Contents

Introduction .............................................................................................................................1

Yield Restriction and Rebate Requirements .........................................................................2

Part I

Basic Concepts and Definitions that Apply for the Arbitrage Requirements ....................4

Part II

Yield Restriction Requirements and Exceptions...................................................................7

Part III

Rebate Requirements and Exceptions ................................................................................11

Part IV

Rebate Amounts and Payments...........................................................................................16

Part V

Accounting for Expenditures and Allocations.....................................................................18

Part VI

Example of Calculation of Rebate Amount and Yield Restriction Analysis ......................19

Part VII

Information and Services......................................................................................................25

Introduction

This publication is a basic guide to the yield restriction and rebate requirements (arbitrage

requirements) of Internal Revenue Code (IRC) Section 148 and related Treasury Regulations

(Treas. Reg.).

1

Understanding the arbitrage requirements can help issuers and conduit borrowers

comply with their obligations and prevent violations of the arbitrage requirements. The IRS

provides information on specific provisions of tax-exempt bond law in IRS publications and on

IRS.gov/bonds. Additional resources are listed at the end of this publication.

This publication has seven parts.

Part I provides basic concepts and denitions that apply to the arbitrage requirements.

Parts II and III describe the yield restriction and arbitrage rebate requirements, and detail the

exceptions to those requirements.

Part IV provides information on how and when an issuer computes rebate amounts and pays

rebate to the U.S. Treasury.

Part V provides information on accounting for expenditures and allocations.

Part VI presents a basic example of rebate amount and yield reduction payment calculations.

Part VII provides additional information on available resources, services and programs to

facilitate compliance with the arbitrage requirements.

The publication is not formal guidance and is not intended as an authoritative source. It

outlines the general arbitrage rules. It does not address all questions or issues that may arise in

complying with the arbitrage requirements, including, for example, special rules that may apply

to bond pools, direct pay bonds, tax credit bonds and certain private activity bonds other than

qualified 501(c)(3) bonds. This document does not provide details on how to apply the arbitrage

requirements to computations. Issuers should review IRC Sections 103 and 148, the related

Treas. Reg. and other official guidance on complying with the arbitrage requirements, and

consult their legal counsel in appropriate circumstances.

This publication does not address other federal tax requirements that must be met for

bonds to be tax-exempt, including those that apply before the bonds are issued and after

issuance. Publication 4078, Tax-Exempt Private Activity Bonds, Publication 4079, Tax-Exempt

Governmental Bonds, and Publication 4077, Tax-Exempt Bonds for 501(c)(3) Charitable

Organizations, provide overviews of federal tax rules that apply post-issuance to tax-exempt

private activity bonds, governmental bonds and qualified 501(c)(3) bonds, respectively. Not

meeting the federal tax law requirements during the life of tax-exempt bonds may jeopardize

their tax-exempt status.

1

Although conduit issuers may require conduit borrowers to contractually assume responsibility for complying with requirements of the

IRC, failure of a bond issue to comply with the requirements may result in the loss of the tax-exempt status of the bonds regardless of

any agreement between the parties about compliance responsibilities. Publication 5005, Your Responsibilities as a Conduit Issuer of

Tax-Exempt Bonds, includes information for issuers of conduit bonds.

1

Yield Restriction and Rebate Requirements

State and local governments receive benefits under the IRC that typically lower borrowing costs

on their valid tax-exempt debt obligations. For example, because interest paid to bondholders on

tax-exempt obligations is not includable in their gross income for federal income tax purposes,

bondholders are willing to accept a lower interest rate than they would if the interest were

taxable. These benefits apply to many types of municipal debt financing arrangements including

bonds, notes, loans, lease purchase contracts, lines of credit and commercial paper (collectively

referred to as “bonds” in this publication). To receive these benefits, issuers must ensure

that they meet IRC and Treas. Reg. requirements, generally for as long as the bonds remain

outstanding. This means that it’s important that issuers and any users of the bond proceeds

regularly monitor how the bond proceeds are being used to ensure continued compliance.

Some of the requirements relate to how bond proceeds are invested. Generally, bonds lose their

tax-exempt status if they are arbitrage bonds under IRC Section 148. To be an arbitrage bond,

certain monies associated with the bonds are used to acquire investments with a yield above

the bond yield. When the investment yield is higher than the bond yield, the excess is called

“arbitrage earnings.” But having arbitrage earnings does not automatically mean that the bonds

are arbitrage bonds. Bonds must be tested under two independent sets of arbitrage rules to

determine if they are arbitrage bonds. If the bonds are arbitrage bonds under either set of rules,

they are arbitrage bonds even if they are not arbitrage bonds under the other set.

The two sets of rules that apply to determine whether bonds are arbitrage bonds are:

The yield restriction rules under IRC Section 148(a), and

The rebate rules under IRC Section 148(f).

Yield Restriction Rules - The yield restriction rules limit the investment yield that may be

earned on bond proceeds. Bonds are arbitrage bonds if the issuer expects to invest or actually

does invest all or part of the bond proceeds at a yield materially higher than the bond yield.

Issuers are permitted to invest in higher yielding investments under certain exceptions. But if

no exception applies, the issuer must limit the yield on its investment of bond proceeds to a

yield that is not materially higher than the yield on the bonds (yield restrict the investments) or,

if permitted, make a yield reduction payment to the U.S. Treasury to prevent its bonds from

violating the yield restriction rules. Part II of this publication will describe and list:

1) Which monies are bond proceeds that must be yield restricted,

2) Which investments must be yield restricted,

3) What is a materially higher yield on an investment,

4) When the issuer may reduce the yield on the investment by making “yield reduction

payments” to the U.S. Treasury, and

5) Exceptions to the yield restriction rules.

Rebate Rules - The arbitrage rebate rules provide that certain arbitrage earnings must be

paid, or “rebated,” to the U.S. Treasury. This means that even if an issuer is permitted to invest

in higher yielding investments under the yield restriction rules, it may have to rebate those

arbitrage earnings to the U.S. Treasury. The yield restriction rules may allow the issuer to earn

the arbitrage, but the rebate rules may not allow the issuer to keep the arbitrage. If an issuer is

required to pay rebate under these rules, but does not, the bonds are “arbitrage bonds.” The

rebate rules include exceptions. Part III of this publication will describe and list:

2

1) Which monies are proceeds subject to rebate,

2) Which investments are subject to rebate,

3) Certain rules for computing and paying rebate, and

4) Exceptions to the rebate rules.

3

Part I

Basic Concepts and Definitions that Apply for the Arbitrage Requirements

Before exploring the yield restriction and rebate rules, we’ll explain some basic concepts that

apply for the arbitrage requirements.

Definitions

Gross Proceeds - Gross proceeds of a bond issue include proceeds and replacement

proceeds.

Proceeds

2

include sale proceeds, investment proceeds and transferred proceeds.

Sale proceeds are amounts the issuer receives from the sale of the bond issue, including

amounts used to pay underwriters’ discount and certain accrued interest on the bonds.

Investment proceeds are amounts received from investing proceeds of an issue. For

example, if the issuer invests sale proceeds and earns interest, that interest is considered

investment proceeds.

Transferred proceeds may result when an issuer issues tax-exempt bonds (the refunding

bonds) to refund an outstanding issue of tax-exempt bonds (the refunded bonds). Unspent

proceeds of the refunded bonds may transfer to and become proceeds of the refunding

bonds, and are no longer considered proceeds of the refunded bonds.

Replacement proceeds

3

are monies that would have been used to finance the project if

the bonds had not been issued. Replacement proceeds may also include amounts expected

to pay debt service on the bonds, including sinking funds (such as a debt service fund,

redemption fund, reserve fund or a replacement fund) and pledged funds (generally meaning

any amount pledged to pay principal of or interest on the bonds).

