INSTRUCTIONS

Individual Taxpayer Annual Local Earned Income Tax Return

Tax Year 2013

FILING:

YATB offers two methods of filing your Local Earned Income Tax Return. Taxpayers are encouraged to complete and file

their returns online through the Pennsylvania Local Income Tax Exchange (PALite) or by mail using the Individual

Taxpayer Annual Local Earned Income Tax Return form (Form 32-1). Please consider filing online. The benefits of

electronically filing your return through PALite (

www.palite.org):

• Safety: Stringent security safeguards are utilized to protect your information.

• Assistance: The system performs math calculations for you and prepares your return.

• Time: YATB is able to process returns in a fraction of the time compared to manually filed paper returns.

• Confirmation: Upon submitting your return with PALite, you will receive confirmation that your return has been

electronically transmitted and received.

Eligibility and exclusion provisions, including complete instructions and conditions, can be found on the PALite individual

online filing webpage (

www.palite.org) which may also be accessed through YATB’s website at www.yatb.com.

Reminder: When filing electronically through PALite, do not mail a copy of your return to YATB - retain it for your

records.

York County taxpayers who reside in the West Shore School District (including the municipalities of Fairview Township,

Newberry Township and Goldsboro Borough) must file with the Cumberland County Tax Bureau,

www.cumberlandtax.org, phone 717-590-7997.

REMITTANCE ADDRESSES:

Please use the enclosed labels to remit your tax return.

FILING DUE DATE:

Your return must be completed and filed on or before April 15

(unless the 15

th

falls on a Saturday, Sunday or Federal

Holiday…then it must be filed the following business day). The Postal Service postmark date on your envelope is to

serve as proof of your filing date. If you cannot file by the due date, you may request an extension by filing the

Individual Taxpayer Annual Local Earned Income Tax Return form with your name, address and social security

information and check the box indicating EXTENSION at the top of form and forward to the applicable YATB office.

NOTE: Extensions apply only to the filing of your return, not to the payment of tax. If tax is not paid in full by the April

due date, penalty and interest charges may apply.

WHO MUST FILE A LOCAL EARNED INCOME TAX RETURN?

An Individual Taxpayer Annual Local Earned Income Tax Return form must be filed by all persons subject to the local

earned income tax regardless of whether or not the taxpayer is employed or any tax amount is due.

Disabled – If you became disabled during the tax year, please check applicable box and indicate date when

disability occurred.

Deceased – If filing on behalf of an individual who passed away during the tax year, please check applicable box

and indicate date of death.

Retired – If you retired during the tax year, please check the applicable box and indicate date of retirement.

If you file an amended Federal or State income tax return, an amended Local Earned Income Tax Return must

also be filed with YATB. Please complete an Individual Taxpayer Annual Local Earned Income Tax Return form

and check the box indicating AMENDED RETURN at the top of form and forward to the applicable YATB office.

SUPPORTING DOCUMENTS:

A tax filing is not complete until all required supporting documentation and schedules have been filed. Failure to

provide required documentation and schedules may not only delay processing of your return, but may also subject you

to late filing penalties and/or legal action.

ENTERING INFORMATION:

• Your Address – If you are using a return form that shows a pre-printed name/address and the information is

incomplete or contains errors, please cross out the incorrect information and print any changes as necessary. For

proper distribution of your local earned income tax, your actual street address MUST be provided. If you utilize a PO

Box for receipt of mail, this would be shown in addition to your actual street address on the second line of address.

If you have moved during the year, please supply your prior address information and dates residing at each location

in the spaces provided at the top of your return form.

• Change of Address During Tax Year – If you moved during the year, please provide each address and account for all

12 months. If you resided in areas with different tax rates, use the Schedule X below to calculate your tax liability.

• Phone Number – Enter the area code and phone number where you can be reached during weekdays.

• Resident PSD Code – The Resident PSD Code is a six-digit number that references the county tax collection district,

school district and municipality in which you reside. Please enter the six digit PSD code where you lived on

December 31 even if you moved after December 31. For PSD Code information please refer to our website or

contact YATB.

• Social Security Number(s) – Carefully enter your SSN, and your spouse’s SSN if applicable, in the boxes provided on

your local earned income tax return form.

