STOCK OPTIONS

WHAT ARE EMPLOYEE STOCK OPTIONS?

An employee stock option is the right or privilege granted by

a corporation to an employee to purchase the corporation’s

stock at a specified price during a specifi ed period.

Those stock option plans that meet the requirements of

Sections 421 through 424 of the Internal Revenue Code (IRC)

are referred to as statutory stock options; those that do not are

referred to as nonstatutory or nonqualified stock options (NSO).

The determination whether a stock option plan meets the

requirements of the IRC are made by the Internal Revenue

Service (IRS).

California’s employment tax treatment of stock

options conforms to the federal tax treatment, which

has evolved through court decisions, IRS rulings and

notices, and amendments to the IRC.

In addition to statutory and nonstatutory stock options

defined in the IRC, there is also a California Qualified

Stock Option, which must meet the requirements of Section

17502 of the Revenue and Taxation Code (R&TC).

The following discussion defines the various types of stock

options and provides a detailed explanation of California’s

employment tax treatment of income derived from stock options.

The attached one-page summary table is provided for quick

reference.

STATUTORY STOCK OPTIONS

There are two types of statutory stock options:

• Incentive Stock Options (ISO), which must meet the

requirements of Section 422 of the IRC and are usually

intended for “key” employees as defined by the IRC.

The gain from the exercise of an ISO is based on the

spread income (the difference between the fair market

value of the stock when the option is exercised, less the

cost to the employee).

• Employee Stock Purchase Plans (ESPP), which must

meet the requirements of Section 423 of the IRC and

are usually intended for “rank and fi le” employees. The

gain from the exercise of an ESPP is based on both the

spread income and the discount portion of the stock

(ESPPs may be granted with an option price below the

full fair market value of the stock as of the date granted,

but this discount may not exceed 15 percent).

The employment tax treatment of a statutory stock option

depends, in part, upon when the employee disposes of

(sells, exchanges, gifts, or transfers) the stock acquired

through the exercise of the option. Stock that is disposed

after a required minimum holding period is said to have

a “qualifying disposition.” Stock not held for this period is

said to have a “disqualifying disposition.” Stock disposed to

comply with conflict-of-interest requirements is an exception

to the minimum holding period.

Employment Tax Treatment of Statutory Stock Options

California’s employment tax treatment of the income realized

from a statutory stock option is the same as the federal

treatment: no income results from the grant or exercise of

the stock option. Any gain from the sale of stock is a capital

gain, not wages, and it is not subject to employment taxes:

Unemployment Insurance (UI), Employment Training Tax

(ETT), State Disability Insurance* (SDI), and Personal Income

Tax (PIT) withholding.

Note: Although no employment taxes are required, in cases

where there has been a disqualifying disposition of a statutory

stock option, the gain from the spread income (and the

discount portion of stock acquired by the exercise of an ESPP)

must be reported as PIT wages on the Quarterly Contribution

Return and Report of Wages (Continuation) (DE 9C).

NONSTATUTORY STOCK OPTIONS

As stated above, an NSO is an employee stock option that

does not meet the requirements of Sections 421 through

424 of the IRC. Consequently, it does not enjoy the same

favorable tax treatment as a statutory stock option.

Employment Tax Treatment of Nonstatutory Stock Options

When an NSO is subject to tax depends on whether, at

the time the option is granted, the stock has a “readily

ascertainable” fair market value. This is determined by

Section 83 of the IRC and corresponding federal regulations.

• Income resulting from an NSO that has a fair market

value at the time it is granted is considered wages for

California employment tax purposes and is subject to

UI, ETT, SDI, and PIT withholding and reportable as PIT

wages at the time the option is granted.

• Income resulting from an NSO that did not have a readily

ascertainable fair market value at the time it was granted

is wages for California employment tax purposes and is

subject to UI, ETT, SDI, and PIT withholding and reportable

as PIT wages at the time the option is exercised.

Note: Most NSOs do not have a readily ascertainable fair

market value at the time they are granted.

CALIFORNIA QUALIFIED STOCK OPTIONS (CQSO)

Section 17502 of the R&TC provides that a stock option

specifically designated as a CQSO will receive the

favorable tax treatment provided by Section 421 of the IRC

if all the following conditions are met:

1. The option was issued on or after January 1, 1997, and

before January 1, 2002.

2. The earned income of the employee to whom the option

is issued does not exceed $40,000 in the tax year in

which the option is exercised.

* Includes Paid Family Leave (PFL).

DE 231SK Rev. 5 (10-12) (INTERNET) Page 1 of 3 CU

3. The number of shares of stock granted in the option does

not exceed 1,000 and the combined fair market value of the

shares is less than $100,000 at the time the option is granted.

4. The employee must be employed by the company at the

time the option is exercised (or within three months of that

date), or within one year if permanently and totally disabled.

Employment Tax Treatment of CQSOs

For federal purposes, CQSOs are subject to federal

employment taxes in the same manner as an NSO (see above).

For California employment tax purposes, a qualifi ed CQSO

receives the favorable tax treatment of a statutory stock

option (see above). However, there is no minimum holding

period for a CQSO, so there can be no disqualifying

disposition. As a result, PIT wages are never reportable

upon the disposition of stock obtained through a CQSO.

