Section 1332 State Relief and

Empowerment Waiver Concepts

Discussion Paper

November 29, 2018

Centers for Medicare & Medicaid Services

Center for Consumer Information & Insurance Oversight

2

Contents

Overview of 1332 Waiver Concepts.................................................................................................... 3

Waiver Concept A: State-Specific Premium Assistance………………………………………………………………….. 8

Waiver Concept B: Adjusted Plan Options………………………………………………………………………………………. 13

Waiver Concept C: Account-Based Subsidies………………………………………………………………………………….. 20

Waiver Concept D: Risk Stabilization Strategies……………………………………………………………………………….25

Appendix A: Types of Waiver Concepts and Policy Options …………………………………………………………….37

3

Overview of 1332 Waiver Concepts

Introduction to Section 1332 Waivers

Under section 1332 of the Patient Protection and Affordable Care Act (PPACA), states can apply for a

State Innovation Waiver (also referred to as a “section 1332 waiver” or “1332 waiver”) from the

Department of Health and Human Services (HHS) and the Department of the Treasury (collectively, the

Departments), which allows states, if approved, to implement innovative programs to provide access to

quality health care. The overarching goal of 1332 waivers is to empower states to develop innovative

health coverage options that best fit the states’ individual needs. This goal aligns with the

Administration’s goal to give all Americans the opportunity to gain quality and affordable health

coverage regardless of income, geography, age, sex, or health status. Through section 1332 waivers, the

Departments aim to assist states with developing health insurance markets that offer more choice,

competition, and affordability to Americans.

These waiver concepts are intended to foster discussion with states by illustrating how states might take

advantage of new flexibilities provided in recently released guidance

1

related to section 1332 on

October 24, 2018, which replaced the previous guidance released on December 16, 2015. The new

guidance aims to lower barriers to innovation for states seeking to reform their health insurance

markets, increases flexibility with respect to the manner in which a section 1332 state plan may meet

section 1332 standards in order to be eligible to be approved by the Departments, clarifies the

adjustments the Secretaries may make to maintain federal deficit neutrality, and allows for states to use

existing state legislative authority to authorize section 1332 waivers in certain scenarios. These waivers

are now called State Relief and Empowerment Waivers to reflect this new direction and opportunity.

The Departments are committed to empowering states to innovate in ways that will strengthen their

health insurance markets, expand choices of coverage, target public resources to those most in need,

and meet the unique circumstances of their state.

Under a section 1332 waiver, a state may receive pass-through funding associated with the resulting

reductions in federal spending on Exchange financial assistance (that is, premium tax credits under

section 36B of the Internal Revenue Code (PTC), small business health insurance tax credits under

section 45R of the Code (SBTC), or cost-sharing reductions (CSR)) consistent with the statute and the

state’s waiver plan. Pass-through funding may only be used to implement the state waiver plan.

To receive approval for a section 1332 waiver, states must demonstrate that the waiver will provide

access to health insurance coverage that is at least as comprehensive and affordable as would be

provided under the PPACA without the waiver, will provide coverage to at least a comparable number of

residents of the state as would be provided coverage without a waiver, and will not increase the federal

deficit. These statutory criteria are referred to as the “guardrails.” Before submitting its section 1332

waiver application, a state must have enacted a law providing for implementation of the waiver,

provided a public notice and period for public comment, and held public hearings sufficient to ensure a

meaningful level of public input.

1

https://www.federalregister.gov/documents/2018/10/24/2018-23182/state-relief-and-empowerment-waivers

4

Support of Section 1332 Waivers and Release of 1332 Waiver Concepts

Since 2015, the Departments have approved a number of state waivers,

2

and continue to work with

states on future waivers. The Departments have developed this series of 1332 Waiver Concepts

(“waiver concepts”) in an effort to spur conversation and innovation with states. The Departments look

forward to engaging with states on these waiver concepts, which are intended to show states concepts

that the Administration supports and that fit within the 1332 framework. States are not required to use

these concepts in their waiver applications; states may use these waiver concepts alone or in

combination with other waiver concepts, state proposals, or policy changes. We encourage states to

couple waiver concepts with other innovative ideas. See Appendix A: Types of Waiver Concepts and

Policy Options for an overview of all waiver concepts included in this document. The four waiver

concepts discussed in this document are:

• Waiver Concept A: State-Specific Premium Assistance;

• Waiver Concept B: Adjusted Plan Options;

• Waiver Concept C: Account-Based Subsidies; and

• Waiver Concept D: Risk Stabilization Strategies.

These waiver concepts are offered to serve as a springboard for innovative ideas that may improve the

health care markets in individual states, and the concepts discuss policy and implementation ideas that

we look forward to discussing with states. However, in order to gain approval, states’ section 1332

waiver applications must meet section 1332 statutory requirements, including satisfaction of the four

guardrails under section 1332(b)(1) (comprehensiveness, affordability, coverage, and federal deficit

neutrality). The Departments cannot assess whether or not a proposal meets the guardrails until we

receive a specific proposal from a state. A state’s incorporation of any waiver concept into a section

1332 waiver application is not a guarantee that the Departments will ultimately approve the waiver.

The Departments retain the discretion to decide whether to grant a 1332 waiver based on the particular

circumstances of each state’s application, and the Departments must in all cases evaluate each

application for compliance with section 1332 statutory requirements. The Departments’ waiver

authority is limited to requirements described in section 1332(a)(2) of the PPACA. Thus, for example, the

Departments have no authority to waive any provision of the Employee Retirement Income Security Act

(ERISA).

The Departments continue to encourage states to propose other innovative approaches to meet the

unique needs of their population, and recommend that states interested in applying for a section 1332

waiver reach out to the Departments promptly for assistance in formulating an approach that meets the

requirements of section 1332. These waiver concepts do not represent the full range of provisions of the

PPACA that can be waived under section 1332; states can and might want to consider developing

applications to use section 1332 waivers to waive other provisions as outlined in the statute, such as the

employer mandate, or the metal tiers. Further questions and comments, including comments on these

waiver concepts, should be directed to StateInnovat[email protected]hs.gov

.

2

For a list of all received waiver applications (including approved waivers) please see:

https://www.cms.gov/CCIIO/Programs-and-Initiatives/State-Innovation-

Waivers/Section_1332_State_Innovation_Waivers-.html#Section 1332 State Waiver Applications

5

Expectations Regarding 1332 Waivers, Guardrails, and Application Timing

As with all 1332 waiver applications, states leveraging waiver concepts designed by the Departments will

need to ensure their proposed plans meet all of the statutory requirements, including satisfying the four

guardrails (comprehensiveness, affordability, coverage, and federal deficit neutrality).

To provide flexibility under the statute to states to explore different options for coverage, the new

guidance issued in October 2018 explains how the Departments’ new interpretation of the

comprehensiveness and affordability guardrails now focuses on access to comprehensive and affordable

coverage. This shift in focus to access ensures that state residents who wish to retain coverage similar

to that provided under the PPACA can continue to do so, while permitting a state 1332 waiver plan to

also provide access to other options that may be better suited to consumer needs and more attractive

or affordable to many individuals. The updated guidance interprets the comprehensiveness and

affordability guardrails to mean that the waiver must provide access to coverage that is at least as

comprehensive and affordable as coverage absent the waiver. The coverage guardrail will be met so

long as a comparable number of residents are covered under the waiver as would have been covered

absent the waiver. The new guidance expands the definition of coverage for purposes of this guardrail

to include more forms of coverage. The guidance also focuses on the aggregate effects of the waiver for

the guardrails.

In light of the requirement to have continued access to comprehensive and affordable coverage, the

new guidance maintains the same strong-protections for people with pre-existing conditions as the law

currently provides absent a 1332 waiver. To be clear, the waiver concepts presented here do not open

any flexibility for states to undermine these protections. This Administration remains firmly committed

to maintaining protections for all Americans with pre-existing conditions, and believes that states can

develop programs that improve upon the status quo and provide necessary support for people with pre-

existing and/or chronic conditions.

States will also need to establish evaluation requirements for the program as outlined in the waiver

specific terms and conditions. Programs will be evaluated periodically for how well they achieve

program goals. Evaluation criteria may include: the number of uninsured, the number of persons

covered, the change in premiums, coverage options, the accessibility of providers and the change in

cost-sharing, the extent of expected choice available to consumers, the extent of expected competition

between insurers, the efficiency of the health care system, and best use of public dollars.

Consistent with the statute, states must have legal authority to pursue a waiver by enacting state laws

or enacting revisions to existing state laws to apply for and implement a state plan for a section 1332

waiver. Per the 2018 guidance, the Departments clarified that in certain circumstances, a state may

satisfy the requirement that the state enact a law under section 1332(b)(2) by using existing legislation

that provides statutory authority to implement or enforce PPACA provisions and/or the state plan,

combined with a duly-enacted state regulation or executive order.

Consistent with the regulations at 31 CFR 33.108(b) and 45 CFR 155.1308(b), states are required to

submit initial waiver applications sufficiently in advance of the requested waiver effective date,

including an appropriate implementation timeline, to allow for enough time to review and to maintain

smooth operations of the Exchange in the state, and for affected stakeholders or issuers of health

insurance plans that are (or may be) affected by the waiver plan to take necessary action based on the

6

approval of the waiver plan, particularly when the waiver impacts premium rates. States should

generally plan to submit their initial waiver applications no later than the end of the first quarter of the

year prior to the year the waiver would take effect in order to allow for sufficient time for review. The

Departments may be able to review waiver concepts discussed in this paper more quickly than novel

waiver applications. However, the Departments cannot guarantee a state’s request for review or

approval by a certain date earlier than the 180-day statutory deadline.

