Construction Auditing,

Cost Types and

Auditability

JakeOrtego,PE,CCA,CCP,CCE

Pollingquestion1

1

PresentationOutline

Important

Definitions

Contracts

AuditClauses

Understandingthe

TotalAgreement

Proactivevs

Reactive

Auditing

Auditing

Timeline

Reasonability

Limitations

2

Audit

DeliveryMethod

Contractors

ContractType

ProjectTypes

ImportantDefinitions

3

DefiningConstructionAudit

Maybeacombinationofauditfunctionsandconsultingfunctions

AUDITFUNCTIONS

• Financial

• Compliance

• Operational

• Quality

• Forensic

CONSULTINGFUNCTIONS

• RiskAssessmentsandAvoidance

• Trending

• BestPractices

• Benchmarking

ImportantDefinitions

4

TypesofConstructionAudits

Project

Program

Process

ImportantDefinitions

Auditingwhencan’trecovercanbeusefulforthefuture

5

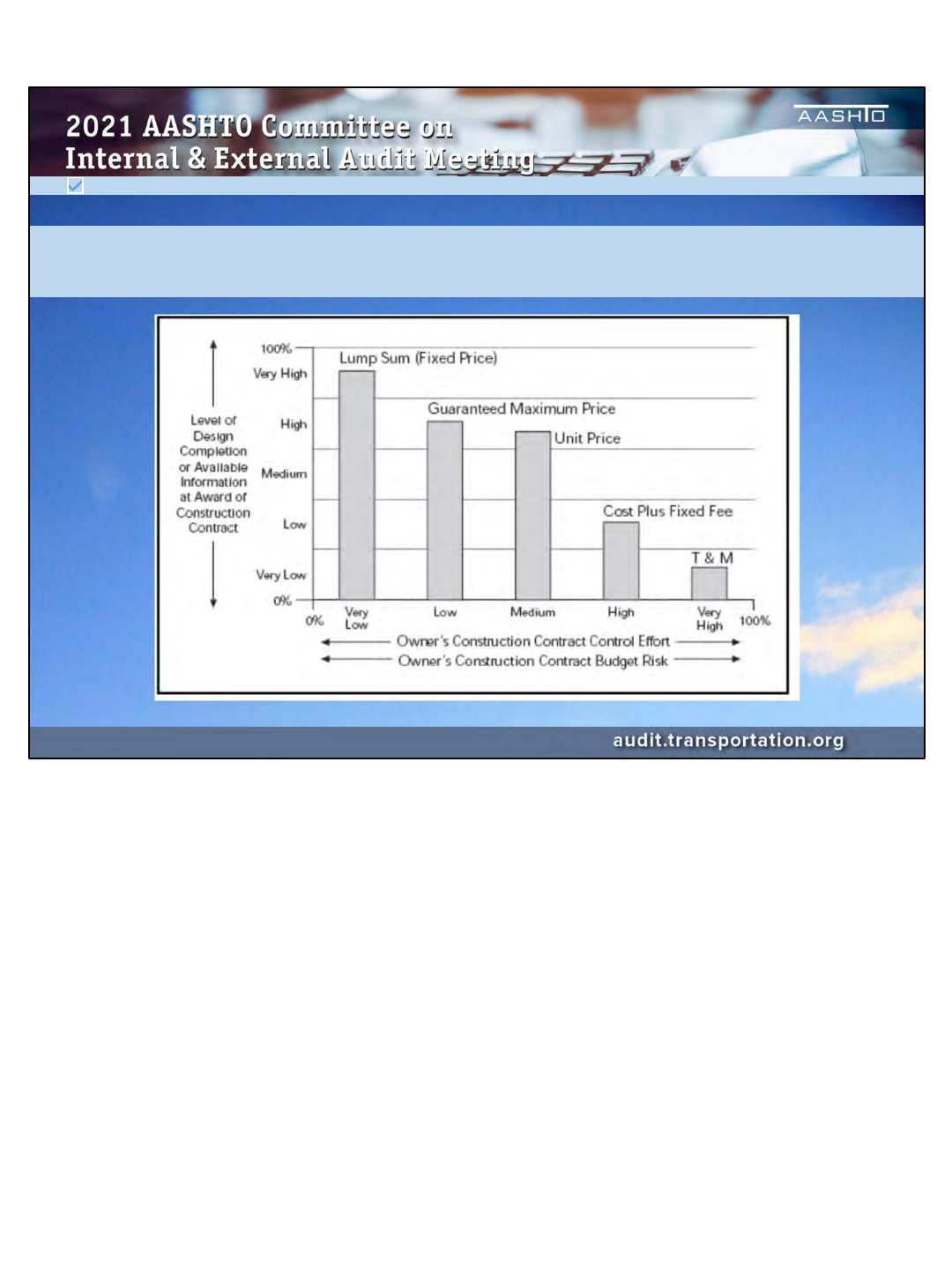

Deliv eryMethod

OnePrice

LumpSum

FixedPrice

StipulatedSum

UnitBased

UnitPrice

TimeandMaterial

EarnedValue

ActualCost

CostPlus

CostPluswith

GMP– GuaranteedMaximumPrice

NTE–NottoExceed

Transparency

GreaterLess

ImportantDefinitions

PollingQuestion2

6

From2010Report“IntegratedProjectDeliveryforPublicandPrivateOwners”– PublishedbytheNASF,COAA,APPA,AGCandAIA

