May 2022

Navigating the

market headwinds:

The state of grocery

retail 2022

North America

Copyright © 2022 McKinsey &

Company. All rights reserved.

This publication is not intended to be

used as the basis for trading

in the shares of any company or for

undertaking any other complex

or signicant nancial transaction

without consulting appropriate

professional advisers.

No part of this publication may

be copied or redistributed in any

form without the prior written

consent of McKinsey & Company.

Cover image:

© Edwin Tan/Getty Images

1

State of Grocery North America

Contents

80

Pushing granular decisions through

analytics

6

The state of grocery in North America

19

The next horizon for

grocery e-commerce: Beyond the

pandemic bump

32

Tech-enabled grocery stores: Lower

costs, better experience

37

Achieving protable online grocery

order fulllment

45

Growing beyond groceries: The

ecosystem expansion

52

Grocers’ sustainability opportunity in

transforming the food system

64

Crisis or opportunity? How grocers

can win the talent war

72

The state of grocery retail in Mexico

3

State of Grocery North America

Foreword

More than two years after the start of the COVID19 pandemic, the grocery industry continues to

face disruption. While some themes shaping the sector—such as the supply chain and the growth of

e-commerce—have resonated throughout this period, additional headwinds are once again testing

the resilience of grocers and the food industry as a whole. Executives at North American grocery

retailers have expressed some uncertainty about market conditions in 2022, pointing to lower profit

margins during the pandemic, increased price sensitivity, greater competition, and rising inflation

that is forcing consumers to grapple with an increased cost of living. These trends, as well as global

events, are likely to only have a greater impact on consumer confidence and spending.

Moving further into 2022 and beyond, grocers will be faced with increased pressure on margins and

pricing as they navigate the need to cater to broader consumer tastes and demands. Omnichannel

complexity will continue to rise, with consumers seeking more seamless experiences and

manageable fulfillment fees.

We recognize the significant uncertainty facing the industry. All grocery executives are grappling

with a series of questions: As consumer behavior continues to evolve, how can grocers best cater to

new trends such as health and wellness and value? E-commerce has become table stakes, but how

can they continue to enhance the omnichannel experience while improving profitability? How much

investment will they need to make in automation, and how can they harness technology to change

the operating model for stores and employees? As sustainability gains traction, what is the right way

to begin the journey or build on existing plans?

This report aims to answer those questions. Its contents are part of McKinsey’s broader global

series The State of Grocery Retail, an annual publication covering three continents (including Asia–

Pacific, the European Union, and North America, with a new article specific to Mexico). Our goal is

to frame major trends and issues for CEOs seeking to stay ahead of market shifts. To offer a holistic

view of industry dynamics, insights and analyses from our colleagues are complemented by surveys

and interviews with grocery executives.

We wish to thank FMI for its collaboration in developing these perspectives and in supporting

the engagement of CEOs from leading North American grocery and consumer packaged goods

companies. We hope the report will offer new insights that can help grocers, and those in the

broader food industry, remain competitive during these unprecedented times.

Becca Coggins

Senior partner

North American leader,

Retail Practice

Sajal Kohli

Senior partner

Global leader,

Retail and Consumer

Packaged Goods Practices

Bill Aull

Partner

North American leader,

Grocery Practice

4 State of Grocery North America

Editors

Operations lead

Bill is a partner in McKinsey’s Charlotte oce and a leader within

the Retail and Consumer Practices for the Americas. He now leads

McKinsey’s North American grocery practice. He has been with McKinsey

for the last 12 years, and his client work has spanned across both retail

and consumer-packaged-goods sectors with a focus on transformation

topics—commercial strategy, organization restructuring, merchandising

(pricing, promotion, assortment, and vendor negotiations), store

operations, and supply chain. He has worked across numerous retail

channels and formats and consumer categories.

Sajal is based in Chicago and leads McKinsey’s global work in the retail

and consumer-goods industries. In more than 25 years of management

consulting, Sajal has counseled leading global retail and packaged-goods

clients as they set growth strategies and face challenges from the changing

international landscape and from domestic-market shifts caused by

digitalization, consolidation, and new entrants. He has served retail and

consumer-goods clients across Asia, Canada, Europe, Latin America, and

North America. He serves retail clients across multiple formats, including

hypermarkets, pure e-commerce players, grocers, restaurant chains,

department stores, and leading consumer-goods companies across food,

consumer-electronics, personal-care, beauty, and other categories. Sajal

focuses on working with senior leaders and their management teams to

drive growth and commercial and operations transformations across both

retail and consumer-goods companies. Over the last few years, he has been

spending a lot of time with organizations on the potential and implications

of tech enablement, including advanced analytics, articial intelligence, and

their implications on the future of work.

Eric Marohn is an expert with McKinsey who has been with the company

for 22 years. He is based in Chicago, IL, focusing his practice on the North

American grocery market. His expertise is in merchandising, marketing,

sales, formats, and consumer research, with extensive knowledge across

North America. He focuses on grocery, food, and consumer trends; corporate

strategy; and growth transformation in international and US-based markets.

Bill Aull

Sajal Kohli

Eric Marohn

5

State of Grocery North America

Contributors

Cara Aiello

Consultant

Boston

Bassel Berjaoui

Associate partner

Paris

Andreas Ess

Partner

Zurich

Tyler Harris

Associate partner

Washington D.C.

Nikola Jakic

Associate Partner

Toronto

Nicholas Landry

Associate partner

Vancouver

Jaya Pandrangi

Partner

Chicago

Patrick Simon

Partner

Munich

Tom Youldon

Partner

London

Manik Aryapadi

Partner

Dallas

Vishwa Chandra

Partner

San Francisco

Ricardo Ferreira

Consultant

Libson

Jake Hart

Director of

Solution Delivery

Cleveland

Jonatan Janmark

Partner

Stockholm

Eric Marohn

Knowledge expert

Chicago

Beatriz Rastrollo

Associate partner

Madrid

Raphaël Speich

Partner

Paris

Sara Bondi

Associate partner

Pittsburgh

Bill Aull

Partner

Charlotte

Gokmen Ciger

Associate partner

Istanbul

Sebastian Gatzer

Partner

Cologne

Jenny Hu

Associate partner

Toronto

Bartosz Jesse

Partner

Zurich

Rahul Mathew

Associate partner

New York

Joshua Reuben

Consultant

Toronto

Sarah Touse

Partner

Boston

Fernando Ayala

Consultant

Mexico City

Becca Coggins

Senior partner

Chicago

Prabh Gill

Associate partner

Vancouver

Karina Huerta

Constultant

Mexico City

Sajal Kohli

Senior partner

Chicago

Varun Mathur

Partner

San Francisco

Daniel Roos

Associate partner

Cologne

Kumar

Venkataraman

Partner

Chicago

Steven Begley

Partner

New York

José Ricardo Cota

Associate partner

Mexico City

Maura Goldrick

Partner

Boston

Holger Hürtgen

Partner

Dusseldorf

Alexandra

Kuzmanovic

Consultant

Chicago

Bill Mutell

Partner

Atlanta

Ricardo Sanromán

Partner

Mexico City

Janice Yoshimura

Consultant

Chicago

Acknowledgments

Special thanks to Janiece Lehmann, Becca Coggins, Daniel Laeubli, and Julia Spielvogel. We would also

like to thank Beatriz Rastrollo and Karin Ringvold for their work in conducting the consumer survey for the

European report and laying the foundation for this one.

Thanks to Leff for providing editorial and design services for this report.

6 State of Grocery North America

The state of grocery in

North America

The emergence of new challenges will force grocery retailers to adapt their

strategies and operations. Executives should focus on five priorities in 2022.

© Jacob Fergus/Getty Images

by Bill Aull, Becca Coggins, Sajal Kohli, and Eric Marohn

7

State of Grocery North America

Over the past two years, grocery

retailers have had to reassess and adapt

nearly every facet of their operations.

Changes to the grocery landscape will

continue, shaped by both macroeconomic

factors (such as supply chain challenges

and ination) and mercurial customer

preferences. To keep pace, retailers should

focus on a handful of trends: the rise of

the value-conscious, healthier-eating

consumer; elevated consumer expectations

for omnichannel; an increased emphasis on

sustainability; strategic workforce planning

and investment in tech and analytics; and

the growing importance of ecosystems

and partnerships.

Looking back on 2021

In our conversations with CEOs, “volatile”

was the word used most frequently to

describe 2021. Since 2019, the market

has grown at an impressive 15 percent,

1

a rise that was the product of increases

to both prices and volumes. But these

top-line numbers belie the roiling retail

landscape beneath. Signicant shifts

in share of stomach, supply and labor

shortages, unprecedented investments in

e-commerce, and rising ination created

widespread disruption for grocers.

Acceleration of pandemic-related

consumer trends

According to recent McKinsey consumer

insights, the trends that took hold at

the start of the pandemic have gained

momentum. Total e-commerce sales

have grown nearly 60 percent since

the beginning of the pandemic, though

penetration rates have leveled o. At the

same time, consumers are making fewer

trips and visiting a smaller number of

stores: they are 20 percent more likely to

go to just one grocery store a week. As

such, consumers are increasingly seeking

out one-stop shops and have expressed an

interest in buying everything in one place

even more frequently in 2022.

