Alternative Performance Measures

In addition to statutory performance measures, the Group also measures performance using Alternative Performance Measures. These are reconciled tostatutory

measures of performance on page 56 of the Group Chief Financial Officer’s Review and defined in full on page 209.

DELIVERING FOR

OUR CUSTOMERS

Saga’s purpose is to deliver exceptional

experiences every day, while being a driver of

positive change in our markets and communities.

At the heart of our business model is the drive to understand

ourcustomers’ needs so that we can provide them with the

products and services they want and the exceptional experiences

they deserve.

Our aim is to become the largest and fastest-growing business for

olderpeople in the UK, ‘The Superbrand’ famous for delivering

exceptionalexperiences every day, building confidence and connections

with our customers.

8

Chairman’s Statement

A statement from our Chairman,

SirRogerDe Haan, outlining his view

oftheyear.

Our key performance indicators

Underlying Profit/(Loss) Before Tax

1

£21.5m

2021/22 – (£6.7m)

Loss before tax

(£254.2m)

2021/22 – (£23.5m)

Available Operating Cash Flow

1

£54.9m

2021/22 – £75.8m

Net Debt

1

£711.7m

2021/22 – £729.0m

Customer net promoter score

51

2021/22 – 49

Colleague engagement

8.0 out of 10

2021/22 – 7.7 out of 10

1 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

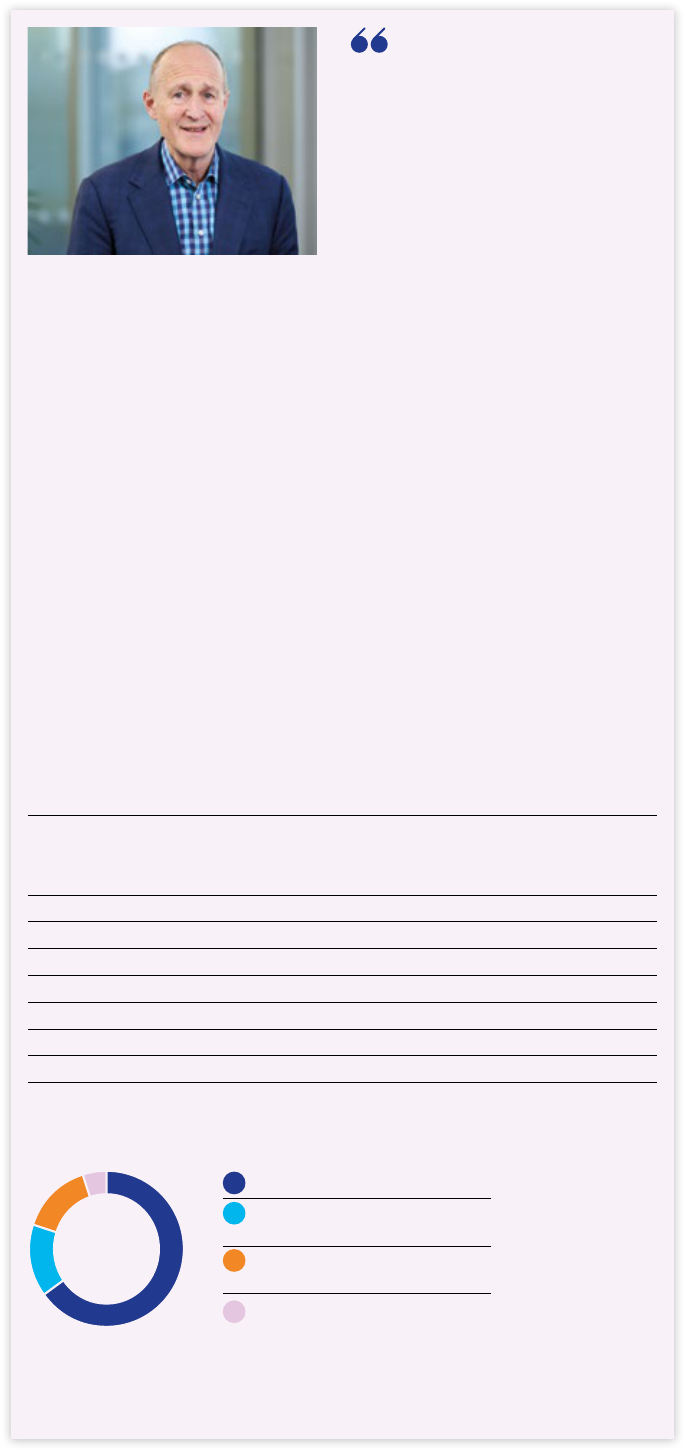

It is evident to me that there is

atremendous opportunity for

Saga to broaden its services

toits customers, reduce its

debt, enlarge its business and

increase its profitability and that

the Company is now well placed

to take advantage of this.”

Sir Roger De Haan

Non-Executive Chairman

Strategic Report

4 The year in review

6 Saga at a glance

8 Chairman’s Statement

10 Group Chief Executive Officer’s Statement

14 Key performance indicators

16 Market review

18 Purpose and business model

20 Engaging with stakeholders

22 Our strategy

26 Environmental, Social and Governance

44 Group Chief Financial Officer’s Review

62 Risk management

65 Principal risks and uncertainties

68 Viability Statement

69 Key disclosure statements

Governance

Corporate Governance Statement

71 Application of UK Corporate Governance Code

72 Chairman’s introduction to governance

74 Board of Directors

76 Governance at a glance

78 Board activities

81 Board leadership and Company purpose

82 Division of responsibilities

83 Composition, succession and evaluation

84 Nomination Committee Report

86 Audit Committee Report

90 Risk Committee Report

Directors’ Remuneration Report

92 Annual Statement

96 Remuneration at a glance

98 Annual Report on Remuneration

111 Directors’ Remuneration Policy

124 Directors’ Report

128 Statements of responsibilities

129 Independent Auditor’s Report to the

Members of Saga plc

Financial statements

Consolidated financial statements

138 Consolidated income statement

139 Consolidated statement of

comprehensiveincome

140 Consolidated statement of financial position

141 Consolidated statement of changes in equity

142 Consolidated statement of cash flows

143 Notes to the consolidated financial statements

Company financial statements of Sagaplc

203 Balance sheet

204 Statement of changes in equity

205 Notes to the Company financial statements

Additional information

209 Alternative Performance Measures Glossary

210 Glossary

213 Shareholder information

1 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

22

Our strategy

Details of our three-step strategic plan,

aimed at returning Saga to sustainable

long-term growth.

Watch our Group CEO,

Euan Sutherland,

outlining our vision

and three-step

growthplan

10

Group Chief Executive

Officer’sStatement

Euan Sutherland, Group Chief Executive Ocer

(CEO), summarises the 2022/23 financial year.

Overall, I am pleased with the

progress made during the year

as we began to make the

strategic pivot towards

becoming a capital-light

marketing, content and

distribution business.”

Euan Sutherland

Group Chief Executive Ocer

44

Group Chief Financial

Officer’s Review

James Quin, Group Chief Financial Ocer

(CFO), details our operating and financial

performance for the year ended

31January2023.

Although the last 12 months

have been challenging in

bothInsurance and Travel,

theGroup returned to an

Underlying Profit Before Tax

1

.”

James Quin

Group Chief Financial Ocer

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 3

Return to underlying

profitasCruise and Travel

recovery continued

Following an extended period of uncertainty,

initially with the pandemic and more recently

geopolitical and macroeconomic uncertainty,

Saga reports an Underlying Profit Before Tax

1

of £21.5m after returning to more normal

Cruise and Travel operations.

Acquisition of the Big Window

tostrengthen our insight

andunderstanding

In February 2022, we announced the

acquisition of the Big Window, a specialist

research and insight business focused on the

ageing process. This move allows us to ensure

we are developing the products and services

our customers want and need.

Launch of our three-step

growthplan

To build on the foundations laid over the past

two years and return Saga to sustainable

growth, we launched our three-step strategic

growth plan, focused on maximising our

existing businesses, step-changing our ability

to scale while reducing debt and creating

‘TheSuperbrand’ for older people.

DEMONSTRABLE PROGRESS

Saga is emerging from the pandemic, focused on

returningto growth

Watch our Group CEO,

Euan Sutherland,

outlining our growthplan

1 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

Underlying Profit Before Tax

1

£21.5m

4 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

The year in review

Launch of new digital

Travelbusiness

In the first half of the year, we combined the

operations of Saga Holidays and Titan Travel

to create the UK’s largest and market-leading

touring business. We also moved away from a

largely paper brochure-based approach to a

digital business, with dynamic pricing and an

enhanced website and booking platform.

Strengthened leadership team

insupport of our growth plan

We were pleased to announce six new

seniorappointments to support the

deliveryof ourstrategy and accelerate

growth. PeterBazalgette, Gemma Godfrey

and Anand Aithal all joined the Board,

alongside three additions to the Executive

Leadership Team to drive the areas of

Money,Media andData.

Introduction of Saga Media

As part of our ambition to become ‘The

Superbrand’ for older people, we introduced

Saga Media, aimed at providing digital media

that represents the needs and interests of

people over 50, giving them great advice,

inspirational stories and a place where they

are heard and valued.

Watch the launch

of Saga Media

atour Capital

Markets Event

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 5

Our investment case is designed to create value for shareholders by returning the business to

sustainable long-term growth and reducing debt.

How we are different

Saga focuses on people over 50, the

fastest-growing, most auent and

influential segment in the UK. Our deep

customer insight gives us a unique view

into our customers’ lives. We exist to

deliver exceptional experiences for

these customers every day, while being

a driver for positive change in our

markets and communities.

The model works

We oer dierentiated products and

services, underpinned by a trusted

brand. Our business model is capital

ecient and cash generative, providing

flexibility to balance investment in our

brand and businesses with debt

reduction and delivery of long-term

returns to shareholders.

Confidence in future delivery

We have a clear and compelling strategy,

focused on returning the business to

growth through maximising our existing

businesses, reducing debt while

step-changing our ability to scale, and

positioning Saga as ‘The Superbrand’

for older people. This will create a truly

customer-orientated experience and

continue to drive longer and deeper

relationships with our customers.

BUILDING OUR FUTURE

Our purpose is to deliver exceptional experiences every day, while

being a driver of positive change in our markets and communities.

Our strategy

Reasons to invest in Saga

Our values

Our aim is to become the largest and fastest-growing

business for older people in the UK. Through our

three-step growth plan, we are focused on the

following priorities:

Our values represent who we are and how we

work,brought to life every day by our colleagues.

We believe that every interaction, in whatever

formthat takes, should reflect these values.

Precision pace

Always owning and

making things happen

We agree clear goals

and plans, move quickly

and take ownership for

our actions.

Curiosity

Always asking why

We are open minded,

always seeking new

insights and learning

about our customers,

markets, competitors

and each other.

Wewelcome and

provide challenge.

Empathy

Always aware of others

We understand and

acknowledge how others

are feeling and we walk

intheir shoes.

Collaboration

Always one team,

theSaga team

We are one team,

working together.

Weare inclusive and

value dierence.

1. Maximising our existing businesses

We plan to maximise our existing businesses

throughaspecific planfor each, enabling growth,

accountability, eciency and delivery of a common

brand purpose.

2. Step-changing our ability to scale

while reducing debt

We will grow our existing businesses while reducing

debt, and develop new businesses through innovation,

in a capital-light way.

3. Creating ‘The Superbrand’ for

olderpeople

We will commercialise and grow our database, build

exceptional insights, deliver a brand repositioning,

create a content platform that reaches millions of

customers every day, and provide an exceptional

colleague experience.

Find out more about our strategy on pages 22-25

6 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Saga at a glance

Underlying (Loss)/Profit Before Tax

2

(£0.8m)

2021/22 – £1.8m

Other Businesses

The Group’s Other Businesses include:

• Money, offering equity release and

savings products;

• Media, providing engaging content

online and through the Saga Magazine;

• Insight, generating unique insights

into‘Generation Experience’; and

• CustomerKNECT (formerly

MetroMail), our in-house mailing

andprintingbusiness.

Highlights for 2022/23

• Delivered revenue and customer

growth within Saga Money.

• Launch of Saga Exceptional,

anewwebsite providing

best-in-class consumer advice

andinspirational stories.

• Development of a detailed customer

segmentation, identifying significant

growth opportunities.

Saga’s business units all focus on the specific needs and wishes of our unique customer group.

Underlying Loss Before Tax

2

Ocean Cruise

(£0.7m)

2021/22 – (£47.7m)

River Cruise

(£5.1m)

2021/22 – (£6.4m)

Underlying Loss Before Tax

2

(£4.1m)

2021/22 – (£25.2m)

Underlying Profit Before Tax

2

£88.2m

2021/22 – £120.5m

Our businesses

Find out more in our Group Chief

Financial Officer’s Review on

pages47-48

Find out more in our Group Chief

Financial Officer’s Review on

pages 47-48

Find out more in our Group Chief

Financial Officer’s Review on

pages 49-52

Cruise

1

Travel

1

Insurance

Insurance is the largest part of the Group,

providing primarily motor, home, travel and

private medical insurance through a panel

of underwriters. This panel includes the

Group’s in-house underwriter, Acromas

Insurance Company Limited (AICL) which

underwrites over 65% of Saga’s motor

insurance policies.

Highlights for 2022/23

• Successfully implemented new

regulatoryrequirements arising from

the Financial Conduct Authority’s (FCA)

review of General Insurance Pricing

Practices (GIPP).

• Introduced a range of new motor

products including a lower-cost

standard one-year policy, alongside

electric vehicle and multi-car products.

• Maintained pricing discipline while

navigating a challenging motor

insurance market.

• Continued improvement in motor and

home customer retention, now at 83.8%

compared with 82.8% in the prior year.

Our Travel business, which has always been

at the heart of the Saga brand, oers:

• hotel stays;

• escorted tours; and

• Tailor-Made holidays.

Highlights for 2022/23

• Combined the operations of Titan

Traveland Saga Holidays to create

theUK’s largest and market-leading

touring business.

• Launched the new Saga Travel business,

moving away from a largely paper

brochure-based approach to a digital

business with dynamic pricing and an

enhanced website and booking platform.

• Introduction of our Saga Deluxe and

Titan’s VIP Travel Services which feature

home-to-airport pick-up, airport lounge

access and fast-track security

clearance at selected UK airports.

• Launched exciting new products

including ‘Tailor-Made by Saga’ and

ourprivate jet tours.

• Strong bookings into 2023/24 of

£137m at 26 March 2023, 32% ahead

ofthe same point in the prior year.

Our Cruise business oers a boutique

cruising experience consisting of:

• ocean cruises on board our two ships,

Spirit of Discovery and Spirit of

Adventure; and

• river cruises along Europe’s waterways

on board our fleet of luxury ships.

Highlights for 2022/23

• Ocean and River Cruise teams

combined to deliver the same

consistently high service across

bothproducts.

• Ocean Cruise delivered target load

factor of 75% and per diem of £318.

• Strong Ocean Cruise bookings into

2023/24 with load factor of 72% and

per diem of £339 at 26 March 2023.

• Achieved excellent guest satisfaction

scores, of 9.0 out of 10 in Ocean and

8.2in River Cruise at 31 January 2023.

1 Cruise was reported within Travel in the 2022 Annual Report and Accounts, however, is now reported separately to reflect the management structure of those businesses

2 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

Find out more in our Group Chief

Financial Officer’s Review on page 53

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 7

I am pleased to report that last year the

performance of our core Cruise, Travel and

Insurance businesses enabled us to return to

underlying profitability whilst we also made

good progress in relation to the strategy

weset out 12 months ago.

Saga continued to build on the progress

reported at the half year, with revenue for

theGroup increasing by over 50% when

compared with the previous year, following

the return to more normal Cruise and Travel

operations post the pandemic.

Our Ocean Cruise business, with its new

ships, performed well in the second half of the

year, sailing with an average 84% occupancy,

testament to the exceptional service we

provide on board, the model that we are now

mirroring on board our River Cruise vessels.

Looking ahead, the level of revenue booked

for the 2023/2024 financial year is very

encouraging and we are now in a good

position to generate our targeted levels of

EBITDA, £80m excluding overheads, from

the two ships.

There have been exciting new developments

in our Travel business in the past year,

including the move to a more agile, more

digital operation, and the launch of our new

“Tailor-Made by Saga” holidays. Currently,

demand for our holidays is strong, particularly

for our touring programmes.

Our Insurance business operated in the

highly competitive market last year following

continued disruption and uncertainty

created by the regulatory changes to the

industry’s pricing and the high cost of settling

insurance claims. We continued to take a

disciplined approach to our pricing.

