commissions and

attorney’s fees exceed the maximum allowance (as set forth in Estates and Trusts § 7-601), the Orphans’

Court Judges will be looking for a time sheet from the attorney that includes the hourly rates, description of

services performed and total hours worked.

Even if the attorney’s fees are within the maximum allowable, the Court may deny the petition if it feels

adequate support for the fees is not provided.

PAYMENT OF CONTINGENCY FEE FOR SERVICES OTHER THAN ESTATE ADMINISTRATION

Md. Rule 6-416(b)

Payment of attorney’s fees may be made without court approval if:

(a) the fee is paid to an attorney representing the estate in litigation under a contingency fee agreement

signed by the decedent or by a previous personal representative;

(b) the fee is paid to an attorney representing the estate in litigation under a contingency fee agreement

signed by the current personal representative of the decedent’s estate provided that the personal

representative is not acting as the retained attorney and is not a member of the attorney’s firm;

(c) the fee does not exceed the terms of the contingency fee agreement;

(d) a copy of the contingency fee agreement is on file with the register of wills; and

(e) the attorney files a statement with each account stating that the scope of the representation by the

attorney does not extend to the administration of the estate.

PAYMENT TO PERSONAL REPRESENTATIVE OR ATTORNEY FOR A CLAIMED DEBT EXISTING PRIOR

TO THE DEATH OF THE DECEDENT Md. Rule 6-414 Estates & Trusts § 7-502(a)

1. Notice. For a claimed debt owed to the personal representative, or attorney for the estate, that existed

prior to the decedent’s date of death, the personal representative must serve a notice on each unpaid

creditor who has filed a claim and on each interested person. A copy of the notice must be filed with

the Register of Wills.

2. Contents of Notice. The notice must state the amount of the proposed payment, the basis for the

payment in reasonable detail, and a statement that each unpaid creditor and interested person has

20 days after service to file with the court written exceptions and to request a hearing.

18

MARYLAND ESTATE TAX

Tax-General Article, Title 7, Subtitle 3.

The Maryland estate tax is a transfer tax imposed on the transfer of assets from the estate. (The inheritance

tax is a separate tax collected by the Register of Wills on the clear value of property that passes from a

decedent to some certain beneficiaries.)

A MARYLAND ESTATE TAX RETURN (Form MET-1) is required for every estate whose federal gross estate,

plus adjusted taxable gifts, plus property for which a Maryland Qualified Terminal Interest Property (QTIP)

election was previously made on a Maryland estate tax return filed for the estate of the decedent’s

predeceased spouse, equals or exceeds the Maryland estate tax exemption amount for the year of the

decedent’s death, and the decedent at the date of death was

(1) a Maryland resident, or

(2) a non-resident but owned real or tangible personal property having a taxable situs

in Maryland.

The filing requirement varies depending on the year of the decedent’s death.

Year

Gross Estate

2019 & After

$5,000.000

2018

$4,000,000

2017

$3,000,000

2016

$2,000,000

2015

$1,500,000

2002-2014

$1,000,000

2000-2001

$675,000

1999

$650,000

Prior to 1999

Contact Comptroller

The gross estate includes all property, real or personal, tangible or intangible, wherever situated, in which the

decedent had an interest. It includes such items as annuities, joint assets with right of survivorship, transfers

made without adequate consideration, the includible portion of tenancies by the entirety, certain life insurance

proceeds, and general power of appointment property, to name a few.

For information about Maryland estate tax, see Tax Tip 42 – What You Need to Know About Maryland’s Estate

Tax, which can be downloaded from the Comptroller of Maryland’s website: www.marylandtaxes.com. You can

also call the Estate Tax Unit at 410-260-7850 in Central Maryland or 1-800-MD TAXES (toll-free from

elsewhere in the state), Monday through Friday, 8:30 a.m. – 4:30 p.m.

MARYLAND FIDUCIARY INCOME TAX

Tax-General Article, Title 10

An estate may be required to file a Maryland fiduciary income tax return, Form 504. Contact the Comptroller

of Maryland, Revenue Administration Division for assistance by calling 410-260-7980 in Central Maryland or

1-800-MD TAXES from elsewhere in the state, Monday through Friday, 8:30 a.m. – 4:30 p.m.

You may also find helpful information in Tax Tip 61 – Maryland Income Tax Law and Fiduciaries, Estates and

Trusts, which can be downloaded from the Comptroller’s website: www.marylandtaxes.com.

