WP/16/187

Regulating Local Government Financing Vehicles and

Public-Private Partnerships in China

by Hui Jin and Isabel Rial

© 2016 International Monetary Fund WP/16/187

IMF Working Paper

Fiscal Affairs Department

Regulating Local Government Financing Vehicles and Public-Private Partnerships in China

Prepared by Hui Jin and Isabel Rial

Authorized for distribution by David Coady

September 2016

Abstract

In this paper, we argue that there is much room for China to strengthen its regulatory

framework for public-private partnerships (PPPs). We show that infrastructure projects carried

out through local government financing vehicles (LGFVs) were largely unregulated PPPs, and

significant fiscal risks have already manifested themselves. While PPPs can potentially provide

efficiency gains, they can also be used by governments to circumvent budgetary borrowing

constraints. Therefore, effective PPP regulation is key to delivering PPPs’ benefits while

containing their potential fiscal risks. The authorities have taken concrete steps in order to

establish a sound regulatory framework and foster a new generation of PPPs. However, to

make the framework effective, we highlight a few issues to be resolved. Based on international

best practice, we propose a four-pillar regulatory framework for China, which could be

implemented gradually in three stages.

JEL Classification Numbers: E62, H54, H83

Keywords: fiscal risk, public investment, subnational government

Author’s E-Mail Address: [email protected] ; [email protected]

IMF Working Papers describe research in progress by the author(s) and are published to elicit

comments and to encourage debate. The views expressed in IMF Working Papers are those of the

author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF

management.

3

Contents Page

I. Introduction ..................................................................................................................................................................... 4

II. Background ..................................................................................................................................................................... 4

A. Why are LGFVs a Fiscal Issue? ................................................................................................................. 4

B. How do LGFVs Work?.................................................................................................................................. 5

C. What is the Link between LGFVs and PPPs? ...................................................................................... 7

III. Policy Response and Issues ..................................................................................................................................... 8

A. Policy Response ............................................................................................................................................ 8

B. Issues with the New Measures ................................................................................................................ 9

IV. International Best Practices on PPPs Regulation and Implications for China ................................... 12

A. Good Project Selection ............................................................................................................................ 12

B. Good Institutional Framework .............................................................................................................. 13

C. Good Laws .................................................................................................................................................... 14

D. Good Accounting and Reporting ........................................................................................................ 16

V. A Strategy to Establish a PPP Regulatory Framework in China ............................................................... 17

VI. Concluding Remarks ............................................................................................................................................... 19

References ......................................................................................................................................................................... 31

Tables

1. Selected PPP Regulatory Documents Issued by the Chinese Government Since 2013 .................... 9

2. Comparison of Three Framework Regulatory Documents Issued by the Chinese

Government on Public-Private Partnerships with International Best Practice ................................... 11

3. A Potential Gateway Process for China ............................................................................................................. 13

Figures

1. Government Managed-fund Income from Land Usage Right Transfer in China ................................. 5

2. Local Government Financing Vehicle as the Project Contractor ................................................................ 6

3. Local Government Financing Vehicle as the Project Owner ........................................................................ 6

Appendixes

1. Examples of Local Government Financing Vehicles in China ................................................................... 20

2. A Primer on PPPs ....................................................................................................................................................... 22

3. International Public Sector Accounting Standard 32 (IPSAS 32) ............................................................. 26

4. IMF Proposal of Disclosure Requirements for PPPs and Guarantees .................................................... 29

Appendix Figures

1. Traditional Public Procurement versus Public-Private Partnership ........................................................ 22

2. NPV: Government Procurement versus PPP.................................................................................................... 24

3. IPSAS 32 Illustrative Examples .............................................................................................................................. 28

4

I. INTRODUCTION

The Chinese authorities are actively promoting public-private partnerships (PPPs) as part

of their policy response to risks arising from Local Government Financing Vehicles (LGFVs).

LGFVs were a common “off-budget” solution used by subnational governments (SNGs) in China

to develop infrastructure. The number and size of LGFVs mushroomed in the 2000s and posed

significant fiscal risks. In response to this challenge, the Chinese authorities have relaxed on-

budget SNG borrowing constraints. Moreover, they are actively promoting PPPs and the

corresponding regulatory framework as a new model to develop infrastructure going forward.

This paper reviews the history of LGFVs and PPPs in China and the recently introduced

regulatory framework and makes recommendations for further reform. By comparing LGFVs

and typical PPPs, we would argue that LGFVs were in fact a specific type of unregulated PPPs.

Therefore, the Chinese authorities are effectively promoting a new generation of PPPs with a new

regulatory framework, which is a positive step forward. However, there is still much room to

improve the regulatory framework.

The rest of the paper is organized as follows. Section I provides background information on

LGFVs in China, their links to PPPs and the history. Section II discusses the government policies in

response to fiscal risks arising from LGFVs, as well as some issues with the recent measures.

Based on international experience, Section III proposes a four-pillar PPP regulatory framework.

Section IV translates the framework into a three-stage reform strategy, and Section V concludes.

II. B

ACKGROUND

A. Why are LGFVs a Fiscal Issue?

LGFVs are companies set up and owned by SNGs to finance and implement public

infrastructure projects. According to the budget law before its revision in August 2014

(effective in 2015), SNGs could not borrow “on budget” without central government approval.

Since the late-1990s, SNGs have gradually established LGFVs as a way of borrowing “off budget”

to finance infrastructure projects. Repayment of loans taken by LGFVs was typically financed by

proceeds from the sale of government-owned land near the location of the infrastructure project.

In practice, once infrastructure projects had been completed, land nearby typically appreciated

sharply during the economic boom of the 2000s, which was then sold to repay the debt.

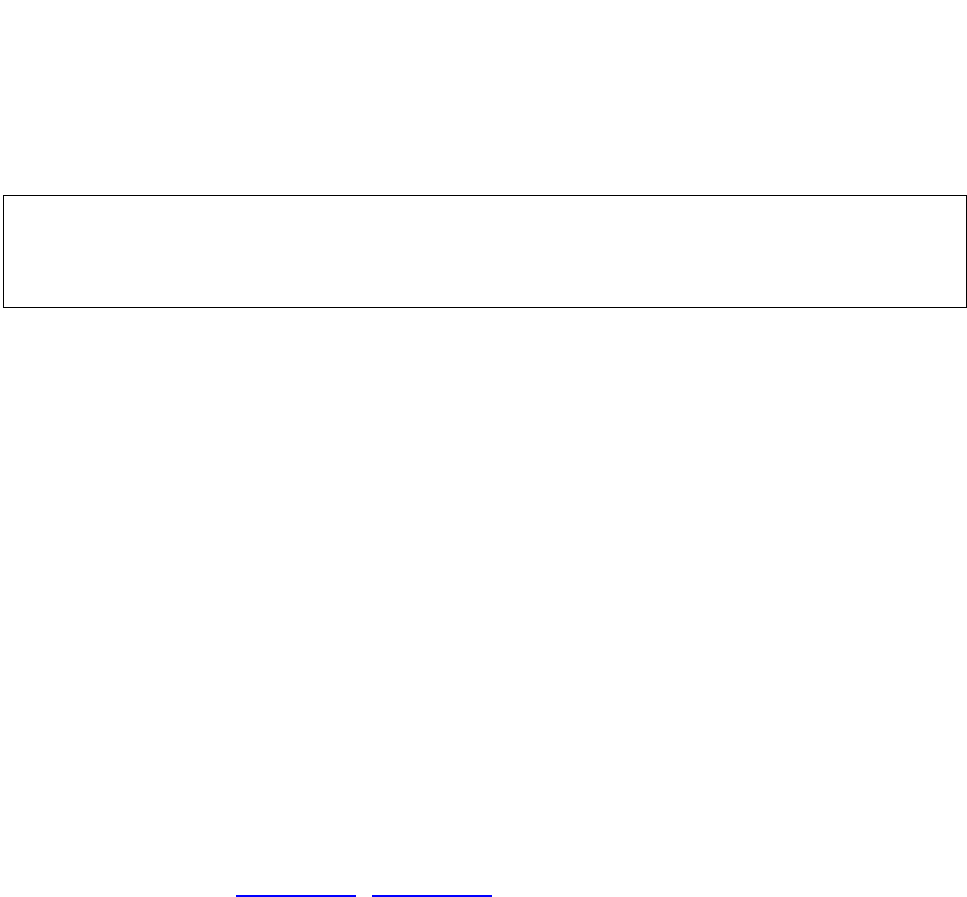

SNG debt—especially that of LGFVs—has posed significant fiscal risks since 2008. The

number and size of LGFVs expanded sharply in the 2008 stimulus package. However, as the

growth of land sale proceeds has slowed down (Figure 1)

1

and not kept up with the increase of

LGFV debt since then, new concerns have arisen about the sustainability of this approach to

financing the expansion of infrastructure. According to a 2013 report issued by the National

1

In China, land is publicly-owned by law. So “selling land” in this paper refers to granting the right of using the

land for several decades (license). According to the IMF GFSM 2014, there is a range of criteria to determine

whether a license represents an asset sale or rent. Based on such criteria we consider that these licenses for the

use of land can be regarded as sales of assets.

