Searching for the Reference Point

AURÉLIEN BAILLON, HAN BLEICHRODT, AND VITALIE SPINU

Erasmus School of Economics,

Erasmus University Rotterdam, The Netherlands

May 2017

Abstract

This paper explores empirically how people form their reference point in decision

under risk. Reference-dependence plays a key role in explaining people’s choices, but

reference-dependent theories, like prospect theory, leave the reference point

unspecified. We assume a comprehensive reference-dependent model that nests the

main reference-dependent theories and that allows isolating the reference point rule

from the other behavioral parameters. We estimate the (posterior) probability that

subjects use a specific reference point rule by Bayesian hierarchical modeling. Our

experiment involved high stakes with payoffs up to a weekly salary. The most common

reference points were the status quo and a security level (the maximum of the minimal

outcomes of the prospects in a choice). Twenty percent of the subjects used an

expectations-based reference point as in the influential theory of Köszegi and Rabin

(2006, 2007).

Key words: reference point formation, reference-dependence, Bayesian hierarchical

modeling, large-stake experiment.

JEL code: D81, C91.

1

Introduction

A key insight of behavioral economics is that people evaluate outcomes as gains and

losses from a reference point. Reference-dependence is central in prospect theory, the

most influential theory of decision under risk, and it plays a crucial role in explaining

people’s attitudes towards risk (Rabin 2000; Wakker, 2010). Evidence abounds, from

both the lab and the field, that preferences are reference-dependent.

1

A fundamental problem of prospect theory and other reference-dependent theories

is that they are silent about how reference points are formed. Back in 1952, Markowitz

(1952) already remarked about customary wealth, which plays the role of the reference

point in his analysis, that “It would be convenient if I had a formula from which

customary wealth could be calculated when this was not equal to present wealth. But I

do not have such a rule and formula (p.157).” This silence is undesirable as it creates

too much freedom in deriving predictions, making it impossible to rigorously test

reference-dependent theories empirically.

2

Reviewing the literature, more than 60

years after Markowitz, Barberis (2013) concludes that addressing the formation of the

reference point is still a key challenge to apply prospect theory to economics (p.192).

The leading theory of reference point formation was proposed by Köszegi and Rabin

(2006, 2007). They argue that the reference point is determined by people’s (rational)

expectations. Köszegi and Rabin’s model for the first time made the reference point

1

Examples of real-world evidence for reference-dependence are the equity premium puzzle, the

finding that stock returns are too high relative to bond returns (Benartzi and Thaler 1995), the

disposition effect, the finding that investors hold losing stocks and property too long and sell winners too

early (Odean 1998, Genesove and Mayer 2001), default bias in pension and insurance choice (Samuelson

and Zeckhauser 1988, Thaler and Benartzi 2004) and organ donation (Johnson and Goldstein 2003), the

excessive buying of insurance (Sydnor 2010, the annuitization puzzle, the fact that at retirement people

allocate too little of their wealth to annuities (Benartzi et al. 2011), the behavior of professional golf

players (Pope and Schweitzer 2011) and poker players (Eil and Lien 2014), and the bunching of

marathon finishing times just ahead of round numbers (Allen et al. forthcoming).

2

For example, different assumptions about the reference point are required to explain two well-

known anomalies from finance: the equity premium puzzle demands that the reference point adjusts over

time, whereas adjustments in the reference point weaken the disposition effect (Meng and Weng

forthcoming).

2

operational and gave testable implications. It is close in spirit to the disappointment

models of Bell (1985), Loomes and Sugden (1986), Gul (1991), and Delquié and Cillo

(2006) in which decision makers also form expectations about uncertain prospects and

experience elation or disappointment depending on whether the actual outcome is

better or worse than those expectations.

3

Empirical evidence on the formation of reference points is scarce and what is

available gives mixed conclusions. Some evidence is consistent with Köszegi and Rabin’s

model of expectations-based reference points (Abeler et al. 2011, Card and Dahl 2011,

Crawford and Meng 2011, Gill and Prowse 2012, Bartling et al. 2015), but other

evidence is not (e.g. Baucells et al. 2011, Allen et al. forthcoming, and Lien and Zheng

2015). Moreover, evidence that has been interpreted as supporting Köszegi and Rabin’s

model may not necessarily exclude other reference point rules.

4

Barberis (2013)

concludes that in finance there are “natural reference points other than expectations.”

Evidence from medical decision making suggests that, instead of using an expectations-

based reference point, people adopt the MaxMin rule described above to determine

their reference point (Bleichrodt et al. 2001, van Osch et al. 2004, van Osch et al. 2006).

This paper explores the formation of reference points in decision under risk. We

performed an experiment in Moldova, an Eastern European country, with large stakes

up to a weekly salary. Guided by the available literature, we specified six reference point

rules, including two expectations-based reference point rules, MaxMin, and the status

quo, which is often used as a reference point in experiments. The selected rules vary

depending on whether they are choice-specific (the reference points is determined by

3

Other models of reference point formation were proposed by Heath et al. (1999), who suggested

that people use goals as their reference points and by Diecidue and Van de Ven (2008), who presented a

model with an aspiration level, which is a form of reference dependence.

4

To illustrate, in the online Appendix we show that the data of Abeler et al. (2011) are also consistent

with MaxMin, a security-based rule according to which subjects adopt the maximum outcome that they

can reach for sure as their reference point.

3

the choice set) or prospect-specific (the reference point is determined by the prospect

itself), stochastic or deterministic, and on whether they are defined only by the outcome

dimension or by both the outcome and the probability dimension.

All the reference points that we consider can be identified through choices. Hence,

we work within the revealed preference paradigm and do not require introspective

data. In this we follow Rabin (2013) approach to develop more realistic theories that

are maximally useful to core economic research. Rabin argues that new models should

be “portable” and use the same independent variables as existing models. The core

economic model of decision under risk is expected utility, which uses probabilities and

outcomes as independent variables. Tversky and Kahneman’s (1992) prospect theory is

not portable because it leaves the reference point unspecified. By contrast, all our

reference point rules can be derived from probabilities and outcomes and are portable.

We define a comprehensive reference-dependent model that includes the main

reference-dependent theories as special cases. This makes it possible to compare

reference point rules ceteris paribus, i.e. to isolate the reference point rule from the

specification of the other behavioral parameters like utility curvature, probability

weighting, and loss aversion. We use a Bayesian hierarchical model to estimate each

subject’s reference point rule. Bayesian hierarchical modeling estimates the parameters

of each individual separately, but accounts for their similarities in the population. This

leads to more precise estimates and prevents inference from being dominated by

outliers (Rouder and Lu 2005, Nilsson et al. 2011).

Our results indicate that two reference point rules stand out: the status quo and

MaxMin. Together these two reference points account for the behavior of over sixty

percent of our subjects. Around twenty percent of our subjects use an expectations-

based reference point rule.

4

1. Theoretical background

A prospect is a probability distribution over money amounts. Simple prospects assign

probability 1 to a finite set of outcomes. We denote these simple prospects as

(

,

; … ;

,

), which means that they pay €

with probability

, = 1, … , . We

identify simple prospects with their cumulative distribution functions and denote them

with capital Roman letters (,). The decision maker has a weak preference relation

over the set of prospects and, as usual, we denote strict preference by , indifference by

, and the reversed preferences by and . The function defined from the set of

simple prospects to the reals represents if for all prospects , , ()

().

Outcomes are defined as gains and losses relative to a reference point . An outcome

is a gain if > and a loss if < .

1.1. Prospect theory

Under prospect theory (Tversky and Kahneman 1992), there exist probability

weighting functions

and

for gains and losses and a non-decreasing gain-loss

utility function : with

(

0

)

= 0 such that preferences are represented by

(

)

=

()

(1 )

+

( )

()

. (1)

The integrals in Eq. (1) are Lebesgue integrals with respect to distorted measures

(1 ) and

(). For losses, the weighting applies to the cumulative distribution

(), for gains to the decumulative distribution (1 ).

The functions

and

are non-decreasing and map probabilities into [0,1] with

(

0

)

= 0,

(

1

)

= 1, = +, . When the

are linear, reduces to expected utility

with referent-dependent utility:

(

)

=

(

)

. (2)

5

Equation (2) shows that reference-dependence by itself does not violate expected utility

as long as the reference point is held fixed.

Based on empirical observations, Tversky and Kahneman (1992) hypothesized

specific shapes for the functions ,

, and

. The gain-loss utility is S-shaped,

concave for gains and convex for losses. It is steeper for losses than for gains to capture

loss aversion, the finding that losses loom larger than gains. The probability weighting

functions are inverse S-shaped, reflecting overweighting of small probabilities and

underweighting of middle and large probabilities.

1.2. Köszegi and Rabin’s model

Tversky and Kahneman (1992) defined prospect theory for a riskless reference

point . Köszegi and Rabin (2006, 2007) added two elements to prospect theory. First,

they distinguished the economic concept of consumption utility and the psychological

concept of gain-loss utility and, second, they allowed for stochastic reference points. Let

be the stochastic reference point. In Köszegi and Rabin’s model preferences over

prospects are represented by

(

)

=

(

)

+

(

)

(

)

. (3)

In Eq. (3), represents consumption utility, which does not depend on the reference

point, but only on the absolute size of the payoffs. is the gain-loss utility function,

which depends on the reference point and reflects the psychological part of utility.

Köszegi and Rabin (2007, p.1052) argue that “for modest-scale risk, such as $100

or $1000,[…] consumption utility can be taken to be approximately linear”. Linear

consumption utility is also commonly assumed in empirical applications of Köszegi and

Rabin’s model (e.g. Heidhues and Kőszegi 2008, Abeler et al. 2011, Gill and Prowse

2012, Eil and Lien 2014). As the incentives in our experiment did not exceed $100 (in

6

PPP) and the prospects in the different choice sets had approximately equal expected

value, we concentrate on the gain-loss function and take

(

)

= :

(

)

=

+

(

)

. (4)

There is no probability weighting in Eq. (4). It is unclear how the rational

expectations reference point should be defined in the presence of probability weighting.

