Table of contents

What are the differences between Original Medicare

and Medicare Advantage? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

What are Medicare Advantage Plans? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

How do Medicare Advantage Plans work? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

What do Medicare Advantage Plans cover? . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

What are my costs? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Who can join a Medicare Advantage Plan? . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

When can I join, switch, or drop a Medicare Advantage Plan? . . . . . . . . . 9

How can I join a Medicare Advantage Plan? . . . . . . . . . . . . . . . . . . . . . . . . . . .11

Types of Medicare Advantage Plans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Compare Medicare Advantage Plans side-by-side . . . . . . . . . . . . . . . . . . . 20

What if I have a Medicare Supplement Insurance

(Medigap) policy? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Where can I get more information? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22

Introduction 1

Getting started:

Introduction

When you first sign up for Medicare and during certain times of the year, you can

choose how you get your Medicare coverage.

There are 2 main ways to get Medicare:

• Original Medicare is a fee-for-service health plan that has two parts:

Part A (Hospital Insurance) and Part B (Medical Insurance). After you pay a

deductible, Medicare pays its share of the Medicare-approved amount, and you pay

your share (coinsurance). If you want Medicare drug coverage

(Part D), you can join a separate Medicare drug plan.

• Medicare Advantage (also known as “Part C”) is a type of Medicare health plan

oered by a private company that contracts with Medicare. These plans include

Part A, Part B, and usually Part D. Plans may oer some extra benefits that Original

Medicare doesn’t cover.

Your decision about how to get Medicare aects how much you pay for coverage, what

services you get, and what doctors you can use.

Understanding Medicare Advantage Plans2

What are the differences between Original Medicare

and Medicare Advantage?

Original Medicare

• Includes Medicare Part A (Hospital

Insurance) and Part B (Medical Insurance).

• You can join a separate Medicare drug plan

to get Medicare drug coverage (Part D).

• You can use any doctor or hospital that

takes Medicare, anywhere in the U.S.

• To help pay your out-of-pocket costs

in Original Medicare (like your 20%

coinsurance), you can also shop for and

buy supplemental coverage.

Part A

Part B

You can add:

Part D

You can also add:

Supplemental

coverage

This includes Medicare Supplement

Insurance (Medigap). Or, you can use

coverage from a current or former

employer or union, or Medicaid.

Medicare Advantage

(also known as Part C)

• A Medicare-approved plan from a private

company that oers an alternative to

Original Medicare for your health and drug

coverage. These "bundled" plans include

Part A, Part B, and usually Part D.

• In many cases, you can only use doctors

who are in the plan’s network.

• In many cases, you may need to get

approval from your plan before it covers

certain drugs or services.

• Plans may have lower or higher

out-of-pocket costs than Original Medicar

You may also have an additional premium.

• Plans may oer some extra benefits that

Original Medicare doesn't cover - like

certain vision, hearing, and dental services

e.

.

Part A

Part B

Most plans include:

Part D

Some extra benefits

Some plans also include:

Lower out-of-pocket-costs

Understanding Medicare Advantage Plans 3

Original Medicare vs. Medicare Advantage

Doctor & hospital choice

Original Medicare Medicare Advantage (Part C)

You can go to any doctor or hospital that

takes Medicare, anywhere in the U.S.

In many cases, you can only use doctors

and other providers who are in the

plan’s network and service area (for

non-emergency care). Some plans

oer non-emergency coverage out of

network, but typically at a higher cost.

In most cases, you don’t need a referral

to use a specialist.

You may need to get a referral to use a

specialist.

Cost

Original Medicare Medicare Advantage (Part C)

For Part B-covered services, you usually

pay 20% of the Medicare-approved

amount after you meet your deductible.

This amount is called your coinsurance.

Out-of-pocket costs vary —plans may

have lower or higher out-of-pocket

costs for certain services.

You pay a premium (monthly payment)

for Part B. If you choose to join a

Medicare drug plan, you’ll pay a separate

premium for your Medicare drug

coverage (Part D).

You pay the monthly Part B premium

and may also have to pay the plan’s

premium. Some plans may have a $0

premium and may help pay all or part of

your Part B premium. Most plans include

Medicare drug coverage (Part D).

There’s no yearly limit on what you pay

out of pocket, unless you have

supplemental coverage—like Medicare

Supplement Insurance (Medigap).

Plans have a yearly limit on what you

pay out of pocket for services

Part A and Part B cover. Once you reach

your plan’s limit, you’ll pay nothing for

services Part A and Part B cover for the

rest of the year.

You can choose to buy Medigap to help

pay your remaining out-of-pocket costs

(like your 20% coinsurance). Or, you can

use coverage from a current or former

employer or union, or Medicaid.

You can’t buy Medigap.

Understanding Medicare Advantage Plans4

Original Medicare vs. Medicare Advantage

Coverage

Original Medicare Medicare Advantage (Part C)

Original Medicare covers most medically

necessary services and supplies in

hospitals, doctors’ oces, and other

health care facilities. Original Medicare

doesn’t cover some benefits like eye

exams, most dental care, and routine

exams.

Plans must cover all medically necessary

services that Original Medicare covers.

Plans may also oer some extra benefits

that Original Medicare doesn’t cover—

like certain vision, hearing, and dental

services.

You can join a separate Medicare drug

plan to get Medicare drug coverage

(Part D).

Medicare drug coverage (Part D) is

included in most plans. In most types

of Medicare Advantage Plans, you can’t

join a separate Medicare drug plan.

In most cases, you don’t need approval

for Original Medicare to cover your

services or supplies.

