REPORT ON EXAMINATION

OF

ORANGE-ULSTER SCHOOL DISTRICTS PLAN

AS OF DECEMBER 31, 2017

EXAMINER: CHARLES J. MCBURNIE

REVIEWER: WAI WONG, CFE

DATE OF REPORT: SEPTEMBER 21, 2022

TABLE OF CONTENTS

ITEM NO.

PAGE NO.

1.

Scope of the examination

2

2.

Description of the Plan

A. Corporate governance

B. Territory and plan of operation

C. Stop-loss coverage

D. Administrative service agreements

E. Municipal cooperative agreement

F. Plan document and summary description

G. Underwriting results

H. Internal controls

4

5

8

10

11

12

17

19

20

3.

Financial statements

A. Balance sheet

B. Statement of revenue and expenses and surplus

20

22

23

4.

Claims payable

24

5.

Claims stabilization reserve

25

6.

Market conduct activities

A. Standards for prompt, fair and equitable settlement of

claims for health care and payments for health care

services (“Prompt Pay Law”)

B. Mental Health Parity and Addiction Equity Act

(“MHPAEA”)

26

26

27

7.

Compliance with prior report on examination

29

8.

Summary of comments and recommendations

32

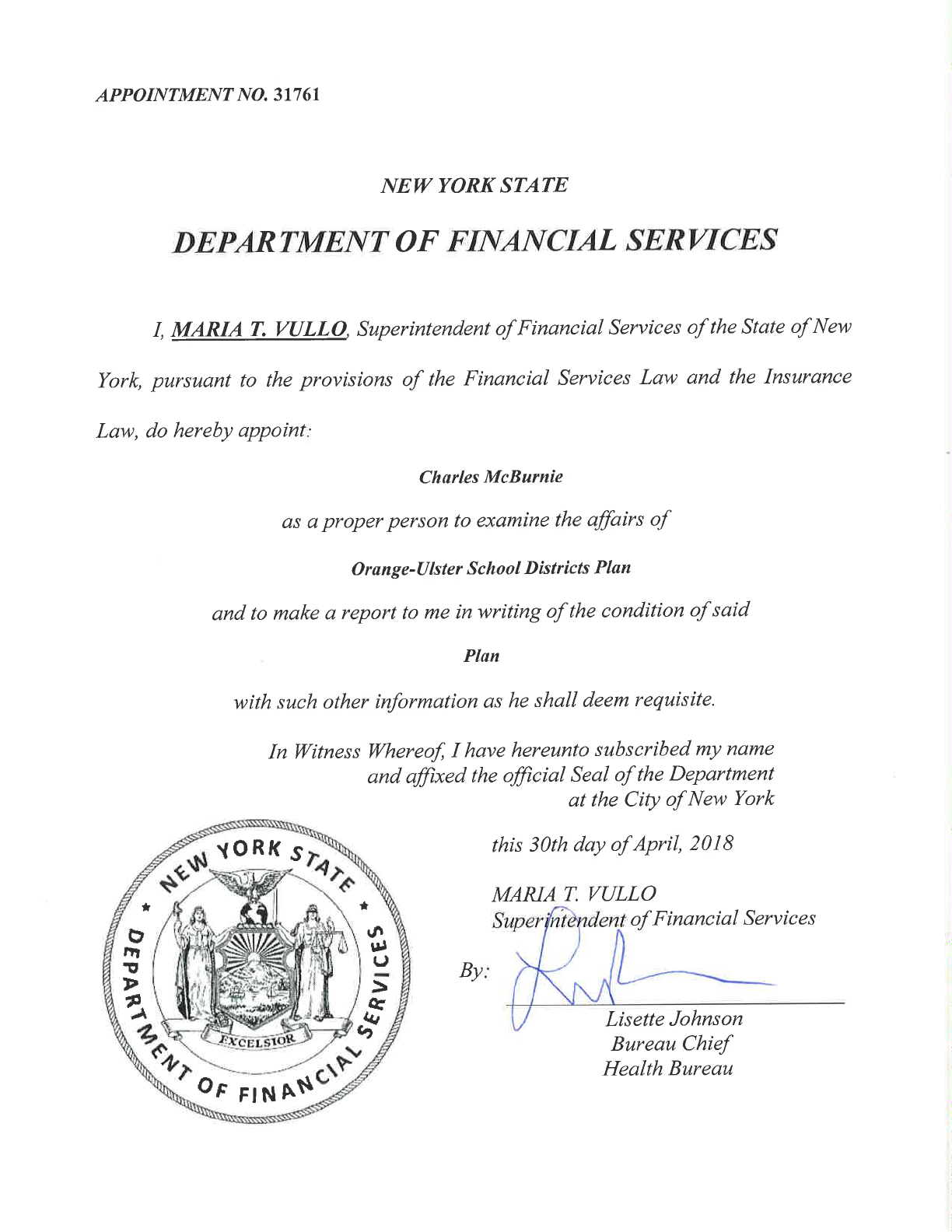

September 21, 2022

Honorable Adrienne A. Harris

Superintendent of Financial Services

Albany, New York 12257

Madam:

Pursuant to the requirements of the New York Insurance Law and acting in accordance

with the instructions contained in Appointment Number 31761, dated April 30, 2018, attached

hereto, I have made an examination into the condition and affairs of Orange-Ulster School Districts

Health Plan, a municipal cooperative health benefit plan certified pursuant to the provisions of

Article 47 of the New York Insurance Law, as of December 31, 2017, and respectfully submit the

following report thereon.

The examination was conducted at the administrative office of Orange-Ulster School

Districts Health Plan, located at 4 Harriman Drive, Goshen, New York.

Wherever the designations the “Plan” or “OUSDP” appear herein, without qualification,

they should be understood to indicate the Orange-Ulster School Districts Health Plan.

Wherever the designation the “Department” appears herein, without qualification, it should

be understood to indicate the New York State Department of Financial Services.

2

1. SCOPE OF THE EXAMINATION

The previous examination was conducted as of December 31, 2013. This examination of

the Plan was a combined (financial and market conduct) examination and covered the four-year

period from January 1, 2014, through December 31, 2017. The financial component of the

examination was conducted on a risk-focused basis as defined in the National Association of

Insurance Commissioners (“NAIC”) Financial Condition Examiners Handbook, 2018 Edition (the

“Handbook”). The examination was conducted observing the guidelines and procedures in the

Handbook. Where deemed appropriate by the examiner, transactions occurring subsequent to

December 31, 2017, were also reviewed.