Köszegi and Rabin (2006, 2007) do not address this problem and leave out probability

weighting, even though they acknowledge its relevance (Köszegi and Rabin 2006,

footnote 2, p. 1137).

While prospect theory does not specify the reference point, Köszegi and Rabin

(2007) present a theory in which reference points are determined by the decision

maker’s rational expectations. They distinguish two specifications of the reference

point, one prospect-specific and one choice-specific. In a “choice-acclimating personal

equilibrium” (CPE), the reference point is the prospect itself. This prospect-specific

reference point gives:

(

)

=

+

(

)

. (5)

In a choice-unacclimating personal equilibrium (UPE), the reference point is choice-

specific and is equal to the preferred prospect in the choice set.

1.3. Disappointment models

Köszegi and Rabin’s (2006, 2007) model is close to the disappointment models of

Bell (1985), Loomes and Sugden (1986), Gul (1991), and Delquié and Cillo (2006). Bell’s

model is equivalent to Eq. (3) with () replaced by the expected consumption value of

the prospect (although Bell remarks that this may be too restrictive and also presents a

more general model), Loomes and Sugden’s model (1986) is equivalent to Eq.(3) with

7

() replaced by the expected consumption utility of the prospect,

5

and Gul’s (1991)

model is equivalent to Eq.(3) with () replaced by the certainty equivalent of the

prospect. Delquié and Cillo‘s (2006) model is identical to Köszegi and Rabin’s (2007)

CPE model (Eq. 5). Masatlioglu and Raymond (2016) formally characterize the link

between Köszegi and Rabin’s (2007) CPE model, the disappointment models, and other

generalizations of expected utility. They show that if the gain-loss utility function is

linear and the decision maker satisfies first-order stochastic dominance, CPE is equal to

the intersection between rank-dependent utility (Quiggin 1981, Quiggin 1982) and

quadratic utility (Machina 1982, Chew et al. 1991, Chew et al. 1994).

2.4 General reference-dependent specification

This paper compares the performance of different reference point rules in

explaining behavior. To isolate the reference point, we must use the same model

specification across all reference point rules and, consequently, all other behavioral

parameters must enter the same way. To address this ceteris paribus principle we adopt

the following general reference-dependent model:

(

)

=

+

(

)

. (6)

Eq. (6) contains prospect theory (Eq. 1), Köszegi and Rabin’s (2006, 2007) model

(Eq. 4) and the disappointment models as special cases. In Eq. (6), probability weighting

plays a role in the psychological part of the model (the second term of the addition), but

it does not affect consumption utility (the first term). This seems reasonable as

consumption utility reflects the “rational” part of utility and probability weighting is

usually considered irrational. Adjusting the model to also include probability weighting

in consumption utility is straightforward.

5

With consumption utility .

8

Probability weighting does not affect the formation of reference points either. In this

we follow the literature on stochastic reference points (Sugden 2003, Delquié and Cillo

2006, Köszegi and Rabin 2006, Köszegi and Rabin 2007, Schmidt et al. 2008). We will

consider alternative specifications in Section 6.4.

2. Reference point rules

A reference point rule specifies for each choice situation which reference point is

used. Table 1 summarizes the reference point rules that we studied. We distinguish

reference point rules along three dimensions. First, whether they are prospect-specific

and determine a reference point for each prospect separately, or choice-specific and

determine a common reference point for all prospects within a choice set. Second,

whether they determine a stochastic or a deterministic reference point. Third, whether

they use only the payoffs to determine the reference point or both payoffs and

probabilities.

Prospect Specific

Stochastic

Uses probability

Status Quo

Choice

No

No

MaxMin

Choice

No

No

MinMax

Choice

No

No

X at Max P

Choice

No

Yes

Expected Value

Prospect

No

Yes

Prospect Itself

Prospect

Yes

Yes

Table 1. The reference point rules studied in this paper

The first reference point rule is the Status Quo, which is often used in experimental

studies of reference-dependence. Our subjects knew that they would receive a

participation fee for sure. Consequently, we took the participation fee as the status quo

reference point and any extra money that subjects could win if one of their choices was

played out for real as a gain. Expected utility maximization is the special case of Eq.(6)

9

with the status quo as the reference point where subjects do not weight probabilities

(expected utility). Expected value maximization is the special case of expected utility

with the status quo as the reference point where subjects have linear utility.

MaxMin, the second reference point rule, is based on Hershey and Schoemaker

(1985). They found that when asked for the probability that made them indifferent

between outcome for sure and a prospect (,

; 1 ,

), their subjects took as

their reference point and perceived

as a gain and

as a loss. Bleichrodt et al.

(2001) and van Osch et al. (2004, 2006, 2008) found similar evidence for such a strategy

in medical decisions. For example, van Osch et al. (2006) asked their subjects to think

aloud while choosing. The most common reasoning in a choice between life duration

for sure and a prospect (,

; 1 ,

) was: “I can gain years if the gamble goes

well or lose if it doesn’t.”

MaxMin generalizes the above line of reasoning to the choice between any two

prospects.

6

It posits that in a comparison between two prospects, people look at the

minimum outcomes of the two prospects and take the maximum of these as their

reference point. This reference point is the amount they can obtain for sure. For

example, in a comparison between (0.50,100; 0.50,0) and (0.25,75; 0.75,25), the

minimum outcomes are 0 and 25, and because 25 exceeds 0, MaxMin implies that

subjects take 25 as their reference point.

MaxMin is a cautious rule and implies people are looking for security. MinMax is the

bold counterpart of MaxMin. A MinMax decision maker looks at the maximal

opportunities and takes the minimum of the maximum outcomes as his reference point.

6

To the best of our knowledge this rule was first proposed in Bleichrodt and Schmidt (2005). See also

Birnbaum and Schmidt (2010) and Schneider and Day (forthcoming).

10

Hence, MinMax predicts that the decision maker will take 75 as his reference point

when choosing between (0.50,100; 0.50,0) and (0.25,75; 0.75,25).

The MaxMin and the MinMax rules both look at extreme outcomes. One reason is

that these outcomes are salient. Another salient outcome is the payoff with the highest

probability and our next rule, X at MaxP, uses this outcome as the reference point. The

importance of salience is widely-documented in cognitive psychology (Kahneman

2011). Barber and Odean (2008) and Chetty et al. (2009) show the effect of salience on

economic decisions. Bordalo et al. (2012) present a theory of salience in decision under

risk.

The final two reference points that we considered are the expected value of the

prospect, as in the disappointment models of Bell (1985) and Loomes and Sugden

(1986)

7

and the prospect itself as in Köszegi and Rabin’s (2007) CPE model and Delquié

and Cillo’s (2006) disappointment model. Unlike the other reference points, these

reference points are prospect-specific. The prospect itself is the only rule that specifies a

stochastic reference point. If the prospect itself is the reference point then the decision

maker will, for example, reframe the prospect (0.50,100; 0.50,0) as a 25% chance to

gain 100 (if he wins 100 and 0 is the reference point, the probability of this happening is

0.50 0.50 = 0.25), a 25% chance to lose 100 (if he wins nothing and 100 is the

reference point) and a 50% chance that he wins or loses nothing (if he either wins 100

and 100 is the reference point or he wins nothing and nothing is the reference point).

The decision maker’s gain-loss utility is then

(.25)

(

100

)

+

(.25)

(

100

)

.

Two points are worth making. First, Köszegi and Rabin (2007) propose the CPE

model to describe choices with large time delays between choice and outcome, like for

example in insurance decisions. We use it outside this specific context, as did others

7

The equivalence with Loomes and Sugden (1986) follows because we assume

(

)

= .

11

before us (e.g. Rosato and Tymula 2016), because it is tractable, both theoretically and

empirically. Hence, our results do not directly test the CPE model the way it was

conceived. Second, we do not consider the rule that specifies that the preferred prospect

in a choice is used as the reference point, as in Köszegi and Rabin’s (2007) UPE model,

because the model in Eq. (6) is then defined recursively and could not be estimated.

3. Experiment

Subjects and payoffs

The subjects were 139 students and employees from the Technical University of

Moldova (49 females, age range 17-47, average age 22 years). They received a 50 Lei

participation fee (about $4, which was $8 in PPP at the time of the experiment). To

incentivize the experiment, each subject had a one third chance to play out one of their

choices for real.

The payoffs were substantial. The subjects who played out their choices for real

earned 330 Lei on average, which was more than half the average weekly salary in

Moldova at the time of the experiment. Two subjects won about 600 Lei, the average

weekly salary.

Procedure

The experiment was computer-run in group sessions of 10 to 15 subjects. Subjects

took 30 minutes on average to complete the experiment including instructions.

Subjects made 70 choices in total. The 70 choices are listed in Appendix A

including the reference points predicted by each of the rules. The different rules

predicted widely different reference points and the predicted reference points varied

substantially across choices (except of course for the status quo).

12

Each choice involved two options, Option 1 and Option 2. The options had between

one and four possible outcomes, all strictly positive. We randomized the order of the

choices and we also randomized whether a prospect was presented as Option 1 or as

Option 2.

Choices were created by an optimal design procedure that minimized their joint

correlation. Just like orthogonal covariates in linear regression, minimally correlated

choices lead to more precise and more robust estimates of the behavioral parameters.

The optimal design procedure is described in Appendix B.

