Private and Proprietary. Prepared for American Benets Council ©2019 Keane – All rights reserved

1

INTRODUCTION TO UNCLAIMED PROPERTY

Unclaimed property is a liability that remains outstanding beyond a specied period of time. These liabilities may

be outstanding because the owner changed address or appears to be unaware of the liability.

State laws require that businesses le an annual report of these outstanding liabilities and ultimately transfer, or

escheat, the property to the state for safekeeping until the ultimate owner comes forward.

The purpose of unclaimed property is to protect the property rights of the owner and reunite lost owners with

their property. Unclaimed property also relieves holders from the property liability and protects holders from

subsequent claims by the owner. The economic benet goes to the state and its citizens, not the individual holder.

Unclaimed property compliance maintains good customer relations, ensures records are current and reduces audit

risk.

NEED FOR CLEAR GUIDANCE

In unclaimed property compliance, we in the industry are accustomed to statutory guidance and we appreciate

clarity. We have seen rsthand the confusion and frustration that can arise from vague recommendations,

especially when they are followed by strict enforcement.

For example, on August 14, 2014 the Department of Labor (DOL) attempted to clarify how the duciaries of

terminated plans can fulll their obligations under ERISA to locate missing participants and properly distribute

the participants’ balances. Included in the bulletin were unclear recommendations to use “free electronic

search tools” and to “consider if additional steps are appropriate” under the duciary duties of “prudence and

loyalty.”

These vague recommendations were followed up with strict enforcement by the DOL, as highlighted by a

letter released from the American Benets Council in 2017 explicitly requesting that “the Department engage

in a rule making process to issue comprehensive guidance on plan duciary responsibilities with respect to

unresponsive and missing participants and cease taking ad hoc enforcement positions until the Department

provides actual guidance.” The below examples from DOL auditors varied actions were cited in the letter:

• Asserted that a plan administrator’s failure to locate a missing person was a breach of duciary duty, even

when the plans procedures were followed

• Threatened to refer plan sponsors to DOL’s Ofce of the Solicitor if plan failed to take action even where, in

some instances, the actions suggested were impermissible under other regulatory regimes

• Suggested that plan sponsors must “do whatever it takes” to locate missing participants

• Asserted that a plan should search without limit for missing participants, rather than annually, thus not

considering their duciary obligation to spend plan resources efciently

UNCLAIMED PROPERTY IS COMPLICATED!

It will be a challenge to create clear guidance for a specic type of property (e.g. uncashed checks from ERISA

plans), but it can certainly be accomplished. To help illustrate the dynamics to consider, we will attempt to

highlight some of the complexities around Unclaimed Property and demonstrate some of the operational

challenges faced by holders who report unclaimed property,

All states, Washington, DC, Puerto Rico, Guan and the U.S. Virgin Islands have unclaimed property programs.

Three Canadian Providences (Quebec, British Columbia and Alberta) have unclaimed property programs. No

two states unclaimed property laws are the same and reporting due dates across jurisdictions vary, depending

Private and Proprietary. Prepared for American Benets Council ©2019 Keane – All rights reserved

2

on the state. Unclaimed property laws and regulations span across many industries and are different per type

of property being reported.

