Assessment Introduction

Page 1 of 19

Introduction

Real Property Appraisal can be accomplished by single property appraisal or mass appraisal. The

credibility each appraisal is judged in the context of the intended use of the appraisal.

Single property appraisals are made for various purposes and involve the appraisal of a single

property as of a given date. Single property appraisals are governed by the Uniform Standards of

Professional Appraisal Practice (USPAP Standards 1 and 2) and the credibility of the appraisal is

judged against comparable sale properties used in the appraisal.

Mass appraisal involves the appraisal of many properties, a universe of properties, as of a given

date. The intended use of mass appraisals is most often for ad valorem purposes, but can be for

other intended uses. Mass appraisals are governed by USPAP – Standard 6.

Both single property and mass appraisal use three traditional approaches to value and require

market research. Both require logical and systematic methods for collecting, analyzing, and

processing data to produce supportive, well-documented value estimates. Single property

appraisal requires only one person to research and analyze data and make appraisal judgments

and decisions, while mass appraisal requires many persons performing many tasks. Appraisal

quality is measured by comparison to comparable sales.

The major difference between the two types of appraisal is the scale of the mass appraisal. It is

much larger, involving many properties, many people (coordination of tasks and appraisal

judgment), with emphasis on standardization in procedures, methods, models and tables. Mass

appraisal requires many people to contribute to the process using standardized procedures.

Quality is measured using statistical procedures to test estimated values against sale prices.

Mass Appraisal

The three traditional approaches considered in valuing real property are the cost approach, the

sales comparison approach, and the income approach. Typically, assessors use a market

calibrated cost model (cost and sales comparison approaches) in ad valorem residential mass

appraisal. For properties bought and sold on their income producing capability (commercial and

industrial property), an income capitalization approach and comparative sales approach are

typically considered.

Minimum standards on appraisal are established in the Uniform Standards of Professional

Appraisal Practice (USPAP) published by the Appraisal Foundation (Washington, DC).

Key mass appraisal concepts are:

MASS APPRAISAL: (is) the process of valuing a universe of properties as of a given date

using standard methodology, employing common data, and allowing for statistical testing.

(USPAP Definitions)

Assessment Introduction

Page 2 of 19

MASS APPRAISAL MODEL: a mathematical expression of how supply and demand factors

interact in a market. (USPAP Definitions)

Model Specification (USPAP/STD 6)

Supply and demand factors affect property value. Identification of these factors and the formal

development of a model statement or equation are called model specification.

Mass appraisers must develop mathematical models that, with reasonable accuracy, represent the

relationship between property value and supply and demand factors, as represented by

quantitative and qualitative property characteristics. The models may be specified using the cost,

sales comparison, or income approaches to value. The specification format may be tabular,

mathematical, linear, nonlinear, or any other structure suitable for representing the observable

property characteristics. Appropriate approaches must be used to value a class of properties. The

concept of recognized techniques applies to both real and personal property valuation models.

Model Calibration (USPAP/STD 6)

After a model is specified, then model calibration occurs. Calibration refers to the process of

analyzing sets of property and market data to determine the specific parameters of a model. Most

simply, it is the development of rates (coefficients) for use in the model. These include such

things building rates, land rates, depreciation rates, adjustments and other items.

Cost manual, depreciation, land rate tables are examples of calibrated parameters.

Market Calibrated Cost Approach

In mass appraisal, assessors use “production line” methods and techniques to value a “universe”

of properties. For many property types a “market calibrated” cost approach to value is used. A

basic cost model formula (specified model structure) is:

Market Value = Replacement Cost New - Depreciation + Land Value

Model calibration of a cost approach occurs by applying tables of rates for improvement costs,

depreciation, and land values. These rates are applied to each property’s relevant characteristics

to produce a land value and building value. The model is analyzed and tested; and re-applied

until acceptable results are attained. Essentially, properties that have sold are valued using this

method and analyzed via sale to assessment ratio studies and other performance measures. Once

the analysis is completed and acceptable performance measures are attained on the sample of

sales, the model (rates/coefficients) is applied to the all properties (sale and non-sale properties)

to estimate their value. Both during and following the re-appraisal, assessment performance

analysis (ratio studies) is conducted to analyze quality.

Accurate property data (relevant property characteristics) is essential for accurate property

values. Thus, the quality and quantity of data is important. Accurate values begin with accurate

data. Assessors must ensure that the appropriate data is being captured accurately and

Assessment Introduction

Page 3 of 19

consistently. Market transfers (property sales) must be timely entered into the valuation system

and existing property data characteristics must be updated for changes.

Properties should be regularly inspected to ensure existing data is accurate and current. IAAO standards

call for routine property inspections at least every six years. Many states have laws requiring more

frequent cycles. Maryland calls for inspections at least every three years. Building permits, aerial/oblique

photography, street view images and the linking of this data with the assessors valuation system allows

for a timely and efficient review and management of property record characteristics. Properties with

changes can be identified and field inspections can be made to verify data as need. In many cases, data

can be updated in the office using these technologies. The largest cost of any mass appraisal is data

collection and review

Geographic Stratification

Market or economic areas are broad geographic areas of properties subject to similar economic

influences and value trends. Subareas or neighborhoods are groupings of homes that share

similar location amenities. In mass appraisal, the universe of properties to be valued is

analyzed and valued based upon type of property within market and submarket areas.

In supporting mass appraisal values, the assessor uses current market transactions of similar

properties within a market or sub market area. The assessor uses land rates, building costs and

depreciation tables in a model to value all similar properties uniformly.

