LoanCare, LLC, Virginia Beach, VA

Ginnie Mae Program

Office of Audit, Region 7

Kansas City, MO

Audit Report Number: 2015-KC-1012

September 30, 2015

To: Michael Drayne, Senior Vice President, Office of Issuer and Portfolio

Management,TS

//signed//

From: Ronald J. Hosking, Regional Inspector General for Audit, 7AGA

Subject: LoanCare Did Not Always File Claims for Foreclosed-Upon Properties Held on

Behalf of Ginnie Mae and Convey Them to FHA in a Timely Manner

Attached is the U.S. Department of Housing and Urban Development (HUD), Office of Inspector

General’s (OIG) final results of our review of LoanCare’s master subservicer responsibilities

related to foreclosed-upon properties held on behalf of the Government National Mortgage

Association (Ginnie Mae).

HUD Handbook 2000.06, REV-4, sets specific timeframes for management decisions on

recommended corrective actions. For each recommendation without a management decision,

please respond and provide status reports in accordance with the HUD Handbook. Please furnish

us copies of any correspondence or directives issued because of the audit.

The Inspector General Act, Title 5 United States Code, section 8M, requires that OIG post its

publicly available reports on the OIG Web site. Accordingly, this report will be posted at

http://www.hudoig.gov.

If you have any questions or comments about this report, please do not hesitate to call me at

913-551-5870.

Highlights

What We Audited and Why

We audited LoanCare, LLC, because of concerns that the Government National Mortgage

Association’s (Ginnie Mae) single-family master subservicers did not file claims with the

Federal Housing Administration (FHA) for foreclosed-upon properties in a timely manner. Our

audit objective was to determine whether LoanCare conveyed foreclosed-upon properties held on

behalf of Ginnie Mae, filed claims with FHA, and remitted the funds to Ginnie Mae on time.

What We Found

LoanCare did not always convey properties to FHA, file claims with FHA, or remit claim funds

to Ginnie Mae on time. It did not always (1) convey foreclosed-upon properties to FHA within

30 days of acquiring possession and title, (2) file the part B portion

1

of its conveyance claim

within 45 days of the date the deed was filed for record or within 15 days of the title approval

letter date, and (3) remit FHA claim funds to Ginnie Mae within 2 business days. As a result,

FHA’s insurance fund was subjected to additional costs, and Ginnie Mae was unable to recover

its costs on time.

What We Recommend

We recommend that Ginnie Mae require LoanCare to repay any additional costs associated with

the violations noted.

1

Servicers file claims with FHA on form HUD-27011, Single-Family Application for Insurance Benefits. The

claim form has two parts: Part A: General Information and Part B: Fiscal Data.

Audit Report Number: 2015-KC-1012

Date: September 30, 2015

LoanCare Did Not Always File Claims for Foreclosed-Upon Properties Held

on Behalf of Ginnie Mae and Convey Them to FHA in a Timely Manner

2

Table of Contents

Background and Objective ...................................................................................... 3

Results of Audit ........................................................................................................ 4

Finding 1: LoanCare Did Not Always Take Timely Actions on Foreclosed-Upon

Properties Held on Behalf of Ginnie Mae ....................................................................... 4

Scope and Methodology ........................................................................................... 7

Internal Controls ...................................................................................................... 8

Appendixes ................................................................................................................ 9

A. Auditee Comments and OIG’s Evaluation ............................................................... 9

B. File Review Summaries ........................................................................................... 17

3

Background and Objective

LoanCare is a nonsupervised mortgage company approved to operate by the U.S. Department of

Housing and Urban Development (HUD) since May 27, 1986. It is headquartered in Virginia

Beach, VA, and is a Government National Mortgage Association (Ginnie Mae) authorized issuer

of mortgage-backed securities. It was contracted with Ginnie Mae to be a single-family master

subservicer from 2009 until 2014, when its contract expired. As a Ginnie Mae single-family

master subservicer, its duties included providing services in connection with issuer defaults and

servicing current, delinquent, and defaulted loans, including foreclosure services, management

and disposition of acquired properties, and preparation and submission of insurance or guarantee

claims to the Federal Housing Administration (FHA), U.S. Department of Agriculture Rural

Development (RD), U.S. Department of Veterans Affairs (VA), and HUD’s Office of Public and

Indian Housing (PIH). Specifically, LoanCare was required to service the mortgages or the

installment loan contracts in accordance with relevant agency regulations, its contract with

Ginnie Mae, and the Ginnie Mae Mortgage-Backed Securities (MBS) Guide.

