Risk, resilience, and rebalancing in global value chains

August 2020

Risk, resilience,

and rebalancing

in global

value chains

McKinsey Global Institute

Since its founding in 1990, the McKinsey Global Institute (MGI) has sought to develop a

deeper understanding of the evolving global economy. As the business and economics

research arm of McKinsey & Company, MGI aims to help leaders in the commercial,

public, and social sectors understand trends and forces shaping the global economy.

MGI research combines the disciplines of economics and management, employing the

analytical tools of economics with the insights of business leaders. Our “micro-to-macro”

methodology examines microeconomic industry trends to better understand the broad

macroeconomic forces affecting business strategy and public policy. MGI’s in-depth

reports have covered more than 20 countries and 30 industries. Current research

focuses on six themes: productivity and growth, natural resources, labor markets, the

evolution of global financial markets, the economic impact of technology and innovation,

and urbanization. Recent reports have assessed the digital economy, the impact of AI

and automation on employment, physical climate risk, global health, income inequality,

the productivity puzzle, the economic benefits of tackling gender inequality, a new era

of global competition, Chinese innovation, and digital and financial globalization.

MGI is led by three McKinsey & Company senior partners: co-chairs James Manyika and

Sven Smit and director Jonathan Woetzel. Michael Chui, Susan Lund, Anu Madgavkar,

Jan Mischke, Sree Ramaswamy, Jaana Remes, Jeongmin Seong, and Tilman Tacke are

MGI partners. Mekala Krishnan is an MGI senior fellow, and Sundiatu Dixon-Fyle is a

visiting senior fellow. Project teams are led by the MGI partners and a group of senior

fellows and include consultants from McKinsey offices around the world. These teams

draw on McKinsey’s global network of partners and industry and management experts.

The MGI Council is made up of McKinsey leaders and includes Michael Birshan,

Andrés Cadena, Sandrine Devillard, André Dua, Kweilin Ellingrud, Tarek Elmasry,

Katy George, Rajat Gupta, Eric Hazan, Acha Leke, Gary Pinkus, Oliver Tonby, and

Eckart Windhagen. The Council members help shape the research agenda, lead high-

impact research, and share the findings with decision makers around the world. In

addition, leading economists, including Nobel laureates, advise MGI research.

This report contributes to MGI’s mission to help business and policy leaders understand

the forces transforming the global economy and prepare for the next wave of growth. As

with all MGI research and reports, this work is independent and reflects our own views.

This report was not commissioned or paid for by any business, government, or other

institution, and it is not intended to promote the interests of McKinsey’s clients. For further

information about MGI and to download reports, please visit www.mckinsey.com/mgi.

Risk, resilience,

and rebalancing in

global value chains

Authors

Susan Lund, Washington, DC

James Manyika, San Francisco

Jonathan Woetzel, Shanghai

Ed Barriball, Washington, DC

Mekala Krishnan, Boston

Knut Alicke, Stuttgart

Michael Birshan, London

Katy George, New Jersey

Sven Smit, Amsterdam

Daniel Swan, Stamford

Kyle Hutzler, Washington, DC

August 2020

Preface

Manufactured goods take lengthy and complex journeys through global value chains as raw

materials and intermediate inputs are turned into the final products that reach consumers.

But global production networks that took shape to optimize costs and efficiency often

contain hidden vulnerabilities—and external shocks have an uncanny way of finding and

exploiting those weaknesses. In a world where hazards are occurring more frequently and

causing greater damage, companies and policy makers alike are reconsidering how to make

global value chains more resilient. All of this is occuring against a backdrop of changing cost

structures across countries and growing adoption of revolutionary digital technologies in

global manufacturing.

Applying MGI’s micro-to-macro methodology, this report considers the issues and investment

choices facing individual companies as well as the implications for global value chains, trade,

and national economies. It builds on a large multiyear body of MGI research on topics such

as global value chains and flows, manufacturing, digitization, and climate risk. This includes

major reports such as Manufacturing the future (2012), Global flows in a digital age (2014),

Digital globalization (2016), Making it in America (2017), Globalization in transition (2019),

and Climate risk and response (2020), among others. This work also draws on McKinsey’s

on-the-ground experience in operations, supply chain management, and risk across

multiple industries.

Our past research highlights important structural changes in the nature of globalization;

goods producing value chains have become less trade-intensive, even as cross-border

services are increasing. The share of global trade based on labor-cost arbitrage has been

declining over the last decade and global value chains are becoming more knowledge-

intensive and reliant on high-skill labor. Finally, goods-producing value chains are becoming

more regionally concentrated. This report extends that research to better understand supply

chain risk and resiliency. While the COVID pandemic has delivered the biggest and broadest

value chain shock in recent memory, it is only the latest in a series of disruptions that has

exposed value chains and companies to damages.

The research was led by SusanLund, an MGI partner based in Washington, DC;

JamesManyika, MGI’s co-chair, based in San Francisco; JonathanWoetzel, an MGI director

based in Shanghai; EdBarriball, a Washington, DC–based partner who specializes in

manufacturing, supply chain, and logistics; MekalaKrishnan, an MGI senior fellow, based in

Boston; KnutAlicke, a Stuttgart-based partner with expertise in manufacturing and supply

chains; MichaelBirshan, a London-based senior partner who focuses on strategy and risk;

KatyGeorge, a New Jersey–based senior partner with expertise in manufacturing, operations

strategy, and operating model design; SvenSmit, MGI’s co-chair, based in Amsterdam;

and DanSwan, who leads McKinsey’s global supply chain practice. The project team, led

by KyleHutzler, included BaderAlmubarak, DjavanehBierwirth, MackenzieDonnelly,

DhirajKumar, KarolMansfeld, PalakPujara, and StephanieStefanski. HenryMarcil also

provided leadership, insight, and support.

Many McKinsey colleagues contributed to this effort, and our research benefited

immensely from their industry expertise and perspectives. We are grateful to IngoAghte,

EmreAkgul, AykutAtali, XavierAzcue, CengizBayazit, StefanBurghardt, OndrejBurkacky,

AnaCalvo, BobCantow, StephenChen, JeffreyCondon, AlanDavies, ArnavDey,

ReedDoucette, HillaryDukart, ElenaDumitrescu, PhilDuncan, KimElphinstone, AnkitFadia,

IgnacioFelix, TacyFoster, KevinGoering, ArvindGovindarajan, PaulHackert, WillHan,

PhilippHärle, LizHempel, DrewHorah, ToreJohnston, RoosKarssemeijer, PeteKimball,

TimKoller, VikKrishnan, RandyLim, Karl-HendrikMagnus, YogeshMalik, AdrianMartin,

BrendenMcKinney, Ricardo Moya-Quiroga, MikeParkins, ParagPatel, FernandoPerez,

ii McKinsey Global Institute

MoiraPierce, JoseMariaQuiros, SreeRamaswamy, RafaelRivera, SeanRoche, PeterRussell,

PaulRutten, JulianSalguero, HamidSamandari, EmilyShao, SmritiSharma, AnnaStrigel,

KrishSuryanarayan, NicoleSzlezak, VaibhavTalwar, and BillWiseman.

We would also like to thank LauraTyson, Distinguished Professor of the Graduate School

at Haas School ofBusiness, University of California, Berkeley, who served as our academic

adviser. We also thank VinodSinghal, Charles W. Brady Chair at the Georgia Tech Scheller

College of Business, and BrianJacobs, associate professor at the Pepperdine Graziadio

Business School, for their insights in the early stages of this effort.

This report was produced by MGI executive editor LisaRenaud, editorial production

manager JuliePhilpot, and senior graphic designers MarisaCarder and PatrickWhite. We

also thank our colleagues DennisAlexander, TimBeacom, NienkeBeuwer, LauraBrown,

AmandaCovington, CathyGui, PeterGumbel, ChristenHammersley, DeadraHenderson,

RichardJohnson, DaphneLautenberg, RachelMcClean, LaurenMeling, LaurenceParc,

RebecaRobboy, DanielleSwitalski, and KatieZnameroski for their contributions and support.

This report contributes to MGI’s mission to help business and policy leaders understand

risks our society and the global economy face and how to build resilience against them. As

with all MGI research, this work is independent, reflects our own views, and has not been

commissioned by any business, government, or other institution. We welcome your comments

on the research at MGI@mckinsey.com.

James Manyika

Director and Co-chair, McKinsey Global Institute

Senior Partner, McKinsey & Company

San Francisco

Sven Smit

Director and Co-chair, McKinsey Global Institute

Senior Partner, McKinsey & Company

Amsterdam

Jonathan Woetzel

Director, McKinsey Global Institute

Senior Partner, McKinsey & Company

Shanghai

August 2020

iiiRisk, resilience, and rebalancing in global value chains

© Out of the Box/Stocksy

In brief

Risk, resilience, and rebalancing

in global value chains

Intricate supplier networks that span

the globe can deliver with great

efficiency, but they may contain

hidden vulnerabilities. Even before

the COVID19 pandemic, a multitude

of events in recent years temporarily

disrupted production at many

companies. Focusing on value chains

that produce manufactured goods,

this research explores their exposure

to shocks, their vulnerabilities, and

their expected financial losses. We

also assess prospects for value chains

to change their physical footprint

in response to risk and evaluate

strategies to minimize the growing cost

of disruptions.

Shocks that affect global production

are growing more frequent and

more severe. Companies face a range

of hazards, from natural disasters

to geopolitical uncertainties and

cyberattacks on their digital systems.

Global flows and networks offer

more “surface area” for shocks to

penetrate and damage to spread.

Disruptions lasting a month or longer

now occur every 3.7 years on average,

and the financial toll associated with

the most extreme events has been

climbing. Shocks can be distinguished

by whether they can be anticipated,

how frequently they occur, the breadth

of impact across industries and

geographies, and the magnitude of

impact on supply and demand.

Value chains are exposed to

different types of shocks based

on their geographic footprint,

factors of production, and other

variables. Those with the highest trade

intensity and export concentration

in a few countries are more exposed

than others. They include some of

the highest-value and most sought-

after industries, such as communication

equipment, computers and electronics,

and semiconductors and components.

Many labor-intensive value chains,

such as apparel, are highly exposed to

pandemics, heat stress, and flood risk.

In contrast, food and beverage and

fabricated metals have lower average

exposure to shocks because they

are among the least traded and most

regionally oriented value chains.

Operational choices can heighten

or lessen vulnerability to shocks.

Practices such as just-in-time

production, sourcing from a single

supplier, and relying on customized

inputs with few substitutes amplify

the disruption of external shocks and

lengthen companies’ recovery times.

Geographic concentration in supply

networks can also be a vulnerability.

Globally, we find 180 traded products

(worth $134 billion in 2018) for which

a single country accounts for the vast

majority of exports.

Value chain disruptions cause

substantial financial losses. Adjusted

for the probability and frequency of

disruptions, companies can expect to

lose more than 40 percent of a year’s

profits every decade on average. But

a single severe event that disrupts

production for 100 days—something

that happens every five to seven

years on average—could erase almost

a year’s earnings in some industries.

Disruptions are costly to societies,

too: after disasters claim lives and

damage communities, production

shutdowns can cause job losses and

goods shortages. Resilience measures

could more than pay off for companies,

workers, and broader societies over

the long term.

The interconnected nature of value

chains limits the economic case for

making large-scale changes in their

physical location. Value chains often

span thousands of companies, and their

configurations reflect specialization,

access to consumer markets around

the world, long-standing relationships,

and economies of scale. Primarily

labor-intensive value chains (such as

apparel and furniture) have a strong

economic rationale for shifting to new

locations. Noneconomic pressures

may prompt movement in others, such

as pharmaceuticals. Considering

both industry economics and national

policy priorities, we estimate that 16

to 26 percent of global goods exports,

worth $2.9 trillion to $4.6 trillion, could

conceivably move to new countries

over the next five years if companies

restructure their supplier networks.

Building supply chain resilience

can take many forms beyond

relocating production. This includes

strengthening risk management

capabilities and improving

transparency; building redundancy

in supplier and transportation

networks; holding more inventory;

reducing product complexity; creating

the capacity to flex production across

sites; and improving the financial and

operational capacity to respond to

shocks and recover quickly from them.

Becoming more resilient does not have

to mean sacrificing efficiency. Our

research highlights the many options

for strengthening value chain resilience,

including opportunities arising from

new technologies. Where companies

cannot directly prevent shocks,

they can still position themselves to

reduce the cost of disruption and

the time it takes to recover. Companies

have an opportunity to emerge

from the current crisis more agile

and innovative.

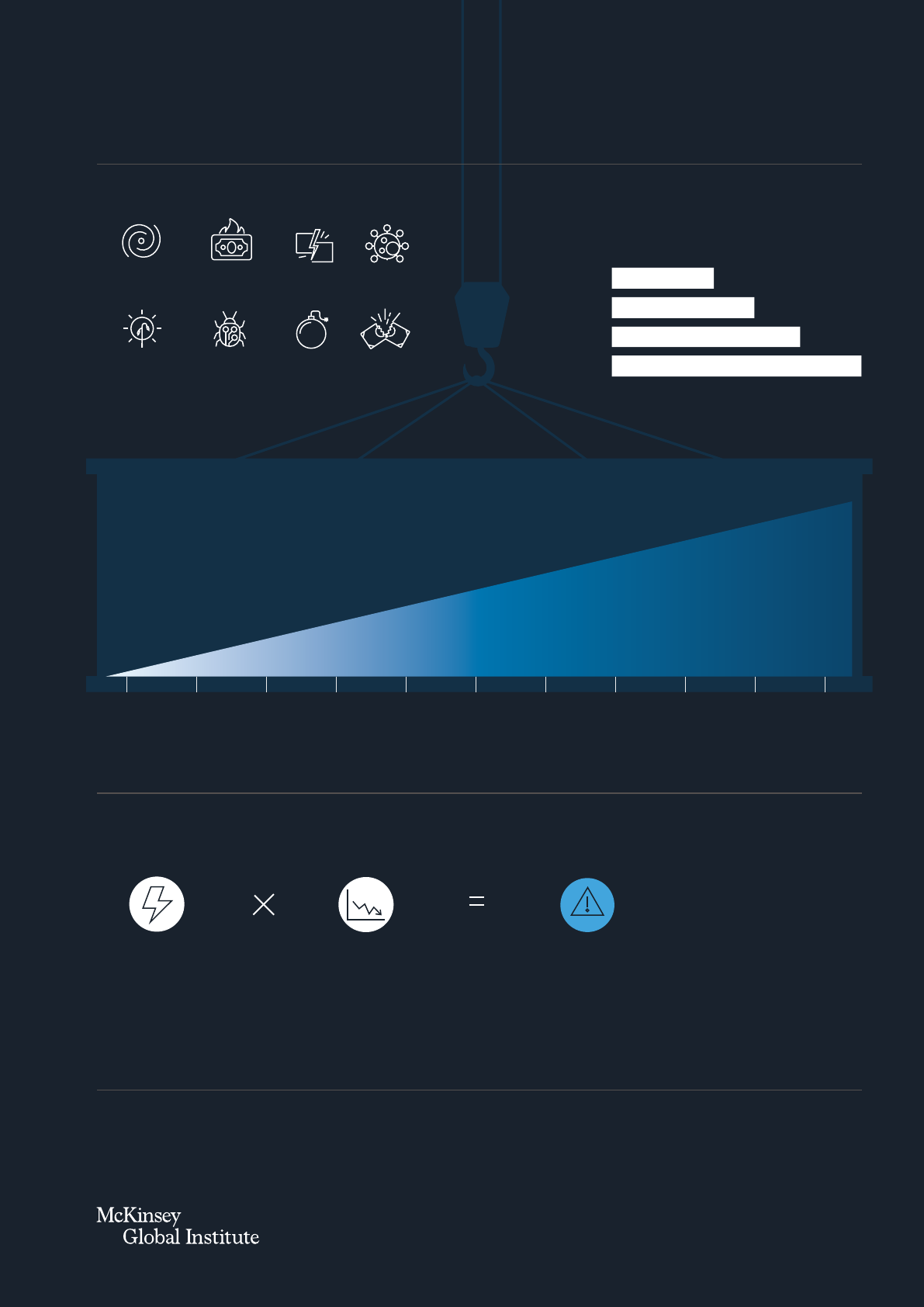

Companies can build resilience by improving supply chain management

and transparency, minimizing exposure to shocks,

and building their capacity to respond

of one year's EBITDA

every decade.