Deliv eryMethod

ImportantDefinitions

7

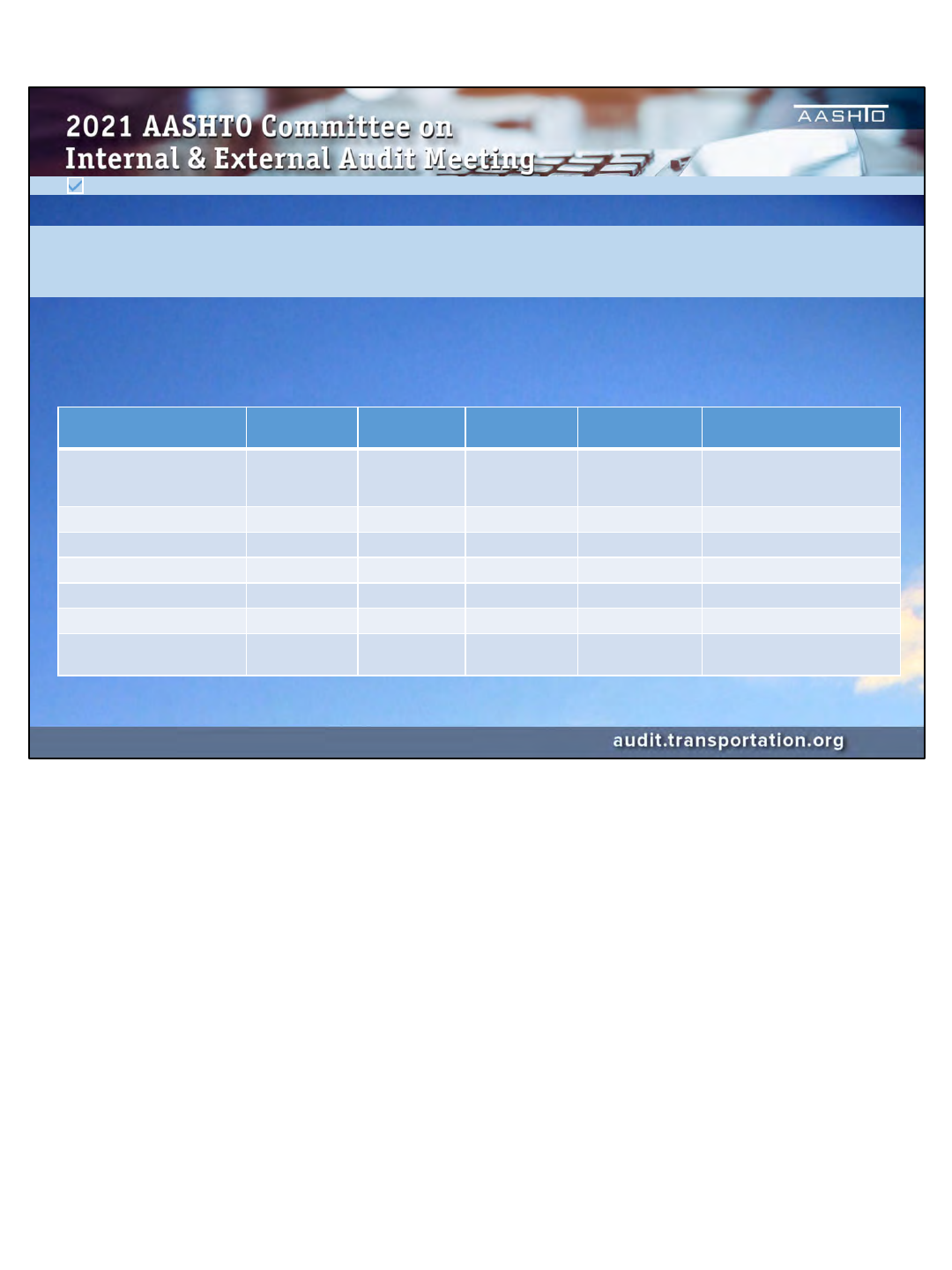

Deliv eryMethod

Description True CostPlus Typical GMP

GM/GC style

GMP

LumpSumwith

Allowances Other PossibleHybrids

SubCcontractors Actual

Each asa

separateLump

Sum

Each asa

separateLump

Sum

PartofLumpSum

Mix ofLumpsum,separate

GMPorunitprice

SelfPerformedWork Actual LumpSum LumpSum PartofLumpSum LumpSum

OtherMisc. DirectCosts Actual Actual Actual PartofLumpSum Actual,T&MorUnit Price

General Conditions Actual Actual LumpSum PartofLumpSum ActualorLumpSum

Ins

urancesandSureties Actual Actual LumpSum PartofLumpSum Actual,MultiplierorLumpSum

OverheadandProfit Multiplier Multiplier LumpSum PartofLumpSum MultiplierorLumpSum

Allowances Actual Actual Actual

Actual orUnit

Price

MixofActualorUnitPrice

Therearemanycombinationsthatcanbeused.This

tableshowssomepossiblecombinations.

