Michigan Justice for All Commission

REPORT & RECOMMENDATIONS

Advancing Justice for All

in Debt Collection Lawsuits

2

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Since January 2021, the Michigan Justice for All Commission has been working toward creating a

path to a better civil justice system – one that is welcoming, understandable, collaborative, adaptive,

and trusted.

1

To help achieve the goals set forth in its strategic plan, the Commission created the

Debt Collection Work Group, which has developed data-driven recommendations to simplify and

streamline processes, rules, and laws so that people can more effectively navigate court processes

and, when appropriate, address their debt collection cases without the assistance of an attorney. In

addition, the Work Group recommends modernizing long outdated laws to help ensure that courts

are adaptable to an ever-changing world and are seen as a trusted place where both creditors and

consumers can resolve their problems.

With the help of The Pew Charitable Trusts and January Advisors, the Work Group sought to

understand the consumer debt collection landscape in Michigan – the vast majority of which are led

in Michigan’s district courts.

• Debt collection cases are dominating Michigan’s District Court, second in ling rate only to

trafc cases in 2019. Ten plaintiffs le almost three-quarters of debt collection cases.

• Third-party debt collectors are ling more cases in Michigan’s district courts, increasing 40%

over the last decade and constituting 60% of all debt collection cases in 2019. The three

plaintiffs with the highest ling rates are all third-party debt collectors.

• While debt collection cases are led across the state, more cases are led against low- and

moderate-income Michiganders.

• Default judgments are entered in almost 70% of debt collection cases after service is recorded

as complete.

• Racial disparities exist with debt collection litigation.

‒ The ling rate against people living in majority Black communities is two to three times

higher than case lings against people living in majority non-Hispanic White communities.

While the ling rate decreases with increasing income for people living in majority White

communities, the ling rate remains fairly consistent across incomes for people living in

majority Black communities.

‒ People living in majority Black communities are also more likely to have cases led against

them dismiss for failure to serve. Once service was recorded as completed, however,

people living in majority Black communities were more likely to have a default judgment in

their case.

• Once a judgment is entered, the judgment creditors seek garnishments in 78% of cases.

• Creditors are almost always represented in debt collection cases, but consumers are rarely

represented. Legal aid providers lack the resources to offer full representation in the vast

majority of cases. When a consumer is represented by counsel, their case is 10 times more

likely to be dismissed with prejudice and twice as likely to reach a settlement.

Overview

3

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

In addition, the Work Group reviewed the procedures for service of process and rules related to

garnishments in Michigan and found both failed to adapt with technology and our modern nancial

world.

Based on these ndings, the Work Group recommends:

i

1. Modernizing serving of process rules to help ensure that consumers receive notice of the

lawsuit led against them

2. Increasing the amount of information to be included in the complaint to help ensure that the

plaintiff has provided sufcient evidence to support a default judgment

3. Creating court documents and forms that consumers can easily understand and use

4. Improving our understanding of debt collection in Michigan through a more optimized use of

court records

5. Engaging with consumers who have faced debt collection litigation to understand the barriers

they encounter in court processes

6. Developing pilot projects to nd alternatives to litigation that help creditors, consumers, and

courts

i The JFA Debt Collection Work Group discussed and agreed upon several recommendations related to garnishment protections,

which were later determined to be outside the scope of reforms to be addressed by the Justice For All Commission. These

proposed changes, which would modernize and update garnishment protections to protect assets consumers need, included:

a. Protecting at least 40 hours per week at the state minimum wage from paycheck/periodic garnishments;

b. Protecting a minimum amount (40 hours of the state minimum wage) in a bank account from garnishment;

c. Better protecting public benets (specically all federal and state public benets, including unemployment insurance,

veterans, and public assistance benets; and the Earned Income Tax Credit) from garnishment;

d. Protecting the value of an operable vehicle up to $15,000;

e. Protecting the family home at a value of $33,000 (with future adjustments for ination);

f. Increasing protections for tools of the trade to $10,000 (with future adjustments for ination);

g. Increasing protection of personal property to $10,000 (with future adjustments for ination); and

h. Revising garnishment forms to provide consumers with the information they need in an understandable manner.

4

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Work Group Members

The Michigan Justice for All Commission Executive Team invited a broad range of practitioners and

judges with diverse perspectives to participate in the Debt Collection Work Group. The Work Group

was composed of District Court judges, attorneys with experience representing both low- and

moderate-income consumers, attorneys with experience representing creditors, members from the

Attorney General’s ofce, and a consumer law academic.

• Hon. Timothy Kelly

74th District Court, JFA Commission Member, Work Group Co-Chair

• Kathryn Hennessey

Former SBM General Counsel, Work Group Co-Chair

• Prof. Mathew Andres

Clinical Assistant Professor of Law, University of Michigan

• Lorray Brown

Co-Managing Attorney, Michigan Poverty Law Program

• Hon. Michael Carpenter

75th District Court

• Lori Frank

Attorney, Markoff Law PLLC

• Elisa Gomez

Staff Attorney, Lakeshore Legal Aid

• Nicole Huddleston

Attorney, Detroit Justice Center

• Tera Jackson-Davis

Civil Division Director, 36th District Court

• Joseph Jammal

Stenger & Stenger, PC

• Kate Klaus

Shareholder, Maddin Hauser

• Aaron Levin

Assistant Attorney General, Corporate Oversight Division, Michigan Dept of Attorney General

• Michael Nelson

Attorney, Michael Nelson Law

• Robert Phillips

Attorney, Phillips & Phillips, PC

• Scott Teter

Division Chief, Financial Crimes Division, Michigan Dept of Attorney General

Special assistance was provided by Natasha Khwaja, Christopher Blythe, and Samantha Bigelow.

5

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Table of Contents

Overview ......................................................................................................................................2

Work Group Members .............................................................................................................4

Table of Contents ......................................................................................................................5

Introduction .................................................................................................................................6

Debt Collection 101: ................................................................................................................ 8

Findings ............................................................................................................................. 9

Case Filing Policy and Trends ........................................................................................9

Case Outcomes .................................................................................................................22

Post-Judgment .................................................................................................................. 32

Representation .................................................................................................................38

Court Record Data ...........................................................................................................41

Policy Recommendations ...........................................................................................43

Modernize Service of Process Rules ......................................................................... 45

Increase Complaint Requirements ............................................................................49

Create Easy to Use Documents & Forms ................................................................ 53

Optimize Use of Court Records & Data ................................................................... 56

Engage with Consumers who Have Faced Debt Collection Litigation ........ 58

Develop Pilot Projects to Find Alternatives to Litigation ...................................59

Acknowledgments .................................................................................................................60

Appendix A: Methodology .................................................................................................. 61

Appendix B: Example of Summons .................................................................................66

Appendix C: Example of Advice of Rights .................................................................... 67

Endnotes ....................................................................................................................................68

6

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Introduction

Debt collection cases are ooding state civil courts

across the country,

2

and household consumer debt is

on the rise.

3

Michigan is no exception to these trends.

An estimated 26% of all Michiganders with a credit

report have at least one debt in collections, as do

53% of people living in communities of color.

4

Many of

these debts – which can originate as past due credit

card balances, medical bills, or auto loans – will make

their way to Michigan District Courts where, in 2019

alone, over 200,000 debt collection cases were led,

representing a staggering 37% of all civil cases led

in District Court.

Debt collection cases stem from delinquent non-

mortgage consumer debts. While the specic causes

of delinquent consumer debt varies by the individual,

national data on household expenditures suggests

that much of it can be attributed to the “plastic

safety net,” or the use of credit to cover basic living

expenses.

5

In 2019, 37% of Americans reported

that they would be unable to completely cover an

unexpected expense of $400 and would need to

resort to other measures such as putting that amount

on a credit card or borrowing from a bank, payday

lender, or friend or family member.

6

This phenomenon

is particularly pronounced for communities of color,

who have fewer assets, less access to low-interest

credit,

7

and less of an ability to borrow from friends or

family.

8

Consumer debts and the costs added by collection

and litigation also damage credit scores, making

it more difcult to obtain housing, employment, or

small business loans, all of which negatively affect

family wealth building and economic mobility.

9

Credit cards account for around 15% of the value

of all non-mortgage consumer debts in the country;

however, due to the high compound interest rates

often applied, credit cards account for the largest

share of outstanding interest consumers owe on

non-mortgage debts.

10

This means that the amount

of credit card debt recovery sought in debt collection

litigation is often far more than the amount that the

consumer actually spent on goods due to the interest

and fees set forth in the user agreement.

11

Auto debt,

which represents almost 11% of the debt collection

cases led in Michigan, can be particularly

damaging to credit scores and often has a long-term

effect on consumers’ ability to obtain a car for basic

transportation needs.

12

Further, medical debt, which

represents 9% of Michigan’s debt collection cases,

can impact people’s ability to afford basic needs;

a recent national survey on medical debt found

that 63% of Americans with medical debt reported

cutting spending on food, clothing, and other basic

living expenses, and 28% delayed buying a home or

seeking further education to pay off medical debts.

13

While many of the policies and circumstances

that have led to more debt collection lawsuits fall

outside the purview of the judiciary,

14

courts play

an important role in inuencing and managing

debt collection lawsuits. First, courts are a key

source for data and information. When creditors

and debt collectors are unable to collect on a debt

through informal means, they turn to the courts,

which in Michigan is primarily its state District

Courts. Therefore, the data and information District

Courts have on these cases can help policymakers

understand debt collection litigation and its impact

on consumers, creditors, and debt collectors. This

data can further help policy makers identify problems

that occur before litigation is initiated surrounding

areas such as lending practices, access to credit, and

pre-litigation collection efforts. Second, the policies

that states adopt through legislation and court rules

directly impact both creditors and consumers. For

example, some states have policies that further

nancially burden consumers by imposing additional

costs in the form of court fees, attorney’s fees, and

post-judgment interest. In some cases, these costs

are so great that taxpayers are forced to bear the

burden when a consumer is unable to secure housing,

employment, and transportation due to their inability

to pay off the debts they owe.

All too often these cases are a lose-lose-lose situation

for courts, creditors, and consumers. While courts

receive considerable revenue from these cases in the

form of ling fees and court costs,

15

these cases can

overwhelm state courts. In Michigan, debt collection

cases are second only to trafc cases in volume of

civil or criminal case type led in District Courts, and

they take time and resources from court staff who

7

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

are already stretched too thin. While some national

third-party debt buyers have proted by using courts

to collect debts they have purchased for pennies

on the dollar,

16

when pursuing litigation, creditors

incur attorney and court fees with no guarantee of

collecting from the consumer and would often prefer

to reach a voluntary payment agreement with the

consumer prior to commencing suit. For consumers,

these cases can be nancially devastating, resulting

in garnishments of wages, bank accounts, and state

tax returns, and thus jeopardizing their ability to pay

other basic expenses, including rent, utilities, and

groceries.

17

Debt collection cases primarily impact low- and

modest-income households. 50% of debt collection

cases led in Michigan were led in neighborhoods

where the median income was $50,000 or less.

Debt collection lawsuits disparately impact Black

communities.

18

Michiganders living in communities

that are majority Black are 2.4 times as likely to have

a debt in collection compared to people living in

White-majority communities. This disparity plays out

in Michigan’s District Courts as well. At all levels of

neighborhood income, people living in neighborhoods

that are majority Black in Michigan see close to

double the debt collection case ling rate compared to

people living in White-majority neighborhoods.

For the past year, the Michigan Justice for All

Commission Debt Collection Work Group has

partnered with The Pew Charitable Trusts and

January Advisors to nd data-driven solutions to

the problems surrounding debt collection litigation

in Michigan’s District Courts. The Work Group is

composed of individuals with a diverse range of

experiences in debt collection litigation, including

district judges, creditor attorneys, consumer attorneys,

and academics.

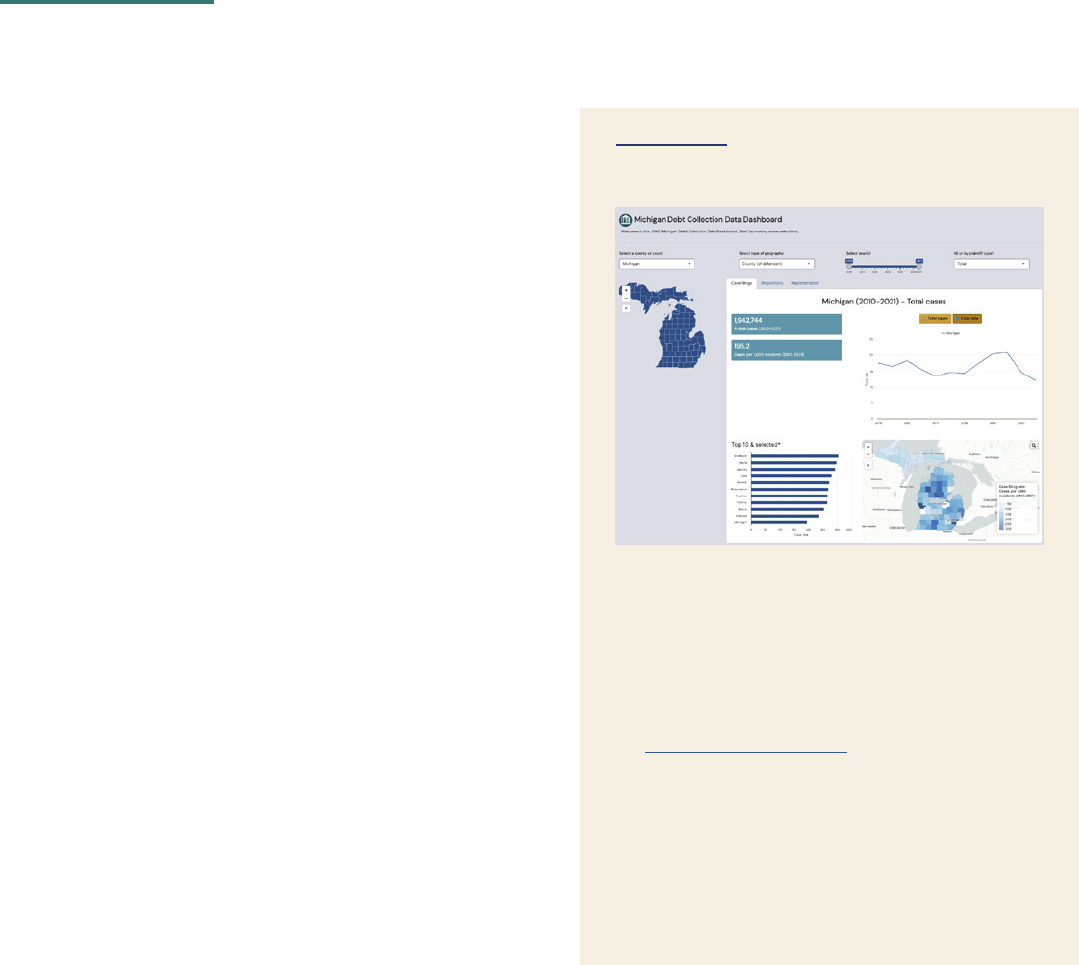

The Work Group reviewed data from the

Judicial Data Warehouse (JDW) and the

Judicial Information System (JIS) from January

2010 to September 2021 to examine rates

and trends in case lings, dispositions, and

various other data points. We have released

an interactive dashboard of debt collection

lawsuits led in Michigan’s District Courts

from 2010-2021 alongside this report. The

dashboard can be ltered by court or county,

year, and plaintiff type. It shows case lling

totals and rates, along with case outcomes

and defendant representation.

