THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF

AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY

Voluntary Report – Voluntary - Public Distribution Date: February 03,2021

Report Number: JA2021-0015

Report Name: Pet Food Market in Japan

Country: Japan

Post: Osaka ATO

Report Category: Market Development Reports

Prepared By: Yumi Baba

Approved By: Jeffrey Zimmerman

Report Highlights:

The United States is the second largest exporter of pet food to Japan with 16.4 percent of the market led

by Thailand (33%) and followed by France (16%). In FY2019, imports equaled 260,000 metric tons

(MT) and represented 44 percent of total domestic pet food consumption (593,000 MT) in Japan. Japan

has had four consecutive years of increased overall value of pet food sales reaching over $3 billion in

FY2019. High value-added products are responsible, such as, health targeted premium and super

premium foods, medical and therapeutic functional foods, and a variety of treats and supplements for

pets. Due to COVID-19, the number of new pet owners year-to-date through October 2020 for both dogs

and cats increased compared to 2019. As of October 2020, the total number of dogs and cats in Japan

was approximately 18.13 million, which surpasses the Japanese citizen population of those under 15

years-old estimated at 15.3 million.

INDEX:

I. Executive Summary

II. Market Overview

A) Domesticated Dogs and Cats in Japan

B) Trends in Pets

C) Pet Food Market

1) Market Size

2) Product Type

3) Major Manufacturer

III. Market Opportunities

A) Pet Food Import

B) Key Market Issues and Trends

C) Distribution System

IV. Market Access

A) Regulation

B) Tariffs

V. Key Contacts and Information

A) Post Contacts

B) USDA Japan Websites

C) USDA Animal and Plant Health Inspection Service

D) Regulations & Standards

E) Other Information Sources

I. Executive Summary

The United States is the second largest exporter of pet food to Japan with 16.4 percent of the market

led by Thailand (33%) and followed by France (16%). In FY2019, imports equaled 260,000 metric

tons and accounted for 44 percent of domestic pet food consumption in Japan.

The Japanese pet food market volume of sales in FY2019 remained steady at around 593,000 metric

tons. Same period value of sales reached over $3 billion or a 3.5% fiscal year increase marking the

fourth consecutive year for increased value of sales.

As of October 2020, the total number of dogs and cats in Japan was approximately 18.13 million,

which surpasses the Japanese citizen population of those under 15 years-old estimated at 15.3

million.

The overall number of pets in Japan is exhibiting a declining trend due to the decrease in the dog

population exceeding the increase in the cat population.

Due to COVID-19, the number of new pet owners year-to-date through October 2020 for both dogs

and cats increased compared to 2019.

The industry experienced steady pet food sales volumes with growth in sales value through

increased purchases of health conscious premium and super premium foods, medical and

therapeutic functional foods, and a variety of treats and supplements for pets.

The most common distribution channel for pet food products in Japan is through wholesalers

specialized in pet food and products. The main consumer outlets include home centers, discount

stores, supermarkets, drug stores and pet shops. E-commerce is also supported by consumers and its

share has been growing steadily.

Exporters and businesses must comply with the Government of Japan’s Pet Food Safety Law.

Note:

This report focuses on pet foods for dogs and cats sold at retail outlets (H.S. 2309.10)

The exchange rate US $1 = ¥105 yen is used in this report unless otherwise mentioned.

The Japanese fiscal year starts in April and ends in March, so FY 2020 runs from April 2019 to

March 2020.

II. Market Overview

A) Domesticated Dogs and Cats in Japan

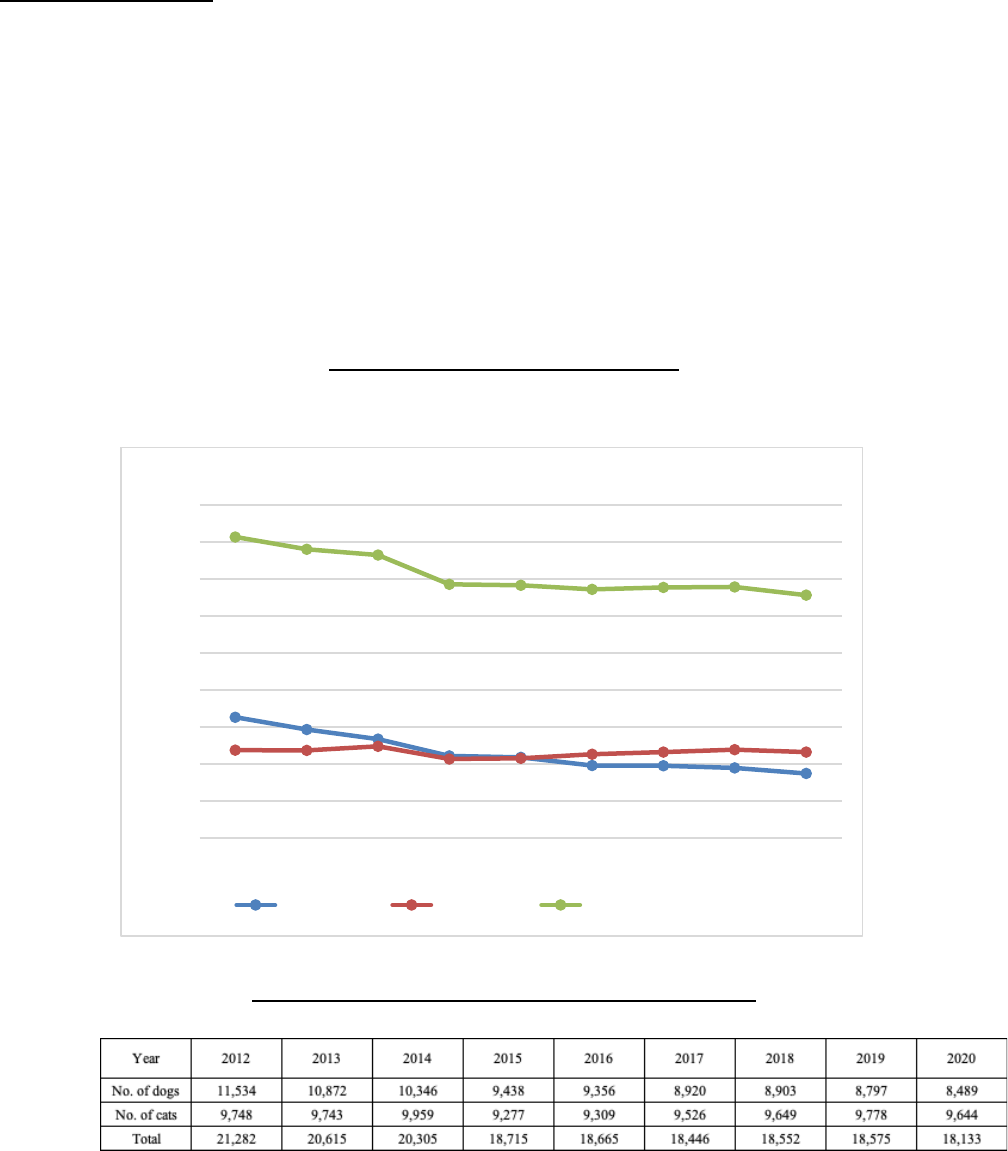

As of October 2020, Japan had approximately 18.13 million dogs (8.5 million) and cats (9.6 million)

domesticated according to the annual survey conducted by Japan Pet Food Association (JPFA). The

number of cats exceeded the number of dogs in 2017 for the first time since the JPFA survey begin in