19

How Will My Estate Be Distributed If I Die Without A Will?

IF THE DECEDENT IS SURVIVED BY:

1. Spouse and Minor Children

1

of the Decedent E&T § 3-102(b)

spouse receives one-half

children share remaining one-half

2. Spouse and Children (all adult) of the Decedent E&T § 3-102(c)

spouse receives $15,000 ($40,000 for a date of death

on or after October 1, 2017) plus one-half of remaining estate;

children divide balance

(the interest of a predeceased child passes to issue

2

of that child)

3. Children only of the Decedent E&T § 3-103

children (does not include step-children) divide entire estate

(the interest of a predeceased child passes to issue of that child)

4. Spouse and Parents of the Decedent E&T § 3-102(d)

spouse receives the first $15,000 ($40,000 for a date of death

on or after October 1, 2017) plus one-half of remaining estate; If married

to decedent less than 5 years and both parents divide balance or surviving

parent takes balance

5. Spouse of the Decedent without Other Heirs listed above E&T § 3-102(e)

spouse receives entire estate (If married to the decedent at least 5 years

or more) even if there are surviving parents.

6. Parents of the Decedent without Other Heirs listed above E&T § 3-104(b)

both parents divide entire estate or surviving parent takes all

7. Brothers/Sisters of the Decedent without Heirs listed above E&T § 3-104(b)

brothers and sisters divide estate equally

(share of deceased sibling goes to their issue – nieces and nephews

of the decedent)

8. Grandparents without Other Heirs listed above E&T § 3-104(c)

grandparents divide entire estate or, if deceased, to their issue

(see applicable law for details)

9. Great-grandparent without Other Heirs listed above E&T § 3-104(d)

great-grandparents divide entire estate or, if deceased, to their issue

(see applicable law for details)

10. Step-children if there are no Heirs listed above E&T § 3-104(e)

11. No living Heirs or Step-children E&T § 3-105

If decedent was a recipient of long-term care benefits under the

Maryland Medical Assistance Program at time of death,

net estate is paid to Department of Health and Mental Hygiene.

Otherwise, the net estate is paid to the Board of Education.

20

1

Child includes a legitimate child, an adopted child and an illegitimate child to the extent provided by law. A child does not

include a stepchild, a foster child, or a grandchild or more remote descendant. Estates & Trusts § 1-205

2

Issue means every living lineal descendant except a lineal descendant of a living lineal descendant. Estates &

Trusts § 1-209

RW1130

Rev. 1/2016

IN THE ORPHANS' COURT FOR

(OR)

, MARYLAND

BEFORE THE REGISTER OF WILLS FOR

IN THE ESTATE OF:

ESTATE NO:

PETITION AND ORDER FOR FUNERAL EXPENSES

I hereby request allowance of funeral expenses and I state that :

(1) The expenses are as follows (or as set forth in the attached statement or invoice):

(2) The estate is (solvent) (insolvent).

I solemnly affirm under the penalties of perjury that the contents of this petition are true to the best of my knowledge,

information, and belief.

Attorney

Personal Representative Date

Address

Personal Representative Date

Personal Representative Date

Telephone Number

Facsimile Number

Email Address

Certificate of Service

I hereby certify that on this

day of

,

I delivered or mailed, postage prepaid, a copy of

the foregoing Petition to the following persons :

(name and address)

Signature

ORDER

Upon a finding that $

is a reasonable amount for funeral expenses, according to the condition

and circumstances of the decedent, it is this

day of

,

,

ORDERED, by the Orphans’ Court for

County, that this sum is allowed

JUDGES

21

RW1138

BEFORE THE REGISTER OF WILLS FOR

MONTGOMERY COUNTY

, MARYLAND

IN THE ESTATE OF:

ESTATE NO:

CONSENT TO COMPENSATION FOR

PERSONAL REPRESENTATIVE AND/OR ATTORNEY

I understand that the law, Estates and Trusts Article, §7-601 provides a formula to establish the maximum total

commissions to be paid for personal representative’s commissions. If the total compensation for personal representative’s

commissions and attorney’s fees being requested falls within the maximum allowable commissions, and the request is

consented to by all unpaid creditors who have filed claims and all interested persons, this payment need not be subject to

review or approval by the Court. A creditor or an interested party may, but is not required to, consent to these fees. The

formula sets total compensation at 9% of the first $20,000 of the adjusted estate subject to administration PLUS 3.6% of

the excess over $20,000. Based on this formula, the adjusted estate subject to administration known at this time is

$ . The total allowable statutory maximum commission based on the adjusted estate subject to

administration known at this time is $ , LESS any personal representative’s commissions and attorney’s

fees previously approved as required by law and paid. To date, $ in personal representative’s

commissions and $ in attorney’s fees have been paid.