AN EXCITING FUTURE LIES AHEAD

I am very positive about the future potential of Saga. We have

managed our way through three dicult years and, in 2023/24,

weexpect all of our three main businesses to be profitable.

Iamconfident that our strategy is the right one and will lead

togrowth and a significant reduction in our levels of debt.”

Sir Roger De Haan

Non-Executive Chairman

8 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Chairman’s Statement

As we have indicated previously, we have

decided to focus on Insurance Broking and

tosell our Insurance Underwriting business,

amove that will reduce the risk we take and

release capital and allow us to further reduce

our debt. With this in mind, I was pleased to

beable to provide a £50m facility to give the

Company additional flexibility.

In order to increase the products and

services we oer and the frequency of

ourcustomer interactions and the

understanding we have of them, I am

delighted that we strengthened our

leadership team during the year. Three very

experienced and talented executives were

appointed to set up and lead our new Media

business, our Personal Finance operations,

Saga Money and our Data team. Each of

these areas has great potential.

Finally, I’d like to thank the team at Saga for

their hard work over the past year. It is evident

to me that there is a tremendous opportunity

for Saga to broaden its services to its

customers, reduce its debt, enlarge its

business and increase its profitability and

that the Company is now well placed to take

advantage of this.

Sir Roger De Haan

Non-Executive Chairman

17 April 2023

As I set out in my statement last year, Saga

has always had a strong sense of purpose

andwe have embraced our Environmental,

Social and Governance (ESG)

responsibilities. During the year, we

conducted an assessment to understand

fully the ESG factors that are most material

to our business. Our new sustainability

strategy ispublished later in this report on

pages 26-28. In due course we will set out

further details of the key metrics that we will

use to track our performance.

I am very positive about the future potential

of Saga. We have managed our way through

three dicult years and, in 2023/24, we

expect all of our three main businesses to be

profitable. I am confident that our strategy

isthe right one and will lead to growth and

asignificant reduction in our levels of debt.

Welcoming three new Non-Executive Directors

Peter Bazalgette

Senior Independent

Non-Executive Director

Peter Bazalgette brings

awealth of experience

fromthemedia and wider

creative industries, including

with Endemol, ITV,the BBC,

YouGov and Channel Four.

Anand Aithal

Independent Non-Executive

Director

Anand Aithal has extensive

non-executive experience from

fintech, insurance broking,

asset management and

accountancy, bringing an

entrepreneurial perspective,

having co-founded his own data

analytics business.

Gemma Godfrey

Independent Non-Executive

Director

Gemma, a founder of two

digital businesses, was a

boardroom adviser to

ArnoldSchwarzenegger on

The Apprentice USA and is

abusiness and money expert

on ITV’sGood Morning Britain

and Sky News.

Find out more about our

Board of Directors on

pages74-75

We were pleased to announce the appointment of three new

Non-Executive Directors to the Board, from 1September 2022,

tosupport the Group’s growth strategy and positioning as

‘TheSuperbrand’ for older people in the UK.

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 9

Continued pandemic recovery

During 2022/23, we made strong progress

against the growth plan that we set out in

March 2022, as our Cruise and Travel

businesses continued to recover from the

pandemic, and we navigated a particularly

challenging motor insurance market as it

adjusted to regulatory changes, a sharp rise

in claims inflation and a highly competitive

environment in light of those changes. This

was achieved alongside the launch of our new

Media business, significant enhancements to

our data capabilities and the strengthening

ofour leadership team.

Return to underlying profit

I am pleased to report that, for the year

ended31 January 2023, Saga generated

anUnderlying Profit Before Tax

1

of £21.5m,

compared with an Underlying Loss Before

Tax

1

of £6.7m in the prior year. This reflects

significant improvements across Cruise and

Travel as those businesses returned to more

normal operations, and consistent Insurance

Broking performance, which was partially

oset by reduced earnings from our

Insurance Underwriting business.

After reflecting the £269.0m Insurance

goodwill impairment that we reported within

our interim results, alongside other smaller

one-o below-the-line items, we report a loss

before tax of £254.2m. This compares to a

loss before tax of £23.5m in the prior year.

In addition, we reduced our level of Net Debt

1

which, at 31 January 2023, was £711.7m and

continued to hold significant Available Cash

1

of £157.5m at the same date. Net Debt

1

and

Available Cash

1

, at 31 January 2022, were

£729.0m and £186.6m respectively.

To further reduce debt and increase liquidity

ahead of the maturity of our £150m bond in

May 2024, we have taken a series of actions

which include the initiation of a sales process

in relation to our Insurance Underwriting

business and the agreement of a £50m

loanfacility with Sir Roger De Haan.

The progress made throughout the course

ofthe year demonstrates that Saga is on the

right track to, in time, deliver long-term

sustainable growth for our stakeholders.

PREPARING FOR GROWTH

The progress made throughout the course of the year

demonstrates that Saga is on the right track to, in time,

deliverlong-term sustainable growth for our stakeholders.”

Euan Sutherland

Group Chief Executive Ocer

Watch our Group CEO,

Euan Sutherland,

presenting our

fullyear results

1 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

10 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Group Chief Executive Ocer’s Statement

Our growth plan

In March 2022, we set out our ambition

to become the largest and

fastest-growing business for older

people in the UK which we will achieve

through delivery of our three-step

growth plan. This plan is focused on the

following three priorities:

1. Maximising our

existing businesses

2. Step-changing our

ability to scale while

reducing debt

3. Creating ‘The

Superbrand’ for

older people

An update on our progress, during the past

year, in each of these areas is set out below.

1. Maximising our

existing businesses

Cruise

Our Ocean Cruise business reported an

Underlying Loss Before Tax

2

of £0.7m for the

year ended 31 January 2023. This comprises

an underlying loss of £6.9m in the first half

and a profit of £6.2m in the second half as the

impact of COVID-19 lessened. This compares

to an Underlying Loss Before Tax

2

of £ 47.7m

in the prior year.

For the 2022/23 financial year, Ocean Cruise

achieved a load factor of 75%, made up of

66% in the first half of the year and 84% in the

second, accompanied by a per diem of £318.

This compares with a 68% load factor and

£299 per diem in the prior year. These

factors, when combined, result in Ocean

Cruise year-on-year revenue growth in

excess of 100%.

Looking ahead to the 2023/24 financial

year,our booked load factor positions us

wellto meet our target of at least 80%.

At26March 2023, we had secured

bookingsequivalent to a 72% load factor

and£339 per diem. This positions us well

todeliver our target of £40m EBITDA

pership, excluding overheads, in the year

ending 31 January 2024.

As our Ocean and River Cruise businesses

are now managed by the same team, we

havetaken steps to not only ensure that our

River Cruise guests experience the same

exceptional service as within Ocean Cruise,

but also provide more visibility over the

performance of our River Cruise operation.

Our River Cruise business, in line with the

guidance within our January Trading Update,

reported an Underlying Loss Before Tax

2

of

£5.1m which compares with a £6.4m loss in

the prior year. This improvement was largely

driven by significantly more guests sailing

with us, being 12,000 in 2022/23 compared

with just 1,000 in the prior year.

