Soft Information in the Financial Press and Analysts’ Recommendation Revisions

Mark T. Bradshaw

a

, Xue Wang

b

and Dexin Zhou

c

a

Carroll School of Management, Boston College

b

Fisher College of Business, The Ohio State University

c

Zicklin School of Business, Baruch College, CUNY

January 2019

Abstract

Prior research establishes that both sell-side analysts and the media act as information intermediaries in

the

capital markets, providing investors with value-relevant pricing information. This study investigates

the association between sell-side analyst recommendations and information from firm-specific print

news coverage. We document descriptive evidence that the quantity of news coverage of a firm is

positively associated with subsequent recommendation revisions, and the tone of the news coverage is,

on average, consistent with the direction of the revisions. Our primary empirical prediction is that soft

information in news coverage is more significant than hard information for informative recommendation

revisions. Indeed, the association between firm news coverage and market reactions to analysts’

recommendation revisions is mostly explained by soft news in news coverage. Taken together, our paper

is the first to document the association between news coverage of firms and analysts’ assimilation of

that news as part of their mosaic of information and their role in the efficiency of capital markets.

Key words: Media, analysts, stock recommendations, tone, soft and hard news

JEL Codes: G

12, G14, G24

We appreciate helpful comments from Beth Blankespoor, Andy Call, Clifton Green, Narasimhan Jegadeesh, Lian Fen Lee, Mark Soliman,

Ben Whipple, as well as workshop participants at Cass Business School, Drexel University, George Mason University, Georgetown

University, Harvard Business School, Iowa State University, Northwestern University, Shanghai Advanced Institute of Finance, University

of Illinois at Chicago, University of Washington, the Wharton School and the FARS Midyear Meeting and University of Utah Winter

Accounting Conference. We thank Danyang Jiang for excellent research assistance, and our respective schools for generous research support.

This paper was previously titled, “Analysts’ assimilation of soft information in the financial press.”

Soft Information in the Financial Press and Analysts’ Recommendation Revisions

1. Introduction

Sell-side analysts are a primary information intermediary in the capital markets (Womack 1996,

Je

gadeesh et al. 2004, Ramnath, Rock and Shane 2008). A growing body of research investigates the

media as another information intermediary. Beginning with studies like Miller (2006) and Tetlock (2007),

finance and accounting researchers have become keenly interested in the direct role the media plays in the

flow of information within capital markets.

1

Bushee et al. (2010) conclude that the media serves as an

information intermediary, which they define as “an agent that provides information that is new and useful

to other parties” (pp. 1-2). In this study, we examine whether sell-side analysts generate more useful

recommendations by assimilating information in the financial press, especially soft information.

2

We

expect that the relation between these two information intermediaries is symbiotic, but there is limited

research that examines the joint roles of the media and analysts in providing new and useful information

to investors.

Analysts extensively use numerous information triggers, such as market prices, financial

information and management disclosures.

3

As a practical example, Regulation Fair Disclosure presumes

that analysts rely on multiple sources and types of information, claiming “Analysts can provide a valuable

1

There are many finance and accounting studies on the role of the press, which precede the dates of these studies, and our

intent with this statement is not to disregard earlier studies. Indeed, our literature review discusses many such studies.

Nevertheless, our review of this literature suggests that beginning around 2006-2007, studies on the role of the business press

have grown into a well-defined area of the capital markets literature.

2

In this study, our use of ‘media’ may include any platform for distributing information, including the broadcast, digital, and

print media. Our use of ‘financial press’ refers specifically to business-focused outlets and, because we ultimately examine the

largest newspapers, primarily captures the print financial press. Due to the cost of acquiring information conveyed via digital

financial media (including the online sites for newspapers), we do not examine this important information environment,

although we see opportunities for future research on these outlets that might parallel our analysis.

3

For example, analysts rely on information garnered from prior earnings changes (Conrad et al. 2006, Ivković and Jegadeesh

2004), stock price changes (Abarbanell 1991), dividend changes (Denis, Denis and Sarin 1994), annual report disclosures

(Hope 2003), management forecasts (Williams 1996), management guidance (Cotter, Tuna and Wysocki 2006), firm

conference calls (Bowen, Davis and Matsumoto 2002), bond rating changes (Ederington and Goh 1998), broker-hosted investor

conferences (Bushee, Jung and Miller 2011, Green et al. 2014), other analysts’ research (Trueman 1994), and so on. Together,

these studies characterize analysts as processing multiple information signals.

1

service in sifting through and extracting information that would not be significant to the ordinary investor

to reach material conclusions.” Thus, we expect analysts to consume information distributed through the

financial press.

4

While a large volume research attempts to understand where analysts obtain their

information and how they process it, there is little research on the likely direct information flow from the

financial media to analysts. Lawrence, Ryans, and Sun (2017) study investor demand for sell-side analyst

research, and find that analysts often do not issue revisions on media coverage days when there is a high

investor demand for analyst research. We investigate whether analysts are able to provide new and useful

information to investors by processing information conveyed by the financial press.

Analysts provide information to their clients by synthesizing numerous information sources and

maki

ng useful recommendations. Analysts should possess a comparative information advantage because

of their ability to generate assessments about the quality of a firm’s fundamentals based on public

information. Public information conveyed through the media could increase information asymmetry but

allow analysts to process information and make informed opinions about a firm’s fundamentals that are

superior to those of other market participants (Kim and Verrecchia 1994, 1997). This is consistent with

the evidence in Kross, Ro and Schroeder (1990) and Lys and Sohn (1990), who document that analysts’

earnings forecasts are more informative when they are preceded by corporate accounting disclosures.

On the other hand, if print news and analyst reports are competing information channels, analysts’

rese

arch based on media information may not be informative to investors for a number of reasons. First,

the mere existence of such widely distributed news may reduce or ‘crowd out’ the informativeness of

4

It is possible to argue that analysts may choose to not rely on the information from the media. First, there is evidence that

analysts ignore or only partially impound public information (Abarbanell and Bernard 1992, Bradshaw, Richardson and Sloan

2001). Much of the ‘news’ in the print press is stale (Tetlock 2011), thus analysts may respond to either new or stale information,

both, or neither. Third, to the extent that the media sometimes serves merely as an information conduit (i.e., pass-through of

information) rather than an information intermediary (i.e., producer of information), it is possible analysts obtain the underlying

information from more direct sources such as the firm itself (Hassell, Jennings and Lasser 1988) or newswires (Li, Ramesh and

Shen 2011). Finally, Jensen (1979) expresses a sardonic characterization of news coverage as a form of entertainment, which

diminishes the role of the media as a source of ‘new and useful’ information.

2

analyst reports (Ivkovic and Jegadeesh 2004). Second, studies like Lin and McNichols (1998) and Irvine,

Lipson and Puckett (2007) argue that analysts’ research has a marketing role, reducing the importance of

any particular source of information, including that conveyed in the media. Third, while prior studies

conclude that analysts are information agents with the ability to process information and affect stock prices

(Womack 1996; Michaely and Womack 2005), Altinkilic and Hansen (2009) characterize analysts’

research as “information free” and argue that analysts “piggyback” on firm news and consequently issue

uninformative reports. To the extent that the media sometimes serves merely as an information conduit

(i.e., a pass-through of information; distribution) rather than an information intermediary (i.e., producer

of information), it is possible analysts obtain the underlying information from more direct sources such as

the firm itself (Hassell, Jennings and Lasser 1988) or newswires (Li, Ramesh and Shen 2011).

