Why Local Food Matters:

Views from the National Landscape

Debra Tropp,

Supervisory Agricultural Marketing Specialist

Farmers Market and Direct Marketing Research

Table of Contents

What do we mean by local food?

Relationship of local food to U.S. food system

Importance of local food demand

Growth of local food marketing outlets

Demand drivers and trends

What does the future of local food look like?

Is there room for further growth?

How do AMS programs facilitate market access for

local food?

What is Local?

A food product that is raised, produced, aggregated,

stored, processed, and distributed in the locality or region

in which the final product is marketed.

No official national designation, though some

individual USDA programs use a broad (maximum)

definition:

Less than 400 miles from the origin of the product, or

Within the State in which the product is produced.

Includes both direct-to-consumer sales AND

intermediated sales by distributors/food hubs

To restaurants, grocery stores, schools/universities,

hospitals, et. al.

How Are Consumer Perspectives Changing?

Phil Lambert, “Supermarket Guru”, 2013:

People are choosing their foods more holistically based on

multiple “food factors”:

Taste

Ingredients

Source

Nutritional composition

Asking who is making their foods

Understanding impact on environment and animal welfare

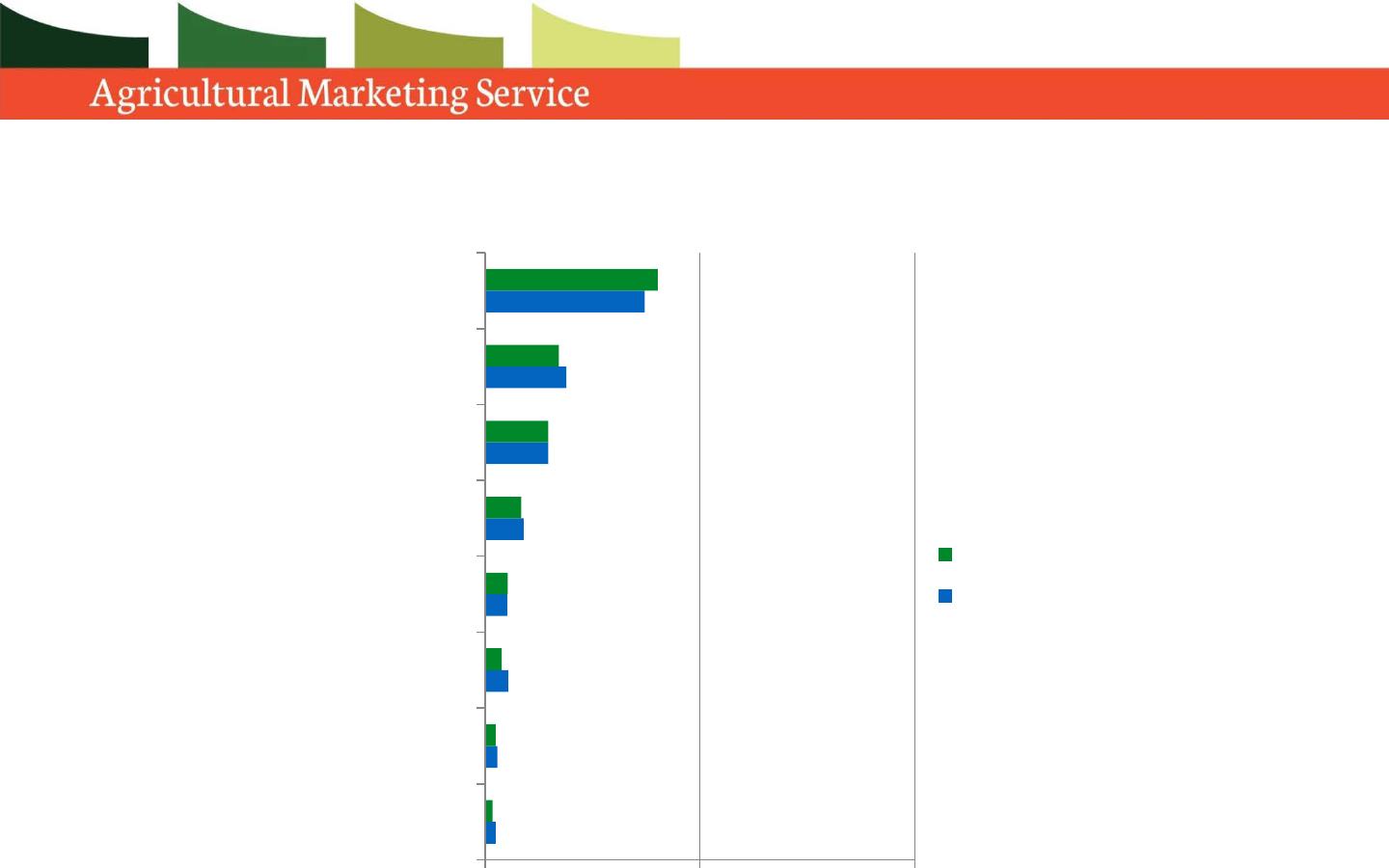

Consumers Lean Toward Alternative Store Formats

2.50

2.90

5.40

5.20

9.00

14.70

18.90

37.20

1.80

2.50

3.90

5.30

8.50

14.70

17.20

40.20

0 50 100

E-commerce

Dollar store

Fresh format/limited assortment

Drug store

Wholesale format

Convenience stores

Supercenters

Traditional supermarket

2013 Market Share

2018 Projected Market Share

2014 Retail Shop Topic, Jones Lang LaSalle, September 2014, available from

http://www.us.jll.com/united-states/en-us/Research/JLL-ShopTopic-Grocery-share.pdf?aa79b615-6518-4080-af03-e6104ea59d91