• Rounding Numbers – On the Local Earned Income Tax Return form, round monetary amounts to the nearest whole

dollar. Reduce any amount that is less than 50 cents to 0 (zero) and increase amounts from 50 to 99 cents to the

next dollar amount.

Example: $4.49 should show as $4.00, $4.50 should show as $5.00

Exception: Rounding will not apply to amounts calculated and shown in Lines 17, 18 and 19.

INDIVIDUAL TAXPAYER ANNUAL LOCAL INCOME TAX RETURN INSTRUCTIONS:

Line 1: Gross Compensation

DOCUMENTATION REQUIRED: W-2(s) must be enclosed (legible copies accepted).

Rule: Do not use Federal Wages as shown in box 1 of W-2

Taxable Local EIT Compensation includes: Salaries; Wages; Commissions; Bonuses; Tips; Stipends; Fees; Incentive

Payments; Employee Contributions to Retirement Accounts (If amounts received as a drawing account exceed the

salaries or commissions earned, the tax is payable on the amounts received. If the employee subsequently repays to the

employer any amounts not in fact earned, the tax shall be adjusted accordingly). Benefits accruing from Employment,

such as: Annual Leave; Vacation; Holiday; Separation; Sabbatical Leave; Compensation Received in the form of Property

shall be taxed at its fair market value at time of receipt. Jury Duty Pay; Active Duty Military Pay if stationed within PA;

Reserve Military Pay or Payments Received from weekend meetings for National Guard Units; Sick Pay (if employee

received a regular salary during period of sickness or disability by virtue of their agreement of employment); and Taxes

Assumed by the Employer. Taxpayers should refer to the PA Department of Revenue regulations regarding taxable

compensation. This list is not exhaustive; please contact YATB if you have additional questions.

Non-Taxable Local EIT Compensation includes: Social Security Benefits; Unemployment Compensation; Pensions;

Public Assistance; Death Benefits; Gifts; Interest; Dividends; Boarding and Lodging to Employees for convenience of

Employer; Lottery Winnings; Supplementary Unemployment Benefits (sub pay); Capital Gains (Capital Losses may not be

used as a deduction against other taxable income). Disability Benefits (periodical payments received by an individual

under a disability insurance plan); Active Military Service outside of PA and Summer Encampment; Personal Use of

Company Vehicles; Cafeteria Plans; and Clergy Housing Allowance; Non-Qualified Deferred Compensation Plan

Contributions made on behalf of the employee. Some forms of distribution payments from Individual Retirement

Programs such as; Keogh, Tax Shelter Annuity, IRA, and 401K are not taxable. Taxpayers should refer to the PA

Department of Revenue regulations regarding taxable compensation. This list is not exhaustive; please contact YATB if

you have additional questions.

Line 2: Unreimbursed Employee Business Expenses

DOCUMENTATION REQUIRED: Pennsylvania Department of Revenue form PA-UE must be enclosed (legible copies

accepted). PA-UE deductions may only apply to W-2 income; a separate UE form is required for each employer. All

expenses are subject to verification by YATB. YATB reserves the right to require further documentation (mileage logs,

receipts, etc.) to substantiate amounts claimed.

Line 3: Other Taxable Earned Income

Include income, from work or services performed, which has not been included on Line 1 or Line 5. Do not include

interest, dividends or capital gains. Do not report 1099 MISC income which is also claimed as part of a PA profit/loss

schedule. Please provide explanation and any applicable supporting documentation.

Line 4: Total Taxable Earned Income

Subtract amount in Line 2 from Line 1, then add Line 3.

Line 5: Net Profit and Line 6: Net Loss

DOCUMENTATION REQUIRED: 1099(s), PA Schedules C, F or RK-1 must be enclosed (legible copies accepted)

Rule: A taxpayer may NOT offset a business loss against wages and other compensation (W-2 Earnings, Line 1). A

taxpayer may offset a loss from one business entity against a net profit from another business entity. “Pass-Through”

income or loss from an S-Corporation is NOT taxable or deductible. If you or your spouse reported an S-Corporation

profit or loss to the PA Department of Revenue, please check the box on Line 5 and enter the amount of S-Corporation

profit or loss reported to the PA Department of Revenue. This is for audit purposes only when comparing income

reported to the PA Department of Revenue to avoid future unnecessary correspondence. Rental Income or loss

reported on a PA Schedule E is not taxable or reportable.

