Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9

Draft Ok to Print

AH XSL/XML

Fileid: … ns/i3115/202212/a/xml/cycle05/source (Init. & Date) _______

Page 1 of 34 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Instructions for Form 3115

(Rev. December 2022)

Application for Change in Accounting Method

Department of the Treasury

Internal Revenue Service

Section references are to the Internal Revenue Code unless

otherwise noted.

All references to Rev. Proc. 2015-13 are to Rev. Proc.

2015-13, 2015-5 I.R.B. 419 (as clarified and modified by

Rev. Proc. 2015-33, 2015-24 I.R.B. 1067, and as

modified by Rev. Proc. 2021-34, 2021-35 I.R.B. 337; Rev. Proc.

2021-26, 2021-22 I.R.B. 116; by Rev. Proc. 2017-59, 2017-48

I.R.B. 543, and section 17.02 of Rev. Proc. 2016-1, 2016-1

I.R.B. 1), or any successor.

All references to Rev. Proc. 2022-14 and the List of Automatic

Changes are to Rev. Proc. 2022-14, 2022-7 I.R.B. 502 (as

modified by Rev. Proc. 2022-23, 2022-18 I.R.B. 105 and Rev.

Proc. 2023-11, 2023-3 I.R.B. 417) or any successor.

All references to Rev. Proc. 2023-1 are to Rev. Proc. 2023-1,

2023-1 I.R.B. 1, or any successor (updated annually).

Future Developments

For the latest information about developments related to Form

3115 and its instructions, such as legislation enacted after they

were published, go to IRS.gov/Form3115.

What's New

Changes related to the deferral method for advance pay-

ments, cost offset methods, and/or the applicable financial

statement income inclusion rule. The instructions for

Schedule B have been updated to include additional information

about accounting method changes relating to the deferral

method for advance payments, cost offset methods, and

methods to conform to the applicable financial statement (AFS)

income inclusion rule under section 451.

Research and experimental expenditures. Effective for

specified research or experimental expenditures paid or incurred

in tax years beginning after 2021, no deduction is allowed for

such expenditures. Instead, you must capitalize and amortize

these amounts over a 5-year period for amounts attributable to

domestic research and over a 15-year period for amounts

attributable to foreign research. See DCN 265 and Rev. Proc.

2023-11, 2023-3 I.R.B. 417.

General Instructions

Purpose of Form

File Form 3115 to request a change in either an overall

accounting method or the accounting treatment of any item.

Method Change Procedures

When filing Form 3115, you must determine if the IRS

has issued any new published guidance which includes

revenue procedures, revenue rulings, notices,

regulations, or other relevant guidance in the Internal Revenue

Bulletin (I.R.B ) For the latest information, go to

IRS.gov.

For general application procedures on requesting accounting

method changes, see Rev. Proc. 2015-13. Rev. Proc. 2015-13

provides procedures for both automatic and non-automatic

accounting method changes.

CAUTION

!

CAUTION

!

Automatic change procedures.

Unless otherwise provided in

published guidance, you must file under the automatic change

procedures if you are eligible to request consent to make an

accounting method change under the automatic change

procedures for the requested year of change. See the

instructions for

Part I Information for Automatic Change Request,

later, and the List of Automatic Changes in Rev. Proc. 2022-14.

No user fee is required for a Form 3115 filed under the

automatic change procedures. An applicant that timely files and

complies with the automatic change procedures is granted

consent to change its accounting method, subject to review by

the IRS National Office and operating division director. If it is

reviewed by the IRS, you will be notified if information in addition

to that requested on Form 3115 is required or if your request is

denied. Ordinarily, you are required to file a separate Form 3115

for each accounting method change. However, in some cases,

you are required or permitted to file a single Form 3115 for

particular concurrent accounting method changes. See section

6.03(1)(b) of Rev. Proc. 2015-13 for more information.

Note. The List of DCNs (Designated automatic accounting

method change numbers) at the end of these instructions is a list

of many accounting method changes and is presented for

informational purposes only and subject to the most recently

issued revenue procedures.

You may qualify for a reduced Form 3115 filing

requirement for certain DCNs. A reduced Form 3115

filing requirement involves completing only certain lines

and schedules of Form 3115. For qualifying changes and filing

requirements, see Rev. Proc. 2022-14. For example, qualified

small taxpayers are eligible for a reduced Form 3115 filing

requirement for DCNs 7, 8, 21, 88, 89, 107, 121, 145, 157,

184-193, 198, 199, 200, 205, 206, 207, and 222.

Non-automatic change procedures. If you do not qualify to

file under the automatic change procedures for the requested

accounting method change for the requested year of change,

you may be able to file under the non-automatic change

procedures. See

Non-automatic change-scope and eligiblity

rules , under Part III, later. If the requested change is approved

by the IRS National Office, the filer will receive a letter ruling on

the requested change. File a separate Form 3115 for each

unrelated item or submethod that is being changed. A user fee is

required. See the instructions for Part III for more information.

Who Must File

The filer is the entity or person required to file Form 3115,

whether on its own behalf or on behalf of another entity. An

applicant is an entity, a person, or a separate and distinct trade

or business of an entity or a person (for purposes of Regulations

section 1.446-1(d)), whose accounting method is being

changed.

For a consolidated group of corporations, the common parent

corporation must file Form 3115 for an accounting method

change for itself and for any member of the consolidated group.

For example, the common parent corporation of a consolidated

group is the filer when requesting an accounting method change

for another member of that consolidated group (or a separate

and distinct trade or business of that member), and the other

TIP

Feb 7, 2023

Cat. No. 63215H

Page 2 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

member (or trade or business) on whose behalf Form 3115 is

filed is the applicant.

For information on the difference between a filer and an

applicant, see Name(s) and Signature(s), later.

For information on a controlled foreign corporation (CFC) or

10/50 corporation without a U.S. trade or business, see section

6.02(6) of Rev. Proc. 2015-13.

Generally, a filer must file a separate Form 3115 for each

applicant seeking consent to change an accounting method. A

separate Form 3115 and user fee (for non-automatic change

requests) must be submitted for each applicant and each

separate trade or business of an applicant, including a qualified

subchapter S subsidiary (QSub) or a single-member limited

liability company (LLC), requesting an accounting method

change. See section 9.02 of Rev. Proc. 2023-1.

However, identical accounting method changes for two or

more of the following in any combination may be included in a

single Form 3115.

1. Entities with a common sponsor.

2. Members of a consolidated group;

3. Separate and distinct trades or businesses (for purposes

of Regulations section 1.446-1(d)) of that entity or member(s) of

a consolidated group. Separate and distinct trades or

businesses include QSubs and single-member LLCs;

4. Partnerships that are wholly owned within a consolidated

group; and

5. CFCs and 10/50 corporations that do not engage in a

trade or business within the United States where (i) all controlling

domestic shareholders (as provided in Regulations section

1.964-1(c)(5)) of the CFCs and of the 10/50 corporations, as

applicable, are members of a consolidated group; or (ii) the

taxpayer is the sole controlling domestic shareholder of the

CFCs or of the 10/50 corporations.

For information on what is an identical accounting method

change, see section 15.07(4) of Rev. Proc. 2023-1.

When and Where To File

Automatic change requests. Except if instructed differently,

you must file Form 3115 under the automatic change procedures

in duplicate as follows.

•

Attach the original Form 3115 to the filer's timely filed

(including extensions) federal income tax return for the year of

change. The original Form 3115 attachment does not need to be

signed.

•

File a copy of the signed Form 3115 (duplicate copy) with the

IRS National Office at the address provided in the Address Chart

for Form 3115, later, no earlier than the first day of the year of

change and no later than the date the original is filed with the

federal income tax return for the year of change. This signed

Form 3115 may be a photocopy. For more on the signature

requirement, see

Name(s) and Signature(s), later. Alternatively,

the duplicate copy of the signed Form 3115 may be submitted by

fax.

The IRS does not send acknowledgements of receipt for

automatic change requests.

