SEPTEMBER 1, 2020

RESOUNDING SUCCESS:

A REVIEW OF THE

PAYCHECK PROTECTION PROGRAM

STAFF REPORT

HOUSE SELECT SUBCOMMITTEE ON

THE CORONAVIRUS CRISIS | MINORITY

Page 2 of 23

TABLE OF CONTENTS

Executive Summary ...................................................................................................................................... 3

President Trump’s Swift Action Provided Relief ......................................................................................... 5

The Administration’s Guidance for Program Lending ................................................................................. 8

SBA and Treasury Guidance .................................................................................................................... 8

PPP Loan Forgiveness .............................................................................................................................. 9

Overview of the Select Subcommittee Democrats’ Partisan Investigation ................................................ 10

Documents and Information Show Democrat Allegations Are Wrong .................................................. 10

Overview of the PPP Lending Process ................................................................................................... 11

PPP Data for Select Financial Institutions .............................................................................................. 12

Impacts on Underserved Communities ....................................................................................................... 19

Conclusion .................................................................................................................................................. 20

Appendix A: Key Statistics ......................................................................................................................... 21

Appendix B: Timeline ................................................................................................................................ 23

Page 3 of 23

EXECUTIVE SUMMARY

The Paycheck Protection Program (PPP) is a forgivable loan program designed to provide

a direct incentive for small businesses to keep their workers on the payroll. Congress

appropriated $659 billion for the program in the Coronavirus Aid, Relief, and Economic Security

(CARES) Act and the Paycheck Protection Program and Health Care Enhancement Act. This

enabled the Small Business Administration (SBA) to fund more than 4.9 million PPP loans.

Data show the PPP supported more than 51 million jobs across the country. The program

demonstrated how the government can work with the private sector to quickly and efficiently get

aid to those in need.

In the early weeks of the coronavirus crisis, much of the country shut down to limit the

spread of the deadly virus. Dr. Megan Ranney – a witness invited by Subcommittee Democrats–

testified at a hearing on May 21, 2020 that the economy was shut down to “flatten the curve of

this infection so our hospitals across the country would not be overrun.” The effects of the broad

shutdown orders, however, went far beyond the hospital population. Essential and non-essential

sectors of the economy were effectively closed. Consequently, many small businesses faced

bankruptcy and the country faced a burgeoning economic crisis. Republicans in Congress and the

Trump Administration designed the PPP to address this need, prioritizing rapid distribution of

funds to small businesses to keep employees on payroll while shutdown orders were in effect and

until the economy was fully restored. The program’s focus on getting money to workers quickly

saved millions of jobs and kept the economy from collapse.

Challenges related to connecting bank systems to the SBA’s E-Tran portal – which was

receiving an unprecedented volume of loan applications – caused delays immediately after PPP

went live on April 3, 2020. SBA and Treasury Department employees worked around the clock

to address those technical issues, and the program was fully operational within a matter of days.

The SBA and Treasury issued a series of guidance documents to clarify certain aspects of the

program, many of which were issued in response to discrete questions from applicants, lenders,

and Congress. The evolving nature of the program’s guidelines predictably caused confusion.

The urgent need to disburse funds to millions of small businesses, however, justified the

expedited rollout of the lending program, as Congress intended.

The SBA distributed PPP loans through thousands of financial institutions across the

country. SBA directed financial institutions to work with small businesses in their communities

and rapidly process loan applications. SBA and our nation’s banks worked tirelessly to provide

$342.3 billion in loans in 14 days. Behind the scenes, SBA and Treasury worked together to

quickly get funds to more than 84 percent of the country’s small businesses, with minimal fraud.

Under the lending terms of the PPP, small businesses may have their loans forgiven if

they abide by the CARES Act and SBA employee retention requirements. These incentives

ensured small businesses used the funds to pay employees and prevented abuses.

Page 4 of 23

The Trump Administration’s fast and efficient work with financial institutions across the

country should be commended. Indeed, SBA and Treasury officials, and their counterparts at

financial institutions, worked around the clock in March and April 2020 to stand up and execute

the PPP. Their efforts may have prevented an apocalyptic scenario for American small

businesses.

Page 5 of 23

PRESIDENT TRUMP’S SWIFT ACTION PROVIDED RELIEF

In the early weeks of the coronavirus crisis much of the country was forced to shut down

to limit the spread of the deadly virus. Dr. Megan Ranney – a witness invited by Democrats to

testify before the Subcommittee – stated, under oath, the economy was shut down to “flatten the

curve of this infection so our hospitals across the country would not be overrun.” These broad

and inflexible shutdowns drastically limited commercial activity. Consequently, many small

businesses faced bankruptcy and the country faced a burgeoning economic crisis. President

Trump and his Administration designed the PPP with Congress to address this need, prioritizing

rapid distribution of funds to small businesses to keep employees on payroll and keep their doors

open. On March 27, 2020, President Trump signed the CARES Act which included $349 billion

in initial funding for the PPP.

1

The PPP saved millions of jobs and kept the economy from

collapse.

Due to the hard work of President Trump, SBA, and the Treasury Department, it took

only six days to stand up the PPP.

2

In the following 14 days, lenders of various shapes and sizes

worked with SBA to process a deluge of loan applications.

3

The scale of this economic relief

effort was unprecedented. Over the course of two weeks, loans totaling $349 billion were

approved for more than 1.6 million small businesses, nonprofits, veterans’ organizations, tribal

businesses, sole proprietors, and independent contractors. Thousands of additional small

businesses remained in the queue when PPP funds ran out.

The demand for PPP loans made clear the program was the most successful aspect of the

CARES Act and was serving as a lifeline for America’s small businesses, as it was intended. On

April 7, 2020, Treasury Secretary Steven Mnuchin asked congressional leaders to provide an

additional $250 billion for the PPP program, which was immediately supported by Republicans,

with the Senate set to pass additional funds on April 9, 2020.

4

House Democrats, however, jeopardized paychecks for millions of small business

employees by attaching conditions to additional funding for the program during negotiations for

the successor to the CARES Act. On April 8, 2020, Speaker Nancy Pelosi and Senate Minority

Leader Chuck Schumer said they would block a vote on additional funds for the PPP.

5

Democrat

leaders used funds for small businesses on the brink of insolvency as a bargaining chip to push

progressive priorities including federal workplace standards and more funding for state and local

1

Pub. L. No. 116-136 (2020).

2

Johnathan O’Connell, et. al, Following messy start, enormous Paycheck Protection Program shows signs of

buttressing economy, Washington Post, (Jun. 10, 2020),

https://www.washingtonpost.com/business/2020/06/09/how-effective-is-ppp-small-business/.

3

Id.