Data Dashboard

8

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

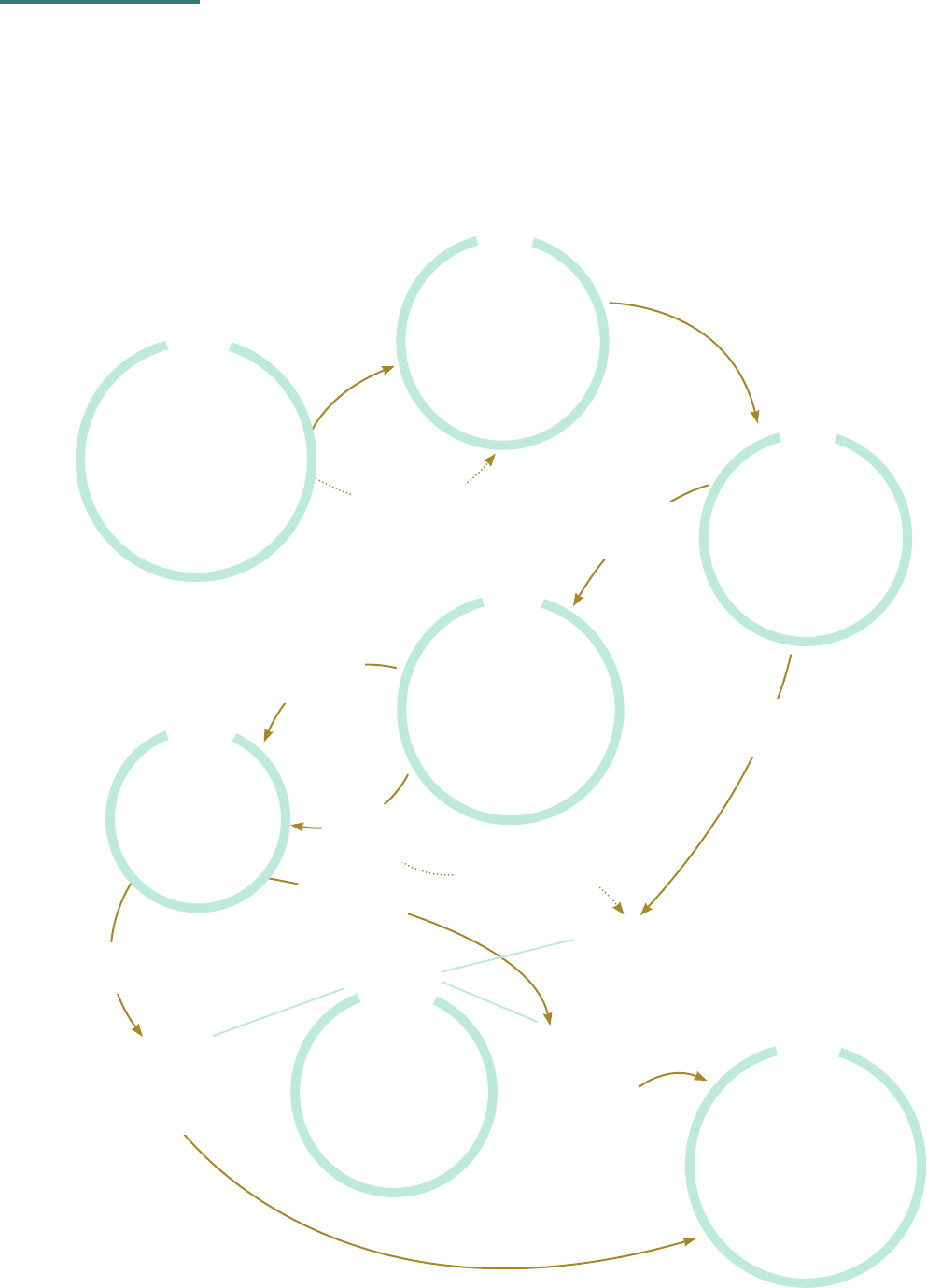

Dismissal:

Court dismisses

the case

7

ENFORCEMENT

If a debt is owed, the

Court may grant the

ability to garnish the

Defendant’s wages,

bank accounts or

tax returns

3

NOTIFICATION

Defendants are

entitled to know a

claim has been led

against them

4

RESPONSE

Defendants can

respond in two ways:

ling a motion to

dismiss or ling an

answer

5

HEARING

A hearing date is

scheduled

Plaintiff is able to

serve Defendant

Default Judgment:

Court enters

judgment without

a hearing

Judgment

(Non-Default or

Stipulated):

Court enters

judgment based on

evidence or

settlement terms

Plaintiff is unable

to serve Defendant

Creditor sells

debt to a

Debt Buyer

1

INITIAL

COLLECTION

ATTEMPTS

Creditor attempts

repayment via email,

phone and mail

2

CASE

INITIATION

Creditor or Debt

Buyer (Plaintiff) les a

complaint and Court

issues a summons

Defendant does

not respond

Defendant

does respond

Plaintiff and

Defendant agree

on settlement

options

6

RESOLUTION

Cases can be

dismissed or court

enters judgment

Defendant

does attend

Defendant does

not attend

Debt Collection 101:

How a Delinquent Debt Becomes a

Garnishment

9

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section A

Findings: Case Filing Policy and Trends

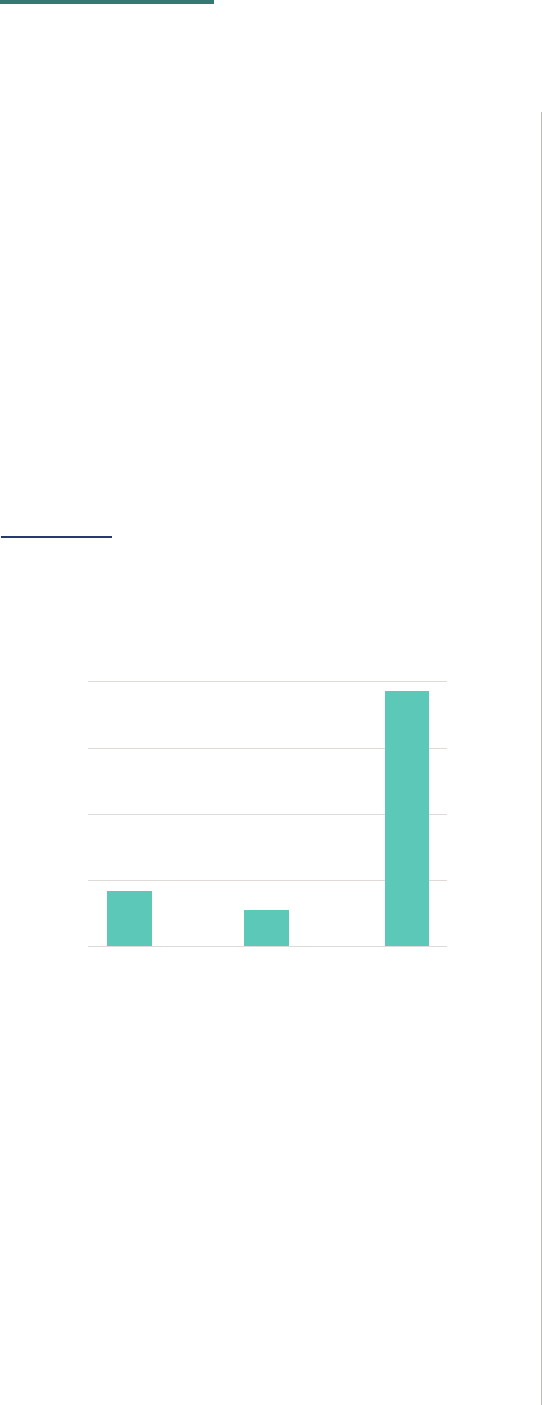

1. Debt collection cases are dominating Michigan’s District Courts.

2. Ten plaintiffs le almost three quarters of debt collection lawsuits in Michigan, a

substantially larger share than other states.

3. Filings by debt buyers have signicantly increased in Michigan.

4. Debt collection cases have relatively low amounts in controversy.

5. Debt collection lawsuits impact consumers across the state.

6. Low-income communities in Michigan have high debt collection case ling rates

7. Black communities in Michigan have high debt collection lings rates across income

levels.

8. Michigan trails other Great Lakes states in debt collection policy reform.

AT A GLANCE

Nationally, debt collection case lings are inundating state civil court dockets, and

third-party debt buyers represent an increasing share of these cases. Findings show

that Michigan reects these national trends, but with some key differences.

10

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section A Findings | Case Filing Policy & Trends

From January 2010 to September 2021, over 1.94

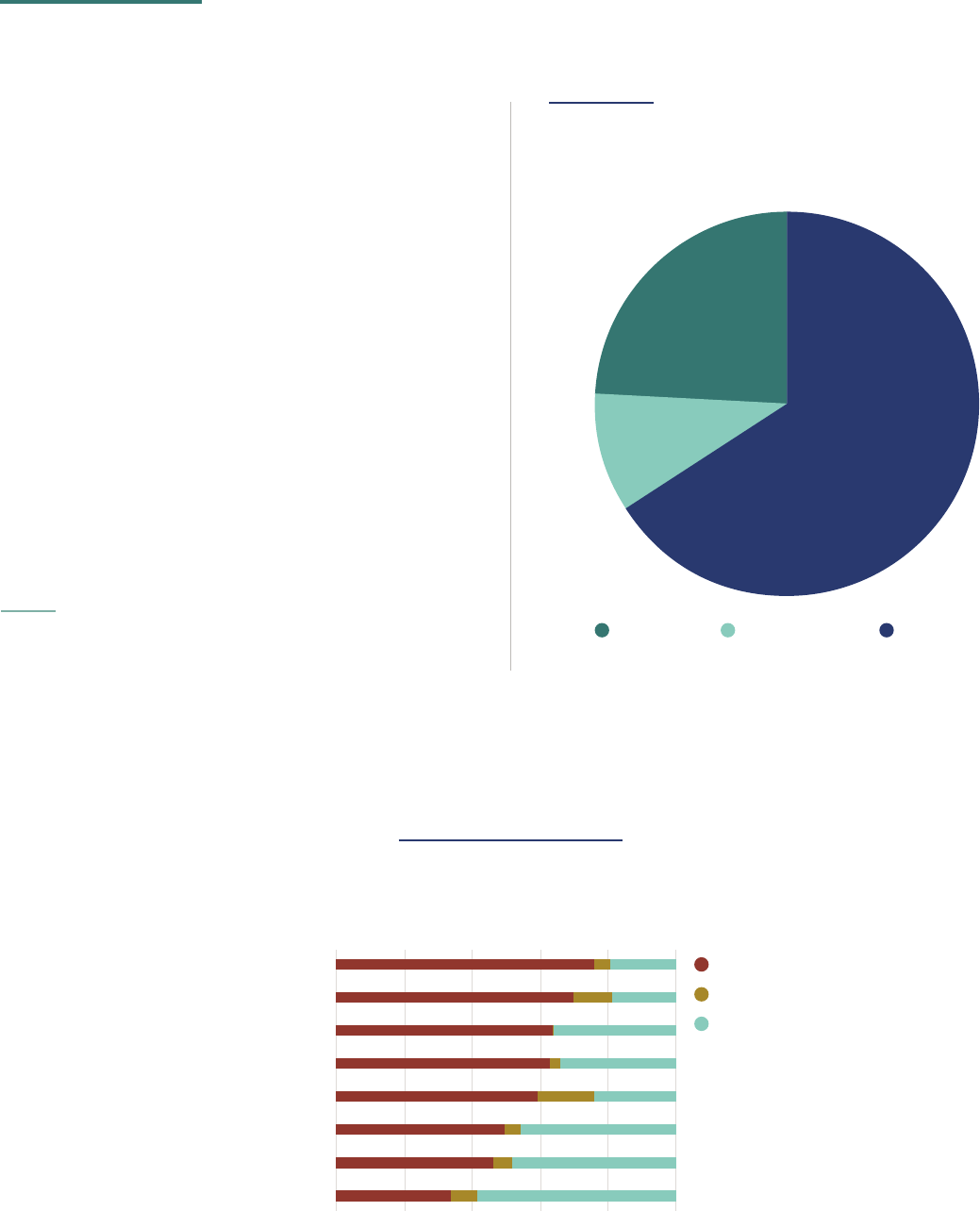

million debt collection cases were led in Michigan

District Courts, representing an estimated $3.1 billion

in controversy.

ii

In 2019, debt collection cases were

second only to trafc cases in the volume of cases

led, representing 9% of all District Court cases and

37% of all civil District Court cases. Debt collection

cases have surpassed summary proceedings as the

most common civil or criminal, non-trafc case type in

Michigan.

The vast majority of cases are led in civil district

court, rather than small claims court. While the

median amount in controversy for these claims is well

below the $6,500 jurisdictional limit for small claims

court,

19

as will be discussed in more detail below,

creditors are almost always represented by counsel,

which disqualies them from small claims court

because Michigan’s small claims court does not allow

parties to be represented by counsel.

20

Credit unions,

however, are one type of creditor that use small

claims court to collect debts, and they are represented

by their staff rather than attorneys. The Work Group

did not focus on these small claims cases for this rst

set of ndings and recommendations.

ii This number is based on the median amount in controversy for

debt collection cases in Michigan, which is approximately $1,600,

with most cases ranging from $800 to $4,000.

1

Debt Collection Cases Are

Dominating Michigan’s

District Courts

Debt Collection Cases Are Second in Volume Only to

Trafc Cases Filed in Michigan District Courts

See Appendix A for full methodology on how debt collection cases

were classied.

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse, 2017-2019.