Assessment Performance

A measure of assessment quality is the assessed value to sale price ratio. In a market calibrated

cost approach, the ratio of total property estimate of value is compared to actual sale prices. The

goal is to achieving a ratio of 100%. Known as an assessment ratio study, these assessment

performance analyses are performed measure assessment quality. These studies measure the

typical level of assessment (measures of central tendency) and the variation between assessments

(coefficient of dispersion, coefficient of variation, or standard deviation). Similarly, assessment

uniformity is analyzed.

Frequency of Reassessment

Property values are constantly changing and each property is affected by market factors unique

to the each properties location, neighborhood or market area.

An underlying precept of ad valorem appraisal is uniformity of assessment – that “similar

properties” are assessed alike. Thus, all similar properties should be assessed similarly. This is

accomplished by appraising at market value.

The Maryland Constitution (Article 15 – Declaration of Rights) and law require appraisal at

market value

1

. Historically, Maryland counties have re-appraised properties on a triennial cycle.

1

Article 15 Declaration of Rights – “…General Assembly shall, by uniform rules, provide for the separate assessment,

classification and sub-classification of land, improvements on land and personal property, as it may deem proper; and

all taxes thereafter provided to be levied by the State for the support of the general State Government, and by the

Assessment Introduction

Page 4 of 19

Many counties have done this since the 1940’s. In the early 1970’s, the state law was amended

to require statewide ad valorem appraisal on a triennial cycle.

In the 1970’s and 1980’s, the state legislature conducted several legislative study groups

regarding real property assessment and enacted numerous provisions of law that govern real

property assessment, tax credits, and real property tax exemptions.

Market Value Standard

The Maryland Constitution and law require a market value appraisal standard and the assessor

must consider the level of assessment and the uniformity of assessments. These are the

underlying principles that guide the assessor.

Some suggest that the assessor should assess every property at 100% of its sale price. Assessors

do not assess to 100% of each sale price. First, all properties do not sell. When they do sell they

may not be current sales. The assessor must consider comparable sales occurring near the date

of appraisal. Also properties are not all the same; and, often the sales may not be indicative of

arms-length market transactions.

Price is a fact – list price, asking price, reduced price, sale price. Cost is a fact or an estimate of

a fact. It cost $100,000 or it will cost $125 a square foot to build. Value is an opinion based

upon fact. The assessor uses arms-length sales as comparables to estimate value.

Residential Property

Article 15 of the Maryland Declaration of Rights, is why the assessor uses a market calibrated

cost approach in valuing residential property. The valuation starts from replacement cost new

(a” common basis” for all similar properties (similar cost new on similar properties). Next,

depreciation (loss in value from all causes) is deducted from replacement cost new depreciation

(similar condition properties have similar depreciation). The result is an estimate of the

improvement value. Next an estimated land value (similar land rates for similar properties) is

added to the improvement value to produce the estimated property value. The formula is RCN –

Dep. = RCND + LV = MV.

The specification of the cost model and the application of the model on a sample of property

sales, allows the assessor calibrate the model and to test it by the use of a sales to value ratio

Counties and by the City of Baltimore for their respective purposes, shall be uniform within each class or sub-class of

land, improvements on land and personal property which the respective taxing powers may have directed to be

subjected to the tax levy;…”

Tax Property Article – Definitions (Section 1-101 (c)

"Assessment" means: (1) for real property, the phased-in full cash value

or use value to which the property tax rate may be applied; and (2) for personal property, the value to which the property tax

rate may be applied.; (pp) Valuation. -- "Valuation" means the process of determining the value of a property; Value. -- "Value"

means the full cash value of property. Case law further defines Full Cash Value as the Market Value of Property.

Assessment Introduction

Page 5 of 19

analysis. When acceptable ratio results are achieved the model is then applied to all other similar

properties. This approach causes like type of property to be assessed alike.

Commercial Property

Assessments on commercial income producing properties must, also, be uniform between like

types of properties. This is why the income approach is used. The “common basis” for income

property valuation is using market rents, market vacancy, and market expense ratios, in

developing an estimate of the properties Net Operating Income (NOI). The assessor then uses a

market capitalization rate to estimate market value. The formula is Income/Capitalization Rate =

Value. We should emphasize that this is Market Income; Market Capitalization Rate equals

Market Value.

The income approach, as with the cost approach (market calibrated cost approach), is related to

the comparative sales approach. Market Capitalization rates consider the relationship of income

to sale price. In other words, the capitalization rate is the percentage that income (NOI) is to

value (sale price). The use of market rent and market cap rates allow the assessor to treat similar

income producing properties similarly for assessment purposes.

Many do not understand the concept of the level of assessment and the uniformity/equalization

requirement for assessments and tend to think of the income capitalization approach is separate

and distinct from the comparative sales approach. The income approach and comparative sales

approach are related. Market capitalization rates must be supported by market information. To

do this, the assessor can develop capitalization rates, when they have income and expense

information on properties that have sold. This is known as the direct comparison method.

Similarly capitalization rates can be developed from the band of investment (mortgage/ equity)

method and other methods.

Sales of income producing properties are not as common as sales of non-income producing

properties or residential properties. Maryland has over 109,000 commercial parcels with

approximately 900 (0.08%) commercial sales per year. Of all commercial sales many are not

income producing properties and often property owners do not comply with the income and

expense form filling requirement, so appraisers and assessors usually subscribe to commercial

services that provide income and expense data summaries.

Discover, List, and Value

Assessment officials are to discover, list and value all property for ad valorem purposes. For real

property, discovery means to find each parcel of real property and assure that it is on the tax roll.