The financial portion of the examination was conducted on a risk-focused basis in

accordance with the provisions of the Handbook, which provides guidance for the establishment

of an examination plan based on the examiner’s assessment of risk in the Plan’s operations and

utilized that evaluation in formulating the nature and extent of the examination. The examiner

planned and performed the examination to evaluate the Plan’s current financial condition, as well

as identify prospective risks that may threaten the future solvency of “OUSDP”

The examiner identified key processes, assessed the risks within those processes and

assessed the internal control systems and procedures used to mitigate those risks. The examination

also included an assessment of the principles used and significant estimates made by management,

an evaluation of the overall financial statement presentation, and determined management’s

compliance with the Department’s statutes and guidelines, Statutory Accounting Principles, as

adopted by the Department, and NAIC Annual Statement instructions and NAIC annual statement

instructions.

3

Information concerning the Plan’s organizational structure, business approach and control

environment were utilized to develop the examination approach. The examination evaluated the

Plan’s risks and management activities in accordance with the NAIC’s nine branded risk

categories.

These categories are as follows:

• Pricing / Underwriting

• Reserving

• Operational

• Strategic

• Credit

• Market

• Liquidity

• Legal

• Reputational

The examination also evaluated the Plan’s critical risk categories in accordance with the

NAIC’s ten critical risk categories. These categories are as follows:

Valuation / Impairment of Complex or Subjectively Valued Invested Assets

Liquidity Considerations

Appropriateness of Investment Portfolio and Strategy

Appropriateness / Adequacy of Reinsurance Program

Reinsurance Reporting and Collectability

Underwriting and Pricing Strategy / Quality

Reserve Data

Reserve Adequacy

Related Party / Holding Company Considerations

Capital Management

OUSDP was audited annually, for fiscal years 2014 through 2017, by the accounting firm

Urbach Hacker Young LLP, (“UHY - LLP”). The Plan received an unmodified opinion in each

of those years. Certain audit work papers of UHY - LLP. were reviewed and relied upon in

conjunction with this examination.

4

The examiner reviewed the corrective actions taken by the Plan with respect to the

recommendations contained in the prior report on examination. The results of the examiner’s

review are contained in Item No. 7 of this report.

This report on examination is confined to financial statements and comments on those

matters which involve departure from laws, regulations or rules, or which require explanation or

description.

2. DESCRIPTION OF THE PLAN

OUSDP is a municipal cooperative health benefits plan operating under the provisions of

Article 47 of the New York Insurance Law. The Plan operates exclusively for the benefit of the

employees, retirees and dependents of the Plan’s member school districts and the Orange-Ulster

Board of Cooperative Educational Services (“BOCES”). The Plan has been in existence since

1982 and is composed of eighteen (18) school districts and the Orange-Ulster BOCES. It was

issued a certificate of authority on November 1, 2000, pursuant to the provisions of Article 47 of

the New York Insurance Law. The Plan was issued a Certificate of Authority by the

Superintendent on November 1, 2000. Pursuant to such Certificate of Authority and in accordance

with the Municipal Cooperative Agreement, each of the participants of the Plan have agreed to

share the costs and assume the liabilities for medical, hospital, surgical, and prescription drug

benefits provided to covered employees (and retirees) and their dependents under the Plan.

For the examination period, there were eighteen (18) school districts and one (1) BOCES

participating in the Plan. As of December 31, 2017, the nineteen (19) municipalities participating

in the Plan were as follows:

5

• Chester Union Free School District

• Monroe-Woodbury Central School District

• Cornwall Center School District

• Orange–Ulster BOCES

• Eldred Central School District

• Pine Bush Central School District

• Florida Union Free School District

• Port Jervis City School District

• Goshen Central School District

• Rondout Valley Central School District

• Greenwood Lake Union Free School

District

• Tuxedo Union Free Central School District

• Highland Central School District

• Valley Central School District

• Highland Falls Central School District

• Warwick Valley School District

• Kiryas Joel Village School District

• Washingtonville School District

• Marlboro Central School District

A. Corporate Governance

Pursuant to its Municipal Cooperative Agreement, management of the Plan is to be vested

in a Governing Board, comprised of one (1) representative from each participating School District,

including the BOCES. The Plan’s Governing Board members, and their principal business

affiliations as of December 31, 2017, was as follows:

Name and Residence

Principal Affiliation

Erin Brennan

Rock Tavern, New York

Director of Business,

Chester Union Free School District

Patrick Cahill

Fishkill, New York

Assistant Superintendent for Management Services,

Monroe-Woodbury Central School District

Lorelei Case

Cuddebackville, New York

Assistant Superintendent for Business,

Port Jervis City School District

Denise Cedeira

Jeffersonville, New York

Assistant Superintendent for Business,

Highland Falls Central School District

Deborah McBride Heppes

Goshen, New York

Assistant Superintendent for Financials,

Orange-Ulster BOCES

Timothy Holmes

Uniondale, New York

Assistant Superintendent for Business,

Warwick Valley School District

Jan Jehring

Middletown, New York

Superintendent,

Florida Union Free School District

6

Name and Residence

Principal Affiliation

Ann Lierow

Lagrangeville, New York

Assistant Superintendent for Business,

Greenwood Lake Union Free School District

Ruth Luis

New Hampton, New York

Business Administrator,

Eldred Central School District

Louise Lynch

Salt Point, New York

Business Administrator,

Highland Central School District

Marc Matatia

Guilderland, New York

Business Administrator,

Tuxedo Union Free Central School District

Kim McEvoy

Accord, New York

Key Personnel,

Rondout Valley Central School District

Robert Miller

Johnson, New York

Assistant Superintendent for Business,

Goshen Central School District

Paul Nienstadt

Washingtonville, New York

Assistant Superintendent for Business,

Washingtonville School District

Michael Pacella

Newburgh, New York

Assistant Superintendent for Business,

Pine Bush Central School District

Lisa Raymond

Neversink, New York

Assistant Superintendent for Business,

Valley Central School District

Harvey Sotland

Poughquaq, New York

Assistant Superintendent for Business,

Cornwall Central School District

Schaye Wercberger

Central Valley, New York

Director of Business,

Kiryas Joel Village School District

Patrick Witherow

Middletown, New York

Business Administrator,

Marlboro Central School District

According to its Municipal Cooperative Agreement, the Board of Directors is to meet at

least once each quarter in the months of October, January, April and July. The time and the place

within New York State of such meetings shall be provided in a written notice to the Board members

provided by the Chairman, Secretary or their designee.