States may propose to leverage the federal platform, HealthCare.gov, to perform eligibility, plan display,

plan selection, and enrollment functions. If a state wishes to rely on the federal platform to implement

its waiver plan and such reliance requires technical changes to the federal platform’s information

technology system or to the operating procedures of the federal platform, additional time may be

needed. States should engage with HHS early in the section 1332 waiver application process to

determine whether the federal platform can accommodate the technical changes that support their

state needs and requested flexibilities. Similarly, states considering a waiver of any federal tax provision

should engage with the Departments early in the process to assess whether the waiver proposal is

feasible for the Internal Revenue Service (IRS) to implement, and to assess the administrative costs to

the IRS of implementing the waiver proposal.

Under state innovation waivers, including waivers that incorporate these waiver concepts, states are

responsible for ensuring that consumers whose coverage choices are impacted by a waiver are aware of

changes that will result from the implementation of a state’s waiver plan. Consumers need to

understand these changes in order to be empowered to make decisions about their health care. States

that are requesting a waiver should consider and describe in their applications how consumers will be

educated about their new coverage options and how they will purchase this coverage.

Financing and Pass-Through Funding

Under a section 1332 waiver, if the waiver proposal is approved, a state may receive funding equal to

the amount of forgone federal financial assistance that would have been provided to its residents

pursuant to programs under title I of the PPACA. A state may only use this funding, known as pass-

through funding, to implement the state’s plan as described in the 1332 waiver application and/or the

state’s specific terms and conditions. In order for a state to receive pass-through funding, a state must

demonstrate that federal spending on financial assistance if the waiver is approved is equal to or less

than the amount the federal government would pay if the waiver were not approved and implemented.

Under the statute, the state will be entitled to funding based on the amount of PTC, SBTC, and CSR that

would have been provided to individuals in the state absent the waiver. Pass-through funding levels will

be reduced by any other increase in spending or decrease in revenue as necessary to ensure the deficit

neutrality guardrail is met.

As part of a state’s waiver application, if the state is seeking pass-through funding, it should include an

explanation of how, due to the structure of the state plan and the waiver of a provision listed under

section 1332(a)(2), the state anticipates that individuals would not qualify for, or would qualify for less

PTC, SBTC, or CSR for which they would otherwise be eligible. The state should also explain how the

state plans to use that funding to implement the state waiver plan.

The Departments will evaluate the estimated pass-through funding amount requested by a state for the

period of the waiver. The actual pass-through amount for the period of the waiver will be calculated by

the Departments annually. If a state receives pass-through funding, the state must use pass-through

7

funding solely for purposes of implementing the state's 1332 waiver plan as approved by the

Departments. Any unused pass-through funds must be returned to the federal government by the end

of the waiver, as specified in the specific terms and conditions. The state is responsible for ensuring any

necessary state funding is available to implement its state plan, as described in its application.

The PPACA includes a provision that applies abortion coverage limitations to plans that are sold through

the Exchange for all individuals who receive federal income-based subsidies to purchase private health

insurance. Furthermore, the Hyde Amendment prohibits federal funds, including section 1332 pass-

through funds, from being used to pay for abortion outside of the exceptions for rape, incest, or if the

pregnancy is determined to endanger the woman’s life. States must ensure that any pass-through

funding complies with these requirements as well.

Administrative Expenses

Under the deficit neutrality requirement, the projected federal spending net of federal revenues under

the waiver must be equal to or lower than projected federal spending net of federal revenues in the

absence of the waiver. The effect on federal spending includes all changes in financial assistance

provided to eligible Exchange enrollees and other direct spending that result from implementation of

the waiver. Projected federal spending under the waiver proposal also includes all administrative costs

to the federal government, including any changes in IRS administrative costs, federal Exchange

administrative costs, or other administrative costs associated with the waiver. Subject to the

requirements of the Intergovernmental Cooperation Act (ICA) and OMB Circular A-97, if a waiver

requires the Centers for Medicare & Medicaid Services (CMS) to make technical changes to the federal

eligibility and enrollment platform, the state will be responsible for reimbursing CMS for any costs

incurred for certain technical and specialized services covered under the ICA (either with 1332 pass-

through funds and/or funds provided by the state to fully reimburse CMS).

Additional Information

In developing a 1332 waiver proposal, states will need to establish program requirements to help

guarantee the integrity and success of their new program. All programs are at risk of waste, fraud, and

abuse; states are responsible for ensuring appropriate measures are in effect to minimize these risks. In

addition, under all 1332 waivers, states must have a plan in place to guarantee that pass-through

funding is only used for the approved waiver plan.

States with an approved waiver must comply with all Federal laws including the applicable civil rights

authorities that prohibit discrimination in healthcare programs and activities on the basis of race, color,

national origin, disability, age, and sex.

8

Waiver Concept A: State-Specific Premium Assistance

With Waiver Concept A: State-Specific Premium Assistance, states could consider options to create and

implement a new state subsidy structure that changes the distribution of subsidy funds compared to the

current PTC structure. A state may design a subsidy structure that meets the unique needs of its

population in order to provide more affordable healthcare options to individuals in their state broadly to

a wider range of individuals or to address structural issues that create perverse incentives, such as the

subsidy cliff

3

. If the waiver is expected to reduce federal spending on PTC, the state will receive federal

pass-through funding that may be used to implement the section 1332 state waiver plan and help fund

the state subsidy program.

Policy

In the State-Specific Premium Assistance waiver concept, states have the flexibility to design a new

subsidy structure implemented by the state in lieu of the federal PTC structure.

States need to ensure that any new subsidy structure meets the 1332 guardrails, including the

affordability guardrail, which is generally measured by comparing each individual’s expected out-of-

pocket spending for health coverage and services to their incomes. Out-of-pocket spending for health

care includes premiums (or equivalent costs for enrolling in coverage) and spending such as deductibles,

co-pays, and co-insurance associated with the coverage, or direct payments for healthcare.

This new state subsidy structure can redefine the amount of financial assistance provided as a state

subsidy, such as a state tax credit, or redefine the populations eligible for such financial assistance, or

both. For example, a state might:

• Replace the federal PTC structure with a new per-member per-month, state premium credit

based on age.

• Determine eligibility using an affordability percentage and award financial assistance when the

costs of health coverage exceed a set percentage of household income.

• Leverage a similar state subsidy or state tax credit structure already in place that could be easily

modified for this purpose.

Implementation Approaches (Concept A: State-Specific Premium Assistance)

In the State-Specific Premium Assistance waiver, states would receive waiver of the PTC for plans offered

through the Exchange in the state (section 36B of the Code and section 1401of the PPACA, both waived

in entirety), in addition to provisions around QHPs, such as 1301(a) and the Exchange’s operations,

1311(d)(2)(B)(i). Under this approach, in place of the PTC, states could develop a state premium subsidy

program. This would likely be easier for existing State-based Exchanges (SBE) to operationalize using

existing SBE infrastructure as outlined in the options below since there are already connections to

federal data sources.

States can also consider how to implement the new subsidy structure. An advanceable subsidy structure

based on consumers’ projecting their income requires much more complexity than an age-adjusted tax

3

The subsidy cliff refers to the point at which a consumer’s income changes and they are ineligible for PTC.

9

credit. Income-based subsidies could also provide perverse incentives that discourage upward mobility

and work, and states may wish to avoid these problems. States considering a subsidy structure based on

income should also consider how consumers can report changes in income or if the state will perform an

income reconciliation. States are encouraged to also consider additional innovations within the subsidy

program. Subsidy design will also have an impact on participation.

Under the State-Specific Premium Assistance waiver, there would not be a FFE operating in the state.

Rather, applications for state financial assistance would be made available to consumers as part of the

state’s plan and administered by the state, and the state would assume all responsibilities associated

with providing financial assistance. These responsibilities specifically include development of the new

subsidy structure, creation and processing of applications, eligibility determinations, payment of

subsidies to issuers, providing consumer support and education to applicants and enrollees, and

adjudicating appeals of eligibility determinations. States would be required to reimburse CMS for

waivers that require CMS to make technical changes to the federal eligibility and enrollment platform.

• Implementation Approach 1: One implementation option for states would be to perform the

eligibility determination using existing Medicaid or CHIP system connections to federal data

sources (e.g., Department of Homeland Security and the Social Security Administration). States

would be required to cost allocate expenses with Medicaid

4

in these circumstances, and

perform data matching issue processing for individuals who are not able to be electronically

verified. This may require new data use agreements or updates to existing data use agreements

with federal agencies, but would have the benefit of streamlining health coverage assistance

programs and consumer support channels within the state. States would be required to have

the authority to access these federal data sources.

o Note: Due to technical limitations and build constraints on the FFE system, this waiver

option may be feasible for implementation as early as Open Enrollment (OE) 7 (plan

year 2020), but the state’s plan and needed technical changes would need to be

confirmed by CMS by the August prior to the start of the same plan year (i.e., August

2019 for implementation in plan year 2020).