IF ALL REQUIRED CONSENTS ARE NOT OBTAINED, A PETITION SHALL BE FILED, AND THE

COURT SHALL DETERMINE THE AMOUNT TO BE PAID

Cross References - See 90 Op. Att’y Gen. 145 (2005).

Total combined fees being requested are $ , to be paid as follows:

Amount

To

Name of Personal Representative/Attorney

I have read this entire form and I herby consent to the payment of personal representative and/or attorney’s fees in the

above amount.

Date

Signature

Name (Typed or Printed)

Attorney

Personal Representative

Address

Personal Representative

Address

Personal Representative

Telephone Number

Facsimile Number

Email Address

22

IN THE ORPHANS' COURT FOR

(OR)

, MARYLAND

BEFORE THE REGISTER OF WILLS FOR

IN THE ESTATE OF:

ESTATE NO:

NOTICE OF PETITION FOR ATTORNEY’S FEES

OR PERSONAL REPRESENTATIVE’S COMMISSIONS

(Pursuant to Maryland Rule 6-416)

YOU ARE HEREBY NOTIFIED that a petition for allowance of attorney’s fees or personal

representative’s commissions has been filed.

YOU HAVE 20 DAYS after service of the petition within which to file written exceptions and to

request a hearing.

CERTIFICATE OF SERVICE

I HEREBY CERTIFY that on this ________ day of ___________________, 20_____, a copy of

the foregoing petition for attorney’s fees or personal representative’s commissions and a copy of this

notice were mailed, postage prepaid, to all interested persons including unpaid creditors as follows:

NAME ADDRESS

________________________________________ ____________________________________________

Attorney for the Estate Personal Representative

____________________________________________ _________________________________________________

Address Address

____________________________________________ _________________________________________________

____________________________________________ _________________________________________________

Telephone Number Telephone Number

____________________________________________

Facsimile Number

____________________________________________

Email Address

23

INDEX

Page

Account

Verification and Notice of Account 13, 14

Attorney’s Fees

Debt owed to estate attorney prior to date of death 18

Disbursement 6, 17, 18

Litigation fee under contingency agreement 18

Petition for Fees 17, 18, 23

Without Court approval 17, 18, 22

Certificate of Service

Account 13, 14

Petition for Fees and/or Commissions 17, 23

Changes in Assets (Including Gains and Losses)