4

Erica Werner, et. al., Treasury’s Mnuchin seeks additional $250 billion to replenish small-business coronavirus

program, The Washington Post, (Apr. 7, 2020), https://www.washingtonpost.com/us-policy/2020/04/07/treasury-

coronavirus-small-business/

5

The Editorial Board, Pelosi Holds Up Small Business, Wall Street Journal, (Apr 8. 2020),

https://www.wsj.com/articles/pelosi-holds-up-small-business-11586388710.

Page 6 of 23

governments, even though the original funds for states and localities had not been expended at

that time.

6

Meanwhile, other senior Democrats refused to fund PPP based on concerns about

transparency and the availability of data. For instance, Small Business Committee Chairwoman

Nydia Velazquez said a lack of borrower data “has left unanswered questions as to whether

taxpayer funding is going to those the program was intended to serve. Before Congress allocates

billions of additional dollars, the administration must show a greater commitment to

transparency.”

7

In fact, the SBA had just released a trove of PPP data voluntarily that showed small

businesses in the manufacturing and health care/social assistance sectors were approved for more

than $58 billion in loans, or nearly one-quarter of the total approved dollars as of the date that

PPP funds expired.

8

According to the North American Industry Classification System (NAICS),

those sectors included businesses that manufacture medical equipment and pharmaceuticals,

9

and

establishments providing health care and social assistance for individuals, among many other

important businesses.

10

The lapse in PPP funding harmed the most vulnerable enterprises. On April 15, 2020,

Citigroup, JPMorgan Chase, and Bank of America provided data that showed the nation’s largest

financial institutions are focused on ensuring PPP and other relief loans are available to a diverse

group of people and entities. For example, Citigroup received nearly 500 applications from not-

for-profit clients including churches, skills training programs, and schools for people with special

needs and at-risk students.

11

JPMorgan Chase established a new program to focus on

underserved entrepreneurs, including women and racial/ethnic minority owners and hardest hit

communities.

12

Bank of America conducted extensive outreach to small business clients in low

and moderate income (LMI) neighborhoods to raise awareness about PPP loans.

13

As Democrats attempted to leverage the desperation of the small business community to

push partisan policies, the need for PPP loans remained urgent, and the queue disproportionately

consisted of small, family-owned, and independent businesses and independent contractors.

Indeed, due to the tactics of Speaker Pelosi and Minority Leader Schumer, PPP funds ran out on

6

Supra n. 12. See also Erica Werner, Mike DeBonis, Worried that $2 trillion law wasn’t enough, Trump and

Congressional leaders converge on need for new coronavirus economic package, Washington Post, (Apr. 6, 2020),

https://www.washingtonpost.com/us-policy/2020/04/06/trump-democrats-coronavirus-stimulus-trillion/

7

Warmbrodt, Everett, and Caygle, supra note 3.

8

SBA Payroll Protection Program (PPP) Report, Approvals Through 4/13/20 (Apr. 14, 2020),

https://content.sba.gov/sites/default/files/2020-04/PPP%20Report%20SBA%204.14.20%20%20-%20%20Read-

Only.pdf (last accessed Apr. 16, 2020).

9

NAICS Sector 32: Manufacturing.

10

NAICS Sector 62: Health Care and Social Assistance.

11

Letter from David Chubak, Head of U.S. Retail Banking, Citigroup, to Hon. Maxine Waters and Hon. Nydia

Velazquez (Apr. 15, 2020).

12

Letter from Jason Rosenberg, Head of U.S. Gov’t Relations, JPMorgan Chase & Co., to Hon. Maxine Waters and

Hon. Nydia Velazquez (Apr. 15, 2020).

13

Letter from John Collingwood, Dir., Fed. Gov’t Relations, Bank of America, to Hon. Maxine Waters and Hon.

Nydia Velazquez (Apr. 15, 2020).

Page 7 of 23

April 16, 2020.

14

As a result, hundreds of thousands of small businesses were unable to access

PPP funds and had to consider layoffs and furloughs.

15

On April 24, 2020, President Trump signed the Paycheck Protection Program and Health

Care Enhancement Act, providing an additional $310 billion in PPP funds.

16

These funds

provided desperately needed relief to small businesses across the country, but the damage was

already done. Many small businesses that missed the first round of PPP funds were unable to

bring back their employees and discontinued services.

17

14

Thomas Franck, Small Business rescue loan program hits $349 billion limit and is now out of money, CNBC,

(Apr. 16, 2020), https://www.cnbc.com/2020/04/16/small-business-rescue-loan-program-hits-349-billion-limit-and-

is-now-out-of-money.html.

15

Tom Huddleston Jr., As small business loan money runs out, many approved businesses still await checks or

clarity on strict guidelines, CNBC, (Apr. 17, 2020), https://www.cnbc.com/2020/04/17/small-businesses-await-

checks-clarity-as-ppp-loan-program-runs-dry.html.

16

Lisa Nagele-Piazza, Trump Signs Coronavirus Relief Bill with $310 Billion More for Small Businesses, SHRM,

(Apr. 24, 2020), https://www.shrm.org/resourcesandtools/legal-and-compliance/employment-law/pages/house-

approves-small-business-coronavirus-relief.aspx

17

Id.

Page 8 of 23

THE ADMINISTRATION’S GUIDANCE FOR PROGRAM LENDING

SBA and Treasury Guidance

Five days after the passage of the CARES Act, on April 2, 2020, SBA posted the Interim

Final Rule (IFR) implementing the Paycheck Protection Program, and on April 3, 2020, released

the affiliation rules so small businesses and lenders could easily determine whether they

qualified for the program.

18

Through April 30, SBA issued five more IFRs and 39 FAQs to

address many aspects of the PPP implementation.

19

The IFRs and FAQs were necessary to

quickly respond to new issues within the rapidly evolving and unprecedented program.

20

Lenders

were frustrated by the evolving nature of the guidance but their employees worked tirelessly to

adapt their interactions with applicants to push the program forward.

On April 23, 2020, in an effort to ensure loans were going to small businesses in need,

SBA and Treasury updated PPP FAQ guidance. The updated guidance stated “a public company

with substantial market value and access to capital markets “is unlikely to be able to make the

certification on its PPP application in good faith that “[c]urrent economic uncertainty makes this

loan request necessary to support the ongoing operations of the Applicant.”

21

Borrowers that

falsely certify their loan application must repay PPP loans in full by May 7, 2020, or else face

agency scrutiny of the loan applications, which carries the possibility of a criminal referral.

22

SBA and Treasury provided private-equity-owned businesses the same opportunity to repay their

loans to avoid such scrutiny.

23

On April 29, 2020, SBA and Treasury created a dedicated window for accepting PPP

applications from “the smallest lenders and their small business customers.”