This is accomplished by reviewing property deeds, and adding each parcel to the jurisdiction’s

tax roll and tax maps.

Listing involves adding each property to the assessment roll and identifying the relevant property

characteristics in the assessment records needed to value the property. This includes relevant

Assessment Introduction

Page 6 of 19

quantitative and qualitative characteristics for improvements and improvement sketches, zoning,

property images, etc.

Value means developing an opinion of market value for all land and improvements to land at the

highest and best use of the property for ad valorem purposes.

Property Characteristics Changes

Modern appraisal systems, such as Computer Assisted Mass Appraisal (CAMA), greatly speed

calculations and valuation in ad valorem mass appraisal. These systems streamline valuation

sales analysis and individual property valuation. CAMA provides for more efficient assessment

performance analysis (ratio analysis, data edits, and management reports). These systems allow

linking of other technology systems which provide for efficient mass appraisal. Maryland’s

current CAMA system, known as AAVS should be linked to the various counties zoning,

permits, and vacant (etc.) departments.

Assessment Calendar

The Maryland Annotated Code prescribes many of the governing criteria for property assessment

administration. In Maryland one third of all properties must be re-valued each year, and

assessment notices are to be mailed by January 1. First level assessment appeal hearings must be

heard (preferably before the assessment/tax roll is certified for real property tax billing July 1).

If first level appeals are not completed timely, tax billing can be complicated by supplemental

billing or by many manual adjustments.

Administrative and assessor staff must complete many administrative functions along with

completing the reassessment program. Major administrative functions of the assessment office

include the real property transfer process, administration of property tax credit and exemption

programs, maintaining parcel maps, maintenance of the tax roll, and maintaining relations with

county government agencies and community groups.

Major assessment functions include the annual revaluation program, pick up of additions and

new construction to be added to the tax roll (full year. semi-annual or quarterly levy), and to hear

and finalize assessment appeal hearings at all appeal levels.

New Construction

• New Property Pick-up includes all new buildings and any renovations over a cost of $100,000

in each triennial group

• New Property Pickup occurs twice a year (July 1 – Full Year Levy and the January 1 -Half year

levy and several counties have a quarterly pickup)

• Renovations with a cost of less than $100,000 are to be picked up in reappraisal cycle once

every three years.

Several counties have a Quarterly Levy – Baltimore City, Baltimore, Charles, Howard,

Montgomery, and Prince George’s Counties

Assessment Introduction

Page 7 of 19

Other characteristics of new construction are:

New property consists of new improvements to land (buildings and site improvements or

additions/renovations to property;

New improvements to land are picked up for Full Year and Half Year (or Quarterly) when

substantially complete;

Additions/renovations to property are picked up for Full Year and Half Year (or Quarterly

when complete if the cost is greater than $100,000. If cost is less than $100,000

additions/renovations are picked up during the triennial valuation cycle;

Change of use to land is picked up for Full Year Levy only;

Building permits are used to identify of new improvements/additions/renovations. However

property owners sometimes make improvements without going through the permit process,

the only way to identify this is through field review or the use of imagery;

Most counties have automated building permit systems for the issuance and processing of

building permits for the county and municipalities within a county;

Some municipalities have their own building permit systems; and

Historically, counties and municipalities forward paper copies of building permits and

certificates of occupancy to each local assessment office and/or listings of permits &

certificates of occupancy.

There are various methods of transmitting permit information to the assessment offices. These

include:

Paper permit or lists

Periodic PDF file (monthly) of what would be paper permits

Assessment office access to the county permit system

Electronic extract from county system, typically Excel files, which can be used by

assessment managers for management of the pick-up process and for loading of permit

information to each account in the AAVS system

It is important for all counties and municipalities to work closely with the local assessment

office to provide permit and certificate of occupancy information as efficiently, as possible