(continued)

5

Audit Office (NAO), total LGFV debt stood at 7.0 trillion RMB

2

(13.1 percent of 2012 GDP) as of

end-June 2013. In addition, total local government debt excluding contingent liabilities was

10.9 trillion RMB (20.4 percent of 2012 GDP) at end-June 2013, which increased to 15.4 trillion

RMB at end-2014 (24.2 percent of 2014 GDP). During the same period, total local government

contingent liability increased from 7.0 trillion RMB (12.1 percent of GDP) to 8.6 trillion RMB

(13.5 percent of GDP). Pressure to repay maturing debt is particularly high for highways built by

LGFVs. (NAO 2013a and 2013b, Lou 2015)

Figure 1. Government-Managed Fund Income from Land Usage Right Transfer in China

Source: CEIC China database, IMF staff estimate.

Note: Only proceeds net of resettlement payments to displaced households are available for use. These

payments are estimated to be around 40 percent of land sale proceeds (i.e. income from land usage right

transfer).

B. How do LGFVs Work?

Typically, a LGFV is established as a special purpose vehicle controlled by an SNG. When a

SNG initially sets up a LGFV to construct one or more infrastructure projects, the LGFV typically

has few physical or financial assets. In order to borrow from banks or the bond market, it needs

to meet certain requirements, such as minimum levels of equity and assets, as well as a

reasonable debt-to-equity ratio. Therefore, the SNG usually transfers some of its “high-quality

assets” to the LGFV to improve its creditworthiness. Such “high-quality assets” may include:

(i) public land, which can be sold by the LGFV to raise cash; and (ii) shares of public utilities

companies (e.g., water, sewage, public transportation) owned by the SNG. The land and the cash

flows generated by public utility companies are used as collateral by LGFVs when borrowing to

develop infrastructure. Appendix 1 details some examples of LGFVs.

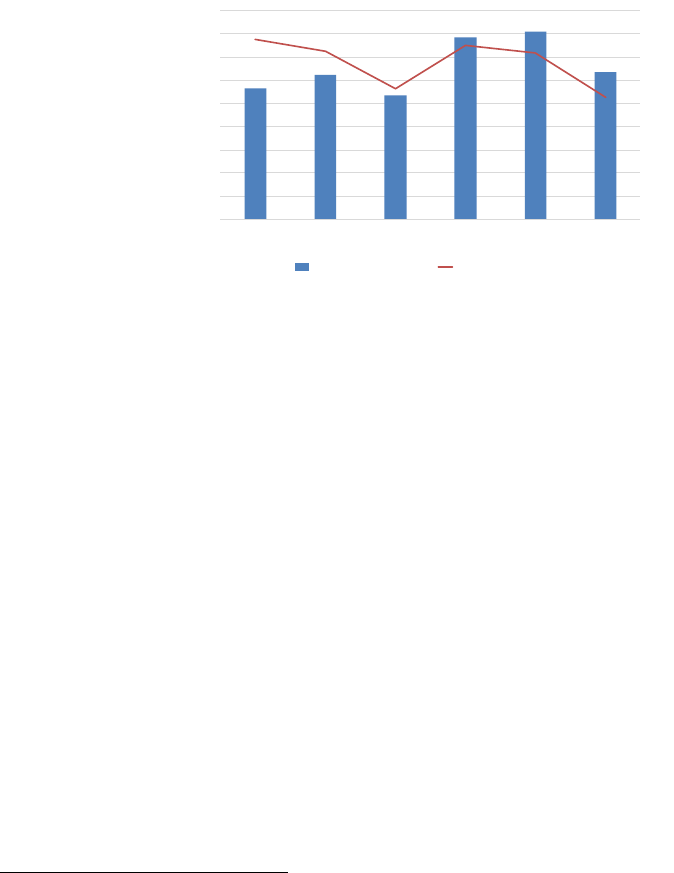

LGFVs can take various roles in an investment project. In some cases, the SNG is regarded as

the project originator

3

and the LGFV takes the role of the project contractor. The SNG signs a

2

The figure includes LGFV debt that is classified by the NAO as contingent liability of the government. Excluding

such contingent liability, LGFV debt that should be repaid by the government stood at 4.1 billion RMB at end-

June 2013.

3

They are called “project owner” in China.

(continued)

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2010 2011 2012 2013 2014 2015 est

In RMB trillions (lhs) In percent of GDP (rhs)

6

contract with the LGFV,

4

which is responsible for building and operating the infrastructure

(Figure 2). In other cases, a LGFV can be the project originator and sign a contract with another

enterprise—private or public—acting as the project contractor. In this case, another special

purpose vehicle is often created for the project (Figure 3). Thus, a web of special purpose vehicles

is created, which ultimately aim at implementing infrastructure projects on behalf of the SNG.

None of these entities, however, were classified as budgetary units in China before 2010.

Therefore, their transactions were not recorded on budget

5

.

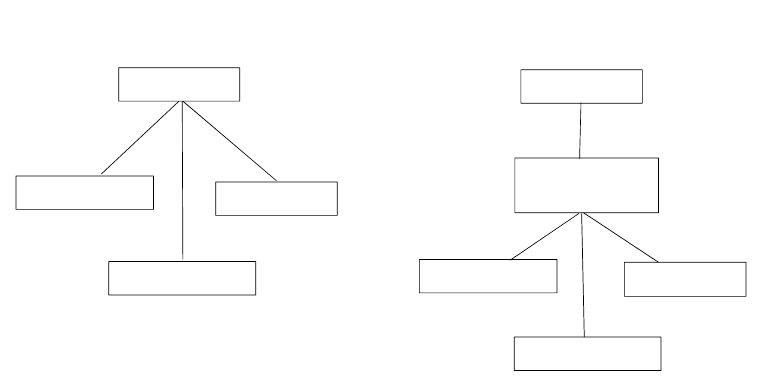

Figure 2. Local Government Financing Vehicle as the Project Contractor

Note: BT is Build-Transfer; BOT is Build-Operate-Transfer.

Figure 3. Local Government Financing Vehicle as the Project Owner

Note: BT is Build-Transfer; BOT is Build-Operate-Transfer.

4

Sometimes there is no clear business contract between an SNG and its LGFV. But in these cases, the LGFV

directly reports to the SNG and carries out projects as instructed.

5

According to the IMF GFSM 2014, a state-owned enterprise like a LGFV should be treated as a general

government unit, if it is a “nonmarket producer”. A nonmarket producer provides all or most of its output to

others for free or at prices that are not economically significant.

Government

(project owner)

Banks or bond

market to provide

financing

Subsidiary 1:

Construction

firm to carry out

the project

LGFV - Special Purpose

Vehicle (project contractor)

Finance

contract

BT or BOT contract

Government

ownership of

LGFV

Subsidiary 2: Shares of

other SOEs transferred

here to enhance LGFV

creditworthiness, such as

land reserve centersand

water companies

Government

Banks or bond

market to provide

financing

LGFV - Special Purpose

Vehicle ( project owner)

Finance contract

for LGFV

Government

ownership of

LGFV

Subsidiaries: Shares of

other SOEs transferred

here to enhance LGFV

creditworthiness, such as

land reserve centers and

water companies

BT or BOT

contract

Project Company - Special

Purpose Vehicle (project

contractor)

Construction company

Banks or bond

market to provide

financing

Finance contract for

the project company

construction

contract

Equity

investor

equity

investment for

the project

company

7

C. What is the Link between LGFVs and PPPs?

PPPs are long-term contracts between the government and a private contractor to build

public infrastructure and provide infrastructure services. In these contracts, the contractor

typically agrees, at its own cost, to build, operate, and maintain an asset in order to provide a

service for which the government remains accountable. In return, the government promises

either to pay for the service or to allow the contractor to collect fees from users. Usually a

special-purpose vehicle is established to run the project. Appendix 2 provides a primer on PPPs,

including their benefits/risks and their comparison with traditional public procurement of public

investment.

By 2010, PPPs had existed in China for two decades with two identifiable generations, with

LGFVs belonging to the second. PPPs in China had taken various contract forms and affected

government finances in different ways.

6

The first generation started in the 1990s, when foreign

companies were the major private-sector players. In the second generation initiated in the 2000s,

state-owned enterprises (SOEs) were the major players, many in the form of LGFVs.

Inadequate risk-sharing arrangements haunted the first generation of PPPs and resulted in

large contract renegotiations. At that time, the limited capacity of subnational authorities,

coupled with more experienced foreign investors, resulted in PPP contracts disproportionately

benefiting the private sector. It was common in this first generation of PPPs for private partners

to charge disproportionally high fees and request fixed or minimum return guarantees. This

situation led the central government to reconsider the economic and social rationale for these

projects. As a result, in 2002, the General Office of the State Council prohibited the practice of

guaranteeing fixed returns for foreign companies at all levels of governments, forcing them to

renegotiate many existing PPP contracts. As a consequence, the participation of foreign

companies in PPPs in China gradually faded away (Wang et al., 2012).

