Informaon Guide

1 July 2024

Australian Government

Home Guarantee

Scheme

Regional First Home Buyer

Guarantee

Contents

Important informaon 3

1. How the Regional First Home Buyer Guarantee works 5

2. Are you an eligible regional home buyer? 9

3. Is your lender approved for the Regional

First Home Buyer Guarantee? 19

4. Which home loans are eligible for the Regional

First Home Buyer Guarantee? 21

5. Which properes are eligible for the Regional

First Home Buyer Guarantee? 25

6. Other Regional First Home Buyer Guarantee features &

important informaon 27

7. Checklists – Your Eligibility Checks 32

8. Glossary 34

About this document

This document is dated 1 July 2024 and

relates to the Australian Government’s

Home Guarantee Scheme (HGS or Scheme) and

the Regional Home Buyer Guarantee (RFHBG).

It has been prepared by Housing Australia for

Parcipang Lenders so that they can provide

general informaon and guidance on the HGS or

RFHBG to regional home buyers.

Some terms used in this document have dened

meanings. These terms are capitalised and are

dened in the ‘Glossary’ secon on page 34.

Distribuon of this document

This document may only be distributed within

Australia and in relaon to Eligible Loans that are

oered by Parcipang Lenders.

If you are receiving this document, it will have

been provided to you by a Parcipang Lender

(or by one of their Representaves).

Providing your personal informaon to

Housing Australia

You will be asked to provide personal informaon

to Housing Australia (directly or via a Parcipang

Lender or its Representaves) if you take steps

to parcipate in the HGS or RFHBG or submit a

Home Buyer Declaraon. Please read the privacy

statement at secon 6.4 ‘Other Regional First

Home Buyer Guarantee features & important

informaon – Privacy statement’. By requesng

a Parcipang Lender to take any steps to have

your home loan covered by the HGS or RFHBG or

by subming a Home Buyer Declaraon to your

lender you consent to the maers outlined in that

privacy statement.

Providing incorrect or incomplete

informaon

As part of its role in administering and operang

the HGS, Housing Australia may verify the

informaon provided by you (or on your behalf)

in submissions for the RFHBG and in any Home

Buyer Declaraon. This is to ensure that you

are eligible to parcipate in the RFHBG. You

may be checked for former home ownership

within Australia and checks for other maers in

respect of the eligibility criteria – such as council

records, property tle informaon and your

nancial parculars – may also be undertaken.

Not providing the informaon requested

or providing incorrect or incomplete

informaon may impact upon the assessment

of your eligibility and ability to parcipate in the

RFHBG.

If it is found that you have provided false,

incorrect or misleading informaon under

a Home Buyer Declaraon and/or generally

in connecon with the RFHBG, criminal and

civil penales may apply. Also, if a guarantee

of your home loan is found to have been

issued mistakenly under the HGS or RFHBG

due to your fraudulent or wilful conduct, that

guarantee may be revoked and the lender may

also consider it as a failure by you to comply

with the terms of your home loan. If you fail to

comply with the terms and condions of your

home loan, the lender will have rights against

you – these rights may include requiring you

to renance your loan and pay some or all of

the home loan, requiring you to renance your

loan and pay for lenders mortgage insurance, an

ability to change or enforce the home loan and/

or to take other legal acon against you.

General informaon and guidance only

This document includes general informaon

and guidance in relaon to some of the features

of the HGS and RFHBG. It should not be relied

upon as being complete for any purpose.

Housing Australia is only providing this

document to Parcipang Lenders and

borrowers (via the Housing Australia website).

To the fullest extent provided by law,

this document does not create any legal

relaonship between you or any other person

and Housing Australia.

The informaon in this document is not nancial

or other advice. It has been prepared without

considering any person’s objecves, nancial

situaon or parcular needs. This document

does not relate to any products or services

provided by any Parcipang Lender. The

appointment of any person as a Parcipang

Lender is expressly not a recommendaon or

statement of approval of any such person.

It is important that you read this document

and all of the materials provided to you by

your Parcipang Lender in full, and take your

own professional advice as appropriate, before

deciding to take any steps to have your home

loan covered by the Scheme or subming a

Home Buyer Declaraon.

No independent vericaon

No Parcipang Lender or Representave

has independently veried any informaon

contained in this document and each

such person disclaims any responsibility for that

informaon. No representaon, warranty or

undertaking (express or implied) is made,

and no responsibility or liability is accepted,

by any of them, in relaon to the accuracy

or completeness of the informaon in this

document.

Enquiries & further informaon

If you have any quesons about the HGS and

RFHBG you should ask your Parcipang Lender

and/or seek advice from a professional adviser.

Further informaon on the HGS and RFHBG is

also available at ww.housingaustralia.gov.au.

Important informaon

4 | Informaon Guide – Regional First Home Buyer Guarantee

Informaon Guide – Regional First Home Buyer Guarantee | 5

1. How the Regional First Home

Buyer Guarantee works

The Regional First Home Buyer Guarantee (RFHBG) is an Australian Government

iniave to support eligible regional home buyers to buy a home sooner, in a

regional area. Under the RFHBG, part of an eligible regional home buyer’s home

loan from a Parcipang Lender is guaranteed by Housing Australia. This enables an

eligible regional home buyer to buy a modest home with as lile as 5% deposit.

1.1 Is your home loan eligible for the Regional First Home Buyer

Guarantee?

For your home loan to be eligible for the RFHBG there are a few checks that need to be sased.

They relate to:

• living in a regional area – you must have lived in a regional area or adjacent regional area to where you

are purchasing for the preceding 12-month period to the Home Loan Date – see secon 2 ‘Are you an

eligible regional home buyer?’ and secon 5 ‘Which properes are eligible for the Regional First Home Buyer

Guarantee?’^

• your personal circumstances – referred to as Your Eligibility Checks, including checks for your income, prior

property ownership, cizenship or permanent residency status, age, deposit and intenon to live in the

property you buy – see secon 2 ‘Are you an eligible regional home buyer?’ and the checklists in secon 7

‘Checklists – Your Eligibility Checks’

• the lender for your home loan – which must be a Parcipang Lender – see secon 3 ‘Is your lender

approved for the Regional First Home Buyer Guarantee?’

• the type of home loan you are applying for – which must be an Eligible Loan – see secon 4 ‘Which home

loans are eligible for the Regional First Home Buyer Guarantee?’, and

• the property you intend to purchase – which must be an Eligible Property – see secon 5 ‘Which properes are

eligible for the Regional First Home Buyer Guarantee?’.

If any one of these checks is not satisfied, you will not be able to participate in the RFHBG. Your lender will need to be

satisfied that these checks are met and will have separate criteria, processes and requirements for consideration of

your home loan application with them.

The RFHBG is open across regional areas in Australia to all eligible regional home buyers in respect of Eligible Loans.

The number of places under the RFHBG is limited and a

place may not be available even if your home loan is eligible.

See secon 1.2 ‘Other key features of the Regional First Home Buyer Guarantee – RFHBG place limits’ below for further

details.

You should discuss with your Parcipang Lender whether the RFHBG is the most appropriate program oered by

the Australian Government for you.

Secon 8 includes a Glossary of dened terms that are used throughout this Informaon Guide.

^ Employees required by their current employer to relocate may be eligible and should check with their Parcipang Lender (see secon 2.1.1)

6 | Informaon Guide – Regional First Home Buyer Guarantee

1.2 Other key features of the Regional First Home Buyer

Guarantee

The RFHBG involves the following key features.

When the RFHBG

commenced

The RFHBG commenced on 1 October 2022.

Parcipaon in the

RFHBG

You cannot apply to Housing Australia directly to have your home loan

parcipate in the RFHBG. You can only do so as part of your home loan

applicaon with a Parcipang Lender.

The eligibility of your home loan to parcipate in the RFHBG will be considered

by your lender and, if eligible, the lender will nofy you that your home loan

is able to parcipate in the RFHBG. They may also take steps to make a RFHBG

Place Reservaon – as described in secon 6.1 ‘Regional First Home Buyer

Guarantee Place Reservaons’.