to help insure proper pickup

Assessment Introduction

Page 8 of 19

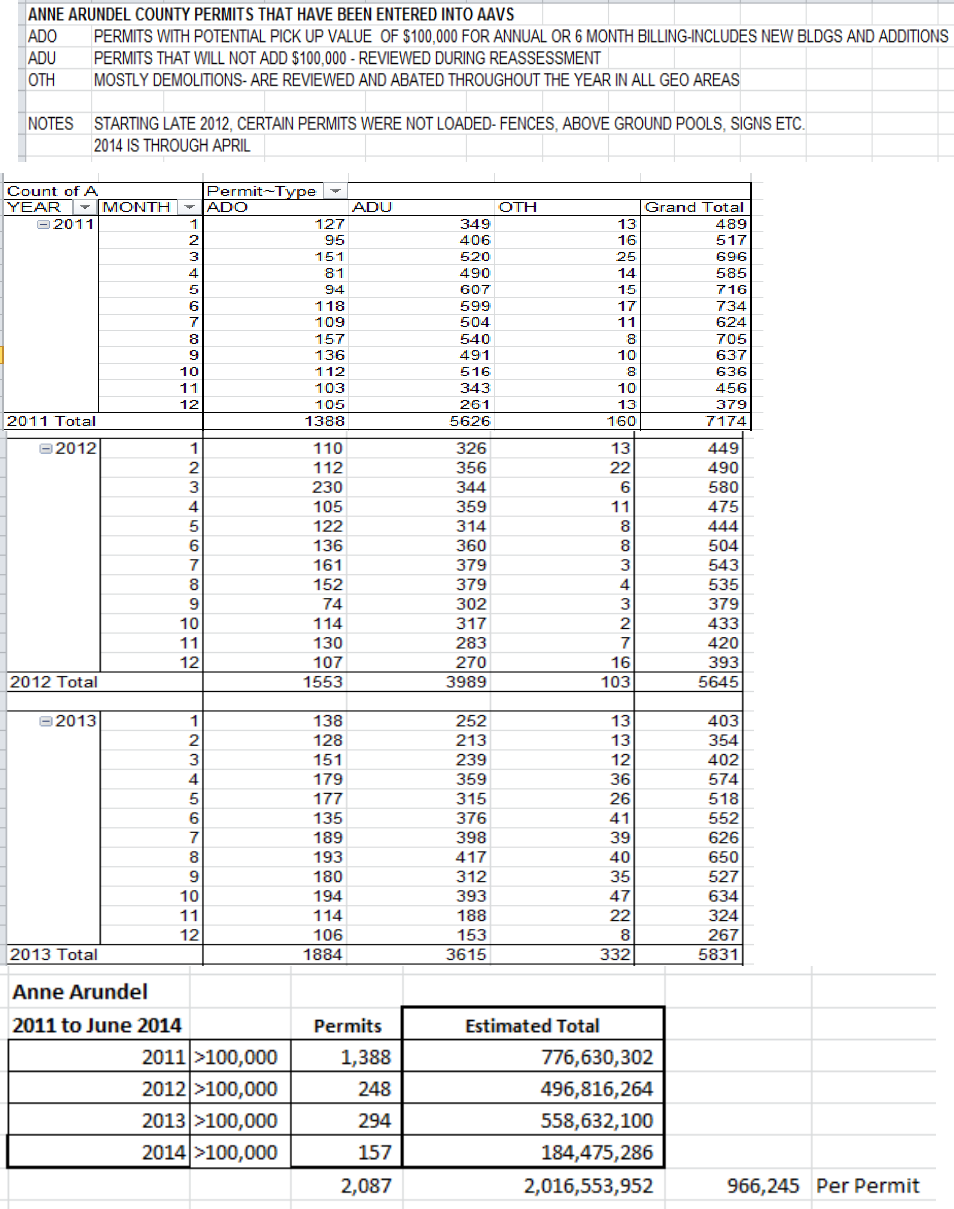

Anne Arundel County building permit data is summarized below:

Assessment Introduction

Page 9 of 19

Assessment Appeals

The assessment appeals process includes:

Supervisors’ level appeal/owner can get a copy of worksheet/that information will be reviewed

at the appeal meeting.

The first level hearing is informal and should be viewed as an opportunity to present

evidence which would indicate that the department's value of the property is inaccurate.

The property owner should focus on points that affect value/math errors/differences in

property characteristics, and property sales that support the property owners’ findings as

to value.

Following the 1

st

level hearing, the property owner will be mailed a Final Notice of

Assessment

Property Tax Assessment Appeal Board

If the property owner does not agree with decision of the assessor, they may appeal to the

Property Tax Assessment Appeal Board in the county where the property is located (three

member independent board)

Property owner can obtain a list of comparable properties if requested 15 days before

hearing.

Property owner is free to submit any supporting evidence.

Maryland Tax Court.

If dissatisfied with the notice of decision from the Appeal Board, you may file (within 30

days) to the Maryland Tax Court.

Assessment appeal levels include:

1

st

Level – Supervisor of Assessment – informal meeting with assessor

2

nd

Level – PTAAB – informal independent board

3

rd

Level – Md. Tax Court – more formal

4

th

Level – Circuit Court – county where property is located.

5

th

Level – Court of Special Appeals

6

th

Level – Court of Appeals

Assessment Introduction

Page 10 of 19

The assessment appeal process is available to allow property owners the opportunity to dispute

the value determined by the department, if they feel the value is wrong.

Appeals may be filed on three occasions:

When an assessment notice is received (reassessment)

Out of cycle review – file a petition for review (in the two years when the property is not

valued)

Upon Purchase (When a property is transferred between Jan. 1 and July 1

Appeals vary by county by year and type (Res. & C&I)

Appeals impact workload each year

Statewide Res and C& I averages mask actual impact by county

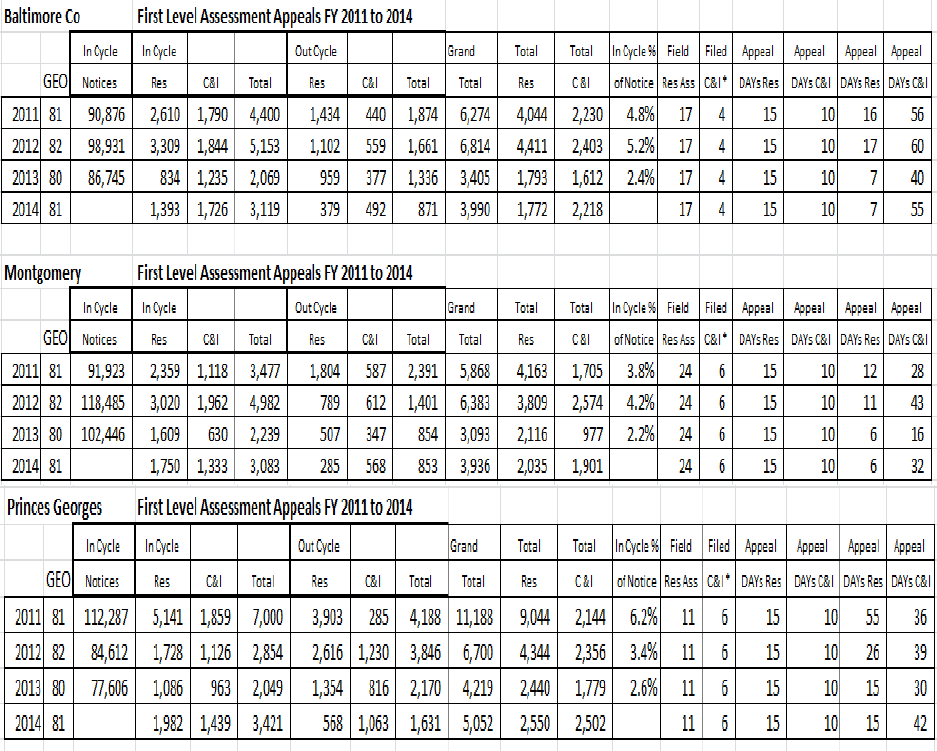

Note typical days to hearings from statewide to big 5 counties on Pages Following