Investing to minimize

these losses can pay

o over the long term

42%

Companies can

expect to lose

Fragility in key areas

Demand planning and inventory

Supplier network structure

Transportation and logistics

Balance sheet

Product and portfolio complexity

Unexpected events that

cause disruption

Force majeure

Macropolitical

Malicious actors

Idiosyncratic

Value chain risk

Vulnerability

Shock exposure

Supply chain disruptions are costly

Risk, resilience, and rebalancing

in global value chains

Less exposed More exposed

Communi-

cation

equipment

Apparel

Petroleum

products

Computers

and

electronics

Aerospace

Semicon-

ductors

ChemicalsAutomotive

Pharma-

ceuticals

Food and

beverage

Medical

devices

Some value chains are more exposed to shocks than others

Based on geographic footprint, factors of production, and other characteristics

4.9 years

3.7 years

2.8 years

2.0 years

2+ months

1–2 months

2–4 weeks

1–2 weeks

. . . occurs at

this interval

A disruption of

this length . . .

Supplier

bankruptcy

Terrorism

Cyberattack

Chronic

climate change

Pandemic

Trade

dispute

Macroeconomic/

nancial crises

Acute climate

change

Supply chain shocks are becoming more frequent and severe

© Miguel Navarro/DigitalVision/Getty Images

In recent decades, value chains have grown in length and complexity as companies expanded

around the world in pursuit of margin improvements. Since 2000, the value of intermediate

goods traded globally has tripled to more than $10 trillion annually. Businesses that

successfully implemented a lean, global model of manufacturing achieved improvements in

indicators such as inventory levels, on-time-in-full deliveries, and shorter lead times.

However, these operating model choices sometimes led to unintended consequences if

they were not calibrated to risk exposure. Intricate production networks were designed for

efficiency, cost, and proximity to markets but not necessarily for transparency or resilience.

Now they are operating in a world where disruptions are regular occurrences. Averaging

across industries, companies can now expect supply chain disruptions lasting a month or

longer to occur every 3.7 years, and the most severe events take a major financial toll.

This report explores the rebalancing act facing many companies in goods-producing value

chains as they seek to get a handle on risk. Our focus is not on ongoing business challenges

such as shifting customer demand and suppliers failing to deliver, nor on ongoing trends

such as digitization and automation. Instead, we consider risks that manifest from exposure

to the most profound shocks, such as financial crises, terrorism, extreme weather, and,

yes, pandemics.

The risk facing any particular industry value chain reflects its level of exposure to different

types of shocks, plus the underlying vulnerabilities of a particular company or in the value

chain as a whole. We therefore examine the growing frequency and severity of a range of

shocks, assess how different value chains are exposed, and examine the factors in operations

and supply chains that can magnify disruption and losses. Adjusted for the probability and

frequency of disruptions, companies can expect to lose more than 40 percent of a year’s

profits every decade, based on a model informed by the financials of 325 companies across

13 industries. However, a single severe shock causing a 100-day disruption could wipe out

an entire year’s earnings or more in some industries—and events of this magnitude can and

do occur.

Recent trade tensions and now the COVID19 pandemic have led to speculation that

companies could shift to more domestic production and sourcing. We examined the feasibility

of movement based on industry economics as well as the possibility that governments might

act to bolster domestic production of some goods they deem essential or strategic from

a national security or competitiveness perspective. All told, we estimate that production of

some 16 to 26 percent of global trade, worth $2.9 trillion to $4.6 trillion, could move across

borders in the medium term. This could involve some combination of reverting to domestic

production, nearshoring, and shifting to different offshore locations.

Moving the physical footprint of production is only one of many options for building resilience,

which we broadly define as the ability to resist, withstand, and recover from shocks. In fact,

technology is challenging old assumptions that resilience can be purchased only at the cost

of efficiency. The latest advances offer new solutions for running scenarios, monitoring

many layers of supplier networks, accelerating response times, and even changing

the economics of production. Some manufacturing companies will no doubt use these tools

and devise other strategies to come out on the other side of the pandemic as more agile and

innovative organizations.

Executive summary

1Risk, resilience, and rebalancing in global value chains

With shocks growing more frequent and severe, industry value chains

vary in their level of exposure

The COVID pandemic has delivered the biggest and broadest value chain shock in recent

memory (see BoxE1, “Globalization before and after COVID19”). But it is actually the latest

in a long series of disruptions. In 2011, for instance, a major earthquake and tsunami in Japan

shut down factories that produce electronic components for cars, halting assembly lines

worldwide. The disaster also knocked out the world’s top producer of advanced silicon wafers,

on which semiconductor companies rely. Just a few months later, flooding swamped factories

in Thailand that produced roughly a quarter of the world’s hard drives, leaving the makers of

personal computers scrambling. In 2017, Hurricane Harvey, a Category 4 storm, smashed

into Texas and Louisiana. It disrupted some of the largest US oil refineries and petrochemical

plants, creating shortages of key plastics and resins for a range of industries.

This is more than just a run of bad luck. Changes in the environment and in the global economy

are increasing the frequency and magnitude of shocks. Forty weather disasters in 2019

caused damages exceeding $1 billion each—and in recent years, the economic toll caused

by the most extreme events has been escalating.

1

As a new multipolar world takes shape,

we are seeing more trade disputes, higher tariffs, and broader geopolitical uncertainty.

The share of global trade conducted with countries ranked in the bottom half of the world for

political stability, as assessed by the World Bank, rose from 16 percent in 2000 to 29 percent

in 2018. Just as telling, almost 80 percent of trade involves nations with declining political

stability scores.

2

Increased reliance on digital systems increases exposure to a wide variety

of cyberattacks; the number of new ransomware variations alone doubled from 2018 to

2019.

3

Interconnected supply chains and global flows of data, finance, and people offer

more “surface area” for risk to penetrate, and ripple effects can travel across these network

structures rapidly.

To understand the full range of potential disruptions and avoid the trap of “fighting the last

war,” companies must look beyond the latest disaster. Not all shocks are created equal.

Some pass quickly, while others can sideline multiple industry players for weeks or even

months. Business leaders often characterize shocks in terms of their source. These may

include force majeure events, such as natural disasters; macropolitical shocks, such as

financial crises; the work of malicious actors, such as theft; and idiosyncratic shocks, such as

unplanned outages. But characteristics beyond the source of a shock determine its scope

and the severity of its impact on production and global value chains.

Exhibit E1 classifies different types of shocks based on their impact, lead time, and frequency

of occurrence. In a few cases, we show hypothetical shocks like a global military conflict or

a systemic cyberattack that would dwarf the most severe shocks experienced to date. While

these may be only remote possibilities, these scenarios are in fact studied and planned for

by governments and security experts. The impact of a shock can be influenced by how long

it lasts, the ripple effects it has across geographies and industries, and whether a shock hits

the supply side alone or also hits demand.

1

Eye of the Storm, “Earth’s 40 billion-dollar weather disasters of 2019,” Scientific American blog entry by Jeff Masters,

January 22, 2020; and Matteo Coronese et al., “Evidence for sharp increase in the economic damages of extreme natural

disasters,” Proceedings of the National Academy of Sciences, October 2019, Volume 116, Number 43.

2

World Bank, Worldwide Governance Indicators 2018 (political stability and absence of violence/terrorism).

3

Anthony Spadafora, “Ransomware mutations double in 2019,” TechRadar, August 20, 2019.

80%

of global trade involves nations

with declining political stability

scores from the World Bank

2

McKinsey Global Institute

BoxE1

1

Digital globalization: The new era of global flows, McKinsey Global Institute, March 2016.

2

All of the structural trends described here are explored in Globalization in transition: The future of trade and value chains, McKinsey Global Institute, January 2019.

3

Defined as exports from a country where GDP per capita is one-fifth that of the importing country or less. Even if we vary the ratio of GDP per capita of the exporter

and importer, we continue to see a decline in labor-cost arbitrage in value chains producing labor-intensive goods.

4

See Globalization in transition: The future of trade and value chains, McKinsey Global Institute, January 2019.

Globalization before and after COVID‑19

Trade flows ultimately reflect where

countless companies decide to invest

and make, buy, or sell things—as well as

the intermediaries and arrangements

they set up to do this as productively as

possible. Trade in manufactured goods

soared in the 1990s and early 2000s,

propelled by China’s entry into the WTO

and the search by multinational

companies for lower-cost inputs and

wages. Digital communication lowered

transaction costs, enabling companies

to do business with suppliers and

customers halfway around the world.

Overall, goods trade grew at more than

twice the rate of global GDP growth

over this period. MGI’s analysis finds

that, over a decade, all types of flows

acting together have raised world GDP

by 10.1 percent over what would have

resulted in a world without any cross-

border flows.

1

The 2008 financial crisis interrupted

those trends, causing global trade flows

to plummet. When the global economy

recovered, they stabilized but did not

return to their past growth trajectory.

As described in MGI’s 2019 research,

this was largely because China and

other emerging economies reached

the next stage of their development.

2

They initially participated in global value

chains as assemblers of final goods, but

increasingly became the world’s major

engine of demand growth and started

to develop more extensive domestic

supply chains, decreasing their reliance

on imported inputs. As a result of

these developments, a smaller share of

the goods produced worldwide is sold

across borders.

The latest wave of manufacturing

technologies also meant shifting

dynamics within global value chains;

only 13 percent of overall goods trade

in 2018 involved exports from a low-

wage country to a high-wage country.

3

In all except the most labor-intensive

industries, companies started to base

location decisions on other factors,

including access to highly skilled talent,

supplier ecosystems, infrastructure,

business environment, and IP

protection. Another long-term evolution

is the regionalization of production

networks. Long-haul trade between

regions took off in the 1990s and

early 2000s as global supply chains

lengthened. But recently, trade has

become more regionally concentrated,

particularly within Europe and Asia–

Pacific. This has enabled companies

to serve major markets quickly and

responsively. With rising complexity of

global production, as well as concerns

over trade disputes pre-COVID, supply

chain risk and resilience have also been

emerging as increasing considerations

on companies’ radars.

In the wake of the pandemic, travel,

tourism, and migration may take years

to return to previous levels. Trade in

goods has taken a substantial hit,

falling by 13 percent in the first three

months of 2020. But much of this is

due to a sharp contraction in demand

that should eventually reverse when

the virus is contained and economies

recover. In the meantime, cross-border

digital flows continue to take on greater

importance as the connective tissue of

the global economy.

COVID19 seems to be accelerating

some of the trends that were already

manifesting within the world’s value

chains, including the regionalization

of trade and production networks,

the growing role of digitization, and

the focus on proximity to consumers.

4

The increasing use of automation

technologies in manufacturing is

lessening the importance of low labor

costs—and more automated plants

could be more resilient in the face of

pandemics and heat waves (although

potentially more vulnerable to

cyberattacks).

Companies and governments alike

are reassessing the way goods flow

across borders, and they may still

make targeted adjustments to shore

up the places where they see fragility.

But the pandemic has not reshaped

the world’s production networks in

dramatic ways thus far. After all, global

value chains took on their current

structures over many years, reflecting

economic logic, hundreds of billions

of dollars’ worth of investment, and

long-standing supplier relationships.

A major multinational’s supplier

network may encompass thousands

of companies, each with its own

specialized contribution.

Tariffs and tax policies are often

used by governments to try to

shift where things are made. But

many considerations go into where

companies place manufacturing and

where they source. These include

growth in consumer demand, speed

to market, changing labor and

input costs, new technologies, and

the availability of specialized workforce

skills. Risk and resilience now feature

prominently on that list as well—and

even though the costs of risk are

growing, they do not imply the end of

globalization’s opportunities.

3Risk, resilience, and rebalancing in global value chains

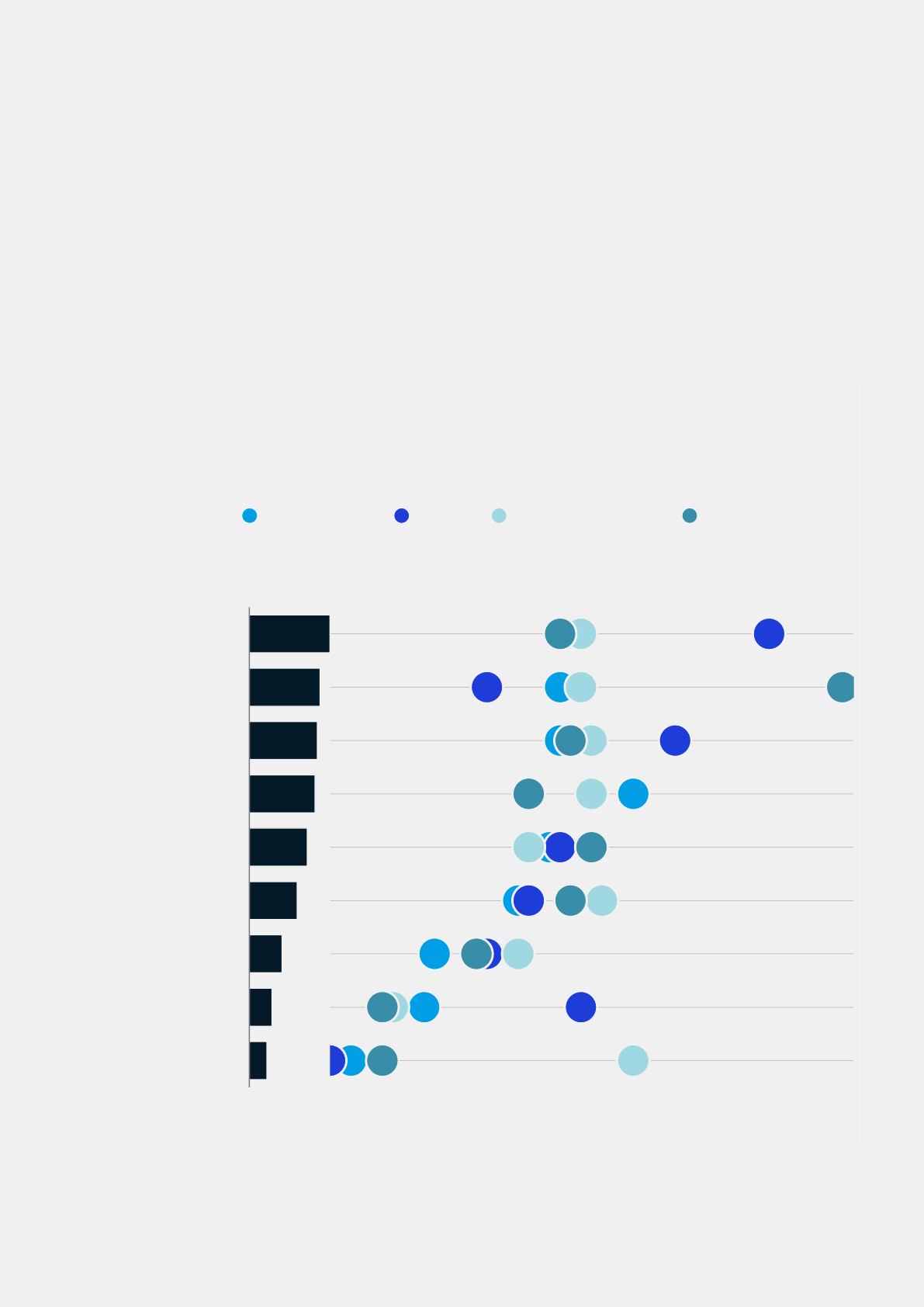

This analysis reveals four broad categories of shocks. Catastrophes are historically

remarkable events that cause trillions of dollars in losses. Some are foreseeable and

have relatively long lead times, while others are unanticipated. Shocks that offer at least

some degree of advance warning include financial crises, major military conflicts, and

pandemics such as the one gripping the world today. Another set of catastrophes includes

extreme weather, geophysical natural disasters, and major terrorist attacks. It may be

possible to anticipate the frequency and magnitude of these events by looking at larger

patterns and probabilities; hurricanes strike in the Gulf of Mexico every year, for example.