In many cases, you may need to get

approval from your plan before it covers

certain services or supplies.

Foreign Travel

Original Medicare Medicare Advantage (Part C)

Original Medicare generally doesn’t

cover medical care outside the U.S.

You may be able to buy a Medicare

Supplement Insurance (Medigap) policy

that covers emergency care outside the

U.S.

Plans generally don’t cover medical

care outside the U.S. Some plans

may oer a supplemental benefit that

covers emergency and urgently needed

services when traveling outside the U.S.

Understanding Medicare Advantage Plans 5

What are Medicare Advantage Plans?

A Medicare Advantage Plan is another way to get your Medicare Part A and

Part B coverage. Medicare Advantage Plans, sometimes called “Part C” or “MA” Plans,

are oered by Medicare-approved private companies that must follow rules set by

Medicare. Most Medicare Advantage Plans include drug coverage (Part D). There are

several types of Medicare Advantage Plans (go to page 12 for more information).

Each of these Medicare Advantage Plan types have special rules about how you get

your Medicare-covered Part A and B services and any supplemental benefits your

plan covers.

If you join a Medicare Advantage Plan you’ll still have Medicare, but you’ll get most

of your Part A and Part B coverage from your Medicare Advantage Plan, not Original

Medicare. You’ll have the same rights and protections you would have under Original

Medicare.

You must use the card from your Medicare Advantage Plan to get your Medicare-

covered services. Keep your red, white, and blue Medicare card in a safe place

because you may need to show your Medicare card for some services. Also, you’ll

need it if you ever switch back to Original Medicare.

How do Medicare Advantage Plans work?

When you join a Medicare Advantage Plan, Medicare pays a fixed amount for your

coverage each month to the company oering your Medicare Advantage Plan.

Companies that oer Medicare Advantage Plans must follow rules that Medicare sets.

However, each Medicare Advantage Plan can charge dierent out-of-pocket costs

and have dierent rules for how you get services (like whether you need a referral

to use a specialist or whether you have to go to doctors, facilities, or suppliers that

belong to the plan’s network for non-emergency or non-urgent care). These rules can

change each year. The plan must notify you about any changes before the start of the

next enrollment year through the Annual Notice of Change, typically mailed to you

before September 30.

What do Medicare Advantage Plans cover?

Medicare Advantage Plans provide all your Part A and Part B benefits, except for

certain costs of clinical trials (clinical research studies), hospice care, the cost of

getting a kidney for transplant, and, for a temporary time, some new benefits that

come from legislation or national coverage determinations.

With a Medicare Advantage Plan, you may have coverage for things Original Medicare

doesn’t cover, like fitness programs (gym memberships or discounts) and some

vision, hearing, and dental services (like routine checkups or cleanings). Plans also

have a yearly limit on your out-of-pocket costs for all Part A and Part B services.

Once you reach this limit, you’ll pay nothing for services Part A and Part B cover.

Understanding Medicare Advantage Plans6

What do Medicare Advantage Plans cover? (continued)

Medicare drug coverage (Part D)

Most Medicare Advantage Plans include Medicare drug coverage (Part D). In certain

types of plans that don’t include Medicare drug coverage (like Medical Savings

Account Plans and some Private Fee-for-Service Plans), you can join a separate

Medicare drug plan.

However, if you join a Health Maintenance Organization or Preferred Provider

Organization Plan that doesn’t cover drugs, you can’t join a separate Medicare drug

plan. Go to pages 12–13 for more information.

Note: If you’re in a plan that doesn’t oer drug coverage, and you don’t have a

Medicare drug plan or other creditable prescription drug coverage, you may have to

pay a late enrollment penalty if you decide to join a Medicare drug plan later. Visit

Medicare.gov/basics/costs/medicare-costs/avoid-penalties to learn more about the

Part D late enrollment penalty.

What are my costs?

Each year, plans set the amounts they charge for premiums, deductibles, and services.

The plan (rather than Medicare) decides how much you pay for the covered services

you get. The plan can only change what you pay once a year, on January 1. You still

have to pay the Part B premium. Most people pay the standard Part B premium

amount every month. To get this year’s standard Part B premium, visit Medicare.gov/

basics/costs/medicare-costs.

When calculating your out-of-pocket costs in a Medicare Advantage Plan, in addition

to your premium, deductible, copayments, and coinsurance, you should also consider:

• The type of health care services you need and how often you get them.

• Whether you go to a doctor or supplier who accepts assignment. Assignment

means that your doctor, provider, or supplier agrees (or is required by law) to

accept the Medicare-approved amount as full payment for services Medicare

covers.

• Whether the plan oers extra benefits (in addition to Original Medicare benefits)

and if you need to pay extra to get them.

• Whether you have Medicaid or get help from your state through a Medicare

Savings Program to pay your Medicare costs. Each type of coverage is called a

“payer.” When there’s more than one payer, “coordination of benefits” rules decide

who pays first.

• The maximum out-of-pocket limit set by your plan.

Understanding Medicare Advantage Plans 7

What are my costs? (continued)

What’s the difference between a deductible, coinsurance,

copayment, and a maximum out-of-pocket limit?

Deductible—The amount you must pay for health care or prescriptions before

Original Medicare, your Medicare Advantage Plan, your Medicare drug plan, or your

other insurance begins to pay.

Coinsurance—An amount you may be required to pay as your share of the cost for

benefits after you pay any deductibles. Coinsurance is usually a percentage (for

example, 20%).