• Implementation Approach 2: A second implementation option for states would be to perform

the eligibility determination using authorities and technologies currently in place through the

FFE connections to federal data sources (e.g., Department of Homeland Security and the Social

Security Administration). Under this approach, the state would request that the FFE perform

verification of certain eligibility factors, such as citizenship and immigration status, on behalf of

the state. Related to the verification requests, the FFE would perform downstream data

matching issue processing, and support the state in related appeals adjudication. States would

use this federally-verified data (for example citizenship/immigration status) in combination with

application responses and other state-verified data (for example state income) to make an

eligibility determination.

o A table outlining state and federal responsibilities for FFE-platform states considering

this approach is included below.

o Note: Due to technical limitations and build constraints on the FFE system, this waiver

option is feasible for implementation as early as OE8 (plan year 2021) and the state’s

plan and needed technical changes would need to be confirmed by CMS by January of

4

Per 2 CFR 200 (previously OMB-A-87), cost allocation principles would apply unless otherwise waived.

10

the prior plan year (i.e., January 2020 for implementation in plan year 2021). CMS will

need detailed design elements to evaluate feasibility and provide estimates on costs.

For either implementation approach, states would communicate the eligibility result to the individual

and provide the individual with information on how to use the subsidy when enrolling in health

coverage. Current FFE states should consider the option described below in Implementation Approach

2. Where necessary, the state would provide follow up information to the individual regarding the

successful resolution of data matching issues (DMIs), or regarding the failure to resolve a DMI and the

associated loss of subsidy eligibility.

Once an eligibility determination is made, consumers could take advantage of the market’s existing sales

channels to purchase coverage. States are encouraged to consider waiving additional Exchange

requirements (section 1311 of the PPACA) in order to maximize flexibility in implementing their tailored

financial assistance program. Examples of policy options and implementation approaches related to

plan option flexibility and provided in the adjusting plan options waiver concept section.