Distribution 11

Inheritance tax exemption 4, 8

Schedule 3 4

Child

Definition for distribution purposes 20

Definition for inheritance tax purposes 8

Claims 6, 15, 17

Commissions 6, 17, 18, 22, 23

Consent to Commissions/Attorney’s Fees 17, 22

Debts 6, 18

Disbursements

Schedule 5 6, 7

Distribution

Inheritance tax exemptions 8, 11

Intestate (without a Will) 20

Schedule 6 8 – 11

Specific bequest 9, 10

Expenses 6, 7, 15

Family Allowance 7, 8, 15

Funeral 6, 15, 21

Heir 20

Income Receipts

Earned on specific bequest 9

Inheritance tax exemption 5, 9, 11

Schedule 4 5

Inheritance Tax

Distribution of rest and residue 9, 11

Exemptions 8, 11

Non-Probate (Information Report) 6

Schedule 6 8 - 11

Information Report 6

Inventory

Schedule 1 2

Issue 20

Market Fluctuation 4

Maryland Estate Tax 6, 19

Maryland Fiduciary Income Tax 6, 19

Notice to Interested Persons

Account 13, 14

Petition for Attorney’s Fees and/or Commissions 17, 18

Personal Representative

Commissions 17, 18, 22, 23

Payment to Personal Representative for claimed debt

existing prior to date of death 18

Principal Receipts

Schedule 2 3

Distribution/Inheritance tax 9, 11

Probate Fees 6, 7, 16

Real Property

Sale 3, 4

Expenses 6, 7

Specific bequest 9

Receipts – see principal receipts and income receipts

Refunds 3

Retained Assets

Schedule 7 12

Sale of Asset

Expenses 6

Gain/Loss 4

Inheritance tax exemption 4, 8

Specific bequest

Income and expenses 9

Distribution and inheritance tax 10, 11

Tax Clause 9, 11

Verification of Account 13, 14

FORMS

Petition and Order for Funeral Expenses 21

Consent to Compensation for Personal Representative 22

and/or Attorney

Notice of Petition for Attorney’s Fees or 23

Personal Representative’s Commissions

DATE OF DEATH January 1, 1998 through June 30, 1999

INHERITANCE TAX RATE Tax-General § 7-204

Direct inheritance tax - 1% applicable for distributions to:

(1) a spouse (certain exemptions to spouse shown below)

(2) a parent

(3) a child or other lineal descendant of the decedent

(4) a stepchild

(5) a stepparent

(6) a grandparent

(7) a corporation if all its stockholders consist of the surviving spouse, parents, stepparents, stepchildren,

lineal descendants of the decedent, and spouses of lineal descendants

Collateral Inheritance tax - 10% applicable for distributions to all others (see exemptions below)

If the Will contains a sufficient tax clause, inheritance tax on a specific bequest is not subtracted from the

bequest and is computed at the higher rate as follows:

1.0% Direct inheritance tax - higher rate is 1.010101%

10.0% Collateral inheritance tax - higher rate is 11.11111%

Absent a tax clause, the bequest is reduced by the inheritance tax at the appropriate rate of 1% or 10%.

When a partial distribution of the residuary estate is reflected in an interim account and inheritance tax is not

withheld from the partial distribution, the higher rate is applied to the actual amount received by the beneficiary. The

tax is considered an expense of the estate.

EXEMPTIONS FROM INHERITANCE TAX Tax-General § 7-203

The inheritance does not apply:

(1) to the receipt of all real property (including leasehold property) and the first $100,000.00 of personal

property when passing to a spouse

(2) if a charitable organization is exempt under Section 501(c)(3) of the Internal Revenue Code, or to which

certain transfers are deductible under § 2055 of the Internal Revenue Code

1

, and in accordance with

Tax-General § 7-203(e)

(3) to the receipt of the family allowance to the surviving spouse and minor child of a decedent under Estates

and Trusts § 3-201

(4) to the receipt of property that passes from a decedent to any one (1) person if the total value of the

property does not exceed $1,000.00

(5) to the receipt of property that is income, including gains and losses, accrued on probate assets after

the date of death of the decedent. (The inheritance tax is not assessed on a gain realized on the sale of a

probate asset. Additionally, the inheritance tax is not reduced by a loss realized on the sale of a probate

asset. The inheritance tax is based on the value of the asset as reported in the Inventory. However, the

realized gains/losses are subject to accounting by a personal representative.)

FAMILY ALLOWANCE Estates and Trusts § 3-201

A surviving spouse of a decedent is entitled to an allowance of $5,000 for personal use.

An allowance of $2,500 for the use of each unmarried child of the decedent who has not attained the age of 18

years at the time of the death of the decedent shall be paid by the personal representative to the guardian of the

minor. If there is a guardian, payment may be made to the parent or grandparent with whom the minor resides, or

deposited in a financial institution as provided in Estates and Trusts § 13-501(b).

FUNERAL EXPENSES Estates and Trusts § 8-106

For an estate opened prior to October 1, 2015, contact the Register of Wills for applicable funeral allowance.

1

Exemption for certain transfers deductible under § 2055 of the Internal Revenue Code effective for date of death on or after October 1,

1998.

DATE OF DEATH July 1, 1999 through June 30, 2000

INHERITANCE TAX RATE Tax-General § 7-204

Direct inheritance tax - .9% applicable for distributions to:

(1) a spouse (certain exemptions to spouse shown below)

(2) a parent

(3) a child or other lineal descendant of the decedent

(4) a stepchild

(5) a stepparent

(6) a grandparent

(7) a corporation if all its stockholders consist of the surviving spouse, parents, stepparents, stepchildren,

lineal descendants of the decedent, and spouses of lineal descendants

Collateral Inheritance tax - 8% applicable for distribution to a brother or sister of the decedent

Collateral Inheritance tax - 10% applicable for distributions to all others (see exemptions below)

If the Will contains a sufficient tax clause, inheritance tax on a specific bequest is not subtracted from the

bequest and is computed at the higher rate shown below.