ImportantDefinitions

8

GeneralContractor

Subcontractor

Owner’sAgent

Owner’sRepresentative

CMA‐ ConstructionManagerasAgent

ProgramManager

DeveloperasAgent

CMARConstructionManagerat

Risk

EPC/EPCM– Engineering

ProcurementConstruction

(Manager)

DesignBuild

IPD–IntegratedProjectDelivery

Con tr act ors

ImportantDefinitions

9

Horizontal

Roads,sidewalks,pipelines,utility

runs

UsuallyUnitPrice

Vertical

BuildingsandStructures

TypicallyLumpSumorCostPlus

Other

AreaBased‐ Excavations,

landscaping,parkinglots

MorelikelytobeLumpSum,Cost

Plus,orT&M

ProjectTypes

ImportantDefinitions

10

• Explicit

• Implicit

• Undefined

Manyare:

• Ambiguous

• Misunderstood

• Missing

AuditClauses

Contracts

UsingTemplatesdonotguaranteetheclausesareinplaceorareadequite

11

MeasurementvsPayment

(FromGerorgia DOT)

MeasurementandPaymentTheOfficeofDesignPolicyandSupportshallsupplya

volumereporttotheAreaManageratthePreconstructionmeetingorshortly

thereafter.TheConstructionManagershouldusethevolumereport toestimate

quantitiesbetweenstationsforpaymenttotheContractorduringconstruction.

Undercutsand/orothergeneralsmalllocationsnotshownonoriginalcross

sectionsshallbecalculatedbyconstructionprojectpersonnelbaseduponfield

measurements.Recordthesequantitiesseparatelyfromthevolumereport

quantities.Contractorrequestedchangesordisputestotheoverallestimated

volumequantitiesshouldbeauditedbyContractLiaisonpriortofinaldecision.

FinalcrosssectionsandvolumereportshallbeauditedbytheContractLiaison

priortofinalpaymentismadeoragreedupon.

AuditClauses

Contracts

12

FromHawaiiDOT

7.18RighttoAuditRecords,RecordsMaintenance,Retention,andAccess.PursuanttoChapter103D‐317,H.R.S.,theState,

atreasonabletimesandplaces,mayauditthebooksandrecordsofaContractor,prospectivecontractor,subcontractor,

andprospectivesubcontractorrelatingtotheContractor’sorsubcontractor’scostorpricingdata.Anysuchauditsma

ybe

conductedbyFederalandStateemployeesorbyconsultantsworkingonbehalfoftheState.TheContractorand

subcontractor(s)shallmaintainthebooksandrecordsforaperiodofthreeyearsfromthedateoffinalpaymentunderthe

contract.

TheContractoranditssubcontractorsshall,inaccordancewithg

enerallyacceptableaccountingpractices,maintainfiscal

recordsandsupportingdocumentsandrelatedfiles,papers,andreportsthatadequatelyreflectalldirectandindirect

expendituresandmanagementandfiscalpracticesrelatedtotheContractorandsubcontractor’sperformanceofwork

underthiscontract.

TherepresentativesoftheState(andFederalgovernmentrepresentativeswhenfe

deralfundsareutilized)havetherightto

inspectandcopyanybook,document,paper,file,orotherrecordthatisrelatedtotheperformanceoftheworkofthe

Contractorandanysubcontractor.TheContractorshallprovidefullcooperationduringanyauditorinspectionandshall

insurethatitssubcon

tractorscomplywiththisrequirement.TheContractorshallbearallcosts(includingattorney’sfees)of

enforcementintheeventofitsoritssubcontractor’sfailureorrefusaltofullycooperate.

AuditClauses

Contracts

13

TypicalAIAAuditclause‐ § 6.11Accounting Records

TheConstructionManagershallkeepfullanddetailedrecordsand

accountsrelatedtothecostoftheWorkandexercisesuchcontrolsas

maybenecessaryforproperfinancialmanagementunderthisContract

andtosubstantiateallcostsincurred.Theaccountingandcontrol

systemsshallbesa

tisfactorytotheOwner.TheOwnerandtheOwner’s

auditorsshall,duringregularbusinesshoursanduponreasonablenotice,

beaffor dedaccessto,andshallbepermittedtoauditandcopy,the

ConstructionManager’srecordsandaccounts,includingcomplete

documentationsupportingaccountingentries,books,correspondence,

instructions,drawings,receipts,subcontracts,Subcontractor’s

proposals,purchaseorders,vouchers,memorandaandotherdat a

relatingtothisContract.TheConstructionManagershallpreservethese

recordsforaperiodofthreeyearsafterfinalpayment,orforsuchlonger

periodasmayberequiredbylaw.

AuditClauses

Contracts

14

AuditClauses

“NotAudit able”vs“Fixed”

NotAuditableorUn‐Auditablearetheonlytermsthattrulylimitanauit

Fixeditemsmaybeauditedbutnotnecessarilybechanged

NoAuditClause

Hardertoconvincecontractorstoallowforanaudit

….butnotimpossible!

Contracts

15

GoverningLa w

FederalLevel

• TruthinNegotiationsAct

StateLevel

• Canvarybystate

• Possiblestatutesof

“KnowinglyMisrepresenting”

information

Contracts

16

TheTotalAgr eemen t

Contracts

• Themaininterfaces

• Contract

• CentralConditions

• DesignDocuments

• Division01

• ExceptionsandClarifications

• ValueEngineering

• QUESTION:

• Inthecaseofconflict,whatshouldgovern?

• Division01

• ConflictwithcontractandGCs

• WhoReadsit?