5

Much of our understanding of analysts’ role in the capital markets is based on their quantitative

outputs (i.e., earnings forecasts, discrete stock recommendations, or target prices), but these items are less

important than qualitative factors such as their industry knowledge, access to management, and written

reports (Bradshaw 2013). Likewise, information conveyed through news coverage is both quantitative and

qualitative. Liberti and Petersen (2017) provide a thoughtful discussion of difference between ‘soft’ and

‘hard’ information, and conclude that there is a continuum and that a crisp dichotomy is unclear. However,

hard information is almost always quantitative. Soft information is not, and in contrast to the ease with

which hard information can be summarized and disseminated, soft information is not so easily shared. As

Liberti and Petersen (2017) describe, “If we don’t know what the information will be used for, or which

parts of the information are relevant or useful, it is difficult to code and catalog it for future use.” (p. 9)

Our examination of whether analysts respond to information in news coverage is focused on separately

measuring the amount of soft versus hard information in firm-specific news coverage and, more

5

Of course, this is also a construct validity issue that we discuss later and attempt to address in our empirical design.

3

importantly, examining which type of news is most strongly associated with analysts’ belief revisions,

captured by changes in recommendations and investor price reactions.

The first link we document is whether cross-sectional variation in the quantity of news coverage

of a firm is associated with subsequent analysts’ recommendation revision activity. We also examine

whether any such association is conditional on the tone of news coverage. While a finding that analysts’

revisions are positively associated with news coverage of the firm might not be surprising, we are not

aware of any prior studies that document such a link. The closest study is Cao et al (2014), who document

an association between country-level media competition and analyst earnings forecast properties. The

confirmation of the existence of such a link is important because it provides preliminary evidence

consistent with analysts processing information conveyed by news coverage. However, such a relation

could also reflect analysts responding to the same information with a lag, analysts merely piggybacking

off of public information disclosure, or some endogenous link between exogenous news and both media

and analyst reactions. We address these alternative explanations through our primary analysis of how soft

information in the financial press is associated with analysts’ research and subject these analyses to

numerous empirical tests.

We focus on stock recommendation revisions conditional on the type of information conveyed in

the fi

nancial press. If analysts process information in news coverage, achieving information discovery,

and this information is not yet impounded into prices, we would expect more pronounced market reactions

to analyst recommendation revisions subsequent to news coverage of a firm. If, however, analysts respond

to information with a lag or piggyback on information releases, we should not see any permanent market

reaction to a duplication of previously released news. Thus, we examine event window market reactions

to analysts’ stock recommendation revisions and investigate whether market reactions are stronger for

firms with greater news coverage preceding the recommendation revision.

4

Our descriptive statistics are consistent with firm-specific news coverage being associated with

higher levels of analysts’ stock recommendation revision activity in the following 30-day window. A

single news article is associated with a 1.66% increase in monthly revision activity, representing a 44%

increase relative to the unconditional average revision frequency of 3.76%. We also find that the tone of

the news corroborates the direction of revision activity.

More importantly, we demonstrate that the market reaction to recommendation changes is stronger

for firms with greater recent news coverage. A one standard deviation change in our variable capturing

news coverage is associated with an incremental 0.6 percent negative return for downgrades and 0.4

percent positive return for upgrades. These incremental impacts are larger than several other mediating

variables for stock recommendation reactions documented in previous literature, such as price momentum

and herding (Loh and Stulz 2010). Our empirical results are robust to a battery of diagnostic and sensitivity

checks. In our final analysis of the relative contribution of soft versus hard news to analysts’

recommendation revisions and the associated stock price reactions, we substantiate an intuitive prediction

that the stronger association between firm-specific news coverage and market reactions to

recommendation revisions is driven primarily by analysts’ interpretation of soft news.

Our study faces several empirical challenges, but we attempt to mitigate such concerns through

our res

earch design in several ways. The primary concern relates to identification, as our basic results

presume the media is the source of firm-specific information impounded by analysts, but both the media

and analysts may obtain the information from the same source. To mitigate this possibility, we omit

newswires, which capture direct firm releases and rely instead on news coverage in the ten largest print

newspapers. We also randomly selected 250 news articles to manually determine the source of the firm-

specific information conveyed in the article. We find that 68% reflect ‘investigative reporting,’ sometimes

supplemented by publicly-available factual information (Appendix A), but 32% of the articles report firm-

5

specific news plausibly sourced from the firm (or another external reporting source).

6

Thus, the majority

of this random sample does not merely transmit information likely sourced from a firm, but acts as an

information intermediary that generates new information. [We are currently collecting and examining a

full sample of analyst reports to specifically identify recommendations that mention the media.]

Even if all of the news coverage we examine were prompted by firm-specific disclosures (which

is unli

kely given our random sample), our focus is on analysts and market reactions in windows centered

on analyst revisions that appear in the month following the associated news coverage. If news coverage is

preceded by firm-specific disclosures through the newswires, the time lag between such disclosures and

analysts’ revisions would be inexplicably long, and in such a case, even in a semi-strong form market

investors would unlikely react to previously publicly-released firm-specific information.

7

More important,

we find that roughly half of all recommendation revisions are contrarian relative to the market reactions

to the initial news article releases, suggesting analyst recommendations do not merely “regurgitate”

information in recent news articles, and investors seem to wait on analysts to process this information.

Nevertheless, despite this small sample evidence to the contrary, some unobservable aspect of the

news coverage we examine could be the driver of both the news coverage, analysts’ revisions and market

reactions. Engelberg and Parsons (2011) describe how this ephemeral identification problem hinders

inferences in numerous studies on causal impacts of the media. To provide preliminary evidence on this

issue, we use a sample of analyst reports of S&P 500 companies in 2012 to identify the proportion of

reports that specifically reference one of the ten largest print newspapers, which corresponds to the news

6

This result is consistent with the inference in Li (2015), who investigates how the media produces information. Li (2015)

finds that financial journalists rely on first-hand access to management, institutional investors, and other external experts to

produce informative news.

7

It is possible that analysts might use the same information from another source. 8-K disclosures are considered one of the

important firm-specific disclosure channels. To test this possibility, we conducted a robustness check by including firm-specific

8-K disclosures during the same period as the news coverage period. Our results remain qualitatively similar as those presented

in the paper (see section 5 for more details).

6

sources of our primary sample.

8

We find a mention rate of 30%, suggesting analysts rely on information

from news coverage to support their research (Appendix B). We also believe that our deliberate delay

between the firm-specific news coverage and our sample analysts’ subsequent revision activity minimizes

concerns that any incremental market reaction to analysts’ subsequent revision activity is merely a proxy

for some unobservable aspect of the news coverage. The questionable alternative is that news would have

to be very slowly processed by both analysts and investors for us to find significant incremental market

reactions with our research design. Even if our data were manifestations of these concerns, our results

nevertheless still speak to the use of information in the print media by analysts given our test specification.

While it is fundamentally challenging to address the identification problem of news attribution, the results

from various sensitivity analyses are collectively consistent with analysts using information in the media.

Our results are consistent with various findings in the literature showing that analysts incorporate

quali

tative information into their analyses. For example, prior research demonstrates associations between

analysts’ recommendations and narrative annual report disclosures (Rogers 1996), an assessment of the

quality of management (Barker 1999), a qualitative ‘strengths-of-argument’ variable (Asquith, Mikhail

and Au 2005), and positive or negative affect in managerial presentations (Mayew and Venkatachalem

2012). More importantly, our study contributes to our understanding of the role of the media as an

information intermediary in the capital markets. Bushee et al. (2010) examine news coverage of firms

during earnings announcement windows and document a significant reduction in information asymmetry.