Ginnie Mae is a unique program in that it uses the explicit full faith and credit guarantee of the

U.S. Government to back its mortgage-backed securities. Ginnie Mae is authorized by Title III

of the National Housing Act, as amended, to guarantee the timely payment of principal and

interest on securities that are issued by approved entities and which are backed by FHA, VA,

RD, or PIH mortgages. It does not make or purchase mortgage loans, nor does it buy, sell, or

issue securities. Instead, private lending institutions approved by Ginnie Mae originate eligible

government loans, pool them into securities, and issue mortgage-backed securities. Ginnie Mae,

in turn, guarantees the performance of the lenders that issue the securities and that continue to

service and manage the underlying loans.

When a Ginnie Mae-approved issuer defaults, Ginnie Mae steps into the role of the issuer and

makes the timely pass-through payments to investors and then assumes the servicing rights and

obligations of the issuer’s entire Ginnie Mae-guaranteed pooled loan portfolio of mortgage-

backed securities using its master subservicer.

Our objective was to determine whether LoanCare conveyed foreclosed-upon properties held on

behalf of Ginnie Mae, filed claims with FHA, and remitted the funds to Ginnie Mae on time.

4

Results of Audit

Finding 1: LoanCare Did Not Always Take Timely Actions on

Foreclosed-Upon Properties Held on Behalf of Ginnie Mae

LoanCare did not always convey properties to FHA, file claims with FHA, or remit claim funds

to Ginnie Mae on time for 10 loans reviewed. It believed that the delays were justified and

beyond its control, and it did not understand that such delays were allowable only if it received

an extension from FHA. As a result, FHA’s insurance fund was subjected to additional costs,

and Ginnie Mae was unable to recover its costs on time.

Delayed Actions

LoanCare did not always convey foreclosed-upon properties to FHA, file claims with FHA, and

remit claim funds to Ginnie Mae on time. The table below breaks down these deficiencies.

Post-foreclosure Delays

Untimely actions Number of properties with delays

Conveying property to FHA 6 of 6

Filing part B claim with FHA 5 of 6

Remitting funds to Ginnie Mae 4 of 5

Ten loans were reviewed, but not all aspects could be evaluated for each loan. See appendix B

for further details.

Delayed Conveyance

LoanCare did not always convey foreclosed-upon properties to FHA on time. Regulations at 24

CFR 203.359 require servicers to convey properties to FHA within 30 days of acquiring

possession and title. Possession is defined as when the property is vacant. LoanCare conveyed

five of the properties reviewed between 91 and 370 days after it took possession of them. It did

not convey a sixth property, instead transferring it to a new master subservicer 59 days after

acquiring possession.

In addition, LoanCare did not always remove personal property from foreclosed-upon homes

within the 30-day timeframe. HUD Handbook 4330.4, paragraph 2-2(D)(4), states that the

servicer must act promptly to ensure that all personal property has been removed within 30 days

after acquiring title and possession.

For example, on one loan, LoanCare completed the removal of personal property 140 days after

it acquired possession and conveyed the property on day 268.

5

Delayed Filing of Part B of the Claim

LoanCare did not always file the part B portion of its conveyance claim within the required

timeframe. HUD Handbook 4330.4, paragraph 2-2(H), states that the servicer must submit part

B of form HUD-27011 to FHA within 45 days of the date the deed is filed for record or submit it

within 15 calendar days of the approval letter received date, whichever is later. LoanCare filed

part B of the conveyance claim for two of the loans reviewed between 51 and 55 days after the

deed was recorded or approval letter received date. It did not file part B for three additional

properties, instead transferring them to a new master subservicer after the 45 days had passed.

Delayed Remittance of Funds

LoanCare did not always remit FHA claim funds to Ginnie Mae on time. Its contract with

Ginnie Mae required it to remit all claim funds received by the second business day following

receipt of the funds. LoanCare did not meet this requirement for four of the five loans reviewed,

remitting funds on the third to fifth business days.

Misunderstood Requirements for Delays

LoanCare believed that the delays were justified and beyond its control, and it did not understand

that such delays were allowable only if it received an extension from FHA. During the audit,

LoanCare noted that the delays in conveying the properties and filing claims were justified and

beyond its control because in many cases, the properties needed repairs before they would be in

conveyance condition and also the records needed to file the claims were often difficult to obtain.