1993. However, the overall number of pets in Japan is exhibiting a declining trend due to the decrease in

the dog population exceeding the increase in the cat population. By comparison, the number of pets in

Japan is larger than the population of Japanese citizens under 15 years-old, which total 15.33 million (as

of April 2019, Ministry of Internal Affairs & Communication).

Number of Dogs and Cat in Japan

(unit: thousand)

Number of Domesticated Dogs and Cats in Japan

(unit: thousand)

Source: Japan Pet Food Association

5,000

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

23,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

No. of Dogs No. of Cats No. of Dogs & Cats

B) Trends in Pets

In recent years, the trend among the Japanese pet population could be described in four key words; 1)

Indoor 2) Small 3) Aging and 4) Sicknesses related to obesity and life-style. These identified trends are

based on the following sources: iPet Insurance Co., Ltd and Anicom Group Holdings Inc. and the Japan

Pet Food Association.

1) Indoor Breeding

Keeping pets indoors is a norm compared to the past in Japan. The JPFA survey shows that 84.7

percent of dogs and 90.4 percent of cats are kept indoors as of the year 2020. Pets kept indoors

are less likely to become sick and tend to live longer. This is also a driving factor in the aging

and obesity of pets.

2) Smaller & Miniature Size Pedigree Dogs vs. Majority of Crossbred Cats

In 2020, the following four dog breeds were ranked highest for ownership in Japan; Toy Poodle

(13.1%), Chihuahua (12.8%), Shiba (11.8%) and Minitour Dachshund (11.3%). Although the

rankings have changed, the top four dog breeds have remained the same since 2016. Crossbred

dogs accounted for only 10.1 percent. On the other hand, the vast majority of pet cats are

crossbred with 75.5 percent, followed by American Shorthair (4.8%) and Scottish Fold (3.4%).

3) Aging

In 2020, the average life expectancy of a dogs and cats was 14.48 years and 15.54, respectively.

The average life expectancy of dogs was only 4.4 years in 1980s and although there are some

differences depending on the breed, it has tripled in the last 30 years. The average life

expectancy of the indoor cats was said to be longer than that of the external cats because

external cats are more likely to be injured and/or contract disease.

With the spread of vaccines in recent decade, infectious diseases such as parvovirus and

distemper virus have decreased for dogs. The ease of prevention also contributes to the

reduction of infectious diseases. The number of filariasis infections (heartworm), which

accounted for the majority of deaths before 1980, has been greatly reduced through easily

administered oral and topical medications. Improved pet care practices through high-quality

nutritious foods, advanced pet medical care by veterinarians (including sterilization) and raising

indoors have all contributed to the increased life expectancy of pets in Japan.

Average Life Expectancy of Dogs & Cats in Japan

(unit: year-old)

(Source: Japan Pet Food Association)

4) Sickness related to Obesity and Life-style

There is an increase pets suffering from obesity and life-style related illnesses as a result of

increased age, indoor habitation, and overnutrition. Common life-style related illnesses include

arthritis, heart disease, bladder and urinary tract disease, chronic kidney disease, liver disease,

diabetes, high blood pressure, spine disease, among others.

C) Pet Food Market

1) Market Size

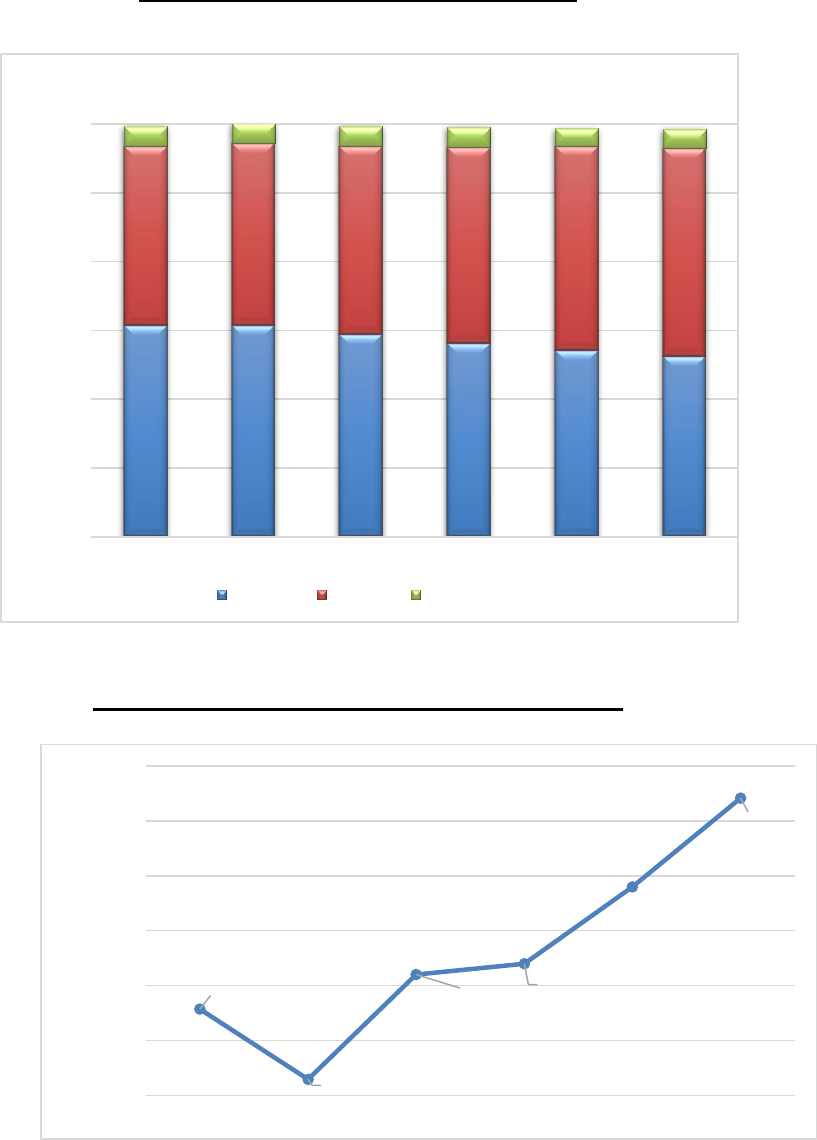

The Japanese pet food market by volume in FY2019 was steady and estimated at around

593,000 metric tons (MT), (99.8% vs. FY2018). Same period value of sales reached over $3

billion (105.6% vs FY2018) marking the fourth consecutive year in increased sales value.