Rise of Fresh Format Stores

Strongest growth in “fresh format” stores

These food stores emphasize perishables and offer

center-store assortments that differ from those of

traditional retailers—especially in the areas of ethnic,

natural, and organic foods

Examples: Whole Foods, The Fresh Market

How Does Local Food Demand Correspond to

Changing Consumer Preferences?

In alignment with growing demand for freshness,

product integrity and transparency, local food

purchasing provides consumers with the opportunity to:

Obtain food items with superior quality characteristics

– freshness, flavor, ripeness, enhanced shelf life – and

possibly enhanced nutritional density (more research still

needed)?

Learn about farming practices used (often directly from

growers if through farmers markets or CSAs)

Have greater confidence in the integrity and quality of

the food they purchase

Reward sustainable production practices

Demand Drivers Among Consumers

Kearney report: grocery shoppers embrace the increase

in local food options because they believe it:

helps local economies (66 percent)

delivers a broader and better assortment of products

(60 percent)

provides healthier alternatives (45 percent)

improves the carbon footprint (19 percent)

increases natural or organic production (19 percent)

Approximately 70% of restaurant operators surveyed in

2014 said their patrons were more interested in locally

sourced items than they were two years earlier.

90% for fine dining restaurants.

A.T. Kearney, “Buying Into the Local Food Movement”, February 2013, National Restaurant

Association's 2014 Restaurant Industry Forecast

Demand Drivers Among Consumers

Observations from a 2015 study by Dr. Ion Vasi, an

associate professor with a joint appointment in the

Department of Sociology and Tippie College of Business

at the University of Iowa:

The local food market is what sociologists call a

moralized market, where people combine

economic activities with their social values.

It’s not just about the economical exchange; it’s a

relational and ideological exchange as well

It’s about valuing the relationship with the farmers and

people who produce the food and believing that how

they produce the food aligns with your personal

values

Demand Drivers Among Consumers

UI researchers discovered local food markets were more

likely to develop in areas where residents had a strong

commitment to civic participation, health, and the

environment

For his study, Vasi examined the development of local

food markets by looking at the number of farmers

markets, food coops, community-supported agriculture

providers, and local food restaurants in cities across the

United States. Researchers also conducted 40 interviews

with consumers and producers in different local food

markets in Iowa and New York.

Demand Drivers Among Consumers

Top 10 Menu Trends for 2015

1. Locally sourced meats and seafood

2. Locally grown produce

3. Environmental sustainability

4. Healthful kids’ meals

5. Natural ingredients/minimally processed foods

6. New cuts of meat (e.g. Denver steak, pork flat iron)

7. Hyper-local sourcing (e.g., restaurant gardens)

8. Sustainable seafood

9. Food waste reduction/management

10. Farm/estate branded items

Source: National Restaurant Association “What’s Hot” Chef Survey

Demand Drivers Among Consumers

Availability of locally grown produce and other local

packaged foods have become major influences on

grocery shopping decisions

87.2% say it is “very or somewhat important” to their

choice of a primary food store, up slightly from the 2013

level of 85.0%

Leading the “very important” component (44.2%)

Hispanics (53.3%)

Single-person households (49.4%)

Adults between the ages of 50 and 64 (46.2%)

2/3 of survey respondents endorse efforts of their

primary supermarket to support nearby local food sources.