LoanCare had inherited these loans from defaulted issuers so it had not been responsible for the

loans during all of the servicing. In several cases, property condition issues prevented timely

conveyance. However, these reasons did not fully account for the delays and in several cases,

damages or title defects occurred after the conveyance deadline. For example, in one case,

LoanCare identified roof damage 14 days after it took possession of the property but failed to

convey it for a full year. LoanCare did not understand that to exceed the established timeframes,

it needed to request and receive an extension of time from FHA. It did not request an extension

for any of the sampled items as it believed that once the prior servicer had missed the initial

deadline to file for foreclosure, an extension request was not necessary since interest was already

being curtailed. However, HUD Handbook 4330.4, section 2-3, states that if the servicer cannot

comply with the time requirements for a particular action because of circumstances beyond its

control, it should submit a form HUD-50012 to FHA to request an extension of time.

Financial Impact

As a result of LoanCare’s noncompliance, the FHA fund was subjected to additional costs, and

Ginnie Mae was unable to recover its costs on time.

The delays in conveyance caused the FHA insurance fund to pay out more claim funds for

property preservation costs, such as lawn maintenance, repairs, and inspections, as well as hazard

insurance costs and property taxes.

Also, Ginnie Mae advanced funds to LoanCare to reimburse it for property preservation costs

and the costs of eviction and repairs. When LoanCare did not convey the properties to FHA

promptly, Ginnie Mae had to continue advancing funds for property preservation costs during the

delay. Further, the delays in filing the part B claims and remitting claim funds to Ginnie Mae

resulted in Ginnie Mae’s carrying these costs longer than necessary before receiving

6

reimbursement. Ginnie Mae’s liquid assets were reduced until it could recover the costs from

FHA’s insurance fund, and it missed out on potential interest from the delayed remittances.

Conclusion

LoanCare did not take prompt actions on foreclosed-upon properties it serviced for Ginnie Mae.

These delays negatively impacted FHA’s insurance fund because of extra outflows. They also

affected Ginnie Mae due to delays in receiving claim funds and lost interest. Because LoanCare

is no longer contracted by Ginnie Mae to perform this function, we are not recommending that

Ginnie Mae require it to receive training or change its practices. However, Ginnie Mae should

require LoanCare to return any funds that it was not entitled to receive for servicing the sampled

loans.

Recommendation

We recommend that Ginnie Mae

1A. Require LoanCare to repay any additional costs associated with the violations noted.

7

Scope and Methodology

Our audit period generally covered October 1, 2013, through September 30, 2014. We

performed our audit work from May through September 2015. We conducted onsite work at

LoanCare’s home office located at 3637 Sentara Way, Virginia Beach, VA.

To accomplish our objective, we

Reviewed the Code of Federal Regulations and HUD handbooks;

Reviewed the contract between Ginnie Mae and LoanCare;

Reviewed LoanCare’s audited financial statements;

Reviewed relevant documents in the loan files, such as inspection reports, claim

packages, reconveyance notices, case chronologies, and other legal documents;

Reviewed information in Neighborhood Watch, a HUD system designed to provide

comprehensive data for tracking the performance of loans originated, underwritten, and

serviced by FHA-approved lenders;

Reviewed claim remittances; and

Interviewed LoanCare and HUD employees.

We selected a sample of 10 loans for review. This was a sample of five properties conveyed to

HUD and five properties transferred to another master subservicer, Selene Finance. For loans

that were conveyed to HUD, we determined the number of days between when the foreclosure

sale was completed and the date the property was conveyed to HUD. We then selected the five

properties that had the greatest number of days between the foreclosure sale completion date and

the conveyance to HUD date, which ranged between 882 and 1,491 days for the five loans

selected. For loans that were transferred to Selene Finance, we determined the number of days

between when the foreclosure sale was completed and the date the property was transferred to

Selene Finance. We then selected the five properties that had the greatest number of days

between the foreclosure sale completion date and the transfer to Selene Finance date, which

ranged between 1,178 and 1,851 days for the five loans selected. The conclusions reached on the

sampled items cannot be projected due to the selection method used.

We used LoanCare’s information system to identify properties that were conveyed to HUD and

those that were transferred to Selene Finance, as well as the time between the foreclosure sale

completion and the conveyance or transfer. We used this information to select our sample and

relied upon it for background information only as all of our conclusions were based on our

review of original source documents.

We conducted the audit in accordance with generally accepted government auditing standards.