24

During that

window, SBA only accepted loans from small lending institutions with asset sizes less than $1

billion because many of these lenders served different communities than their larger

counterparts.

25

This dedicated window guaranteed the smallest borrowers had access to funds.

During the course of the Subcommittee’s investigation, Democrats stated certain banks were

unnecessarily limiting access to the PPP to existing customers to the detriment of applicants who

lacked pre-existing banking relationships. Documents and information obtained by the

Subcommittee, however, show lenders were constrained by the requirements to vet new

18

SMALL BUSINESS ADMINISTRATION OFFICE OF THE INSPECTOR GENERAL, FLASH REPORT SMALL BUSINESS

ADMINISTRATION’S IMPLEMENTATION OF THE PAYCHECK PROTECTION PROGRAM REQUIREMENTS, (May 8, 2020),

https://www.sba.gov/sites/default/files/2020-05/SBA_OIG_Report_20-14_508.pdf

19

Id.

20

Id.

21

U.S. Small Bus. Admin., Paycheck Protection Program Loans Frequently Asked Questions (Jun. 25, 2020),

https://home.treasury.gov/system/files/136/Paycheck-Protection-Program-Frequently-Asked-Questions.pdf

(emphasis added).

22

Id.

23

Id.

24

Press Release, U.S. Small Bus. Admin., Joint Statement by Administrator Jovita Carranza and Secretary Steven T.

Mnuchin on Establishing Dedicated Hours for Small Lender Submissions of PPP Applications (Apr. 29, 2020),

https://www.sba.gov/about-sba/sba-newsroom/press-releases-media-advisories/joint-statement-administrator-jovita-

carranza-and-secretary-steven-t-mnuchin-establishing-dedicated

25

Id.

Page 9 of 23

customers pursuant to the Bank Secrecy Act, also known as the Anti-Money Laundering law

(BSA/AML) – statutes aimed at thwarting criminal activity and terrorist financing.

On April 30, 2020, SBA and Treasury issued an IFR stating that “businesses that are part

of a single corporate group shall in no event receive more than $20 [million] of PPP loans in the

aggregate.” Businesses are part of a single corporate group if they are majority owned, directly

or indirectly, by a common parent. The limitation goes into effect for any loan that has not been

fully disbursed as of April 30, 2020. It is the PPP loan applicant's responsibility to notify the

lender if the applicant has applied for or received PPP loans in excess of the amount permitted

and withdraw or request cancellation of any pending PPP loan application or approved PPP loan

not in compliance with the limitation.

Since April 30, SBA and Treasury have continued to respond to all manner of questions

from small businesses, financial institutions, Congress, and the public on the implementation of

the PPP.

26

These responses include 16 additional IFRs and guidance documents, near daily

updates of the FAQs, and additional information for the loan forgiveness process.

27

SBA’s rapid

response has enabled it to quickly and efficiently implement the PPP saving millions of small

businesses and American jobs.

PPP Loan Forgiveness

Loan forgiveness is dependent upon an employer maintaining or quickly rehiring

employees and maintaining salary levels.

28

To qualify for loan forgiveness, employers may use

PPP funds on payroll, payments of mortgage interest, rent, and utilities.

29

Originally, employers

were required to use 75 percent of PPP funds received on payroll costs within eight weeks in

order to qualify for forgiveness.

30

In response to concerns from borrowers whose unique

circumstances made it difficult to comply with the eight week deadline, Congress responded and

on June 5, President Trump signed the PPP Flexibility Act, which reduced the payroll obligation

to 60 percent and increased the expenditure period to 24-weeks or December 31, 2020,

whichever comes first, to qualify for forgiveness.

31

All these actions ensured the smallest businesses got relief quickly. Instead of helping

American workers, Democrats bullied companies that complied with the terms of PPP loan and

fought against extending the program.

32

President Trump and his Administration provided

lenders and borrowers with the guidance necessary to make PPP a success.

26

U.S. Small Business Administration, Paycheck Protection Program, https://www.sba.gov/funding-

programs/loans/coronavirus-relief-options/paycheck-protection-program

27

Id.

28

13 C.F.R. 120 (2020).

29

Id. see also

30

Id.

31

PPP Flexibility Act of 2020, Pub. L. No. 116-142.

32

SELECT SUBCOMM. ON THE CORONAVIRUS CRISIS, HOUSE CORONAVIRUS PANEL DEMANDS THAT LARGE PUBLIC

CORPORATIONS RETURN TAXPAYER FUNDS INTENDED FOR SMALL BUSINESSES, (May 8, 2020),

https://coronavirus.house.gov/news/letters/letter-ceo-tim-abood-evo-transportation-energy-services-inc, (Letters

from Chairman Clyburn to EVO Transportation & Energy Services, Inc., Gulf Island Fabrication, Inc., MiMedx

Group, Inc., Quantum Corporation, and Universal Stainless & Alloy Products, Inc.). See also supra n. 13.

Page 10 of 23

OVERVIEW OF THE SELECT SUBCOMMITTEE DEMOCRATS’ PARTISAN

INVESTIGATION

On June 15, 2020, Select Subcommittee Democrats initiated a partisan investigation into

the disbursement of PPP funds by sending letters to the Treasury Department, SBA and eight

banks (JPMorgan Chase, Bank of America, PNC Bank, Truist Bank, Wells Fargo Bank, U.S.

Bank, Citibank, and Santander) seeking thousands of documents and written responses.

33

These

letters came as banks were still working to get PPP funds to small businesses across the country,

and made baseless accusations that banks had created a two-tiered system benefiting the most

wealthy clients.

34

All eight banks responded to the Democrats’ burdensome requests by June 29, 2020, with

thousands of documents, detailed responses to the Democrats’ questions, and lengthy virtual

briefings to Select Subcommittee staff.

35

After receiving these responses, Ranking Member

Steve Scalise wrote Chairman James Clyburn urging him to narrow his inquiry because the

evidence available to the Select Subcommittee “shows the systems [the banks] built – in a matter

of weeks – did not consider an applicant’s wealth, as you allege. In fact, bank staff who

processed and submitted applications to SBA had no way to determine whether an application

came from an existing client or a new customer.”

36

Documents and Information Show Democrat Allegations Are Wrong

The evidence clearly shows that the Democrats mischaracterized why banks processed

categories of applications in different ways, and confirmed that the banks were limited by the

requirement to collect and verify BSA/AML information from any new customers.

37

The

information required from new customers is extensive to prevent money laundering, and failure

to abide by those requirements can carry significant fines. Financial institutions therefore take

BSA/AML requirements very seriously.

38

The evidence shows the regulatory framework for the

banking and lending industries made implementation of such an enormous program difficult.