LGFVs can be considered as a specific form of unregulated PPPs of the second generation

for several reasons. First, they were tasked with developing infrastructure projects on behalf of

government for a relatively long period, which went beyond the annual budgetary cycle. Second,

their typical structures as illustrated in Figures 2 and 3 are very similar to a typical PPP structure

with special purpose vehicles (Appendix 2.A). Third, LGFVs were also state-owned enterprises not

subject to regular budget constraints.

There were strong incentives for SNGs to use LGFVs to provide infrastructure off budget.

Given the pre-2015 balanced budget rule which forbade borrowing without central government

approval, SNGs had a strong incentive to develop infrastructure through LGFVs instead of

traditional procurement. This was especially the case before 2010, because SNGs’ firm and

contingent liabilities related to LGFVs projects were typically not disclosed or recorded in their

annual budgets, financial statements, and fiscal statistics. In addition, in a booming economy

with rapidly increasing land prices at that time, LGFVs did not appear to pose major liquidity

6

Many projects were not called PPPs per se. Instead, they were often referred to as “project financing,”

“concessions,” “BT,” “BOT,” “social capital in infrastructure,” etc.

8

issues before 2010. However, fiscal risks from fast-expanding LGFV debt became a major concern

for both market participants and the authorities starting in 2010 (State Council, 2010).

Fiscal risks arising from China’s first and second generations of PPPs warrant more

effective regulation. China’s past history with these PPPs shows that fiscal risks were not

managed satisfactorily ex ante. Therefore, regardless of the labels and formats of contracts or

arrangements, all PPP projects should be subject to a strong regulatory framework. This will allow

the government to strike a balance between infrastructure development and fiscal sustainability.

The following sections will discuss regulatory issues in more detail.

III. P

OLICY RESPONSE AND ISSUES

A. Policy Response

The government has taken various measures to stop the rapid increase of LGFV debt along

three dimensions since 2013. These include (1) overall fiscal management reform; (2) relaxing

SNG fiscal rules and developing the domestic municipal bond market; (3) introducing a new PPP

regulatory framework and promoting a new generation of PPPs.

The 2014 revision of the budget law was key developments along the first and second

dimensions. The revised budget law lifts the prohibition on local government borrowing. The

provincial governments are now allowed to borrow up to a ceiling set by the central government

for capital spending only

7

, including from the domestic municipal bond market. They are also

subject to more information disclosure requirement and fiscal responsibility oversights. In

addition, the law expands the budget coverage, by requiring the inclusion of government-

management funds, state-owned assets, and social security funds in the budget document.

Moreover, LGFVs are prohibited from financing local governments going forward. A three-year

medium-term fiscal framework has also been introduced.

The third dimension, promotion of a new generation of PPPs and a modern regulatory

framework, is expected to serve multiple purposes. The government has publicly stated three

purposes on promoting such PPPs:

8

(1) to accelerate the government’s own reform, which will

reduce the government role in the micro economy but enhance its market regulatory capacity;

(2) to remove red tapes and encourage private capital to provide public service; (3) to improve

fiscal management and the efficiency of budget spending. In particular, it was stated that PPPs

will help mitigate government debt risks, by reducing current-year budgetary spending needs

and distributing public investment financing over different generations.

Accordingly, the government is now actively promoting a third generation of PPPs and its

regulatory framework. Since 2013, the State Council, the National Development and Reform

Commission (NDRC), the Ministry of Finance (MOF), and several line ministries have issued over

40 PPP regulatory documents. A few representative documents were selected in Table 1 below.

Many local governments have also issued their own PPP regulatory documents. In addition, the

7

Such a debt ceiling applies to all borrowing needs of all levels of SNGs within one province.

8

General Office of State Council (2015).

9

MOF introduced 233 pilot PPP projects in 2014-2015, worth about 800 billion RMB. Both the

NDRC and the MOF have created databases for potential PPP projects, covering over 2,000

projects (worth about 3.5 trillion RMB) and 7,700 projects (about 8.8 trillion RMB) by April 2016,

respectively. Also, the MOF and various local governments have created their own PPP units in

order to centralize PPP regulation.

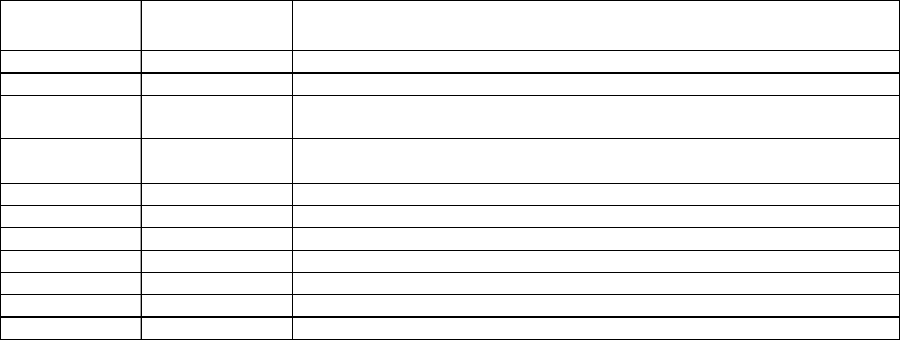

Table 1. Selected PPP Regulatory Documents Issued by the Chinese Government

Since 2013 1/

Notes:

1/ Selected from about 40 PPP-related documents issued by the central government since 2013.

2/ The NDRC and MOF versions of PPP contract guidelines differ in quite a few important areas, which were also

reflected in the two ministries’ respective framework regulatory documents. Also, the targeted government

bodies are different: the NDRC guidelines were issued to development and reform commissions at various local

government levels, while the MOF guidelines were issued to local Bureaus of Finance.

3/ It was issued by NDRC in coordination with MOF, People’s Bank of China and a few line ministries.

B. Issues with the New Measures

The promotion of a third generation of PPPs and its regulatory framework is a positive

step forward. LGFVs were largely unregulated PPPs, therefore transforming some LGFV projects

into regulated PPPs will increase transparency and efficiency. Moreover, using PPPs to improve

government capacity and remove red tapes is particularly beneficial in the Chinese context,

where the government has played a heavy role in economic decisions. Piloting PPP projects

under the new regulatory framework will ensure good practice be tested first and then

expanded.

However, the government should stay vigilant against potential bias in favor of PPPs over

traditional government procurement. It is a common misunderstanding in many countries that

PPPs can reduce government spending needs and government debt. In fact, ceteris paribus, PPPs

only change the timing of government cash flows, not the total net present value (NPV) of

government spending over the lifetime of the project. PPPs also largely change the form of

government liabilities from bank loans or T-bonds to other forms (e.g. commitments to pay the

private partner). Because the time frame of the budget or medium-term fiscal framework is much

shorter than that of PPPs, governments tend to have a bias in favor of PPPs over traditional

Issuance

Authorities

Issuance Date Document Title

State Council

September 26, 2013 Instruction regarding government purchases of service from social sources

State Council

May 19, 2015 Notice of instruction on promoting public-private partnerships in public service

NDRC

December 2, 2014

Instruction regarding carrying out Public-Private Partnerships; Including the NDRC

version of PPP contract guidelines 2/

NDRC and China

Development Bank

March 10, 2015

Notice regarding promotion of development financing to support public-private

partnerships

NDRC et al.

April 25, 2015 Administration method for concession in infrastructure and public works 3/

MOF

November 29, 2014 Operational guidelines for public-private partnerships (pilot)

MOF

December 30, 2014 PPP contract guidelines (pilot) 2/

MOF

December 31, 2014 Government procurement administration method for public-private partnerships

MOF

April 7, 2015 Guidelines for fiscal affordability evaluation in public-private partnerships

MOF

December 18, 2015 Guidelines for Value for Money evaluation in PPP (pilot)

MOF

December 18, 2015 Notice regarding standardization of PPP comprehensive information platforms

10

government procurement. PPPs may or may not be more efficient than traditional government

procurement. Therefore, Value for Money (VfM) should be checked to determine if a project is

more suitable for PPPs or traditional government procurement (Appendix 2.B.).

Moreover, most “private partners” in China are still SOEs, and truly private investors are

hesitant to participate. The official Chinese wording for PPPs can be literally translated as

“government and social capital partnership”. Social capital may cover all forms of firms, whether

owned by the government or not. In fact, in the Chinese context, some SOEs enjoy natural

advantages as private partners of PPPs. First, some construction-related SOEs owned by the

central government or big municipalities (such as Beijing) have gained extensive experience in

providing infrastructure to various local governments and their LGFVs. Second, banks are more

willing to lend to SOEs than truly private companies on the same project. Third and perhaps most

importantly, SOEs are in a much stronger position in potential disputes than truly private

companies. SOEs could resort to their connections within the government to resolve disputes, as

the official ranks of some SOE managers may be equal to or even higher than that of the partner

local government. Private companies may only resort to arbitration, administrative dispute

resolutions or administrative lawsuits. Past experience has shown that private companies’ chance

of winning is not very high. Obviously, a PPP market dominated by SOEs is not ideal, which goes

against the reform goal to grant “the market” (the private sector) a larger role. Therefore, a level

playing field is needed for SOEs and truly private companies to compete for PPPs.