For filing procedures relating to automatic change

requests for certain foreign corporations and foreign

partnerships, see section 6.03(1)(a)(ii) and (iii) of Rev.

Proc. 2015-13.

Non-automatic change requests. You must file Form 3115

under the non-automatic change procedures during the tax year

for which the change is requested, unless otherwise provided by

published guidance. See section 6.03(2) of Rev. Proc. 2015-13.

TIP

File Form 3115 with the IRS National Office at the address listed

in the Address Chart for Form 3115 below. Alternatively, Form

3115 may be submitted by secure electronic facsimile or

encrypted electronic mail. File Form 3115 as early as possible

during the year of change to provide adequate time for the IRS to

respond prior to the due date of the filer's return for the year of

change.

The IRS normally sends an acknowledgment of receipt within

60 days after receiving a Form 3115 filed under the

non-automatic change procedures. If the filer does not receive

an acknowledgment of receipt for a non-automatic change

request within 60 days, the filer can inquire to:

Internal Revenue Service

Control Clerk

CC:IT&A, Room 4512

1111 Constitution Ave. NW

Washington, DC 20224

In specified circumstances, you are required to send

additional copies of Form 3115 to another IRS

address. For example, another copy of Form 3115

would be sent when an applicant is under examination, before

an Appeals office, or before a federal court, or is a certain foreign

corporation or certain foreign partnership. See section 6.03(3) of

Rev. Proc. 2015-13 for more information. Also see the

instructions for Part II, lines 6 and 8, later.

Address Chart for Form 3115

File Form 3115 at the applicable IRS address listed below.

A non-automatic change

request

An automatic change

request (Form 3115 copy)

Delivery by mail Internal Revenue Service

Attn: CC:PA:LPD:TSS

P.O. Box 7604

Benjamin Franklin Station

Washington, DC 20044

Internal Revenue Service

Ogden, UT 84201

M/S 6111

Delivery by

private delivery

service

Internal Revenue Service

Attn: CC:PA:LPD:TSS

Room 5336

1111 Constitution Ave. NW

Washington, DC 20224

Internal Revenue Service

1973 N. Rulon White Blvd.

Ogden, UT 84201

Attn: M/S 6111

Delivery by

facsimile

877-773-4950 (Secure) 844-249-8134

Delivery by

encrypted

electronic mail

gov

N/A

Late Application

In general, a filer that fails to timely file a Form 3115 will not be

granted an extension of time to file except in unusual and

compelling circumstances. See section 6.03(4)(b) of Rev. Proc.

2015-13 and Regulations section 301.9100-3 for the standards

that must be met. For information on the period of limitations,

see section 5.03(2) of Rev. Proc. 2023-1.

However, an automatic 6-month extension from the due date

(excluding any extension) of the federal income tax return to file

Form 3115 may be available for automatic change requests. For

details, see section 6.03(4)(a) of Rev. Proc. 2015-13, and

Regulations section 301.9100-2.

An applicant submitting a ruling request for an extension of

time to file Form 3115 must pay a user fee for its extension

request and, in the case of a non-automatic change request, a

separate user fee for its accounting method change request. For

the schedule of user fees, see section (A)(3)(b), (A)(4), and (A)

(5)(d) in Appendix A of Rev. Proc. 2023-1.

CAUTION

!

-2-

Page 3 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Useful Items

Refer to the following items for more information on changing an

accounting method.

Rev. Proc. 2023-1. See Rev. Proc. 2023-1. This revenue

procedure provides specific and additional procedures for

requesting an accounting method change, including the user fee

for non-automatic method of change requests.

Rev. Proc. 2015-13. See Rev. Proc. 2015-13. This revenue

procedure provides the automatic and non-automatic method

change procedures to obtain consent of the IRS to change an

accounting method.

Rev. Proc. 2022-14. See Rev. Proc. 2022-14. This revenue

procedure contains a list of accounting method changes that

may be eligible to file under the automatic method change

procedures.

Inflation-adjusted amount. Certain automatic accounting

method changes require that the applicant’s average annual

gross receipts for the 3 preceding tax years be at or less than the

“inflation-adjusted amount” (set forth in an annual revenue

procedure) See, for example, DCN 22. For years beginning in

2022, the inflation adjusted amount is $27,000,000. See

Rev.

Proc. 2021-45.

Pub. 538, Accounting Periods and Methods. This

publication provides general information on accounting

methods.

Specific Instructions

Name(s) and Signature(s)

Enter the name of the filer on the first line of page 1 of Form

3115.

In general, the filer of Form 3115 is the applicant. However, in

circumstances where Form 3115 is filed on behalf of the

applicant, enter the filer's name and identification number on the

first line of Form 3115 and enter the applicant's name and

identification number on the fourth line. Receivers, trustees, or

assignees must sign any Form 3115 they are required to file.

If Form 3115 is filed for multiple (i) applicants in a

consolidated group of corporations, (ii) applicants with a

common sponsor, (iii) CFCs, (iv) wholly owned partnerships

within a consolidated group, and/or (v) separate and distinct

trades or businesses (including QSubs or single-member LLCs),

attach a schedule listing each applicant and its identification

number (where applicable). This schedule may be combined

with the information requested for Part III, line 24a (regarding the

user fee), and Part IV (section 481(a) adjustment). If multiple

names and signatures are required (for example, in the case of

CFCs—see instructions below), attach a schedule labeled

“SIGNATURE ATTACHMENT” to Form 3115, signed under

penalties of perjury using the same language as in the

declaration on page 1 of Form 3115.

Individuals. If Form 3115 is filed for a couple who file a joint

income tax return, enter the names of both spouses on the first

line and the signatures of both spouses on the signature line.

Partnerships. Enter the name of the partnership on the first line

of Form 3115. In the signature section, include the signature of

one of the general partners or LLC members who has personal

knowledge of the facts and who is authorized to sign. Enter that

person's name and official title in the space provided. If the

authorized partner is a member of a consolidated group, then an

authorized officer of the common parent corporation with

personal knowledge of the facts must sign.

Non-consolidated corporations, personal service corpora-

tions, S corporations, and cooperatives. Enter the name of

the filer on the first line of Form 3115. In the signature section,

enter the signature of the officer who has personal knowledge of

the facts and authority to bind the filer in the matter. Enter that

officer's name and official title in the space provided.

Consolidated group of corporations. Enter the name of the

common parent corporation on the first line of Form 3115. Also

enter the name(s) of the applicant(s) on the fourth line if a

member of the consolidated group other than, or in addition to,

the parent corporation is requesting an accounting method

change. In the signature section, enter the signature of the

officer of the common parent corporation who has personal

knowledge of the facts and authority to bind the common parent

corporation in the matter, and that officer's name and official title

in the space provided.

Multiple entities with a common sponsor. Enter the name of

the common sponsor on the first line of Form 3115. Enter on the

fourth line the name of each entity with the common sponsor that

is requesting an accounting method change. In the signature

section, enter the signature of the officer who has personal

knowledge of the facts and authority to bind the common

sponsor and the applicants with that common sponsor in the

matter, and that officer’s name and official title in the space

provided.

Separate and distinct trade or business of an entity. Enter

the name of the entity (or common parent corporation if the entity

is a member of a consolidated group) on the first line of Form

3115. Also enter the name of the separate and distinct trade or

business requesting an accounting method change on the fourth

line. In the signature section, enter the signature of the individual

who has personal knowledge of the facts and authority to bind

the separate and distinct trade or business of the entity in the

matter, and that person's name and official title in the space

provided.

CFC or 10/50 corporation. For a CFC or 10/50 corporation

with a U.S. trade or business, enter the name of the designated

(controlling domestic) shareholder that retains the jointly

executed consent as provided for in Regulations section

1.964-1(c)(3)(ii) (or, if the designated shareholder is a member

of a consolidated group, the common parent corporation) on the

first line of Form 3115. Enter the name of the CFC or 10/50

corporation on the fourth line of Form 3115. In addition, a Form

3115 filed on behalf of the CFC or 10/50 corporation by its

controlling domestic shareholder(s) (or the common parent)

must be signed by an authorized officer of the designated

(controlling domestic) shareholder (or the common parent). If

there is more than one shareholder, the statement described in

Regulations section 1.964-1(c)(3)(ii) must be attached to the

application. Also, the controlling domestic shareholder(s) must

provide the written notice required by Regulations section

1.964-1(c)(3)(iii).