Copayment—An amount you may be required to pay as your share of the cost for

benefits after you pay any deductibles. A copayment is a fixed amount, like $30.

Maximum Out-of-Pocket Limit—Plans have a yearly limit on what you pay out of

pocket for services Part A and Part B cover. Once you reach your plan’s limit, you’ll

pay nothing for Part A and Part B services the plan covers for the rest of the year.

More cost details from each plan

If you join a Medicare Advantage Plan, review these notices you get from your plan

each year:

• Annual Notice of Change: Includes any changes in coverage, costs, provider

networks, service area, and more that will be eective in January. Your plan will

mail a copy to you, typically before September 30.

• Evidence of Coverage: Gives you details about what the plan covers, how much

you pay, and more. Your plan will send you a notice (or printed copy) by October

15, which will include information on how to access the Evidence of Coverage

electronically or request a printed copy.

Organization determinations

You or your provider can get a decision, either verbally or in writing, from your plan

in advance to find out if it covers a service, drug, or supply. You can also find out how

much you’ll have to pay. This is called an “organization determination.” Sometimes

you have to do this as prior authorization for your plan to cover the service, drug, or

supply.

You, your representative, or your doctor can request an organization determination. A

representative is someone you can appoint to help you. Your representative can be a

family member, friend, advocate, attorney, financial advisor, doctor, or someone else

who will act on your behalf. Based on your health needs, you, your representative, or

your doctor can ask for a fast decision on your organization determination request. If

your plan denies coverage, the plan must tell you in writing, and you have the right to

appeal.

Understanding Medicare Advantage Plans8

What are my costs? (continued)

Plan Directed Care

If a plan provider refers you for a service or to a provider outside the network, but

doesn’t get an organization determination in advance, this is called “plan directed

care.” In most cases, you won’t have to pay more than the plan’s usual cost sharing.

Check with your plan for more information about this protection.

Who can join a Medicare Advantage Plan?

To join a Medicare Advantage Plan, you must:

• Have Part A and Part B.

• Live in the plan’s service area.

• Be a U.S. citizen or lawfully present in the U.S.

What if I have a pre-existing condition?

You can join a Medicare Advantage Plan even if you have a pre-existing condition.

What if I have End-Stage Renal Disease (ESRD)?

You can join a Medicare Advantage Plan even if you have ESRD. In many Medicare

Advantage Plans, you can only use health care providers who are in the plan’s

network and service area. Before you join, you may want to check with your providers

and the plan you’re considering to make sure the providers you currently use (like

your dialysis facility or kidney doctor), or want to use in the future (like a transplant

specialist), are in the plan’s network. If you’re already in a Medicare Advantage Plan,

check with your providers to make sure they’ll still be part of the new plan’s network.

Read the plan materials or contact the plan you’re considering for more information.

What if I have other coverage?

Talk to your employer, union, or other benefits administrator about their rules before

you join a Medicare Advantage Plan. In some cases, joining a Medicare Advantage

Plan might cause you to lose your employer or union coverage for yourself, your

spouse, and your dependents and you may not be able to get it back. In other cases,

if you join a Medicare Advantage Plan, you may still be able to use your employer or

union coverage along with the Medicare Advantage Plan you join. Your employer or

union may also oer a Medicare Advantage retiree health plan that they sponsor.

Understanding Medicare Advantage Plans 9

When can I join, switch, or drop a Medicare Advantage

Plan?

You can only join, switch, or drop a Medicare Advantage Plan during these enrollment

periods:

Open Enrollment Period—Between October 15 and December 7 each year, anyone

with Medicare can join, switch, or drop a Medicare Advantage Plan. Your coverage will

begin on January 1 (as long as the plan gets your request by December 7).

Medicare Advantage Open Enrollment Period—Between January 1 and

March 31 of each year, you can make these changes:

• If you’re in a Medicare Advantage Plan (with or without drug coverage), you can

switch to another Medicare Advantage Plan (with or without drug coverage).

• You can drop your Medicare Advantage Plan and return to Original Medicare. You’ll

also be able to join a separate Medicare drug plan.

During the Medicare Advantage Open Enrollment Period, if you have Original

Medicare you can’t:

• Switch to a Medicare Advantage Plan.

• Join a Medicare drug plan.

• Switch from one Medicare drug plan to another.

You can only make one change during the Medicare Advantage Open Enrollment

Period, and any change you make will be eective the first of the month after the

plan gets your request. If you’re returning to Original Medicare and joining a separate

Medicare drug plan, you don’t need to contact your Medicare Advantage Plan to

disenroll. The disenrollment will happen automatically when you join the drug plan.

Understanding Medicare Advantage Plans10

When can I join, switch, or drop a Medicare Advantage Plan?

(continued)

Initial Enrollment Period—When you first become eligible for Medicare, you can join

a Medicare Advantage Plan during your Initial Enrollment Period. For many, this is

the 7-month period that begins 3 months before the month you turn 65, includes the

month you turn 65, and ends 3 months after the month you turn 65.

If you’re under 65 and have a disability, you’ll automatically get Part A and

Part B after you get disability benefits from Social Security or certain disability

benefits from the Railroad Retirement Board for 24 months.

If you sign up during the first 3 months of your Initial Enrollment Period, in most

cases, your coverage starts the first day of your birthday month. However, if your

birthday is on the first day of the month, your coverage will start the first day of the

prior month.

If you join a Medicare Advantage Plan the month you turn 65, your coverage will start

the first day of the following month.

If you sign up during the last 3 months of your Initial Enrollment Period, your

coverage will start the first day of the month after you sign up.