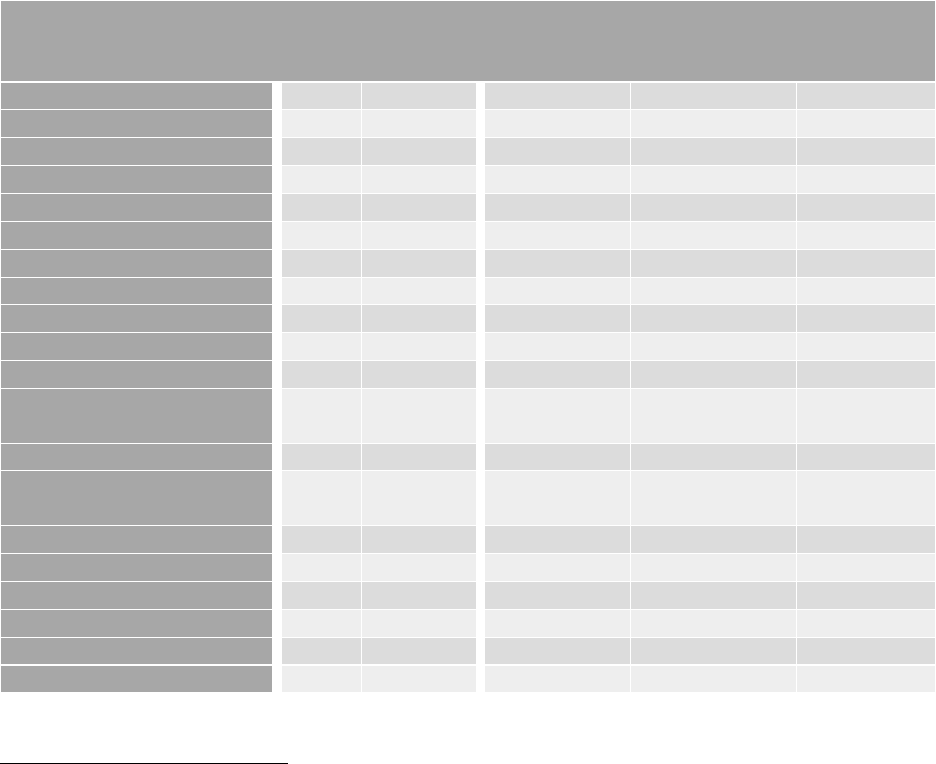

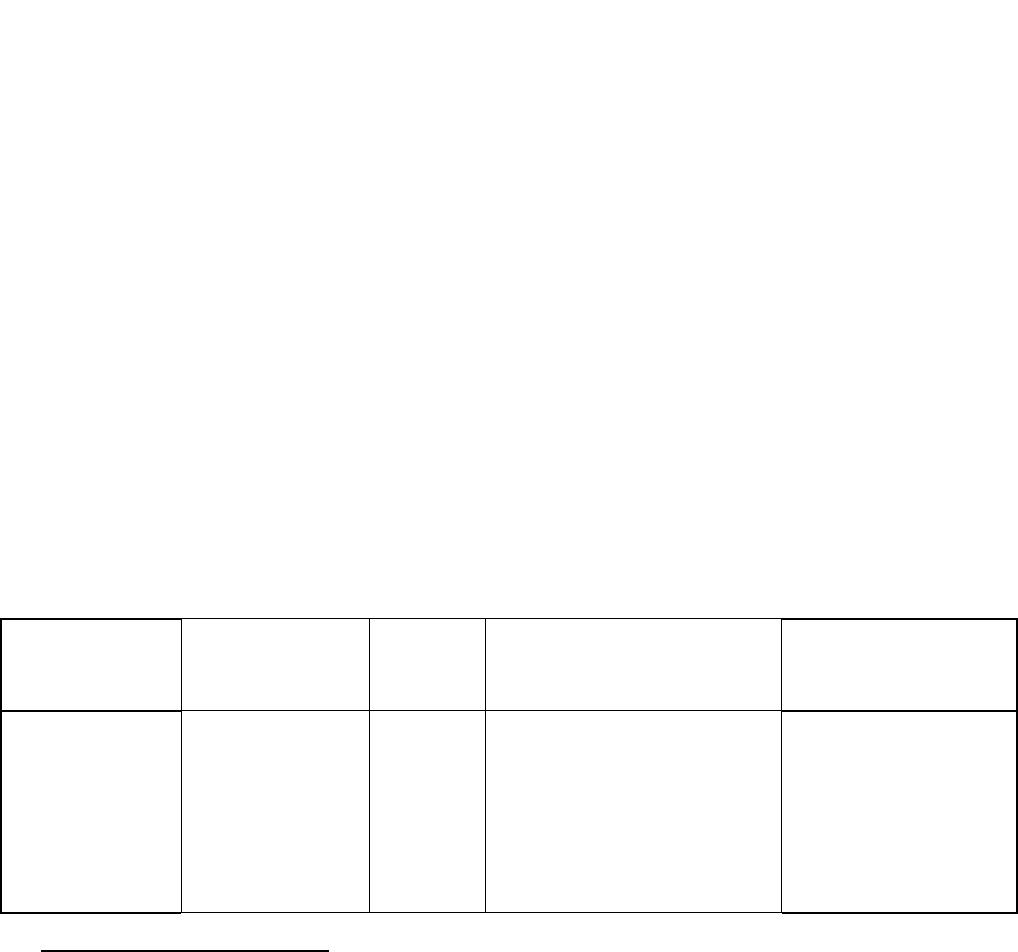

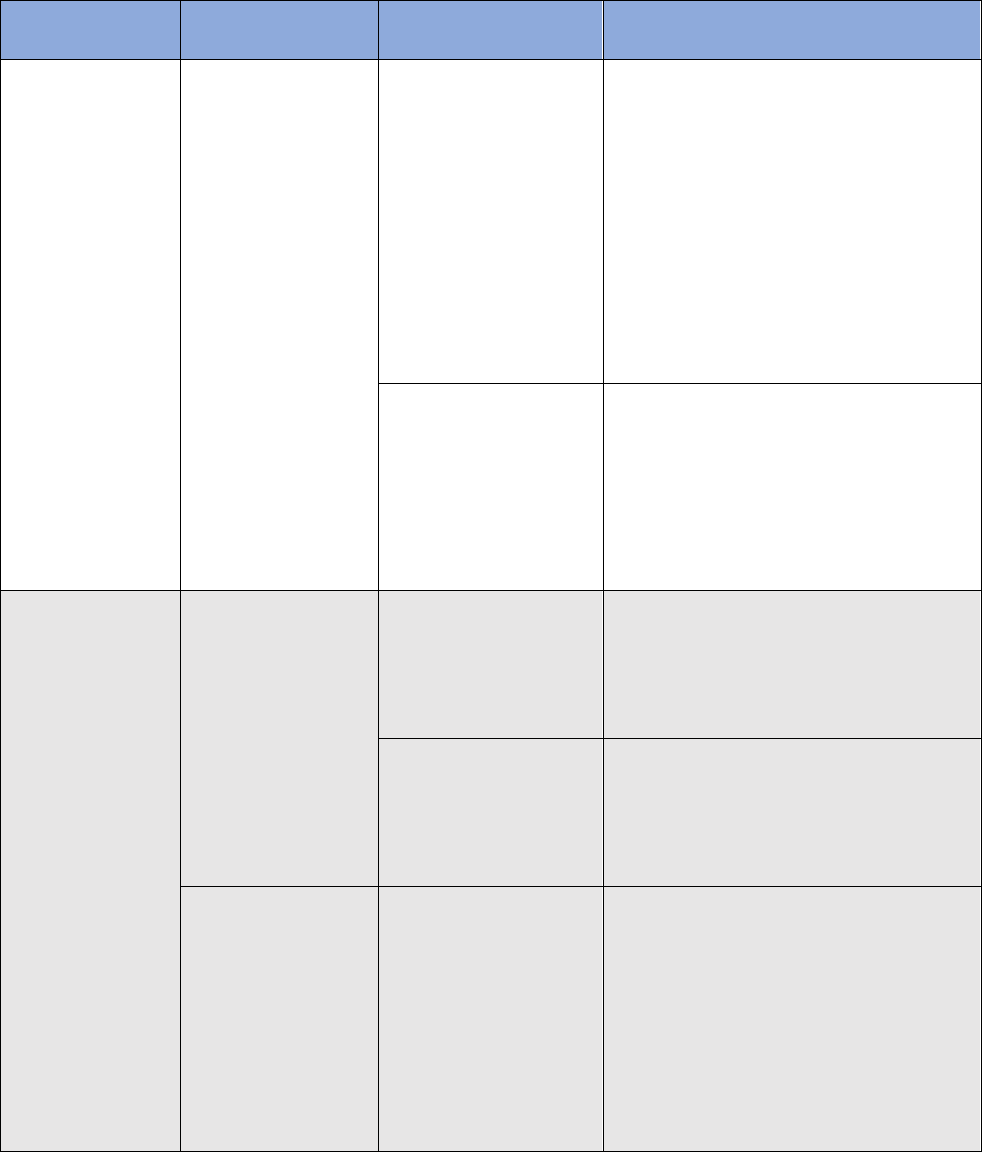

State and federal responsibilities for implementing a new subsidy structure under a new State-Specific

Premium Assistance Waiver (Concept A)

Without Waiver

(FFE platform state

status quo)

Option for FFE support of State-specific

Premium Assistance Waiver

State

Federal

State

State or Vendor

Federal

Consumer call center

X

X

Consumer website

X

X

Consumer marketing

X

X

Consumer noticing

X

X

DMI only

Agent/broker support

X

X

X

X

Assister support

X

Optional

5

Plan certification

X

X

Optional

Anonymous shopping

X

Optional

ID proofing

X

X

Application

X

X

Verifications:

citizenship/immigration

X

X

Verifications: income

X

Optional

Optional

Verifications: non-ESI

coverage check

X

Optional

Verifications: SEP

X

Optional

DMI follow up

X

X

Eligibility determination

X

X

Benefit calculation

X

X

Appeals

X

X

Casework

X

X

X

5

Items listed as optional are listed as optional since they are waivable provisions under section 1332 of the PPACA.

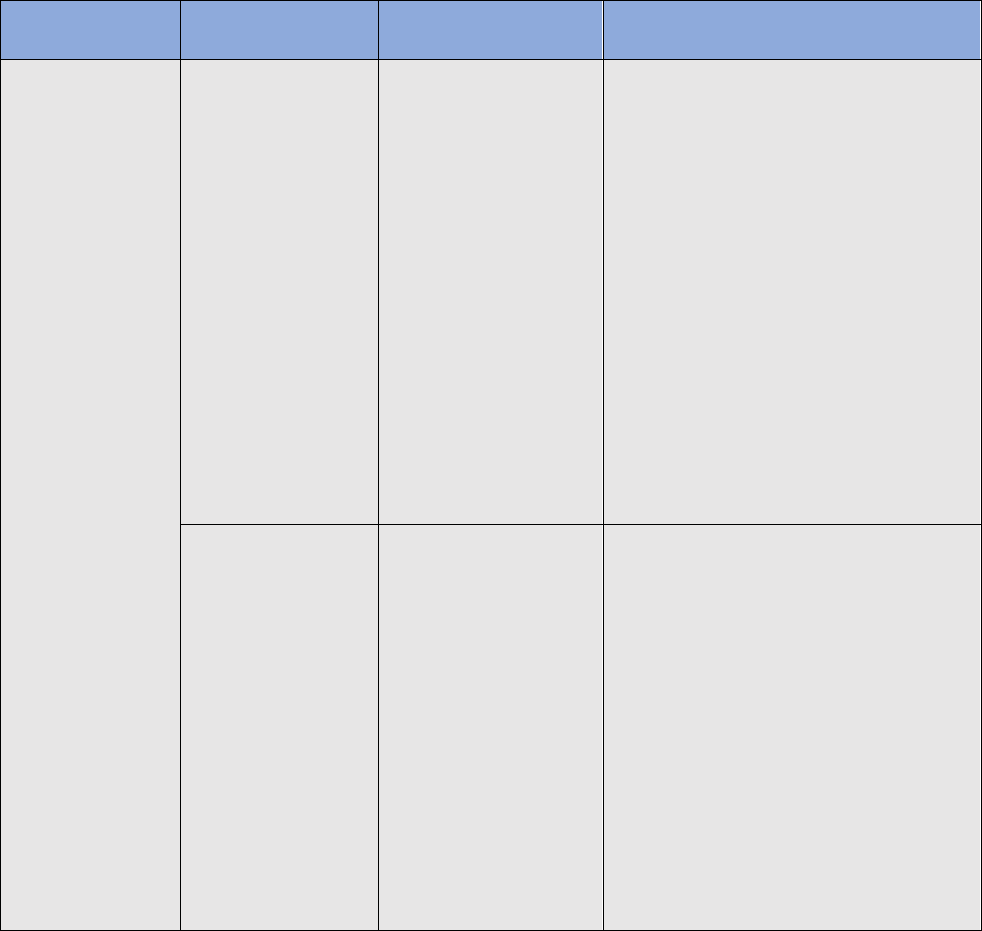

11

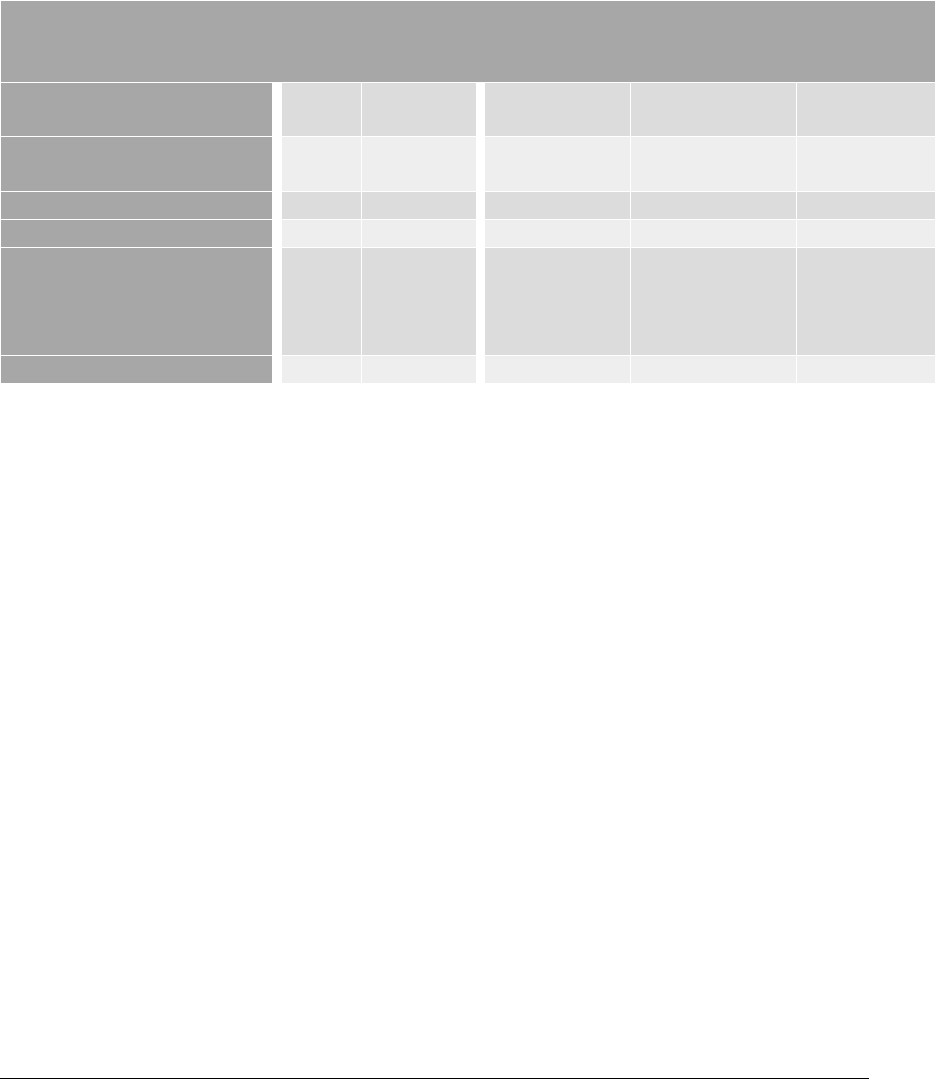

Without Waiver

(FFE platform state

status quo)

Option for FFE support of State-specific

Premium Assistance Waiver

Account transfer –

Medicaid/CHIP

X

X

Optional

Plan shopping and

selection

X

Optional

Enrollment transactions

X

Optional

Enrollment reconciliation

X

Optional

1095A generation

X

Not a part of

Implementation

for this waiver

option

Issuer payment

X

X

Administrative Expenses

States may use pass-through funding associated with waived PTC to implement the state plan and help

fund the alternative state subsidy program. Any additional costs to fund the state subsidy program

would be the state’s responsibility. For example, if additional state premium subsidy costs are incurred

through additional enrollment under these policy changes, the state would be responsible for covering

that additional cost (either with 1332 pass-through funds or funds provided by the state). Please refer

to the Overview of 1332 Waiver Concepts for information on when states can receive pass-through

funding, and administrative costs to the federal government associated with the waiver.