Banks are particularly concerned with the BSA/AML risks of new small business clients

because small businesses are more likely than medium and large businesses to be used as shell

33

Select Subcomm. on the Coronavirus Crisis, Select Subcommittee Launches Investigation into Disbursement of

PPP Funds, (Jun. 15, 2020), https://coronavirus.house.gov/news/letters/select-subcommittee-launches-investigation-

disbursement-ppp-funds.

34

Id.

35

Documents on file with the Select Subcommittee on the Coronavirus Crisis.

36

Letter from Steve Scalise, Ranking Member, Select Subcomm. on the Coronavirus Crisis, to James Clyburn,

Chairman, Select Subcomm. on the Coronavirus Crisis, (Jul 2, 2020) (citing numerous briefings from some of the

largest PPP lender banks), https://republicans-oversight.house.gov/wp-content/uploads/2020/07/Scalise-to-Clyburn-

re-withdraw-PPP-requests.pdf

37

Id.

38

Know Your Customer in Banking, Thales Group, (2019), https://www.thalesgroup.com/en/markets/digital-

identity-and-security/banking-payment/issuance/id-verification/know-your-customer

Page 11 of 23

companies for money laundering.

39

BSA/AML violations carry potential monetary penalties of

millions of dollars for financial institution’s negligence or willful violation.

40

Employees of

financial institutions also share BSA/AML risk because violations can result in criminal fines of

$250,000 and up to five years in prison.

41

Recent legislative proposals to amend the BSA would

create new information requirements for small businesses to enable law enforcement and

financial institutions to better identify entities being used for money laundering.

42

While these

legislative proposals are still being negotiated they highlight the risks associated with small

business lending, in particular the need for rigorous review of new customers’ information and

continuous review of existing client information.

Overview of the PPP Lending Process

Every financial institution created a proprietary approval process to suit its existing

infrastructure and potential customers. Each one also made individual decisions including: (1)

whether to serve new customers or only existing customers, (2) how to engage in outreach within

their communities, (3) how to target minority or underserved communities and businesses, and

(4) whether to proceed on a first come, first served basis or provide preference to a certain

category of applicants. Some financial institutions chose to only provide loans to existing

customers due to concerns that they would be unable to conduct adequate research into the

background of those companies to meet their obligations under the Anti-Money Laundering and

Bank Secrecy Act (BSA/AML).

43

The need to quickly develop the online or manual infrastructure to process thousands of

applications required banks to make decisions that in any other circumstance would likely take

months of review. SBA and the Treasury Department enabled banks to make their own decisions

within a set framework in order to get PPP funds to small businesses in need. Congress was clear

that the goal for SBA, the Treasury Department and the banks was to get funds to small

businesses as quickly as possible while still meeting regulatory requirements. This effort did not

come without challenges. Banks told the Subcommittee they struggled to establish online portals

for small businesses to apply, their systems were inundated with applications, and transmitting

the information to the SBA was initially problematic.

44

39

Kristin Broughton, Small Businesses Brace for Compliance Hurdles Under Shell-Company Bills, Wall Street

Journal, (Nov. 3, 2019), https://www.wsj.com/articles/small-businesses-brace-for-compliance-hurdles-under-shell-

company-bills-11572782401.

40

Shari Pogach, et. al., BSA Violation Civil Penalties Increase, National Association of Federally-Insured Credit

Unions, (Nov. 13, 2019), https://www.nafcu.org/compliance-blog/bsa-violation-civil-penalties-

increase#:~:text=As%20the%20chart%20indicates%2C%20a,range%20from%20%2457%2C317%20to%20%24229

%2C269.

41

Id.

42

Supra n. 1.

43

Bank Secrecy Act (BSA) & Related Regulations, Office of the Comptroller of Currency Dep’t of the Treasury,

(last visited Aug. 14, 2020); AML/BSA was created to in 1970 to combat money laundering by requiring financial

institutions to keep detailed records, report suspicious activities, and work with government agencies. Among the

many requirements is one called Know Your Customer (KYC) which requires a financial institution to verify the

identity of a client opening an account and over time. Failure to abide by KYC regulations can carry significant fines

therefore financial institutions take it very seriously and include it in their risk assessment protocols for any new

customer.

44

Briefing from Banks for SSOCC Staff (June 29 – July 6, 2020).

Page 12 of 23

Generally, the process for borrowers was very similar regardless of the financial

institution that processed the loan application. Below is a general description of the application

process:

1. The client completes the SBA Paycheck Protection Program Borrower Application Form

on the lender’s website.

2. The application goes through the financial institution’s eligibility check, based on SBA

eligibility guidelines. Some financial institutions implemented additional checks to

determine whether the potential borrower had an existing relationship with the financial

institution.

3. The financial institution may require additional information or corrections to incomplete

information provided by the client.

4. The application is sent to SBA for approval through the E-Transaction (E-Tran) system.

5. The SBA approves or denies the application.

6. If approved, the client is provided with documentation related to the terms of the PPP

loan and offered the opportunity to sign the loan documents.

7. The client receives the loan distribution.

PPP Data for Select Financial Institutions

JPMorgan Chase & Co.

• Total Loans: 280,000+

• Total Amount: $29 billion+

• Average Loan: $104,760

45

JPMorgan Chase & Co. (JPM) launched its digital intake form on April 3. Within one

hour, they received more than 75,000 expressions of interest from clients and non-clients.

46

JPM

initially chose to serve only existing clients who had an account open with the bank prior to

February 15, 2020.

47

In a letter to Treasury and SBA on April 6, 2020, JPM stated that the need

for a lender to have “exercised due diligence to obtain true and correct information,” conflicted

with the SBA Interim Final Rule, in SBA Form 2484, which set forth relaxed due diligence

requirement intent on getting funds to businesses quickly.

48

While there was an initial lack of

clarity, that was resolved and most other major financial institutions allowed non-customers to

apply for PPP funds, though JPM has maintained they will only provide PPP loans to existing

45

Supra n. 4.

46

HSSC_JPMC_00000013

47

HSSC_JPMC_00000074

48

HSSC_JPMC_00000002-00000005

Page 13 of 23

customers. The week before the Paycheck Protection Program and Health Care Enhancement

Act was signed, JPM’s focused on underserved communities and worked to develop a plan for

outreach to such communities. JPM submitted loan applications to SBA on a first come first

serve basis.

49

Citi Group Inc.

• Total Loans: 29,000+

• Total Amount: $3.3 billion+

• Average Loan: $175,000

50

Prior to the PPP program, Citi Group Inc. (Citi) did not have a digital lending capability

for small businesses, instead requiring small businesses to go to the bank’s physical locations to

apply for a small business loan.