Meanwhile, the food-at-home market,

which had been slowly losing share to

food away from home before 2020, has

surged 8.7 percent, four times its historical

growth rate. The move to food at home

coincides with a growing emphasis on

healthier eating.

Together, these trends suggest consumer

behaviors have fundamentally changed—

and grocers should take notice.

A steadying but still-fragile supply chain

Disruptions to supply chains during the

pandemic have increased out-of-stock

rates by upward of 15 percent, compared

with historical rates of 5 to 10 percent.

2

Issues over the past two years have been

attributed to a host of factors, including

bottlenecks at ports, labor shortages, and

huge, unanticipated spikes in consumer

demand. The good news is that some of

these challenges, such as overseas vessel

delays and container shortages, will pass.

Others—such as labor shortages and the

ongoing shift toward automation—have

been a long time in the making and will

require a sustained commitment to resolve.

Signicant shocks to the labor market

The grocery industry employs nearly three

million people in the United States.

3

Every

aspect of the industry’s people model—

1

Total grocery sales across traditional grocery, supercenters, mass market, drug stores, convenience stores,

clubs, discounters, and online channels inclusive of drug spending; Kantar LLC, Copyright 2022. All rights

reserved 2022.

2

Kelly Tyko, “Grocery stores still have empty shelves amid supply chain disruptions, omicron and winter storms,”

USA Today, January 12, 2022.

3

“Supermarkets & grocery stores in the US - Employment statistics 20022027,” IBISWorld, updated December

29, 2021.

8 State of Grocery North America

corporate, in-store, and across every part of

its operation—is experiencing an upheaval

caused by a rise in absenteeism and

attrition as well as by employee demands

for exible labor scheduling. The workforce

participation rate plunged dramatically

during the pandemic; as of August 2021,

it was still 1.6 percentage points below

prepandemic levels. The accelerating

adoption of automation (such as the

increased use of self-checkout, image

technology to perform in-stock checks, and

automated picking in warehouses) is also

changing the workforce dynamic.

Emergence of unprecedented ination

At the beginning of 2022, ination exceeded

7 percent, fueled by historic rises in labor,

freight, and commodities costs during the

latter half of 2021. Today’s inationary

environment continues to stem from a blend

of cyclical, structural, and global supply

chain issues. The recognition of supply chain

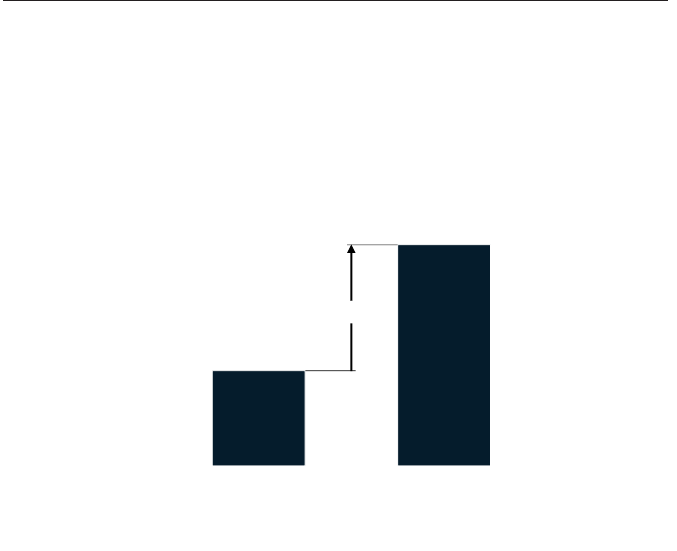

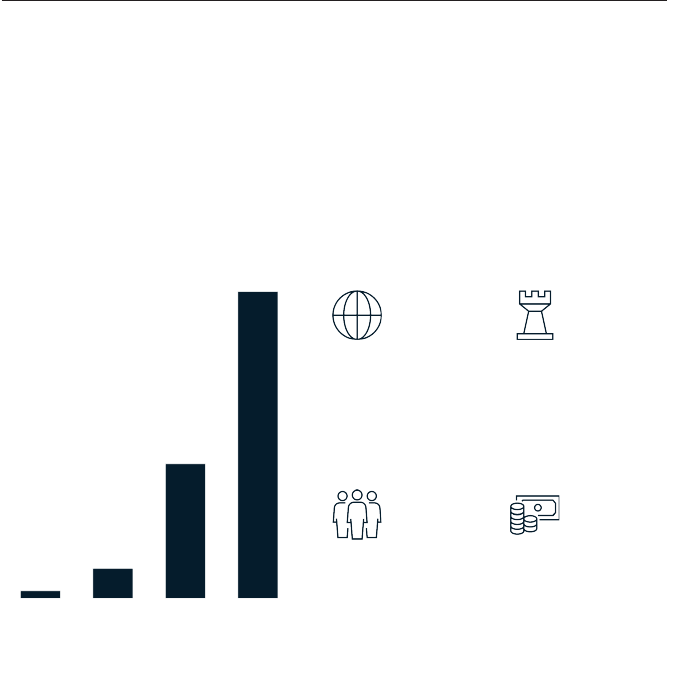

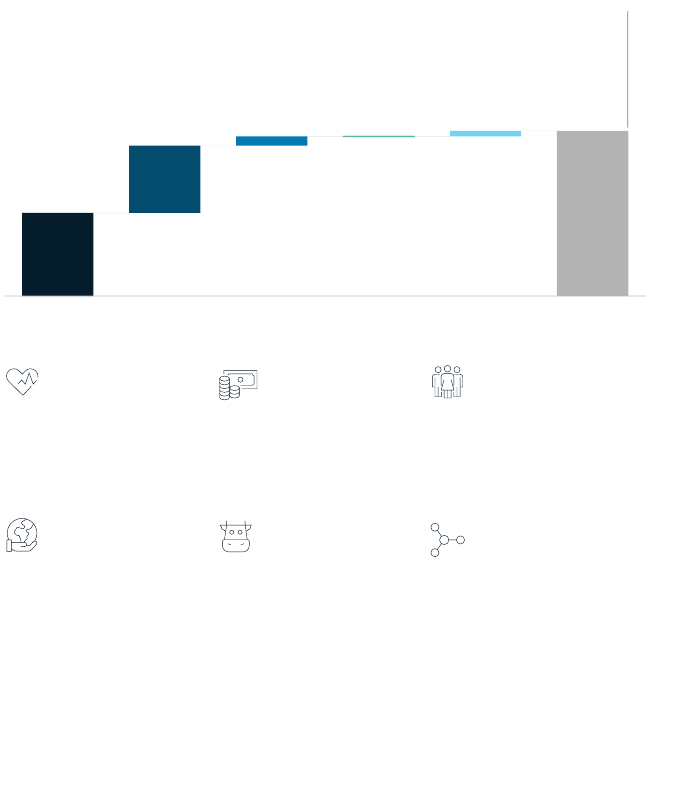

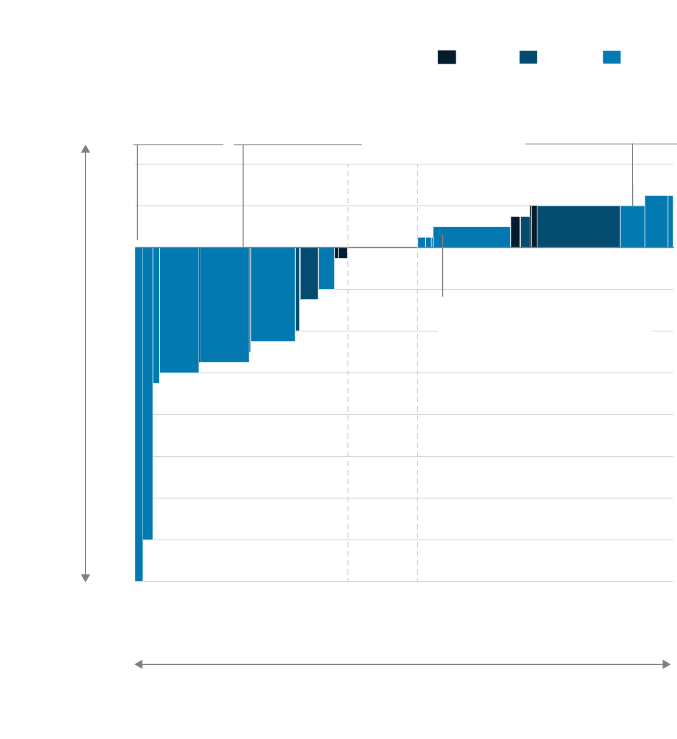

1.8%

4.2%

2018–202010–18

1.3x

Capital expenditure CAGR,¹ %

Source: McKinsey analysis of annual reports from grocery retailers

Grocers signicantly increased their capital spending to keep pace with a

changing ecosystem.

For a collection of 16 publicly traded hypermarkets and super centers, food retailers, and general merchandise stores.