The minutes of all meetings of the Board of Directors were reviewed. Such meetings were

generally well attended.

7

Article IV of the Plan’s Municipal Cooperative Agreement states:

“The following officers of the Health Plan Committee shall be elected

annually at the November meeting and shall have the duties set forth

below:

(i) Chairperson: The chairperson shall have general supervisory

responsibilities for the Plan; and the Health Plan Committee such as

(1) develop the agenda, (2) preside over meetings; and. (3) appoint

sub-committees as required upon authorization from the full Board.

(ii) Secretary: The Secretary includes (1) keeping official minutes of all

Board meetings, send copies to all Board members, superintendents,

plan administrator and claims administrator, (2) send out notices of

all meetings, (3) conduct correspondence for the Board as directed

by Chairperson and (4) act as Chairperson in the absence of the

Chairperson.

(iii) Plan Administrator: The Administrator shall be (1) responsible for

custody of all Board minutes, correspondence and other official

records of the Plan except for claims information, (2) designate the

Plan’s attorney in fact to receive process of summons or other legal

process.

(iv) Chief Fiscal Officer: The Chief Fiscal Officer is appointed by the

Chairperson annually in November, who shall be a fiscal officer of a

participating school district.”

Review of the Board of Directors’ meeting minutes of the Health Plan Committee noted

that the Plan’s management failed to appoint the Chairman, Secretary, Plan Administrator and

Chief Fiscal Officer, as required by Article IV of the Plan’s Municipal Cooperative Agreement.

It is recommended that the Plan comply with Article IV of its Municipal Cooperative

Agreement, by electing the Chairman, Secretary, Plan Administrator and Chief Fiscal Officer, in

accordance with its Municipal Cooperative Agreement.

It was noted that although the Plan’s Board authorized and established specific committees,

such committees were not formalized within the Plan’s Municipal Cooperative Agreement or

other corporate documents.

It is recommended that the Plan revise its Municipal Cooperative Agreement or by-laws to

include any and all of its standing committees.

8

During the examination period, the Plan did not maintain any committee minutes for the

Plan. As a good business practice, the Plan should maintain minutes of the proceedings of its

committees.

It is also recommended that the Plan, as a best practice, and in conformance with Section

624(a) of the New York Business Corporation Law, keep meeting minutes of its established

committees.

The principal officers of the Plan as of December 31, 2017, were as follows:

Officers

Title

Deborah McBride Heppes

President

Lorelei Case

Chief Financial Officer

Lisa Raymond

Secretary

John Staiger

Interim Administrator

The Governing Board of the Plan designated John Staiger, Jr. as the Attorney-in-Fact, who

is authorized to receive service on a summons or other legal paper in any action, suit or proceeding

arising out of any contract, agreement or transaction involving the Plan.

B. Territory and Plan of Operation

As of December 31, 2017, the Plan held a Certificate of Authority to operate the business

of a municipal cooperative health benefit plan as authorized by Section 4704 of the New York

Insurance Law in the counties of Orange, Sullivan and Ulster. Pursuant to the requirements of

Article 47 of the New York Insurance Law, the Plan is required to maintain contingency reserves

equal to 5% of the annualized earned premium. The Plan met the contingency reserves

requirement throughout the examination period.

9

It was noted that the Plan’s official name on its Certificate of Authority, is the Orange

Ulster School Districts Plan, however, the Plan at times refers to itself as the Orange Ulster School

Districts Health Plan, in their filings and correspondence.

It is recommended that if the Plan continues to refer to itself as Orange Ulster School

Districts Health Plan that it, officially submit to the Department a request to change its name on

its Certificate of Authority to reflect the name it uses.

The Plan provides medical, hospital, surgical, prescription and drug benefits to eligible

members and retirees of the participating school districts in Orange, Ulster and Sullivan counties.

The Plan reported annual written premiums of $148,976,223 for the fiscal year ending December

31, 2017. The Plan’s total lives covered as of December 31, 2017, was 19,274, a decrease of 2,234

from prior year December 31, 2016.

A review of the meetings minutes of the Plan noted that the Minisink Valley Central School

and the Enlarged City School District, withdrew from the Plan, effective August 31, 2016, and

September 30, 2017, respectively.

Below is a summary of the Plan’s annual premium writings and corresponding member

enrollment for the four-year examination period:

Calendar Year

Net Premium Income

Enrollment*

2014

$129,549,701

9,923

2015

$138,370,916

10,316

2016

$144,331,545

9,766

2017

$148,976,223

8,764

*Enrollment for covered employees and retirees

10

The Plan’s total written premium increased to a total of $27,567,802 ($148,976,223-

$121,408,421) or 22.7% for the examination period. Such increases were attributable to annual

rate increases during the examination period for the examination period. Conversely, the Plan’s

member enrollment decreased by a total of 998 members or 10.2% from 2013 (9,762) through

2017 (8,764) due to withdrawal of two school districts, consolidations of some employment

positions within the Plan’s participating school districts and attrition.

C. Stop-Loss Coverage

As required by Section 4707 of the New York Insurance Law, the Plan maintains both

aggregate stop-loss coverage and specific stop-loss coverage. The issuer of the stop-loss coverage,

American Alternative Insurance Corporation, is a New York authorized reinsurer.

The following is a summary of the Plan’s stop-loss coverage program as of December 31,

2017:

Type Limits

Excess of loss (one layer) 100% of excess of $950,000 per member, per

contract year.

Aggregate excess-of loss $1,000,000 excess of the annual aggregate

attachment point (100% of incurred claims

expenses), for the current contract period.

As of January 1, 2018, the Plan replaced its stop loss coverage with America Alternative

Insurance Corporation with stop-loss coverage from United States Fire Insurance Company, which

is also a New York authorized reinsurer in New York State.

11

D. Administrative Services Agreements

The Plan entered into contractual agreements with the following vendors for various

services, for the examination period:

Envision Pharmaceutical Services, Inc.