51

As it became clear that PPP was going to be included in the

CARES Act, Citi began working with Fundation, a company that specializes in small business

lending capabilities, to create a digital lending capability for small businesses in less than three

weeks.

52

Citi required Fundation to complete the BSA/AML Know-Your-Customer (KYC)

verification and any mismatches were reviewed by a Citi branch KYC team.

53

Additionally, Citi

still required loans of more than $1 million to go through a separate more difficult underwriting

process to reduce the risks associated with larger loans.

54

Citi operated on a “first in first out” basis and no loan amount preference was given to

any borrower.

55

Citi made a $100 million commitment to get PPP loans to the communities

hardest hit by the coronavirus crisis. That commitment contained a partnership with Community

Development Financial Institutions (CDFIs) to get funds to underserved communities. Citi

recognized that “not taking non-customers might create a heightened risk of disparate impact on

minority and women-owned businesses.”

56

Citi provided loans to only existing customers due to

BSA/AML concerns, then opened the program to non-customers after working with their risk

management team to develop controls to limit their risks.

57

49

Tel. Call, JPMorgan Chase Staff and minority staff, Select Subcomm. on the Coronavirus Crisis H. Comm. on

Oversight & Reform (Jul. 6, 2020).

50

Letter From David Chubak, Head of U.S. Retail Banking, Citigroup, to James Clyburn, Chairman, Select

Subcomm. on the Coronavirus Crisis, (Jun. 29, 2020).

51

CITI_PPP_00000037

52

CITI_PPP_00000005

53

CITI_PPP_00000011.jpg

54

CITI_PPP_00000112

55

CITI_PPP_00000112

56

Id.

57

CITI_PPP_00000186

Page 14 of 23

Bank of America

• Total Loans: 343,000+

• Total Amount: $25.5 billion+

• Average Loan: $74,376

58

Bank of America (BofA) was able to leverage its existing systems to begin accepting PPP

applications at 9:00 a.m. on April 3, 2020, making them the first financial institution to begin

accepting PPP applications.

59

While these capabilities enabled BofA to quickly accept

applications for clients with pre-existing business relationships, the bank still had AML concerns

for businesses without a pre-existing relationship.

60

BofA was accused but has denied that it

prioritized larger clients, citing that near the end of the first round of funding the bank focused on

the smallest loan applications first.

61

BofA conducted outreach to existing small business clients, and clients in low- and

moderate-income (LMI) areas to get them involved in the process.

62

In addition, BofA

committed $250 million to CDFIs and Minority Depository Institutions (MDIs) to provide funds

to underserved communities.

63

More than 74,000 loans went to businesses in low- and moderate-

income areas.

64

Wells Fargo

• Total Loans: 194,000+

• Total Amount: $10.5 billion+

• Average Loan: $54,501

65

Wells Fargo began accepting expressions of interest on April 4, while the bank began

preparing an online application.

66

During this time, Wells Fargo also began conducting outreach

to its existing customers.

67

Wells Fargo began accepting PPP applications on April 6.

68

Due to

the pre-existing asset cap imposed on Wells Fargo by the Federal Reserve, the bank initially

provided $10 billion in loans to non-profits and businesses with fewer than 50 employees.

69

On

April 8, the Federal Reserve temporarily relaxed these restrictions, and Wells Fargo expanded its

58

Supra n.4.

59

Supra n. 54.

60

Id.

61

Id.

62

Letter from Reginald Brown et. al, att’y WilmerHale, to James Clyburn, Chairman of the Select Subcomm. on the

Coronavirus Crisis, (Jun. 29, 2020).

63

Id.

64

Id.

65

Supra n. 4.

66

Letter from Steve Troutner, Head of Small Business at Wells Fargo, to James Clyburn, Chairman of the Select

Subcomm. on the Coronavirus Crisis, (Jun. 29, 2020).

67

Id.

68

Id.

69

WF-Subcommittee-00000159-00000162. See also, WF-Subcommittee-00001075-1079

Page 15 of 23

PPP loan capabilities to their small business customers with more than 50 employees.

70

Wells

Fargo had three requirements for PPP loan eligibility for businesses: (1) meet SBA’s eligibility

requirements; (2) have a Wells Fargo business checking account as of February 15, 2020; and (3)

be enrolled in one of Wells Fargo’s online banking platforms.

71

The second requirement was

based on Wells Fargo’s determination that in order to meet its BSA/AML obligations without

causing significant delays in getting funding to businesses, they could only service existing

customers.

72

Applications were transmitted to SBA on a first come, first served basis.

In addition, 41 percent of Wells Fargo’s PPP loans went to low- and moderate-income

areas or to areas with over 50 percent minority populations.

Truist

• Total Loans: 82,000+

• Total Amount: $12 billion+

• Average Loan: $153,956

73

Truist began accepting PPP loan applications on April 4.

74

Truist received a significant

number of PPP applications between April 4 and April 7, but many of these businesses missed

the first round of PPP funds.

75

As a result, Truist prioritized the applications received on those

dates for the second round of funding, regardless of whether another application was ready for

approval.

76

If Truist’s underwriters determined that the amount a client could receive was less

than the client’s PPP worksheet or less than the E-Tran determination, Truist would adjust the

amount down to the underwriter’s determination, without communicating that with the client.

77

If

the underwriters determined that the amount a client could receive was more than the E-Tran

amount, within $500, they would fund the higher loan amount.

78

If the difference was greater

than $500, Truist would work with SBA to make the appropriate adjustment.

79

Truist worked hard to serve as many existing business clients as possible during the first

round of PPP funding and well into the second round.

80

Truist opened the application process to

sole proprietors and non-business clients in accordance with the proscribed SBA schedule.

81

During the second round of funding, Truist began accepting existing clients without an existing

70

Id.

71

Supra n. 63.

72

Id.

73

Supra n. 4.

74

Truist_PPP_0001964.

75

Truist_PPP_0001455.

76

Id.

77

Truist_PPP_0001456.

78

Id.

79

Id.

80

Truist_PPP_0001177

81

Email from Peter Mahoney, Executive Vice President, Truist, to Republican Staff, Select Subcomm. on the

Coronavirus Crisis, (Aug. 26, 2020, 1:11p.m.).

Page 16 of 23

business relationship.

82

The company’s retail banks also began outreach within their local

communities to existing customers that owned and operated small businesses.

83

U.S. Bank

• Total Loans: 108,000+

• Total Amount: $7.6 billion+

• Average Loan: $70,212

84

U.S. Bank launched its online platform for accepting applications on April 4, for single-

owned businesses.

85

A few days later, the company expanded lending to dual-owned businesses,

and on April 19, for multi-owner businesses.