The less than one percent year-on-year decline in the pet food market volume is attributed to the

decrease in the total number of pets coupled with smaller-framed dog breeds gaining popularity.

The industry observes a shift toward increased consumer spending on a variety of premium and

super-premium high-quality pet foods as well as specialized healthy and therapeutic pet foods

labeled as sickness prevention, allergen-free, vitamins/supplements fortified, gluten-free,

carbohydrate and protein specified and more.

14.50

14.39

14.19

14.29

14.44

14.48

15.43

15.09

15.33

15.32

15.03

15.54

13.50

14.00

14.50

15.00

15.50

16.00

2015 2016 2017 2018 2019 2020

Average life-span of dogs Average life-span of cats

Pet Market by Volume FY2014 to FY 2019

(unit: metric ton)

Source: Japan Pet Food Association

Total Pet Food Market in Value FY 2014 – FY 2019

(unit: US$ million, $1=105 yen)

Source: Japan Pet Food Association, modified to U.S. dollar by ATO Osaka

307,150 307,151

294,844

281,083

271,212

262,360

260,436

265,490

273,766

285,790

296,533

303,527

29,284

28,987

28,811

29,397

25,980

26,912

0

100,000

200,000

300,000

400,000

500,000

600,000

FY 2014 FY 2015 FY 2016 FY 2017 FY 2018 FY 2019

For Dogs For Cats For Other Pets

$2,656.99

$2,529.11

$2,720.07

$2,739.81

$2,879.65

$3,041.50

$2,500.00

$2,600.00

$2,700.00

$2,800.00

$2,900.00

$3,000.00

$3,100.00

2014 2015 2016 2017 2018 2019

2) Pet Food Categories

All pet foods - dry, semi-moist, soft-dry, wet ettc. - have been heat-treated to improve digestion

and absorption of raw materials and to prevent microbial contamination. This is contrast to

animal feed that may or may not be heated treated.

Pet foods are divided into four main categories: General nutrition food, Snacks, Therapeutic

food, and Other purpose foods. Pet food as a staple food is called "Sogo Eiyoshoku” (translated

as “general nutrition food”) and is manufactured for necessary nutrient intake in conjunction

with a supply of water. Although snacks are not necessary as a nutrient supplement, it is a pet

food intended to be given in a limited amount for pet discipline, exercise, and reward.

There are growing variety of therapeutic foods for pets. Veterinarians may recommend specific

nutritional diets when treating diseases in dogs and cats. These foods assist the treatment of

disease by adjusting the amount and ratio of nutritional components in the food accordingly as

recommended under veterinarian guidance. Products examples are; kidney support, urolithiasis,

diabetic, dermatological and allergy disorder, weight control and more.

“Other purpose foods” serve a specific purpose such as adjustments to nutrition profile,

supplementing calories, enhancing palatability, among other uses and are provided in

conjunction with pet food or ingredients.

Dog and cat foods are categorized into the following five types based on its water content:

Pet Food Product Type in Japan

Type

Definition

Dry

Water content of about 10% or less. The raw materials are crushed and

compounded, foamed and molded by an extruder (heated and pressured), then dried

and cooled. The heating temperature in the extruder reaches 235-275F (115-

135℃). Depending on the raw material, it goes up to as high as 320F (160℃).

Soft-dry

Water content of 25-35%. Manufactured by an extruder. It is foamed like a dry

food and cooled like a semi-moist food without being dried. Moistening agents are

often used. Packed using high barrier packaging materials and often uses oxygen

scavengers.

Semi-moist

Water content of 25-35%. Manufactured by an extruder but not foamed.

Moistening agents are often used. Packed using high barrier packaging materials

and often uses oxygen scavengers.

Wet

Water content of about 75% and undergoes a sterilization process to maintain

quality. The temperature and time for sterilization differ depending on the size of

the can and contents. To contain, usually steel or aluminum cans are used as well as

aluminum trays and retort pouches.

Other (snack)

Other than above, including biscuit, gum, jerky, dry meat and bone products. As a

general rule, caution is given to limit the amount within 20% of the daily energy

requirement in order to maintain proper nutrition.