• Preparation and distribution of identification cards;

• Maintenance of appropriate records of each Plan participant;

• Preparation and distribution of enrollment forms and benefit claim forms; and

• Notification to the Plan’s claimant of denials, the basis for the denials and the claimant’s

right to appeal the denials

Quantum Health Solutions, Inc.

• Evaluate data on specific provider patterns;

• Maintain a cohesive provider panel with ongoing orientations to the program Billing

procedures;

• Contract preferred rates with outpatient and impatient providers in the company region;

• Orient Providers on the Orange-Ulster Contract;

• Data reports; and

• Coordinate with Plan’s third-party administrator and medical network agreements

Empire HealthChoice Assurance, Inc. d/b/a, Empire BlueCross BlueShield

• Pharmacy benefits administrative services;

• Rebate and reporting services to Medicare D plans; and

• Pharmacy network contracting, claims processing services for covered drugs, perform

standard concurrent utilization review analysis and formulary management services;

• First level review of written requests for appeal from members or participating pharmacies

that consist of ministerial verification that claim(s) were processed in accordance with the

Plan’s benefits package member eligibility

HealthCare Strategies, (“HCS”)

• Utilization Review, and case management;

• Outpatient Services Review; and

• Medical Information Help Line

12

Segal Consulting

• Provides annual actuarial certification of compliance regarding the Plan’s premium rating

and claims reserve process and stop-loss requirement as required by Article 47 of the New

York State Insurance Law

Harris Beach PLLC

• Provides outside General Counsel Services to the Plan

Urbach Hacker Young LLP.

• Serves as the Plan’s Certified Public Accountant (“CPA”). Provides financial audit

services

The agreements between the Plan and Empire BlueCross BlueShield did not include a

provision for the Plan to audit or have a third-party audit Empire BlueCross BlueShield’s

compliance with its obligations under the contract.

It is recommended that the Plan initiate audits of all services, including claims processing,

provided by all its contracted third-party administrators.

It is further recommended that if the Plan is unable to have audits done of its third-party

claims administrators that the Plan obtain annual certifications from its third-party claims

administrators that claims are being processed in accordance with the Plan’s Document and

applicable statutes, rules and regulations (relative to claims submitted by the Plan’s participants).

E. Municipal Cooperative Agreement

Section 4710(a)(1) of the New York Insurance Law states:

“The governing board of the municipal cooperative health benefit plan shall:

13

(1) file for approval with the superintendent a description of material changes in any

information provided in the application for a certificate of authority in the form and

manner proscribed by the superintendent.”

During the review of the Plan’s Municipal Cooperation Agreement, it was determined that

the Plan used an MCA, dated 2012, which was never approved by the Superintendent.

It is recommended that the Plan submit its Municipal Cooperation Agreement to the

Superintendent for approval prior to use.

During the examination period, the Plan amended its 2012 Municipal Cooperative

Agreement (“MCA”) without filing for approval with the Superintendent. It should be noted the

Plan is obligated to comply with the most recently approved version of its MCA until the

Department approves an amended version.

It is recommended that the Plan comply with Section 4710(a)(1) of the New York

Insurance Law by filing for approval with the Superintendent, a description of the material changes

in any information provided in the application for its Certificate of Authority.

Section 4705 (a)(7) of the New York Insurance Law states:

“The municipal cooperation agreement, under which the municipal

cooperative health benefit plan is established and maintained, and any

amendment thereto, shall be approved by each participating municipal

corporation by majority vote of each such corporation's governing body,

and shall:

(7) designate the plan's attorney-in-fact to receive service of summons or

other legal process in any action, suit or proceeding arising out of any

contract, agreement or transaction involving such municipal cooperative

health benefit plan; and”

14

During the examination, the Plan was unable to provide any evidence that the Municipal

Cooperation Agreement was approved by each participating municipal corporation by majority

vote of each such corporation body.

It is recommended that the Plan adhere to Section 4705(a) of the New York Insurance Law,

by having the Municipal Cooperation Agreement approved by each participating municipal

corporation by a majority vote of each such corporation’s governing’s body.

The last approved Municipal Cooperation Agreement the Plan had in effect was dated as

of 1999. A review of the agreement found the following deficiencies:

The Plan’s MCA failed to designate the Plan’s attorney-in-fact to receive service of

summons or other legal processes in any action, suit or proceeding arising out of any contract,

agreement or transaction involving such municipal cooperative health benefit plan.

It is recommended that the Plan adhere to Section 4705(a)(7) and designate the Plan’s

attorney-in-fact to receive summons or other legal process in any action, suit or proceeding arising

out of any contract, agreement or transaction involving such municipal cooperative health benefit

plan.

Section 4705(b)(2) of the New York Insurance Law states, in part:

“(b) The municipal cooperation agreement shall provide that the plans

chief fiscal officer…

(2) shall, notwithstanding any provision of the general municipal law make

payment in accordance with procedures developed by the plan's governing

board and acceptable to the superintendent…”

15

The Plan’s MCA failed to state that the Chief Financial Officer (“CFO”) shall,

notwithstanding any provision of the General Municipal Law make payment in accordance with

procedures developed by the Plan’s governing Board and acceptable to the Superintendent.

It is recommended that the Plan comply with the provisions of Section 4705(b)(2) of the

New York Insurance Law, by including in its MCA that the CFO shall, notwithstanding any

provision of the General Municipal Law, make payment in accordance with procedures developed

by the Plan’s governing Board and which are acceptable to the Superintendent.

Section 4705(b)(4) of the New York Insurance Law states, in part:

“(b) The municipal cooperation agreement shall provide that the plans

chief fiscal officer…

(4) shall receive no remuneration, except that the participating municipal

corporation employing the chief fiscal officer may be reimbursed for

reasonable expenses incurred in connection with the duties of such fiscal

officer in connection with the plan…”

The Plan’s MCA failed to state the Plan’s CFO, shall receive no remuneration, except that

the participating municipal corporation employing the chief fiscal officer may be reimbursed for

reasonable expenses incurred regarding the duties of such fiscal officer relating to the Plan.

It is recommended that the Plan comply with Section 4705(b)(4) of the New Insurance

Law, by including in its MCA that the CFO, shall receive no remuneration, except that the

participating municipal corporation employing the chief fiscal officer may be reimbursed for

reasonable expenses incurred relating to the duties of such fiscal officer regarding the Plan.