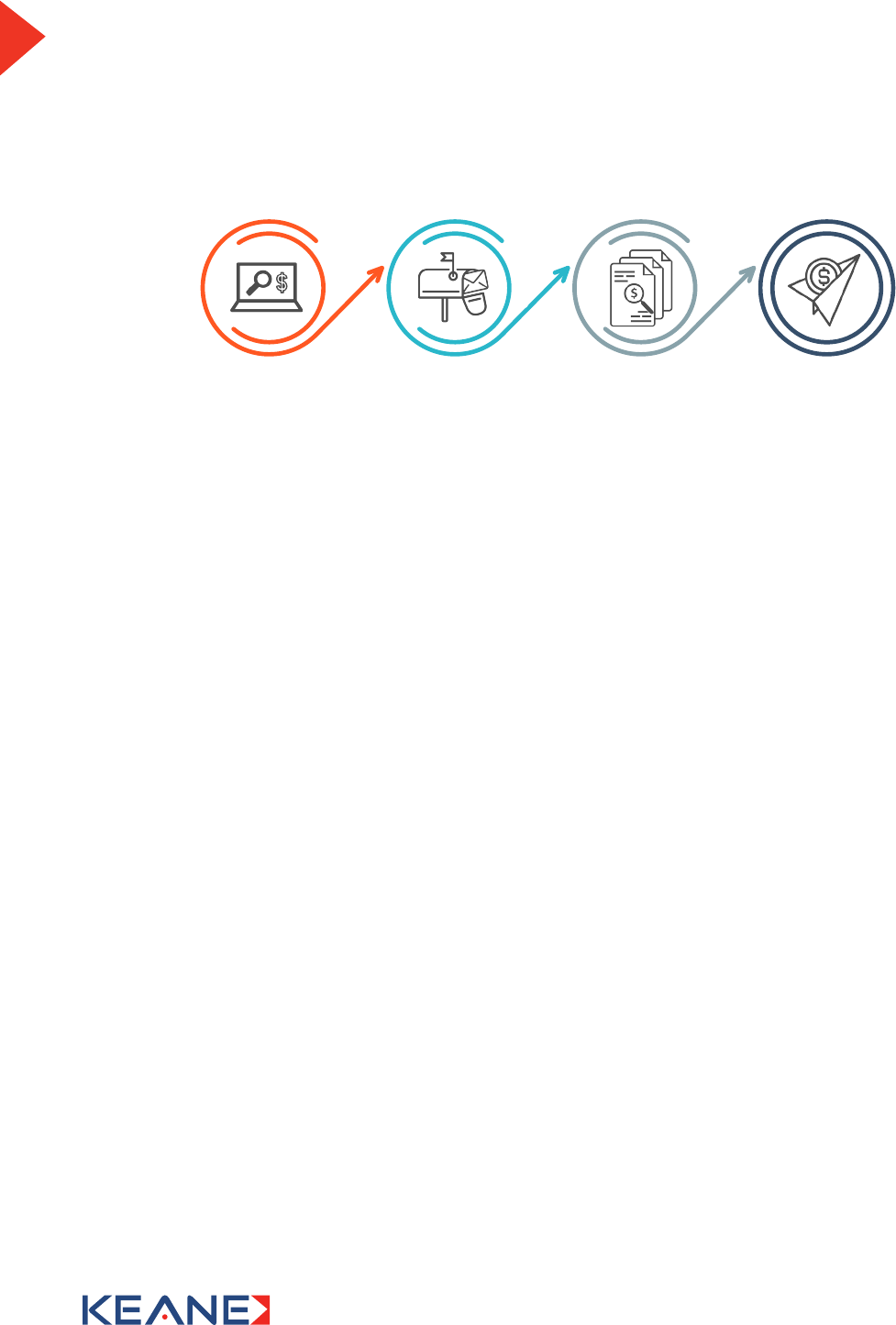

There are four primary steps to unclaimed property reporting and compliance, and there are numerous

complexities with each one.

Analysis RemittanceReporting

Due

Diligence

DATA COLLECTION AND ANALYSIS

Quite possibly, the most challenging aspect of unclaimed property reporting is determining exactly what to

report, where to report it, and when it should be reported. Identifying outstanding items that are eligible for

due diligence and reporting on the upcoming reporting deadlines requires up to date information about state

dormancy triggers, dormancy periods, cut-off dates and reporting deadlines and how they are applied.

Maintaining current state administrative guidance, statutory directives, and rules and regulations can be a

formidable task. However, for uncashed checks, the eligibility analysis entails an easy calculation of check issue

date plus the state prescribed dormancy period.

If using unclaimed property software or a third-party provider to perform escheat reporting, conrm with

your provider that any rules engines that perform an eligibility analysis can appropriately handle the multiple

dormancy calculations that may be necessary to accurately report certain property types.