We extend their research by demonstrating that one of the channels through which the media contributes

to the information flow in the capital markets is through another intermediary – financial analysts. Our

analysis links firm-specific news coverage to analyst revision activity and incremental impacts on stock

price reactions to those revisions. Our study also extends the large literature on analysts’ role as a primary

8

We collected analyst reports from the Investext database of Thomson ONE.

7

user of financial information. Prior research analyzes how analysts differentially use various sources of

information such as the income statement versus balance sheet (Previts et al. 1994), audited versus

unaudited information (Rogers 1996), and management sourced versus independently gathered

information (Williams, Moyes and Park 1996). Our results confirm the conjecture in Lawrence et al.

(2017) that analysts require time to process soft information in media coverage, which implies that “the

largest opportunity for analysts to meet unmet demand for analyst information is after media coverage”

(p. 145). We document that firm-specific news coverage provides information that not only impacts

analysts’ subsequent firm-specific revision activity, but interacts with that revision activity to strengthen

market reactions to analysts’ revisions.

2. Background and predictions

2.1 Background

Our study is related to several strands of research. First, a growing body of research is interested

i

n how market participants react to information disseminated through the media. A seminal study in this

area is Cutler, Poterba and Summers (1988), who document on average small stock market reactions to

major news events (and the reverse, limited news events to justify the largest stock price movements),

which for many years cast doubt on the view that stock price movements are attributable to news coverage.

However, recent empirical evidence suggests news coverage sometimes leads, and sometimes lags stock

price movements. For example, using a popular Wall Street Journal column “Abreast of the market,”

Tetlock (2007) documents that news coverage predicts stock market movements. Tetlock (2011)

investigates investors’ reaction to ‘stale news stories,’ and documents evidence of strong return reversals

for stocks with above-average individual investor trading activity. Other evidence suggests news coverage

contains value relevant information on firm fundamentals that is not directly impounded into stock prices

(e.g., Tetlock, Saar-Tsechansky and Macskassy 2008, Engelberg 2008, and Tetlock 2011), which allows

8

some market participants to obtain an advantage from processing this information (see Engelberg, Reed

and Ringgenberg 2012 for short sellers; Bushman, Williams and Wittenberg-Moerman 2013 for banks;

Chuprinin, Gaspar and Massa 2013 and Fang, Peress and Zheng 2013 for mutual funds; and Bonsall,

Green and Muller 2013 for rating agencies).

9

We contribute to this line of research by investigating the

extent to which financial analysts facilitate security price discovery in the capital markets through the

incorporation of relevant information from news coverage into their research products.

Second, our research is related to the extensive literature on financial analysts (see Brown 1993

and Sc

hipper 1991 for commentaries on early research, and Ramnath, Rock and Shane 2008 and Bradshaw

2013 for reviews on recent research). Financial analysts are considered sophisticated information

intermediaries in the capital markets. Beyer et al. (2010) review recent literature on firms’ financial

reporting environment, and suggest that analysts provide 22% of accounting-based information about a

firm. Prior research has almost exclusively focused on analysts’ use of hard information, such as stock

prices (Lys and Sohn 1990, Abarbanell 1991), financial statement information (Mendenhall 1991,

Bradshaw, Richardson and Sloan 2001), and other performance measures (Han and Wild 1990).

10

Analysts have access to other information sources such as private communication with managers

and public information including news coverage. Our objective in this paper is to shed light on whether

and how analysts incorporate the information content of news coverage in their research outputs. The

information in the financial press seems largely qualitative (i.e., “soft” information, as opposed to “hard”

information that characterizes much of financial reports and earnings announcements). The cost of

9

Recent commentators (Goldberg 2003) argue that major media outlets report news with a political bias. However,

Mullainathan and Shleifer (2005) examine the determinants of media accuracy using a demand-side model, and find that in the

aggregate readers should have an unbiased perspective if they have access to all news sources.

10

Prior studies also investigate the sources of the usefulness of analyst research, such as the discovery of private information

and/or interpretation of public information (Ivkovic and Jegadeesh 2004, Asquith, Mikhail and Au 2005). While Francis,

Schipper and Vincent (2002) document evidence supporting the complementarity of analyst research and earnings

announcements, Chen, Cheng and Lo (2010) find that information discovery (interpretation) dominates in the week before

(after) firms’ earnings announcements, supporting the co-existence of both roles.

9

processing soft information is high (Liberti and Petersen 2017; Engelberg 2008), which presents an

opportunity for analysts to transform such soft information into inputs for their research. Indeed, soft

information is a key element of the “mosaic” of information discussed in Reg FD.

Empirical evidence is generally consistent with the media providing news coverage of corporate

events, creating new information, and disseminating the information (Dyck, Volchkova and Zingales

2008, Miller 2006, Bushee et al. 2010, and Ahern and Sosyura 2013). Further, news coverage contains

value relevant information on firm fundamentals and is processed and used by different capital market

participants. For example, Bonner, Hugon and Walther (2006) document that media coverage of an analyst

is positively related to investors’ reactions to forecast revisions. Similarly, Rees, Sharp and Twedt (2013)

study the determinants of news about individual analysts in the financial press and the effects of that news

on the career outcomes of analysts. Their evidence suggests that media coverage provides valuable

exposure for analysts. However, these two studies focus on the information flow from analysts to the

financial press, which leaves open the question of the other direction of information flow. The media and

analysts serve similar roles as information intermediaries, gathering, processing, and disseminating

information, and both are likely to use the outputs from each other.

Anecdotal evidence appears in analysts’ formal reports and suggests that analysts consume and

thei

r opinions are shaped by news coverage. For example, Barclays analysts covering Apple (NASDAQ:

AAPL) noted, “As we previously reported, according to the Wall Street Journal (‘Apple Plots its TV

Assault,’ 12/19/11), Apple executives have been meeting with media executives to discuss the future of

television” (Reitzes and Thorwart 2012). In a report on Wachovia Corp (NYSE: WB), a Punk, Ziegel &

Company analyst states, “If published reports in the Wall Street Journal and New York Times are correct,

it would appear that Wachovia’s stock is about to plunge once again and stay down for an extended period.

Both newspapers report that the company is close to a deal to acquire Golden West Financial” (Bove

10

2006). Finally, Janney Capital Markets analysts discuss a promising product for Crumbs Bake Shop

(NASDAQ: CRMB) by referencing that, “A Boston Globe article describes the … croissant-doughnut

hybrid as a food portmanteau. Ansel’s Cronut has been featured on Late Night with Jimmy Fallon, The

Today Show, Good Morning America, and Piers Morgan Live on CNN with host Anthony Bourdain”

(Kalinowski and Babington 2013). Consistent with the anecdotal evidence, we find that for a sample of

analyst reports of S&P 500 companies in 2012, 30% of the analyst reports refer to news coverage to

support their research, further supporting that news coverage is an important information source for

analysts (Appendix B).

While anecdotal evidence shows analysts sometimes refer to the financial press in their reports, it

i

s an open empirical question whether and how analysts assimilate information in financial press, and

whether their research outputs incorporating such information facilitate security price discovery and

improve efficiency in the capital market. Our objective is to provide evidence on this direct flow of

information from the media to analysts.