16

Section 4705(d)(2)(D) of the New York Insurance Law states:

“The municipal cooperation agreement shall provide that the governing

board:

(2) may enter into an agreement with a contract administrator or other

service provider, determined by the governing board to be qualified, to

receive, investigate, recommend, audit, approve or make payment of

claims under the municipal cooperative health benefit plan, provided

that…

(D) all such agreements shall comply with the requirements of subdivision

six of section ninety-two-a of the general municipal law.”

The Plan’s MCA failed to include a statement that any agreements entered into with a

contract administrator or other service provider “…shall comply with the requirements of

subdivision six of section ninety-two-a of the general municipal law.

It is recommended that the Plan include in its MCA a provision that all agreements entered

into with a contract administrator or other service provider shall comply with the requirements of

subdivision six of Section ninety-two-a of the general municipal law.

Section 4705(f) of the New York Insurance Law states:

“The municipal cooperation agreement shall specify the rights and

obligations of a municipal corporation withdrawing from a municipal

cooperative health benefit plan to any contribution (or premium

equivalent) refund or reserve fund or for any contingent assessment

liability or other obligation.”

The Plan’s MCA did not specify the rights and obligations of a municipal corporation

withdrawing from a municipal cooperative health benefit plan to any contribution (or premium

equivalent) refund or reserve fund or for any contingent assessment liability or other obligation.

It is recommended that the Plan comply with Section 4705(f) of the New York Insurance

Law and specify the rights and obligations of a municipal cooperation withdrawing from the

17

municipal cooperation health benefit plan to any contribution (or premium equivalent) refund or

reserve fund or for any contingent assessment liability or other obligation.

Section 4705(g) of the New York Insurance Law states:

“(g) Every municipal cooperation agreement shall contain a provision

stating that nothing contained in such agreement shall be construed to

waive any right a covered person possesses with respect to the

confidentiality of medical records and that such right may only be waived

upon the written consent of such covered person.”

The Plan’s MCA did not contain a provision stating that “nothing contained in such

agreement shall be construed to waive any right a covered person possesses with respect to the

confidentiality of medical records and that such right may only be waived upon the written consent

of such covered person”, in accordance with Section 4705(g) of the New York Insurance Law.

It is recommended that the Plan comply with Section 4705(g) of the New York Insurance

Law and incorporate the language in its MCA that nothing contained in such agreement shall be

construed to waive any right a covered person possesses with respect to the confidentiality of

medical records and that such right may only be waived upon the written consent of such covered

person.

F. Plan Document and Summary Description

Section 3217-a(a)(18) of the New York Insurance Law states, in part:

“(a) Each insurer subject to this article shall supply each insured, and upon

request each prospective insured prior to enrollment, written disclosure

information, which may be incorporated into the insurance contract or

certificate, containing at least the information set forth below. In the event

of any inconsistency between any separate written disclosure statement

and the insurance contract or certificate, the terms of the insurance contract

or certificate shall be controlling. The information to be disclosed shall

include at least the following…

18

(18) a description of the method by which an insured may submit a

claim for health care services”

FA review of the Plan Document and Summary Description (2006), found that it failed to

include a description of the method by which an insured may submit a claim for health care

services.

It is recommended that the Plan discloses the method by which an insured may submit

claims for health care services in accordance with Section 3217-a(a)(18) of the New York

Insurance Law.

Section 3224-a (j) of the New York Insurance Law states in part:

“(j) An insurer or an organization or corporation licensed or certified

pursuant to article forty-three or forty-seven of this chapter or article forty-

four of the public health law or a student health plan established or

maintained pursuant to section one thousand one hundred twenty-four of

this chapter shall accept claims submitted by a policyholder or covered

person, in writing, including through the internet, by electronic mail or by

facsimile.”

A review of the Plan’s Summary Plan Document determined that said Document did not

contain the provision that a policyholder or covered person may submit claims via internet,

electronic mail, paper, or facsimile, in accordance with Section 3224-a(j) of the New York

Insurance Law.

It is recommended that the Plan, amend its Summary Plan Document, to reflect that a

policyholder or covered person may submit claims via internet, electronic mail, paper, or facsimile,

in accordance with Section 3224-a(j) of the New York Insurance Law.

19

Section 4709(c) of the New York Insurance Law states:

“(c) Conspicuously printed on the first page of the plan document and

summary plan description, in at least ten point bold-face type, shall be the

following statement:

This municipal cooperative health benefit plan is not a licensed insurer. It

operates under a more limited certificate of authority granted by the

superintendent of financial services. Municipal corporations participating

in the municipal cooperative health benefit plan are subject to contingent

assessment liability.”

A review of the Plan Document and Summary Description (2006), determined that the Plan

failed to include the statement “This municipal cooperative health benefit plan is not a licensed

insurer. It operates under a more limited certificate of authority granted by the superintendent of

financial services. Municipal corporations participating in the municipal cooperative health

benefit plan are subject to contingent assessment liability.”

It is recommended that the Plan comply with Section 4709(c) of the New York Insurance

Law by including the above statement.

G. Underwriting Results

The underwriting results presented below are on an earned-incurred basis and encompass

the four-year period covered by this examination:

Amounts

Ratios

Claims

$567,554,917

97.89%

General administrative expenses

45,660,709

7.87%

Net underwriting (loss)

(33,422,353)

(5.76%)

Premium

$579,793,273

100%

20

H. Internal Controls

The Plan relies on third-party administrators to process and pay claims to providers. A

review of the Plan’s oversight of its third-party administrators found the following deficiencies:

1. The Plan does not have an internal control function nor an Internal Audit Department.

As a result, the Plan is unable to exercise proper oversight of the third-party

administrators it uses to process and pay claims

2. The third-party service providers used by the Plan do not adequately review the

eligibility of Out-of-Network providers for payments. This could result in payments to

ineligible providers.

It is recommended that as a best business practice the Plan exercise greater oversight of its

third-party administrators.

It is also recommended as a best business practice the Plan ensures that Out-of-Network

providers are eligible to receive payments.

