Tax Exempt and Government Entities

EXEMPT ORGANIZATIONS

A Donor’s

Guide to

Vehicle

Donation,

BEFORE YOU GIVE

YOUR VEHICLE TO

A CHARITABLE

ORGANIZATION:

n

CHECK OUT THE CHARITY ,

n

SEE IF YOU’LL GET A TAX BENEFIT ,

n

CHECK THE VALUE OF YOUR VEHICLE ,

n

SEE WHAT YOUR RESPONSIBILITIES

ARE AS A DONOR TO A CHARITY

1

A Donor’s

Guide

to

Vehicle

Donation.

I

f a tax deduction is an important consideration for you when

donating a vehicle to a charity, you should check out the charity,

check the value of your vehicle, and see what your responsibilities

are as a donor.

Through this Publication 4303, the Internal Revenue Service (IRS)

and state charity officials provide general guidelines for individuals

who donate their vehicles.

A companion brochure, Publication 4302, A Charity’s Guide to Vehicle Donations,

provides guidelines for charities that receive donated vehicles.

Note: This publication is not intended as a guide for corporate donors.

2

Selecting a Charity,

If you are eligible to deduct charitable contributions for federal income tax purposes (see

Qualifying for a Tax Deduction, below) and you want to claim a deduction for donating your

vehicle to charity, then you should make certain that the charity is a qualified organization.

Otherwise, your donation will not be tax deductible. The most common types of qualified

organizations are section 501(c)(3) organizations, such as charitable, educational, or religious

organizations. This publication refers to section 501(c)(3) organizations generally as “charities.”

To verify that an organization is a charity qualified to receive tax-deductible contributions,

use the “EO Select Check” tool on the IRS website, http://www.irs.gov/Charities-&-Non-Profits/

Exempt-Organizations-Select-Check. You may also verify an organization’s status by calling

the IRS Customer Account Services division for Tax Exempt and Government Entities at

(877) 829-5500 (toll-free). Be sure to have the charity’s correct name. It is also helpful to know

the charity’s address.

Not all qualified organizations are listed in EO Select Check (Pub.78 data). For example, churches,

synagogues, temples, and mosques are not required to apply to the IRS for recognition of exemp-

tion in order to be qualified organizations and are frequently not listed. If you have questions, call

Customer Account Services at the above number.

If you want to learn more about a charity before donating your vehicle, use the resources listed

under Assistance Through the Charity, Through State Officials, and Through the IRS on page 8.

Qualifying for a Tax Deduction,

You can deduct contributions to charity only if you itemize deductions on your Schedule A

of Form 1040.

You must take into account certain limitations on charitable contribution deductions. For

example, your deduction cannot exceed 50% of your adjusted gross income. Other limitations

may apply. Publication 526, Charitable Contributions, provides detailed information on claiming

deductions and the deduction limits. It also describes the types of organizations that are qualified

to receive tax-deductible contributions. Publication 526 is available online at www.irs.gov or by

calling (800) 829-3676 (toll-free).

3

Determining the Amount You Can Deduct ,

The following rules on deductibility apply to donations of qualified vehicles. A qualified vehicle

is any motor vehicle manufactured primarily for use on public streets, roads, and highways; a

boat; or an airplane. However, a vehicle held by you primarily for sale to customers, such as

inventory of a vehicle dealer, is not a qualified vehicle. If you donated a non-qualified vehicle, see

Publication 526 for the rules and limits that apply to property donations.

The amount you may deduct for a vehicle contribution depends upon what the charity does with

the vehicle as reported in the written acknowledgment you receive from the charity. Charities

typically sell the vehicles that are donated to them. If the charity sells the vehicle, generally your

deduction is limited to the gross proceeds from the sale. However, there are certain exceptions,

described below.