Informaon on how your home loan can be covered by the RFHBG can be

obtained through a Parcipang Lender and their Representaves.

Regional area denion

A regional area is dened as:

• the Stascal Area Level 4 (ASGS SA4 2016) areas in a State or the

Northern Territory that are not a capital city of that State or Territory;

and

• Norfolk Island; or the Territories of Jervis Bay, Christmas Island or Cocos

(Keeling) Islands;

as dened in the Australian Stascal Geography Standard 2016 published

by the Australian Bureau of Stascs (ABS).

The greater capital city areas of each state and the Northern Territory; and the

enre Australian Capital Territory are excluded from the RFHBG.

RFHBG place limits

10,000 home loans can be guaranteed under the RFHBG in each nancial

year (up unl 30 June 2025).

Issue of guarantees under

the RFHBG

If your home loan is covered by the RFHBG, Housing Australia will issue a

guarantee to the Parcipang Lender who made that loan to you.

The guarantee is not a cash payment or a deposit for your home loan.

Rather, the guarantee is a legal arrangement between Housing Australia and

your lender to pay up to a certain amount that you owe to your lender if

you default under the terms of your home loan and your property has been

sold (as further described below).

A guarantee issued under the RFHBG is not made to you, and you are not

able to take any acon in relaon to a guarantee of your home loan under

the RFHBG (if one applies).

Informaon Guide – Regional First Home Buyer Guarantee | 7

What a guarantee covers

Any guarantee of your home loan is for up to a maximum amount of 15% of

the Value (as assessed by your lender) of the property that you buy but may

be lesser where the deposit you are able to contribute is above 5%. If you

default on your home loan and aer your property is sold, the guarantee

can be claimed by your Parcipang Lender.

The guarantee is only able to be claimed by the Parcipang Lender for

amounts owing by you to them under your home loan aer:

• you have defaulted on your home loan

• your property has been sold

• the sale proceeds (and any other amounts available to the lender) have

been applied to pay the amounts you owe to your lender under the terms

of your home loan, and

• an amount that you owe remains outstanding.

Specically, any guarantee of your home loan under the RFHBG will not

apply to:

• help you make any payments on your home loan that you miss during the

ordinary course of your home loan

• prevent you from defaulting on your home loan

• stop the lender from taking action against you for any default under your

home loan or mortgage (including where they have rights to take

possession and sell off the property), or

• cover the payment of any amounts which remain owing by you to the lender

a

fter (1) sale proceeds and other amounts are applied to pay what you owe

on your home loan and after amounts under the guarantee have been

claimed and paid to the Participating Lender, or (2) if they do not make a

claim under the guarantee.

Circumstances where your

home loan may cease

parcipang in the RFHBG

If your home loan is covered by the RFHBG, there are certain events which

may cause the RFHBG guarantee to stop applying to your home loan. These

include where:

• it is found at any me that your home loan was not eligible to parcipate

in the RFHBG – including where it is discovered at a later me that Your

Eligibility Checks were not sased

• you no longer live in the property unless you are eligible for an

exempon (circumstances to be discussed with your lender). In this

instance, your lender may require you to pay Lenders Mortgage

Insurance (LMI) or signicant other addional costs relang to your loan,

at your own obligaon.

• you have repaid your home loan in full – including where you renance

your home loan with another lender that is not a Parcipang Lender

– see secon 6.3 ‘Other Regional First Home Buyer Guarantee features

& important informaon – Renancing your Regional First Home Buyer

Guarantee-guaranteed home loan’ for further details, or

• you have repaid your loan down to a principal balance that is 80% or less

of the original Value of your property at the me of purchase – calculated

based on your scheduled home loan repayments. Any amounts that you

prepay and can freely redraw are not counted.

8 | Informaon Guide – Regional First Home Buyer Guarantee

There are also addional events that rely upon your agreements with, and the

acons of, your Parcipang Lender. These include where:

• the terms of your home loan (or mortgage) are changed by your lender

except for changes to the interest rate, changes made to the terms that

your lender oers to all of its owner-occupied home loans, changes for

where you are in nancial hardship, changes between your lender’s

standard home loan products and other limited circumstances

• further nance is provided to you by your lender and secured against the

same property (known as a ‘top up’)

• your loan is assigned or transferred by your lender, or

• if your lender noes Housing Australia that the guarantee may be

released.

If your home loan is no longer covered by the RFHBG at an earlier me

than your lender expected, you may be subject to addional fees,

charges and expenses as set out in the terms of your home loan.

Other government

programs

If your home loan is covered by the RFHBG, you are not restricted under the

terms of the RFHBG from also accessing other government programs – such

as the Australian Government’s First Home Super Saver Scheme or First Home

Owner Grant and concessions that may be oered by State and Territory

governments.

These other programs apply their own criteria and condions, and your

eligibility or parcipaon under the RFHBG does not mean that you will

denitely be eligible and able to parcipate under another program. You

should make your own enquiries on the terms of those other programs.

You should discuss with your Parcipang Lender whether the RFHBG is the

most appropriate guarantee for you.

1.3 Geng ready – what will I need to provide to my lender?

Your Parcipang Lender or their Representave will let you know what informaon and materials you will need to

provide for your home loan applicaon and any parcipaon of your home loan under the RFHBG.

However, the following informaon will need to be submied by your lender in connecon with the inial RFHBG Place

Reservaon process. It is recommended that you collect and have this informaon available when you rst contact your

lender (directly or through their Representave):

9 your full name and date of birth

9 your Medicare number (including your posion on your card)

9 your Noce of Assessment for your taxable income for the 2023-24 income year – see secon 2.1.3 ‘Are you

an eligible regional home buyer? – What was your taxable income for the preceding income year? (Income

test)’, and

9 other details to assist the lender to assess whether you will be eligible to parcipate in the RFHBG – your

lender will conrm what these are.

If you do not have a Medicare number, or have not been issued with a Noce of Assessment for your taxable

income (because you did not earn taxable income above the tax-free threshold), your lender will conrm what other

informaon will be required to be provided by you in your circumstances.

Informaon Guide – Regional First Home Buyer Guarantee | 9

2. Are you an eligible

regional home buyer?

2.1 Your Eligibility Checks

First, you should consider whether your personal circumstances sasfy all of the

following checks. They relate to your eligibility as a regional home buyer who can

parcipate in the RFHBG.

The key checks for your personal circumstances are:

9 living and buying in a regional area – see secons 2.1.1 and 2.1.2

9 an income test – see secon 2.1.3

9 a prior property ownership test – see secon 2.1.4

9 a cizenship and permanent residency test – see secon 2.1.5

9 a minimum age test – see secon 2.1.6

9 a deposit requirement – see secon 2.1.7

9 an owner-occupier requirement – see secon 2.1.8, and

9 others – see secon 2.1.9

Some of these checks may dier depending on whether you are applying for a home

loan as an individual, as joint applicants, or whether you are an employee who has

been required by your current employer (employed for at least 12 months) to relocate.

If you do not sasfy any one of these checks – which are described in further detail

below and are together referred to as Your Eligibility Checks – you should not ask

your lender to take any steps to have your home loan parcipate in the RFHBG. This

includes that you should not ask your lender to make a RFHBG Place Reservaon. If

you are unsure of any of these maers, you should ask your lender or seek your own

independent nancial and legal advice.

Secon 7 ‘Checklists – Your Eligibility Checks’ includes checklists that are provided

to help you to record your answers as you consider the quesons for each of Your

Eligibility Checks.

If you are eligible for the RFHBG, you are not eligible for the First Home

Guarantee. Home buyers who are not eligible for the RFHBG, may be eligible

for the First Home Guarantee or the Family Home Guarantee.

To nd out more about your eligibility, try the Eligibility Tool at

www.housingaustralia.gov.au

10 | Informaon Guide – Regional First Home Buyer Guarantee

2.1.1 Are you an eligible regional home buyer?

You will only be eligible to participate if:

• at least one borrower under your loan agreement has lived in the regional area or adjacent to the regional area

they are purchasing in for the preceding 12-month period to the Home Loan Date.