Those standards require that we plan and perform the audit to obtain sufficient, appropriate

evidence to provide a reasonable basis for our findings and conclusions based on our audit

objective(s). We believe that the evidence obtained provides a reasonable basis for our findings

and conclusions based on our audit objective.

8

Internal Controls

Internal control is a process adopted by those charged with governance and management,

designed to provide reasonable assurance about the achievement of the organization’s mission,

goals, and objectives with regard to

Effectiveness and efficiency of operations,

Reliability of financial reporting, and

Compliance with applicable laws and regulations.

Internal controls comprise the plans, policies, methods, and procedures used to meet the

organization’s mission, goals, and objectives. Internal controls include the processes and

procedures for planning, organizing, directing, and controlling program operations as well as the

systems for measuring, reporting, and monitoring program performance.

Relevant Internal Controls

We determined that the following internal controls were relevant to our audit objective:

Controls to ensure that all foreclosed-upon properties were conveyed to HUD within the

required timelines after the foreclosure sales and evictions were completed.

We did not assess the relevant controls identified above because of the limited scope of the audit.

9

Appendixes

Appendix A

Auditee Comments and OIG’s Evaluation

Auditee Comments

Ref to OIG

Evaluation

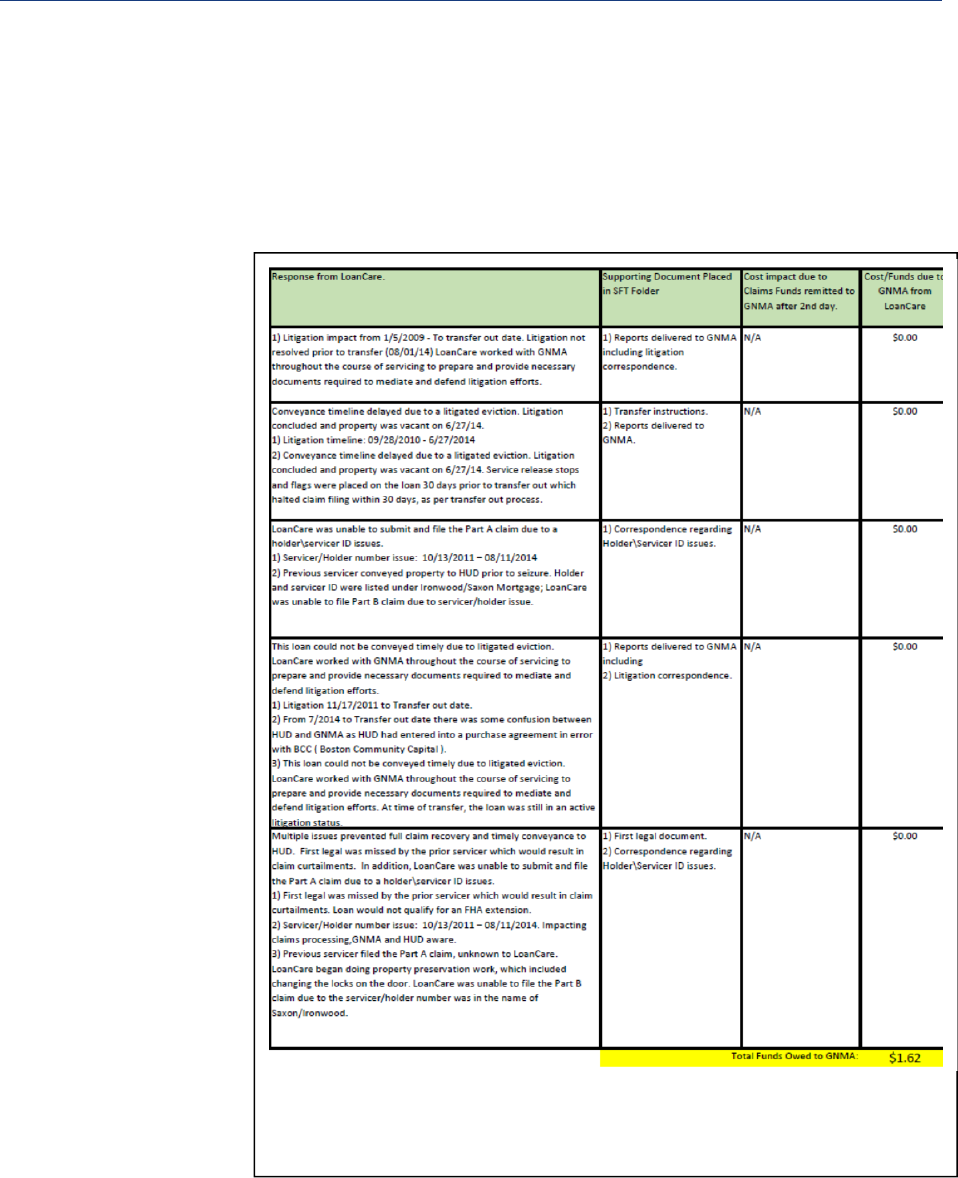

Comment 1

10

Auditee Comments and OIG’s Evaluation

Auditee Comments

Ref to OIG

Evaluation

Comment 2

11

Auditee Comments and OIG’s Evaluation

Auditee Comments

Ref to OIG

Evaluation

Comment 5

12

Auditee Comments and OIG’s Evaluation

Auditee Comments

Ref to OIG

Evaluation

Comment 3

( Loan 1)

Comment 4

( Loan 2)

13

Auditee Comments and OIG’s Evaluation

Auditee Comments

Ref to OIG

Evaluation

Comment 5

( Loan 3)

Comment 6

( Loan 4)

Comment 7

( Loan 5)

14

Auditee Comments and OIG’s Evaluation

Auditee Comments

Ref to OIG

Evaluation

Comment 8

( Loan 6)

Comment 9

( Loan 7)

Comment 10

( Loan 8)

Comment 8

( Loan 9)

Comment 10

( Loan 10)

Comment 11

15

OIG Evaluation of Auditee Comments

Comment 1 Our audit objective was to determine whether LoanCare conveyed foreclosed-

upon properties held on behalf of Ginnie Mae, filed claims with FHA, and

remitted the funds to Ginnie Mae on time. This involved verifying that LoanCare

was in compliance with all of HUD’s regulations as well as its contract. It is not

sufficient to just notify Ginnie Mae and HUD about servicing issues but LoanCare

also had to comply with the regulations involving timely conveyance and claim

filing.