• ExceptionsandClarifications

• Howdothesefitinwiththedesign

• Recommendation:A/Eshouldacceptorrejecteachonelinebyline

• Sometimes,theE/Ccanbeinconflictwiththedesignintent

• Or,ifaccepted,couldchangethedesign

• ValueEngineering

17

• ShoulditbetheContractor’sresponsibility

17

ProactiveandReactiveAuditing

CostRecoveryCost/RiskAvoidance

Proactive

BidReviews

ContractTerms

RateReviews

MutualUnderstanding

Hybrid

InterimAudits

ContinuousAudits

ChangeOrderReview

PayApplicationReview

Reactive

CloseoutAudit

ForensicAudit

ComplianceAudit

HistoricAudit

POLLINGQUESTION3

18

Reasonability andIndus tryStandards

Manycostsareacceptedwiththe

conceptofthevaluebeing“Reasonable”

basedonexperienceorwithin“Industry

Standards”foritemslike:

InsuranceRates

BondRates

LaborBurden

FullBurdenedRates

ContingencyPercentage

OverheadandProfit

…andmuchmore…

Manypublicsectorprojectsareawardedonlowestresponsivebid

Maylimitabilitytoexaminemaincosts

Doesnotlimitabilitytoexaminecostthatmaymakeupchangeorders

19

On to Auditing!

20

AfterorNear

FinalCompletion

Purpose:Verifytotalfinal costsareincompliance

withthecontractto:

‐ VerifyContractorbilledincompliance

withthecontract

‐ Recoveranyoverbilledfunds

‐ Identifyanymajorroot causesofcost

overrunsorscheduledelays

Pros

Thereshouldnotbeanytrailingcostsorpayments

Allwaiversoflienshouldbeavailable

Allsettlementsareknown

Allrebatesandcreditsareknown

Therearenopendingchanges

Thereisnodisruptiontoprojectbeingaudited

Cons/Risks

Diminishingknowledgeovertime

“Wecan’tfindthepaperwork,butev erythingwasagreedto!”

Increaseddifficultyiftherearefundstoberecovered

“Allofthemoneyhasbeenpaidout,thereisnothingtogiveback!”

21

Increasedlikelihoodofadversarialsituations

“Theprojectwascompletedlongago,whyisitbeingaudited?”

“Theowneragreedwiththepayments,whyisitbeingaudited?”

21

HorizontalConstruction

UnitPrice

Whatistypicallyaudited

InvoicesandPayapplications

correctlycalculated

Supported

Quantity

FieldInspection

AuditofQuantityVerification

Other“Non‐Unit”partsofcontract

Whatwaspaidfordelays,acceleration,

unforeseenconditionsandotheritemsbeyond

theunitprice

UseofContingenciesandallowances

ChangeOrders

22

VerticalandOther

GMP/CostPlus/T&M

• ChangeOrders

• ContingencyUse

• AllowanceUse

• Subcontractors

• Changes

• Invoices/PayApplications

• FinalWaiversofLien

• FinalSettlement

• AccountsPayable

• InternalChangesandTransfers

• Back‐charges

• ReimbursableMaterials

• ReimbursableLaborCosts

• WithactualsforHealth&

Retirement

• ReimbursableRentals

• ReimbursableGeneralConditions

• FinalCostswithrebatesfor:

• Bond

• Insurances

• RiskP

oolUsage(Maybe)

• FinalCalculationsfor:

• OHP

• SharedSavings(ifapplicable)

• LiquidatedDamages

23

TheIssueofChangeOrderTiming

Itisrecommendedtohaveallchangesapprovedor

rejectedbeforethefinalaudit.

• Somecontractorswillholdafinal“postaudit”changeto

trytooffsetpossiblesignificantfindingsagainstthem.

• Someownerswill waitfortheauditbeforeapproving

changeswiththeideathattheywillbasetheapproval

onanyavailablefundingthathasbeenmadebythe

audit.

Bothcasesareunadvisableaschangesshouldbe

basedonmodificationstothescopeandcontract

24

DuringConstruction

Purpose:Todeterminehowtheexecutionoftheprojectaligns

withtheexpectationsaswellas:

• Lookforrisksthatmaybeavoided

• ReviewPayApplications

• ReviewChangestoDate

• InterimAudit–Costtodate

• Trendingandforecasting

25

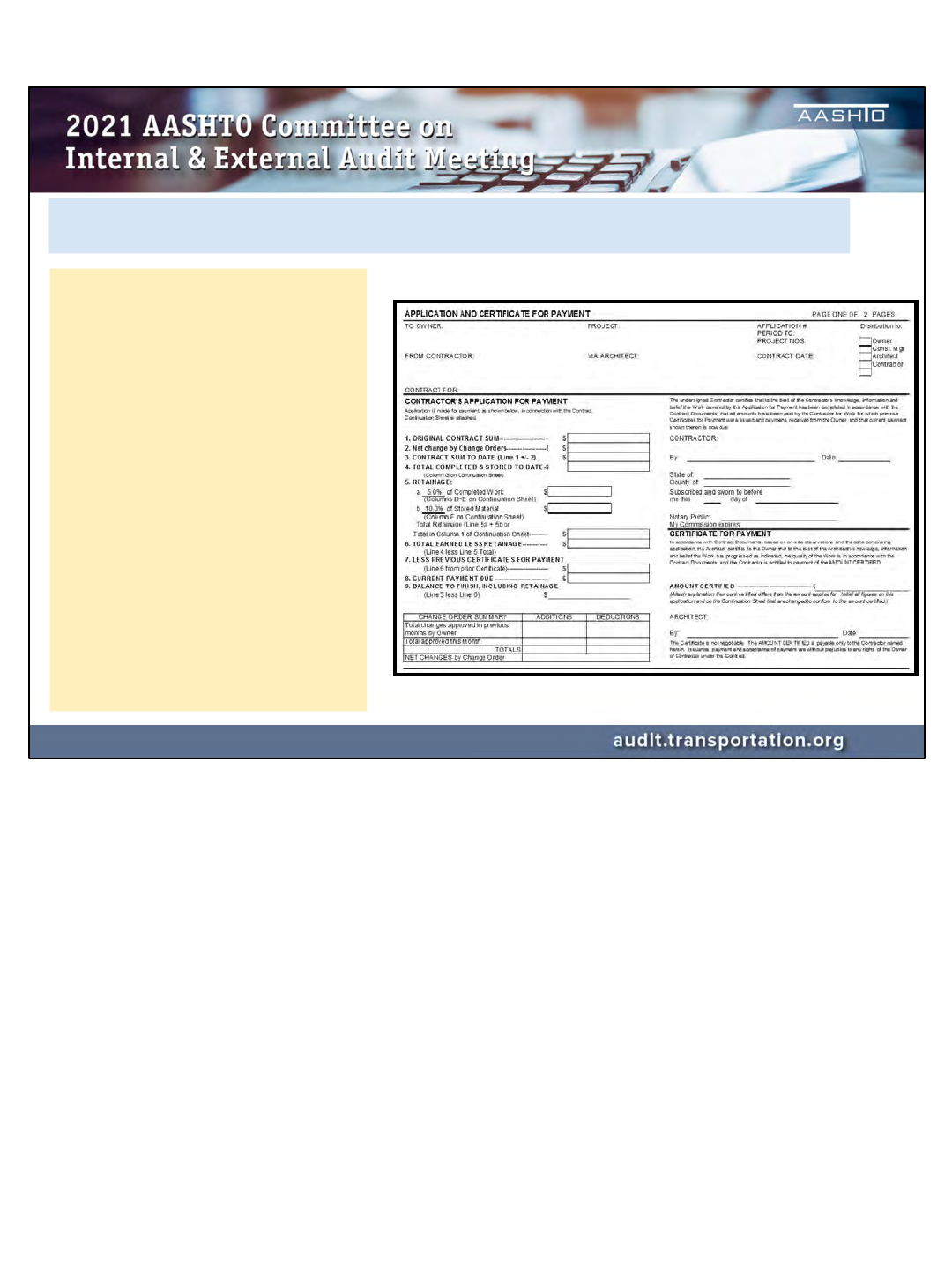

Payapplications

• Conformanceto

Contract

• Progress

• Terms

• Timing

• SupportingDocuments

• VerificationofMath

NOTES:

• Signaturesdonotensure

accuracy

• PAsarenotprogress

reports

Theremaybetimeconstraintsfromthedaythepayappisissuedtothedaytheauditneedstobe

completed

10Daysistypical

Timeconstraintswilloftenremovetheabilitytoauditthechangeorderseachmonth

AuditingoftheCOscanbegroupedintointerimauditsorfinalaudit

NOTE–SwornstatementsvsPAs

26

WhatcanbeAuditedandtheLimitations

• Det ailedcostestimates

• Quantitytakeoffs

• Drawings

• Designdirection(RFI,ASI,bulletins,

sketches,etc.)