For employees who have been required by their current employer (employed for at least 12 months) to relocate,

you may be eligible if you have lived during some of the previous 12 month period in the regional area you are

purchasing in or an adjacent regional area and were only unable to complete the 12 month requirement due to the

relocaon/posng.

Please talk to your Parcipang Lender about the informaon they will require under their lending policy to verify

your eligibility. This informaon may include one of the following:

• a copy of ulity noces for the preceding 12 month period

• a copy of a rental agreement for the preceding 12 month period

• a copy of your recent Noces of Assessment where this can validate residence over the preceding 12 month

period; and

• where applicable and if the borrower is an employee who has been required by their current employer (employed

for at least 12 months) to relocate, an ocial statement conrming any relocaon required in the course of the

person performing their dues over the preceding 12 months and conrms their employment tenure with their

current employer of at least 12 months.

To help you idenfy whether you live in a regional area, and where you may be able to purchase, you can use the

Regional Checker at www.housingaustralia.gov.au

Scenario 1 - Joint applicants eligible for the RFHBG

Two people are jointly applying for the Regional First Home Buyer Guarantee to purchase in Orange (NSW) and

they sasfy all eligibility requirements for the Guarantee. One applicant lived in Orange for the preceding 14

months to the Home Loan Date, whilst the other applicant lived in Orange for the preceding 5 months. The joint

applicants are eligible for the RFHBG because one borrower has lived in the region they are purchasing in for the

preceding 12 month period. Importantly, both borrowers met all other eligibility requirements as well.

Scenario 2 - Individual applicant eligible for the RFHBG

An individual is applying for the Regional First Home Buyer Guarantee to purchase in Townsville (QLD) and

sases all requirements of the Guarantee. The applicant has lived in an adjacent regional area to Townsville

for 18 months preceding the Home Loan Date. The applicant is eligible for the RFHBG as they have sased the

requirement to have lived in the region they are purchasing in (or an adjacent region) for the preceding 12 month

period. Importantly, they met all other requirements and had validated with their lender that the region they

were purchasing in was classied as a regional centre or regional area.

Scenario 3 - Joint applicants NOT eligible for the RFHBG

Two people are jointly applying for the Regional First Home Buyer Guarantee to purchase in Geelong (VIC) and

are discussing with their lender whether they sasfy all requirements of the Guarantee. One applicant lived in

Geelong for the preceding 8 months to the Home Loan Date and the other lived in Melbourne for the past 5

years. The joint applicants are not eligible for the RFHBG because neither borrower has lived in the region they

are purchasing in for the preceding 12 month period to the Home Loan Date and neither qualify for a relocaon

exempon. They discussed their scenario with their parcipang lender, who then provided lending opons to

suit their needs. For example, they may have been eligible for another Government Guarantee (e.g., First Home

Guarantee or Family Home Guarantee) or they could wait a further 4 months for the applicant living in Geelong

to meet the 12 month requirement for the RFHBG.

Informaon Guide – Regional First Home Buyer Guarantee | 11

2.1.2 Are you buying your home in a regional area on your own

or with another person?

The RFHBG is open to individuals and joint applicants. It is not possible for a guarantee under the RFHBG to apply to

more than one home loan arrangement involving you.

Individuals

If you are looking to buy your home in a regional area as the only person named as a borrower on your home loan,

then you would apply under the RFHBG as an individual, regardless of your relaonship status.

This means that you need to sasfy each of the checks by reference to your own circumstances. Maers for joint

applicants (such as the combined income test) will not apply to you.

Joint applicants

If you are looking to buy your home in a regional area with another person, where you are both named as borrowers on

your home loan, then you would both apply under the RFHBG as joint applicants. Home loans with 3 or more borrowers

are not eligible for the RFHBG.

This means that you need to sasfy each of the checks by reference to your combined circumstances and apply

together. Maers for individuals (such as the individual income test) will not apply to you. For 2.1.1, only one

borrower under your home loan agreement has to have met the requirement for the preceding 12 month period

(as at the Home Loan Date), having lived in the regional area being purchased in or an adjacent regional area to the

regional area being purchased in.

Quesons to ask yourself

Q. Will you be applying under the RFHBG as an individual or as joint applicants?

As an individual

If your answer is ‘as an individual’, then you should pay close aenon to the checks that apply for individuals

and disregard the maers that apply for joint applicants.

As joint applicants

If your answer is ‘as joint applicants’, then

• you will need to have one borrower under your home loan agreement provide evidence as per your

Parcipang Lender’s own requirements for having lived in the regional area being purchased in or an adjacent

regional area to the regional area being purchased in, for the preceding 12 month period (as at the Home Loan

Date)

• you will need to apply for a home loan together, and

• you should pay close aenon to the checks that apply for joint applicants and disregard the maers that

apply only for individuals.

12 | Informaon Guide – Regional First Home Buyer Guarantee

2.1.3 What was your taxable income for the preceding income

year? (Income test)

The RFHBG includes an income test.

To sasfy this test:

• for individuals – your taxable income for the previous income year must not be more than $125,000, or

• for joint applicants – your combined taxable income for the previous income year must not be more than

$200,000.

For all RFHBG place applicaons made from 1 July 2024 up to 30 June 2025, the relevant income year will be the 2023-24

nancial year. Income from previous nancial years is not able to be considered for the income test.

The income test is assessed by your lender using your taxable income (as per the Income Tax Assessment Act) from

the previous income year from when you apply. This is shown on your Noce of Assessment issued to you by the

Australian Taxaon Oce.

Each income year starts on 1 July in a calendar year and ends on 30 June in the next calendar year – so if you

apply for the RFHBG with your lender between 1 July 2024 and 30 June 2025, you would need to be able to

provide your income tax assessment noce for the 2023-24 nancial year.

If you are applying under the RFHBG:

• ‘as an individual’, you will need to sasfy the income test for individuals, or

• ‘as joint applicants’, together you will need to sasfy the combined income test for joint applicants. This will be

the only income test you need to sasfy – so you can disregard the income test for individuals – and you will need

to be able to show your lender a copy of the Noce of Assessment for each of you.

Before you enter into a home loan agreement, you should consider talking with your lender (or broker) about

the potenal implicaons of changing interest rates or house prices on your individual circumstances.

Quesons to ask yourself

Q1. Do you have your Noce of Assessment for the 2023-24 income year (as issued by the Australian Taxaon

Oce)?

No, I don’t have it (or I can’t nd it)

If your answer to the above queson is ‘no’, you may not be able to sasfy the income test.

You would need to take steps to le for or obtain a copy of your Noce of Assessment for the 2023-24 income

year. Doing so does not necessarily qualify you as being able to parcipate in the RFHBG and any acon you

decide to take is your own responsibility.

If you did not receive a Noce of Assessment because your taxable income is below the tax-free threshold in the

relevant income year, you will need to conrm with your lender what informaon you would need to provide.

Yes, I do

If your answer is ‘yes’ to the above queson, you will need to be able to show a copy of your Noce of

Assessment to your lender.

The next queson for you is below.

Q2. Do you sasfy the income test?

No, I / we don’t sasfy the income test

If your answer to the above queson is ‘no’, your home loan will not be eligible under the RFHBG.

Yes, I / we sasfy the income test

If your answer is ‘yes’ to the above queson, your home loan may be eligible for the RFHBG.

Informaon Guide – Regional First Home Buyer Guarantee | 13

2.1.4 Have you held an interest in property in Australia? (Prior

property ownership test)

It is important that the RFHBG assists genuine eligible regional home buyers.

The prior property ownership test to be eligible for the RFHBG is that you have not held any of the following in the

10 years prior to your Home Loan Date:

• a freehold interest in real property in Australia (this includes owning land only)

• an interest in a lease of land in Australia with a term of 50 years (or more), or

• a company tle interest in land in Australia.

These tests apply for property interests in all States and Territories of Australia, regardless of whether the property

was residenal or commercial property, for investment or owner-occupied purposes and whether or not it was ever

lived in.

They also apply to you whether or not any of the interests listed above have been held by you on your own or together

with someone else – for example, where you held an interest in property with a former partner.