If you join a Medicare Advantage Plan during your Initial Enrollment Period, you can

change to another Medicare Advantage Plan (with or without drug coverage) or go

back to Original Medicare (with or without a separate Medicare drug plan) within the

first 3 months you have Medicare.

If you have Part A coverage and you get Part B for the first time between January 1

and March 31, you can also join a Medicare Advantage Plan. Your coverage will start

the first day of the month after you sign up.

Special Enrollment Period—In most cases, if you join a Medicare Advantage Plan, you

must keep it for the calendar year starting the date your coverage begins. However, in

certain situations, like if you move or you lose other insurance coverage, you may be

able to join, switch, or drop a Medicare Advantage Plan during a Special Enrollment

Period.

You may also qualify for a Special Enrollment Period to sign up for Medicare (and

join a Medicare Advantage Plan) if you miss an enrollment period because of

certain exceptional circumstances, like if you’re impacted by a natural disaster or an

emergency. Visit Medicare.gov or check with your plan for more information.

Understanding Medicare Advantage Plans 11

How can I join a Medicare Advantage Plan?

Not all Medicare Advantage Plans work the same way. Before you join, you can find

and compare Medicare plans in your area by visiting Medicare.gov/plan-compare or

calling 1-800-MEDICARE (1-800-633-4227). TTY users can call 1-877-486-2048. Once

you understand the plan’s rules and costs, you can join by:

• Visiting Medicare.gov/plan-compare and searching by ZIP code to find a plan and

join. You can also log in to your secure Medicare account for personalized results.

If you have questions about a plan, select “Plan Details” on the search results page

to get the plan’s contact information.

• Calling the plan you want to join, or visiting the plan’s website to find out if you can

join online.

• Filling out a paper enrollment form. Contact the plan to get an enrollment form, fill

it out, and return it to the plan. All plans must oer this option.

• Calling 1-800-MEDICARE.

When you’re ready to join a Medicare Advantage Plan, you’ll need this information

from your Medicare card:

• Your Medicare Number

• The date your Medicare Part A and/or Part B coverage started

Remember, when you join a Medicare Advantage Plan, in most cases, you must use

the card from your Medicare Advantage Plan to get your Medicare-covered services.

For some services (like hospice care), you may need to show your red, white, and

blue Medicare card.

Understanding Medicare Advantage Plans12

Types of Medicare Advantage Plans

There are different types of Medicare Advantage Plans:

• Health Maintenance Organization (HMO) Plan: Go to page 12.

• Preferred Provider Organization (PPO) Plan: Go to page 13.

• Private Fee-for-Service (PFFS) Plan: Go to page 14.

• Special Needs Plan (SNPs): Go to page 15.

• Medical Savings Account (MSA) Plan: Go to page 17.

The area where you live might have all, some, or none of these plan types available.

In addition, multiple plans of the same type might be available in your area, if private

companies choose to oer them. To find available Medicare Advantage Plans,

visit Medicare.gov/plan-compare, read your “Medicare & You” handbook, or call

1-800-MEDICARE (1-800-633-4227). TTY users can call 1-877-486-2048.

Health Maintenance Organization (HMO) Plan

An HMO Plan is a type of Medicare Advantage Plan that generally provides health

care coverage exclusively from doctors, other health care providers, or hospitals in the

plan’s network (except emergency care, out-of-area urgent care, or temporary out-

of-area dialysis). A network is a group of doctors, hospitals, and medical facilities that

contract with a plan to provide services. Most HMOs also require you to get a referral

from your primary care doctor for specialist care, so that your care is coordinated.

Can I get my health care from any doctor, other health care provider, or

hospital?

No. You generally must get your care and services from doctors, other health care

providers, or hospitals in the plan’s network (except for emergency care, out-of-

area urgent care, or temporary out-of-area dialysis, which is covered whether it’s

provided in the plan’s network or outside the plan’s network). However, some HMO

plans, known as HMO Point-of-Service (HMOPOS) plans, oer an out-of-network

benefit for some or all covered benefits, but you’ll usually pay a higher copayment

or coinsurance.

If you get non-emergency health care outside the plan’s network without

authorization, you may have to pay the full cost. It’s important that you follow

the plan’s rules, like getting prior approval for a certain service when needed. In

most cases, you need to choose a primary care doctor. Certain services, like yearly

screening mammograms, don’t require a referral. If your doctor or other health

care provider leaves the plan’s network, your plan will notify you. You may choose

another doctor in the plan’s network.

Understanding Medicare Advantage Plans 13

Types of Medicare Advantage Plans (continued)

Health Maintenance Organization (HMO) Plan (continued)

Do these plans cover prescription drugs?

In most cases, yes. If you’re planning to enroll in an HMO and you want Medicare

drug coverage (Part D), you must join an HMO Plan that oers Medicare drug

coverage. If you join an HMO Plan without drug coverage, you can’t join a separate

Medicare drug plan.

Preferred Provider Organization (PPO) Plan

A Preferred Provider Organization (PPO) Plan is a Medicare Advantage Plan that has a

network of doctors, specialists, hospitals, and other health care providers you can use.

Can I get my health care from any doctor, other health care provider, or hospital?

Yes. You can also use out-of-network providers for covered services, usually for a

higher cost, if the provider agrees to treat you and hasn’t opted out of Medicare

(for Medicare Part A and Part B items and services). You’re always covered for

emergency and urgent care.

Before you get services from an out-of-network provider, you may want to ask

for an organization determination of coverage from your plan to ensure that the

services are medically necessary and that your plan covers them. Go to page 7 for

more information on organization determinations.