Finally, and perhaps most importantly, the lack of close coordination within the

government has created confusion and uncertainties for private investors. The State

Council, the NDRC, and the MOF have all issued framework documents for PPP regulation since

late 2014. Table 2 below shows that many important regulatory details either differ notably in the

three documents or warrant further clarification. Also, the exact roles of the two powerful

ministries, the NDRC and the MOF, are still unclear for the whole life of PPP projects. In practice,

the NDRC instructs local-governments’ development and reform commissions (local DRCs) to

follow its documents, while the MOF instructs local governments’ bureaus of finance (local BOFs)

to abide by its regulation. Such a fragmented approach may give rise to fiscal risks similar to

those of LGFVs: Many LGFVs’ projects were approved by NDRC or local DRCs, but the fiscal risks

were not checked by MOF or local BOFs. The next section will compare the three framework

documents and other government measures taken so far with international best practice, and

make more detailed recommendations.

11

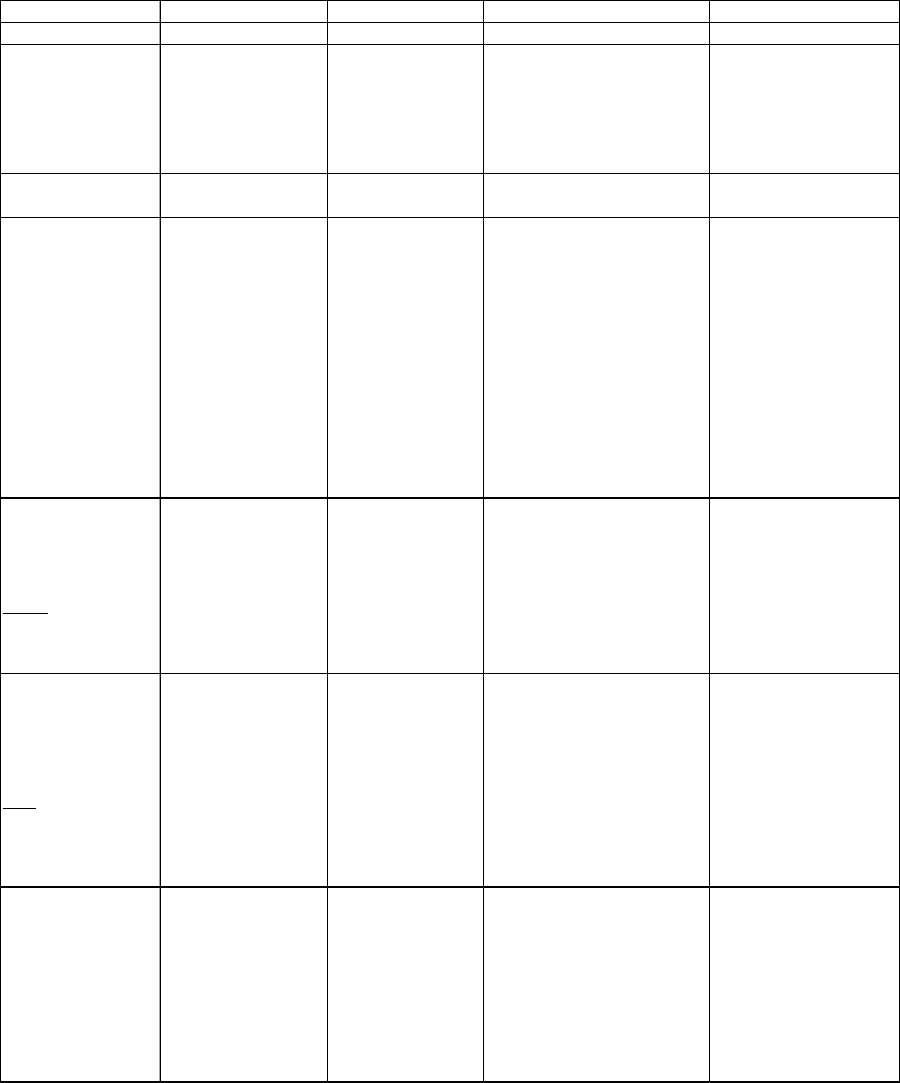

Table 2. Comparison of Three Framework Regulatory Documents Issued by the Chinese

Government on Public-Private Partnerships with International Best Practice

Issuance Authorities

MOF NDRC et al. State Council International Best Practice

Issuance date November 29, 2014 April 25, 2015 May 19, 2015

Document title

Operational guidelines

for public-private

partnerships (pilot)

Administration method

for concession in

infrastructure and

public works

Notice of instruction on

promoting public-private

partnerships in public service

(submitted by MOF, NDRC, PBoC;

approved and forwarded by State

Council General Office)

One single law

Key legal term

public-private

partnerships

concession public-private partnerships One single legal term

Whether LGFVs and

other SOEs qualify as

private partner

LGFVs and other SOEs

owned by the same local

government do not

qualify

Unclear LGFVs do not qualify unless (1)

the firm has been transformed to

be market-oriented; (2) The

government debt it assumed in

the past has been included in the

government budget; (3) The firm

explicitly announces that it will not

assume the role of local

government financing in the

future. LGFVs are prohibited from

assuming local government

financing through minimum return

guarantees etc. in PPPs.

A level playing field should

be provided to SOEs and

private companies that

compete for PPPs. Also, an

SOE's own debt should be

included in the general

government debt statistics,

if it produces goods and

services primarily on a

nonmarket basis.

Whether VfM and

fiscal affordability

should be checked

before

the PPP project

is awarded

Both VfM and fiscally

affordability should be

checked before

government approval;

otherwise the project is

not suitable for PPP.

If the government

needs to provide

availability subsidy or

evaluate VfM, follow

the instruction of MOF.

Fiscal affordability should be

checked. No mentioning of VfM.

Both VfM and fiscal

affordability should be

checked at various stages

before the project is

awarded: pre-feasibility,

feasibility, tendering,

bidding, negotiation and

contract signing.

Whether VfM and

fiscal affordability

should be checked

after

the PPP project

is awarded

Government approval is

needed for contract

revisions, and the

government should

evaluate the project

every 3-5 years.

However, it is unclear if

VfM and fiscal

affordability should be

checked.

The signatories of the

contract should reach

an agreement if the

contract needs

revision, but it is

unclear if VfM and

fiscal affordability

should be checked.

The public and the private

partners should negotiate in case

of disputes, but it is unclear if

VfM and fiscal affordability

should be checked.

Both VfM and fiscal

affordability should be

checked at various stages

after the project is awarded:

regular monitoring; contract

re-negotiation.

Legal instruments to

resolve disputes

The private partner can

resort to arbitration or

file civil lawsuits against

the public partner. The

private partner can file

administrative lawsuits

against government

regulatory decisions.

The concessioner and

the government can

invite expert or third-

party mediation. The

concessioner can file

administrative lawsuits

against specific

administrative

decisions.

Unclear. The applicable laws should

be clarified, and the judges

of the applicable courts

should have enough

expertise to rule on

complicated PPP issues.

12

IV. INTERNATIONAL BEST PRACTICES ON PPPS REGULATION AND IMPLICATIONS FOR CHINA

International best practices suggest four elements for an effective regulatory framework

to manage the fiscal risks from PPPs:

(1) Good project selection. Infrastructure projects for both PPPs and traditional public

investment should be chosen on the basis of cost-benefit analysis. All investment

projects should be integrated into the capital budget cycle, medium-term fiscal

framework, and overall public investment strategy; the MOF should be able to reject

projects that are not fiscally affordable, i.e. reject projects that will jeopardize the

country’s debt sustainability;

(2) Good institutional framework. This should include a dedicated PPP unit or public

investment unit in the MOF to examine the fiscal affordability of projects.

(3) Good laws. This can be achieved with a national PPP framework law or by improving

and harmonizing existing legal frameworks; and

(4) Good accounting and reporting. PPPs should be recorded and reported in a

transparent way in budget documents, financial statements, and public sector statistics.

This framework is consistent with recent works by both the IMF and OECD on managing fiscal

risks and international best practices.

9

The main features of the framework vis-a-vis the measures

taken so far in China are discussed as follows.

A. Good Project Selection

PPPs should be integrated into the government’s capital budget cycle, medium-term fiscal

framework, and overall public investment strategy. In all cases, PPP projects should not be

allowed to move forward outside the regular budget process applied to other investment

projects. This implies three steps in the decision-making process:

In the first step, the government decides whether a project is worthwhile from an

economic and social perspective. The project is evaluated in the context of national

priorities using standard project appraisal techniques (e.g. cost-benefit analysis). And it is

included in the government’s overall investment planning framework, medium-term fiscal

framework, and budget cycle

.

In the second step, the government decides whether a project that went through the first

step should be implemented as traditional public procurement or as a PPP. This decision

should be based on which method provides better “value for money (VfM)”—i.e, which

method provides high-quality infrastructure services at a lower cost over the long run.