Comment 2 The audit focused on the conveyance and claim timelines after the foreclosure

sales were completed, any legal challenges in eviction were resolved, and

LoanCare had possession and title to the properties. Therefore the “robo signing”

issues and foreclosure delays were before the part of the process our audit was

concerned with and were not relevant to LoanCare’s ability to convey the

properties after it had possession.

Comment 3 LoanCare did not provide any documentation to show that HUD would not grant

an extension for the delayed conveyance or to show any attempt to obtain an

extension of the conveyance timelines for loan 1. We have amended the table in

appendix B to show that HUD received the part B claim within 8 days of title

approval and revised the report with the addition of HUD criteria allowing for the

part B claim to be filed up to 15 days after HUD approves the title.

Comment 4 For loan 2, LoanCare conveyed the property 144 days after it obtained possession,

well beyond the 30-day limit. The title issue did not delay the conveyance as

HUD was the one that discovered the issue after the conveyance.

Comment 5 For loan 3, LoanCare obtained possession when the property was vacated in July

2012. LoanCare had contact with the former principal of Ironwood (Smaller) in

January 2013, after which he deeded the property to another company. LoanCare

was not aware of the title issues until May 2013, about two weeks after it

conveyed the property in April 2013. LoanCare should have conveyed the

property in August 2012, well before any title issues arose.

Comment 6 Based on the information provided for loan 4, we recalculated the number of days

that LoanCare took to file the claim from 116 to 51. We updated the table in

Appendix B to show the corrected number of days. However, LoanCare was still

late in filing the claim.

Comment 7 For loan 5, LoanCare’s property preservation records show that the property was

vacant and the locks changed on 06/06/2013 and therefore they should have

conveyed it by 07/06/2013. Its records show that the property was vandalized

after the required conveyance date.

16

Comment 8 Our report did not include any findings for missed timeframes for these loans

(loans 6 and 9).

Comment 9 For loan 7, LoanCare did not provide any evidence of a service release stop and

flag before 07/27/2014, which was the required conveyance date. In addition, on

08/01/2014, LoanCare’s system log notes stated that the property was ready to be

conveyed and that it was awaiting recording instructions.

Comment 10 While LoanCare did document its effort with HUD to resolve the situation, it did

not file the part B within FHA’s timeframes or submit an extension request to

receive written approval to exceed these timeframes for these loans (loans 8 and

10).