Do these plans cover prescription drugs?

In most cases, yes. If you’re planning to join a PPO and you want Medicare drug

coverage (Part D), you must join a PPO Plan that oers Medicare drug coverage. If

you join a PPO Plan without drug coverage, you can’t join a separate Medicare drug

plan.

Understanding Medicare Advantage Plans14

Types of Medicare Advantage Plans (continued)

Private Fee-for-Service (PFFS) Plans

A Private Fee-for-Service (PFFS) Plan is another kind of Medicare Advantage Plan

oered by a private health insurance company. The plan determines how much it will

pay doctors, other health care providers, and hospitals, and how much you must pay

when you get care.

Can I get my health care from any doctor, other health care provider, or

hospital?

You can go to any Medicare-approved doctor, other health care provider, or

hospital that accepts the plan’s payment terms, agrees to treat you, and hasn’t

opted out of Medicare (for Medicare Part A and Part B items and services). If you

join a PFFS Plan that has a network, you can also use any of the network providers

who have agreed to treat plan members. You can also choose an out-of-network

doctor, hospital, or other provider who accepts the plan’s terms, but you may pay

more. Typically, your plan ID card tells your provider that you belong to a PFFS

Plan.

If your provider doesn’t agree to the plan’s terms and conditions of payment, the

plan is only required to pay them for emergency services, urgently needed services,

and out-of-area dialysis. For other covered services, you’ll need to find another

provider that will accept your PFFS Plan.

Note: A PFFS Plan may also allow “balance billing,” which means that a provider

can charge up to 15% more than the amount Medicare pays, and bill you for that

amount.

If your plan allows balance billing, you may have to pay both the plan’s copayment

or coinsurance and the dierence between what the provider charged and the

amount Medicare pays.

Do these plans cover prescription drugs?

Sometimes. If your PFFS Plan doesn’t oer Medicare drug coverage, you can join a

separate Medicare drug plan to get Medicare drug coverage

(Part D).

Understanding Medicare Advantage Plans 15

Types of Medicare Advantage Plans (continued)

Special Needs Plans (SNP)

Special Needs Plans provide benefits and services to people with specific diseases,

certain health care needs, or who also have Medicaid coverage. SNPs tailor their

benefits, provider choices, and what drugs they cover to best meet the specific needs

of the groups they serve.

Each SNP limits its membership to people in one of the groups listed below, or a subset

of one of these groups. You can only stay enrolled in an SNP if you continue to meet

the special eligibility rules for the SNP.

You may qualify for an SNP if you live in the plan’s service area and meet the

requirements for one of the 3 SNP types:

1. Chronic condition SNP (or C-SNP): You have one or more specific

severe or disabling chronic conditions like:

• Chronic alcohol and other drug dependence

• Certain autoimmune disorders

• Cancer (excluding pre-cancer conditions)

• Certain cardiovascular disorders

• Chronic heart failure

• Dementia

• Diabetes mellitus

• End-stage liver disease

• End-Stage Renal Disease (ESRD) requiring any mode of dialysis

• Certain severe hematologic disorders

• HIV/AIDS

• Certain chronic lung disorders

• Certain chronic and disabling mental health conditions

• Certain neurologic disorders

• Stroke

Understanding Medicare Advantage Plans16

Types of Medicare Advantage Plans (continued)

2. Institutional SNP (or I-SNP): You live in the community but need the level of care

a facility oers, or if you live (or are expected to live) for at least 90 days straight

in a facility like a:

• Nursing facility

• Intermediate care facility

• Skilled nursing facility

• Rehabilitation hospital

• Long-term care hospital

• Swing-bed hospital

• Psychiatric hospital

• Other facility that oers similar long-term health care services, and whose

residents have similar needs and health care status as residents of the facilities

listed above

3. Dual Eligible SNP (or D-SNP): You’re eligible for both Medicare and

Medicaid. D-SNPs also contract with your state Medicaid program to help

coordinate your Medicare and Medicaid benefits.

SNPs are either PPO, HMO, or HMOPOS plan types, and cover the same Medicare Part

A and Part B services that all Medicare Advantage Plans cover. However, SNPs might

also cover extra services tailored to the special groups they serve. For example, if

you have a severe or chronic condition, like cancer or chronic heart failure, and you

require a hospital stay, an SNP may cover extra days in the hospital.

Understanding Medicare Advantage Plans 17

Types of Medicare Advantage Plans (continued)

Can I get my health care from any doctor, other health care provider, or

hospital?

If your SNP is also an HMO, you generally must get your care and services from

doctors, other health care providers, or hospitals in the plan’s network (except

for emergency care, out-of-area urgent care, or out-of-area dialysis). You may be

required to have a primary care doctor.

However, if your SNP is also a PPO, then you may get services from any qualified

provider or hospital, but usually at a higher cost than you would pay for services

from a network provider.

SNPs typically have specialists in the diseases or conditions that aect their

members. Both an HMO and PPO SNP may require you to have a care coordinator

to help with your health care. A care coordinator is someone who helps make

sure people get the right care and information. For example, an SNP for people

with diabetes might provide the services of a care coordinator to help members

monitor their blood sugar and follow their diet.

Do these plans cover prescription drugs?

Yes. All SNPs must provide Medicare drug coverage (Part D).

Medicare Medical Savings Account (MSA) Plans

Medicare Medical Savings Account (MSA) plans combine a high-deductible insurance

plan with a medical savings account:

1. High-deductible health plan: The first part of an MSA Plan is a special type of

high-deductible Medicare Advantage Plan. The plan will only begin to cover your

costs once you meet a high yearly deductible, which varies by plan.