Assessment Introduction

Page 11 of 19

Assessment Introduction

Page 12 of 19

CORE Work Processes

Assessors must annually complete certain core processes besides field inspection in the general

reassessment. Work production studies can be developed for any work segment of a years’

work. Each staff member is only available for work a certain number of days a year.

Total work days would typically be about 200 days per year after weekends, holidays, sick days,

vacation, and training days are deducted from 365 days per year

Each year supervisors of assessment year plan for the revaluation cycle, make assessor

assignments, review exempt accounts, prepare AAVS for next revaluation, and complete a work

production analysis next revaluation cycle.

CORE Processes include:

Inspection and verification property sales information for each area being appraised and

conducting market research;

Re-appraise each triennial group once every three years including conducting market

analysis, field inspections, and valuation analysis (sales analysis, market value index analysis

and valuation edits).

Revaluing new subdivision plats, splits and combinations

Completing and reviewing ratio reports, making final edit checks and percent change edit

reports checks

Picking up New Buildings and Major Renovations (over $100,000 in cost) at least twice a

year (Full year and Half Year Levy and quarter year levy where applicable) – conduct field

inspections and value

Conducting 1

st

Level assessment appeals

Conducting 2

nd

Level assessment appeals

Conducting 3

nd

Level assessment appeals

Daily completing all real property transfers and entering that information on the tax roll in

the AAVS system – sales data and owner information

Completing mapping prep for all splits and combinations and subdivision plats

Performing customer service duties– phone and tax roll counter

Processing change reports (abatements and increases)

Processing address and occupancy changes

Staffing production reports allow management to estimate staff requirements

CORE processes must be completed daily as required. After CORE processes are complete, the

assessors can focus reassessment physical inspections. In staffing analysis the supervisor of

assessments estimates the number of days for all CORE Processes. If CORE process days are

subtracted from total available work days for all assessors, the remaining days are available for

reassessment physical inspection.

Assessment Introduction

Page 13 of 19

If there are not enough personnel to complete the physical review in the days available for

physical review, additional resources would have to be added to complete field reviewed. If

additional personal are not added, then the physical review cannot be accomplished.

CORE days and Reassessment field days can vary from county to county and are due to the

property complexity, property density (urban, suburban, and rural), method of valuation, etc.

For each county, work production estimates can be developed and consider the various job

functions, standard production rates per day, and a difficulty factor.