Comment 11 Ginnie Mae will not only consider interest but other costs when calculating the

amount to be repaid, therefore $1.62 would be understating its potential recovery.

17

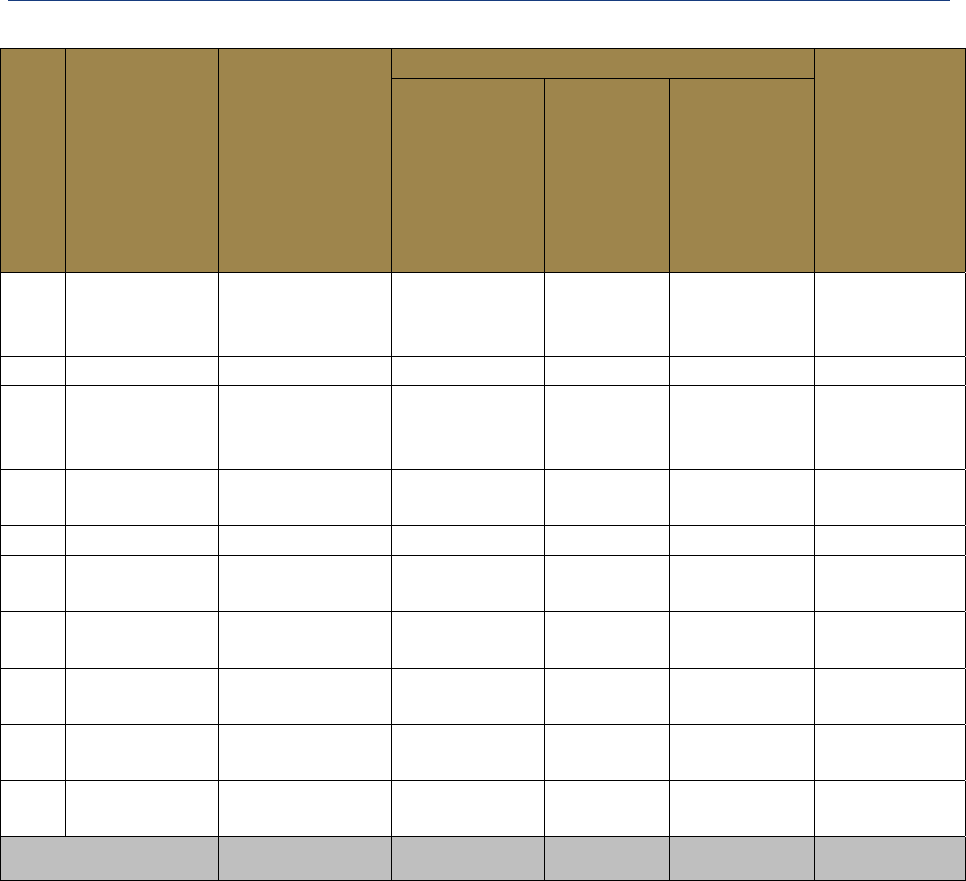

Appendix B

File Review Summaries

#

Loan

number

Disposition

Days between Remittances

(business

days to

remit claim

funds to

Ginnie Mae)

Possession

and

conveyance

Possession

and

personal

property

removal

Deed filing

or title

approval

and

submission

of part B

claims

1 0005182159 Conveyed 370 A 8

a) Same day

b) Same day

c) 3

2 0005338827 Conveyed 144 46 >45

B

3

3 0006562177 Conveyed 268 140 52

a) 3

b) 2

c) 5

4 0005192976 Conveyed 91 24

C

51

a) 2

b) 1

5 0005340344 Conveyed 370 A B 3

6 0005341318

Transferred to

Selene Finance

D D D

F

7 0005287669

Transferred to

Selene Finance

>30

B

>30

B

B

F

8 0006566558

Transferred to

Selene Finance

E E >45

B

F

9 0005219985

Transferred to

Selene Finance

D D D

F

10 0006559827

Transferred to

Selene Finance

E E >45

B

F

Number of delays 6 of 6 5 of 6 4 of 5

A – The file does not reveal the personal property removal date or has conflicting information.

B – Transferred to Selene Finance without taking the relevant action

C – Conflicting information in the file but personal property removed within 30 days

D – LoanCare never had possession of the property; it transferred the loan to Selene Finance.

E – The defaulted issuer conveyed the property before LoanCare serviced the loan.

F – LoanCare did not receive claim funds from FHA for the loan, so it had none to remit to Ginnie Mae.