Line 7: Total Taxable Net Profit

Subtract amount in Line 6 from Line 5.

Line 8: Total Taxable Earned Income and Net Profit

Add amount in Lines 4 and 7.

Line 9: Total Tax Liability

Multiply Line 8 by your applicable Resident EIT Rate as shown on the Local EIT Tax Rates chart on the reverse side of the

YATB Taxpayer Annual Local Earned Income Tax Return form. A copy of the Local EIT Tax Rates chart, as well as the Tax

Return form may be obtained on our website www.yatb.com

.

Line 10: Total Local Earned Income Tax Withheld as Reported on W-2(s)

The amount of local earned income tax withheld should be shown in Box 19 of your W-2(s). You may claim credit for

local earned income tax withheld up to the rate as shown on the Local EIT Tax Rate chart. NOTE - Several municipalities

within PA have enacted NON-RESIDENT earned income tax rates that may be higher than your resident earned income

tax rate. You may be liable for this additional amount if your place of employment is located in one of these

municipalities. In this event, the additional earned income tax amount would NOT be refundable.

Line 11: Quarterly Estimated Payments/Credits from Previous Tax Year

List any quarterly estimated payments made to date for the applicable filing year. Do not include any penalty and

interest amounts that may have been made as part of the quarterly payments. Add any amount of tax overpaid as listed

on your previous year’s return to be applied to your current tax liability.

Line 12: Miscellaneous Tax Credits

GENERAL RULES APPLICABLE TO ALL LINE 12 TAX CREDITS

DOCUMENTATION REQUIRED: Out-of-State Return, PA State Return, PA Schedule G

1. Credits for income taxes paid to other states must first be used against your Pennsylvania state income tax liability;

any credit remaining thereafter may be used against your local earned income tax liability.

2. Credits for income taxes paid to political subdivisions located outside of Pennsylvania, or for wage taxes paid to

Philadelphia, may be taken directly against your local earned income tax liability.

3. In calculating your credit for income taxes paid to another state or political subdivision, please note that the same

items of income must be subject to both your local earned tax and the out-of-state tax.

4. No credit for income taxes paid to another state or political subdivision may exceed your total local earned

income tax liability.

Credit for Taxes Paid to Other States: You may take a credit based upon the gross earnings taxed both in another state

and in Pennsylvania that may be greater than the Pennsylvania state personal income tax rate. THIS CREDIT WILL BE

DISALLOWED IF THE NON-RESIDENT OR FOREIGN US STATE RETURN AND YOUR W-2 FORM SHOWING STATE INCOME

TAX WITHHELD ARE NOT INCLUDED.

No credits are given for state income taxes paid to states that reciprocate with the Commonwealth of Pennsylvania.

These states include: Indiana, Maryland, New Jersey, Ohio, Virginia and West Virginia.

Example: Taxpayer earned wages of $10,000.00 in Delaware and paid an income tax liability to that state in the amount

of $317.00. Assuming the current Pennsylvania state tax rate is 3.07% for the tax year in question; the $317.00 liability

for Delaware would exceed the (PA Tax) liability amount of $307.00 by $10.00. In this case, the $10.00 amount may be

credited against your local earned income tax.

Gross Income taxed by other state (1) $10,000

Local Earned Income Tax rate of 1% (.01) x .01

Local Tax Liability (2) $ 100.00

Tax paid to Delaware (3) 317.00

PA Income Tax (3.07% x $10,000) (4) - 307.00

Credit to be used against Local EIT(Line 3 minus Line 4) (5) $ 10.00

On Line 12 of the Local EIT Return form enter $ 10.00

or the amount on Line 2 of worksheet, whichever is less.

If all your wages or gross earnings are subject to Delaware state income tax (not PA), use the above example to calculate

your tax obligation. If you had earned income NOT taxed by Delaware, this income would be subject to the earned

income tax applicable where you reside and must be shown separately on the Local Earned Income Tax Return form.