But the manifestation of a specific event can strike with little to no warning. This includes

some calamities that the world has avoided to date, such as a cyberattack on foundational

global systems.

Exhibit E1

Disruptions vary based on their severity, frequency, and lead time

—and they occur

with regularity.

Source: McKinsey Global Institute analysis

Meteoroid strike

Counterfeit

Financial crisis

Common

cyberattack

Extreme

pandemic

Acute climatological

event (hurricane)

2

Extreme terrorism

(eg, dirty bomb)

Acute climatological

event (heat wave)

2

Global

military

conflict

Regulation

Idiosyncratic

(eg, supplier

bankruptcy)

Localized

military

conflict

Major geo-

physical

event

Man-made

disaster

Pandemic

Solar storm

Supervolcano

Systemic cyberattack

Terrorism

Theft

Trade dispute

Foreseeable catastrophes

Magnitude of estimated cost of shock, $

Millions

10s of

billions

100s of

billions Trillions

10s of

trillions

Ability to anticipate (lead time)

None Days Weeks Months or more

Unanticipated

business disruptions

Unanticipated catastrophes

Foreseeable disruptions

Magnitude and ability to anticipate

Expected frequency of

a disruption, by duration, years

Based on expert interviews, n = 35

Duration

disruption

Expected

frequency

4.9

years

2.0

years

1–2

weeks

2.8

years

2–4

weeks

1–2

months

3.7

years

2+

months

More

frequent

Less

frequent

Has not (yet)

occurred at scale

1

Historical

frequency

REPEATS

ES and report

1.

Shocks that have not occurred either at scale (eg, extreme terrorism, systemic cyberattack, solar storm) or in modern times (eg, meteoroid strike,

supervolcano).

2.

Based on experience to date; frequency and/or severity of events could increase over time.

4 McKinsey Global Institute

Disruptions are serious and costly events, although on a smaller scale than catastrophes.

They, too, can be split into those that telegraph their arrival in advance (such as the recent

USChina trade disputes and the United Kingdom’s exit from the European Union)

and unanticipated events such as data breaches, product recalls, logistics disruptions,

and industrial accidents. Disruptions do not cause the same cumulative economic toll

as catastrophes.

Companies tend to focus much of their attention on managing the types of shocks they

encounter most often, which we classify as “unanticipated disruptions.” Most companies now

consider cybersecurity part of their overall risk management processes, for example. Some

other shocks such as trade disputes have made headlines in recent years and, as a result,

companies have started to factor them into their planning. But other types of shocks that

occur less frequently could inflict bigger losses and also need to be on companies’ radars.

The COVID pandemic is a reminder that outliers may be rare—but they are real possibilities

that companies need to consider in their decision making.

Shocks may emerge within or from outside the affected supply chain ecosystem. Disruptions

that are internal to the ecosystem, such as a supplier bankruptcy or unexpected plant shut-

down, are often preventable. By contrast, companies cannot hold off external disruptions

such as pandemics and natural disasters—but they can assume a posture focused on

minimizing their impact. Managing each of these shocks requires companies to analyze

their exposure and vulnerability and put different types of resilience measures in place.

For example, shocks that come with long lead times may require establishing early warning

systems. Those that are difficult to anticipate may require more backup capacity and

inventory that can be activated once a shock occurs.

All four types of shocks can disrupt operations and supply chains, often for prolonged

periods. We surveyed dozens of experts in four industries (automotive, pharmaceuticals,

aerospace, and computers and electronics) to understand how often they occur. Respondents

report that their industries have experienced material disruptions lasting a month or longer

every 3.7 years on average. Shorter disruptions have occurred even more frequently.

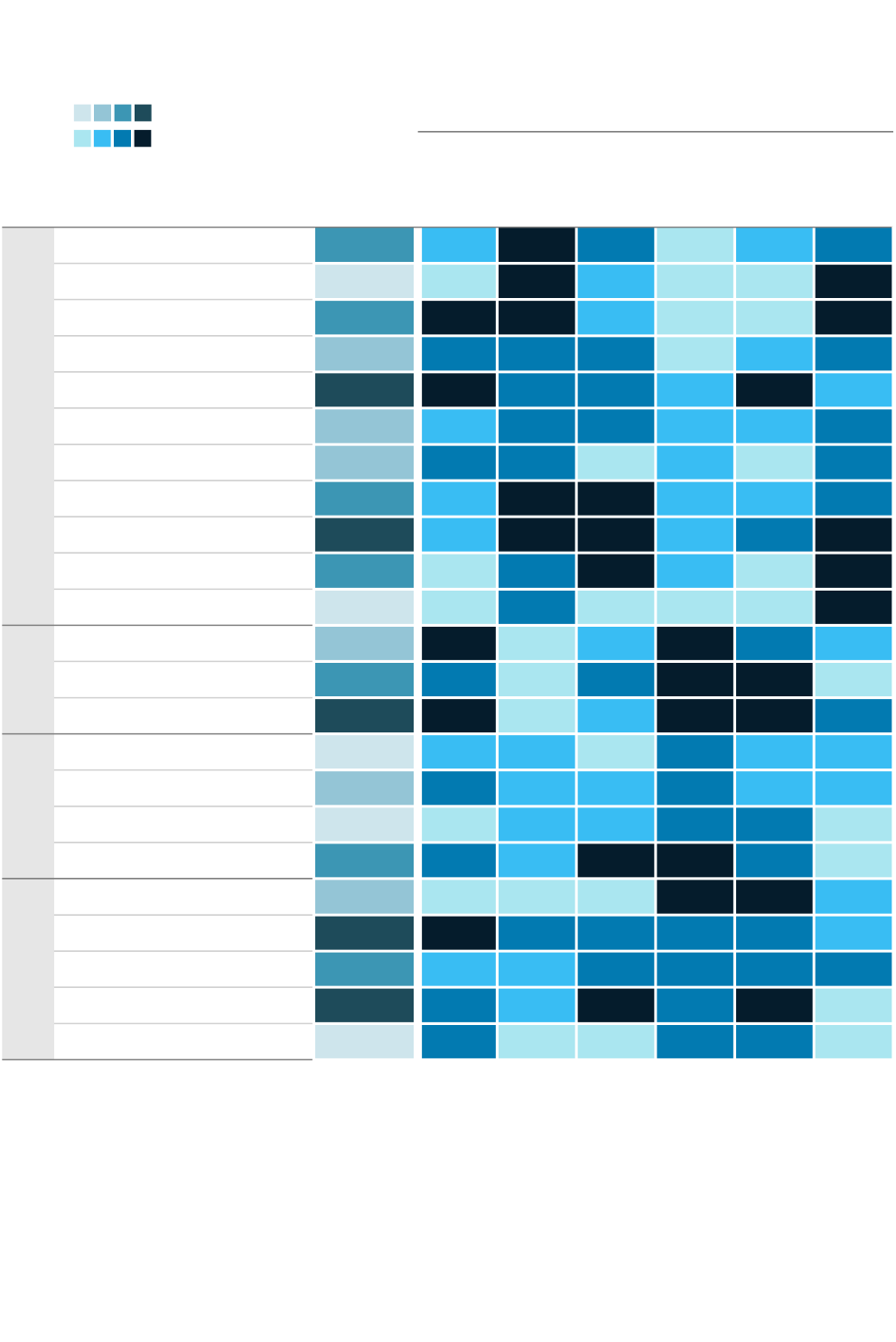

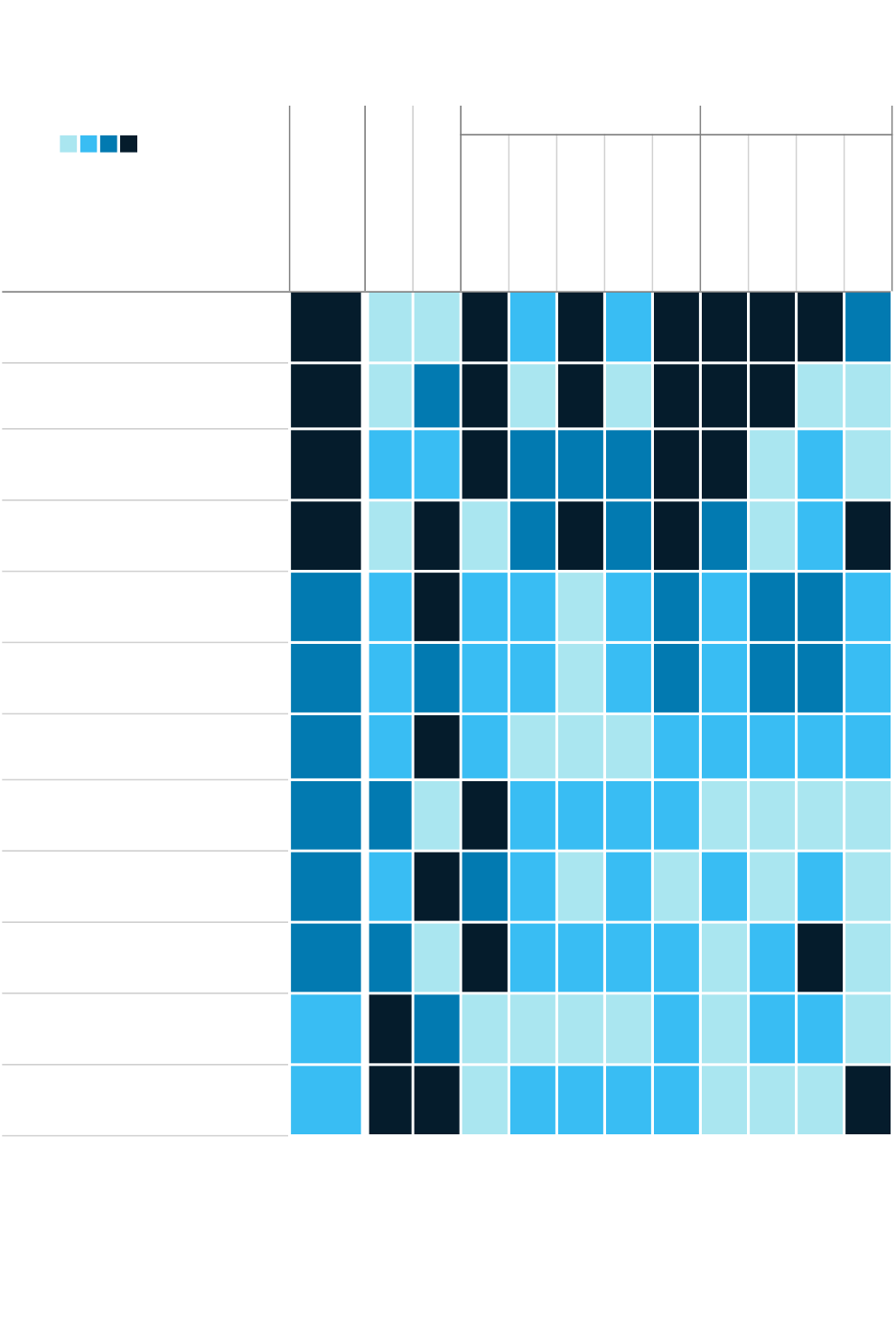

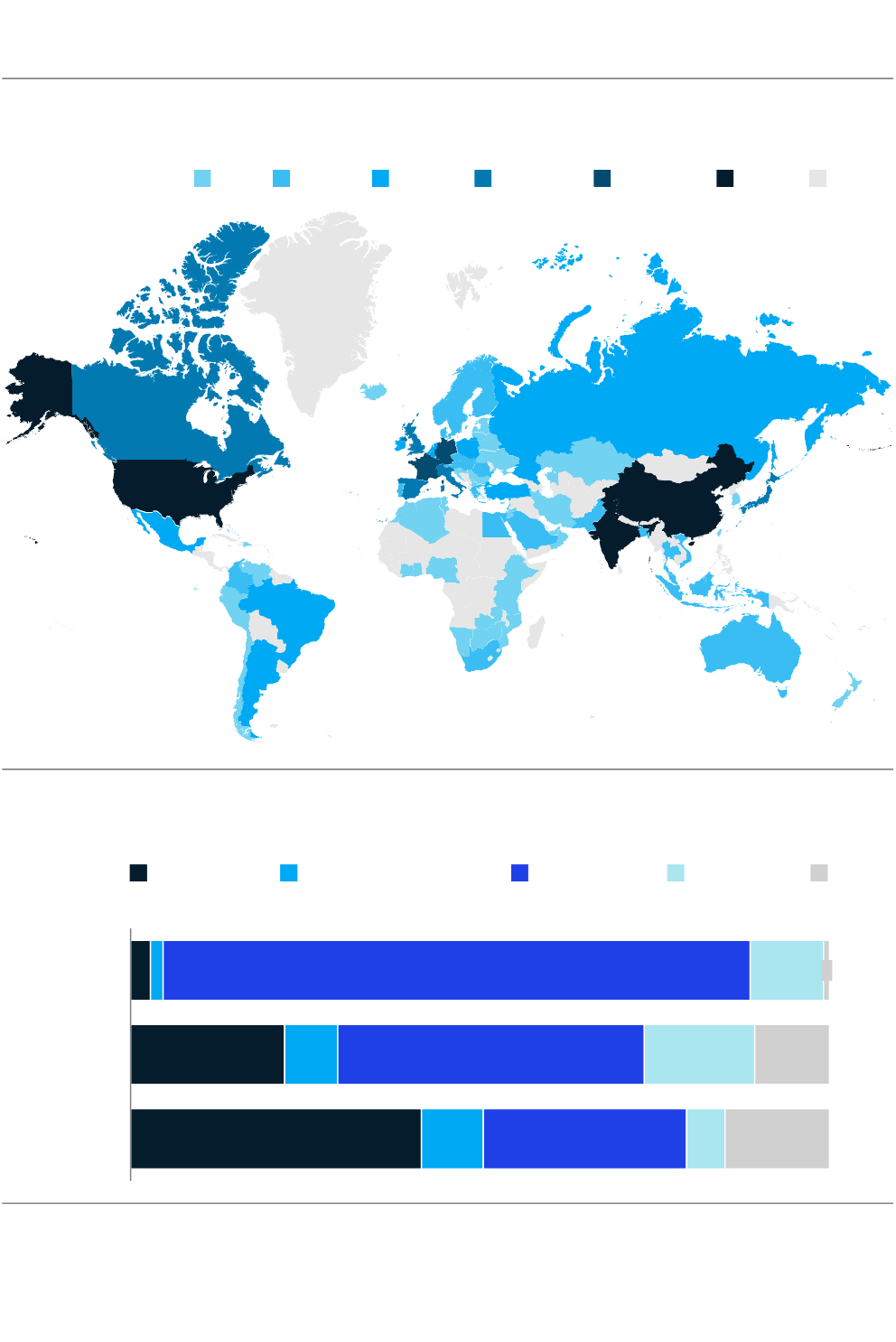

We analyzed 23 industry value chains to assess their exposure to specific types of

shocks. The resulting index (ExhibitE2) combines multiple factors, including how much of

the industry’s current geographic footprint is found in areas prone to each type of event,

the factors of production affected by those disruptions and their importance to that value

chain, and other measures that increase or reduce susceptibility. For example, heat waves

affect some regions more than others. Within them, labor-intensive value chains are at

comparatively higher risk—and within that group, those with the highest concentration of

workers in outdoor or non-climate-controlled settings are most exposed to disruption.