Source: National Grocery Association and Supermarket Guru

Consumer Panel Survey 2014

Demand Drivers Among Consumers

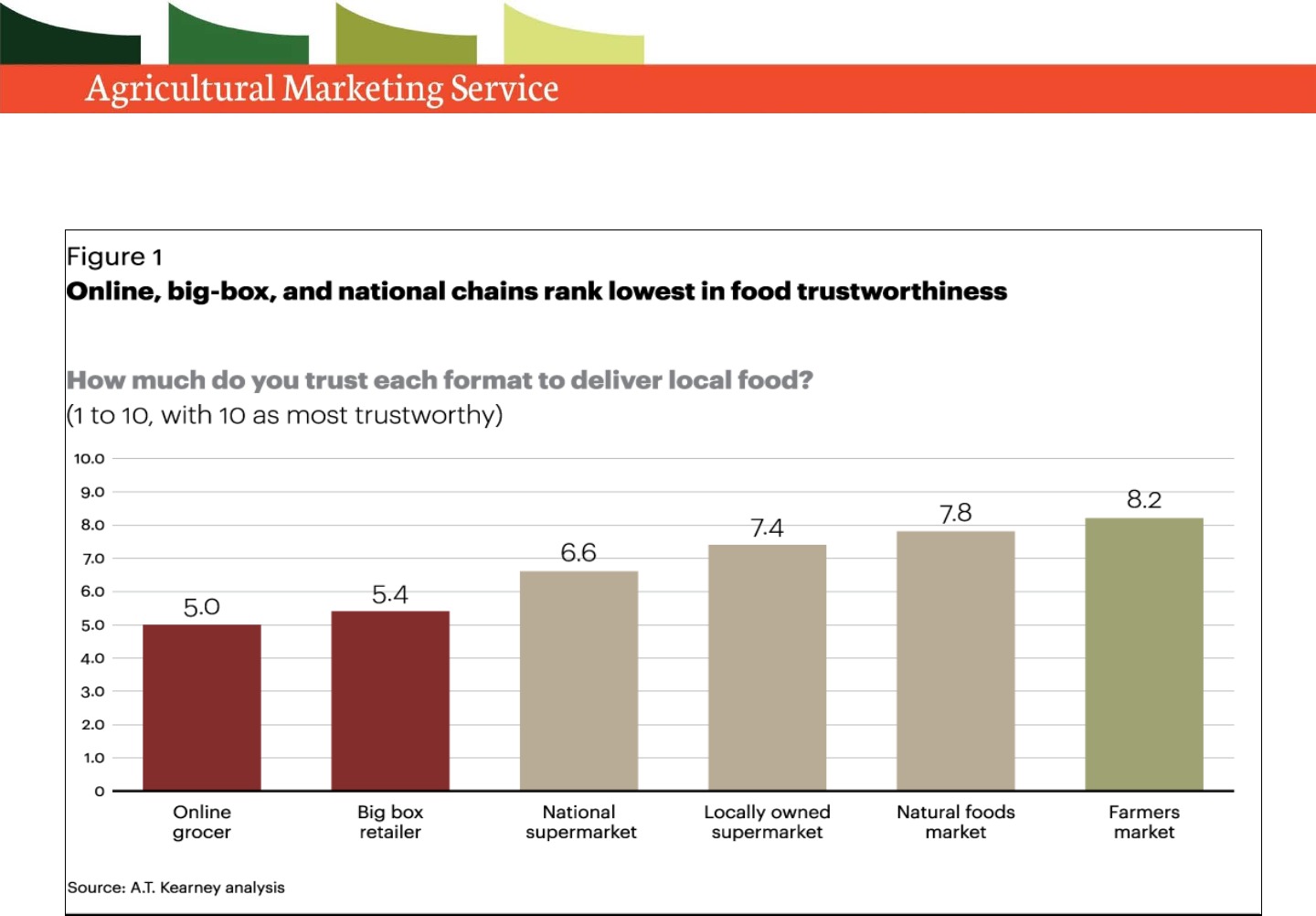

Shoppers will switch stores for local food selection

Almost 30% of grocery shoppers say they

consider purchasing food elsewhere if their

preferred store does not carry local foods.

Respondents say their main source for local food

is still the local farmers market and farm stores.

Only 5% indicate they shop for local foods at

big-box retailers, and 15% at national

supermarkets

Source: A.T. Kearney, “Buying Into the Local Food Movement”, January 2013

Demand Drivers Among Consumers

Consumers Willing to Shop Around for Quality Perishables

Channel

Primary Food

Source

Primary Source

of Fresh

Produce

Secondary

Source of Fresh

Produce

Supermarkets 76% 56% ↓

29%

Warehouse

clubs/supercenters

19% 10% ↓

23%

Health food stores 2% 2% 8%

Farmers markets 1% 25% ↑

12%

Other direct from

producer

1% 5% ↑

3%

Specialty store 1% 1% 3%

No preference – – 22%

Colorado State University Survey of U.S. Adults (2006), based on national consumer

panel data

Demand Drivers Among Consumers

Demand Drivers Among Consumers

Direct to consumer (DTC) food sales for human

consumption still represent a very small share of the

national food supply:

But if we take into account direct and intermediated

sales of local food products, the picture begins to

change:

Nearly 8 percent of U.S. farms participated in local

food marketing channels as of 2012 (Low, 2015)

Local Food’s Contribution to National Food System

Year

Total

Agricultural

Sales ($000)

Direct-to-Consumer

Sales of Ag. Products

for Human

Consumption ($000)

Ratio of Direct-to-

Consumer Sales to

Total Agricultural

Sales (%)

2012 394,644,481 1,309,827 0.3

Estimated 2012 local food sales: $6.11 billion

Of which

$3.35 billion (54.8 percent) was generated by farms that

exclusively

used intermediated wholesale marketing

channels

• Only 22,600 farms, 148K per farm

$1.15 billion (18.8 percent) was generated by farms which

exclusively

used DTC channels

• Approximately 5x as many farms (112,304) as those

which only used intermediated channels, 10.2K per farm

Remaining $1.61 billion sold through both channels

.

Most Local Food Sold Through Intermediaries

Source: Low (USDA Economic Research Service, January 2015)

Why Intermediated Sales?

430

288

180

0 200 400 600

Farm to School Programs

Food Hubs

Farmers Markets

Growth between 2007 and 2014 (Percent)

Prompted by:

Growing retail and food service buyer interest in meeting

consumer demand for local foods

Producer interest in catering to higher- volume wholesale clients

Comparatively low revenues from labor-intensive direct to

consumer marketing

Growing producer ability to provide deliveries of local products

in commercial-sized volume over longer portions of the year,

supported by aggregation services and season extension technology

Farm Level Challenges with Local Food

Not always so easy for local farmers to access

larger-volume marketing channels

Individual farm operators often lack individual capacity to

meet buyer requirements for product volume, quality,

consistency, variety, or extended availability.