Exhibit 1

Grocers significantly increased their capital spending to keep pace

with a changing ecosystem.

challenges among suppliers, retailers, and

consumers has increased these groups’

receptiveness to higher prices—a fortunate

development for retailers because no

single player can absorb the full magnitude

of price increases and remain protable. In

2021, grocery retailers raised prices even

while doing their best to mitigate costs.

One CEO noted, “Ination is exceeding

customer income growth. If cost increases

are just passed through, it will lead to lower

sales and prots and a greater migration

of customers to EDLP

4

grocers. It will be

critical to balance when to absorb the cost

ination versus passing some or all of it

through to optimize business performance

and retain customers.”

Greatly increased capital investment

The grocery ecosystem has begun to

change dramatically as new partnerships

and entrants have challenged the status

quo. Grocers increased their capital

4

Everyday low pricing.

9

State of Grocery North America

With continued uncertainty

around the COVID-19

pandemic and grocery ination

the highest it has been in ten

years, consumers have become

more focused on shopping for

the best value in an eort to

stretch their dollars.

1. Rise of the value-conscious,

healthier-eating consumer

With continued uncertainty around the

COVID19 pandemic and grocery ination

the highest it has been in ten years,

consumers have become more focused on

shopping for the best value in an eort to

stretch their dollars (Exhibit 2). Moreover,

90 percent of CEOs expect increasing

pricing pressure from consumers to

continue in 2022. When choosing where

to shop in the year ahead, 45 percent of

consumers indicate they plan to explore

more ways to save money, a level virtually

expenditures at an amount 1.3 times their

historical levels thanks in part to an inux of

funding (Exhibit 1). Consider that venture-

capital rms raised $10 billion for grocery

start-ups in the rst six months of 2021

alone. As investments continue to pour in,

we expect these enhanced capabilities to

disrupt the food ecosystem.

What’s ahead for 2022

Grocers will face ve trends that can broadly

be described by changing consumer tastes

and the responses necessary to keep pace

with them.

10 State of Grocery North America

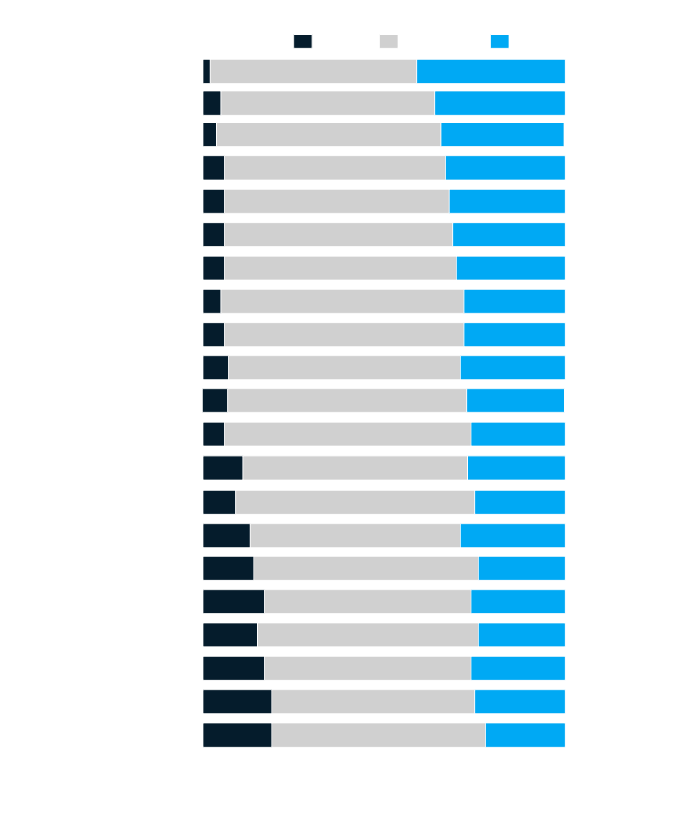

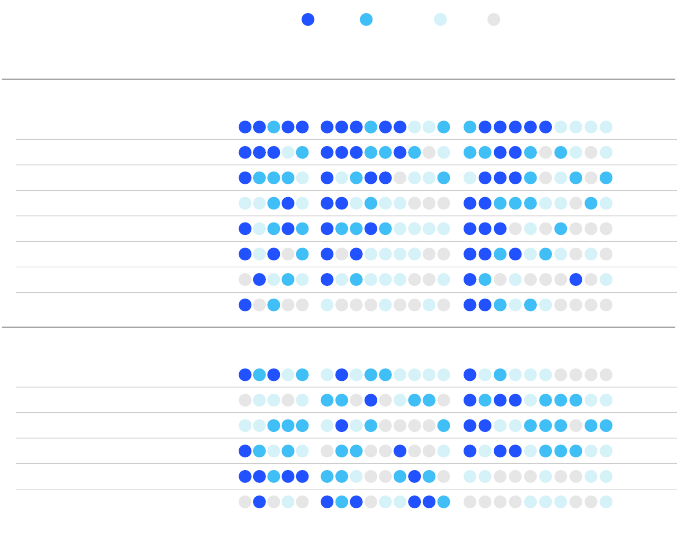

Grocery shopping attitudes

in 2021 vs 2020,

3

% change

+42

+21

+23

+11

–22

0

+38

+21

–7

–6

Grocery shopping attitudes

in 2022 vs 2021,

1

% change

Net intent,

2

%

+42

+17

+21

+13

–19

+1

+35

+22

–7

–4

3

10

8

8

29

16

4

4

27

21

52

63

63

71

61

67

57

70

53

62

45

27

29

21

10

17

39

26

20

17

Buy imported products

Buy groceries in large stores, where

I can buy everything in one place

Focus on healthy eating and nutrition

Buy food from fresh bars and deli

counters in stores

Actively research best promotions

Switch to less expensive products

to save money

Look for ways to save money

when shopping

Buy private-brand products

instead of known brands

Buy groceries online

Pay a higher price to get an

en

vironmentally friendly product

8

7

9

30

18

3

6

26

21

53

63

63

71

62

64

55

67

54

64

45

29

30

20

8

18

42

27

20

15

Buy groceries in large stores, where

I can buy everything in one place

Focus on healthy eating and nutrition

Buy food from fresh bars and deli

counters in stores

Buy private-brand products

instead of known brands

Buy imported products

Actively research best promotions

Look for ways to save money

when shopping

2

Switch to less expensive products

to save money

Buy groceries online

Interact with store employees at

ch

eckout vs self-checkout

Stay the same IncreaseDecrease

Source: State of Grocery Consumer Survey, November 19–December 7, 2021 (n = 3,007) and January 13–25, 2021 (n = 4,691); sampled

and weighted to match the US general population over 18 years old

In 2022, consumers will look for ways to save money while focusing on

healthier eating and nutrition.

Question: Think about 2022. Are you planning to do more, less, or about the same of the following?

Question: Which of the following statements best describes your attitudes toward grocery shopping in 2021 as compared with 2020?

Net intent is calculated by subtracting the percent of respondents stating decrease from the percent of respondents stating increase.

Exhibit 2

In 2022, consumers will look for ways to save money while focusing

on healthier eating and nutrition.

11

State of Grocery North America

unchanged from the year before. In

contrast, 29 percent intend to actively

research the best promotions more

frequently.

Consumers are balancing their emphasis

on value with an interest in healthier

foods. About 40 percent of consumers

expect to increase their focus on healthy

eating and nutrition. Consumers intend

to purchase more regional and local

goods (41 percent), high-protein options

(34 percent), and oerings that are free

from certain ingredients (33 percent),

along with other naturally healthy

options (Exhibit 3). This combination of

saving money and eating healthier, more

nutritious foods is more prevalent among

millennial and Gen Z consumers, in part

because they are still waiting for their

nances to return to normal.

The emergence of this younger, value-

conscious, and healthier eater in 2022

creates opportunities for grocers to tailor

their value-priced private-label products to

include healthier oerings.

2. Elevated consumer expectations

for omnichannel

Online buying is here to stay. Customer

preference for online and delivery orders

increased by around 50 percent during the

pandemic and is expected to rise further

in 2022 (Exhibit 4). Consumers continue to

be drawn to the convenience and relative

safety of online shopping, an attraction that

becomes even more appealing as delivery

costs decline and promotions increase.

The main barriers to online shopping are

consumer preferences for personal contact

in stores and expensive delivery charges,

The emergence of this

younger, value-conscious, and

healthier eater in 2022 creates

opportunities for grocers

to tailor their value-priced

private-label products to

include healthier oerings.

12 State of Grocery North America

though consumers are less concerned

about these issues today than they were

in 2020 (Exhibit 5). Consumers also prefer

home delivery when grocery shopping

online, marking a change from the

preference for click and collect in 2020.

To shift more spending to online,

successful grocers will invest to create a

more seamless, personalized experience.

