Consumer’s EdgeConsumer’s Edge

Consumer Protection Division, Maryland Office of the Attorney General

Rent-to-Own: Worth the Convenience?

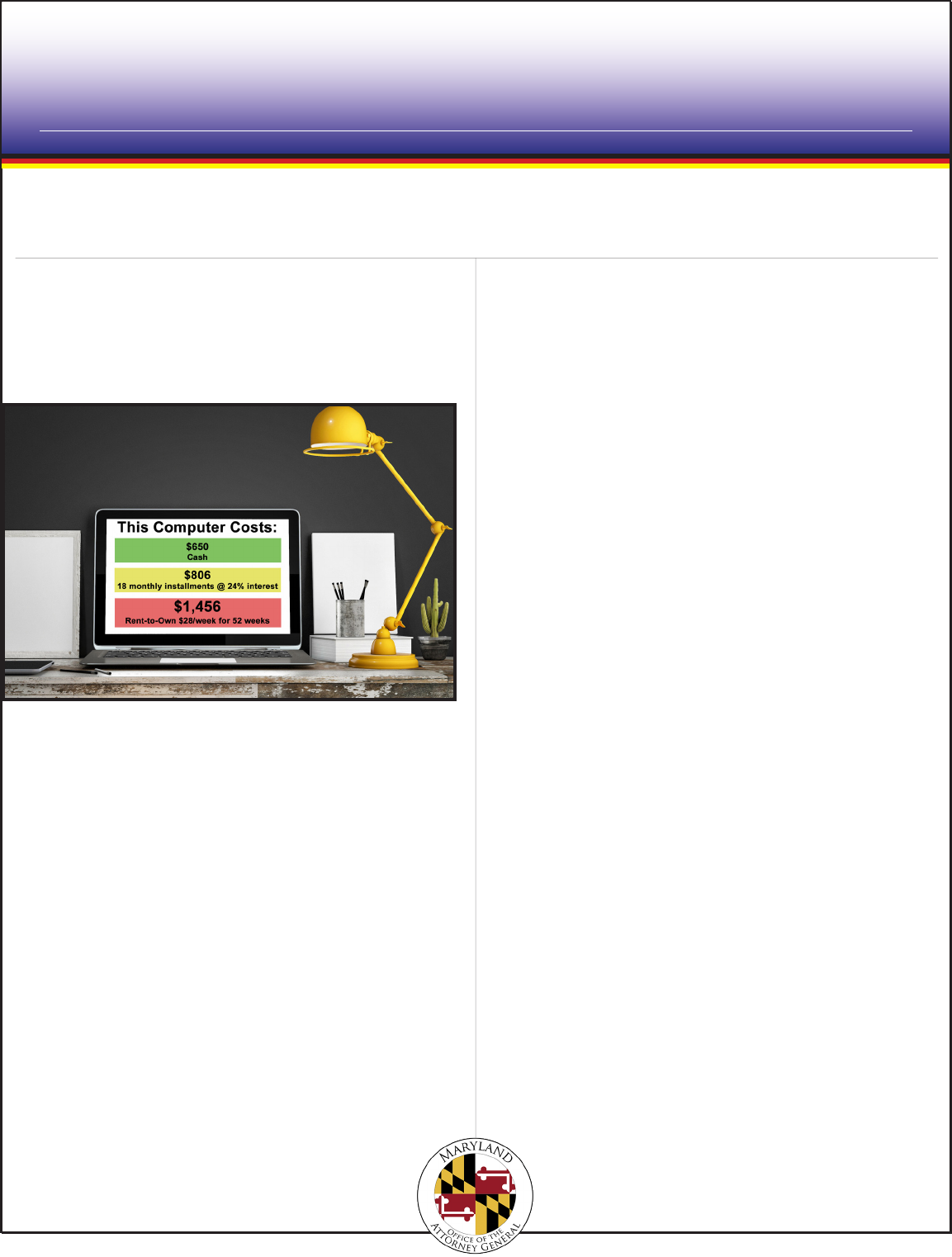

A Maryland woman signed a rent-to-own agreement for

a computer. The weekly payments were $28 for a period

of 52 weeks. If she made all the payments, she would pay

a total of $1,456 to own the computer, which was used

and had a cash price of only $650.

If you need a television, major appliance, or furniture

but you don’t have the cash or credit to buy it outright,

you might be tempted to go to a rent-to-own store. These

stores advertise that you can take home the item imme-

diately, simply by agreeing to make a weekly or monthly

payment. You’re obligated only to pay each rental pay-

ment as it comes due, and you are free to end the arrange-

ment by returning the merchandise to the store.

This arrangement may sound convenient, but it comes at

a very high price. Buying on a rent-to-own plan will often

cost you double what you would pay for the item with

cash, on layaway, or on an installment plan.

For example, a new $400 washing machine purchased on

an 18-month installment plan at the maximum allowable

interest (24%) would cost $480 total. Under an 18-month

rent-to-own plan, you’d typically pay $1,000 or more for

the same washing machine. Plus, the rent-to-own washing

machine might be a couple of years old and previous-

ly rented to many other people.