Estates or trusts. Enter the name of the estate or trust on the

first line of Form 3115. In the signature section, enter the

signature of the fiduciary, personal representative, executor,

administrator, etc., who has personal knowledge of the facts and

legal authority to bind the estate or trust in the matter, and that

person's official title in the space provided.

Exempt organizations. Enter the name of the organization on

the first line of Form 3115. In the signature section, enter the

signature of a principal officer or other person who has personal

knowledge of the facts and authority to bind the exempt

organization in the matter, and that person's name and official

title in the space provided.

Preparer (other than filer/applicant). If the individual

preparing Form 3115 is not the filer or applicant, the preparer

-3-

Page 4 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

must also sign, and include the firm's name, where applicable.

Generally, for both automatic and non-automatic changes, the

preparer (if not the filer or applicant) must sign the original and

copies of Form 3115. If Form 3115 is e-filed, the preparer need

not sign the original e-filed Form 3115 but must still complete the

preparer information and, if applicable, must sign the duplicate

automatic Form 3115 copy.

Identification Number

Enter the filer's taxpayer identification number on the first line of

Form 3115 as follows.

•

Individuals enter their social security number (SSN). For a

resident or nonresident alien, enter an individual taxpayer

identification number (ITIN). If Form 3115 is for a couple who file

a joint return, enter the identification numbers of both spouses.

•

All others enter the employer identification number (EIN).

•

If the filer is the common parent corporation of a consolidated

group of corporations or a common sponsor of multiple entities,

enter the EIN of the common parent or common sponsor on the

first line of Form 3115. If a member of a consolidated group other

than, or in addition to, the common parent, or if an entity with a

common parent, or if an entity with a common sponsor is

requesting an accounting method change, enter the EIN of the

applicant on the fourth line.

•

If the common sponsor is filing Form 3115 on behalf of

multiple applicants with that common sponsor, or if the common

parent is filing Form 3115 on behalf of multiple applicants in a

consolidated group of corporations, multiple CFCs or 10/50

corporations, or multiple and distinct trades or businesses of a

member (including QSubs or single-member LLCs), attach a

schedule listing each applicant and its identification number (if

applicable).

•

If the applicant is a foreign entity that is not otherwise required

to have or obtain an EIN, enter “Not applicable” in the space

provided for the identifying number.

Principal Business Activity Code

If the filer is a business, enter the 6-digit principal business

activity (PBA) code of the filer. The principal business activity of

the filer is the activity generating the largest percentage of its

total receipts. See the instructions for the filer's income tax return

for the filer's PBA code and definition of total receipts.

Address

Include the suite, room, or other unit number after the street

address. If the post office does not deliver mail to the street

address and the filer has a P.O. box, show the box number

instead of the street address.

Year of Change

The year of change is the first tax year the applicant uses the

proposed accounting method, even if no affected items are

taken into account for that year. Each applicant (and filer, if also

an applicant) must list its respective year of change.

Example. A calendar year taxpayer that has consistently

capitalized certain building repair costs from 2015 to 2020 files a

Form 3115 to change its method of accounting for building repair

costs to begin deducting these repair costs in 2021. The year of

change is calendar year 2021. Each applicant (and filer, if also

an applicant) must list its respective year of change.

Contact Person

The contact person must be an individual authorized to sign

Form 3115, or the filer's authorized representative. If this person

is someone other than an individual authorized to sign Form

3115, you must attach Form 2848, Power of Attorney and

Declaration of Representative.

Form 2848

Authorization to (1) represent the filer before the IRS, (2) receive

a copy of the requested letter ruling, or (3) perform any other

act(s) must be properly reflected on Form 2848. For further

details for an authorized representative and a power of attorney,

see section 9.03(8) and (9) of Rev. Proc. 2023-1.

A Form 2848 must be attached to Form 3115 in order for the

IRS to discuss a Form 3115 with the filer's representative, even if

the filer's representative prepared and/or signed the Form 3115.

If the filer intends to have the authorized representative

receive copies of correspondences regarding its Form

3115, it must check the appropriate box on Form 2848.

Fax Number for Option To Receive

Correspondence by Fax or Electronic Facsimile

Check the box to indicate whether the filer wants to receive, or

wants its authorized representative to receive, a copy of

correspondence regarding its Form 3115 (for example,

additional information letters or the letter ruling) by fax or

electronic facsimile. If the filer answered yes, the filer must

attach a statement indicating the applicant’s intention to request

to correspond by fax or electronic facsimile and include the

contact person’s fax number. The listed person(s) must be either

authorized to sign the Form 3115 or an authorized

representative of the filer that is included on Form 2848. For

further details on the fax procedures, see section 9.04(3) of Rev.

Proc. 2023-1.

Option To Receive Correspondence by

Encrypted Email Attachment

A filer that wants to receive, or wants its authorized

representative to receive, correspondence regarding its Form

3115 (for example, additional information letters or the letter

ruling) by encrypted email attachment must attach to Form 3115

a statement requesting the service. The request must specify

which email encryption method is to be used and, if the taxpayer

has not already provided the appropriate memorandums of

understanding (MOUs) to use encrypted email attachments,

must include those MOUs. For acceptable email encryption

methods and procedures, see section 9.05(3) of Rev. Proc.

2023-1.

Type of Accounting Method Change

Requested

Check the appropriate box on Form 3115 to indicate the type of

change being requested.

•

Depreciation or amortization. Check this box for a change

in (1) depreciation or amortization (for example, the depreciation

method or recovery period); (2) the treatment of salvage

proceeds or costs of removal; (3) the method of accounting for

dispositions of depreciable property; or (4) the treatment of

depreciable property from a single asset account to a multiple

asset account (pooling), or vice versa.

•

Financial products and/or financial activities of financial

institutions. Check this box for a change in the treatment of a

financial product (for example, accounting for debt instruments,

derivatives, mark-to-market accounting), or in the financial

activities of a financial institution (for example, a lending

institution, a regulated investment company, a real estate

investment trust, or a real estate mortgage investment conduit).

•

Other. For non-automatic change requests, check this box if

neither of the above boxes applies to the requested change. In

the space provided, enter a short description of the change and

the most specific applicable Code section(s) for the requested

change (for example, change within section 263A costs;

deduction of warranty expenses, section 461; or change to the

CAUTION

!

-4-

Page 5 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

completed contract method for long-term contracts, section

460).

For automatic change requests, this informational

requirement is satisfied by properly completing Part I, line 1, of

Form 3115.