3. FINANCIAL STATEMENTS

The following statements show the assets, liabilities and surplus as of December 31, 2017,

as contained in the Plan’s 2017 filed annual statement, a condensed summary of operations, and a

reconciliation of the surplus account for each of the years under examination. The examiner’s

review of a sample of transactions did not reveal any differences which materially affected the

Plan’s financial condition as presented in its December 31, 2017, financial statements.

The firm of Urbach Hacker Young LLP. was retained by the Plan to audit the Plan’s

combined statutory-basis statements of financial position as of December 31

st

, of each year in the

21

examination period, and the related statutory-basis statements of operations, surplus, and cash

flows for the year then ended.

Urbach Hacker Young LLP. concluded that the statutory financial statements presented

fairly, in all material respects, the financial position of the Plan at the respective audit dates.

Balances reported in these audited financial statements were reconciled to the corresponding year’s

annual statements with no discrepancies noted.

22

A. Balance Sheet

Assets

Bonds

$30,210,906

Cash and cash equivalents

25,202,087

Investment income due and accrued

131,716

Health care and other amounts

2,173,188

Aggregate write-in: Restricted Deposit

380,000

Total assets

$58,097,897

Liabilities

Unpaid claims

$16,570,000

Reserve and surplus requirement (per NYIL §4706(a)(1))

6,836,563

Premiums received in advance

12,441,931

Accounts payable

3,844,545

Total liabilities

$39,693,039

Surplus

Unassigned funds (surplus)

10,956,047

Surplus (per NYIL §4706(a)(5))

7,448,811

Total surplus

$18,404,858

Total liabilities and surplus $58,097,897

23

B. Statement of Revenue and Expenses and Surplus

Surplus decreased by $4,493,626 during the four-year examination period, January 1, 2014,

through December 31, 2017, detailed as follows:

Revenue

Premiums

$561,273,385

Non- health revenues

2,338,521

Aggregate write-ins for other revenue

16,181,367

Total revenue $579,793,273

Expenses

Hospital and medical claims

$411,548,052

Prescription drugs

156,426,326

Net reinsurance recoveries

(459,461)

Compensation

1,085,796

Professional fees

265,330

Aggregate write-ins

44,309,583

Total expenses

613,175,626

Net loss

$ (33,382,353)

24

Surplus, per report on examination, as of

December 31, 2013

$22,898,484

Gain in

Surplus

Loss in

Surplus

Net loss

$33,382,353

Change in surplus per NYIL §4706(a)(5)

2,929,008

Aggregate write-ins for changes in other

net worth items

$31,817,735

0

Net decrease in surplus $ 4,493,626

Surplus, per report on examination,

as of December 31, 2017

$18,404,858

4. CLAIMS PAYABLE

The examinations total claims payable of $24,243,405 using the approved percentages and

expected incurred claims and expenses as of December 31, 2017 is $836,842 or 3.58% more than

the $23,406,563 reported by the Plan in its filed annual statement as of December 31, 2017. The

Plan failed to comply with Section 4706(a)(1) of the New York State Insurance Law.

Section 4706(a)(1) of the New York Insurance Law requires that the Governing Board of

a municipal cooperative health benefit plan establish a reserve fund, including a reserve for the

payment of claims and expenses thereon reported but not yet paid, and claims and expenses thereon

incurred but not yet reported, which shall not be less than an amount equal to twenty-five percent

(25%) of expected incurred claims and expenses thereon for the current plan year, unless a

qualified actuary has demonstrated to the superintendent’s satisfaction that a lesser amount will be

adequate. The Plan was granted approval by this Department on June 15, 2005 to reduce its

reserves for claims and related expenses to 17% from 25% of the current year’s expected incurred

25

claims and expenses. The Plan was granted additional approval by the Department on November

29, 2017 to reduce its reserves for prescription drug reserves and related expenses to 12% from

17% for the Plan’s prescription drug reserve factor for year ending December 31, 2017.

The examination analysis of the captioned account was conducted in accordance with

generally accepted actuarial principles and practices and was based on statistical information

contained in the Plan's internal records and in its filed annual and quarterly statements, as well as

additional information provided by the Plan.

The examination reserve was based upon actual payments made through a point in time,

plus an estimate for claims remaining unpaid at that date. Such estimate was calculated based on

actuarial principles which utilized the Plan’s experience in projecting the ultimate cost of claims

incurred on or prior to December 31, 2017.

It is recommended that the Plan’s claim payable reserve comply with the requirements of

Section 4706(a)(1) of the New York Insurance Law.

5. CLAIMS STABILIZATION RESERVE

As of December 31, 2017, the Plan did not maintain a claim stabilization reserve. This

Plan has total reserves and surplus of about $41.8 million which is about 135.5% of the sum (about

$30.9 million) of the claims reserve (about $23.4 million) and surplus (at $7.4 million).

Claim Stabilization Reserve and stop-loss insurance are mechanisms for maintaining

solvency and stability of the Plan. The required minimum reserves and surplus for waiving the

requirement for stop-loss insurance is assumed to be an indicator for providing a Claim

26

Stabilization Reserve. The assumption is that if total reserves and surplus is less than 150% of the

sum of the claims reserve and surplus, then the Plan should gradually accumulate a Claim

Stabilization Reserve.

The Claim Stabilization Reserve of $0 was reasonable but it is recommended that Orange-

Ulster should gradually accumulate a Claim Stabilization Reserve and concurrently maintain

overall financial solvency.

6. MARKET CONDUCT ACTIVITIES

In the course of this examination, a review was made of the manner of which the Plan

conducts its business practices and fulfills its contractual obligations to subscribers and claimants.

The review was general in nature and is not to be construed to encompass the more precise scope

of a market conduct examination.

The review was directed at the practices of the Plan in the following areas:

A . Prompt Pay Law

B. Mental Health Parity and Addiction Equity Act (“MHPAEA”)

A. Standards for Prompt, Fair and Equitable Settlement of Claims for Health Care and

Payments for Health Care Services (“Prompt Pay Law”)

The examination included a review of the Plan’s claims settlement practice and oversight

of the claims adjudication process. INDECS is the Plan’s Third-Party Administrator of claims.

As such, INDECS is responsible for some aspects of claims settlement, including out-of-network

claim payments, issuance of explanation of benefits statements (“EOB”), and appeals. However,

management of Orange-Ulster School District Plan retains the ultimate responsibility for

27

compliance with applicable provisions of the New York Insurance Law and related Regulations,

and therefore its management must be diligent in its oversight of the claims settlement and related

functions.