In the third step, if a PPP is considered the better procurement option for the project, it

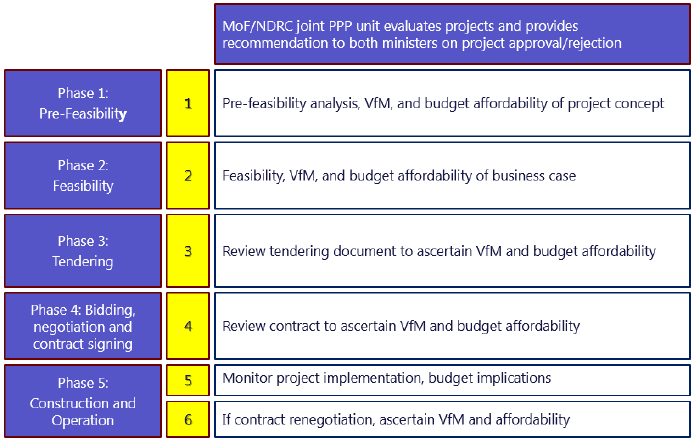

should follow a “gateway process” (Table 3). The latter is a due-diligence process under

9

Hemming et al. (2006), Schwartz et al. (2008), IMF (2012), OECD (2012), Cangiano et al. (2013).

13

which a PPP project can be stopped or suspended at any point in time during its lifecycle,

if it is not deemed fiscally affordable or is regarded as too risky.

In China, clarification of NDRC and MOF’s respective roles in the whole life of PPPs is

paramount. Currently, the NDRC and local DRCs are responsible for approving infrastructure

projects based on existing national priority, feasibility studies, and administrative requirements.

This seems similar to the first step above and presumably applies to both traditional government

procurement and PPPs. The NDRC framework document does not require the checking fiscal

affordability or VfM for each PPP project; rather, it refers to MOF instructions “if the government

needs to provide availability subsidy or evaluate VfM”. The MOF framework document requires

the checking of both VfM and fiscal affordability before government approval of the project, but

it is unclear if they should also be checked at later stages. The State Council document requires

checking fiscal affordability but not VfM. Ideally, China could follow the above three steps by

clarifying the roles of NDRC and MOF, and ensure VfM and fiscal affordability are checked at

each important gateway. Also, potential PPP projects above certain thresholds could be

consolidated into a single national PPP pipeline, which should be consistent with national

priorities stated in the 13th Five-Year Plan.

Table 3. A Potential Gateway Process for China

B. Good Institutional Framework

Effective management of the fiscal risks from PPPs requires a strong institutional

framework. International experience suggests that a dedicated PPP unit (or public investment

unit) can be helpful, preferably in the MOF. Such a unit could carry out technical work to evaluate

the fiscal risks of PPPs and control the gateway process. As of 2009, a dedicated PPP unit had

been set up in over half (17) of all OECD member countries, of which at least 11 such units reside

in the MOF (OECD 2010). This allows the MOF to ensure that investment projects are affordable.

However, other typical functions of PPP/investment units, such as the promotion of PPPs to

attract private sector participation and technical advisory functions, can reside in other entities—

e.g. other ministries, SNGs—as long as the MOF retains affordability and risk oversight.

14

In China’s context, a national PPP unit is necessary to ensure close coordination between

the NDRC and the MOF. The MOF has established a PPP unit (called PPP center) in 2014, which

is generally consistent with common international practice. However, given the important role of

the NDRC in public investment, the PPP unit certainly needs to coordinate daily with the NDRC

on individual projects. Or, the PPP unit could be expanded by inviting NDRC representatives and

possibly other line ministries to make itself a “one-stop shop” for any PPP regulatory issues. In

the latter case, the MOF and the NDRC are jointly responsible for the gateway process (Table

3)

10

. Moreover, the national PPP unit will need to coordinate with the People’s Bank of China

(PBoC) and the China Banking Regulatory Commission (CBRC) since: (1) the major state-owned

banks are the key creditors of LGFVs/PPPs, and they hold significant levels of PPP risk; and

(2) sound collaboration between the fiscal arm of the government and the monetary authorities

would bolster the generation of high-quality fiscal and debt statistics. The same principles on

DRC-BOF coordination could also apply to PPP units already established at the SNG level.

Moreover, post-contractual regulation and audits need to be strengthened significantly.

The focus of the current regulation has been project selection and appraisal before the contract

is signed. However, the regulatory framework and institutional arrangement still lack details for

the post-contractual phase (i.e. after the contract is signed but before the contract ends). As

more projects become operational in the next few years, risks might emerge without appropriate

regulation. In particular, any form of renegotiation between the public partner and the private

partner, including ad-hoc price adjustments and changes of financing models, should be

approved by the PPP unit at the appropriate level. Similarly, the audit offices at the national and

subnational levels could also be actively involved in post-contractual audits and ex-post audits

(i.e. after the contract ends) of PPPs.

C. Good Laws

Countries have implemented diverse legal arrangements on PPPs. These range from PPP

framework laws to sector regulations. For example, Brazil, France, Korea, and South Africa have

passed PPP framework laws, while Australia and the United Kingdom have dedicated national

regulatory guidelines. In most countries, PPPs are only governed by fragmented low-level sector

regulations or even the contracts themselves.

PPPs governed by framework laws are generally more successful in reducing fiscal costs

and risks.

11

Fiscal risks often materialize in renegotiations, particularly when circumstances

change but neither the contract nor the low-level sector regulation provides clear risk

assignments. Therefore, a PPP framework law will provide the best legal clarification to reduce

fiscal costs and risks, as well as legal assurances for potential private investors in infrastructure.

10

The example of gateway process is based on the South Africa and Australia, State of Victoria case, which are

considered international best practices. The recommendation of a joint MOF/NDRC PPP unit to control the

gateway process is one option for setting up a similar institutional framework in China.

11

Guasch (2004).

15

Best international practice suggest that a PPP framework law should address seven key

areas:

(1) Clearly define PPPs and their scope (i.e., in terms of level of governments and sectors

of the economy to be covered);

(2) Fully promote the integration of PPPs with the government’s overall investment

strategy and budgetary process;

(3) Clearly assign roles and responsibilities between the various public and private entities

typically involved in PPP operations. The role of the MOF as the gatekeeper of public

finances should be clearly described in the law;

(4) Set and/or require transparent mechanisms for competitive bidding processes;

(5) Provide explicit guidelines for renegotiation and termination of PPP contracts,

including dispute resolution mechanisms;

(6) Establish limits/ceilings on aggregate public sector exposure to PPPs as well as

contract renegotiation; and

(7) Specify transparent accounting, reporting, and auditing procedures in line with

international standards.

In China, the three PPP framework documents certainly need to be consolidated into a

single high-level PPP regulatory document to reduce confusion and uncertainties. In

particular, the respective scopes of “concession” and “PPP” need to be clarified. Generally

speaking, concessions are in fact user-funded PPPs, and therefore the concept of PPP is more

comprehensive. Regardless of the exact label of a project, it should be covered by the single

document as long as it involves a long-term contract between the government and a private

contractor to build infrastructure and provide services. Also, whether disputes in PPPs should

resort to civil laws or administrative laws are important in the Chinese context. Civil laws

generally put both public and private partners on an equal footing as business counterparts,

which may encourage more private sector participation in infrastructure. Administrative laws

generally treat the public partner as the authorities answering to specific requests of the private

sector, as the current relationship stands. In most countries, such disputes are governed by civil

laws. In any case, the applicable laws need to be clarified, and the judges of the applicable courts

should have enough expertise to rule on complicated PPP issues. Finally, transparent mechanisms

for competitive bidding processes will significantly improve governance, because projects were

assigned by the SNGs to the LGFVs mostly in a noncompetitive fashion

12

.

The consolidated high-level document could be developed into a PPP framework law at a

later stage. The State Council could first issue the consolidated PPP regulatory document. Once

experience is gained after several years under these regulations, a revised version could be

submitted to the National People’s Congress (NPC) to become the formal PPP law. It is crucial

12

Many of these important elements may have implications for other laws or legal practices in China, which

might need to be addressed in a broader legal reform in China.

16

that future PPP regulations are kept consistent with the revised budget law, to ensure

appropriate budget coverage and maximum disclosure of information.

D. Good Accounting and Reporting

Standards and practices on PPPs vary across countries, but recent international standards

are in line with the best practices. Many countries have not established national accounting

and reporting standards for PPPs, while others’ practices can be considered more advanced in

monitoring all PPPs, including user-funded projects. For example, Australia and Canada record

most PPPs on the government balance sheet. France accounts for government-funded PPPs in

the government balance sheet, while it reports data on user-funded PPPs in complementary

budget documents. These best practices are consistent with the recently approved international

standards: For accounting purposes, International Public Sector Accounting Standards 32 (IPSAS

32); for reporting purposes, the IMF’s Government Finance Statistics Manual 2014 (GFSM 2014)

and the 2011 Guide on Public Sector Debt Statistics (PSDS 2011). These standards are all accrual-

based.