As noted on Form 3115, the filer must provide all information

relevant to the requested accounting method change. All

relevant information includes all information requested on Form

3115, these instructions, and any other relevant information,

even if not specifically identified on Form 3115 or in these

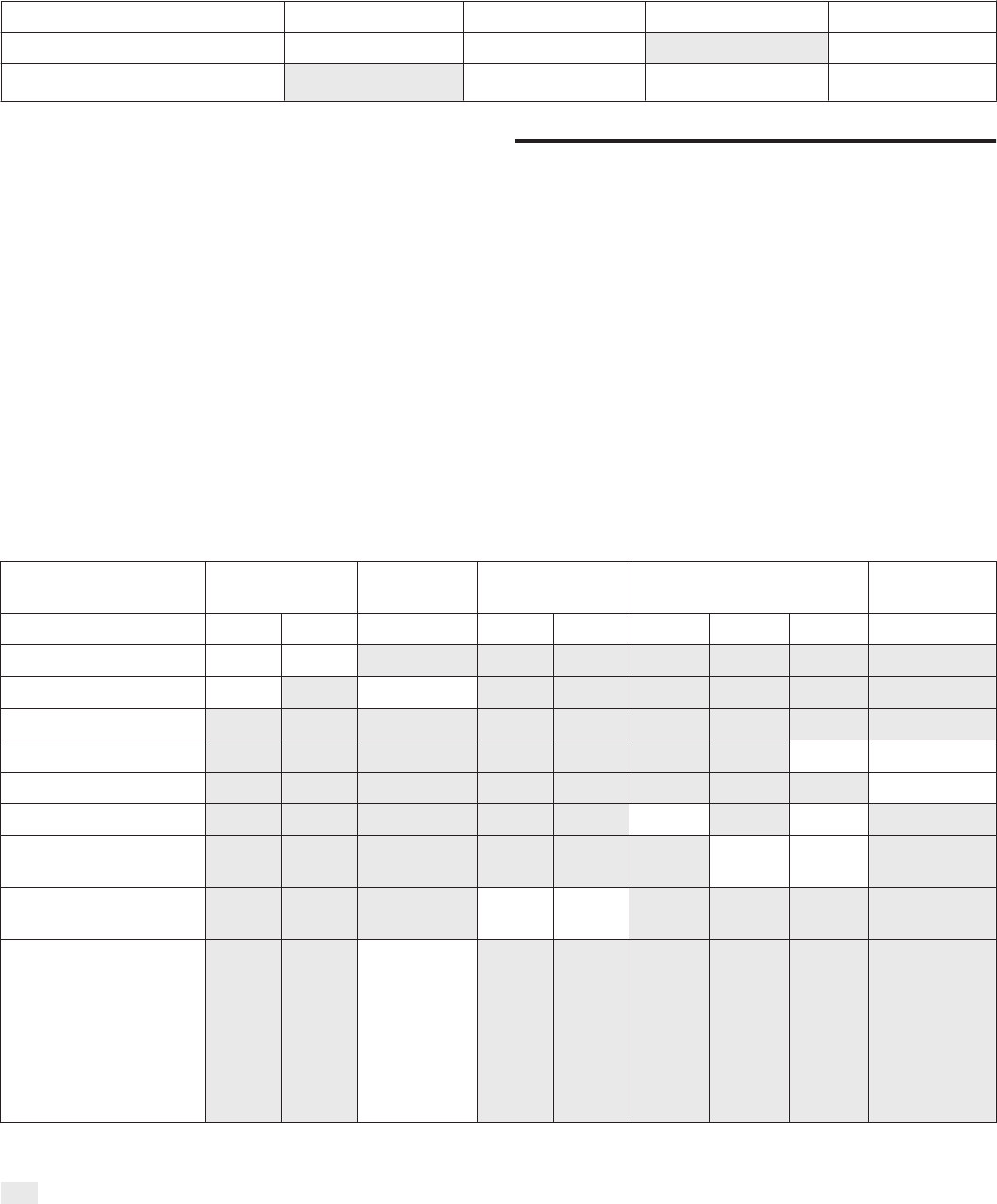

instructions. Table A illustrates, for automatic and non-automatic

changes, the Parts of Form 3115 that must be completed. Table

B illustrates the Schedule(s) to be completed for common

method changes.

Part I—Information for Automatic

Change Request

Automatic Changes—Scope and Eligibility

Rules

Line 1a. Enter the DCN on line 1a. These numbers may be

found in the List of DCNs at the end of the instructions, the List

of Automatic Changes, or in subsequently published guidance.

In general, enter a number for only one change. However, the

numbers for two or more changes may be entered on line 1a if

specifically permitted in applicable published guidance to file a

single Form 3115 for particular concurrent accounting method

changes. See section 6.03(1)(b) of Rev. Proc. 2015-13. For

example, an applicant requesting both a change to deduct repair

and maintenance costs for tangible property (DCN 184) and a

Table A: Parts To Complete on Form 3115 for Accounting Method Changes

Information to be completed for automatic and non-automatic change requests

Part I Part II Part III Part IV

Automatic Change X X X

Non-Automatic Change X X X

Table B: Schedules To Complete on Form 3115 for Common Accounting Method Changes

Information to be completed for common method change requests

Common Method

Changes

Schedule A Schedule B Schedule C Schedule D Schedule E

Part I Part II Part I Part II Part I Part II Part III

Accrual to Cash X X

Cash to Accrual X X**

Capitalize to Expense

Expense to Capitalize X* X*

Depreciation X

Long-Term Contracts X X

Inventory Valuation

Change

X X*

LIFO Change—Including

Pooling

X X

Revenue Recognition

Change for Deferral

Method for Advance

Payments, Cost Offset

Methods, and/or

Applicable Financial

Statement Income

Inclusion Rule

X

X Must fully complete section

Section does not need to be completed.

X* To be completed if applicable—See instructions regarding Schedules D and E, later

X** To be completed if applicable—See instructions regarding Schedule B, later.

-5-

Page 6 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

change to capitalize acquisition or production costs (DCN 192)

may file a single Form 3115 for both changes by including both

DCNs 184 and 192 on line 1a of Form 3115.

Line 1b. If the accounting method change is not included in the

List of Automatic Changes or assigned a number in the

published guidance providing the automatic accounting method

change, check the box for “Other” on line 1b and identify the

revenue procedure or other published guidance under which the

automatic accounting method change is being requested.

Line 2. If “Yes,” provide an explanation as to why the

applicant(s) qualifies to file under the automatic change

procedures. If other published guidance provides for an

automatic accounting method change not listed in the List of

Automatic Changes, attach a statement citing the guidance. For

example, for an applicant electing out of certain exemptions from

securities dealer status to the mark-to-market method under

section 475, attach a statement citing Rev. Proc. 97-43. If the

eligibility rules otherwise restrict the applicant from requesting

the change under the automatic change procedures, but such

rules are waived for the requested change, then check “No.”

Certain automatic method change requests require

concurrent method changes to be made in order to

qualify for the automatic change procedures. For

example, a taxpayer making a change for accrued bonuses

under DCN 133 must make the concurrent UNICAP change if

the taxpayer is subject to section 263A but is not capitalizing the

accrued bonuses under section 263A.

Generally, an applicant is only eligible to use the automatic

change procedures of Rev. Proc. 2015-13 if it satisfies the

following requirements (see section 5.01(1) of Rev. Proc.

2015-13).

1. On the date the applicant files a Form 3115, the change is

described in the List of Automatic Changes.

2. On the date the applicant files a Form 3115, the applicant

meets all requirements for the change provided in the applicable

section of the List of Automatic Changes.

3. The requested change is not to the principal method

under Regulations sections 1.381(c)(4)-1(d)(1) or

1.381(c)(5)-1(d)(1).

4. The requested year of change is not the final year of the

trade or business (but see the instructions for line 4).

5. For an overall method of accounting change, the

applicant has not made or requested an overall method change

during any of the 5 tax years ending with the year of change.

6. The applicant has not made or requested a change for

the same item during any of the 5 tax years ending with the year

of change, and

7. In the case of a taxpayer that uses the AFS cost offset

method in Regulations section 1.451-3(c) and/or the advance

payment cost offset method in Regulations section 1.451-8(e)

and wants to make a cost-offset related inventory method

change, as defined in section 5.06 of Rev. Proc. 2015-13, as

modified by section 4.02 of Rev. Proc. 2021-34, 2021-35 I.R.B.

337 (that is described in the List of Automatic Changes) the

taxpayer makes a concurrent change under section 16.10(2)(a)

(iii)(E) and/or section 16.10(2)(a)(iv)(F) or section 16.10(2)(b)(ii)

(E) of Rev. Proc. 2022-14, as applicable.

Note. Some automatic changes in methods of accounting waive

some of the above requirements. These changes may be found

in the List of Automatic Changes or the published guidance

providing the automatic accounting method change.