86

The technical rollout of the online platform was

delayed, particularly during round one of PPP funding, causing some applications for multi-

owner businesses to need to be input manually.

87

Those technical issues were quickly addressed

and only three percent of the U.S. Bank PPP loan applications required manual applications.

88

On June 19, U.S. Bank stopped accepting PPP loan applications even though there was more

than $130 billion left in available PPP funds.

89

U.S. Bank has said it is shifting its focus to

preparing for and managing the loan-forgiveness phase of PPP, though it is unclear how many

resources will be necessary for this portion of the program.

90

Only 10 percent of U.S. Bank’s PPP loan applications came from new customers, though

new customers were not included until round two. U.S. Bank was largely a first come, first

served provider of PPP loans, however, new customer applications took longer to process due to

BSA/AML requirements. In June, U.S. Bank prioritized direct outreach to minority-owned

business customers.

91

Around 23.9 percent of U.S. Bank’s PPP loans went to LMI communities

and 8.7 percent of their loans went to rural areas.

92

U.S. Bank also provided $50 million to seven

CDFIs focused on providing funds to women and minority-owned businesses, and LMIs.

PNC Bank

• Total Loans: 73,000+

• Total Amount: $13 billion+

• Average Loan: $175,906

93

82

Truist_PPP_0001299

83

Id.

84

Supra n. 4.

85

Letter from Timothy Welsh, Vice Chair, Consumer and Business Banking, U.S. Bank, to James Clyburn,

Chairman, Select Subcomm. on the Coronavirus Crisis, (Jun. 29, 2020).

86

Id.

87

Id.

88

Id.

89

Id.

90

Id.

91

Id.

92

Id.

93

Supra n. 4.

Page 17 of 23

PNC Bank built a new online portal to accept PPP loan applications, which launched on

April 4, 2020.

94

PNC resolved some early technical difficulties and quickly and efficiently

processed applications.

95

PNC chose to only accept PPP applications from existing customers

“[d]ue to the Bank Secrecy Act and anti-money launder (BSA/AML) compliance obligations . . .

as well as the volume of PPP applications that we expected to (and did) receive from existing

PNC customers.”

96

PNC dedicated more than 4,000 employees to processing PPP applications.

97

This

massive effort enabled PNC to provide more than 85 percent of its loans to businesses with less

than $5 million in annual revenues.

98

PNC did not prioritize applicants from larger businesses, or

prioritize based on the requested loan.

99

PNC also specifically targeted small businesses in LMI

communities soon after the PPP went online.

100

As a result, they provided more than $3.3 billion

in loans to small businesses in LMI communities.

101

PNC also committed more than $45 million

to eight CDFIs starting in March of 2020, even before the PPP was created.

102

Santander

• Total Loans: 10,700+

• Total Amount: $1.2 billion+

• Average Loan: $112,150

103

Prior to the start of the PPP, Santander averaged between 25 and 30 SBA loan

applications per month, but did not have a digital platform for SBA loans.

104

Santander

contracted with a technology vendor to develop a digital platform for the PPP applications, while

the bank made an expression of interest form available to begin collecting customer interest and

information.

105

The vendor was unable to provide the platform, requiring manual entry and

causing a delay in Santander’s ability to process loan applications.

106

After the first round of

PPP, Santander continued processing applications into a batch in preparation for Congress’

approval of a second round of PPP funding.

107

During this time, Santander also streamlined its

manual submission process.

108

Santander is a smaller financial institution and did not have a

digital platform to meet BSA/AML requirements which partially delayed their ability to quickly

94

Letter from Lakhibir Lamba, Executive Vice President, Head of Retail Lending and Asset Resolution, PNC Bank,

to James Clyburn, Chairman, Select Subcomm. on the Coronavirus Crisis, (Jun. 29, 2020).

95

Id.

96

Id.

97

Id.

98

Id.

99

Id.

100

Id.

101

Id.

102

Id.

103

Supra n. 4.

104

Letter from Emily Loeb, Counsel for Santander, to James Clyburn, Chairman of the Select Subcomm. on the

Coronavirus Crisis, (Jun. 29, 2020).

105

Id.

106

Id.

107

Id.

108

Id.

Page 18 of 23

review applications, though they only provided loans to existing customers.

109

Santander

processed loans on a first come, first served basis in batches.

Oriental Bank:

• Total Loans: 4,700+

• Total Amount: $304 million+

• Average Loan: $63,825

110

Banco Popular

• Total Loans: 28,000+

• Total Amount: $1.42 billion+

• Average Loan: 45,000

111

On August 20 and 21, 2020, leadership of two large banks in Puerto Rico (PR) – Oriental

Bank and Banco Popular – provided voluntary briefings for Subcommittee staff. Bank executives

expressed appreciation for the PPP program and discussed the positive effects it had on the

island. Accounting firms were not deemed essential businesses in Puerto Rico, which made it

difficult for loan applicants to access their financial documents. Employees at both banks went to

extraordinary lengths to provide service for the island’s small business population. Banco

Popular, for instance, kept branches open to provide access to PPP for those applicants who had

no internet access – a vestige of the island’s ongoing remediation from recent hurricanes and

other weather events.

The bank executives stated the program was a success – the PPP saved countless small

businesses on the island. The banks identified the fact that the program was managed by the

federal government, and not the local government, as one of the reasons for its effectiveness.

109

Id.

110

Paycheck Protection Program (PPP) Our numbers, Oriental, (Aug. 18, 2020), https://covid.orientalbank.com/en-

us/ppp.

111

Popular Updates Loans Granted Under the SBA Payroll Protection Program (PPP), Newsroom, (Jul. 8, 2020),

https://newsroom.popular.com/press-release/english/popular-updates-loans-granted-under-sba-payroll-protection-

program-ppp

Page 19 of 23

IMPACTS ON UNDERSERVED COMMUNITIES

On April 24, 2020, President Trump signed the Paycheck Protection Program and Health

Care Enhancement Act (PPPHCEA), which increased the total lending authority in the PPP to

$659 billion, an increase of $310 billion over the $349 billion authorized in the CARES Act. The

PPPHCEA included a set aside of no less than $30 billion for “community financial institutions,”

which includes Community Development Financial Institutions (CDFIs) and Minority

Depository Institutions (MDIs).

The Administration made additional efforts to ensure that PPP loans were reaching small

businesses that need capital. For example, the Department of Treasury and SBA issued

supplemental guidance that required applicants to consider an applicant’s access to other sources

of liquidity before certifying the necessity of their application. Moreover, the SBA and Treasury

committed to reviewing loans in excess of $2 million as part of the forgiveness determination.