Written Acknowledgment for Vehicle Contribution Deduction of More Than $500,

What the written acknowledgment must contain depends upon what the charity does with the

vehicle. However, all acknowledgments must contain the following information:

n

your name and taxpayer identification number,

n

the vehicle identification number,

n

the date of the contribution, and one of the following:

●

a statement that no goods or services were provided by the charity in return for the donation,

if that was the case,

●

a description and good faith estimate of the value of goods or services, if any, that the charity

provided in return for the donation, or,

●

a statement that goods or services provided by the charity consisted entirely of

intangible religious benefits, if that was the case.

Note: If the acknowledgment does not contain all required information, the deduction may not

exceed $500.

Gross Proceeds Limit Applies — Generally, if the charity sells your vehicle, your deduction

is limited to the gross proceeds the charity receives from its sale. In addition to the information

indicated above, the contemporaneous written acknowledgment must contain:

n

a statement certifying that the vehicle was sold in an arm’s length transaction between

unrelated parties,

n

the date the vehicle was sold,

n

the gross proceeds received from the sale, and ,

n

a statement that your deduction may not exceed the gross proceeds from the sale.

4

Exceptions to Gross Proceeds Limit — Generally, if one of the following applies, you may be

eligible to deduct your vehicle’s fair market value on the date you donated it.

n

The acknowledgment contains a statement certifying that the charity intends to make a signif-

icant intervening use of the vehicle, a detailed description of the intended use, the duration of

that use, and a certification that the vehicle will not be sold before completion of the use.

n

The acknowledgment contains a statement certifying that the charity intends to make a material

improvement to the vehicle, a detailed description of the intended material improvement and a

certification that the vehicle will not be sold before completion of the improvement.

n

The acknowledgment contains a statement certifying that the charity intends to give or sell

the vehicle to a needy individual at a price significantly below fair market value and that the

gift or sale is in direct furtherance of the charity’s charitable purpose of relieving the poor and

distressed or the underprivileged who are in need of a means of transportation. This exception

will not apply if the charity merely applies the proceeds from the sale of the vehicle to a needy

individual for any charitable purpose.

n

A special rule applies if the acknowledgment indicates that the donated vehicle sold for $500

or less. In this case, you may claim a deduction for the lesser of the vehicle’s fair market value

on the date of the contribution, or $500, provided you get a written acknowledgment from the

charity that complies with the requirements described under Written Acknowledgment for a

Vehicle Contribution Deduction of $500 or Less, page 5.

EXAMPLE 1: On April 1, you donated your car to the local food bank. When you donated

the car, you had determined that the fair market value was $4,300. On November 10, the charity

sold your car (to someone other than a needy individual), without any significant intervening

use or material improvement, and received gross proceeds of $3,700. Your deduction may

not exceed $3,700.

EXAMPLE 2: The charity certifies in an acknowledgment that it will make significant intervening

use of the vehicle by using it daily for at least a year to deliver food to needy individuals. Your

deduction may not exceed the fair market value of your car, $4,300.

EXAMPLE 3: The facts are the same as in Example 1 except the charity only received gross

proceeds of $400 from the sale. Your deduction may not exceed $500.

Time and Manner of Providing Acknowledgment — You must obtain the written

acknowledgment from the charity within 30 days from the date of the vehicle’s sale,

or if an exception applies, within 30 days of the date of the donation.

The charity may use Form 1098-C, Contributions of Motor Vehicles, Boats, and Airplanes, as

acknowledgment or provide its own statement containing the information described above. Be

5

sure to attach the acknowledgment and Form 8283, Noncash Charitable Contributions (see

below), to your return.

Written Acknowledgment for a Vehicle Contribution Deduction of $500 or Less,

If you are claiming at least $250 but not more than $500 as the value of your vehicle, the acknowl-

edgment must include the name of the charity, a description (but not value) of your vehicle, and

one of the following:

n

a statement that no goods or services were provided by the charity in return for the donation, if

that was the case,

n

a description and good faith estimate of the value of goods or services, if any, that the charity

provided in return for the donation, or ,

n

a statement that goods or services provided by the charity consisted entirely of

intangible religious benefits, if that was the case.