STOCK OPTIONS TRANSFERRED IN A

COMMUNITY PROPERTY SETTLEMENT

In California, a stock option granted during the period of a

marriage (or, effective January 1, 2005, during a registered

domestic partnership) is community property. Any stock

option transferred in a community property settlement is

an NSO, either because it did not qualify as a statutory

stock option initially or by virtue of the transfer. If a statutory

stock option is transferred due to a divorce or pursuant to

a domestic relations order, the option no longer qualifies

as a statutory stock option as of the day of the transfer.

Thereafter the option is treated as an NSO.

When an NSO is transferred to the nonemployee spouse/

partner as part of a community property settlement, there is

no income to either party until the nonemployee exercises the

option. When the option is exercised, the income is subject

wages for UI, ETT, SDI, and PIT withholding purposes.

However, the income is not reportable as PIT wages.

The employee’s ex-spouse (or former registered domestic

partner) realizes income based on the employee’s services.

The employer should report the income as follows, based

on the requirements established by the IRS in Revenue

Rulings 2002-22 and 2004-60:

• Employee: The income is reportable on behalf of the

employee for California UI, ETT, and SDI purposes

since it resulted from the employee’s prior services.

However, the income is not subject to PIT withholding

and is not reportable as PIT wages for the employee.

• Ex-spouse or former registered domestic partner: The

income is reportable as nonemployee compensation on

federal Form 1099-MISC. California PIT withholding is

required, but the income is not reportable as PIT wages.

MULTISTATE JURISDICTIONAL ISSUES

Stock options, as explained above, may not immediately

become “wages” subject to taxation. An employee may

be granted an option in one state, exercise the option in

a second state, and dispose of the stock in a third state.

For UI, ETT, and SDI purposes, wages derived from the

exercise of a stock option are subject to the jurisdiction of

the state in which services are otherwise subject at the time

the “wages” are paid (when the option becomes taxable).

For California PIT purposes, wages derived from stock

options are allocated between the states in which the

employee performs services for the employer that grants

the option. This allocation begins when the option is granted

and ends when the income derived becomes taxable.

For California Residents, all taxable wages resulting

from stock option transactions are to be reported to the

Employment Development Department (EDD) as PIT wages

regardless of where the services that generated the wages

were performed. If the same wages are taxed in another

state, then the California PIT withholding required is reduced

by the amount of state income tax withheld and paid to the

other state. If the employee is not a resident of California,

then only the wage allocated to California must be reported

to the EDD and are subject to California PIT withholding.

Example - California Resident

On March 1, 2009, your company grants nonstatutory stock

options to an employee who is a resident of Michigan. On

June 1, 2011, the employee is transferred to your California

location and takes up permanent residency in California. On

August 1, 2011, the employee exercises the options.

Because the employee is a California resident, the wages

resulting when the nonstatutory stock options are exercised

(difference between the fair market value of the shares on

August 1, 2011, and the option price) must be reported to

the EDD and are subject to California PIT withholding. If

the wages are also subject to state income tax withholding

by Michigan, then the amount of California PIT withholding

required is reduced by the amount of state income tax

withheld and paid to Michigan.

Example - Nonresident

An employee is granted an NSO (without a readily

ascertainable fair market value) for services performed in

California employment. The employee retires and moves to

Nevada, where he exercises his option.

In this case, the spread income is subject to UI, ETT, and

SDI in California because the services that resulted in the

stock option were localized in California. Similarly, for PIT

withholding and wage reporting purposes, because all the

employee’s services were performed in California, the income

(and tax thereon) is allocated exclusively to California.

ADDITIONAL INFORMATION

For further assistance, please contact the Taxpayer

Assistance Center at 888-745-3886 or visit the nearest

Employment Tax Office listed in the California Employer’s

Guide (DE 44) and on the EDD website at

www.edd.ca.gov/Office_Locator/.

The EDD is an equal opportunity employer/program.

Auxiliary aids and services are available upon request to

individuals with disabilities. Requests for services, aids, and/

or alternate formats need to be made by calling

800-745-3886 (voice), or TTY 800-547-9565.

This information sheet is provided as a public service and is intended to provide nontechnical assistance. Every attempt has been made

to provide information that is consistent with the appropriate statutes, rules, and administrative and court decisions. Any information that

is inconsistent with the law, regulations, and administrative and court decisions is not binding on either the Employment Development

Department or the taxpayer. Any information provided is not intended to be legal, accounting, tax, investment, or other professional advice.