Debt Collection (208k)

Trafc (1.46M)

Summary Proceedings (197k)

Misdemanor (130k)

Misc. Civil (119k)

Felony (68k)

Civil Infractions (68k)

Small Claims (44k)

11

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section A Findings | Case Filing Policy & Trends

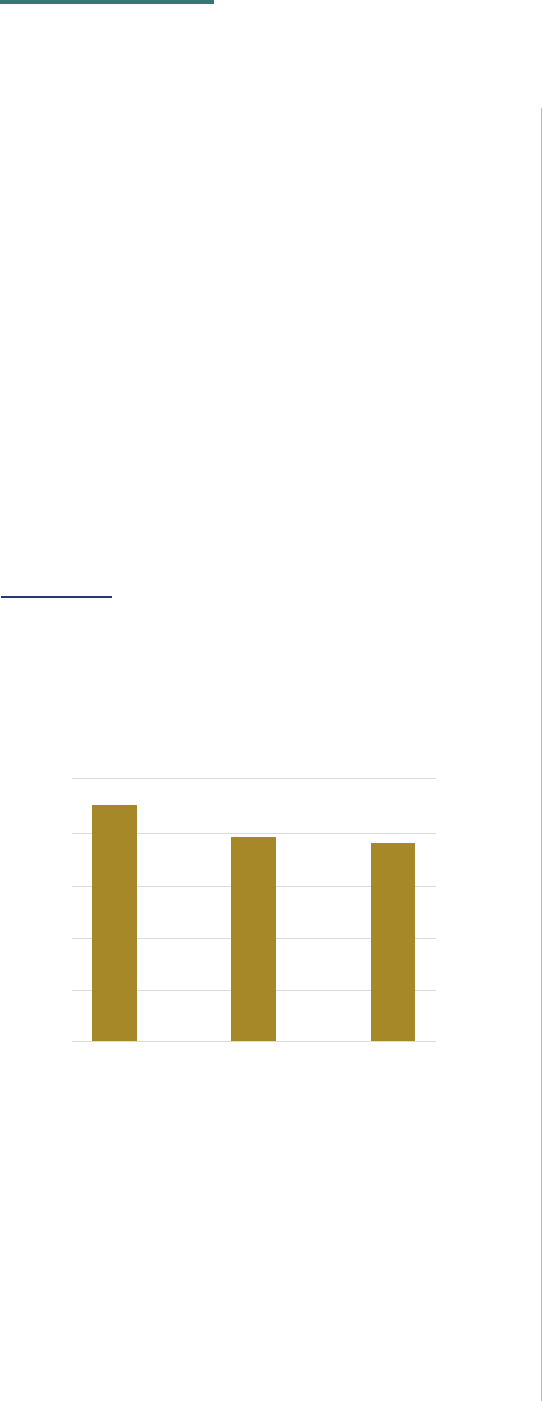

Michigan’s high case ling rates are driven primarily

by a small number of high-volume plaintiffs, which le

a substantially larger percentage of cases in Michigan

compared to other states. In Michigan, debt collection

lawsuits led by the 10 highest volume plaintiffs

made up a substantial majority (71%) of these cases

led from 2020-2021. While there is limited court

record data available on debt collection lawsuits

across the country, Michigan is comparable to two

states that do have such data available: Missouri

and Indiana. The top ler burden for debt collection

lawsuits in Indiana and Missouri is approximately

20% lower than Michigan, even though all three

states have comparable lawsuit and pre-litigation

in collection rates. In fact, the top ve plaintiffs in

Michigan le a greater proportion of cases (55%) than

the top 10 plaintiffs in Indiana (50%) and Missouri

(54%).

2

Ten Plaintiffs File Almost

Three Quarters of Debt

Collection Lawsuits in

Michigan, A Substantially

Larger Share Than Other

States

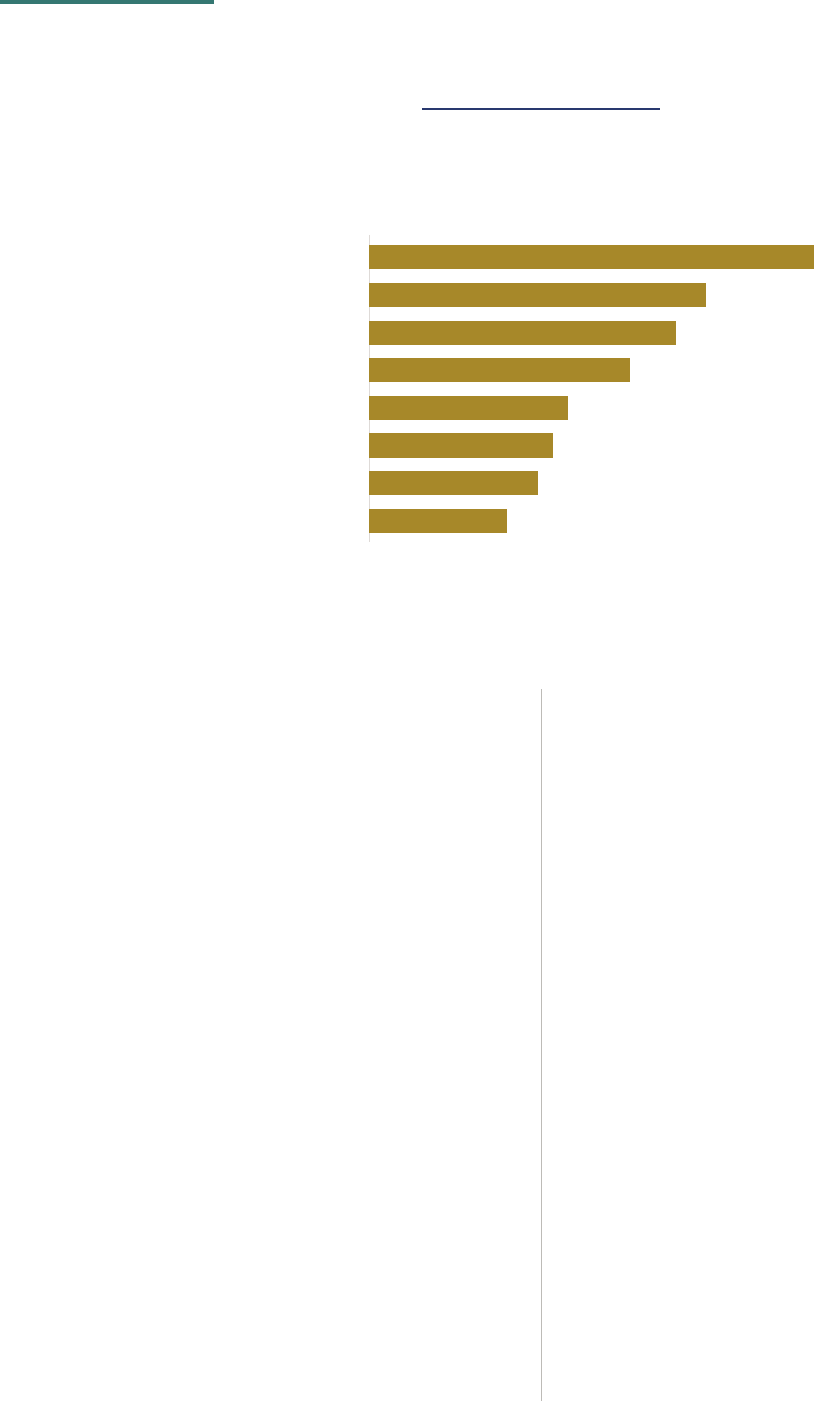

Highest Volume Debt Collection Filers in Michigan

Plaintiff % of Cases

1. Midland Funding 20%

2. Portfolio Recovery Assoc 12%

3. Jefferson Capital Systems 8.8%

4. Capital One Bank 7.8%

5. LVNV Funding 7.6%

6. Credit Acceptance Corp 6.3%

7. Cavalry SPV 1 3.2%

8. Discover Bank 2.6%

9. Razor Capital 1.8%

10. Bronson Healthcare 1.5%

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse, 2017-2019.

Top Filer Burden from 2020 - 2021

Source: January Advisors

+a

71%

MICHIGAN

+a

50%

INDIANA

+a

54%

MISSOURI

Section A Findings | Case Filing Policy & Trends

12

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Debt buyer cases present unique concerns because

their business is based on purchasing high volumes

of debts, and the consumers do not have any

relationship with debt buyers until the debt buyers

initiate their collection efforts. The consumer may

not recognize the debt buyer’s name and think

communications from them are a scam and ignore

collection efforts and court documents, raising

more barriers to consumers participating in court

processes.

22

Debt buyer cases also present hurdles

in understanding the types of debts for which

consumers are sued. While it is possible to make

some assessment as to the origin of the underlying

debt claim based on the plaintiff’s name (e.g., a debt

claim brought by a hospital is likely a medical debt),

this cannot be done with debt buyers because they

purchase portfolios from a variety of original creditors.

Debt buyers purchase portfolios of delinquent or

charged-off debts from creditors, such as credit

card or utility companies, at highly discounted rates

when a creditor ceases its own collection efforts on

particular debts.

21

60% of the debt collection cases

led in Michigan are debt buyers, with the top three

lers by volume all being debt buyers. The remaining

40% of debt collection cases are brought by original

creditors, including banks, credit card companies,

auto loan companies, hospitals, and retailers.

The rise in total debt collection cases in the second

half of the decade was driven almost entirely by

debt buyer companies. Between 2016 and 2019, the

number of cases led by debt buyers increased from

73,000 to 125,000 annually. By 2019, cases led by

debt buyers represented 60% of all debt collection

cases led in Michigan, up from 40% in 2010.

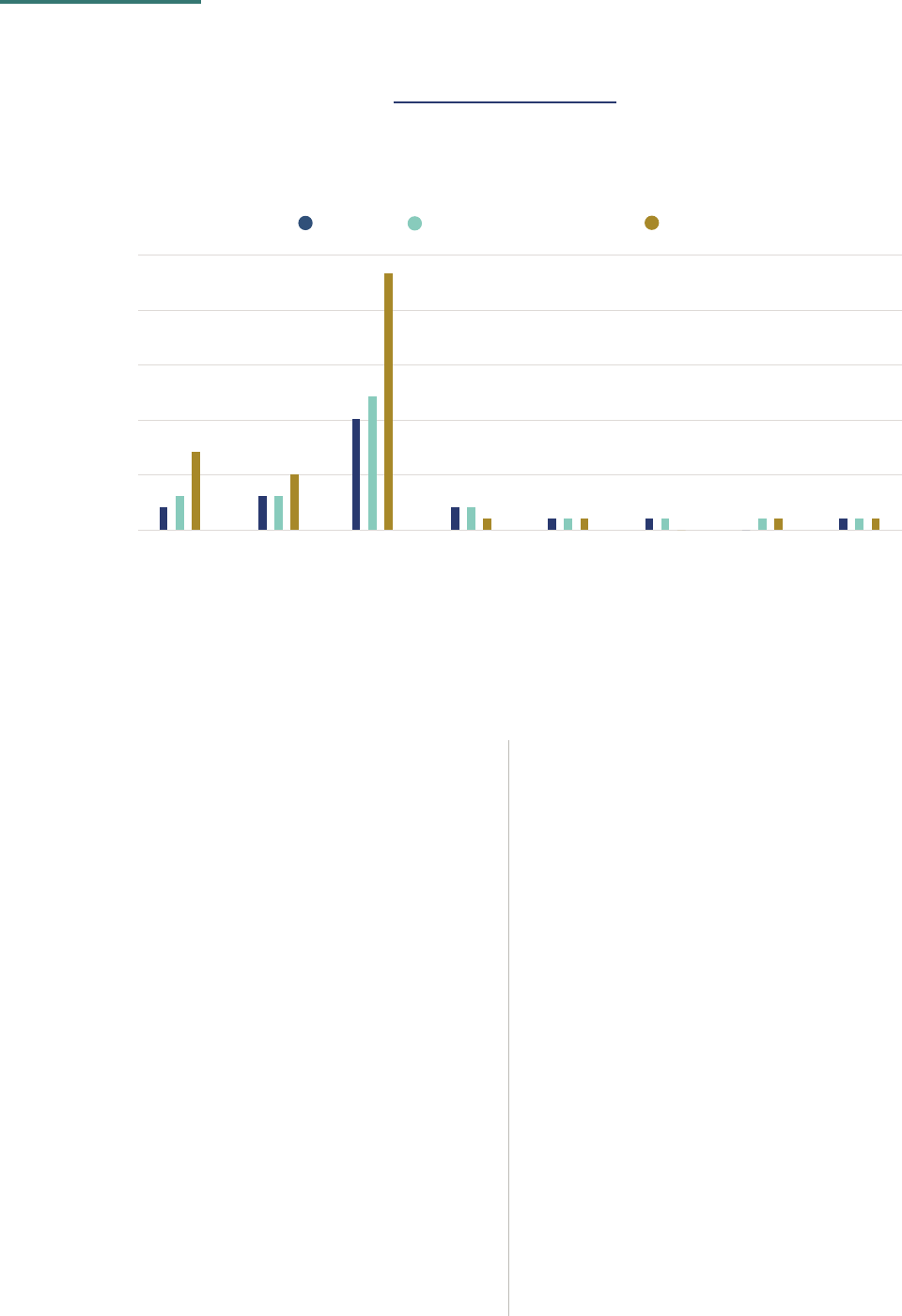

Cases Filed by Debt Buyers Are Increasing

as Cases Filed by Banks and Credit Card Companies Are Decreasing

Number of debt collection cases by type of plaintiff, 2010-2021. Plaintiff type is based on classication of

100 plaintiffs who led the most general civil cases in Michigan District Courts.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2010 - 2021.

Debt Buyer

Bank/Credit Card

Other Plaintiffs

2010 2012 2014 2016 2018 2020

150k

120k

90k

60k

30k

3

Filings by Debt Buyers

Have Signicantly

Increased in Michigan

Section A Findings | Case Filing Policy & Trends

13

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

This data aligns with national data that indicates

consumers do not have an adequate nancial safety

net to cover unexpected expenses; in 2019, 37% of

Americans reported that they would be unable to

completely cover an unexpected expense of $400

and would need to resort to other measures such as

putting that amount on a credit card or borrowing

from a bank, payday lender, or friend or family

member.

24

While debt collection cases represent a large volume

of District Court cases, most of these claims are for

relatively small sums of money. The median amount

in controversy was $1,600 among courts where data

was available in 2018-2019, which is slightly higher

than the median pre-ling amount of debt collection

in Michigan of $1,375 based on 2022 credit panel

data.

23

The middle 50% of cases were for amounts

between $850 and $3,700, meaning that the amount

of controversy for 75% cases is under $3,700.

Based on classication of the top 100 plaintiffs who led general civil cases in Michigan’s District Courts from

2017-2019.

Note: “Retail” includes stores acting as original creditors, making direct loans to consumers for the purchase

of products they directly sell such as furniture, appliances, and jewelry. Store credit cards would be included

in the bank/credit card or debt buyer category. All plaintiffs, except Debt Buyers, are original creditors.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2017-2019.

Debt Buyers Filed Almost 60% of Debt Collection Cases in Michigan from 2017-2019.