• Implementation Approach 1: States would perform the eligibility determination using existing

Medicaid or CHIP system connections to federal data sources

o Administrative Expenses: In this option, very few costs would be incurred by CMS, and

the state would be treated by CMS in a similar manner as a state operating its own

Exchange with a redirect to the independent state website.

• Implementation Approach 2: States would perform the eligibility determination using

authorities and technologies currently in place through the FFE’s connections to federal data

sources

o Administrative Expenses: In this option, costs would be incurred by the state to support

up-front technical changes and ongoing processing of citizenship or immigration-related

DMIs. The state will be responsible for reimbursing CMS for both types of costs incurred

as part of the section 1332 state waiver program.

Things to consider and/or additional information on implementation approaches under Concept A

Below are some questions to consider as the state develops these programs, and to include in the 1332

waiver application.

Questions for Concept A:

1) How will the state implement a new subsidy structure?

12

a. Which entity will administer the program? Is it a new or existing entity? To what extent

will the entity be subject to state insurance laws? To what extent will the entity

coordinate activities with other public programs (e.g., Medicaid and CHIP)?

b. How much funding is necessary for the subsidy structure?

c. What populations or eligibility requirements will the state have for this program (e.g.,

age, income, etc.?

d. What plan options will be available?

e. If state funding is required, how much funding does the state anticipate will be

necessary to implement the state plan and how will the state generate the required

state funding?

2) When and how will consumers be notified of their subsidy amount?

3) Will there be a process for consumers to report changes to eligibility criteria (i.e. income, age,

address etc.)?

4) What process will be used for consumers to appeal their eligibility determination and subsidy

amount?

5) What sources is the state using to verify eligibility for coverage and/or the subsidy (if

applicable)? Will the state be using their Medicaid/CHIP Agency or the FFE to do eligibility

verifications and determinations? Is the state using any state sources for verification?

6) How will issuers receive payments for the subsidy? What is the timing and mechanism for pay-

out?

7) Will the state reconcile state subsidy amounts based on current or prior year household income

or some other income definition If so, how will that be operationalized?

8) Will the new subsidy program include incentives for providers, enrollees, and plan issuers to

continue managing health care costs and utilization and lower overall health care spending (if

any)?

9) Does the state have the authority/ability to adjust the program requirements on a yearly or

other basis to account for market changes? If so what is the schedule and process for this?

10) Will the state require issuers to include the impact of the program in initial and/or final rates?

11) Is there any existing legislation and/or regulations related to the state program, or is new state

legislation and/or regulation needed?

12) If the state is leveraging the FFE’s system, does the state anticipate requesting any changes to

the FFE? If the state is leveraging the SBE, does the state anticipate requesting any changes to

the SBE? Related to question #2 above, does the state envision that applicants will be able to

see their subsidy amount during the plan selection process?

13) If implementing a state subsidy program what (if any) federal tax consequences will there be for

the individuals enrolled and/or reporting requirements for the state as a result?

14) How does the state plan to ensure access to health coverage that is at least as comprehensive

and affordable as would be provided under the PPACA as compared to without the waiver?

13

Waiver Concept B: Adjusted Plan Options

In the Adjusted Plan Options waiver concept, states would have the flexibility to provide state financial

assistance for non-QHPs, potentially increasing consumer choice and making coverage more affordable

for individuals. States also could choose to expand the availability of catastrophic plans beyond the

current eligibility limitations by waiving section 1302(e)(2) of the PPACA, for example, to make them

available to a broader group of individuals. With the Adjusted Plan Options waiver, states may be able

to increase consumer choice and affordability by allowing consumers to use a state subsidy towards

catastrophic plans, individual market plans that are not QHPs, or plans that do not fully meet PPACA

requirements. Under the PPACA, consumers can use PTC only towards non-catastrophic QHPs offered

through the Exchanges. Under this waiver concept, states may be able to waive the QHP requirement

under section 36B of the Code and allow PTC for a non-QHP if the non-QHP is offered through the

Exchanges and if certain other conditions are met.

As with all 1332 waiver requests, a state must ensure that the waiver plan meets the four statutory

guardrails including affordability, comprehensiveness, coverage, and federal deficit neutrality. In

particular, to the extent the proposal impacts the individual market risk pool in any adverse way, a state

will need to clearly identify how the waiver plan will continue to provide access to coverage that is at

least as affordable and comprehensive as without the waiver. Under each of the options for

implementing this concept, the state would need to take on responsibilities for certification of plans.

Option 1: Allow state financial assistance for non-QHPs

Policy

States should consider what, if any, state requirements there will be for the state subsidy to apply to

non-QHPs and what types of plans would be eligible for the state subsidy. For example, a state may

wish to prevent subsidies for people purchasing products that do not meet some minimum standard.

States may allow state-specific financial assistance to be applied to QHPs and/or non-QHPs such as: all

plans approved for sale in the individual market (including non-QHP off-exchange individual market

plans); plans that do not meet (or that exceed) a specific AV/metal level; short-term, limited-duration

plans; catastrophic plans, employer -based plans, association health plans; plans that do not meet all

EHB requirements, but are at least as comprehensive as those that do; value-based insurance design

(VBID) plans; or condition-specific benefit plans that might exceed EHB requirements. In designating

plans eligible for subsidies, states would need to ensure that any changes result in a plan that will meet

the 1332 guardrails and other requirements of the Departments. This option could allow for more plan

options for consumers. States should consider if the subsidies may have federal tax consequences for

consumers and whether the subsidies may lead to IRS reporting requirements for the state.

Implementation Approaches

In Option 1: Allow state financial assistance for non-QHPs, states would request to waive provisions

relating to the PTC under section 36B of the Code and section 1402 of the PPACA. In addition states

would receive a waiver of provisions related to QHPs, such as section 1311(d)(2)(B)(i) of PPACA, which

14

prohibits Exchanges from making available any health plan that is not a QHP. Due to the way the federal

Exchange platform operates, a state interested in this option would have to administer a state-specific

premium assistance program as described in Waiver Concept A: State-Specific Premium Assistance

waiver component if it wants to offer a subsidy to non-QHPs. Besides looking at the type of plans

offered, one other area for innovation is in cost sharing, which would likely require waiving the PPACA’s

metal level requirements in section 1301(a)(C)(ii).

Below is a discussion of how the state could implement the policy options, with a focus on plan design,

enrollment processing, and payment to issuers. All implementation approaches under Option 1 assume

that a state is also administering its own state-specific premium assistance program.

Plan design implementation approaches:

1) While meeting state innovation waiver guardrails, a state could choose how broadly or narrowly

to define eligibility for the subsidies that would apply to plans that do not meet the cost-sharing

or actuarial value (AV) level requirements. All or a select group of people or employers such as

small employers or consumers eligible for a different existing state tax credit (for example, state

EITC programs) could be offered subsidy eligibility. These changes could apply across the state’s

insurance market or to a select group via a new coverage level. States may refer to Waiver

Concept A: State-Specific Premium Assistance.

2) A state may also wish to support innovation in the benefits provided by plans. The 2019

Payment Notice provided substantially more options in what states can select as an EHB-

benchmark plan, starting for plan year 2020.

6

Enrollment implementation approaches:

1) One implementation option for states is to allow enrollment to occur directly with participating

issuers or web broker websites; similar to how small businesses enroll in FF-SHOP plans, how

individuals are currently enrolled when they purchase coverage off-Exchange, and the direct

enrollment process for consumers signing up for individual market coverage through Exchanges

that use HealthCare.gov. To activate subsidies, consumers would provide a voucher or other

proof of subsidy eligibility when enrolling. This may be more appropriate for states wishing to

keep the set of subsidy-eligible plans as broad as possible.

a. Note: Due to technical limitations and build constraints on the FFE system, this waiver

option may be feasible for implementation as early as OE8 (plan year 2021) and the

state’s plan and needed technical changes would need to be confirmed by CMS by

January of the prior plan year (i.e., January 2020 for implementation in plan year

2021). CMS will need detailed design elements to evaluate feasibility and provide

estimates on costs.

2) A second implementation option for states is to design a system where enrollment would occur

through a specific website separate from the HealthCare.gov website and back-end platform

used by the FFE. For example, states may consider developing their own portal. This could be

paired with the subsidy determination process and host the subsidy eligibility application to save

6

https://www.federalregister.gov/public-inspection/current

15

on administrative costs, and may be more appropriate for states wishing to restrict plan options

to a specific plan or set of plans.

a. Note: Due to technical limitations and build constraints on the FFE system, this waiver

option may be feasible for implementation as early as Open Enrollment (OE) 7 (plan

year 2020), but the state’s plan and needed technical changes would need to be

confirmed by CMS by the August prior to the start of the same plan year (i.e., August

2019 for implementation in plan year 2020).