Source: Japan Pet Food Association

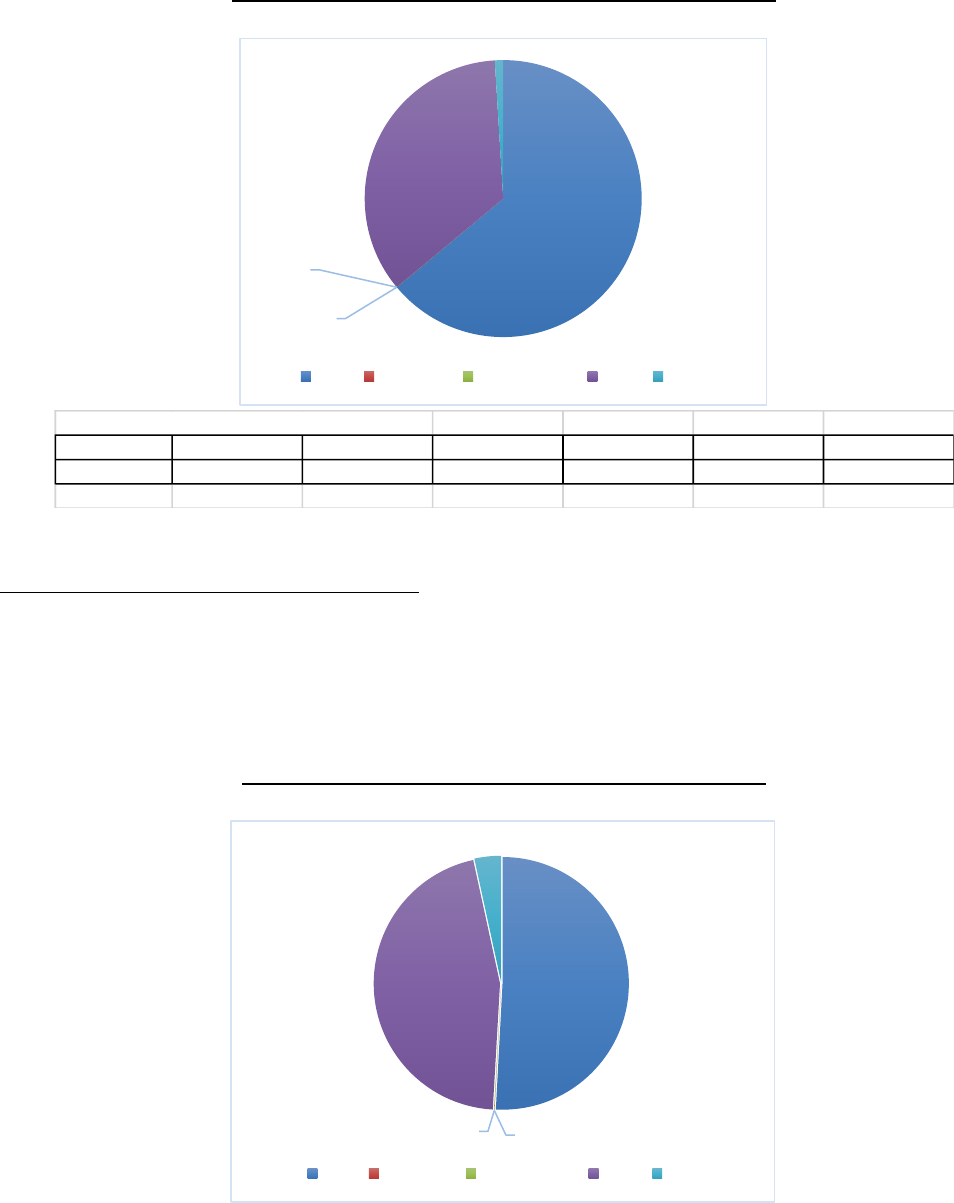

Dog Food Market by Product Type in FY 2019

Dog Food Market by Product Type (in volume):

In FY2019, dry food still dominated the dog food market with 67.3 percent market share in volume of

sales after a 5.1 percent decrease when compared to FY2018. Similarly, both soft-dry and semi-moist

volume of sales decreased to 3.2 percent and 1.0 percent, respectively, while wet-type food increased to

4.1 percent compared to FY2018. In total volume, Japan’s FY2019 dog food market decreased 3.3

percent compared to FY2018.

Dog Food Market by Product Types in FY 2019 (volume)

Dog Food Market by Food Types in FY2019

Dry Soft Dry Semi-moist Wet Other Total

in volume 176,609 21,570 5,104 34,017 25,061 262,361

(unit: metric ton)

Source: Japan Pet Food Association

Dog Food Market by Product Type (in value):

In FY2019, overall pet food sales value in Japan increased 3.5 percent compared to FY2018. All types

of dog food, except “other type,” increased their value of sales in FY2019 compared to FY2018. Both

dry and wet food increased 5.6 percent and 8.1 percent respectively.

Dry

67.3%

Soft-dry

8.2%

Semi-moist

1.9%

Wet

13.0%

Other

9.6%

Dry Soft-dry Semi-moist Wet Other

Dog Food Market by Food Types in FY2019 (value)

Dog Food Market by Food Types in FY2019

Dry Soft Dry Semi-moist Wet Other Total

in value ($) $718 $64 $27 $207 $339 $1,355

(unit: million, $1=105 yen)

Source: Japan Pet Food Association, modified to U.S$ by ATO Osaka

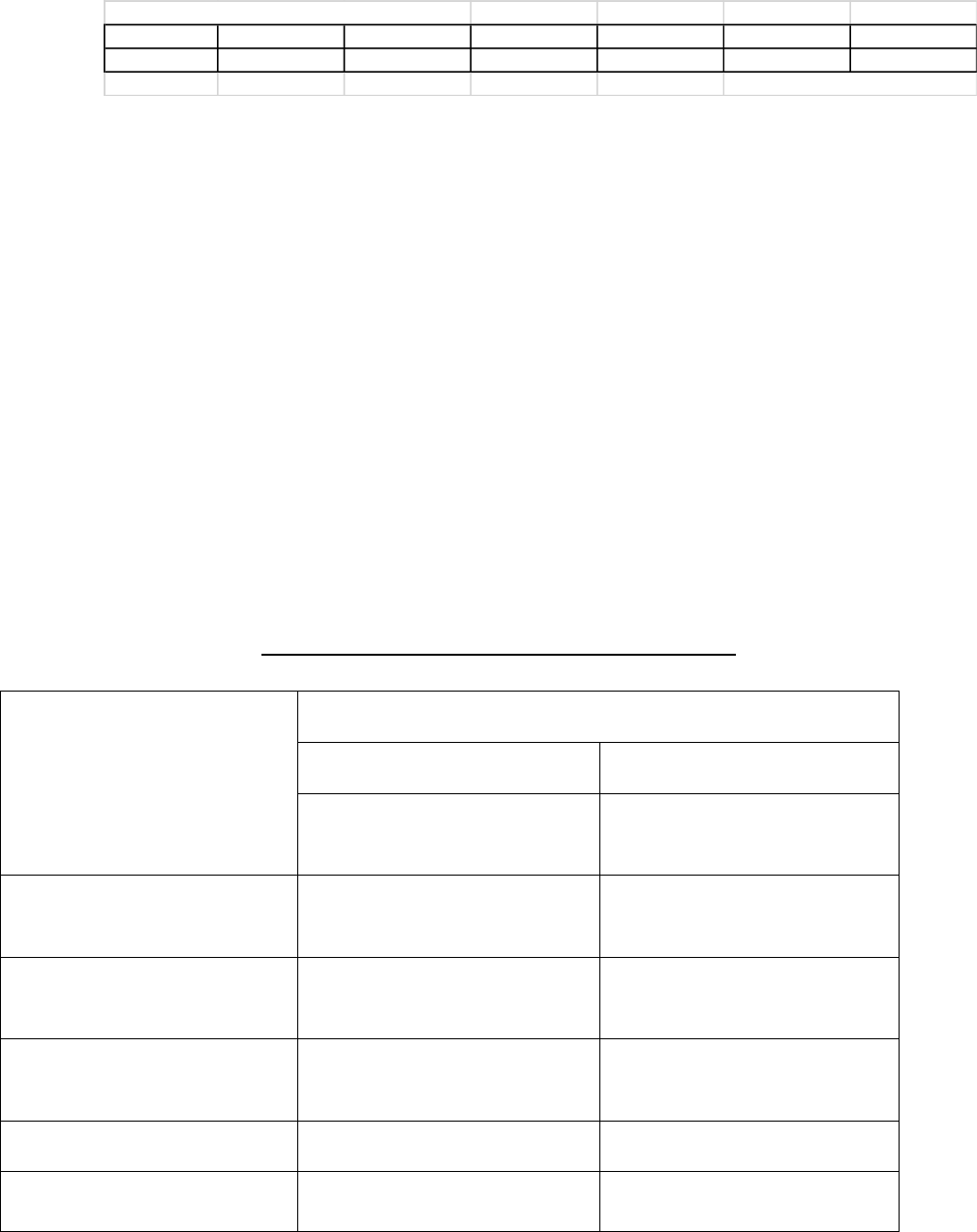

Cat Food Market by Product Types in FY 2019

Cat Food Market by Food Types (in volume):

In FY2019, the cat food market was dominated by dry food with 63.9 percent market share and this

category increased 2.1 percent compared to FY2018. Semi-moist cat food marked a significant increase

at 365 percent compared to FY2018 together with wet food (2.1%) and other food (32.3%), which led

total cat food volumes to increase 2.4 percent in FY2019.