2 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

3 Refer to the key performance indicators on pages 14-15 for definition and explanation

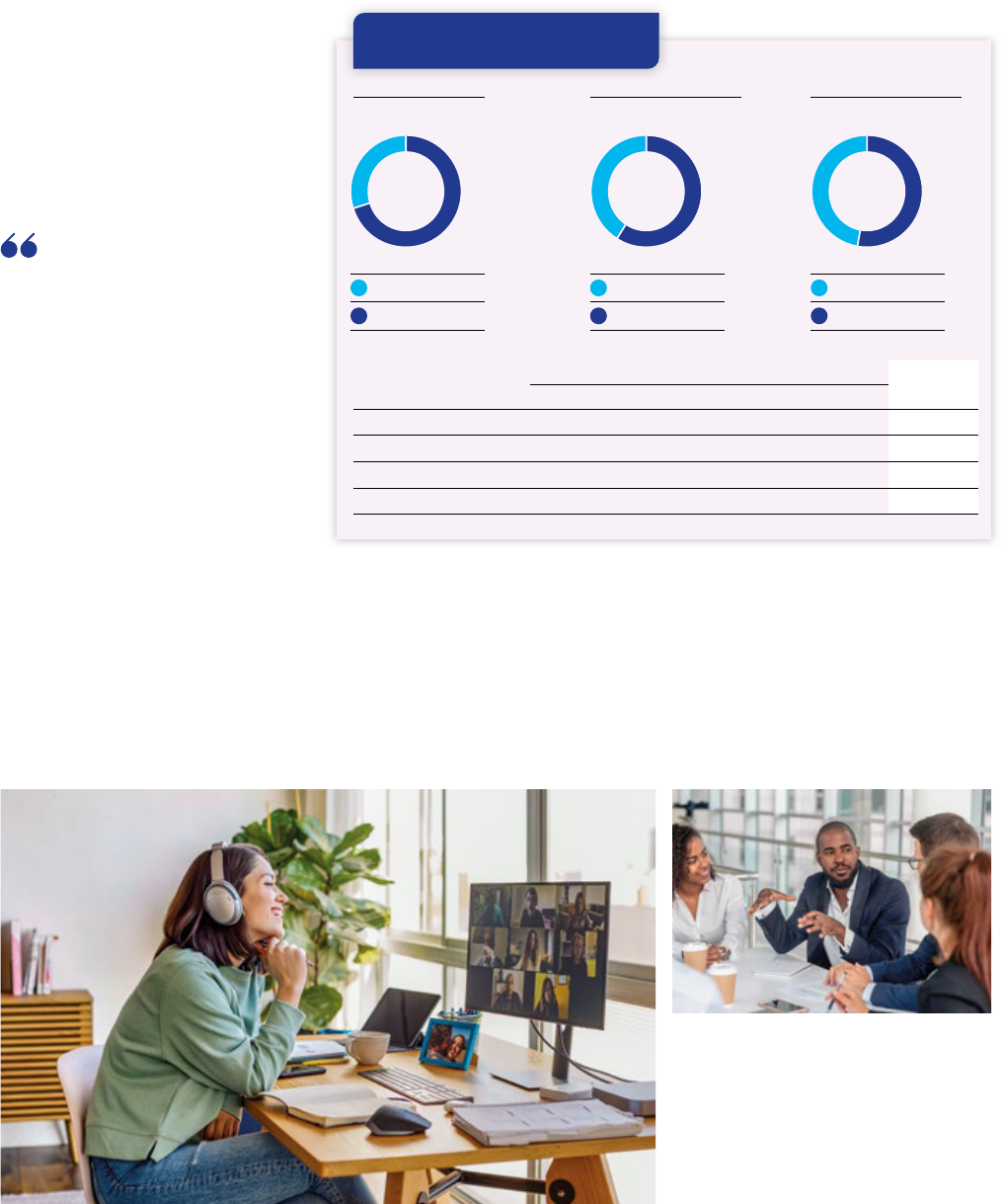

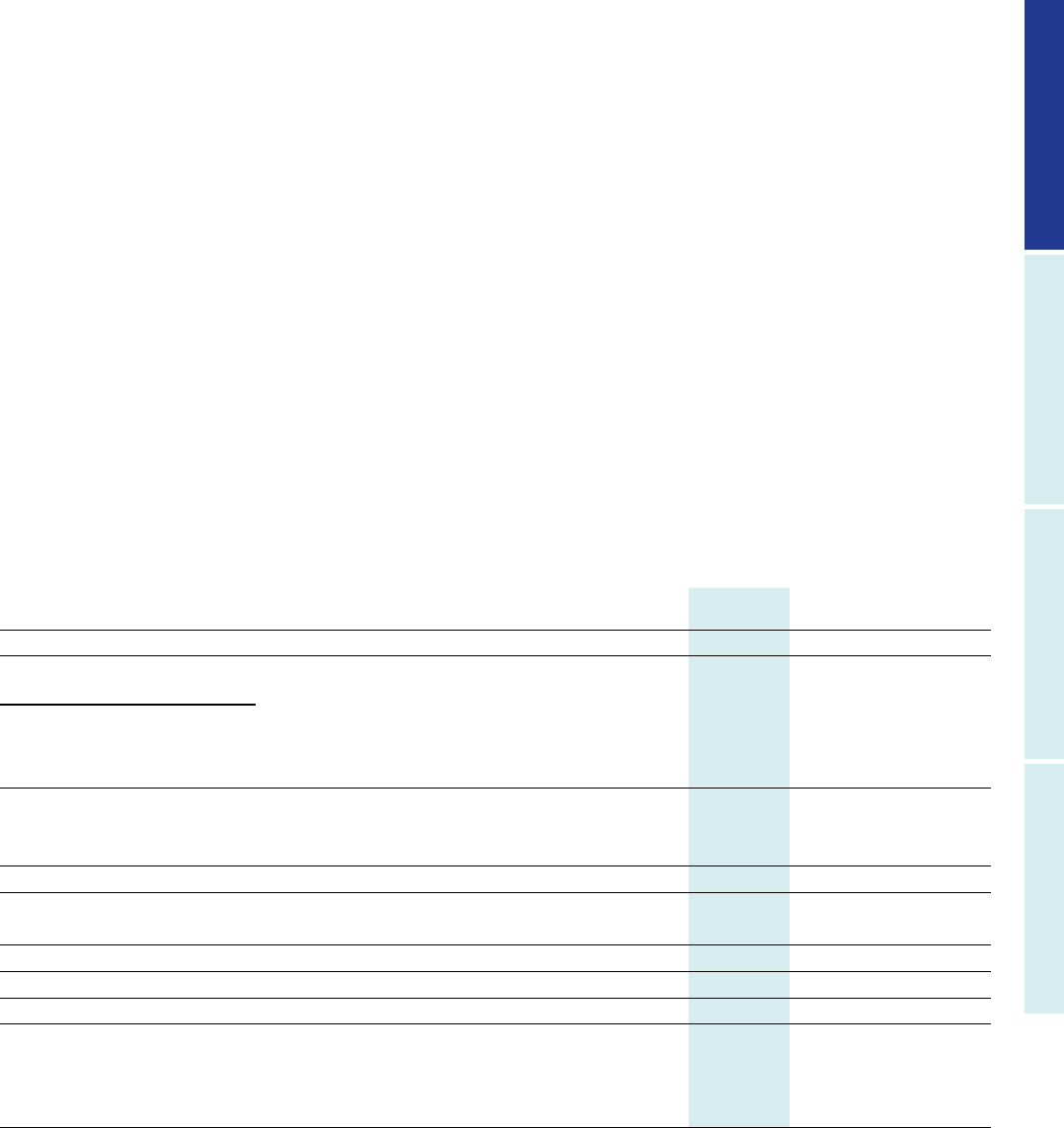

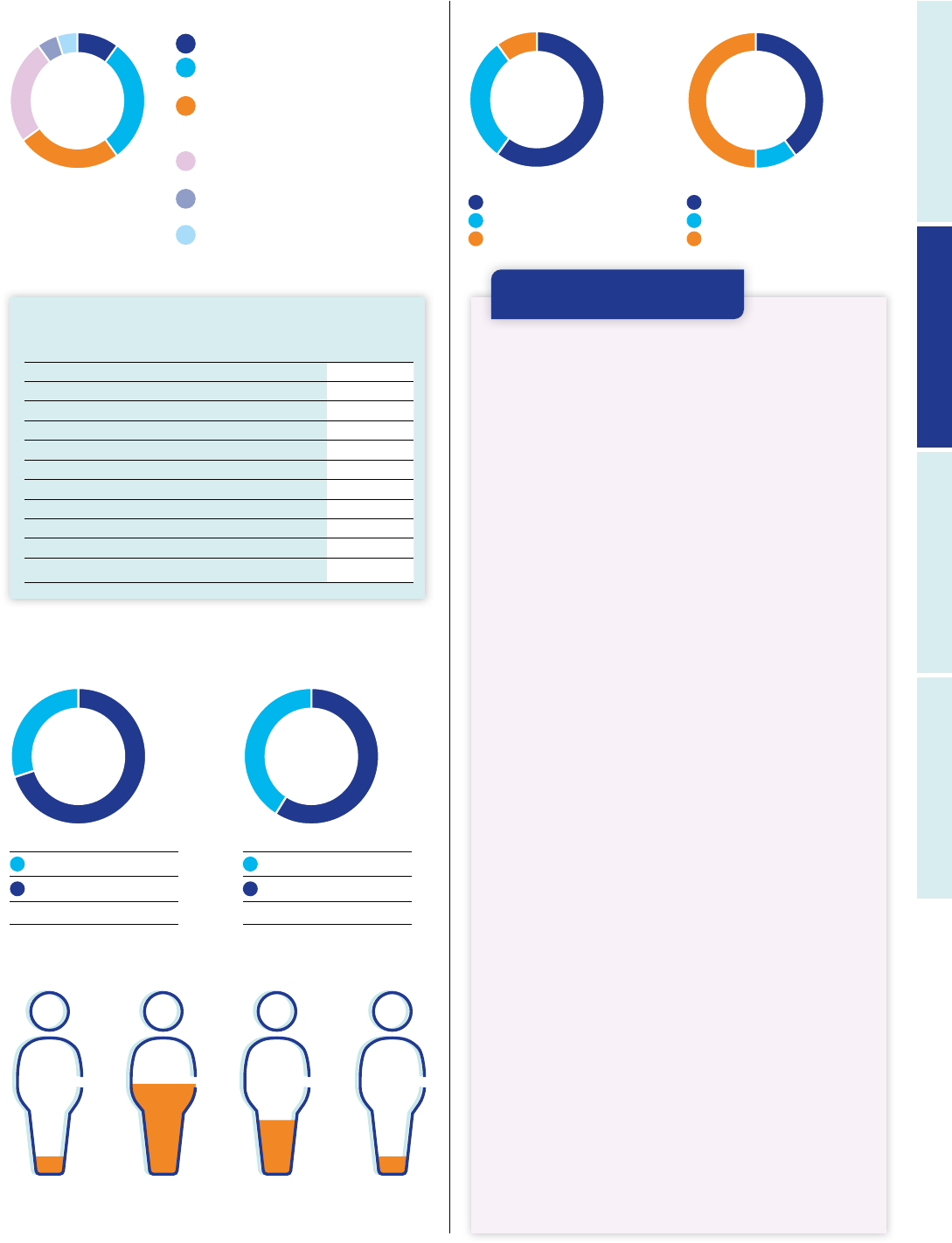

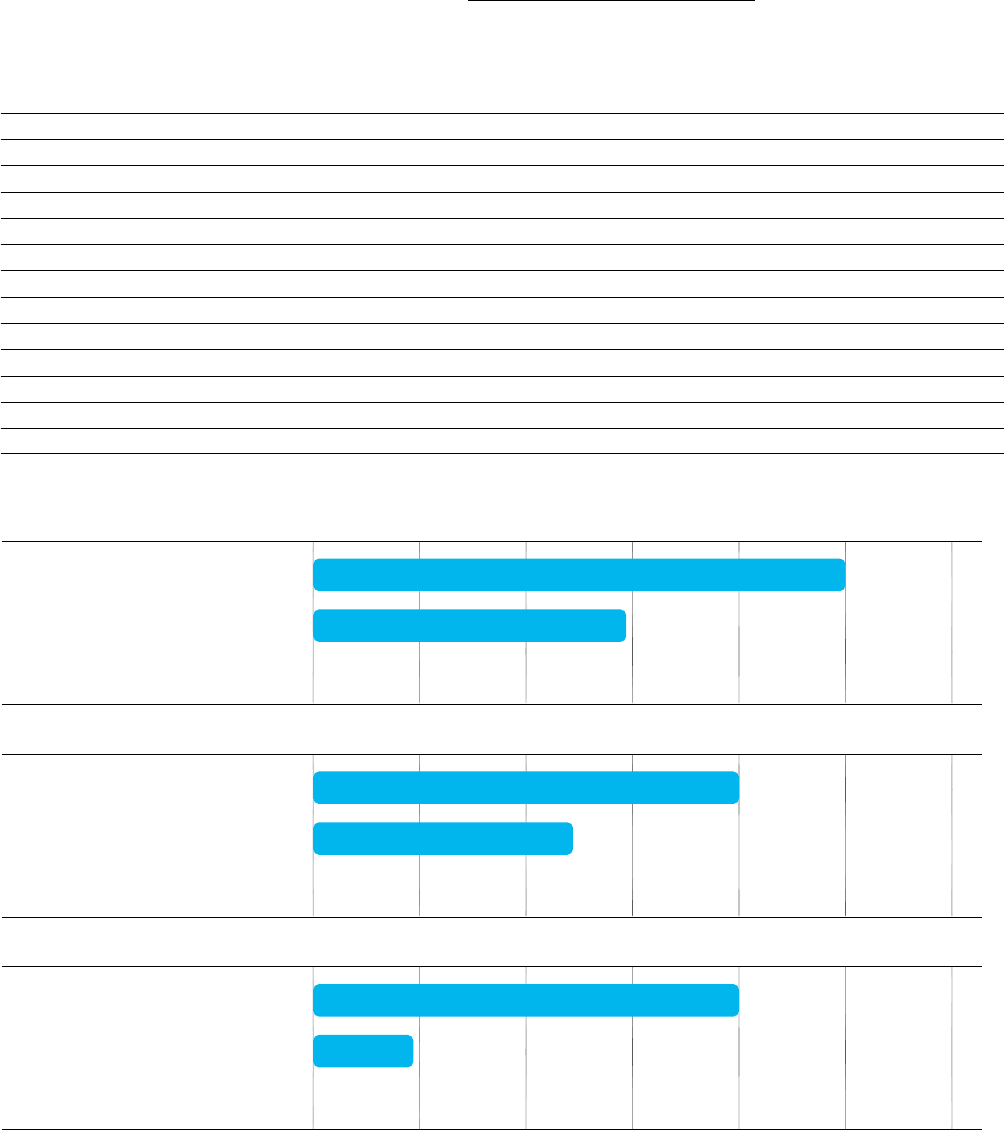

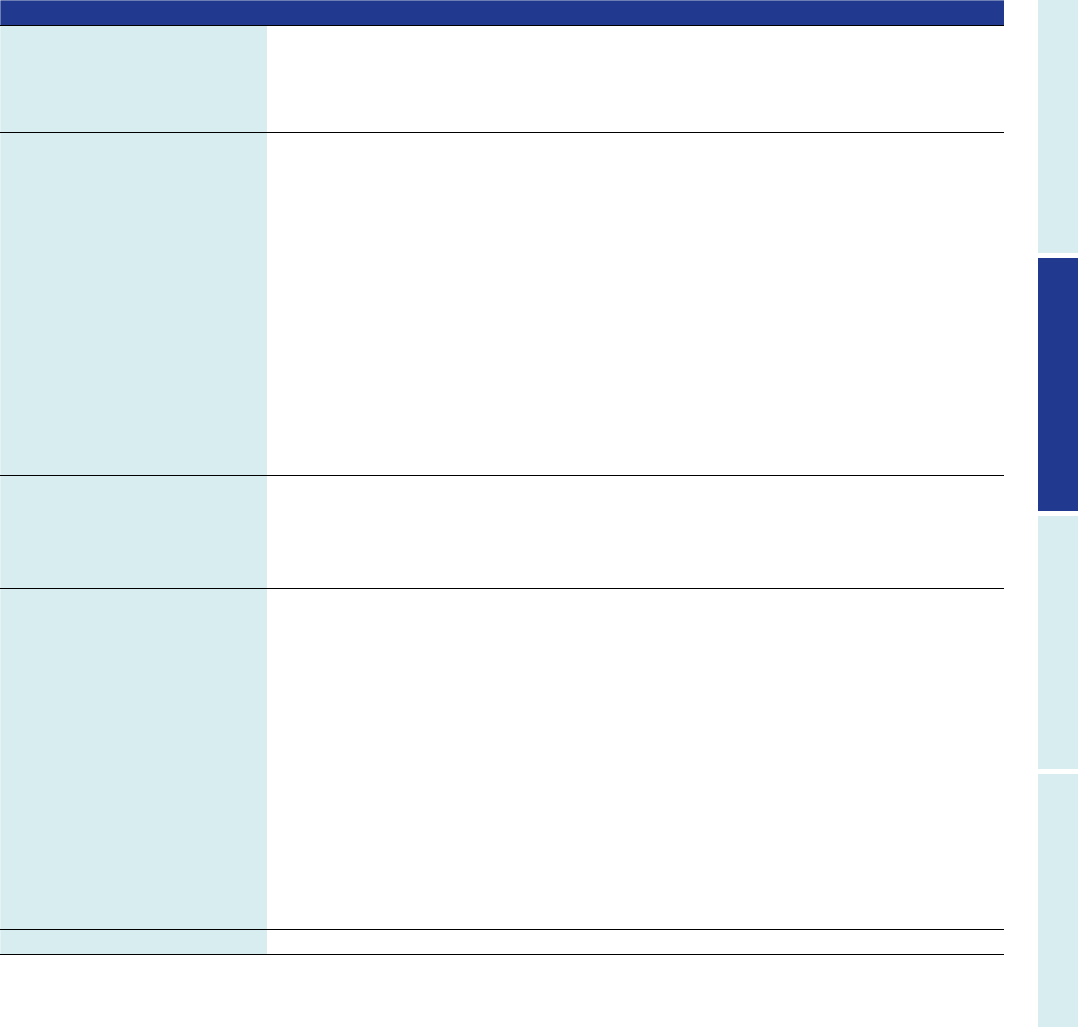

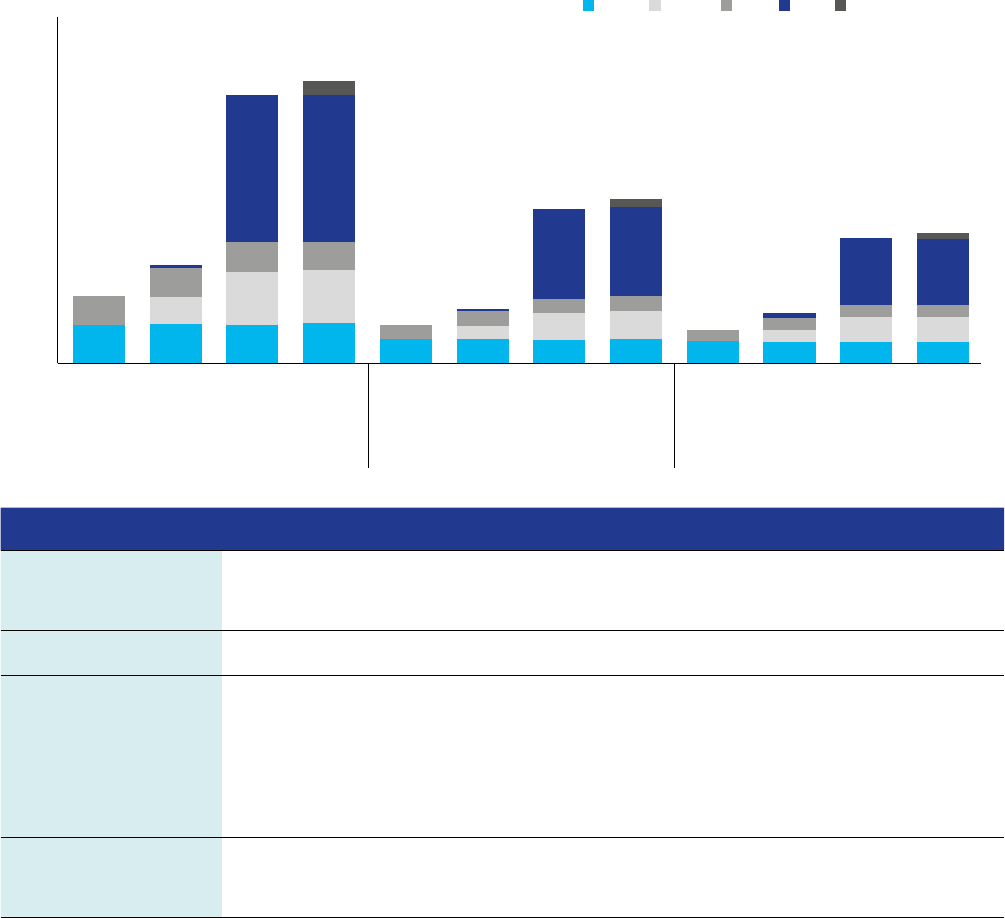

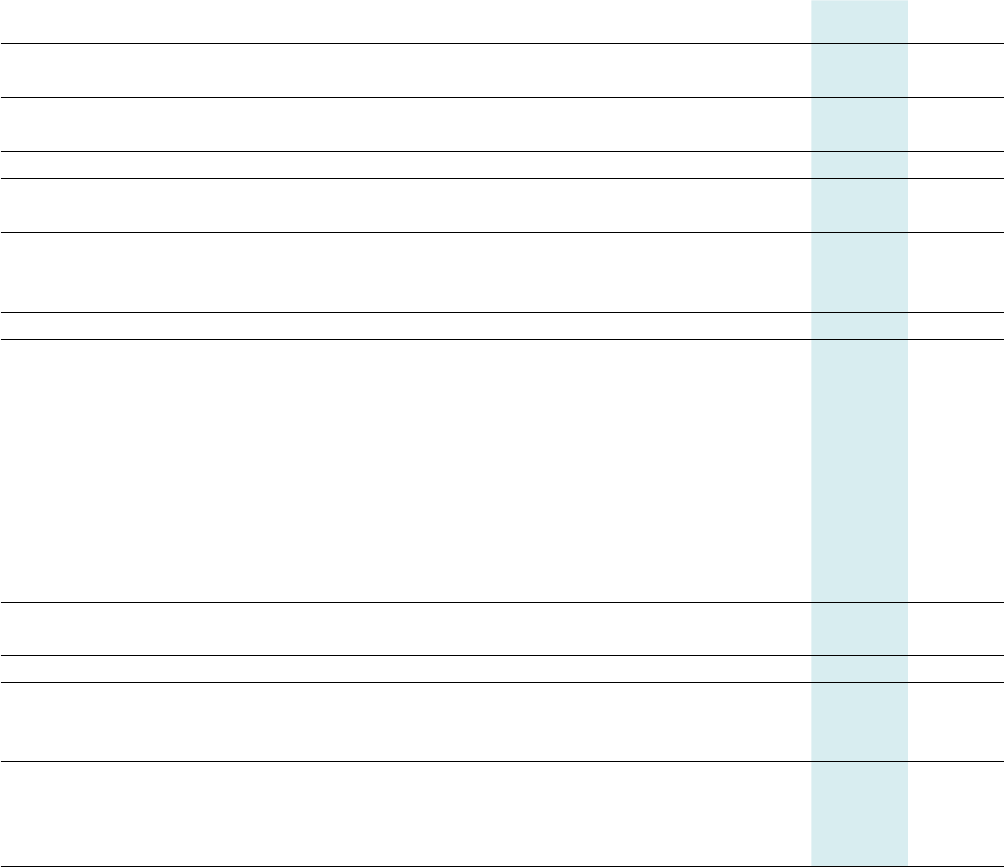

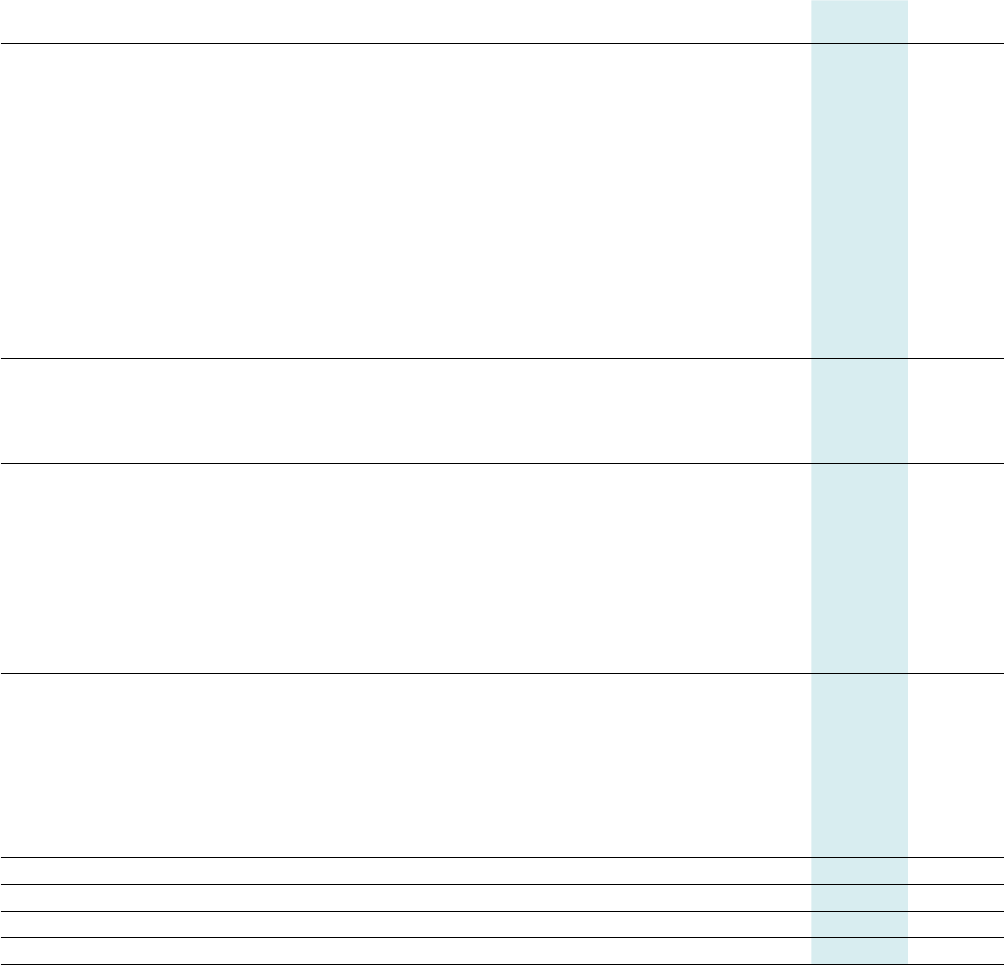

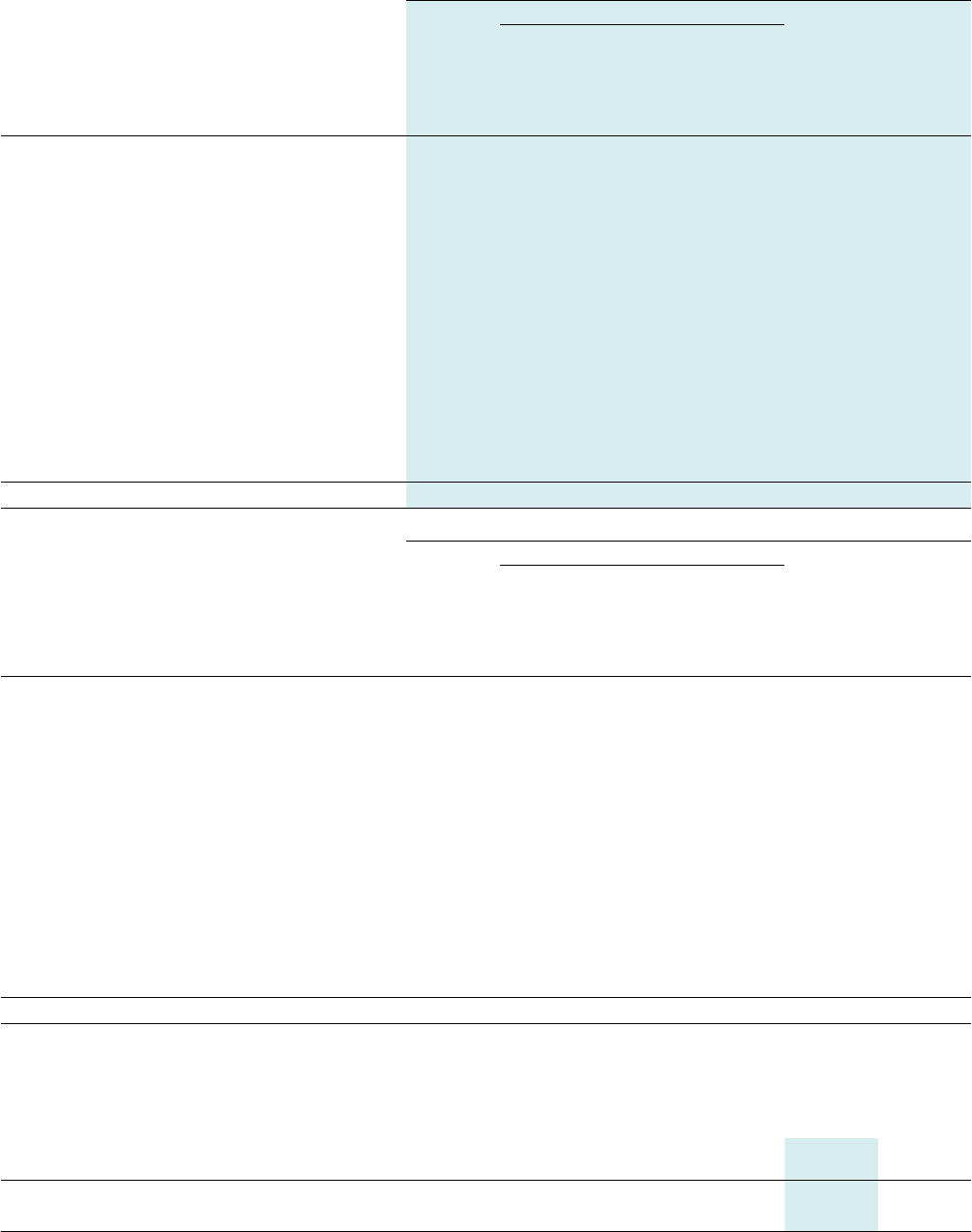

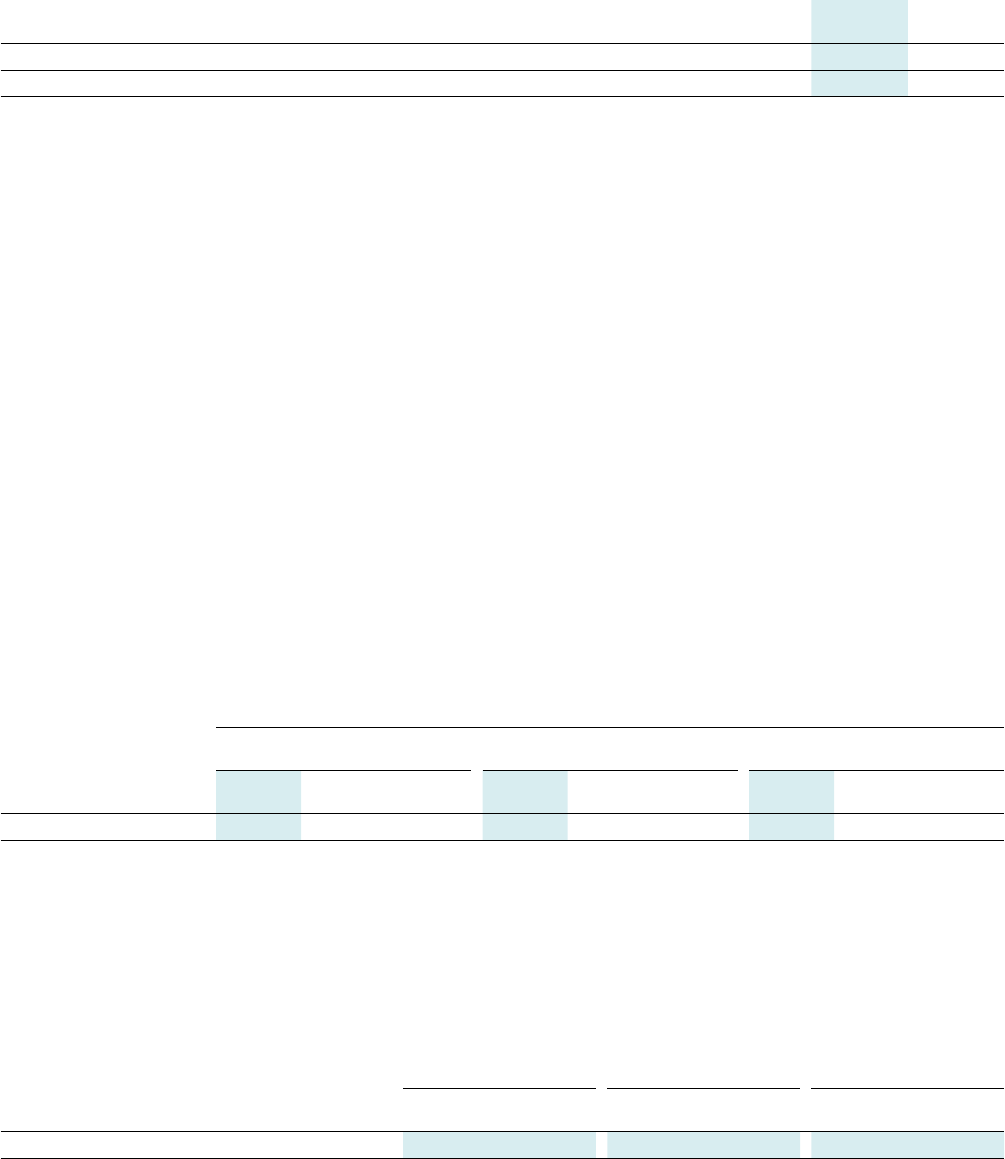

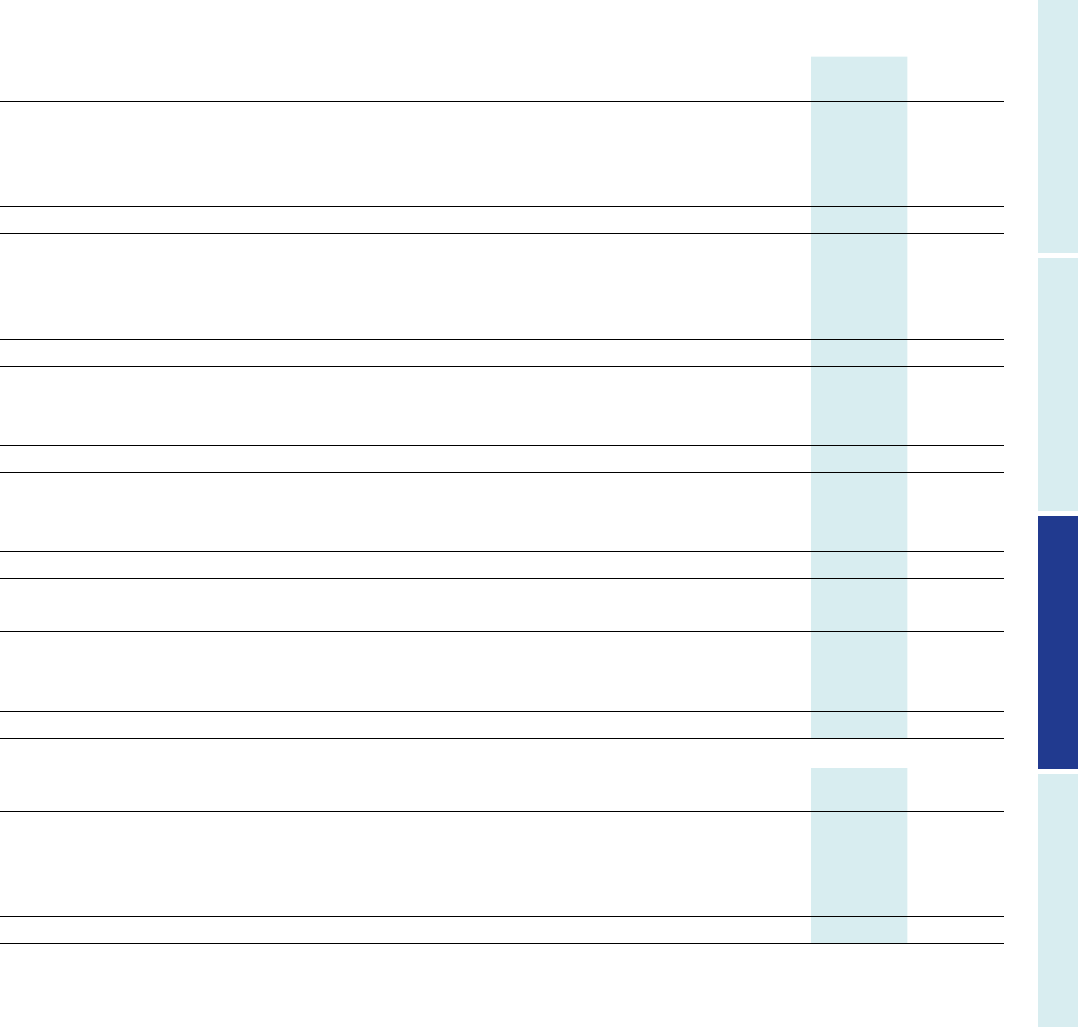

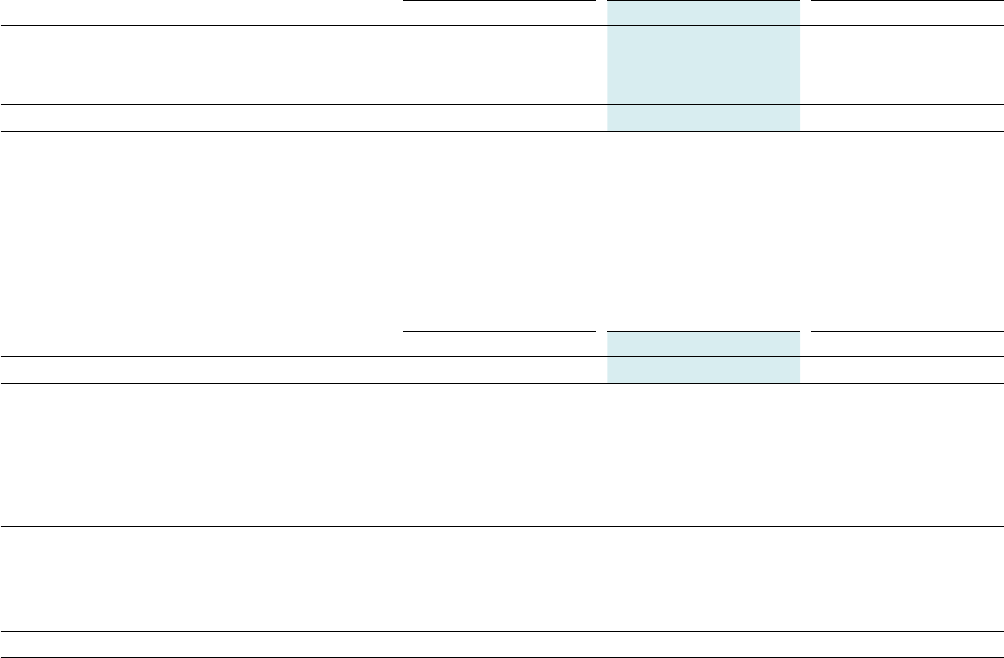

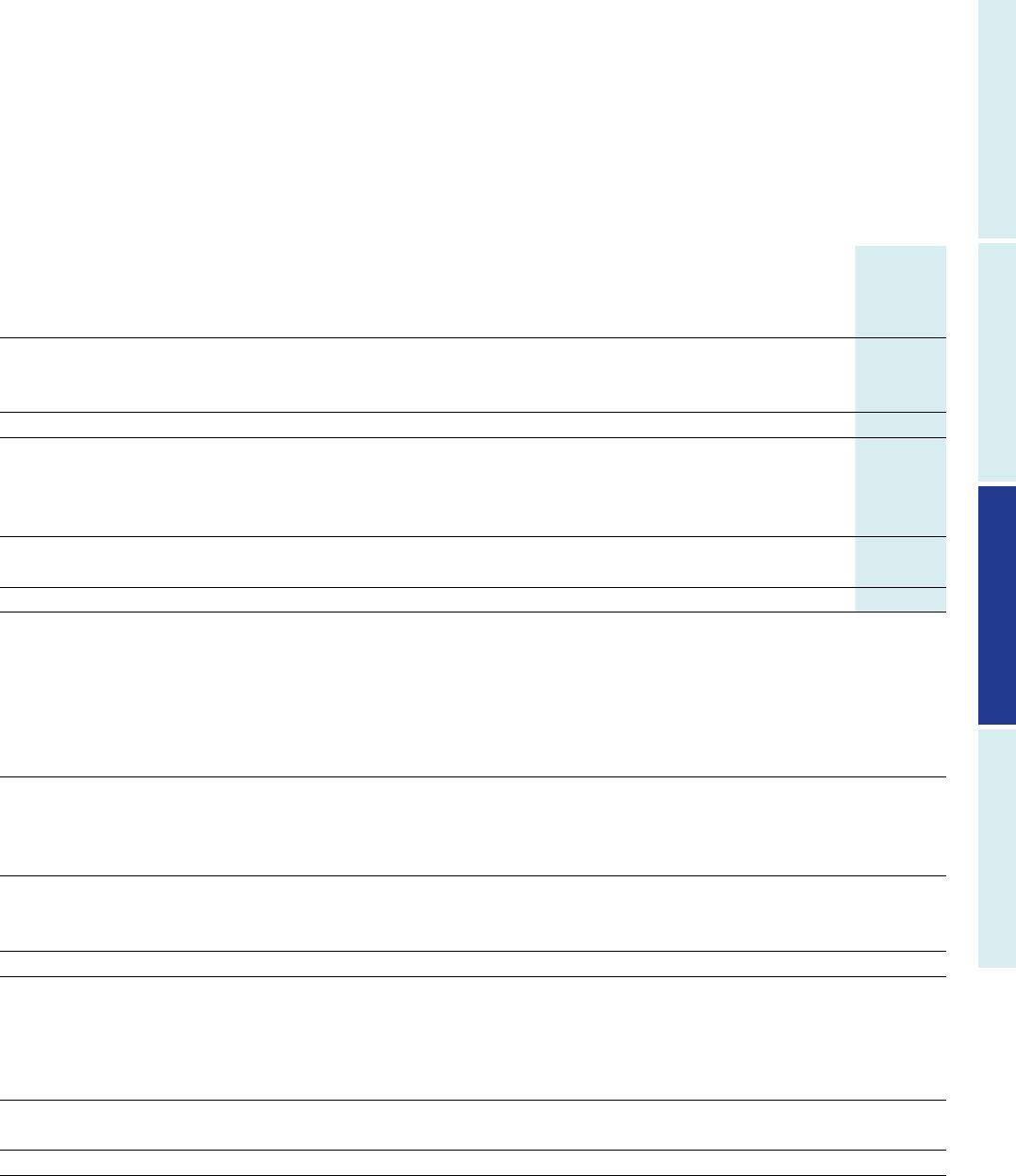