Farmers continue to be challenged by the lack of

distribution, processing and marketing infrastructure

that would give them wider market access to larger volume

customers

Meanwhile, Commercial Buyers Are Looking For:

Traceback mechanisms and recordkeeping

Many commercial, institutional and retail buyers want to

procure local food products that can be traced back to the

originating farm in the event of a foodborne illness outbreak.

Smaller and mid-scale farmers often lack capacity to

establish adequate recordkeeping or product

monitoring systems by themselves

Food safety

Commercial and institutional customers are increasingly

demanding third-party certifications of production/handling

processes (e.g., GAP, GHP), which many smaller farmers

have not had to address in the past

Food Safety Modernization Act may result in new

requirements and expectations

USDA believes regional food hubs can play an

important role in supporting these small and mid-size

farmers through aggregation, collective marketing, and

facilitative services

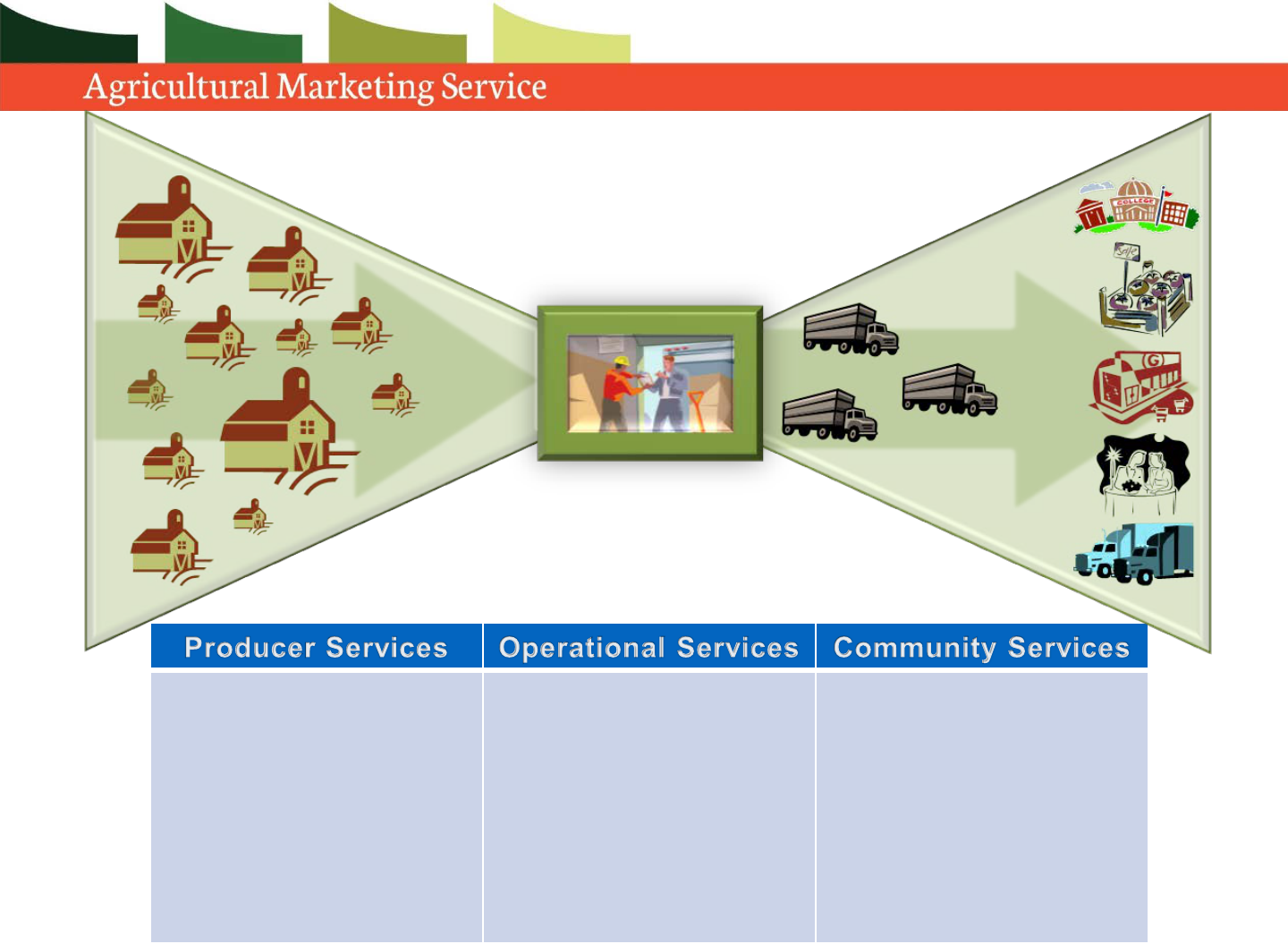

Defining Characteristics of Regional Food Hubs

Carry out or coordinate the aggregation, distribution,

and marketing of primarily locally/regionally

produced foods

Move product from multiple producers to multiple

markets

Producers considered valued business partners

instead of interchangeable suppliers

Committed to buying from small to mid-sized

producers whenever possible.