Line 3. The filer must complete Form 3115, including any

required statements or attachments. See Table A for the Form

3115 Part(s) required to be completed for all automatic and

CAUTION

!

non-automatic change requests. See

Table B for a sample of

common method changes and the Form 3115 Schedule(s) to be

completed for each. Additionally, see published guidance for any

additional required information or statements. For example, an

applicant that wants to use the mark-to-market method of

accounting under section 475(e) or (f) (DCN 64) must, by the

due dates provided in section 5.03 of Rev. Proc. 99-17, file a

statement that satisfies the requirements of section 5.04 of Rev.

Proc. 99-17.

Part II—Information for All Requests

Line 4. If no, check “No.” If yes, check “Yes” and attach a

statement explaining why the applicant is eligible to change its

accounting method. For example, specific guidance may permit

an applicant to change its method of accounting in its final tax

year. See section 5.03(2) of Rev. Proc. 2015-13 and sections

6.01 (DCN 7) and 6.07 (DCN 107) of Rev. Proc. 2022-14, or any

successor.

Ordinarily, the IRS will not consent to a request for an

accounting method change when an applicant ceases to engage

in the trade or business or terminates its existence. Generally,

an applicant is considered to cease to engage in a trade or

business if the applicant terminates its existence for federal

income tax purposes, ceases operation of the trade or business,

or transfers substantially all the assets of the trade to another

taxpayer. For example, a cessation of a trade or business occurs

when a trade or business is incorporated or the assets of the

trade or business are contributed to a partnership. See sections

3.04, 5.01, and 5.03 of Rev. Proc. 2015-13.

Line 5. When an acquiring corporation operates the trades or

businesses of the parties as separate and distinct trades or

businesses after the date of distribution or transfer, the acquiring

corporation must use a carryover method. See Regulations

sections 1.381(c)(4)-1(a)(2) and 1.381(c)(5)-1(a)(2). On the

other hand, when the acquiring corporation does not operate the

trades or businesses of the parties as separate and distinct

trades or businesses after the date of distribution or transfer, the

acquiring corporation will generally use the principal method.

The applicant does not need to secure the Commissioner's

consent to use the principal method. See Regulations sections

1.381(c)(4)-1(d)(1) and 1.381(c)(5)-1(d)(1).

Line 6a. Generally, the applicant is under examination with

respect to a federal income tax return as of the date the

applicant (or filer) is contacted in any manner by a representative

of the IRS for the purpose of scheduling or conducting any type

of examination of the return. See section 3.18 of Rev. Proc.

2015-13.

Line 6b. Generally, the applicant's accounting method is an

issue under consideration if the examining agent has given the

applicant (or filer) written notification specifically citing the

treatment of the item as an issue under consideration. If an

examining agent does not propose an adjustment for the item

that is an issue under consideration during the examination, the

item continues to be an issue under consideration after the

examination ends only if the issue is placed in suspense. The

applicant's accounting method is an issue placed in suspense if

the examining agent has given the applicant (or filer) written

notification of the IRS's intent to examine the issue during the

examination of the subsequent tax year(s) to be examined. See

section 3.08 of Rev. Proc. 2015-13. A partnership or an S

corporation has an issue under consideration before

examination if the same item is an issue under consideration in

an examination of a partner’s, member’s, or shareholder's

federal income tax return. For consolidated groups, see section

3.08 of Rev. Proc. 2015-13 for issue under consideration rules.

-6-

Page 7 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

For CFCs and 10/50 corporations, the issue under

consideration rules are different. See section 3.08(4) of

Rev. Proc. 2015-13.

Lines 6c and 6d. If you answered “Yes” to line 6a, include the

name and telephone number of the examining agent, and the tax

year(s) under examination in the designated places on line 6c.

For any present or former consolidated groups, if there is a tax

year under examination, complete the information on line 6c.

Provide a copy of Form 3115 to the examining agent no later

than the date the filer timely files Form 3115. See section 6.03(3)

(a) of Rev. Proc. 2015-13.

Line 7a. In general, audit protection applies when an

application for change in accounting method is granted. See

section 8.01 of Rev. Proc. 2015-13. For exceptions where audit

protection is not provided, see section 8.02 of Rev. Proc.

2015-13. You should answer “Yes” even if you do not receive

audit protection when the change is granted but might receive it

at the end of the exam under section 8.02(1)(f) of Rev. Proc.

2015-13. For example, a change made under DCN 17 for an

applicant that wants to change its treatment of research and

experimental expenditures does not receive audit protection.

See the List of Automatic Changes for additional method

changes not subject to audit protection. If you are making a

change on behalf of one or more applicants that are CFCs or

10/50 corporations and audit protection is unavailable for any

such applicants for one or more years due to the application of

section 8.02(5) of Rev. Proc. 2015-13, you should check “No”

and attach an explanation stating the applicants and the years

for which there is no audit protection under section 8.02(5).

If no audit protection is given for the requested change, check

“No” and attach an explanation. For example, if you are making a

change under DCN 17, your explanation is DCN 17. If you are

making a change under DCN 7, your explanation could be that

none of the items on line 7b apply. If multiple items are being

changed on one Form 3115 and at least one item has audit

protection and another item does not have audit protection,

check both “Yes” and “No.”

Line 7b. Generally, the applicant receives audit protection for

tax years prior to the year of change if they fall into one of the

following categories listed below. If Form 3115 is being filed on

behalf of multiple applicants or if multiple items are being

changed on one Form 3115, check all that apply and attach a

statement identifying which category applies to which applicant

or item. Except for “Not under exam” and “Other,” the following

only apply to applicants under examination.

•

Not under exam. Check this box if (A) the applicant is not

under exam, and (B) audit protection applies to the item(s) being

changed.

•

3-month window. The 3-month window is the period

beginning on the 15th day of the 7th month following the close of

the applicant's tax year and ending on the 15th day of the 10th

month following the close of the applicant's tax year. For

52-53-week applicants, the tax year begins on the 1st day of the

calendar month nearest to the 1st day of the 52-53-week tax

year. See Rev. Proc. 2015-33. For applicants with a short tax

year ending before the 15th day of the 10th month after the short

tax year begins, the 3-month window is the period beginning on

the 1st day of the 2nd month preceding the month in which the

short tax year ends and ending on the last day of the short tax

year. An applicant qualifies under the 3-month window period

when (A) it has been under examination for at least 12

consecutive months as of the 1st day of the 3-month window,

and (B) the accounting method for the same item the applicant is

requesting to change is not an issue under consideration. See

section 8.02(1)(a) of Rev. Proc. 2015-13. Checking this box

satisfies the statement requirement of section 8.02(1)(a)(iv) of

Rev. Proc. 2015-13.

CAUTION

!

•

120-day window period. The 120-day window is the

120-day period following the date an examination of the

applicant ends, regardless of whether a subsequent examination

has commenced. An applicant qualifies under the 120-day

window period if Form 3115 is filed in a 120-day window and the

accounting method for the same item the applicant is requesting

to change is not an issue under consideration. See section

8.02(1)(b) of Rev. Proc. 2015-13. If the applicant checks this

box, also include the date the examination ended in the

designated space on line 7b.

•

Method not before the director. The present method is not

before the director when it is (A) a change from a clearly

permissible method of accounting or (B) a change from an

impermissible method of accounting and the impermissible

method was adopted subsequent to the tax year(s) under

examination on the date the applicant files Form 3115. Checking

this box satisfies the statement requirement of section 8.02(1)(c)

(ii) of Rev. Proc. 2015-13.

•

Change resulting in a negative adjustment. Check this

box if the change results in a negative adjustment. A negative

adjustment occurs where an item (A) results in a negative

section 481(a) adjustment for that item for the year of change,

and (B) would have resulted in a negative section 481(a)

adjustment in each tax year under examination if the change in

accounting method for that item had been made in the tax

year(s) under examination. Checking this box satisfies the

statement requirement in section 8.02(1)(e)(iii) of Rev. Proc.

2015-13.

•

CAP. This box applies only to consolidated group members

participating in the compliance assurance process (CAP). In

general, audit protection applies to a new member if the new

member is under audit solely by joining a consolidated group

that participates in the CAP. See section 8.02(1)(d) of Rev. Proc.