In either implementation approach above, states would be responsible for communicating to issuers

and to individuals in the states information on what types of plans are eligible for the state subsidy. Part

of a state’s implementation plan should include how it will inform the public of the upcoming changes

for plan options. In this option, the Exchange call center would no longer be available for consumers to

enroll in or select a plan, so the state will want to consider whether or not to offer a similar type of

service.

The state would receive pass-through funding from the federal government to the extent that it waives

PTC under section 36B of the Code or waives another provision under section 1332(a)(2) that results in

savings of PTC. The state would determine a method for applying such funding to the state subsidy. The

state also would remain responsible for any costs in excess of the pass-through amount that are

necessary to implement its plan as described in the state’s approved application. Costs could exceed

expectations if the state lacks adequate controls on eligibility determinations, if the selection of plans

was wide enough to attract many new subsidy-eligible enrollees, or for other reasons.

Payment implementation approaches:

1) One implementation option for states is to aggregate payment to issuers to cover appropriate

levels of premium subsidy payment per enrollment.

2) A second implementation option for states is to make payment to individuals at the time of

subsidy eligibility determination, and direct the individuals to make payment to their

participating issuer (similar to an Electronic Benefit Transfer (EBT) card)

Administrative Expenses (Option 1: Allow state financial assistance for non-QHPs)

Because this change in plan options would require a state to concurrently waive the PTC and implement

a state-run eligibility program as outlined in the Waiver Concept A: State-Specific Premium Assistance,

states should review the waiver options for additional information on administrative expenses. Please

refer to the Overview of 1332 Waiver Concept for information on when states can receive pass-through

spending, and on administrative costs to the federal government associated with the waiver.

Option 2: Allow non-QHPs to be sold on the existing Exchange and/or expand the availability of

catastrophic plans (additional option to apply PTC to catastrophic plans and non-QHPs sold on the

existing Exchange)

Policy

States with FFEs or with State-based Exchanges that rely on the federal platform (SBE-FPs) that maintain

the basic tenets of PPACA QHPs may elect to make plan oversight changes that can provide additional

flexibility while maintaining the technical requirements to continue use of the HealthCare.gov platform.

16

Note that some flexibility in performing QHP certification reviews already exists for states that perform

plan management functions in FFEs, and additional flexibility is available for SBEs, so a waiver may not

be necessary for some changes. This option focuses on changes that may require a state innovation

waiver. Under this option, the state could waive the requirement in section 36B(c)(2)(A)(i) of the Code

that to be eligible for PTC, the taxpayer or a member of the taxpayer’s family must be enrolled in a QHP

through the Exchange for one or more months during the year. States should consider whether plans

offered under a waiver can conform to the data elements required for QHP templates when this option

would use HealthCare.gov. If a state waiver allows PTC for a non-QHP offered through the Exchange,

the state must ensure that the non-QHP provides Form 1095-A to individuals with all the same

information that QHPs provide now, and also provides Form 1095-A information to the IRS in the

manner that QHPs provide now. In addition, the non-QHP must perform certain eligibility activities to

ensure that consumers enrolling in the non-QHP coverage generally are eligible for PTC. This option

could potentially allow for multiple plan options for consumers.

Implementation Approaches (Option 2)

The second policy option would have a smaller impact on plan design, such that a state could maintain

the option to continue using HealthCare.gov and to continue to have the PTC available to their

population.

• In order to determine eligibility for PTC and calculate the amount of premium tax credit

available to consumers on the FFE, issuers must continue to submit traditional silver-level QHPs

for sale on the Exchange in order to calculate the state’s benchmark plan.

• A state may want to allow issuers to sell a plan without the plan having to meet all QHP

certification standards by waiving some or all of section 1311(c) of the PPACA, while still making

it available through HealthCare.gov. In these cases, technical feasibility may limit variation from

existing federal Exchange data structures. The state would need to collaborate with CMS early

in the process to assure that new plans conform to the data elements required for the QHP plan

templates. This option could be helpful for states that do not want to implement their own

subsidy structure.

• Regarding catastrophic plans, states could expand the availability of catastrophic plans beyond

the current eligibility limitations by waiving section 1302(e)(2) of the PPACA, for example, to

make them available to a broader group of individuals. Currently, catastrophic plans are

available only to individuals under the age of thirty, or to individuals who have qualified for an

Exchange affordability or hardship exemption. Catastrophic plans’ risk is adjusted separately

from other metal level plans. Waiving these limitations would expand plan options to more

individuals. However, wider enrollment in catastrophic plans is likely to lead to issuers

increasing their cost because it would change the risk profile of their enrollees.

• In addition to making non-QHP and expanded catastrophic plans available through the

Exchange, states should determine whether or not PTC (and APTC) could be applied to such

plans. Currently, individuals enrolling in catastrophic plans are not eligible for PTC. A state may

choose to waive this limitation and thereby make the plans more affordable, in addition to

allowing PTC to be applied to new non-QHP plans. Note that such an option may have an

impact on PTC spending and premiums which would be evaluated as part of the overall waiver

analysis.

17

The state would receive pass-through funding from the federal government to the extent that it waives

eligibility for PTC under section 36B of the Code or waives another provision under section 1332(a)(2)

that results in savings of PTC, for example if the waiver lowers premiums as a result of improving the risk

pool. The state would remain responsible for any costs in excess of the pass-through amount that are

necessary to implement its plan as described in the state’s application. Costs could exceed expectations

if the selection of plans was wide enough to attract many new subsidy-eligible enrollees, or for other

reasons.

Catastrophic or non-QHP plans offered on the Exchange for which PTC is allowable will need to provide

certain information to IRS and taxpayers about these plans on Form 1095-A. There would need to be

technical changes to allow APTC or PTC to apply to catastrophic or non-QHP plans on HealthCare.gov.

Note: Due to technical limitations and build constraints on the FFE system, this waiver option may be

feasible for implementation as early as Open Enrollment (OE) 7 (plan year 2020) for catastrophic plans

on the FFE, but the state’s plan and needed technical changes would need to be confirmed by CMS by

the January prior to the start of the same plan year (i.e., January 2019 for implementation in plan year

2020). We expect this would involve a moderate cost to the FFE for catastrophic plans, and may be a

higher cost depending on the type of non-QHPs offered on the Exchange. The state would be

responsible for funding the technical build to adjust the HealthCare.gov system for this purpose.

Administrative Expenses (Option 2)

Technical changes to the federal Exchange would be necessary in order to support changes to

catastrophic plan eligibility or the application of APTC to non-QHPs. States are encouraged to reach out

to the Departments with proposals early in the process, in order for cost estimates and feasible

technical timelines to be determined. Please refer to the Overview of 1332 Waiver Options for

information on when states can receive pass-through spending, and administrative costs to the federal

government associated with the waiver.

Things to consider and/or additional information on implementation approaches under Concept B

Options 1 and 2

Below are some questions to consider as the state develops these programs, and to include in the 1332

waiver application.

Questions for Concept B Option 1:

1) How will the state implement a new subsidy structure?

a. Which entity will administer the program? Is it a new or existing entity? To what extent

will the entity be subject to state insurance laws? To what extent will the entity

coordinate activities with other public programs (e.g., Medicaid and CHIP)?

b. How much funding is necessary for the subsidy structure?

c. What populations or eligibility requirements will the state have for this program (e.g.,

age, income, etc.?

d. What plan options will be available?

e. If state funding is required, how much funding does the state anticipate will be

necessary to implement the state plan and how will the state generate the required

state funding?

2) When and how will consumers be notified of their subsidy amount?

18

3) Will there be a process for consumers to report changes to eligibility criteria (i.e. income, age,

address etc.)?

4) What process will be used for consumers to appeal their eligibility determination and subsidy

amount?

5) What sources is the state using to verify eligibility for coverage and/or the subsidy (if

applicable)? Will the state be using their Medicaid/CHIP Agency or the FFE to do eligibility

verifications and determinations? Is the state using any state sources for verification?

6) How will issuers receive payments for the subsidy? What is the timing and mechanism for pay-

out?

7) Will the state reconcile state subsidy amounts based on actual or earned income? If so, how will

that be operationalized?

8) Will the new subsidy program includes incentives for providers, enrollees, and plan issuers to

continue managing health care costs and utilization and lower overall health care spending (if

any)?

9) Does the state have the authority/ability to adjust the program requirements on a yearly or

other basis to account for market changes? If so what is the schedule and process for this

adjustment?

10) Will the state require issuers to include the impact of the program in initial and/or final rates?

11) Is there any existing legislation and/or regulations related to the state program, or is new state

legislation and/or regulation needed?

12) If the state is leveraging the FFE’s system, does the state anticipate requesting any changes to

the FFE? If the state is leveraging the SBE, does the state anticipate requesting any changes to

the SBE? Related to question #2 above, does the state envision that applicants will be able to

see their subsidy amount during the plan selection process?

13) If implementing a state subsidy program what (if any) federal tax consequences will there be for

the individuals enrolled and/or reporting requirements for the state as a result?

14) How does the state plan to ensure access to health insurance that is at least as comprehensive

and affordable as would be provided under the PPACA as compared to without the waiver?

15) How will a state monitor affordability and coverage for new plans offered that may have

different cost sharing, annual and lifetime limits, and may not have reporting requirements

equal to comprehensive coverage?