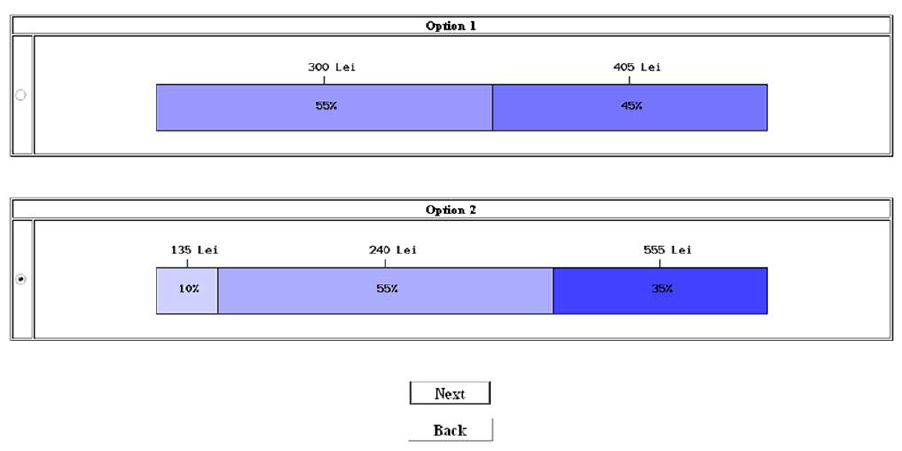

Figure 1. Presentation of the choices in the experiment

Figure 1 shows the display of the choices. Prospects were presented as

horizontal bars with as many parts as there were different payoffs. The size of each part

corresponded with the probability of the payoff. The intensity of the color (blue) of each

part increased with the size of the payoff. The payoffs were presented in increasing

13

order. Subjects were asked to click on a bullet to indicate their preferred option (Figure

1 illustrates a choice for Option 2).

4. Bayesian hierarchical modeling

We analyzed the data using Bayesian hierarchical modeling. Economic analyses of

choice behavior usually estimate models either by pooling all data or by individual

estimation. Both approaches have their limitations. Pooling ignores individual

heterogeneity and may result in estimates that are not representative of any individual

in the sample. Individual-level estimation relies on relatively few data points, which

may lead to unreliable results. Bayesian hierarchical modeling is an appealing

compromise between these two extremes. It estimates the model parameters for each

subject separately, but it assumes that subjects share similarities and that their

individual parameter values come from a common (population-level) distribution.

Hence, the parameter estimates for one individual benefit from the information that is

obtained from all others. This improves the precision of the estimates (in Bayesian

statistics this is known as collective inference) and it reduces the impact of outliers.

Individual parameters are shrunk towards the group mean, an effect that is stronger for

individuals with noisier behavior, thus making the overall estimation more robust. This

is particularly true for parameters that are estimated with lower precision. An example

is the loss aversion coefficient in prospect theory, for which the standard deviation of

the parameter estimates is usually high. Nilsson et al. (2011) illustrate that Bayesian

hierarchical modeling leads to more accurate and more efficient estimates of loss

aversion than the commonly-used maximum likelihood estimation.

14

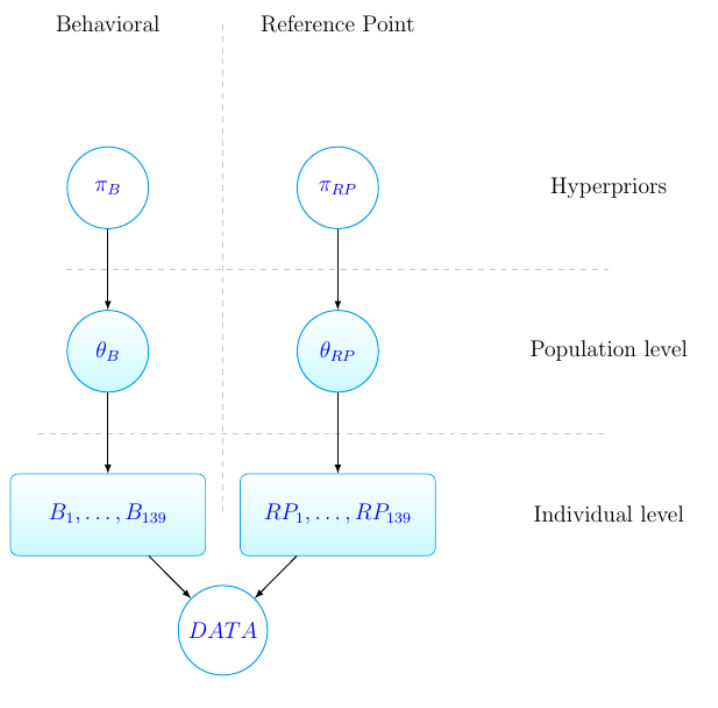

Figure 2 shows a schematic representation of our statistical model. The model

consists of two parts: the specification of the behavioral parameters in Eq. (6), utility

and probability weighting, and the specification of the reference point rule.

Figure 2. Graphical representation of our model.

Non-shaded nodes are known or predefined quantities, shaded nodes are the unknown

latent parameters.

We adopt the following mnemonic conventions. For individual {1, … , 139} the

vector of behavioral parameters is denoted

and his reference point rule is denoted

. We assume that a subject uses the same reference point rule in all choices, where

the reference point rule is one of the candidates listed in Table 1. This may appear

15

restrictive as subjects could use a mixture of reference point rules. Our analysis will

estimate the posterior probabilities of the subjects using each of the different reference

point rules. In that sense, our analysis does allow for the possibility that subjects use a

mixture of reference point rules.

The distributions of the behavioral parameters and the reference point rules in the

population are parameterized by unknown vectors

and

, respectively. Both

and

are estimated from the data. The parameters

and

also follow a

distribution, but with a known shape. This final layer in the hierarchical specification is

commonly referred to as a hyper prior. The hyper priors are denoted by

and

respectively. The vector of the observed choices (data) of the individual is denoted by

= (

, … ,

) . We will now describe our estimation procedure.

5.1. Specification of the behavioral parameters

We assume that the utility function in Eq. (6) is a power function:

(

)

=

( )

( )

<

. (7)

In Eq. (7) reflects the curvature of utility and indicates loss aversion. We

assumed the same curvature for gains and losses. It is hard to estimate loss aversion

when utility curvature for gains and for losses can both vary freely (Nilsson et al. 2011).

For probability weighting, we assumed Prelec‘s (1998) one-parameter specification:

(

)

= exp ((ln )

). (8)

We used the same probability weighting for gains and losses. Empirical studies

usually find that the differences in probability weighting between gains and losses are

relatively small (Tversky and Kahneman 1992, Abdellaoui 2000, Kothiyal, Spinu, and

Wakker, 2014).

16

To account for the probabilistic nature of people’s choices we used Luce‘s (1959)

logistic choice rule. Let () and () denote the respective values of prospects

and according to our general reference-dependent model, Eq. (6). Luce’s rule says that

the probability (, ) of choosing prospect over prospect equals

(

,

)

=

[

(

)

()

]

. (9)

In Eq. (9), > 0 is a precision parameter that measures the extent to which the

decision maker’s choices are determined by the differences in value between the

prospects. In other words, the -parameter signals the quality of the decision. Larger

values of imply that choice is driven more by the value difference between prospects

and . If = 0, choice is random and if goes to infinity choice essentially becomes

deterministic. In his comprehensive exploration of prospect theory specifications, Stott

(2006) concluded that power utility, the Prelec one-parameter probability weighting

function, and Luce’s choice rule gave the best fit to his data. We, therefore, selected

these specifications.

To test for robustness, we also ran our analysis with exponential utility, Prelec’s

(1998) two-parameter specification of the weighting function, and an alternative,

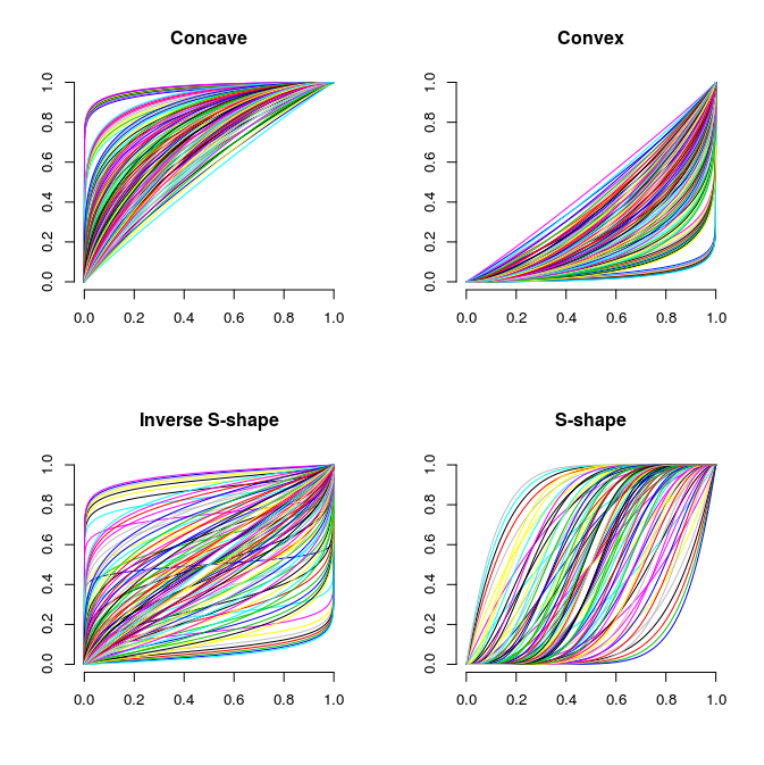

incomplete beta (IBeta) probability weighting function (Wilcox 2012). IBeta is a flexible,

two parameter family that can accommodate many shapes (convex, concave, s-shaped

and inverse s-shaped) (see Appendix C and the online Appendix for details). The

robustness analyses confirmed our main conclusions. The results of these analyses are

in the online appendix.