The adoption of IPSAS 32, GFSM 2014, and PSDS 2011 should lead, in practice, to most

PPPs being treated on-budget (Funke et al., 2013). For example, according to IPSAS 32, projects

undertaken in the form of a PPP should be considered public, and therefore affect the main fiscal

aggregates, as long as the government controls or regulates what services, to whom, at what

price the services are provided. Otherwise, the project carries out a commercial activity, and

should be recorded differently. As a result, the incentive to pursue PPPs as a way to circumvent

budgetary restrictions and/or debt limits would be minimized. This is because debt and the

overall deficit would increase, regardless of whether the infrastructure is procured through PPPs

or traditional public procurement.

13

This would be a major improvement in government

reporting, where most PPPs are currently treated as off-budget. Appendix 3 provides further

details on the fiscal implications of the implementation of IPSAS 32. The IMF and the World Bank

have also jointly developed the PPP Fiscal Risk Assessment Model (PFRAM) to assess fiscal risks

from individual PPP projects based on IPSAS 32.

As in many other emerging economies, China’s government accounting is cash based

which tends to underestimate fiscal risks from PPPs. The discrepancy between cash and

accrual accounting of PPPs can be substantial, particularly at early stages of the project cycle. In

principle, cash-based systems do not require that expenditures or debt be recorded at early

stages of the PPP project cycle, when the private partner, instead of the government, spends

cash to construct the project. This can result in an underestimation of the medium and long-term

impact of PPPs (Appendix 2.B).

However, it should be stressed that transition from cash to accrual standards will take

time, which necessitates a gradual approach in China. Applying IPSAS 32 will most likely be a

13

In China’s context, government liabilities will increase regardless whether the project will be procured through

PPPs or traditional public procurements, as long as the government controls or regulates what services, to whom,

at what price. Also in this case, government liabilities will increase regardless whether the private partner is an

SOE or a truly private company.

17

long-term process for China, because the standard needs to be tailored to the country’s specific

circumstances. Its implications on headline fiscal indicators should be carefully evaluated,

particularly in the context of existing fiscal rules. Also, the coverage needs to be as broad as

possible to monitor all PPPs. Finally, such a reform needs to aim at improving fiscal transparency

and management of fiscal risks while ensuring budget affordability and macro-fiscal

sustainability. All these will require significant efforts to reform current information systems and

to develop internal capacity to handle them. In addition, the move to accrual accounting need to

be appropriately sequenced with other public financial management reforms.

As a start of the long-term transition process, China could first disclose new projects in the

budget. For example, the contract value and long term implications of new PPP projects could

be first disclosed in complementary budget documents. This could include cash spending and

other commitments beyond the timeframe of the medium-term fiscal framework. When

government capacity improves, the NPV of total government assets and liabilities arising from

individual PPP projects could also be disclosed, following international standards such as IPSAS

32. As more and more projects are disclosed in this way, a partial government balance sheet

could be gradually compiled. Appendix 4 describes a suggested proposal of disclosure

requirements for PPPs and guarantees.

With the above disclosure requirement, PPP ceilings could be imposed to complement

formal fiscal rules in China. Fiscal rules are common across countries, which typically include

ceilings on debt, deficit, and/or spending. In China, SNGs essentially had an explicit fiscal rule of

“no borrowing without central government approval” before 2015; now the provincial

governments are subject to debt ceilings set by the central government. However, fiscal rules can

be easily circumvented by PPPs, particularly in countries with cash-based accounting systems and

limited coverage of headline fiscal indicators. In China, SNGs used LGFVs to circumvent

borrowing prohibition in the past, and they still have strong incentives to use PPPs to circumvent

the recently imposed debt ceilings. To contain fiscal risks, some countries have introduced

ceilings/limits for overall government exposure to PPPs, which complement existing debt

ceilings. Potential PPP ceilings for SNGs in China could be the following:

PPP contract value over current revenue ratio (excluding land sale proceeds) or over GDP

ratio.

PPP debt over current revenue or GDP ratio.

Government commitments in PPPs over current revenue or GDP ratio.

V. A

STRATEGY TO ESTABLISH A PPP REGULATORY FRAMEWORK IN CHINA

Based on the four-pillar framework described above, we propose a three-stage strategy for

gradually implementing a new regulatory scheme for PPPs. It should be noted from the

outset that careful policy sequencing is crucial. For that reason, our proposal distinguishes

actions to be taken in the near, medium, and long-term. The authorities in fact have made

notable progress in the “near-term” stage of our proposed strategy, but more work is needed to

ensure the effectiveness of the regulatory framework. Following the reform tradition in China, our

18

proposed strategy starts at the central government level and gradually expands to the SNG level,

once capacity has been strengthened.

In the near term (1-2 years), the central government could aim to:

Classify and disclose existing LGFV projects and new PPPs as part of the budget

documents. The MOF has classified SNG debt identified by the 2013 NAO report into

three types: (1) general obligations, (2) obligations arising from specific revenue-

generating projects, and (3) debt converted to company debt through PPPs. In addition,

the MOF documents require the disclosure of government commitments in PPPs in the

government’s comprehensive fiscal report, when such a reporting system is ready.

However, to mitigate fiscal risks, converting LGFVs to PPPs cannot be limited to

“relabeling” or “reclassification”; rather, more effective regulation is the key, with steps

recommended in detail below.

Evaluating the introduction of ceilings/limits for PPPs at the central and subnational

government level. In addition to the newly introduced SNG debt ceilings, the MOF could

discuss with SNGs potential PPP ceilings, taking into consideration their current

outstanding debt, infrastructure needs, and economic growth prospects.

Gradually introducing PPP regulations in line with the seven key areas discussed above.

Progress has been made since 2013, with over 40 regulatory documents issued by central

government entities. However, consolidation of these documents, especially the three

framework documents into a single framework document, is urgently needed to reduce

confusion and uncertainties.

14

Improving the coordination between MOF, NDRC, PBoC, CBRC over LGFVs and other PPP

issues. This is of paramount importance at the current stage.

In the medium term (2–5 years), the following key elements of an effective regulatory

framework could gradually take shape:

A consolidated PPP regulatory document could be issued by the State Council. Any new

central government or SNG PPP projects should follow the national PPP regulation and

be integrated into the normal budgetary process. They are subject to the scrutiny of the

corresponding people’s congress.

The PPP unit in the MOF could be expanded into a national PPP/public investment unit

as a “one-stop shop” for all PPP regulatory issues. As noted earlier, the PPP unit could

include representatives of NDRC and line ministries, and coordinate with PBoC and CBRC.

The unit could oversee fiscal risks of all major PPP projects above a certain threshold,

regardless of the level of government. To avoid the possibility of having too many small

projects to circumvent the threshold, key documents of projects below the threshold

14

A notice issued jointly by the MOF and the NDRC on My 28, 2016 called for more coordination on PPPs

between BOFs and DRCs at the subnational level, which is a positive step forward. But the three framework

documents have yet to be consolidated.

19

should be submitted to the unit for monitoring purposes. By consolidating the two PPP

contract guidelines already issued by the MOF and NDRC (Table 1), the unit would also

develop standardized contracts as well as detailed procedures and methodologies for

selecting, evaluating, and approving PPP projects. At this point, SNGs could outsource

the evaluation of main PPP/investment projects to the national unit, while capacities are

being developed at the subnational level.

PPP ceilings could be enforced at both central and subnational government levels. The

enforcement of PPP ceilings for SNGs would be supervised by both the central

government and the subnational people’s congress.

Reporting of PPP transactions could be gradually improved in line with international

standards and the plan of statistical improvement.

In the longer term (5-10 years), an effective regulatory framework would be fully

developed in accordance with international best practice:

After 5-10 years of experience, the consolidated PPP regulatory document could be

upgraded into a PPP framework law passed by the NPC.

Monitoring PPP projects would become a regular part of the annual budget and the

medium-term fiscal framework of all levels of the government.

The national PPP/public investment unit would be able to effectively oversee fiscal risks

of major projects, while provincial PPP/public investment units would oversee smaller

projects within a consistent oversight framework.

Information about PPP projects and their fiscal impact in the near-, medium-, and long-

term would be regularly disclosed in detail to the public in budget documents.

VI. C

ONCLUDING REMARKS

This paper has shown that there is still much room to strengthen the PPP regulatory

framework in China. The increase in local government debt through LGFVs — essentially a

specific form of unregulated PPPs — points to major regulatory weakness in this area. The

government’s recent promotion of a third generation of PPPs and its regulatory framework is a

welcome development. However, a few key issues need to be resolved. These include vigilance

against government bias in favor of PPPs, providing a level playing field for SOEs and truly

private companies to compete for PPPs, and improving coordination within the government (in

particularly between the MOF and the NDRC). Also, all the framework regulatory documents

need to be consolidated to remove confusion and uncertainties. We propose a four-pillar

regulatory framework that promotes good project selection, good institutional framework, good

laws and good accounting and reporting practices. Our proposal can help improve the current

Chinese framework in a three-step strategy, in order to ensure a balance between promoting

infrastructure and containing fiscal risks.