2. Medical savings account: The second part of an MSA is a special type of savings

account. The MSA Plan deposits money into your account that you can use to pay

for your health care costs.

Understanding Medicare Advantage Plans18

Types of Medicare Advantage Plans (continued)

Medicare Medical Savings Account (MSA) Plans (continued)

Who can’t join an MSA Plan?

You can’t join an MSA Plan if:

• You have health coverage that would cover the Medicare MSA Plan deductible.

• You joined another Medicare Advantage Plan.

• You get benefits from the U.S. Department of Defense (TRICARE) or the U.S.

Department of Veterans Aairs (VA).

• You’re a retired Federal government employee and part of the Federal Health

Benefits Program (FEHBP).

• You’re eligible for Medicaid.

• You’re currently getting hospice care.

• You live outside the U.S. more than 183 (total) days a year.

Once you decide which MSA Plan you want, you’ll need to contact the plan for

enrollment information and to join. The plan will tell you how to set up your medical

savings account with a bank that the plan selects. You must set up this account

before the plan can process your enrollment. After you join, you’ll get a letter from

the plan telling you when your coverage begins. Once you join and have MSA

coverage:

• Medicare gives the plan an amount of money each year for your health care.

• The plan deposits money into your account on your behalf. You can’t deposit your

own money.

• You can use the money in your account to pay for health care costs, including

health care costs that aren’t covered by Medicare.

• If you use all the money in your account and you have additional health care costs,

you’ll have to pay for your Medicare-covered services out of pocket until you reach

your plan’s deductible.

• During the time you’re paying out of pocket for services before the deductible

is met, doctors and other providers can’t charge you more than the Medicare-

approved amount.

• Your payments for Medicare-covered Part A and Part B services count toward your

plan’s deductible. After you reach your deductible, your plan will cover your Medicare-

covered services.

• Money left in your account at the end of the year stays in the account and may be

used for health care costs in future years. If you stay with the same MSA Plan the

following year, the new deposit will be added to any leftover amount.

Understanding Medicare Advantage Plans 19

Types of Medicare Advantage Plans (continued)

MSA plans and your taxes

If you use funds from your account, when you file your income taxes you must include

IRS Form 8853 with information on how you used your account money.

Each year, you should get a 1099-SA form from your bank that includes all of the

withdrawals from your account. You’ll need to show that you’ve had Qualified Medical

Expenses equal to at least this amount, or you may have to pay taxes and additional

penalties.

Visit irs.gov/forms-pubs/about-publication-969 to get more tax information related

to MSA plans, like a list of Qualified Medical Expenses.

If you have one, talk to your personal financial advisor about how choosing an MSA

Plan could aect your financial situation.

Can I get my health care from any doctor, other health care provider, or

hospital?

MSA plans generally don’t have a network of health care providers. You can get

Medicare Part A and Part B services from any Medicare-eligible provider in the

U.S. or U.S. territories.

Do these plans cover prescription drugs?

No. If you join a Medicare MSA Plan and want Medicare drug coverage (Part D),

you’ll have to join a separate Medicare drug plan.