What this means is that, if you are applying under the RFHBG:

• ‘as an individual’, then you will need to sasfy the prior property ownership test, or

• ‘as joint applicants’, then you will both need to sasfy the prior property ownership test.

Note that if either of you – whether individually or with someone else, in the 10 years prior to your Home Loan

Date – have held any of the interests listed in the test, you do not sasfy the prior property ownership test as

joint applicants.

For your home loan to parcipate in the RFHBG, you will need to make a statutory declaraon that conrms you have

not held any interests of this kind in Australia in the 10 years prior to your Home Loan Date. This declaraon is made

under the Home Buyer Declaraon.

In addion, your lender, Housing Australia and others may conduct independent checks on whether or not you have

held any such interests in Australia in the 10 years prior to your Home Loan Date. They may do this at any me –

including aer you have signed a contract of sale or paid a deposit in relaon to a property and aer your home loan

has been advanced.

If you are unsure of whether or not you have held any of the kinds of interests listed above in the 10 years prior to

your Home Loan Date, you should ask a professional adviser, as you will need to be sure that you are not giving a

false declaraon.

Quesons to ask yourself

Q3. Will you sasfy the prior property ownership test at your Home Loan Date?

You should check this against each of the three types of property interest holdings that could restrict you from

being eligible.

For joint applicants, each of you must sasfy the prior property ownership test.

No, I have held an interest in property in the 10 years prior to my Home Loan Date.

If your answer to the above queson is ‘no’, you will not be able to sasfy the prior property ownership test.

Your home loan – as an individual or as joint applicants – will not be eligible to parcipate under the RFHBG.

Yes, I do, because I don’t hold an interest in property or haven’t held an in interest in property in the last 10

years (and, for joint applicants, neither does the person I’m applying with).

If your answer to the above queson is ‘yes’, you will be able to make the necessary declaraons and sasfy the

prior property ownership test.

14 | Informaon Guide – Regional First Home Buyer Guarantee

2.1.5 Are you an Australian cizen or permanent resident?

(Cizenship and permanent residency test)

The RFHBG is only open to Australian cizens and permanent residents.

The cizenship and permanent residency test for the RFHBG is that you will need to be an Australian cizen or

permanent resident at your Home Loan Date. If you are applying under the RFHBG:

• ‘as an individual’, you will need to sasfy the cizenship and permanent residency test, or

• ‘as joint applicants’, you will both need to sasfy the cizenship and permanent residency test.

You will not sasfy the cizenship and permanent residency test if at the Home Loan Date:

• you are a temporary resident of Australia (and not an Australian cizen or permanent resident)

• you are applying with an Australian cizen or permanent resident, but you are not an Australian cizen or

permanent resident

• you were formerly an Australian cizen or permanent resident, but have not resumed your cizenship or

permanent residency, or

• you have applied for, are eligible for, or have received noce of a posive decision of Australian cizenship

or permanent residency, but have not received your cizenship cercate or eligible Australian permanent

resident visa.

Quesons to ask yourself

Q4. Will you be an Australian cizen or permanent resident at your Home Loan Date?

For couples, each of you must sasfy the Australian cizenship and permanent residency test.

No, I will not be.

If your answer to the above queson is ‘no’, you will not be able to sasfy the cizenship and permanent

residency test.

Your home loan – as an individual or as joint applicants – will not be eligible to parcipate under the RFHBG.

Yes, I will be (and, for joint applicants, so will the person I’m borrowing with).

If your answer to the above queson is ‘yes’, you will be able to make the Home Buyer Declaraon and sasfy

the cizenship and permanent residency test.

2.1.6 Are you 18 years or older? (Minimum age test)

The RFHBG is only open to persons who are 18 years of age or over.

The minimum age test for the RFHBG is that you will need to be 18 years of age or over at your Home Loan Date.

If you are applying under the RFHBG:

• ‘as an individual’, you will need to sasfy the minimum age test, or

• ‘as joint applicants’, you will both need to sasfy the minimum age test.

Quesons to ask yourself

Q5. Will you be 18 years or over at your Home Loan Date?

For joint applicants, the answer must be ‘yes’ for both of you.

No, I will not be.

If your answer to the above queson is ‘no’, you will not be able to sasfy the minimum age test.

Your home loan – as an individual or as joint applicants – will not be eligible to parcipate under the RFHBG.

Yes, I will be.

If your answer to the above queson is ‘yes’, you will be able to make the necessary declaraons and sasfy the

minimum age test.

Informaon Guide – Regional First Home Buyer Guarantee | 15

2.1.7 Do you have a deposit of at least 5% of the Value of the

property (but less than 20%)? (Deposit requirement)

There is a minimum and maximum deposit requirement for the RFHBG.

Your Parcipang Lender will be able to tell you if you sasfy this requirement.

The RFHBG is to assist eligible regional home buyers who have at least 5% of the Value of an eligible property saved

as a deposit. It is a requirement of the RFHBG that you use the maximum amount of your savings as possible towards

your deposit (subject to the policies of your lender and your nancial circumstances). If you have 20% or more saved

aer paying other home purchasing costs (e.g., stamp duty, legal costs), then your home loan will not be covered by

the RFHBG.

As the RFHBG is aimed at helping eligible regional home buyers, it is important that you do not try to disadvantage

other Australians by seeking to change your circumstances just to take advantage of the RFHBG. This includes where

you have a 20% or greater deposit and legally transfer your cash and other assets in order only to access the RFHBG,

or where your 5% deposit has not been genuinely saved by you and is being provided to you only so that you can

qualify for the RFHBG.

Parcipang Lenders must comply with responsible lending pracces – if you have any quesons about these

requirements in the context of the RFHBG, please discuss these with your Parcipang Lender directly.

You should conrm with your Parcipang Lender whether any cash grants under other Australian Government,

State or Territory schemes or programs you may receive can be considered as part of genuine savings by that

Parcipang Lender.

Note: you are responsible for meeng all costs and repayments for your home loan associated with the Home

Guarantee Scheme, including but not limited to stamp duty, bank fees and legal costs.

Quesons to ask yourself

Q6. Do you have a deposit of between 5% and 20% of the Value of the property you would like to purchase?

For joint applicants, your answer should refer to your combined circumstances.

No, I won’t – I’ll have less than the 5% minimum or more than the 20% maximum

If your answer to the above queson is ‘no’, you will not be able to sasfy the deposit requirement. Your home loan –

as an individual or as joint applicants – will not be eligible to parcipate under the RFHBG.

Yes, I do or will (and, for joint applicants, this is together with the person I’m borrowing with)

If your answer to the above queson is ‘yes’, you will be able to make the necessary declaraons and sasfy the

deposit requirement.

2.1.8 Will you live in the property you buy as an owner-

occupier?

(Owner-occupier requirement)

The RFHBG assists eligible regional home buyers to buy a modest home in a regional area. Investment properes are

not being supported by the RFHBG.

Under your Home Buyer Declaraon, you will need to declare that you intend to:

• start living in the Eligible Property you purchase within 6 months from either the selement date of your loan or,

for new builds, the date an occupancy cercate is issued, and

• connue to live in that property for as long as your home loan has a guarantee under the RFHBG unless you are

eligible for an exempon (circumstances to be discussed with your lender).

16 | Informaon Guide – Regional First Home Buyer Guarantee

If you are applying under the RFHBG:

• ‘as an individual’, you will need to sasfy the owner-occupier requirement unless you are eligible for an exempon

(circumstances to be discussed with your lender), or

• ‘as joint applicants’, you will both need to sasfy the owner-occupier requirement unless either one or both of you

are eligible for an exempon (circumstances to be discussed with your lender).

If you don’t live in your property – including where you move out of the property at a later me – your home

loan may cease to be guaranteed by the RFHBG.

In these circumstances there may be terms of your home loan that require you to take certain actions – including that

you may need to pay fees and charges and/or take out Lenders Mortgage Insurance (LMI) that would not have

otherwise applied if your home loan was eligible under the RFHBG.

Quesons to ask yourself

Q7. Do you intend to reside in the property you purchase as an owner-occupier while your home loan is

guaranteed under the RFHBG?