Each of the 139 subjects in the experiment had his own parameter vector

=

(

,

,

,

). We assumed that each parameter in

comes from a lognormal

distribution:

~(

,

),

~(

,

),

~(

,

), and

~(

,

).

17

Thus, the complete vector of unknown parameters at the population-level is

=

,

,

,

,

,

,

,

. For the hyper-priors,

=

(

,

)

, {, , , } of the

parent distributions we made the usual assumption that the

follow a lognormal

distribution and that the

follow an inverse Gamma distribution. We centered the

hyper-priors at linearity (expected value) and chose the variances such that the hyper-

priors were diffuse and would have a negligible impact on the posterior estimation.

The joint probability distribution of the behavioral parameters = (

, … . ,

)

and

is

(

,

|

)

=

(

(

|

)

)

(

|

). (10)

Given reference point rule

, the likelihood of subject ’s responses is

(

|

,

) =

,

|

,

. (11)

The probability of each choice

,

is computed using Luce’s rule, Eq.(9). From Eqs.

(10) and (11), it follows that the joint probability distribution of all the unknown

behavioral parameters and

and all the observed choices = (

, … ,

) is

(, ,

|

,

) =

,

|

,

(

(

|

)

)

(

|

)

. (12)

In Eq.(12), = (

, … ,

) is the vector of individual reference point rules.

5.2. Specification of the reference point rule

We assume that subjects use one of the six reference point rules in Table 1. For each

of these rules, we estimated the posterior probability that a subject used it given the

data: (

|

).

is a (six-dimensional) categorical variable for which it is common to

use the Dirichlet distribution:

~

(

)

, where

is a probability vector in

a six-dimensional simplex and

is a diffuse hyper prior parameter for the Dirichlet

distribution. Then the joint probability density of and

becomes:

18

(

,

|

)

=

(

(

|

)

)

(

|

)

. (13)

Substituting Eq.(13) into Eq.(12) gives the complete specification of our statistical

model:

(, ,

, ,

|

,

) =

,

|

,

(

(

|

)

)(

(

|

)

)

(

|

)

(

|

)

. (14)

5.3. Estimation

To compute the marginal posterior distributions

(

|

,

,

)

,

(

|

,

,

)

,

(

|

,

,

)

, and

(

|

,

,

)

, we used Markov Chain Monte Carlo (MCMC)

sampling (Gelfand and Smith 1990) with blocked Gibbs sampling.

8

We first used 10,000

burn-in iterations with adaptive MCMC and then 20,000 standard MCMC burn-in

iterations. The results are based on the subsequent 50,000 iterations.

6. Results

6.1. Consistency

To test for consistency, five choices were asked twice. In 68.7% of these repeated

choices, subjects made the same choice. Reversal rates up to one third are common in

experiments (Stott 2006). Moreover, our choices were complex, involving more than

two outcomes and with expected values that were close. Hence, we believe that the

consistency of our data was satisfactory.

8

For the behavioral parameters

, … ,

we used Metropolis-Hasting MCMC with symmetric

normal proposal on the log-scale, for the block

, … ,

we used Metropolis-Hasting MCMC with

uniform proposal, and the group-level blocks

and

were sampled directly from the conjugate

Gamma-Normal and Dirichlet-Categorical distributions, respectively.

19

6.2. Reference points

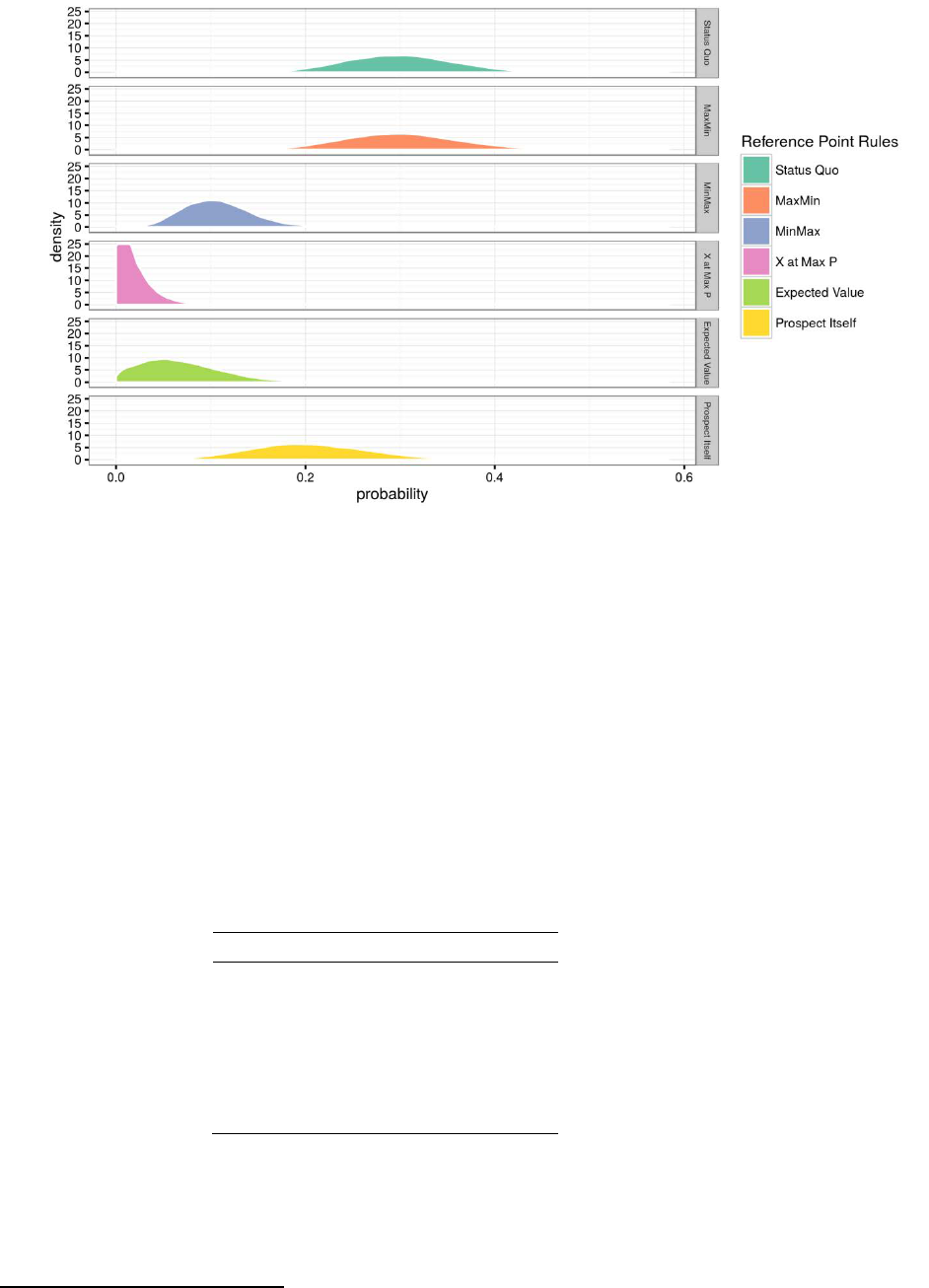

Figure 3. Marginal posterior distributions of each reference point rule

We first report the estimates of

, which indicate for each reference point rule the

probability that a randomly chosen subject behaved in agreement with it. Figure 3

shows for each RP rule the marginal posterior distribution of

in the population.

Table 2 reports the medians and standard deviations of these distributions.

9

Median

SD

Status Quo

0.30

0.06

MaxMin

0.30

0.06

MinMax

0.10

0.04

X at Max P

0.01

0.02

Expected Value

0.06

0.04

Prospect Itself

0.20

0.06

Table 2. Medians and standard deviations of the marginal posterior distributions of

the reference point rules in the population.

9

Note that the medians need not add to 100%.

20

The reference points that were most likely to be used were the status quo and

MaxMin. According to our median estimates, each of these two rules was used by 30%

of the subjects. The prospect itself (the rule suggested by Köszegi and Rabin (2006,

2007) and Delquié and Cillo (2006)) was used by 20% of the subjects. The other three

rules were used rarely.

We also estimated for each subject the likelihood he used a specific reference

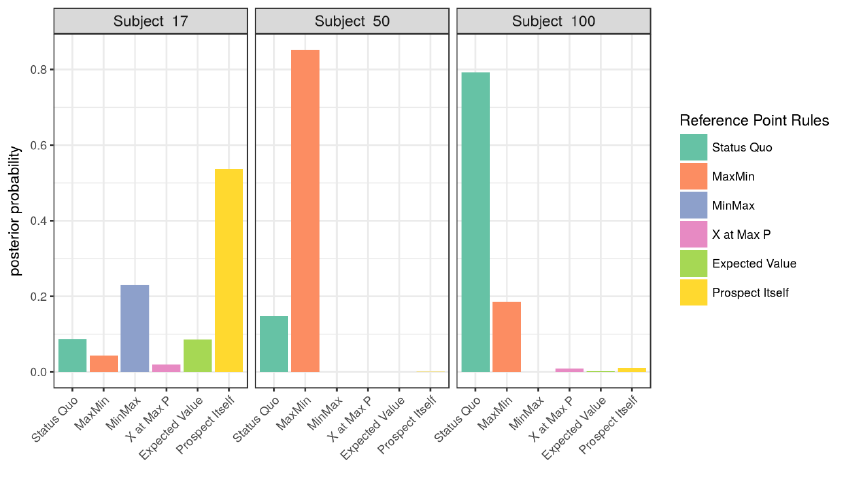

point by looking at his posterior distribution. Figure 4 shows, for example, the posterior

distributions of subjects 17, 50, and 100. Subject 17 has about 60% probability to use

the prospect itself as his reference point and 25% probability to use the minimum of the

maximums. Subject 50 almost surely uses MaxMin and subject 100 almost surely uses

the status quo as his reference point.