2015-13. Checking this box satisfies the statement requirement

of section 8.02(1)(d)(ii) of Rev. Proc. 2015-13. If the applicant

checks this box, include the date the member joined the

consolidated group in the designated space on line 7b.

•

Other. The List of Automatic Changes or other guidance

published in the I.R.B. may provide applicants with audit

protection. For example, specific guidance may provide a filer

under exam with audit protection. If this box is checked, attach a

statement citing the guidance providing audit protection.

•

Audit protection at end of exam. If the applicant does not

fall into one of the categories listed above for line 7b, this box

should generally be checked. The applicant may receive audit

protection at the end of the examination, provided the examining

agent does not propose an adjustment for the same item and the

accounting method for that same item is not an issue under

consideration. For certain foreign corporations, the applicant

must satisfy additional requirements in order to receive audit

protection at the end of the examination. See section 8.02(1)(f)

of Rev. Proc. 2015-13.

For CFCs and 10/50 corporations, the rules for audit

protection are different. See section 8.02 of Rev. Proc.

2015-13 (different rules for the 3-month window,

120-day window, and audit protection at end of exam).

Line 8a. If you answered “Yes,” complete lines 8b–d.

Line 8b. To determine if the applicant’s accounting method is

an issue under consideration by Appeals and/or a federal court,

see sections 3.08(2) and 3.08(3) of Rev. Proc. 2015-13.

Line 8c. If you answered “Yes” to line 8a, include the name and

telephone number of the Appeals officer(s) and/or counsel to the

government, as well as the tax year(s) before Appeals and/or

federal court in the designated places.

Line 8d. If you answered “Yes” for line 8a, provide a copy of the

signed Form 3115 to the Appeals officer(s) and/or all counsel to

the government, as applicable, no later than the date the filer

CAUTION

!

-7-

Page 8 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

timely files Form 3115. See section 6.03(3)(a) of Rev. Proc.

2015-13.

Line 9. If you answered “Yes” to line 6a or 8a, complete line 9.

The information requested on line 9 should be included on a

separate attachment.

Line 10. If you answered “Yes,” attach an explanation. Unless

otherwise provided, the applicant does not receive audit

protection for the requested change if it is an issue under

consideration. See sections 3.08 and 8.02(7) of Rev. Proc.

2015-13.

Lines 11a–c. Unless otherwise provided, an applicant is not

eligible to file under the automatic change procedures if the

applicant made or requested a prior overall method change or a

prior item change (for the same item) within the 5 tax years

ending with the requested year of change. For additional details,

see section 9.03(6)(a) of Rev. Proc. 2023-1 and section 11.02(2)

of Rev. Proc. 2015-13.

Line 12. For further details, see section 9.03(6)(b) of Rev. Proc.

2022-1.

Line 13. If you answered “Yes,” complete Schedule A of Form

3115. For example, an overall accounting method change

includes a change from an accrual method to the cash receipts

and disbursements method or vice versa. See section 446(c).

Line 14. Provide the information requested on lines 14a–d if the

applicant answered “No” to question 13 or if the applicant

answered “Yes” to question 13 and is also changing to a special

accounting method for one or more items.

With the information requested on line 14b, the applicant is

also required to provide a statement of whether or not the

applicant has claimed any federal tax credit, grant, or subsidy

relating to the item(s) being changed (for example, the employee

retention credit for a change in method related to payroll taxes).

A special accounting method for an item is an accounting

method (other than the cash method or an accrual method)

expressly permitted by the Code, regulations, or guidance

published in the I.R.B. that deviates from the rules of sections

446, 451, and 461 (and the related regulations) that is applicable

to the applicant's overall accounting method (proposed overall

method if being changed). For example, the installment

accounting method under section 453, the mark-to-market

method under section 475, and the long-term contract method

under section 460 are special methods of accounting. See

section 15.01(2)(d) of Rev. Proc. 2022-14.

Lines 15a and 15b. Provide the requested information for each

applicant. For guidance on using different methods of

accounting for each trade or business, see section 446(d).

An applicant may include each member of a consolidated

group, each wholly owned partnership within a consolidated

group, each separate and distinct trade or business of each

member of a consolidated group or other entity (even if the

change is for all of a member's or other entity's trades or

businesses), and each eligible CFC or 10/50 corporation filing a

single Form 3115 requesting the identical accounting method

change. Also see

Who Must File, earlier.

Lines 16a–c. For non-automatic changes, the applicant is

required to provide a full explanation of the legal basis to support

the proposed method, including all authorities supporting the

proposed method, and a discussion of all contrary authorities.

For further details on what is to be included, see Rev. Proc.

2023-1, sections 7.01(9) (statement of supporting authorities),

9.03(1) (facts and other information), 9.03(2) (statement of

contrary authorities), 9.03(4) (analysis of material facts), and

9.03(7) (statement identifying pending legislation).

For the following automatic method changes, the applicant is

only required to complete lines 16a–b, unless the information on

lines 16a–b is otherwise provided in the applicable Form 3115

Schedules A–E: DCNs 6, 7, 28, 54, 55, 64, 65, 108, 111, 114,

127, 194, and 200 (only for changes listed in sections 6.12(3)(a)

(ix), 6.12(3)(a)(x), and 6.12(3)(b)(viii) in the List of Automatic

Changes; 205 (only for changes listed in sections 6.13(3)(h) and

6.13(3)(j) in the List of Automatic Changes); 206 (only for

changes listed in sections 6.14(3)(a), 6.14(3)(h), and 6.14(3)(j)

in the List of Automatic Changes; 207 (only for changes listed in

sections 6.15(3)(a) and 6.15(3)(d) in the List of Automatic

Changes); 211, 218, 231, 237, 241, 242, 250, 251, 252, 253,

254, 255, and 256. Line 16c does not need to be completed for

applicants filing automatic method changes. For further details

on what is to be included, see Rev. Proc. 2023-1, sections

7.01(9) (statement of supporting authorities), 9.03(1) (facts and

other information), and 9.03(4) (analysis of material facts).

If the automatic DCN is not specifically listed in the paragraph

above, or subsequent guidance released after the issuance of

these instructions, skip lines 16a–c.

Line 17. Insurance companies must also attach a statement

indicating whether the proposed accounting method will be used

for annual statement accounting purposes.

Line 18. For details on requesting and scheduling a

conference, see sections 9.04(4) and 10 of Rev. Proc. 2023-1.

Lines 19a and 19b. For certain automatic method changes, the

applicant must demonstrate that it meets the gross receipts test

under section 448(c) to qualify for the change. This gross

receipts test is met if a taxpayer has average annual gross

receipts for the 3 prior tax years at or below the inflation-adjusted

amount. See

Useful Items earlier, for guidance on the

inflation-adjusted amounts.

For the calculation of gross receipts for an overall accounting

method change request, whether an applicant qualifies as a

small business taxpayer for purposes of applying sections 263A

and 471, or whether an applicant qualifies as an eligible small

business under section 474(c), see section 448(c) and

Regulations section 1.448-2(c), and, as applicable, Regulations

section 1.263A-1(b)(1)(j) or Regulations section 1.471-1(a)(2).

For the calculation of gross receipts for determining whether

the applicant has an exempt construction contract under

Regulations section 1.460-3(b), for contracts entered into after

December 31, 2017, in tax years ending after December 31,

2017, see section 448(c) and Regulations sections 1.448-2(c)

and 1.460-3(b)(3).

Part III—Information for

Non-Automatic Change Request

Non-automatic change—scope and eligibility rules. An

applicant may not use the non-automatic change procedures if

any of the following eligibility limitations apply at the time Form

3115 is filed with the IRS National Office.

1. The change in accounting method is required to be made

according to a published automatic change procedure, such as

Rev. Proc. 2022-14.

2. The requested year of change is the final year of the trade

or business, unless (a) the change is a result of a transaction to

which section 381(a) applies; or (b) the applicant demonstrates

to the satisfaction of the IRS National Office compelling

circumstances, or that it is in the interest of sound tax

administration for the applicant to change in its final year.