112

In addition to the PPP, lenders have taken steps to ensure funding reaches diverse and

vulnerable populations. On April 15, 2020, in response to a request from House Democrats,

lenders such as Citigroup, JPMorgan Chase, and Bank of America provided data highlighting

their work to ensure that PPP is available to a diverse group of customers. For example,

JPMorgan set up a new program to focus on underserved entrepreneurs, including women and

minority owners and those in the hardest hit communities.

113

Additionally, Bank of America

conducted extensive outreach to small business clients in low- and moderate-income

neighborhoods to raise awareness about PPP and other loans facilities.

114

The Administration’s and the financial institutions’ focus on reaching diverse

communities and businesses helped support those hit hardest by the coronavirus. Most financial

institutions made direct outreach to minority-owned businesses and underserved communities

early in the process.

115

Around $117 billion in loans were provided to small businesses in

economically distressed areas known as Historically Underutilized Business (HUB) zones.

116

In

addition, PPP supports 13 million jobs in HUB zones.

117

The PPP program provided $79.8

billion in loans and about 12 million jobs in rural communities.

118

These efforts were all part of a dedicated outreach program by the Trump Administration

to ensure those communities hit hardest by the ongoing pandemic, particularly minority

communities, had access to the relief necessary to withstand the crisis.

112

https://home.treasury.gov/system/files/136/Paycheck-Protection-Program-Frequently-Asked-Questions.pdf.

113

JPMC response to House Democrat Request, April 15, 2020, on file with the Committee. See also

https://www.jpmorganchase.com/corporate/news/pr/eocf-exceeds-9mm-with-new-investments.htm.

114

Bank of America response to House Democrat Request, April 15, 2020, on file with the Committee.

115

Briefings from eight banks for SSOCC staff.

116

Supra n. 5.

117

Id.

118

Supra n. 2.

Page 20 of 23

CONCLUSION

The deliberate actions by President Trump’s Administration, in partnership with financial

institutions, to stand up the PPP program saved the small business community. Small businesses

are the backbone of our nation’s economy, employing more than 58 million Americans. Without

access to PPP loans, the vast majority of small businesses would likely go bankrupt or lay off

employees due to broad economic shutdowns.

SBA has never engaged in a program near the scale of PPP. Yet, through the focused

resolve of the Trump Administration, SBA accepted applications within six days of the passage

of the CARES Act. While there were some challenges implementing the program, as would be

expected in implementing a program of this size on an expedited timeline, SBA processed

applications quickly and avoided fraud to the extent that is typical of disaster relief and other

large government programs, such as those associated with Hurricane Sandy,

119

Hurricane

Katrina,

120

and Medicaid.

121

As the PPP transitions from processing loan applications to reviewing loan forgiveness

applications, SBA should remain vigilant to ensure loan forgiveness only extends to businesses

who complied with the letter of the law. Given the success of the development and

implementation of the program, it is expected SBA will be well positioned to oversee this

process and provide further relief for America’s small businesses, if needed.

President Trump’s leadership guided many of America’s small businesses through this

crisis. Coast to coast, America’s main street is recovering. The policies established by this

Administration will restore the American way of life and rebuild the greatest economy in the

world.

119

Luis Ferre-Sadurni, City Admits Defrauding FEMA After Hurricane Sandy; Agrees to pay $5.3 Million,

NYTimes, (Feb. 20, 2020), https://www.nytimes.com/2019/02/20/nyregion/fema-hurricane-sandy-fraud.html.

120

Sarah Westwood, 10 years later, extent of Katrina fraud still unknown, Washington Examiner, (Aug. 28, 2015),

https://www.washingtonexaminer.com/10-years-later-extent-of-katrina-fraud-still-

unknown#:~:text=Botched%20contracts%2C%20rampant%20fraud%20and,help%20the%20victims%20of%20Katr

ina.&text=A%20Disaster%20Fraud%20Task%20Force,Hurricanes%20Katrina%2C%20Rita%20and%20Wilma.

121

Peter Viechnicki, Shutting down fraud, waste, and abuse, Deloitte, (May 12, 2016),

https://www2.deloitte.com/us/en/insights/industry/public-sector/fraud-waste-and-abuse-in-entitlement-programs-

benefits-fraud.html.

Page 21 of 23

APPENDIX A: KEY STATISTICS

▪ The PPP supports more than 51 million jobs for American workers.

122

o For example, the PPP supports 4.5 million jobs in Texas, 3.2 million in Florida, 1.8

million in Pennsylvania, 1.9 million in Ohio, 1.6 million in Michigan, 1.5 million in

Georgia, and 1.2 million in North Carolina.

123

▪ The PPP obligated $659 billion under the CARES Act and the Paycheck Protection

Program and Health Care Enhancement Act.

124

▪ The PPP supports as much as 84 percent of all small business employees in the country.