53.0%

4.7%

2.0%

15.2%

25.0%

Dry Soft Dry Semi-moist Wet Other

Cat Food Market by Food Types in FY2019 (volume)

Cat Food Market by Food Types in FY2019

Dry Soft-dry Semi-moist Wet Other Total

in volume 194,078 3 33 106,463 2,951 303,528

(unit: ton)

Source: Japan Pet Food Association

Cat Food Market by Food Types (in value):

In FY2019, the overall total value of cat food sales in Japan increased 7.9 percent compared to FY2018.

All types of cat food except soft-dry food (decreased by 33.3%) increased their value in FY2019

compared to FY2018. As a newer market category, the FY2019 increase in value of semi-moist cat food

jumped 9,795 percent as well as both wet (8.6%) and other food (10.4%).

Cat Food Market by Food Types in FY2019 (value)

Dry

63.9%

Soft-dry

0.0%

Semi-

moist

0.0%

Wet

35.1%

Other

1.0%

Dry Soft-dry Semi-moist Wet Other

50.8%

0.0%

0.1%

45.7%

3.4%

Dry Soft-dry Semi-moist Wet Other

Cat Food Market by Food Types in FY2019

Dry Soft-dry Semi-moist Wet Other Total

in value ($) $806.9 $0.2 $0.9 $724.9 $54.0 $1,586.9

(unit: million$, $1=105 yen)

Source: Japan Pet Food Association, modified to U.S. dollar by ATO Osaka

3) Major Manufacturers and Name Brands

The Japan pet food manufacturing sector has the presence of long-standing and large foreign-

affiliated companies such as Mars Japan, Nestlé Japan and Hill’s Holgate Japan. However,

domestic manufacturing companies are also growing through attracting pet owners that have a

preference for nationally produced products. Japanese pet food manufacturers are also growing as a

result of increased international marketing and sales. Japan’s Nisshin Pet Food announced their

merger with PETLINE in December 2019, which is expected to advance PETLINE within the top

five pet food manufactures in Japan. With the steady increase in cats as pets, there has been an

increase in cat food manufacturers to provide increased cat food options. Store shelves are now built

more around cat products and sales of domestic cat food companies. For example, domestic Inaba

Pet Food is a growing cat food company with increasing sales of very popular cat treat “Ciao

Chuuru” and easy-to-serve cup wet cat food.

The major pet food manufacturers and their product brands are listed in the following table:

Table: Major Pet Food Manufacturers in Japan

Manufactures

Major Pet Food Brands

Dog Foods

Cat Foods

Mars Japan Ltd.

Pedigree, Cesar, Nutro,

IAMS, Greenies

Kalkan, Sheba, KiteCat

Unicharm Corporation

(Pet Care Division)

Gran Deli, Best Balance,

Aiken-Genki

Neko-Genki, Gin-no-spoon,

Mitsuboshi Gourmet

Royal Canin Japon Inc.

(under Mars Group)

Royal Canin

Royal Canin

Nestlé Japan (Pet Division)

Purina One, Purina, Pro Plan

Purina One, Mon Petit,

Friskies

Inaba Pet Food Co., Ltd

Zeitaku, Toromi

Kin-no-dashi, Ciao

Hill's - Kolgate Japan Ltd.

Science Diet, Prescription

Science Diet

Diet

Nisshin Pet Food

Run, JP Style

Carat, JP Style

Doggy Man H.A. Co., Ltd.

Saya

Seko-Saya

Nihon Pet Food

Vita Wan, Lacine Dog,

Combo-dog, Beauty Pro Dog

Mio, Lacine Cat, Combo-cat,

Beauty Pro Cat

PETLINE

Medycoat, Professional

Balance

Cannet, Luna, Medyfas

Reference: ATO Osaka modified the table from PEDGE adding information from company URLs.