20

Appendix 1. Examples of Local Government Financing Vehicles in China

15

City C’s example

City C is a major city in Western China. City C set up its LGFV in 1993 to finance infrastructure

projects, manage state-owned infrastructure assets, and manage land on behalf of the

government of City C. The LGFV is fully owned by the state-owned enterprise committee of the

government.

As of end-2007, the LGFV had nine subsidiaries. Three subsidiaries were fully owned by the

LGFV: (1) City C Chengtou Real Estate Development Company, (2) City C Chengtou Road and

Bridge Management Company, and (3) City C Hengcheng Investment Company. The other six

subsidiaries were majority controlled by the LGFV: (4) City C Development Company, (5) City C

QJZB Airport Company, (6) City C South District Construction Investment Company, (7) City C

Jiashiheng Construction and Development Company, (8) City C Pufeng Construction Engineering

Company, and (9) City C Renewable Energy Development Company.

The core business of the LGFV covers the following four areas in City C: (1) infrastructure

construction, (2) road and bridge maintenance and management, (3) real estate development,

and (4) land reserves and management. On behalf of the government of City C, the LGFV can

improve a piece of land allocated to it and then submit to the government to sell the land.

Proceeds from land sales can be used to repay loans for infrastructure projects.

The LGFV issued a bond in 2008 to partly finance six infrastructure projects. One project

was to renovate an old district and the other five were all road and bridge construction projects

for modern transportation. There was no collateral for the bond. The issuer and bond were rated

AA+ and AAA, respectively, by a rating agency based in Shanghai.

City H’s example

City H is a medium-sized city in central China. City H established its LGFV in 1999. In 2002, the

government of City H transferred three public utilities companies to be the subsidiaries of the

LGFV: City H Public Transportation Company, City H Water Company, and City H Sewage

Company. In 2006, the government transferred another three companies to be the LGFV

subsidiaries: City H Investment Company, City H Local Railway Company, and City H High

Technology Development Company. In the same year, City H’s land reserve center was also

transferred to the LGFV. In 2008, some other “high-quality assets” were given to the LGFV. The

LGFV is fully owned by the state-owned enterprise committee of the government of City H.

The core business of the LGFV covered the following four areas in City H: (1) infrastructure

construction, (2) public utilities, (3) land development and management, and (4) management of

state-owned assets.

15

Based on disclosure documents published in China Securities Newspaper for LGFVs in City C, City H and City S

before they issued corporate bonds.

21

In 2009, the LGFV issued a bond to partly finance seven infrastructure projects: two water

pipeline projects, two sewage projects, two road construction projects, and an environmental

project for lakes.

The creditworthiness of the bond was enhanced by two measures: (1) The LGFV had

previously signed build-transfer (BT) contracts with the government of City H and expected to

receive payments in the next few years. Such future BT payments were put up as collateral for the

bond; and (2) another company provided a guarantee for the bond. The guarantor is a steel

company in City D (in the same province as City H), which is fully owned by the provincial

government. The issuer and the bond were rated AA- and AA+, respectively, by a rating agency

based in Beijing.

City S’s example

City S is a fairly large city in northern China. City S established its LGFV in 2005. From 2005 to

2008, City S government transferred three public utilities companies to the LGFV: City S Sewage

Company, City S Water Company, and City S Public Transportation Company. In December 2009,

the LGFV established four new subsidiaries: City S Chengtou Engineering Detection Company,

City S Chengtou Engineering Consulting Company, and City S Chengtou Construction and

Development Company, and City S Chengtou Pipeline Construction Company. The LGFV is fully

owned by the Construction Bureau of the City S government.

In early 2011, the LGFV issued a bond to partly finance two projects: a bridge and a road.

Funds to repay the bond will come from the LGFV’s “ordinary business” and possibly sales of

certain assets. There was no collateral for the bond. The issuer and the bond were both rated

AA+ by a rating agency based in Beijing.

22

Appendix 2. A Primer on PPPs

Part A: Benefits and Risks of PPPs

What are PPPs? PPPs are long-term contracts between the government and a private contractor

in which the contractor agrees, at its own cost, to build, operate, and maintain an asset in order

to provide a service for which the government remains accountable; in return the government

promises either to pay for the service or to allow the contractor to collect fees from users. Usually

a special-purpose vehicle (SPV) is established to run the project (see Appendix Figure 1 for the

comparison between a traditional public procurement project and a typical PPP structure). In

practice, there may be more layers of subcontractors and more SPVs involved. The time horizon

of a long-term contract goes beyond the regular government budgetary exercise, which obliges

the government to make financial payments and/or commitment outside its annual budget and

medium-term fiscal framework (if there is any). The PPP projects are ultimately government-

funded (e.g. through availability payments, revenue guarantees), user-funded (e.g. through

highway tolls), or a combination of both.

Appendix Figure 1. Traditional Public Procurement versus Public-Private Partnership

Compared to traditional public procurement, the main benefit of PPPs is potential

efficiency gains. This is because the private partners focus on cost-effectiveness through the

introduction of better technology, innovation and know-how, as well as improved accountability,

transparency, and competition. However, the efficiency gains from PPPs could be offset by the

typically higher borrowing costs faced by the private sector, as well as the significantly higher

transaction costs of PPPs. Empirical analyses suggest that whether or not PPPs have achieved

their efficiency objectives in practice remains an open question (IMF 2007).

A common misperception about PPPs often results in a government bias in favor of PPPs

over traditional procurement. The private partner in fact provides a “bridge-loan” style of

financing to the government in PPPs. Therefore, the government may be relieved temporarily

from cash drains when infrastructure projects are being constructed. From the perspective of

cash-based government budget, PPPs may seem to allow for infrastructure “off-budget” and “for

Government

Government

Operating firm

Banks

Construction firm

Operating firm

Banks

Construction firm

PPP-- Special

Purpose Vehicle

Traditional Public Procurement Public Private Partnership

Operating contract

Finance contract

Construction contract

Operating contract

Finance contract

Construction contract

Long-term service

contract

23

free” in the short term. Such a misperception results in a common government bias in favor of

PPPs. Many governments even set up PPPs to take advantage of the feature and circumvent

budget constraints. However, ceteris paribus, PPPs only change the timing of government cash

spending, but not the total net present value (Part B below).

Large fiscal costs and fiscal risk have arisen from PPPs in both developing and advanced

countries. Both traditional procurement and PPPs share common project risks, such as

construction and demand risks. However, the above government bias and possible manipulation

of PPPs add an important layer to the common project risks. An inadequate budgetary and/or

statistical treatment may allow governments to ignore the impact of PPPs on public debt and

deficit. In practice, governments often end up bearing more fiscal costs and risks than expected

in the medium and longer term. Here are some examples:

Mexico in mid 1990s. The government undertook an ambitious program of private toll

road concessions in the early 1990s. Most concessionaires soon ran into financial

difficulties due to both cost overruns and traffic shortfalls. In 1997, the government

eventually took over the private concessions and assumed about US$7.7 billion in debt.

Hungary in late 1990s. The M1 highway was built using PPPs, but the traffic forecasts

turned out to be too optimistic. There was a strong diversion of traffic to a toll-free

parallel road. The project was eventually nationalized with the government fully assuming

the traffic risk.

Portugal in early 2000s. Most of the highway system was built using PPPs by a

government agency outside the central government. For example, Estradas de Portugal

was regarded as a state-owned enterprise and thus excluded from the coverage

monitored by the European standards. The highway system was over-built resulting in

many highways with insufficient traffic, which make them not profitable. In the

aftermaths of the 2009 global financial crisis, the fiscal risks materialized. Following the

agreement between the Eurostat and the Portuguese authorities in 2011, Estradas de

Portugal was reclassified as part of the central government. The government took over

many of these PPPs, adding to its deficit and debt by a large amount.

Spain in early 2000s. Several local airports and railways were built by local governments

using PPPs. The projects were financed through local banks (“cajas”), reportedly at times

facilitated by political interests. Traffic demand was largely overestimated, resulting in

insufficient revenues that cannot even cover maintenance costs. By late 2000s, many of

these airports and railway lines were closed shortly after their completion. However, local

governments had to continue to honor their long-term commitments with the private

sector, in many cases financed through transfers from the central government.