Figure 4. Posterior distributions of subjects 17, 50, and 100.

A subject is classified sharply if he has a posterior probability of at least 50% to

use one of the six reference point rules. For example, subjects 17, 50, and 100 were all

21

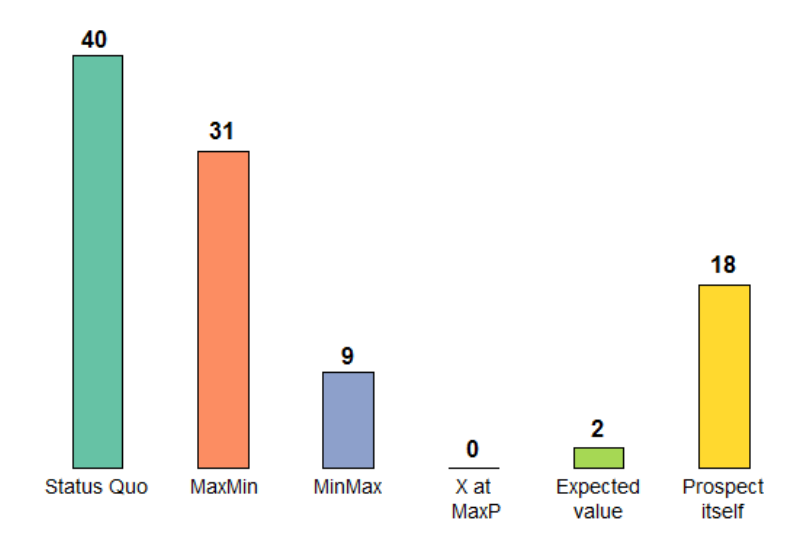

classified sharply. Out of the 139 subjects, 107 could be classified sharply. Figure 5

shows the distribution of the sharply classified subjects over the six reference point

rules. The dominance of the Status Quo and MaxMin increased further and around 70%

of the sharply classified subjects used one of these two rules.

Figure 5. Proportion of sharply classified respondents satisfying a particular

reference point rule (percent)

6.3. Behavioral parameters

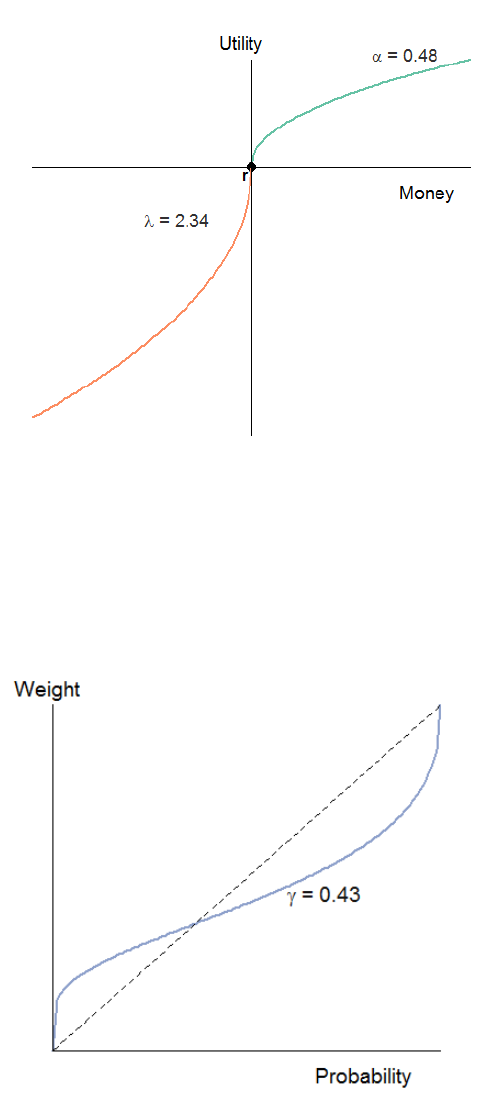

Figure 6 shows the gain-loss utility function in the psychological (PT) part of Eq.

(6) based on the estimated behavioral population level parameters (

). The utility

function is S-shaped: concave for gains and convex for losses. We found more utility

curvature than most previous estimations of gain-loss utility (for an overview see Fox

and Poldrack 2014), but our estimated utility function is no outlier. It is, for example,

close to the functions estimated by Wu and Gonzalez (1996), Gonzalez and Wu (1999),

22

and Toubia et al. (2013). The loss aversion coefficient was equal to 2.34, which is

consistent with other findings in the literature.

Figure 6. The gain-loss utility function based on the estimated group parameters

Figure 7. The probability weighting function based on the estimated group parameters

23

Figure 7 shows the estimated probability weighting function in the population. The

function has the commonly observed inverse S-shape, which reflects overweighting of

small probabilities and underweighting of intermediate and large probabilities.

10

Our

estimated probability weighting function is close to the estimated functions in Gonzalez

and Wu (1999), Bleichrodt and Pinto (2000) and Toubia et al. (2013).

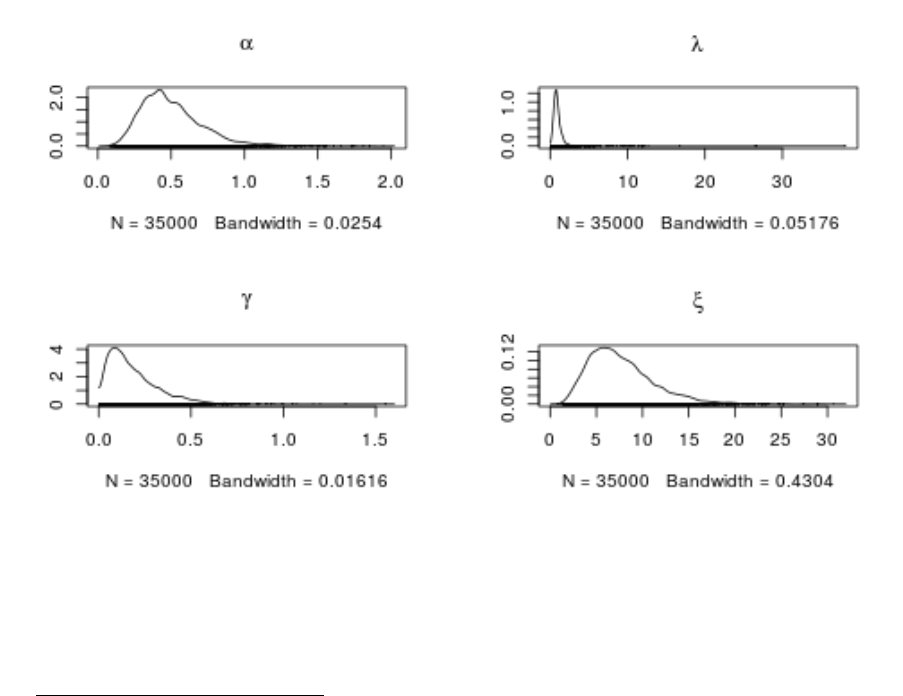

Bayesian hierarchical modeling expresses the uncertainty in the individual

parameter estimates by means of the posterior densities. To illustrate, Figure 8 shows

the posterior densities of subject 17. As the graph shows, subject 17’s parameter

estimates varied considerably, although it is safe to say that he had concave utility and

inverse S-shaped probability weighting.

Figure 8. Posterior densities of the behavioral parameters for subject 17.

10

The Prelec one-parameter probability weighting function only allows for inverse- or S-shaped

weighting. However, the two-parameter Prelec function and the IBeta function allow for all shapes and

their estimated shapes were also inverse S.

24

Table 3 shows the quantiles of the posterior point estimates of all 139 subjects. The

table shows that utility curvature and, to a lesser extent, probability weighting were

rather stable across subjects. Loss aversion varied much more although the estimates of

more than 75% of the subjects were consistent with loss aversion.

2.5%

25%

50%

75%

97.5%

.31

.40

.44

.50

.60

.09

.14

.24

.44

1.66

.36

1.19

1.59

2.25

4.63

6.11

8.26

10.89

14.41

25.76

Table 3. Quantiles of the point estimates of the behavioral parameters of the 139

subjects

Status Quo

.42

.28

1.51

11

11.75

MaxMin

.46

.24

2.24

10.30

MinMax

.40

.15

.50

14.34

Expected Value

.36

.25

2.44

6.14

Prospect Itself

.45

.16

2.23

10.89

Table 4: Median individual level parameters for the sharply classified subjects in each

group.

Table 4 shows the median behavioral parameters of the sharply classified subjects in

each group.

12

A priori, it seemed plausible that subjects who used different rules might

also have different behavioral parameters, in particular loss aversion. The table

confirms this conjecture. While utility curvature and probability weighting were rather

stable across the groups, the loss aversion coefficients varied from 0.50 in the MinMax

group to 2.44 in the Expected Value group. The loss aversion coefficient of 0.50 in the

MinMax group has the interesting interpretation that these optimistic subjects weight

11

The reason that is not equal to 1 for subjects who were sharply classified as using the status quo

rule is that a subject’s behavioral parameters stayed the same for all reference point rules. Consequently,

even when a subject was (sharply) classified as a status quo type, there was still a non-negligible

probability that he used any of the other reference point rules and was loss averse.

12

X at MaxP is not in the table as there were no sharply classified subjects who behaved according to

this rule.

25

gains twice as much as losses and they exhibit what might be seen as the reflection of

the preferences of the cautious MaxMin subjects who weight losses more than twice as

much as gains.

Table 4 also shows that subjects who used the status quo as their reference point

were typically no expected utility maximizers as there was substantial probability

weighting in this group. Table 5 gives a more detailed overview. It shows the

subdivision of the subjects who used the status quo as their reference point based on

the 95% Bayesian credible intervals of their estimated utility curvature and probability

weighting parameters. Twelve subjects (those with = 1) behaved according to

expected utility, three of whom (those with = 1 and = 1) were expected value

maximizers. Thus, less than 10% of our subjects were expected utility maximizers.