DUE DILIGENCE

In general, states require a notice to be sent to the last known address of the owner of the funds as indicated

in the holder’s records. The purpose of the requirement is to give the owner one last opportunity to claim their

funds or reactivate their account before it is turned over to the state. Over the years, states have placed greater

emphasis on due diligence, with new or enhanced requirements on qualications for due diligence, timing of

the mailing, letter content, method of delivery and even attestations of mailing.

In evaluating whether or not due diligence is required, there are several factors that must be considered,

including: property type, state of the owner’s last known address, value of the account, and possibly,

whether or not the address is a known “bad” address. There are a few states that exempt the due diligence

requirement if the address of record is known to be a “bad” address, meaning that mail has been returned as

undeliverable to that address.

Mailing within 60 to 120 days prior to the reporting deadline is the most common time frame either mandated

or recommended by the states. States began to impose timeframes for sending due diligence to discourage

holders from mailing letters too close to the reporting deadline. Instead, the states wanted to allow the owner

at least thirty days to respond to the letter, and acknowledge his or her ownership interest in the property held

by the holder, prior to escheatment.

Like all aspects of unclaimed property regulation, there are states that vary from the norm. Some, like

California, require letters to be mailed within 180 to 365 days prior to the property becoming reportable.

Private and Proprietary. Prepared for American Benets Council ©2019 Keane – All rights reserved

3

Michigan requires letters to be mailed within 60 to 365 days prior to the report deadline, and New York

requires rst class letters to be mailed 90 days prior to the deadline and a certied mailing to take place (on

accounts valued over $1,000) 60 days prior to the deadline. Mailing letters to owners in foreign countries is

also required. Keep in mind that additional time may be needed for the mail to reach the owner and for the

owner to respond. While most states do not mandate how much response time should be given to the owner,

the standard recommendation is 30 to 45 days.

State requirements on letter content vary. Most states require:

• Nature and identifying number and/or description

• A statement relaying that the property must be validated by the owner otherwise the property will be

transferred to the state

• Information on the steps required to claim the property

• The date the property will be reported to the state, id proof of claim is not satised

• Contact information for your company

First class mail is generally the mandated method of delivery but there are a few states that require a notice to

be sent via Certied Mail. Some states even require different mailing type based on the value of the unclaimed

property. State auditors will ask for proof of due diligence compliance. Therefore, it is recommended that a

holder retain documentation showing that statutory due diligence was performed including copied of the

letters that were reported.

REPORTING

Unfortunately, like the state due diligence specications, state requirements for reporting and remitting are

anything but uniform. State reporting deadlines are at different times throughout the year and some states

even require reports to be led on different dates based on the type of property.

The widely accepted electronic format for unclaimed property reports is called the “NAUPA II Standard

Electronic File Format.” The National Association of Unclaimed Property Administrators (NAUPA) devised this

format which every state unclaimed property program now requires for reports. Generally, states will no longer

accept reports in an Excel format.

In addition, most states require the use of “property type” and “relationship” codes when reporting property.

The NAUPA II le format has corresponding standard property type and relationship codes that are accepted

by almost all states. The property type code designates the category of property and the relationship code

provides information as to the connection between owners when more than one owner is associated with the

property. Each property type is represented by two letters and two numbers, i.e., CK13 = vendor check. The

relationship is represented by a code comprised of two letters, i.e., JT = joint tenants.

It is important to note that states frequently modify some of the NAUPA relationship and property type codes,

customize the codes by changing the transactions included under particular codes, add new codes to the

NAUPA set, or do not use or accept particular codes in the NAUPA set. For this reason, the practitioner should

retrieve and use the code listings for the states to which reports will be led. These listings are often included

in reporting manuals or guides that state ofcials publish on their unclaimed property websites.

REMITTANCE

Typically, most businesses report cash as unclaimed property and the remittance that accompanies the

unclaimed property would be a check or electronic funds transfer (EFT). Instructions are usually provided

with state report forms and/or in state reporting manuals or guides published on state websites. Due to

technological advancements, some states now require EFT, Fed Wire or ACH transfer. Reports must be delivered

Private and Proprietary. Prepared for American Benets Council ©2019 Keane – All rights reserved

4

to the state by the appropriate reporting deadline.