Investment Property

4

includes any security (for example, a share of stock in a corporation), any

obligation (for example, debt obligations such as U.S. Treasury obligations and agency bonds),

any annuity contract and any other kind of investment-type property (for example, guaranteed

investment contracts). Cash is not investment property. For issues of governmental and

qualified 501(c)(3) bonds, investments in other tax-exempt governmental bonds and tax-exempt

qualified 501(c)(3) bonds (bonds not subject to the Alternative Minimum Tax) are not investment

property under IRC Section 148(b)(3). For issues of other types of bonds, no tax-exempt bond

is investment property. Consequently, investments in these tax-exempt bonds are not subject

to the arbitrage requirements, and earnings received from these bonds are not subject to the

yield restriction or rebate requirements.

5

Investment property can be a purpose or nonpurpose

investment.

6

A purpose investment is one acquired for the governmental purpose of an issue. For

example, if an issuer issued bonds to make a loan to a 501(c)(3) organization or to fund

student loans, the loans the issuer makes to the 501(c)(3) or students are investments but

because the bonds were issued for this purpose, these loans are “purpose investments.”

2

Treas. Reg. Section 1.148-1(b).

3

Treas. Reg. Section 1.148-1(c).

4

IRC Section 148(b)(2).

5

Treas. Reg. Section 1.148-2(d)(2)(v). Generally, investments in bonds subject to the Alternative Minimum Tax (AMT bonds) made

with non-AMT bond proceeds are subject to yield restriction, but investment in AMT bonds made with AMT bond proceeds are not.

Similarly, investments in non-AMT bonds made with non-AMT bond proceeds are not subject to yield restriction. See IRC Section

148(b)(3).

6

Treas. Reg. Section 1.148-1(b).

4

A nonpurpose investment is an investment that is not a purpose investment. For example,

if the issuer sells bonds to build a school but invests some of those proceeds while

construction is ongoing, the investments are not acquired for the governmental purpose of

the issue (construction of the school) so they are nonpurpose investments. Examples of a

nonpurpose investment include buying U.S. Treasury notes during the construction period

as a temporary investment until the funds are spent on the project, or buying federal agency

bonds to hold in a debt service reserve fund.

Funds and Accounts Descriptions - Issuers and conduit borrowers create funds and accounts

in connection with a bond issue in which bond proceeds are deposited. Below is a description

of certain funds and accounts commonly used in tax-exempt bond financings and the typical

use of proceeds deposited in each type of fund or account. Frequently, there will be more than

one type of fund for a bond issue, and for each type, there may be more than one account.

For example, there could be several construction accounts for separate projects within a

construction fund.

Construction fund or project fund - An issuer or conduit borrower might establish a

construction or project fund into which it will deposit bond proceeds to be used to pay costs

of the project. This fund might also include proceeds to pay capitalized interest and costs of

issuing the bonds (or proceeds for these costs may be held in separate funds or accounts).

Debt service fund and bona fide debt service fund - An issuer or conduit borrower might

establish a debt service fund to hold revenues or other monies to pay upcoming debt service

payments on the bonds. A bona fide debt service fund is used for proper matching of annual

revenues and debt service. Revenues are deposited into the fund until needed to pay debt

service. The fund generally must be depleted at least once each bond year to qualify as a

bona fide debt service fund.

7

Reserve fund and reasonably required reserve or replacement fund - Reserve funds

secure payment of debt service on the bonds in the event the issuer is unable to pay debt

service. A reasonably required reserve or replacement fund is a fund in which gross proceeds

do not exceed the lesser of:

10% of the principal amount of the issue,

Maximum annual debt service on the bonds, or

125% of the average annual debt service on the bonds.

8

Refunding escrow fund - An issuer might establish a refunding escrow fund to hold monies

to be used to pay principal, interest and premium, if any, on one or more prior bond issues

(the refunded bonds). These funds might contain proceeds of a refunding issue and possibly

other amounts, such as tax receipts or other revenues pledged to pay off the refunded bonds.

A refunding escrow may be associated with a current refunding or an advance refunding bond

issue.

A current refunding bond refunds bonds that are redeemed within 90 days of the

refunding bonds being issued.

9

7

Treas. Reg. Section 1.148-1(b). Generally, “bond year” means each one-year period that ends on the day selected by the issuer. The

requirements for depletion appear in the definition of “bona fide debt service fund.”

8

Treas. Reg. Section 1.148-2(f)(2)(ii). For a refunding issue, a reserve is reasonably required for purposes of this exception only if the

aggregate amount invested in higher yielding investments for both the refunding issue and the refunded issue does not exceed these

limits by reference only to the refunding issue (whether or not the proceeds of the refunded issue have become transferred proceeds).

Treas. Reg. Section 1.148-9(e).

9

Treas. Reg. Section 1.150-1(d)(3).

5

An advance refunding bond refunds bonds that are redeemed more than 90 days after

the refunding bonds are issued.

10

Cost of issuance fund - An issuer or conduit borrower might establish a cost of issuance

fund to deposit bond proceeds to be used to pay various costs of issuing bonds. These

costs include, but are not limited to, payment for the services of bond counsel, underwriter’s

counsel, financial advisor, verification agent, rating agencies and fees for printing offering

documents.

10

The Tax Cuts and Jobs Act (Public Law No. 115-97, 131 Stat. 2054 (2017)) repealed the exclusion from gross income for interest on

bonds issued to advance refund another bond. The repeal applies to advance refunding bonds issued after December 31, 2017. A bond

is classified as an advance refunding if it is issued more than 90 days before the redemption of the refunded bonds.

6

Part II

Yield Restriction Requirements and Exceptions

The yield restriction rules provide that bonds are arbitrage bonds if the issuer expects to

invest or actually invests all or part of the gross proceeds in investment property having a yield

materially higher than the bond yield. The yield restriction rules apply both to purpose and

nonpurpose investments. The yield restriction rules provide special treatment when proceeds are

used for:

Certain general uses of the bonds, for example, construction or refunding purposes (some of

which may have special exceptions);

Certain types of investments depending on how the invested funds are intended to be used,

for example, a construction or escrow fund may be subject to different denitions of materially

higher yield; and

Certain classes of investments (yield is computed separately for purpose and nonpurpose

investments).

To follow the yield restriction requirements, the issuer or conduit borrower must correctly treat all

investments based on the general uses of the bonds and the type and class of the investment.

Materially Higher Yield

The yield restriction rules limit investment yield on gross proceeds. Gross proceeds invested

at a yield materially higher than the bond yield will result in the bonds being arbitrage bonds.

11

Generally, an investment yield is materially higher if it exceeds the bond yield by more than 1/8

of 1%;

12

however, the definition of materially higher can differ depending on the type and class of

investment and the general uses of the bonds.

13

Cases in which a different definition of

“materially higher” applies

Investment yield is materially higher if it

exceeds the bond yield by more than

Proceeds held in an advance refunding escrow 1/1000 of 1%

14

Replacement proceeds 1/1000 of 1%

15

For example, if a fixed-yield bond issue has a yield of 5%, the investment yield on an advance

refunding escrow or on replacement proceeds is not materially higher if the yield of the

investments is not greater than 5.001%.

Yield Reduction Payments

In certain cases, an issuer can make a payment to the U.S. Treasury to reduce the yield on

an investment (a yield reduction payment). In this case, an issuer may invest proceeds at

a materially higher yield, but by paying the yield reduction payment, the issuer causes the

investment yield to be treated within the permitted yield. Yield reduction payments may only

be made for certain types of investments and certain types of proceeds.

16

Generally, a yield

reduction payment is made at the same time and in the same manner as a rebate payment by

11

IRC Section 148(a) and Treas. Reg. Section1.148-2(a).

12

Treas. Reg. Section1.148-2(d)(2)(i).