Time and Manner of Providing Acknowledgment — You must obtain the written acknowledgment

on or before the earlier of the date you file your return for the year you donated the vehicle, or the

due date, including extensions, for filing the return. A charity can provide you with a paper copy

of the acknowledgment, or it can provide the acknowledgment electronically, such as via an email

addressed to you. Do not attach the acknowledgment to your income tax return; instead, retain it

with your records to substantiate your donation.

Determining the Fair Market Value of Your Vehicle,

If an exception to the gross proceeds limit applies to your deduction or if you are claiming a

deduction of $500 or less, you will need to determine your vehicle’s fair market value as of the

date of the contribution. Generally, fair market value is the price a willing buyer would pay and a

willing seller would accept for the vehicle, when neither party is compelled to buy or sell, and

both parties have reasonable knowledge of the relevant facts.

If you use a vehicle pricing guide to determine fair market value, be sure that the sales price

listed is for a vehicle that is the same make, model, and year, sold in the same condition, and

with the same or substantially similar options or accessories, as your vehicle. Moreover, the

fair market value of a vehicle cannot exceed the price listed for a private-party sale.

EXAMPLE: You donate your car to a local charity that provides you with an acknowledgment

certifying that it intends to make a significant intervening use of the car. Your credit union

representative told you that the price listed for a private-party sale in a vehicle pricing guide

could be as high as $1,600. However, your car needs extensive repairs, and after some checking,

you find that you could only sell your car for $750. $750 is the fair market value of the car.

For more information on determining the value of your vehicle, see Publication 561, Determining the

Value of Donated Property.

6

Recordkeeping and Filing Requirements,

You must attach to your return the written acknowledgment received from the charity if you

are deducting more than $500. Depending on the amount you are claiming as a charitable

contribution deduction, you may need to get and keep certain records and file an additional

form or statement to substantiate your charitable contributions. See the chart Recordkeeping

and Filing Requirements on page 7.

Form 8283,

Noncash Charitable Contributions

,

If the deduction you are claiming for a donated vehicle is greater than $500, but not more

than $5,000, you must complete Section A of Form 8283 and attach it to your Form 1040.

If the deduction you are claiming is greater than $5,000, you must complete Section B of Form

8283, which must include the signature of an authorized official of the charity, and attach it to your

return. In addition, if the deduction is over $5,000 and not limited to the gross proceeds from the

sale of your vehicle, you must get a written appraisal of your vehicle (see Written Appraisal, below).

Written Appraisal,

Your written appraisal must be from a qualified appraiser. See Publication 561, Determining

the Value of Donated Property. The appraisal must be made no more than 60 days before you

donate the vehicle. You must receive the appraisal before the due date (including extensions) of

the return on which you first claim a deduction for the vehicle. For a deduction first claimed on

an amended return, the appraisal must be received before the date the amended return is filed.

When you file your income tax return (Form 1040 or Form 1040X), you will need to complete

Section B of Form 8283, and attach it to your return.

If Section B is required and the charity sells or otherwise disposes of a vehicle within three years

after the date of receipt, the charity must file Form 8282, Donee Information Return, with the IRS.

On Form 8282, the charity reports information identifying the donor and itself, and the amount it

received upon sale or other disposition of the vehicle. The charity must provide you with a copy

of the form.

The chart on page 7 lists recordkeeping and filing requirements, based on the amount you claim

as a deduction.

Definitions,

Below are definitions of material improvement and significant intervening use as they apply to

vehicle donations.

n

Material improvement includes a major repair or improvement that results in a significant

increase in the vehicle’s value. Cleaning, minor repairs, and routine maintenance are not

material improvements. In addition, a material improvement to the vehicle will not qualify if

the donor funded the improvement by giving the charity an additional payment.

n

Significant intervening use means that a charity must actually use the vehicle to substantially

further its regularly conducted activities, and the use must be considerable. There is no signifi-

cant intervening use if the charity’s use is incidental or not intended at the time of the donation.