Assessment Office Production

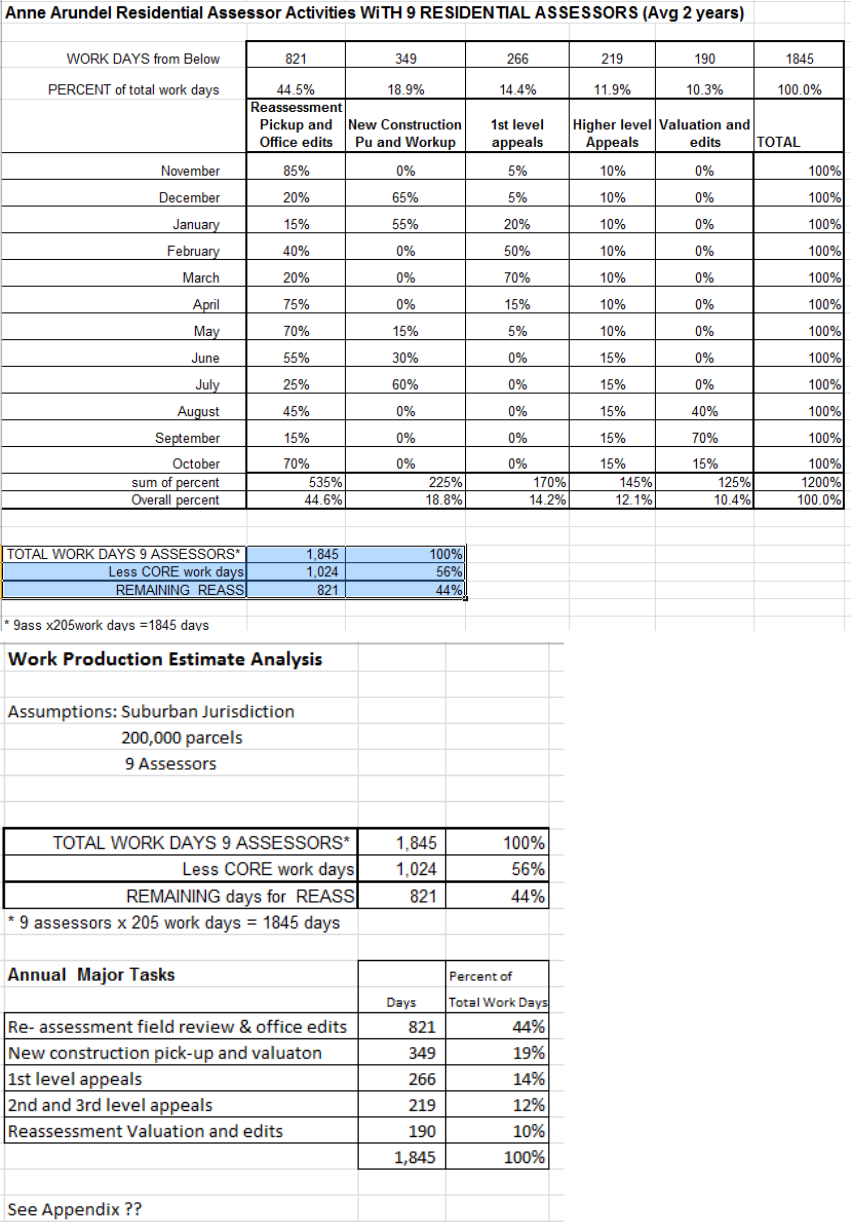

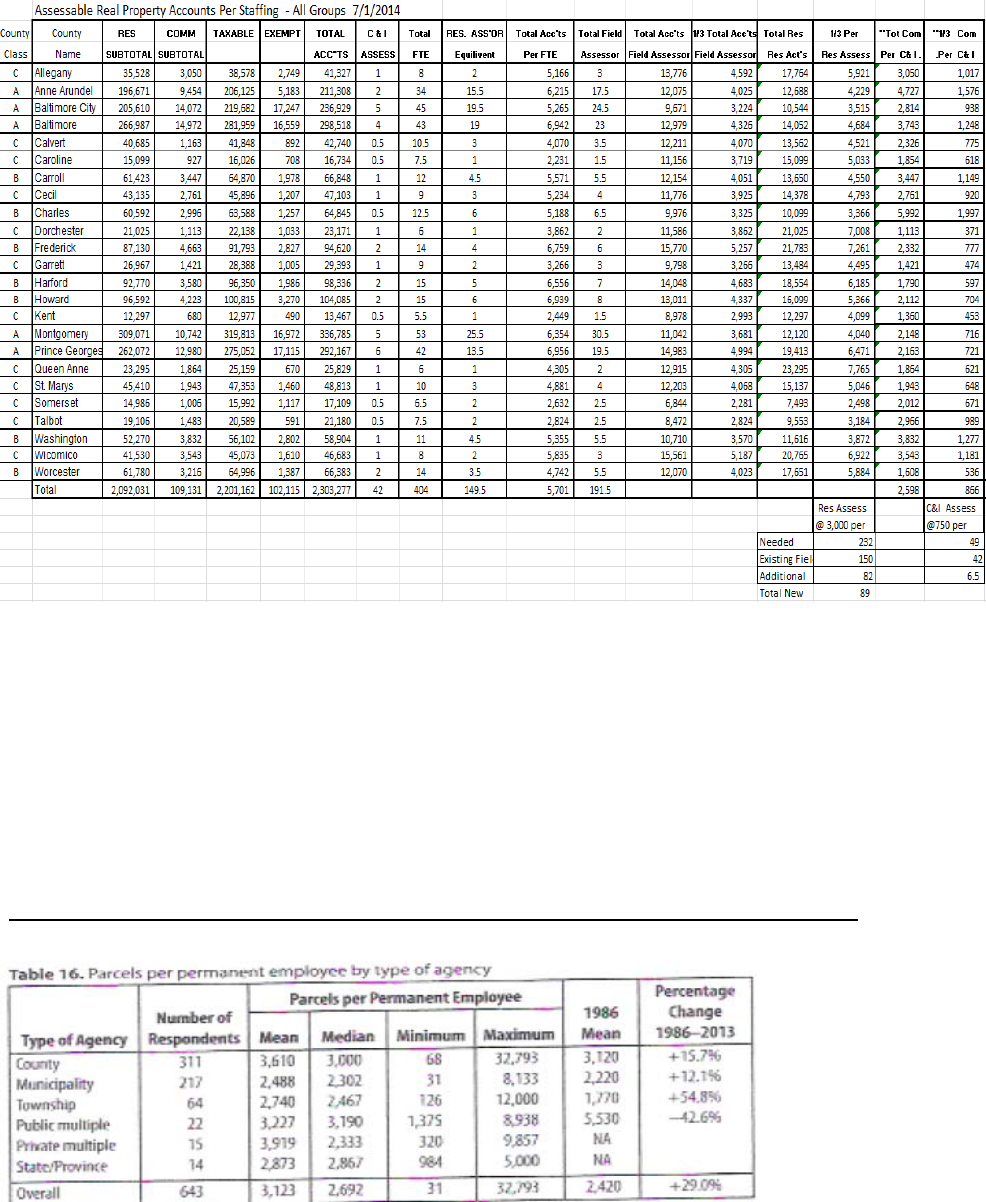

An example of a CORE work production report follows. It is a suburban jurisdiction with

approximately 200,000 total parcels. Assuming the production for residential and commercial

properties are roughly the same (which it is not) and 9 assessors would produce the following

results.

Assuming 1/3 of the 200,000 total parcels are valued each year, 66,700 parcels would have to be

reassessed. If total work days for the 9 assessors is 1,845 and the CORE days are 1,024, the

remaining days for reassessment are 821.

With 9 assessors and 821 reassessment days, there are 91 man days for reassessment field review

and edit. If the average field review is 45 accounts per day, 1 assessor could review 4,100

parcels and 9 assessors would complete 36,900 of a total of 66.700. In this case, all properties

could be field reviewed in about 6 years

Rural Counties or counties with more complex properties would take longer to field and office

review as the distance between properties or the complexity of the property increases.