13

Treas. Reg. Section 1.148-2(d)(1). If yield-restricted investments in the same class are subject to different definitions of materially

higher, the definition of materially higher that produces the lowest permitted yield applies to all the investments in the class.

14

Treas. Reg. Section 1.148-2(d)(2)(ii).

15

Treas. Reg. Section 1.148-2(d)(2)(ii).

16

Treas. Reg. Section 1.148-5(c)(3).

7

filing Form 8038-T, Arbitrage Rebate, Yield Reduction and Penalty in Lieu of Arbitrage Rebate,

with the IRS.

17

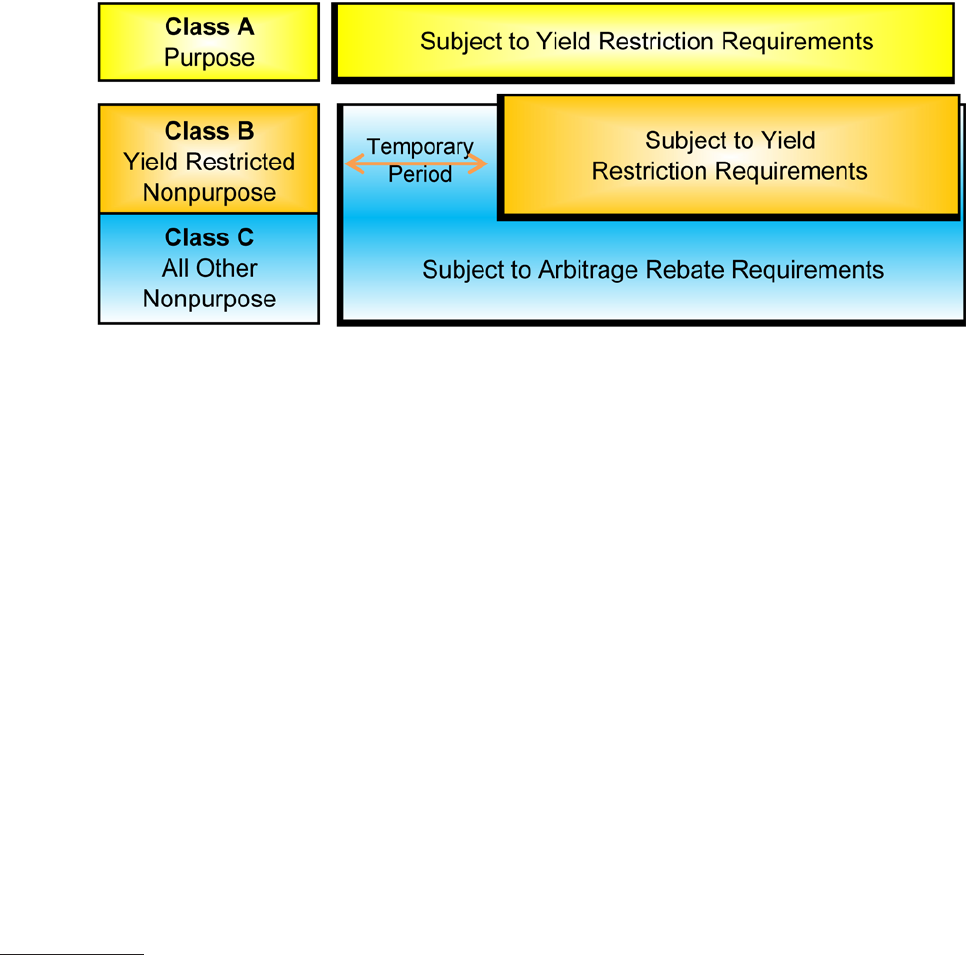

Yield Computation Done for Entire Class of Investments

In figuring whether investments acquired with gross proceeds have a materially higher yield,

combine similar investments into three classes

18

and compute the yield for each class. Class

A includes all purpose investments that are subject to certain yield restriction limits. Class B

includes the nonpurpose investments subject to yield restriction after the temporary period.

Class C consists of all other nonpurpose investments.

Illustration of classes of investments and their arbitrage requirements

Note that nonpurpose investments not subject to yield restriction are subject to the rebate

requirements. This means that during the temporary period Class B investments are subject to

rebate requirements, even though they aren’t subject to yield restriction requirements until a later

date. In this illustration, the Class B investments could be a construction fund while the Class C

investments could be a reasonably required reserve fund.

Exceptions to Yield Restriction Rules

The exceptions to the yield restriction requirement are for gross proceeds:

Held during “temporary periods,”

19

Held in a “reasonably required reserve or replacement fund,”

20

or

Representing a “minor portion.”

21

Remember, if an exception applies, the issuer may invest the bond proceeds covered by

the exception at an unrestricted yield, but those proceeds might be subject to the rebate

requirements. For example, bond proceeds deposited in a reasonably required reserve or

replacement fund are subject to rebate requirements even though an issuer can invest those

proceeds at an unrestricted yield under a specific exception to the yield restriction requirements.

This is an example of how an issuer may earn arbitrage, but may not keep it.

17

Treas. Reg. Section 1.148-5(c)(2).

18

Treas. Reg. Section 1.148-5(b)(2)(ii).

19

IRC Section 148(c).

20

IRC Section 148(d).

21

IRC Section 148(e).

8

Temporary Period Exceptions - Exceptions Subject to a Time Limit

During a “temporary period,” the issuer may invest bond proceeds at an unrestricted yield

without causing the bonds to be arbitrage bonds under the yield restriction rules. The length of

the “temporary period” depends on the purpose (use) for which the bonds are issued and the

type of investment (or fund) that holds the proceeds.

3-Year Temporary Period for Capital Projects

A 3-year temporary period is available for bond proceeds deposited in a construction or project

fund when those proceeds are expected to be allocated to acquisition or construction costs of

a capital project.

22

The temporary period begins on the date the bonds are issued and ends 3

years later. The 3-year temporary period may be extended another 2 years for a total of 5 years

if the issuer and a licensed architect or engineer certify that more than 3 years are necessary

to complete the capital project. This fund is made up of the net sale proceeds

23

and investment

proceeds.

The 3-year temporary period applies as long as the issuer reasonably expects as of the issue

date to:

Allocate at least 85% of the bond’s net sale proceeds for expenditures on the capital project

within three years of the bond’s issue date,

Have a binding obligation to a third party within six months of the bond’s issue date to allocate

at least 5% of the net sale proceeds to expenditures for the capital project, and

Proceed toward completing the project and allocating the net sale proceeds to expenditures

with due diligence.

24

Other Temporary Periods

Other temporary period exceptions to the yield restriction requirements include:

1) 13-month temporary period exceptions for bona fide debt service funds and working capital

expenditures.

25

The 13-month temporary period may be extended to the maturity date for

issues that are tax and revenue anticipation notes (TRANs)

26

if certain requirements are met.

2) 1-year temporary period for investment proceeds.

27

3) 90-day temporary period for certain current refundings. The temporary period for current

refunding proceeds, other than transferred proceeds, is generally 90 days.

28

4) 30-day temporary periods for replacement proceeds, advance refunding proceeds and other

proceeds. Replacement proceeds qualify for a 30-day temporary period. The temporary

period for proceeds (other than transferred proceeds) of an advance refunding issue is

generally 30 days.

29

Gross proceeds not qualifying for any other special temporary period

exception qualify for a 30-day temporary period exception from date of receipt.

30

22

See Part V for a discussion of what it means to allocate to expenditures.

23

“Net sale proceeds” of a bond issue are the sale proceeds reduced by those sale proceeds deposited in a “reasonably required

reserve or replacement fund” and proceeds invested as part of a “minor portion.” Treas. Reg. Section 1.148-1(b).

24

Treas. Reg. Section 1.148-2(e)(2).