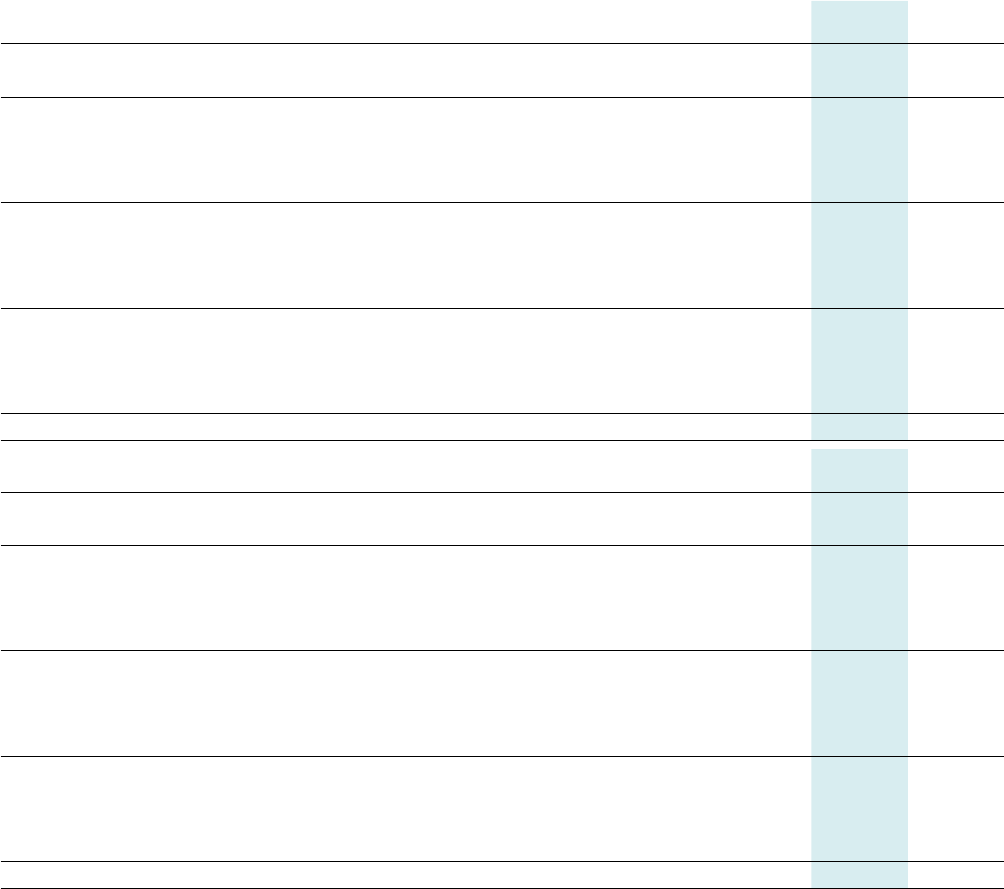

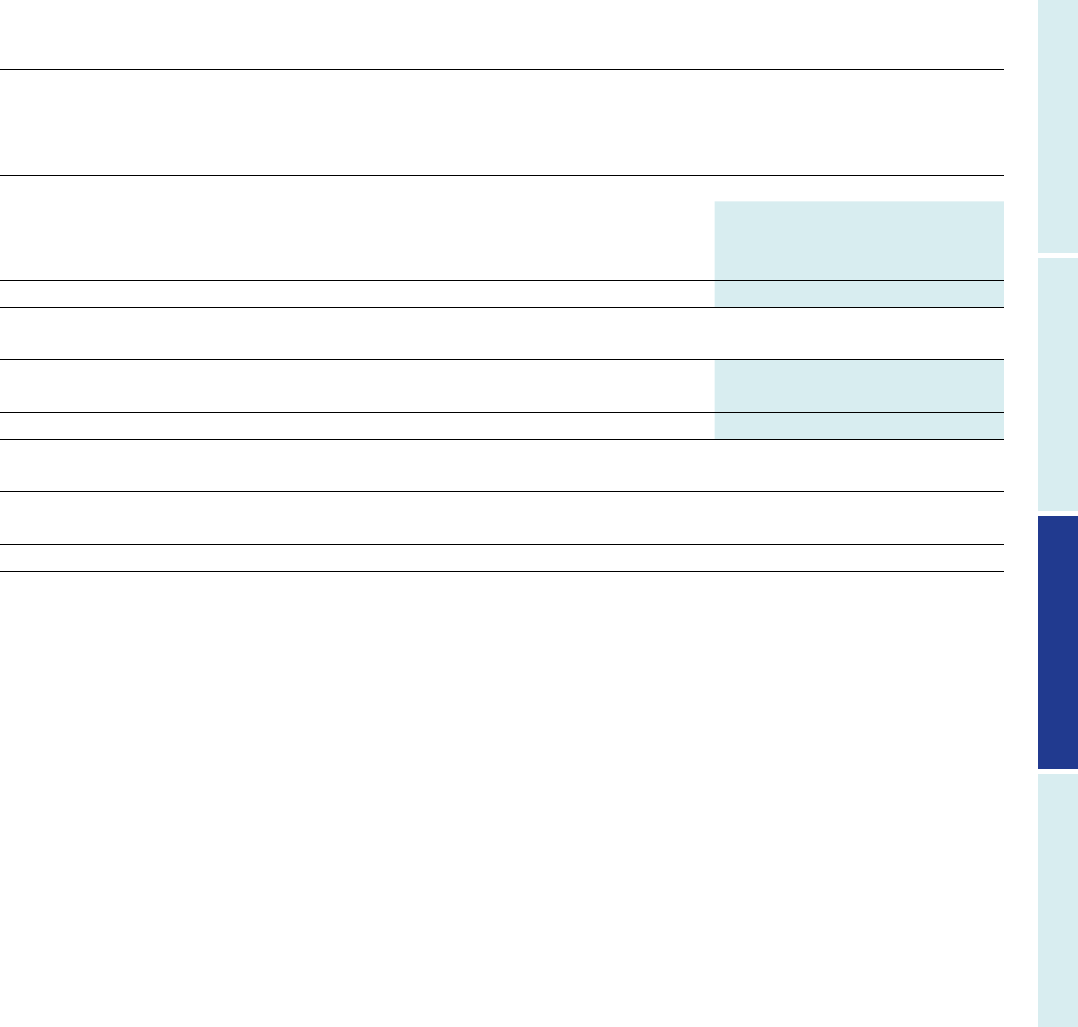

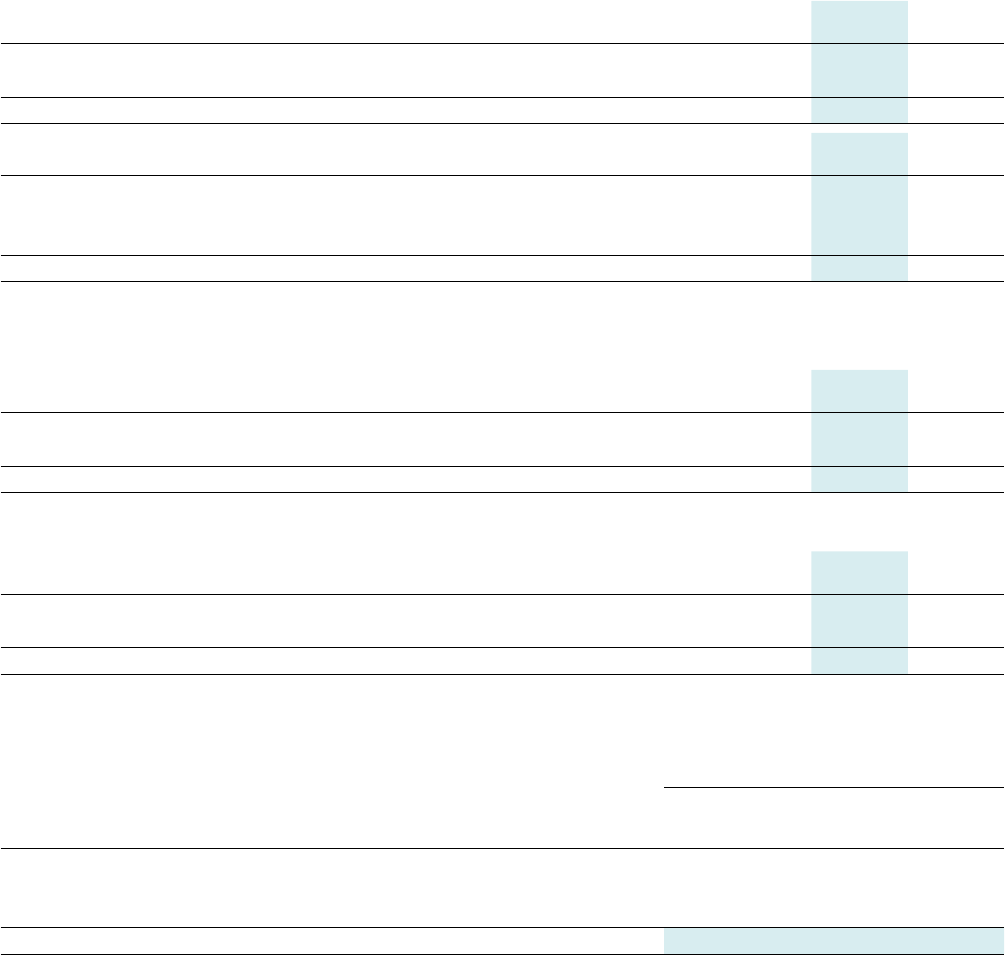

Financial performance

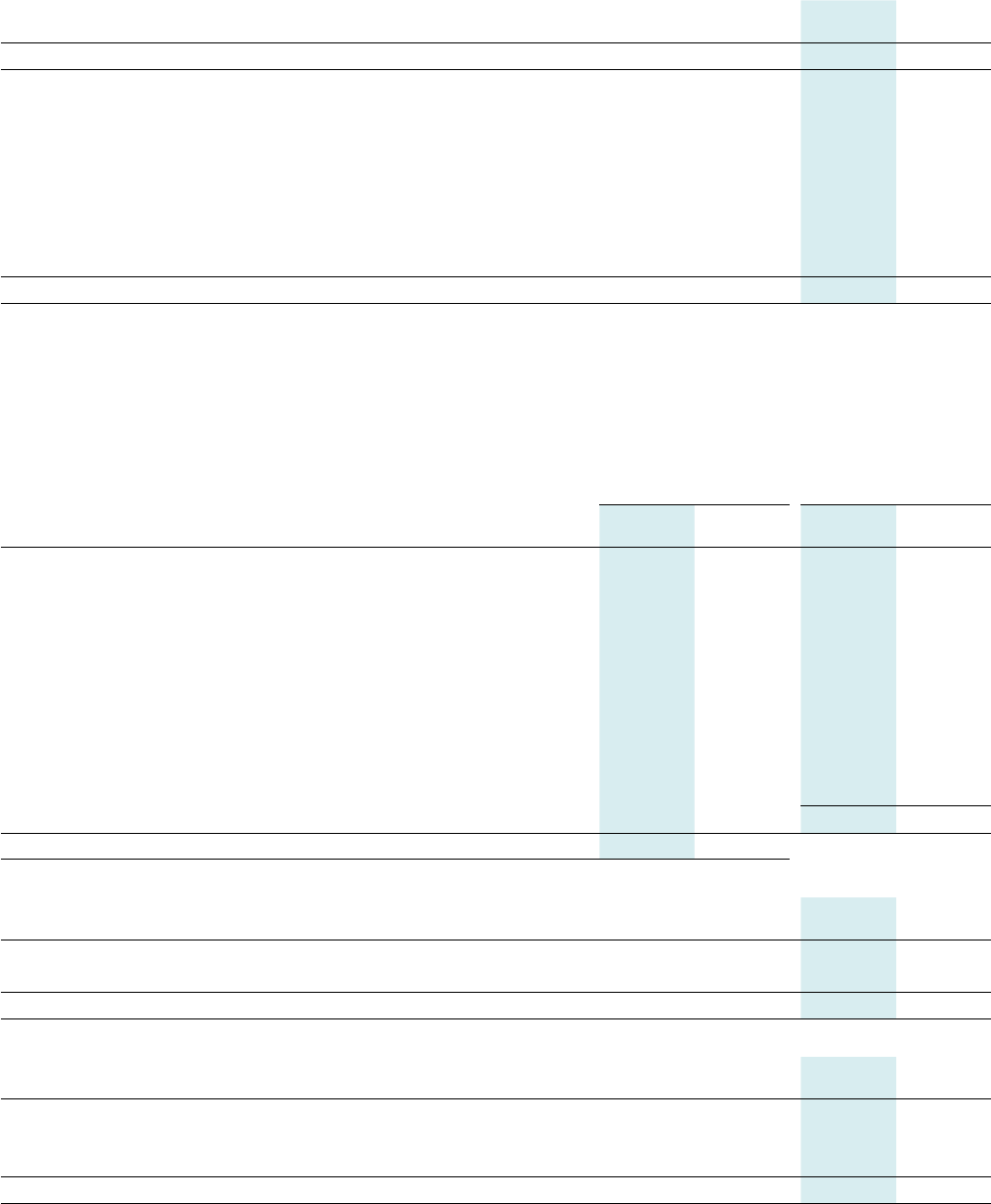

Loss before tax

(£254.2m)

Basic loss per share

(185.8p)

Underlying Earnings/(Loss)

PerShare

2

11.9p

Leverage ratio

7.5x

Underlying Profit/(Loss)

BeforeTax

2,3

£21.5m

Available Operating Cash Flow

2,3

£54.9m

-200

-150

-100

-50

0

2022/232021/222020/21

(67.0p)

(20.1p)

(185.8p)

0

2

4

6

8

10

12

2022/232021/222020/21

10.3x

11.7x

7.5x

-15

-10

-5

0

5

10

15

2022/232021/222020/21

13.2p

(11.1p)

11.9p

0

20

40

60

80

2022/232021/222020/21

£3.4m

£75.8m

£54.9m

-300

-250

-200

-150

-100

-50

0

(£61.2m)

(£23.5m)

(£254.2m)

2022/232021/222020/21

-10

0

10

20

30

2022/232021/222020/21

£17.1m

(£6.7m)

£21.5m

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 11

For the 2023/24 financial year, the River

Cruise business is expected to generate a

small Underlying Profit Before Tax

4

before

becoming a more meaningful proportion of

the Group’s earnings over time. In support of

this, bookings for the year ending 31 January

2024 are strong and, at 26 March 2023,

wehad already secured bookings from more

than 12,500 guests which equated to a load

factor of 63% and per diem of £298.