24

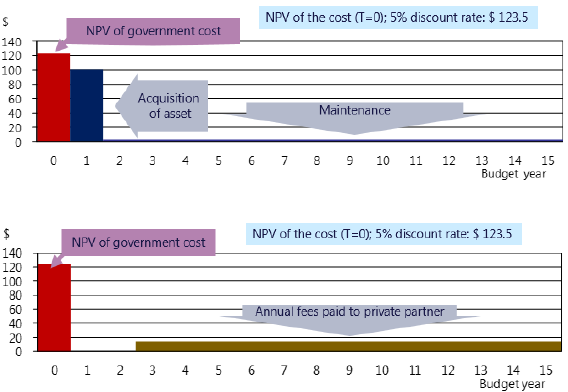

Part B: Government Procurement versus PPP: A Simple Model of Cash Flows

A simple model can illustrate that ceteris paribus PPPs only change the timing of

government cash flows, but not the total net present value (NPV). First, assume a non-toll

road will be constructed and operated through government procurement. The government will

spend $100 to construct the road in Year 1 and $3 each year during Year 2 to 15 to maintain the

road. Using a discount rate of 5 percent, the NPV of total government commitment in Year 0 is

$123.5. Then, assume the same project is carried out as a government-funded PPP. A private

company will spend $100 to construct the road in Year 1 and then spend $3 each year during

Year 2 to 15. However, the government will compensate the company with an annual fee from

Year 3 to Year 15. If there is no efficiency difference, no company profit, no borrowing costs,

NPVs of government commitment using both methods should be exactly the same. That is, both

NPVs will be $123.5, and the annual fee paid by the government to the company will be

$14.5 per year. Therefore, under these assumptions, procuring through a PPP only changes the

timing of government cash outflows, not the total NPV of government commitment, if the PPP is

equally efficient as traditional procurement. See Appendix Figure 2 below.

Appendix Figure 2. NPV: Government Procurement versus PPP

NPV of Government Cost in Government Procurement

NPV of Government Cost in PPP

What if the road can charge user fees? NPVs are still the same. In the government

procurement, the government will receive the user fees as its revenue. Therefore, the

government procurement NPV will decrease. In the PPP, the company will receive user fees. Thus,

it will charge the government lower annual fees and reduce the PPP NPV by the same amount.

What if the government and the company need to borrow to build the road? NPVs are still

the same. The government procurement NPV will increase by the interest costs. In the PPP, the

company will charge the government higher annual fees to cover its own interest costs.

Assuming the interests paid by the government and the company are the same, both NPVs

increase to the same level.

25

Can there be efficiency gains? Yes, but it depends. If the company is more efficient than the

government, then the PPP NPV should be lower than that of the government procurement.

However, some other factors may offset such efficiency gains and push the PPP NPV upward.

This includes company profits, typically higher company interest costs and PPP transaction costs.

Therefore, a value-for-money analysis is needed to determine which method is more efficient.

What is the implication for cash-based budget decision? Government will have a bias in

favor of PPPs. When a government prepares a cash-based annual budget for Year 1, it will show

a very high cash expense with the government procurement ($100 to construct the road).

However, it shows no cash expense at all with a PPP. Because most government budgets

(including China’s) are cash based, this results in a bias in favor of PPPs. However, ceteris paribus,

PPPs do not change the total NPV of the government, which can only be captured by accrual-

based accounting rules such as IPSAS 32.

26

Appendix 3. International Public Sector Accounting Standard 32

International Public Sector Accounting Standard 32 (IPSAS 32) is the current international

public sector accounting standards for PPPs. Its formal name is “Service Concession

Arrangements: Grantor”, which was released by the International Public Sector Accounting

Standards Board (IPSASB) in October 2011. It is compatible with IFRIC 12, “Service Concession

Arrangements”, which is the corresponding international accounting standard for the private-

sector companies (operator). Both standards are accrual based.

IPSAS 32 covers both government-funded and user-funded PPP contracts. A service

concession arrangement (PPP contract) is a binding arrangement between a grantor (the

government) and an operator (private sector contractor): (a) The operator uses the service

concession asset to provide a public service on behalf of the grantor for a specified period of

time; and (b) The operator is compensated for its services over the period of the service

concession arrangement. Thus, both government-funded and user-funded PPP contracts, as

defined in Appendix 2, are covered by this standard.

IPSAS 32 requires that the assets of a PPP and the corresponding liabilities be recorded on

the grantor (government)’s balance sheet if the following conditions are met:

(a) The grantor controls or regulates what services the operator must provide with the asset, to

whom it must provide them, and at what price; and

(b) The grantor controls—through ownership, beneficial entitlement or otherwise—any

significant residual interest in the asset at the end of the term of the arrangement.

In addition, for an asset used in a service concession arrangement for its entire useful life (a

“whole-of-life” asset), only the conditions in paragraph (a) need to be met.

For a government-funded project (financial liability model), IPSAS specifies the following

accounting treatments. Initially, the grantor (government) records the same amount of asset

and liability at the fair value. Then, the grantor accounts the following as expenses: asset

depreciation (consumption of fixed capital), finance charge (interests), charges for services paid

to the operator. The grantor accounts as financing reduction in liability (repayment of principal).

For a user-funded project (grant of a right to the operator model), IPSAS specifies

different accounting treatments. Initially, the grantor (government) records the same amount

of asset and liability at the fair value. Then, the grantor accounts only one expense: asset

depreciation. Most importantly, the grantor records the revenue accrued during the contract

period. And the grantor accounts as financing reduction in liability, which is equivalent to the

accrued revenue in each year.

What if a project is funded by the combination of the government and the users? IPSAS

requires that it be divided into a government-funded part and a user-funded part. The above

accounting rules are then applied to each part, respectively.

27

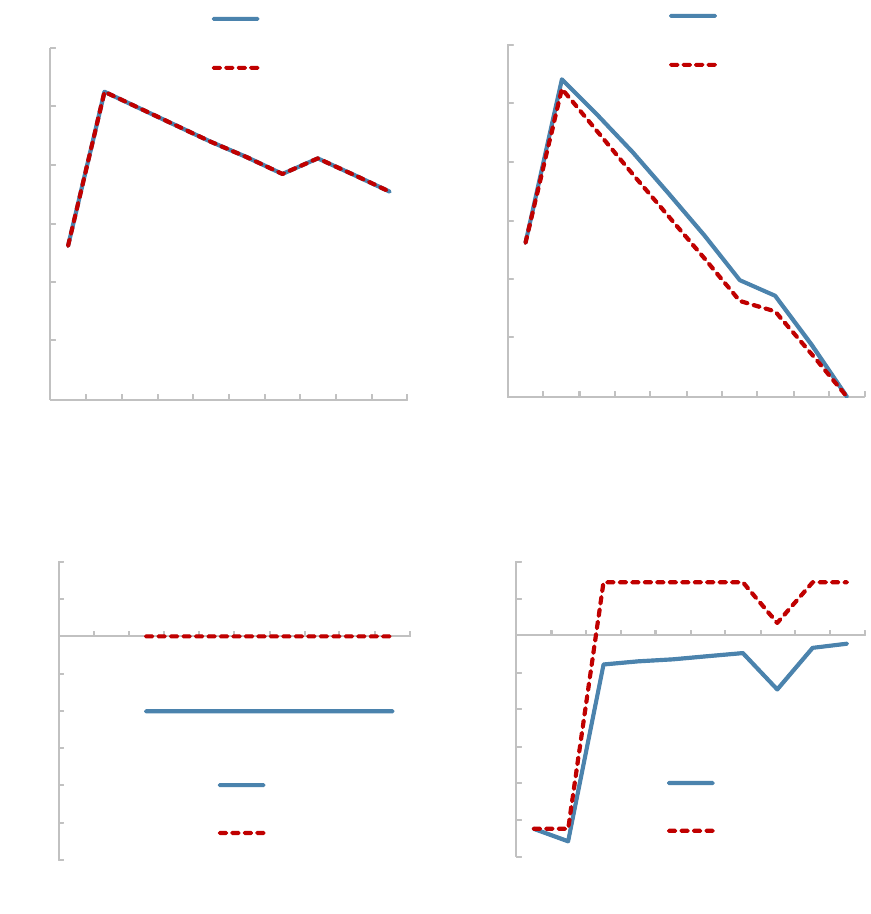

IPSAS 32 provides an illustration example. The example is to build a road through a build-

operate-transfer (BOT) contract. The contract lasts for 10 years, during which the road will be

constructed in the first 2 years, and the private-sector company will operate the road for the

remaining 8 years. The cost of constructing the road base and the surface is $940 and $110,

respectively. The usable life of the base and the surface is 25 years and 6 years, respectively. This

means that in year 8, the surface will be re-constructed. There are two approaches of financing

the project through PPPs: (1) Government-funded: the government pays the operator $200 per

year during years 3-10. (2) User-funded: the government allows the operator to charge users

$200 per year during years 3-10.

The major accounting items of the IPSAS 32 examples are illustrated in Appendix Figure 3.

In the top-left chart, government nonfinancial assets are recorded identical in both user-funded

and government-funded PPPs. In the top-right chart, government liabilities are broadly similar in

both cases, with the only difference arising from the different treatment of interest and

amortization. Government liability in user-funded PPP is only slightly lower, because it does not

incur interest cost. In the bottom-left chart, there are no cash flows in user-funded PPP, while

government-funded PPP requires cash payments by the government to the private partner. In

the bottom-right chart, total government net lending/borrowing (i.e., the overall surplus/deficit

on an accrual basis) in user-funded PPP is higher due to the imputation of accrued revenue (i.e.,

revenue is imputed as if the government collects the user fees directly and use these fees to

repay the private partner).

According to IPSAS 32, PPPs should be recorded similarly to traditional government

procurement, which will reduce the government bias in favor of PPPs. The assets and