4

4

This is an assessment of value chain exposure to shocks; it does not consider vulnerability, or an industry’s degree of

resilience against the shocks to which it is exposed. For instance, while semiconductor production is common in places

that are earthquake prone, engineering standards may mean that factories are built to withstand them.

Shocks lasting a month

or more occur every

3.7

years

5Risk, resilience, and rebalancing in global value chains

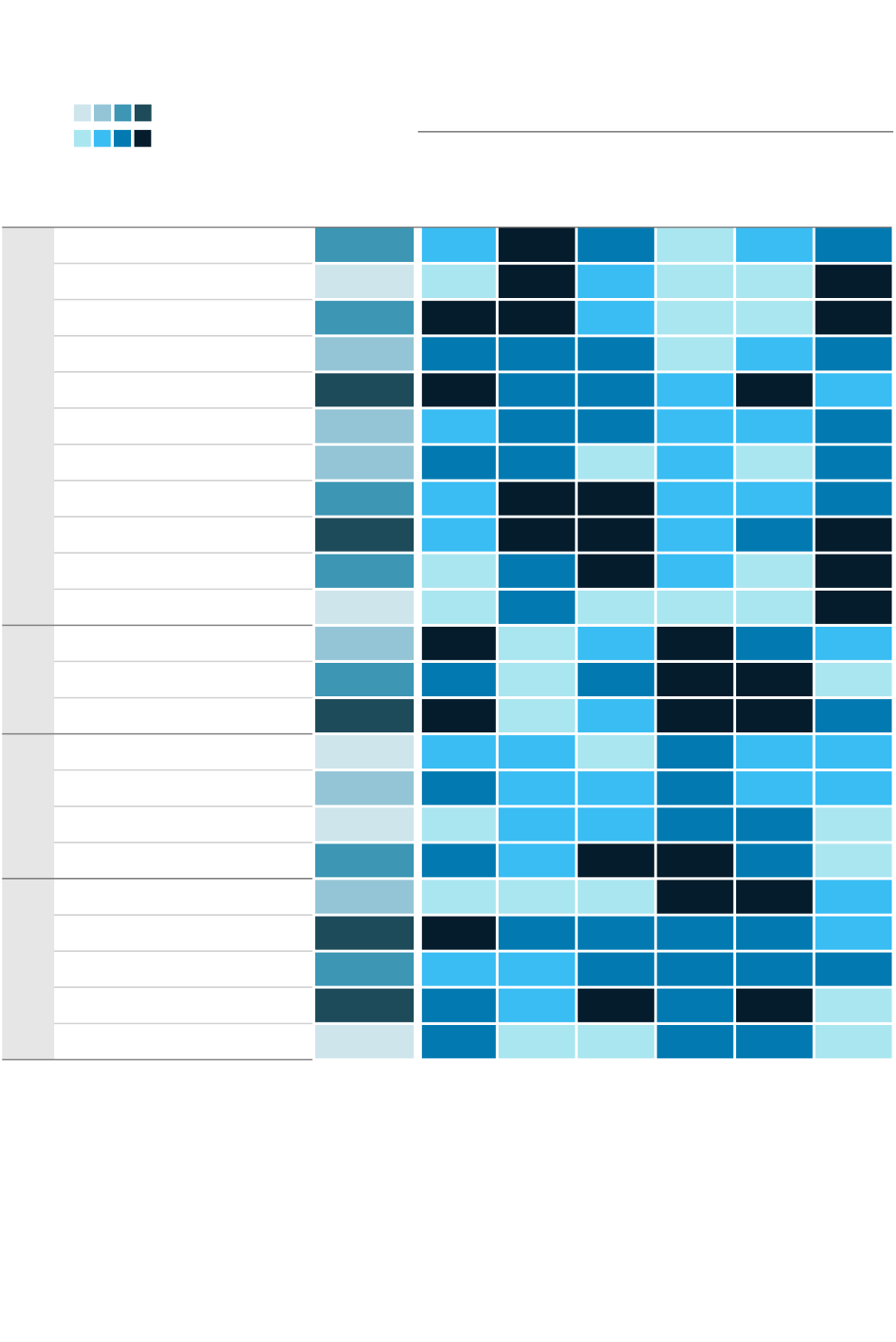

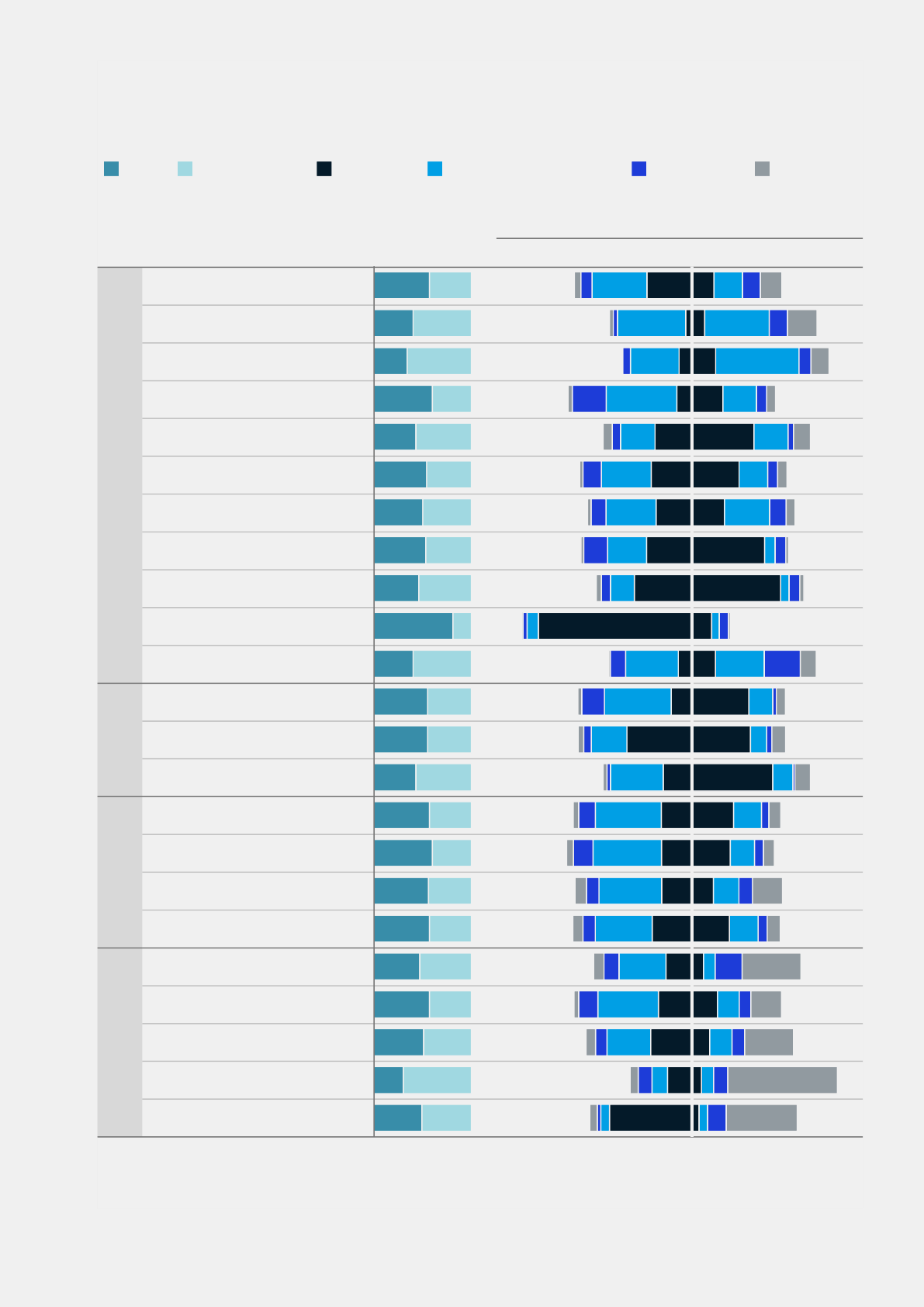

Exhibit E2

Rank of exposure (1 = most exposed)

Value chain

Overall

shock

exposure

Pan-

demic

1

Large-

scale

cyber-

attack

2

Geo-

physical

event

3

Heat

stress

4

Flood-

ing

5

Trade

dispute

6

Global

innovations

Chemical 11 16 4 6 19 16 8

Pharmaceutical 19 23 2 17 23 19 4

Aerospace 8 2 1 18 20 21 5

Automotive 14 6 9 12 21 18 6

Transportation equipment 4 5 12 7 13 5 15

Electrical equipment 16 17 11 9 15 15 10

Machinery and equipment 18 9 10 20 17 20 7

Computers and electronics 6 15 5 4 14 14 9

Communication equipment 1 13 3 2 16 7 2

Semiconductors and components 9 19 6 1 18 23 1

Medical devices 23 22 8 22 22 22 3

Labor-

intensive

Furniture 13 3 21 14 4 12 17

Textile 7 7 22 11 3 2 21

Apparel 2 1 20 15 2 1 11

Regional

processing

Fabricated metal products 21 14 18 19 6 17 15

Rubber and plastic 15 8 17 16 8 13 13

Food and beverage 19 21 14 13 12 6 22

Glass, cement, and ceramics 10 11 16 5 5 11 20

Resource-

intensive

Agriculture 17 20 19 23 1 4 14

Petroleum products 3 4 7 10 7 10 18

Basic metal 12 18 13 8 11 8 12

Mining 5 10 15 3 10 3 19

Wooden products 22 12 23 21 9 9 23

Each value chain’s exposure to shocks is based on its geographic footprint and

factors of production.

Less

exposed

More

exposed

Source:

McKinsey Global Institute analysis

1.

Based on geographic footprint in areas with high incidence of epidemics and high people inflows. Also considers labor intensity and demand

impact. Sources: INFORM; UN Comtrade; UN World Tourism Organization; US BEA; World Input-Output Database (WIOD).

2. Based on knowledge intensity, capital intensity, degree of digitization, and presence in geographies with high cross

-border data flows.

Sources: MGI Digitization Index; MGI LaborCube; Telegeography; US BLS.

3. Based on capital intensity and footprint in geographies prone to natural disasters. Sources

: INFORM; UN Comtrade; WIOD.

4. Based on footprint in geographies prone to heat and humidity, labor intensity, and relative share of outdoor work. Sources

: MGI Workability Index;

O*Net; UN Comtrade; US BLS.

5. Based on footprint in geographies vulnerable to flooding. Sources

: UN Comtrade; World Resources Institute.

6. Based on trade intensity (exports as a share of gross output) and product complexity, a proxy for substitutability and nat

ional security relevance.

Sources: Observatory of Economic Complexity; UN Comtrade.

Note: Overall exposure averages the six assessed shocks, unweighted by relative severity. Chart considers exposure but not mi

tigation actions.

Demand effects included only for pandemics.

6 McKinsey Global Institute

Read horizontally, the chart shows each value chain’s level of exposure to different types of

shocks, which can vary sharply. Aerospace and semiconductors, for example, are susceptible

to cyberattacks and trade disputes because of their high level of digitization, R&D, capital

intensity, and exposure to digital data flows. However, both value chains have relatively low

exposure to the climate-related events we have assessed here (heat stress and flooding)

because of the footprint of their production. By contrast, agriculture, textiles, apparel, and,

to a lesser extent, food and beverage, are labor-intensive. As a result, these value chains

are highly exposed to heat stress. Much of their activity also takes place in regions that face

disruption due to flooding.

Read vertically, the index shows which value chains are likely to be touched by specific types

of shocks. Pandemics, for example, have a major impact on labor-intensive value chains. In

addition, this is the one type of shock for which we assess the effects on demand as well as

supply. As we are seeing in the current crisis, demand has plummeted for nonessential goods

and travel, hitting companies in apparel, petroleum products, and aerospace. By contrast,

while production has been affected in value chains like agriculture and food and beverage,

they have continued to see strong demand because of the essential nature of their products.

In general, heat stress is more likely to strike labor-intensive value chains (and some resource-

intensive value chains) because of their relatively high reliance on manual labor or outdoor

work. Perhaps surprisingly, these same value chains are relatively less susceptible to trade

disputes, which are increasingly focused on value chains with a high degree of knowledge

intensity and high-value industries. Cyberattacks are more likely to affect value chains with

a high degree of digitization, such as communication equipment.

Overall, value chains that are heavily traded relative to their output are more exposed than

those with lower trade intensity. Some of these include value chains that are the most

sought after by countries: communication equipment, computers and electronics, and

semiconductors and components. These value chains have the further distinction of being

high value and relatively concentrated, underscoring potential risks for the global economy.

Heavily traded labor-intensive value chains, such as apparel, are highly exposed to pandemic

risk, heat stress (because of their reliance on labor), and flood risk. In contrast, the value

chains including glass and cement, food and beverage, rubber and plastics, and fabricated

metals have much lower exposure to shocks; these are among the least traded and most

regionally oriented value chains.

All in all, the five value chains most exposed to our assessed set of six shocks collectively

represent $4.4 trillion in annual exports, or roughly a quarter of global goods trade (led by

petroleum products, ranked third overall, with $2.4 trillion in exports). The five least exposed

value chains account for $2.6 trillion in exports. Of the five most exposed value chains,

apparel accounts for the largest share of employment, with at least 25 million jobs globally,

according to the International Labor Organization.