7

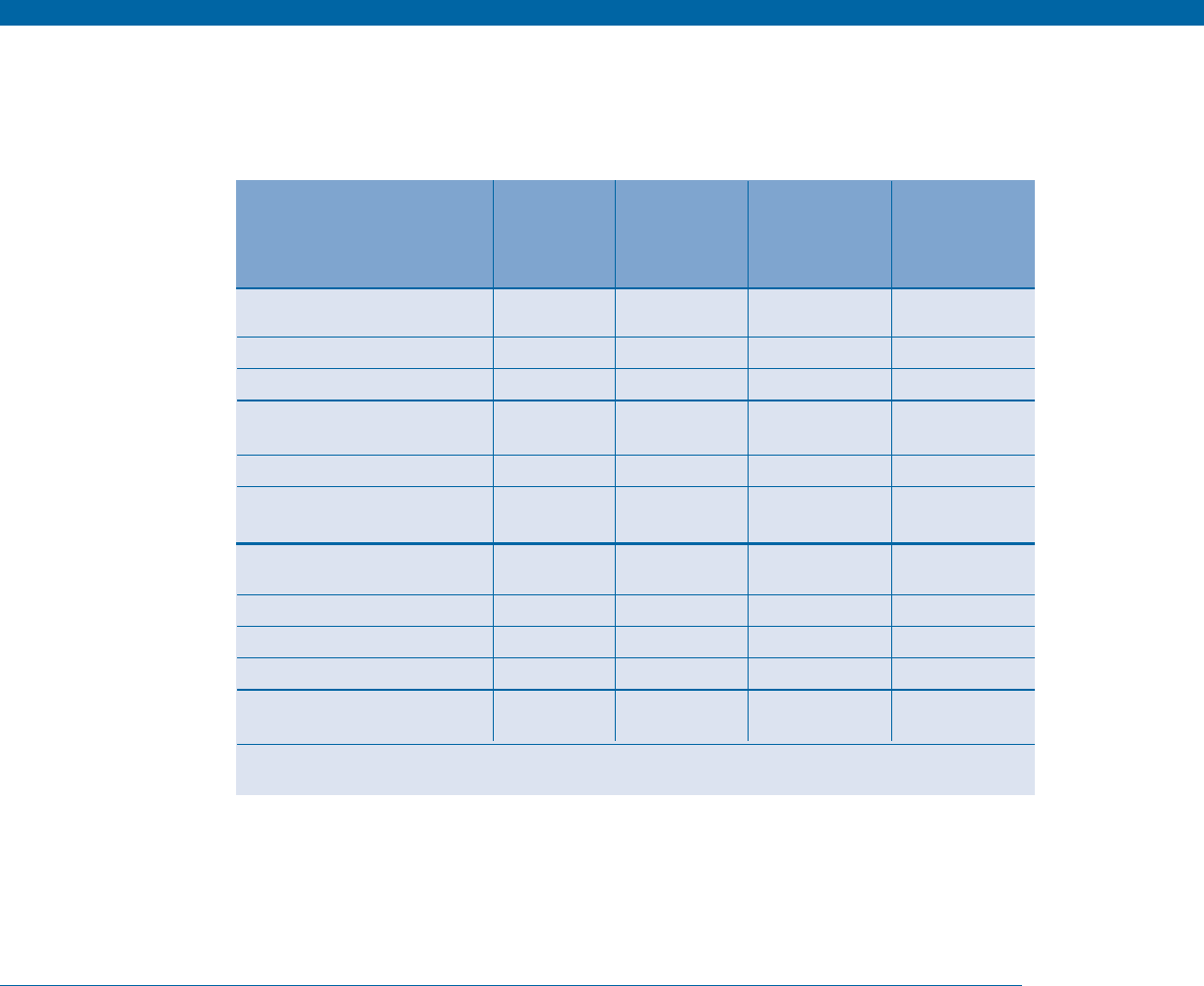

Recordkeeping and Filing Requirements,

Requirement,

Deductions

of Less

Than $250,

Deductions

of $250 or

More, But

Not More

Than $500,

Deductions

Greater Than

$500, But Not

More Than

$5,000 ,

Deductions

Greater

Than

$5,000 ,

Recordkeeping Requirements,

n

name/address of charity,

n

date of donation

,

n

place where you

donated vehicle

,

n

description of vehicle

,

n

contemporaneous written

acknowledgment from charity*

,

Filing Requirements,

n

written acknowledgment*

,

n

Form 8283, Section A

,

n

Form 8283, Section B

,

n

written appraisal — if deduction

is not limited to gross proceeds

,

X X X X

X X X X

X X X X

X X X X

X X X

X X

X

X

X

* For information on what the acknowledgment must contain, see Determining the Amount You Can Deduct, page 3.