2.2 Empirical predictions

Our empirical analysis proceeds in several stages. In the first stage, we provide descriptive baseline

e

vidence about the link between the incidence of news coverage and analysts’ recommendation revision

activity. Our unit of analysis here is a firm and the population of analysts providing stock

recommendations for that firm. It seems obvious that firm-specific news coverage is associated with

subsequent analysts’ recommendation revisions, as analysts assimilate information in the news coverage

in their recommendations. However, Lawrence, Ryans, and Sun (2017) find that analysts do not always

issue revisions on the media coverage days when there is a high investor demand for analyst research,

suggesting that analysts might need time to process information in news coverage. We note that we are

not aware of any empirical evidence on this association, but the confirmation of such a link is an important

11

first step to investigate the role of media in providing information that is subsequently used by analysts in

generating research.

After documenting the association between firm-specific news coverage and analysts’ revision

activity, our primary focus turns to evidence of information processing by analysts. As discussed

previously, we are primarily interested in whether part of analysts’ information set is information provided

by the news coverage. If so, then the descriptive evidence would be consistent with news coverage

possibly being used by analysts to trigger updates to existing stock recommendations. However, a stronger

test is to examine whether the market reaction to analysts’ revisions is incremental in the presence of

recent news coverage on the firm being followed by the analyst. Altinkilic and Hansen (2010) argue that

analysts tend to piggyback on public news about firms, so piggybacking may explain any association

between news coverage and recommendation revision activity. Our primary prediction relies on investors’

processing of analyst revisions. If analysts use superior information processing skills to convert

information in the news coverage to inputs for stock recommendations, and if such information in the

news coverage reflects aspects of firms’ fundamentals that have not been impounded in stock prices, we

would expect more pronounced market reactions to analyst recommendation revisions when there is more

coverage of the firm. Our first hypothesis is as follows.

H

1

: The association between analysts’ stock recommendation revisions for a firm and stock returns

is positively related to recent news coverage of the firm.

We are also interested in capturing the nature of the information reflected in news coverage. One

approach to characterizing the content of news would be to perform a content analysis, and manually code

the specific types of information conveyed in news coverage (see, Asquith, Mikhail and Au 2005, for

example). This is costly and subject to coding bias. An alternative that permits processing of a large sample

of news articles and number of firms is to use machine-based textual analysis to characterize the

composition of hard versus soft news and the tone of the information contained in the news coverage.

12

These partitions are coarse relative to a manual content analysis, but they are popular in the literature due

to their ease of computation and demonstrated ability to provide insights at a relatively low cost.

11

We predict that the primary value obtained by analysts from consuming news coverage is in the

soft information provided. Our argument is similar in spirit to that offered by Schneider (1972). He laments

the lack of soft information in Securities and Exchange Commission filings because soft information is

“highly relevant to investment decisions” (p. 254).

12

Accordingly, we believe that analysts’ processing of

information lies largely in the piecing together of various soft and hard information into a cogent opinion

on the suitability of investing in a security. Analysts are typically viewed as quantitatively focused, using

inputs from the financial statements. However, as noted in any text on financial analysis, much of the

process is qualitative in nature, involving the selective processing of different strategic and economic

conditions that are not amenable to quantification. Sedor (2002) discusses theories regarding information

processing, and states that communication of information often takes place as “narratives.” For example,

narratives are used by managers in conference calls to discuss soft information like future plans, new

products, timelines, and trends. Sedor (2002)’s fieldwork interviews of financial analysts also suggest that

they generate forecasts by integrating historical quantitative financial information with qualitative,

forward looking narratives from managers and other information sources (Webby and O’Connor 1996).

As such, we predict that this type of information is the most likely to be useful to analysts assembling a

mosaic of information that would trigger market reactions. Our second hypothesis is as follows.

H

2

: The association between analysts’ stock recommendation revisions for a firm and stock returns

is more strongly related to soft news as opposed to hard news.

11

See Tetlock, SaarTsechansky and Macskassy (2008), Kothari, Li and Short (2009), and Engelberg, Reed and Ringgenberg

(2012) for the use of dictionary method to extract tonal information from news media. We use Loughran and McDonald’s

(2011) dictionary, which is more suitable for interpreting financial information based on 10-K filings.

12

He acknowledges that there is no sharp dividing line between hard and soft information. For example, “Audited historical

financial statements are normally considered to be a classic type of hard information. Accounting is not an exact science,

however, and many subjective evaluations and other types of soft information must be considered in order to prepare audited

financials.” (p. 256)

13

Our final prediction relates to the tone of the news coverage. Tone has been examined in several

contexts of financial disclosures. For example, Henry (2008) finds that the tone of earnings

announcements significantly affects investors’ reactions. She cites (Maat 2007), who explains that tone

affects information processing because tone is “a stronger argument for a particular conclusion than the

non-reinforced version” (p. 365). Similarly, Rogers, Van Buskirk and Zechman (2011) examine the impact

of earnings announcement disclosure tone on shareholder litigation. Following this interpretation of the

effect of tone on the receiver, we also predict that tone will affect analysts’ use of the information. The

differential impact of positive versus negative tone is more salient in the context of management press

releases and disclosures that are affected by strategic disclosure (e.g., Lang and Lundholm 2000).

In our empirical context, we are not aware of any evidence suggesting a strategic objective of

fina

ncial news coverage. Further, we do not have any priors on whether analysts might differentially

process positive versus negative tone. On one hand, analysts’ ability to assemble and process a mosaic of

information is expected to be neutral to the tone of the news coverage, so tone will be associated with the

direction of recommendation changes, and by extension, market returns. On the other hand, it is well

documented that sell-side analysts’ forecasts are routinely optimistic. The typical explanation for this

phenomenon is that analysts wish to maintain cordial relationships with the covered firms. If this is the

case, analysts might react more strongly to positive tone of news coverage relative to negative tone of

news coverage.

13

Given that the investors are aware of analysts’ optimistic bias, the market is not expected

to strongly react to analysts’ recommendation revisions associated with good news. In contrast, the market

is likely to respond strongly to react to analysts’ recommendation revisions associated with bad news

because such revisions are more credible. Given that we do not have a clear prediction related to the tone

of the news coverage, we form our final hypothesis as a null hypothesis.

13

It is also possible that analysts might strategically reference the media because of the need to provide cover, which would

apply primarily for bad news coverage, i.e., news coverage with negative tone. We examine this possibility in section 5.3.

14

H

3

: The association between analysts’ stock recommendation revisions for a firm and stock returns

is not correlated with the tone of the news.

3. Data and Variable Measurement

3.1 Data

The financial news texts are downloaded from Factiva. Following Engelberg (2008) and Gurun

a

nd Butler (2012), we use Factiva's Intelligent Indexing to match firms and news, and require that the

firm’s name appear at least once in the article to ensure the accuracy of matching.

14

We employ Factiva’s

algorithm to exclude duplicates. We omit newswires that would capture direct firm releases, and rely

instead on news coverage in the ten largest print newspapers. The news sources include top national

newspapers (Wall Street Journal, New York Times, Washington Post, and USA Today) and top local

newspapers (Atlanta Journal Constitution, Boston Globe, Denver Post, Pittsburgh Post-Gazette, St Louis

Post-Dispatch, and Minnesota Star Tribune).

15

Following Tetlock (2011), we exclude news articles with

fewer than 50 words to alleviate the concerns about articles being a short summary. We collect analyst

data from I/B/E/S, stock return data from CRSP, and financial data from Compustat.