Here are four key trends to keep in mind:

Spend preference by food type

in 2022 vs 2021,

1

% change

Net intent,

2

%

+39

+30

+27

+26

+25

+24

+23

+22

+22

+31

+20

+20

+16

+16

+16

+10

+9

+9

+9

+6

+3

4

6

6

6

6

5

6

7

5

6

7

11

13

9

14

17

15

17

19

19

57

62

61

62

63

64

67

66

64

59

68

66

62

58

66

62

57

61

57

56

59

41

34

33

32

31

30

28

28

29

36

26

27

27

29

25

24

26

24

26

25

22

Lactose free

Vegetarian

Gluten free

Products with low-emissions

footprint

Meat alternatives

Organic

Low fat

Animal welfare friendly

Packaging-free or

minimized packaging

Low calories

Uses 100% recyclable packaging

Low sugar

"Free from" environmentally

hazardous ingredients or materials

"Free from" articial ing

redients

High protein

Environmentally friendly

2

Dairy alternatives

Regional or local

Naturally healthy

Vegan

Halal products

IncreaseStay the sameDecrease

Source: State of Grocery Consumer Survey, November 19–December 7, 2021 (n = 3,007) and January 13–25, 2021 (n = 4,691); sampled and weighted to match

the US general population over 18 years old

Consumers expect to spend more money on food with specic attributes, such

as high protein and natural ingredients.

Question: Thinking about 2022, do you expect that you will spend more, the same, or less on following types of food products as compared to 2021?

Net intent is calculated by subtracting the percent of respondents stating decrease from the percent of respondents stating increase.

Exhibit 3

Consumers expect to spend more money on food with specific

attributes, such as high protein and natural ingredients.

13

State of Grocery North America

Customers expect a consistent value

proposition across online and in-store

channels. Shoppers are engaging in

omnichannel across a variety of shopping

missions—weekly grocery shopping and

midweek top-ups, for example—and they

expect similar assortments, pricing, and

promotions, among other factors, across

channels.

User experience on apps is becoming

more important. Consumers increasingly

value the ability to search for products

quickly and build their baskets while

shopping online. Winning grocers

have responded by investing in their

e-commerce capabilities and forging

partnerships with tech companies (for

example, Albertsons with Google) to

improve user experience.

Loyalty and personalization are more

important than ever. Grocers are improving

their share of wallet with omnichannel

shoppers by expanding their capabilities

in personalized promotions and product

recommendations.

Grocers are also experimenting with

shopper engagement in omnichannel. For

example, some are using mobile product

scanning to get product information.

In addition, scan-and-go commerce is

changing the way shoppers interact with

grocers both in stores and on apps.

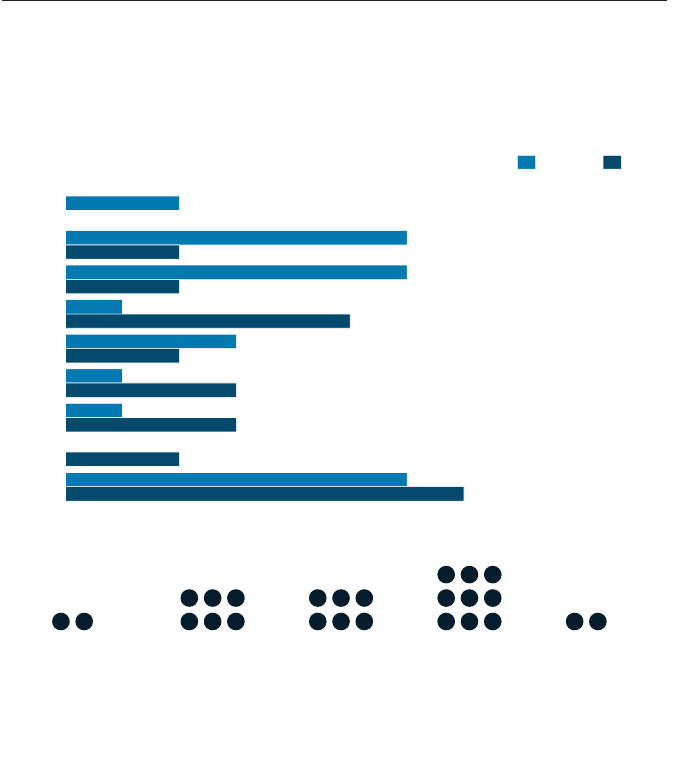

Online and delivery orders increased by about 50 percent during the pandemic

and are expected to rise further in 2022.

Source: State of Grocery Consumer Survey, November 19–December 7, 2021 (n = 3,007) and January 13–25, 2021 (n = 4,691); sampled and weighted to match

the US general population over 18 years old

Question: How did your preference to shop across the following channels change during the COVID-19 outbreak?

Question: In the next 12 months, do you expect to shop more, less, or the same in the following channels?

Net intent is calculated by subtracting the percent of respondents stating decrease from the percent of respondents stating increase.

Consumer expectations for

channel change in 2022,

2

% change

+4

+5

+2

0

Consumer channel change during

COVID-19 outbreak,

1

% change

Net intent,

3

% change

+42

+42

+41

–14

10

13

12

29

38

32

35

56

52

55

53

15

In a physical store or food market

Online (scheduled delivery)

Online (click and collect)

Instant delivery

IncreaseStay the sameDecrease

23

20

25

13

50

55

48

74

27

25

27

13

In a physical store or food market

Instant delivery

Online (scheduled delivery)

Online (click and collect)

Exhibit 4

Online and delivery orders increased by about 50 percent during the

pandemic and are expected to rise further in 2022.

14 State of Grocery North America

Grocers are also starting to see the upside

from omnichannel; the omnichannel

shopper spends two to four times more

than the in-store customer. Now the focus

has shifted from protecting in-store sales

to supporting business both online and in

stores through omnichannel excellence.

3. Increased emphasis on sustainability

Several developments—the success of the

UN Climate Change Conference (COP26)

in Glasgow, the dip in emissions at the

beginning of the pandemic, and the uptick

in climate-related natural disasters—have

made many consumers more aware of

the consequences of their purchasing

behaviors. This emergence of socially

conscious consumers is forcing Fortune

500 companies to act.

Companies beyond those known for their

environmental, social, and governance

(ESG) policies—such as Ben & Jerry’s,

FedEx, and LEGO—are increasingly

making more decisions based on social

and environmental issues compared with

2020. In our survey, grocery CEOs largely

expect consumers in 2022 to place a

Cost, quality, and merchandising authority are keys to increasing grocery

e-commerce.

Quality and freshness of food remain obstacles for consumers in online grocery shopping

Source: State of Grocery Consumer Survey, November 19–December 7, 2021 (n = 3,007) and January 13–25, 2021 (n = 4,691); sampled and weighted to match

the US general population over 18 years old

Question: What prevents you from buying groceries online more frequently? Indicate all applicable reasons.

Factors preventing consumers from buying

groceries online more frequently,

1

%

Change

in

2021, %

–15

–14

–3

–1

+1

–6

0

–1

–4

–1

31

25

21

17

16

14

13

10

10

10

The possible delivery times

are unsuitable for me

The selection is not

large enough

The minimum order values

are too high for me

Too often I receive products that have

not been ordered or that are damaged,

or there are products missing on delivery

My desired products are

not available

Dicult to nd products

I am looking for

I prefer personal contact

in stores

The products are too

expensive for me

Quality and fresh

ness of

fresh foods not sucient

The delivery charges are

too expensive for me

Exhibit 5

Cost, quality, and merchandising authority are keys to increasing

grocery e-commerce.

15

State of Grocery North America

greater emphasis on sustainability across

all dimensions (for example, packaging and

supply chain) and make dierent choices

because of it.

The industry has experienced a

groundswell of interest and activity

(Exhibit 6). Five years ago, Walmart was

the only retailer with ESG targets based

on public science; today, grocers, apparel

manufacturers, quick-service restaurants,

and stores of all formats are seeking

assistance with their ESG strategies. For

example, Kroger aims to end hunger and

eliminate waste in its communities by 2025,

and Albertsons has committed to making

100 percent of its Own Brands packaging

recyclable, reusable, or industrially

compostable by 2025.

5

Many retailers

recognize the connection between Scope

3 emissions (the result of activities from

assets beyond a company’s operations,

such as vendors) and a global supply

chain and are, accordingly, reevaluating

operations and ESG simultaneously to

enhance resilience while decreasing their

carbon footprint.

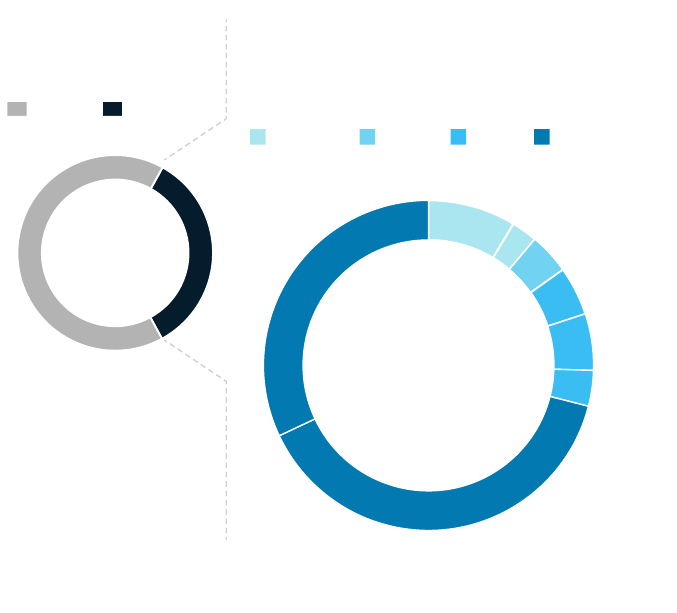

Global retailers with public science-based

targets, number of retailers

Source: McKinsey analysis

The emergence of socially conscious consumers is compelling Fortune 500

companies to act.

