In the loop | 1

In the loop

New human capital disclosure rules:

Getting your company ready

October 2020

(updated April 2021)

With up to 85% of a company’s costs tied up in people (pwc.com), stakeholders looking

to allocate investment dollars want to understand how management sees the company’s

strategic and operational requirements. The SEC introduced new disclosure requirements

in August 2020 designed to provide stakeholders insight into human capital—from the

operating model, to talent planning, learning and innovation, employee experience, and

work environment. The disclosures may help stakeholders evaluate whether a business

has the right workforce to meet immediate and emerging business challenges and the

nature and magnitude of the related investments. However, there are questions as to what

is required to comply with the principles-based rules.

In certain SEC lings, a public company is now required to disclose:

• the number of employees and a description of its human capital resources, if material

to the business as a whole; and if material to a particular segment, that segment should

be identied

• any human capital measures or objectives, if material, that the registrant focuses on

in managing its business, such as those related to the development, attraction, safety,

engagement, and retention of employees

The rules do not include a denition of “human capital” or a list of required measures

to disclose. The principles-based approach (1) reects an expectation that disclosures

will be tailored to a company’s own business or industry using management’s

judgment and (2) allows for the disclosures to evolve in response to changes in a

company’senvironment.

We also are not adopting a denition of the term “human capital”

…because this term may evolve over time and may be dened by

different companies in ways that are industry specic. This approach

is consistent with the view expressed by a number of commenters

that noted that there are many denitions of human capital and that

the concept, while generally well understood, is often tailored to the

circumstances and objectives of individual companies.

– Release on Modernization of Regulation S-K Items 101, 103, and 105

“

I am particularly

supportive of the

increased focus

on human capital

disclosures, which for

various industries and

companies can be an

important driver of

long-term value.

– Jay Clayton, then SEC Chairman

This

In the loop

was updated in April 2021 to include insights from our review of human

capital disclosures in recent Form 10-K filings.

In the loop | 2

National Professional Services Group

The new rules, which are part of the SEC’s broader project to modernize Regulation

S-K, became effective November 9, 2020. As a result, 2020 Form 10-Ks and other lings

subject to Regulation S-K led on or after this date need to include the new disclosures.

Step 1 Step 2 Step 4

Scoping Reliability and consistency

Inventory all

human capital

measures or

objectives that

you focus on in

managing the

business.

Narrow the

inventory to

include the

measures that

are material to an

understanding of

the business.

Step 3

Implement

processes and

controls over

the preparation

and reporting of

human capital

measures.

Consider subsequent

measurement and reporting.

Human capital measures

should be consistent from

period to period. Changes to

how the measures are used or

calculated should be disclosed.

While every company will differ, the following can help guide your approach.

Scoping

Companies are evaluating which objectives or measures to disclose to comply with the

principles-based requirements and meet investor and regulator expectations. Jay Clayton,

then SEC Chairman, noted that he expects to see "meaningful qualitative and quantitative

disclosure, including, as appropriate, disclosure of metrics that companies actually use in

managing their affairs.” But beyond that general guidance, companies have broad

flexibility. Although specific to each company depending on its workforce strategy, we

recommend companies consider the following, including a specific focus on two areas that

significantly impacted most companies in 2020: COVID-19 and diversity, equity, and

inclusion (DEI).

Human capital resources

Human capital resources, while not dened

in the rules, may include employees,

non-employees, such as contract

workers, and others.

Objectives or measures

The rules require disclosure

of human capital objectives

or measures used to

manage the business

if material to an

understanding of the

business. Companies

need to consider

whether to include a

qualitative objective

and/or a quantitative

measure in each area

of human capital.

Example human

capital metrics

Number

ofemployees

in well-being

programs

Succession

planning

rates

Number of

employees

per manager

Development

and training

costs

Revenue or

prot per

employee

Diversity

(e.g., gender,

age, ethnicity)

Number

of safety

incidents

Recruitment

rates

Employee

retention or

turnover rate

Total

workforce

costs; labor

cost per

FTE

Ethics &

compliance

training

completion

In the loop | 3

National Professional Services Group

Sources of measures

The rules require companies to consider the measures used by management in running

the business, which may include those reported in an enterprise balanced scorecard, or

board or executive reporting, or considered in executive compensation.

Companies might also consider what aspects of human capital have been previously

communicated as being critical to the business, whether in public lings, investor and

employee briengs, or other public statements. For example, companies may have

included explicit references to their human capital resources in their proxy lings;

environmental, social, and corporate governance (ESG) disclosures; as well as during

shareholder engagement.