125

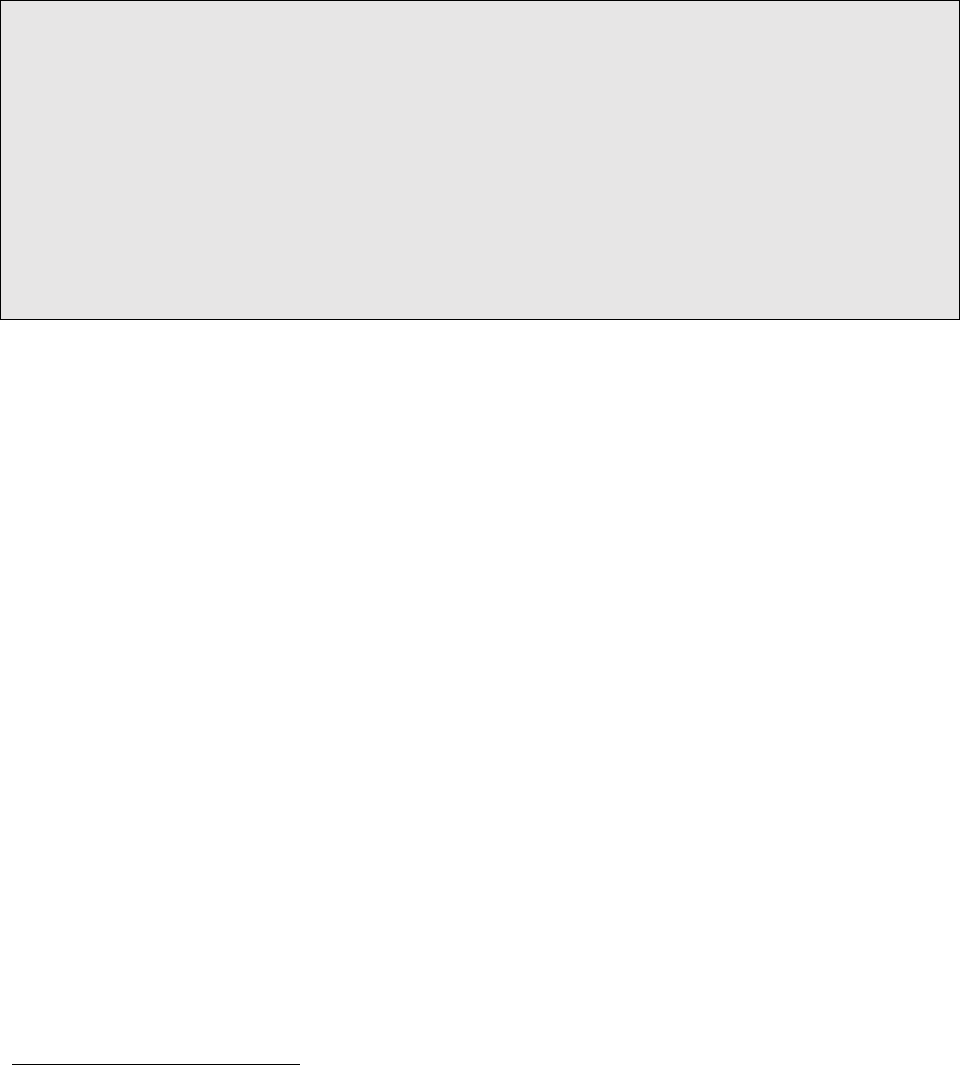

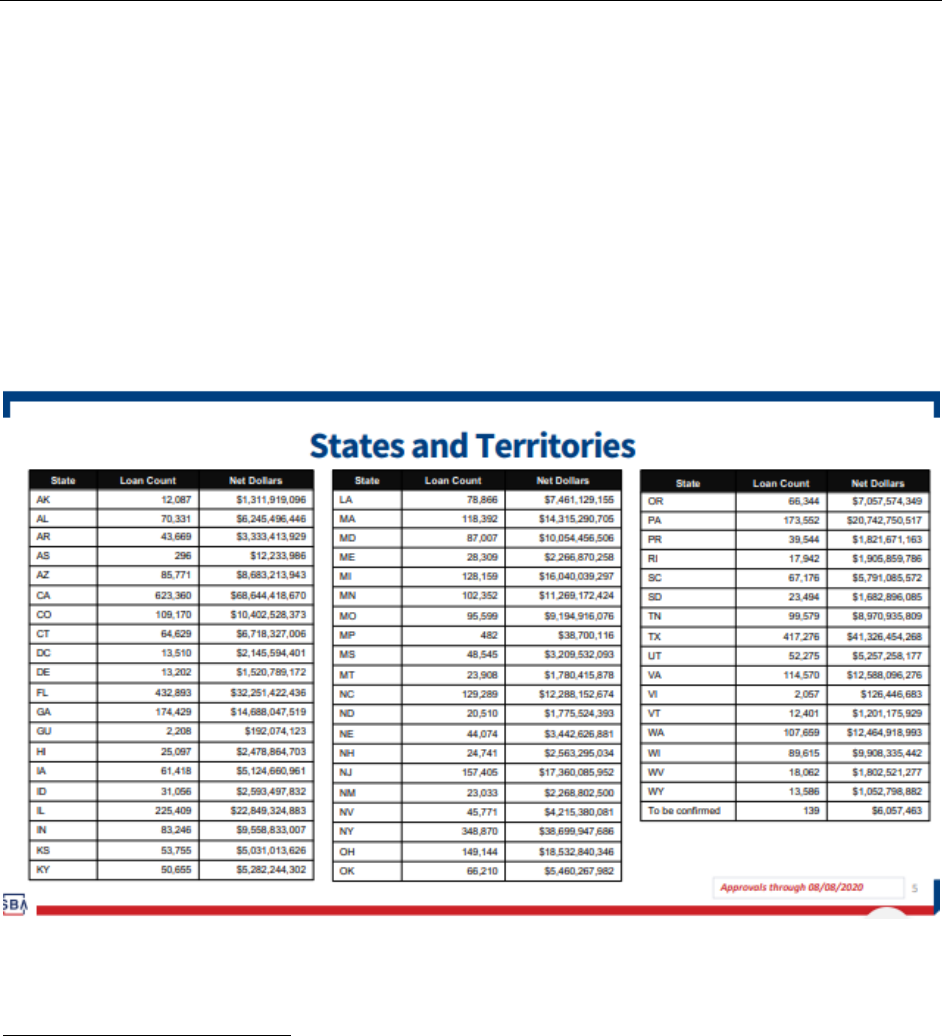

Figure 1: PPP Loans by State and Territory

126

122

U.S. SMALL BUSINESS ADMIN., PAYCHECK PROTECTION PROGRAM (PPP) REPORT (Jun. 30, 2020),

https://home.treasury.gov/system/files/136/PPP-Results-Sunday.pdf

123

Kathy Morris, The States that Received the Most (and Least) in PPP Funds, ZIPPIA (July 2020)

https://www.zippia.com/advice/states-least-most-ppp-loans/.

124

Supra n. 2.

125

U.S. SMALL BUSINESS ADMIN., PAYCHECK PROTECTION PROGRAM (PPP) REPORT (Aug. 8, 2020),

https://home.treasury.gov/system/files/136/SBA-Paycheck-Protection-Program-Loan-Report-Round2.pdf.

126

Id.

Page 22 of 23

▪ The PPP provided loans to nearly 4.9 million small businesses across the country totaling

$521 billion.

127

▪ The PPP sent loans to our nation’s smallest businesses in need, with 87.4 percent of all

loans for less than $150,000 and more that 67 percent for $50,000 or less.

128

▪ As of August 8, the PPP is still funded at over $133 million.

129

127

Id.

128

Id.

129

Id.

Page 23 of 23

APPENDIX B: TIMELINE

▪ March 27: President Trump signed the CARES Act signed into law.

▪ April 2: Treasury published an Interim Final Rule and SBA released an updated

borrower application, lender application form, and updated borrower information sheet.

▪ April 3: SBA began accepting PPP applications.

▪ April 3 – 16: First round of PPP funding.

▪ April 16: $349 billion in CARES Act funding for the PPP was exhausted.

▪ April 16 – 27: Many banks prepared for a second round of funding.

▪ April 24: The Paycheck Protection Program and Health Care Enhancement Act was

passed, providing an additional $310 billion in PPP funds, bringing the total to $659

billion.

▪ April 27: SBA began accepting applications for the second round of funding.

▪ August 8: SBA stopped accepting new PPP applications due to the statutory deadline

leaving roughly $136 billion left in the program.