DE 231SK Rev. 5 (10-12) (INTERNET) Page 2 of 3

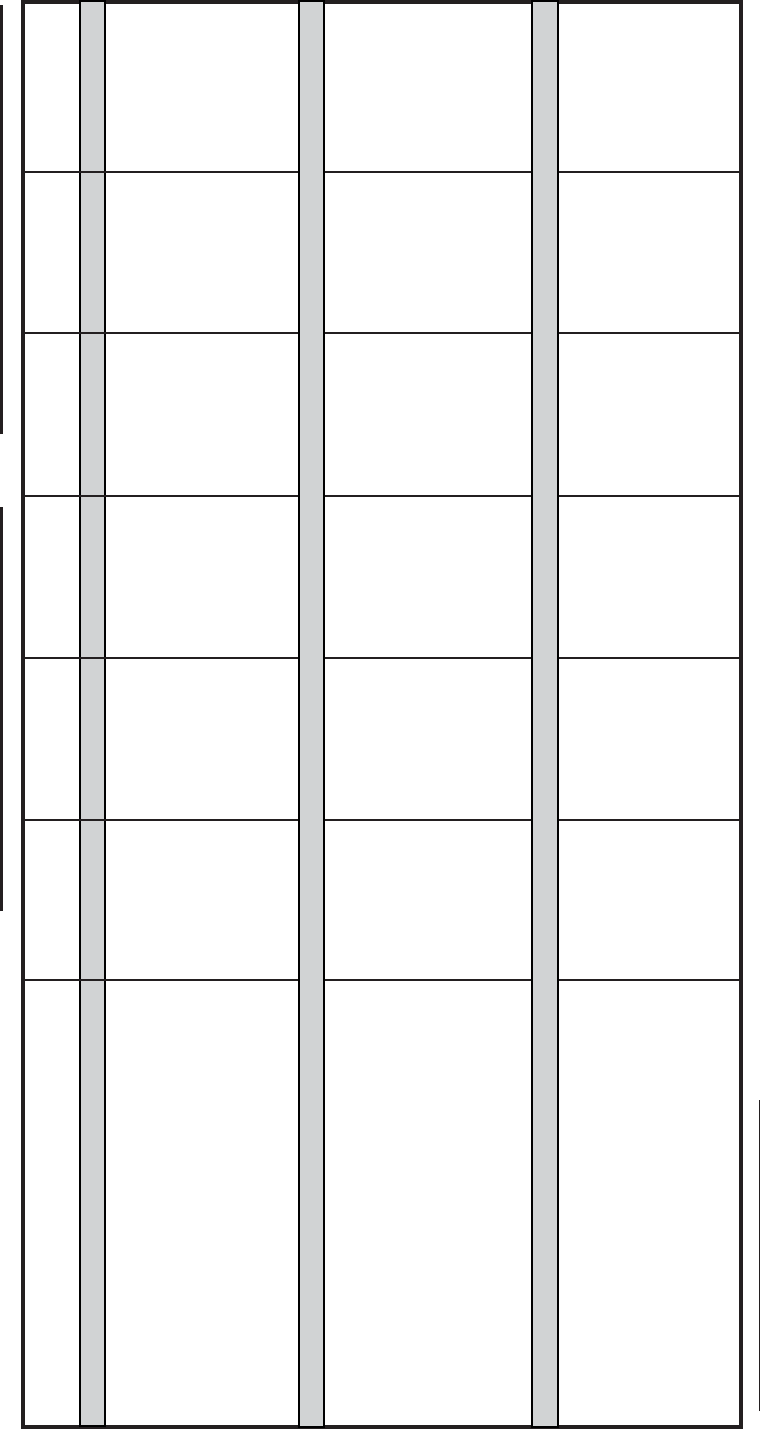

Employment Tax Treatment of Stock Options

Federal Employment Tax Treatment California Employment Tax Treatment

Type of Stock Option FUTA FICA

Federal Income

Tax Withholding UI/ETT/SDI

PIT

Withholding PIT Wages

Statutory Stock Option

Includes Incentive Stock Option (ISO) and

Employee Stock Purchase Plan (ESPP)

Qualifying Disposition

Not subject

1

Not subject

2

Not subject

3

Not subject Not subject Not reportable

Disqualifying Disposition

Not subject

1

Not subject

2

Not subject

,5 4

Not subject

Not subject

Reportable when

disposed

Nonstatutory Stock Option (NSO)

With Readily Ascertainable Fair Market

Value When Granted

Subject when

granted

,7 6

Subject when

granted

,7 6

Subject when

granted

,7 6

Subject when

granted

Subject when

granted

Reportable when

granted

Without Readily Ascertainable Fair

Market V

alue When Granted

Subject when

exercised

,8 7

Subject when

exercised

,8 7

Subject when

exercised

,8 7

Subject when

exercised

Subject when

exercised

Reportable when

exercised

California Qualifi ed Stock Option (CQSO)

Must meet all the requirements of R&TC,

Section 17502 of the R&TC. If the requirements

are not met, the CQSO will receive NSO

treatment for California employment tax

purposes. See NSO above.

See NSO above See NSO above See NSO above Not subject Not subject Not reportable

1

IRC, Section 3306(b)(1)

2

IRC, Section 3121(a)(22)

3

IRC, Section 421(a)

4

IRC. Section 421(b)

5

IRC. Section 423(c)

6

IRC, Section 83(a)

7

Code of Federal Regulations, Title 26, Section 1.83-7(a)

8

IRC, Section 83(e)(3)

(INTERNET) . 5 (10-12) DE 231SK Rev Page 3 of 3