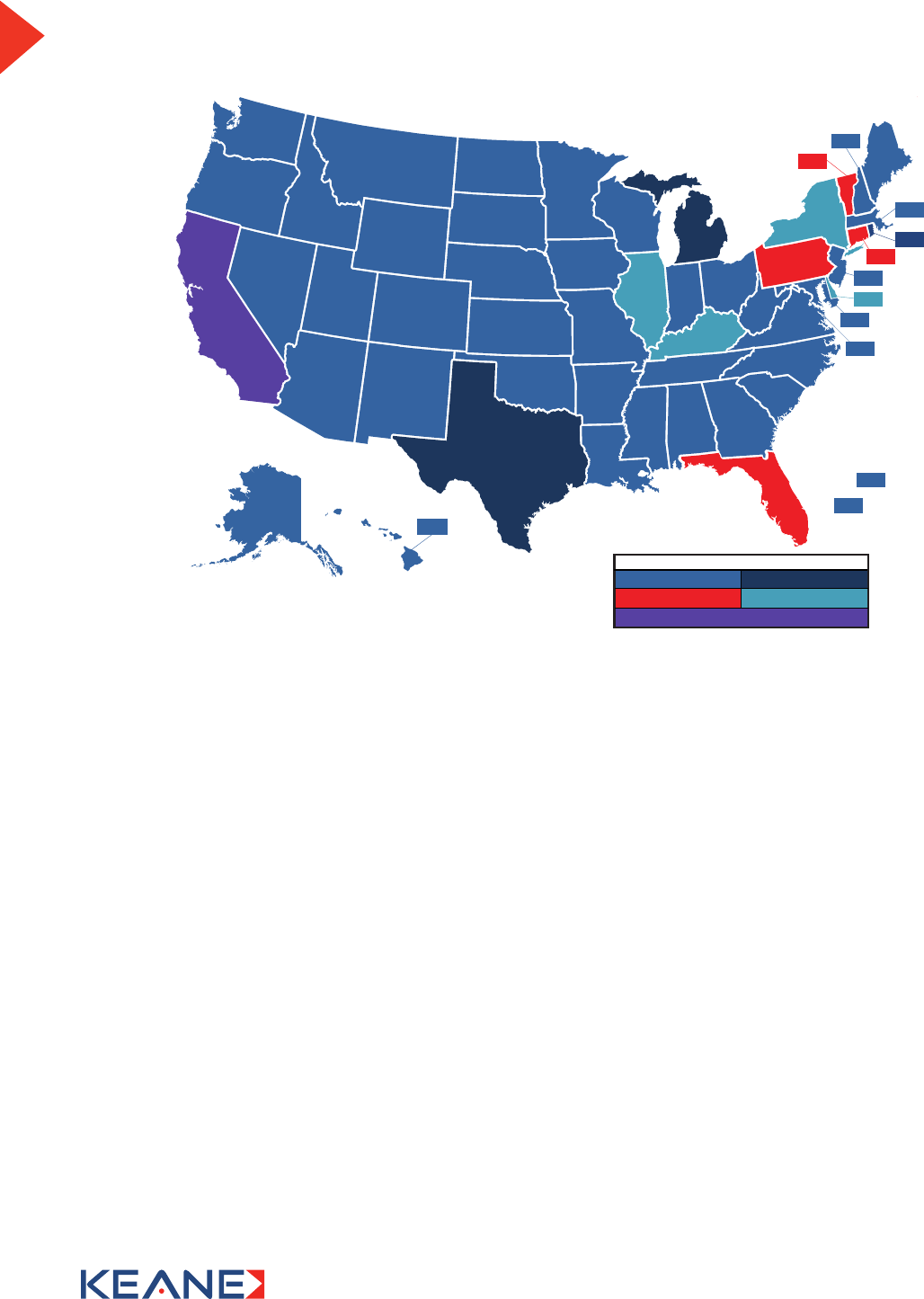

Reporting deadlines vary by industry and sometimes by property type, depending on the state:

WY

MT

ND

SD

ME

NE

MO

IL

OH

VA

NY

VT

RI

MD

MA

HI

NJ

NH

CT

DE

PR

PA

WV

NC

IN

KY

SC

TN

ALMS GA

FL

MI

WI

IA

MN

KS

AR

LA

OK

CO

ID

WA

OR

CA

NV

UT

AZ

NM

AK

TX

Fall: August 10 - December 10

LEGEND

Summer: July 1

DC

VI

Spring: March 1 - May 1 Fall or Spring: By Holder Type

Report: November 1, Remit: June 1-15

*KY: Life & Non-Life Insurance holders to report on April 30; all other

holders report on October 31.