The sample period spans 1998 to 2012. We begin with 1998 because Intelligent Indexing is not

reliable before 1998. We limit our firm universe to the S&P 1500 because smaller firms rarely receive any

coverage in these larger publications. Our empirical tests are conducted at different samples, and we also

impose restrictions on data as they become necessary in testing the hypotheses. As a result, our samples

14

Given analysts’ value as industry specialists (Kadan et al. 2012; Bradshaw 2013), news articles that contain macro or

industry-specific information might be more useful to an analyst. However our sampling procedure on firm-specific news

articles precludes us from including such articles in the sample. Along those lines, it would be interesting to examine how

analysts incorporate information from industry trade journals because they contain a real cogent set of news that analysts would

be in the position to capitalize upon. This is an appealing approach to investigate the interaction between analysts’ industry

expertise and industry level media coverage, but it is beyond the scope of the current paper.

15

The initial list of newspapers is from Engelberg and Parsons (2011). When we collected data from the Factiva database, some

local newspapers used in Engelberg and Parsons (2011) were not retrievable through the system. We thus only collected news

articles available from the Factiva system at the time of data collection. We only consider the version of print news, but not

online version or the blogs.

15

vary across different tests. We explain the sample details when we discuss the results of each empirical

test.

3.2 Variable Measurement

3.2.1 Media Variables

The key media variables used in the paper are the overall frequency of news coverage, the

di

stribution of soft versus hard information included in news coverage, and the tone of the news. We proxy

the frequency of press coverage for each firm as the number of news articles about the firm between days

{-30, -3} centered on the analyst recommendation revision date (#NEWS). #NEWS is highly right-skewed,

so we use a log transformation in the empirical analyses (log#NEWS), calculated as log (1+#NEWS). We

argue that #NEWS also captures important news about the firm. While it is difficult to measure the

importance of news coverage, we use the market reactions to the news articles as a proxy of the importance

of the news. Given that the sum of news announcement returns is mechanically correlated with #NEWS,

we use the maximum of absolute value of news announcement returns. We find a positive and significant

correlation of 0.55 between #NEWS and the maximum of absolute value of news announcement returns,

our proxy of the importance of news.

16

This result supports the use of #NEWS as a proxy of the import

news about the firm. As an additional validity check, we use the sample of analyst reports of S&P 500

companies in 2012. Specifically, for each analyst report, we find that the number of news counts over the

(t-30, t-3) window before the analyst report date is positively and significantly correlated with the

probability of one or more of the major newspapers being mentioned in the report (Appendix B).

We also measure the frequency of soft versus hard information within news coverage. While soft

i

nformation is difficult to observe, we need proxies to capture it. There are three empirical approaches to

16

We also replace log (1+#NEWS) with the maximum of absolute value of news announcement returns in the regression

analysis, and find qualitatively similar results.

16

measure soft/hard information in the literature based on (1) whether the information is verifiable or not;

(2) whether the information is quantitative or qualitative; (3) specific empirical settings such as the

distance between borrower and lender as a proxy for the lender’s ability to use soft information (Agarwal

et al. 2010). It is challenging to capture whether the information is verifiable or not using textual analysis.

To the extent quantitative information is more likely to be verifiable than qualitative information, we adopt

the quantitative (hard) versus qualitative (soft) approach suggested in Liberti and Petersen (2017).

Specifically, we designate textual information as soft and numerical information as hard, and

construc

t a variable HSRATIO, equal to the number of numerical words in an article (phrases consist of

digits, decimal points, commas, percentage and/or dollar such as $1.08, 50% or 20,000) divided by the

sum of the number of positive words, negative words, and numerical words in the article. We use the

classification method by Loughran and Mcdonald (2011) to identify positive and negative words.

17

We

estimate HSRATIO for each article, and classify an article as a hard news article if HSRATIO is above 0.4,

the median HSRATIO of all news articles, and as a soft news article otherwise. We present examples of

the hard and soft news articles and the associated HSRATIO in Appendix C. We count the number of soft

news articles and the number of hard news articles, and use a log transformation for the empirical analyses

(log#SOFTNEWS and log#HARDNEWS).

Finally, we adopt a dictionary method to evaluate the tone of news article. We parse the news

articles and count the number of positive and negative words using the classification method proposed by

Loughran and McDonald (2011), who show that their word classification scheme is more suitable in the

finance and economics context than the Harvard IV classification used in Tetlock (2010). We follow

17

Loughran and McDonald (2011) propose a new financial dictionary based on the words used in the 10-K filings. The authors

manually classify the word lists into negative, positive, uncertainty, litigious, strong modal and weak modal categories, and we

follow their approach to identify positive and negative words in the news article. On the other hand, numbers are identified

using the following rule: the string needs to start with a space or a dollar sign, and then a string that combines digits, commas,

and dots follows immediately. For example, $1.35 is considered as a number and FY13 is not counted as a number. To exclude

numbers that mark the years, whole numbers from 1950 to 2020 are not included in the total counts.

17

Tetlock (2007) and Dougal et al. (2012) to define several measures of the tone of articles: (1) the

percentages of positive words (%POS) is defined as the number of positive words divided by the total

number of words in the article, and the percentage of negative words (%NEG) is defined similarly; (2) the

net tone of the article is defined as TONE = %POS − %NEG. TONE is constructed to capture the net

effects from both the positivity and negativity of an article. In some regressions, we also include a variable

%HARD, which is measured as the percentage of numerical words in an article, to capture the proportion

of quantitative information (hard information) in the news coverage.

3.2.2 Analyst Variables

We focus on analyst recommendation revisions to make inferences on analysts’ assimilation of

use

ful information in the financial process. Specifically, we examine three recommendation revision

variables during month t of any given year.

%REVISING

t

: The proportion of analysts revising their recommendation, calculated as the

percentage of analysts revising recommendations (of all analysts covering the firm) during

month t.

∆REC

t

: The change in mean recommendation for firm i from month t-1 to month t. I/B/E/S

defines recommendation level 1 as strong buy and 5 as strong sell, but we invert these measures

so that higher numbers reflect higher recommendation levels.

CAR: The market reactions to analyst recommendation revisions, proxied by the abnormal

stock returns upon analyst recommendation revisions. Following Loh and Stuz (2010), we use

a two-day window (0, 1), and calculate abnormal stock returns upon analyst recommendation

revisions as

, where

is the return of firm i, and

is

the return on a benchmark portfolio with the same size, book-to-market, and momentum

characteristics as the stock (constructed in similar fashion as in Daniel et al. 1997 and Wermers

2003, DGTW hereafter).

3.2.3 Control Variables

In our regression analyses, we include a number of control variables as suggested in the prior

research on analyst recommendation revisions (Jegadeesh et al. 2004, Green 2006 and Loh and Stulz 2010,

among others). They include firm size (logMV), analyst following (#ANALYSTS), the book-to-market ratio

18

(logB/M), six month price momentum ending 30 days prior to the recommendation revision

(MOMENTUM), stock return volatility in the 60-days preceding the recommendation revision,

(logVOLATILITY), average daily share turnover in the 60-days preceding the recommendation revision

(TURNOVER), earnings forecast revision (∆EPS), the deviation of the recommendation from the

consensus (RECDEV), the analyst’s lagged earnings forecast accuracy (ACCRANK), lagged 30-day stock

returns (lagRET), and indicators for whether a firm makes an earnings announcement before (POSTEARN)

or subsequent to (PREEARN) the recommendation revision

4. Empirical Results

4.1 Descriptive Statistics

Table 1 reports descriptive statistics for each newspaper. The Wall Street Journal has the highest

numbe

r of news articles followed by the New York Times and the Washington Post. Local newspapers in

general have fewer number of articles compared to national newspapers. The average number of words

per article ranges from 496 to 706 words. There are slightly more negative than positive words for each

article, which might reflect the need to attract the attention of readers (Hamilton and Zeckhauser 2004).