25

Treas. Reg. Section 1.148-2(e)(5)(ii) and Treas. Reg. Section 1.148-2(e)(3)(i).

26

Treas. Reg. Section 1.148-2(e)(3)(ii).

27

Treas. Reg. Section 1.148-2(e)(6).

28

Treas. Reg. Section 1.148-9(d)(2)(ii)(A) and (B).

29

Treas. Reg. Section 1.148-9(d)(2)(i). This 30-day temporary period ends 30 days after the date the advance refunding bonds are

issued.

30

Treas. Reg. Section 1.148-2(e)(7).

9

Start of Temporary Period

Most temporary periods begin on the bond’s issue date. Other temporary periods begin after the

issue date, such as when proceeds are received or earned (for example, investment earnings),

allocated to the bonds (for example, replacement proceeds deposited in a sinking fund) or first

treated as replacement proceeds.

31

Certain temporary periods for repayments of loans made

with proceeds begin on the date of the repayment.

Temporary Periods and Refunding Bonds

For proceeds that are transferred proceeds of a refunding issue, the temporary period generally

begins on the date of transfer of the proceeds and ends when it would have otherwise ended

if the proceeds had remained proceeds of the refunded bonds.

32

However, in an advance

refunding, for example, the 3 or 5-year temporary period for capital projects or the 13-month

temporary period for working capital for the proceeds of the prior issue ends on the issue date

of the advance refunding issue.

33

Yield Restriction Exceptions Having No Time Limit

The following exceptions to the yield restriction rules apply throughout the life of the bond issue.

If one of these exceptions applies, the yield restriction limitations do not apply to the proceeds

or funds described in the exception.

1) Reasonably required reserve or replacement fund.

34

2) Minor portion exception - This exception applies to proceeds in an amount which is the lesser

of $100,000 or 5% of the sale proceeds of the issue.

35

31

Treas. Reg. Section 1.148-2(e)(5).

32

Treas. Reg. Section 1.148-9(d)(2)(iii)(A).

33

Treas. Reg. Section 1.148-9(d)(2)(iii)(B).

34

Treas. Reg. Section 1.148-2(f)(2)(i).

35

Treas. Reg. Section 1.148-2(g).

10

Part III

Rebate Requirements and Exceptions

Under IRC Section 148(f), bonds are arbitrage bonds if an issuer does not make rebate

payments to the U.S. Treasury in the amounts and at the times required. The issuer must rebate

the amount by which the yield on investment property acquired with proceeds of the issue

exceeds the yield on the bonds. The rebate requirements apply only to nonpurpose investments.

Purpose investments are not subject to the rebate rules.

The rebate rules generally provide that issuers must periodically calculate arbitrage earnings

and, unless an exception applies, pay those earnings to the U.S. Treasury within 60 days after

the computation date for the period. While issuers have flexibility in determining the computation

periods, an issuer must compute and pay any required rebate at least once every five years.

Payments must be made by filing Form 8038-T, Arbitrage Rebate, Yield Reduction and Penalty

in Lieu of Arbitrage Rebate. Parts IV and VI include more information about the rebate calculation

and examples of this calculation.

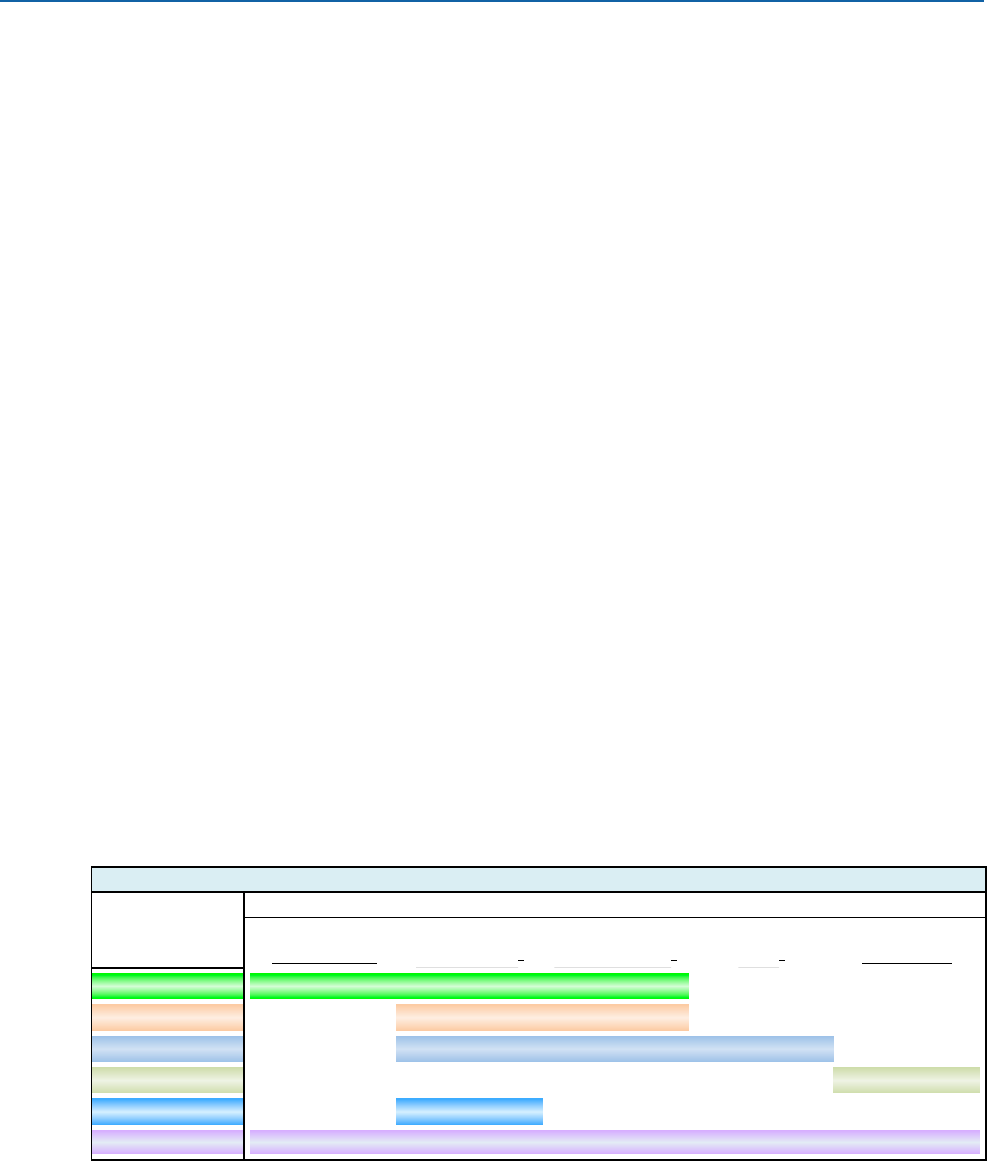

Exceptions to the Rebate Requirements

Exceptions to the rebate requirements may apply based on how quickly the issuer spends the

bond proceeds, the size of the issuer and the category of proceeds being invested. Some of

these exceptions apply only to certain types of bonds (for example, governmental bonds) and

some of these exceptions apply only to proceeds in certain funds. For exceptions applying

to specific types of funds, the issuer’s allocation of proceeds to these funds is important to

determine whether a particular exception’s requirements are met. The purposes and uses of the

proceeds in a fund and the purpose of the bond issue control whether an exception applies,

regardless of the label of the fund.

The two general exception categories to the rebate requirements are the spending exceptions

and the special exceptions.

The following chart illustrates certain funds and exceptions that may be available for proceeds

held in those funds.

