Working Together for Mutual Benefit:

Non-Recourse Receivables Purchase and

Trade Receivables Securitization

October 21, 2020

Merryn Craske

Partner, London

+44 20 3130 3029

Alex Dell

J. Bradley Keck

Partner, London

+44 20 3130 3121

adell@mayerbrown.com

Partner, Chicago

+1 312 701 7240

jkeck@mayerbrown.com

Massimo Capretta

Partner, Chicago and New York

+1 312 701 8152 (Chicago)

+1 212 5-6 2632 (New York)

2

Who Are We?

• Global Receivables and Supply Chain Finance Team

– Over 50 professionals across our platform focused on receivables and supply

chain finance

– Coverage across our firm including the US, the UK, France, Germany, Hong

Kong, Singapore, Brazil and Mexico

– We are a go-to law firm for a number of the world’s leading participants in

the supply chain finance and trade receivables finance markets.

3

Welcome To Our Webinar Series!

• Supply Chain and Working Capital Finance Webinars

– 9 webinars from July to November (repeated twice daily)

• Upcoming Programs:

– October 28 – Credit Insurance –– How Does It Actually Work in Supply Chain

Finance?

– November 4 - The UN Convention on the Assignment of Receivables – What

Is It, and How Will It Change Trade Finance?

• We will have our normal live programs in New York, London, Singapore

and Hong Kong in 2021 – circumstances permitting.

4

Supply Chain and Distribution Offering

• Mayer Brown is the only law firm with an end-to-end supply chain and

distribution offering including:

Finance (Receivables, Payables, Other Financial Assets, Inventory)

Tax

Customs and Trade

Technology Transactions and IP

Cash Management

Litigation / Enforcement

Regulation

5

Today’s Speakers

M a s s i m o C a p r e t t a

Partner, Chicago and New York

T: +1 312 701 8152 (Chicago)

T: +1 212 5-6 2632 (New York)

E: mcaprett[email protected]

A l e x D e l l

Partner, London

T: +44 20 3130 3121

E: adell@mayerbrown.com

M e r r y n C r a s k e

Partner, London

T: +44 20 3130 3029

E: mcrask[email protected]

J . B r a d l e y K e c k

Partner, Chicago

T: +1 312 701 7240

E: jkeck@mayerbrown.com

6

Trade receivables securitization

• Traditionally used for investment grade companies but increasingly

seen as an important tool in the wider receivables financing arena

– Can be structured as off-balance sheet - improves balance sheet debt to equity

ratios

– May accelerate cash from operating activities

– Diversify funding sources

• Useful product to finance:

– cross border receivables originated in multiple jurisdictions – cross-collateralisation

provides greater financing availability against the assets

– large pools efficiently (subject to concentration limits)

7

Trade receivables securitization - SPV

• Concentration of receivables in a single insolvency-remote special purpose

vehicle (SPV) mitigates exposure to multiple legal and insolvency regimes

• SPV either established as a new group company (typical in the U.S.) or “orphan”

company (typical in Europe - shares held in charitable trust) in jurisdictions with

tax neutrality and legal ring-fencing

• Insolvency remoteness afforded by limited constitutional powers and/or

contractual restrictions (purchase of receivables and obtaining financing only)

and independent directors

• Profit extraction – servicing fee, deferred purchase price and/or interest payable

on subordinated loans

• Tax/regulatory considerations on choice of SPV location and method of sale

8

Trade receivables securitization - Documents

• Core documents include:

– Receivables Loan Agreement or Notes (funding the SPV’s purchase of receivables)

– Receivables Purchase Agreements (under which the SPV purchases the receivables)

– Servicing Agreement

– Performance and Indemnity Deed

– Bank Account Security and Account Control Agreements (to secure cashflows)

9

Trade receivables securitization

– Key points to consider

• True sale formalities in each country where receivables are originated

• Anti-assignment provisions need legal diligence

• Any conflicts or collateral overlaps with existing secured credit facilities

• Cash management and servicing – commingling, sweeps, security

• Perfection requirements specific to each country

10

EU Securitization Regulation

• EU Securitisation Regulation applies to securitisations that issue new

securities or create new securitisation positions from 1 January 2019

• Is it a “securitisation”?