On the other hand, the levels of news tone do not appear to differ across publications.

Table 2 presents summary statistics on analyst recommendation revision and firm level variables

used in the paper. The mean (median)

∆REC is -0.019 (0.000), and the mean (median) CAR is -0.385 (-

0.039), indicating that our sample includes more downward revisions (50,983) than upward revisions

(45,666). The table also shows that sample firms are quite heterogeneous on dimensions such as size,

growth opportunity, and performance. The TONE of news articles is slightly negative, echoing the results

in table 1 regarding %NEG. The average proportion of analysts who revise their recommendations is 4.2

percent, which we use as the baseline revision frequency when discussing the economic significance of

19

our results later. Finally, the average numbers of articles deemed to be hard news versus soft news are

both just larger than 1, but both are right-skewed, which is why we use log transformations in our tests.

4.2 News Coverage and Analyst Research Updates

To examine the link between firm-specific news coverage and analyst revisions, we perform the

followi

ng regression analysis:

%REVISING

i,t

= α + β

1

log#NEWS

i,t-1

+ β

2

|lagRET

i,t-1

|+ β

3

logMV

i,t-1

+ β

4

#ANALYSTS

i,t-1

+ ε

i,t

(1)

The dependent variable (PROP_REVISING) captures the likelihood of analysts revising their

recommendations for firm i in month t. In this analysis, we start with S&P 1500 firms for a period of 15

years, and we arrive at a sample of 268,197 firm-month observations after losing observations in the

process of merging with CRSP, IBES, and the media data. log#NEWS is the variable of interest that

captures the frequency of news coverage in the (-30, -3) window relative to the analyst revision month. In

a different regression specification, we replace log#NEWS with two indicator variables, I (#NEWS=1) and

I (#NEWS>1), to capture the incidences when firms have one news article and when firms have more than

one news article in month t. Control variables include the absolute value of lagged stock returns

(|lagRET|), firm size (logMV), and the number of analysts covering the firm (#ANALYSTS). We

standardize all continuous explanatory variables at mean 0 and standard deviation 1 to facilitate

comparison of the economic magnitudes of coefficients.

Panel a of Table 3 presents the panel regression results, with standard errors clustered by year-

mont

h. Column (1) shows the results using indicator variables of news coverage, and column (2) reports

the results using the continuous variable of news coverage log#NEWS. In column (1), we find that both

indicator variables, I (#NEWS=1) and I (#NEWS>1), are positive and statistically significant. Regarding

economic significance, the coefficient on I (#NEWS=1) indicates that a single news article is associated

with a 1.66% increase in monthly recommendation revision activity, representing a 44% increase relative

20

to the regression intercept of 3.76%. Given that all independent variables are demeaned, the intercept

therefore reflects the proportion of analysts revising for the mean firm in the sample. However, the

coefficient on I (#NEWS>1) has similar magnitude and significance as that on I (#NEWS=1). In column

(2), we find a positive and significant coefficient on log#NEWS, supporting the intuition that firm-specific

news coverage is associated with greater subsequent analyst revisions.

We next investigate whether analysts’ revisions are associated with the tone of recent news

coverage. We restrict the sample to the firm-month observations with available news coverage in the prior

month, thus the sample is reduced to 41,101 firm-month observations. We expect the direction of

recommendation changes to be associated with the tone of the financial news. We perform Fama-Macbeth

regressions of ∆REC on the lagged news tone measures along with control variables. The regression model

is as follows:

(2)

Table 3 panel B presents the Fama-Macbeth regression results. Tone is measured as %NEG,

%POS, and TONE in columns (1), (2), and (3), respectively. We again standardize all continuous

explanatory variables at mean 0 and standard deviation 1 to facilitate comparison of the economic

magnitudes of coefficients. Column (1) shows that the percentage of negative words in news coverage is

associated with downward recommendation revisions with statistical significance at better than the 5%

level. On the other hand, we find that the percentage of positive words in news coverage is associated with

upward recommendation revisions, but the coefficient on %POS is not statistically significant. We control

for %HARD when we examine the composite measure TONE in column (3). The results show a positive

and statistically significant coefficient on TONE, supporting analysts’ recommendations being associated

the information content in news coverage. We control for %HARD and other control variables (listed in

equation 2) in column (4). The inclusion of these control variables does not affect the sign and significance

21

∆REC

i,t

=

α + β

1

TONE

i,t-1

+ β

2

%HARD

i,t-1

+ β

3

logMV

i,t-1

+ β

4

logBM

i,t-1

+ β

5

MOMENTUM

i,t-1

+ β

6

lag∆REC

i,t-1

+ ε

i,t

level on the tone measure, and we continue to observe a positive and significant coefficient on TONE in

column (4).

18

4.3 News Coverage and Market Reactions to Analysts Recommendation Revisions

The descriptive results in section 4.2 are consistent with the notion that analysts respond to news

coverage by updating their recommendations, and that their recommendation revisions incorporate the

qualitative signal from the news articles. Our primary set of analyses are discussed next, and focus on the

market reactions to analyst recommendation revisions, which capture investors’ evaluation of analyst

research updates. We perform separate regressions of CAR for recommendation downgrades and

upgrades, and regressions of |CAR| for both upgrade and downgrade revisions.

19

The regression models

are as follows:

CAR

i,t

or |CAR

i,t

| = α + β

1

log#NEWS

i,t-1

+ β

2

logMV

i,t-1

+ β

3

logBM

i,t-1

+ β

4

MOMENTUM

i,t-1

+ β

5

logVOLATILITY

i,t-1

+ β

6

TURNOVER

i,t-1

+ β

7

∆EPS

i,t

+ β

8

RECDEV

i,t

+ β

9

ACCRANK

i,t-1

+ β

10

lagRET

i,t-1

+ β

11

PREEARN

i,t

+ β

12

POSTEARN

i,t-1

+ ε

i,t

where CAR is the DGTW adjusted abnormal announcement return to analyst recommendation revision,

and |CAR| is the absolute value of the return. The variable of interest is log#NEWS. Similar to Green (2006)

and Loh and Stulz (2010), we include a number of control variables as listed in equation (3).

(3)

The unit of analysis in this test is each individual analyst recommendation revision. This sample

starts with the 268,197 firm-month observations in table 3. Given that each firm has an average of nine

analysts following it and the mean proportion of analyst recommendation revision is 0.042, we arrive at a

sample of 103,631 analyst recommendation revisions. Further requirements such as having necessary

return data to calculate CAR reduces the sample to 96,649 recommendation revisions, with 50,983 upward

18

Note that the results in table 3 are also consistent with the strategic timing story, in which analysts await the arrival of news

for cover. We provide additional analyses to address this possibility in Section 5.3.

19

Reiterations are excluded from our analyses.

22

and 45,666 downward revisions.

20

A legitimate concern on this sample is that the fact that analysts not

revising recommendations does not suggest that they did not use the information from the media.

However, restricting the sample to recommendation changes makes empirical inferences feasible (e.g.,

Beaver 1968; Loh and Stulz 2010).