Generic Types of Accounts (Funds) and Available Exceptions to Rebate

Exceptions

Type of Fund Containing Bond Proceeds

Refunding Construction or Costs of Reserve Debt Service

Escrow Fund

Project Fund

a

Issuance Fund

b

Fund

c

Fund (DSF)

Limited

6-Month

18-Month

2-Year

Bona Fide DSF

Working Capital

Small Issuer

a

Or Working Capital Fund

b

Proceeds used for issuance costs are eligible for the 2-year spending exception if they meet the

requirements under Treas. Reg. Section 1.148-7(i)(4).

c

A reasonably required reserve or replacement fund can only be excluded from the rebate requirement under

the two-year spending exception through the earlier of the close of the two year period or the date the

construction is substantially completed under IRC Section 148(f)(4)(C)(vi)(II).

11

Spending Exceptions

The three spending exceptions are the:

6-month spending exception,

18-month spending exception, and

2-year spending exception.

If an issuer satisfies a spending exception, proceeds in the eligible funds will be exempt from the

rebate requirements.

The spending exceptions depend on an issuer allocating certain proceeds to expenditures within

specified time periods. To determine whether these exceptions apply, it is necessary to identify:

Which proceeds the issuer allocated to expenditures, and

When the issuer allocated those proceeds.

Part V provides information on accounting for expenditures and allocations.

6-Month Spending Exception

If the requirements of the 6-month spending exception are met, the issue is treated as satisfying

the rebate requirements for the proceeds meeting that exception. This means that earnings on

investments of certain gross proceeds of the issue that exceed the yield on the issue don’t need

to be paid as rebate to the U.S. Treasury. Generally, the issuer must meet both the following

requirements:

1) The issuer must allocate the gross proceeds to expenditures for the governmental purposes

of the issue within the 6-month period beginning on the issue date. For this purpose, gross

proceeds do not include gross proceeds:

a) Held in a bona fide debt service fund or a reasonably required reserve or replacement

fund,

b) Not previously anticipated to become gross proceeds but that become gross proceeds

after the end of the 6-month spending period,

c) That are proceeds derived from any purpose investment of the issue, and

d) That are repayments of certain grants financed by the issue.

If the issue is a governmental bond issue other than TRANs or if the issue is qualified

501(c)(3) bonds, the 6-month time period is extended to one year for a limited amount of

gross proceeds.

2) The issuer meets the rebate requirements for the issue’s proceeds (excluding earnings on

amounts in any bona fide debt service fund) not covered by the 6-month exception.

When an issuer satisfies the requirements for the 6-month spending exception, it may retain

earnings on only the gross proceeds specifically described by the exception. The 6-month

spending exception does not create an exception for amounts in a reasonably required reserve

or replacement fund or for unanticipated gross proceeds that appear after the 6-month period.

TRANs are treated as meeting the 6-month spending exception for the issue’s net proceeds

36

and any investment earnings on those net proceeds if the issuer meets certain IRC

requirements.

37

36

IRC Section 150(a)(3).

37

IRC Section 148(f)(4)(B)(iii).

12

18-Month Spending Exception

An issuer satisfying the requirements of the 18-month spending exception may retain certain

investment earnings during that 18-month period starting on the issue date. The three

requirements are:

1) The issuer must allocate gross proceeds to expenditures for a governmental purpose of the

bonds under the following schedule, with the periods starting on the issue date of the bonds:

a) At least 15% of the proceeds are allocated within 6 months,

b) At least 60% within 12 months, and

c) 100% within 18 months.

The spending requirement for the third period allows for a limited amount of unspent

proceeds in connection with reasonable retainage

38

(retention to ensure compliance with

a construction contract), if the reasonable retainage is allocated to expenditures within 30

months of the issue date. An issuer’s failure to meet the spending requirements will be

disregarded if the issuer exercised due diligence to complete the financed project and the

amount of the proceeds that didn’t meet the schedule doesn’t exceed the lesser of 3% of the

bond’s issue price or $250,000.

39

As with the 6-month spending exception, gross proceeds

has a special definition for applying the spending schedule.

40

2) The issuer must meet the rebate requirement for all proceeds not required to be spent within

the 18-month spending period (excluding earnings on a bona fide debt service fund).

3) All the bond’s gross proceeds, as defined for the 18-month spending exception, must also

qualify for the 3-year temporary period available under the yield restriction requirements.

As is the case for the 6-month spending exception, the 18-month spending exception does not

create an exception for amounts in a reasonably required reserve or replacement fund. The

18-month spending exception also doesn’t apply to a bond issue any portion of which is treated

as meeting the rebate requirement under the 2-year construction spending exception.

41

2-Year Spending Exception

The 2-year spending exception applies only to non-refunding construction issues that finance

property owned by a governmental unit or a 501(c)(3) organization. To qualify as a construction

issue, the issuer must reasonably expect, as of the issue date, that at least 75% of the “available

construction proceeds”

42

of the issue will be allocated to construction expenditures.

43

If the

issue meets the requirements of the 2-year construction spending exception, then the issue is

treated as meeting the rebate requirements for available construction proceeds—with the result

that arbitrage earnings on investments of those proceeds are not required to be paid to the U.S.

Treasury.

38

Treas. Reg. Section 1.148-7(d)(2) and Treas. Reg. Section 1.148-7(h).

39

Treas. Reg. Section1.148-7(b)(4).

40

Treas. Reg. Section1.148-7(d)(3)(i).

41

Treas. Reg. Section 1.148-7(d)(4).

42

The term “available construction proceeds” is defined in IRC Section 148(f)(4)(C)(vi) and Treas. Reg. Section 1.148-7(i).

43

Treas. Reg. Section 1.148-7(g).

13

Generally, an issuer meets the requirements of the 2-year spending exception if it allocates

available construction proceeds to expenditures for governmental purposes of the issue

according to the following schedule (with periods starting on the issue date):

1) At least 10% of the proceeds are allocated within 6 months,

2) At least 45% within 1 year,

3) At least 75% within 18 months, and

4) 100% within 2 years.

The spending requirement for this fourth and final period allows limited unspent proceeds for

reasonable retainage

44

(retention to ensure compliance with a construction contract), if the

reasonable retainage is allocated to expenditures within 3 years of the issue date. If the issuer

doesn’t meet the requirements of the final spending period, there is an exception if:

1) The unspent proceeds do not exceed the lesser of 3% of the issue price or $250,000, and

2) The issuer exercises due diligence to complete the project.

45

An issuer of a construction issue may elect by the issue date to pay a “penalty in lieu of rebate”

under the 2-year construction spending exception.

46

Special Exceptions

Two additional exceptions to the rebate requirement are the small issuer exception for

governmental bonds and the bona fide debt service fund exception.

Small Issuer Exception

A governmental unit that does not expect to issue more than $5 million of tax-exempt

governmental bonds in a calendar year might be eligible for an exception from the rebate

requirements for proceeds of a governmental bond issue issued during that calendar year.

47

The limit is increased to $15 million for bonds issued to finance construction of public school

facilities.

48

To determine the amount of bonds that will be issued, the issuer must include certain

additional tax-exempt governmental bonds issued by any:

Entity (other than political subdivisions) that issues bonds on behalf of the issuer; and

Subordinate entity (for example, an entity that is directly or indirectly controlled by the issuer,

per Treas. Reg. Section 1.150-1(e)).

The issuer must also include any bonds issued by an entity formed or otherwise used to avoid

the amount limitation.

49

An issuer may exclude certain refunding bonds when computing the

limit.

50

In addition to the limit on the amount of governmental bonds that an issuer expects to issue, an

issue must meet these requirements to qualify for the small issuer exception:

1) The issue is issued by a governmental unit with general taxing powers,

51

and

2) 95% or more of the proceeds of the issue (other than those in a reasonably required reserve

or replacement fund) are to be used for the issuer’s local governmental activities.

44

IRC Section 148(f)(4)(C)(iii), Treas. Reg. Section 1.148-7(e)(2) and Treas. Reg. Section 1.148-7(h).

45

Treas. Reg. Section1.148-7(b)(4).