Maryland law does not place any limits on the nance

charges or interest rent-to-own dealers can charge. The

dealers are also not required to disclose as an annual

percentage rate (APR) the nance charge or interest con-

sumers end up paying to own the product. Therefore, you

cannot easily compare the cost of buying under a rent-to-

own plan with buying on, for example, an installment plan.

If rent-to-own dealers did have to disclose an APR, con-

sumers would see that their rates are often as high as 120%

to 150%.

Dealers, however, are required to disclose the “Cost of

Lease Services,” which is the dierence between the nal

purchase price of the rental property if you make all pay-

ments due under the lease and the cash price of the rental

property. The rental agreement must contain a disclosure,

similar to the one below, above your signature that states

the costs under your rental agreement:

Consider All Your Options

Rent-to-own stores market to people who may think they

have no other options, because of low income or bad credit.

But there may be less-expensive alternatives:

• Can you do without the item until you have saved

enough money in the bank to pay cash? If the

woman who wanted a computer could wait a few

months, perhaps by using a friend’s computer or

one at the public library, she could save $28 a

week instead of paying a rent-to-own dealer. In six

months she would have enough to buy a new com-

puter priced at $650. She would own the computer

in half the time and save more than $700.

• Can you buy the item on a layaway plan? You may

only need a small down payment.

• Can you buy the item on an installment plan at a

retail store? With an installment plan you can take

the item home immediately, as with rent-to-own.

The law limits the amount of interest that can be

charged on installment plans (maximum 24%), so

Issue #109

January 2023

Anthony G. Brown, Maryland Attorney General

these plans are less costly than rent-to-own agree-

ments.

• Can you get a short-term loan from a lending

institution such as a bank or credit union to pur-

chase the item?

• Can you nd a used item through on online

marketplace, the classied ads, a yard sale, or

second-hand store? You may be able to nd what

you need for the cost of only a few rent-to-own

payments.

Your Rights Under the Law

If you do decide to enter a rent-to-own agreement, be

aware that Maryland law provides some protections

for rent-to-own consumers. The lessor must give you a

written receipt for any payment made by cash or money

order. The required disclosures must be available in any

language that the lessor uses to advertise rental purchases.

Rent-to-own contracts must disclose the following import-

ant information:

Whether the item is new or used. This information may

be especially important to know when considering pur-

chasing an appliance, a TV, or a computer.

What it will cost you. The contract must state how much

the item would cost if you paid cash, how many rental

payments you must make to own the item, how much each

payment will be, and how much you’ll have to pay in total

to own the item. With this information, you can look at the

total amount you will pay to own the item and consider if

it’s worth it.

Your early purchase option. The contract must give

you the option to purchase the item earlier than original-

ly planned by paying a certain amount. The method for

determining that amount must be described.

Your right to “reinstate” after late payments or repos-

session. The law allows consumers who are late in making

payments to retain their rights to the item, even after it has

been repossessed, if they make all outstanding payments.

These provisions protect consumers who have made a

substantial investment toward owning the property.

If the dealer repossesses an item you were renting because

you failed to make a payment, the dealer must give you

a written notice that states your right to reinstate the

rent-to-own agreement, the last date by which you

can reinstate the agreement, and the amount you will have

to pay to reinstate. You may reinstate the rent-to-own agree-

ment within 15 days of the repossession by paying all past

due charges, the reasonable costs of pickup and redelivery

and a reinstatement fee of $5.

Maintenance and damage. The dealer is responsible for

keeping your rented items in good working order without

extra charge to you, as long as you have not damaged it.

You are responsible for loss, damage, theft, or destruction

of the property while it’s in your possession. If the item is

lost, damaged, or stolen while in your possession, you must

pay the dealer the early purchase option price of the item.

Warranties. If any part of a manufacturer’s warranty

covers the rental item at the time you acquire ownership,

the warranty will be transferred to you if allowed by the

warranty.

A sample rental-purchase agreement can be found on the

next page.

If you have a problem with a rent-to-own transaction,

contact the Consumer Protection Division at 410-528-8662

(toll-free in Maryland: 1-888-743-0023).

Consumer Protection Division

200 St. Paul Place, 16th Fl., Baltimore, MD 21202

• General Consumer Complaints: 410-528-8662

Toll-free: 1-888-743-0023 TDD: 410-576-6372

• En español: 410-230-1712

9 a.m. to 3 p.m. Monday-Friday

www.marylandattorneygeneral.gov/Pages/CPD/

• Health Consumer Complaints: 410-528-1840

Toll-free: 1-877-261-8807 TDD: 410-576-6372

9 a.m. to 4:30 p.m. Monday-Friday

www.marylandcares.org

• For information on branch oces in Largo, Salisbury,

Hagerstown, and a full list of oces across Maryland, visit:

www.marylandattorneygeneral.gov/Pages/contactus.aspx

How to contact us

The Consumer’s Edge is produced by the Maryland Attorney

General’s Office. Reproductions are encouraged.

Maryland

Attorney General

Anthony G. Brown

www.marylandattorneygeneral.gov