Companies are engaging with the public on environmental, social, and governance (ESG) factors at scale

76%

of consumers buy or boycott

brands based on values

$30 trillion

sustainably invested globally,

up 10 times from 2004

>75%

of global GDP is generated

in countries with net-zero

carbon mandates in law or

policy development

44%

of Fortune 500 companies

are integrating ESG into

core business strategy

1

4

18

41

2020201920182017

Exhibit 6

The emergence of socially conscious consumers is compelling

Fortune 500 companies to act.

5

“Kroger celebrates zero hunger | Zero waste momentum in 2020,” Kroger, April 20, 2021; “Plastics & packaging,”

Albertsons, accessed May 5, 2022.

16 State of Grocery North America

4. Strategic workforce planning and

investment in tech and analytics

Automation and AI will aect millions of

jobs in the coming years, and retail is

one of the most susceptible industries:

for example, 54 percent of current work

activities in retail can be automated. By

2030, estimates suggest retail could

capture 35 percent of this automation

potential, resulting in the displacement

of approximately six million full-time

employees.

6

Leading organizations have already made

bold bets to keep pace with changing

workforce requirements. Several

organizations are leading the way in eorts

to reskill their employees:

Kroger has a tuition reimbursement

program that oers up to $21,000 to

part- and full-time associates. More than

6,000 associates have beneted from this

program.

7

Giant Food Stores partnered with Central

Penn College to oer a $1,000 scholarship

for its employees to attend the college.

Giant also provides $5,250 a year in tuition

reimbursement to full-time associates.

8

Publix oers varying levels of tuition

reimbursement for education options that

enhance an employee’s ability to perform

in a current or future role, ranging from

$4,400 for two-year community colleges

to a total of $16,000 for four-year colleges

and universities.

9

Walmart has invested $5 billion in a range

of upskilling initiatives. For example,

employees can earn college credits online

through the company’s Live Better U

program. Tenured employees can take

part in the Walmart Academy—dedicated

locations near Walmart Supercenters that

oer two to six weeks of training to support

career advancement. In scal year 2021

alone, 95,000 associates were trained via

the Walmart Academy. In addition, Walmart

and the Walmart Foundation have invested

more than $100 million in the broader

“retail opportunity” ecosystem.

10

Amazon provides free education to

employees through its Career Choice

program—part of the company’s $1.2 billion

commitment to upskill more than 300,000

employees for in-demand elds through its

AWS Grow Our Own Talent, Surge2IT, and

the User Experience Design and Research

Apprenticeship programs, for example.

11

5. Growing importance of ecosystems

and partnerships

Margin pressure for grocers will likely

continue through 2022, forcing business

leaders to search for growth beyond the

core. Grocers have signicant loyalty from

their core customers and a treasure trove

of customer data. They can use these

advantages to build broader ecosystems

that improve the overall nancial prole

of their business. We expect grocers to

pursue three main ecosystem strategies

in 2022:

6

McKinsey Global Institute analysis.

7

“The Kroger family of companies to hire 10,000 associates,” Kroger, June 7, 2021.

8

“Giant Food Stores partners with Central Penn College,” Central Penn College, October 7, 2019.

9

“Tuition reimbursement,” Publix, accessed May 5, 2022.

10

PrepScholar blog, “Walmart’s Live Better U: Reviews and requirements,” blog entry by Ashley Robinson,

College Entrance Examination Board, November 14, 2021; “What is a Walmart Academy? How they’re building

confidence and careers,” Walmart, April 17, 2017; 2020 Environmental, social and governance report, Walmart,

2020.

11

“Amazon boosts upskilling opportunities for hourly employees by partnering with more than 140 universities and

colleges to fully fund tuition,” Amazon, March 3, 2022.

17

State of Grocery North America

Partner with tech companies to modernize

operations and enhance capabilities.

For instance, microfulllment center

technology players such as Swisslog and

Takeo Technologies are collaborating

with grocers Ahold Delhaize and HEB,

respectively. Google and Microsoft are

also forging partnerships with grocers

to introduce AI in replenishment and

commerce (for example, implementing

online tools to enable consumers to build

grocery shopping lists).

Join forces with delivery companies for

cost eciencies and e-commerce reach.

Beyond Instacart, Shipt is expanding

its engagements with grocers, while

DoorDash has partnerships with Smart &

Final, Meijer, Fresh Thyme, and Albertsons,

among others.

Create new and innovative value

propositions to customers. In Europe,

Morrisons has partnered with Deliveroo to

oer a ten-minute grocery delivery service

called Deliveroo Hop, while Albert Heijn

is expanding its “to go” format across BP

retail sites. In the United States, Kroger is

doubling down on prepared meals through

its partnership with Kitchen United.

Ecosystems are not only for the largest

grocers to pursue; midsize and regional

grocers can also participate by taking a

nonleading role or nding a niche to own.

Priorities for 2022

The year ahead is already full of challenges.

Leading grocers will be dened by the

dierentiation, innovation, and defensibility

of their strategies. As executives consider

Ecosystems are not only for

the largest grocers to pursue;

midsize and regional grocers

can also participate by taking

a nonleading role or nding a

niche to own.

18 State of Grocery North America

Bill Aull is a partner in McKinsey’s Charlotte office; Becca Coggins and Sajal Kohli are senior

partners in the Chicago office, where Eric Marohn is a consultant.

The authors would like to thank Cara Aiello and Karina Huerta for their contributions to this article.

Copyright © 2022 McKinsey & Company. All rights reserved.

their course and priorities for 2022, they

should address several questions:

1. Changing consumer habits are here

to stay. How will you pivot—and

continue to pivot—to cater to these

evolving needs?

2. Omnichannel is table stakes. How

will you continue to build your digital

and advanced-analytics capabilities

to achieve omnichannel excellence?

3. ESG is gaining importance, and

consumers are voting with their

feet. Where are you with your

commitments?

4. Talent will remain under pressure.

Do you have a model in place to

attract and replace those leaving

the industry?

5. Forward-thinking partnerships are

proliferating. Are you creatively

looking to push capabilities in the

face of new competitors?

Grocery executives that can successfully

navigate these ve issues will be poised for

better performance in the years ahead.

19

State of Grocery North America

The next horizon

for grocery e-commerce:

Beyond the pandemic bump

Consumers will increasingly shop for groceries online in the years ahead.

Retailers must make a series of strategic investments to keep pace.

© Edwin Tan/Getty Images

This article is a collaborative eort by Vishwa Chandra, Prabh Gill, Sajal Kohli, Varun Mathur, Kumar

Venkataraman, and Janice Yoshimura.

20 State of Grocery North America

Over the past 24 months, e-commerce

in the North American grocery industry

has continued to mature and scale. The

pandemic served as an accelerator for

grocery e-commerce, with much of the

sector experiencing the equivalent of

more than ve years of growth in just

ve months.

1

We recently completed extensive research

that included surveys of grocery CEOs,

functional and operations executives,

and consumers (see sidebar, “About

the research”). Our surveys conrmed

that consumers will continue to favor

e-commerce as one of many ways to shop.

However, many grocers don’t believe they

have the necessary capabilities to manage

this channel. In this article, we examine

the actions organizations must take to win

in e-commerce.

E-commerce takes hold

The industry is now on the edge of the next

transformation in e-commerce: grocery

executives expect e-commerce penetration

to more than double for their own

organizations in the next three to ve years,

to an average of 23 percent (Exhibit 1).

Source: Grocery Retail B2B Survey, February 2022, n = 25

Surveyed experts expect grocery e-commerce penetration to double in the

next ve years.

Question: What was your organization’s level of e-commerce penetration as a percentage of total sales in the last year (2021)?

Question: What do you think the maximum e-commerce penetration rate as a percentage of total sales for your organization will be in the next 5 years?

Respondents self-identied as from mass markets, specialty, and small-assortment retailers reporting more than 40% e-commerce penetration today are

expected to skew overly bullish given assortment in nongrocery items. These respondents potentially considered both grocery and nongrocery goods in their

forecasts.

Question: When do you believe this maximum penetration rate will be achieved in the industry?

Respondent organization e-commerce penetration,

historical

1

and anticipated

2

share of total revenue, %, n = 25

8

12

8

12

20

4

8

24

4

0

26–30%

24

8

21–25%

8

16–20%

28

11–15%

6–10%

0–2%

31–35%

4

12

24

Greater

than 35%

0

3–5%

ForecastHistorical

11%

Reported average

e-commerce

penetration, 2021

3

23%

Average forecast

e-commerce penetration

in 5 years

3

Expected time frame for industry e-commerce peak,

4

number of respondents, n = 25

This year 2–3 years 4–5 years 6–10 years 10+ years

Exhibit 1

Surveyed experts expect grocery e-commerce penetration to double

in the next five years.