Understanding Medicare Advantage Plans20

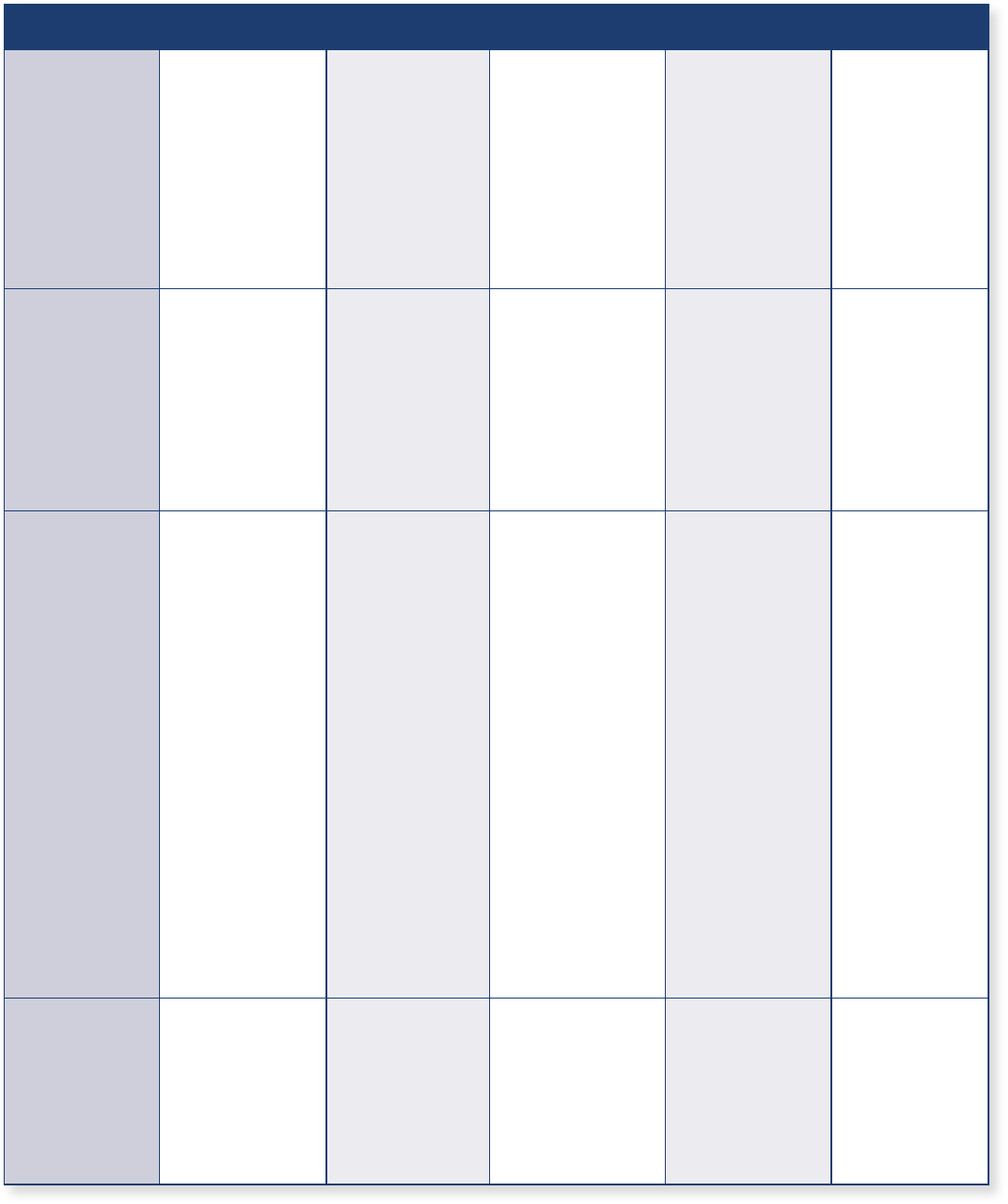

Compare Medicare Advantage Plans side-by-side

The chart below shows basic information about each type of Medicare Advantage Plan.

HMO PPO PFFS SNP MSA

Premium

Do most

plans charge

a monthly

premium?

Yes

Many charge

a premium in

addition to the

monthly Part B

premium.

Yes

Many charge

a premium in

addition to the

monthly Part B

premium.

Yes

Many charge

a premium in

addition to the

monthly Part B

premium.

Yes

Many charge

a premium in

addition to the

monthly Part B

premium.

No

You won’t

have to pay

a separate

monthly

premium, but

you’ll continue

to pay the

monthly Part B

premium.

Drugs

Does the plan

oer Medicare

drug coverage

(Part D)?

Usually

If you join an

HMO Plan that

doesn’t oer

drug coverage,

you can’t get a

separate Medicare

drug plan.

Usually

If you join a

PPO Plan that

doesn’t oer

drug coverage,

you can’t get

a separate

Medicare drug

plan.

Usually

If you join a

PFFS Plan that

doesn’t oer drug

coverage, you can

get a separate

Medicare drug

plan.

Yes

All SNPs must

provide Medicare

drug coverage

(Part D).

No

You may join

a separate

Medicare drug

plan.

Providers

Can I use

any doctor

or hospital

that accepts

Medicare

for covered

services?

Sometimes

You generally

must get your

care and services

from doctors,

other health

care providers,

or hospitals

in the plan’s

network (except

emergency or

urgent care

or out-of-area

dialysis).

In an HMOPOS

Plan, you may be

able to get some

services out of

network for a

higher copayment

or coinsurance.

Yes

Each plan has

a network

of doctors,

hospitals, and

other providers

that you may go

to. You may also

go out of the

plan’s provider

network, but your

costs may be

higher.

Yes

You can go to

any Medicare-

approved doctor,

other health

care provider,

or hospital that

accepts the plan’s

payment terms

and agrees to treat

you. If the plan

has a network, you

can use any of the

network providers

(if you go to an

out-of-network

provider that

accepts the plan’s

terms, you may

pay more).

Sometimes

If your SNP is an

HMO, you must

get your care

and services

from doctors

or hospitals

in the SNP’s

network (except

emergency or

urgent care

or out-of-area

dialysis). However,

if your SNP is

a PPO, you can

get Medicare-

covered services

out of network.

Yes

MSA Plans

generally don’t

have network

providers. You

may go to

any Medicare-

approved

provider for

services Original

Medicare covers.

Referral

Do I need a

referral from my

doctor to use a

specialist?

Yes No No Maybe

If the SNP is an

HMO, you need

a referral. If the

SNP is a PPO,

you don’t need a

referral.

No

Understanding Medicare Advantage Plans 21

What if I have a Medicare Supplement Insurance (Medigap)

policy?

If you’re in a Medicare Advantage Plan, it’s illegal for anyone to sell you a Medigap

policy unless you’re switching back to Original Medicare. If you aren’t planning

to drop your Medicare Advantage Plan, and someone tries to sell you a Medigap

policy, report it to your State Insurance Department. If you have Medigap and join a

Medicare Advantage Plan, you may want to drop Medigap. You can’t use Medigap to

pay your Medicare Advantage Plan copayments, deductibles, and premiums.

If you want to cancel your Medigap policy, contact your insurance company.

In most cases, if you drop your Medigap policy to join a Medicare Advantage Plan,

you may not be able to get the same policy back.

If you join a Medicare Advantage Plan for the first time and you aren’t happy with the

plan, you have a “trial right” under federal law to buy a Medigap policy and a separate

Medicare drug plan if you return to Original Medicare within 12 months of joining the

Medicare Advantage Plan.

• If you had Medigap before you joined a Medicare Advantage Plan, you may be able

to get the same policy back if the company still sells it. If it isn’t available, you can

buy another policy.