Assessment Introduction

Page 14 of 19

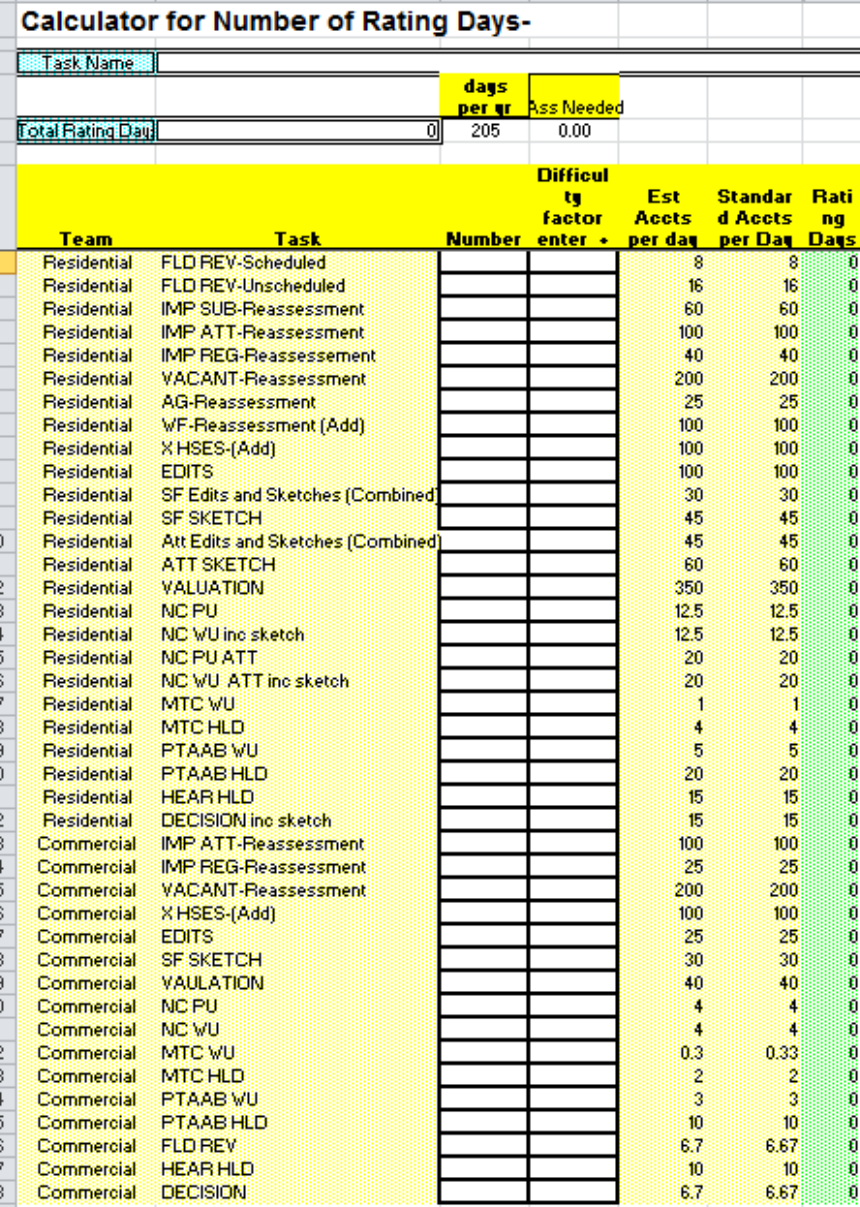

Example - CORE day analysis worksheet

Assessment Introduction

Page 15 of 19

Assessment Introduction

Page 16 of 19

Staffing

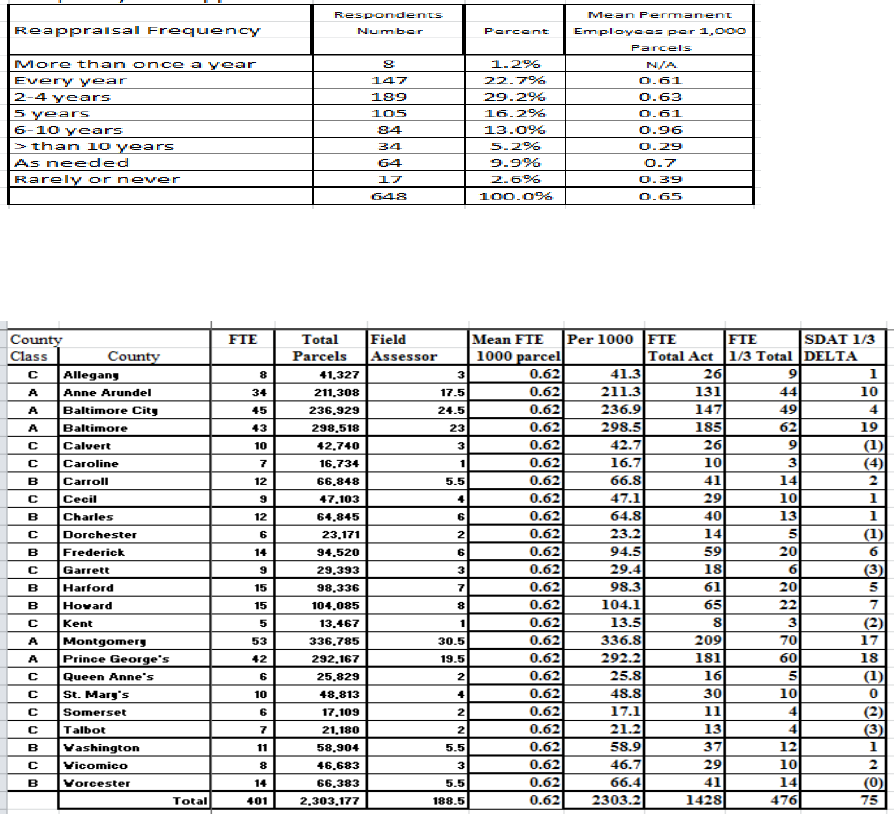

Staffing production reports allow management to estimate staff requirements

CORE processes must be completed daily as required

After CORE processes are complete, the assessors can focus on the reappraisal physucak