Identifying the media through which the state accepts reports is essential in developing compliant reports

and avoiding state scrutiny. Most states no longer accept paper reports. Instead, they require that reports be

submitted on CD, diskette, or electronically via Internet upload if the number of items to be reported is greater

than a specied threshold. There are some states, like Iowa, Michigan and Tennessee, that require all reports

to be led in this manner regardless of the number of items reported. In addition to the reports, states often

require a specic state-created cover sheet be completed and led. In some instances, states provide this cover

sheet as a part of the online upload process or they publish the cover sheet on their websites and/or as part

of their holder reporting manuals or guides. States that permit reports to be submitted on CD typically require

a particular cover sheet to be included with the physical report delivery. Usually, an appropriate ofce of the

business must sign the cover sheet and in many cases the signature must be notarized.

In some years, a holder may not have any unclaimed property to report to a particular state. Unfortunately,

some unclaimed property laws or regulations require that the holder le a “negative” report if the holder

has no unclaimed property eligible for reporting in a particular report year. States like California and Texas do

not require a negative report and other states, such as Maine, require negative reporting only if the business

is located or incorporated in Maine and have never led an unclaimed property report before or have led a

positive report within the last three years.

Private and Proprietary. Prepared for American Benets Council ©2019 Keane – All rights reserved

5

OTHER CONSIDERATIONS

For the permissive transfer of uncashed checks from ERISA plans into State Unclaimed Property funds, on a

voluntary basis, these additional details should be considered:

• Denition of an uncashed check – how long must it be outstanding before it can be voluntarily escheated?

Would it be a different timeframe for someone with a “bad” mailing address? What if they are deceased?

• States affected – would a plan duciary have the option of only escheating uncashed checks to certain

states?

• Check Amounts – would there be a dollar threshold for reporting? Would plan duciaries be required to

report property under a certain amount “in aggregate” based on that state’s requirement? Could a plan

voluntarily report certain amounts to a state, but not others?

• Frequency – once a plan voluntarily reports property, would there be an expectation to report the same

type of property in subsequent years?

• Due Diligence – is the plan prepared to handle the increased owner communications and check reissuance

requests that will result from the required “due diligence” notice mailings?

• What legislation has passed that has altered state reporting requirements?