• If you joined a Medicare Advantage Plan when you were first eligible for Medicare

(and you aren’t happy with the plan), you can choose any Medigap policy if you

switch to Original Medicare within the first year of joining.

• Some states provide additional special rights to buy a Medigap policy. Check with

your State Insurance Department for more information.

Medigap plans sold to people who are newly eligible for Medicare aren’t allowed

to cover the Part B deductible. For more information about Medigap plans, visit

Medicare.gov/health-drug-plans/medigap or read or download the booklet,

“Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare”

at Medicare.gov/publications.

Accessible Communications22

Where can I get more information?

Find a Medicare plan

Visit Medicare.gov/plan-compare to shop and compare plans that meet your needs.

You can also enter your drugs and pharmacies to get more accurate costs for plans in

your area.

1-800-MEDICARE

Call 1-800-MEDICARE (1-800-633-4227) to get help with specific questions about

billing, claims, medical records, expenses, and more. TTY users can call

1-877-486-2048.

SHIPs (State Health Insurance Assistance Programs)

SHIPs are state programs that get money from the federal government to give

local health insurance counseling to people with Medicare at no cost. SHIPs aren’t

connected to any insurance company or health plan. SHIP volunteers can help you

with these Medicare questions or concerns:

• Your Medicare rights

• Billing problems

• Complaints about your medical care or treatment

• Plan choices

• How Medicare works with other insurance

• Finding help paying for health care costs

You can find the phone number for your state’s SHIP by visiting shiphelp.org or

calling 1-800-MEDICARE.

Medicare Advantage Plans

Contact the plans you’re interested in for detailed information about costs and

coverage.

Accessible Communications 23

Accessible communications

Medicare provides free auxiliary aids and services, including information in

accessible formats like braille, large print, data or audio files, relay services and

TTY communications. If you request information in an accessible format, you

won’t be disadvantaged by any additional time necessary to provide it. This

means you’ll get extra time to take any action if there’s a delay in fulfilling your

request.

To request Medicare or Marketplace information in an accessible format you

can:

1. Call us:

For Medicare: 1-800-MEDICARE (1-800-633-4227)

TTY: 1-877-486-2048

For Marketplace: 1-800-318-2596

TTY: 1-855-889-4325

2. Email us: altformatreques[email protected]v

3. Send us a fax: 1-844-530-3676

4. Send us a letter:

Centers for Medicare & Medicaid Services

Oces of Hearings and Inquiries (OHI)

7500 Security Boulevard, Mail Stop DO-01-20

Baltimore, MD 21244-1850

Attn: Customer Accessibility Resource Sta (CARS)

Your request should include your name, phone number, type of information

you need (if known), and the mailing address where we should send the

materials. We may contact you for additional information.

Note: If you’re enrolled in a Medicare Advantage Plan or Medicare drug plan,

contact your plan to request its information in an accessible format. For

Medicaid, contact your State Medical Assistance (Medicaid) oce.

Nondiscrimination Notice24

Nondiscrimination Notice

The Centers for Medicare & Medicaid Services (CMS) doesn’t exclude, deny

benefits to, or otherwise discriminate against any person on the basis of race,

color, national origin, disability, sex (including sexual orientation and gender

identity), or age in admission to, participation in, or receipt of the services and

benefits under any of its programs and activities, whether carried out by CMS

directly or through a contractor or any other entity with which CMS arranges

to carry out its programs and activities.

You can contact CMS in any of the ways included in this notice if you have any

concerns about getting information in a format that you can use.

You may also file a complaint if you think you’ve been subjected to

discrimination in a CMS program or activity, including experiencing issues with

getting information in an accessible format from any Medicare Advantage Plan,

Medicare drug plan, state or local Medicaid oce, or Marketplace Qualified

Health Plans. There are 3 ways to file a complaint with the U.S. Department of

Health & Human Services, Oce for Civil Rights:

1. Online:

HHS.gov/civil-rights/filing-a-complaint/complaint-process/index.html

2. By phone:

Call 1-800-368-1019.

TTY users can call 1-800-537-7697.

3. In writing: Send information about your complaint to:

Oce for Civil Rights

U.S. Department of Health & Human Services

200 Independence Avenue, SW

Room 509F, HHH Building

Washington, D.C. 20201

Need a copy of this booklet in Spanish?

To get a free copy of this booklet in Spanish, visit

Medicare.gov or call 1-800-MEDICARE

(1-800-633-4227). TTY users can call 1-877-486-2048.

Esta publicación está disponible en Español. Para

obtener una copia gratis, visite Medicare.gov o llame al

1-800-MEDICARE.

U.S. Department of Health & Human Services

Centers for Medicare & Medicaid Services

7500 Security Blvd.

Baltimore, MD 21244-1850

Ocial Business

Penalty for Private Use, $300

CMS Product No. 12026 • 12/2023

The information in this booklet describes the Medicare Program at the time this booklet was printed.

Changes may occur after printing. Visit Medicare.gov, or call 1-800-MEDICARE (1-800-633-4227) to get the

most current information. TTY users can call 1-877-486-2048.

“Medicare Rights & Protections” isn’t a legal document. Ocial Medicare Program legal guidance is

contained in the relevant statutes, regulations, and rulings.

You have the right to get Medicare information in an accessible format, like large print, braille, or audio.

You also have the right to file a complaint if you feel you’ve been discriminated against. Visit

Medicare.gov/about-us/accessibility-nondiscrimination-notice, or call 1-800-MEDICARE

(1-800-633-4227) for more information. TTY users can call 1-877-486-2048.

This product was produced at U.S. taxpayer expense.