Section 3224-a of the New York Insurance Law, “Standards for prompt, fair and equitable

settlement of claims for health care and payments for health care services” (“Prompt Pay Law”),

requires all insurers to pay undisputed claims within thirty (30) days of receipt of a claim that is

transmitted via the internet or electronic mail or forty-five (45) days of receipt of a claim submitted

by other means such as paper or facsimile. If such undisputed claims are not paid within the

respective thirty (30) or forty-five (45) days of receipt, interest may be payable.

A review of the Plan’s submitted medical and hospital claims data for the period January

1, 2017, through December 31, 2017, relative to compliance with Section 3224-a of the New York

Insurance Law did not reveal any problem areas.

B. Mental Health Parity and Addiction Equity Act (“MHPAEA”)

Sections (a)(1)(v)(2), (c)(1) and (e)(1)(i) of 45 CFR 146.180 - Treatment of non-Federal

governmental plans states the following:

“(a) Opt-out election for self-funded non-Federal governmental plans

(1) Requirements subject to exemption. The PHS Act requirements

described in this paragraph are the following…

(v) Parity in mental health and substance use disorder benefits under

section 2726 of the PHS Act…

(2) General rule. For plan years beginning on or after September 23, 2010,

a sponsor of a non-Federal governmental plan may elect to exempt its plan,

to the extent the plan is not provided through health insurance coverage

(that is, it is self-funded), from one or more of the requirements described

in paragraphs (a)(1)(iv) through (vii) of this section…

(c) Filing a timely election

28

(1) Plan not governed by collective bargaining. Subject to paragraph

(c)(4) of this section, if a plan is not governed by a collective bargaining

agreement, a plan sponsor or entity acting on behalf of a plan sponsor must

file an election with CMS before the first day of the plan year…

(e) Notice to enrollees

(1) Mandatory notification.

(i) A plan that makes the election described in this section must notify each

affected enrollee of the election and explain the consequences of the

election. For purposes of paragraph (e) of this section, if the dependent(s)

of a participant reside(s) with the participant, a plan need only provide

notice to the participant.”

The Plan failed to comply with Sections 146.180(a)(1)(v)(2), (c)(1) and (e)(1)(i) of 45 CFR

146 - Treatment of non-Federal governmental plans by failing to file the required exemption notice

with the Center for Medicare and Medicaid Services (“CMS”).

Additionally, the Plan failed to provide notice to its enrollees that it elected not to comply

with the requirements of the Mental Health and Substance Abuse Parity Act for the years 2015,

2016, 2017 and 2018.

It is recommended that the Plan comply with Sections 146.180(a)(1)(v)(2), (c)(1) and

(e)(1)(i) of 45 CFR 146.180 - Treatment of non-Federal governmental plans by filing the required

exemption notice with the Center for Medicare and Medicaid Services (“CMS”).

It is also recommended that the Plan comply with Sections 146.180(a)(1)(v)(2), (c)(1) and

(e)(1)(i) of 45 CFR 146.180 and provide notice to its enrollees that it has elected not to comply

with the requirements of the Mental Health and Substance Abuse Parity Act.

29

7. COMPLIANCE WITH PRIOR REPORT ON EXAMINATION

The prior report on examination included eleven (11) recommendations detailed as follows

(page number refers to the prior report on examination):

ITEM NO.

PAGE NO.

Management and Controls

1.

The Department recommends that directors who are unable

or unwilling to attend board meetings consistently should

resign or be replaced. Furthermore, in selecting prospective

members of the board, a key criterion should be their

willingness and commitment

to attend meetings and

participate in the board’s responsibility to oversee the

operations of the Plan.

The Plan has complied with this recommendation.

9

Report on Examination

2.

The Department recommends that the Plan comply with

Section 312(b) of the New York Insurance Law and obtain

signed statements by each board member confirming that

such member has received and read the report on

examination.

The Plan has complied with this recommendation.

10

Stop Loss Coverage

3.

The Department recommends that the Plan obtain and

maintain aggregate stop-

loss coverage in compliance with

Section 4707(a)(1) of the New York Insurance Law.

A similar finding was cited in the prior report on

examination.

The Plan did comply with this recommendation.

12

30

ITEM NO.

PAGE NO.

Municipal Cooperation Agreement

4.

The Department recommends that the Plan comply with

Section 4710(a)(1) of the New York Insurance Law by filing

for approval with the Superintendent, a description of the

material changes in any information provided in the

application for Certificate of Authority.

The Plan has not complied with this recommendation.

13

.

Plan Document

5.

It is recommended that the Plan revise its Plan Document to

comply with the Affordable Care Act and submit such

document to the Superintendent for approval.

The Plan has complied with this recommendation.

18

Claim Processing

6.

The Department recommends that the Plan require INDECS

to implement or undergo periodic audits within a proactive

quality assurance program in order to identify and correct

errors that may be occurring on an ongoing basis, in addition

to retroactive reviews. The results of such audits should be

reported to the Plan’s management, at least annually. A

similar finding was cited in the prior report on examination.

The Plan has complied with this recommendation.

21

Rating

7.

The Department recommends that the Plan comply

completely with Section 4705(e)(3) of the New York

Insurance Law by obtaining an annual independent actuarial

opinion on the soundness of the Plan’s premium equivalent

rates. A similar finding was cited in the pr

ior report on

examination.

The Plan has complied with this recommendation.

21

31

ITEM NO.

PAGE NO.

Utilization Review

8.

The Department recommends that the Plan not require

members to utilize a Local School District Representative as

ombudsman during the appeal of claims. A similar finding

was cited in the prior report on examination.

The Plan has not complied with this recommendation.

22

9.

The Department recommends that the Plan ensure that the

appeal instructions issued

to its members are orderly,

complete, and consistent, stating specifically that the Level

One appeal is also the Final Adverse Determination. A

similar finding was cited in the prior report on examination.

The Plan has complied with this recommendation

23

10.

The Department recommends that the Plan’s Denial letters

accurately and completely reflect the member’s right of

appeal, in accordance with the requirements of Article 49 of

the Insurance Law. A similar finding was cited in the prior

report on examination.

The Plan has complied with this recommendation.

24

Explanation of Benefit Statements

11.