Use product differentiation strategies (e.g., identity

preservation, group branding, sustainable production

practices, etc.) to ensure that producers maximize

returns from their products.

Regional Food Hubs

Actively linking producers to

markets

On-farm pick up

Production and post-harvest

handling training

Business management

services and guidance

Value-added product

development

Food safety and GAP training

Liability insurance

Aggregation

Distribution

Brokering

Branding and market

development

Packaging and repacking

Light processing (trimming,

cutting, freezing)

Product Storage

“Buy Local” campaigns

Distributing to “food deserts”

Food bank donations

Health screenings, cooking

demonstrations

SNAP redemptions

Educational programs

Youth and community

employment opportunities

Regional Food Hubs

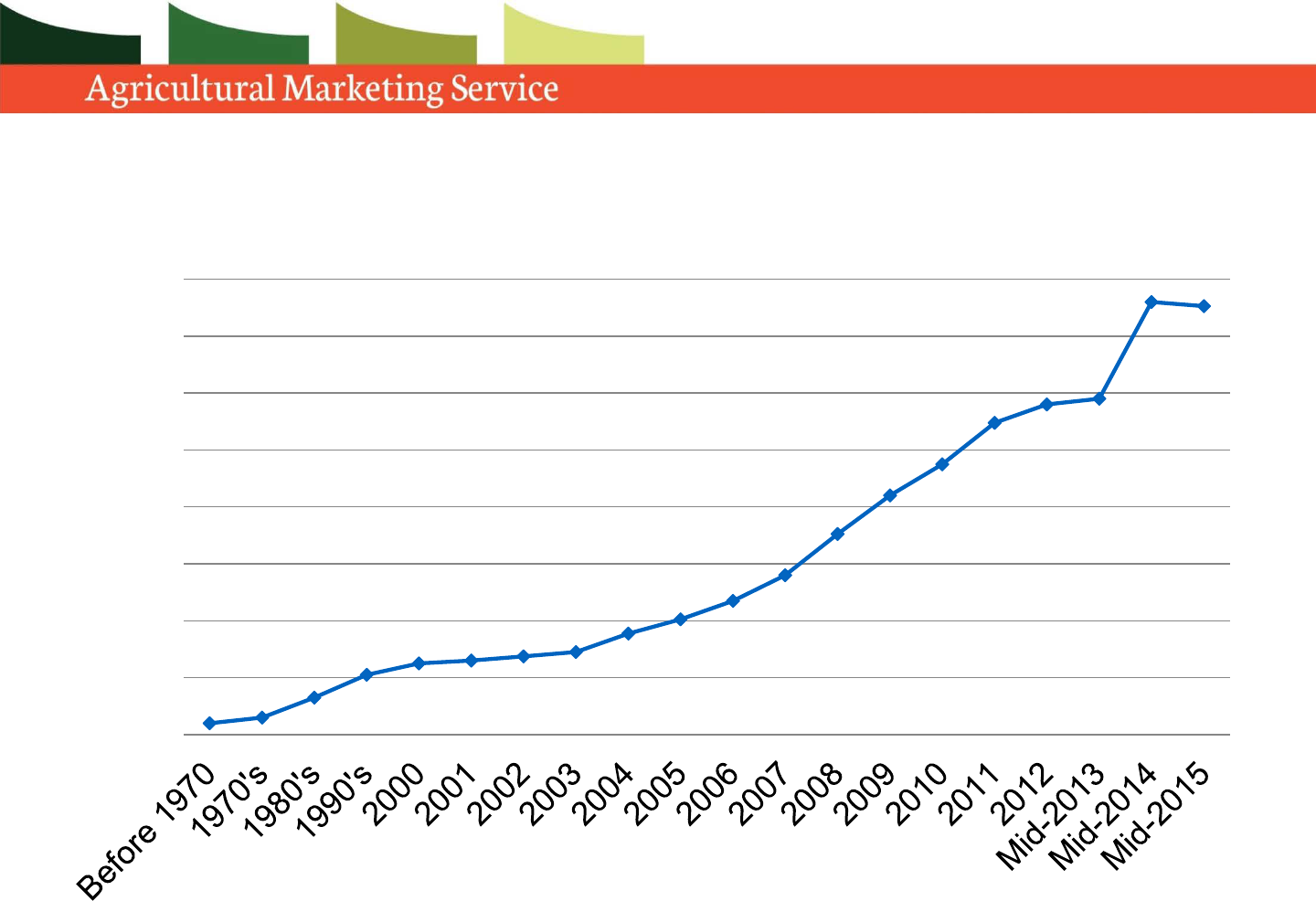

0

40

80

120

160

200

240

280

320

Growth in the Number of Food Hubs (1970s-2014)*

Based on a working list of food hubs identified by the NGFN Food Hub Collaboration

http://www.ers.usda.gov/data-products/food-dollar-series/documentation.aspx

Farm Share of U.S. Consumer Food Dollar (2012)

Different story in local food

systems…

In “short” supply chains, local

producers received up to seven

times the share of the retail price

compared to mainstream chains -

USDA ERS report

http://www.ers.usda.gov/media/122609/err99_1_.pdf

Food hubs often return between

75 to 85 percent of their wholesale

sales revenues to their producers -

USDA AMS report

http://dx.doi.org/10.9752/MS046.04-

2012

In mainstream supply chains,

farmers retain only 17.4 cents

of the consumer food dollar on

average

Example One: Intervale Food Hub,

Burlington, VT

Intervale works with producers to determine prices

based on actual production costs for producers and

what the market can realistically manage.