No, I don’t (or I don’t think I will)

If your answer to the above queson is ‘no’, you will not be able to sasfy the owner-occupier requirement.

Your home loan – as an individual or as joint applicants – will not be eligible to parcipate under the RFHBG.

Yes, I do intend to live in the property as an owner-occupier

If your answer to the above queson is ‘yes’, you will be able to make the Home Buyer Declaraon and sasfy

the owner-occupier requirement.

For joint applicants, the answer must be ‘yes’ for both of you.

2.1.9 Are there any maers that could disqualify you from being

an eligible regional home buyer?

This is a nal check to make sure that you don’t provide any incorrect, untrue or misleading informaon nor make any

false declaraons in relaon to your personal circumstances. It is not an addional criteria, and is included only to

make sure you have considered all possible maers and are aware of the possible consequences for providing untrue,

incorrect, misleading or false informaon or materials.

You should consider all of the above checks carefully. If you are unsure of any maer relang to your

circumstances, or (for joint applicants) of the person you’re borrowing with, you should speak to your lender

and/or ask your professional adviser(s).

If your Parcipang Lender takes any acon for your home loan to be covered by the RFHBG – including making

RFHBG Place Reservaons or seeking to have a guarantee apply for your home loan – you will need to provide

informaon to them and make a statutory declaraon.

This informaon and declaraons you make may be invesgated at future mes. You need to be certain that you are

giving true and correct informaon and make a true statutory declaraon.

If your informaon and/or statutory declaraon are found to be untrue, incorrect, misleading or false –

including at a later me aer you have paid a deposit or the full purchase price on your property – there may be

signicant consequences.

These may include that:

• legal acon is taken against you – including for criminal penales and civil acons. If you intenonally make a false

statement in a statutory declaraon, you are guilty of an oence under secon 11 of the Statutory Declaraons Act

1959 (Cth). The maximum penalty for this oence is imprisonment for 4 years.

• your home loan is not covered by the RFHBG, and/or

Informaon Guide – Regional First Home Buyer Guarantee | 17

• there are terms of your home loan that require you to take certain acons – including you may need to pay fees

and charges and/or take out lenders mortgage insurance that would not have otherwise applied if your home loan

was covered by the RFHBG.

You should understand the terms of your home loan carefully so that you know what would happen under your

home loan if this were to happen.

Quesons to ask yourself

Q8. Are you sure there are no maers in your personal circumstances that could mean you aren’t eligible for

the RFHBG?

No, I’m not sure

If your answer to the above queson is ‘no’, you could risk signicant consequences if you give incorrect, untrue

or misleading informaon or make a false statutory declaraon.

You should speak to your lender and/or ask your independent nancial and/or legal adviser(s).

Yes, I am sure

If your answer to the above queson is ‘yes’, you will be able to make the Home Buyer Declaraon and sasfy

the eligible regional home buyer test.

You should note that all informaon and declaraons provided by you are able to be invesgated at any

me.

18 | Informaon Guide – Regional First Home Buyer Guarantee

Informaon Guide – Regional First Home Buyer Guarantee | 19

3. Is your lender

approved for the

Regional First Home

Buyer Guarantee?

3.1 Parcipang Lenders

The RFHBG is only open to Eligible Loans that are made by Parcipang Lenders. For a

lender to be a Parcipang Lender under the RFHBG they must have been approved by

Housing Australia.

A list of Parcipang Lenders is on www.housingaustralia.gov.au. Even if you are told

that a parcular instuon is a Parcipang Lender, you should check that they are

listed on www.housingaustralia.gov.au.

Parcipang Lenders may oer Eligible Loans themselves or via Representaves. If

you are unsure whether any instuon or person is a Representave of a Parcipang

Lender, you should contact the lender directly to ask.

3.2 Your home loan applicaon and your

relaonship with your lender

You are able to apply for nance for your home loan from more than one Parcipang

Lender. The terms of your home loan will be agreed between you and your lender.

Housing Australia will not be involved in any home loan applicaon procedures,

assessments or approvals nor the administraon or management of your home

loan (including in circumstances of default and enforcement).

See secon 4 ‘Which home loans are eligible for the Regional First Home Buyer

Guarantee?

for further details on which home loans qualify as Eligible Loans.

3.3 What if I have a complaint about my

lender?

General complaints about your lender should be made to your lender and/or any

relevant complaints authority.

If you are not sure who the relevant Complaints Authority is, contact the Australian

Financial Complaints Authority at afca.org.au.

20 | Informaon Guide – Regional First Home Buyer Guarantee

Informaon Guide – Regional First Home Buyer Guarantee | 21

4. Which home loans

are eligible for the

Regional First Home

Buyer Guarantee?

4.1 Eligible Loans

Not all home loans are eligible for the RFHBG.

The RFHBG is restricted to ‘Eligible Loans’, which are home loans:

• made by Parcipang Lenders to eligible regional home buyers, and

• that are for the purchase of an Eligible Property that is to be occupied by you as

the owner – see secon 5 ‘Which properes are eligible for the Regional First Home

Buyer Guarantee? for further informaon.

There are addional requirements that apply in relaon to these home loans that

rely upon the terms that you agree with your Parcipang Lender. These include

that your home loan will need to be for a term of 30 years or less, have regular

repayments of principal (with limited excepons for interest-only loans, which mainly

relate to construcon lending), include a mortgage over your purchased property,

be in Australian dollars, have appropriate lending limits to recognise the RFHBG’s

deposit requirements, sele aer your lender commences as a Parcipang Lender

under the RFHBG and comply with relevant laws and your lender’s own policies. Your

Parcipang Lender will need to ensure that the terms of your home loan arrangement

comply with these maers.

4.2 Home loan products

The RFHBG permits certain categories of home loan products to take the benet of the

RFHBG. These general categories relate to home loans for:

• the purchase of an established dwelling

• a house and land package

• a land and separate contract to build a home, and

• an ‘o-the-plan’ purchase.

If you are intending to buy vacant land and construct a dwelling on that land, you will

need to enter into a building contract to build a home on the land within six months of

the loan selement date for the eligible loan to acquire the land.

If you already own vacant land and intend to take a new home loan to construct a

dwelling on that land, your home loan is not eligible for the RFHBG. This is because you

do not sasfy the property ownership test.

You will need to contact your lender to clarify whether your home loan is eligible

under the RFHBG.

22 | Informaon Guide – Regional First Home Buyer Guarantee

The condions under the RFHBG for home loan product categories that may be Eligible Loans are as follows.

Contract & selement

dates

To be eligible for the RFHBG, the contract of sale and (if applicable) eligible

building contract may have parcular dates when they can be signed by

you (all as described further below). There are no excepons from these

required dates.

Purchase of exisng

dwelling

If you are purchasing an exisng dwelling:

• you must move into the property within 6 months of the selement of

your home loan, and

• the property must be purchased under a contract of sale that you sign on

or aer 1 October 2022.

This category does not include ‘o-the-plan’ purchases, which are

described below.

House and land packages

A house and land package is where you build a home by entering into a

contract of sale to purchase land from the same person (or persons within

the same corporate group) as the person who you enter into a contract with

to build your home.

For a house and land package, prior to the selement date for your home

loan you will need to have entered into:

• a contract of sale for the land, and

• an eligible building contract to build your home on that land.

These can either be in the same contract or two separate contracts. Your

home loan will also include a requirement for you to:

• start building your home within 12 months, and

• nish building your home within 24 months of the selement date for

your home loan.

You will also need to move into the property within 6 months of an

occupancy cercate being issued.

Informaon Guide – Regional First Home Buyer Guarantee | 23

Land and separate contract

to build a home

A land and separate contract to build a home is where you build a home

by entering into a contract of sale to acquire land from a person who is

dierent to the person you enter into a contract with to build your home.

For a land and separate contract to build a home, you will need to have

entered into a contract of sale to acquire the land under a contract of sale

or, an eligible lease instrument. You will also need to move into the property

within 6 months of an occupancy cercate being issued.