– Transaction or scheme where the credit risk of an exposure/pool of exposures is

tranched

– Payments are dependent on the performance of the exposure/pool of exposures

– Subordination of tranches determines distribution of losses through life of

transaction or scheme

• Obligations relating to due diligence, risk retention and transparency

11

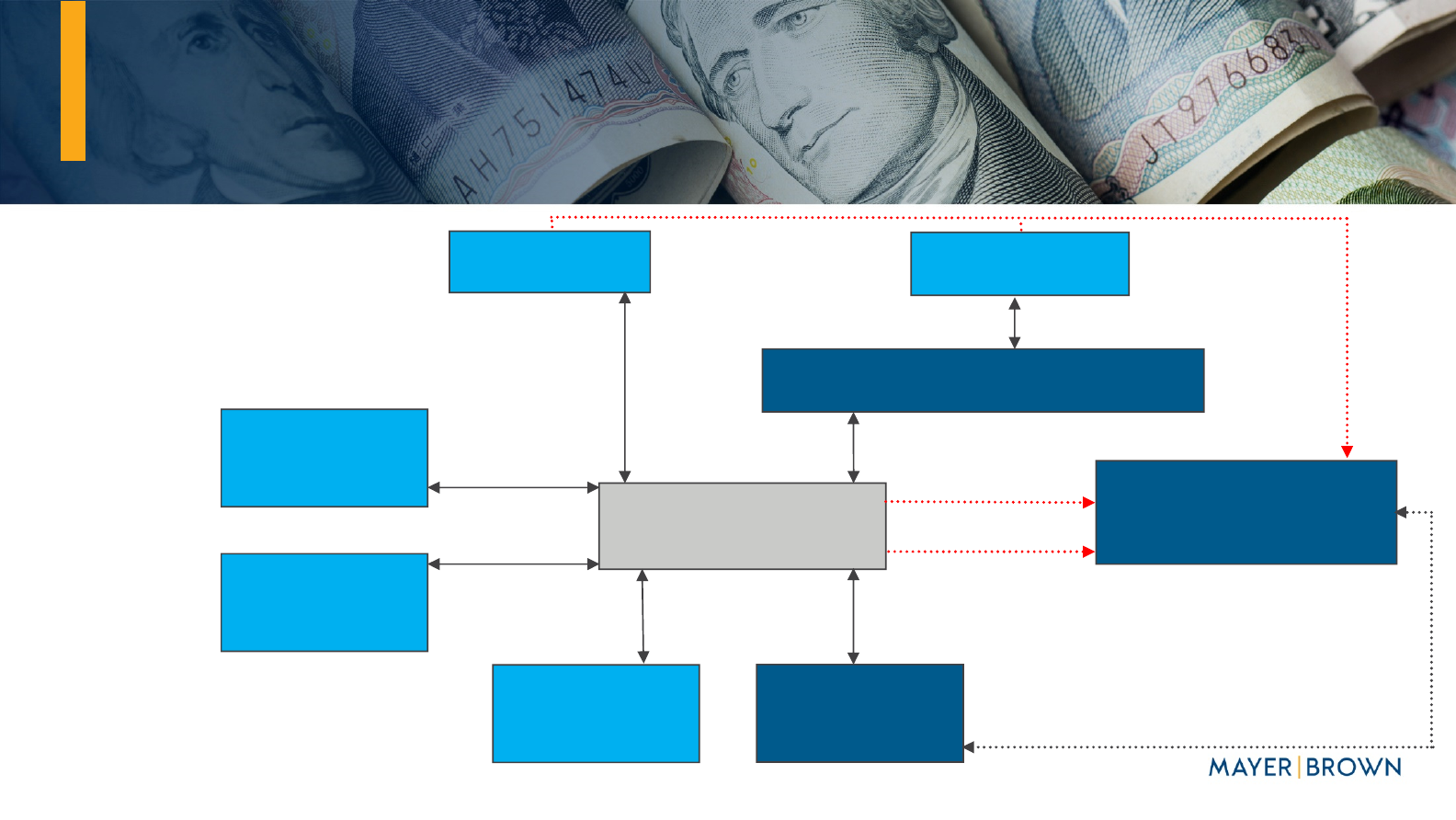

Typical multi-country securitization structure

SPV

SELLER

SELLER

INTERMEDIATE PURCHASER

SUBORDINATED

LENDER

SENIOR LENDERS/

NOTEHOLDERS

PERFORMANCE

UNDERTAKING

PROVIDER

SERVICER

Servicing

Agreement

Performance

Undertaking &

Indemnity Deed

Receivables Purchase

Agreement

Receivables Purchase

Agreement

Receivables Loan

Agreement/Notes

Subordinated Loan

Agreement

Intermediate Transfer

Agreement

ADMINISTRATIVE AGENT/

SECURITY TRUSTEE

Security Agreement

Local law security

over collection

accounts

Local law security over

SPV accounts

Agent for

the Lenders

12

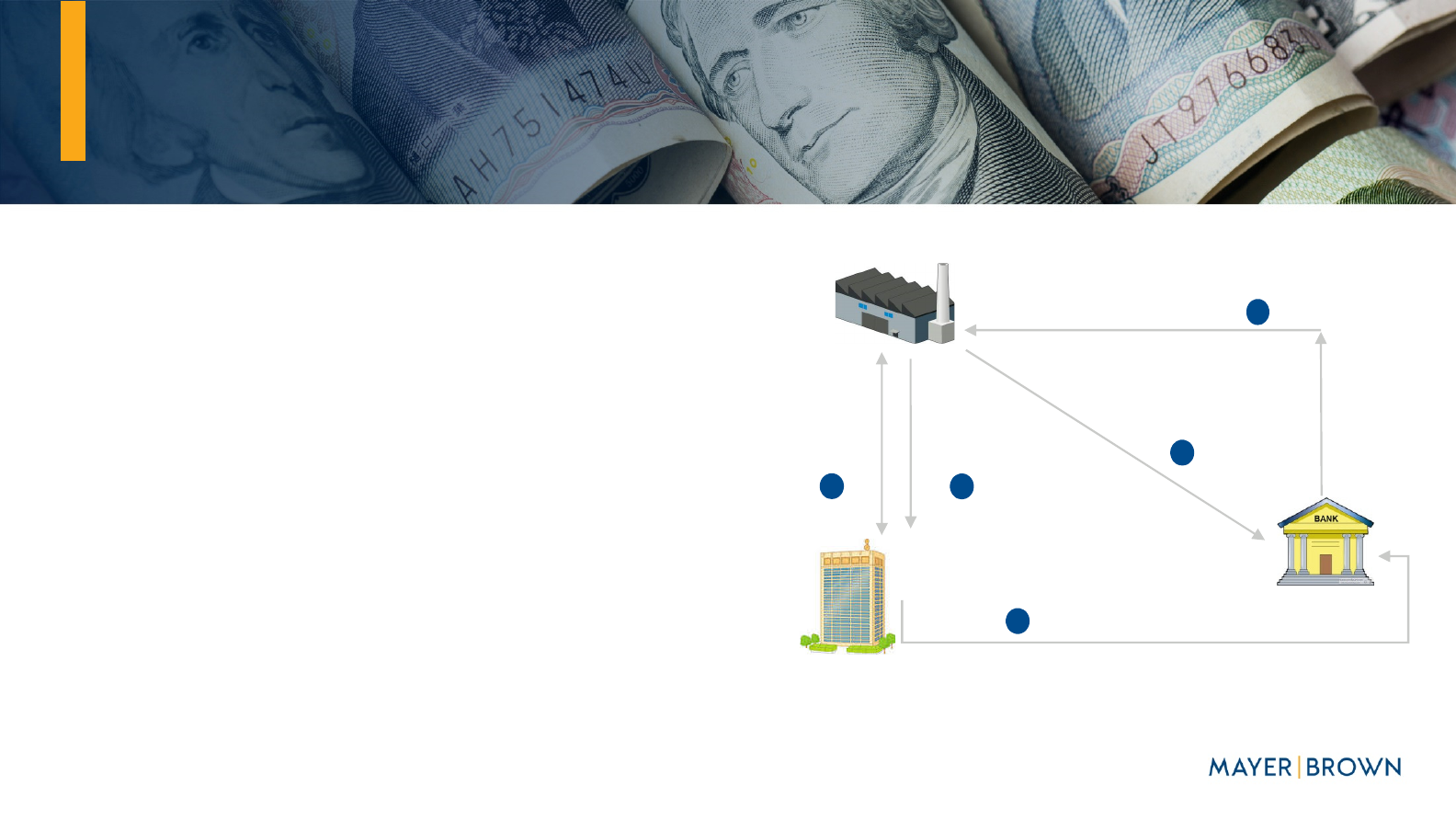

Non-Recourse Receivables Purchase

(NON-RECOURSE FACTORING)

Transaction Flow:

1. Buyer purchasing department purchases

goods or services from a Supplier under

a standard purchase contract

2. Supplier ships goods and sends invoice

to Buyer

3. Supplier sends the bank a purchase

request

4. The bank purchases the receivable in a

“true sale” and sends the Supplier

discounted proceeds of receivable

5. The Buyer pays the receivable on its

maturity date as instructed by Supplier

Discounted Proceeds / Sale of Receivable to Bank