5

Even value chains with limited exposure to all types of shocks we assessed are not immune to

them. Despite recent headlines, we find that pharmaceuticals are relatively less exposed than

most other industries. But the industry has been disrupted by a hurricane that struck Puerto

Rico, and cyberattacks are a growing concern. In the future, the industry may be subject

to greater trade tensions as well as regulatory and policy shifts if governments take action

with the intent of safeguarding public health. Similarly, the food and beverage industry and

agriculture have relatively low exposure overall, as they are globally dispersed. Yet these value

chains are subject to climate-related stresses that are likely to grow over time. In addition to

disrupting the lives and livelihoods of millions, this could cause the industries to become more

dependent on trade or force them to undertake expensive adaptations.

6

5

International Labor Organization, “Employment by sex and economic activity—ILO modelled estimates,” ILOSTAT,

accessed June 20, 2020.

6

Will the world’s breadbaskets become less reliable?: Case study, McKinsey Global Institute, May 2020.

$4.4

trillion

in global trade flows through the

five most exposed value chains

7

Risk, resilience, and rebalancing in global value chains

In addition to observing variations in exposure across industry value chains, it is important to

note that risk exposure varies for individual companies within those value chains. Similarly,

each company has unique vulnerabilities, as we discuss below. Some have developed far more

sophisticated and effective supply chain management capabilities and preparedness plans

than others.

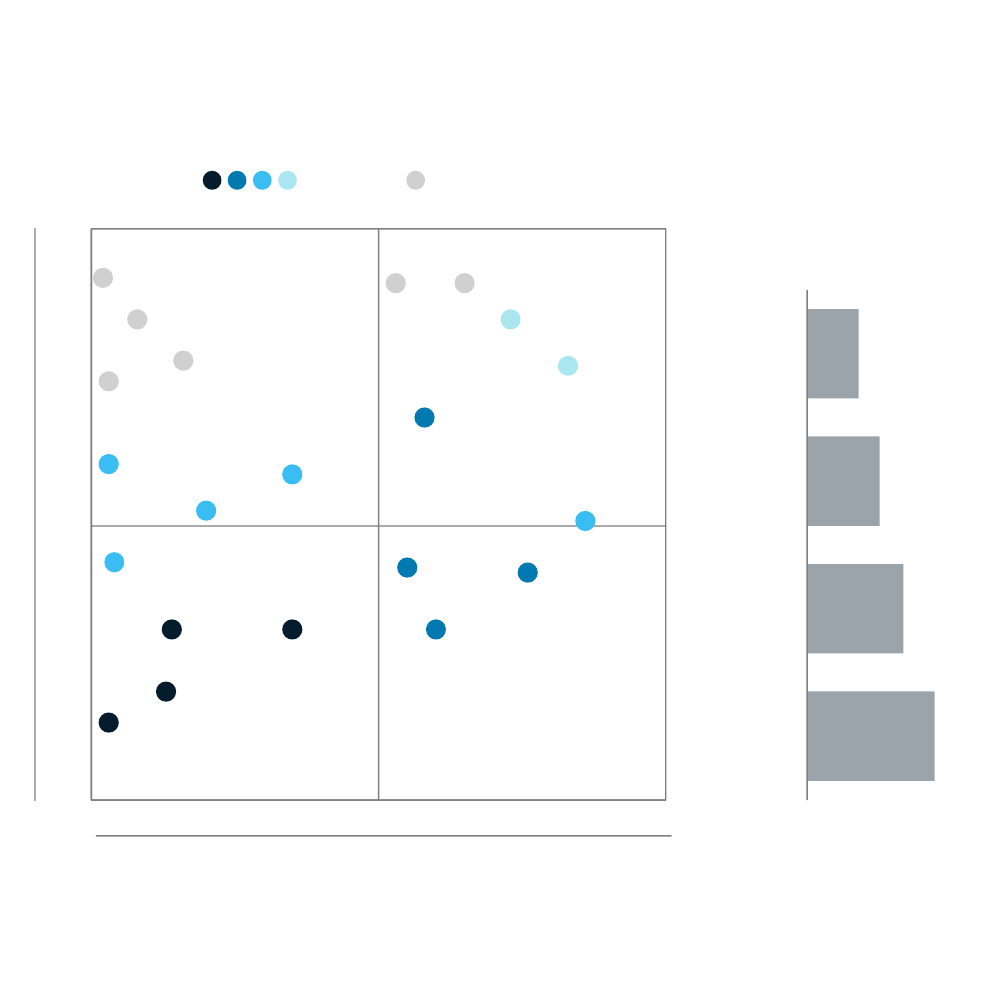

Shocks exploit vulnerabilities within companies and value chains

Shocks inevitably seem to exploit the weak spots within broader value chains and specific

companies. An organization’s supply chain operations can be a source of vulnerability

or resilience, depending on its effectiveness in monitoring risk, implementing mitigation

strategies, and establishing business continuity plans. We explore several key areas of

vulnerability, including demand planning, supplier networks, transportation and logistics,

financial health, product complexity, and organizational effectiveness.

7

Some of these vulnerabilities are inherent to a given industry; the perishability of food and

agricultural products, for example, means that the associated value chains are vulnerable to

delivery delays and spoilage. Industries with unpredictable, seasonal, and cyclical demand

also face particular challenges. Makers of electronics must adapt to relatively short product

life cycles, and they cannot afford to miss spikes in consumer spending during limited

holiday windows.

Other vulnerabilities are the consequence of intentional decisions, such as how much

inventory a company chooses to carry, the complexity of its product portfolio, the number of

unique SKUs in its supply chain, and the amount of debt or insurance it carries.

8

Changing

these decisions can reduce—or increase—vulnerability to shocks.

Weaknesses often stem from the structure of supplier networks in a given value chain.

Complexity itself is not necessarily a weakness to the extent that it provides companies with

redundancies and flexibility. But sometimes the balance can tip. Complex networks may

become opaque, obscuring vulnerabilities and interdependencies. A large multinational

company can have hundreds of tier-one suppliers from which it directly purchases

components. Each of those tier-one suppliers in turn can rely on hundreds of tier-two

suppliers. The entire supplier ecosystem associated with a large company can encompass

tens of thousands of companies around the world when the deepest tiers are included.