You may obtain a home loan to buy the land and nance the building of your

home. If you do so, then your Parcipang Lender will require you to enter

into an eligible building contract before the selement of your home loan

and:

• start building your home within 12 months, and

• nish building your home within 24 months of the selement date for

your home loan.

You may be able to obtain a home loan to buy the land before obtaining

a loan to nance the building of your home. If you do so, then your

Parcipang Lender will require you to:

• enter into an eligible building contract within 6 months,

• start building your home within 12 months, and

• nish building your home within 24 months, of the selement date of

your home loan to buy the land.

If you choose to buy the land before obtaining a loan to nance the building

of your home, you will need to ensure that at the me your loan agreement

is entered into to nance the building of your home, the purchase price for

your land and the cost to build your home does not exceed the price cap

that is applicable to your property. If they do exceed the price cap, then

your home loan will not be eligible for the RFHBG and your Participating

Lender may require you to obtain Lenders Mortgage I

nsurance (LMI) or

provide a higher deposit to continue with your home loan.

If you are considering entering into contracts relang to purchasing

land and for the construcon of a home, you may wish to discuss with

your Parcipang Lender (and broker, if applicable) all of the potenal

risks that may be associated with these tr

ansacons. It is worth nong

that you are required to sign a xed price building contract, and that

any amendments to this after signing, may impact the validity of the

Guarantee and your lender may require you to pay Lenders Mortgage

Insurance (LMI) or fund these addional costs yourself.

‘O-the-plan’ purchases

If you are making an ‘o-the-plan’ purchase:

• you must have signed the contract of sale before the settlement date for

your home loan, and

• the settlement date for your home loan must occur within 90 days of your

home loan being guaranteed under the RFHBG.

You will also need to move into the property within 6 months of the

selement date for your home loan.

24 | Informaon Guide – Regional First Home Buyer Guarantee

Eligible building contracts

For a building contract to be eligible under the RFHBG it must:

• be with a licensed or registered builder; and

• specify a xed price for the construcon of the dwelling.

‘Owner builder’ contracts are not eligible building contracts for the

RFHBG.

Parcipang Lenders may, or may not, oer these types of home loan products. Even if they do oer these

products, the terms of the home loan may be more limited than described above. You should contact your

lender and/or ask your professional adviser(s) about the home loan products that are oered and whether they

suit the purchase you are intending to make.

Parcipang Lenders require your land to be tled prior to the issuance of a Housing Australia guarantee,

therefore the land will need to be tled before the end of your 90 day pre-approval period.

Informaon Guide – Regional First Home Buyer Guarantee | 25

5. Which properes are

eligible for the Regional

First Home Buyer

Guarantee?

5.1 Eligible Properes

Not all properes are eligible for the RFHBG.

The key eligibility checks for any property that you want to purchase are that:

• the property is located in a regional area that is the same or adjacent to a regional

area to where you have lived for the preceding 12 months to the Home Loan Date

• it is a ‘residenal property’ – under the RFHBG this term has the same meaning as

under the Naonal Consumer Credit Protecon Act, and you should ask your lender

if there is any doubt

• the purchase price of the property is under the price cap for its locaon – see

secon 5.2 ‘Property price caps’

• the property is (1) an established dwelling, or (2) a new-build dwelling that you

purchase under a house and land package, a land and separate contract to build a

home or an ‘o-the-plan’ arrangement that is nanced under an Eligible Loan – see

secon 4 ‘Which home loans are eligible for the First Home Guarantee? for further

details, and

• at the selement date for your home loan, the borrower(s) will be the sole

registered owner of the property.

5.2 Property price caps

The price caps are outlined in the tables below. Your lender will be able to conrm

which price cap is applicable to your property by its suburb. If the purchase price, or in

the case of a new build, land and separate contract to build home, the land purchase

price and construcon costs, for your property is more than the price cap for its

locaon (as listed in the table over the page), the property will not be eligible for the

RFHBG. Note the greater capital city areas of each state and the Northern Territory;

and the enre Australian Capital Territory are excluded from the RFHBG.

26 | Informaon Guide – Regional First Home Buyer Guarantee

State Regional centre* All other

regional areas

New South Wales $900,000 $750,000

Victoria $800,000 $650,000

Queensland $700,000 $550,000

Western Australia $450,000

South Australia $450,000

Tasmania $450,000

Territory All areas

ACT Not applicable

NT Regional $600,000

Jervis Bay Territory & Norfolk Island $550,000

Christmas Island & Cocos (Keeling) Islands $400,000

* Regional centres are Newcastle and Lake Macquarie, Illawarra, Geelong, Gold Coast and Sunshine Coast.

A postcode look-up tool is available at www.housingaustralia.gov.au for general informaon on price caps per each

dierent Guarantee available under the Home Guarantee Scheme in a parcular area. You are able to use this tool to

get an idea of whether a property is in a parcular price cap area. However, you should not rely upon the informaon

provided by the tool and must conrm the price cap for any property you are thinking about purchasing with your

lender.

A Regional Checker is also available at www.housingaustralia.gov.au to assist conrming whether you live in a

regional area, and what postcodes you may be able to purchase in.

Informaon Guide – Regional First Home Buyer Guarantee | 27

6. Other Regional First

Home Buyer Guarantee

features & important

informaon

6.1 Regional First Home Buyer Guarantee Place

Reservaons

Depending upon your circumstances, your Parcipang Lender may be able to reserve

a place under the RFHBG in conjuncon with you making your home loan applicaon.

Requests for RFHBG Place Reservaons can only be made by Parcipang Lenders.

A RFHBG Place Reservaon does not guarantee that your home loan will parcipate

in the RFHBG. There are other checks and ming requirements that apply before your

home loan is able to be guaranteed under the RFHBG.

If your Parcipang Lender elects to reserve a place under the RFHBG in conjuncon

with you making your home loan applicaon, the following steps apply.

28 | Informaon Guide – Regional First Home Buyer Guarantee

Your inial home loan

applicaon

Your Participating Lender will be able to make a RFHBG Place

Reservation for up to 14 days while they assess your finance application.

This reservaon:

• is made by a Participating Lender at the same time as your home loan

application is made or is being assessed, and you will need to provide

them with some personal information for this to happen – see section 1.3

‘Getting ready – what will I need to provide to my lender?’

• is for a set period (usually, 14 days but your lender will advise you if the

period is different) from when it is first made by any Participating Lender

–

you can make home loan applications to more than one Participating

Lender in this period, but the 14-day reservation is counted from the day

when the first lender makes the reservation – see Scenario 1 below for an

illustration of how this works

• will be able to be extended by your lender if finance pre-approval is given

for your home loan – see ‘Getting finance pre-approval’ below, and

• will expire if (1) you are not pre-approved for finance from a Participating

Lender during this period, or (2) if you are pre-approved for finance and

your lender does not let Housing Australia know to extend the reservation

by the end of the 14-day period.

Scenario 1 – inial reservaon

Annabel makes a home loan inquiry with Lender A on 1 July 2024, and

Lender A makes an inial RFHBG Place Reservaon on that date. The

reservaon period for Annabel and her home loan is open for 14 days

and will expire at 11.59 pm (Sydney me) on 15 July 2024. This will be

the expiry me for all RFHBG Place Reservaons that are submied

for Annabel’s home loan applicaons by Parcipang Lenders in that

reservaon period.

She also makes another home loan applicaon with Lender B on 5 July

2024 and Lender B makes another inial RFHBG Place Reservaon on

that date. The reservaon period for Annabel and her home loan is

already open and so Lender B has 10 days to take necessary acons

before the period expires.

For the reservaon to be extended (see ‘Geng nance preapproval’

below), Lender A or Lender B will need to provide nance pre-approval

to Annabel and take the necessary acon to extend the reservaon

before the expiry me of 11.59 pm (Sydney me) on 15 July 2024.

Geng nance

pre-approval

If your lender has given you a nance pre-approval, your RFHBG Place

Reservaon can be extended for a further 90 days (starng on the rst date

that it is extended by a Parcipang Lender) – see Scenario 2 below for a

further illustraon of how this works.

This further reservaon period is to allow you to nd and sign a contract of

sale for an Eligible Property that you want to buy.