Plaintff Type Total Cases % of Cases

Debt Buyer 343,356 58.8%

Bank/Credit Card 110,049 18.8%

Auto 62,402 10.7%

Medical 52,397 9%

Student 7,677 1.3%

Payday Loan 2,920 0.5%

Retail 2,828 0.5%

Municipal 2,691 0.5%

4

Debt Collection Cases

Have Relatively Low

Amounts in Controversy

14

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section A Findings | Case Filing Policy & Trends

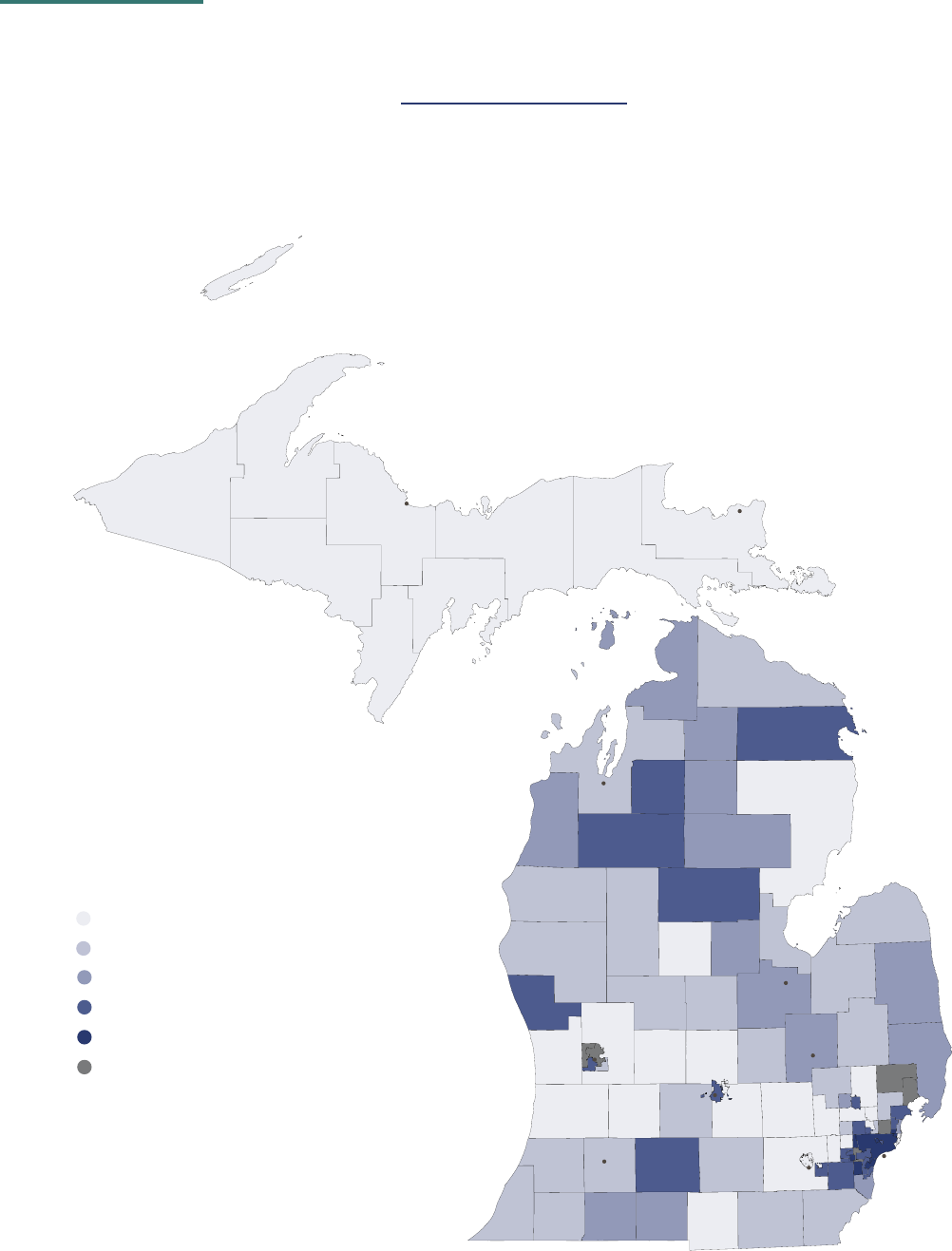

Courts had higher average annual lings rates

than Detroit’s 36

th

District Court’s average annual

ling rate of 5.1 cases per 100 residents. Highland

Park – an enclave city surrounded by Detroit with a

46% poverty rate and average household income

of $20,666

25

– had the highest per capita ling rate

during this time period with an annual average rate of

13 cases led per 100 residents.

With the exception of Van Buren County (D-7), the

ten District Courts with the highest per capita debt

collection ling rates are all located in the Detroit

metro area, representing over 62% of all debt

collection cases led between 2017 and 2019. Debt

collection litigation, however, affects consumers

across the state. District Courts across Michigan

saw above average debt collection case lings rates

– over 3 per 100 residents – between 2017-2019.

This includes more urbanized areas like Lansing

(D-54A), Flint (D67-5), and Muskegon (D-60) and

less urbanized areas like the 7

th

District (Van Buren

County), the 80

th

District (Clare and Gladwin counties),

the 84

th

District (Missaukee and Wexford counties),

and the 88

th

District (Alpena and Montmorency

counties).

The vast majority of debt claims are led in District

Courts that cover the population-dense urban and

suburban areas such as Detroit, Grand Rapids,

Kalamazoo, and Lansing. Indeed, Detroit’s 36

th

District

Court alone averaged almost 30,000 debt collection

lings between 2017-2019, which represents 15% of

all debt collection lings in Michigan.

The number of lings, however, is impacted by the

size of population in each District Court’s jurisdiction.

Detroit’s 36

th

District Court has the most populous

jurisdiction of all of Michigan’s District Courts. Looking

at case ling from a per capita perspective – the

number of case lings per 100 residents – other

District Courts have higher debt collection ling rates.

Between 2017-2019, Highland Park (D-30), Taylor

(D-23), Inkster (D-22), and Romulus (D-34) District

District Courts in the Detroit Metro Area Have the

Highest Case Filing Rates

Average cases led per 100 residents from 2017-2019.

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse, 2017-2019.

D30 Highland Park 5.9

D22 Inkster 5.1

D32A Harper Woods 4.9

D38 Eastpointe 4.8

D17 Redford 4.5

D36 Detroit 4.4

D25 Lincoln Park 4.1

D2 Taylor 4

D50 Pontiac 3.7

D54A Lansing 3.7

5

Debt Collection Lawsuits

Impact Consumers Across

the State

Section A Findings | Case Filing Policy & Trends

15

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

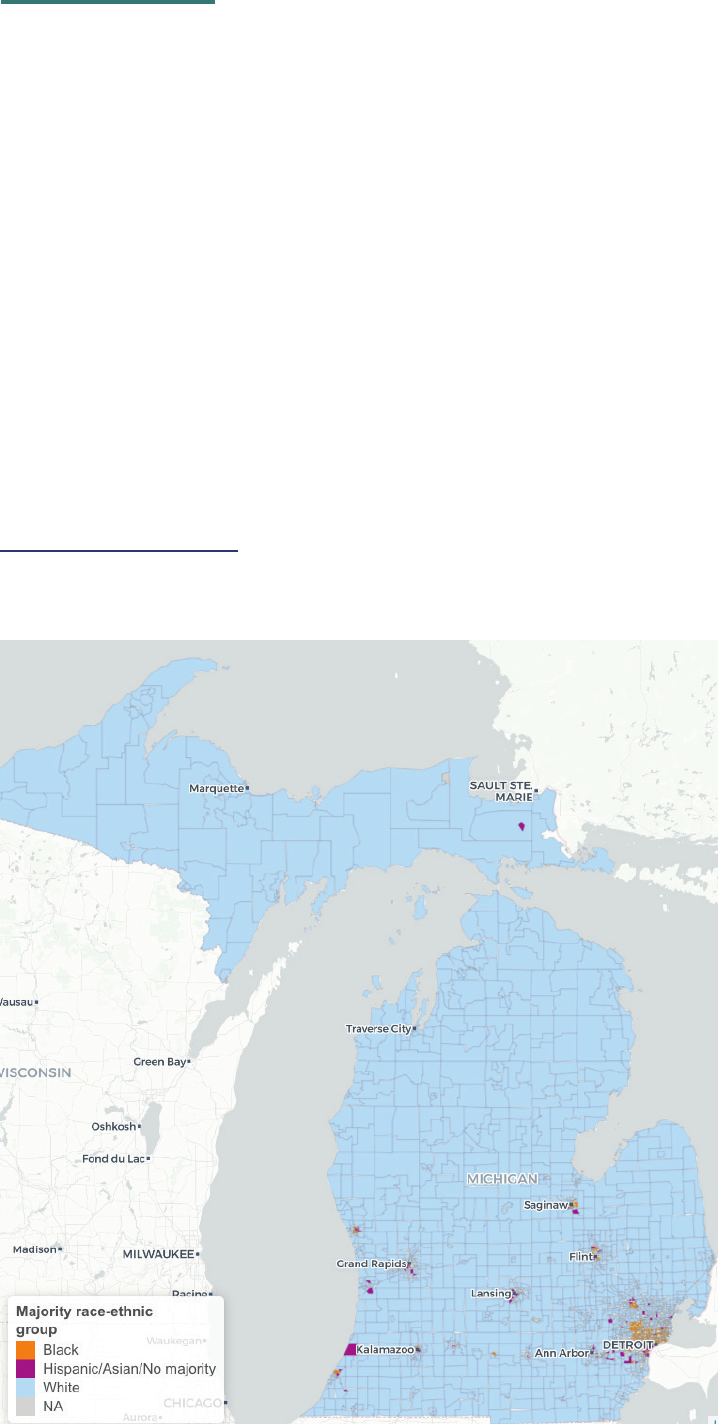

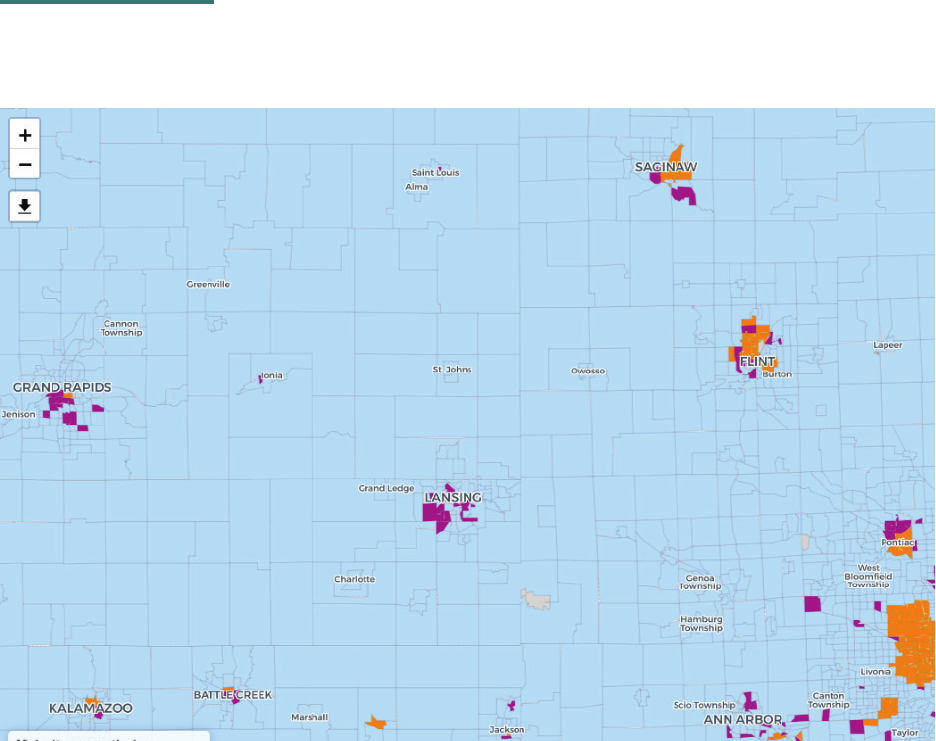

High Case Filing Rates Found in Northern Rural Areas

(Clare, Gladwin, Missaukee, Wexford, Alpena, and Montmorency Counties)

0 - 1.4%

1.5 - 1.9%

2 - 2.5%

2.5 - 3.9%

4%+

NA

Sault Stre Sault Stre

MarieMarie

MarquetteMarquette

Traverse CityTraverse City

SaginawSaginaw

FlintFlint

DETROITDETROIT

Ann ArborAnn Arbor

KalamazooKalamazoo

LansingLansing

Grand RapidsGrand Rapids

Michigan district courts by number of debt collection cases led annually, 2017-2019.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2017-2019.

16

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section A Findings | Case Filing Policy & Trends

Middle- and high-income neighborhoods in Michigan

see far fewer debt collection case lings. On average,

neighborhoods where median income is $50,000 or

lower see 2.6 lawsuits per 100 residents. By contrast,

middle-income neighborhoods ($50,000-$75,000

median income) see 1.6 lawsuits per 100 residents,

and high-income neighborhoods ($75,000-$220,000

median income) see 1.0 lawsuits per 100 residents.

These numbers align with national data on

borrowing, which show that while the amount owed

on credit cards increases with increasing income, this

amount becomes a decreasing percentage of monthly

income and liquid assets. For example, for the bottom

20

th

percentile of income, the median amount owed

in credit card debt was $1,100, which represents

81% of median monthly income and 136% of liquid

assets in bank accounts. If we take the median claim

amount in Michigan of $1,600, this constitutes 118%

of median monthly income and 198% of liquid assets

in bank accounts among these consumers. This

suggests that a substantial number of consumers

being sued for debt collection in Michigan could not

afford to pay off their debt with their existing wages

and assets.

26

By contrast, those in the top 10% of income had a

median amount of $12,600 owed in unpaid credit

card debt, yet this represented only 25% of median

monthly income and 9% of liquid assets in bank

accounts, making it nancially much more feasible to

make monthly payments.

27

While debt collection cases are led against

consumers across the state of all income levels,

the highest case ling rates are against low-

income consumers. Half of all debt collection case

lings in Michigan are led against consumers

living in neighborhoods with median household

incomes of $50,000 or less. Debt collection cases

are disproportionately led against residents of

neighborhoods with the lowest incomes – four times

as many cases were led in the poorest 10% of

neighborhoods (3.3 led per 100 residents) compared

to the richest 10% of neighborhoods (0.8 per 100

residents).

6

Low-Income Communities

in Michigan Have High

Debt Collection Case

Filing Rates

Low-Income Neighborhoods Bear the Brunt of

Debt Collection Filings

Number of debt collection cases led per 100 residents by

neighborhood median household income quintile from 2017-2019.

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse, 2017-2019. American Community Survey 2015-2019.