We actively encourage our guests to openly

express their views and provide feedback in

relation to our Cruise oering as it is this that

allows us to continuously enhance our guest

experience. We are exceptionally proud that,

at 31 January 2023, our guest satisfaction

score was 9.0out of 10 for Ocean Cruise and

8.2 for River Cruise.

Travel

Our Travel business returned to more normal

operations following the COVID-19 pandemic

and, as such, revenue for the year ended

31January 2023 increased by more than

10times when compared with the year

before. The business reported a small

Underlying Loss Before Tax

4

of £4.1m.

2022/23 was a year of transformation for

ourTravel business, moving from a largely

traditional paper-based business to one that

oers awe-inspiring holidays through a more

digital and agile operating model.

As part of the move, we developed a series of

exciting new products, including ‘Tailor-Made

by Saga’, which oers customers a truly

personalised travel experience, and our

private jet tours which represent our most

luxurious holidays yet with a succession of

unforgettable encounters and travel

exclusively by chartered plane. In addition, all

bookings now benefit from our Saga Deluxe

and Titan VIP Travel Services which include

home-to-airport pick up, airport lounge

access and fast-track security clearance

atselected UK airports.

Customer feedback received to date in

relation to our revamped Travel oering has

been incredibly positive and is reflected in

ourforward bookings. At 26 March 2023,

booked revenue totalled £136.6m which is

32% ahead of the same point in the prior year.

This level of bookings places the business

firmly on track to return to profit in 2023/24.

Insurance

The UK insurance market has faced

particularly challenging times over the past

year as insurers adjusted to market-wide

regulatory changes and high levels of

claimsinflation.

Overall, Insurance Broking reported an

Underlying Profit Before Tax

4

, on a written

basis, of £67.7m which compares to £66.6m

in the previous year.

The number of policies in force across all

products, at 31 January 2023, was 1.7m or

3%behind the position at 31 January 2022.

Total policy sales for the year as a whole were

2% behind the prior year, reflecting a 103%

increase in the number of travel insurance

policies sold, broadly stable sales ofprivate

medical insurance and motor andhome sales

that were 7% behind the prior year.

While the level of new motor and home

policies sold was significantly behind the prior

year at 50% and 17% respectively, customer

retention improved to 83.8%, or 1.0ppt

ahead of the prior year. The average margin

per policy was £71, compared with £74 in

theyear before.

The proportion of customers coming

toSagadirectly, rather than through

price-comparison websites, was 49%,

compared with 59% in the prior year,

reflecting the competitive nature of

themarket.

Our Insurance Underwriting business

reported an Underlying Profit Before Tax

4

of

£19.1m for the year, supported by £25.1m of

underlying prior year reserve releases.

Excluding the impact of these reserve

releases, and our quota share reinsurance

arrangements, our current year underlying

combined operating ratio was 125.8% which

compares with 96.3% in the prior year.

Thisreflects the expected unwind of the prior

year COVID-19 frequency benefits, a sharp

rise ininflation to the cost of settling claims

and anabove-average level of current year

largeclaims.

In response to the rise in claims inflation,

throughout the year, we applied material

increases to our pricing which incorporated

both the level of inflation already observed,

and the expected inflation in the coming year.

Money

Our personal finance business, Saga Money,

reported an Underlying Profit Before Tax

4

of

£2.3m for the 2022/23 financial year, broadly

in line with that of the prior year.

In equity release, which was supported by

thelaunch of our new television advertising,

total loan volumes were 29% ahead of the

prior year, with the average loan value also

19% higher.

Our savings product, provided in partnership

with Goldman Sachs, secured 17% more

accounts than in the year ended 31 January

2022, with assets under management of

around £3.5bn.

2. Step-changing our ability

to scale while reducing debt

The second focus within our growth plan is on

reducing our level of debt and step-changing

our ability to scale the business. At 31 January

2023, Net Debt

4

was £711.7m, £17.3m lower

than at 31 January 2022. This represents the

Group’s gross debt at that date, less £157.5m

of Available Cash

4

.

Following two years of agreed deferrals, we

re-commenced payments on our two ocean

cruise ship facilities and a total of £46.4m

wasrepaid during 2022/23. Future Cruise

bookings are encouraging and, over time,

weexpect to generate sucient cash from

Ocean Cruise to meet interest and capital

repayments, including catch-up payments

onelements deferred during the pandemic.

We developed a series of

exciting new products, including

‘Tailor-Made by Saga’ and

ourprivate jet tours which

represent our most luxurious

holidays yet.”

4 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

12 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Group Chief Executive Ocer’s Statement continued

To maintain flexibility in relation to our

short-term liquidity needs, we concluded

discussions with the lending banks behind

ourrevolving credit facility and agreed a

series of amendments, including changes to

the leverage and interest cover covenants

attached to the facility. Full details of the

changes and revised covenant levels can be

found on page 58.

As part of our property strategy, we are

continuously assessing our ways of working

and how best to support colleagues.

Following the pandemic, and in line with our

hybrid working approach, we saw that far

fewer colleagues were choosing to work

regularly from our Enbrook Park

headquarters in Folkestone. We made the

decision to close the site in favour of two

smaller hubs in Kent, inaddition to our

existing London hub. This will reduce

operating expenses while we explore

longer-term options for the site.

As part of our plan to reduce debt and move

towards a more capital-light model, we are

continuing to evaluate our options in relation

to our Insurance Underwriting business and

an active sales process is ongoing.

3. Creating ‘The Superbrand’

for older people

The final step in our growth plan is to create

‘The Superbrand’ for older people through

focus on our brand, data, insights and

customer interactions.

Saga is a brand that has exceptionally high

awareness amongst people over 50, however,

historically too many have seen Saga as

something that ‘isn’t for them’. Over the past

couple of years, our mission has been to

reframe the conversation with a focus on

experience as opposed to age. The brand

relaunch in 2021 was only the start and, since

then, we have expanded our new marketing

campaigns to cover more products, and

increased our customer net promoter

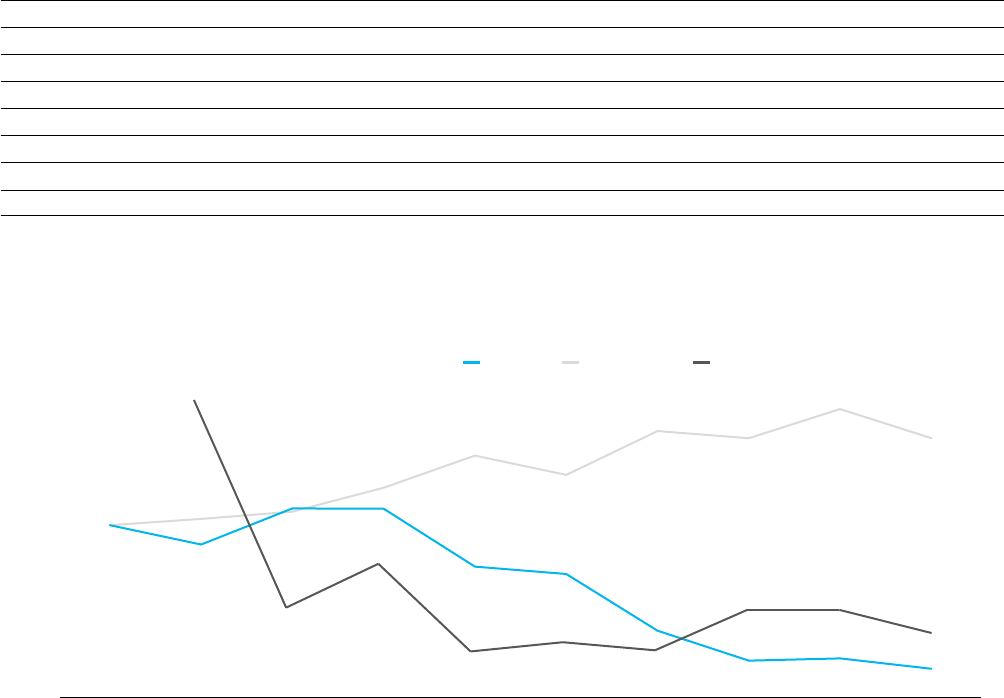

score(NPS) to its highest ever level. When

compared to 2021, NPS in the fourth quarter

was two points higher, at 51. This reflects

improvements within our contact centres

which reduce wait times and improve the

customer journey.

As we highlighted at our Capital Markets

Event in January 2023, the data we hold

andthe way that we use it, will be key to our

success in becoming a superbrand. At the

beginning of the year, we set a target to

achieve three million new consents by

31January 2023 which would allow us to

communicate our products and services to

awider audience than before. I am pleased

toconfirm that we achieved this, and more.

The insights we hold about ‘Generation

Experience’ are crucial as they allow us to

develop products and services that meet the

specific needs of our customers. Following

the acquisition of The Big Window Consulting

Limited at the start of the year, we have taken

great strides in this space. These include

developing our detailed customer

segmentation, building our Experienced

Voices panel which now consists of more than

10,000 of our customers and championing a

conversation on positive ageing, most

recently supported by the release of our

‘Generation Experience’ economic study.

In addition, increasing the depth, and

frequency, of our interactions with customers

is a key part of our superbrand plan. Through

this, we are able to learn more about their

specific interests and viewpoints, enabling us

to continuously improve the products and

services we oer. Saga Media, which was

launched in January 2023, is pivotal to this

process. Through Saga Media, and our

brand-new Saga Exceptional website, we are

providing people over 50 with an online home

and a corner of the internet that is designed

specifically for them. Not only does this allow

us to become part of our customers’ lives and

learn more about what they want, but it will

also become a profit-generative business

inits own right within five years, through

advertising and aliate partnerships.

In order to transform Saga into ‘The

Superbrand’ for older people, we need to

create an exceptional colleague experience,

giving each and every colleague the

opportunity to do the best work of their lives.

During 2022/23, we made great progress

inthis space, providing colleagues with

access to a new reward platform and

enhancing the financial support available

through acceleration of our annual pay

reviewcycle and two additional cost of living

support payments for our colleagues with

lower earnings.

The engagement of our colleagues, measured

through a survey hosted by an independent

third party, remains high at 8 out of 10.

Building Saga into the largest and

fastest-growing business for

olderpeople

We are continuing with the delivery of our

three-step growth plan, focused on

maximising our existing businesses, reducing

debt while step-changing our ability to scale

and creating ‘The Superbrand’ for older

people. We will continue to pay down our

ocean cruise ship debt, and we expect to

repay the £150m bond maturing in May 2024

from Available Cash

5

.

Overall, I am pleased with the progress

madeduring the year as we began to make

the strategic pivot towards becoming a

capital-light marketing, content and

distribution business. We now have the right

team, strategy and structure in place that will

return Saga to sustainable long-term growth.

Finally, I would like to pass my thanks on to our

colleagues for their relentless eorts during

this period of change. I recognise that any

business is only as strong as its colleagues

and, looking at the team around me, that fills

me with confidence.

Euan Sutherland

Group Chief Executive Ocer

17 April 2023

In order to transform Saga

into‘The Superbrand’ for

olderpeople, we need to

createan exceptional colleague

experience, giving each and

every colleague the opportunity

to do the best work of their lives.”