Table 4 panel A reports the results from the regressions on the market reactions to analyst

recommendation revisions for the event window [0, +1], with standard errors two-way clustered by firm

and analyst. We standardize all continuous explanatory variables at mean 0 and standard deviation 1 to

facilitate comparison of the economic magnitudes of coefficients. Columns (1) and (2) show the results

for downgrade revisions, columns (3) and (4) show the results for upgrade revisions, and the last two

columns include both upgrade and downgrade revisions. We find a negative and significant coefficient on

log#NEWS for downgrade revisions (columns (1) and (2)), suggesting more negative market reactions to

downgrade revisions when there is more news coverage on the firm. Likewise, we observe a positive and

significant coefficient on log#NEWS for upgrade revisions (columns (3) and (4)), suggesting more positive

market reactions to upgrade revisions when there is more news coverage on the firm. Finally, the

coefficient on log#NEWS is positive and significant in columns (5) and (6) when we examine |CAR| for

both upgrade and downgrade revisions. In terms of economic significance, the results indicate that a one

standard deviation of log#NEWS is associated with a 0.59 percent change in abnormal returns for

downward revisions (column 2), corresponding to roughly 19% of the mean abnormal returns in the two-

day window. Similarly, the change in abnormal returns associated with one standard deviation of

log#NEWS is 0.36 percent for upward revisions, equivalent to 14.5% of the mean abnormal returns in the

two-day window (column 4). Collectively these results provide support for

H

1

.

20

We consider the possibility that overlapping news coverage surrounding analyst revisions might contaminate our main

results. We thus conduct a sensitivity analysis by removing from our sample revisions with overlapping news coverage, which

leaves us with 41,135 downward revisions and 37,316 upward revisions. The regression results from this sensitivity analysis

are similar to those reported in the paper.

23

The signs of coefficients on control variables are in general opposite to each other in downgrade

and upgrade regressions, consistent with results in prior studies (see Green 2006, for example). Large,

high BM, high MOMENTUM, and low VOLATILITY firms experience less negative returns upon

downward revisions, and less positive returns upon upward revisions. When there is a concurrent EPS

revision and when the revision deviates from consensus, the abnormal returns are more negative upon

downward revisions, and more positive upon upward revisions.

The lag between our measurement of financial news and the analysts’ subsequent

recommendations lessens the likelihood that the revisions are merely piggybacking on financial press

news. The lag is also consistent with the observation in Lawrence et al. (2017) that analysts do not issue

revisions immediately on media news days. Moreover, stronger market reactions in the presence of recent

press coverage are inconsistent with the piggybacking explanation of Altinkilic and Hansen (2009).

However, it is important for us to establish the robustness of our primary results. Before we investigate

analysts’ processing of hard versus soft information in media coverage, we conduct supplemental analyses

and robustness tests to mitigate concerns that other factors might explain our findings.

We first consider the possibility that the market price reactions at high volume news days could

be a

result of investor attention to content, rather than the revelation of firm fundamentals. For example,

investors may more strongly react to information in recommendations preceded by more news coverage,

which leads to stronger price reactions around the event date. To explore this possibility, we investigate

the price reaction from day 2 to day 5 after the analyst recommendation revision date. If higher price

reactions are merely due to investor attention, then we would expect the price reaction to reverse in day 2

to day 5. We find that the coefficient on log#NEWS becomes smaller on each of the subsequent days and

lacks statistical significance, but there is no evidence of price reaction reversals. The results are not

tabulated for brevity, but are available upon request.

24

To illustrate the results, we estimate both upgrade and downgrade regressions of CAR

i,t

= α + β

log#NEWS

i,t-1

+ ε

i,t

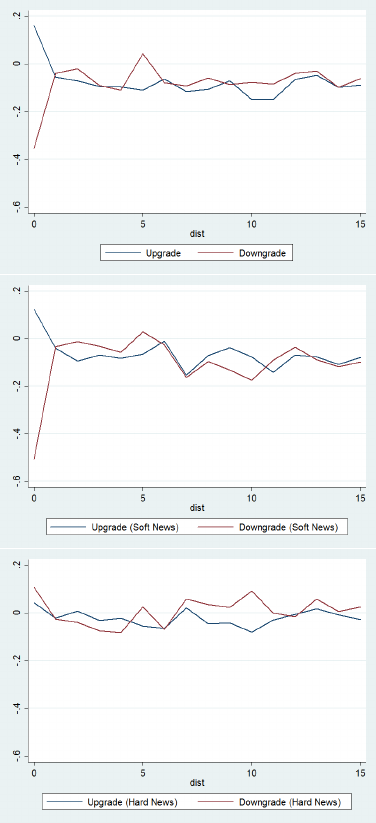

for each trading day after the recommendation revision date. The first graph of Figure

1 shows the plot of the β coefficients (on the vertical axis) that correspond to the number of days after the

recommendation revision day (on the horizontal axis). As is evident from the graph, the β coefficient has

the largest magnitude at day 0, and declines rapidly after the revision day. Taken together, these results

are consistent with the view that analyst recommendation revisions, in particular those associated with

more intense news coverage, are informative to the capital market.

Second, we address concerns about the impact of several confounding factors: (1) we collect data

on firms’ 8-K filings, and include the number of firm-specific 8-K filings during the same news coverage

period in the regression model to address the possibility of media coverage as a proxy of firm-specific

news releases from other information sources; (2) we remove recommendation revisions concurrent with

earnings announcements to separate the impact of earnings announcement events; (3) we control for stock

market reactions to the initial news article releases; (4) we remove articles related to analysts (17,000

articles, 3.6% of the sample); and (5) we include firm fixed effects. The regression results after

incorporating the above considerations are reported in panel B of table 4. Row (1) to Row (5) show the

results of incorporating each of the above controls/sample restrictions, and row (6) presents the results of

incorporating all the five in one regression. We continue to observe similar results on media coverage for

each regression specification, suggesting that those factors, either individually or collective, are unlikely

to be the primary driver of our empirical results.

21, 22

21

In additional to the five modifications to the regression model, we additionally take into consideration of the impact of

management earnings forecasts. Rogers and Van Buskirk (2013) show that bundled forecasts as a percentage of all forecasts

increased substantially to 70% in the post Reg FD period. Therefore we restrict the sample period to the post Reg FD period

and repeat the regression. We continue to observe qualitatively similar results on media coverage (untabulated).

22

Additional robustness tests include controlling for earnings surprises and the direction of change in recommendation revisions

in the market reaction regressions. The inferences from these alternative specifications are the same as those from the main

specification reported in the paper. These results are not tabulated, but are available upon request.

25

4.4 Analyst Interpretation of Hard versus Soft Information

Although the collective empirical evidence thus far suggests that analysts incorporate firm-specific

information from news coverage in their research updates and such research updates are valuable to

investors, it is not clear what type of information in the news coverage analysts primarily rely on to revise

their opinions. While information conveyed by the financial press is both quantitative and qualitative,

recent studies suggest the media contains important soft information. The cost of processing soft

information is considerably high (Liberti and Petersen 2017), which creates a demand for analysts to

process this type of information. In addition, soft information seems to be an important element of the

“mosaic” of information discussed in Reg. FD. Our investigation of whether analysts respond to business

press information allows us to separately measure the amount of soft versus hard information in the news

coverage, and shed light on whether analysts respond to the information content of firm-specific soft

information. Specifically we revisit the market reactions to analyst recommendation revisions, and

examine whether the market reactions differ in response to hard (quantitative) versus soft (qualitative)

information in press coverage. We implement the following panel regressions:

CAR

i,t

or |CAR

i,t

| = α + β

1

log#SOFTNEWS

i,t-1

+ β

2

log#HARDNEWS

i,t-1

+ β

3

X

i,t-1

+ ε

i,t

(4)

where CA

R is the DGTW adjusted abnormal announcement returns to analyst recommendation revisions.

The variables of interest are log#SOFTNEWS and log#HARDNEWS. The vector X represents the same set

of control variables as in equation (3).