Line 20. If you answered “Yes,” attach an explanation

describing why the applicant is not eligible to file a request under

the automatic change procedures.

-8-

Page 9 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Line 21. Attach true copies of all contracts, agreements, and

other documents directly related to the proposed accounting

method change. See section 9.03(3) of Rev. Proc. 2023-1.

Line 22. Include a statement explaining the reason for the

proposed change. See sections 7.01(1)(d) and 9.03(1) of Rev.

Proc. 2023-1.

Line 23. If you answered “No” to line 23, a common parent

requesting an accounting method change on behalf of a member

of the consolidated group must attach a statement explaining the

accounting method used by each member of the consolidated

group for the particular item that is the subject of the method

change request. See section 6.02(5) of Rev. Proc. 2015-13.

Lines 24a and 24b. For non-automatic change requests, you

must pay a user fee for each applicant. Where the filer is not an

applicant, a fee is not required for the filer. See section 15 and

Appendix A of Rev. Proc. 2023-1 for information regarding user

fees, including reduced user fees and user fees for additional

applicants filing identical changes in methods of accounting.

Pay the user fees through PAY.gov.

Note. Filers filing under the automatic change procedures do

not pay a user fee.

Example 1. Filer is the common parent of a consolidated

group of corporations. Filer files a single Form 3115 on behalf of

itself and two other members of the consolidated group for an

identical accounting method change. There are three applicants

(Filer and the two other members of the consolidated group).

Therefore, for a non-automatic change request, all three

applicants are required to pay a user fee. The filer applicant

must submit the regular user fee under section (A)(3)(b)(i) of

Appendix A of Rev. Proc. 2023-1 (or a reduced fee per section

(A)(4) of Appendix A of Rev. Proc. 2023-1, if applicable), and the

two other applicants qualify for the reduced user fee under

section (A)(5)(b) of Appendix A of Rev. Proc. 2023-1.

Example 2. Filer is the common parent of a consolidated

group of corporations. Filer is filing a single Form 3115 on behalf

of two other members of the consolidated group for an identical

accounting method change. There are two applicants on Form

3115 (the two members of the consolidated group). Filer is not

changing its accounting method and, therefore, does not pay a

fee on account of itself. For a non-automatic change request,

both applicants are required to pay a user fee. One applicant

must submit the regular user fee under section (A)(3)(b)(i) of

Appendix A of Rev. Proc. 2023-1 (or a reduced fee per section

(A)(4) of Appendix A of Rev. Proc. 2023-1, if applicable), and the

other applicant qualifies for the reduced user fee under section

(A)(5)(b) of Appendix A of Rev. Proc. 2023-1. This example

applies similarly to a filer that is the common sponsor of multiple

entities.

Example 3. Filer, a single taxpayer, files Form 3115 on

behalf of its three separate and distinct trades or businesses.

The request is for an identical accounting method change.

Notwithstanding that Filer is a single taxpayer, there are three

applicants on Form 3115. For a non-automatic change request,

all three applicants are required to pay a user fee. One applicant

must submit the regular user fee under section (A)(3)(b)(i) of

Appendix A of Rev. Proc. 2023-1 (or a reduced fee per section

(A)(4) of Appendix A of Rev. Proc. 2023-1, if applicable), and the

other two applicants qualify for the reduced user fee under

section (A)(5)(b) of Appendix A of Rev. Proc. 2023-1.

Part IV—Section 481(a) Adjustment

Line 25. Ordinarily, an adjustment under section 481(a) is

required for accounting method changes. The section 481(a)

adjustment period is generally 1 tax year (year of change) for a

negative section 481(a) adjustment and 4 tax years (year of

change and next 3 tax years) for a positive section 481(a)

adjustment. However, when an applicant is under examination,

the section 481(a) adjustment period is 2 tax years (year of

change and next tax year) for a positive section 481(a)

adjustment for a requested accounting method change unless

one of the following categories described on line 7b applies:

3-month window, 120-day window period, method not before the

director, or CAP.

For some accounting method changes, there may be special

rules relating to the section 481(a) adjustment period. See, for

example, section 16.10(4)(b)(iv)(D) of Rev. Proc. 2022-14

pertaining to certain section 451 cost offset accounting method

changes resulting from concurrent cost-offset related inventory

method changes.

Also, for certain accounting method changes, the applicant

must make the change on a cut-off basis or modified cut-off

basis. See, for example, Regulations section 1.446-1(e)(2)(ii)

(d)

(5)(iii). In those cases, there is no section 481(a) adjustment.

Under a cut-off basis, only the items arising on or after the

beginning of the year of change are accounted for under the new

method of accounting. Any items arising before the year of

change continue to be accounted for under the applicant's

former accounting method.

For a change in accounting method for accruing a foreign

income tax expense, do not compute a section 481(a)

adjustment. Instead, apply the modified cut-off rules in

Regulations section 1.905-1(d)(5). Attach a statement showing,

for each separate statutory or residual grouping, the upward and

downward adjustment (accounted for in the currency in which

the foreign tax liability is denominated) that is required by

Regulations section 1.905-1(d)(5)(ii). Provide a separate upward

and downward adjustment for foreign income taxes for which the

foreign tax credit is disallowed and to which section 275(a)(4)

does not apply. See Regulations section 1.905-1(d)(5) and the

examples in Regulations section 1.905-1(d)(6) for additional

information.

If multiple items are being changed on one Form 3115 and at

least one item is changed on a cut-off basis or modified cut-off

basis and another item is changed with a section 481(a)

adjustment, check both “Yes” and “No” and attach a statement

identifying which item(s) is being made on a cut-off basis or

modified cut-off basis.

An eligible terminated S corporation (as defined in section

481(d)(2)) that is required to change an accounting method as a

result of a revocation of its S corporation election must take into

account the resulting positive or negative section 481(a)

adjustment ratably during the 6-year period beginning with the

year of change. In addition, an eligible terminated S corporation

that is permitted to continue to use the cash method after the

revocation of its S corporation election and that changes to an

overall accrual method for the C corporation’s first tax year after

such revocation may take into account the resulting positive or

negative adjustment required by section 481(a)(2) ratably during

the 6-year period beginning with the year of change. See Rev.

Proc. 2018-44, 2018-37 I.R.B. 426. Section 481(d)(2) defines an

eligible terminated S corporation as any C corporation that (1)

was an S corporation on December 21, 2017; (2) revokes its S

corporation election after December 21, 2017, but before

December 22, 2019; and (3) has the same owners of stock in

identical proportions on December 22, 2017, and the revocation

date.

If the accounting method change is an automatic change in

functional currency under section 985 (see section 29.01 of Rev.

Proc. 2022-14), the adjustments required under Regulations

section 1.985-5 must be made on the last day of the tax year

ending before the year of change. Any gain or loss that must be

recognized under Regulations section 1.985-5 is included in

income or earning and profits on the last day of the tax year

-9-

Page 10 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

ending before the year of change, and is not subject to section

481. Attach a statement showing the adjustment required under

Regulations section 1.985-5. The statement should include the

amount of the adjustment required pursuant to Regulations

section 1.985-5, a summary of the computation of such

adjustment, and an explanation of any other adjustments

required by Regulations section 1.985-5.

Except if instructed differently, you must attach a statement

showing the (net) section 481(a) adjustment for each change in

method for each applicant included on Form 3115. Include a

summary of how the (net) section 481(a) adjustment was

computed and an explanation of the methodology used to

determine it. The summary of computation and explanation must

be sufficient to demonstrate that the (net) section 481(a)

adjustment is computed correctly. If the applicant is a CFC or

10/50 corporation, or a trade or business of a CFC or 10/50

corporation, and its functional currency is not the U.S. dollar,

state the (net) section 481(a) adjustment in that functional

currency. The statement may be combined with the information

requested on the fourth line on page 1 (list the applicants and

their identification numbers) and on line 24 (user fee).

Section 481(a) adjustments (or components of section

481(a) adjustments) from changes under DCN 248

included in the same Form 3115 must be stated in

accordance with section 6.22(8) of Rev. Proc. 2022-14.