46

IRC Section 148(f)(4)(C)(vii) and Treas. Reg. Section1.148-7(k).

47

IRC Section 148(f)(4)(D). All proceeds are excepted, including proceeds in a reasonably required reserve or replacement fund, if any.

48

IRC Section 148(f)(4)(D)(vii).

49

Treas. Reg. Section 1.148-8(c)(2)(iii).

50

IRC Section 148(f)(4)(D)(v).

51

An issuer does not have general taxing power if the issuer’s ability to tax is contingent on approval by another governmental unit.

Treas. Reg. Section 1.148-8(b). See also, IRC Section 148(f)(4)(D)(iv).

14

Bona Fide Debt Service Fund Exception

Certain earnings on bona fide debt service funds are exempt from the rebate requirement

52

if the

issue meets either of the following criteria:

1) The gross earnings on the fund for a bond year are less than $100,000. The issue meets this

requirement if the issue has an average annual debt service not greater than $2,500,000.

53

2) The issue consists of governmental bonds, the issue has an average maturity of at least five

years, and the bonds bear interest at a fixed rate.

54

52

IRC Section 148(f)(4)(A)(ii).

53

Treas. Reg. Section 1.148-3(k).

54

IRC Section 148(f)(4)(A).

15

Part IV

Rebate Amounts and Payments

The rebate rules require that certain arbitrage earnings (rebate) be paid to the U.S. Treasury.

Generally, an issuer must compute and pay rebate owed at least once every five years over the

life of the bond issue.

55

Within that five-year period, issuers have some flexibility choosing the

date they use to compute rebate. The final computation date, however, is the date the bond issue

is fully discharged.

On a computation date, if the issuer determines that it owes rebate, it files a Form 8038-T,

Arbitrage Rebate, Yield Reduction and Penalty in Lieu of Arbitrage Rebate, with the IRS and pays

the required rebate amount generally within 60 days of the computation date. For computation

dates other than the final computation date, the issuer must pay at least 90% of the rebate owed,

taking into account previous rebate payments. The final payment for the final computation date

must be 100% of the rebate amount less previous payments.

Computation of Rebate Amounts

The rebate payment is based on the “rebate amount” on the computation date. The rebate

amount reflects the investment yield earned on nonpurpose investments in excess of the amount

these would have earned if invested at the bond yield. Because payments for, and receipts on, an

investment can happen at different times, an issuer must future value the receipts and payments

to a single date in making a rebate computation. The rebate amount as of each computation

date reflects a snapshot of actual and allowable investment earnings as of those computation

dates over the life of the bonds. The past receipts on, and payments for, the investments are

future valued at the bond yield to give their value as of the computation date, using the same

compounding interval and financial conventions used to compute the yield on the issue.

56

The

rebate amount is the amount by which the value of all the receipts exceeds the value of all the

payments on the computation date.

57

The rebate payment is determined by reducing the rebate

amount by any previous rebate the issuer paid, which is also future valued to that computation

date. Amounts the issuer pays as yield reduction payments on nonpurpose investments are

treated as payments for the investment that are considered in computing rebate. Other payments

that are considered in computing the rebate amount include:

Amounts paid to acquire a nonpurpose investment;

The value of a previously acquired investment that becomes allocated to an issue; and

A computation credit on the last day of each bond year during which there are nonpurpose

investments subject to the rebate requirements and on the nal maturity date.

58

Receipts include:

Amounts received from a nonpurpose investment, such as earnings and return of principal;

The value of a nonpurpose investment that is no longer allocated to an issue, or is no longer

subject to the rebate requirement, before its disposition or redemption date; and

The value of a nonpurpose investment held at the end of a computation period.

55

IRC Section 148(f)(3) and Treas. Reg. Section 1.148-3(f)(1).

56

Treas. Reg. Section 1.148-3(c).

57

Treas. Reg. Section 1.148-3(b).

58

Treas. Reg. Section1.148-3(d)(1)(iv) and Treas. Reg. Section1.148-3(d)(4). These regulations provide a computation credit of $1,400

for bond years ending in 2007, with annual adjustments for inflation thereafter, for bonds sold on or after October 17, 2016. An issuer

may also apply these regulations to bonds sold before October 17, 2016, with the increased computation credit applying to bond years

ending on or after July 18, 2016. A similar credit is available for bond years ending on or after September 26, 2007, under proposed

regulations issued in 2007. REG-106143-07, 72 FR 54606, 54611, 2007-43 IRB 881, 887.

16

Recovering an Overpayment of Rebate

Because rebate is computed by looking at receipts and payments from issuance to the

computation date, it’s possible that an issuer pays rebate for a computation date (because

the value of the receipts exceeded the value of the payments as of that date), but finds that

on a subsequent computation date, the value of the payments exceeds the value of the

receipts so that the rebate amount is reduced or eliminated. In this case, the issuer’s earlier

rebate payment exceeds the rebate amount as of the subsequent computation date because

of investment results after the earlier computation date. An issuer can get a refund of the

overpayment in certain circumstances. The issuer determines the amount of overpayment by

using the future value method to calculate rebate amount (excluding any rebate payments). The

overpayment is the excess of the amount of rebate the issuer paid over the sum of the rebate

amount for the issue as of the most recent computation date and all amounts that the issuer

is otherwise required to pay under IRC Section 148, as of the date the recovery is requested.

59

An issuer requests a refund by completing and filing Form 8038-R, Request for Recovery of

Overpayments Under Arbitrage Rebate Provisions. An issuer must file the form no later than two

years after the final computation date for the issue.

60

59

Treas. Reg. Section 1.148-3(i).

60

Treas. Reg. Section 1.148-3(i)(3)(i).

17

Part V

Accounting for Expenditures and Allocations

Proceeds are no longer subject to the arbitrage requirements when they are properly allocated

to an appropriate expenditure. To make these allocations, issuers must follow special rules and

maintain adequate records. If an issuer improperly treats bond proceeds as allocated to an

expenditure, it may miscalculate the rebate amount, fail to adequately restrict investment yield,

or fail to satisfy the requirements for a spending exception or temporary period. By properly

recording, monitoring and tracking allocations of bond proceeds, issuers can stay in compliance

with the arbitrage requirements.

Generally, proceeds are no longer proceeds of an issue when they are allocated to an

expenditure for a governmental purpose or are deallocated from the bond issue because of

the transferred proceeds or universal cap rules.

61

Proceeds may be allocated to an expenditure

using any reasonable, consistently applied accounting method for an issue’s gross proceeds,

investments and expenditures.

There are special rules and time limits for making allocations, but in general, to allocate gross

proceeds to an expenditure, an issuer must reasonably expect an outlay of cash not later

than five banking days after it allocates gross proceeds to that expenditure.

62

Payment of

gross proceeds of an issue to a related party of the payor is not an expenditure of those gross

proceeds. An issuer must make its allocations no later than 18 months after the later of the date

when the expenditure is paid or the project is placed in service, and in any event no later than

the date the first rebate payment would be due (that is, the earlier of (i) 60 days after the fifth

anniversary of the date the bonds were issued or (ii) 60 days after the date the issue is retired).

63

If the project is funded with tax-exempt bond proceeds and another source of funds, there may

be questions about which sources of funds were used for which expenditures. Here again, the

issuer may use any reasonable, consistently applied accounting method for gross proceeds and

other funds. Examples of reasonable accounting methods

64

an issuer may use include:

1) Specific tracing - bond proceeds are allocated to the specific expenditures actually paid

with the proceeds.

2) Gross proceeds spent first - bond proceeds are allocated to the earliest expenditures.

3) First-in, first-out - the source allocated to the expenditure is based on the order in which

each source becomes available.

4) Ratable allocation - funds from each source are allocated to each of the expenditures

ratably.