5 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

Read our ‘Generation

Experience’ economic study

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 13

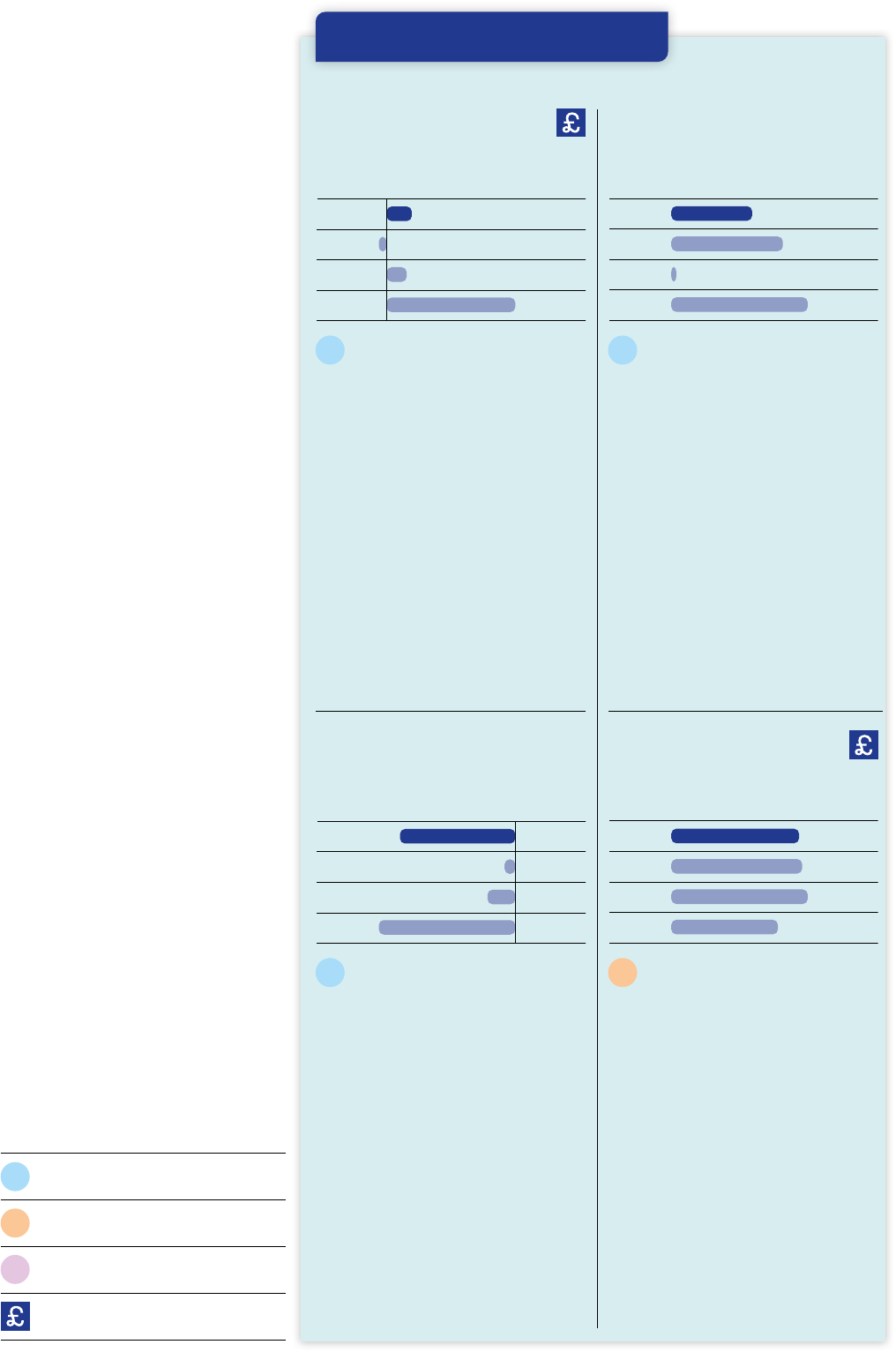

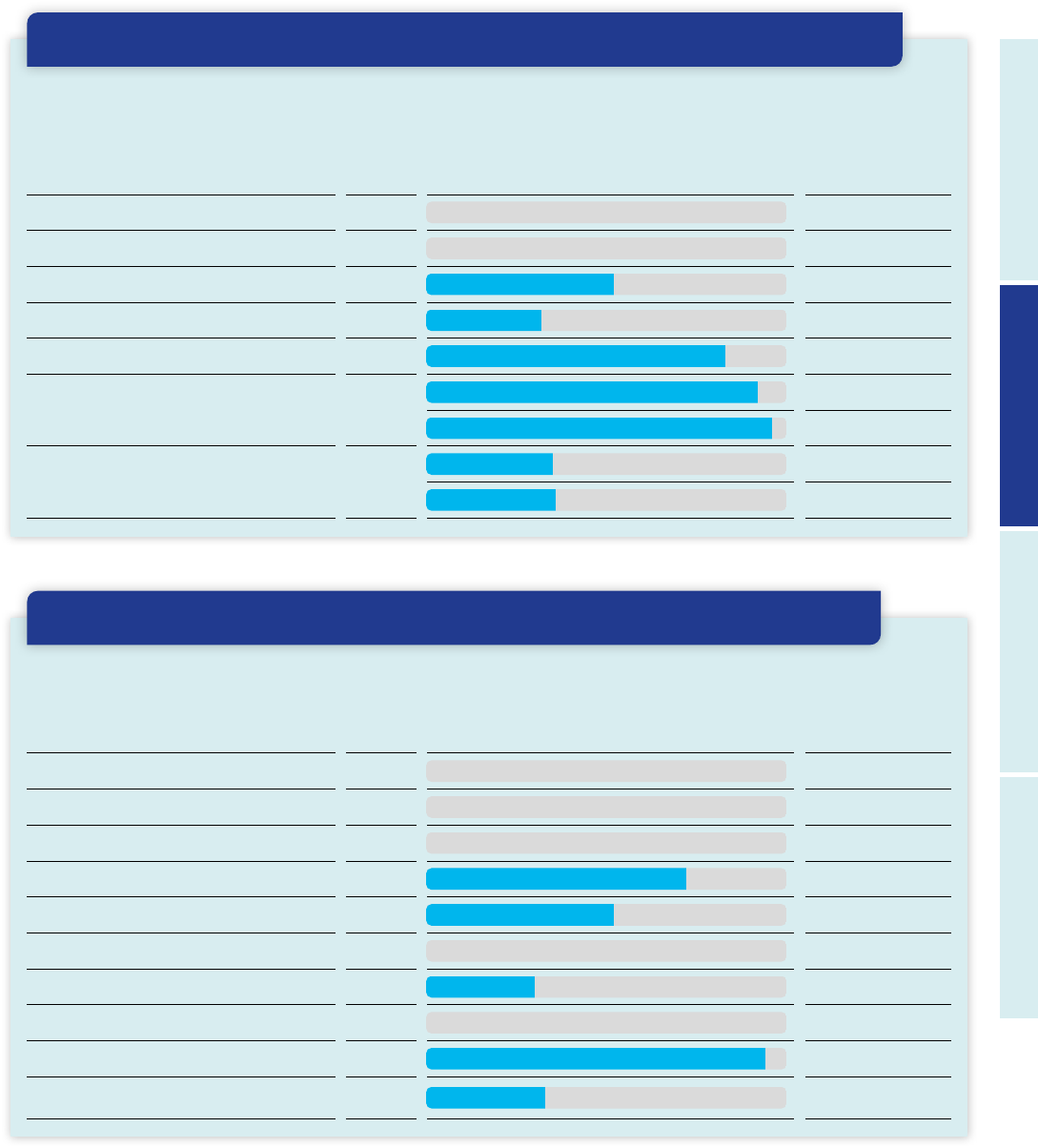

During the financial year,

thefollowing key performance

indicators (KPIs) were used

toassess the financial and

operational performance

ofthebusiness against our

three-step growth plan.

Theseinclude an additional

KPImeasuring our marketable

database, which isone of

severalcontributing elements

to the directors’ remuneration.

RESILIENT

PERFORMANCE

2022/23 Bonus KPIs

References to our three-step growth plan

Creating ‘The Superbrand’

for older people

3

Step-changing our ability to

scale while reducing debt

2

Maximising our existing

businesses

1

1 Refer to the Alternative Performance Measures Glossary on page 209 for definition and explanation

Purpose and definition

Available Operating Cash Flow

1

represents net cash flow from operating

activities which is not subject to regulatory

restriction, after capital expenditure but

before tax, interest paid, restructuring

costs, proceeds from business and

property disposals and other non-trading

items. Refer to page 209 for full definition

and explanation.

Performance

Decrease in Available Operating

CashFlow

1

due to higher central costs,

movements in working capital, lower

dividends from our Underwriting

business and higher capital expenditure,

partly offset by increased cash

generation from Cruise and Travel.

Financial KPIs

Purpose and definition

Underlying Profit/(Loss) Before Tax

1

isthe Group’s primary KPI and a

meaningful representation of the

Group’s underlying trading performance.

It is defined as loss before tax excluding

items which are not expected to recur.

Refer to page 209 for full definition

andexplanation.

Performance

Increase of £28.2m in comparison to

2021/22, largely as a result of our Cruise

and Travel operations returning to more

normal operating conditions as we

emerge from the pandemic.

1

Purpose and definition

Loss before tax as presented in

accordance with UK-adopted

international accounting standards.

Performance

Loss before tax for the year of £254.2m,

reflecting a £269.0m Insurance goodwill

impairment alongside other smaller

one-off below the line items.

1

Loss before tax

(£254.2m)

(£254.2m)

(£23.5m)

(£61.2m)

(£300.9

m)

2019/20

2020/21

2021/22

2022/23

Underlying Profit/(Loss)

BeforeTax

1

£21.5m

£21.5m

(£6.7m)

£17.1m

£109.9m

2019/20

2020/21

2021/22

2022/23

1

Available Operating CashFlow

1

£54.9m

£54.9m

£75.8m

£3.4m

£92.7m

2019/20

2020/21

2021/22

2022/23

Purpose and definition

Net Debt

1

represents the sum of the

carrying value of the Group’s debt

facilities, less the amount of Available

Cash

1

it holds. Refer to page 59 of the

Group Chief Financial Officer’s Review

for a full breakdown.

Performance

Net Debt

1

reduced by £17.3m compared

with 31 January 2022, as a result of

thenet operating cash generated

anddividends received from our

Underwriting business being only

partially offset by movements in working

capital, cash injections into our River

Cruise and Travel businesses, capital

expenditure and the servicing of debt.

Refer to page 54 of the Group Chief

Financial Officer’s Review for full details.

2

£711.7m

Net Debt

1

£711.7m

£729.0m

£760.2m

£593.9m

2019/20

2020/21

2021/22

2022/23

14 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Key performance indicators

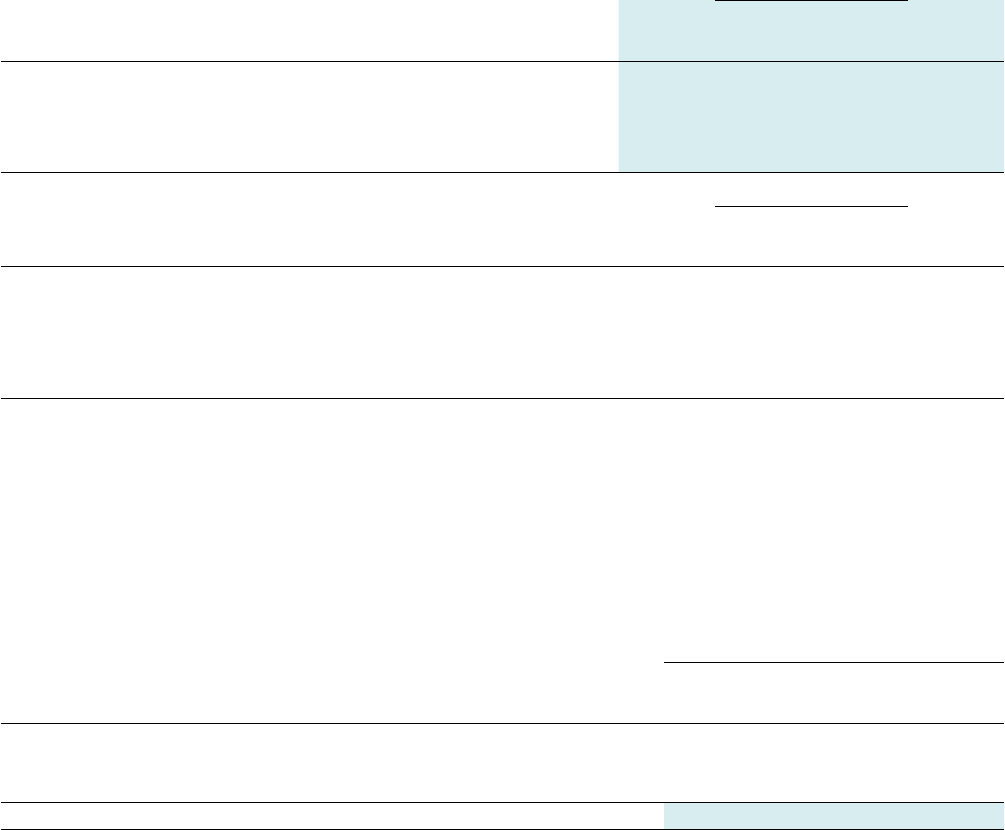

1 1 1

3 3 3

Motor and home insurance

customer retention

Ocean Cruise load factor

2

Ocean Cruise per diem

2

83.8% 75% £318

Purpose and definition

Motor and home retention is a key

indicator of performance within the

Insurance business and represents

theproportion of motor and home

customers who choose to remain with

Saga when their policy is due for renewal.

Performance

Motor and home retention is 1.0ppt

ahead of 2021/22, due to market-wide

regulatory changes that give customers

more reason to stay loyal to their insurer.

Purpose and definition

Load factor is the most sensitive

driverof Cruise profit before tax and

represents the booked proportion of

the total capacity across our two ocean

ships. It is calculated by dividing the

number of berths booked by the total

berths available.

Performance

Load factor of 75% for 2022/23,

reflecting 66% in the first half of the

year, following residual impacts from the

pandemic and geopolitical uncertainty,

and 84% in the second half of the year

aswe returned to more normal

operating conditions.

Purpose and definition

Per diem provides an indication of

pricing within the Cruise business and

reflects the average revenue charged

per guest per night on board our

oceancruise ships.

Performance

The £318 per diem for 2022/23 is

significantly ahead of the prior year,

reflecting the impact of inflation

andimprovements made to our

Cruiseproducts to enhance the

guestexperience.

Customer net promoter

score(NPS)

Colleague engagement

3

Marketable database

51 8.0 out of 10 5.9m

Purpose and definition

Customer NPS represents the

willingness of customers to recommend

Saga products and services to family,

friends and colleagues. The score is

calculated by analysing customer

surveyresponses and subtracting the

percentage of detractors (those scoring

six or less) from the percentage of

advocates (those scoring nine or more)

which is then weighted by business unit.

Performance

Customer NPS reached a record high

of51, reflecting improvements within our

contact centres which reduce wait times

and improve the customer journey.

Purpose and definition

Colleague engagement provides an

indication of how committed and

enthusiastic colleagues are towards

both Saga and their work. It is measured

through responses to quarterly

colleague surveys hosted by an

independent third party.

Performance

Overall colleague engagement increased

to 8.0 from our previous score of 7.7

reflecting higher scores in loyalty and

satisfaction as a result of the support

that colleagues received in response to

the rising cost of living.

Purpose and definition

Our marketable database reflects the

number of people over 50 for whom

wehold details and are able to contact

via either post or email in relation to the

products and services offered byat

least one of our business units.

Performance

Our marketable database has been in

decline due to lapsing permissions and

ahigher proportion of customers opting

out of postal communications. The rate

of decline has, however, slowed over

time due to an increase in customers

opting in to email.

Non-financial KPIs

83.8%

82.8%

80.5%

75.1%

2019/20

2020/21

2021/22

2022/23

51

49

44

38

2019/20

2020/21

2021/22

2022/23

75%

68%

2021/22

2022/23

8.0

7.7

November 2021

November 2022

£318

£299

2021/22

2022/23

5.9m

6.2m

7.9m

31 January 2020

31 January 2021

31 January 2022

31 January 2023

8.2m

2 No comparative data prior to 2021/22 has been provided for Cruise, as operations were suspended for much of 2020/21, with the offering prior to that not

comparable with our two current ocean ships

3 During 2020/21, Saga appointed a new third-party survey provider. As such, the data prior to February 2021 is not comparable

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 15

Saga operates in highly attractive

markets, serving the fastest-growing

and wealthiest demographic with

significant opportunity for growth.

DELIVERING IN CHALLENGING MARKETS

Our customers

…and this population is expected to grow

faster than any other age group

1

There were an

estimated

26.1m

individuals in the UK aged

over 50 during 2022

1

…spending

£292bn

per year on non-household

expenditure

2

Saga exists to serve people over 50 with uniquely

tailored products and services, accompanied

byexceptional experiences. This segment of

theUK population is the fastest-growing

demographic in the UK today with considerable

disposable wealth.

We know that people, their views and their needs change as they

age and that these changes impact their spending behaviours.

AtSaga, we are uniquely positioned to fulfil these needs by

utilising our in-depth insights and data to oer meaningful,

relevant and compelling products and services to this group.

Our businesses

While we continue to face significant competition in

the more commoditised areas of the business, with

the use of our unique insight and data, we have, and

will continue to develop differentiated products to

suit the specific needs of our customers.

Cruise

In Cruise, while we have a significant number of competitors, we

are uniquely placed within the market, oering a truly all-inclusive

UK-to-UK experience on board smaller, purpose-built luxury

ships that consistently deliver exceptional service.

Travel

In what continues to be a commoditised market, our recently

relaunched Travel business constantly develops and launches

new products that set us apart, with our new private jet tours

being a prime example of this.

Insurance

The UK market remains competitive, particularly within motor

insurance, following the regulatory changes arising from the

FCA’s review into GIPP andthe impact of inflation on the cost

ofsettling claims. We will continue to grow the range of products

weoer our customers, focusing not only on motor and home

insurance but also on how we can provide our customers with

great value and peace of mind for their wider insurance needs.

1 Office for National Statistics – 2020-based principal projections

2 ‘Generation Experience’ economic study – Total VAT receipts for the 2021/22 tax year were £117.4bn. While no age breakdowns of that data exist, using the Office

for National Statistics data on total expenditure per person based on the age of the ‘household reference person’, we estimate that VAT receipts from individuals

aged 50 years and over amount to £58.4bn. Assuming the standard 20% rate of VAT, this equates to an estimated £292bn of non-household expenditure from

this age group

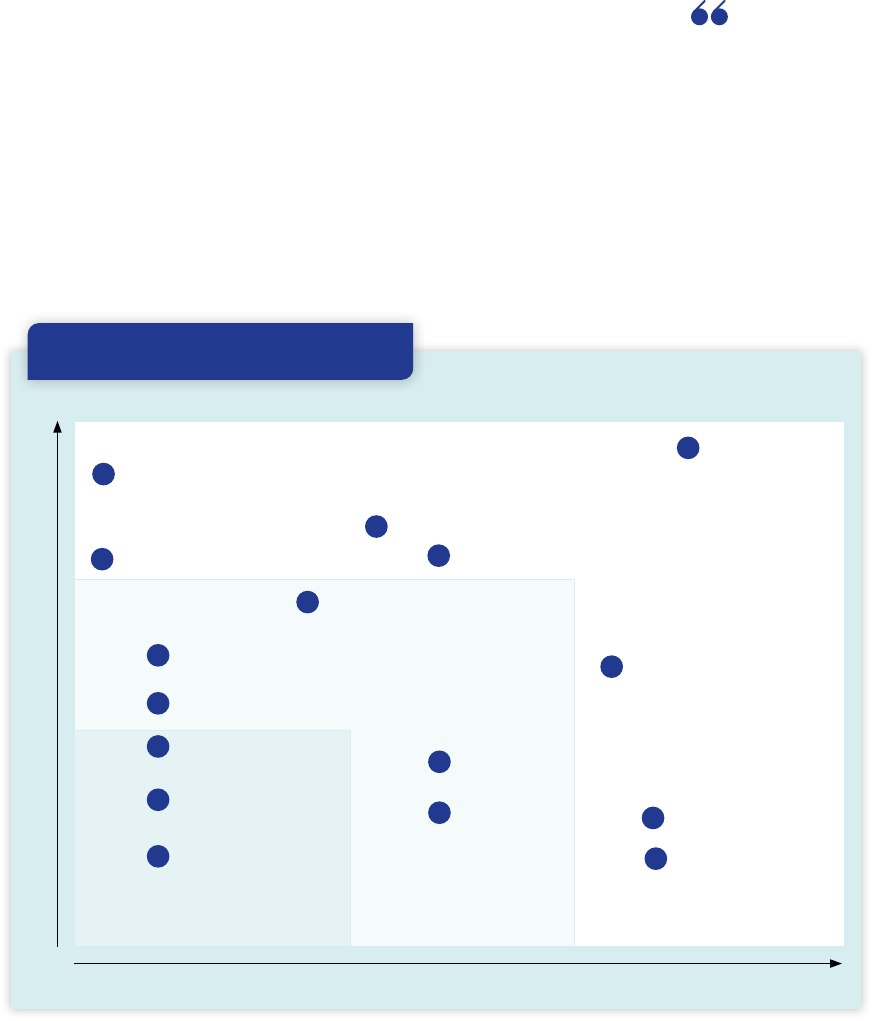

2022 2024 2026 2028 2030 2032

(1.0)

(0.5)

–

0.5

1.0

1.5

2.0

2.5

0-29-year-olds

Predicted population

growth by age (m)

30-49-year-olds 50+ year-olds

16 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Market review

Regulatory and legislative developments

Macroeconomic conditions

Background

Our Insurance Broking and Money

businesses are regulated by the FCA,

withthe Insurance Underwriting business

regulated by the Gibraltar Financial

Services Commission operating under the

Solvency II Directive. The Travel business is

regulated by the Civil Aviation Authority

and is a member of the Association of

British Travel Agents (ABTA) as well as an

Accredited Agent of the International

AirTransport Association. The Cruise

business is regulated by the International

Maritime Organisation, the Maritime and

Coastguard Agency and is a member of

the Cruise Lines International Association,

the UK Chamber of Shipping and ABTA.