The Department recommends that the Plan comply with

Section 3234(b)(7) of the New York Insurance Law by

ensuring that its Explanation of Benefits statements

accurately and clearly explain member appeal rights. A

similar finding was cited in the prior report on examination.

The Plan has complied with this recommendation.

24

32

8. SUMMARY OF COMMENTS AND RECOMMENDATIONS

ITEM

PAGE NO.

A.

Corporate Governance

i.

It is recommended that the Plan comply with Article IV of its

Municipal Cooperative

Agreement, by electing the Chairman,

Secretary, Plan Administrator and Chief Fiscal Officer, in

accordance with its Municipal Cooperative Agreement.

7

ii.

It is recommended that the Plan revise its Municipal Cooperative

Agreement or by-laws to include

any and all of its standing

committees.

7

iii.

It is also recommended that the Plan, as a best practice, and in

conformance with Section 624(a) of the New York Business

Corporation Law, keep meeting minutes of its established

committees.

8

B.

Territory and Plan of Operation

It is recommended that if the Plan continues to refer to itself as

Orange Ulster School Districts Health Plan that it, officially

submit to the Department a request to change its name on its

Certificate of Authority to reflect the name it uses.

9

C.

Administrative Services Agreements

It is recommended that the Plan initiate audits of all services

including claims processing provided by all of

its contracted

third-party administrators.

12

It is further recommended that if the Plan is unable to have audits

done of its third-party claims administrators that the Plan obtain

annual certifications from its third-party claims administrators

that claims are being processed in accordance with the Plan’s

Document and applicable statutes, rules and regulations (relative

to claims submitted by the Plan’s participants).

12

D.

Municipal Cooperative Agreement

i.

It is recommended that the Plan submit its Municipal

Cooperation Agreement to the Superintend for approval prior to

use.

13

33

ITEM

PAGE NO.

D.

Municipal Cooperative Agreement (cont’d)

ii.

It is recommended that the Plan comply with Section 4710(a)(1)

of the New York Insurance Law by filing for approval with the

Superintendent, a description of the

material changes in any

information provided in the application for its Certificate of

Authority.

13

iii.

It is recommended that the Plan adhere to Section 4705(a) of the

New York Insurance Law, by having the Municipal Cooperation

Agreement approved b

y each participating municipal

corporation by a majority vote of each such corporation

governing’s body.

14

iv.

It is recommended that the Plan adhere to Section 4705(a)(7) and

designate the Plan’s attorney-in-fact to receive summons or other

legal process in any action, suit or proceeding arising out of any

contract, agreement or transaction involving such municipal

cooperative health benefit plan.

14

v.

It is recommended that the Plan comply with the provisions of

Section 4705(b)(2) of the New York Insurance Law, by including

in its MCA that the CFO shall, notwithstanding any provision of

the General Municipal Law, make payment in accordance with

procedures developed by the Plan’s governing Board and which

are acceptable to the Superintendent.

15

vi.

is recommended that the Plan comply with Section 4705(b)(4) of

the New Insurance Law, by including in its MCA that the CFO,

shall receive no remuneration, except that the participating

municipal corporation employing the chief fiscal officer may be

reimbursed for reasonable expenses incurred relating to the

duties of such fiscal officer regarding the Plan.

15

vii.

It is recommended that the Plan include in its MCA a provision

that all agreements entered into with a contract administrator or

other service provider shall comply with the requirements of

subdivision six of Section ninety-two-a of the general municipal

law.

16

34

ITEM

PAGE NO.

D.

Municipal Cooperative Agreement (cont’d)

viii.

It is recommended that the Plan comply with Section 4705(f) of

the New York I

nsurance Law and specify the rights and

obligations of a municipal cooperation withdrawing from the

municipal cooperation health benefit plan to any contribution (or

premium equivalent) refund or reserve fund or for any contingent

assessment liability or other obligation.

16

ix.

It is recommended that the Plan comply with Section 4705(g) of

the New York Insurance Law and incorporate the language in its

MCA that nothing contained in such agreement shall be

construed to waive any right a covered person possesses with

respect to the confidentiality of medical records and that such

right may only be waived upon the written consent of such

covered person.

17

E.

Plan Document & Summary Description

i.

It is recommended that the Plan disclose the method by which an

insured may submit claims for health care services in accordance

with Section 3217-a(a)(18) of the New York Insurance Law.

18

ii.

It is recommended that the Plan, amend its Summary Plan

Document, to reflect that a policyholder or covered person may

submit claims via internet, electronic mail, paper or facsimile, in

accordance with Section 3224-a(j) of the New York Insurance

Law.

18

iii.

It is recommended that the Plan comply with Section 4709(c) of

the New York Insurance Law by including the above statement.

19

F.

Internal Controls

i.

It is recommended that as a best business practice the Plan

exercise greater oversight of its third-party claim processors.

20

ii.

It is also recommended as a best business practice the Plan

ensures that Out-of-

Network providers are eligible to receive

payments.

20

35

ITEM

PAGE NO.

G.

Claims Payable

It is recommended that the Plan’s claim payable reserve comply

with the requirements of Section 4706(a)(1) of the New York

Insurance Law.

25

H.

Claim Stabilization Reserve

The Claim Stabilization Reserve of $0 is reasonable but it is

recommended that Orange-Ulster should gradually accumulate a

Claim Stabilization Reserve and concurrently maintain overall

financial solvency.

26

I.

Mental Health Parity and Addiction Equity Act (“MHPAEA”)

i.

It is recommended that the Plan comply with Sections

146.180(a)(1)(v)(2), (c)(1) and (e)(1)(i) of 45 CFR 146.180 -

Treatment of non-Federal governmental plans

by filing the

required exemption notice with the Center for Medica

re and

Medicaid Services (“CMS”).

28

ii.

It is also recommended that the Plan comply with Sections

146.180(a)(1)(v)(2), (c)(1) and (e)(1)(i) of 45 CFR 146.180 and

provide notice to its enrollees that it has elected not to comply

with the requirements of the Mental Health and Substance Abuse

Parity Act.

28

STATE OF NEW YORK )

) SS.

)

COUNTY OF NEW YORK )

Alice McKenney, being duly sworn, deposes and says that the foregoing submitted report is true

to the best of his knowledge and belief.

_____________________________

Wai Wong, CFE