9

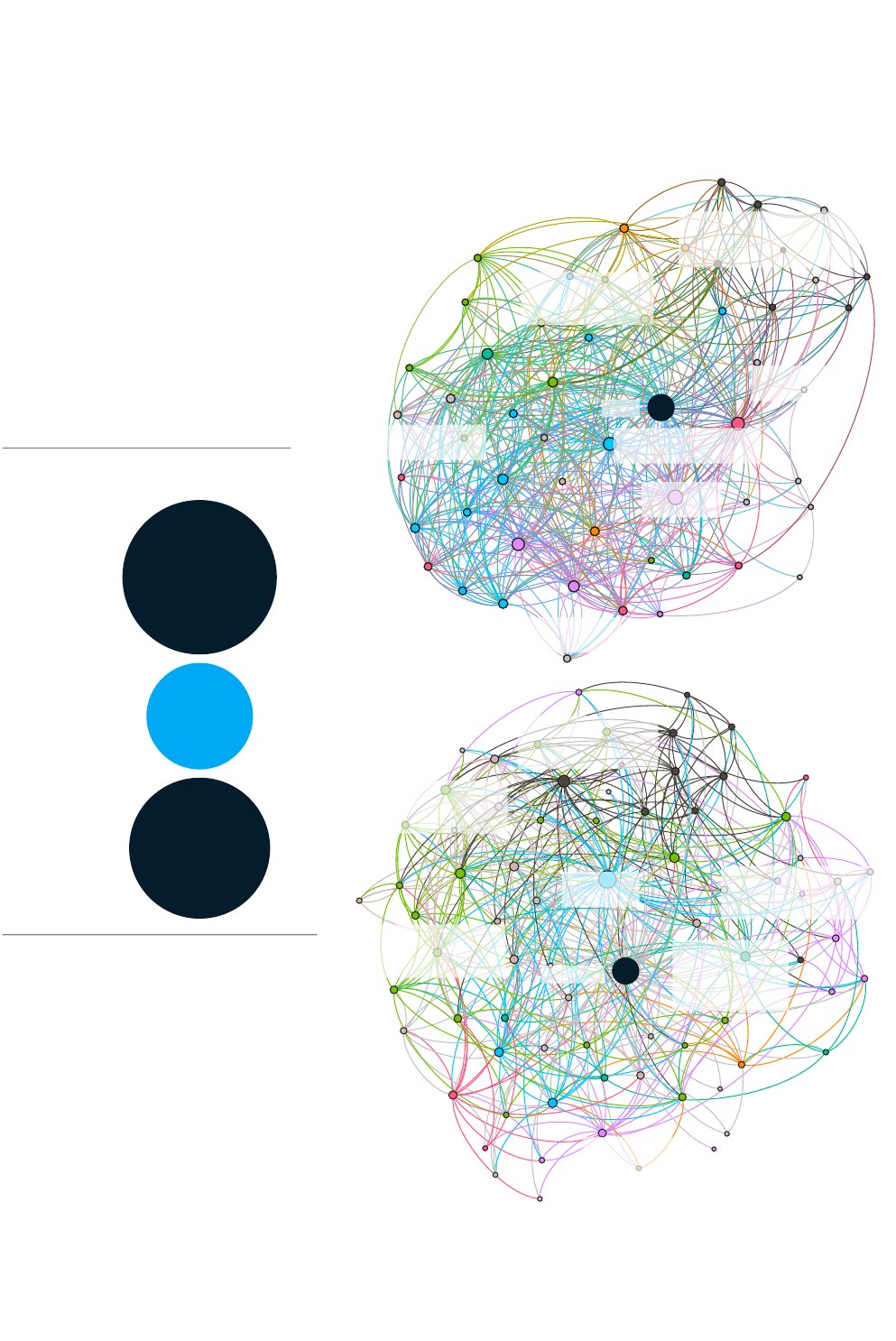

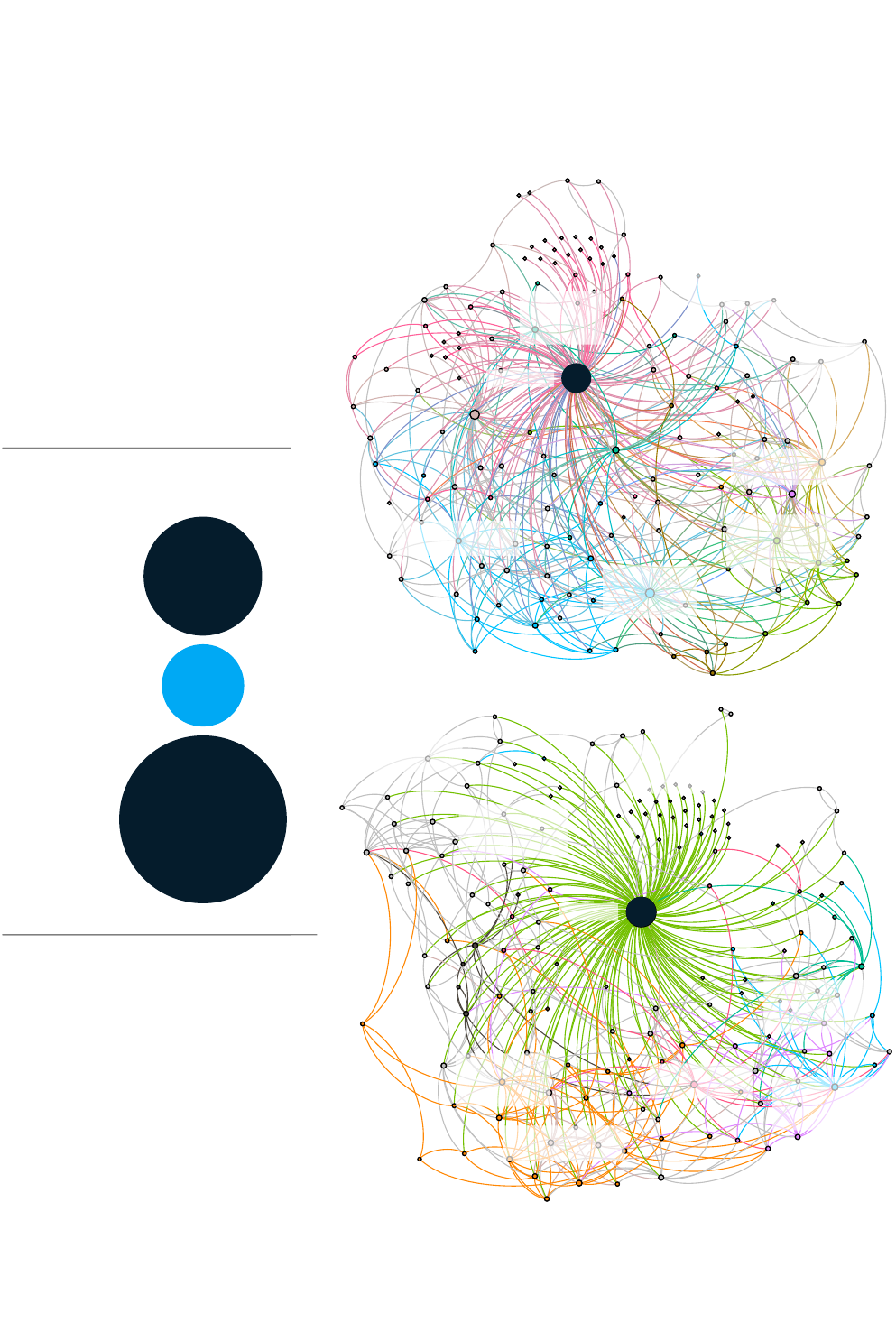

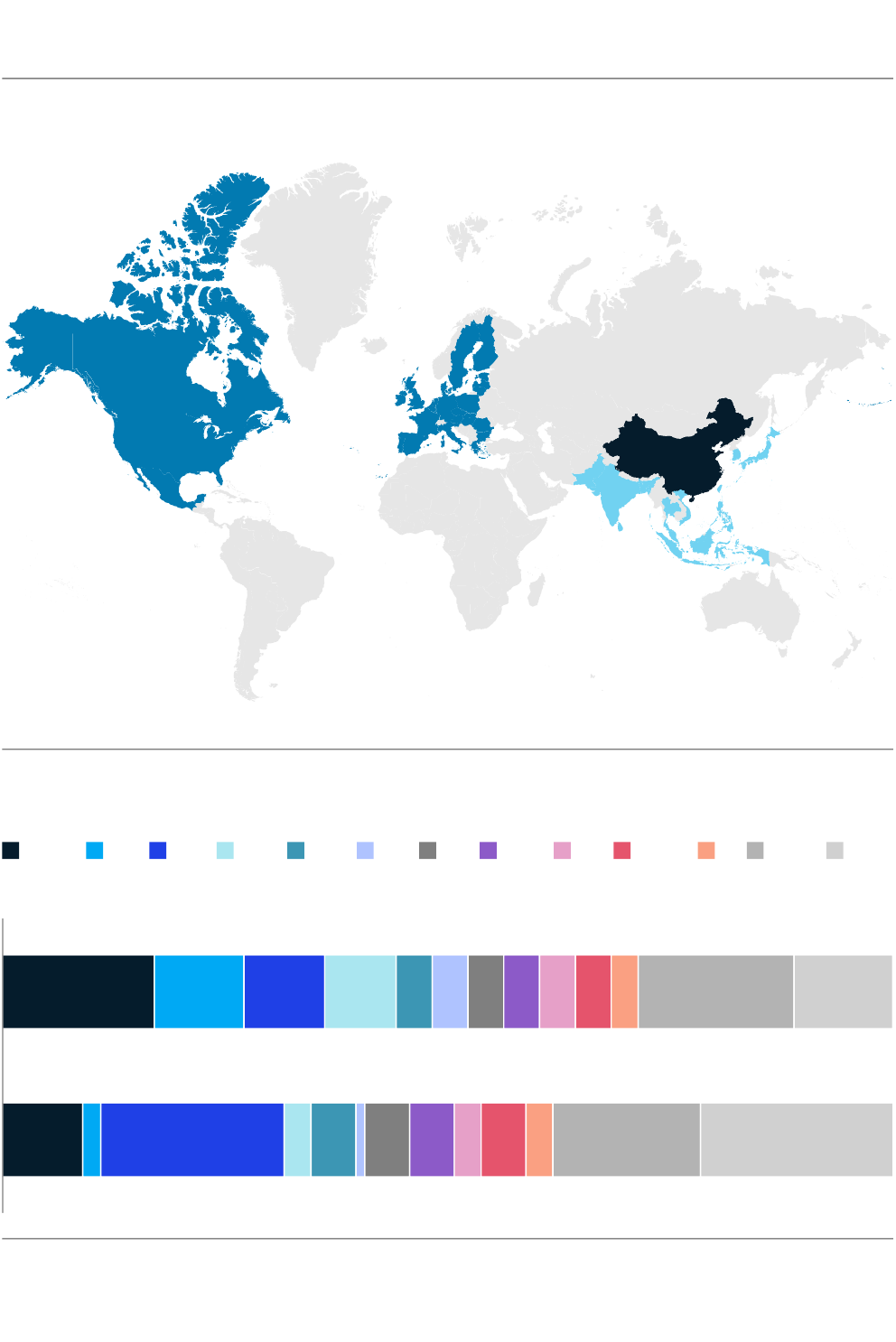

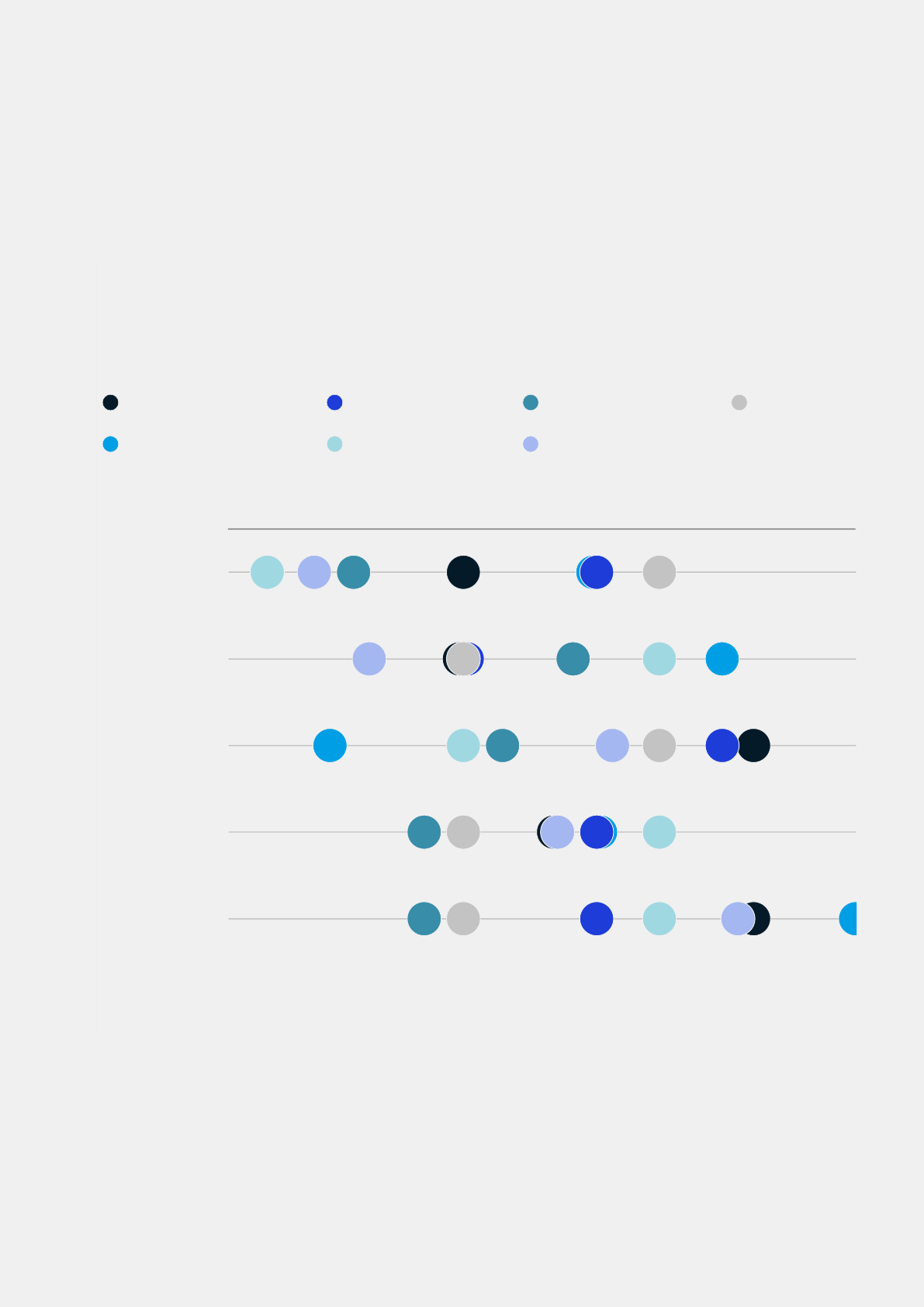

ExhibitE3 applies network analytics to illustrate the complexity of the first- and second-

tier supply ecosystems for two Fortune 500 companies in the computer and electronics

industry. This is based on publicly available data and may therefore not be exhaustive.

10

These

multitiered, multinational networks span thousands of companies and extend to deeper tiers

that are not shown here. This illustration also underscores the fact that, even within the same

industry, companies may make materially different decisions about how to structure their

supply ecosystems, with implications for risk.

7

Knut Alicke, Ed Barriball, Susan Lund, and Daniel Swan, “Is your supply chain risk blind—or risk resilient?,” McKinsey.com,

2020.

8

SKUs are stock-keeping units, indicating a distinct type of product for sale.

9

We refer to supply chains when specifically discussing the tiers of vendors that provide inputs and services to create

products for a downstream company. We refer to industry value chains when discussing the broader end-to-end journey

from producers of raw inputs to distribution channels and, eventually, customers. The latter view is important because

companies increasingly consider proximity to customers when deciding where to base production; furthermore, customer

product usage data can form the basis of design improvements and after-sales services.

10

Data from the Bloomberg Supply Chain database, based on regulatory filings and other public disclosures. The database

does not capture all supplier relationships, but the results provide a relative overview of connectivity and network

structure compared to other companies with similar data availability.

8

McKinsey Global Institute

Exhibit E3

Even within the same industry, companies can have very different supply chain structures—

and significant overlap.

Source: Bloomberg Supply Chain database; McKinsey Global Institute analysis

1. Clustering is based on the clustering coefficient, which is calculated with network analysis of all supplier-customer relationships. The clustering

coefficient measures the degree to which nodes cluster together and form interconnected subgroups.

2. The level of network depth is measured through the network diameter, using network analysis of all supplier-customer relationships. The network

diameter is a measurement of network size that accounts for the overall structure by measuring the longest shortest path in the network.

Companies rely on complex, multitiered. and interconnected networks

Example: Semiconductors, computers and electronics, and communication equipment

Dell

Revenue, 2019 = $90 billion

Dell’s supplier ecosystem is more

clustered, meaning it is potentially more

exposed to bottlenecks

1

Lenovo

Revenue, 2019 = $51 billion

Lenovo’s supplier ecosystem is deeper,

meaning it has potentially less visibility

2

Known tier 1 and 2 suppliers

Dell only

Shared

Lenovo only

4,761

2,272

3,968

Suppliers of displays,

advanced optics, and

other glass components

Electronics

manufacturing

service providers

Chemical

manufacturers

Original equipment

manufacturers

Semiconductor

manufacturers

Software

companies

Maritime trans-

port suppliers

DELL

Electronics

manufacturing

service companies

Semiconductors

and electronic

components

Software

providers

Suppliers of other

electronic

components

Mobile and

communication

devices and

components

Chemical

and plastics

manufacturers

Suppliers of displays,

advanced optics, and

other glass components

LENOVO

9Risk, resilience, and rebalancing in global value chains

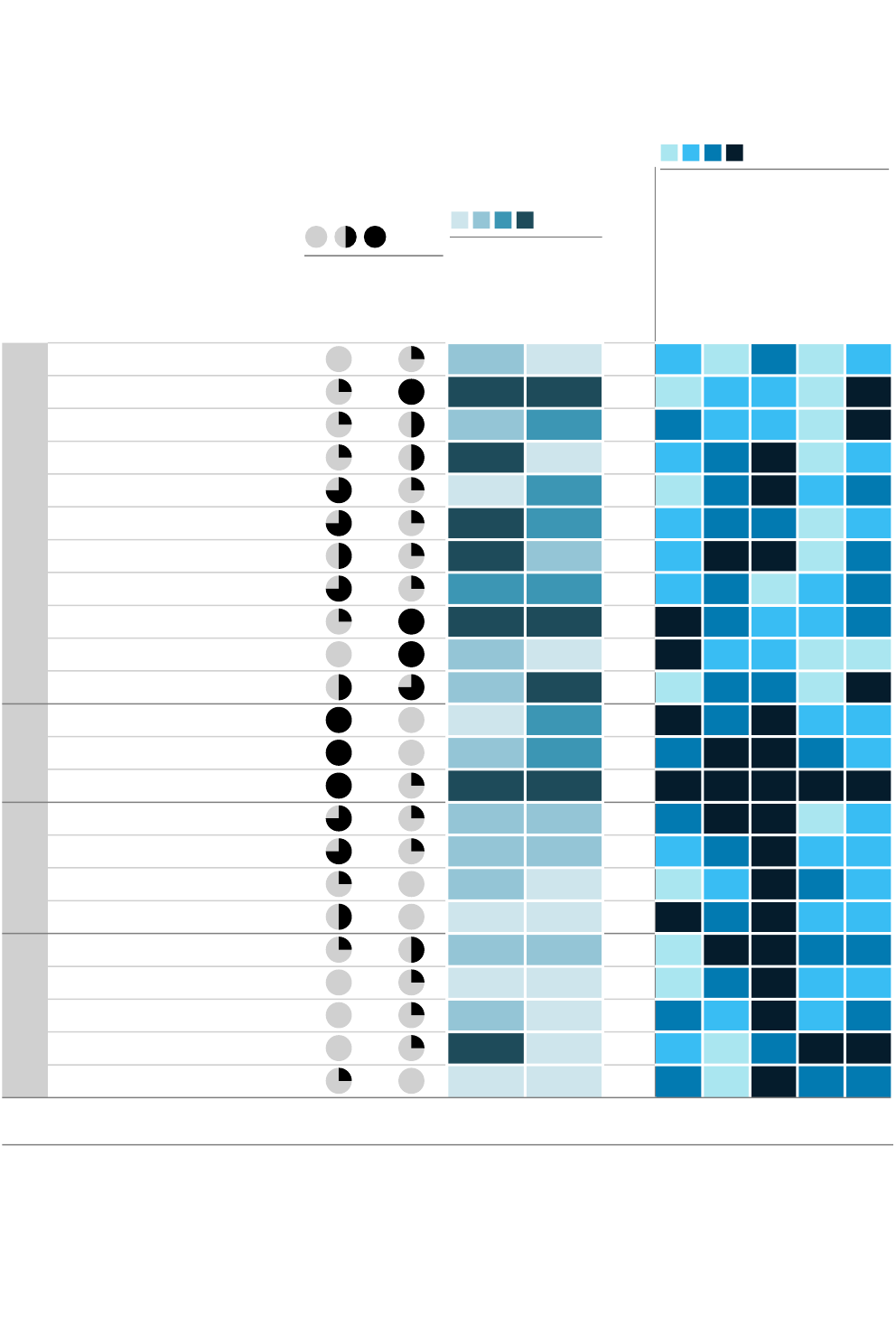

Companies’ supplier networks vary in ways that can shape their vulnerability. Spending

concentrated among just a few suppliers may make it easier to manage them, but it also

heightens vulnerability should anything happen to them. Suppliers frequently supply each

other; one form of structural vulnerability is a subtier supplier that accounts for relatively little

in spending but is collectively important to all participants. The number of tiers of participating

suppliers can hinder visibility and make it difficult to spot emergent risks. Suppliers that are

dependent on a single customer can cause issues when demand shocks cascade through

a value chain. The absence of substitute suppliers is another structural vulnerability.

In some cases, suppliers may be concentrated in a single geography due to that country’s

specialization and economies of scale. A natural disaster or localized conflict in that part

of the world can cause critical shortages that snarl the entire network. Some industries,

such as mobile phones and communication equipment, have become more concentrated in

recent years, while others, including medical devices and aerospace, have become less so

(ExhibitE4). The aerospace value chain, for example, has diversified in part due to secure

market access.

Exhibit E4

Globalization has led to diversification of production across countries in some sectors,

but others have grown more concentrated.

Change in geographic concentration by sector, 2000–18, measured by change in Herfindahl-Hirschman Index of exports

(HHI)

1

Source: UN Comtrade; McKinsey Global Institute analysis

1. A measure of concentration that is the sum of the square of each country’s share of exports.

Note: Data includes 5,444 unique final and intermediate products from 2018 trade data. The weighted average is weighted by the share of trade for

each product within each value chain. All other measurements of HHI are calculated using the raw, unweighted score.

Total export value, 2018, $

Resource-intensiveGlobal innovations Regional processingLabor-intensive

% change in HHI

1

120

100

40

180

20

0

-

20

60

80

220

-40

200

140

160

Aerospace

Passenger

vehicles

Industrial

machinery

Petroleum

products

Pharmaceuticals

Heavy

vehicles

Chemicals

Food and

beverage

Basic

metals

Semiconductors

Agriculture

Electrical

equipment

Fabricated metal products

Mining

Appliances

Apparel

Textiles

Furniture

Computers and peripherals

Mobile and communication equipment

REPEATS

ES and report

10 McKinsey Global Institute

Even in value chains that are generally more geographically diversified, production of certain

key products may be disproportionately concentrated. Many low-value or basic ingredients

in pharmaceuticals are predominantly produced in China and India, for instance. In total,

we find 180 products across value chains for which one country accounts for 70 percent

or more of exports, creating the potential for bottlenecks. The chemicals value chain has

a particularly large number of such highly concentrated products, but examples exist in

multiple industries. Other products may be produced across diverse geographies but have

severe capacity constraints, which creates bottlenecks in the event of production stoppages.