Intervale’s producers generally net 60-70% of the

retail revenue obtained from CSAs and 85% of the

revenue obtained from distribution to wholesale

customers through the hub.

Example Two: Red Tomato, Canton, MA

Coordinates aggregation, transportation and

sales for roughly 40 farmers to grocery stores in

the NE (including Trader Joe’s)

Employs a variety of product differentiation

strategies – regional branding, source

identification and the verified use of sustainable

production practices like IPM

November 2009 case study: retailer agreed to

sell RT’s tomatoes at $2.79/lb. compared to

standard retail price for the same commodity of

$1.99/lb. given the unique attributes of the

product

Combination of cost savings in shared logistics

and a higher wholesale price led RT’s producers

to receive 3x higher returns than they received

for comparable items outside the value chain

Example of Food Hub/Retail Partnership

In August 2013, Milwaukee-based Roundy's Inc.,a large

regional supermarket chain and the market leader in

metropolitan Milwaukee, formed a partnership with the

Madison-based Wisconsin Food Hub Cooperative. The

cooperative, based in Madison, supplies a variety of produce

to Roundy’s stores in Wisconsin operating under the Pick 'n

Save, Copps and Metro Market banners.

Participating stores frequently use point-of-purchase

displays to promote the program.

The Wisconsin Food Hub Cooperative generated

approximately $3 million in produce revenues in 2013,

after only a year in operation

Example of Food Hub/Retail Partnership

The partnership with Roundy's is

designed to get food from farm to

warehouse and on its way to grocery

stores as quickly as 24 hours from

when the produce is picked, said Ron

Balsimo, sales manager for the

cooperative. "You can't get any fresher

unless you walked into a field and picked

it yourself,“

The cooperative has grown to more than

100 members, "and they keep coming,"

Balsimo said.

Starting to see some farmers expand

their plantings because of the hub

Benefits of Food Hub/Retail Partnership

There are demonstrated sales gains that come from

locally grown food programs in grocery stores, says Bill

Justin, president of W.L. Justin & Assoc., a supermarket

consulting company based in Atlanta. "We find that you can

actually increase total store sales," he said.

He has seen examples of such programs increasing sales

by as much as 15% to 20% in the produce department.

Having sources of local produce can also help mitigate

any potential supply concerns brought about by the

extreme drought in California’s produce-growing regions.

Future Demand Drivers?