Saga also operates processes and

procedures to comply with other

regulations and legislation that apply to

itsbusiness including, but not limited to,

the Data Protection Act 2018, the Bribery

Act 2010, the Equality Act 2010 and health

and safety legislation.

Developments during the year

During 2022, Saga implemented the FCA

policy requirements for GIPP to address

the dierence between new business and

renewal pricing for motor and home

policies. The changes came into eect on

1January 2022 and we believe they are

positive for consumers as a whole and

encourage more focus on service and

claims handlings as prices become more

aligned across the industry.

In July 2022, the FCA published its policy

statement, ‘A new Consumer Duty’, which

incorporates new consumer protection

standards in retail financial services,

designed to raise overall customer

outcomes and to encourage firms to

‘getitright first time’. It is supported

through a set of rules and four customer

outcomes, and is the cornerstone of

theFCA’s three-year strategy. The new

rules come into force on 31 July 2023

andSagais well positioned to meet

thesenew standards, building upon

customer-orientated working practices

already embedded and operating to

goodeect.

The macroeconomic environment was

volatile during 2022, with rapid changes

tosanctions, rising food, energy and wage

costs, and supply chain shortages which

were partly driven by the Russian invasion

of Ukraine, but also impacted by Brexit,

theCOVID-19 pandemic, UK Government

leadership changes, and adjustment to a

post-pandemic operating environment.

These significant events, often viewed

as‘black swan’-type events, have led to

interlinked and compounded impacts

which have been complex to navigate

across industries. The factors which

posedthe most risk to Saga were increases

to claims inflation which impacts our

Insurance business, the costs of goods

andservices, wage inflation, the ability

toattract and retain colleagues and the

cost of living crisis.

Post-pandemic operating

With no COVID-19 restrictions throughout

the majority of 2022 in most jurisdictions,

the Cruise business continued its return

toservice. A COVID-19 crew vaccination

programme remained in place to ensure

the safety of all on board, and tried and

tested COVID-19 protocols are ready to

be re-initiated if needed.

Elsewhere in the business, although

absences due to COVID-19 fluctuated

throughout 2022, they were significantly

lower than the previous year. We continue

to see higher rates in the contact centre

incomparison with other areas however,

this is managed through the absence

protocols in place.

Increased claims inflation

Material increases in claims inflation have

proved a challenging environment for the

insurance market, with inflation emerging

o the back of changing claims trends

through COVID-19 periods and the

impacts of the FCA’s review into GIPP.

OurUnderwriting business focused on

disciplined management of the result,

actioning material price increases as well

as developing and delivering a range of

initiatives to mitigate inflationary impacts.

Claims inflation is now tracking in line with

expectations and is forecast to reduce

next year.

Recruitment and retention

During the latter half of 2021, UK

companies started to suer high levels

ofresignations, commonly referred to

asthe ‘Great Resignation’. This elevated

attrition continued into 2022 across

theindustry, and, in Saga, particularly

impacted those with less than 12 months’

service in the contact centres.

We adapted our recruitment approach

during 2022 and began recruiting

nationwide to mitigate the issue. Attrition

plans were in place throughout 2022 to

fully understand and address the reasons

behind colleagues leaving, and continued

focus on this in 2023 is expected to further

reduce colleague turnover.

Cost of living crisis

With rising cost of living pressures in 2022,

we supported our colleagues in a number

of ways. We awarded all colleagues a 2.5%

pay increase in February 2022 and brought

forward our February 2023 pay increase

to award a further 5% in December 2022

for colleagues below senior leadership

level. Additionally, we provided a lump sum

payment of £500 in September 2022,

andagain in February 2023, to all

colleagues below senior management

level. Overall, for 2022, colleagues below

senior management received an average

11% pay increase in the year and senior

management received a 7.5% pay increase

to assist with the rising cost of living.

Colleagues also had access to a wide

rangeof benefits including an Employee

Assistance Programme, mental health

first aiders, a hardship fund and retail and

supermarket discounts.

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 17

Our purpose is to deliver exceptional experiences every day, whilst being a driver of positive change

inour markets and communities. We are a direct-to-customer marketing, content and distribution

business with unique insights into our customers that help us build long and deep relationships.

Our colleagues and culture

We recognise that our colleagues are key to delivering

exceptional experiences every day for our customers.

Therefore, focus on, and investment in, our colleagues

and the culture in which they work is a priority to ensure

that we inspire colleagues to do the best work of their

lives, empowering them to better serve our customers.

Find out more in Environmental, Social and

Governance on pages 26-43

Our brand

The Saga brand has always been exceptionally

well-known amongst people over 50. This is a key

strength in the highly competitive markets that we

operate in, as the brand is often associated with trust.

As part of our strategy, we aim to build Saga into

‘TheSuperbrand’ for older people, which will allow us

toreach a wider audience and further build on our

already distinct brand.

Find out more in our strategy on pages 22-25

Our customers and insight

At Saga, our customers are the heart of our business

and we aim to create exceptional experiences for

them every day. Through our unique customer insight,

we are able to develop a deep understanding of the

ageing experience and what is important to this unique

group so that we are able to develop products and

services that meet their wants and needs.

Supplier partnerships

Our supplier partnerships are integral to our business

model as leveraging their specialist expertise,

resources and capital allows us to deliver the best

possible products and services to our customers.

Proprietary data and technology

The size of our database, and the depth of information

we hold on our customer group, is one of Saga’s core

assets. The continual expansion and development of

this data, coupled with our unique insights, allows us to

develop products and services that are tailored

specifically for this unique group.

How we add value

• Our Saga Deluxe and Titan

VIP Travel Services provide

ease and reassurance through

home-to-airport pick-up,

airport lounge access and

fast-track security clearance

at selected UK airports.

• Customer money is

safeguarded in a trust

arrangement until they return

from their holiday, providing

further peace ofmind.

Marketplace and position

We are one of the leading travel

businesses serving people

over50 in the UK.

Key competitors

TUI, On the Beach, Trailfinders

and Kuoni

Guests travelled

47k

2021/22 – 8k

What we do

We provide our guests with a

variety of travel experiences

through hotel stays, escorted

tours and Tailor-Made holidays.

How we add value

• We offer guests a truly

all-inclusive cruising experience

which includes all meals and

drinks, a chauffeur service,

private balconies as standard

and selected excursions.

• Guests travel with the added

peace of mind through

inclusion of travel insurance

and a price promise guarantee.

Marketplace and position

We are one of the smaller cruise

businesses operating from the

UK, however, our unique oering

and value for money leaves us

well-placed within the market.

Key competitors

Royal Caribbean, Carnival, Fred

Olsen and Riviera

Guests travelled

48k

2021/22 – 23k

What we do

We provide our guests with ocean

and river cruises on board our

luxury ships.

Our distinct business units are ambitious and autonomous,

whilst leveraging our core strengths tobuild deep and

long-lasting relationships with ourcustomers.

Our strengths Our diverse business

Cruise

Travel

BUILDING ON OUR STRENGTHS

18 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Purpose and business model

How we add value

• Saga Money partners our

in-house expertise with

specialist third parties to

deliver personal finance

products that meet the needs

of our customers.

• Saga Media delivers engaging

and insightful content through

Saga Exceptional and the

Saga Magazine.

• Saga Insight specialises in

understanding the ageing

process and what it means

toget older, allowing us to

develop products and services

that our customers want.

What we do

The Group’s Other Businesses

oer personal finance products

through Saga Money and a range

of online and printed content

through Saga Media. We also

operate Saga Insight, which

specialises in generating unique

insights into ‘Generation

Experience’, and CustomerKNECT

(formerly MetroMail), our mailing

and printing business.

Saga Money customers

1

139k

2021/22 – 128k

Saga Media weekly

newsletterreach

2

0.5m

Saga is committed to maximising value

for our key stakeholders

Customers

Delivering for our customers is what drives us to

succeed. We develop tailored, dierentiated products

that allow them to live a life unlimited.

Community

Saga strives to have a positive impact on our

communities through our colleague volunteering

schemes and charitable giving.

Colleagues

So that our colleagues feel highly engaged with

Sagaand their work, we continually invest in their

development and wellbeing, creating a culture of high

performance and high support across the Group.

Shareholders and investors

Saga is committed to creating long-term value for our

investors by maximising our businesses, returning to

sustainable growth and reducing our debt.

Partners and suppliers

To provide our customers with the best products and

services possible, we partner with carefully chosen

suppliers who, in return for their expertise, experience,

or financial resources, gain access to our knowledge,

brand and deep customer insight.

Creating value

Find out more in engaging with stakeholders on

pages 20-21

Other Businesses

How we add value

• We offer customers flexibility

through a range of products

from our lower-cost standard

one-year motor policies

through to our premium

three-year fixed-price policies.

• We use a combination of our

own in-house underwriter,

AICL, anda third-party panel of

underwriters to ensure that

customers receive the

bestprice.

• We aim to acquire as many

customers as possible

directly, reducing the cost

ofacquisition.

Marketplace and position

We are the UK’s specialist in

insurance products for people

over 50 in the UK.

Key competitors

Admiral, Direct Line, Hastings,

LV,RSA and Aviva

Total policies in force

1.7m

2021/22 – 1.7m

What we do

We provide our customers with

tailored insurance products,

principally motor, home, private

medical and travel insurance.

Insurance

1 2021/22 Saga Money customers have been restated from those published in the 2022 Annual

Report and Accounts to align with current reporting methodology

2 No comparable data exists for 2021/22 as the weekly newsletter was introduced in May 2022

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 19

Our customers continue to be the heart

of our brand. Our success relies on

engaging new customers and building

and maintaining the loyalty of our

existingcustomers.

What matters to them

• Value for money products and

services that are designed

specifically for their needs.

• Exceptional customer service in

every interaction with Saga.

• Clear and informative communication

in the format that best suits them.

How we engage

Our ambition is to increase the

frequency of engagement with our

customers from once a year to daily. In

addition to our existing telephone and

email support, social media interactions,

publication of Saga Magazine and

utilisation of our customer panel, we also

launched a brand-new website, Saga

Exceptional, which was created to

provide a dedicated space online for

people over 50.

How the Board is kept informed

The Board receives regular reports

from management based on customer

insights and feedback, and reviews

NPSscores as part of a range of

customer scorecards from each of our

business units which are presented at

each meeting.

Customer-facing colleagues are also

invited to Board meetings to present

details of customer experiences.

Customer NPS

51

In order for us to deliver exceptional

experiences every day for our

customers, we depend on the support

ofour partners and suppliers. Our

ambition is to develop long-term,

mutually beneficial relationships with

allour key suppliers.

What matters to them

• Reliable relationships that

supportthe delivery of their

ownstrategic objectives.

• Regular and open communication.

• Innovation that encourages

simplification and efficiency

wherepracticable.

How we engage

Our relationships with our supply

chainare governed by our supplier

relationship management and supplier

risk management policies, which provide

a framework for our operations. This

ensures that communication with our

partners and suppliers is regular and

consistent, allowing us to continually

develop the way we work together.

Ourindividual business units are

responsible for management and

control of these relationships.

How the Board is kept informed

The Risk Committee is kept informed

ofany changes to supplier risk

management through the Executive

Leadership Team Committee.

Customers

Partners and

suppliers

Our colleagues will always be an integral

part of the business and so creating an

inclusive and supportive culture that

allows them to reach their full potential

iscrucial.

What matters to them

• A culture where they feel not only

accepted but understood and

valued for the characteristics

thatmake them individual.

• Regular, honest and open

communication that encourages

them to speak up and know

they’llbe heard.

• Receiving fair reward

andrecognition.

How we engage

We strive to maintain active two-way

communication with our colleagues

through a variety of channels including

our internal communications platform,

Workplace, quarterly engagement

surveys, regular one-to-one meetings

with line managers, collaborative team

events, Tell Euan About sessions and

through our People Committee.

Find out more in Environmental,

Social and Governance on

pages26-43

How the Board is kept informed

Our nominated ‘People Champion’

isEvaEisenschimmel, one of our

Non-Executive Directors who regularly

attends our People Committee

meetings. The Board are also kept

informed through regular updates from

our Chief People Ocer (CPO) on

colleague engagement, feedback from

our colleague engagement survey and

progress against our colleague strategy.

Colleague engagement

8.0

out of 10

Colleagues

20 Saga plc Annual Report and Accounts 2023

STRATEGIC REPORT

Engaging with stakeholders

CREATING STAKEHOLDER VALUE

Our regulators set the framework in

which we operate, and it is therefore

crucial that we maintain strong

relationships with them.

What matters to them

• Proactive and transparent

communication.

• Protection of our customers

andthe markets we operate in.

• Increasing the trust of the

publicand encouraging

marketcompetition.

How we engage

Regulator relationships are maintained

at subsidiary level and monitored by

therespective audit, risk and

compliance committees.

How the Board is kept informed

The Risk Committee escalates any

matters of strategic or reputational

importance to the Board. The chairs of

our regulated businesses, Saga Personal

Finance (SPF) Limited, Saga Services

Limited (SSL)and AICL, are also plc

Directors and report on our

relationships with regulators.

Find out more in our Risk Committee

Report on pages 90-91

We are focused on creating a business

which delivers long-term sustainable

value to our shareholders. We aim to

treat all shareholders fairly, providing

them with opportunities to express

theirviews.

What matters to them

• Active engagement with the

GroupCEO, Group CFO and

Investor Relations (IR) team.

• Regular updates on the Group’s

financial performance and progress

against our strategy.

How we engage

We have frequent communication

withour shareholders and investors

through results announcements, press

releases, updates to our corporate and

shareholder websites, group events,

one-on-one meetings and ad hoc

telephone and email interaction.

How the Board is kept informed

The agenda for each Board meeting

includes review of an IR report that

provides an update on investor

engagement and feedback received.

Our Non-Executive Chairman, Group

CEO, and Group CFO meet with

investors on a regular basis, assisted

byour Head of IR. Additionally, the

chairof our Remuneration Committee

interacts with shareholders throughout

the year and relays any feedback to the

Board. Our Annual General Meeting,

Capital Markets Events and results

presentations also provide the

opportunity for in-person interaction

with investors.

Part of our purpose is to drive positive

change in our markets and communities

so we therefore aim to understand and

carefully consider the impact of every

decision we make.

What matters to them

• Maintaining clear and open

communication with us to ensure

that they are aware of our strategy

and plans, as well as any impact it

may have on them.

• The chance to share what matters

to them and how we may be able

tosupport.

• Opportunity to share knowledge

and skills between our colleagues

and the wider community.

How we engage

Our Group CEO, alongside specific

members of the wider Saga team, host

two meetings a year with community

stakeholders which include a business

update and the opportunity to ask

questions and engage with us on

keytopics.

In addition, our colleagues are each

provided with one paid volunteering

dayper year, allowing them to give back

to our communities.

How the Board is kept informed

Our Group CEO attends each meeting,

enabling him to directly feed back to

theBoard.

Colleague volunteering time

1,078

days

Communities

Shareholders

andinvestors

Regulators

Strategic report Financial statements Additional informationGovernance

Saga plc Annual Report and Accounts 2023 21

Challenges

• Impact of COVID-19 pandemic posing

restrictions on the industry, alongside

increased consumer caution.

• Geopolitical factors requiring

amendments to itineraries and some

limited guest cancellations.

• Potential for the cost of living crisis to

impact levels of discretionary spending

oncruises.

• Regulatory, financial and physical impacts

associated with climate change.

Progress in 2022/23

• Appointment of Ian Simkins, who brings a

wealth of experience from the luxury travel

market, to chair the Cruise board.

• Uninterrupted sailing with the last of the

COVID-19 restrictions lifted during

summer 2022.

• Ocean Cruise load factor of 75% for the

full year and 84% for the second half.

• Awarded ‘Best Value For Money Cruise

Line’ at the 2022 Wave Awards.