If an issuer doesn’t have sufficient books and records to establish an accounting method for

a bond issue and allocation of proceeds of that issue, specific tracing applies for the yield

restriction and rebate rules.

65

Specific rules apply for accounting for purpose investments, certain working capital (“proceeds

spent last” method), grants, reimbursements and commingled funds.

61

Treas. Reg. Section 1.148-6(b)(1). For more information on the universal cap rules, see Treas. Reg. Section1.148-6(b)(2).

62

Treas. Reg. Section 1.148-6(d)(1)(ii).

63

Treas. Reg. Section 1.148-6(d)(1)(iii).

64

Treas. Reg. Section 1.148-6(d)(1)(i).

65

Treas. Reg. Section1.148-6(a)(3).

18

Part VI

Example of Calculation of Rebate Amount and Yield Restriction Analysis

The following is an example to demonstrate the application of basic concepts of the yield

restriction and rebate requirements.

Facts: $49,000,000 variable yield bond issue with an issue date of January 1, 1994. The bond

issue’s first interim computation date is January 1, 1999.

66

The bond yield calculated for the first

computation period is 7.00%.

In this example, the issuer received $49,000,000 in gross proceeds from the sale of bonds,

and on the issue date applied $41,000,000 to purchase a U.S. Treasury note investment with

an annual coupon yield of 7.53% and $8,000,000 to purchase a U.S. Treasury money fund

investment bearing an annual interest rate of 4.97%.

67

In this example, receipts from investments,

unless reinvested, are disbursed immediately for the governmental purpose of the bonds.

The investment transactions used in this example are categorized as either payments or

receipts. The general types of investment transactions, and their treatment, appear in the

following chart. Within a typical computation of the rebate amount (or yield reduction payment),

payments are represented by a negative number (monies going out) and receipts by a positive

number (monies coming in).

Payments Receipts

(Purchase)

(Accrued interest)

(Premium)*

Discount*

(Value at initial allocation)

(Prior period value)

(Prior period rebate amount, if

negative)

(Computation credit)**

(Yield reduction payment)

Maturity

Sale

Accrued interest

Gain*

(Loss)*

Interest

Dividends

Value at end of allocation

End of period value

Prior period rebate amount, if positive

*These are only used as adjustments if the par value of an investment is used to represent the purchase, maturity or sale of an investment.

**Excluded from payments for purposes of computing yield reduction payments.

66

See the discussion of computation dates in Part IV.

67

For ease of illustration, all transactions (purchases and sales) of the note and the fund are at par and interest payments on the fund

only occur on dates when there are purchases or sales. Transaction totals are rounded to whole dollar amounts.

19

The accounting entries for payments and receipts on the note investment are shown in Table 1.

The note purchase is shown as a $41,000,000 payment on January 1, 1994. The semiannual

interest payments received on the note on each January 1 and July 1 are reflected as receipts.

Sales of portions of the note occur periodically on January 1, 1995, September 1, 1995, and

March 1, 1996, and are also reflected as receipts.

Table 1

U.S. Treasury Note 7.530%

Date

Buy

Payment (-)

Sell

Receipt (+)

Interest

Receipt (+)

Investment

Balance

01/01/94 (41,000,000) 41,000,000

02/01/94 41,000,000

05/01/94 41,000,000

07/01/94 1,543,650 41,000,000

01/01/95 1,780,000 1,543,650 39,220,000

07/01/95 1,476,633 39,220,000

09/01/95 18,275,000 231,844 20,945,000

01/01/96 788,579 20,945,000

03/01/96 20,945,000 259,971 0

(41,000,000) 41,000,000 5,844,328

Table 2 illustrates the accounting entries for payments and receipts on the fund investment. The

purchase of the initial investment in the fund is shown as an $8,000,000 payment on January 1,

1994. Purchases of subsequent investments in the fund (representing immediate reinvestment

in the fund of all receipts from interest earnings on the note and the fund on each date) are

reflected as additional payments on July 1, 1994, July 1, 1995, and January 1, 1996. The periodic

interest payments received on the fund are reflected as receipts. Sales of portions of the fund

occur on February 1, 1994, May 1, 1994, January 1, 1995, September 1, 1995, and March 1,

1996, which are also reflected as receipts.

Table 2

U.S. Treasury Money Fund 4.970%

Date

Buy

Payment (-)

Sell

Receipt (+)

Interest

Receipt (+)

Investment

Balance

01/01/94 (8,000,000) 8,000,000

02/01/94 2,966,230 33,770 5,033,770

05/01/94 4,938,996 61,004 94,774

07/01/94 (1,544,437) 787 1,639,212

01/01/95 1,635,279 41,071 3,932

07/01/95 (1,476,730) 97 1,480,662

09/01/95 1,480,655 12,500 7

01/01/96 (788,579) 0 788,586

03/01/96 788,586 6,443 0

(11,809,746) 11,809,746 155,672

20

Table 3 combines the amounts of payments and receipts for each date from Table 1 and Table 2

to summarize the payments and receipts included in the computation of rebate amount and the

computation of yield on investment. The total payments column represents the sum of payments

for purchases of the note and the fund, represented as negative amounts. The total receipts

column represents the sum of receipts from investment earnings on and sales of the note and

the fund, represented as positive amounts. The net payments and receipts column is the sum of

the payments and receipts columns.

Table 3

Total Total Net Payments

Date Payments (-) Receipts (+) and Receipts

01/01/94 (49,000,000) 0 (49,000,000)

02/01/94 0 3,000,000 3,000,000

05/01/94 0 5,000,000 5,000,000

07/01/94 (1,544,437) 1,544,437 0

01/01/95 0 5,000,000 5,000,000

07/01/95 (1,476,730) 1,476,730 0

09/01/95 0 20,000,000 20,000,000

01/01/96 (788,579) 788,579 0

03/01/96 0 22,000,000 22,000,000

(52,809,746) 58,809,746 6,000,000

Generally, on dates when investments mature or are sold, or interest earnings are received, a

receipt is included in the calculation of rebate amount. On dates when investments roll over or

are purchased, or interest earnings are reinvested, a payment is included in the calculation of

rebate amount. The payments and receipts on a corresponding date offset each other and the

daily net total is included in the calculation of rebate amount.

Rebate Amount Calculation

Table 4 illustrates the calculation of rebate amount for the January 1, 1999, computation date

based on the net payments and receipts column from Table 3 and the permitted computation

credit on the last day of each bond year during which there are amounts allocated to gross

proceeds of an issue subject to the rebate requirement. The rebate amount for the computation

date is calculated as the sum of the future values of each payment, receipt and computation

credit

68

as of the computation date using the bond yield (7.00% per year) as the rate of return in

the future value computation. The rebate amount as of January 1, 1999, is $452,432.

68

Prior to 2007, the amount of the computation credit available under Treas. Reg. Section 1.148-3(d)(1)(iv) was $1,000. See also

footnote 58 for more information on the increase in the computation credit.

21

Table 4

Date

Net Payments

and Receipts

Future Value

at Bond Yield

01/01/94 (49,000,000) (69,119,339)

02/01/94 3,000,000 4,207,602

05/01/94 5,000,000 6,893,079

07/01/94 0 0

01/01/95 5,000,000 6,584,045

01/01/95 (1,000) (1,317)

07/01/95 0 0

09/01/95 20,000,000 25,155,464

01/01/96 0 0

01/01/96 (1,000) (1,229)

03/01/96 22,000,000 26,735,275

01/01/97 (1,000) (1,148)

452,432

Table 4 demonstrates that the rebate amount is $452,432 as of the January 1, 1999, computation

date. The issuer must submit a rebate payment of at least 90% of this amount within 60 days

of this interim computation date by filing Form 8038-T and including the required payment. If

January 1, 1999 was the final computation date, the issuer must submit 100% of the rebate

amount.