2.5

$50k or less $50k to $75k $75k or more

2.0

1.5

1.0

0.5

NUMBER OF CASES FILED PER 100 RESIDENTS

Section A Findings | Case Filing Policy & Trends

17

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

their way to Michigan’s District Court – 23% of all

debt collection lawsuits led from 2015-2019 were

against consumers living in neighborhoods that are

majority Black, despite only 9% of Michigan’s total

population living in those neighborhoods. Based on

court data, signicantly more debt collection lawsuits

are led against consumers in neighborhoods that

are majority Black compared to those living in

neighborhoods that are majority White at all income

levels. In neighborhoods that are majority Black, as

income levels rise, debt collection lawsuits remain

high. This goes against the trend in White and other

demographic majority neighborhoods, where higher

income neighborhoods see fewer debt lawsuits. For

low-income neighborhoods, the ling rate against

consumers in neighborhoods that are majority Black

is 1.9 times higher compared to majority White

neighborhoods; for higher-income neighborhoods, the

ling rate against consumers in neighborhoods that

are majority Black is 2.8 times higher compared to

Black Communities in Michigan Have High Debt

Collection Filings Rates Across Income Levels.

Data analysis from other cities – Chicago, St.

Louis, and Newark – reveal that the rate of default

judgments entered against consumers living in

neighborhoods that are majority Black is twice as

high as the rate in White-majority neighborhoods.

28

Michigan experiences similar disparities.

Michiganders living in communities that are majority

Black are more than twice as likely to have a debt in

collection compared to people living in communities

that are majority White.

29

These disparities make

7

Black Communities in

Michigan Have High Debt

Collection Filings Rates

Across Income Levels

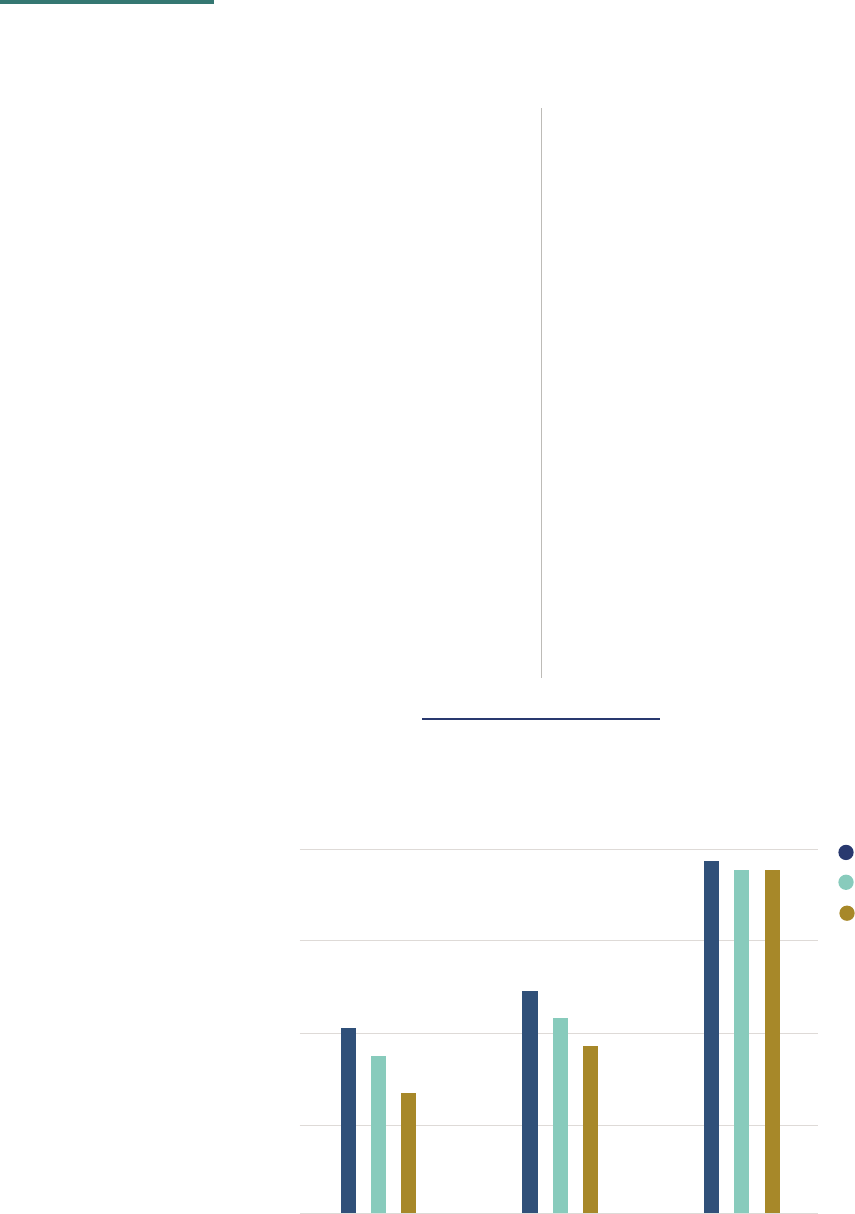

More Debt Collection Cases Are Filed Against Consumers

Living in Predominantly Black Neighborhoods

Predicted annual average number of debt collection cases led per 100 residents by census tract median

household income and race-ethnic majority group. Predicted values calculated from linear regression model

that includes median household income, race-ethnic majority group, their interaction, and controls for

population size.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse , 2015-2019. American

Community Survey 2015-2019.

4.0

3.0

2.0

1.0

White BlackHispanic/Asian/No Majority

$25k

$50K

$75k

Section A Findings | Case Filing Policy & Trends

18

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

must understand what debts they are purchasing,

from whom, and at what discount rate.

Data on racial disparities in credit scores may point

to problems that occur much earlier in the lending

process, such as racial disparities in access to low-

cost credit. A study on credit scores conducted by

the Urban Institute showed that in 50 of the 60 cities

it reviewed had communities of color with below-

prime median credit scores (660 or lower), and the

majority were subprime median scores (600 or lower).

By contrast, only four of the 60 cities in the study

had majority White areas with below-prime median

credit scores (660 or less).

30

People with lower credit

scores have fewer options for credit and often obtain

credit with less favorable terms, such as higher

interest rates. In the context of auto loans, which

have the highest case ling disparities, research from

the Consumer Financial Protection Bureau shows

that individuals with subprime credit scores (600 or

less) may have less access to lower-cost loans from

a bank or credit union but need to turn to different

types of lenders. These lenders may charge higher

neighborhoods that are majority White.

At all levels of neighborhood income, neighborhoods

that are majority Black in Michigan see approximately

2-3 times as many case lings for debt collection as

Non-Hispanic White-majority neighborhoods.

The highest disparities are seen in cases led by

debt buyers, auto nancing, banks, and credit card

companies, with Credit Acceptance Corporation (an

auto nancing company), Jefferson Capital Systems

(a debt buying company), and RaZor Capital, LLC (a

debt buying company) as the top plaintiffs ling more

cases in majority Black neighborhoods compared to

their lings in majority White neighborhoods.

More information is needed to understand the

reasons for these disparate ling rates. Debt buyers,

for example, have the second highest case ling

disparities in case lings; however, they buy portfolios

of debt from other creditors and typically have no

previous relationship with the consumer. Therefore, to

understand the reasons for this racial disparity, one

Predicted annual average number of debt collection cases led per 100 residents by plaintiff type and race-ethnic

majority group among middle-income neighborhoods only ($50,000 median household income). Patterns are similar

in low- and high-income neighborhoods

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2015-2019. American Community

Survey 2015-2019.

Sharpest Filing Disparities for Predominantly Black Neighborhoods

Found in Auto, Debt Buyer, and Credit Card Cases

White

Hispanic/Asian/No majority

Black

2.5

2.0

1.5

1.0

0.5

Auto Bank &

Credit Card

Debt Buyer Medical Municipal Payday

Lender

Retail Student

Black-White

ling disparity

310% higher

47% higher

143% higher

11% higher 33% higher

37% lower

2% lower 7% lower

19

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section A Findings | Case Filing Policy & Trends

In 2010, the Federal Trade Commission issued a

report calling debt collection litigation across the

country a “broken system.” Since that time, several

states ranging from Arizona to Maryland to New York

and Colorado have implemented policies to improve

how debt collection lawsuits are handled. Many of

these policies have focused on ensuring creditors and

debt buyers have and disclose the necessary proof

to substantiate their claims. The implementation

of these policies has included updating court rules

and state statutes to account for the particular

documentation needed to prove consumer debt

claims, which has three components: 1) proof that the

defendant being sued incurred the alleged debt, 2)

proof that the amount being claimed is accurate, and

3) proof that the plaintiff initiating the lawsuit actually

owns the debt in question. Given the high default

judgment rate in debt collection cases, these policies

help ensure that judgments are entered for the

creditor or debt buyer who actually owns the debt,

against the correct consumer who actually owes the

debt, and for the correct amount. Documentation

can also aid the consumer in identifying the debt and

allow them to more effectively seek legal or other

assistance in resolving the lawsuit.

While Michigan has special pleading requirements for

debt collection cases, they only require the plaintiff to

include 1) the name of the creditor; 2) account number

for the debt; and 3) the balance due. Michigan has

no requirement that plaintiffs submit a breakdown

of fees and interest and no requirement that a debt

buyer establish their ownership of the debt, such as

providing a chain of assignment.

35

With the exception

of Ohio, Michigan has the most lenient pleading

requirements among the Great Lake states prior to

entry of a default judgment.

interest rates or, if the nancing comes directly from

the car dealership, may offer below-market interest

rates for over-priced cars.

31

Indeed, some auto loan

providers target individuals with bad or no credit.

Credit Acceptance – the highest auto loan case ler in

Michigan – explicitly advertises on its website that it

can get car nancing for people with bad or no credit

through car dealers enrolled in its program.

32

In addition, people living in communities of color are

more likely to have a debt in collection compared to

people living in predominantly white communities.

Data from the Urban Institute shows that, in

Michigan, 53% of people living in communities of

color have a debt in collection compared to 22% of

people living in white communities.

33

These studies indicate that Black consumers face

additional barriers to paying debt – such as higher

interest rates, predatory lending terms, or the inability

to borrow money from family or friends – due, at

least in part, to “policies and practices such as race-

based redlining, which prevented access to affordable

real estate mortgages or fair property appraisals,

undermined the ability of people of color to build

wealth through homeownership and created unequal

credit markets based on that lack of wealth.”

34

While further research and investigation is

needed to understand consumer, creditor, and

debt buyer behavior, these ndings are relevant

to Michigan courts and its Justice for All efforts in

that they illuminate which communities are being

disproportionately brought into the court’s jurisdiction

and for what types of claims.

8

Michigan Trails Other

Great Lakes States in Debt

Collection Policy Reform

Section A Findings | Case Filing Policy & Trends

20

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

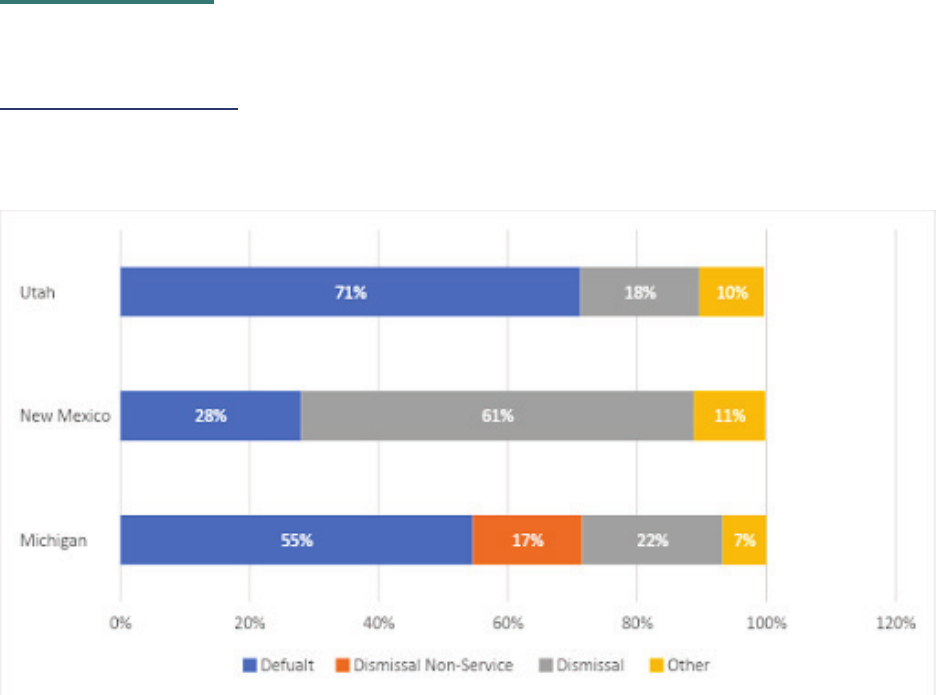

Michigan Has More Lenient Pleading Requirements than All Great Lakes States (Except Ohio)

iii

iii Pennsylvania is not included because of extensive variation in local court rules that apply to debt collection lawsuits.

Source: Based on an analysis of court rules and state statutes that apply to debt collection lawsuits in state civil courts.

Proof of account Proof of amount Proof of ownership Policy applies to?

When

disclosed?

Michigan

account number balance due to date none all consumer on complaint

Illinois

account number and

agreement or any monthly

statement showing activity

charge-off balance and

fees, last payment or

default date

list chain of

ownership

consumer credit and

debt buyers

with the

complaint

Indiana

account number and

agreement or any monthly

statement showing activity

balance due to date and

fees

attach all

assignments of claim

AND chronological

list of prior owners

all consumer

with the

complaint

Minnesota

consumer’s SSN, account

number, and agreement or any

monthly statement showing

activity

charge-off balance and

fees, last payment or

default date

attach all

assignments of claim

debt buyers &

collectors only

to obtain

default

judgment

New York

account number and

agreement or most recent

monthly statement showing

activity

charge-off balance and

fees, last payment or

default date

attach all

assignments of claim

AND chronological

list of prior owners

consumer credit and

debt buyers

to obtain

default

judgment

Ohio

general civil computation of

damages

none none no specic policies not specied

Wisconsin

agreement or any monthly

statement showing activity

charge-off balance and

fees, last payment or

default date

none consumer credit only

upon

consumer

request

Section A Findings | Case Filing Policy & Trends

21

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Other states in the region require documentation

such as the original agreement or a monthly billing

statement showing the defendant used the account

in question, the balance due with fees and interest

broken out, and documentation showing the chain of

ownership of the debt if it was sold to a debt buyer.

A new federal regulation by the Consumer Financial

Protection Bureau enacted in November 2021

requires that debt collectors provide consumers with

information to substantiate the amount of debt owed

as part of collections efforts – including the amount

of debt on the itemization date and all subsequent

interest, fees, payments, and credits

36

– but whether

these practices are integrated into litigation and the

court process remains contingent on state policy and

practice.

Additionally, courts in Illinois and Wisconsin have

taken steps to better implement these policies in ways

that empower litigants to meaningfully participate in

their case by expanding their understanding of the

court process, debt claim, and potential defenses, as

well as ensuring an effective administration of justice.