19

Questions for Concept B Option 2:

1) Which non-QHPs will be newly available on or off-Exchange?

a. What is the eligibility criteria for these plans and how does it differ from QHPs? Are they

eligible for PTC and if so, are they also eligible for APTC?

b. What is the duration of these plans and how does it differ from QHPs?

c. Will the plans be available only during an open enrollment period, or will they also offer

special enrollment periods?

d. What additional information will need to be collected from consumers in order to

determine their eligibility for these plans?

e. Are there enrollment caps under these plans?

f. Do these new plans meet state licensing requirements?

2) How will consumers be able to identify the non-QHP plans?

a. Will they need to be displayed differently?

b. Is there new or additional information about these plans that will need to be available?

How will consumers learn how these plans differ from QHPs?

3) Will the state provide supplemental information about these plans?

4) If expanding eligibility for catastrophic plans, what new population will be newly eligible for

these plans?

5) Is the state leveraging the federal system? In what ways does this program require changes to

the FFE?

a. Changes to application questions? (not possible at this time)

b. Changes to plan display? (not possible at this time)

c. Changes to information elsewhere on HealthCare.gov (outside of the application)?

d. Changes to APTC eligibility or calculation?

e. Changes to plan enrollment, i.e. enrollment caps?

6) If PTC is made available for non-QHPs on the Exchange, how will the state ensure that the non-

QHP or the Exchange (1) provides Form 1095-A to consumers and the IRS, and (2) screens

consumers for PTC eligibility during the enrollment process (for example, verifying lawful

presence; determining eligibility for other minimum essential coverage, including Medicaid; and

determining affordability of any employer coverage, etc. for all family members enrolling in the

plan)?

20

Waiver Concept C: Account-Based Subsidies

In the Waiver Concept C: Account-Based Subsidies waiver option, states would have the flexibility to

direct public subsidies into a defined-contribution, consumer-directed account that an individual uses to

pay health insurance premiums or other health care expenses. The account could be primarily funded

with pass-through funding made available by waiving the PTC (section 36B of the Code and section 1401

of the PPACA) or the SBTC (section 45R of the Code), along with any additional state funds to implement

the 1332 waiver plan. The account could also allow individuals to aggregate funding from additional

sources, including individual and employer contributions. An account-based approach, depending on

how the state designs the program, could give beneficiaries more choices, improve incentives to make

cost-conscious health care spending decisions through the responsibility for managing a health care

budget, and better enable them to maintain health coverage regardless of changes in income or other

life circumstances. This approach could also allow a consumer greater ability to select a plan based on

the individual’s or their family’s needs, including a higher deductible plan with lower premiums.

States will need to create their own subsidy structure, consider which plan options will be offered, and

how to aggregate funding from various sources. More specifically, in the Waiver Concept A: State-

Specific Premium Assistance waiver option, states could have the flexibility to design a new subsidy

structure to target public assistance to better help the vulnerable and to expand the risk pool. In the

Waiver Concept B: Adjusted Plan Options waiver concept, states could change the types of plans that are

eligible for premium subsidies to make coverage more affordable for individuals and to increase

consumer choice. The type of subsidy and types of plans would depend on the state plan. Depending

on how the health expense account is structured it may have tax implications for the individual or

states.

As a reminder, a state must ensure that the waiver meets the four statutory guardrails of affordability,

comprehensiveness, coverage, and federal deficit neutrality and any other requirements of the

Departments. As discussed in the 2018 guidance and principles, the state should also address in the

application for the section 1332 waiver how the section 1332 state plan addresses the Administration’s

priority to support and empower those people with low incomes as well as those people with high

expected health care costs. In particular, this model could be structured in a variety of ways that may

have diverging impacts on individual market coverage and affordability. For example, there may be

scenarios where even though a state provides subsidies to an account on behalf of a consumer, the

consumer’s overall cost for premiums and out of pocket health care spending would increase. The

state’s waiver plan should take into account how the plan will meet the affordability guardrail.

Health Expense Account

Policy

Similar to Waiver Concept A: State-Specific Premium Assistance, in the Account-Based Subsidies waiver

concept, states would have the flexibility to design a new subsidy structure to, for instance, make

coverage more affordable for a wider range of individuals and to attract more young and healthy

consumers into their market. One option is to use subsidies as a contribution towards funding a

defined-contribution, consumer-directed Health Expense Account (HEA). This would be a new type of

account a state could create where consumers could use an HEA to pay health insurance premiums and

other health care expenses. An HEA promotes a number of important policy goals. Giving the

21

beneficiary ownership and control over a health care budget creates better incentives for them to

obtain higher value from their spending decisions. An HEA could potentially also help people maintain

continuous coverage and reduce churn in and out of health programs because under the plan a

consumer could maintain private coverage.

An HEA establishes a personal health care budget for beneficiaries to manage. A state could consider

whether the HEA would need to first be used to pay premiums to guarantee the beneficiary maintained

health coverage. States would need to consider if and how any money left over in the account could be

used on a yearly basis. For example, such funds could:

• Stay with the individual to be used to pay other health care expenses incurred during the year or

saved to pay for future health care expenses for that plan year or future plan years.

• Be split between who contributed to the account (for example the state and the individual) for

eligible health care expenses.

• Be directed to wellness programs.

• Be directed to programs that support personal health (i.e. smoking cessation programs)

The structure of the subsidy could also be tailored to accomplish the same policy goals as Waiver

Concept A: State-Specific Premium Assistance, including making coverage more affordable for a wider

range of individuals. Like state-specific premium assistance, a state can adjust contributions to redefine

eligibility parameters to accomplish specific goals and reach specific populations. For example:

• A state may provide a flat, per-member per-month contribution to the account based on age.

• A state may provide a sliding scale per-member per-month credit based on income and other

eligibility factors.

• A state can structure the contribution on a sliding scale to those over 400% of the federal

poverty level (FPL) or under 100% FPL to reduce or eliminate the current subsidy cliffs.

(See Waiver Concept A: State-Specific Premium Assistance for additional subsidy structure ideas.)

A state may choose to provide an additional state contribution towards the state subsidy program than

what is provided by waiving section 36B of the Code to increase the generosity of the subsidy. A state

might also allow employers to contribute to the account.

Implementation Approaches

In the HEA option, states could request to waive federal laws relating to PTC (section 36B of the Code

and section 1402 of the PPACA) to establish a new subsidy program and also fund HEAs.

States could continue using the current Exchange enrollment platform and plan certification, create a

new platform, or waive the PPACA’s Exchange and QHP provisions and rely entirely on the private

market. If a state chooses to waive the PPACA’s provisions related to Exchanges (section 1311) and

QHPs (section 1301), the implementation could be similar to the implementation approach for Waiver

Concept B: Adjusted Plan Options, Option 1, which allows state-specific financial assistance to be applied

to non-QHPs. This has the potential for consumers to use the account to purchase a wider variety of

plans.

22

Another approach is for a state to leverage the existing FFE in the state. States would need to work with

the FFE and effectively “turn off” the financial assistance component of the FFE for the state. In this

option, states would cover costs incurred for the technical build to adjust the HealthCare.gov website

and backend system and changes to consumer support channels (including the call center, messaging,

etc.). This option would be similar to the Waiver Concept A: State-Specific Premium Assistance as

outlined above.

In establishing HEAs, states will need to consider a number of design elements and issues, including:

• Contribution Amount: A state will need to establish a framework for setting the contribution

amount. For instance, the contribution amount could be a flat amount by age and family size or

scaled for income or a percentage of the premium for a benchmark plan.

o A state could set up a matching program where the HEA contribution would match a

portion of contributions from an individual and/or employer.

o A state could couple the account with a wellness program. Consumers could earn

contributions towards their account by participating or meeting certain requirements

outlined in the wellness program.

• Restrictions on the Use of Funds: While a state generally could allow the funds to pay for health

plans and health expenses, a state may want to restrict what the HEA can reimburse. For

instance, a state may want to limit an HEA to paying for plans with an actuarial value that

minimizes out-of-pocket exposure or health expenses that go toward reaching out-of-pocket

spending limits; or a state may choose to limit the HEA to premium payments, a new standard,

or another existing standard like section 213(d) of the Internal Revenue Code.

• Family Account Structure: Having multiple family members under a single account generally

makes it easier to administer for both the state and the family. However, a single account

approach requires procedures for removing family members from the account under certain

circumstances, such as a divorce or a child aging out of the plan. To avoid issues with removing

family members from the account, a state may opt for an approach that provides an individual

account for each family member. Or a state may consider an approach where all dollars remain

with the family in one account.

• Account Administrator: States would be responsible for setting up and administering these

accounts. A state could establish each HEA as a trust administered by a private financial

institution on behalf of the beneficiary or the state itself could hold and administer the HEA.

• HEA Savings: States would need to consider if and how an enrollee can use savings built up

within the HEA, including what will happen with any money left over after the plan year. For

example any money left over in the account (or a portion) could be used as a funding source to

implement part of the state’s waiver plan for healthcare coverage or services as defined in the

Specific Terms and Conditions (STCs) for the period of the waiver

7

:

o Go back to the state to use towards the state waiver plan (this option would have less of

an impact on consumer behavior).

o Stay with the individual irrespective of whether they were still in the individual market

to be used to pay other health care expenses incurred during the month or saved to pay

for future health care expenses for that plan year or future plan years.