Probability weighting

< 1

= 1

> 1

Total

Utility

< 1

28

9

0

37

= 1

3

3

0

9

> 1

0

0

0

0

Total

31

12

0

43

Table 5. Behavioral parameters of the subjects using the status quo as their reference

points (classification into groups is based on the 95% Bayesian credible intervals).

6.4. Robustness

In the main analysis, we assumed Eq. (6) for all reference point rules, allowing us

to keep all behavioral parameters constant when comparing reference point rules. We

also tried several other specifications, which are summarized in Table 6. Model 1

corresponds to the results reported in Sections 6.2 and 6.3. The two variables we varied

in the robustness checks were the inclusion of consumption utility and probability

weighting. While models with prospect-specific reference points need consumption

26

utility to exclude implausible choice behavior,

13

models with a choice-specific reference

point do not. Prospect theory, for example, does not include consumption utility.

Consequently, we estimated the models with a choice-specific reference point both with

and without consumption utility.

Model

Choice-specific reference point

Prospect-specific reference point

Consumption

utility

Probability

weighting

Consumption

utility

Probability

weighting

1

Yes

Yes

Yes

Yes

2

No

Yes

Yes

Yes

3

Yes

Yes

Yes

No

4

No

Yes

Yes

No

5

Yes

No

Yes

No

6

No

No

Yes

No

Table 6: Estimated models

In Eq. (6) we assumed that subjects weight probabilities when they evaluate

prospects relative to a reference point, but, following the literature on stochastic

reference points, we abstracted from probability weighting in the determination of the

stochastic reference point. This may be arbitrary and we, therefore also estimated the

models without probability weighting. We performed two sets of estimations: one in

which the models with a choice-specific reference point included probability weighting,

but the models with a prospect-specific reference point did not (models 3 and 4) and

one in which no model had probability weighting (models 5 and 6).

The results of the robustness checks were as follows. First, our main conclusion

that the status quo and MaxMin were the dominant reference points remained valid.

The behavior of 60% to 75% of the subjects was best described by a model with one of

these two reference points. Second, excluding consumption utility from models with a

13

For example, in Köszegi and Rabin’s (2007) CPE model without consumption utility any prospect

that gives with probability 1 has a value of 0, regardless of the size of . So the decision maker should be

indifferent between $1 for sure and $1000 for sure. Consumption utility prevents this.

27

choice-specific reference point (models 2 and 4) led to a substantial increase in the

precision parameter . This suggests that there is no need to include consumption

utility in models like prospect theory. Third, probability weighting played a crucial role.

Excluding probability weighting from the models with a prospect-specific reference

point (model 3) decreased the share of the prospect itself as a reference point to 10%

(8% if we only include the sharply classified subjects) and increased the share of the

MaxMin reference point to 44% (52% if we only include the sharply classified subjects).

The shares of the other rules changed only little. Hence, prospect-specific models like

Köszegi and Rabin’s (2006, 2007) benefit from including probability weighting. Ignoring

probability weighting altogether, as in models 5 and 6, led to unstable estimation

results.

The behavioral parameters were comparable across all models that we

estimated. The power utility coefficient was approximately 0.50 in all models, the

probability weighting parameter varied between 0.40 and 0.60 (except, of course, when

no probability weighting was assumed), and the loss aversion coefficient varied

between 2 and 2.50. Detailed results of the robustness analysis are in the online

appendix.

6.5 Cross-validation

Throughout the paper we considered 6 reference point rules. Even though these

rules cover many of the rules that have been proposed in the literature and used in

empirical research, it might be that subjects adopted another rule. In that case the

model would be misspecified and would poorly predict subjects’ choices. To explore this

possibility, we performed the following cross-validation exercise. We estimated the

model on 69 questions and predicted the choice made by each of the 139 subjects for

28

the remaining question. This out-of-sample prediction procedure was repeated 70

times, once for each hold-out question. The models predicted around 70% of the choices

correctly. Given that the consistency rate was also around 70%, we conclude that the

rules that we included captured our subjects’ preferences well and that there is no

indication that the model was misspecified. The part that could not be explained

probably reflected noise.

7. Discussion

Empirical studies of decisions under risk that want to account for reference-

dependence often assume that subjects take the status quo as their reference point. In

our data this assumption was justified for 30-40% of the subjects, but a majority used a

different reference point. Our data also suggest how experimental researchers can

increase the likelihood that subjects use the participation fee as their reference point.

For example, in choosing between mixed prospects, researchers could include a

prospect with 0 as its minimum outcome in each choice. This ensures that MaxMin

subjects will also use 0 as their reference point and our results suggest that then a

substantial majority of the subjects will use 0 as their reference point. Our results help

to assess the validity of empirical studies that take the status quo as the reference point.

We tested the reference point rules in a lab experiment with large incentives

(subjects could win up to a weekly salary) and used a Bayesian hierarchical approach to

analyze the data. Bayesian analysis strikes a nice balance between pooling and

individual estimation and it leads to more precise parameter estimates. A potential

limitation of Bayesian analysis is that the selected priors can affect the estimations, but

in our analysis the choice of priors had negligible impact on the estimates.

29

To make inferences about the different reference point rules, we used a

comprehensive model which allowed isolating the impact of the reference point rule

from the other behavioral parameters. This approach is cleaner and better interpretable

than the common practice in mixture modeling where each model in the mixture is

specified separately and parameterizations can differ across models and also than horse

races between models based on criteria like the Akaike Information Criterion. Using a

Bayesian model has the additional advantage that we could obtain the parameter

estimates for both the distribution of reference point rules in the population and each

subject separately.

Our robustness tests have two interesting implications for the modeling of

reference-dependent preferences. First, they indicate that models with a choice-specific

reference point do not benefit from including consumption utility. Kahneman and

Tversky (1979, p.277) argue that even though an individual’s attitudes to money

depend both on his asset position and on changes from his reference point, a utility

function that is only defined over changes from the reference point generally provides a

satisfactory approximation. Our results provide support for their argument.

Second, we concluded that probability weighting played an important role and could

not be ignored. The fit of expectation-based prospect-specific models like Köszegi and

Rabin’s (2006, 2007) model, which in their original form do not assume probability

weighting, clearly improved when probability weighting was included. A complication

in these model is how the reference point is determined when decision makers weight

probabilities.

Our analysis assumed that subjects consider each choice in isolation from the other

choices and from the one third chance that they would be selected to play out one of

their choices for real. This assumption is common in experimental economics and there

30

exists support for it (Starmer and Sugden 1991, Cubitt et al. 1998, Bardsley et al.

2010).

14

If some subjects did not isolate choices, but instead viewed the experiment as a

compound lottery, then this would create additional support for the status quo as

Maxmin and MaxP subjects would then also use the status quo as their reference point.

An interesting question to explore is whether our results can be generalized to other

decision contexts than the one we considered. For example our experiment involved

discrete distributions whereas in economic contexts continuous distributions are often

relevant. Also, the minimum probability that we included was 5% whereas real-world

decisions frequently involve smaller probabilities, e.g. the annual risk of contracting a

fatal disease. It is, for instance, unclear whether MaxMin would perform as well if the

lowest outcome occurred with only a very small probability.

We did not test all reference points that have been proposed in the literature. As we

explained in the introduction, we followed Rabin’s (2013) approach and studied

reference point rules that used the same independent variables as the core economic

theory of decision under risk, expected utility. This implied, for example, that we did not

test explicitly for subjects’ goals or aspirations as these require other inputs based on

introspection. On the other hand, subjects may have had few goals or aspirations for the

current experiment and it is also possible that their goals were equal to one of the

reference points that we used (e.g. expected value or the security level). We also did not

test reference point rules that would be based on previous choices. Such rules would

introduce new degrees of freedom (which piece of information from these choices,

number of past choices remembered, aggregation/updating rule…). Our cross-

validation exercise indicated that the rules that we included captured our subjects’

14

Cox et al. (2015) found evidence against isolation.

31

preferences accurately and that the model was not misspecified due to the omission of

reference point rules.

8. Conclusion

Reference-dependence is a key concept in explaining people’s choices, but little insights

exists into the question how reference points are formed. Reference-dependent theories

give no guidance about this question. This paper has estimated the prevalence of six

reference point rules using a unique data set in which we used stakes up to a weekly

salary. We modeled the reference point rule as a latent categorical variable, which we

estimated using Bayesian hierarchical modeling. Our results indicate that the status quo

and MaxMin are the most commonly used reference points. Around twenty percent of

the subjects used an expectations-based reference point.

32

Appendix A: The experimental questions and the predicted reference points.

Table A1 describes the 70 choices of the experiments, between prospects =

(

,

;

,

;

,

; 1

,

)

and =

(

,

;

,

;

,

; 1

,

)

. The last five columns give the choice-specific reference points of the MaxMin, MinMax and X at

Max P rules, and the prospect-specific reference points of the Expected Value rule. The reference point of the Satus Quo rule is always 0

and the prospect-specific reference points of the sixth and last rule were and themselves.