Example 1. Under its present method, XYZ Corporation is

deducting certain costs that are required to be capitalized into

inventory under section 263A. XYZ Corporation is proposing to

change its account method to properly capitalize such costs.

The computation of the section 481(a) adjustment with respect

to the accounting method change is demonstrated as follows.

Beginning inventory for year of change under

proposed method ................. $120,000

Beginning inventory for year of change under present

method .......................

$100,000

Section 481(a) adjustment .............. +$20,000

Example 2. WXY Corporation, a calendar year taxpayer, is a

producer and capitalizes costs that are required to be capitalized

into inventory under section 263A. Each February, WXY

Corporation pays a salary bonus to each employee who remains

in its employment as of January 31 for the employee's services

provided in the prior calendar year. Under its present method,

WXY Corporation treats these salary bonuses as incurred in the

tax year the employee provides the related services. For 2022,

WXY Corporation proposes to change its accounting method to

treat salary bonuses as incurred in the tax year in which all

events have occurred that establish the fact of the liability to pay

the salary bonuses and the amount of the liability can be

determined with reasonable accuracy, pursuant to section

20.01(2) of Rev. Proc. 2022-14. The computation of WXY

Corporation's net section 481(a) adjustment for the change in

accounting method for salary bonuses is demonstrated as

follows.

CAUTION

!

Salary bonuses treated as incurred

under the present method, but not

incurred under the proposed

method ................ $40,000

Beginning inventory as of January. 1,

2022, with capitalized salary bonuses

computed under the present

method ................ $100,000

Beginning inventory as of January. 1,

2022, with capitalized salary bonuses,

computed under the proposed

method ................

$92,000

Decrease in beginning inventory as of

January. 1, 2022 ...........

($8,000)

Net section 481(a) adjustment .... +$32,000

Line 26. In computing the net section 481(a) adjustment, an

applicant must take into account all relevant accounts. For some

changes (for example, a change that affects multiple accounts),

the section 481(a) adjustment is a net section 481(a)

adjustment. See

Example 2 above and the example under

Schedule A, Part l, line 2h, later. If there is more than one

method change requested, the section 481(a) adjustment is

generally separately stated for each method change. However,

some changes may require the netting of section 481(a)

adjustments with those for certain other method changes made

during the same year of change. See, for example, certain

changes under section 16.10 of Rev. Proc. 2022-14.

If an election has been made under Regulations section

1.59A-3(c)(6)(i) to waive an allowed deduction for purposes of

determining the section 59A base erosion and anti-abuse tax,

and the method of accounting for the waived deduction is being

changed, the amount of the net section 481(a) adjustment is

determined without regard to the waived deduction. See

Regulations section 1.59A-3(c)(6)(iii)(D). As a result, a waived

deduction has no effect on the calculation of the amount of a

section 481(a) adjustment. For an example illustrating how to

calculate a section 481(a) adjustment with respect to a method

of accounting for which an applicant has waived deductions, see

Regulations 1.59A-3(d)(9)

(Example 9).

Line 27. Certain automatic method changes require an

applicant with a section 481(a) adjustment remaining on a prior

change in accounting method to take the remaining portion of

the prior section 481(a) adjustment into account in the year of

change. See, for example, DCNs 234 and 262. If applicable,

enter the amount of the remaining portion of the section 481(a)

adjustment from the prior change.

Line 28. An applicant may elect a 1-year section 481(a)

adjustment period for a positive section 481(a) adjustment that is

less than $50,000. See section 7.03(3)(c) of Rev. Proc. 2015-13.

An applicant may also elect a 1-year section 481(a) adjustment

period for all positive section 481(a) adjustments for the year of

change if an eligible acquisition transaction occurs during the

year of change or in the subsequent tax year on or before the

due date for filing the applicant's federal tax return for the year of

change. For more details about the eligible acquisition

transaction election, see section 7.03(3)(d) of Rev. Proc.

2015-13.

Line 29. If “Yes,” explain the nature and amount of the section

481 adjustment attributable to the intercompany transaction(s).

-10-

Page 11 of 34 Fileid: … ns/i3115/202212/a/xml/cycle05/source 9:08 - 7-Feb-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Schedule A—Change in Overall

Method of Accounting

Part I—Change in Overall Method

All applicants filing to change their overall accounting method

must complete Schedule A, Part I, including applicants filing

under DCNs 122, 126, 127, 128, 233, 257, 258, and 259 in the

List of Automatic Changes.

Lines 2a–g. Enter the amounts requested on lines 2a through

2g, even though the calculation of some amounts may not have

been required in determining taxable income due to the

applicant's present accounting method. Applicants with an

applicable financial statement changing to an accrual method

and entering an amount on line 2a should complete Schedule B

if the income is subject to section 451(b).

Note. Do not include amounts that are not attributable to the

accounting method change, such as amounts that correct a

math or posting error or errors in calculating tax liability. In

addition, for a bank changing to an overall cash/hybrid method of

accounting, do not include any amounts attributable to a special

method of accounting. See DCN 127.

Line 2b. Enter amounts received or reported as income in a

prior year that were not earned as of the beginning of the year of

change. For example, an advance payment received in a prior

year for goods that were not delivered by the beginning of the

year of change may be reported in the subsequent year if the

applicant qualifies under Regulations section 1.451-8(c) or (d),

as applicable. If any amounts entered on line 2b are for advance

payments, complete Schedule B.

Line 2h. Enter the net amount, which is the net section 481(a)

adjustment, on line 2h. Also, enter the net section 481(a)

adjustment on Part IV, line 26. See the instructions for Part IV,

line 26, earlier.

The following example illustrates how an applicant calculates

the section 481(a) adjustment when changing to an accrual

method, a nonaccrual-experience method, and the recurring

item exception.

Example. ABC Corporation, a calendar year taxpayer using

the cash method of accounting, has the following items of

unreported income and expense on December 31, 2021.

Accrued income ...................... $250,000

Uncollectible amounts based on

the nonaccrual-experience method ......... 50,000

Accrued amounts properly deductible

(economic performance has occurred) ....... 75,000

Expenses eligible for recurring item

exception ......................... 5,000

ABC Corporation changes to an overall accrual method, a

nonaccrual-experience method, and the recurring item

exception for calendar year 2022. The section 481(a) adjustment

is calculated as of January 1, 2022, as follows.

Accrued income (line 2a) ............ $250,000

Less:

Uncollectible amount .............. (50,000)

Net income accrued but not received .... $200,000

Less:

Accrued expenses (line 2c) .......... (75,000)

Expenses deducted as recurring item

(line 2g) .....................

(5,000)

Total expenses accrued but not paid ..... (80,000)

Section 481(a) adjustment ............ +$120,000

Line 3. Check “Yes” if the applicant is requesting to use the

recurring item exception (section 461(h)(3)). The section 481(a)

adjustment must include the amount of the additional deduction

that results from using the recurring item exception.

Line 5. Check "Yes" if the applicant is requesting a change to

the overall cash method or to a method in which a taxpayer uses

an accrual method for purchases and sales of inventories and

uses the cash method for computing all other items of income

and expense under section 15.17 of Rev. Proc. 2022-14 (DCNs

233 and 259). See section 15.17(5)(a) of Rev. Proc. 2022-14 to

determine whether an applicant qualifies as a small business

taxpayer.

Part II—Change to the Cash Method for

Non-Automatic Change Request

Limits on cash method use. Except as provided below, C

corporations and partnerships with a C corporation as a partner

may not use the cash method. Tax shelters are also precluded

from using the cash method. For this purpose, a trust subject to

tax on unrelated business income under section 511(b) is

treated as a C corporation with respect to its unrelated trade or

business activities.

The limit on the use of the cash method under section 448

does not apply to the following.

1. Farming businesses as defined in section 448(d)(1).

2. Qualified personal service corporations as defined in

section 448(d)(2).

3. C corporations and partnerships with a C corporation as a

partner that meets the section 448(c) gross receipts test for the