The Illinois Supreme Court, for example, mandated

a statewide afdavit of debt that breaks down proof

of debt components such that defendants can more

easily identify the debt and understand the lawsuit

being brought against them. LaCrosse County in

Wisconsin has adopted a standard checklist for clerks

to use when reviewing the documentation provided

for sufciency.

Section B

22

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Findings: Case Outcomes

Debt collection cases are ooding civil dockets, yet these cases rarely see a

courtroom. While some cases are dismissed because the plaintiff is unable to serve

the consumer or the parties reach a settlement agreement, the vast majority of

debt collection cases result in the entry of a default judgments against consumers

because they failed to respond to the complaint or attend a hearing. Indeed, data in

other states indicate that once service is accomplished, approximately 70% of debt

collection cases result in default judgment.

1. Cases dismissed for failure to serve are increasingly common.

2. Default judgments are entered in most debt collection cases in Michigan.

3. Dismissals with prejudice, non-default judgments, and setting aside default

judgments rarely occur in debt collection cases.

4. The default judgment rate declined during the pandemic.

5. Racial disparities found in dismissal for failure to serve and default judgment rates.

6. Michigan District Courts have fairly similar case outcomes, but case outcomes have

become less similar over time.

7. The amount awarded in judgments aligns with the amount in controversy sought by

plaintiff.

AT A GLANCE

23

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section B Findings | Case Outcomes

After plaintiffs le lawsuits in District Court, they must

properly serve defendants with court documents

– including the summons and complaint – to notify

them that they are being sued. Plaintiffs typically

have 90 days to serve defendants.

37

If the plaintiff

is able to serve the defendant, then the plaintiff les

a proof of service with the court. If, however, the

plaintiff is unable to serve the defendant before the

summons expires, the court clerk will dismiss the

case without prejudice.

38

Plaintiffs can have difculty

serving defendants for a number of reasons, including

when the defendant is trying to avoid service or

when they have an outdated address and are unable

to locate the defendant using information such as

information from the Secretary of State’s ofce or a

skip tracing service.

Debt collection cases in Michigan are typically

resolved in one of the following ways:

1. Dismissal or withdrawal. The plaintiff

withdraws the case or the court dismisses the

case. The court may dismiss the case for a

number of reasons, such as when the plaintiff

is unable to properly serve the defendant or

when the defendant raises meritorious defenses

in a motion to dismiss. The plaintiff can also

request that the court allow it to withdraw the

case; this can occur when the plaintiff realizes

it has made a mistake in the pleadings, such as

naming the wrong defendant. Dismissals can

be without prejudice, meaning that the plaintiff

can bring the claim again; this occurs, for

example, when the plaintiff is unable to properly

serve the defendant. Dismissals can also be

with prejudice, meaning that the plaintiff cannot

bring the claim again; this occurs, for example,

when the defendant brings a meritorious motion

to dismiss.

2. Default judgment. The court enters a default

judgment in the plaintiff’s favor because the

defendant failed to respond to the complaint or

appear at court hearing.

3. Settlement. The court enters a stipulated

judgment based on the parties reaching a

settlement agreement, such as a payment plan.

4. Judgment. The court enters a judgment on the

merits after a hearing.

1

Cases Dismissed for

Failure to Serve Are

Increasingly Common

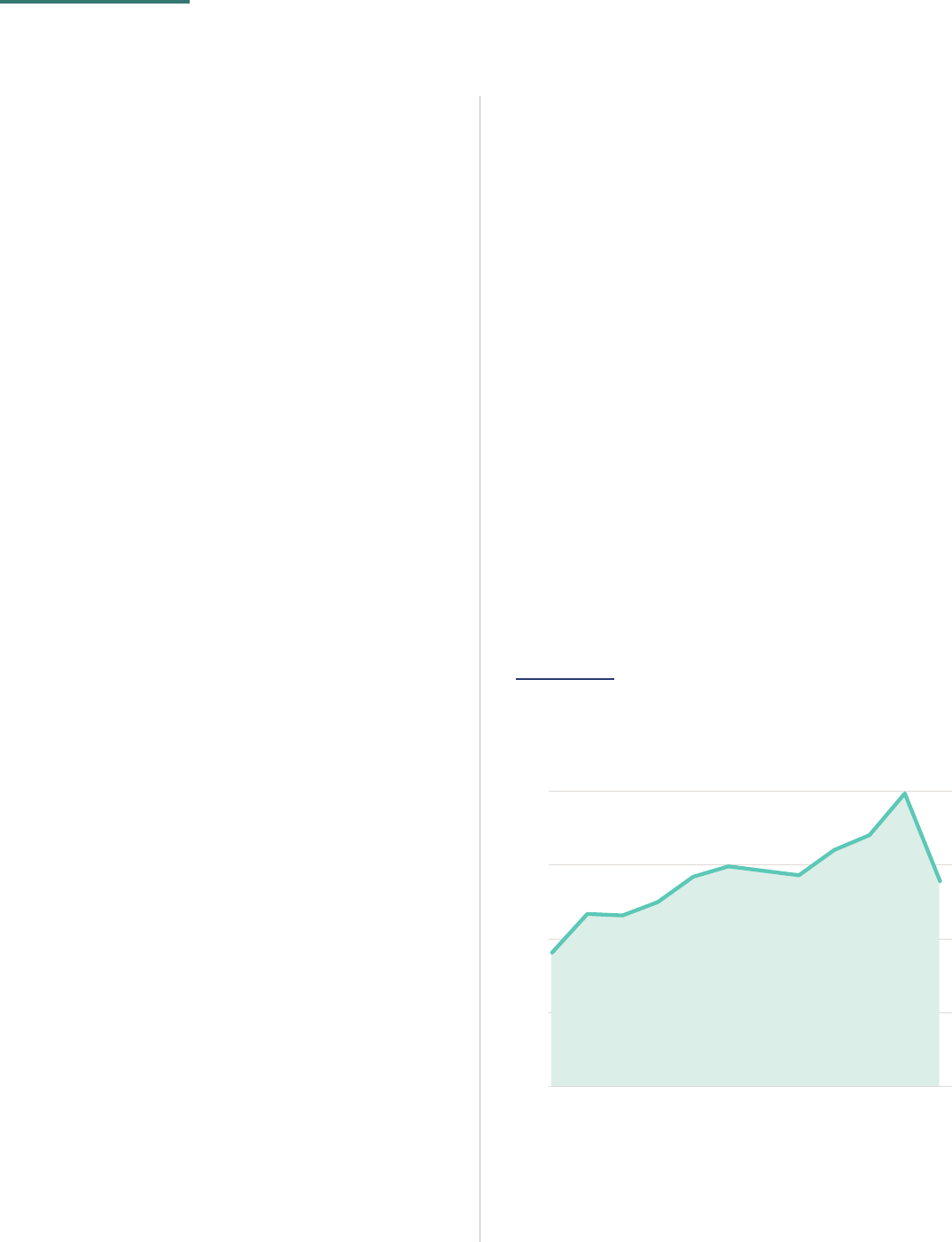

Rate of Cases Dismissed for Non-Service Has

Doubled Since 2010

Share of disposed cases dismissed for non-service led 2010-

September 2021 annually.

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse, 2010-2021

20

15

10

5

2010 2012 2014 2016 2018 2020

Section B Findings | Case Outcomes

24

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

If the defendant fails to le a timely response after

being served, the plaintiff may request a default

judgment from the court based on the information

provided in the complaint. Default judgments are

entered in the majority of debt collection cases in

Michigan. From 2017-2019, courts entered default

judgments in 57% of all debt collection cases. This

calculation, however, includes the 16% of cases that

were dismissed because the plaintiff was not able

to serve the defendant, meaning that the defendant

had no opportunity or expectation to respond. Taking

away the cases that were dismissed for failure to

serve, the default rate for cases in which the court

had an expectation for defendants to respond to

contest the claims increases to 68%.

Roughly 16% of debt collection cases – 1 in 6 cases

– led in 2017-2019 were dismissed for failure to

serve. This represents an increase from earlier in the

decade: Between 2010 and 2019, the share of cases

dismissed for non-service nearly doubled, from 9%

to 17%. During the height of the pandemic in 2020,

nearly 1 in 5 cases were dismissed for non-service.

The rate of dismissal for failure to serve varies by

plaintiff type. Cases led by municipal, auto, retail,

and debt buyer plaintiffs have higher dismissal rates

for failure to serve compared to cases led by bank

and credit card companies, payday lenders, and

student and medical creditors. Medical debt had the

lowest rate, with only 9% of cases led by medical-

related plaintiffs dismissed for failure to serve.

Share of disposed cases dismissed for non-service from 2017-2019.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2017-2019.

Highest Rates for Dismissal for Non-Service Found in Municipal,

Auto, Retail, and Debt Buyer Cases

Municipal 29%

Auto 22%

Retail 20%

Debt Buyer 17%

13%

12%

Bank/Credit Card

Payday Lender

Student 11%

Medical 9%

2

Default Judgments Are

Entered in Most Debt

Collection Cases in

Michigan

Section B Findings | Case Outcomes

25

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

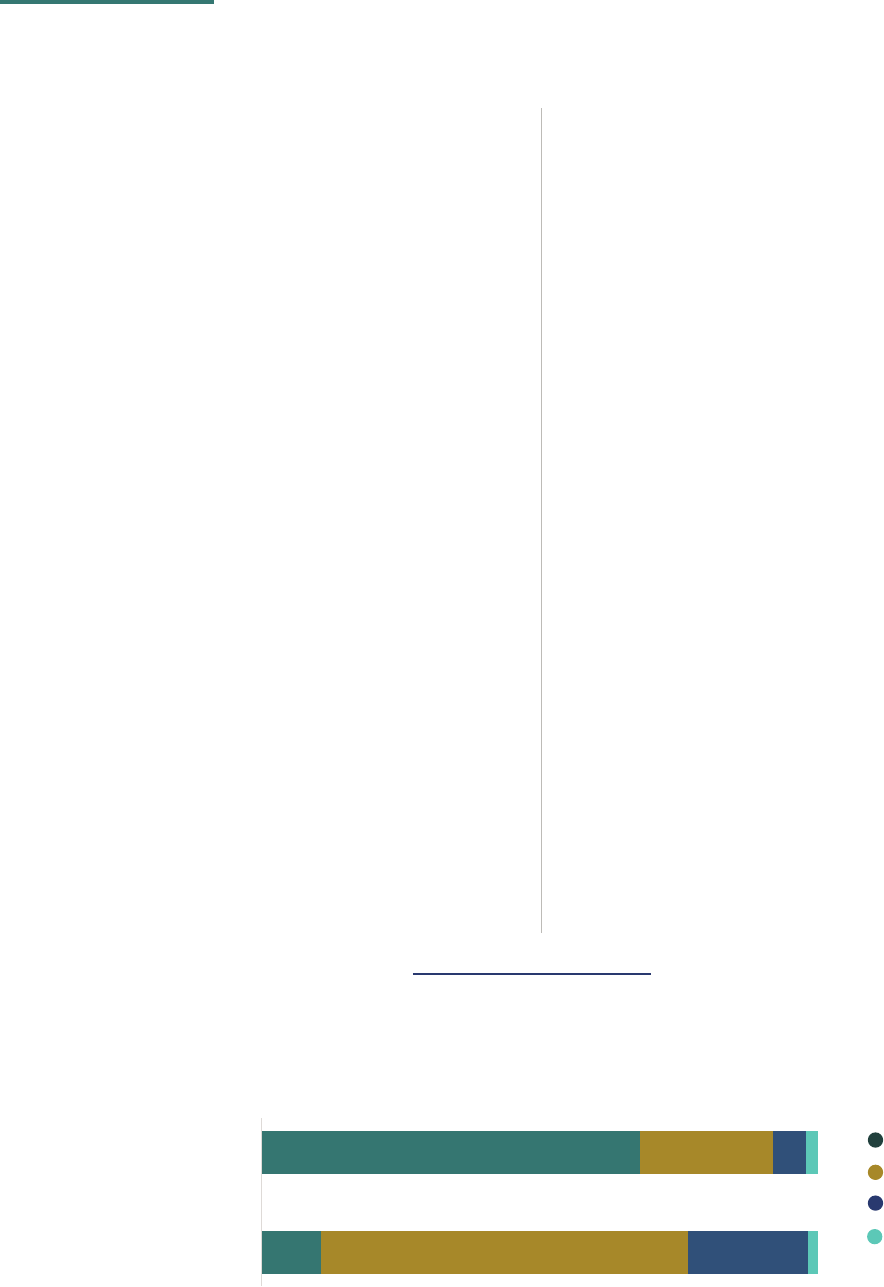

The default judgment rate is generally high for all

plaintiff types, except for municipal plaintiffs. Cases

led by auto creditors, in particular, have an above

average default judgment rate of 79%, meaning that

almost 4 out of 5 Michiganders notied about an auto

loan lawsuit are not participating in their court case.

This could be explained by the fact that cars can

be repossessed quickly – even after just one or two

missed payments

40

– before any attempt to collect the

outstanding balance, and consumers may mistakenly

believe that the repossession of the car fullls their

debt obligation.

A default judgment can be used as an indicator for

a defendant’s lack of engagement with and access

to the courts. Several theories exist as to why

defendants do not participate in their debt collection

lawsuits. Studies indicate that public condence in the

courts is low.

41

For debt collection cases, consumers

may not respond because they cannot afford to pay

the debt or they do not understand how to negotiate

a settlement or even how to assess whether the

debt is valid.

42

For invalid debts, the consumer may

not have sufcient information to understand how to

To compare Michigan’s default judgment rate with

other states, it is important to take out the cases

dismissed for failure to serve because many states

allow for pre-ling service where a case is not on

record with the court until service is completed.

A review of studies of multiple jurisdictions between

2013 and 2018 revealed that at least 70% of

debt collection lawsuits were resolved by default

judgment.

39

At 68%, Michigan’s default judgment rate

is comparable to this number.

Appendix A-3 has more information on how and why

Michigan’s default judgment rate was calculated

to make it more comparable to states with varying

policies on when debt collection lawsuits can be led,

and service can take place.

Nearly 7 in 10 cases

result in default judgment where

service is recorded as completed.