7

Note funds remaining at the end of a waiver will be returned to Treasury consistent with the STCs.

23

o Be split between the state and the individual for health related expenses and/or the

state waiver plan.

o Be directed to wellness programs.

o Be directed to programs that support personal health (i.e. smoking cessation programs)

• Tax Implications: States should consider what (if any) federal tax consequences there will be for

the individual and/or reporting requirements for the state as a result of establishing an HEA.

Administrative Expenses

States may use pass-through funding associated with waiving section 36B of the Code for the Account-

Based Subsidies waiver option to implement the state plan and help partially fund the state account-

based subsidy program. In place of the PTC, states could receive federal pass-through funding in the

amount individuals would have otherwise received in PTC. States would use this federal funding to

contribute to the HEAs based on rules established by the state and consistent with Federal law.

As a reminder, a state must ensure that the waiver meets the four statutory guardrails of affordability,

comprehensiveness, coverage, and federal deficit neutrality. Any additional costs to fund the account-

based subsidy program would be the state’s responsibility.

Please refer to the Overview of 1332 Waiver Concept for information on when states can receive pass-

through spending, and administrative costs to the federal government associated with the waiver.

Things to Consider and/or additional information on implementation approaches under Option 1

Below are some questions to consider as the state develops these programs, and to include in the 1332

waiver application.

Questions for Concept A Option 1 that are applicable for Concept C:

1) How will the state implement a new subsidy structure?

a. Which entity will administer the program? Is it a new or existing entity? To what extent

will the entity be subject to state insurance laws? To what extent will the entity

coordinate activities with other public programs (e.g., Medicaid and CHIP)?

b. How much funding is necessary for the subsidy structure?

c. What populations or eligibility requirements will the state have for this program (e.g.,

age, income, etc.?

d. What plan options will be available?

e. If state funding is required, how much funding does the state anticipate will be

necessary to implement the state plan and how will the state generate the required

state funding?

2) When and how will consumers be notified of their subsidy amount?

3) Will there be a process for consumers to report changes to eligibility criteria (i.e. income, age,

address etc.)?

4) What process will be used for consumers to appeal their eligibility determination and subsidy

amount?

5) What sources is the state using to verify eligibility for coverage and/or the subsidy (if

applicable)? Will the state be using its Medicaid/CHIP Agency or the FFE to do eligibility

verifications and determinations? Is the state using any state sources for verification?

24

6) How will issuers receive payments for the subsidy (i.e. is the individual responsible for paying

the issuer directly with savings from their HEA?)? What is the timing and mechanism for pay-

out?

7) Will the state reconcile state subsidy amounts based on actual or earned income? If so, how will

that be operationalized?

8) Will the new subsidy program includes incentives for providers, enrollees, and plan issuers to

continue managing health care costs and utilization and lower overall health care spending (if

any)?

9) Does the state have the authority/ability to adjust the program requirements on a yearly or

other basis to account for market changes? If so what is the schedule and process for this?

10) Will the state require issuers to include the impact of the program in initial and/or final rates?

11) Is there any existing legislation and/or regulations related to the state program, or is new state

legislation and/or regulation needed?

12) If the state is leveraging the FFE’s system, does the state anticipate requesting any changes to

the FFE? If the state is leveraging the SBE, what operational changes does it intend to make?

Related to question #2 above, does the state envision that applicants will be able to see their

subsidy amount during the plan selection process?

13) If implementing an HEA what (if any) federal tax consequences will there be for the individuals

enrolled and/or reporting requirements for the state as a result?

14) How does the state plan to ensure access to health insurance that is at least as comprehensive

and affordable as would be provided under the PPACA as compared to without the waiver?

Questions for Concept C Option 1 specific to the Account-Based Subsidies Option:

1) Would an individual be allowed to withdraw any portion of his or her contributions at the end of

the year?

2) What entity owns the account and/or administers the account as part of the state’s plan?

3) What expenses can the account be used for?

4) What protections will be in place to protect program integrity and reduce improper payments?

5) What entities can contribute to the account?

6) How will the state treat any savings remaining in the account at the end of the year? Will the

savings be rolled over to the next year and how can the consumer use them?

7) What are the eligibility requirements for an individual to access the account?

a. Are they for certain types of plans?

b. Would a person be required to enroll in coverage in order to receive the contribution? If

so, what would be the requirements on the coverage?

c. What happens if the individual or a family member becomes eligible for Medicaid or

CHIP during the year? Could he or she use the savings in the account to pay for any cost

sharing that Medicaid/CHIP require?

8) Does the state plan to have a single account for a family or individual account for each family

member?

9) What is the structure for the contribution amount? Is there a match and/or other requirements?

10) Can employers contribute to the account?

25

Waiver Concept D: Risk Stabilization Strategies

In the risk stabilization strategies waiver component, states can consider ways to address the costs of

individuals with expensive medical conditions to mitigate the impact of those expenses on people who

purchase coverage in the individual market. For example, states can implement a state-operated

reinsurance program or high-risk pool by waiving the single risk pool under 1312(c)(1) of the PPACA and

can be coupled with the other waiver idea options discussed. Reinsurance programs have lowered

premiums for consumers, improved market stability, and increased consumer choice. Some states have

chosen to use a claims cost-based model (OR, MN, WI), a conditions-based model (AK), or a hybrid

conditions and claims cost-based model (ME) for their reinsurance program. This paper includes

examples of state approaches to date, but states are encouraged to think creatively about what model

makes the most sense for their state. If the state shows an expected reduction in federal spending on

PTC, the state will receive federal pass-through funding to help partially fund the state’s high-risk

pool/reinsurance program.

Policy Options to Design a Risk Stabilization Program

Option 1: Implement a Reinsurance Program

Policy

Reinsurance programs compensate insurers for people with significant medical expenditures during a

year, lowering premiums in the individual market (both in and outside the Exchange). Reinsurance

payments are based on actual costs, so along with high-risk individuals it also helps mitigate insurer

losses for low-risk individuals who may have unexpectedly high costs (such as costs incurred due to an

accident or sudden onset of an illness). Under reinsurance, some plans may receive payments for high-

cost enrollees and below we discuss three choices for states to design reinsurance programs. As a

reminder to states, the risk adjustment high-cost risk pool has been effective since plan year 2018 and

will reimburse 60% of claims above $1 million, with no cap. This risk adjustment high-cost risk pool

program will work in conjunction with state reinsurance programs to provide relief from catastrophic

claims costs so states should take this into consideration as they establish parameters for their

reinsurance program so the state-operated reinsurance program does not duplicate claims covered

under the risk adjustment high-cost risk pool.

Choice 1 - Claims cost-based reinsurance program: One option for states is a claims cost-based

reinsurance program where issuers are reimbursed for a portion of the costs of enrollees whose

claims exceed a certain threshold (i.e. the attachment point). Typically, issuers are reimbursed

for only a portion of costs (i.e., the coinsurance rate) above the attachment point, and in some

cases, up to a set cap. High-cost individuals remain in the same risk pool as other enrollees (for

both claims cost-based reinsurance programs and conditions-based reinsurance programs) and

enroll in the same commercial plans available to the general public. Claims are eligible for

payment through a reinsurance program using funds separately raised for that purpose when

certain criteria are met. A few state examples of this option are outlined below in Table 1.

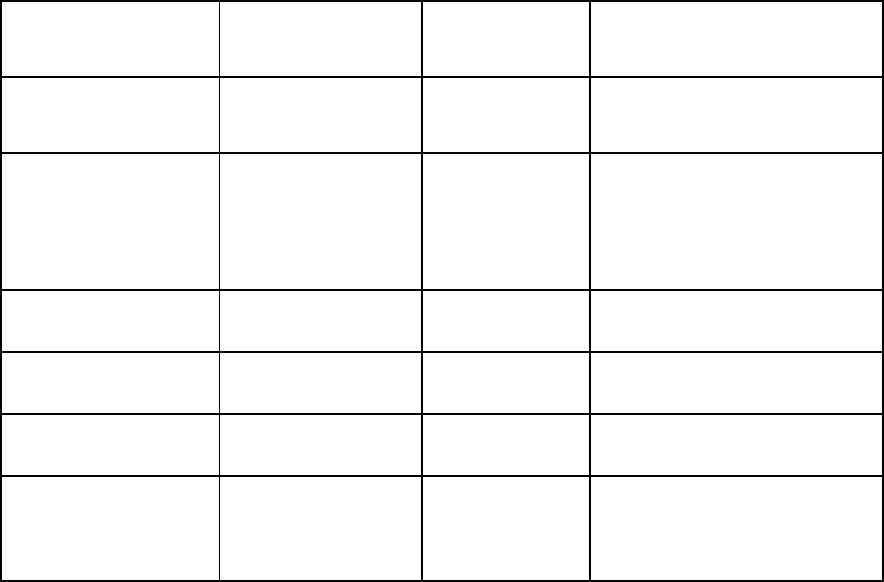

Table 1: Examples of reinsurance programs using the claims-cost based option:

26

Program Attachment Point

Coinsurance

Rate Cap

Minnesota

$50,000

(2018/2019)

80%

(2018/2019)

$250,000 (2018/2019)

Oregon

$95,000 (2018)

$90,000 (2019)

50%

(2018/2019)