III. Market Opportunities

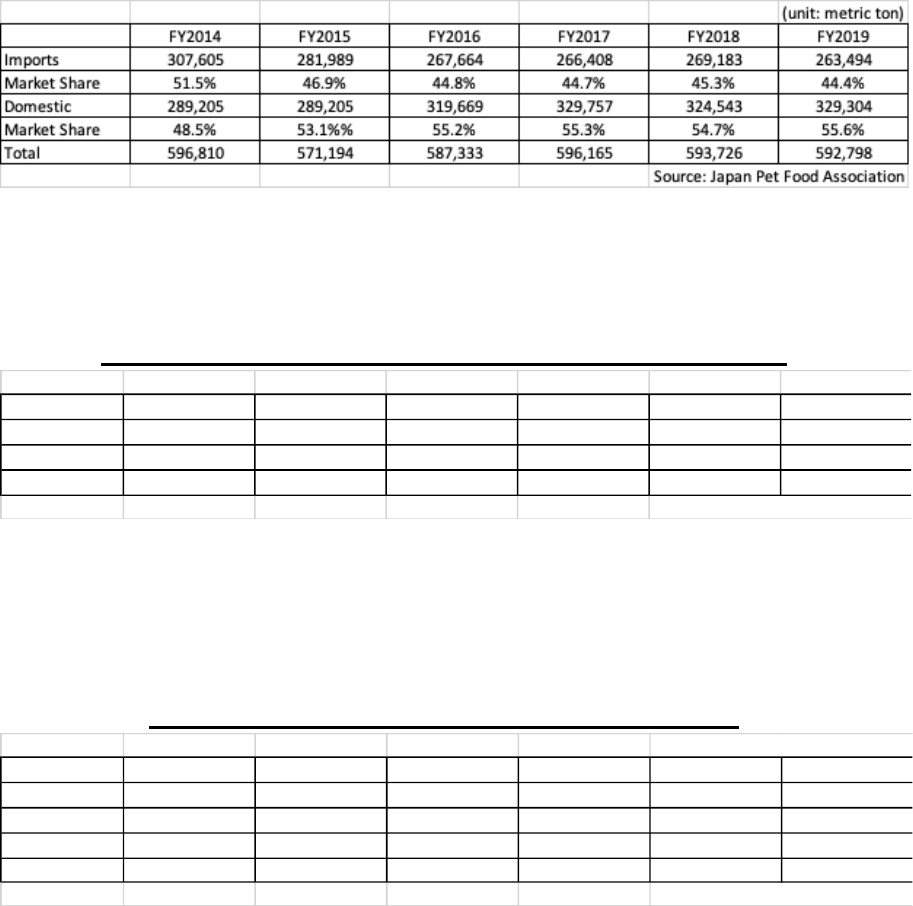

(A) Pet Food Import

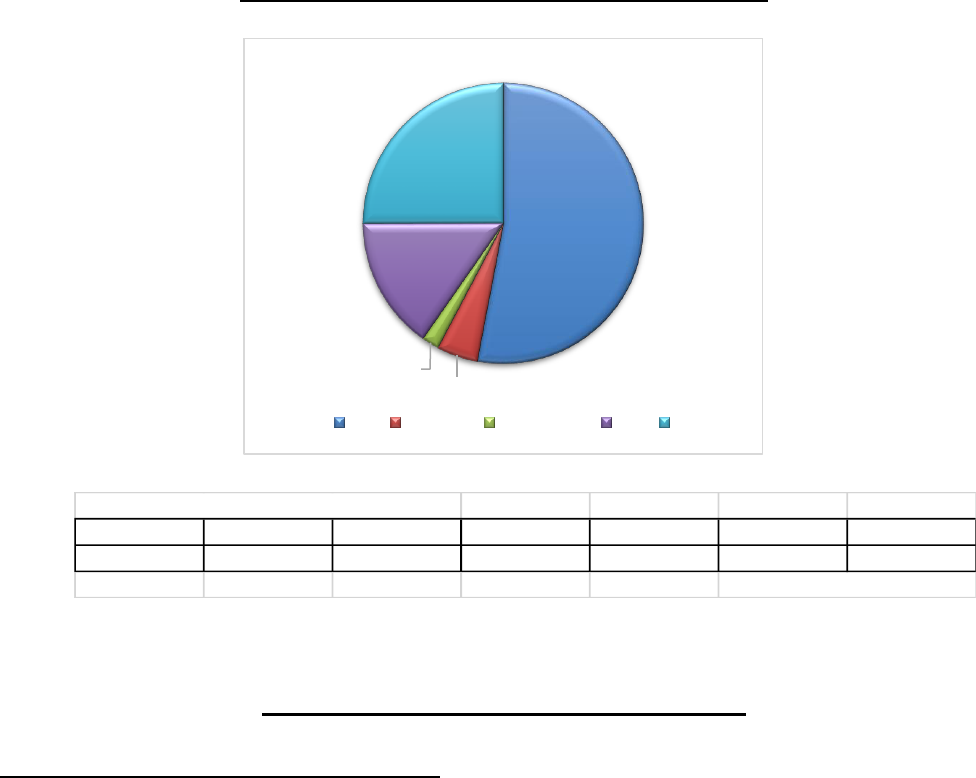

The pet food volume of sales in Japan reached 592,799 metric tons in FY2019, of which imports

accounted for 263,494 metric tons or 44.4 percent of the total volume. Japanese domestic share

of the pet food market has gradually increased over the past several years to again reach over 50

percent levels last seen in 2009 and pre-1994. This is attributed to the general Japanese consumer

preference to purchase domestically produced products under a perceived "food safety and

security" notion associated with made in Japan products.

Domestic v.s. Imported Pet Food in Volume (FY2014 to FY2019)

(unit: metric ton)

307,605

281,989

267,664

266,408

269,183

263,494

289,205

289,205

319,669

329,757

324,543

329,304

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

FY2014 FY2015 FY2016 FY2017 FY2018 FY2019

Imports Domestic

Domestically produced pet foods account for over 50 percent of all pet food types in 2019 in volume and

the industry expects this trend to continue. The table below shows both imported and domestically

produced pet foods in volume by pet type (dog, cat and other pets).

Imported vs. Domestic Pet Food - Volume in FY2019 (by Pet Type)

(unit: metric ton)

for dogs share for cats share for other pets share

Domestic 134,317 51.2% 170,524 56.2% 24,463 90.9%

Imported 128,043 48.8% 133,002 43.8% 2,449 9.1%

Total 262,360 100.0% 303,526 100.0% 26,912 100%

Source: Japan Pet Food Association

Total value for imported pet food exceeds domestically produced product indicating strong brand and

consumer awareness. Even declining pet ownership and smaller breed preference, the pet food industry

foresees continued growth in value through increased supply of premium and super premium foods,

health & medical/therapeutic functional foods, variety of treats and supplements for pets.

Imported vs. Domestic Pet Food - Value (FY2014 to 2019)

(unit: $million, $1=105)

FY2019

FY2018 FY2017 FY2016 FY2015 FY2014

Imported $1,680 $1,622 $1,535 $1,562 $1,442 $1,632

Domestic $1,362 $1,258 $1,204 $1,158 $1,087 $1,025

Total $3,042 $2,880 $2,740 $2,720 $2,529 $2,657

vs previous year 105.6% 105.1% 100.7% 107.6% 95.2% 104.0%

Source: Japan Pet Food Association

The top three exporting countries – Thailand, United States, France - to the Japanese pet food market

accounted for over 65 percent of the total imports in FY2019. Thailand became top exporting country

for Japan’s pet food market mainly due to the increasing in the number of pet cats in Japan and their

comparative advantage in low-cost seafood-based ingredients for cat foods. The table below lists

exporting countries to the Japanese pet food market. These three exporting countries collectively.

Exporting Countries to the Japanese Pet Food Market in FY2019

(unit: metric ton / %)

No. Country for dog for cat for pet fish

for small

animals

for birds for other pets Total (MT)

Market Share

(%)

vs FY2018

(%)

1 Thailand 16,165 70,746 0 70 0 20 87,000 33.0% 99.2%

2 U.S.A. 24,527 18,015 0 635 143 0 43,320 16.4% 104.10%

3 France 27,704 14,417 0 14 0 0 42,135 16.0% 93.7%

4 Australia 10,291 10,098 0 83 0 0 20,472 7.8% 88.8%

5 China 14,147 2,054 123 116 18 612 17,070 6.5% 118.5%

6 Netherland 11,695 2,247 0 192 0 0 14,134 5.4% 96.9%

7 Czech Republic 8,038 3,403 0 0 0 0 11,441 4.3% 90.4%

8 Korea 839 9,082 2 1 2 0 9,926 3.8% 203.8%

9 Germany 5,116 0 0 0 0 0 5,116 1.9% 54.9%

10 Canada 3,158 1,451 0 0 4 7 4,621 1.8% 57.6%

11 Austria 2,299 1,291 0 0 0 0 3,590 1.4% 224.2%

12 Poland 3,279 0 0 0 0 0 3,279 1.2% 67.9%

13 New Zealand 602 51 0 0 0 0 653 0.2% 107.1%

14 Vietnam 144 142 0 1 0 44 331 0.1% 44.5%

15 Taiwan 5 0 110 0 0 3 118 0.04% 84.9%

16 Indonesia 0 0 0 64 0 0 64 0.02% 1280.0%

17 Others* 34 5 0 183 2 0 224 0.09% 240.9%

Total 128,043 133,002 235 1,359 169 686 263,494 100.0%

% vs Total 48.6% 50.5% 0% 1% 0% 0% 100%

*Others includes: Nepal, Mexico, Spain, Hungury and other countries. Source: Japan Pet Food Association