Similarly, some products may have many exporting countries, but trade takes place within

clusters of countries rather than on a global basis. In those instances, importers may struggle

to find alternatives when their predominant supplier experiences a disruption. Geographic

diversification is not inherently positive, particularly if production and sourcing expands into

areas that are more exposed to shocks.

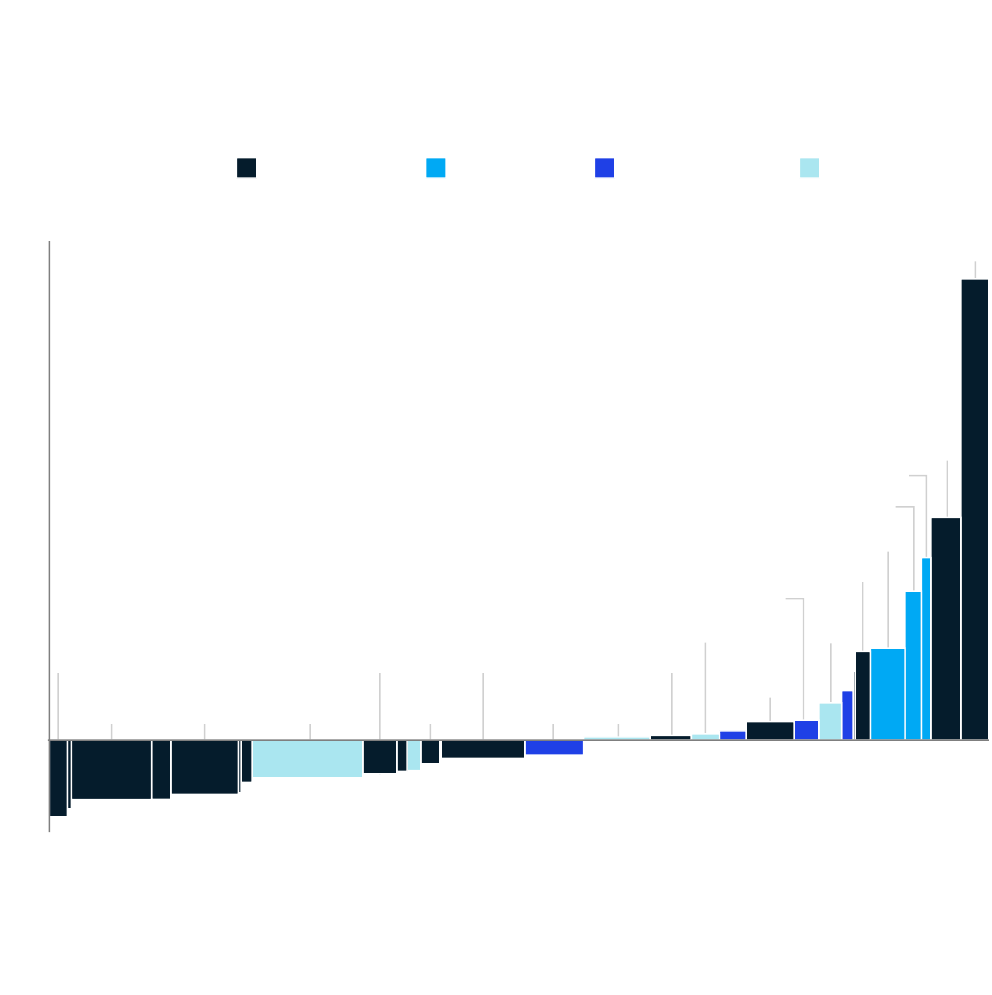

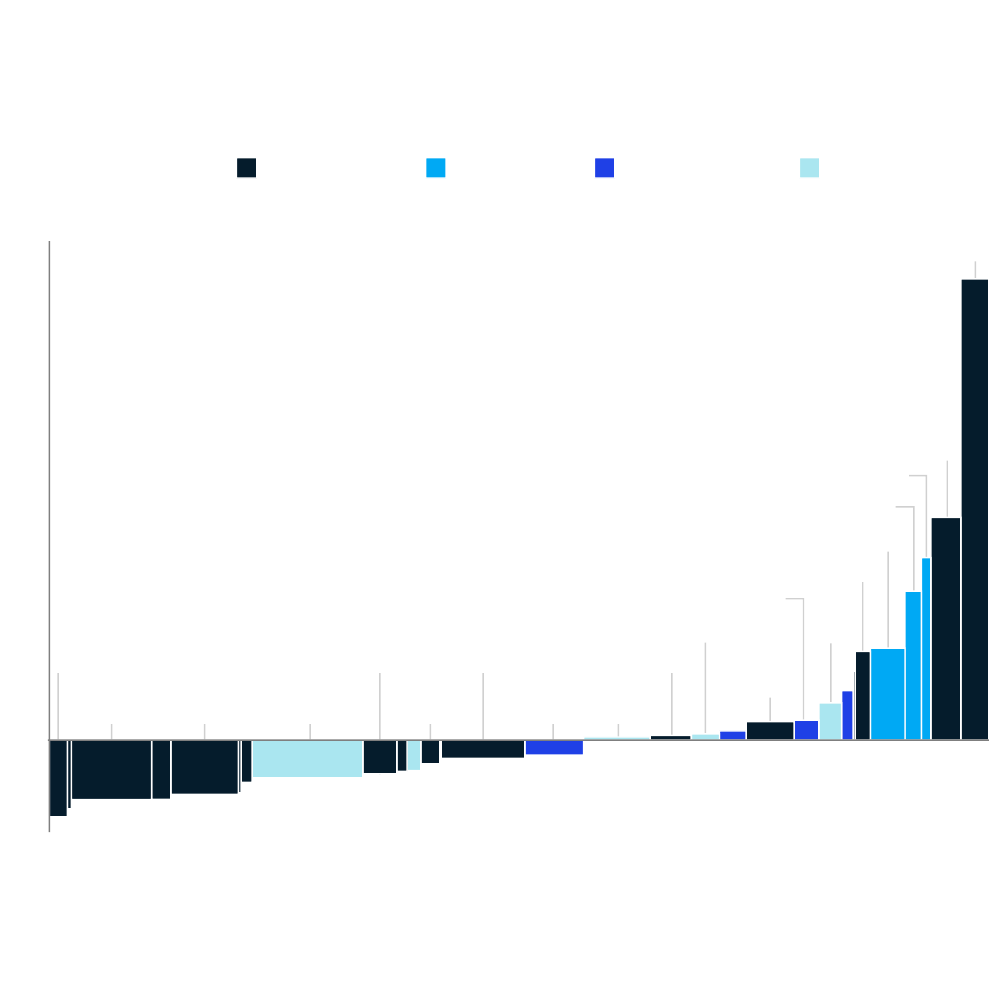

Over the course of a decade, companies can expect disruptions to

erase half a year’s worth of profits or more

When companies understand the magnitude of the losses they could face from supply chain

disruptions, they can weigh how much to invest in mitigation. We built representative income

statements and balance sheets for hypothetical companies in 13 different industries, using

actual data from the 25 largest public companies in each. This enables us to see how they fare

financially when under duress.

We explore two scenarios involving severe and prolonged shocks:

— Scenario 1. A complete manufacturing shutdown lasting 100 days that affects raw

material delivery and key inputs but not distribution channels and logistics. In this

scenario, companies can still deliver goods to market. But once their safety stock is

depleted, their revenue is hit.

— Scenario 2. The same as above, but in this case, distribution channels are also affected,

meaning that companies cannot sell their products even if they have inventory available.

Our choice to model a 100-day disruption is based on an extensive review of historical events.

In 2018 alone, the five most disruptive supply chain events affected more than 2,000 sites

worldwide, and factories took 22 to 29 weeks to recover.

11

Our scenarios show that a single prolonged production-only shock would wipe out between

30 and 50 percent of one year’s EBITDA for companies in most industries. An event that

disrupts distribution channels as well would push the losses sharply higher for some.

Industries in which companies typically hold larger inventories and have lower fixed costs

tend to experience relatively smaller financial losses from shocks. If a natural disaster hits

a supplier but distribution channels remain open, inventory levels become a key buffer.

However, the downstream company will still face a cash drain after the fact when it is time to

replenish its drawn-down safety stock. When a disruption outlasts the available safety stock,

lower fixed costs become important to withstanding a decline in EBITDA.

11

Shahzaib Khan and Andrew Perez, Eventwatch 2018 annual report, Resilinc, 2019.

180

products are predominantly

exported from a single country,

opening the door to bottlenecks

11

Risk, resilience, and rebalancing in global value chains

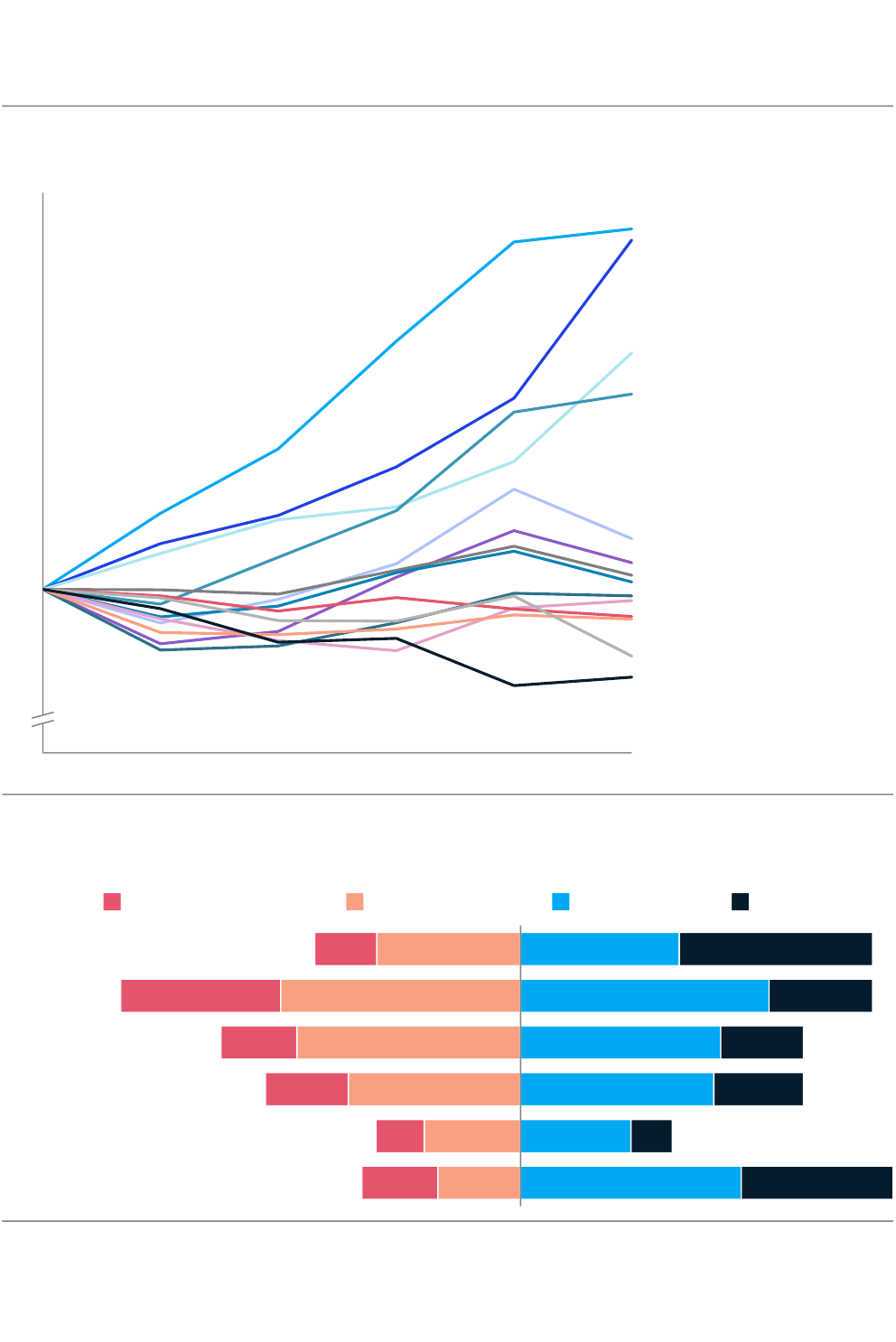

Having calculated the damage associated with one particularly severe and prolonged

disruption, we then estimated the bottom-line impact that companies can expect over

the course of a decade, based on probabilities. We combined the expected frequency of value

chain disruptions of different lengths with the financial impact experienced by companies in

different industries. On average, companies can expect losses equal to almost 45 percent of

one year’s profits over the course of a decade (ExhibitE5). This is equal to seven percentage

points of decline on average. We make no assessment of the extent to which the cost of these

disruptions has already been priced into valuations.

These are not distant future risks; they are current, ongoing patterns. On top of those losses,

there is an additional risk of permanently losing market share to competitors that are able to

sustain operations or recover faster, not to mention the cost of rebuilding damaged physical

assets. However, these expected losses should be weighed in the context of the additional

profits that companies are able to achieve with highly efficient and far-reaching supply chains.

Companies can expect to lose almost

45%

of one year’s profits over

the course of a decade

Exhibit E5

Net present value (NPV) of expected losses

over 10 years,

1

% of annual EBITDA

NPV for a major

company,

2

$ million

NPV of expected

losses,

2

EBITDA margin, pp

Aerospace (commercial) 1,564 7.4

Automotive 6,412 7.3

Mining 2,240 8.4

Petroleum products 6,327 8.9

Electrical equipment 556 5.4

Glass and cement 805 6.2

Machinery and equipment 1,084 6.5

Computers and electronics 2,914 5.9

Textiles and apparel 788 7.8

Medical devices 431 8.7

Chemicals 1,018 5.7

Food and beverage 1,578 7.6

Pharmaceuticals 1,436 6.0

Expected losses from supply chain disruptions equal 42 percent of one year’s EBITDA

on average over the course of a decade.

Source: S&P Capital IQ; McKinsey Global Institute analysis

66.8

56.1

46.7

45.5

41.7

40.5

39.9

39.0

38.9

37.9

34.9

30.0

24.0

SIMILAR

ES and report

1.

Based on estimated probability of a severe disruption twice per decade (constant across industries) and proportion of revenue at risk due to a

shock (varies across industries). Amount is expressed as a share of one year’s revenue (ie, it is not recurring over modeled 10-year period).

Calculated by aggregating cash value of expected shocks over a 10-year period based on averages of production-only and production and

distribution disruption scenarios multiplied by probability of event occurring for a given year. Expected cash impact is discounted based on each

industry’s weighted average cost of capital.

2.

Based on weighted average revenue of top 25 companies by market cap in each industry.

Average

Above

average

12 McKinsey Global Institute

Will global value chains shift across countries?

Today much of the discussion about resilience in advanced economies revolves around

the idea of increasing domestic production. But the interconnected nature of value chains

limits the economic case for making large-scale changes in their physical location. Value

chains often span thousands of interconnected companies, and their configurations reflect

specialization, access to consumer markets around the world, long-standing relationships,

and economies of scale.