Credit for Taxes Paid to Political Subdivisions Outside of Pennsylvania: You may take a credit based upon the gross

earnings taxed in both another political subdivision and where you reside in Pennsylvania. THIS CREDIT WILL BE

DISALLOWED IF THE FOREIGN CITY RETURN AND YOUR W-2 FORM SHOWING CITY INCOME TAX WITHHELD IS NOT

PROVIDED. NOTE: No credits are given for taxes paid to foreign countries.

Credit for Taxes Paid to Philadelphia: You may use any wage tax paid to Philadelphia as credit toward your local earned

income tax liability. No refunds or credits will be allowed for any overpayment made to Philadelphia. Enter the amount

of Philadelphia wage tax paid on Line 12 of the Local Earned Income Tax Return form. THIS CREDIT WILL BE

DISALLOWED IF A COPY OF YOUR W-2 AND/OR VERIFICATION OF TAXES PAID TO PHILADELPHIA IS NOT PROVIDED.

Line 13: TOTAL PAYMENTS and CREDITS

Enter the sum amounts of Lines 10 + 11 + 12

Line 14: Refund

If Total Tax Liability from Line 9 is less than your Total Payments and Credits in Line 13, enter the amount of

overpayment you wish to have refunded. If you have an overpayment of taxes in excess of $2.00, you may elect to

receive a refund or apply as credit against the next year’s tax liability (please check applicable box in Line 15).

Line 15: Credit Taxpayer/Spouse

If Total Tax Liability from Line 9 is less than your Total Payments and Credits in Line 13 you may also select the option of

crediting this amount to your spouse’s tax liability (please check applicable box).

Line 16: EARNED INCOME TAX BALANCE DUE

If Total Tax Liability from Line 9 is greater than your Total Payments and Credits in Line 13, enter amount of tax due. If

amount is less than $2.00, enter 0 (zero).

Line 17: Penalty after Due Date

If for any reason the tax is not paid by due date, an additional penalty of 1% multiplied by the amount of unpaid tax for

each month or fraction thereof during which tax due remains unpaid, shall be added and collected.

Line 18: Interest after Due Date

If for any reason the tax is not paid by the due date, an interest rate of 3% percent per annum (.000082/day) on the

amount of unpaid tax shall be calculated to the date of payment of the tax, and shall be added and collected.

Line 19: TOTAL PAYMENT DUE

The tax liability or amount due is sum amount of Lines 16 + 17 + 18. If amount due in Line 19 is less than $1.00, enter 0

(zero). Make checks payable to “YATB.”

For additional information, guidelines and worksheets, please access YATB’s website at