Various resources may also help companies focus on what investors and other

stakeholders consider to be meaningful:

• International Organization for Standardization recommendations on human capital

reporting standards

• Sustainability Accounting Standards Board sector-specic human capital metrics

• World Economic Forum report (published with the Big 4 accounting rms) that denes

common metrics for sustainable value creation and ESG reporting, which includes

human capital

• PwC’s Saratoga benchmarking tool that provides industry-specic metrics in various

areas of human capital: workforce productivity, span of control, succession, recruiting

costs, hire quality, labor costs, turnover, diversity, HR cost, and organizational

structures

• Other frameworks, such as those developed by Morgan Stanley Capital International

(MSCI) or Institutional Shareholder Services (ISS)

Lastly, companies might consider whether peer disclosures create an expectation for

comparable disclosures.

Material to the business

The requirements are rooted in materiality. The SEC considers information material if there

is a substantial likelihood that a reasonable investor would consider it important in making

an investment or voting decision. This may be an appropriate benchmark in identifying

which human capital measures or objectives are material to the business.

Focusing human capital disclosures in light of current events

As the rule indicates, human capital disclosures should evolve over time as companies

respond to risks and challenges. There are perhaps no better examples of risks and

challenges a company needs to address than the COVID-19 global pandemic and the

need for diversity, equity, and inclusion. In this rst year of adoption, we suggest focusing

human capital disclosures in these areas if material to the business.

In the loop | 4

National Professional Services Group

COVID-19

The COVID-19 crisis spotlighted the importance of having policies that protect employees

and invest in their well-being. For months, companies have grappled with how to adapt

their human capital management to retain their workforce, provide a safe workplace,

accommodate remote workers, and respond to difculties in supply chains. Areas of a

company’s human capital management that might be impacted by COVID-19 include

thefollowing.

Diversity, equity, and inclusion

DEI has become not only an area of public policy, but also an issue of corporate

responsibility. Stakeholders want to know how companies are creating an equitable

workplace, and how they plan to respond to other DEI matters, including ensuring

diversity at the management and board levels. DEI measures or objectives to consider

that might be material to a company’s business include the following:

• Diversity measures related to employee identities, such as race and ethnicity, gender

identity and expression, sexual orientation, culture, veteran status, age, disability,

marital status, or religious and spiritual beliefs

• Equity measures related to providing employees equal access to opportunities, such

as equity in pay, the percentage of a company’s management team that is diverse, or

recruiting strategies aimed at providing fair opportunities for diverse talent

• Inclusion efforts, such as networks or programs that connect employees so

they can support one another and advise company leadership on the needs of diverse

employees

Metrics alone may not tell the full story of a company’s values, the scope of its DEI

programs, or the true investment it has made in its employees. A thorough narrative that is

linked to a company’s corporate purpose and mission can help bridge this gap.

Well being

Recognizing the toll remote work and other

challenges can take on their employees,

many companies are implementing

various programs or initiatives to invest

in their employees’ well being.

Succession

planning

Some companies are seeing

increased focus by their Boards and

stakeholders on key roles beyond

the C-suite and future plans for

thoseroles.

Furloughs/

Lay offs

Some companies especially hard hit

by the pandemic have had to either

temporarily or permanently let go of

some of theirworkforce.

Mental

health

Health and safety of employees,

especially in essential services, has

become a top priority for companies.

Onboarding

Onboarding new employees while

much of the workforce is working

remotely has posed signicant

challenges, often requiring companies

to digitally upskill theiremployees.

Compensation

Many companies have had to change

compensation or pay structure for

employees and/or management in

response to declines in business

orprotability.

COVID-19 and the impact on human capital

In the loop | 5

National Professional Services Group

Reliability and consistency

The new human capital disclosures should be supported by effective controls and

procedures. For example, when included in the annual report, they will be subject to the

company’s disclosure controls and procedures (DCP), but when included in other lings,

such as registration statements, separate controls may be needed. As your company

considers the appropriate controls over these new disclosures, questions could include:

• What is the quality of the data underlying the disclosures?

• What governance exists over this data? Does it ow through the disclosure committee,

board of directors, and/or audit committee?

• Based on the type of ling, are the disclosures subject to DCP or are there other

processes and controls that support the reliability of the information reported?

• Do we have a policy on scoping, measurement, and presentation of the information to

aid consistency between periods?

• Will consumers of the human capital information be condent in its accuracy

andcompleteness?

• Do we have a process for determining when changes to measures are needed and disclosed?

Follow the data

Quality data is foundational to disclosures. Companies may face challenges in obtaining,

analyzing, and reporting on the data, including the following.