(B) Key Market Issues and Trends

1. COVID Impact

As a result of COVID, on April 7, 2020 the Government of Japan (GOJ) declared a state of

emergency and asked people to stay home. During these stressful days, the demand for pets,

especially kittens and puppies increased significantly. According to several industry press

reports, many pet shops revealed that they were unable to maintain pets in inventory on

display due to record sales between May and July 2020. In Japan, the average cost per kitten

is between US$2000 to US$3000 and per puppy is over US$4000 to US$8000. Usually the

summer represents a low sales season with a greater number of kitten available on discount,

but this past year the price for pets did not decrease. The distribution of GOJ’s special fixed-

amount benefit of 100,000 yen (about $920) per person, seems to have spurred an increase in

pet purchases. The majority in the industry see this as a temporary phenomenon but

anticipate additional increases in sales of pet related products. This change has already been

confirmed across varieties of pet foods with increased sales of higher-priced wet and semi-

moist types. In addition, a few industry press reports showed a 10 to 15 percent increase in

the sales of pet foods during Japan’s state of emergency as a large number of pet owners

stockpiled pet foods together with their groceries.

2. Progressing Product Segmentation and Diversification

Today it is very common for pet foods to be categorized by age, breed, and size. Moreover,

pet owners recognize their pets as part of the family nucleus and seek to provide “tastier” and

“healthier” pet food for their pet. As a result, Japan’s pet food categories have become more

specialized than they were five to ten years ago and exhibit wider consumer choice to attend

to multiple pet health or preventative care needs. Therefore, sales of traditional large-bagged

more economical pet foods have declined in favor of new value-added products to meet

diversified consumer demands that also have higher per unit value.

3. Growing Premium Pet Food Sector

The premium pet food market has been growing steadily at the rate of few percentage points

annually for the past decade. According to Fuji Keizai’s June 3, 2020 press release on pet

related product research, the sales of premium pet foods increased by 3.7 percent in 2019

compared to 2018 and reached a market value of 72.4 billion yen (about US$687.5 million,

$1=105.54yen). Some industry experts anticipate continued growth to surpass sales valued at

100 billion yen (about $951million, $1=105.2 yen) in only a few years.

As premium pet food market is steadily growing, market competition has become fiercer. If

one does not have an innovative product with targeted attributes developed before entering

the market, it will be very hard to obtain success in Japanese market. There are already a

variety of premium pet food brands from major to small companies and developing new and

loyal customers is challenging. In Japan, competition is further intensified due limited shelf

space at the majority of retailers who have extremely small store footprints.

Premium Pet foods could be divided into two approaches: “health” and “epicure”. Products

focused on “health” possess excellent nutritional components and care for health problems

and/or symptoms (i.e. therapeutic foods) particular to the pet’s needs such as food allergies,

urolithiasis, obesity, kidney diseases, gastroenteropathy. Products focusing “epicure” having

carefully selected ingredients and high palatability. These products more commonly are

associated with cats that tend to exhibit quicker disaffection with their foods with owners

prone to switch offerings more often. .

4. Launching Super Premium Pet Food

To differentiate from premium pet food and highlighting further added value, some pet food

manufacturers have started to launch so called “Super Premium” pet food. Some examples of

super premium pet foods are; organic approved and human grade ingredients, gluten-free,

grain-free, low-fat and high-protein, low-temperature processed, air-dried, frozen, and

custom tailor-made with home delivery system and more.

5. Internet and Smartphone

The pet industry has long been centered on an off-line business model. However, pet industry

businesses are fast building D2C (Direct to Consumer) approaches of manufacturers to

consumers that include product specific promotion apps to build customer loyalty. This is in

tandem with conventional marketing means of TV commercial, press, magazine and other

publications approaches. Emergence of internet-based malls and shops include niche markets

and e-commercialization within the pet industry.

(C) Distribution System

1. Distribution Channels

The most common distribution channel for pet foods in Japan is through importers,

wholesalers and in some cases secondary wholesalers to retailers. In the case of Japanese

manufacturers that own production facilities abroad, products are imported directly inside the

company or through their subsidiaries and then distributed to the retailers through

wholesalers as described above. Although there are cases in which retailers buy directly from

importers, these cases are limited.

2. Major Wholesalers

Wholesalers who handle pet food and related supplies are roughly divided into three types: 1)

pet specialty wholesalers, 2) food related wholesalers and 3) daily sundries wholesalers. The

top three pet specialty wholesalers have a combined estimated 70 percent market share and

include: Japell Co., Ltd. (Aichi-based, annual sales of about U.S.$1.2 billion as of March

2020), Echo Trading Co. Ltd. (Hyogo-based, US$775 million annualized as of February

2020) and Lovely Pet Trading Co. (Osaka-based, US$227 million annualized as of June

2020). For food related wholesalers, two major companies Mitsui Foods Co. Ltd. and

Ryoshoku Petcare (a part of Mitsubishi Shokuhin Co. Ltd.) utilize their own internal and

logistical networks to provide rapid comprehensive services nationwide. Overall, the sector

exhibits oligopolist characteristics further advanced since 2013 when Echo Trading Co., Ltd.

concluded a capital and business alliance agreement the third largest specialized trading

company Kokubu Group Corporation. As a result, small- to medium-sized wholesalers face

constraints to expand services.

3. Retailers

There are six main retail outlets for pet food and related products: a) home center and

discount store b) e-commerce c) supermarket d) pet shop e) drug store and f) convenience

stores.

a. Home Center and Discount Store

Home centers and discount stores are the largest retail channels for pet related supplies

including pet foods as they stock a large amount of discount pet food products and often

as a loss leader. Home centers and discount stores possess a larger store footprint and

24/7 or extended business hours compared to other retail outlets. However, market share

is gradually decreasing as e-commerce sales increase.

b. E-commerce

An abundant product lineup, 24/7 around-the-clock service and convenient home delivery

upon purchasing are strongly supported by consumers. E-commerce market share has

grown steadily and is expected to continue. Amazon is the predominate market leader.