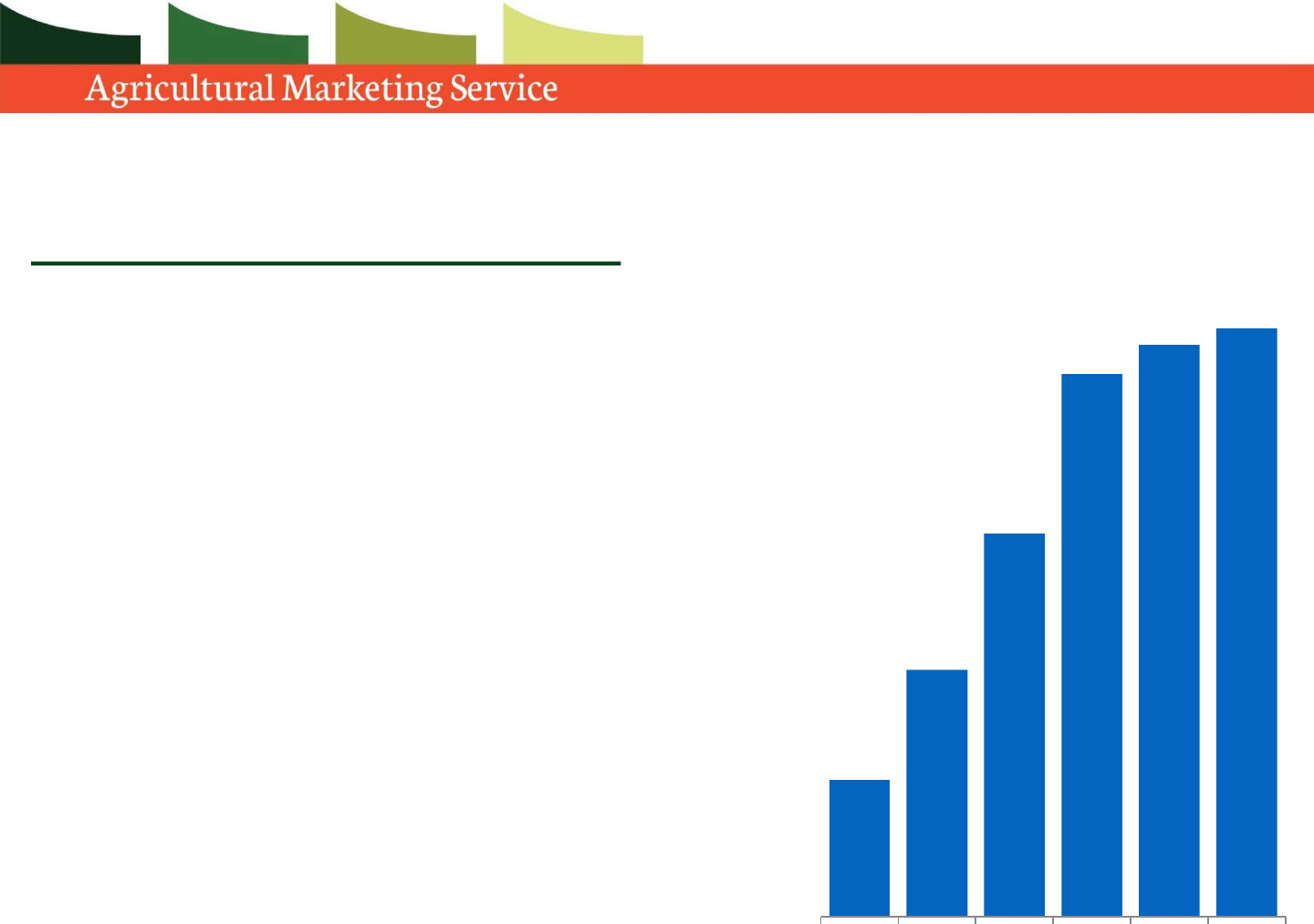

Nutrition Assistance Programs

Acceptance of SNAP benefits at farmers

markets and farm stands rose from

approximately 900 sites in 2009 to more

than 6,400 in 2014. The value of

redemptions grew from $4 million to

nearly $19 million, due to:

Pro-active outreach by USDA Food and

Nutrition Service (FNS) to certify markets

and vendors

AMS and FNS grants for EBT equipment

installation

Rise of non-profit voucher programs (i.e.,

Wholesome Wave, Fair Food Network)

Rise of mobile FMs in low-income areas

$4,173,323

$7,547,028

$11,725,316

$16,598,255

$17,500,000

$18,800,000

2009 2010 2011 2012 2013 2014

Future Demand Drivers?

Schools

Farm to school programs now exist in more than 42,000 schools

Schools spent more than $600 million on local food in the 2013-14

school year, up 55% from the previous year.

Hospitals

Growing number of farmers markets operating at hospitals and

health care facilities

More than 90 reported in USDA National Farmers Market Directory

at hospitals or public health facilities

Kaiser Permanente lead in early years; recent campaign to

introduce them at VA hospitals

Military Bases

New DoD “healthy base initiative” aims to expand farmers

markets on base, local food in commissaries

Joint USDA/DoD Report on FMs at military bases released in

November 2015

AMS Programs and Services

AMS Connection to Local Food

Division Structure

Applied Research Reports

Facility Design

Grants

Farmers Market Promotion Program (FMPP)

Local Food Promotion Program (LFPP)

Specialty Crop Block Grant (SCBG)

Federal-State Marketing Improvement Program

(FSMIP)

Cost-Share for Organic Certification

Legislative Authority Supports USDA/AMS Interest

in Locally-Grown Food

1946 Agricultural Marketing Act:

Agency mandated to reduce distribution costs and the

price spread between producers and consumers

Directed to market the “full production” of American

farmers—regardless of scale—in a useful, economical,

profitable, and orderly manner

Improvement of overall dietary and nutritional

standards is a primary policy goal

1976 Farmer to Consumer Direct Marketing Act:

Encourages promotion of direct farm marketing

activities for mutual benefit of farmers and consumers

Legislative Authority Supports USDA/AMS Interest

in Locally-Grown Food

Bottom line: USDA/AMS is mandated to:

Support the development and creation of shorter food

supply chains wherever feasible

Work to ensure that food producers receive a greater

share of the final retail price that consumers pay

Support profitable marketing of all American farmers at

all scale levels

Promote direct marketing of farm products where it

provides mutual benefit to farmers and consumers

Farmers Markets and Direct-to-Consumer Marketing

Through market research, analysis, data products and

other tools, we help stakeholders better understand

trends in the rapidly evolving direct to consumer

marketplace.

Maintains four national directories on local food (FMs

[8,527], CSAs [668], food hubs [153], on-farm markets

[1,313]) at www.usdalocalfooddirectories.com

FM directory selected as first Federal API in 2013!

Administers voluntary FM market manager surveys

Developing national surveys for CSAs, food hubs, on-farm

markets (directories launched in 2014)

Structure of AMS Local Food Research &

Development Division

Food Hubs and Other Aggregation Models

Conducts research on emerging business enterprises

that offer aggregation, distribution, and/or marketing

services to small and mid-sized agricultural producers

who cater to local food markets.

Facility Design

Provides targeted site assessment, design services

and layout analysis for food market and facility

personnel to improve the efficiency of permanent food

market, distribution and warehouse facilities.