1

“Disruption and uncertainty: The state of grocery retail 2021North America,” McKinsey, July 2021.

21

State of Grocery North America

Executives are even more bullish on

e-commerce’s upside potential, noting

that penetration could nearly triple to as

high as 35 percent (nearly $600 billion

versus about $150 billion at 11 percent

penetration). Our research suggests

continued support for e-commerce from

consumers, who indicated a positive net

intent to buy more groceries online (click

and collect as well as delivery) in 2022

(Exhibit 2).

The main drivers of e-commerce’s

growth during COVID19 were safety and

convenience, but our research found

consumers also value the channel’s unique

features—such as product comparisons,

assortment, and personalized promotions.

Source: State of Grocery Consumer Survey, November 19–December 7, 2021, n = 3,007, sampled and weighted to match the US general population 18+ years

Online and delivery orders increased by about 50 percent during the COVID-19

outbreak and are expected to rise further in 2022.

Question: How did your preference to shop across the following channels change during the COVID-19 outbreak?

Question: In the next 12 months, do you expect to shop more, less, or the same in the following channels?

Net intent is calculated by subtracting the percent of respondents stating decrease from the percent of respondents stating increase.

Consumer expectations for

channel change in 2022,

2

% change

+4

+5

+2

0

Consumer channel change during

COVID-19 outbreak,

1

% change

Net intent,

3

% change

+42

+42

+41

–14

10

13

12

29

38

32

35

56

52

55

53

15

In a physical store or food market

Online (scheduled delivery)

Online (click and collect)

Instant delivery

IncreaseStay the sameDecrease

23

20

25

13

50

55

48

74

27

25

27

13

In a physical store or food market

Instant delivery

Online (scheduled delivery)

Online (click and collect)

Exhibit 2

Online and delivery orders increased by about 50 percent during the

COVID-19 outbreak and are expected to rise further in 2022.

About the research

To get a better sense of

e-commerce trends in North

American grocery, McKinsey

conducted research on retailers

and consumers. In January and

February 2022, we surveyed

31 CEOs as well as 25 C-level

executives, directors, and vice

presidents. Our team augmented

these results with extensive

insights from surveys conducted

in 2021 among consumers in the

United States (4,691 respondents),

Mexico (1,005), and Canada (967).

22 State of Grocery North America

In parallel, consumers increasingly prefer

home delivery (a rise from 48 percent in

December 2020 to 63 percent a year

later, which translates to an approximately

$100 billion market today) and appreciate

its product and service enhancements,

including speed, reliability, assortment

breadth, and exibility (Exhibit 3).

We are also seeing consumers

demonstrate dierent preferences for

how their digital orders are lled based

on need and occasion, a shift that reects

continued maturity in consumers’ approach

to online grocery (Exhibit 4). Their use

of dierent options based on occasion

Source: State of Grocery Consumer Survey, November 19–December 7, 2021, n = 3,007; US Online Grocery Consumer Survey, December 10–December 17,

2021, n = 2,007, September 18–23, 2020, n = 1,014 , sampled and weighted to match the US general population 18+ years

Consumers have shifted from click and collect to home delivery.

Question: Which mode of shopping for food online do you prefer?

Question: Rank 1 reason for preference of home delivery.

Consumer preferences for online food shopping,

1

%

37

52

50

63

48

50

Sept 2020

Dec 2020

Dec 2021

47

16

12

9

9

7

47

18

12

10

6

7

33

19

16

11

12

10

I have been able to get an appointment

for delivery easier/quicker than for

click and collect

Home delivery is more reliable for on-time

order fulllment/I have experienced

delays in click and collect

Home delivery is more convenient/

I do not need to drive to store

Home delivery gives better products,

especially for my fresh and frozen foods

Home delivery oers me exibility/

I don’t need to be physically presen

t for

the order to be delivered

Home delivery is faster to fulll my order

vs click and collect

Dec 2020 Dec 2021Sept 2020

Top reasons for preferring home delivery,

2

%

Click and collect Home delivery

Exhibit 3

Consumers have shifted from click and collect to home delivery.

23

State of Grocery North America

Source: State of Grocery Consumer Survey, November 19–December 7, 2021, n = 3,007, January 13–25, 2021, n = 4,691, sampled and weighted to match the

US general population 18+ years

Consumers are moving beyond convenience and safety, the primary drivers of

online shopping during COVID-19.

Question: Why do you shop for groceries online?

Question: You will now see some factors that might make buying food online more attractive to you. Please select up to 3 most attractive factors.

Factors that would make online grocery shopping more attractive to online shoppers,

2

%

Change vs

2020

–10

–6

+5

–9

+2

+3

+4

Factors driving consumers to online grocery shopping,

1

%

29

26

23

19

18

17

16

13

13

13

12

12

12

11

11

10

7

3

Other

Additional features that make shopping easier

There are always new brands/products to try

I can set up recurring orders/save my favorite items

I nd the quality is better than elsewhere

Products are always in stock

I like being able to read product reviews before I buy

I generally prefer to shop online

The range of products is better

It is easier to nd the items I need

I like the conve

nience of having products delivered

I like that I can get products delivered

The prices are cheaper

It saves me time/eort going into store

I can shop when it is convenient for me (eg, 24/7)

It is easier to compare products

There are more oers/promotions

It is safer than shopping in store during COVID-19

47

42

32

28

20

15

14

More precise delivery windows

Faster delivery

Possibility to receive grocery delivery

without having to be present

Lower delivery costs

Lower minimum order values

Delivery also at o-peak times

More promotions

Exhibit 4

Consumers are moving beyond convenience and safety, the primary

drivers of online shopping during COVID-19.

24 State of Grocery North America

(Exhibit 5) compels retailers to oer a full

portfolio of e-commerce options (such

as same-day delivery, two-hour delivery,

instant delivery, and click and collect). As

demand spreads across dierent trips, the

result is smaller baskets.

This degree of channel shifting within the

grocery sector has precedents. Over the

past couple of decades, the emergence

and adoption of new oerings and

channels have spurred signicant changes

in consumer behavior. For example, the rise

of mass merchants with 150,000-square-

foot stores created a dierent in-store

experience than the one oered by the

traditional neighborhood store. The mass-

merchant category now accounts for

about 26 percent of the market. Similarly,

club retailers encouraged consumers

to buy in bulk, and the rapid growth of

discount and value grocery, featuring a

predominantly private-label oering, deed

the conventional wisdom that consumers

wanted only consumer-packaged-goods

(CPG) brands. Each of these “new”

oerings has been accompanied by

changing consumer behavior.

Source: State of Grocery Consumer Survey, November 19–December 7, 2021, n = 3,007, sampled and weighted to match the US general population 18+

years

Consumers are starting to demonstrate dierent behaviors

by occasion and need.

Question: What share of your monthly grocery budget is spent on the following types of occasions?

Question: What do you typically do when you need to get food on the following occasions? Respondents could select up to two options per occasion.

Consumer monthly grocery spend,

1

%

80

79

71

78

15

17

15

18

7

8

17

8

4

2

3 3

Shop for a

specic item

Buy the meal

for that day

Shop for a

few items

Stock up

Order delivery from

online retailer

Order click and collect

Order instant deliveryGo to store or food market

Consumer behavior when making various types of grocery trips,

2

%

24

41

16

19

Stock up

Shop for a specic item

Buy the meal for that day

Shop for

a few items

Exhibit 5

Consumers are starting to demonstrate different behaviors by

occasion and need.

25

State of Grocery North America

Keeping pace with

e-commerce growth

As consumers have shifted toward

e-commerce, two-thirds of retailers

don’t feel well prepared to meet the dual

challenges of delivering on growth while

achieving protability. Our research

revealed that retailers feel some

trepidation. Two-thirds of respondents

expect to lose some share in the shift

to digital, and more than half believe it

will be dicult to attract the necessary

talent to support digital growth (Exhibit 6).

Meanwhile, grocers are considering how

to allocate capital across multiple parallel

eorts, including supply chain resilience,

store remodels, digitalization, and talent

acquisition.

To enhance their capabilities in the

short term, grocers have responded by

implementing three specic strategies.

First, some grocers are building

partnerships with technology companies.