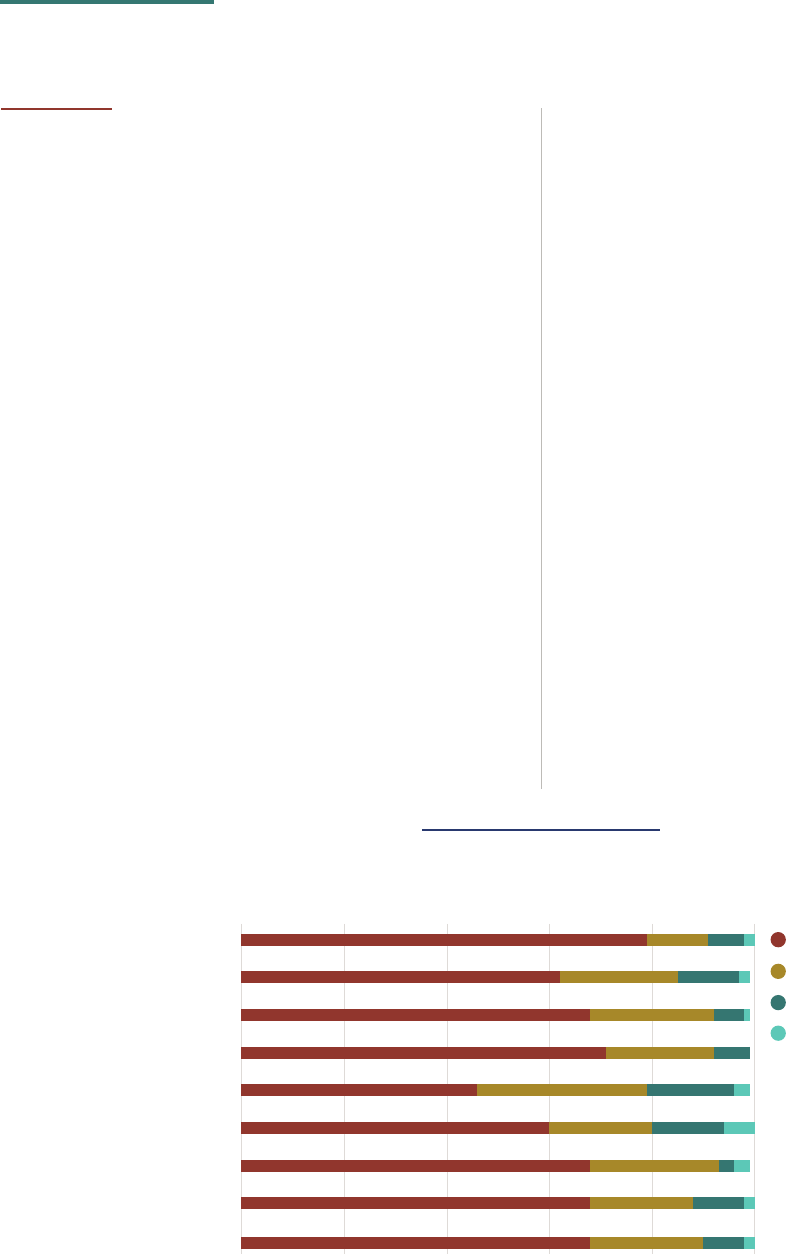

Share of disposed cases by disposition type & plaintiff type, 2017-2019. Does not include 16% of cases

dismissed for non-service because in those instances it is clear that the defendant had no opportunity to

respond.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2017-2019.

Highest Default Judgment Rates Found in Auto and Medical Debt Cases

Default Judgment

Stipulation

Dismissal/Withdrawal

Non-Default Judgment

Auto

0 20 40 60 80 100

Bank/Credit Card

Debt Buyer

Medical

Municipal

Payday Lender

Retail

Student

Overall

26

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section B Findings | Case Outcomes

Putting aside the cases that were dismissed for non-

service, case outcomes have held steady through

most of the decade. Between 2010 and 2019, the

default judgment rate remained high at around 70%.

The pandemic, however, saw a slight decline in the

default rate. Between 2019 and 2020, the default

judgment rate decreased from 67.8% to 59%.

More information is needed to understand the

reasons for the decline in default judgment rates

during the pandemic. One factor that may have

contributed to this decline was the switch to

virtual court options, like Zoom, that were in place

contest the debt.

43

Other practical barriers may exist

for consumers, such as not being able to take time off

of work, not being able to nd childcare, or not having

reliable transportation to attend a hearing.

44

As will

be discussed in more detail below, some defendants

do not respond because they never received notice of

the lawsuit.

45

The second most common case outcome is a

dismissal once service is recorded as complete.

Dismissals can be with or without prejudice. If the

dismissal is without prejudice, then the plaintiff may

le the complaint again against the same consumer. If

a dismissal is with prejudice, then the plaintiff cannot

le the complaint again against that consumer.

Dismissals without prejudice occur in 11% of cases,

while dismissals with prejudice only occur in 3% of

cases.

It is far rarer, however, for debt collection cases to

have a formal hearing in front of a judge. Judgments

entered after a hearing (i.e., non-default judgments)

occur in only 2% of debt collection cases after service

is recorded as complete.

While default judgments are entered in most debt

collection cases, consumers have the opportunity to

submit a motion requesting that the court set aside

the default judgment upon a nding that the court

lacks jurisdiction over the defendant or that the

defendant has a meritorious defense.

46

This happens

less than 1% of the time in Michigan District Courts

where this data was available.

iv

iv Based on an analysis of data from JIS Courts. See Appendix A

for more details.

Default Judgment Rate Held Steady in Michigan with

Slight Decline During the Pandemic

Share of disposed cases by disposition type and plaintiff type

annually. Does not include ~16% of cases dismissed for non-service.

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse data, 2010-2021.

80

72%

16%

11%

1%

59%

34%

2%

60

40

20

2010 2012 2014 2016 2018 2020

Default Judgment

Stipulation

Dismissal/Withdrawal

Non-Default Judgment

3

Dismissals with Prejudice,

Non-Default Judgments,

and Setting Aside Default

Judgments Rarely Occur

in Debt Collection Cases

4

The Default Judgment

Rate Declined During the

Pandemic

27

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section B Findings | Case Outcomes

that are majority Black also saw lower dismissal rates

and stipulation rates for debt collection cases than

consumers living in White-majority neighborhoods.

Notably, Michigan rules and procedures related to

dismissals for non-service appear to serve as a

backstop against wider racial disparities in debt

collection cases. When dismissals for non-service

are taken into account, cases in Black-majority and

White-majority neighborhoods have similar default

judgment rates (~58%).

Although these racial disparities in default judgment

rates are smaller than those observed in debt

collection ling rates, they should still be of concern

to Michigan court ofcials and stakeholders. High

default judgment rates result from low levels of

participation by defendants in the judicial process.

To provide justice for all, courts must understand

why some populations in their communities do not

participate in the judicial process, whether it be due to

barriers to participating in court processes or a lack of

trust in the system.

The court system strives for equal justice with case

outcomes based on the merits of the case and

actions of the parties, independent of the specic

court in which the case is led. The data, however,

indicate variations in case outcomes that could not be

explained by other factors.

for much of 2020 across Michigan district courts.

Consumers may have been more likely to respond to

a complaint knowing that they could participate in

the hearing virtually rather than physically attending

at a courthouse, leading to a decline in the default

judgment rate. As Michigan Supreme Court Chief

Justice Bridget M. McCormack noted, the pandemic

“is not the disruption courts wanted, but it is the

disruption that courts needed.”

47

Remote court

practices “provide […] for efcient and effective access

to the courts for most hearings.”

48

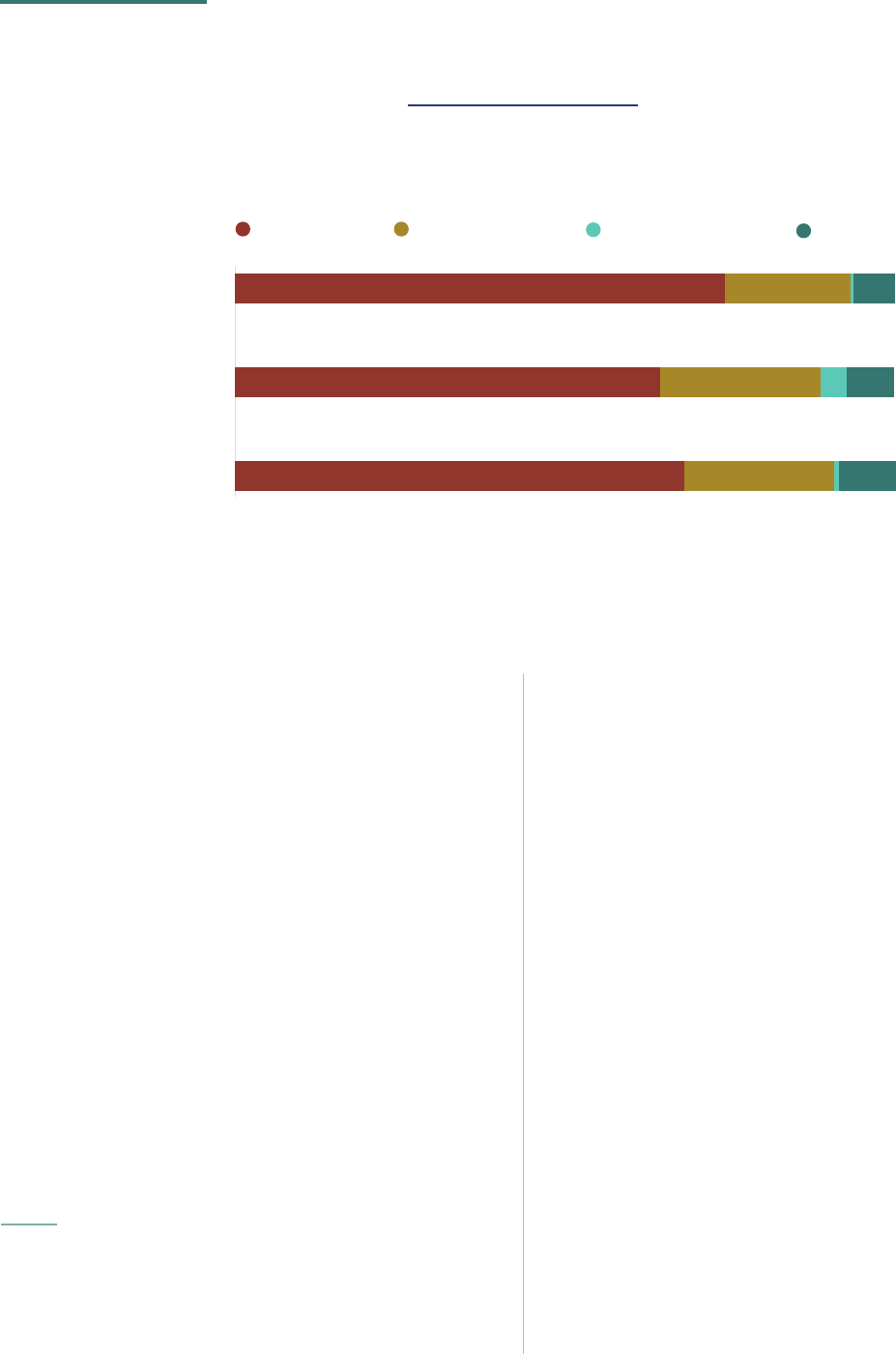

Consumers living in neighborhoods that are majority

Black are more likely to have their cases dismissed

for non-service compared to consumers living in

White-majority neighborhoods. However, once

service is recorded as completed, cases led against

defendants living in neighborhoods that are majority

Black are more likely to have a default judgment

entered.

Nearly 25% of cases led in neighborhoods that

are majority Black were dismissed for failure to

serve in 2017-2019 compared with 14% in other

neighborhoods.

Taking the subset of cases where service is recorded

as complete, data also indicate racial disparities

in the default judgment rate. Consumers living in

neighborhoods that are majority Black were more

likely to have a default judgment entered in their case

compared to consumers living in other neighborhoods.

Nearly 3 in 4 cases (74%) in neighborhoods that are

majority Black (that were not dismissed for non-

service) had a default judgment compared with 68%

in White-majority neighborhoods and 64% in other

neighborhoods. Consumers living in neighborhoods

Consumers in Predominantly Black Neighborhoods

Are More Likely to Have Their Cases Dismissed for

Failure to Serve

Share of disposed cases dismissed for non-service led 2010-

September 2021 annually.

Source: Michigan State Court Administrative Ofce Judicial Data

Warehouse, 2017-2019.

Black 23%

White 14%

Hispanic,

Asian,

No Majority

14%

5

Racial Disparities Found

in Dismissal for Failure

to Serve and Default

Judgment Rates

Section B Findings | Case Outcomes

28

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

for default judgment rates across courts in Michigan

from 2018-2019 shows some variation in the type of

outcome issued for similar claims in Michigan courts.

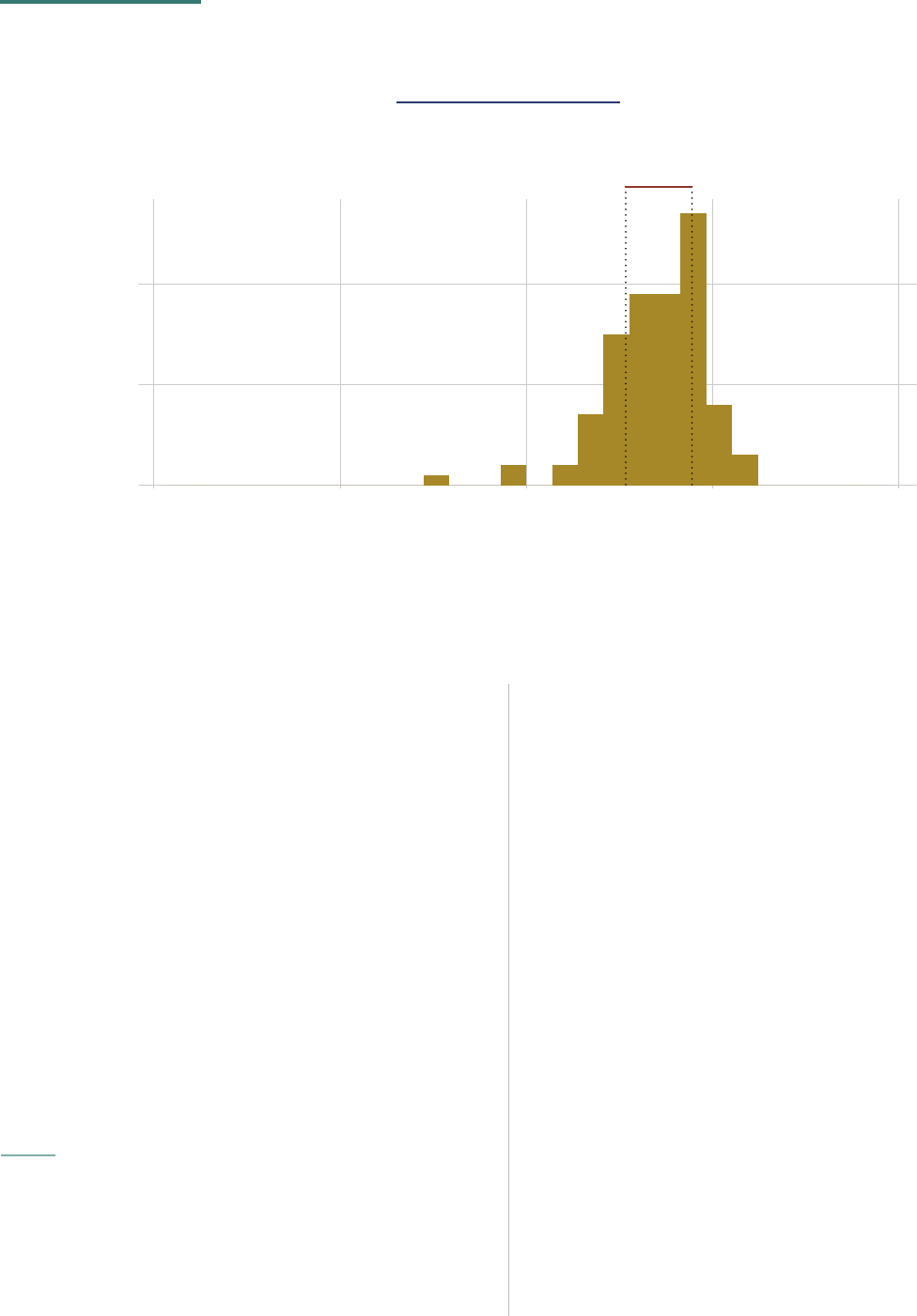

The median court had a default judgment rate of 69%

and the middle of the courts range from 64% to 72%

with an IQR of 8.