#

MaxMin

MinMax

X at Max P

Expected Value

1

267

313

453

546

0.1

0.8

0.05

127

220

406

0.15

0.05

0.8

267

406

313

327.05

354.85

2

159

221

408

0.7

0.1

0.2

34

97

346

0.1

0.3

0.6

159

346

159

215

240.1

3

183

233

384

485

0.7

0.05

0.1

32

132

334

0.15

0.05

0.8

183

334

334

250.9

278.6

4

223

263

383

0.4

0.5

0.1

143

183

343

0.1

0.4

0.5

223

343

263

259

259

5

127

255

287

0.7

0.05

0.25

95

191

223

0.15

0.05

0.8

127

223

223

173.4

202.2

6

103

213

377

0.6

0.15

0.25

48

158

267

322

0.3

0.1

0.05

103

322

103

188

220.65

7

92

245

0.85

0.15

16

130

206

0.1

0.7

0.2

92

206

92

114.95

133.8

8

135

290

329

0.55

0.35

0.1

96

213

251

0.25

0.05

0.7

135

251

251

208.65

210.35

9

209

309

459

0.35

0.55

0.1

159

259

359

409

0.05

0.55

0.1

209

409

309

289

309

10

221

504

0.85

0.15

80

292

434

0.05

0.7

0.25

221

434

221

263.45

316.9

11

64

188

313

0.4

0.1

0.5

2

126

251

375

0.25

0.4

0.1

64

313

313

200.9

169.75

12

122

270

418

0.15

0.8

0.05

48

196

344

492

0.1

0.35

0.45

122

418

270

255.2

277.4

13

224

416

0.55

0.45

95

352

480

0.25

0.7

0.05

224

416

352

310.4

294.15

14

100

211

0.2

0.8

64

137

285

0.2

0.5

0.3

100

211

211

188.8

166.8

15

257

427

0.8

0.2

143

370

484

0.35

0.45

0.2

257

427

257

291

313.35

16

223

416

0.45

0.55

159

287

544

0.05

0.7

0.25

223

416

287

329.15

344.85

17

219

448

0.2

0.8

143

296

372

601

0.1

0.1

0.7

219

448

448

402.2

364.4

18

99

225

0.8

0.2

16

141

183

266

0.1

0.4

0.45

99

225

99

124.2

153.65

19

94

187

0.3

0.7

64

125

156

248

0.25

0.3

0.05

94

187

187

159.1

160.5

33

20

203

317

0.75

0.25

127

241

279

354

0.35

0.05

0.45

203

317

203

231.5

235.15

21

138

245

0.55

0.45

30

84

191

352

0.05

0.05

0.85

138

245

191

186.15

185.65

22

118

200

0.8

0.2

64

91

173

228

0.2

0.1

0.6

118

200

118

134.4

148.5

23

232

374

0.4

0.6

91

161

303

515

0.05

0.1

0.6

232

374

374

317.2

331.2

24

233

344

0.7

0.3

159

196

307

381

0.3

0.2

0.1

233

344

233

266.3

270

25

251

358

0.7

0.3

143

304

412

465

0.05

0.85

0.05

251

358

304

283.1

309.4

26

105

278

0.25

0.75

48

163

336

394

0.25

0.4

0.1

105

278

278

234.75

209.3

27

183

302

0.6

0.4

64

242

361

421

0.15

0.7

0.1

183

302

242

230.6

236.15

28

61

179

0.45

0.55

22

101

218

257

0.4

0.05

0.5

61

179

179

125.9

135.7

29

147

367

0.6

0.4

0

74

367

0.25

0.05

0.7

147

367

367

235

260.6

30

99

251

0.6

0.4

48

251

0.4

0.6

99

251

99

159.8

169.8

31

259

558

0.75

0.25

159

359

558

0.15

0.7

0.15

259

558

259

333.75

358.85

32

168

397

0.6

0.4

16

92

397

0.05

0.4

0.55

168

397

168

259.6

255.95

33

209

407

0.75

0.25

143

407

0.5

0.5

209

407

209

258.5

275

34

120

243

0.75

0.25

80

161

243

0.15

0.7

0.15

120

243

120

150.75

161.15

35

142

209

277

0.7

0.05

0.25

74

108

277

0.4

0.1

0.5

142

277

142

179.1

178.9

36

151

230

348

0.5

0.15

0.35

111

269

348

0.25

0.6

0.15

151

348

269

231.8

241.35

37

140

200

261

0.85

0.05

0.1

80

110

261

0.05

0.55

0.4

140

261

140

155.1

168.9

38

79

170

308

0.25

0.7

0.05

33

216

308

0.15

0.8

0.05

79

308

216

154.15

193.15

39

192

341

0.15

0.85

192

390

439

0.55

0.4

0.05

192

341

341

318.65

283.55

40

15

290

0.3

0.7

15

382

0.5

0.5

15

290

290

207.5

198.5

41

95

443

0.3

0.7

95

327

559

0.1

0.8

0.1

95

443

327

338.6

327

42

102

311

0.15

0.85

102

381

450

0.55

0.25

0.2

102

311

311

279.65

241.35

43

127

284

0.2

0.8

127

336

0.45

0.55

127

284

284

252.6

241.95

44

54

259

0.3

0.7

54

191

328

0.05

0.85

0.1

54

259

191

197.5

197.85

45

127

259

390

0.05

0.4

0.55

127

456

521

0.45

0.15

0.4

127

390

390

324.45

333.95

46

57

221

331

0.3

0.1

0.6

57

167

386

0.1

0.6

0.3

57

331

331

237.8

221.7

47

111

194

277

0.1

0.05

0.85

111

318

359

0.5

0.3

0.2

111

277

277

256.25

222.7

48

6

229

377

0.05

0.8

0.15

6

155

451

0.1

0.7

0.2

6

377

229

240.05

199.3

49

100

1

13

186

0.45

0.55

100

100

100

100

108.15

34

50

224

1

12

294

0.25

0.75

224

224

224

224

223.5

51

276

1

80

374

472

0.35

0.45

0.2

276

276

276

276

290.7

52

203

1

106

154

299

0.45

0.05

0.5

203

203

203

203

204.9

53

196

1

95

146

246

297

0.3

0.05

0.5

196

196

196

196

203.35

54

383

1

171

453

0.25

0.75

383

383

383

383

382.5

55

297

404

0.55

0.45

189

243

350

511

0.05

0.05

0.85

297

404

350

345.15

344.65

56

220

338

0.45

0.55

181

260

377

416

0.4

0.05

0.5

220

338

338

284.9

294.7

57

238

329

467

0.25

0.7

0.05

192

375

467

0.15

0.8

0.05

238

467

375

313.15

352.15

58

301

368

436

0.7

0.05

0.25

233

267

436

0.4

0.1

0.5

301

436

301

338.1

337.9

59

259

1

172

345

0.45

0.55

259

259

259

259

267.15

60

362

1

265

313

458

0.45

0.05

0.5

362

362

362

362

363.9

61

213

418

0.3

0.7

213

350

487

0.05

0.85

0.1

213

418

350

356.5

356.85

62

223

347

472

0.4

0.1

0.5

161

285

410

534

0.25

0.4

0.1

223

472

472

359.9

328.75

63

306

526

0.6

0.4

159

233

526

0.25

0.05

0.7

306

526

526

394

419.6

64

251

358

0.7

0.3

143

304

412

465

0.05

0.85

0.05

251

358

304

283.1

309.4

65

95

443

0.3

0.7

95

327

559

0.1

0.8

0.1

95

443

327

338.6

327

66

223

416

0.45

0.55

159

287

544

0.05

0.7

0.25

223

416

287

329.15

344.85

67

209

407

0.75

0.25

143

407

0.5

0.5

209

407

209

258.5

275

68

138

245

0.55

0.45

30

84

191

352

0.05

0.05

0.85

138

245

191

186.15

185.65

69

111

207

223

0.5

0.4

0.1

80

95

207

0.1

0.4

0.5

111

207

111

160.6

149.5

70

111

175

207

0.1

0.4

0.5

80

159

191

0.25

0.25

0.5

111

191

207

184.6

155.25

Table A1. Choices and reference points

35

Appendix B: The procedure to construct the experimental choices

The selection of experimental questions was guided by the following contrasting

principles:

- Questions must be diverse in terms of number of outcomes and magnitudes of

probabilities involved.

- Questions within each choice must have non-matching maximal or minimal

outcomes.

- Questions must be diverse in terms of relative positioning in the outcome space

(a.k.a. shifting; see the description below).

- Questions must have similar expected value to avoid trivial or statistically non-

informative choice situations.

- Question pairs must be "orthogonal" in some sense in order to maximize statistical

efficiency.