Structure of AMS Local Food Research &

Development Division

Regional Food Hub Resource Guide

Food hub impacts on regional food systems, and the resources

available to support their growth and development

Moving Food Along the Value Chain:

Innovations in Regional Food Distribution

Food Value Chains:

Creating Shared Value to Enhance Marketing Success

Building a Food Hub from the Ground Up:

A Facility Design Case Study of Tuscarora Organic Growers

Research/TA Reports on Local Food Systems

Upcoming Releases in early CY 2016:

The Evolving CSA Business Model (results of national survey and

focus group interviews in six states)

Potential Demand for Local Agricultural Products by Mobile

Markets

Local Food Economic Assessment Toolkit: a guide to creating

your own community assessment using secondary/primary data and

IMPLAN input/output software

Research Reports on Local Food Systems

Why an Economic Impact Toolkit?

The recent sharp increase in market demand for local

foods, currently estimated by USDA to be over $6 billion

in value, has sparked a groundswell of interest and

investment in local food systems.

Community planners, public officials, and private

foundations are increasingly interested in exploring the

potential of local food in generating economic growth

and business development.

Unfortunately, many of these initiatives lack a clear

roadmap for measuring and evaluating their overall

impact.

Why an Economic Impact Toolkit?

To provide community planners and other stakeholders

with better ways of assessing outcomes of proposed local

food investments, USDA/AMS asked Colorado State

University to convene a group of leading U.S.

researchers and consultants to synthesize current best

practices

The project team members chosen to create the Toolkit

were deliberately selected because of their specific

research expertise in local food systems and

economic impact assessment.

Toolkit Learning Objectives

The Toolkit contains seven modules that offer real-world,

practical guidance to planners, economic development

specialists, and others interested in assessing the

economic impact of local food system interventions. Topics

covered include:

Framing research approaches

Collecting primary data

Compiling data from secondary sources

Developing a solid grasp of economic multipliers

and their limitations as measurement tools

Making effective use of input/output software

Customizing it as needed to better reflect local food

system conditions.

Grants: Farmers Market Promotion Program

Mission: To increase domestic consumption of, and

access to, locally and regionally produced agricultural

products, and to develop new market opportunities for

farm and ranch operations serving local markets

Diverse applicant eligibility (non-profits, local governments,

producer networks, etc.) Excludes state governments and

individual producers

Only funds direct producer-to-consumer marketing activities

(e.g., FMs, CSAs, on-farm markets)

Approximately $13 million in funding available in FY 2016

$25,000-$100,000 per grant

RFA likely to be released in March 2016

Mission: To increase domestic consumption of, and

access to, locally and regionally produced

agricultural products marketing through

intermediaries (not direct to consumer)

Launched in FY 2014, result of new Farm Bill

Approximately $13 million in funding available in FY 2016

Planning Grants – up to $25,000 each

Implementation Grants - up to $100,000 each

Diverse applicant eligibility (State governments and

individual producers are prohibited)

RFA for FY 2016 likely to be released in March 2016

Grants: Local Food Promotion Program

Agency oversees management of grants administered

by State Departments of Agriculture solely to enhance

the competitiveness of specialty crops

Specialty crops are defined as “fruits, vegetables, tree

nuts, dried fruits, horticulture, and nursery crops (including

floriculture)”

$63 million in funding was available in FY 2015 (pro-rated

based on state share of specialty crop production)

Grants: Specialty Crop Block Grant Program

NEW: Multi-State Specialty Crop Block

Grant Program

Designed to:

Support food safety and research

Address plant pests, disease, and crop-specific

issues

Increase marketing opportunities for specialty crops

Announced September 4, 2015

Applications must be submitted to www.grants.gov

by January 14, 2016

Program is open to state departments of agriculture in

the 50 States, the District of Columbia, the

Commonwealth of Puerto Rico, Guam, American Samoa,

the United States Virgin Islands, and the Commonwealth

of the Northern Mariana Islands.

Involves at least two partners located in different

states. USDA encourages other State agencies, Tribal

governments, universities, non-profits, and other

specialty crop organizations to partner with participating

State departments of agriculture

NEW: Multi-State Specialty Crop Block

Grant Programs

NEW: Multi-State Specialty Crop Block

Grant Program

Priority areas:

• Benefitting underserved communities and veterans

• Improving producers’ and facilities’ capacity to comply

with the requirements of the Food Safety Modernization

Act

• Developing adaptation and mitigation strategies for

farmers in drought-stricken regions of the country

• Increasing opportunities for new and beginning farmers

• Developing strong local and regional food systems

• Protecting pollinator habitats/improving pollinator

health

• Supporting the growth of organic specialty crops.

Provides matching funds to State Departments of

Agriculture, State agricultural experiment stations,

and other appropriate State agencies

Assists in exploring new market opportunities for U.S.

food and agricultural products, and to encourage

research and innovation aimed at improving the

efficiency and performance of the marketing system

About $1 million per year

Funds approximately 20 projects per year at an average

of $50,000 per grant

Grants: Federal-State Marketing Improvement Program

As of FY 2016, being administered by AMS/TM/Grants Division

(not NOP)

Organic producers can be reimbursed up to 75 percent of their

certification costs (not to exceed $750)

Two organic certification cost share programs were offered in

2015, valued at $11.9 million

National Organic Certification Cost Share Program

(NOCCSP) - $11 million per year

Agricultural Management Assistance (AMA) Organic

Certification Cost Share Program - $900K per year

• Available to organic producers (crop and livestock operators only)

in CT, DE, HI, MA, ME, MD, NH, NJ, NV, PA, RI, VT, WV, WY

Cost-Share for Organic Certification