If during this 90-day reservaon period:

• you are unable to nd an Eligible Property that you want to buy, or

• your lender withdraws your nance pre-approval or believes that you are

not likely to enter into a home loan for an Eligible Property, the RFHBG

Place Reservaon for your home loan will expire.

Informaon Guide – Regional First Home Buyer Guarantee | 29

Scenario 2 – pre-approval reservaon

In considering Annabel’s home loan applicaon, Lender A provides her

with a nance pre-approval on 14 July 2024 and takes the necessary

steps to extend the RFHBG Place Reservaon for her home loan on

that date. The RFHBG Place Reservaon is then extended by 90 days

from the day that Lender A takes those steps. This extension will

apply for both Lender A and Lender B, to now expire at 11.59 pm on

12 October 2024.

Lender B does not provide Annabel with pre-approval before the expiry

me for the inial reservaon but because Lender A has extended

her RFHBG Place Reservaon, Lender B will have unl 11.59 pm on 12

October 2024 to provide Annabel with nance pre-approval.

Signing your contract

for sale

Once you have signed a contract for sale to purchase an Eligible Property,

your RFHBG Place Reservaon can be extended for an addional 30 days

from the signing date.

This addional period is to enable you and your lender to nalise the

paperwork and checks for your home loan. Your lender may ask you to

provide informaon and materials in a shorter period than the 30 days.

To ensure that this extension applies, you will need to tell your lender

immediately once you have signed your contract for sale so that your lender

can nofy Housing Australia.

If you are unable to nalise your loan within this period, the RFHBG Place

Reservaon for your home loan will expire.

Before entering into a contract of sale, you should consider discussing

your lending needs with your relevant Parcipang Lender, broker or

nance professional.

You should also consider discussing the impacts of any amendments to

this contract aer signing, and how they may potenally impact your

RFHBG place.

What happens if a

reservaon expires

If any reservaon period expires without being extended, the RFHBG Place

Reservaon for your home loan will lapse and your Parcipang Lender

would need to make a new reservaon under the RFHBG.

With the number of places under the RFHBG being limited, there may not

be a place under the RFHBG that is available to be reserved or taken up at

that later me and you may need to wait unl the next nancial year to

apply for a place.

In all circumstances, the decision to enter into a home loan arrangement with a Parcipang Lender, and the

choice of property to purchase, is your own responsibility. Even though the availability of the RFHBG for home

loans is limited – by number of places and the me periods for the reservaon process – you should seek your

own independent nancial and legal advice as to whether a parcular home loan or property, and the terms of

the RFHBG suit your personal circumstances and objecves.

6.2 Home Buyer Declaraon

A Home Buyer Declaraon is provided to you by a Parcipang Lender for the purposes of them applying to Housing

Australia for your home loan to be covered by the RFHBG. You must sign and submit your Home Buyer Declaraon to

your lender in accordance with their instrucons.

Housing Australia will not take any acon or steps in relaon to a Home Buyer Declaraon that is delivered to it

by any person (including you) or instuon that is not a Parcipang Lender (or a Representave or agent of it).

It is recommended that you provide the completed and signed declaraon to your lender as soon as possible. A copy

of this declaraon will also be provided by your lender to Housing Australia, who will retain the copy as a record.

You should be aware that this form is separate to (1) your applicaon for a home loan from your lender, and (2) any

forms that you are required to submit in relaon to any other home buyer schemes or programs.

Before compleng a Home Buyer Declaraon, you should carefully read all secons and informaon contained in the

form and ask your lender and/or your professional adviser(s) if anything is unclear.

You must ensure that all informaon contained in your Home Buyer Declaraon is complete and correct. If you are

unsure about any of your obligaons or informaon that is required as part of any applicaon for your home loan to

be covered by the RFHBG it is important that you contact your lender for claricaon.

You must nofy your lender if you believe that you cease at any me to meet the eligibility requirements of the

RFHBG or if there is any change to the informaon provided in the Home Buyer Declaraon aer you have signed and

submied it.

Penales may apply for a false Home Buyer declaraon.

6.3 Renancing your Regional First Home Buyer Guarantee-

guaranteed home loan

If you have a home loan that is already parcipang under the RFHBG, you may be able to renance your home loan

with another Parcipang Lender and connue to have the benet of the RFHBG.

Any such renancing is subject to condions, and you should contact your new lender for further details if you are

considering renancing your exisng RFHBG home loan with another Parcipang Lender.

It is not possible for your home loan to connue to have the benet of the RFHBG if it is renanced with another

lender that is not a Parcipang Lender.

6.4 Privacy statement

Your personal informaon may be used by your lender, Housing Australia and/or the Australian Government for

the

administraon and operaon of the RFHBG and assessing your eligibility under the RFHBG.

By requesng a Parcipang Lender to take any steps to have your home loan covered by the RFHBG or by

compleng and subming a Home Buyer Declaraon, you consent to your lender, Housing Australia and/or the

Australian Government collecng, using and disclosing your personal informaon for the abovemenoned purposes

and any other incidental or related purpose.

Your lender, Housing Australia and/or the Australian Government may disclose your personal information to any party

engaged in the assessment or administration of the RFHBG.

Your lender, Housing Australia and/or the Australian Government will store personal informaon collected through

your home loan applicaon process (including informaon to assess your eligibility under the RFHBG), supporng

documents, the loan agreement and any monitoring, research and evaluaon acvies in compliance with their

respecve obligaons under the Privacy Act and any other privacy legislaon applicable in their jurisdicon.

Your personal informaon will not be disclosed overseas. You may access or correct your personal informaon at any

me by contacng your lender.

Further informaon about your lender’s privacy policy and Housing Australia’s privacy policy, including rights of

access and complaints handling, may be accessed at your lender’s website or

www.housingaustralia.gov.au (as applicable).

30 | Informaon Guide – Regional First Home Buyer Guarantee

Informaon Guide – Regional First Home Buyer Guarantee | 31

7. Checklists – Your Eligibility

Checks

The following checklists are to assist you to work through Your Eligibility Checks. You should refer back to the relevant

secons of this document for further informaon on each check.