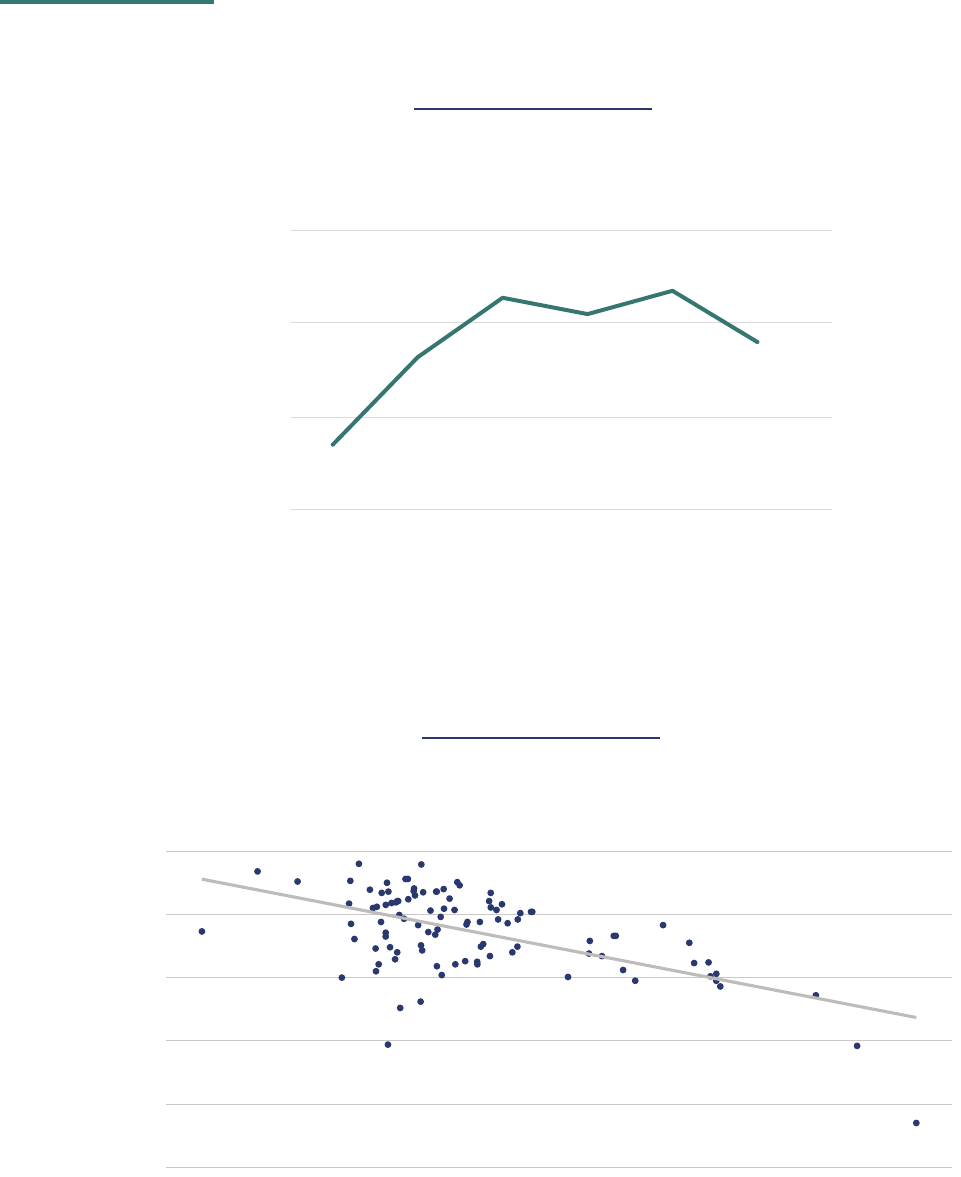

The IQR can also be used to track how courts have

become more or less similar in case outcomes over

time. In 2010, courts had a relatively low IQR value of

5.4 in their rates of default judgment, which indicates

that District Courts across the state had relatively

similar rates of default judgment. The IQR increased

from 2012 to 2019, peaking at 8.7 in 2019 and

indicating an increase in variation in default judgment

rates across District Court. The variation, however,

dropped during the pandemic to 7.6, which indicates

a decrease in variation among District Courts for the

default judgment rate.

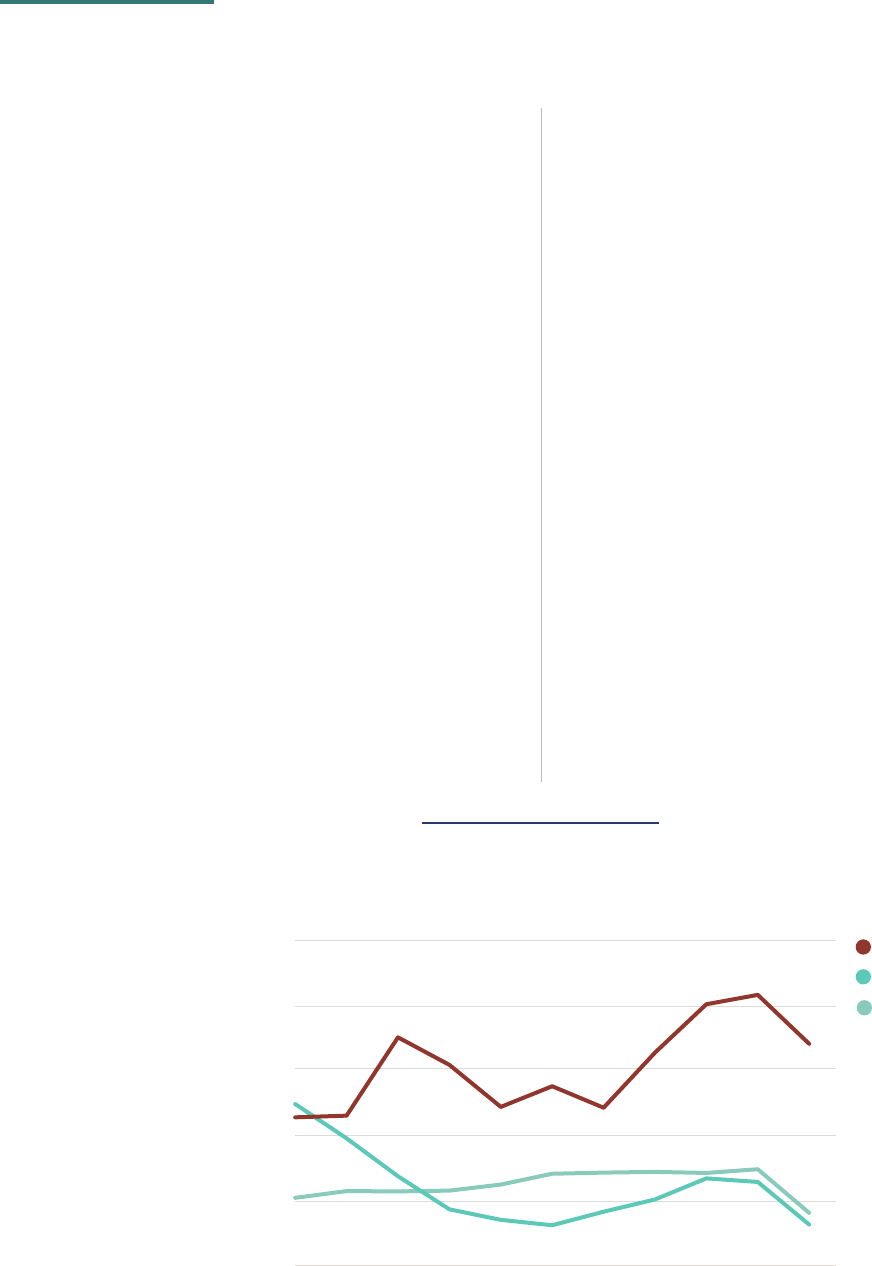

Default judgment rates may vary across courts for

several reasons, many of which have little to do with

how courts are handling cases. Potential factors

Tracking the interquartile range (IQR) of the

distribution of case outcomes is a method of

measuring case outcome variation across courts.

v

A

higher IQR value indicates that case outcomes vary

more. Given that debt collection lawsuits are usually

brought by the same bulk ling plaintiffs for similar

causes of action, we would expect there to be almost

no variation in case outcomes, especially when

controlling for demographic and other confounding

factors that could inuence case outcomes. The IQR

v When measuring default judgment rates, the interquartile range

is the distance between the 25th percentile court and the 75tn

percentile court. A greater distance between the 25th percentile and

the 75th percentile indicates a greater variation in default judgment

rates across courts. By contrast, a smaller distance between the

25th and 75th percentile indicates more similarity among courts’

default judgment rates.

Share of disposed cases by disposition type & plaintiff type annually. Does not include ~16% of cases

dismissed for non-service.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2010 - 2021.

Consumers in Predominantly Black Neighborhoods

Are More Likely to Have a Default Judgment

Default Judgment

Stipulation

Dismissal/Withdrawal

Non-Default Judgment

Black

White

Hispanic,

Asian,

No Majority

74%

64%

68%

19%

24%

22%

>1%

4%

1%

6%

7%

9%

6

Michigan District Courts

Have Fairly Similar Case

Outcomes, But Case

Outcomes Have Become

Less Similar Over Time

Section B Findings | Case Outcomes

29

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

have lower default judgment rates than lower-income

communities, which would suggest that a defendant’s

ability to afford a debt or to attend court could

inuence their level of participation and whether they

engage with the court process.

behind court variability include the following:

• Type of cases and plaintiffs

• Demographic and economic differences

between communities

• Overall case volume

• Overall debt rates in the community

• Legal Aid and availability of attorneys

• Case management systems

To account for their impact on default judgment rates

across courts, January Advisors estimated a linear

regression model based on available data related

to these factors.

vi

Based on this analysis, one of the

strongest predictors of a court’s default judgment

rate is median household income. District Courts that

are home to residents with higher incomes tend to

vi To test how much variation in case outcomes across courts

is explained by these factors, January Advisors estimated a linear

regression model that predicted the default judgment rate based on

court demographics (% of residents who are Black/African American

and Hispanic Latino), economic conditions and resources (median

household income, unemployment rate, and % households that rent),

the county overall debt rate (collected by the Urban Institute), court

case load (debt collection cases per 100 residents), plaintiff type (%

cases led by different plaintiffs), defendant legal representation

rate, Legal Aid region, and CMS provider.

Default Judgment Rates Vary Across Michigan District Courts

0

10

20

0 25 50 75 100

Default judgment rate

Number of courts

20

10

NUMBER OF COURTS

DEFAULT JUDGMENT RATE

25 50 75 100

Number of courts by percentage of cases with a default judgment from 2018-2019. Does not include ~16% of cases

dismissed for non-service.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2018-2019.

25th percentile

64%

75th percentile

72%

IQR: 8

Section B Findings | Case Outcomes

30

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Default Judgment Rates Have Become Less Similar Over Time

Across Michigan District Courts

Interquartile range (75th percentile – 25th percentile) of default judgment rates in

debt collection cases across District Courts by year.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2010-

2021.

2010-11 2012-13 2014-15 2016-17 2018-19 2020-21

10

8

6

4

INTERQUARTILE RANGE

Courts Serving Higher Income Residents Have Lower Default Judgment Rates

80

70

60

50

40

30

DEFAULT JUDGMENT RATE

MEDIAN HOUSEHOLD INCOME

$25,000 $50,000

30

40

50

60

70

80

$25,000 $50,000 $75,000 $100,000 $125,000

Median houehold income

Default judgment rate

$75,000 $100,000 $125,000

Scatter plot showing median household income vs default judgment rate at the District Court level,

2017-2019. Each dot represents a District Court.

Source: Michigan State Court Administrative Ofce Judicial Data Warehouse, 2017-2019.

31

Michigan Justice for All Commission | Debt Collection Work Group Report and Recommendations

Section B Findings | Case Outcomes

contract rate or 15% of the claim amount.

In Michigan, the amount of the judgment entered

against defendants in debt collection cases only

increases slightly to include statutory costs, fees, and

pre-judgment interest.

52

On average, the judgment

amount is only $164 more than the initial claim

amount, with the middle 50% of judgments ranging

from $117 to $200 more than the claim amount.

Based on the median claim amount of $1,600, this

means that average costs and fees added by the

court process add up to approximately 10% of the

initial claim amount.

These factors, however, only explain a portion

of the variation. After accounting for differences

in community demographics and socioeconomic

conditions, overall debt rate, caseloads, plaintiff type,

defendant legal representation, Legal Aid region,

and CMS provider, the linear regression model was

only able to explain 42% of the variation in default

judgment rates across courts – meaning that other

factors, such as differences in local court practices

and implementation of statewide policies, contribute

to the remaining 58% of variation.

While a portion of the variation may be due to

differences in court practices, this analysis does

not indicate which specic practices might be

behind the variation. Regardless, there are enough

differences in case outcomes across courts to warrant

further investigation, which could include creating

inventories of local court practices and available legal

resources. Variation in outcomes when controlling for

demographic and other factors suggests that where

someone lives, rather than the merits of the case

or their level of engagement in the process, could

inuence the type of justice they receive from the

court.

State policies on court fees and attorney fees can

greatly impact the amounts awarded in judgments

entered against consumers. A recent study in Utah

found that the judgment amount was on average

30% higher than the original amount the plaintiff

sought to recover for the debt due to costs and fees

added to the judgment.

49

Indeed, other states have

recently implemented reforms to help control these

costs – both Nevada

50

and D.C.

51

have acted to cap

debt collection attorney’s fees to the lesser of the

7