.9% Direct tax - higher rate is .9081736%

8.0% Collateral tax - higher rate is 8.6956522%

10.0% Collateral tax - higher rate is 11.111111%

Absent a tax clause, the bequest is reduced by the inheritance tax at the appropriate rate of .9%, 8% or 10%.

When a partial distribution of the residuary estate is reflected in an interim account and inheritance tax is not

withheld from the partial distribution, the higher rate is applied to the actual amount received by the beneficiary. The

tax is considered an expense of the estate.

EXEMPTIONS FROM INHERITANCE TAX Tax-General § 7-203

The inheritance does not apply:

(1) to the receipt of all real property and the first $100,000.00 of personal property when passing to a spouse

(2) if a charitable organization is exempt under Section 501(c)(3) of the Internal Revenue Code, or to which

certain transfers are deductible under §2055 of the Internal Revenue Code, and in accordance with

Tax-General §7-203(e)

(3) to the receipt of the family allowance to the surviving spouse and minor child of a decedent under Estates

and Trusts § 3-201

(4) to the receipt of property that passes from a decedent to any one (1) person if the total value of the

property does not exceed $1,000.00.

(5) to the receipt of property that is income, including gains and losses, accrued on probate assets after the

date of death of the decedent. (The inheritance tax is not assessed on a gain realized on the sale of a

probate asset. Additionally, the inheritance tax is not reduced by a loss realized on the sale of a probate

asset. The inheritance tax is based on the value of the asset as reported in the Inventory. However, the

realized gains/losses are subject to accounting by a personal representative.)

FAMILY ALLOWANCE Estates and Trusts § 3-201

A surviving spouse of a decedent is entitled to an allowance of $5,000 for personal use.

An allowance of $2,500 for the use of each unmarried child of the decedent who has not attained the age of 18

years at the time of the death of the decedent shall be paid by the personal representative to the guardian of the

minor. If there is no guardian, payment may be made to the parent or grandparent with whom the minor resides, or

deposited in a financial institution as proved in Estates & Trusts § 13-501(b)

FUNERAL EXPENSES Estates and Trusts § 8-106

For an estate opened prior to October 1, 2015, contact the Register of Wills for applicable funeral allowance.

DATE OF DEATH July 1, 2000 through June 30, 2004

INHERITANCE TAX EXEMPTIONS Tax-General § 7-203

The inheritance tax does not apply to the receipt of property that passes from a decedent to or for the use of:

(1) a spouse

(2) a parent

(3) a child of the decedent or other lineal descendant of the decedent

(4) a stepchild

(5) a stepparent

(6) a grandparent

(7) a brother or sister of the decedent

(8) a spouse of a child of the decedent or other lineal descendant of the decedent

(9) a corporation if all of its stockholders consist of the surviving spouse, parents, stepparents, stepchildren,

brothers, sisters, and lineal descendants of the decedent and spouses of the lineal descendants

Note: For the spouse of a child of the decedent or spouse of other lineal descendant to be exempt from tax, the child or other lineal descendant had to

be living at the decedent’s date of death

ADDITIONAL EXEMPTIONS FROM INHERITANCE TAX Tax-General § 7-203

The inheritance does not apply:

(1) if a charitable organization is exempt under Section 501(c)(3) of the Internal Revenue Code, or to which

certain transfers are deductible under § 2055 of the Internal Revenue Code, and in accordance with

Tax-General § 7-203(e)

(2) to the receipt of the family allowance to the surviving spouse and minor child of a decedent under Estates

and Trusts § 3-201

(3) to the receipt of property that passes from a decedent to any one (1) person if the total value of the

property does not exceed $1,000.00

(4) to the receipt of property that is income, including gains and losses, accrued on probate assets after

the date of death of the decedent. (The inheritance tax is not assessed on a gain realized on the sale of a

probate asset. Additionally, the inheritance tax is not reduced by a loss realized on the sale of a probate

asset. The inheritance tax is based on the value of the asset as reported in the Inventory. However,

any gain/loss realized on a transaction is subject to accounting by a personal representative.)