Other retailers have also launched and strengthen their e-commerce and digitalization as

well as teaming up with other companies such as distributors and telecommunication

companies to compete against Amazon in this space.

c. Supermarket

Supermarkets meet the regular needs of customers who purchase pet food while shopping

for their groceries. Most supermarkets do not have large store footprints and offer limited

products. On the other hand, General Merchandize Stores (GMS) of Aeon and Ito Yokado

have large store footprints and offer a large selection of products including their own

private brand pet products.

d. Pet Shop

Pet shops are characterized by having a wide range of products, especially a variety of

premium foods coupled with store staff expertise. As more and more pet owners seek

quality pet food for their pet(s), pet shops continue to receive a steady number of

customers. Customers tend to buy pet foods and pet-related products when they purchase

pet(s) at pet shops and usually rely on advice from the store staff and continue coming

back for routine shopping and use of other store services, i.e. pet hotel, pet trimming, pet

insurance and more.

e. Drug Store

The number of drug stores has expanded to provide, in part, products targeting the

increase in number of working women. These products include pet related products,

especially for cat(s) and small dog(s) along with their usual line of cosmetics and

everyday sundries. Almost all major drug stores (Tsuruha, Welcia, Cosmos,

Matsumotokiyoshi, Sugi Drug) co-host internet shopping sites where much more variety

of products, including pet-related products, are offered beyond what is available in store.

f. Convenience Store

Although convenience stores are not a major outlet for pet-related products with their

extremely limited sales space, there are over 52,000 stores among three major

convenience store brands; Seven-Eleven (20,987 stores as of September 2020),

FamilyMart (16,634 stores as of August 2020) and Lawson (14,444 stores as of February

2020) that carry pet-related products in Japan. Convenience stores see value in carrying

pet related products as customers who purchase pet related products tend to spend more

compared to regular customers.

IV. Market Access

A. Regulation on Safety of Pet Foods

The Pet Food Safety Law came into force on June 1, 2009 in order to ensure the safety of pet

food. Prior to this law, there was no legislation to regulate the production and distribution of pet

food in the Japanese market, except that some pet foods with medical claims were subject to the

Pharmaceutical Affairs Law. The 2007 incident with adulterated pet foods from China that were

contaminated with melamine prompted enhanced regulatory action and oversight by the

Japanese Ministry of Agriculture, Forestry and Fisheries (MAFF) and the Ministry of

Environment (MOE).

The Pet Food Safety Law defines the responsibilities of pet food manufacturers, importers,

wholesalers and retailers as well as the scope of government authority to regulate the market. It

also outlines specifications and standards for pet food products to be distributed within the

market. The law defines the minimum criteria for labeling, while a voluntary labeling code is

being maintained as an industry-wide self-imposed requirement in addition to the law.

For more details on Pet Food Safety Law, please visit below sites;

Information for manufactures, importers, and distributers of pet foods

1. For Securing Safety of Pet Food (PDF : 407KB)

2. Notification and Record-Keeping Manual Based on the Pet Food Safety Act (PDF :

708KB)

3. In Order to Supply Safe Pet Foods (PDF : 872KB)

4. Are your pet food products properly labeled with their COUNTRY OF

ORIGIN ?(PDF : 129KB)

5. Manual for the Manufacturing of Safe Pet Foods (PDF : 305KB)

6. Pet Food Sanitation Management Manual (PDF : 2,752KB)

7. Use of wild animal meat in pet food production (PDF : 206KB)

8. Pet Food Safety Act: Labeling Check Sheet (PDF : 180KB)

Related Laws and Regulations

Document List on the Pet Food Safety Law (Food and Agricultural Materials Inspection

Center)

1. Summary of Law for Ensuring the Safety of Pet Food

2. List of Specifications and Standards of Pet Food

3. Act on Ensuring the Safety of Pet Food

4. Government Ordinance Pursuant to Act on Ensuring the Safety of Pet Food

5. Ministerial Ordinance for Enforcement of the Pet Food Safety Act

6. Ministerial Ordinance on Specifications and Standards of Pet Food

7. Concerning the Enforcement of Act on Ensuring the Safety of Pet Food

Batch Download

B. Tariffs

Please refer to below link of Japan Customs for tariff rates on H.S. code 2309.10 (010 to

099) and 2309.90 (110 to 2999):

https://www.customs.go.jp/english/tariff/2020_4/data/e_23.htm

V. Key Contacts and Further Information

A. Post Contacts

For further information, please contact the U.S. Agricultural Trade Offices (ATO) in Japan at the

following addresses:

ATO Office in Tokyo ATO Office in Osaka

U.S. Embassy, Tokyo U.S. Consulate General, Osaka-Kobe

1-10-15, Akasaka, Minato-ku 2-11-5, Nishi-tenma, Kita-ku

Tokyo, 107-8420 Osaka, 530-8543

Tel: +81-3-3505-5115 Tel: +81-6-6315-5904

Fax: +81-3-3582-6429 Fax: +81-6-6315-5906

B. USDA Japan Websites

http://www.usdajapan.org/ (in English)

http://www.usdajapan.org/ja/ (in Japanese)

C. USDA Animal and Plant Health Inspection Service

Japan - pet food, chews, and treats (animal-origin)

https://www.aphis.usda.gov/aphis/ourfocus/animalhealth/export/iregs-for-animal-product-

exports/sa_international_regulations/sa_products_japan/ct_pet-food-chews-and-treats-animal-

origin

D. Related Japanese Ministry Websites

Ministry of Agriculture, Forestry and Fisheries (MAFF)

https://www.maff.go.jp/e/index.html (in English)

Ministry of Environment (MOE)

https://www.env.go.jp/en/index.html (in English)

Ministry of Health, Labor, Welfare (MHLW)

https://www.mhlw.go.jp/english/ (in English)

Food and Agriculture Material Inspection Center (FAMIC)

http://www.famic.go.jp/english/ (in English)

Japan Customs

https://www.customs.go.jp/english/index.htm (in English)

Animal Quarantine Service (Bringing Animal Products into Japan)

https://www.maff.go.jp/aqs/english/product/import.html (in English)

Designated establishment lists for some pet food or pet food materials

U.S. powdered poultry meat for pet food production

https://www.maff.go.jp/aqs/tetuzuki/product/attach/pdf/index-6.pdf

U.S. pork-meat-derived for pet food production

https://www.maff.go.jp/aqs/tetuzuki/product/attach/pdf/index-9.pdf

E. Other Information Sources

Japan Pet Food Association

https://petfood.or.jp/English/message/index.html (in English)

https://petfood.or.jp/index.html (in Japanese)

Japan Pet Food Fair Trade Association

https://pffta.org/soshiki/greeting.html (in Japanese only)

Attachments:

No Attachments.