Payment at Maturity

Shipment and

Invoicing

5

1

2

3

Purchase

Request

4

Commercial

Contract

13

Key Differences To Securitization

• Typically “off-balance sheet”.

– The receivables financed are removed from the balance sheet of the

Supplier, cash from operations generated.

– Much easier to create an off-balance sheet result than under a trade

receivables securitization (although somewhat less flexible).

• The funder is taking the credit risk on the obligors/Buyers on the actual

receivables, not on the Supplier/originator

– Diversification is not particularly helpful.

• Typically uncommitted facilities or, if committed, commitments will often run

only 30/60/90 days.

• Concepts like acceleration don’t exist.

14

Receivables Purchase Arrangements

• Trade Receivables Securitization

• Factoring

• Invoice Discounting

• Supply Chain programs

• Vendor finance

• Dealer floorplanning

• Asset based lending

• Fintech Platforms

15

Common Features

• Assignability

• Cash Management

• Balance Sheet Treatment

• Customer tolerance for complexity

• Global businesses

• Trade credit insurance

• Legal true sale opinions

16

Why One and not the Other?

• Which team

• Internal structure

• Seller/Issuer experience

• Seller/Issuer preference

• Risk Retention

• Revolving requirements

• Working capital or balance sheet management

17

Where the two roads meet

• Common methods of combining securitization with other methods include:

– Selling, participating or financing individual or groups of