To expand fulllment capabilities, grocers

such as Ahold Delhaize, Wakefern, and

HEB have partnered with microfulllment

center (MFC) technology players like

Dematic, Takeo Technologies, and

Swisslog. Google and Microsoft are

also working with grocers to introduce

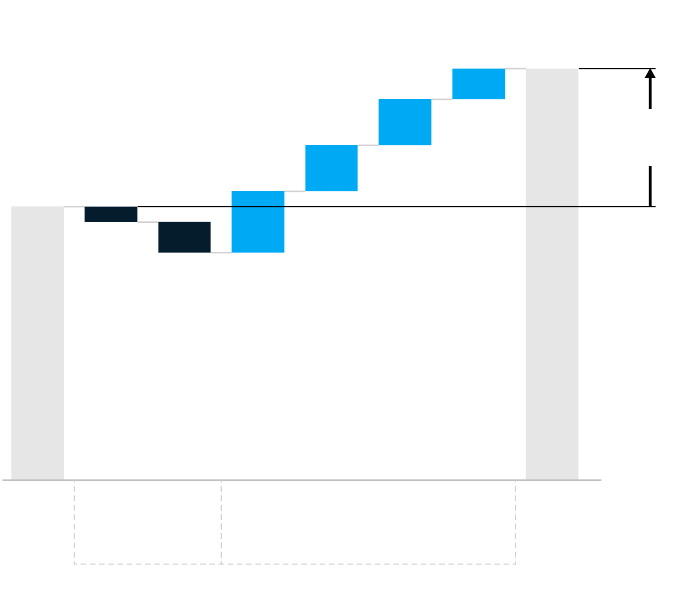

Source: Grocery Retail B2B Survey, February 2022, n = 25

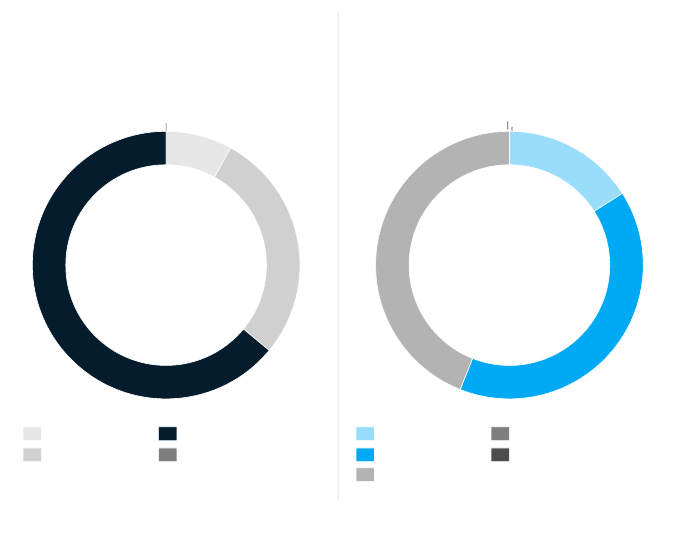

Retailers are not prepared for the shift to digital, and they are limited in their

ability to attract the talent needed to capture this opportunity.

Retailer preparedness for the shift to

digital, %, n = 25

How dicult will it be for your organization to attract the

necessary technical talent to support digital capability-

building in the next 5 years?

8

28

64

0

Do you feel that your organization is prepared for the

transition toward more digital commerce?

16

40

44

0

0

Not prepared at allWell prepared

Somewhat well preparedVery well prepared

Somewhat dicult

Very dicult Not at all dicult

My organization already has

the necessary technical talen

t

Dicult

~2 of 3

Respondents expect

to lose some share

in the shift to digital

55%+

Believe it will be

dicult or very

dicult to attract

the necessary talent

Diculty to attract talent, %, n = 25

Exhibit 6

Retailers are not prepared for the shift to digital, and they are limited

in their ability to attract the talent needed to capture this opportunity.

26 State of Grocery North America

articial intelligence in replenishment

and commerce (for example, to enable

consumers to build grocery lists while

shopping online).

Second, grocers continue to rely on third

parties to manage costs and expand their

e-commerce oerings. Instacart became

a leader through its early market entry,

but it has been joined by players such as

Shipt and DoorDash. The latter handles

fulllment for Albertsons, alongside

Instacart and Uber. Grocers are also using

partnerships to provide new and innovative

value propositions to customers. In Europe,

for example, Morrisons has partnered with

Deliveroo to make deliveries in as little as

ten minutes.

Last, the shift to e-commerce is also

challenging how retailers think about

capabilities across the e-commerce value

chain, from in-store digitalization and

pricing and promotion to trade spending

and media and advertising. The role of

the store will continue to be signicant,

with grocers investing in digitalization

to improve the in-store experience for

consumers—for example, through self-

checkout and grab and go.

How grocers can win in

e-commerce—delivering on

both growth and protability

To excel in the next horizon of e-commerce,

grocers need to develop an integrated

value proposition that meets consumer

needs while protecting their own

protability.

Our research found consumers are looking

to save money, be healthier, build on

their (rediscovered) joy of cooking, and

nd the best promotions more easily. For

each of these needs, an evolved digital

presence (both app- and web-based) can

help grocers highlight their assortment,

personalize their promotions, and

engage consumers in a more meaningful

To draw more consumers to

e-commerce, retailers must

oer lower costs, reduce

minimum order requirements,

protect quality and freshness,

and enhance the breadth

and discoverability of their

assortments.

27

State of Grocery North America

manner—something that a purely

brick-and-mortar oering cannot do.

Organizations, especially retailers that

have underinvested in the past, are

planning to make aggressive investments

in their digital capabilities to support

these tasks.

However, simply redening the value

proposition will not be enough. To draw

more consumers to e-commerce, retailers

must oer lower costs, reduce minimum

order requirements, protect quality and

freshness, and enhance the breadth

and discoverability of their assortments

(Exhibit 7).

To deliver on the dual objective of growth

and protability, grocers need to take a

range of simultaneous actions:

Engage customers meaningfully in

their omnichannel journeys and invest

in user experience

Omnichannel has become table stakes.

After spending the past few years building

this core oering, grocers are now

focusing on retention eorts by forging

personal relationships with customers to

increase basket size through upselling

and increased frequency of trips, both

Source: State of Grocery Consumer Survey, November 19–December 7, 2021, n = 3,007, January 13–25, 2021, n = 4,691, sampled and weighted to match the

US general population 18+ years

Cost, quality, and merchandising authority are the keys to increasing

grocery e-commerce.

Question: What prevents you from buying groceries online more frequently? Indicate all applicable reasons.

Quality and freshness of food remain obstacles for consumers in online grocery shopping.

Factors preventing consumers from buying

groceries online more frequently ,

1

%

Change vs

2020, %

–15

–14

–3

–1

+1

–6

0

–1

–4

–1

31

25

21

17

16

14

13

10

10

10

The possible delivery times

are unsuitable for me

The selection is not

large enough

The minimum order values

are too high for me

Too often I receive products that have

not been ordered or that are damaged,

or there are products missing on delivery

My desired products are

not available

Dicult to nd products

I am looking for

I prefer personal contact

in stores

The products are too

expensive for me

Quality and fresh

ness of

fresh foods not sucient

The delivery charges are

too expensive for me

Exhibit 7

Cost, quality, and merchandising authority are the keys to increasing

grocery e-commerce.

28 State of Grocery North America

online and in store. Grocers are also

experimenting with new ways to engage

shoppers in omnichannel. For example,

mobile scan–based product information

and scan-and-go commerce are changing

the way shoppers interact with grocers

in-store and on apps. Establishing and

maintaining a social connection with

consumers and reaching out daily will

be important for grocers hoping to move

from share of stomach to share of mind. A

social-rst, video-rich capability will also be

a must-have. E-grocer Weee, for example,

which specializes in products for Asian

and Hispanic shoppers, uses gamied,

video-rich social media oerings to nurture

a highly engaged customer base.

The convergence of value propositions

across the industry is raising the bar

on user experience in e-commerce.

Consumers increasingly value the ability

to nd products quickly and build their

baskets while shopping online. Grocers are

responding by investing in e-commerce

capabilities and forming partnerships

with technology companies to improve

the user experience. For example,

Albertsons and Google have partnered

to create in-store shoppable maps with

dynamic hyperlocal features, AI-powered

conversational commerce, and predictive

grocery-list building.

At the same time, retailers must enhance

the in-store experience through continued

investments in store technology. Solutions

include self-checkout, digital shelf tags,

and payments innovation to improve

personalization and eciency.

All of these oerings will have the dual

objective of enabling growth while

increasing protability. However, focused

investments will be needed to build both

the talent bench and the core technology

infrastructure. Successful grocers will

seek to attract the right talent to their

organizations and address the legacy

technology debt from the past couple

of decades.

Successful grocers will seek to

attract the right talent to their

organizations and address the

legacy technology debt from

the past couple of decades.

29

State of Grocery North America

Build a distinct—but connected—

capability in e-commerce category

management

Because e-commerce is set to account

for a signicant share of overall business,

retailers are starting to be more deliberate

about standing up channel-specic

management capabilities and getting

sharper on assortment choices (breadth

and depth, online versus oine), pricing,

and online-only promotions, among other

factors. Grocers need to make investments

in data, analytics, and IT infrastructure to

get a deeper understanding of their online

business performance—for example,

the eectiveness of online promotions

and digital shopping trends by consumer

segment. They must also dedicate

resources to building their organizational

muscle through eorts such as upskilling

merchants. These capabilities should be

integrated into a broader omnichannel

category management strategy, which

can provide a holistic and thoughtful

merchandising experience anchored in a

single view of the customer.