TAX RATE Tax-General § 7-204

Direct inheritance tax - no longer applicable

Collateral Inheritance tax - 10% applicable for distributions not exempted per Tax-General § 7-203

If the Will contains a sufficient tax clause, inheritance tax on a specific bequest is not subtracted from the

bequest and is computed at the higher rate as follows:

10.0% Collateral inheritance tax - higher rate is 11.11111%

Absent a tax clause, the bequest is reduced by the inheritance tax at the rate of 10%.

When a partial distribution of the residuary estate is reflected in an interim account and inheritance tax is not

withheld from the partial distribution, the higher rate is applied to the actual amount received by the beneficiary. The

tax is considered an expense of the estate.

FAMILY ALLOWANCE Estates and Trusts § 3-201

A surviving spouse of a decedent is entitled to an allowance of $5,000 for personal use.

An allowance of $2,500 for the use of each unmarried child of the decedent who has not attained the age of 18

years at the time of the death of the decedent shall be paid by the personal representative to the guardian of the

minor. If there is no guardian, payment may be made to the parent or grandparent with whom the minor resides, or

deposited in a financial institution as proved in Estates & Trusts § 13-501(b).

FUNERAL EXPENSES Estates and Trusts § 8-106

For an estate opened prior to October 1, 2015, contact the Register of Wills for applicable funeral allowance.

DATE OF DEATH July 1, 2004 through June 30, 2010

INHERITANCE TAX EXEMPTIONS Tax-General § 7-203

The inheritance tax does not apply to the receipt of property that passes from a decedent to or for the use of:

(1) a spouse of the decedent;

(2) a parent of the decedent (“parent” includes a stepparent or former stepparent);

(3) a child of the decedent or a lineal descendant of a child of the decedent (“child” includes a stepchild or

former stepchild);

(4) a grandparent of the decedent;

(5) a brother or sister of the decedent;

(6) a spouse of a child of the decedent or a spouse of a lineal descendant of a child of the decedent;

(7) a corporation, partnership, or limited liability company if all of its stockholders, partners, or members

consist of individuals specified in items 1 through 6 above.

Note: For the spouse of a child of the decedent or spouse of other lineal descendant to be exempt from tax, the child or other lineal descendant had to

be living at the decedent’s date of death.

TAX RATE Tax-General § 7-204

Collateral Inheritance tax - 10% applicable for distributions to all others

If the Will contains a sufficient tax clause, inheritance tax on a specific bequest is not subtracted from the

bequest and is computed at the higher rate as follows:

10.0% Collateral inheritance tax - higher rate is 11.11111%

Absent a tax clause, the bequest is reduced by the inheritance tax at the rate of 10%,

When a partial distribution of the residuary estate is reflected in an interim account and inheritance tax is not

withheld from the partial distribution, the higher rate is applied to the actual amount received by the beneficiary. The

tax is considered an expense of the estate.

ADDITIONAL EXEMPTIONS FROM INHERITANCE TAX Tax-General § 7-203

The inheritance does not apply:

(1) if a charitable organization is exempt under Section 501(c)(3) of the Internal Revenue Code, or to which

certain transfers are deductible under § 2055 of the Internal Revenue Code, and in accordance with

Tax-General § 7-203(e)

(2) to the receipt of the family allowance to the surviving spouse and minor child of a decedent under Estates

and Trusts § 3-201

(3) to the receipt of property that passes from a decedent to any one (1) person if the total value of the

property does not exceed $1,000.00.

(4) to the receipt of property that is income, including gains and losses, accrued on probate assets

after the date of death of the decedent. (The inheritance tax is not assessed on a gain realized on the sale

of a probate asset. Additionally, the inheritance tax is not reduced by a loss realized on the sale of a

probate asset. The inheritance tax is based on the value of the asset as reported in the Inventory.

However, any gain/loss realized on a transaction is subject to accounting by a personal representative.)

FAMILY ALLOWANCE Estates and Trusts § 3-201

A surviving spouse of a decedent is entitled to an allowance of $5,000 for personal use.

An allowance of $2,500 for the use of each unmarried child of the decedent who has not attained the age of 18

years at the time of the death of the decedent shall be paid by the personal representative to the guardian of the

minor. If there is no guardian, payment may be made to the parent or grandparent with whom the minor resides, or

deposited in a financial institution as provided in Estates & Trusts § 13-501(b).

FUNERAL EXPENSES Estates and Trusts § 8-106

For an estate opened prior to October 1, 2015, contact the Register of Wills for applicable funeral allowance.