Key challenges Where to start

Applicable

framework

and key

metrics

• No requirements for specic

metrics—companies have to decide

what is material and most applicable

• What is “material to the business”

changes from period to period,

but the principles surrounding the

evaluation should remain the same

• Dene a set of relevant metrics and

proactively identify what information to

report, how to source it, and who the

key stakeholders are

• Establish processes for revisiting key

metrics each period

Data

sources and

transformation

• Data comes from various nancial

and nonnancial systems

• Manual intervention is often required

• Historical data may not be available

• Identify standardized data

sources/attributes

Process and

governance

• Limited controls or attestations over

the data

• Limited governance - data was

not reviewed by the disclosure

committee, board of directors, and/

or audit committee

• Establish clear processes, controls,

and attestations appropriate for each

disclosure (e.g., DCP for disclosures in

the annual report)

• Establish governance protocols,

including ensuring key information is

shared with the disclosure committee

and the audit committee

Reporting

and analytics

• No standardized reporting process

• Data consolidation may be manual

and may not always lend itself to

actionable insights

• Limited self service analytics tools

• Expand existing reporting frameworks

to include this data when applicable

• Increase communication and

collaboration between human resource

and nance personnel to proactively

drive actionable insights

• Use data analysis and visualization tools

to automate reporting and analysis

In the loop | 6

National Professional Services Group

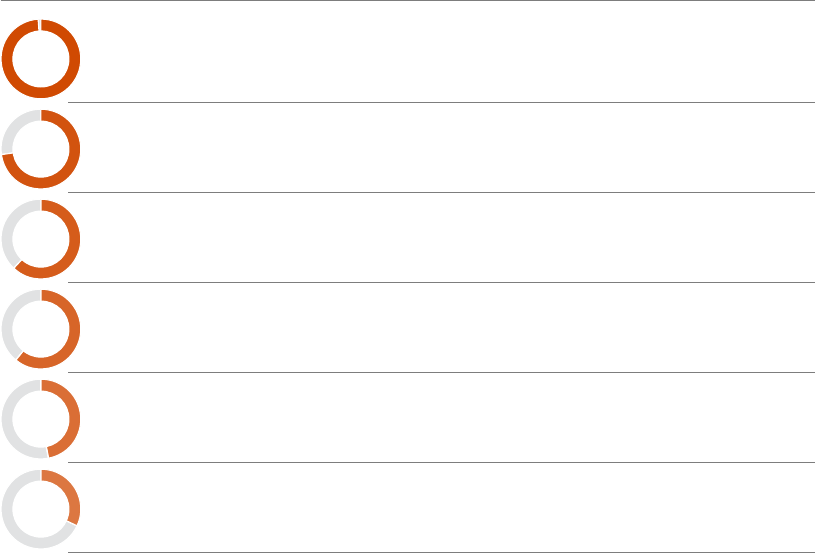

What have filers disclosed?

We looked at more than 2,000 Form 10-Ks led from November 9, 2020, the effective date

of the new rules, through February 28, 2021. In these Form 10-Ks, we noted:

• 89% included both qualitative and quantitative metrics

• 75% included disclosures related to COVID-19 and the impact to human capital,

the majority of which were qualitative

• 66% disclosed DEI information (e.g., gender, sexual orientation, ethnicity, veteran status,

culture, strategy, age, religion), much of which was qualitative; many companies did not

include measures or objectives related to diversity at the management level, and the

q

uantitative DEI metrics disclosed primarily included the total number of employees and

gender percentages

• Other trends include:

99%

73%

62%

61%

47%

32%

Percent of 10-K lings that include*:

Employee demographics

Employee headcount, geographical distribution, job function, education level, regular/part-time

Employee lifecycle

Hiring/recruitment, learning/development, mobility, retention, succession planning, turnover

Safety

Health and safety

Total rewards

Employee compensation, benets

Labor relations

Collective bargaining

Employee feedback

Engagement/satisfaction scores

*Includes both quantitative and qualitative disclosures

The

future of human capital reporting

The change of administration in the White House and the SEC could inuence the focus

on human capital disclosures. Two SEC Commissioners dissented to the nal rule and

pushed the Commission to play a more active role in enhancing reporting for topics such

as ESG, including climate change.

Amid these broader

unknowns, a company should make sure it accurately and thoroughly

describes the impacts on human capital of current events, COVID-19 and the focus on

DEI in particular, if material. In addition, it should periodically assess whether the human

capital measures disclosed continue to be the most relevant. Appropriate controls and

processes will need to be maintained, especially when it comes to the underlying data

supporting human capital disclosures.

Effective and transparent disclosure of human capital initiatives will provide stakeholders

with a new window into how a company manages its workforce and invests in its people

to create long-term value.

© 2021 PwC. All rights reserved. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes

refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional

advisors.

Sheri Wyatt

Partner, Digital Assurance &

Transparency – ESG

sheri.wyat[email protected]m

Brandon Yerre

Principal – Organization and

WorkforceTransformation

brandon.w.yerre@pwc.com

To have a deeper discussion, contact:

For more PwC accounting and reporting content, visit us at viewpoint.pwc.com.