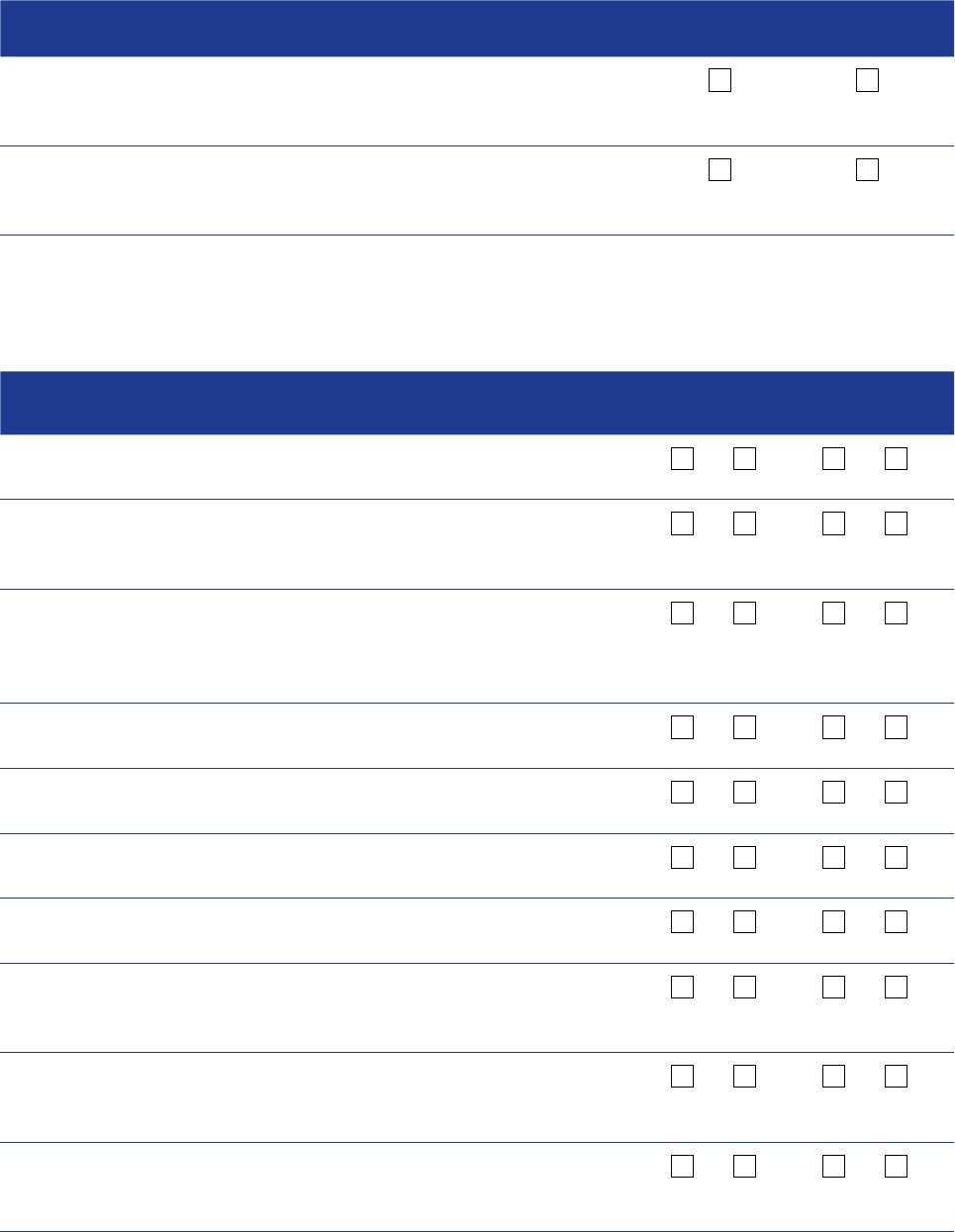

7.1 Inial check – eligibility as an individual or as joint applicants

No. Queson

RFHBG Guide

secon Your answer

Q. Will you be applying under the RFHBG as an

individual or as joint applicants?

2.1.2

Individual

You should

complete the

checks for

individuals at

secon 7.2

Joint

applicants

You should

complete the

checks for joint

applicants at

secon 7.3

7.2 Checks for individuals

The following checks are applicable for individuals. If you answer ‘no’ to any of the quesons, you will not be eligible

to parcipate in the RFHBG.

No. Queson

RFHBG Guide

secon Your answers

Q1. Have you lived in a regional area for the preceding

12 month period?^

2.1.1

Yes No

Q2. Is the property you intend to buy located in

the regional area you live in or an adjacent

regional area?

2.1.1 & 2.1.5

Yes No

Q3. Do you have your Noce of Assessment for the

2023-24 income year (as issued by the Australian

Taxaon Oce) (or did you earn less than the tax-

free threshold)?

2.1.3

Yes No

Q4.

Do you satisfy the income test (for individuals) at

your Home Loan Date?

2.1.3

Yes No

Q5. Will you sasfy the prior property ownership test

at your Home Loan Date?

2.1.4

Yes No

Q6. Will you be an Australian cizen or permanent

resident at your Home Loan Date?

2.1.5

Yes No

Q7. Will you be 18 years or over at your Home

Loan Date?

2.1.6

Yes No

Q8. Do you have a deposit of at least 5% and less

than 20% of the Value of the property you would

like to buy?

2.1.7

Yes No

32 | Informaon Guide – Regional First Home Buyer Guarantee

No. Queson

RFHBG Guide

secon Your answers

Q9. Do you intend to reside in the property you buy

as an owner-occupier while your home loan is

guaranteed under the RFHBG?

2.1.8

Yes No

Q10. Are you sure there are no maers in your personal

circumstances that could mean you aren’t eligible

for the RFHBG?

2.1.9

Yes No

7.3 Checks for joint applicants

The following checks are applicable for joint applicants.

If either of you answer ‘no’ to any of the quesons, you will not be eligible to parcipate in the RFHBG.

No. Queson

RFHBG Guide

secon

Your answer

Applicant 1 Applicant 2

Q1. Have either of you lived in a regional area for the

preceding 12 month period?^

2.1.1

Yes No Yes No

Q2. Is the property you intend to buy located in

the regional area you live in or an adjacent

regional area?

2.1.1 & 2.1.5

Yes No Yes No

Q3. Do you have your Noce of Assessment for the

2023-24 income year (as issued by the Australian

Taxaon Oce) (or did you earn less than the tax-

free threshold)?

2.1.3

Yes No Yes No

Q4. Do you (together) sasfy the income test (for

joint applicants) at your Home Loan Date?

2.1.3

Yes No Yes No

Q5. Will you sasfy the prior property ownership test

at your Home Loan Date?

2.1.4

Yes No Yes No

Q6. Will you be an Australian cizen or permanent

resident at your Home Loan Date?

2.1.5

Yes No Yes No

Q7. Will you be 18 years or over at your Home

Loan Date?

2.1.6

Yes No Yes No

Q8. Do you (together) have a deposit of at least 5%

and less than 20% of the Value of the property

you would like to buy?

2.1.7

Yes No Yes No

Q9. Do you intend to reside in the property you buy

as an owner-occupier while your home loan is

guaranteed under the RFHBG?

2.1.8

Yes No Yes No

Q10. Are you sure there are no maers in your

personal circumstances that could mean you

aren’t eligible for the RFHBG?

2.1.9

Yes No Yes No

^ Employees required by their current employer to relocate may be eligible and should check with their Parcipang Lender (see secon 2.1.1)

Informaon Guide – Regional First Home Buyer Guarantee | 33

8. Glossary

Eligible Loan A home loan made by a Parcipang Lender that is eligible to parcipate

under the RFHBG.

Eligible Property A residenal property that is eligible to parcipate under the RFHBG.

Home Buyer Declaraon The form of statutory declaraon provided to you by your Parcipang

Lender in relaon to the RFHBG.

HGS Home Guarantee Scheme.

Home Loan Date The date when you sign your home loan agreement with your Parcipang

Lender.

You will need to conrm what this date is with your Parcipang Lender, as it

may dier between you and another home buyer and may be dierent from

other lenders and for parcular purposes, depending upon their procedures

for loan approvals and how they parcipate under the RFHBG.

Income Tax Assessment Act Income Tax Assessment Act 1997 (Cth).

Naonal Consumer Credit Protecon Act Naonal Consumer Credit Protecon Act 2009 (Cth).

Parcipang Lender Each eligible lender that has been approved by Housing Australia, as listed

on the Scheme webpage at www.housingaustralia.gov.au. These include

the Major Bank Lenders and the Non-Major Lenders. A reference in this

document to “your lender” is a reference to your Parcipang Lender.

Permanent resident An Australian permanent resident has the same meaning as in the Australian

Cizenship Act 2007 (Cth)

Privacy Act Privacy Act 1988 (Cth).

Real property “Real property” means the land, everything permanently aached to it, and

all of the interests, benets, and rights inherent in the ownership of real

estate.

Representave For any Parcipang Lender, any third-party broker or other person that is

authorised by the Parcipang Lender to suggest that Eligible Borrowers

may apply for, or to assist Eligible Borrowers to apply for, Eligible Loans with

the Parcipang Lender.

Regional First Home Buyer Guarantee The Regional First Home Buyer Guarantee (RFHBG) is part of the Home

Guarantee Scheme.

RFHBG Place Reservaon A reservaon made by a Parcipang Lender for a guarantee to apply for

your home loan under the RFHBG.

Scheme The Australian Government’s Home Guarantee Scheme (HGS).

Scheme Webpage The Scheme Webpage for the Home Guarantee Scheme is at

www.housingaustralia.gov.au

Informaon in relaon to the Scheme that is included on or available

through the Scheme Webpage is general informaon only and it does not

form part of this document.

Value The ‘Value’ of the property you purchase as assessed by the Parcipang

Lender for your home loan in accordance with the requirements of the

RFHBG.

^ Employees required by their current employer to relocate may be eligible and should check with their parcipang lender (see secon 2.1.1)

LDS 1200 06/24