overconcentration in a separate agreement with SPV – “out the side”

– Selling, participating or financing individual or groups of over

concentrations before they are sold to the SPV – “from the bottom”

– Single bank or fund funding whole pool and participating or selling

certain overconcentrations or exposures to third parties

– Providing a separate facility to the SPV to finance some or all of the

expected residual cash flows (including overconcentrations)

– Financing, including secured loans or repurchase facilities, related to the

SPVs equity (held by an affiliate)

Questions?

18

19

Appendix - Upcoming webinars

• 22 July: 10 Most Common Insolvency Questions in Receivables and Payables Finance – A Focus on US

• 29 July: 10 Most Common Insolvency Questions in Receivables and Payables Finance – A Focus on Asia and Europe

• August 12: Capital Markets/Alternative Investors; Investing in the Trade Receivable Asset Class

• August 19: 5 Most Common Questions About Financing Receivables and Payables Through a Platform

• September 2: 5 Most Common Questions About Financing Foreign Receivables; Issues Beyond Simple Perfection, Priority and

Enforcement

• September 16: Supply Chain Finance Using Drafts and Bills of Exchange

• October 21: Working Together for Mutual Benefit: Non-Recourse Receivables Purchase and Trade Receivables Securitization

• October 28: Credit Insurance – How Does It Actually Work in Supply Chain Finance?

• November 4: The UN Convention on the Assignment of Receivables – What Is It, and How Will It Change Trade Finance?