www.yatb.com

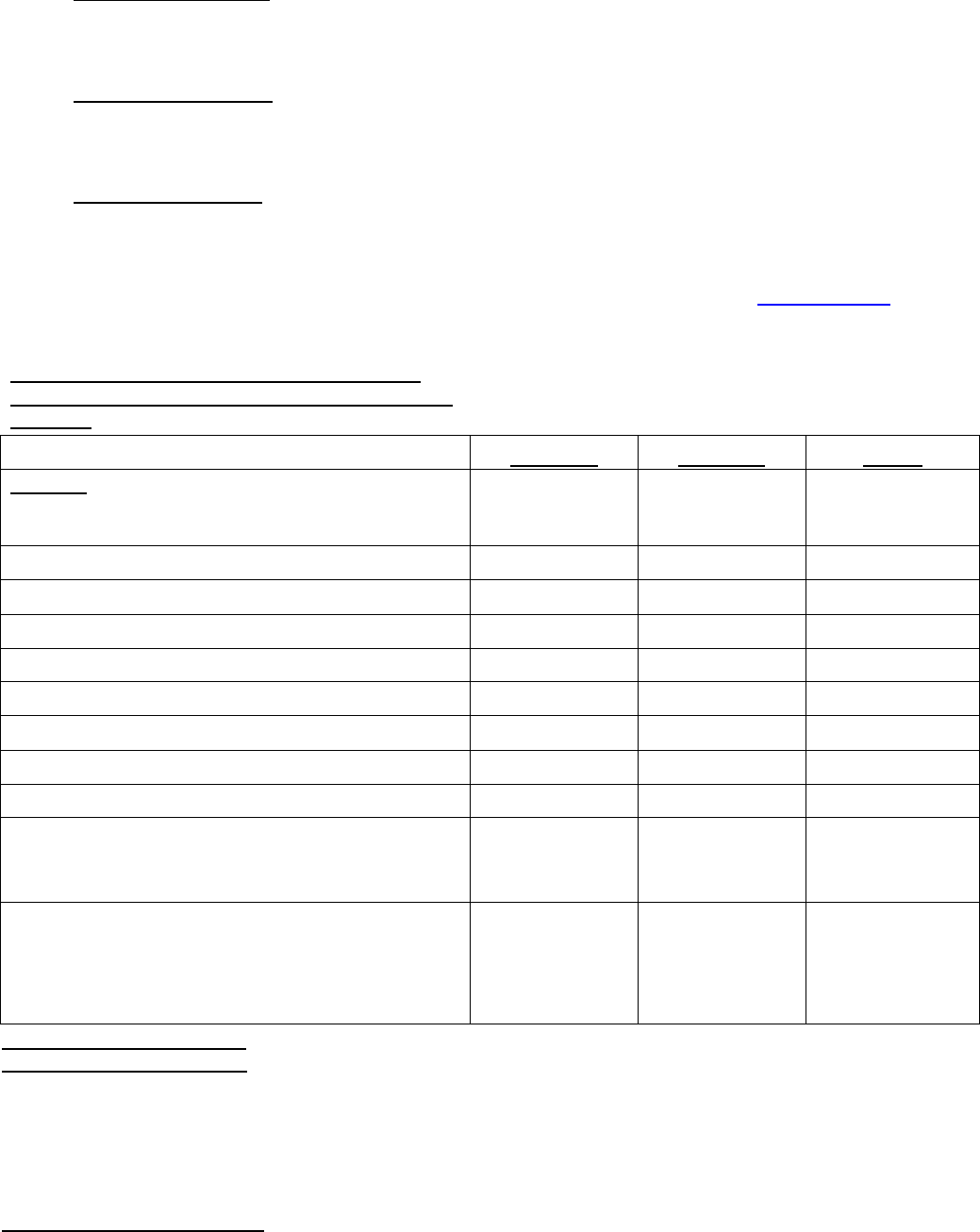

SCHEDULE X CALCULATOR

USE TO CALCULATE PRORATED TAX LIABILITY IF YOU

RESIDED IN AREAS WITH DIFFERING TAX RATES DURING

THE YEAR.

COLUMN A

COLUMN B

TOTALS

Column A: Number of months you resided at 1

st

address

during the year. Column B: Number of months you

resided at 2nd address during the year.

1. W-2 EARNINGS

2. LESS UNREIMBURSED EMPLOYEE BUSINESS EXPENSES

3. OTHER TAXABLE EARNED INCOME

4. TOTAL TAXABLE EARNED INCOME

5. NET BUSINESS PROFIT

6. NET BUSINESS LOSS (ENTER AS A NEGATIVE)

7. TOTAL TAXABLE NET PROFIT

8. TOTAL TAXABLE EARNED INCOME AND NET PROFIT

9. TOTAL TAX LIABILITY (SEE TAX RATE CHART)

COLUMN A -

Line 8 Total x Tax Rate A

COLUMN B - Line 8 Total x Tax Rate B

Column C is the TOTAL of both columns A & B. Enter

these figures in the corresponding lines on the front of

the return. Complete a separate worksheet for each

taxpayer who moved between districts having different

tax rates during the year.

REMITTANCE ADDRESSES:

FOR YORK COUNTY RESIDENTS:

PAYMENT DUE NO PAYMENT/NO REFUND DUE REFUND DUE

YORK ADAMS TAX BUREAU YORK ADAMS TAX BUREAU YORK ADAMS TAX BUREAU

PO BOX 15627 PO BOX 15628 PO BOX 15629

YORK PA 17405 YORK PA 17405 YORK PA 17405

FOR ADAMS COUNTY RESIDENTS:

PAYMENT DUE NO PAYMENT/NO REFUND DUE REFUND DUE

YORK ADAMS TAX BUREAU YORK ADAMS TAX BUREAU YORK ADAMS TAX BUREAU

PO BOX 4374 PO BOX 4344 PO BOX 4343

GETTYSBURG PA 17325 GETTYSBURG PA 17325 GETTYSBURG PA 17325