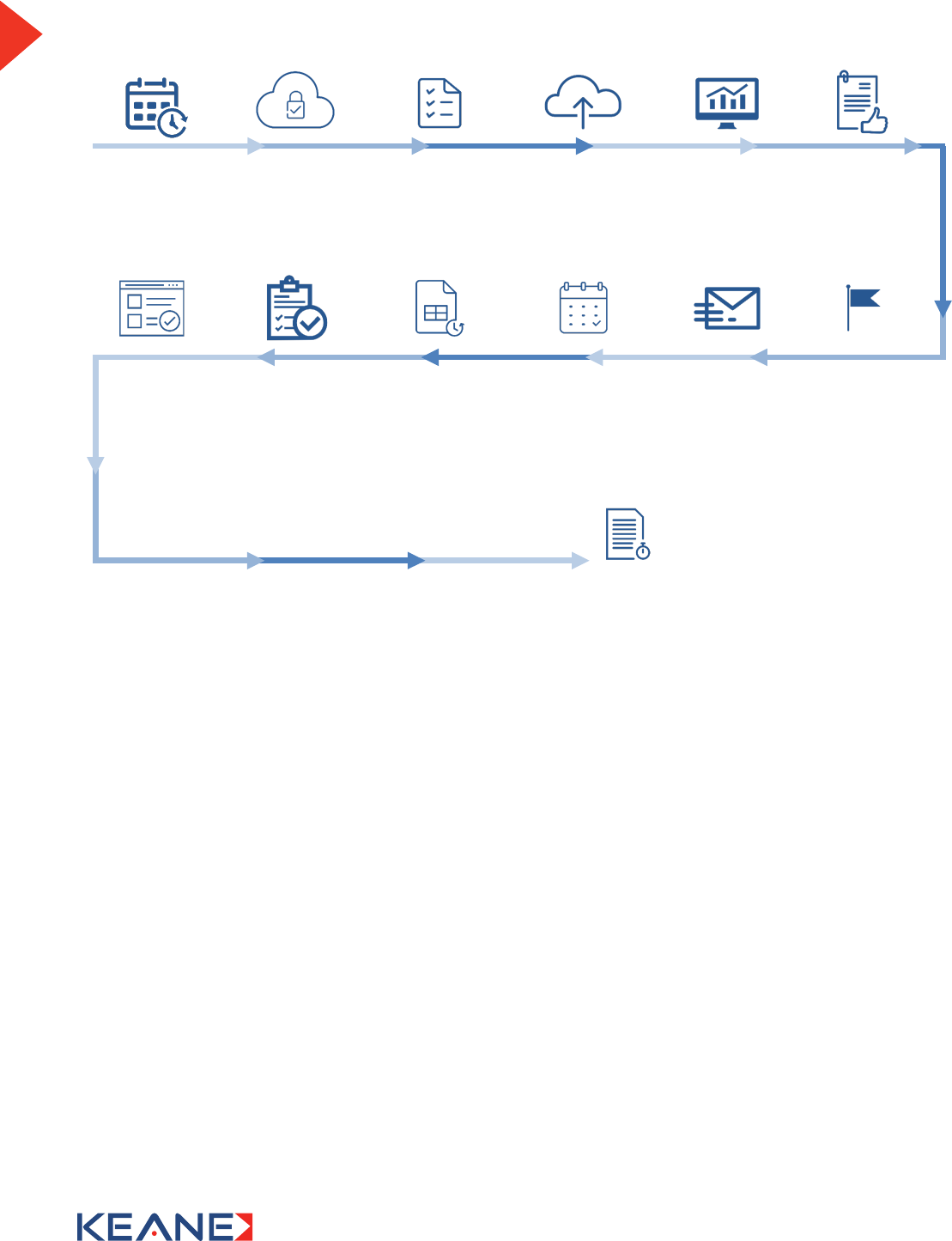

Overview of the Reporting Cycle

Operational Unit

confirms data file

delivery date and

Reporting Unit

provides Operational

Unit with Reporting

Cycle Timeline

Operational Unit

collects full

population of

outstanding

(6 months and prior)

property and uploads

data file via Keane’s

SecureFT portal

Reporting Unit

confirms totals and

data points via the File

Processing Agreement

(FPA)

Reporting Unit uploads

data into proprietary rules

engine & reporting

platform

Reporting Unit

performs liability

analysis on clients

data file

Reporting Unit

flags records

requiring state-

mandated due

diligence mailings

Reporting Unit sends

the Due Diligence

template to the

Operational Unit for

approval

Reporting Unit or

Operational Unit

performs due

diligence mailing

Reporting Unit allows

a 30 day window to

receive due diligence

responses

Reporting Unit provides

the Operational Unit

with a Preliminary

Report which includes

current due property

(DD Responses will be

marked if Reporting Unit

takes the responses)

Operational Unit returns the

Preliminary Report with records

marked for removal and

updated balances (if applicable).

Reporting Unit reconciles the

Preliminary Report and provides

State Totals to be confirmed by

the Operational Unit.

If Reporting Unit Signs & Remits a

funding request will accompany

State Totals

Reporting Unit

Generates Final

Reports for each state

Reporting Unit or Operational Unit

Signs and notarizes Final Reports, cuts remittance checks,

uploads electronic files to individual state websites and

submits Final Reports with CD if applicable to individual states

by the REQUIRED Reporting Deadline Date