• Communication

• Thelimitationistypicallywithcontractors

andsubcontractorsthatarenotusedto

providingdetailedchanges

Asignedchangedoesnotmeanthatyoucan

neverre‐examineit

Chang es

27

TrendingandForecasting

28

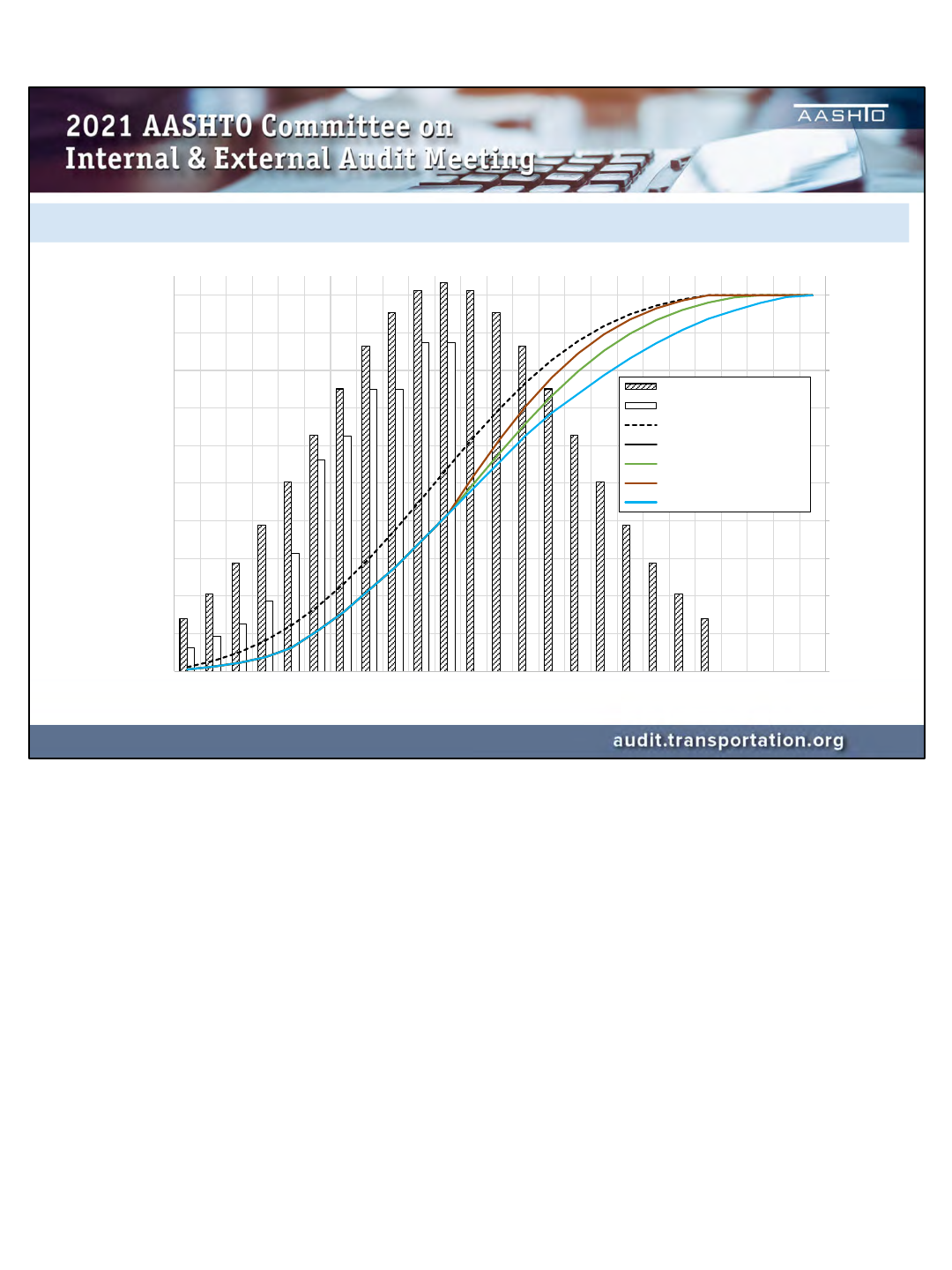

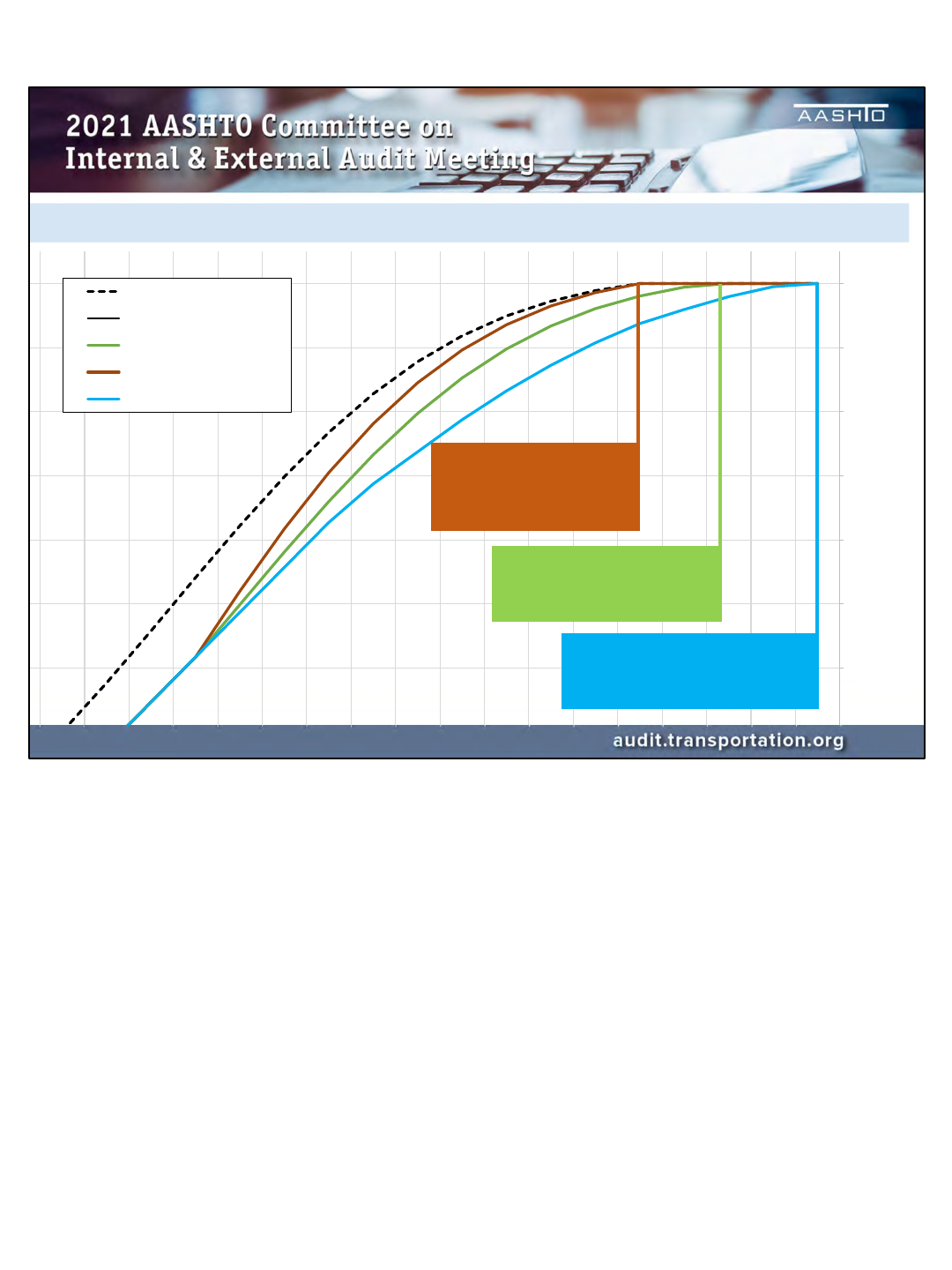

Expend ituresatthe50%completionpoint

TrendingExample–CashflowandSchedule

0

10

20

30

40

50

60

70

80

90

100

‐

80

160

240

320

400

480

560

640

720

800

‐ 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100 105 110 115 120

%ofTotalPojectValue

UnitsperMonth

%ofPlannedProjectDuration

PlannedMonthly

ActualMonthly

PlannedCurve

AcutalCurve

FollowOriginalCurve

TrytoMeetOriginalFinishCurve

SPICurve

Notes:

Unitpermonthare$

Projectdurationisa%ofthetotalduration

Durationmonthscanbeusedinsteadofduration%

29

Change satthe50%completionpoint

TrendingExample–CashflowandSchedule

30

40

50

60

70

80

90

100

%ofTotalPojectValue

PlannedCurve

AcutalCurve

FollowOriginalCurve

TrytoMeetOriginalFinishCurve

SPICurve

TomeettheoriginalSchedule,

thenextseveralperiodspend

ratemustbecloseto150%more

thanthemaxspendforanygiven

periodtodate.

TomeettheoriginalSchedule,the

nextseveralperiodspendratemust

becloseto120%morethanthemax

spendforanygivenperiodtodate.

Projectdurationwillincreaseby10%

A“SchedulePerformanceIndicator”

equationmaintainsahistoricspendrate.

Projectdurationwillincreaseby20%

Notes:

Unitpermonthare$

Projectdurationisa%ofthetotalduration

Durationmonthscanbeusedinsteadofduration%

30

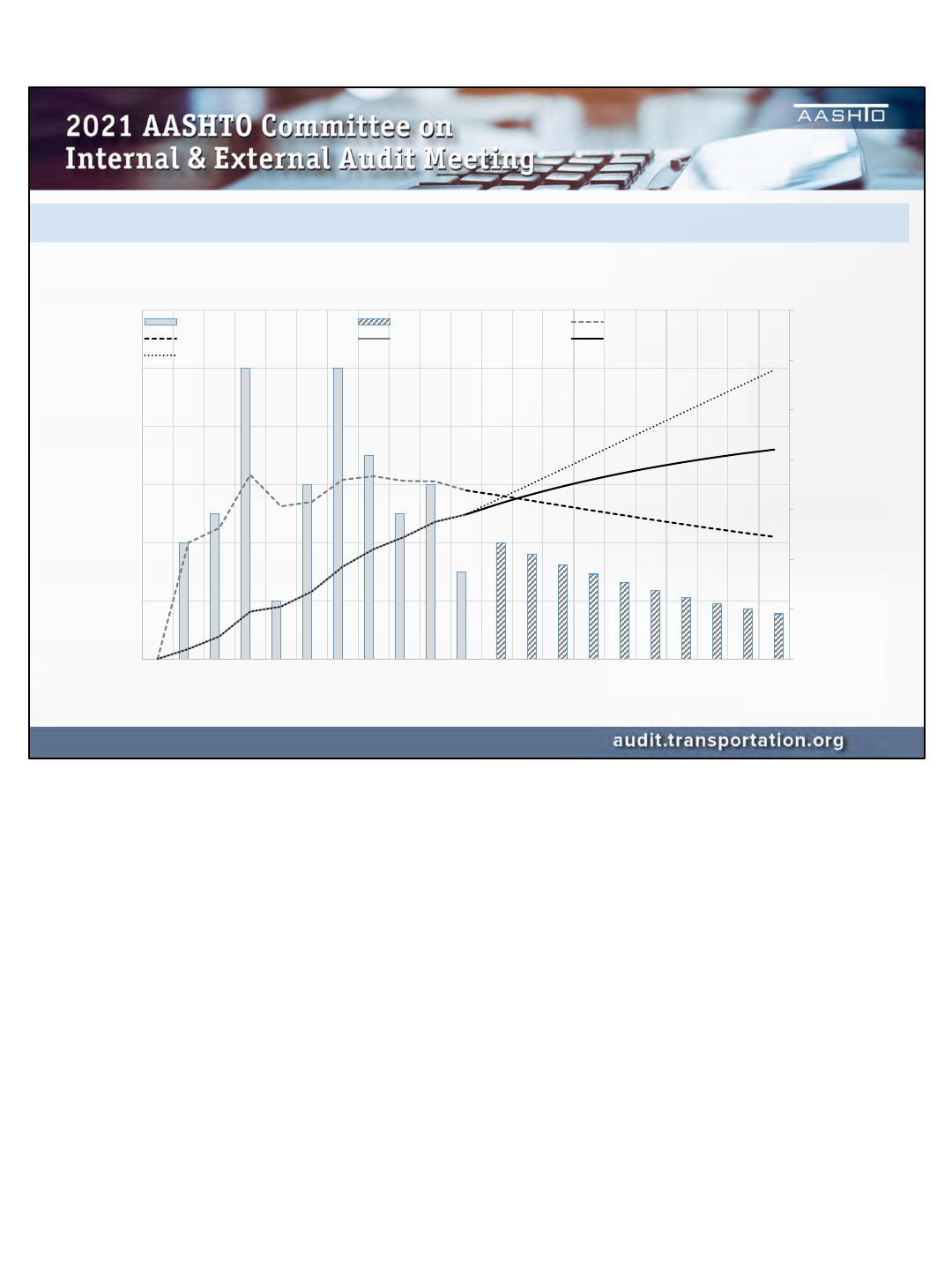

TrendingExample–ChangeOr ders

Expend ituresatthe50%completionpoint

0

200

400

600

800

1000

1200

1400

0

20

40

60

80

100

120

‐ 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100

CumulativeUnits

MOnthlyUnits

%DurationoftheProject

ValueofChangesperMonth

ValueofChangesperPeriod ForecastChangesperPeriod CumulativeMovingAverage

ForecastCumulativeMovingAverage Cumulative ForecastCumulative

CumulativeStraightLine

Cumulativemovingaverageshowstherateofchangebetweeneachmonth

WhenthecurveslopesUP,theaveragevalueofchangesisGREATERthanthepreviousperiod

WhenthecurveslopesDOWN,theaveragevalueofchangesisLESSthanthepreviousperiod

Byforecastingtheperiodvalues,youcanmodeltheCMAcurvefortherestofthe project

ThemonthlyvaluesareonlyusedtomodeltheCMAandcumulativecurvesandshouldnotbeused

topredicttheactualvaluesexpectedpermonth

Forcomparison,astraightlinewasinsertedusingtheaveragechangesatthe50%mark

31

Be foreConstructionBegins

Mostsavingspotentialforleastamountof

work

Hardtoquantifyasitisspeculative

Purpose: Verifythatallpartiesareinagreementinregardsto

thebudget,designstatus,schedule,andproject

executionplan.

Additionally,identifypotentialrisksthatmaynot

havebeenpreviouslyaddressed.

Ideallyshouldhappenbeforecontractsaresigned

POLLINGQUESTION4

32

• Contracts

• Subcontracts

• CM/GCBidDocuments

• SubcontractorBids

• Estimates

• BasisofContractValue

• Schedule

• InsurancePolicies

• LaborRateBuildups

• ClarificationsandExceptions

• Value EngineeringEfforts

• ProjectControlSystems

• Changes

• PayApplications

• ProjectReporting

• Allowances

• Contingencies

• ProjectExecutionPlans

• RolesandResponsibilities

• Subcontracting

• Schedule

• QualityControl

• Closeout

WhatCanbeAudited?

33

WhatCan’tbeAudit ed?

• Intheory,everythingisauditablepriortosigningof

aconstructor'scontract.

• Thatdoesnotguaranteethatthecontractorwillcomply

• Auditorsshouldbemindfulthatacontractormaystill

walkawayfromanegotiationpriortosigningthe

contract

• Auditingafterthecontracthasbeensignedmaybe

limitedtowhatwasagreedtointhecontr act.

34

Projectinception

Purpose: Verifythatthestepsforscoping,

budgeting,andschedulehavea

reasonableandrealisticbasis.

TimeFrame: Thismaybeperformedatmultiple

stagesincluding:

• Inception

• SelectionoftheArchitect

• ProgramDesign

• SchematicDesign

• DrawingsIssueforBid

• ReviewoftheGMP

35

Projectinception

WhatcanbeAudited

• Scopehasbeendefinedandisclear

• Viabilityandneedoftheprojectwithintheorganization,

location,industry,andmarketisunderstood

• Budgetgoalsarerealisticandachievable

• ConsidersA/E,Construction, Land,Legal,FFE,Contingencies,etc.

• Schedulegoalsarerealisticandachievable

• GiveadequatetimeforA/E,weather,commissioning,etc.

• Fundingsourcesareviableandavailable

• Riskhasbeenconsideredinthebudget,schedule,andfunding

• Uncertaintyinthebudgetandscheduleaccuracyhasbeen

considered

Thehardpartisgettingtothetable

36

Trackingconstructioncostsarenotthesameasa

business’sfinancialsystem

TherearenoGenerallyAcceptedAccountingPrinciples

(GAAP)specifictoconstructionaccounting

ConstructionAccountingisNOTthatsameasaccountingfora

constructioncompany

Therearenoaccountingstandardsbywhichall

constructioncompaniesmustfollowing

Constructionhasmorethanjustexpenditures

Commitments

Retainages

Absorbingcosts

Somethingsmustbefullyreconciledratherthan

sampled

Changes

Allowances

Commitments*

Insurances*

ContingencyUse*

*Ifthecontracttypehasthisleveloftransparency

NuancesofConstructionAuditing

37

QUESTIONS?

JakeOrtego,PE,CCA,CCP,CCE

Construction Auditing, Cost Types

and Auditability

38