State Law Rules on Liability — Vehicle Title,

Generally, state charity officials recommend that the donor take responsibility for transfer of title

to ensure termination of liability for the vehicle. In most states, this involves filing a form with the

state motor vehicle department which states that the vehicle has been donated. Before donating

the vehicle, you should remove the license plates, unless state law requires otherwise. This may

help you avoid any liability problems after the vehicle is transferred.

8

Assistance Through the Charity, Through

State Officials, and Through the IRS,

Charity Assistance,

A charity must make available for public inspection its application for tax exemption, its

determination letter, and its most recent annual information returns (Forms 990). A charity

also must provide copies of these documents upon request (unless it makes the documents

widely available). A charity may not charge you for inspecting the documents, but it may

charge a reasonable fee for copying and mailing the documents.

Note: Certain charities, including churches, synagogues, and mosques, are not required to file

exemption applications and annual information returns.

State Charity Official Assistance,

Many states require charities that solicit contributions to register and file certain documents with

a state charity regulator, such as the state attorney general or the secretary of state. Most charities

must file in their state of incorporation and in other states where they have activities. Many of the

state charity officials provide useful information about charities and fundraisers on Web sites and

in brochures and publications.

A listing of state charity offices is available through the National Association of State Charity

Officials at www.nasconet.org. A listing of state attorneys general is available through the

National Association of Attorneys General at www.naag.org.

Contact your state charity official if you have a concern or complaint that a charity or fundraiser

is not complying with state laws.

IRS Assistance,

The IRS can answer your tax questions and can provide tax forms, publications, and other

reading materials for further assistance. IRS materials are accessible through the Internet at

www.irs.gov, through telephone ordering at (800) 829-3676, and at IRS walk-in offices in many

areas across the country. The IRS also must make available the charity’s application for tax

exemption, determination letter, and Form 990.

If you have a concern or complaint about a charity, write to:

IRS Examination Division ,

Attn: T:EO:E, MC 4910 DAL ,

1100 Commerce Street ,

Dallas, TX 75242,

Specialized Assistance on Tax-Exempt Organizations

Through the Exempt Organization (EO) Division of the IRS,

www.irs.gov/Charities-&-Non-Profits,

Customer Account Services,

(877) 829-5500 (toll-free),

Internal Revenue Service,

TE/GE,

P.O. Box 2508,

Cincinnati, OH 45201,

IRS tax forms and publications useful to donors are available on the EO Web site above and

through the IRS services noted under General IRS Assistance below.

Form 1040, U.S. Individual Income Tax Return ,

Form 1040, Schedule A, Itemized Deductions ,

Form 1098-C, Contributions of Motor Vehicles, Boats, and Airplanes ,

Form 8282, Donee Information Return ,

Form 8283, Noncash Charitable Contributions ,

Publication 526, Charitable Contributions ,

Publication 557, Tax-Exempt Status for Your Organization ,

Publication 561, Determining the Value of Donated Property,

Publication 1771, Charitable Contributions – Substantiation and Disclosure Requirements ,

Publication 4302, A Charity’s Guide to Vehicle Donations,

General IRS Assistance on the latest tax laws,

forms and publications, and filing information:

www.irs.gov,

Federal tax questions, (800) 829-1040,

Small business federal tax questions, (800) 829-4933,

IRS tax forms and publications, (800) 829-3676,

Publication 4303 (Rev. 1-2015) Catalog Number 38162P Department of the Treasury Internal Revenue Service www.irs.gov