Yield Restriction Analysis

An issuer determines whether it has complied with the yield restriction requirements by

comparing the yield on investment with the maximum yield that is not materially higher than the

yield on the bond issue. The issuer should include all unconditionally payable receipts and all

unconditionally payable payments.

Computation of Yield Reduction Payments

For certain investments, an issuer can make yield reduction payments (including rebate

payments) to the U.S. Treasury that reduce the yield on the investments for the yield restriction

requirements. For an eligible investment class, an issuer must pay the amount that will result in

the yield on that class not being materially higher than the bond yield.

The example below assumes that the bond issue is entitled to the general 30-day temporary

period and the general 1/8th of 1% materially higher yield limit.

Table 5 shows the payments for and receipts from investments in the note and the fund.

The amounts entered for January 31, 1994 (the first day after the end of the general 30-day

temporary period) are the values of the investments as of that date for the note and the fund,

originally purchased on January 1, 1994. As permitted under the arbitrage requirements, the

issuer values the note at present value and the fund at fair market value (essentially par plus

accrued interest). The yield restriction requirements provide for certain temporary periods during

which yield restriction does not apply. Consequently, the initial temporary period is not included

in the determination of yield on investment. The result is that instead of the calculation starting

on the issue date, it starts when the temporary period ends.

22

Table 5

U.S. Treasury Note 7.530% U.S. Treasury Money Fund 4.970%

01/01/94 N/A N/A

01/31/94 (41,245,085) (8,032,681)

02/01/94 2,966,230 33,770

05/01/94 4,938,996 61,004

07/01/94 1,543,650 (1,544,437) 787

01/01/95 1,780,000 1,543,650 1,635,279 41,071

07/01/95 1,476,633 (1,476,730) 97

09/01/95 18,275,000 231,844 1,480,655 12,500

01/01/96 788,579 (788,579) 0

03/01/96 20,945,000 259,971 788,586 6,443

Date

Value

Payment (-)

Sell

Receipt (+)

Interest

Receipt (+)

Value/Buy

Payment (-)

Sell

Receipt (+)

Interest

Receipt (+)

(41,245,085) 41,000,000 5,844,328 (11,842,427) 11,809,746 155,672

Table 6 summarizes the payments and receipts from Table 5 included in the computation of

yield on investment. The total payments column represents the sum of payments from the value

of investments (as of January 31, 1994) and purchases of the fund. The total receipts column

represents the sum of receipts from investment earnings on and sales of the note and the fund.

Under the yield restriction requirements, the yield on investments cannot be materially higher

than the yield on the bonds. The yield on an investment allocated to an issue is the discount rate

that, when used in computing the present value as of the date the investment is first allocated

to the issue of all unconditionally payable receipts from the investment, produces an amount

equal to the present value of all unconditionally payable payments for the investment. When the

net receipts and payments in Table 6 are present valued to January 31, 1994, that discount rate

(which is the yield on investment) is 7.451%, exceeds the materially higher yield limit of 7.125%.

Table 6

Date

Total

Payments (-)

Total

Receipts (+)

Net Payments

and Receipts

01/01/94 0

01/31/94 (49,277,766) 0 (49,277,766)

02/01/94 0 3,000,000 3,000,000

05/01/94 0 5,000,000 5,000,000

07/01/94 (1,544,437) 1,544,437 0

01/01/95 0 5,000,000 5,000,000

07/01/95 (1,476,730) 1,476,730 0

09/01/95 0 20,000,000 20,000,000

01/01/96 (788,579) 788,579 0

03/01/96 0 22,000,000 22,000,000

(53,087,512) 58,809,746 5,722,234

Table 7 illustrates a method of calculating the excess arbitrage earnings equaling the amount

23

of a yield reduction payment necessary to reduce the yield on investment to the maximum

permitted yield of 7.125%, which is not materially higher than the bond yield. The yield reduction

payment is calculated using the sum of the future values of each payment and each receipt as of

the relevant computation date (January 1, 1999) using the bond yield adjusted to the materially

higher yield (7.125% per year) as the interest rate in the future value computation.

Table 7

Net Payments Future Value to

Date and Receipts Yield Restriction Limit

01/01/94 0 0

01/31/94 (49,277,766) (69,538,765)

02/01/94 3,000,000 4,232,654

05/01/94 5,000,000 6,932,027

07/01/94 0 0

01/01/95 5,000,000 6,615,919

07/01/95 0 0

09/01/95 20,000,000 25,256,907

01/01/96 0 0

03/01/96 22,000,000 26,826,890

5,722,234 325,632

Table 7 demonstrates that the yield on investments exceeds the bond yield increased to the

materially higher limit by $325,632, which, unless reduced, would cause the bonds to be

arbitrage bonds. In this example, the issuer can make a yield reduction payment because this is

a variable yield bond. The yield reduction payment necessary to reduce the yield on investment

to the allowable materially higher limit (that is, 7.125%) is $325,632. The issuer must submit a

yield reduction payment within 60 days of the interim computation date by filing Form 8038-T

together with the required payment, but need not submit a payment more than once every five

years.

In this example, the issuer’s arbitrage liability to the U.S. Treasury, as of the January 1, 1999

computation date, would include a yield reduction payment of $325,632 and rebate of $126,800

($452,432 minus $325,632), because the yield reduction payment is treated as a payment in

the determination of rebate amount under Treas. Reg. Section 1.148-3(d)(1)(v). The issuer would

report this arbitrage liability and submit payment using Form 8038-T. Because January 1, 1999

is an interim computation date, the issuer need only make a payment equal to at least 90% of

the rebate amount as of that date to satisfy the rebate requirements.

69

For the final computation

date, an issuer must pay 100% of the rebate amount.

69

Treas. Reg. Section 1.148-3(f)(1).

24

Part VII

Information and Services

You can find information about the tax laws that apply to tax-exempt bonds and other municipal

financing arrangements at IRS.gov/bonds, including:

Published guidance about the tax laws that apply to municipal nancing arrangements,

including revenue rulings, revenue procedures, notices and announcements.

Tax forms, instructions and publications related to tax-exempt bonds.

Additional educational resources on Voluntary Compliance.

If you have account specific questions, call Customer Account Services toll-free at 877-829-5500.

What to do if you discover a violation - The TEB Voluntary Closing Agreement

Program

The IRS is committed to resolving federal tax violations with the issuer. The TEB Voluntary

Closing Agreement Program (TEB VCAP) provides remedies for issuers of tax-exempt bonds,

tax credit bonds, and direct pay bonds that voluntarily come forward to resolve a violation that

cannot be corrected under self-correction programs found in the Treas. Reg. or other published

guidance. Notice 2008-31 provides information and general guidance about TEB VCAP. Internal

Revenue Manual (IRM) Section 7.2.3 provides general procedures under which the IRS will

enter into closing agreements. Closing agreement terms and amounts vary by the degree of the

violation as well as the facts and circumstances.

TEB VCAP offers standardized methods for resolving certain types of noncompliance,

referred to as resolution standards. For example, TEB VCAP offers a resolution standard for

circumstances in which a failure of an escrow agent or trustee to perform obligations under an

escrow agreement to purchase U.S. Treasury Securities – State and Local Government Series

necessary to maintain compliance with yield restriction requirements results in a yield restriction

violation. TEB VCAP is also available to resolve other violations of the yield restriction and rebate

requirements.

An issuer must use Form 14429, Tax Exempt Bonds Voluntary Closing Agreement Program

Request, to submit a request and provide the required information. While the IRS generally

enters into closing agreements with the issuer of the bonds, in certain cases other parties to the

bond transaction (including an entity borrowing the bond proceeds) may also participate in the

negotiations and jointly execute the agreement.

For more information about this program, including request submission requirements, case

processing procedures and resolutions standards, see IRM Section 7.2.3.

25