review for the current assessment year

Supervisors of Assessment can calculate the number of Rating Days for each assessor

function

Total Parcels

Assessment Introduction

Page 17 of 19

Staffing and Parcels

SDAT Total FTE staffing from 1976 to 1992 reduced by 18% while Total Accounts

increased by 33.3 %

SDAT Field Assessor staff from 1990 to 2014 reduced 70% while the number of

accounts increased by 25.5%

Current county FTE staffing is 401 with 131 personnel having more than 30 years service

(32%)

IAAO Staffing Survey conducted in 1986 and 2013

Staffing in Assessment Offices in the United States and Canada Results of 2013 Survey – IAAO

Research Committee and Lawrence C. Walters, PH.D. - 62 pages

Assessment Introduction

Page 18 of 19

FTE Maryland vs. 2013 IAAO Study Table 35 SDAT needs 85 personnel

Maryland FY 15 budget per parcel

• Maryland Class A (largest) Counites Median Budget per parcel $ 11.74

• Maryland Class B (midsize) Counites Median Budget per parcel $ 13.26

• Maryland Class C (smallest) Counites Median Budget per parcel $ 21.35

IAAO Staffing Study 2013 – Budget Per Parcel

Mean Median

• County $ 26.38 $ 21.85

• Municipality $ 30.79 $ 28.02

• State Provence $ 24.04 $ 21.00

Assessment Introduction

Page 19 of 19

Should assessor staff have to be added one Assessor III salary with fringe benefits is listed below

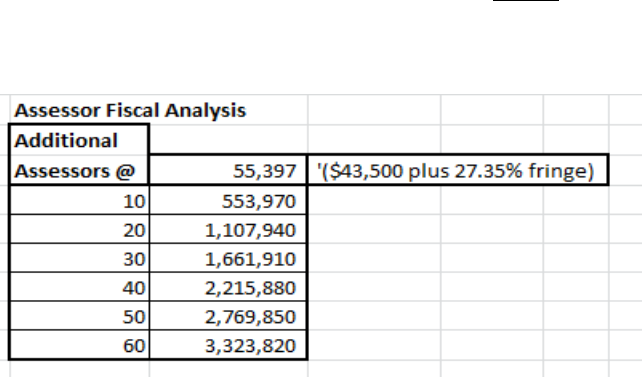

this includes costs for multiples of 10 assessors.

Typical Assessor Salary

Maryland Assessor 3 Salary

Salary over 6 years $40,547 to $45,194

Average Salary $43,500

Fringe Benefits (Dept./ Leg. Ser.) 27.35 % 11,897

Total $55,397

Representative Key Data

Market Areas and Neighborhoods (geographic stratification) SDAT statewide:

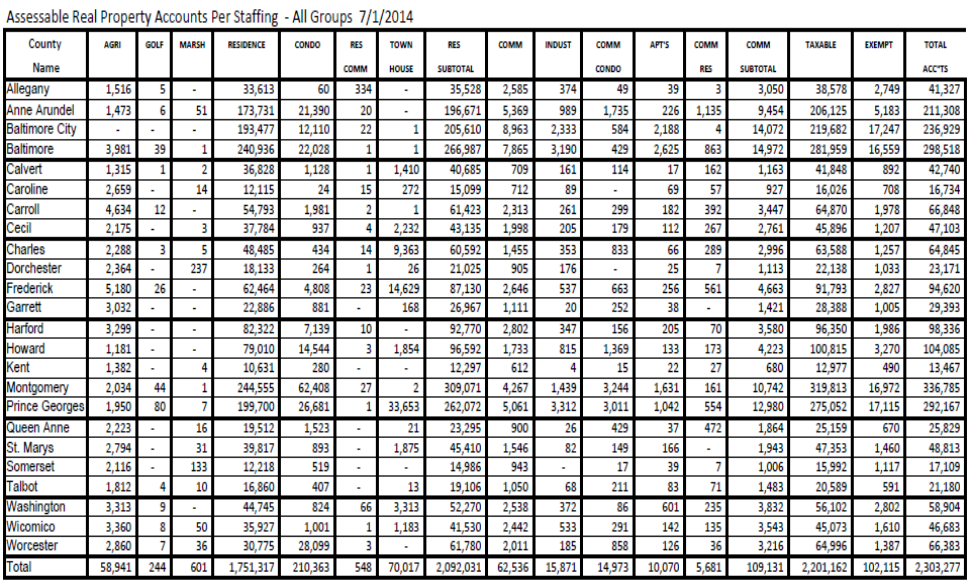

Market Areas Neighborhoods Parcels

1,250 15,722 2,275,062

Total Parcel Transfers (arms length/non-arms length

2012 2013 2014 (7 months)

141,501 160,378 80,902

Estimated annual arms length residential sales (all groups statewide) – 50,000

Owner-Occupied residential sales – 35,000 to 40,000

Estimated arms length com/ind sales - 900