As consumers continue the shift toward

buying through mobile apps, grocers

are starting to use the full suite of

e-merchandising levers—such as product

placement, product recommendations,

personalized promotions, and digital

media—to monetize their digital assets with

consumer goods companies. The launch of

retail media networks (such as Instacart’s

new Carrot Ads platform) allows retailers

to capture a greater share of marketing

spending from brands beyond what they

have traditionally captured. This source will

be a key driver of protability for grocers in

the coming years.

Making this shift will not be easy, and

our survey indicates that retailers

recognize this challenge. Retailers and

CPG companies have deep and complex

ways of optimizing trade promotions

and advertising in the brick-and-mortar

channel. There are dozens of mechanisms

through which CPGs and retailers invest

in advertising and trade, and ROI is often

hard to track and measure. Both retailers

and CPGs will need to lean on digital

capabilities to optimize their investments

for greater impact on revenue

and protability.

Develop a portfolio of fulllment

options that are aligned to individual

markets’ needs

As demand for online grocery continues

to scale, grocers are going to have to

revisit how and where they fulll orders.

The network of the future for grocers will

encompass a mix of automated MFCs,

manual dark stores, and store fulllment.

Matching the right fulllment option to

each specic location based on a market’s

demand prole and service promise will

be critical.

Retailers are conducting pilots with

automated MFCs and manual dark stores.

Many grocers are now locating MFCs

close to their customers to improve

speed at a lower cost. Both aggregate

demand and consistency of demand are

key factors in ensuring ROI. Grocers are

also implementing centralized fulllment

centers to handle larger order volumes

and support next-day delivery in highly

concentrated geographies.

In parallel, grocers are experimenting

with new last-mile models (for example,

autonomous vehicles with precise

delivery slots) and tech-enabled logistics

optimization to lower costs while

maintaining service levels.

30 State of Grocery North America

While automation will be a key lever

for retailers to increase eciency and

speed, grocers will need to make at-scale

investments to build out a comprehensive

network along with a focused eort to drive

volume at each node. Since the benets of

automation will accrue to all participants

in the industry, there is an opportunity for

collaboration among grocers, technology

companies, marketplaces, and CPG

companies to rapidly scale these networks.

Use e-commerce as a way to innovate

and harness the broader ecosystem

Grocers are approaching e-commerce as

an opportunity to push the boundaries of

their current oerings. Some retailers are

deploying e-commerce to strengthen their

current assortments (for example, to push

private brands and prepared meals) and to

promote new oerings (such as meal kits,

partnerships with dark kitchens and local

restaurants, and expansion into catering

services to capture new meal occasions).

In response, grocers need to dene their

operating models to fully harness their

own capabilities while participating in

third-party ecosystems to serve customers

through dierent missions. Retailers should

also seek to engage consumers where they

are spending their time; whether on social

channels, on content sites (for example,

Eater magazine online), or in the metaverse,

grocers need to be there.

Grocers must also quickly determine

which components of their end-to-end

e-commerce value chain they want to

fully own as a core capability and what

partners can provide. The answer will vary

across the value chain as retailers assess

where they can compete with distinctive

oerings and where they have the requisite

capabilities and resources. Eciency and

speed will be critical factors in deciding

whether to invest in in-house solutions or

partner with a third party. The market is

likely to be segmented into large retailers

with the resources to develop ecient in-

house capabilities and smaller companies

that must rely on third parties.

Implications for other

industry players

While many of these recommendations

are applicable to all grocery players,

the rapid growth of e-commerce has

signicant additional implications for

various players within the broader

ecosystem. Besides Amazon, players such

as Cornershop by Uber and DoorDash

also oer marketplaces for shoppers.

Investments continue to pour into instant

delivery, with multiple players including

Instacart, Gopu, Gorillas, and JOKR now

testing and oering delivery in less than

30 minutes. More rst-party services are

also emerging: Gopu and DashMart by

DoorDash are now playing in this space

with their own warehouse-based grocery-

delivery models.

Digital-native third-party marketplaces

have notched signicant growth in the past

few years. They now have an opportunity

to use their technical capabilities to ensure

their retail partners have access to the best

digital technology and user experiences.

Another priority will be improving eciency

and reducing costs to customers through

the accelerated adoption of technology

(such as microfulllment), increased

batching of grocery e-commerce orders on

delivery milk runs, and shared resources

in delivery across vehicles and drivers.

Marketplaces can also unlock additional

value pools (such as advertising) that

used to ow to media players outside the

sector—for example, by luring spending

31

State of Grocery North America

from traditional media channels such as

television ads to grocery marketplace

advertising via retail media networks.

Pure-play, rst-party online grocers

have the opportunity to make headway

by deploying dierent delivery models

(such as a scheduled, milk-run approach),

expanding their oerings to address more

need states and occasions, and further

distinguishing themselves from traditional

competitors (for example, through

subscription models). They can also

dierentiate their oerings by assortment

authority (including breadth, depth, and

brands covered) and experiment with

adopting social-rst, video-rst oerings to

engage consumers.

Despite the substantial growth of online

grocery and the increased number of

players, the market truly is on the verge of

its next transformation. Executives should

recognize that the leaders of today are

not guaranteed to be winners tomorrow.

Retailers that take decisive action and

make strategic investments today will be

well positioned to carve out a protable

position for the future.

Vishwa Chandra is a partner in McKinsey’s San Francisco office, Prabh Gill is an associate

partner in the Vancouver office, Sajal Kohli is a senior partner in the Chicago office, where

Kumar Venkataraman is a partner and Janice Yoshimura is a consultant; Varun Mathur is an

associate partner in the Austin office.

Copyright © 2022 McKinsey & Company. All rights reserved.

32 State of Grocery North America

Tech-enabled grocery

stores: Lower costs,

better experience

Grocers must reimagine physical stores to keep pace with consumer

preferences. Technology will be a critical enabler in this shift.

© SDI Productions/Getty Images

by Tyler Harris, Alexandra Kuzmanovic, and Jaya Pandrangi

33

State of Grocery North America

The past year continued to reveal the

ways in which the pandemic, evolving

customer preferences for grocery, and

macroeconomic trends have converged

to reshape the traditional role of

physical stores. As grocers seek to

adapt, technology can streamline store

operations—from checkout and talent

management to merchandising and

replenishment—and provide a better in-

store environment for customers, all while

helping to manage costs.

Stores under pressure

In many ways, the four-wall operating

model for grocery has changed only

incrementally over the past several

decades. However, four primary forces will

challenge long-held conventional wisdom

and compel grocers to adapt.

Stang shortages and rising labor costs.

About one million roles remain open in

the US retail industry, even with upgraded

incentives and benets such as year-end

bonuses for in-store employees and tuition

assistance.

1

As erce competition for

retail store employees has pushed wages

and benet costs higher, grocers have

responded by investing more in retention

and upskilling eorts.

Increased stockouts. While omnichannel

oerings have increased the complexity

of supply chains, broader shifts in the

economy have had a greater impact on

operational resilience and cost structures.

Logistics carriers continue to operate at

reduced capacity, with a declining supply

of container ships and overall capacity

down by 11 percent from September 2020

to June 2021.

2

These developments are

further squeezing the industry’s already-

tight margins. Our analysis shows that

the pandemic’s impact on retailers could

decrease EBITDA by 20 to 40 percent in

the near term, with 15 to 20 percentage

points of that decrease enduring if these

supply chain shocks go unaddressed.

Fluctuating foot trac. Lockdowns in the

early phases of the pandemic resulted

in a precipitous drop in foot trac, but

the grocery sector has rebounded. After

vaccines became widely available to the

public in spring 2021, foot trac increased,

even eclipsing prepandemic levels at times:

for example, foot trac was 7.6 percent

higher in December 2021 compared

with 2019.

3

Superstores illustrated a

similar trend in the latter half of the year,

although the shopping week that included

Thanksgiving and Black Friday was down

12.5 percent from 2019.

A shift from stores to e-commerce.

While all these factors are putting added

pressure on the role of stores, the capstone

trend is that e-commerce has increasingly

lured shoppers from traditional grocery

stores. The move toward convenience and

safety has fueled the rise of new delivery

models, blurring the strict boundaries of

the traditional store’s four walls. In the

next ve years, we estimate that 20 to 40

percent of grocery e-commerce volume

could be fullled from alternative locations.

Losing this volume will challenge the

economics of many stores. Consumers

who continue to shop in store are already

seeking a dierent experience: self-

checkout adoption has increased by

1

“Table A. Job openings, hires, and total separations by industry, seasonally adjusted,” Job Openings and Labor

Turnover Survey, US Bureau of Labor Statistics, May 3, 2022.

2

“Ten steps retailers can take to shock-proof their supply chains,” McKinsey, November 11, 2021.

3

Brin Snelling, “What 2021 foot traffic trends mean for the future of physical retail,” Forbes, December 22, 2021.

34 State of Grocery North America

almost 20 percent since the beginning of

the COVID19 pandemic, and 75 percent of

respondents who have started or increased

their use of self-checkout said they intend

to continue.

4

Using in-store technology to

improve customer experience

and reset cost structures

In light of these challenges, 2022 will be a

critical year for retailers to use technology

to future-proof their physical stores.

Many grocers and retailers have already

experimented with tech-enabled customer

experiences and store operations. The