We set out to estimate what share of global exports could move to different countries based

on the business case and how much might move due to policy interventions. To determine

whether industry economics alone support a future geographic shift, we considered a number

of factors. One is whether there is already some movement under way. Between 2015

and 2018, for instance, the share of trade produced by the three leading export countries

in apparel dropped. In contrast, the top three countries in semiconductors and mobile

communications increased their share of trade markedly.

Other considerations include whether the value chain is capital- or knowledge-intensive,

or tied to geology and natural resources. All of these make relocation less feasible. Highly

capital-intensive value chains are harder to move for the simple reason that they represent

hundreds of billions of dollars in fixed investments. These industries have strong economies

of scale, making them more costly to shift. Value chains with high knowledge intensity

tend to have specialized ecosystems that have developed in specific locations, with unique

suppliers and specialized talent. Deciding to move production outside of this ecosystem to

a novel location is costly. Finally, value chains with comparatively high levels of extraregional

trade have more scope to shorten than those that are already regionalized. We also consider

overall growth, the location of major (and rising) consumer markets, trade intensity, and

innovation dynamics.

With respect to noneconomic factors, we consider governments’ desire to bolster national

security, national competitiveness, and self-sufficiency. Some nations are focusing on

safeguarding technologies with dual-use (civilian and military) implications, which could affect

value chains such as semiconductors and communication equipment (particularly as 5G

networks are built out). In other cases, governments are pursuing industrial policies intended

to capture leading shares of emerging technologies ranging from quantum computing and

artificial intelligence to renewable energy and electric vehicles. This, too, has the potential

to reroute value chains. Finally, self-sufficiency has always been a question surrounding

energy. Now the COVID pandemic has driven home the importance of self-sufficiency in food,

pharmaceuticals, and certain medical equipment as well.

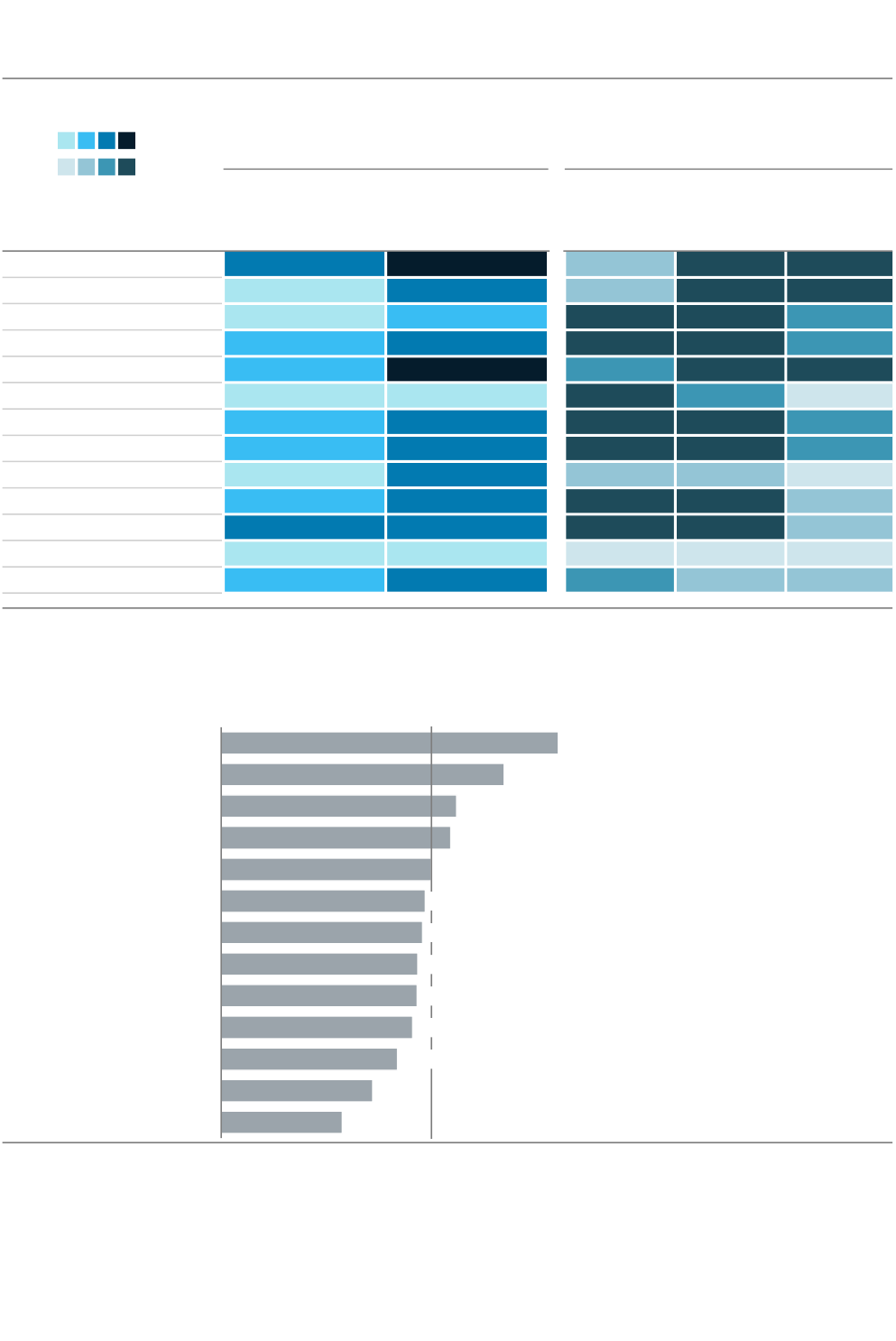

ExhibitE6 compiles these metrics for individual value chains and estimates what proportion

of production for export has the potential to move to new countries. We estimate that 16 to

26 percent of exports, worth $2.9 trillion to $4.6 trillion in 2018, could be in play—whether

that involves reverting to domestic production, nearshoring, or new rounds of offshoring to

new locations. It should be noted that this is not a forecast: it is a rough estimate of how much

global trade could relocate in the next five years, not an assertion that it will actually move.

The value chains with the largest share of total exports potentially in play are pharmaceuticals,

apparel, and communication equipment. In dollar terms, the value chains with the largest

potential to move production to new geographies are petroleum, apparel, and

pharmaceuticals.

12

In all of these cases, more than half of their global exports could potentially

move. With few exceptions, the economic and noneconomic feasibility of geographic shifts

do not overlap. Thus, countries would have to be prepared to expend considerable sums to

induce shifts from what are otherwise economically optimal production footprints.

12

The potential to move petroleum production is of course limited by the presence of geologic deposits. But if the price of oil

rises, exploration and extraction now considered uneconomic in some sites could become viable. New technologies, too,

could make it possible to expand into new locations.

16–

26%

of global exports could shift to

different countries due to economic

and noneconomic factors

13

Risk, resilience, and rebalancing in global value chains

Exhibit E6

Value chain

Eco-

nomic

factors

Non-

eco-

nomic

factors

2

Range,

$ billion

Share of

value

chain

exports,

%

Total exports, 2018,

$ billion

Top 3 exporter share

change, 2015–18, pp

Capital intensity,

3

%

Knowledge intensity,

4

%

Product complexity

5

Intraregional trade,

6

%

Global

innovations

Chemicals 86–172 5–11 1,584 -1.4 72 26 5 57

Pharmaceuticals 236–377 38–60 626 0 58 41 5 40

Aerospace 82–110 25–33 333 -2.9 53 40 5 34

Automotive 261–349 15–20 1,730 -1.6 51 16 5 60

Transportation equipment 60–89 29–43 209 0 48 18 5 43

Electrical equipment 213–319 23–34 928 -2.5 43 23 5 54

Machinery and equipment 271–362 19–25 1,455 -2.2 36 19 6 50

Computers and electronics 165–247 23–35 708 -1.9 47 57 5 53

Communication equipment 227–363 34–54 673 9.5 51 45 5 46

Semiconductors and components 92–184 9–19 995 10.5 62 39 5 81

Medical devices 100–120 37–45 268 0.1 47 29 5 40

Labor

intensive

Furniture 37–74 22–45 164 -5.7 40 15 4 55

Textiles 67–134 23–45 297 -3.2 34 15 4 55

Apparel 246–393 36–57 688 -8.1 30 18 3 43

Regional

processing

Fabricated metal products 94–141 21–32 440 -3.5 33 16 5 57

Rubber and plastic 97–145 20–30 488 -2.7 40 16 5 60

Food and beverage 63–125 5–11 1,149 -1.1 57 14 4 56

Glass, cement, and ceramics 22–45 11–21 209 -4.5 48 15 5 57

Resource

intensive

7

Agriculture 112–149 20–26 568 0.4 24 10 4 47

Wooden products 8–17 5–11 155 0.9 43 11 4 57

Basic metal 77–153 6–12 1,250 -3.6 54 16 4 51

Petroleum products 212–423 9–18 2,414 1.3 81 32 3 30

Mining 29–57 6–13 452 3.8 72 16 3 49

Total Low

High

2,900

4,600

16

26

The potential for value chains to shift across borders over the next five years depends on

economic and noneconomic factors.

Source: Federal Reserve Bank of St. Louis; Observatory of Economic Complexity; UN

Comtrade; US Bureau of Economic Analysis; US Bureau of

Labor Statistics; World Input

-Output Database; McKinsey Global Institute analysis

Value of exports

with shift feasibility

(annual exports)

1

Low High

Drivers of economic

shift feasibility

Low High

Feasibility of

geographic shift

Low High

1

. Low-end sizing = global imports from outside importing country’s region average of economic and noneconomic feasibility. High-end sizing =

global imports from outside importing country’s

region maximum of economic and noneconomic feasibility. 2. Noneconomic factors take into

account goods deemed essential or targeted for national security or economic competitiveness considerations, based on propose

d and enacted

government policies and definitions of essential goods

. 3. Amount of capital compensation as a share of gross output. 4. Defined as share of

labor with a tertiary education

. 5. Product Complexity Index measures the relative substitutability of production across sites of products in value

chain

. 6. Percent of total trade that takes place within same region as its importer. 7. Dependent on access to resources that are geographically

determined.

14 McKinsey Global Institute

In general, the economic case to move is most viable for labor-intensive value chains such

as furniture, textiles, and apparel. These value chains were already experiencing shifts away

from their current top producers, where the cost of labor has risen, to other developing

countries. The continuation of this trend could represent a real opportunity for some nations.

By contrast, resource-intensive value chains, such as mining, agriculture, and energy, are

generally constrained by the location of natural resources that provide crucial inputs. But

policy considerations may encourage new exploration and development that can shift value

chains at the margins.

The value chains in the global innovations category (semiconductors, automotive,

aerospace, machinery, communication, and pharmaceuticals) are subject to the most

scrutiny and possible intervention from governments, based on their high value, cutting-

edge technologies as well as their perceived importance for national competitiveness. But

the feasibility of moving these value chains based on the economics alone is low. For example,

the recent decision to site a new semiconductor fabrication plant in the United States was

contingent upon significant government subsidies.

Production networks have begun to regionalize in recent years, and this trend may persist

as growth in Asia continues to outpace global growth. But multinationals with production

facilities in countries such as China, India, and other major emerging economies are typically

there to serve local consumer markets, whether or not they also export from those places. As

prosperity rises in these countries, they are key sources of global growth that companies will

continue to pursue.

Four industry case studies illustrate what could drive the complexity of geographic

rebalancing of value chains

Pharmaceuticals. Overall, the pharmaceutical value chain has become less concentrated

and more globally dispersed over the past 20 years. But the manufacture of some

specific products is highly concentrated. While China and India export a relatively small

share (3 percent each) of overall pharmaceutical products by value, they are the world’s

key producers of active pharmaceutical ingredients and small-molecule drugs. In some

categories, such as antibiotics, sedatives, ibuprofen, and acetaminophen, China is the world’s

dominant producer, accounting for 60 percent or more of exports. India is the world’s leading

provider of generic drugs, accounting for some 20 percent of global exports by volume, but

it relies on China for most of the active pharmaceutical ingredients that go into them. When

the flow of these ingredients dried up in the early stages of the COVID pandemic, India

temporarily placed export controls on dozens of essential drugs, including antibiotics.

Based on economics alone, there is little reason to believe that pharmaceutical production

will shift unless companies respond to the rise of new consumers in developing countries.

But many governments are weighing whether to boost domestic production of some key

medicines (as well as medical equipment). As a result, we estimate that 38 to 60 percent of

the pharmaceutical value chain could shift geographically in the coming years. However,

production of small-molecule drugs would likely need to be highly digitized and automated to

be viable in advanced economies; otherwise, the higher cost of doing business might lead to

higher drug prices.

Automotive. The auto industry has some of the most intricate value chains in the global

economy, and the most regionalized. Most exports of intermediate parts circulate within three

broad regions: Asia, Europe, and North America. The US auto industry is integrated with

Mexico and Canada; Germany has production networks in Eastern Europe; and Japan and

South Korea source from China, Thailand, and Malaysia. Despite the largely regional nature

of automotive production, OEMs rely on some imported Chinese parts—and the initial COVID

outbreak centered in Hubei Province quickly produced global ripple effects in the industry.

Up to

60%

of global pharma exports

could shift to different

countries due to economic

and noneconomic factors

15Risk, resilience, and rebalancing in global value chains

Automotive is a prized industry from the standpoint of jobs, innovation, and competitiveness,

and nations have historically enacted tariffs, trade restrictions, and local content

requirements to try to attract and retain auto manufacturing. Trade disputes are an ongoing

concern, leading companies to build in more flexibility and redundancy. We estimate

that a relatively modest share of auto exports, between 15 and 20 percent by value, has

the potential to shift in the medium term, driven predominantly by noneconomic factors.

Semiconductors. While the United States designs advanced chips, their manufacturing

is highly concentrated in places like South Korea and Taiwan. Overall, Asia accounts for

more than 95 percent of outsourced semiconductor assembly and testing capacity. This

concentration brings potential risks. MGI research has found that companies sourcing

advanced chips from South Korea, Japan, Taiwan, or other hubs in the western Pacific can

expect that hurricanes severe enough to disrupt suppliers will become two to four times more

likely by 2040.

13

Other dynamics can also invite potential complications. A single firm leads

production of lithographic machines, which place circuits on the wafers.

Economies of scale and high barriers to entry leave very little room for semiconductor

production to move on its own. A semiconductor fabrication plant can cost $10 billion or more

to build, and the industry requires specialized engineers. But geopolitical and trade tensions

could reshape the value chain in ways that market forces alone might not. National security

and competitiveness concerns could lead governments to take action, potentially shifting

an estimated 9 to 19 percent of trade flows.

Textiles and apparel. Apparel and textiles are highly traded, labor-intensive value chains

that are already moving. China has long been the dominant player, and it still accounts for

some 29 percent of apparel sold globally. But its wages are rising, and Chinese producers can

now focus on meeting domestic demand. In 2005, China exported 71 percent of the finished

apparel goods it produced. By 2018, that share was just 29 percent.

Relative to all other value chains, textiles and apparel feature the highest proportion of trade

that could feasibly shift due to purely economic factors (36 to 57 percent in apparel, and 23 to