Table 5 presents the results from the regressions on the market reactions to analyst

re

commendation revisions for the event window [0, +1], with standard errors two-way clustered by firm

and by analyst. We again standardize all continuous explanatory variables at mean 0 and standard

deviation 1 to facilitate the comparison of the economic magnitudes of the coefficients. Columns (1) and

(2) show the results for downgrade revisions, columns (3) and (4) show the results for upgrade revisions,

26

and the last two columns include both upgrade and downgrade revisions. For downward revisions

(columns (1) and (2)), we find a negative and significant coefficient on log#SOFTNEWS, but an

insignificant coefficient on log#HARDNEWS. The difference in the two coefficients is statistically

significant at better than the 5% level. We interpret the results as more negative market reactions to

downgrade revisions when there is more qualitative press coverage on the firm, but not quantitative

coverage. For upgrade revisions (columns (3) and (4)), we observe positive and significant coefficients on

both log log#SOFTNEWS and log#HARDNEWS. Although the coefficient on log#SOFTNEWS is larger

in magnitude, the difference in the two coefficients is not statistically significant. When we examine |CAR|

for both upgrade and downgrade revisions in columns (5) and (6), we find that the coefficient on

log#SOFTNEWS is positive and significant, but the coefficient on log#HARDNEWS is not statistically

significant. The difference in the two coefficients is statistically significant at better than the 1% level.

To illustrate the results, we estimate both upgrade and downgrade regressions of CAR

i,t

= α + β

log#SOFTNEWS

i,t-1

+ ε

i,t

and CAR

i,t

= α + β log#HARDNEWS

i,t-1

+ ε

i,t

on each trading day after the

recommendation revision date. The second graph of Figure 1 shows the plot of the β coefficients (on the

vertical axis) of log#SOFTNEWS that correspond to the number of days after the recommendation revision

day (on the horizontal axis), and the third graphs shows the plot of the β coefficients (on the vertical axis)

of log#HARDNEWS. The β coefficient of log#SOFTNEWS has the largest magnitude at day 0, and declines

rapidly over time. In contrast, we do not observe patterns on the β coefficients of log#HARDNEWS.

Collectively, these results are consistent with H

2

, supporting that analysts contribute to the security price

discovery by sifting through and extracting soft information in news coverage.

Descriptive results in table 3 suggest that analysts impound the qualitative signal from news

coverage (i.e. the tonal information) in their recommendation revisions. We now formally document that

the stock market responds to the tonal information contained in analyst recommendation revisions. First,

27

we note that our results from both table 4 and table 5 suggest that the market responds significantly to the

amount of news coverage for both upward revisions and downward revisions. The upward (downward)

revisions are generally triggered by the positive (negative) tone of the media coverage. The significant

coefficients on log#NEWS in both upward and downward revision samples provide support that these

revisions are informative to the investors. Second, we employ another research design to test such a link,

and also consider the interactions between the tone measures and news coverage intensity. Given that we

need news articles to calculate tonal measures, we remove all observations without news coverage, which

results in a sample of 29,993 recommendation revisions. Specifically, we estimate the following panel

regressions:

CAR

i,t

= α + β

1

TONE

i,t-1

+ β

2

log#NEWS

i,t-1

+ β

3

TONE

i,t-1

* log#NEWS

i,t-1

+ β

4

X

i,t-1

+ ε

i,t

(5)

CAR

i,t

= α + β

1

TONE

i,t-1

+ β

2

log#SOFTNEWS

i,t-1

+ β

3

TONE

i,t-1

* log#SOFTNEWS

+ β

4

log#HARDNEWS

i,t-1

+ β

5

TONE

i,t-1

* log#HARDNEWS

+ β

6

X

i,t-1

+ ε

i,t

(6)

where CA

R is the DGTW adjusted abnormal announcement returns to analyst recommendation revisions.

The variables of interest are the tone measures and the interactions between the tone and news coverage

measures. Again, the vector X represents the same set of control variables from equation (3).

23

Table 6 presents the results from these panel regressions, with standard errors two-way clustered

by firm and by analyst. We again standardize all continuous explanatory variables at mean 0 and standard

deviation 1 to facilitate the comparison of the economic magnitudes of the coefficients. The results on the

control variables are not tabulated for brevity, but they are in general consistent with those presented

earlier in table 3. Columns (1) to (3) report the regression results with three different tone measures,

23

Given that we are interested in the effect of tone measure, we pool all the recommendation revisions together to run the

regression, which is different from the research design in tables 4 and 5.

28

%POS, %NEG, and TONE, but without news coverage measures. Consistent with the expectation (H

3

),

we observe a positive coefficient on %POS, a negative coefficient on %NEG, and a positive coefficient

on TONE, with all three coefficients highly statistically significant. We infer from the results that the stock

market responds to the tonal information analysts extract from news coverage and impound in their

research updates.

Column (4) presents the results estimating equation (5). Our focus is on the interaction of the tone

and the news coverage measures. The results reveal that TONE is no longer statistically significant, but

there is a positive and significant coefficient on the interaction term. Thus, the qualitative signal in the

news coverage has a significant market impact when the press coverage is more intense.

Column (5) presents the results estimating equation (6). Our focus is again on the interaction of

the tone and the news coverage measures, but we also separate quantitative news coverage from qualitative

news coverage. Similar to column (4), we do not find a significant coefficient on TONE. However, the

coefficients on the two interaction terms are positive and statistically significant, although the coefficient

on the log#SOFTNEWS interaction is higher in magnitude relative to that on the log#HARDNEWS

interaction. This result implies that the tone signal in the news coverage has a significant market impact

when press coverage, in particular the qualitative press coverage, is more intense. Taken together, we

interpret the empirical evidence in the paper as analysts extracting qualitative information from the news

coverage, and providing such information to investors through recommendation revisions.

5 Extensions

5.1 Investors’ Reactions to Initial News Articles and Their Reactions to Recommendation Revisions

We first investigate investors’ reactions to initial news articles (NEWSCAR) to provide further

e

vidence on analysts’ information role in the capital markets. For each stock recommendation revision,

we measure NEWSCAR as the average two-day stock market reactions to the initial news article releases.

29

We then link NEWSCAR to the direction of analyst recommendation revisions. The results are presented

in Table 7, panel A. For recommendation revisions preceded by positive market reactions (NEWSCAR>0),

46.8% of the revisions are upgrades (confirming revisions) compared to 53.2% downgrades (contrarian

revisions). Likewise for recommendation revisions preceded by negative market sentiment

(NEWSCAR<0), 48.1% of the revisions are upgrades (contrarian revisions) relative to 51.9% downgrades

(confirming revisions). Therefore, roughly half of the recommendation revisions are contrarian to the

prevailing market reactions following news coverage, consistent with the slight negative correlation

between NEWSCAR and CAR.

24

The evidence from this analysis suggests analyst recommendations do

not merely “regurgitate” recent news articles and investors seem to wait on analysts’ opinions.

25

We provide preliminary evidence on differences between ‘confirming’ and ‘contrarian’

recommendation revisions. We estimate equation (6) again but separately for confirming and contrarian

revisions. Column (1) in Table 7 panel B presents the regression results for contrarian revisions, and

column (2) reports the results for confirming revisions. Our focus is on how the interactions of the tone

and the soft/hard news coverage measures vary for confirming versus contrarian revisions. For contrarian

revisions, we find a positive and significant coefficient on the interaction of TONE and log#SOFTNEWS,

but an insignificant coefficient on the interaction of TONE and log#HARDNEWS, suggesting that analysts’

processing of the tonal information in soft news articles is more informative to investors. In contrast, we

24