Recordings of previous programs can be found here: Global Receivables & Supply Chain Finance Webinar Series

20

Presenter Bios

Massimo Capretta | Partner, Chicago and New York | mc[email protected]

Massimo Capretta is a partner in Mayer Brown’s Chicago and New York offices and a member of the Global Banking & Finance practice. Massimo

helps lead the Firm’s Global Receivables and Supply Chain Finance Group. Massimo's transactional practice focuses on representing both financial

institutions and companies across a broad spectrum of domestic and international financing transactions. He has been involved in transactions

spanning a number of key industries including technology, life sciences, automotive, heavy manufacturing, chemicals, metals and energy. Massimo

has particular experience with domestic and cross-border trade receivables securitization, asset-based finance, structured inventory finance, factoring,

participations, supply chain/vendor finance, trade finance and other receivables monetization strategies platforms. He regularly advises clients on the

creation and management of bespoke receivables finance transactions.

Alex Dell | Partner, London | adell@mayerbrown.com

Merryn Craske | Partner, London | [email protected]

Merryn Craske is a partner in Mayer Brown’s London office, focusing on financial assets, securitization and structured finance transactions. She has

extensive experience of advising banks, originators and others on securitization and structured finance transactions in a range of asset classes

including trade receivables, dealer floorplan, auto loans and leases, residential mortgages, commercial mortgages, consumer loans and insurance

premium loans. She regularly assists clients with structuring and documenting multi-jurisdictional securitizations, working closely with local counsel to

provide solution-focused advice with respect to transactions in the United Kingdom and across Europe, the United States, Canada, Asia and elsewhere.

Alex Dell is head of the Banking & Finance group of the London office, as well as co-chair of the firm’s asset based lending (ABL) practice. He is focused

on multi-jurisdictional receivables financing programs and ABL transactions. Alex advises on a range of true sale issues as well as borrowing base

techniques, both from a lender and borrower perspective. He also has an in-depth knowledge of off balance sheet considerations, payables finance,

fintech platforms, bill discounting and floorplanning. Alex represents banks, credit funds, sponsors and corporates including some of the world’s largest

financial institutions and companies. He is widely-recognized as a leading ABL and receivables financing lawyer in the UK. Prior to joining Mayer Brown

in 2015, Alex led the Structured Trade & Receivables Finance team with another leading international law firm.

21

Presenter Bios

J. Bradley Keck | Partner, Chicago | [email protected]

J. Bradley Keck ("Brad") is a partner in Mayer Brown’s Chicago office and global co-lead of the Global Banking & Finance practice. He

concentrates his practice on private securitizations, financial asset sales, other structured finance and global receivables as well as payables

transactions. He has worked with a full array of market participants in a wide variety of transactions, including structuring and maintaining

ABCP conduits, private securitizations, whole-loan sales and participations. He has a deep knowledge of, and experience with, trade

receivables; IP, franchise and “whole-business” assets; inventory; auto paper (retail and wholesale); leases; loans and various other financial

assets.

22

Disclaimer

• These materials are provided by Mayer Brown and reflect information

as of the date of presentation.

• The contents are intended to provide a general guide to the subject

matter only and should not be treated as a substitute for specific

advice concerning individual situations.

• You may not copy or modify the materials or use them for any purpose

without our express prior written permission.

Mayer Brown is a global services provider comprising associated legal practices that are separate entities, including Mayer Brown LLP (Illinois, USA), Mayer Brown International LLP (England), Mayer Brown (a Hong Kong partnership) and Tauil & Chequer Advogados (a Brazilian law partnership) (collectively the “Mayer Brown

Practices”) and non-legal service providers, which provide consultancy services (the “Mayer Brown Consultancies”). The Mayer Brown Practices and Mayer Brown Consultancies are established in various jurisdictions and may be a legal person or a partnership. Details of the individual Mayer Brown Practices and Mayer

Brown Consultancies can be found in the Legal Notices section of our website. “Mayer Brown” and the Mayer Brown logo are the trademarks of Mayer Brown. © Mayer Brown. All rights reserved.

mayerbrown.comAmericas | Asia | Europe | Middle East