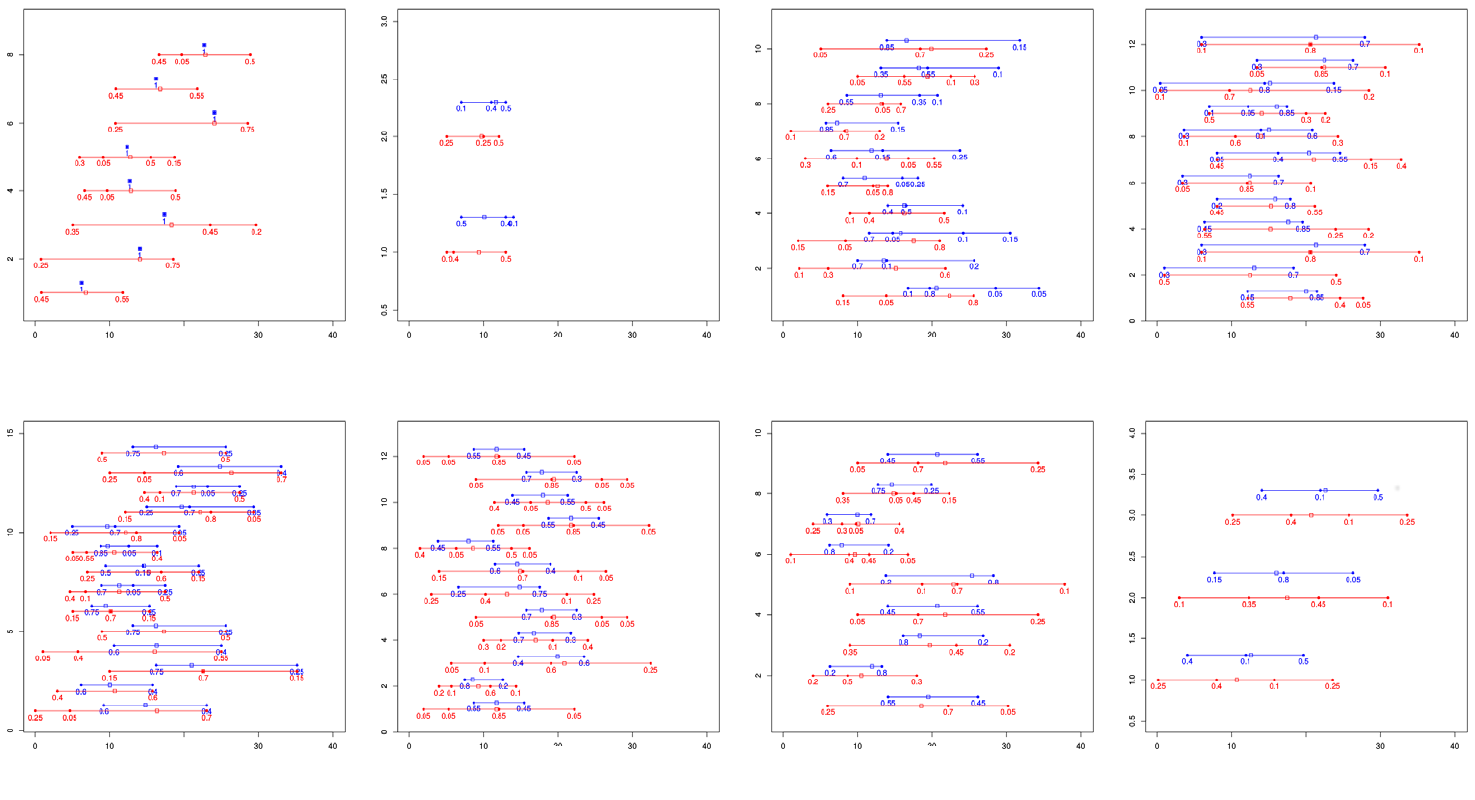

Our question set (Table A1) consists of six homogeneous groups which are illustrated

graphically in Figure B1. The first group is a set of 8 questions where one of the

prospects is certainty and the other option is a two to four outcome prospect (Figure

B1a). The second set consists of two choice situations where one prospect stochastically

dominates the other (Figure B1b). The third set comprises 10 choices where one

prospect is relatively shifted - both minimum and maximum are relatively higher than

for the other prospect (Figure B1c). The fourth group consists of 12 questions for which

minimum outcome coincides (Figure B1d). The fifth group consists of 14 questions for

which the maximum outcome coincides (Figure B1e). The last three groups (Figure B1f-

h) consists of 24 questions where the range of one prospect is within the range of the

other prospect. This group is further split into three homogeneous sub-groups

determined by number of outcomes in the smaller prospect (2 vs 3) and by the amount

36

of shift of the smaller prospect with respect to the bigger one (1 or 2 outcomes). Choices

in all groups are roughly balanced with respect to the relative shift (there are both one-

and two-outcome shifted questions on the either side of the prospects).

In order to maximize statistical efficiency and minimize redundancy, within each group

of questions we perform the exhaustive search that minimizes the sum of the pairwise

cross-choice covariance within that group. We defined the cross-choice covariance for a

choice pair (1, 2), (2, 2) as (

((,) (,))

)

. This is an intuitive counterpart

of the statistical co-variance. For each sub-group of choices, we optimized the sum of all

pairwise cross-choice co-variances within that group.

37

Figure B1: Choices used in the experiment.

Each sub-figure represents a group of homogeneous choices. Each question consists of two prospects (blue and red). X axis represents

the amounts in euro and Y axis has no quantitative meaning. Numbers below the prospect lines are the outcome probabilities. Small

squares are the expectations of the prospects. (a) group with certainty equivalents, (b) stochastic dominance group, (c) shifted group

(extremes of blue prospect are shifted with respect to the red prospect), (d) minima of blue and red prospects coincide, (e) maxima of

red and blue prospects coincide, (f-h) three groups for which the range of the blue object is inside the range of the red prospect.

(a)

(b)

(c)

(d)

(e)

(f)

(g)

(h)

38

Appendix C: IBeta

The incomplete regularized beta function (), is a very flexible monotonically

increasing

[

0,1

]

[0,1] function. It can capture a wide range of convex, concave, S-

shape and inverse S-shape functions without favoring specific shapes or inflection

points. The family is symmetric in the sense that (; , ) = 1 (1

; , ). Various shapes of function are illustrated in Figure C.1.

Figure C.1. Various shapes of the function

40

References

Abdellaoui M (2000) Parameter-free elicitation of utility and probability weighting functions.

Management Science 46: 1497-1512.

Abeler J, Falk, A, Goette, L, Huffman, D (2011) Reference points and effort provision. The

American Economic Review 101: 470-492.

Allen EJ, Dechow, PM, Pope, DG, Wu, G (forthcoming) Reference-dependent preferences:

Evidence from marathon runners. Management Science .

Barber BM, Odean, T (2008) All that glitters: The effect of attention and news on the buying

behavior of individual and institutional investors. Review of Financial Studies 21: 785-

818.

Barberis NC (2013) Thirty years of prospect theory in economics: A review and assessment.

Journal of Economic Perspectives 27: 173-196.

Bardsley N, Cubitt, R, Loomes, G, Moffatt, P, Starmer, C, Sugden, R (2010) Experimental

economics: Rethinking the rules (Princeton University Press, Princeton and Oxford).

Bartling B, Brandes, L, Schunk, D (2015) Expectations as reference points: Field evidence

from professional soccer. Management Science 61: 2646-2661.

Baucells M, Weber, M, Welfens, F (2011) Reference-point formation and updating.

Management Science 57: 506-519.

Bell DE (1985) Disappointment in decision making under uncertainty. Operations Research

33: 1-27.

Benartzi S, Previtero, A, Thaler, RH (2011) Annuitization puzzles. The Journal of Economic

Perspectives 25: 143-164.

Benartzi S, Thaler, RH (1995) Myopic loss aversion and the equity premium puzzle.

Quarterly Journal of Economics 110: 73-92.

Birnbaum MH, Schmidt, U (2010) Testing transitivity in choice under risk. Theory and

Decision 69: 599-614.

Bleichrodt H, Schmidt, U (2005) Context- and reference-dependent utility: A generalization

of prospect theory. Working Paper.

Bleichrodt H, Pinto, JL (2000) A parameter-free elicitation of the probability weighting

function in medical decision analysis. Management Science 46: 1485-1496.

Bleichrodt H, Pinto, JL, Wakker, PP (2001) Making descriptive use of prospect theory to

improve the prescriptive use of expected utility. Management Science 47: 1498-1514.

41

Bordalo P, Gennaioli, N, Shleifer, A (2012) Salience theory of choice under risk. The

Quarterly Journal of Economics 127: 1243-1285.

Card D, Dahl, GB (2011) Family violence and football: The effect of unexpected emotional

cues on violent behavior. Quarterly Journal of Economics 126: 103-143.

Chetty R, Looney, A, Kroft, K (2009) Salience and taxation: Theory and evidence. The

American Economic Review 99: 1145-1177.

Chew SH, Epstein, LG, Segal, U (1991) Mixture symmetry and quadratic utility.

Econometrica 139-163.

Chew SH, Epstein, LG, Segal, U (1994) The projective independence axiom. Economic

Theory 4: 189-215.

Cox JC, Sadiraj, V, Schmidt, U (2015) Paradoxes and mechanisms for choice under risk.

Experimental Economics 18: 215-250.

Crawford VP, Meng, J (2011) New york city cab drivers' labor supply revisited: Reference-

dependent preferences with rational expectations targets for hours and income. American

Economic Review 101: 1912-1932.

Cubitt R, Starmer, C, Sugden, R (1998) On the validity of the random lottery incentive

system. Experimental Economics 1: 115-131.

Delquié P, Cillo, A (2006) Disappointment without prior expectation: A unifying perspective

on decision under risk. Journal of Risk and Uncertainty 33: 197-215.

Diecidue E, Van de Ven, J (2008) Aspiration level, probability of success and failure, and

expected utility. International Economic Review 49: 683-700.

Eil D, Lien, JW (2014) Staying ahead and getting even: Risk attitudes of experienced poker

players. Games and Economic Behavior 87: 50-69.

Fox CR, Poldrack, RA (2014) Prospect theory and the brain. Glimcher Paul, Fehr Ernst, eds.

Handbook of Neuroeconomics (2nd Ed.) (Elsevier, New York), 533-567.

Gelfand AE, Smith, AF (1990) Sampling-based approaches to calculating marginal densities.

Journal of the American Statistical Association 85: 398-409.

Genesove D, Mayer, CJ (2001) Loss aversion and seller behavior: Evidence from the housing

market. Quarterly Journal of Economics 116: 1233-1260.

Gill D, Prowse, V (2012) A structural analysis of disappointment aversion in a real effort

competition. The American Economic Review 102: 469-503.

Gonzalez R, Wu, G (1999) On the form of the probability weighting function. Cognitive

Psychology 38: 129-166.

Gul F (1991) A theory of disappointment aversion. Econometrica 59: 667-686.

42

Heath C, Larrick, RP, Wu, G (1999) Goals as reference points. Cognitive Psychology 38: 79-

109.

Heidhues P, Kőszegi, B (2008) Competition and price variation when consumers are loss

averse. The American Economic Review 1245-1268.

Hershey JC, Schoemaker, PJH (1985) Probability versus certainty equivalence methods in

utility measurement: Are they equivalent? Management Science 31: 1213-1231.

Johnson EJ, Goldstein, D (2003) Do defaults save lives? Science 302: 1338-1339.